Embed Size (px)

Citation preview

GOTHAM SOUNDPRESENTS

2017 TAX UPDATEFEBRUARY 18, 2018

Nancy L. Adams, CPASullivan, Field & Smith, LLC1468 S. Saint Francis Drive

Santa Fe, NM [email protected]

Ph: (505) 982-4901

Deborah Hammett, CPAAdelman, Katz & Mond, LLP230 West 41st Street, 15th Fl

New York, NY [email protected]

Ph: (212) 382-0404

Nancy L. Adams recently moved to Santa Fe, NM and is a partner in the firm of Sullivan, Field & Smith, LLC. She has been a CPA for approximately 30 years. She has a Masters in Taxation from Pace University. She is a member of the American Institute of Certified Public Accountants (AICPA) and the New York State Society of CPAs (NYSSCPAs), where she is a member of the Entertainment Committee. She specializes in working with clients in the entertainment industry, including documentary filmmakers, feature filmmakers, talent and other production personnel.

Debbie Hammett is a supervisor at Adelman Katz & Mond LLP. She has been a CPA for approximately 15 years. She has a MBA in taxation/international business from Pace University. She is a member of the American Institute of Certified Public Accountants (AICPA), the New York State Society of CPAs (NYSSCPAs), where she is co-chair of the Closely Held and S Corp Committee, NY Tax Study Group, Accountant’s Club of America and the Estate Planning Council of NYC. She works with a number of entertainment entities, including the production companies of a well known entertainment personality.

OBJECTIVES

▶ DISCUSS THE BASIS OF TAX DEDUCTIONS

▶ COMPARE RULES IN EFFECTS FOR TAX YEAR 2017 TO 2018

▶ PLANNING OPPORTUNITIES IN 2018

The presentation is designed to address tax considerations for entertainment professionals. It is not intended to be a complete recap of the new tax laws.

Tax Deductions – Basics

▶ IRC Section 162 allows one engaged in “Trade or Business” to deduct expenses that are ordinary & necessary

▶ Trade or Business is not defined in the Code, but has come to mean an activity carried on for profit or as one’s livelihood

▶ Ordinary and necessary – facts and circumstances test (appropriate and common to one’s industry)

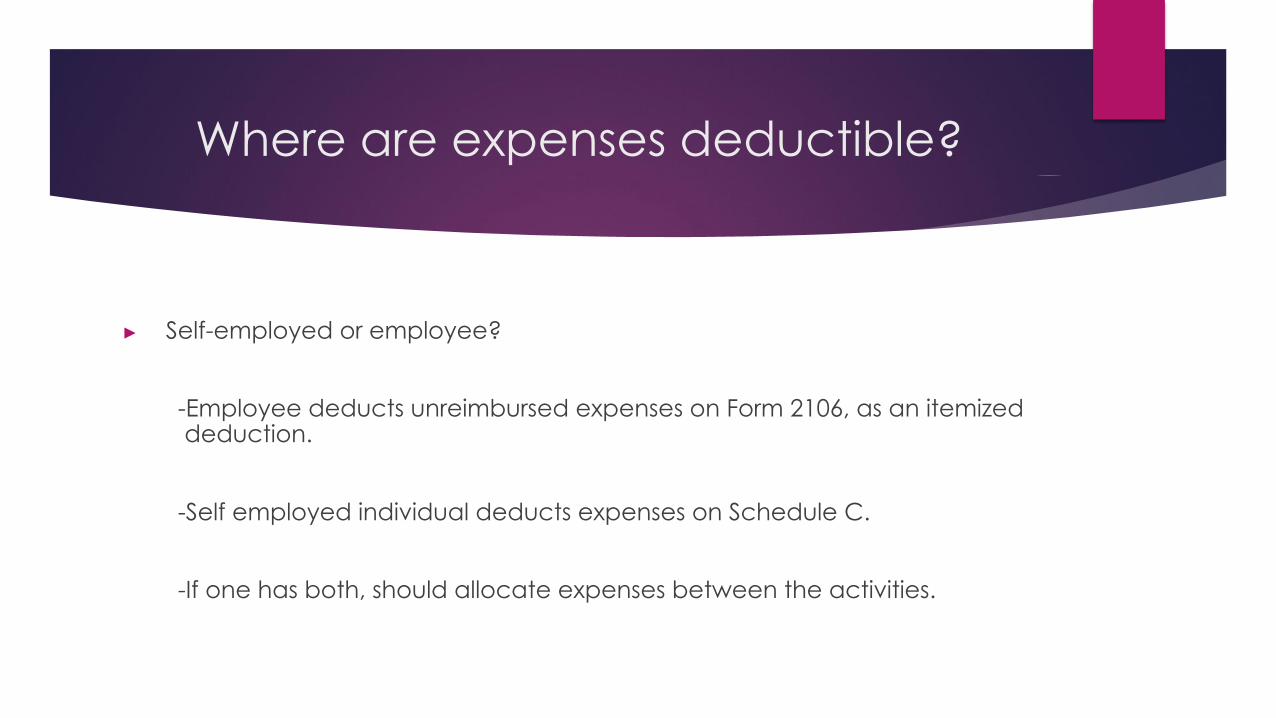

Where are expenses deductible?

▶ Self-employed or employee?

-Employee deducts unreimbursed expenses on Form 2106, as an itemized deduction.

-Self employed individual deducts expenses on Schedule C.

-If one has both, should allocate expenses between the activities.

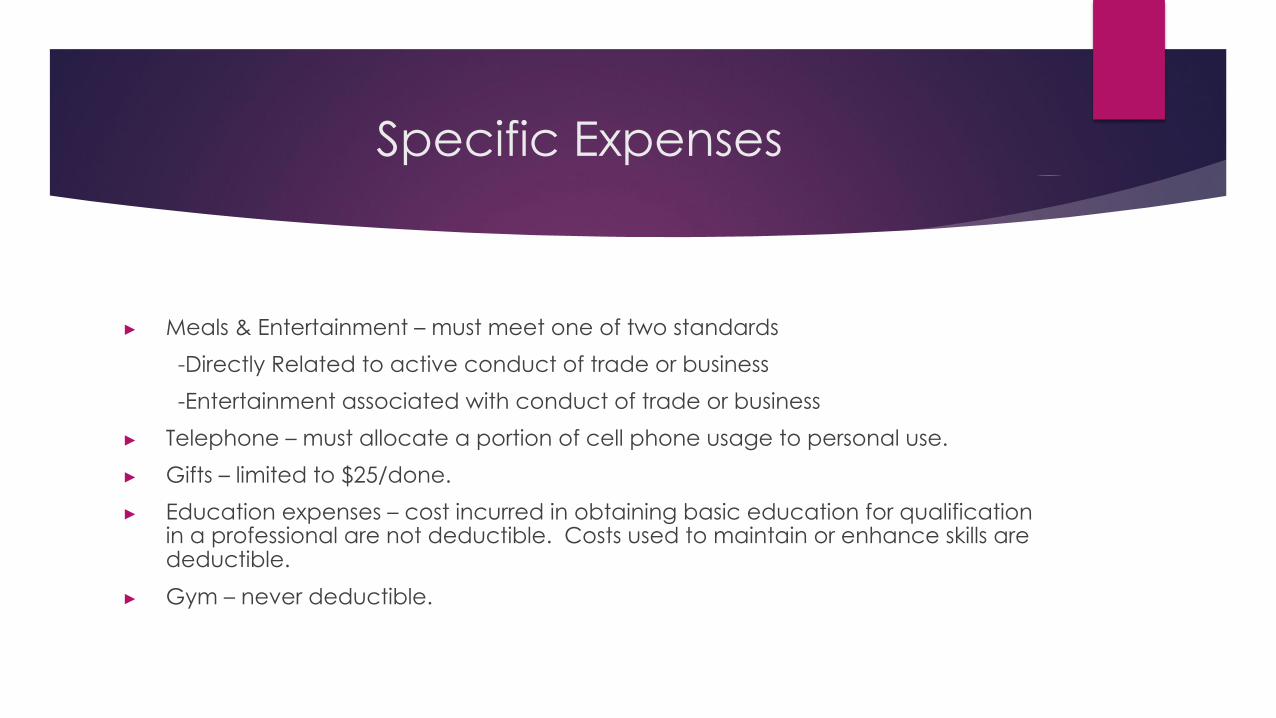

Specific Expenses

▶ Meals & Entertainment – must meet one of two standards-Directly Related to active conduct of trade or business-Entertainment associated with conduct of trade or business

▶ Telephone – must allocate a portion of cell phone usage to personal use.▶ Gifts – limited to $25/done.▶ Education expenses – cost incurred in obtaining basic education for qualification

in a professional are not deductible. Costs used to maintain or enhance skills are deductible.

▶ Gym – never deductible.

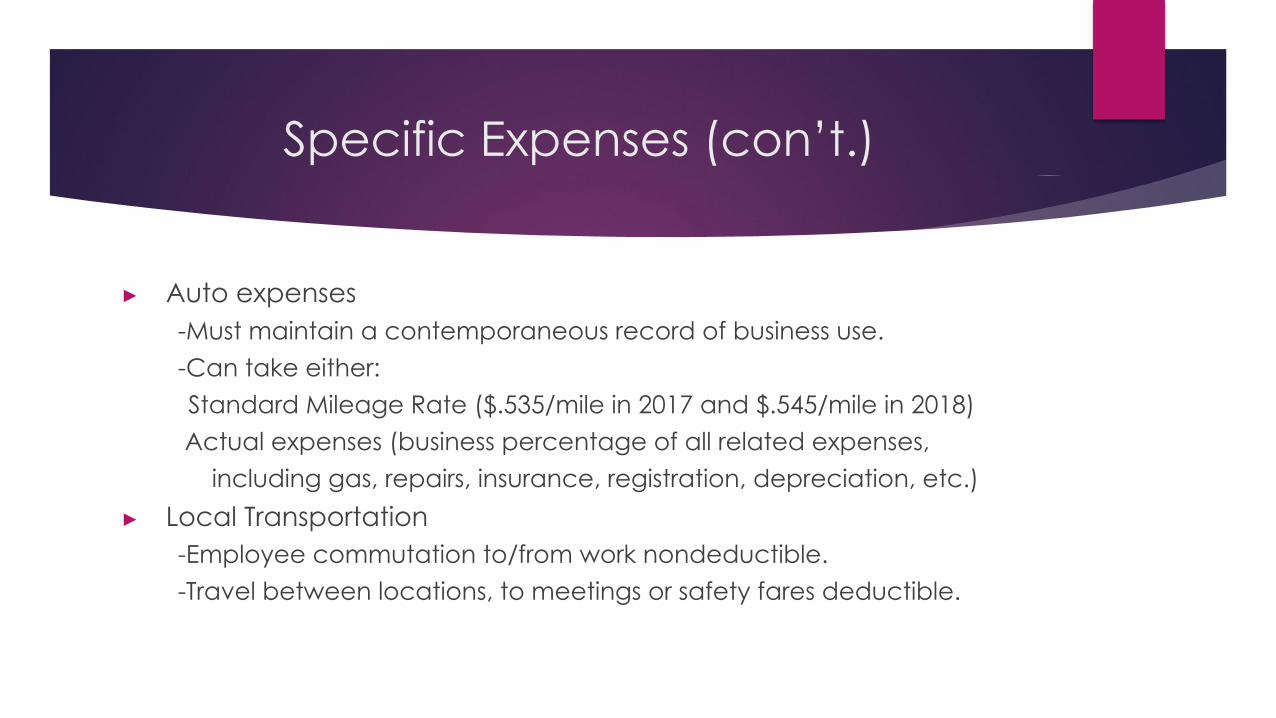

Specific Expenses (con’t.)

▶ Auto expenses-Must maintain a contemporaneous record of business use.-Can take either: Standard Mileage Rate ($.535/mile in 2017 and $.545/mile in 2018) Actual expenses (business percentage of all related expenses,

including gas, repairs, insurance, registration, depreciation, etc.)▶ Local Transportation

-Employee commutation to/from work nondeductible.-Travel between locations, to meetings or safety fares deductible.

Specific Expenses (con’t.)

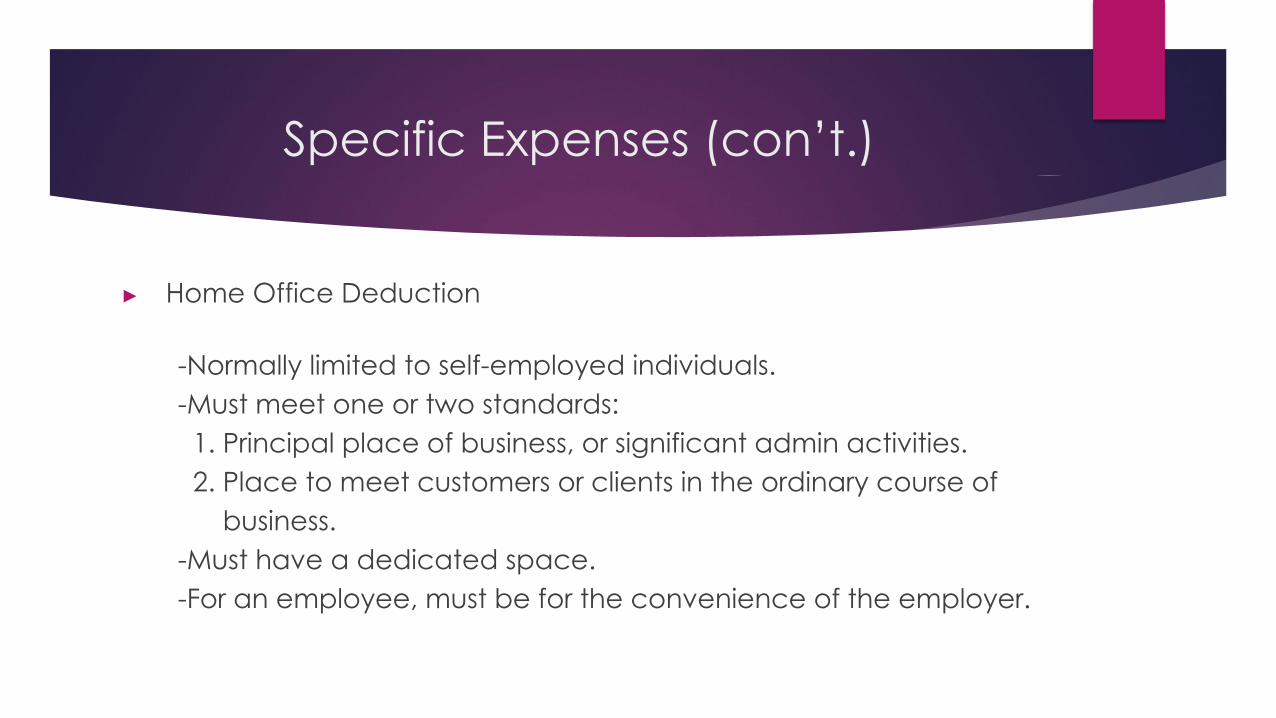

▶ Home Office Deduction

-Normally limited to self-employed individuals.-Must meet one or two standards: 1. Principal place of business, or significant admin activities. 2. Place to meet customers or clients in the ordinary course of business.-Must have a dedicated space.-For an employee, must be for the convenience of the employer.

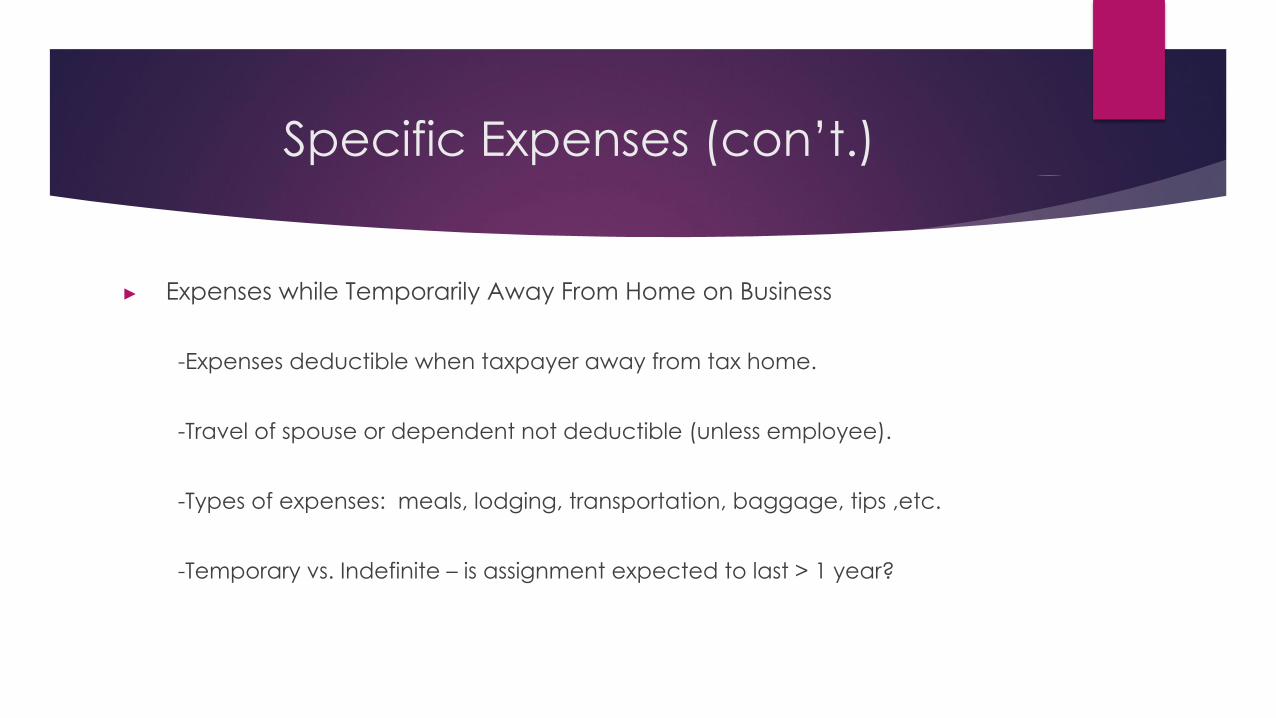

Specific Expenses (con’t.)

▶ Expenses while Temporarily Away From Home on Business

-Expenses deductible when taxpayer away from tax home.

-Travel of spouse or dependent not deductible (unless employee).

-Types of expenses: meals, lodging, transportation, baggage, tips ,etc.

-Temporary vs. Indefinite – is assignment expected to last > 1 year?

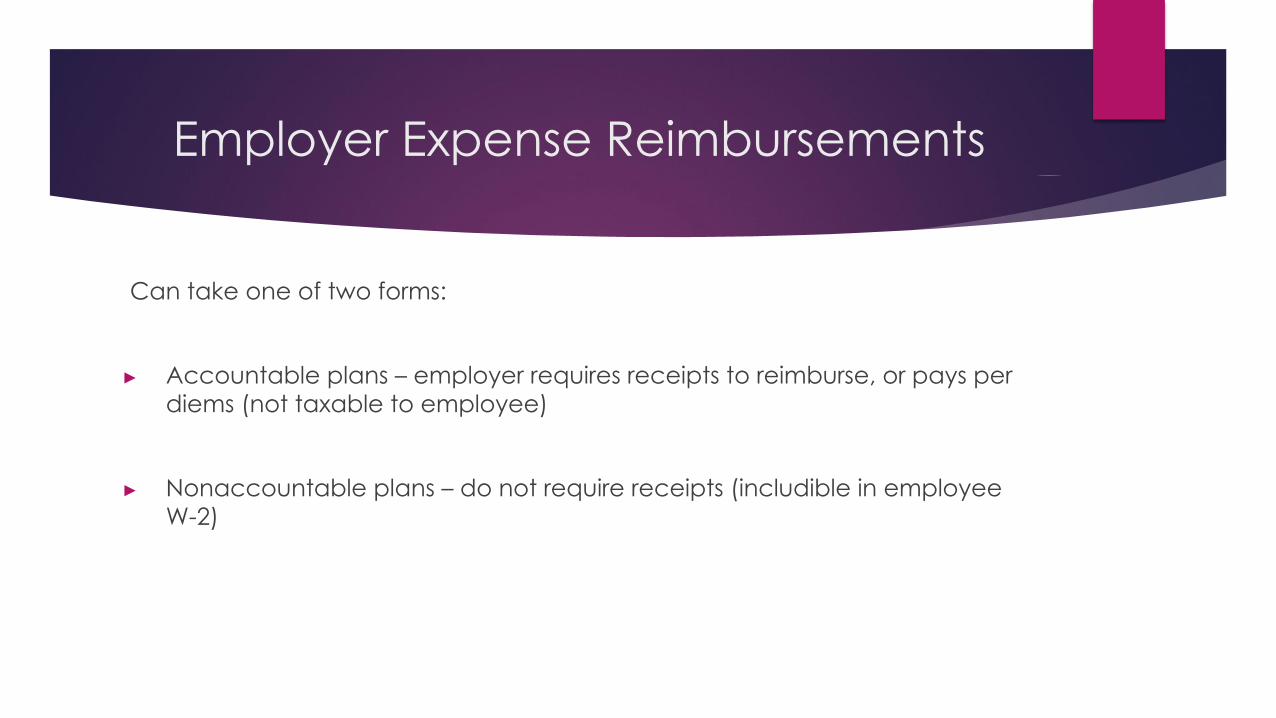

Employer Expense Reimbursements

Can take one of two forms:

▶ Accountable plans – employer requires receipts to reimburse, or pays per diems (not taxable to employee)

▶ Nonaccountable plans – do not require receipts (includible in employee W-2)

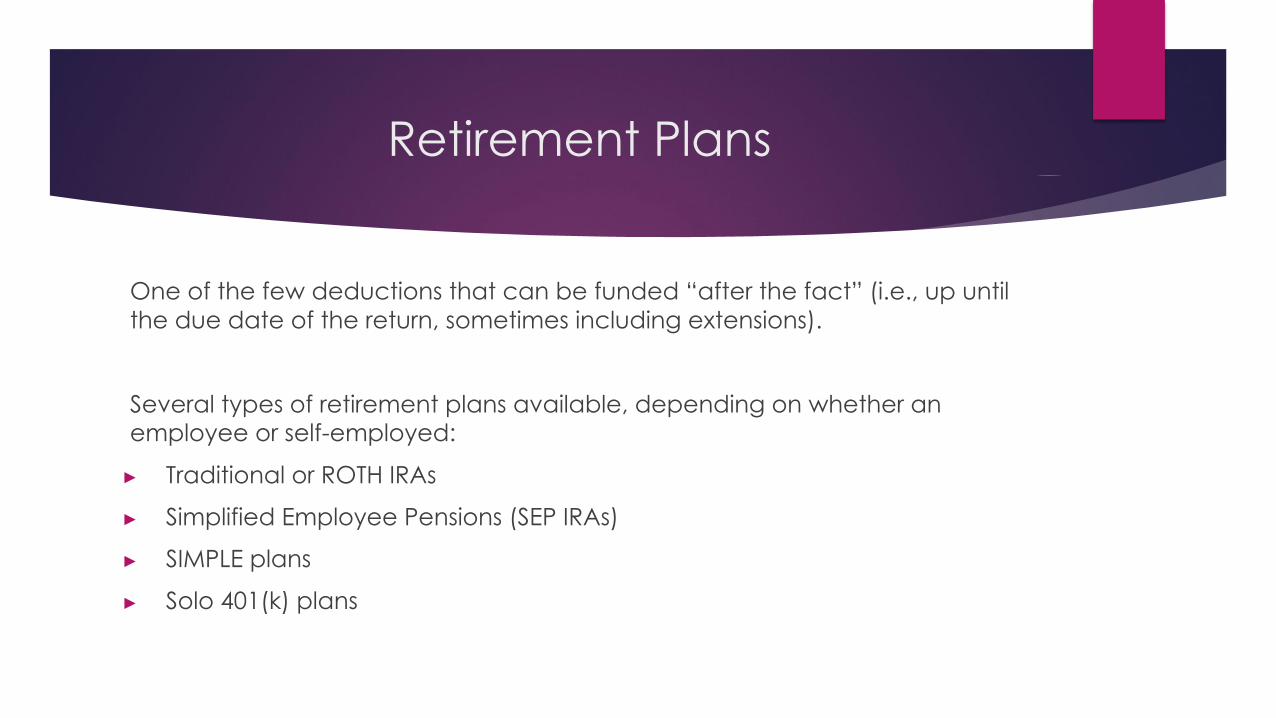

Retirement Plans

One of the few deductions that can be funded “after the fact” (i.e., up until the due date of the return, sometimes including extensions).

Several types of retirement plans available, depending on whether an employee or self-employed:

▶ Traditional or ROTH IRAs

▶ Simplified Employee Pensions (SEP IRAs)

▶ SIMPLE plans

▶ Solo 401(k) plans

COMPARISON OF 2017 AND 2018

2017▶ Tax Rates – range from 10% - 39.6%

▶ Exemptions - $4,050 for taxpayer, spouse and any dependents

▶ Standard DeductionSingle $ 6,350

HOH $ 9,350

MFJ $12,700

2018▶ Tax Rates – range from 10% - 37%

▶ Exemptions – eliminated

▶ Standard DeductionSingle $12,000

HOH $18,000

MFJ $24,000

COMPARISON OF 2017 AND 2018 (con’t)

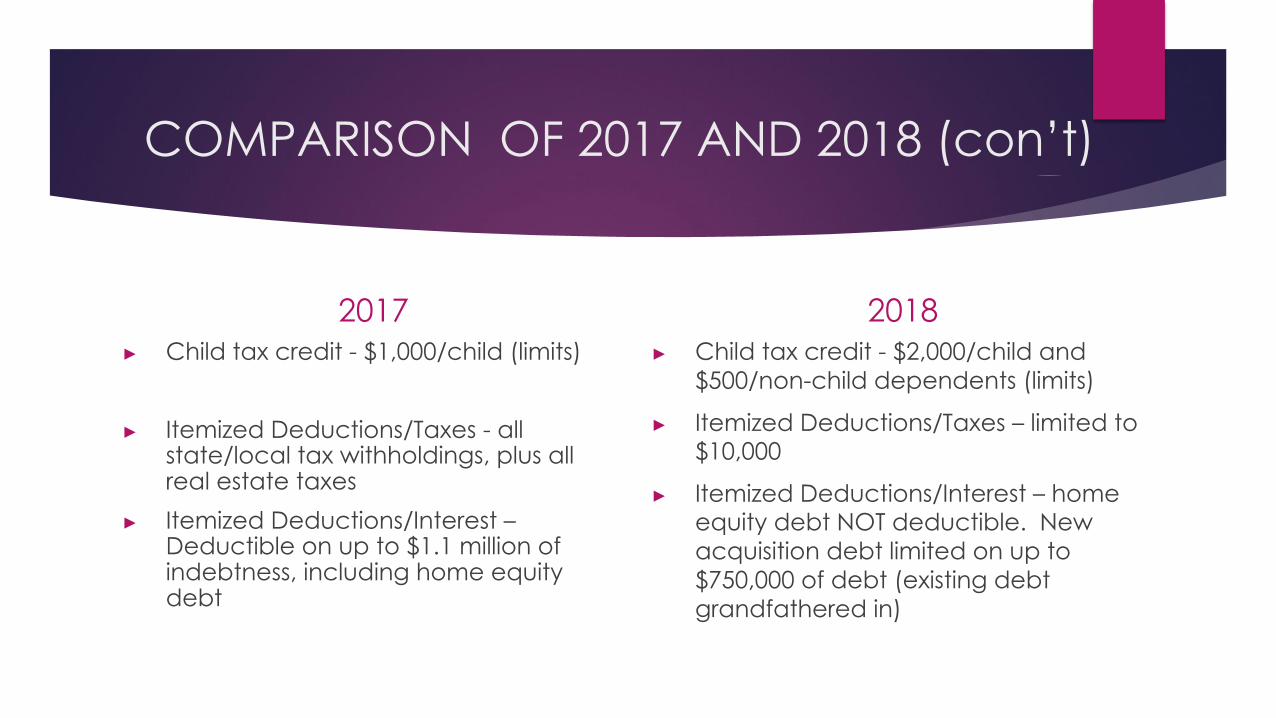

2017▶ Child tax credit - $1,000/child (limits)

▶ Itemized Deductions/Taxes - all state/local tax withholdings, plus all real estate taxes

▶ Itemized Deductions/Interest – Deductible on up to $1.1 million of indebtness, including home equity debt

2018▶ Child tax credit - $2,000/child and

$500/non-child dependents (limits)

▶ Itemized Deductions/Taxes – limited to $10,000

▶ Itemized Deductions/Interest – home equity debt NOT deductible. New acquisition debt limited on up to $750,000 of debt (existing debt grandfathered in)

COMPARISON OF 2017 AND 2018 (con’t)

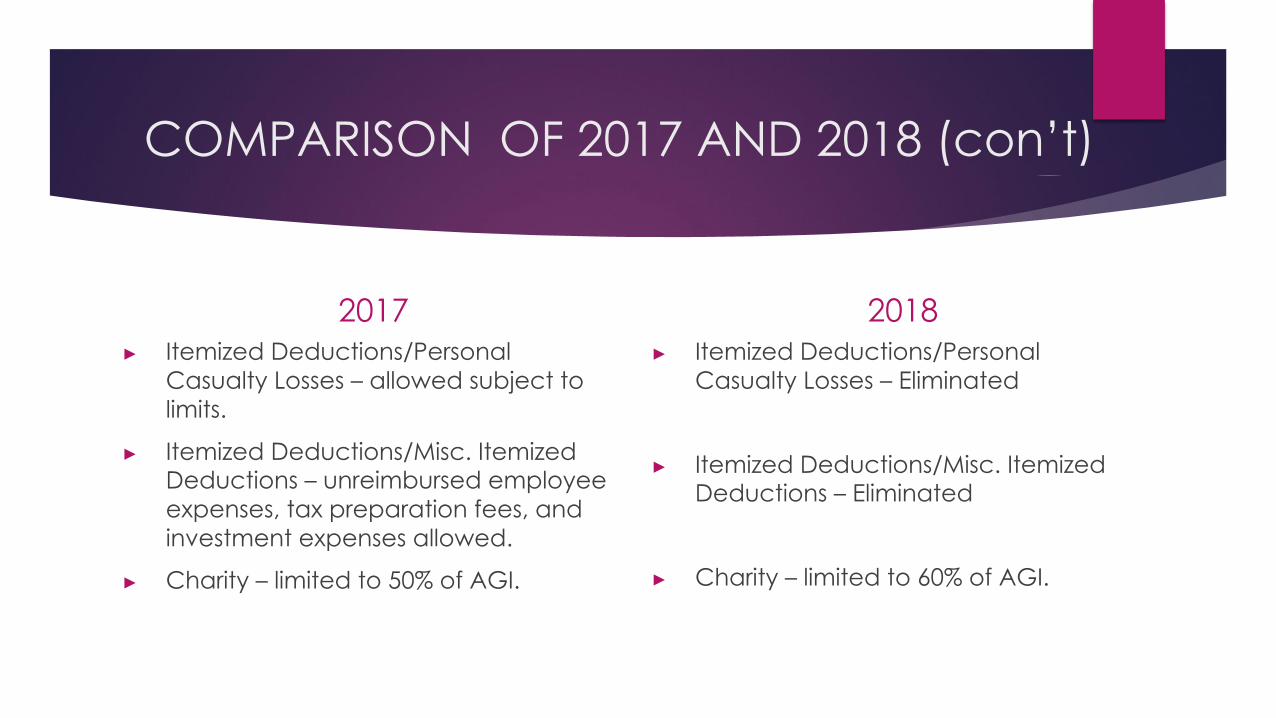

2017▶ Itemized Deductions/Personal

Casualty Losses – allowed subject to limits.

▶ Itemized Deductions/Misc. Itemized Deductions – unreimbursed employee expenses, tax preparation fees, and investment expenses allowed.

▶ Charity – limited to 50% of AGI.

2018▶ Itemized Deductions/Personal

Casualty Losses – Eliminated

▶ Itemized Deductions/Misc. Itemized Deductions – Eliminated

▶ Charity – limited to 60% of AGI.

COMPARISON OF 2017 AND 2018 (con’t)

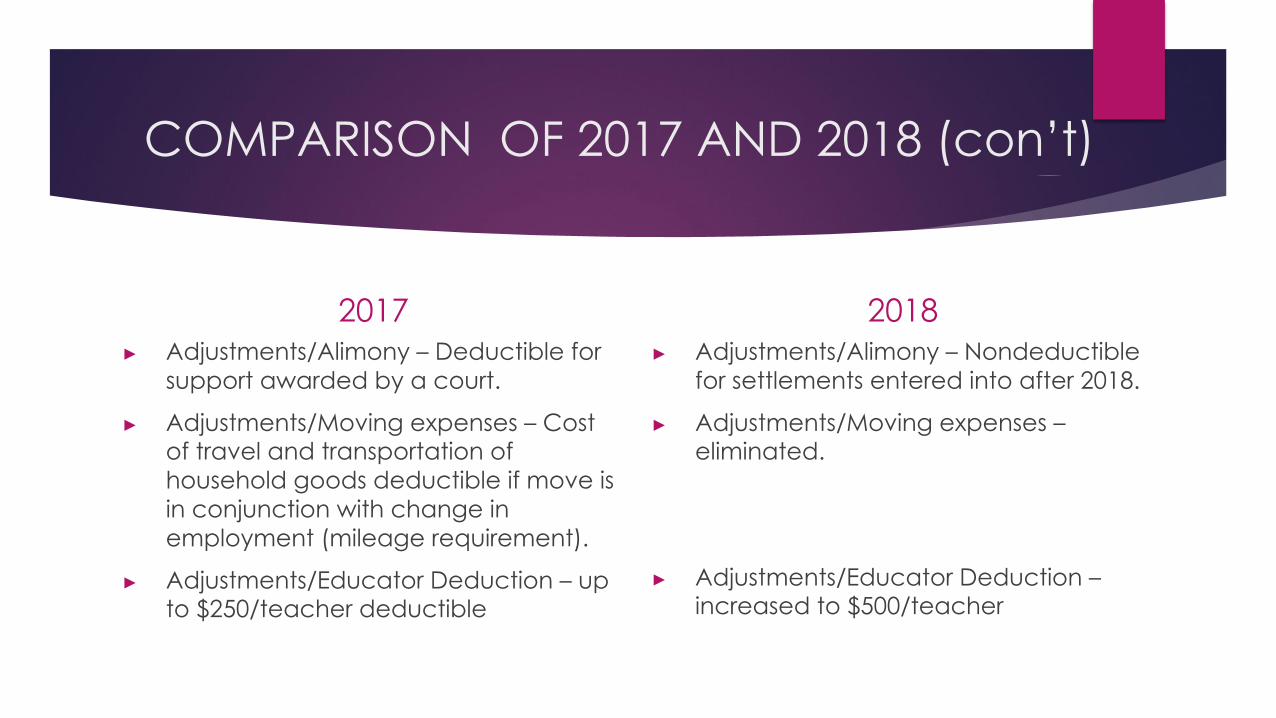

2017▶ Adjustments/Alimony – Deductible for

support awarded by a court.

▶ Adjustments/Moving expenses – Cost of travel and transportation of household goods deductible if move is in conjunction with change in employment (mileage requirement).

▶ Adjustments/Educator Deduction – up to $250/teacher deductible

2018▶ Adjustments/Alimony – Nondeductible

for settlements entered into after 2018.

▶ Adjustments/Moving expenses – eliminated.

▶ Adjustments/Educator Deduction – increased to $500/teacher

COMPARISON OF 2017 AND 2018 (con’t)

2017▶ Section 199 – Domestic Production

Activities Deduction (DPAD) is deduction available to manufactures, producers, growers, extractors, under which film production has fallen been allowed a limited deduction.

▶ Section 181 – Film expensing election retained for 2017 in recently passed budget bill

2018▶ Section 199 – Repealed and replaced.

▶ Section 199A – New Qualified Business Income Deduction for “pass-thru” entities

▶ Section 181 – Retained with limitations (cannot take deductions until the year the film is released)

DISCUSSION OF NEW 199A DEDUCTION

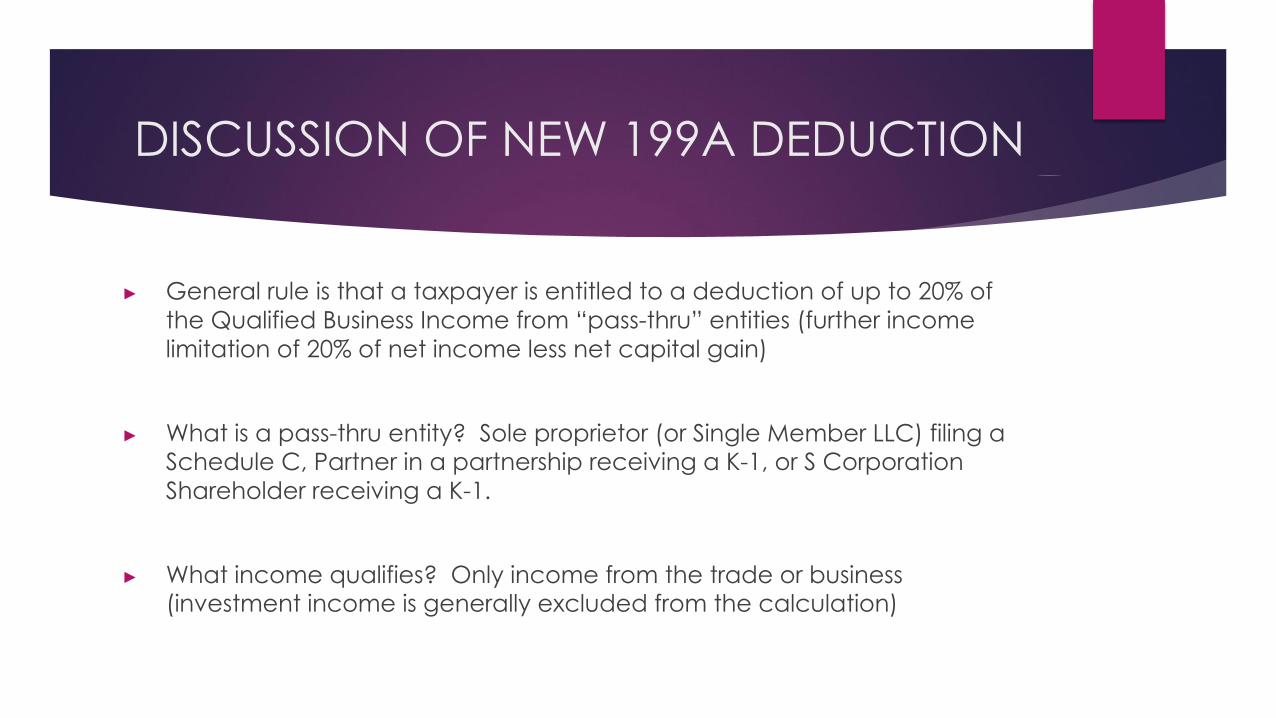

▶ General rule is that a taxpayer is entitled to a deduction of up to 20% of the Qualified Business Income from “pass-thru” entities (further income limitation of 20% of net income less net capital gain)

▶ What is a pass-thru entity? Sole proprietor (or Single Member LLC) filing a Schedule C, Partner in a partnership receiving a K-1, or S Corporation Shareholder receiving a K-1.

▶ What income qualifies? Only income from the trade or business (investment income is generally excluded from the calculation)

DISCUSSION OF NEW 199A DEDUCTION

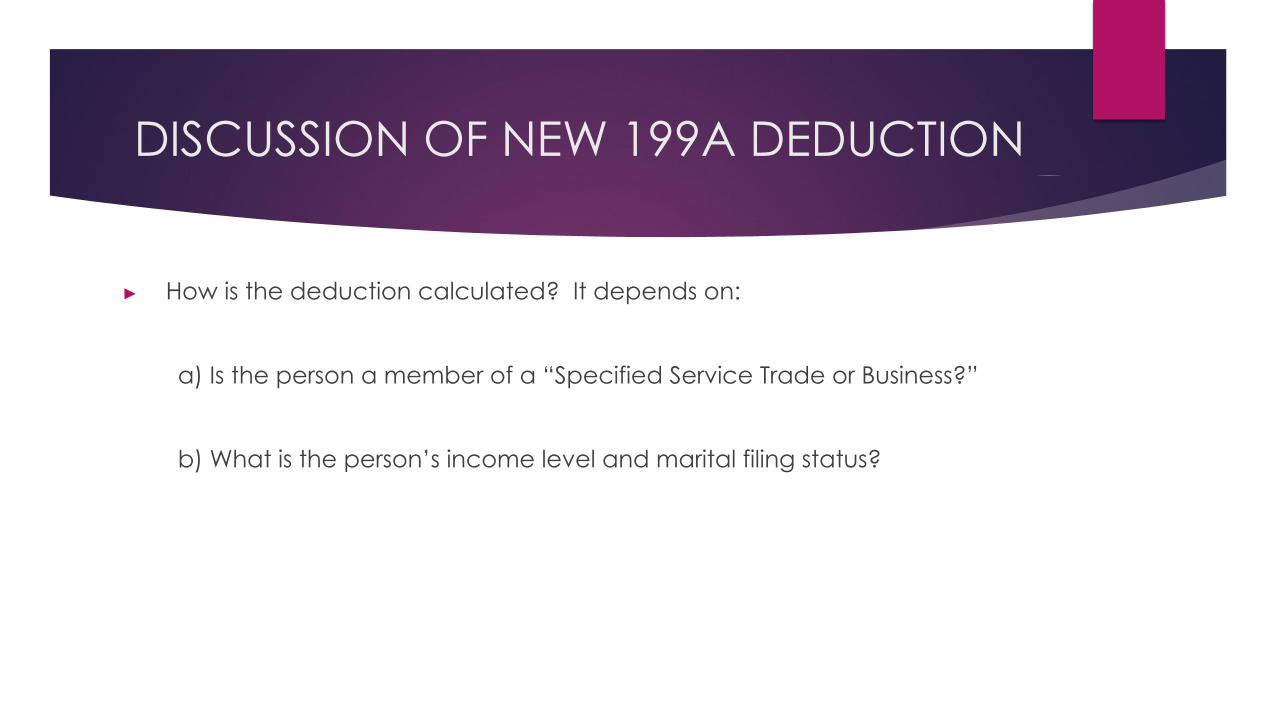

▶ How is the deduction calculated? It depends on:

a) Is the person a member of a “Specified Service Trade or Business?”

b) What is the person’s income level and marital filing status?

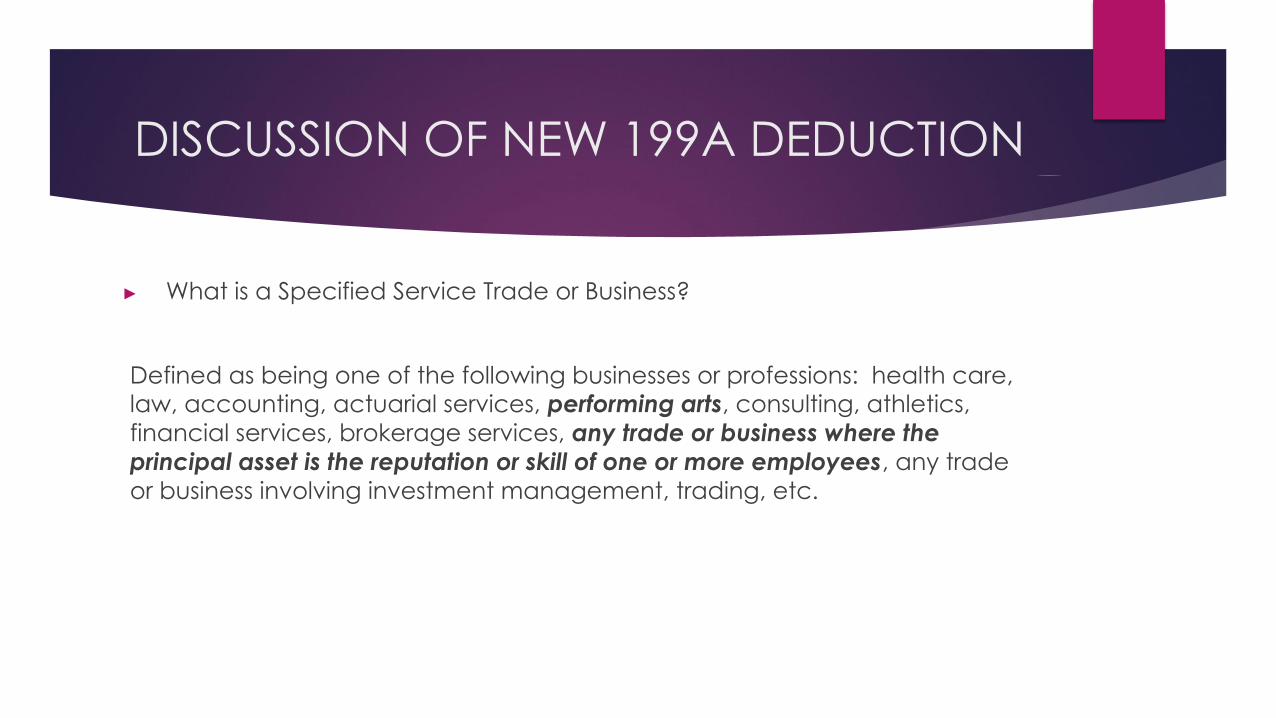

DISCUSSION OF NEW 199A DEDUCTION

▶ What is a Specified Service Trade or Business?

Defined as being one of the following businesses or professions: health care, law, accounting, actuarial services, performing arts, consulting, athletics, financial services, brokerage services, any trade or business where the principal asset is the reputation or skill of one or more employees, any trade or business involving investment management, trading, etc.

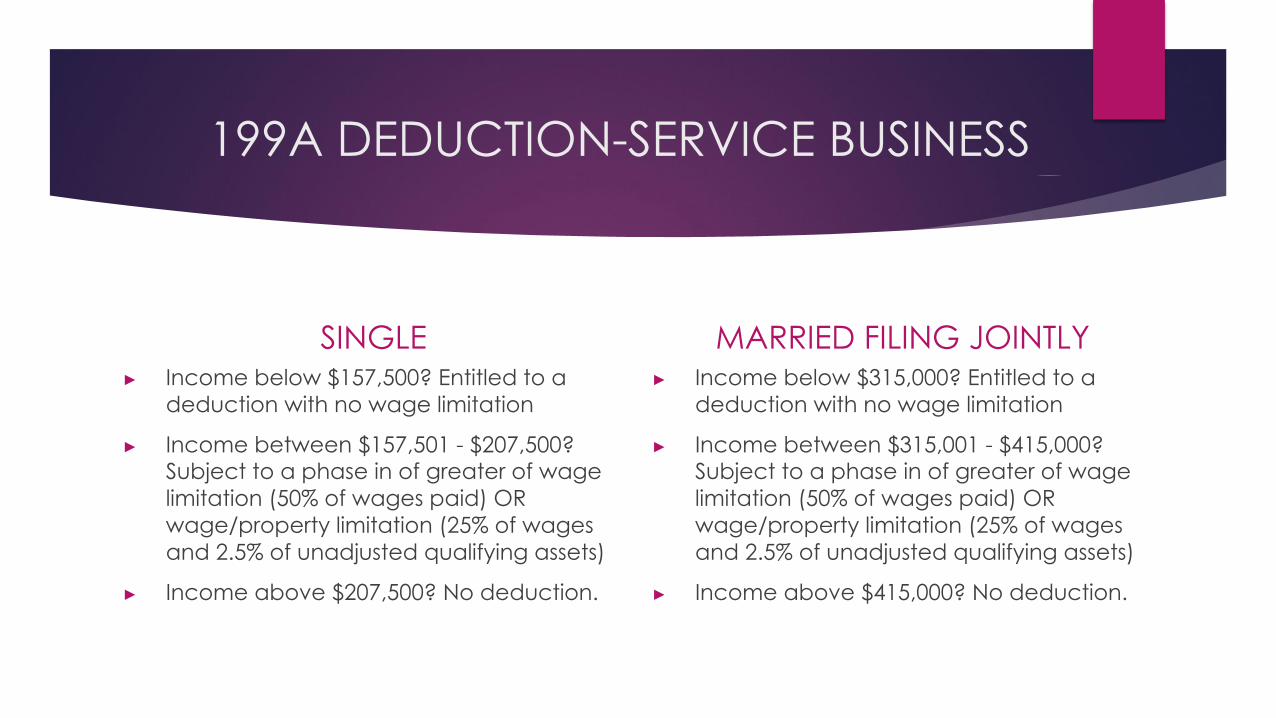

199A DEDUCTION-SERVICE BUSINESS

SINGLE▶ Income below $157,500? Entitled to a

deduction with no wage limitation

▶ Income between $157,501 - $207,500? Subject to a phase in of greater of wage limitation (50% of wages paid) OR wage/property limitation (25% of wages and 2.5% of unadjusted qualifying assets)

▶ Income above $207,500? No deduction.

MARRIED FILING JOINTLY▶ Income below $315,000? Entitled to a

deduction with no wage limitation

▶ Income between $315,001 - $415,000? Subject to a phase in of greater of wage limitation (50% of wages paid) OR wage/property limitation (25% of wages and 2.5% of unadjusted qualifying assets)

▶ Income above $415,000? No deduction.

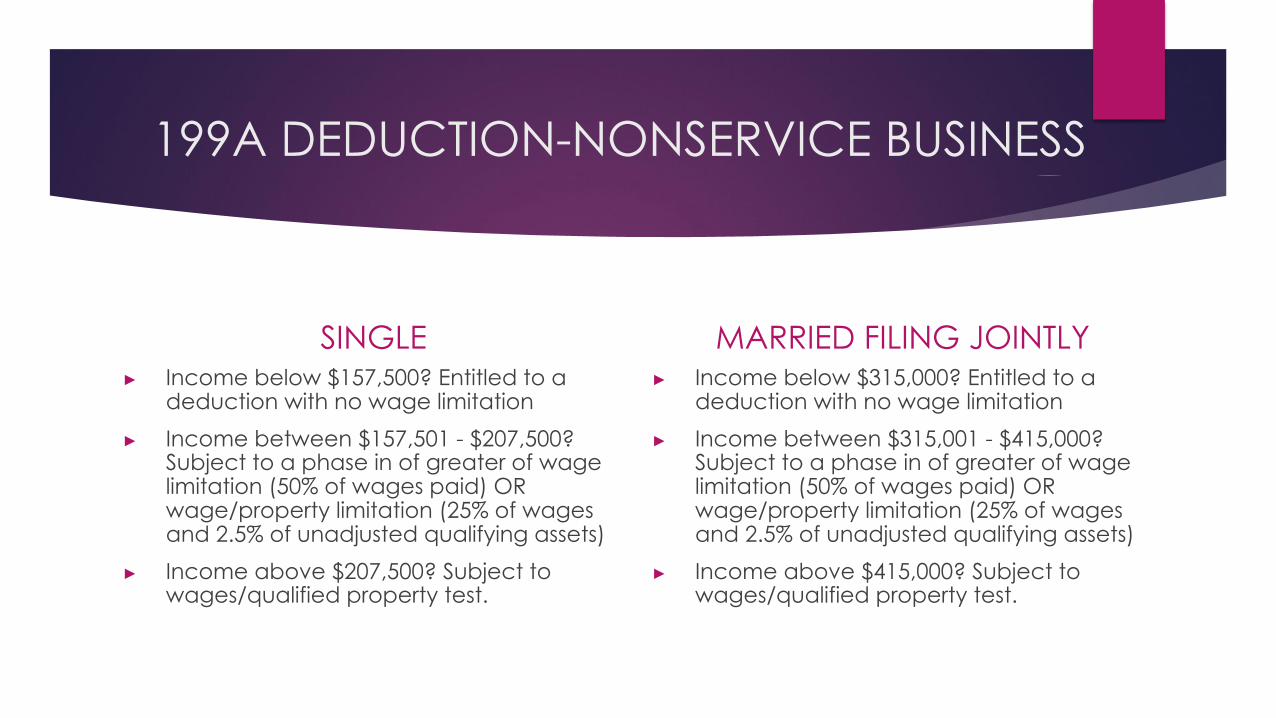

199A DEDUCTION-NONSERVICE BUSINESS

SINGLE▶ Income below $157,500? Entitled to a

deduction with no wage limitation▶ Income between $157,501 - $207,500?

Subject to a phase in of greater of wage limitation (50% of wages paid) OR wage/property limitation (25% of wages and 2.5% of unadjusted qualifying assets)

▶ Income above $207,500? Subject to wages/qualified property test.

MARRIED FILING JOINTLY▶ Income below $315,000? Entitled to a

deduction with no wage limitation▶ Income between $315,001 - $415,000?

Subject to a phase in of greater of wage limitation (50% of wages paid) OR wage/property limitation (25% of wages and 2.5% of unadjusted qualifying assets)

▶ Income above $415,000? Subject to wages/qualified property test.

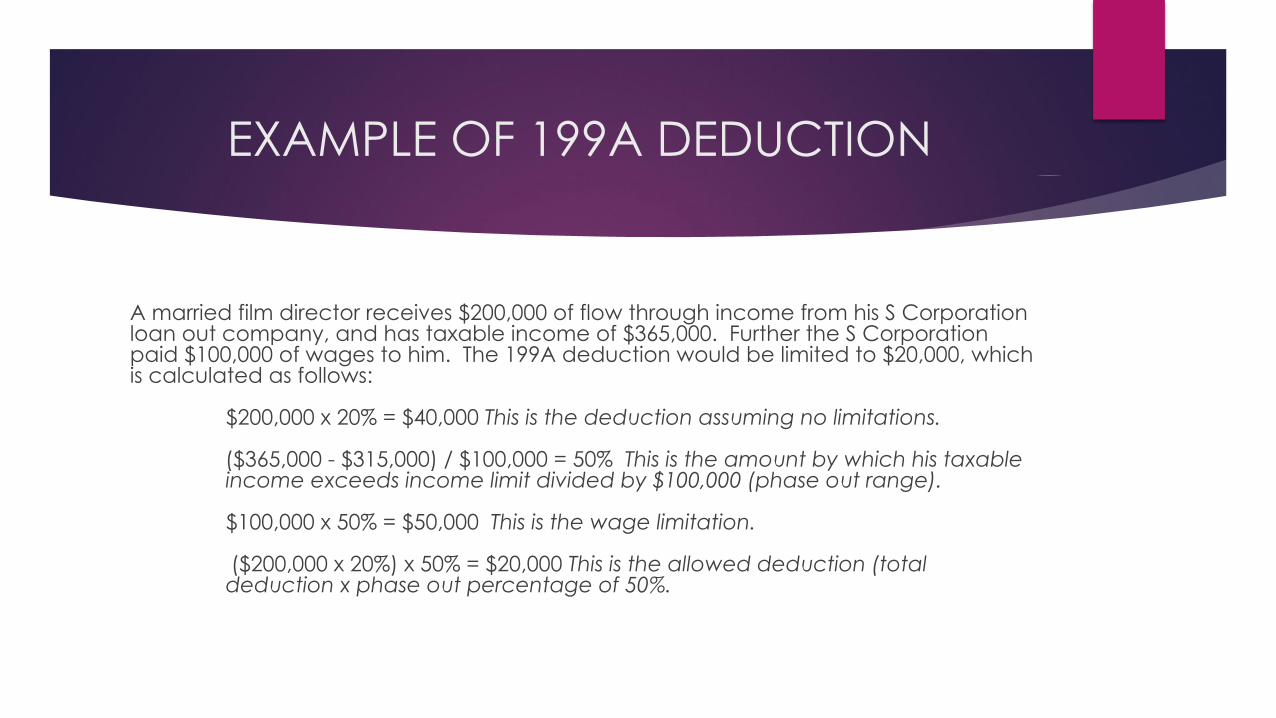

EXAMPLE OF 199A DEDUCTION

A married film director receives $200,000 of flow through income from his S Corporation loan out company, and has taxable income of $365,000. Further the S Corporation paid $100,000 of wages to him. The 199A deduction would be limited to $20,000, which is calculated as follows:

$200,000 x 20% = $40,000 This is the deduction assuming no limitations.

($365,000 - $315,000) / $100,000 = 50% This is the amount by which his taxableincome exceeds income limit divided by $100,000 (phase out range).

$100,000 x 50% = $50,000 This is the wage limitation.

($200,000 x 20%) x 50% = $20,000 This is the allowed deduction (total deduction x phase out percentage of 50%.

FINAL COMMENTS ON 199A DEDUCTION

▶ Income limitations are applied at the partner/S Corp shareholder level, not at the corporation level.

▶ Deduction is allowed after adjusted gross income but before taxable income.

▶ Deduction does not affect the calculation of self-employment tax for partners or sole proprietors.

PLANNING OPPORTUNITIES FOR 2018

▶ New Section 199A Deduction – Pros and cons

▶ Time to form an LLC or Corporation? Pros and cons

▶ Employer expense reimbursement

▶ C Corporation? Flat tax of 21%