Embed Size (px)

Citation preview

SPE DISTINGUISHED LECTURER SERIESis funded principally

through a grant of the

SPE FOUNDATIONThe Society gratefully acknowledges

those companies that support the programby allowing their professionals

to participate as Lecturers.

And special thanks to The American Institute of Mining, Metallurgical,and Petroleum Engineers (AIME) for their contribution to the program.

E & PA Dynamic Growth Business

Aidan McKay, SPEShell Exploration & Production Company

SPE Paper 84433Originally presented at SPE – ATCE Denver, CO

October 2003

History of Supply / Demand and Growth

Potential Investment Levels Required

Six Competitive Forces Shaping the EP Industry

Profits

Conclusions

SPE 84433 A McKay

Hydrocarbon (Oil & Gas ) Demand from Wellbores

Aggregate global production decline is ~ 5+% per annum.Aggregate long term oil & gas growth is 1.5% per annum average.

Dai

ly P

rod

uct

ion

(M

illio

n B

oe/

d)

0

40

80

120

160128 mln boe/d

1980 1990 2000 2010

200

240

2030

Oil (?)

Gas (?)

19951985 2005 20202015 2025

Current estimated decline rate

SPE 84433 A McKay

0

200

400

600

800

1000

1200

1400

1940 1950 1960 1970 1980 1990 2000 2010 2020 2030

Nu

mb

er o

f C

ars

& L

igh

t T

ruck

s G

lob

ally

(m

illio

ns)

Number of Vehicles Globally (History and Forecast)

Range of Forecasts

[Assumes an 8 Bln population by 2030]

USA ~ 200 mln vehicles (adding 15 mln pa)China ~ 5 mln (Growth undefined)

SPE 84433 A McKay

0

5

10

15

20

25

30

35

1940 1950 1960 1970 1980 1990 2000 2010 2020 2030

Time (Years)

Nu

mb

er

of

Co

mm

erci

al A

irc

raft

(th

ou

sa

nd

s)

Range of Forecasts

Number of Commercial Aircraft

[Assumes an 8 Bln population by 2030 AND economic progress ] SPE 84433 A McKay

Oil 1100 Bln bbl(Expect+ Undiscov.= 2000 Bln)

Gas 700 Bln boe4000 Tcf

0

1000

2000

3000

4000

5000

6000

Hydrocarbon Demand from

WellboresGrowing at ~1-

2% pa

World Proven Hydrocarbons (Bln Boe)

1000-3000 Bln boeOil sands/BitumenHeavy etc

• The planet may have 40 - 100 years supply• 80% of hydrocarbons are in onshore areas; 20% offshore• Much is low cost access…..most owned by governments…• New ones (mature) opening each day.

2002 203044 Bln boe 88 Bln boe

Hy

dro

carb

on

Res

erv

es &

De

ma

nd

(B

ln b

oe

)

?

SPE 84433 A McKay

Private Oil Company Annual EP Capex Actuals & Forecasts

0

50

100

150

200

250

300

1960 1970 1980 1990 2000 2010 2020 2030

Ca

pit

al In

ve

stm

en

t C

ap

ex

($ B

ln)

Time (Years)

~ $1 Bln scale “giant” projects, start of offshore, DW etc

Big 5 oil companies ’93 ~18 Bln pa, 2003 ~$34 Bln toincrease oil by 15 % & Gas by 20 % in 10 years to 14.8 mln Exxon, BP, Shell, Chev, TFE

Big US Independents ~ $8 Bln pa, for 2 mln boe/d

Excludes OPEC Countries and Russia Spend]

SPE 84433 A McKay

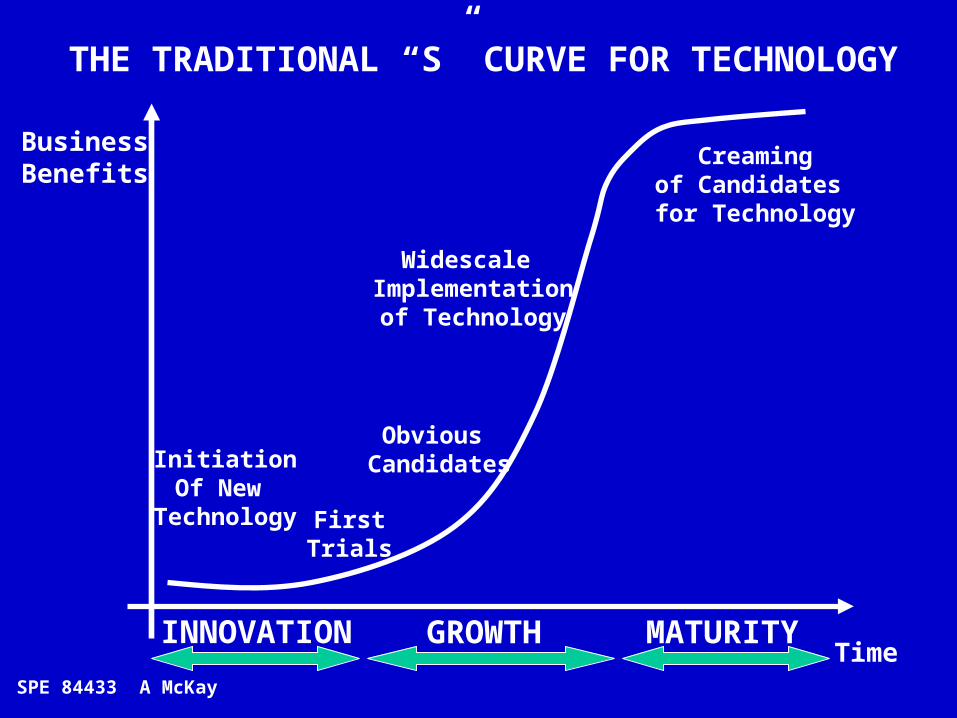

THE TRADITIONAL “S” CURVE FOR TECHNOLOGY

InitiationOf New

Technology

Widescale Implementationof Technology

Creamingof Candidates for Technology

Time

BusinessBenefits

FirstTrials

Obvious Candidates

INNOVATION GROWTH MATURITY

SPE 84433 A McKay

New Well Technology S Curve Evolution

Vertical &Deviated Wells

1970 1980 1990 2000

Time 2010

HydraulicFracturing

HorizontalWells

MultilateralWells

MultilateralMulti-fracced

Wells

Underbalanced Drilling Offshore

HorizontalWells with

Hydraulic Fracturing

Coiled TubingDrilling

Business

Benefits?

Slim HoleExploration

Intelligent Wells

GAINS CONTINUE ?

SPE 84433 A McKay

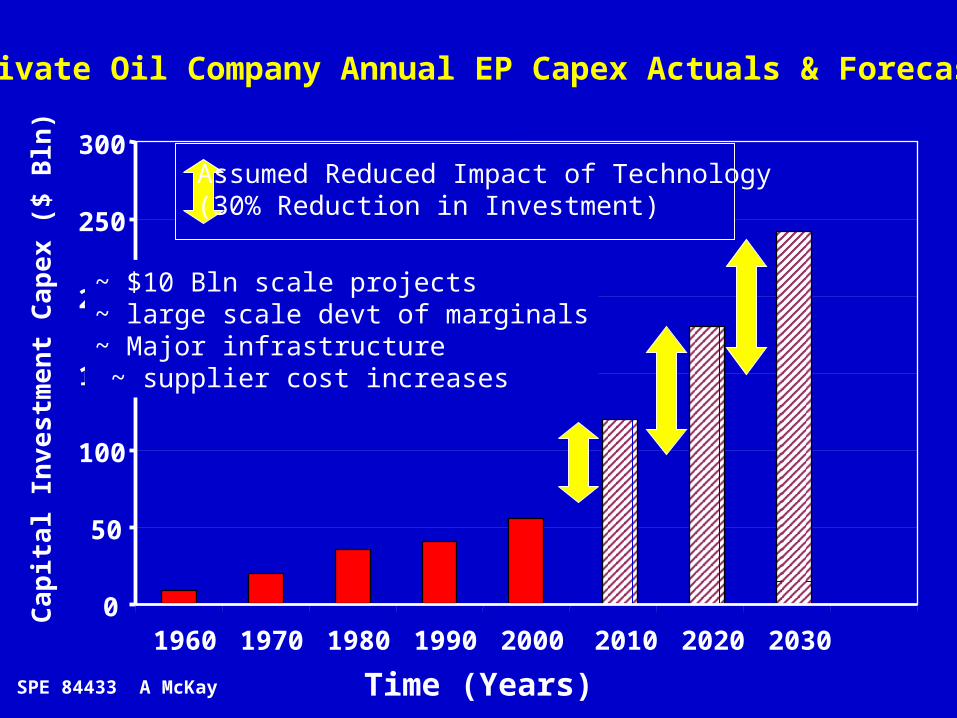

Private Oil Company Annual EP Capex Actuals & Forecasts

0

50

100

150

200

250

300

1960 1970 1980 1990 2000 2010 2020 2030

Ca

pit

al In

ve

stm

en

t C

ap

ex

($ B

ln)

Assumed Reduced Impact of Technology(30% Reduction in Investment)

Time (Years)

~ $10 Bln scale projects~ large scale devt of marginals~ Major infrastructure ~ supplier cost increases

SPE 84433 A McKay

Industry Sector Research and Development Spend 2001

01020304050607080

IT &

Har

dware

Autom

otive

Indust

ry

Pharm

aceu

tical

s

Elect

ronic

s & E

lect

rical

Softwar

e & IT

Ser

vice

s

Chemic

als

Aerosp

ace

& Def

ense

Telec

oms

Oil & G

as

Perso

nal C

are

Diver

sifie

d Indust

rials

(Conglo

mer

ates

)

Industrial Sector

An

nu

al R

&D

In

vest

men

t ($

Bln

)

$3.3 Bln in totalEP ~ $2 Bln in total

Source: UK Financial Times Monday 14th October 2002 pages 10 -11

NB : 1995 equivalent R&D spend was ~ $4 Bln

SPE 84433 A McKay

Oil & Gas Company Research and Development Spend

0

100

200

300

400

500

600

700

800

900

Schlu

mber

ger

Total,

Fina

Elf

ExxonM

obil

Shell/R

oyal D

utch BP

Hallib

urton

Chevro

nTexac

o

ENI (AGIP

)

200120001999

An

nu

al R

&D

Sp

en

din

g (

$ m

ln )

Source : Company Annual Reports

• Pressures from Shareholders to cut R&D spending in 1990s.• Service Industry starts to do material “ tech devt”, but significantly lower profits mean less R&D funding SPE 84433 A McKay

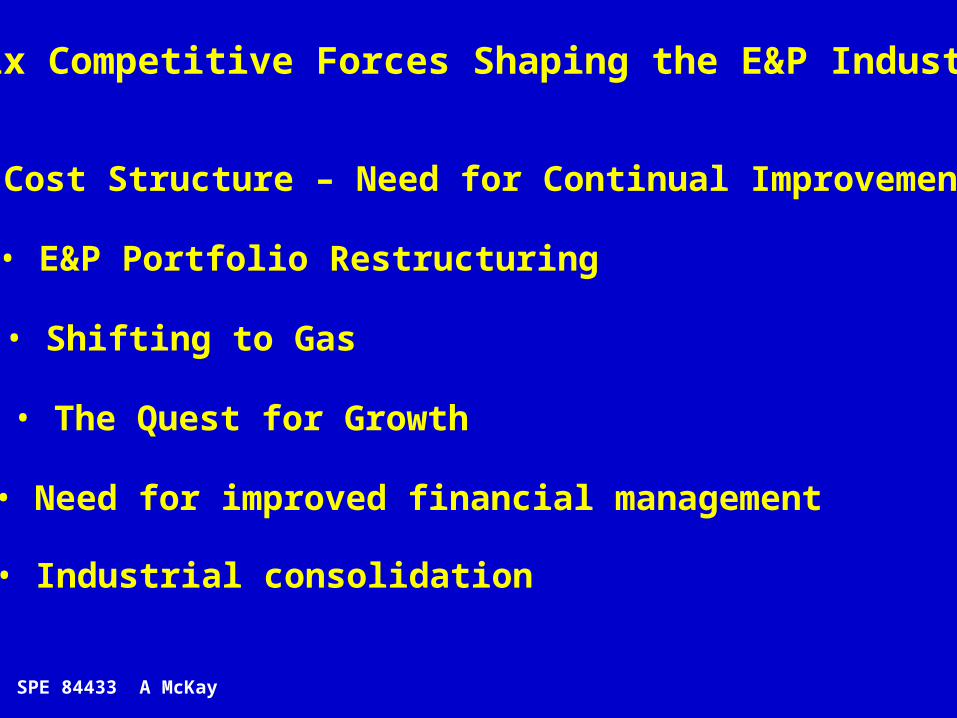

• Cost Structure – Need for Continual Improvement

• E&P Portfolio Restructuring

• Shifting to Gas

• The Quest for Growth

• Need for improved financial management

• Industrial consolidation

Six Competitive Forces Shaping the E&P Industry

SPE 84433 A McKay

Where to Exploit the Hydrocarbons in Longer Term

“OLD” EP Business “NEW” EP Business

USA, Canada, North Sea,Small ME CountriesSelected others

Brazil, Angola, Iran, CIS, Sakhalin, Kazakhstan, ChinaOther OPEC Countries, S. America, Pakistan, Bangladesh

+ Low Govt Take, stable terms- High UTCs- Mature Basins (limited growth)- Capital intensive, - high costs on supply curve+ Long asset tenure+ High upside at higher prices + gas markets are developed

- High Govt Take, less stable terms- Commercially risky- Limited upside @ higher prices- gas markets are emerging- ultra competitive (“loss leading”)- Lower degree of control with govt+ Green/Brownfield (high growth)+ Low UTCs- MRH ; DW High UTCs

Natural Shift with Declines

Where EP Industry made most of the money in the past …..But margin is small @ low pricesand where capex treadmill potential exists

Where the EP industry must go in the future, but where EP margin may be thin.....at all oil/gas prices like R&M or Chemicals

SAUDI, KUWAIT,IRAN, IRAQ, UAE

BIG 5 MEO

- High Govt Take, - Commercially risky- Limited upside @ higher prices- gas markets are emerging- ultra competitive (“loss leading”)- Low degree of control with govt+ Green/Brownfield (high growth)+ Low UTCs resources

QATAR, Russia

BIG GAS

SPE 84433 A McKay

E&P UNIT MARGINS ($/bbl) FOR E&P ENVIRONMENTS

00.5

11.5

22.5

33.5

44.5

55.5

66.5

77.5

88.5

99.510

10.511

11.5

USAUK

Canad

a

Nether

lands

Denm

ark

Germ

any

Egypt

Gabon

Thaila

nd

Niger

ia

Venez

uela

Angola

Brazil

Kazak

hstan

China

Russia

Abu Dhab

i

Kuwait

Saudi

$16/bbl oil & $3/mln scf gas

$22/bbl oil & 3.5/mln scf gas

$30/bbl oil & $4.75/mln scf gas

Ne

t In

com

e A

fter

Tax

pe

r B

oe

($/b

oe

)

OLD E&P(examples)

NEW E&P(examples)

BIG5MEO(likely rents)

BIG- GASQatar

(likely rents)

Which is better: “bond-like” investments or investments with more risks but with price upside?SPE 84433 A McKay

Standard Oil (NJ)Socony VacuumSuperior OilStandard Oil (IN)Standard Oil (OH)AtlanticRichfieldSinclair British Petroleum

PhillipsAminoilGeneral American Oil

1950 1960 1970 1980 1990 2000Exxon/MobilMobil

BP

The Texas Co.TidewaterPacific Western GettySkellyGulf Standard Oil (CA)Standard Oil (KY)

Texaco

Chevron

Chev/Tex

ConocoPhillips

Royal Dutch/ShellShell Oil

Royal Dutch/Shell

AmocoArcoVastar

Union OilPure Oil

Unocal

50 years of EP Consolidation Continues, Nationals Join, What Next?

Continental

OccidentalCities Service

Occidental

Marathon

2005+

State Oils & Former State OilsTFE, ENI, REPSOL, PETROBRAS,

Britoil+ TNK

2003 2005 - 2010Exxon/Mobil

BP

Chev/Tex

Phillips/Conoco

Royal Dutch/Shell

Will Consolidation Continue? In What Form?

TFE

+ Repsol (?)

ENI

Petrobras

Statoil + Norske Hydro (?)

YUKOS Sibneft (?) GaZprom (?)

SPE 84433

• Alignment around geography & cultures• Regulatory involvement is likely • National Oils rightly playing away from home

• Does Aramco marry or eat the survivors• How will Gasprom play going forward ?

Rosneft

SPE 84433 A McKay

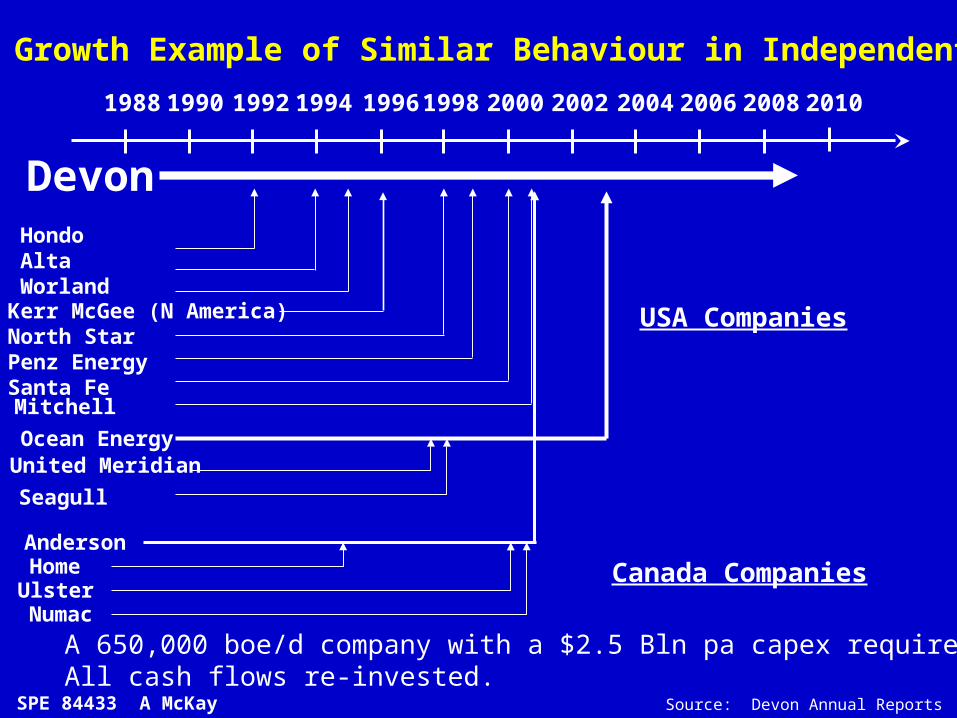

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008

HondoAltaWorlandKerr McGee (N America)North StarPenz EnergySanta Fe

Anderson

Mitchell

Ocean Energy

HomeUlsterNumac

United Meridian

Seagull

2010

Canada Companies

USA Companies

An Growth Example of Similar Behaviour in Independents

Devon

Source: Devon Annual Reports

A 650,000 boe/d company with a $2.5 Bln pa capex requirement,All cash flows re-invested.

SPE 84433 A McKay

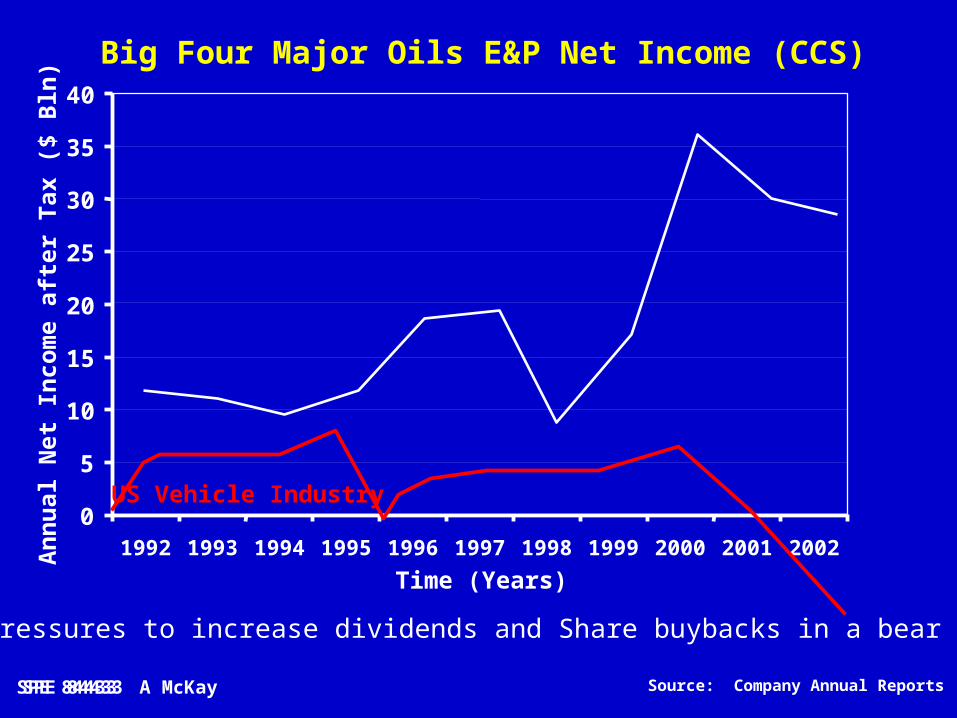

Big Four Major Oils E&P Net Income (CCS)

0

5

10

15

20

25

30

35

40

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

Time (Years)

An

nu

al N

et I

nco

me

afte

r T

ax (

$ B

ln)

Source: Company Annual ReportsSPE 84433

Large pressures to increase dividends and Share buybacks in a bear market

US Vehicle Industry

SPE 84433 A McKay

General MotorsAT&TUS SteelS..O. N.J. (Exxon)

G.E. DuPont

F.W. WoolworthS.H. KressS.Oil of California

NY Central Railroad

1.2.3.4.

5.6.

7.8.9.

10.

221899

98

776

6

CompanyMkt Cap(S Bln )Rank

1928

IBMAT&TGeneral MotorsEastman Kodak

Exxon Sears Roebuck

TexacoXeroxGE

Gulf Oil

1591027651

5140

323127

24

CompanyMkt Cap($ Bln )

1969

GEMicrosoftCitigroupCisco

ExxonMobil Pfizer

IntelWal-MartIBM

Nokia

459335314306

284271

244239194

187

CompanyMkt Cap($ Bln )

1999

The Ten Largest US Market Capitalisations Versus Time

Source: VariousSPE 84433

Wal-Mart

GE

Citigroup

ExxonMobil

Pfizer

Merck

Johnson & JIBMAIG

266256231217

178173

163137128

114

CompanyMkt Cap($ Bln )

2003

Microsoft

Oil Companies will continue to play huge global role

SPE 84433 A McKay

Conclusions E&P is a dynamic, profitable, growth business

E&P business is capital intensive and requires high technology like space travel or the defence industry

We have interesting conflicts in meeting global hydrocarbon demand whilst meeting the needs of stakeholders

The scale of investment required will be challenging and is not recognised in society.

Sustaining the industry success will require R&D success levels at least equal to those of the past to keep future investment costs down. We need to avoid under-investing in the research we need.

We have met the energy needs of the planet in the past and will do so in future. This is a great place to work.

SPE 84433SPE 84433 A McKay

Key Points to Reflect on: Can we get OEDC individuals out of cars, into buses/trains ?

Quality E&P investments are very, rare (ie risk/reward balance)

Portfolio Management & Mergers add nothing to global supply

Selling assets in production returning WACC+, is dubious.

Role of Exploration 2005 –2030 is very uncertain, If so then where

BI5MEO, BIGGAS, NEW EP, or Frontier exploration

Impact of Technology in Future in Cost Redn (Is it large or small)

Not at all clear that material steps are being made

R&D Spend is low (vs industries & history), so what breakthroughs

Majors & Service Industry may not be doing enough

Cash Today is Mantra, (Dividends & Buybacks) not investment

Having a large surplus of cash today, is not valued in market.

SPE 84433SPE 84433 A McKay

Backup Slides

Not likely to be Used

SPE 84433 A McKay

02468

101214161820222426283032343638

1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000 2010 2020 2030

Oil

Pri

ce (

$/b

bl)

Act

ual

Low Oil Price World1910-1970

VolatileOil Price

World1971-2002

VolatileOr Low Oil

PriceWorld again

Possible Outlooks on Oil Prices?

?

SPE 84433 A McKay

March 1999SPE 84433 A McKay

We Tend To Get Overly Pessimistic in Downturns

September 2000SPE 84433 A McKay

Then rapidly revert 12-18 months later ….Yet the big supply demand did not change?

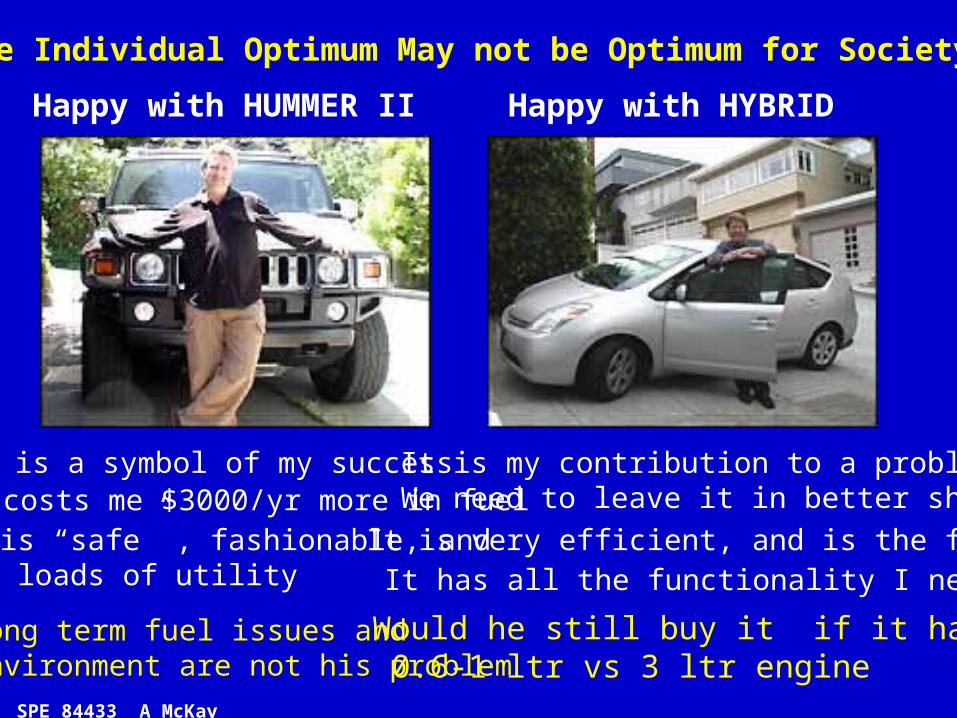

Happy with HUMMER II Happy with HYBRID

It is a symbol of my successIt costs me $3000/yr more in fuelIt is “safe” , fashionable, andHas loads of utility

It is my contribution to a problem,We need to leave it in better shape

It is very efficient, and is the futureIt has all the functionality I need

The Individual Optimum May not be Optimum for Society

SPE 84433 A McKay

Would he still buy it if it had a 0.6-1 ltr vs 3 ltr engine

Long term fuel issues and Environment are not his problem

0123456789

10

Gener

al M

otors

Toyota

Ford

Volksw

agon

Damlie

rChry

sler

PSA/Peu

geot/C

itroen

Hyundai

Auto

motiv

e

Nissa

n

Honda

Renau

lt

Annual Car Sales By Top Ten ManufacturersN

umbe

r of

Car

s (M

lns)

(Does not include Trucks or buses etc)

SPE 84433 A McKay

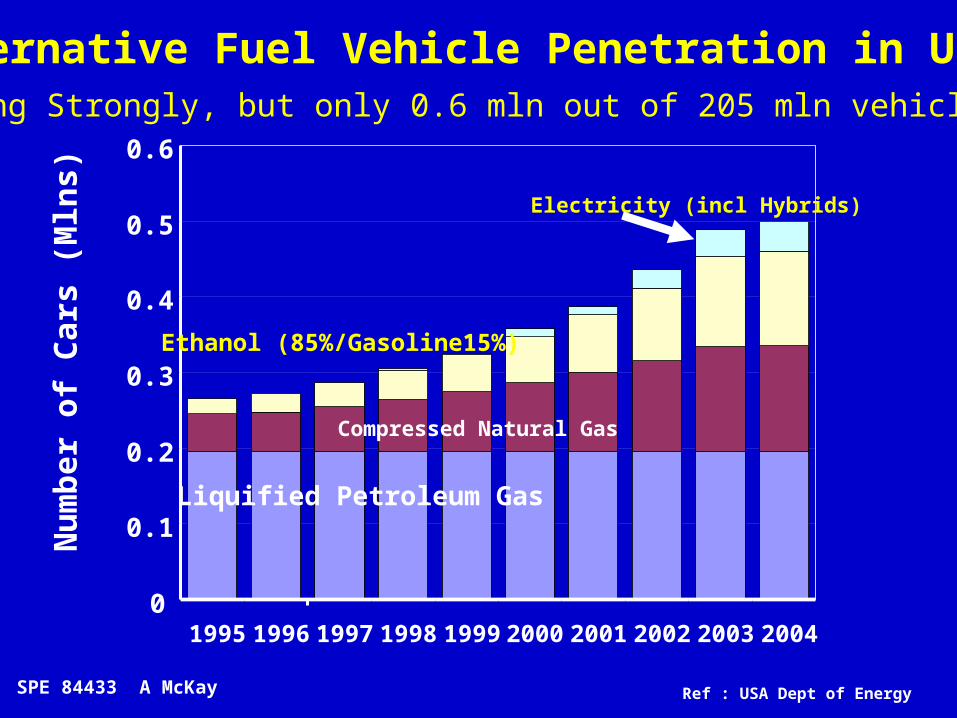

Alternative Fuel Vehicle Penetration in USA N

um

ber

of

Car

s (M

lns)

0

0.1

0.2

0.3

0.4

0.5

0.6

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Electricity (incl Hybrids)

Ethanol (85%/Gasoline15%)

Compressed Natural Gas

Liquified Petroleum Gas

Ref : USA Dept of Energy

Growing Strongly, but only 0.6 mln out of 205 mln vehicles

SPE 84433 A McKay

EP Technology S Curve Evolution

Vertical &Deviated Wells

1970 1980 1990 2000

Time 2010

HydraulicFracturing

HorizontalWells

MultilateralWells

MultilateralMulti-fracced

Wells

Underbalanced Drilling Offshore

HorizontalWells with

Hydraulic Fracturing

Coiled TubingDrilling

Business

Benefits?

Slim HoleExploration

Intelligent Wells

GAINS CONTINUE ?

SPE 84433

CREAMING OCCURS ?[Capital Intensity rises]