Embed Size (px)

Citation preview

SQM: Results for 1H08 and Market Outlook

August 20, 2008

Patricio ContesseChief Executive Officer

Eugenio Ponce Senior Commercial Vice President

2

Important Notice

Statements in this presentation concerning the Company’s business outlook or future economic performances, anticipated profitability, revenues, expenses, or other financial items, anticipated cost synergies and product or service line growth, together with other statements that are not historical facts, are “forward-looking statements” as that term is defined under Federal Securities Laws.

Any forward-looking statements are estimates, reflecting the best judgment of SQM based on currently available information and involve a number of risks, uncertainties and other factors that could cause actual results to differ materially from those stated in such statements.

Risks, uncertainties, and factors that could affect the accuracy of such forward-looking statements are identified in the public filing made with the Securities and Exchange Commission, and forward-looking statements should be considered in light of those factors.

3

Results for 1H08

• Increase in prices of nitrates and potassium-based fertilizers

• Increases in iodine sales volumes

• Higher lithium prices and sales volumes than originally expected

1H08 Net Income

US

$ M

illio

ns

93.9

190.5

0

40

80

120

160

200

240

1H 2007 1H 2008

∆∆∆∆+ 102.8%

51.0

125.7

0

50

100

150

2Q 2007 2Q 2008

2Q08 Net Income

∆∆∆∆+ 146.6%

US

$ M

illio

ns

4

Seven consecutive years of earnings growth: • Quarterly earnings higher than earnings for the same quarter of the previous year

SQM’s long-term development strategy continues to de liver positive results

Results for Last Seven Years: Sustained Growth

Earnings growth observed in 2008 is part of an ongo ing, systematic trend resulting from several factors:

• Capex plan focused on core businesses

• Increases in sales volumes • New products and development of international supply chain • Technological development, innovation and operating flexibility

• Price increases in all our business lines

5

Positive outlook in our main markets:• Nitrates and potassium: favorable pricing conditions

� Growing demand exceeds effective supply � Low inventories of potassium-based fertilizers and grains/cereals

• Significant increase in KCl sales during 2009• Iodine and lithium: sustained demand growth exceeds original projections

Short-Term Expectations

We expect results for the second half of 2008 to be significantly higher than the first half of the year.

The positive trend observed in 2008 should continue in 2009.

6

• Sustained demand growth projected for our core busi nesses• Scarcity of high-quality natural resources

� High investment and operating costs associated with new projects� Implementation of new projects requires long lead-times

• Growing margins on the crops that use our fertilize rs and the industrial products that use iodine and lithium

� Increased margins in the whole supply chain � Opportunity to increase the prices of our products

Structural Changes in our Markets

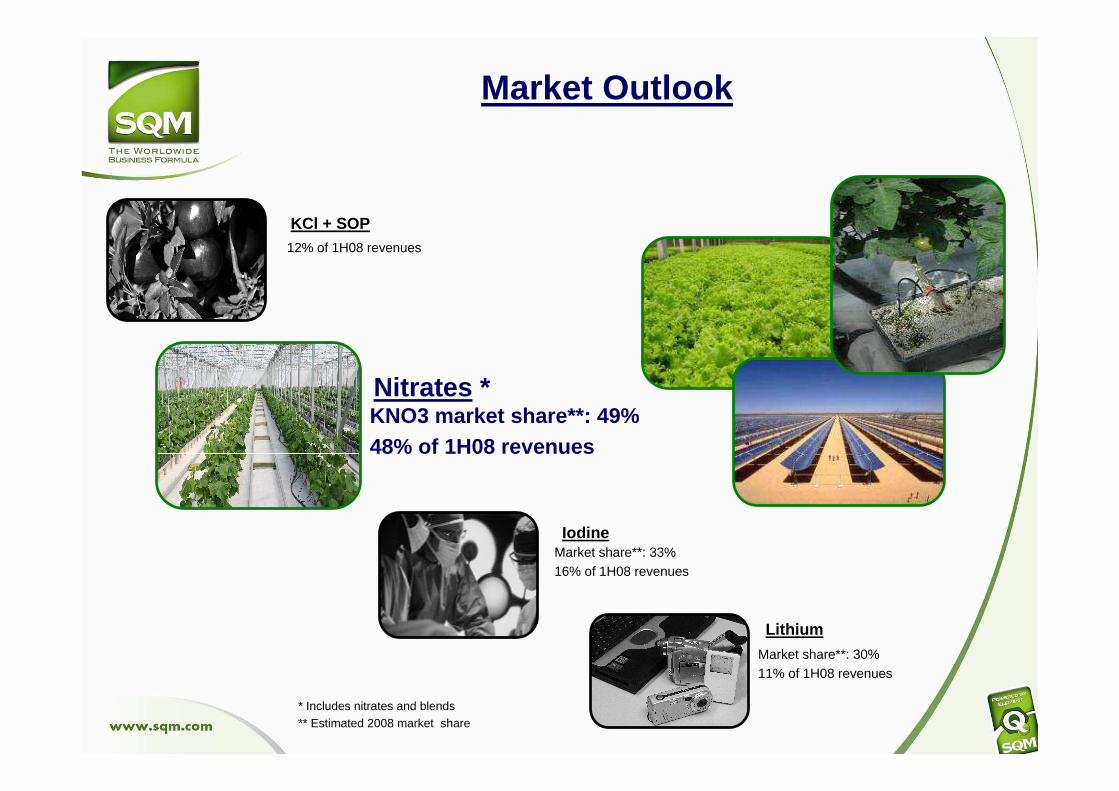

Market share**: 33%16% of 1H08 revenues

Iodine

Nitrates *KNO3 market share **: 49%48% of 1H08 revenues

Lithium

Market share**: 30%11% of 1H08 revenues

KCl + SOP12% of 1H08 revenues

* Includes nitrates and blends ** Estimated 2008 market share

Market Outlook

8

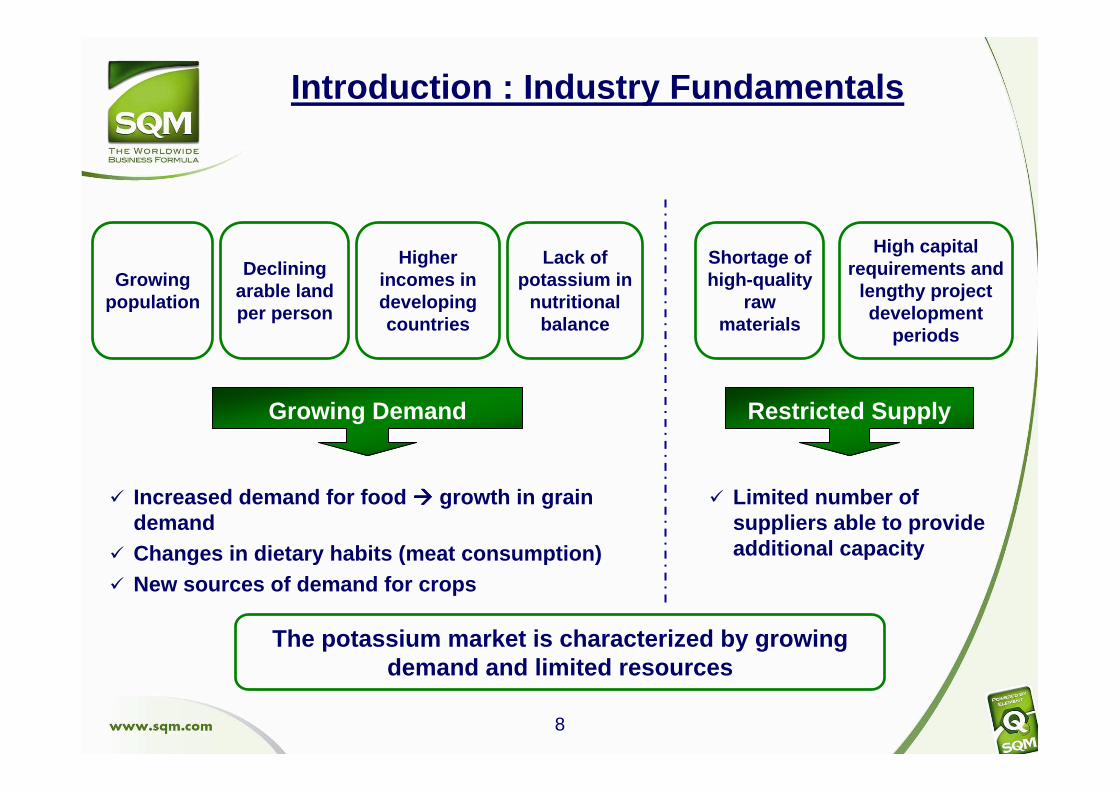

Growing population

Declining arable land per person

Higher incomes in developingcountries

Lack of potassium in

nutritional balance

Shortage of high-quality

raw materials

High capital requirements and

lengthy project development

periods

Growing Demand Restricted Supply

� Increased demand for food ���� growth in grain demand

� Changes in dietary habits (meat consumption)� New sources of demand for crops

� Limited number of suppliers able to provide additional capacity

The potassium market is characterized by growing demand and limited resources

Introduction : Industry Fundamentals

9

0

100

200

300

400

500

600

700

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

E

12%

16%

20%

24%

28%

32%

36%

Inventory Stock-to-Use

Demand: Inventories vs. Consumption

Strong decrease in total grain inventories beginnin g in 2000• Global consumption of grains and oilseeds has exceeded production in 7 of the

last 8 years • Increased food consumption � increased grain demand• Stock-to-use ratio has fallen to 16%, an all-time low (equal to 2 months’ worth

of global consumption)

Source: USDA, PCS

Mill

ions

ofM

T

10 * Source: Fertecon - Odepa

Demand: Crop Prices vs. KCl

0

100

200

300

400

500

600

700

Mar-9

3Nov

-93

Jul-9

4Mar

-95

Nov-9

5Ju

l-96

Mar-9

7Nov

-97

Jul-9

8Mar

-99

Nov-9

9Ju

l-00

Mar-0

1Nov

-01

Jul-0

2Mar

-03

Nov-0

3Ju

l-04

Mar-0

5Nov

-05

Jul-0

6Mar

-07

Nov-0

7Ju

l-08

0

200

400

600

800

1000

1200

1400

Corn (Yellow no. 2, FOB Gulf, USA)

Wheat (Hard red winter no. 2, FOB Gulf, USA)

Soy (FOB Rosario, BB.AA., Argentina)

KCl (FOB Vancouver - Standard)

Crop Prices vs. KCI Prices*C

rop

Pric

es (

US

$ / M

T)

KC

lP

rices (US

$ / MT

)

11 * Source: Merrill Lynch

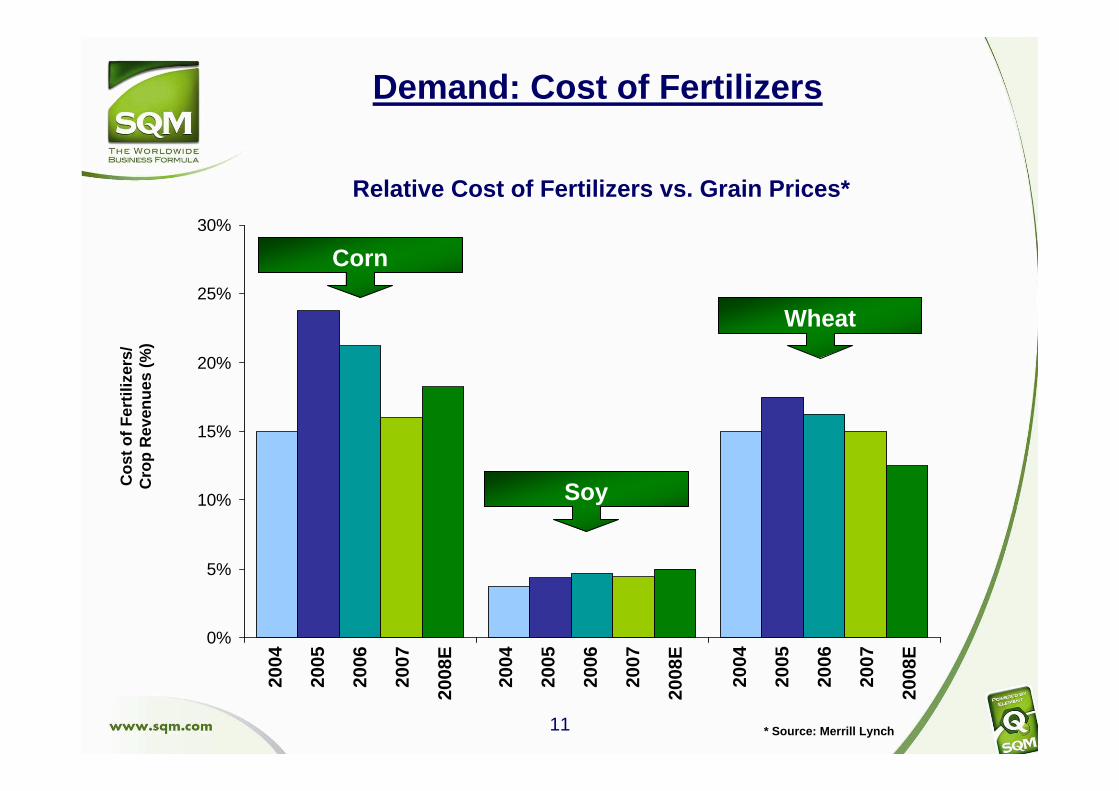

Demand: Cost of Fertilizers

0%

5%

10%

15%

20%

25%

30%

Cos

t of F

ertil

izer

s/

Cro

p R

even

ues

(%)

Relative Cost of Fertilizers vs. Grain Prices*

Corn

Soy

Wheat

2004

2005

2006

2007

2008

E

2004

2005

2006

2007

2008

E

2004

2005

2006

2007

2008

E

12

Demand: Volume Trends

40.8

55.6

0

10

20

30

40

50

60

2000 2001 2002 2003 2004 2005 2006 2007

Mill

ions

ofM

T

KCl Demand*CAGR 2000-2007: 4.5%

• Consumption levels in 2008 are expected to be the same as in 2007, due to insufficient supply

• Beginning in 2009, consumption growth is expected to continue at a rate of approximately of 4.5%

* Source: IFA, British Sulphur

13

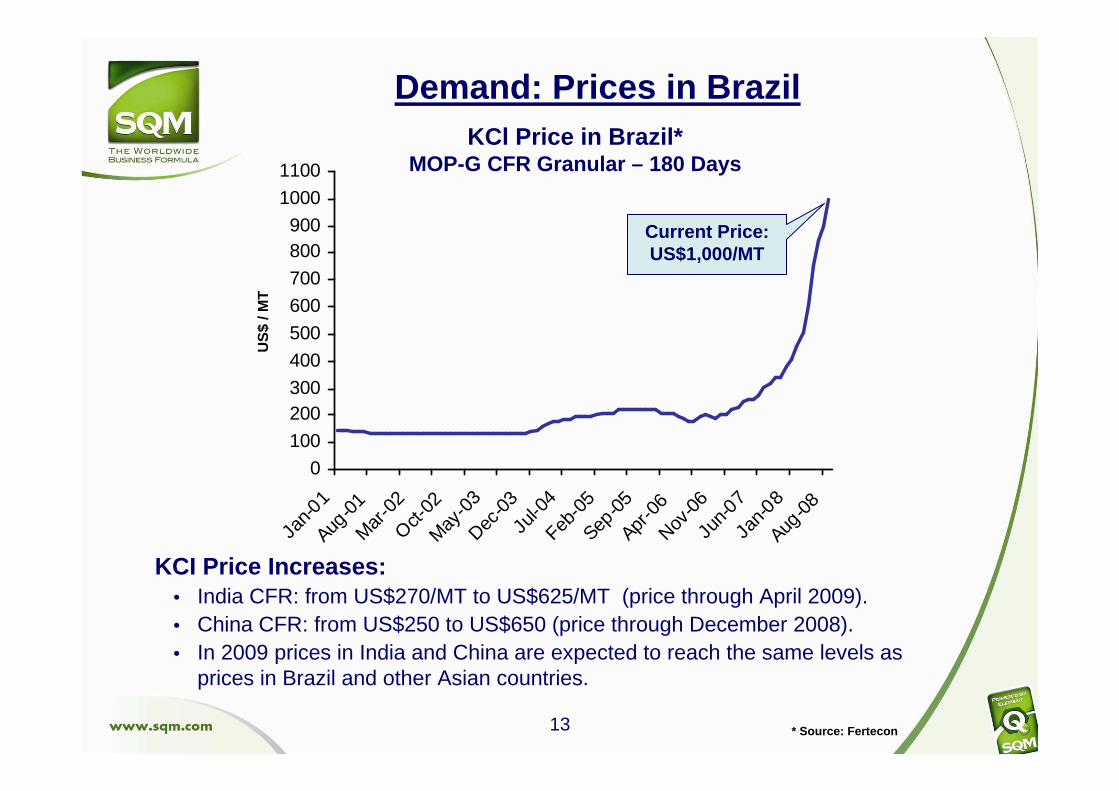

Demand: Prices in Brazil

* Source: Fertecon

0

100

200300

400

500

600

700

800900

1000

1100

Jan-0

1Aug

-01

Mar

-02

Oct-02

May-0

3Dec

-03

Jul-0

4Feb

-05

Sep-0

5Apr

-06

Nov-0

6Ju

n-07

Jan-0

8Aug

-08

KCl Price in Brazil*MOP-G CFR Granular – 180 Days

Current Price: US$1,000/MT

KCI Price Increases:• India CFR: from US$270/MT to US$625/MT (price through April 2009).• China CFR: from US$250 to US$650 (price through December 2008). • In 2009 prices in India and China are expected to reach the same levels as

prices in Brazil and other Asian countries.

US

$/ M

T

14

Projected Supply and Demand Balance

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

2008E 2009E 2010E 2011E 2012E0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

110%Demand Installed Capacity Demand/Capacity

Mill

ions

ofM

T

Source: Fertecon, IFA, British Sulphur

• Capacity utilization rate expected to be close to 9 0% in coming years.

Utilization rate

15

SQM’s Supply: ProjectionT

hous

ands

of

MT

* SQM estimates. Sales of KNO3 are projected to increase in 2009 and to increase significantly in 2010. Consequently, a significant part of the KCl production will be used in the production of KNO3. Current projections indicate that in 2009 SQM will sell approximately 100,000 MT of inventory generated during 2008. These figures may change significantly, depending on effective production, the start-up dates for the potassium expansions and the start-up dates for the KNO3 expansion.

820900

10001100

0

200

400

600

800

1000

1200

2008E 2009E 2010E 2011E

330

500-550500-550550-600

0

100

200

300

400

500

600

700

2008E 2009E 2010E 2011E

KCl + SOP Production * KCl + SOP Sales *

Tho

usan

ds o

f M

T

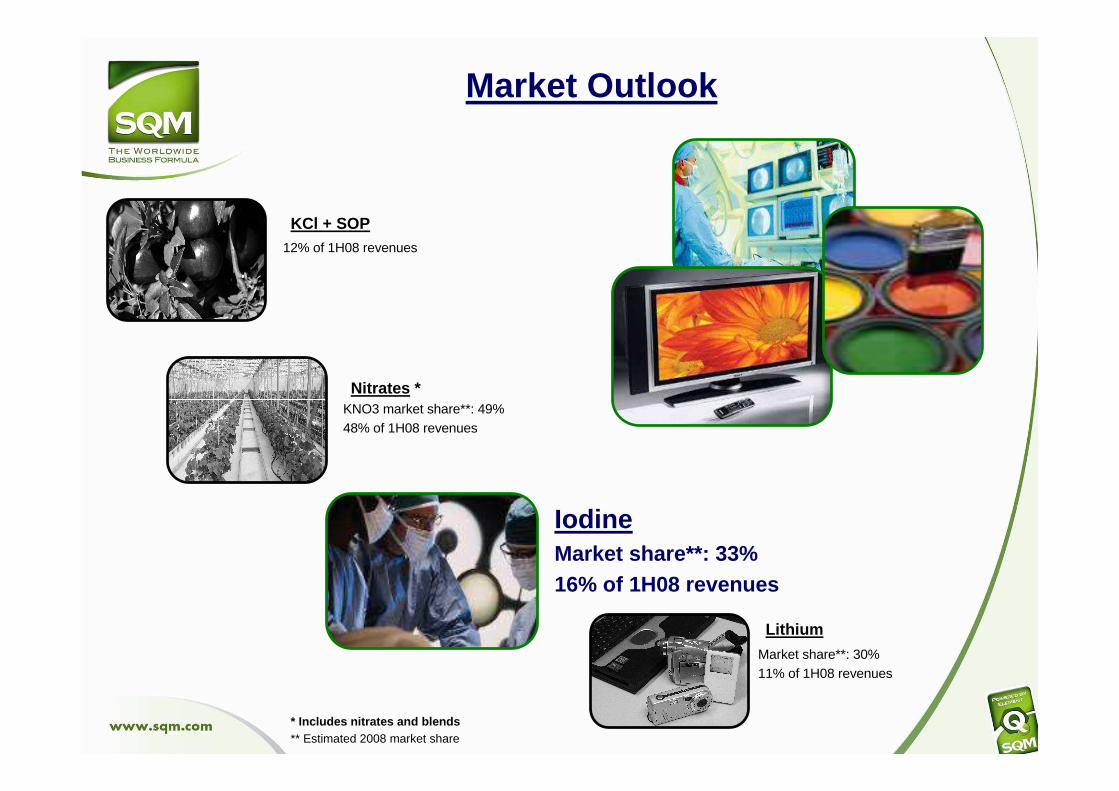

Market share**: 33%16% of 1H08 revenues

Iodine

Lithium

Market share**: 30%11% of 1H08 revenues

Nitrates *KNO3 market share**: 49%48% of 1H08 revenues

KCl + SOP12% of 1H08 revenues

Market Outlook

* Includes nitrates and blends** Estimated 2008 market share

17

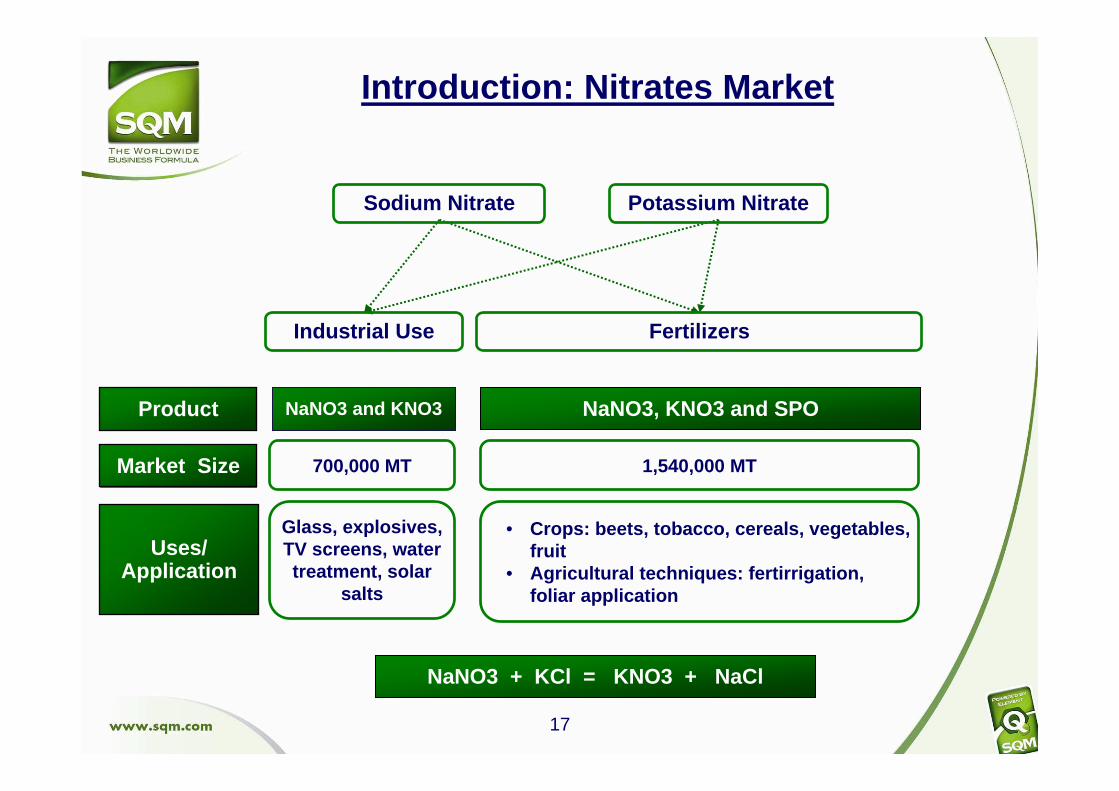

Market Size

Uses/ Application

Product NaNO3 and KNO3 NaNO3, KNO3 and SPO

Sodium Nitrate Potassium Nitrate

Industrial Use Fertilizers

Introduction: Nitrates Market

700,000 MT

Glass, explosives, TV screens, water treatment, solar

salts

1,540,000 MT

• Crops: beets, tobacco, cereals, vegetables, fruit

• Agricultural techniques: fertirrigation, foliar application

NaNO3 + KCl = KNO3 + NaCl

18

Demand for agricultural potassium nitrate:• Demand Growth : during the last 10 years, the CAGR has been close to 5%.

• Soluble Segment : scarcity of water, high cost of land and growing demand for high-quality fruits and vegetables have driven the growth of modern agricultural techniques (Micro-irrigation, hydroponics, greenhousing, etc.)

• Geographic Area : KNO3 demand has increased substantially in countries like China, India, Turkey, México, Middle East countries.

Demand: Agricultural KNO3

1.11.7

3.2

6.0

0.5

0.0

1.5

3.0

4.5

6.0

7.5

1980 1986 1991 2000 2006

Global Micro-Irrigation Surface Area**CAGR: 10%

Mill

ions

ofhe

ctar

es

KNO3 Prices and Demand*

KN

O3 P

rice(U

S$

/ MT

)

* SQM estimates for 2008

** Source: ICID

Dem

and

(tho

usan

dsof

MT

)

853

607

0

100

200

300

400

500

600

700

800

900

2002 2003 2004 2005 2006 2007 2008 E

0

200

400

600

800

1,000

1,200

1,400Demand Average Price

19

Demand for industrial-grade potassium nitrate and s odium nitrate• Demand for current applications has been stable• New demand for storage of thermal energy in solar energy plants will significantly

increase the consumption of nitrates� Mixture of sodium nitrate and potassium nitrate� 50 projects will be developed in the next 5 years.

Demand: Industrial Nitrates

28 48

250300

350

100

100

200

300

400

500

2007 2008E 2009E 2010E 2011E 2012E

Projected Demand for Solar Salts*

Tho

usan

dsof

MT

* SQM estimates

Price

(US

$/ M

T)

Dem

and

(tho

usan

dsof

MT

)

Industrial Nitrates Prices and Demand*

358381

0

50

100

150

200

250

300

350

400

450

2003 2004 2005 2006 2007 2008 E

0

100

200

300

400

500

600

700

800Demand Average Price

20

Main Projects• ACS Cobra-Sener, Man Solar Millenium, Abengoa, Acciona, SAMCA,

Endesa España, Ibereolica

Demand: Solar Salts Projects

21

Projected Supply and Demand Balance

0

500

1,000

1,500

2,000

2,500

20052006

20072008E

2009E2010E

2011E2012E

2013E2014E

2015E

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

110%Demand Installed Capacity Demand/Capacity

Tho

usan

dsof

MT

SQM estimates

• Capacity utilization rate expected to be close to 1 00% in comingyears.

Utilization

Rate

Market Outlook

Lithium

Market share**: 30%11% of 1H08 revenues

* Includes nitrates and blends** Estimated 2008 market share

KCl + SOP12% of 1H08 revenues

Nitrates *KNO3 market share**: 49%48% of 1H08 revenues

IodineMarket share**: 33%16% of 1H08 revenues

23

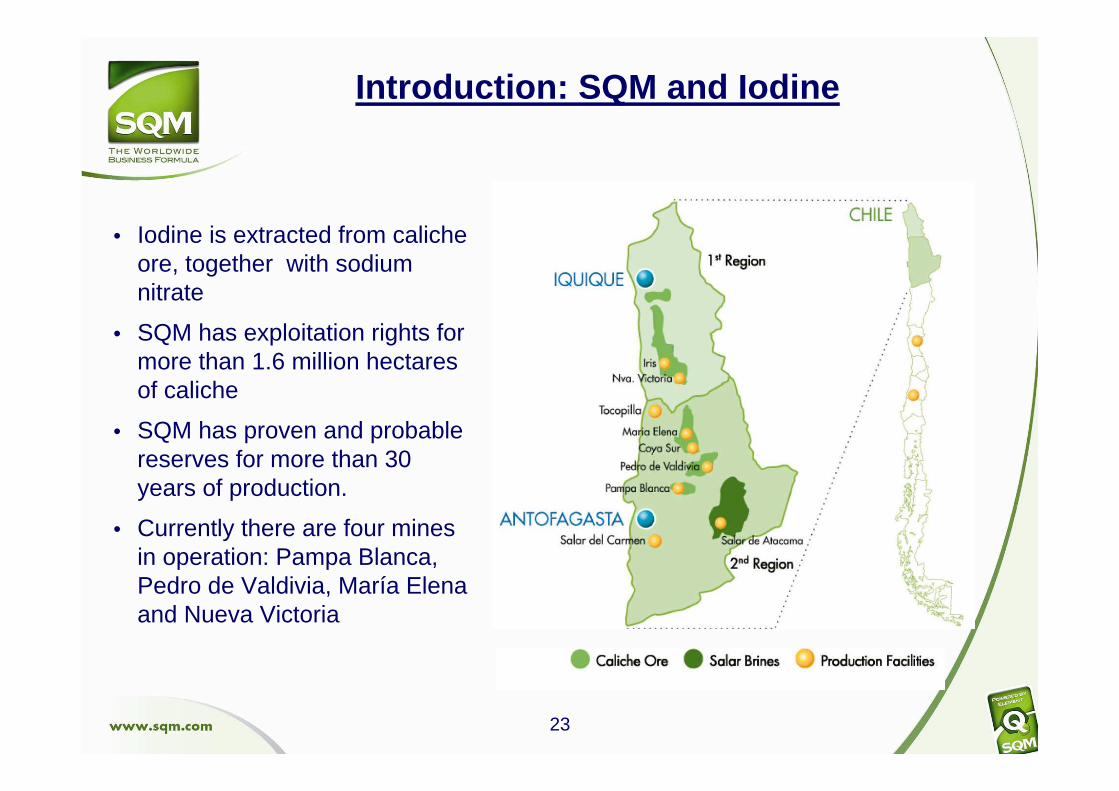

• Iodine is extracted from caliche ore, together with sodiumnitrate

• SQM has exploitation rights formore than 1.6 million hectaresof caliche

• SQM has proven and probable reserves for more than 30 years of production.

• Currently there are four mines in operation: Pampa Blanca, Pedro de Valdivia, María Elena and Nueva Victoria

Introduction: SQM and Iodine

24

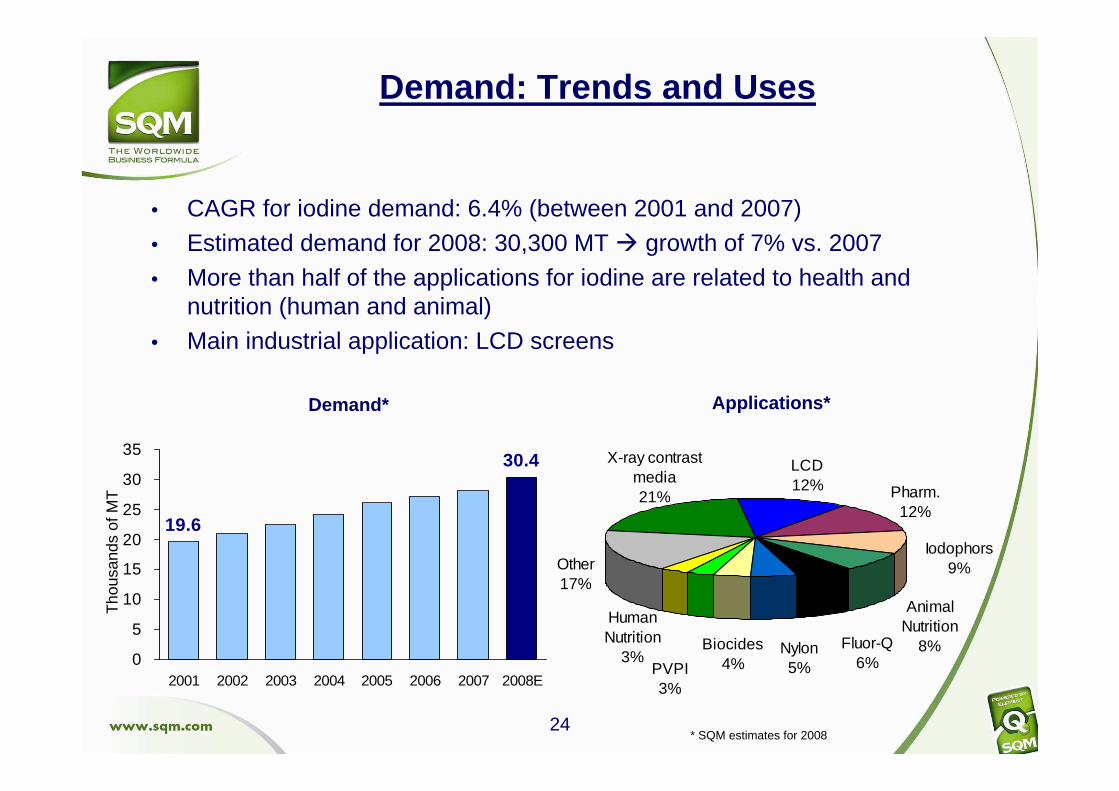

• CAGR for iodine demand: 6.4% (between 2001 and 2007)• Estimated demand for 2008: 30,300 MT � growth of 7% vs. 2007

• More than half of the applications for iodine are related to health andnutrition (human and animal)

• Main industrial application: LCD screens

Demand: Trends and Uses

19.6

30.4

0

5

10

15

20

25

30

35

2001 2002 2003 2004 2005 2006 2007 2008E

Demand*

Tho

usan

dsof

MT

Applications*

LCD12% Pharm.

12%

X-ray contrast media21%

PVPI3%

Human Nutrition

3%

Other17%

Biocides4%

Nylon5%

Animal Nutrition

8%Fluor-Q6%

Iodophors9%

* SQM estimates for 2008

25

Iodine demand is expected to grow at an average rat e of 3.5% - 4.0% in the next ten years, reaching a total of 43,000 MT in 2018

• The LCD application will have an important role, with an expected average growth rate of 7.5% between 2008 and 2018

• Another demand driver in the future will be the use of iodine as an agrochemical. Demand for this new use is expected to reach approximately 2,200 MT in 2018

Projected Demand

25

30

35

40

45

2008

E

2009

E

2010

E

2011

E

2012

E

2013

E

2014

E

2015

E

2016

E

2017

E

2018

E

Agrochemicals

Other Applications

Tho

usan

dsof

MT

43

Projected Iodine Demand*

* SQM estimates

30

26

Japan21% Others

6%

Recycling11%

USA4%

Others Chile25%

SQM33%

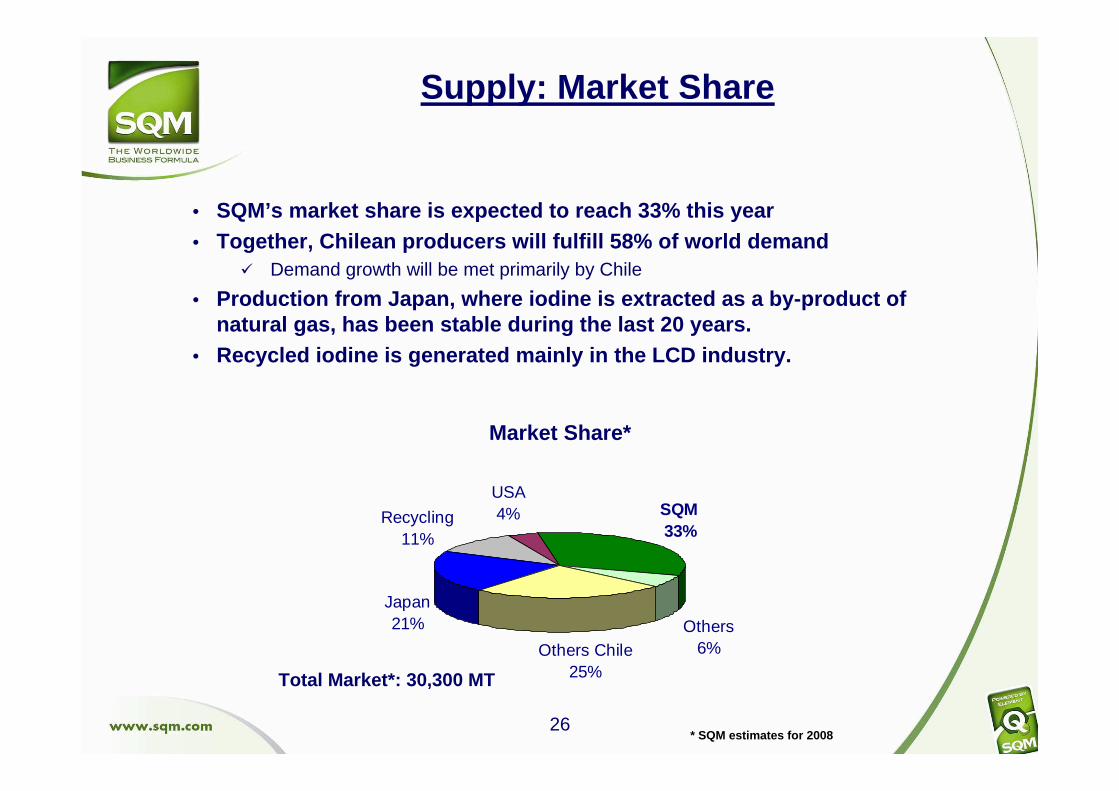

• SQM’s market share is expected to reach 33% this yea r• Together, Chilean producers will fulfill 58% of wor ld demand

� Demand growth will be met primarily by Chile

• Production from Japan, where iodine is extracted as a by-product of natural gas, has been stable during the last 20 yea rs.

• Recycled iodine is generated mainly in the LCD indu stry.

Supply: Market Share

Market Share*

Total Market*: 30,300 MT

* SQM estimates for 2008

27

20

25

30

35

40

45

50

2008E 2009E 2010E 2011E 2012E 2013E 2014E 2015E 2016E 2017E 2018E0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

110%Demand Installed Capacity Demand/Capacity

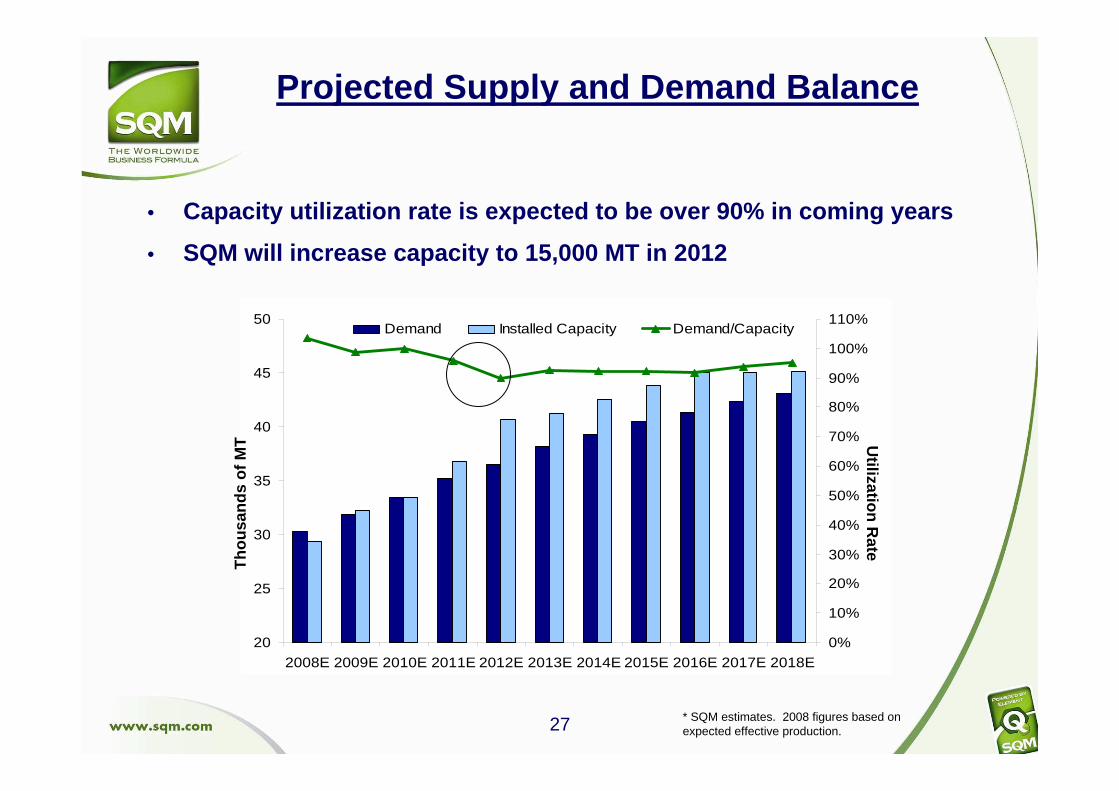

• Capacity utilization rate is expected to be over 90 % in coming years

• SQM will increase capacity to 15,000 MT in 2012T

hous

ands

ofM

T

* SQM estimates. 2008 figures based onexpected effective production.

Utilization

Rate

Projected Supply and Demand Balance

Market Outlook

* Includes nitrates and blends** Estimated 2008 market share

KCl + SOP12% of 1H08 revenues

Nitrates *KNO3 market share**: 49%48% of 1H08 revenues

Market share**: 33%16% of 1H08 revenues

Iodine

LithiumMarket share**: 30%11% of 1H08 revenues

29

• The Salar de Atacama contains the best and most abundant commercially exploitable reserves in the world

• These reserves are located in the core of the Salar de Atacama, a salt-encrusted depression within the Atacama Desert, which contains deposits of brines fed by an underground inflow of water from the Andes Mountains

Introduction: SQM and Lithium

• The brines from the Salar de Atacama have sustainable competitive advantages on a global level, because they have the highest concentrations of potassium, lithium and boron

30

Frits9%

Lubricating Greases

12%

Glass8%

Batteries27%

Otros38%

A/C6%

95

59

40

50

60

70

80

90

100

110

2001 2002 2003 2004 2005 2006 2007 2008E

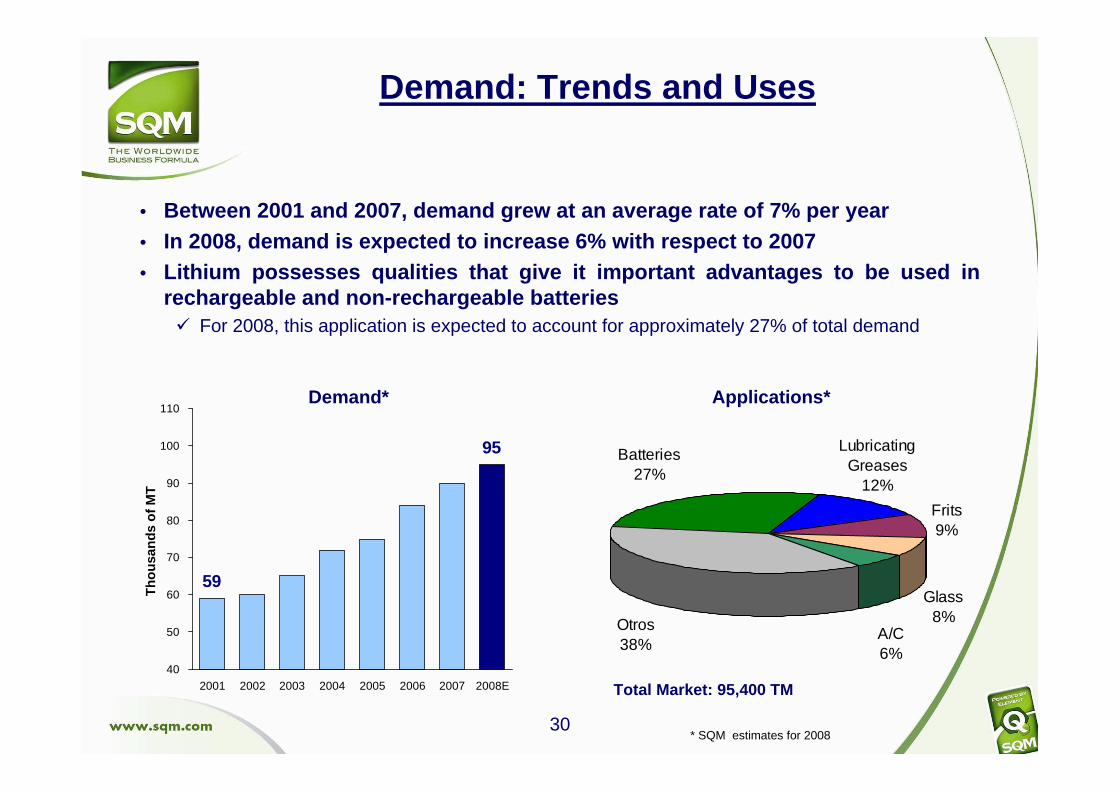

• Between 2001 and 2007, demand grew at an average ra te of 7% per year• In 2008, demand is expected to increase 6% with res pect to 2007 • Lithium possesses qualities that give it important advantages to be used in

rechargeable and non-rechargeable batteries� For 2008, this application is expected to account for approximately 27% of total demand

Demand: Trends and Uses

Demand* Applications*

Tho

usan

dsof

MT

Total Market: 95,400 TM

* SQM estimates for 2008

31

• Expected growth in lithium demand (2008 – 2018): ove r 5% per year• Rechargeable batteries should drive growth, with ra tes near 10% per year

� By 2018 batteries should account for 42% of total demand (2008: 27%)

• Within the batteries market, the batteries with gre ater growth potential are those that are more lithium-intensive, such as batteries for e lectric vehicles.

Projected Demand

Projected Lithium Demand*

80

100

120

140

160

2008

E20

09E

2010

E20

11E

2012

E20

13E

2014

E20

15E

2016

E20

17E

2018

E

Batteries for VehiclesOther Applications

Tho

usan

dsof

MT

* SQM estimates

95

158

32

Demand: Hybrid and Electric Vehicles

• There is a consensus in the industry that lithium batteries are the best option to store energy in electric and hybrid electric vehicles (HEVs).

• In 2007 more than half a million hybrid vehicles were sold

� Toyota is the main manufacturer of HEVs, with its Prius model being the best-selling car in this category.

� By 2012 the number of electric and hybrid electric vehicles could exceed 2 million units.

• Some estimates indicate that the first HEVs using lithium-ion batteries will be available for sale by the end of 2009.

• This application has significant potential for the lithium market. A battery for a hybrid or electric vehicle should contain between 1 and 5 kilograms of lithium-carbonate equivalent.

• By 2018, batteries for hybrid and electric vehicles could account for between 10% and 15% of total demand.

33

• SQM is the main producer of lithium, with an estimated marke tshare of approximately 30% for 2008.

Supply: Market Share

FMC17%

Chemetall28%

Others1%

China24%

SQM30%

Market Share 2008*

Total Market: 95,400 MT

* SQM estimates for 2008

34

80

100

120

140

160

180

2008

E

2009

E20

10E

2011

E20

12E

2013

E

2014

E20

15E

2016

E20

17E

2018

E

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

110%Demand Installed Capacity Demand/Capacity

• SQM: Capacity expansion to 40,000 MT LCE is complet e• China: New operations have been announced, but ther e is still uncertainty

regarding actual production capacities• Capacity utilization rate is expected to be over 90 % in coming years

* SQM estimates. Balance will depend on effective capacity of China

Tho

usan

ds o

f MT

Utilization

Rate

Projected Supply and Demand Balance