Embed Size (px)

Citation preview

University of St. Thomas, MinnesotaUST Research Online

Accounting Faculty Publications Accounting

6-2012

Staff Auditors’ Observations of Questionable PeerBehavior: The View from the Other SideEileen TaylorNorth Carolina State University at Raleigh, [email protected]

Mary CurtisUniversity of North Texas, [email protected]

Lawrence ChuiUniversity of St. Thomas, Minnesota, [email protected]

Follow this and additional works at: http://ir.stthomas.edu/ocbacctpub

Part of the Accounting Commons

This Article is brought to you for free and open access by the Accounting at UST Research Online. It has been accepted for inclusion in AccountingFaculty Publications by an authorized administrator of UST Research Online. For more information, please contact [email protected].

Recommended CitationTaylor, Eileen; Curtis, Mary; and Chui, Lawrence, "Staff Auditors’ Observations of Questionable Peer Behavior: The View from theOther Side" (2012). Accounting Faculty Publications. 27.http://ir.stthomas.edu/ocbacctpub/27

Violations of audit standards threaten audit quality andincrease litigation risk, while violations of workplace behav-ior lead to demoralization and employee turnover, a sig-nificant threat to CPA firms focused on attracting and

retaining qualified and talented professionals. Identification ofthese activities can help managers understand which types of activ-ities employees consider unethical. Knowledge of these activi-ties can help management address employee concerns and worktoward developing a positive organizational culture.

The study described below reported and classified publicauditors’ observations of unethical behavior within their offices.Of the 238 survey respondents, 66 reported observing 80 instancesof unethical behavior. The majority of these behaviors were relat-ed to audits, but many were related to the workplace.

ObservationsA second-year staff auditor—a new CPA—looks around to see

who is watching before placing a page of uncleared review notes

R E S P O N S I B I L I T I E S & L E A D E R S H I P

e t h i c s

JUNE 2012 / THE CPA JOURNAL66

By Eileen Z. Taylor, Mary B. Curtis, and Lawrence Chui

Staff Auditors’ Observations of Questionable Peer BehaviorThe View from the Other Side

JUNE 2012 / THE CPA JOURNAL 67

in a client’s shredder. Back at the office, asenior auditor receives an e-mail from a col-league containing a sexually offensive joke.Another staff person, working toward a pro-motion to manager, is staying late again;however, she won’t record those extra hoursbecause she has to come in under budgetor risk a poor evaluation.

These examples are actual behaviorsobserved by audit staff in their workplaces.As members of a profession that has aprimary responsibility to protect the pub-lic, auditors have an obligation to behavewith the utmost integrity. But as employ-ees working in a for-profit business, theyare also subject to company pressures,organizational politics, and individualmoral values. Violations of professionalstandards or company policies reduceeffectiveness and efficiency and threatena company’s overall success. In addition,violations of professional standards reduceaudit quality and increase litigation risk.Violations of company policy might leadto employee demoralization and increasedturnover in the organization; this, in turn,drives up recruiting, training, and salarycosts. Creating and maintaining an ethicalworkplace is critical, especially at a timewhen executives at large firms state thatattracting and retaining talented profes-sionals is what keeps them up at night(Ira Solomon, “Conversations with the Big4 Accounting Firms’ Chief Executives,”Current Issues in Auditing, vol. 2, pp.C13–C27, 2008). In a recent ethics andcompliance report, accounting firm part-ners and executives stressed the importanceof integrating ethics in training and prac-tice in order to attract and retain the bestemployees (Speaking of Ethics: Ethics andCompliance Report 2010, KPMG).

The sections below present practicing staffauditors’ observations on behavior that theyconsidered unethical—also called workplacedeviance—within their own offices. For thepast three years, this article’s authors usedan open-ended survey to ask 238 in-chargeauditors to provide information about anyunethical or questionable acts they witnessedwithin their firm. Of the participants, 66(27.7%) reported 80 instances of unethicalbehavior, which fall into two broad cate-gories: those related to audits and those relat-ed to the general workplace environment.While inappropriate audit behaviors were the

most common issues identified (57.5%),workplace environment issues were also amajor concern.

Furthermore, participants rarely reportedtheir observations to firm management,despite the availability of an anonymous hotline. This lack of reporting is a concern,especially given the recent revisions to the

NYSSCPA Code of Professional Conduct,which elevate integrity and due professionalcare of CPAs (Joanne S. Barry, “A RevisedCode of Conduct for the New Law,” TheCPA Journal, September 2010). Unless man-agers make a concerted effort to identify thesebehaviors by encouraging auditors to reportthem early on, they might miss the opportu-

JUNE 2012 / THE CPA JOURNAL68

nity to address employees’ concerns. Withknowledge of the specific activities employ-ees have identified, managers can more ade-quately address those concerns and build apositive organizational climate. In addition,management can implement more effectivegovernance tools in order to reduce unethi-cal behavior before it becomes an establishednorm in the organization.

On Ethics and Audit FirmsWithin an audit firm, management is

rightly concerned by the presence of dys-functional or (audit) quality-threateningbehaviors (QTB). These include, but arenot limited to, insufficient audit evidence,inadequate documentation and review, vio-lations of U.S. generally accepted audit-ing standards (GAAS) and U.S. generallyaccepted accounting principles (GAAP),truncating of small samples, false or pre-mature sign-off, failure to do adequateresearch, and underreporting of time (JeanBedard, Donald Dies, Mary Curtis, and J.Gregory Jenkins, “Risk Monitoring andControl in Audit Firms: A ResearchSynthesis,” Auditing: A Journal of Practiceand Theory, vol. 27, no. 1, pp. 187–218,2008). In a 1990 survey of practicing audi-tors in the United States, Tim Kelley andLoren Margheim found that 54% of staff

auditors reported engaging in at least oneof five QTBs on a specific, recent audit.The two most frequently reported acts werethe acceptance of weak client explanations(33%) and the reduction of the amount ofwork performed on audit to below a rea-sonable level (31%) (“The Impact of TimeBudget Pressure, Personality, andLeadership Variables on DysfunctionalAudit Behavior,” Auditing: A Journal ofPractice and Theory, vol. 9, no. 1, 1990).

QTBs are undoubtedly harmful.Lawsuits accusing CPA firms of violatingprofessional standards negatively impactthose firms—directly, via defense costs andfines, and indirectly, via reputation dam-age and time spent preparing a defense.Managers must realize that they signifi-cantly influence staff members’ behavioralchoices. Several research studies havefound that auditors underreport time whenpressured by management and also sign offon materially misstated financial statementsto demonstrate their obedience to managers(Michael D. Akers and Tim V. Eaton,“Underreporting of Chargeable Time:The Impact of Gender and Characteristicsof Underreporters,” Journal of ManagerialIssues, vol. 15 (spring), 2003; Lawrence A.Ponemon, “Auditor Underreporting ofTime and Moral Reasoning: An

Experimental Lab Study,” ContemporaryAccounting Research, vol. 9, no. 1, 1992).

While management plays a role in per-petuating or preventing QTBs, a deficientworkplace environment can also result inemployee QTB. Employees who are sat-isfied with their work environmentexhibit high organizational commitment,which results in belief and acceptance ofthe organization’s values and willingnessto work hard for the organization.Workplaces that contribute to low orga-nizational commitment might result inauditors shirking audit steps or puttingforth reduced effort on audit engagements.U.S. accounting professionals’ organiza-tional commitment is positively related toa principled ethical climate, one in whichmembers look to rules and codes for guid-ance when faced with an ethical dilemma(John Cullen, K. Praveen Parboteeah,and Bart Victor, “The Effects of EthicalClimates on Organizational Commitment:A Two-study Analysis,” Journal ofBusiness Ethics, vol. 46, 2003). Thus,because workplace behavior can impactQTB, it is important to be aware not onlyof audit-related unethical behaviors, butalso of workplace-related behaviors thatmight be perceived as unethical.

This study examined ethics in audit firmsfrom the perspective of staff and senior-level auditors. By being aware of the con-cerns of those at the staff level, manage-ment can develop improved strategies foraddressing such issues before they becomepart of the firm’s culture.

Data CollectionOver a three-year period, the authors sur-

veyed 238 senior-level auditors at variouscontinuing professional education (CPE)and training sessions held by the Big Four,representing CPA offices located through-out the United States. Session topics pri-marily focused on audit and financialaccounting issues. Participants did notreceive compensation for completing thepaper-based survey, and all responses wereanonymous. Participants answered thefollowing open-ended question, and pro-vided demographic data at the end ofeach CPE session:

Have you ever faced a situation atwork in which you observed unethicalbehavior? If so, please write a fewlines describing the situation and the

Panel A: Continuous Variable:

Mean Std. Deviation Range

Age 27.20 3.00 21–41

Panel B: Dichotomous Variables:

Male Female

Gender 57% 43%

U.S. International

Birthplace 84% 16%

Education 94% 6%

Ethics Training: Yes No

CPE 83% 17%

College Section 66% 34%

College Course 68% 32%

CPA Certified 55% 45%

EXHIBIT 1Descriptive Statistics

JUNE 2012 / THE CPA JOURNAL 69

actions you did/did not take.(Remember, this survey is anonymousso please do not include any identify-ing information, especially the names ofclients or individuals.)As shown in Exhibit 1, the average

participant was 27.2 years old, which indi-cates that respondents have pursued a tra-ditional career path, entering publicaccounting directly after college. The sam-ple was 57% male. For the most part,participants were either born (84%) or edu-cated (94%) in the United States, elimi-nating the ability to investigate cultural dif-ferences in this study.

Nearly all participants (94%) indicatedthat they previously had some ethicstraining. The most common form of ethicstraining was CPE (83%), followed by acollege course (68%) and a section of acollege course (66%). CPAs comprised aslight majority of participants (55%); onewas a certified management accountant(CMA), and no respondents were certi-fied internal auditors (CIA) or certifiedfinancial examiners (CFE). With respect tothe low percentage of respondents with aCPA license, the authors have observedthat many accountants who graduated inthe years following the Sarbanes-Oxley Actof 2002 (SOX) delayed taking the CPAexam because they had such a high work-load. In more recent years, more studentsappear to be taking the exam earlier.Over the three-year period, the percentageof auditors reporting observations of uneth-ical behavior increased. In the first year,24% of participants reported observingunethical behavior; reports increased to28% and 36% in the second and thirdyears, respectively. This trend could indi-cate that unethical behavior is increasing,but it could also suggest that more audi-tors are less willing to overlook unethicalbehavior in the workplace. (For an in-depthdiscussion about the potential causes ofworkplace deviance in public accounting,see Ronald Jelinek and Kate Jelinek,“Auditors Gone Wild: The ‘Other’Problem in Public Accounting,” BusinessHorizons, pp. 223–233, 2008.)

Based upon an analysis of the reportedobservations, the authors identified two dis-tinct categories of behavior: audit-relatedand general workplace environment. Thesebehaviors were then grouped into severaldistinct types. The first category, audit-

related behaviors, includes behaviors thatdirectly influence audit quality—that is,they violate audit standards, company poli-cies or procedures about auditing process-es, or the AICPA Code of ProfessionalConduct. The two types within this cate-gory are audit steps and auditor review.Audit steps are nonsupervisory actionsundertaken by an audit team member, such

as skipping or falsifying audit steps, orother activities that endanger audit quali-ty, such as violations of independence.Auditor review violations relate to super-visory activities completed on the audit andinclude actions of in-charge individuals,managers, and partners in assigning tasks,supervising staff, and reviewing auditworkpapers.

JUNE 2012 / THE CPA JOURNAL70

The second category, general workplaceenvironment, includes all activities that donot directly affect audit quality, such as inter-personal issues, violations of company poli-cies related to general business activities, andofficial or nonofficial norms that could cre-ate a hostile work environment or lead anindividual to violate standards, procedures, orcodes. This study identified three types:gossip/morale, employee fraud, and sexualharassment. Gossip/morale issues includeinterpersonal events or activities that influ-ence the morale of an audit firm’s mem-bers. Employee fraud includes actions thatarise from intentional dishonesty for person-al gain, such as misappropriation of assets,stealing, fraud, or lying about activities notdirectly related to audit quality. Sexual harass-ment is defined as “unwelcome sexualadvances, requests for sexual favors, and otherverbal or physical harassment of a sexualnature” (U.S. Equal Employment OpportunityCommission, http://www.eeoc.gov/laws/types/sexual_harassment.cfm).

FindingsThe authors reviewed auditors’ respons-

es to the open-ended question that askedthem to describe any “situation at work in

which you observed unethical behavior.”The responses were independently codedaccording to the mutually exclusive cate-gories described above.

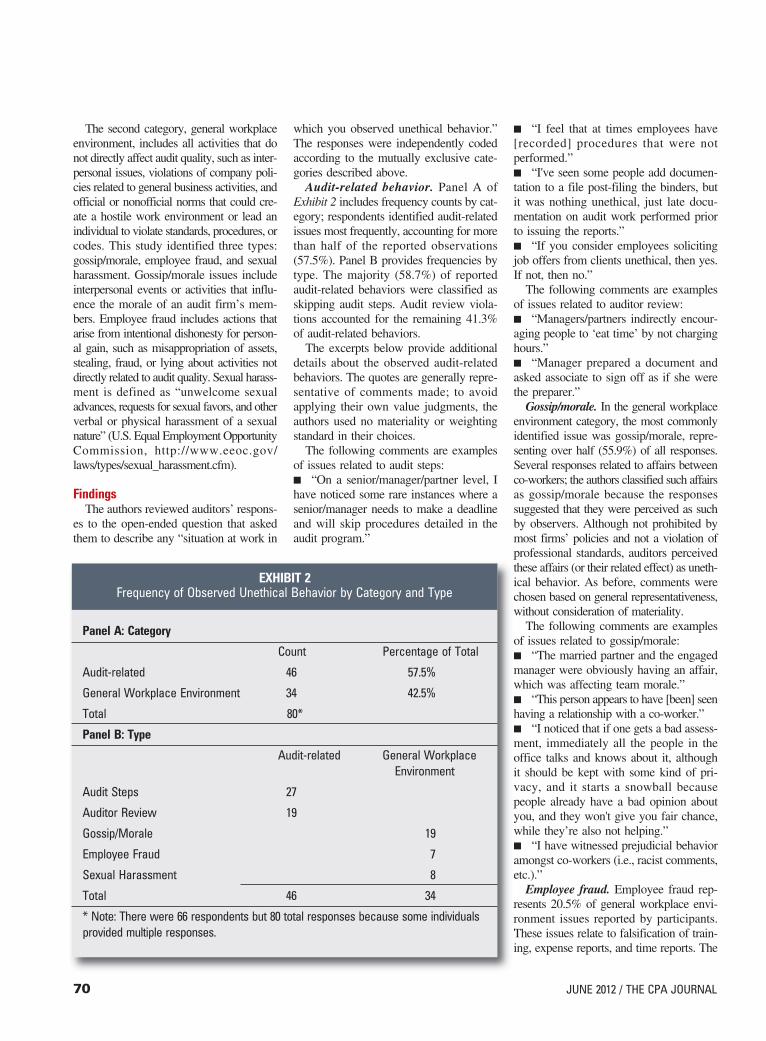

Audit-related behavior. Panel A ofExhibit 2 includes frequency counts by cat-egory; respondents identified audit-relatedissues most frequently, accounting for morethan half of the reported observations(57.5%). Panel B provides frequencies bytype. The majority (58.7%) of reportedaudit-related behaviors were classified asskipping audit steps. Audit review viola-tions accounted for the remaining 41.3%of audit-related behaviors.

The excerpts below provide additionaldetails about the observed audit-relatedbehaviors. The quotes are generally repre-sentative of comments made; to avoidapplying their own value judgments, theauthors used no materiality or weightingstandard in their choices.

The following comments are examplesof issues related to audit steps:■ “On a senior/manager/partner level, Ihave noticed some rare instances where asenior/manager needs to make a deadlineand will skip procedures detailed in theaudit program.”

■ “I feel that at times employees have[recorded] procedures that were not performed.”■ “I've seen some people add documen-tation to a file post-filing the binders, butit was nothing unethical, just late docu-mentation on audit work performed priorto issuing the reports.”■ “If you consider employees solicitingjob offers from clients unethical, then yes.If not, then no.”

The following comments are examplesof issues related to auditor review: ■ “Managers/partners indirectly encour-aging people to ‘eat time’ by not charginghours.”■ “Manager prepared a document andasked associate to sign off as if she werethe preparer.”

Gossip/morale. In the general workplaceenvironment category, the most commonlyidentified issue was gossip/morale, repre-senting over half (55.9%) of all responses.Several responses related to affairs betweenco-workers; the authors classified such affairsas gossip/morale because the responsessuggested that they were perceived as suchby observers. Although not prohibited bymost firms’ policies and not a violation ofprofessional standards, auditors perceivedthese affairs (or their related effect) as uneth-ical behavior. As before, comments werechosen based on general representativeness,without consideration of materiality.

The following comments are examplesof issues related to gossip/morale:■ “The married partner and the engagedmanager were obviously having an affair,which was affecting team morale.”■ “This person appears to have [been] seenhaving a relationship with a co-worker.”■ “I noticed that if one gets a bad assess-ment, immediately all the people in theoffice talks and knows about it, althoughit should be kept with some kind of pri-vacy, and it starts a snowball becausepeople already have a bad opinion aboutyou, and they won't give you fair chance,while they’re also not helping.”■ “I have witnessed prejudicial behavioramongst co-workers (i.e., racist comments,etc.).”

Employee fraud. Employee fraud rep-resents 20.5% of general workplace envi-ronment issues reported by participants.These issues relate to falsification of train-ing, expense reports, and time reports. The

Panel A: Category

Count Percentage of Total

Audit-related 46 57.5%

General Workplace Environment 34 42.5%

Total 80*

Panel B: Type

Audit-related General WorkplaceEnvironment

Audit Steps 27

Auditor Review 19

Gossip/Morale 19

Employee Fraud 7

Sexual Harassment 8

Total 46 34

* Note: There were 66 respondents but 80 total responses because some individualsprovided multiple responses.

EXHIBIT 2Frequency of Observed Unethical Behavior by Category and Type

JUNE 2012 / THE CPA JOURNAL 71

following comments are examples of issuesrelated to employee fraud:■ “Other than minor incidents of skimmingthrough [training assignments] and othertraining things. No big deal breakers.”■ “Roommate at training a few years agocharged through cab fare for a ride he did nottake to pay for a more expensive dinner.”

Sexual harassment. Sexual harassmentissues represent 23.5% of general work-place cases and relate directly to unwant-ed conduct based on gender. While theseincidences can certainly affect morale, theycan also subject the firm to legal liabilityand regulatory action. Issues included send-ing inappropriate e-mails, viewing sexual-ly explicit websites at work, and sexuallyharassing a female co-worker. The fol-lowing comments are examples of thoserelated to inappropriate behavior: ■ “Individual viewing inappropriateemail/Internet content.”■ “Yes, a partner has hit on an associateof mine and said inappropriate things.”

RecommendationsThis study identified two types of uneth-

ical activities occurring within publicaccounting firms that accountants viewedas unethical. In a survey of public account-ing audit seniors over a three-year period,approximately 28% reported observationsof workplace wrongdoing. Behaviorsranged from the objective (e.g., excludingsample items) to the subjective (e.g., sex-ual harassment). Behaviors also differed intheir potential effect on the firm’s reputa-tion and liability risk. Audit-related behav-iors increase the risk of professional lia-bility litigation, while general workplaceenvironment behaviors lead to employeedissatisfaction and turnover, and possiblyworkplace rights litigation. In addition,workplace violations could ultimatelylead to audit-quality problems because poormorale might lead to poor performance,and thus to increased risks of liability andregulatory action.

Public accounting firm managers cangain insight into these issues by identify-ing the types of questionable activities iden-tified by their employees. Although confi-dentiality constraints render research onworkplace wrongdoing difficult to perform,the available research suggests that auditfirm managers can make a difference inthe incidence and severity of such wrong-

doing by paying careful attention to poli-cies and procedures for assessing, moni-toring, and controlling the risk of violationsof professional standards and humanresource policies (Bedard 2008). Althoughnot permitted by the limitations of thisstudy’s data, comparing observations acrosslevels, geographic areas, firms, and clienttypes might have provided greater insights.

Managers can also lower the negativeimpact of workplace wrongdoing bytaking swift action when they becomeaware of wrongdoing and by clearly com-municating to all employees the actionsthat were taken. Lastly, exit interviews,an often overlooked avenue for detec-tive and corrective action, could providean additional confidential information-collection point. These data could be themost effective method of identifyingbehaviors that have become entrenched;some behaviors become embedded in anorganization’s culture, which reduces thelikelihood that normal governance mea-sures will reduce the occurrence ofthose behaviors. Additional recommen-dations include developing and imple-menting a comprehensive training pro-gram for new and current employees thatclarifies and provides examples aboutwhat behavior the organization considerswrong, and what to do if an employeeobserves those behaviors.

This study found that participants report-ed few of these activities to their firms’management and did not mention firm hot-lines as an alternative for internal report-ing, even though the participant firms’ poli-cies recommended these two solutions. Bynot reporting these activities, auditors cancontribute to the creation of a new socialnorm within the firm, providing tacit accep-tance of unethical behavior and reducingthe likelihood that others will report obser-vations of these activities. If these behav-iors shape the firm negatively, high-qual-ity auditors might choose to leave, ratherthan work in an organization whose pro-fessional values conflict with their own.

To address underreporting of observa-tions, management must clearly communi-cate its expectations regarding the report-ing of unethical behavior. To appeal to audi-tors with a strong professional identity, theycan frame reporting as a professional obli-gation, rather than a disruptive action thatresults in retaliation or “bad feelings.” Someresearch has found that hotlines do not needto be anonymous; as long as they protectthe whistleblower’s identity, auditors areas likely to report using an anonymous orprotected hotline (Mary B. Curtis and EileenZ. Taylor, “Whistleblowing in PublicAccounting: Influence of IdentityDisclosure, Situational Context, and PersonalCharacteristics,” Journal of Accounting andthe Public Interest, vol. 9, no. 1, 2009).Further study of the effectiveness of hotlinesand employees’ perceptions of them mightprovide greater insight into what encouragesor discourages individuals from using them.

Clear policies, clear communications,and available reporting mechanisms shouldreduce unethical behavior over time. Swiftand consistent responses will detect andcorrect unethical behavior before itbecomes the norm, reducing firm risk andimproving the workplace overall.

Eileen Z. Taylor, PhD, CPA, is an asso-ciate professor of accounting at NorthCarolina State University, Raleigh, N.C.Mary B. Curtis, PhD, CPA, CISA, is aprofessor of accounting at the Universityof North Texas, Denton, Tex. LawrenceChui, PhD, CPA, is an assistant profes-sor of accounting at the Opus College ofBusiness, University of St. Thomas, St.Paul, Minn.

Clear policies, clear

communications, and available

reporting mechanisms should reduce

unethical behavior over time.