Embed Size (px)

Citation preview

Page 1

London, October 3 rd 2007

STAR CONFERENCE 2007 PRESENTATION

Page 2

Business Overview

Strategy

Financial highlights

Dividends

Annexes

CONTENTS

Page 3

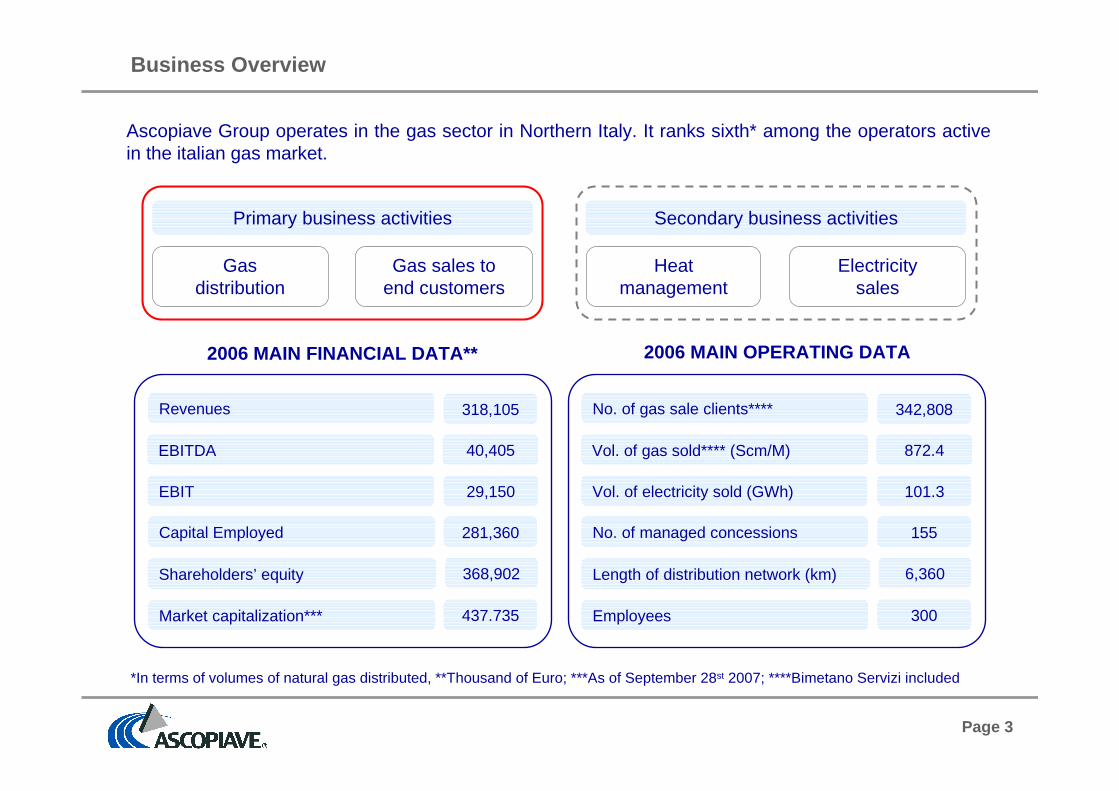

Business Overview

2006 MAIN FINANCIAL DATA** 2006 MAIN OPERATING DATA

Ascopiave Group operates in the gas sector in Northern Italy. It ranks sixth* among the operators activein the italian gas market.

*In terms of volumes of natural gas distributed, **Thousand of Euro; ***As of September 28st 2007; ****Bimetano Servizi included

No. of gas sale clients**** 342,808

Vol. of gas sold**** (Scm/M) 872.4

Vol. of electricity sold (GWh) 101.3

No. of managed concessions 155

Length of distribution network (km) 6,360

Employees 300

Primary business activities

Gas sales toend customers

Gasdistribution

Secondary business activities

Electricitysales

Heatmanagement

Revenues 318,105

EBITDA 40,405

EBIT 29,150

Capital Employed 281,360

Shareholders’ equity 368,902

Market capitalization*** 437.735

Page 4

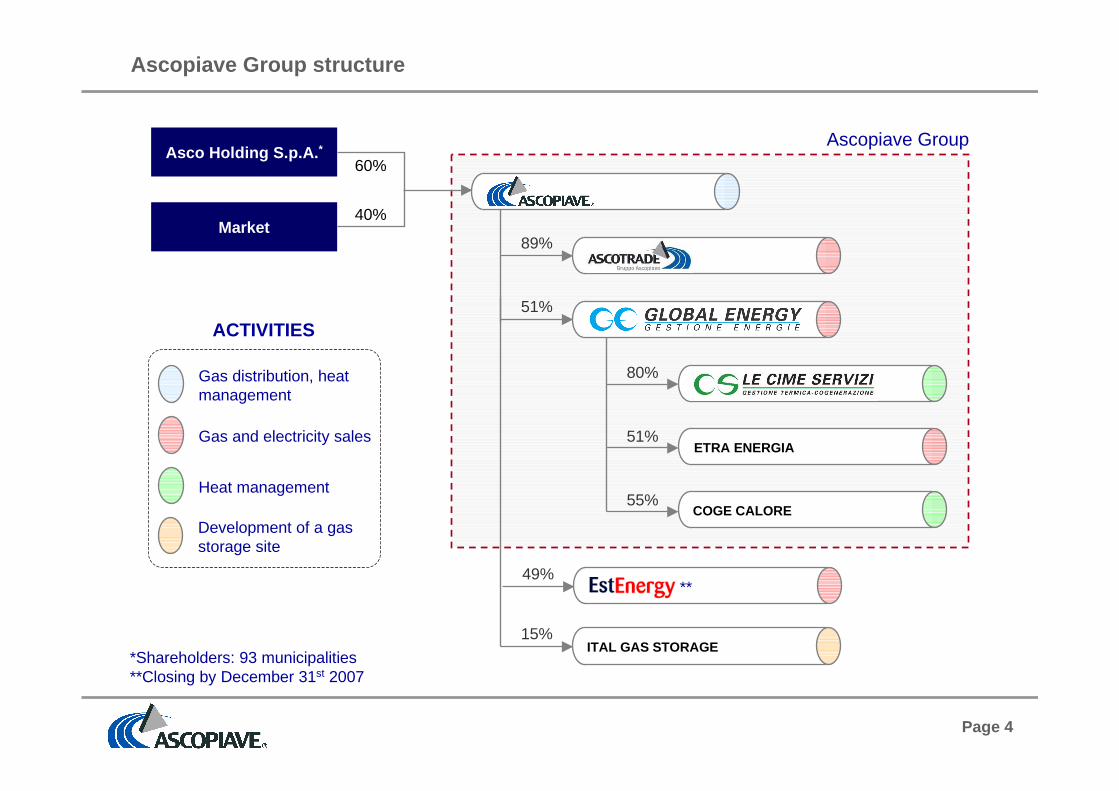

Ascopiave Group

Ascopiave Group structure

60%

40%

Asco Holding S.p.A. *

Market

*Shareholders: 93 municipalities**Closing by December 31st 2007

ACTIVITIES

Development of a gasstorage site

89%

51%

80%

15%ITAL GAS STORAGE

49%

ETRA ENERGIA51%

COGE CALORE55%

Gas distribution, heatmanagement

Heat management

Gas and electricity sales

**

Page 5

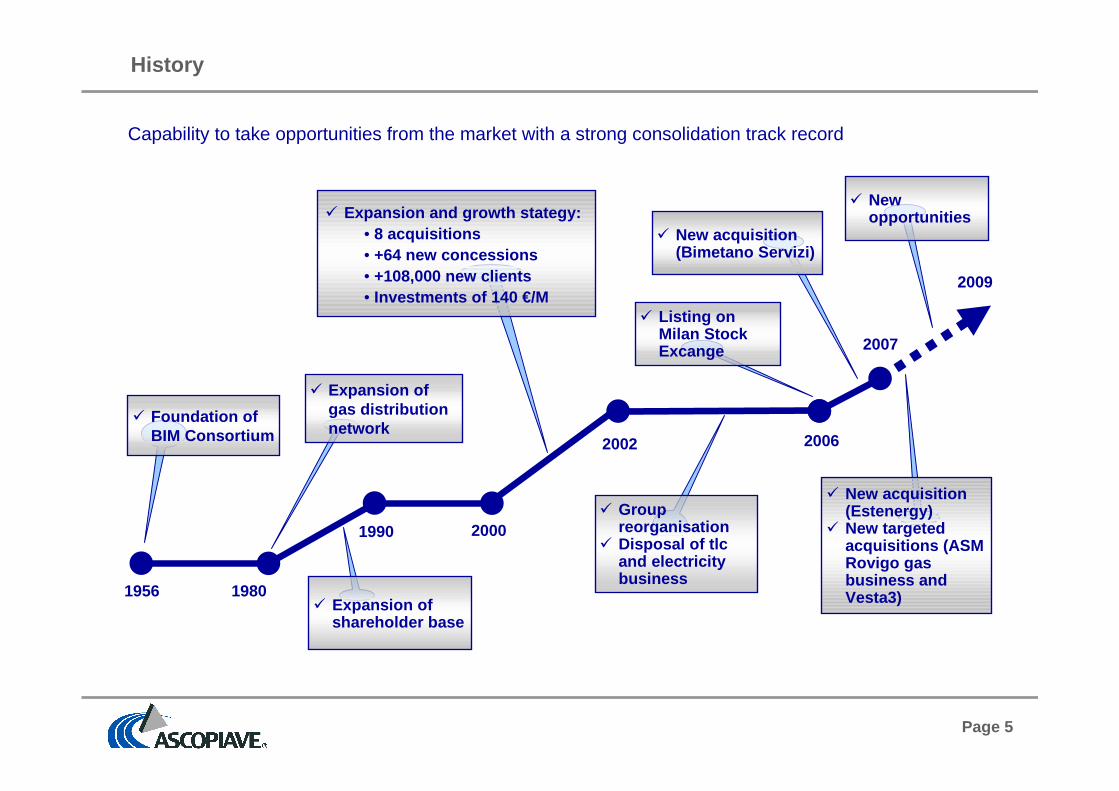

History

1956 1980

2000

2002 2006

2009

1990

� Expansion and growth stategy:• 8 acquisitions• +64 new concessions• +108,000 new clients• Investments of 140 €/M

� Expansion ofshareholder base

� Foundation ofBIM Consortium

� Expansion ofgas distributionnetwork

� Groupreorganisation

� Disposal of tlcand electricitybusiness

� Newopportunities

� Listing onMilan StockExcange 2007

� New acquisition(Bimetano Servizi)

Capability to take opportunities from the market with a strong consolidation track record

� New acquisition(Estenergy)

� New targetedacquisitions (ASMRovigo gasbusiness andVesta3)

Page 6

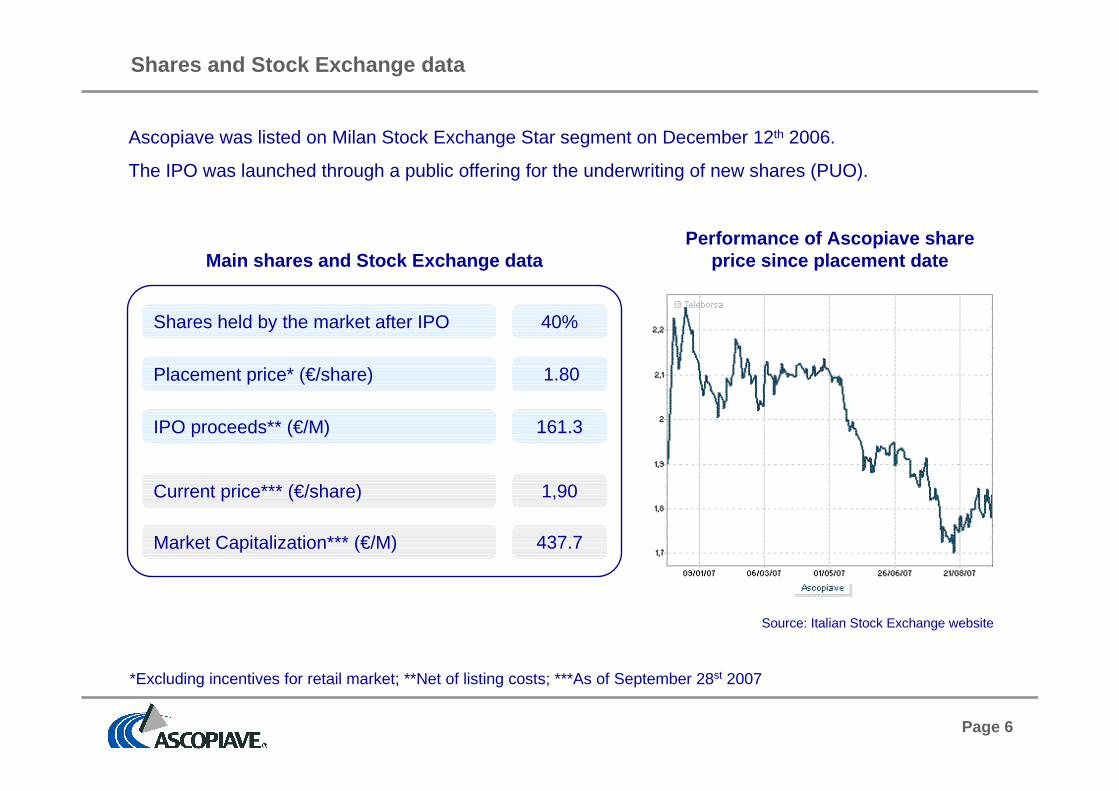

Shares and Stock Exchange data

*Excluding incentives for retail market; **Net of listing costs; ***As of September 28st 2007

Source: Italian Stock Exchange website

Performance of Ascopiave shareprice since placement dateMain shares and Stock Exchange data

Shares held by the market after IPO 40%

Placement price* (€/share) 1.80

IPO proceeds** (€/M) 161.3

Ascopiave was listed on Milan Stock Exchange Star segment on December 12th 2006.

The IPO was launched through a public offering for the underwriting of new shares (PUO).

Current price*** (€/share) 1,90

Market Capitalization*** (€/M) 437.7

Page 7

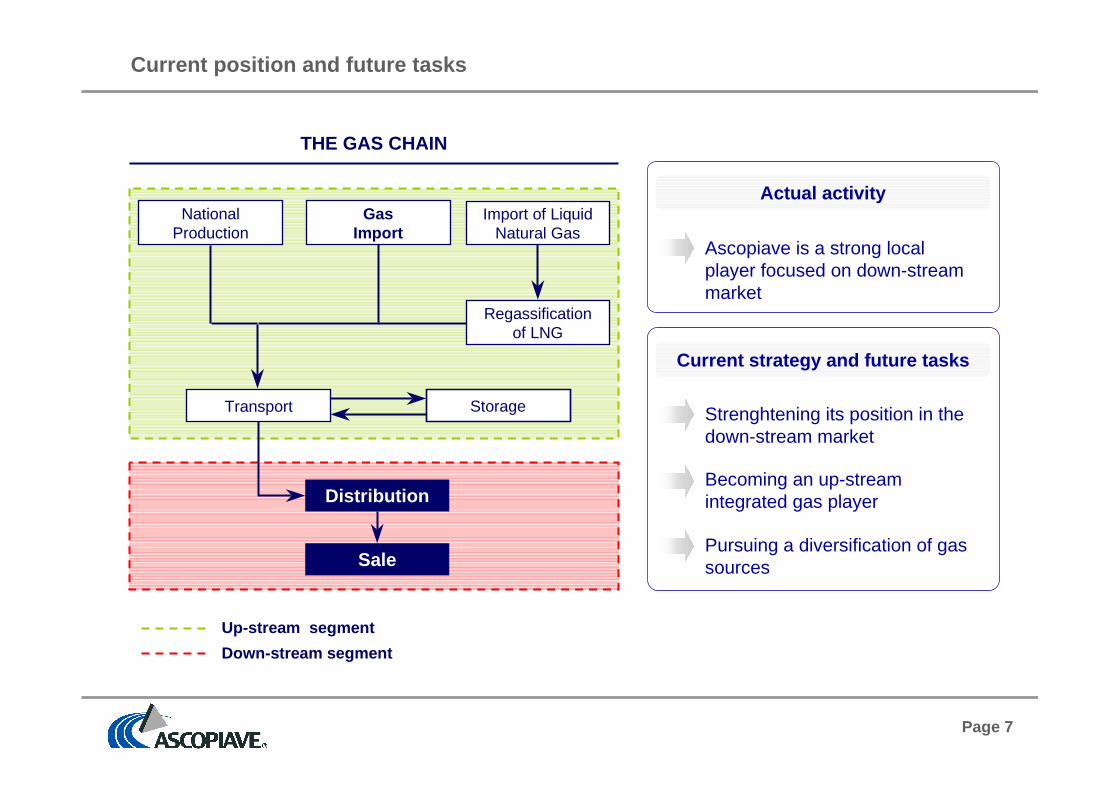

Current position and future tasks

THE GAS CHAIN

Up-stream segment

Down-stream segment

NationalProduction

Import of LiquidNatural Gas

Transport

Regassificationof LNG

Storage

GasImport

Distribution

Sale

Actual activity

Current strategy and future tasks

Ascopiave is a strong localplayer focused on down-streammarket

Strenghtening its position in thedown-stream market

Becoming an up-streamintegrated gas player

Pursuing a diversification of gassources

Page 8

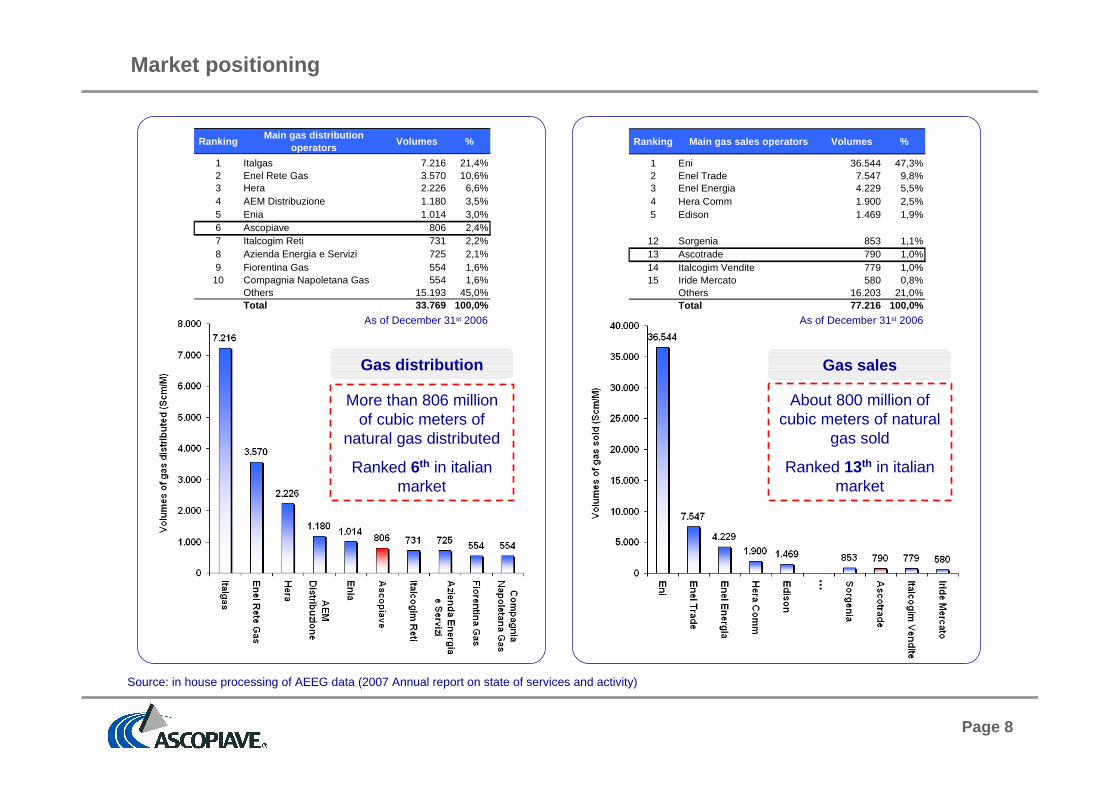

Market positioning

Source: in house processing of AEEG data (2007 Annual report on state of services and activity)

As of December 31st 2006 As of December 31st 2006

More than 806 millionof cubic meters of

natural gas distributed

Ranked 6th in italianmarket

Gas distribution

...

About 800 million ofcubic meters of natural

gas sold

Ranked 13th in italianmarket

Gas sales

RankingMain gas distribution

operatorsVolumes %

1 Italgas 7.216 21,4%2 Enel Rete Gas 3.570 10,6%3 Hera 2.226 6,6%4 AEM Distribuzione 1.180 3,5%5 Enia 1.014 3,0%6 Ascopiave 806 2,4%7 Italcogim Reti 731 2,2%8 Azienda Energia e Servizi 725 2,1%9 Fiorentina Gas 554 1,6%

10 Compagnia Napoletana Gas 554 1,6%Others 15.193 45,0%Total 33.769 100,0%

Ranking Main gas sales operators Volumes %

1 Eni 36.544 47,3%2 Enel Trade 7.547 9,8%3 Enel Energia 4.229 5,5%4 Hera Comm 1.900 2,5%5 Edison 1.469 1,9%

12 Sorgenia 853 1,1%13 Ascotrade 790 1,0%14 Italcogim Vendite 779 1,0%15 Iride Mercato 580 0,8%

Others 16.203 21,0%Total 77.216 100,0%

Page 9

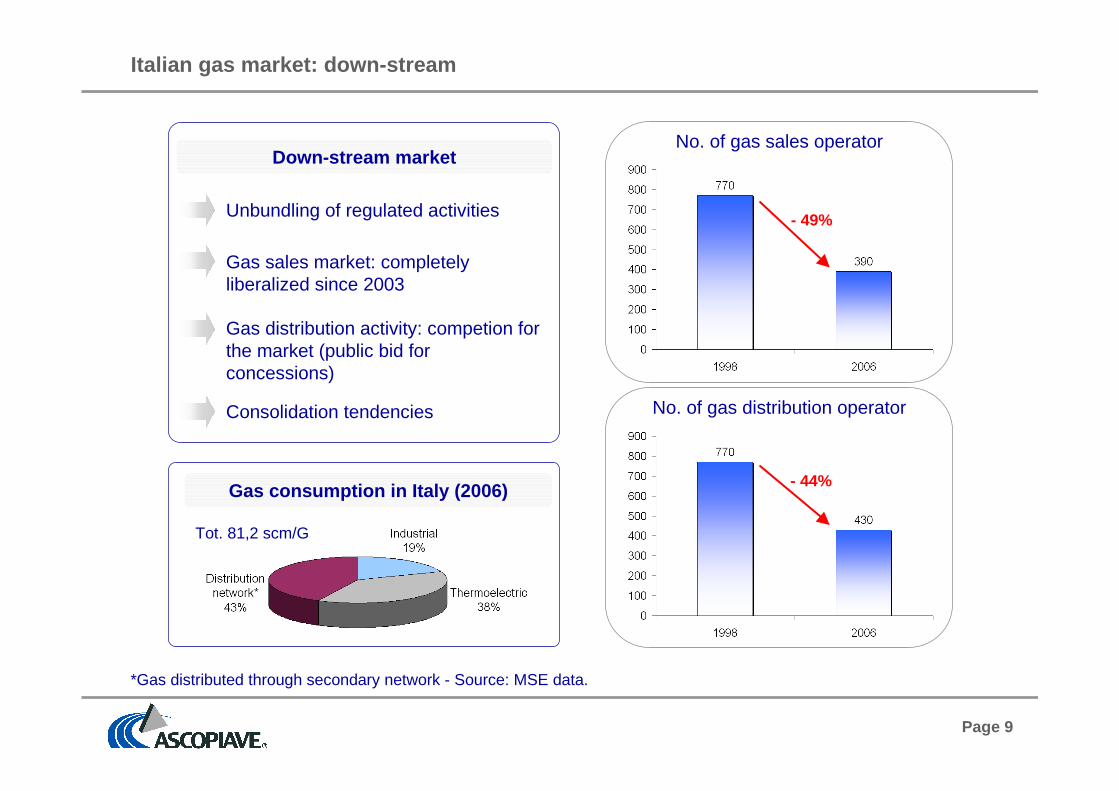

Italian gas market: down-stream

Down-stream market

- 49%

No. of gas sales operator

No. of gas distribution operator

- 44%

Consolidation tendencies

Gas distribution activity: competion forthe market (public bid forconcessions)

Gas sales market: completelyliberalized since 2003

Unbundling of regulated activities

Gas consumption in Italy (2006)

*Gas distributed through secondary network - Source: MSE data.

Tot. 81,2 scm/G

Page 10

Number Populations* Network (km)**

Award from Asco Holding member municipalities 92 631.992 3,710Concessions from other municipalities 62 356.793 2,644

Total 154 988.785 6,354

Gas distribution: Ascopiave concessions as of Septe mber 30 th 2007

*Data as of December 31th 2006, Source: ISTAT; **Data as of June 30th 2007; ***Including a municipality where Ascopiavehas left the concession

60% of concessions from shareholder municipalities

81% of users on concessions expiring beyond 2010

% o

f use

rs

Concessions from Asco Holding Shareholders

Concessions from other municipalities

No. ofconcessions

6*** 2 13 28 92 14

Page 11

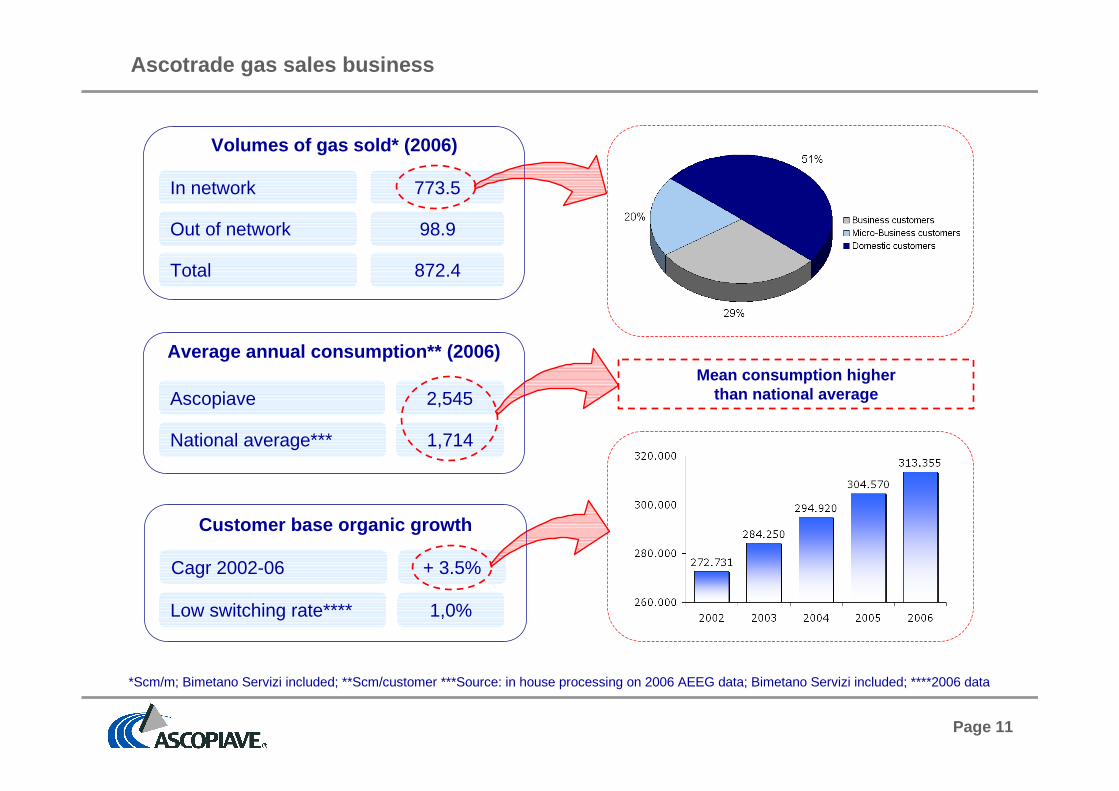

Ascotrade gas sales business

Mean consumption higherthan national average

*Scm/m; Bimetano Servizi included; **Scm/customer ***Source: in house processing on 2006 AEEG data; Bimetano Servizi included; ****2006 data

Volumes of gas sold* (2006)

In network

Out of network

Total

773.5

98.9

872.4

Ascopiave

National average***

2,545

1,714

Average annual consumption** (2006)

Cagr 2002-06

Low switching rate****

+ 3.5%

1,0%

Customer base organic growth

Page 12

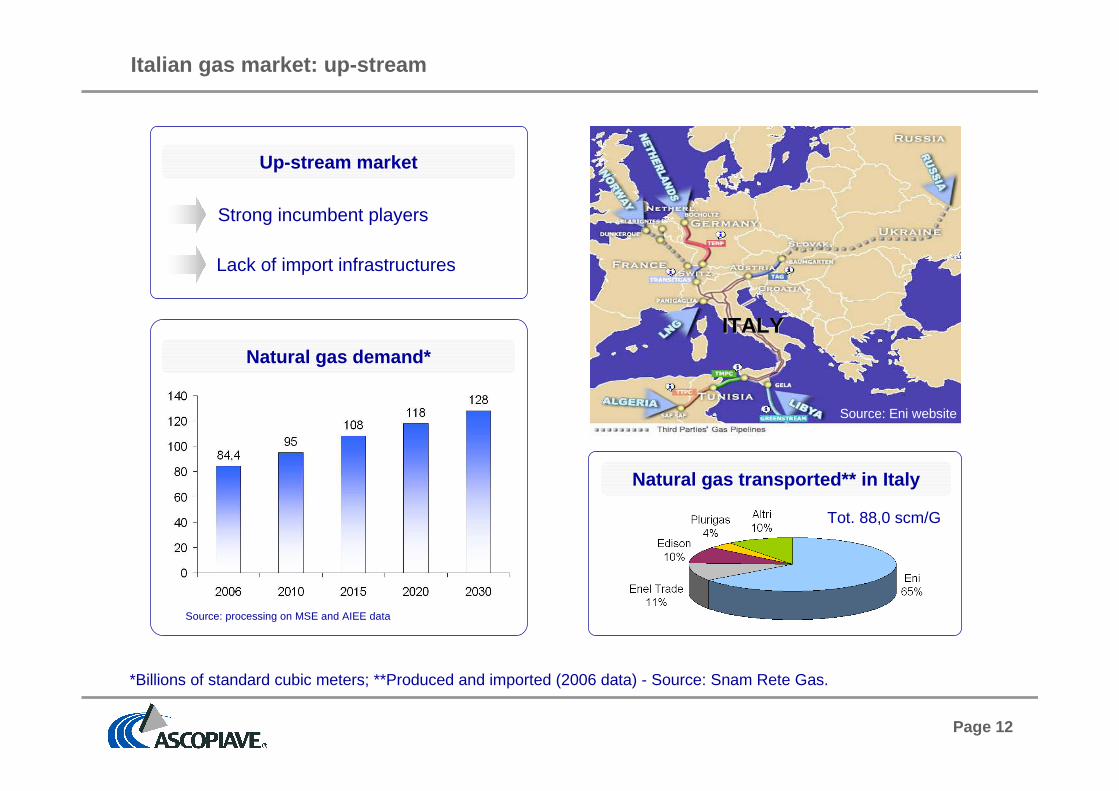

Italian gas market: up-stream

ITALYITALY

Source: Eni website

Up-stream market

Lack of import infrastructures

Strong incumbent players

Natural gas demand*

Source: processing on MSE and AIEE data

*Billions of standard cubic meters; **Produced and imported (2006 data) - Source: Snam Rete Gas.

Natural gas transported** in Italy

Tot. 88,0 scm/G

Page 13

CONTENTS

Business Overview

Strategy

Financial highlights

Dividends

Annexes

Page 14

Strategic guidelines

Strategic guidelines :

taking advantage of opportunities arising from the liberalisation of the gas market, includingopportunities in the national and international gas wholesale, transportation and storage market

consolidating its presence as a utility provider in northern Italy, by rationalising and optimising itsoperating process and increasing its efficiency through economies of scale

Up-stream integration

Participation inthe consolidation

processGrowth

p

p

Page 15

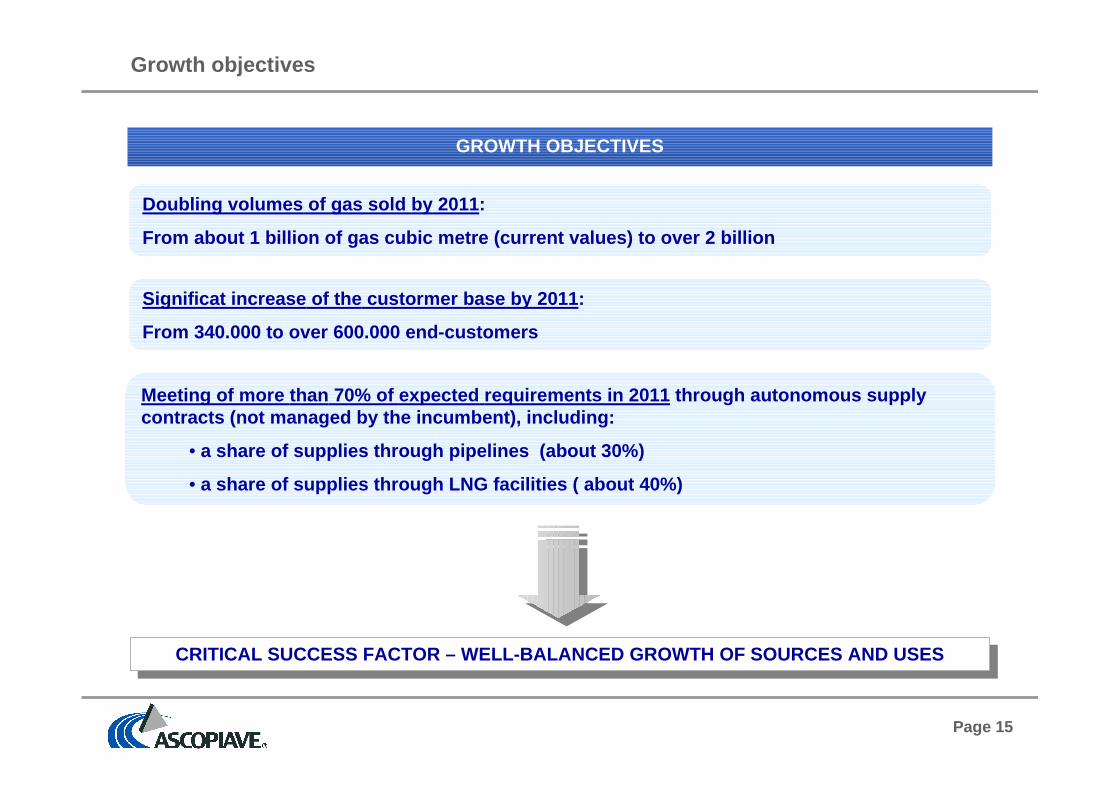

Growth objectives

CRITICAL SUCCESS FACTOR – WELL-BALANCED GROWTH OF S OURCES AND USESCRITICAL SUCCESS FACTOR – WELL-BALANCED GROWTH OF S OURCES AND USES

GROWTH OBJECTIVES

Doubling volumes of gas sold by 2011:

From about 1 billion of gas cubic metre (current va lues) to over 2 billion

Meeting of more than 70% of expected requirements in 2011 through autonomous supplycontracts (not managed by the incumbent), including :

• a share of supplies through pipelines (about 30%)

• a share of supplies through LNG facilities ( about 40%)

Significat increase of the custormer base by 2011 :

From 340.000 to over 600.000 end-customers

Page 16

Swot analysis

WeaknessWeakness

� Not present in upstream gas market

� Dependence on incumbent gas imports

� Limited knowledge of the brand outside the regionserviced

� Electric business in start-up phase

� Regulatory uncertainty (e.g. Res. N. 248/04, etc.)

� Conflicts within the gas chain

� Entrance and consolidation of foreign groups and m ajorItalian utilities

� Competitive pressure increase and attacks from newentrants

� Enel’s role in dual-fuel market

� Gas concessions expiring (2009/2010)

� Total market ‘opening’ (also for electricity, as of 1 July2007) – Cross selling on customer base

� Infrastructure development projects likely to incr easethe country’s gas importing capacity and createbusiness opportunities abroad

� Trends towards a liquid market in the medium term(establishment of the Gas Exchange)

� Temporary push towards aggregations of companies –increase in geographical coverage by expanding thecorporate structure

� Tenders for gas distribution concessions

� Strong liquidity and high investment potentials (wi th‘third party access’ exemption right)

� Large end customer base

� Deeply rooted presence in reference geographical a rea

� Strong local brand reputation

� Local Authorities are stakeholders in the Group

� High degree of customer loyalty

StrengthsStrengths

ThreatsThreatsOpportunitiesOpportunities

Page 17

Up-stream integration (1)

� Long-term gas supply contracts with international operators

� Targeted acquisition of capabilities in terms of gas transportation infrastructures into Italy

� Trading operations in Italy (transactions at the border and “PSV”) and abroad

� Investments in new storage sites (i.e. acquisition of shares in viable companies)

� Investments in new LNG plants (i.e. acquisition of shares in viable companies)

� Investments in foreign gas exploitation and production business (i.e. acquisition of shares in viablecompanies)

Integration within the gas chain (both mid-stream a nd up-stream) to ensure gas supply fullautonomy and reliability, alongside with an efficie nt cost structure and a competitive edgeon the market

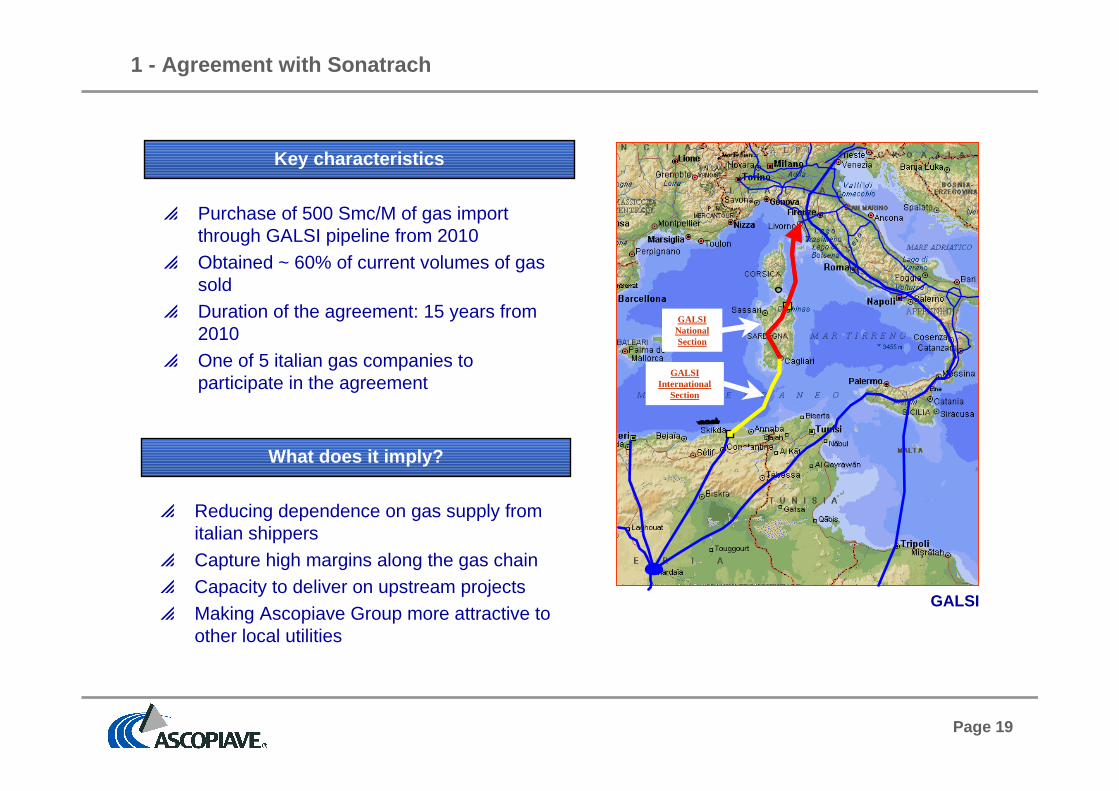

Page 18

Gas ImportGas Import p Signing an agreement with Sonatrach for 500Scm/M of gas

Up-stream integration (2)

Gas wholesale andtrading

Gas wholesale andtrading

p Wholesales tradingp Foreign tradingp Autonomous structuring of the operations along

the value chain

Acquisition of storagecapacity

Acquisition of storagecapacity

p Ital Gas Storage acquisition completed in may2006

p Ital Gas Storage is active in gas storage inCornegliano

Other upstreamprojects

Other upstreamprojects

p Participation in initiative of other gas pipelines

p Considering acquisition of a qualified stake in re-gasification terminals

1

2

3

4

Page 19

p Purchase of 500 Smc/M of gas importthrough GALSI pipeline from 2010

p Obtained ~ 60% of current volumes of gassold

p Duration of the agreement: 15 years from2010

p One of 5 italian gas companies toparticipate in the agreement

1 - Agreement with Sonatrach

p Reducing dependence on gas supply fromitalian shippers

p Capture high margins along the gas chainp Capacity to deliver on upstream projectsp Making Ascopiave Group more attractive to

other local utilities

Key characteristics

What does it imply?

GALSI

GALSINationalSection

GALSIInternational

Section

Page 20

2 - Gas wholesale and trading (1)

Objectives of the new activities

Entering new segments of the value chain capturing extramargins

Increasing and stabilizing gas sale volumes

Maximizing margin on traditional activities

Page 21

2 - Gas wholesale and trading (2)

~ 50 million of scm – Y 2007Foreign trading

~ 750 million of scm – Y 2007-2008Import spot

120 million of scm – Y 2007-2009Gas release

Autonomous management of logistic operations

~ 150 million of scm – Y 2007-2008Trading at “PSV”

~ 300 million of scm – Y 2007-2008Wholesales

~ 120 million of scm – Y 2008-2029Acquisition of transportation capacity on existinginternational pipelines

Page 22

3 - Gas storage

Storage technical characteristics

Working gas (Scm/M) 590-1,010

Cushion gas (Scm/M) 900

Maximum storage capacity (Scm/M) 1,910

Maximum daily use (Scm/M) 16.5

Investments expected (€/M) 400*

Ital Gas Storage

is active in gas storage in Cornegliano

acquisition completed in May 2006

ITALYLOMBARDY

Cornegliano

*220 €/M of cushion gas.

Page 23

4 - Import infrastructures and new projects

Eni2Greenstream

Endesa8Trieste

Nuove Energie Srl8P.Emped.

Gas Natural

Gas Natural

Erg, Shell

Cross Energy

Edison, BP

OLT, Endesa,AMGA

BG

Edison, QP Exxonl

Eni

Eni

Edison, Depa

Sonatrach, Edison,Enel, Wintershall, Hera

Operator

>110Total

8Zaule

8Taranto

8Priolo Augusta

12Gioia Tauro

8Rosignano

4Livorno

8Brindisi

8Rovigo

3,2 +3,3Rep. TTPC

3,2 +3,3Rep. TAG

8IGI

8/10GALSI

CapacityPlan

National production declining from 10.9Scm/G in 2006 to 4.3 Scm/G in 2012

+6.5 Gmc31 Gmc

+ 6.5 Gmc27 Gmc

TRANSMED/TTPC

BG/Brindisi

8 Gmc

Edison/Rovigo

8 Gmc

Gas NaturalTaranto

8 Gmc

GasNaturalTrieste8 Gmc

CrossEnergy

Gioia Tauro

12 Gmc

Olt Livorno

4 Gmc

GALSI

8/10 Gmc

Edison/BPRosignano

8 Gmc

Erg,Shell/Priolo

8 Gmc

8-12 Gmc

Endesa Trieste

1,5 Gmc

PIPELINESlovenia

GREENSTREAM

8 Gmc+ 2 Gmc

P. Empedocle

8 Gmc

18 Gmc

PIPELINENetherlands/

Norway

4 Gmc

ENI Panigaglia

8 Gmc

IGI

Projected pipelines

Current pipelines Current LNG terminals

Projected LNG Terminals

Page 24

Growth in size through a significant expansion of i ts customer base

Growth in the gas down-stream market (1)

Increase number ofclients and

concessionsmanaged

Increase number ofclients and

concessionsmanaged

p Participation in competitive bidding for the awardof contracts to manage the gas distribution service

p An integrated service offer with a dual fuel salespolicy (a joint commercial proposal for gas andelectricity)

p Make selective acquisitions

Natural gas market (2006)

*Through secondary network; data in Scm/M

Italy "Triveneto"

Number of gas distributors 416 61

Number of gas concessions 5,861 832

Number of gas customers 20,214,000 2,500,000

Volumes of gas distributed* 34,656 5,784

Length of the distribution network (km) 225,792 38,26 0

Page 25

Growth in the gas down-stream market (2)

1. Acquisitions(both gas distributionand sales business)

Gas saleCompany A

Gas saleCompany B

Gas saleCompany N

AscopiaveS.p.A.

EstenergyS.p.A.

AscotradeS.p.A.

…

2. Acquisitions(only gas sales

business)

Model

3. Partnershipon sales activity

AscotradeS.p.A.

Partner A

Partner B

Partner N

BimetanoServizi S.r.l.

AscopiaveS.p.A.

…

> 50%

Model

AscopiaveS.p.A.

…

Model

Gas saleCompany A

Gas distributionCompany A

Gas saleCompany N

Gas distributionCompany N

Page 26

Growth in the gas down-stream market (3)

Concluded deal

Deals Customers Gas sold

Acquisition of Bimetano Servizi gas sale business + 29,453 + 82 scm/M

Acquisition of a 51% stake in Global Energy Start-up n.a.

Establishment of Etra Energia Start-up n.a.

Acquisition of a 49% stake in Estenergy + 243,237 + 512 scm/M

Total concluded deals + 272,690 + 594 scm/M

To be negotiated

Deals Customers Gas sold

Vesta3 + Spim Energia + 18,462 + 49 scm/M

ASM Set + 24,526 + 55 scm/M

Total to be negotiated deals + 42,988 + 104 scm/M

Total + 315,678 + 698 scm/M

Ascopiave before operations + 313,355 + 790 scm/M

Change % + 100.7% + 88.4%

Page 27

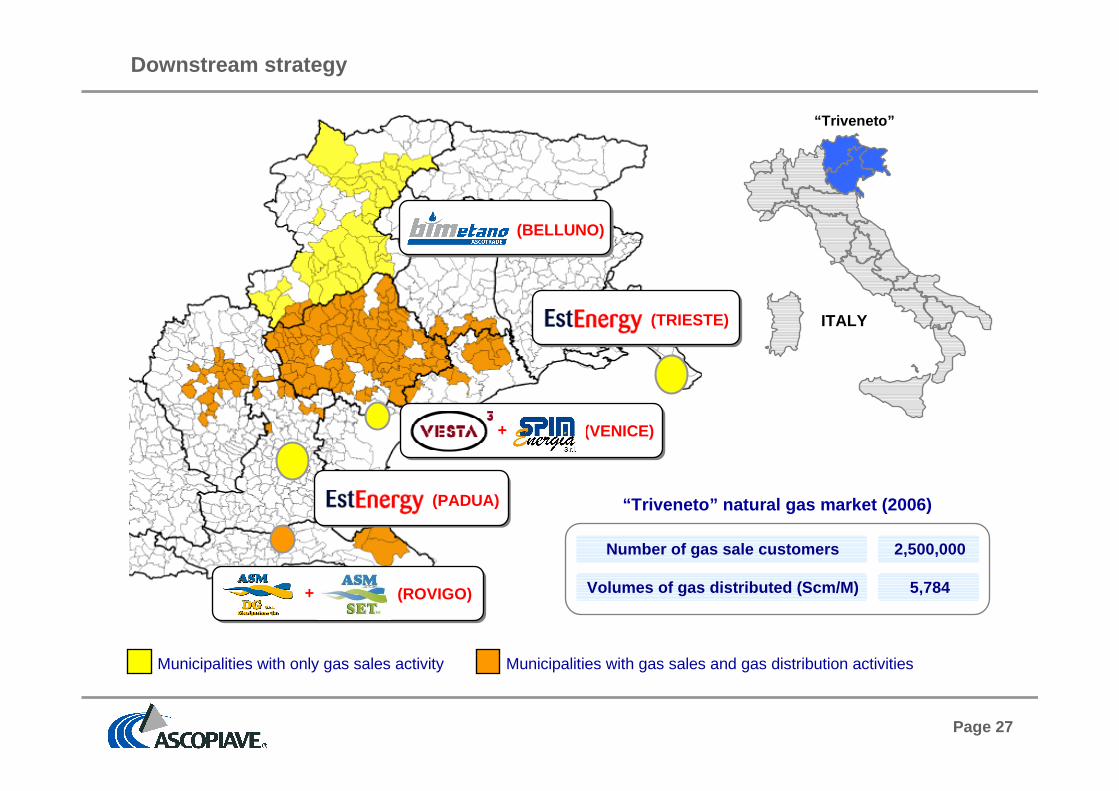

Municipalities with only gas sales activity Municipalities with gas sales and gas distribution activities

(TRIESTE)

(BELLUNO)

Downstream strategy

“Triveneto”

ITALY

“Triveneto” natural gas market (2006)

Number of gas sale customers 2,500,000

Volumes of gas distributed (Scm/M) 5,784

(PADUA)

(VENICE) +

+ (ROVIGO)

Page 28

Operation Estenergy (1)

As of September 13th 2007, Ascopiave has signed an agreement with Acegas-APS S.p.A. for theacquisition of a quota of 49% of Estenergy S.p.A., the gas sale company controlled by Acegas-APS.

100%

89%

BEFORE THE OPERATION...

49%

51%

...AFTER THE OPERATION

Estenergy Ascotrade Aggregated Chg %

No. of gas sale customers 243.237 342.808 586.045 71%

Volumes of gas sales (Mcm) 512 872 1.385 59%

89%

Page 29

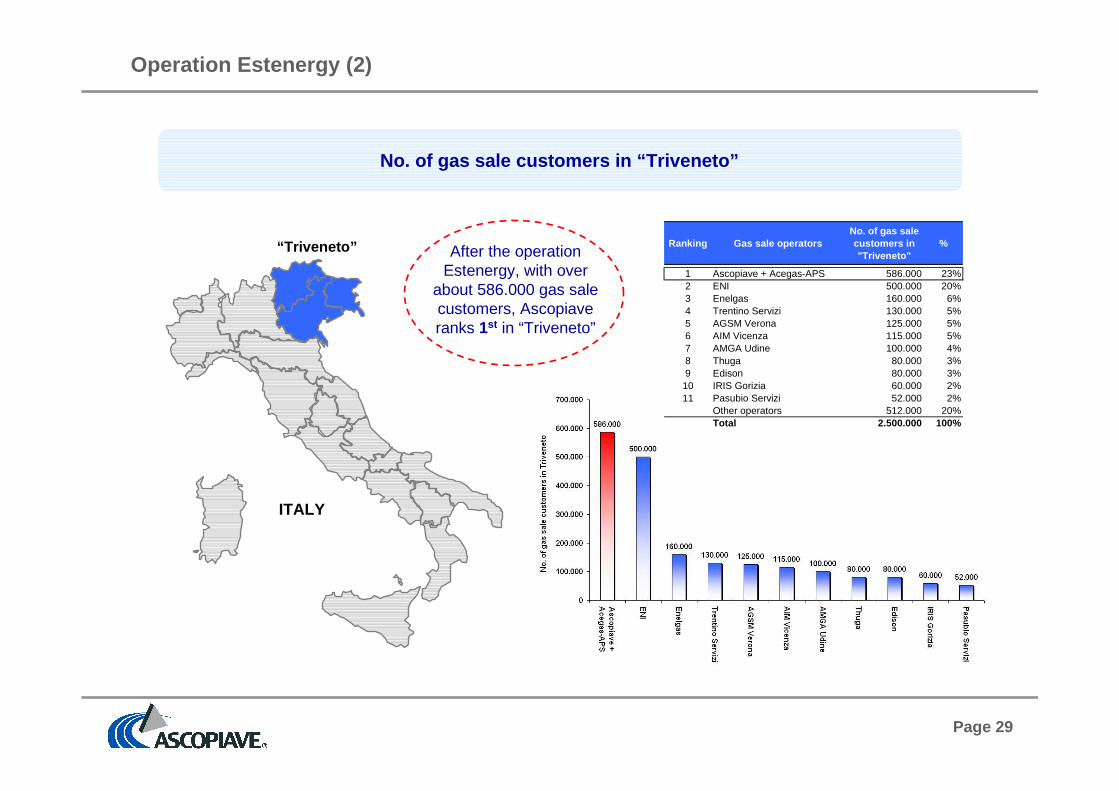

Operation Estenergy (2)

No. of gas sale customers in “Triveneto”

After the operationEstenergy, with over

about 586.000 gas salecustomers, Ascopiaveranks 1st in “Triveneto”

“Triveneto”

ITALY

Ranking Gas sale operatorsNo. of gas sale customers in "Triveneto"

%

1 Ascopiave + Acegas-APS 586.000 23%2 ENI 500.000 20%3 Enelgas 160.000 6%4 Trentino Servizi 130.000 5%5 AGSM Verona 125.000 5%6 AIM Vicenza 115.000 5%7 AMGA Udine 100.000 4%8 Thuga 80.000 3%9 Edison 80.000 3%10 IRIS Gorizia 60.000 2%11 Pasubio Servizi 52.000 2%

Other operators 512.000 20%Total 2.500.000 100%

Page 30

Operation Estenergy (3)

Volumes of natural gas sold in Italy

After the operationEstenergy, with over about1,4 billion of cubic meters

sold, Ascopiave ranks 6th inItaly

ITALY

Ranking Gas sale operatorVolumes of gas sold in

Italy%

1 Eni 36.544 47%2 Enel Trade 7.547 10%3 Enel Energia 4.229 5%4 Hera Comm 1.900 2%5 Edison 1.469 2%6 Ascopiave + Acegas-APS 1.385 2%7 Gaz de France 1.142 1%8 E.ON Vendita 1.117 1%9 Plurigas 1.059 1%

10 AEM Acquisto e Vendita Energia 1.014 1%11 Blumet 1.003 1%12 Toscana Energia Clienti 987 1%

Other 18.415 24%Total 77.811 100%

Page 31

CONTENTS

Business Overview

Strategy

Financial highlights

Dividends

Annexes

Page 32

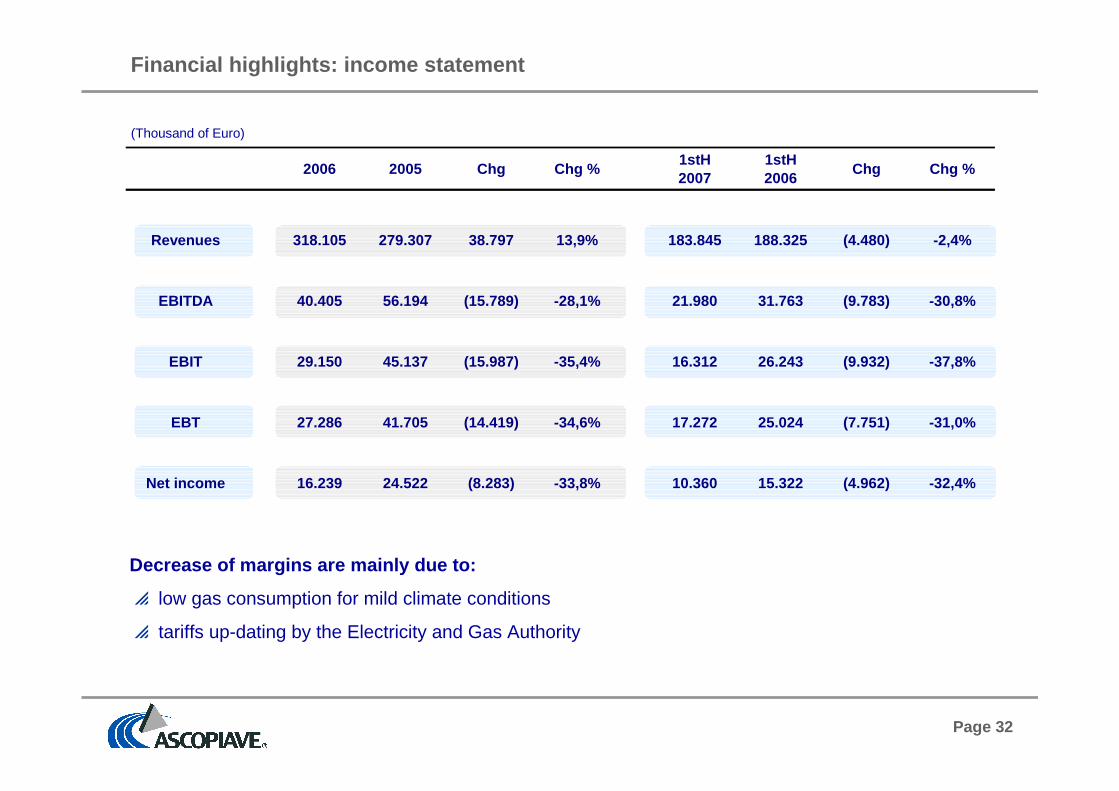

Financial highlights: income statement

(Thousand of Euro)

2006 2005 Chg Chg %1stH2007

1stH2006

Chg Chg %

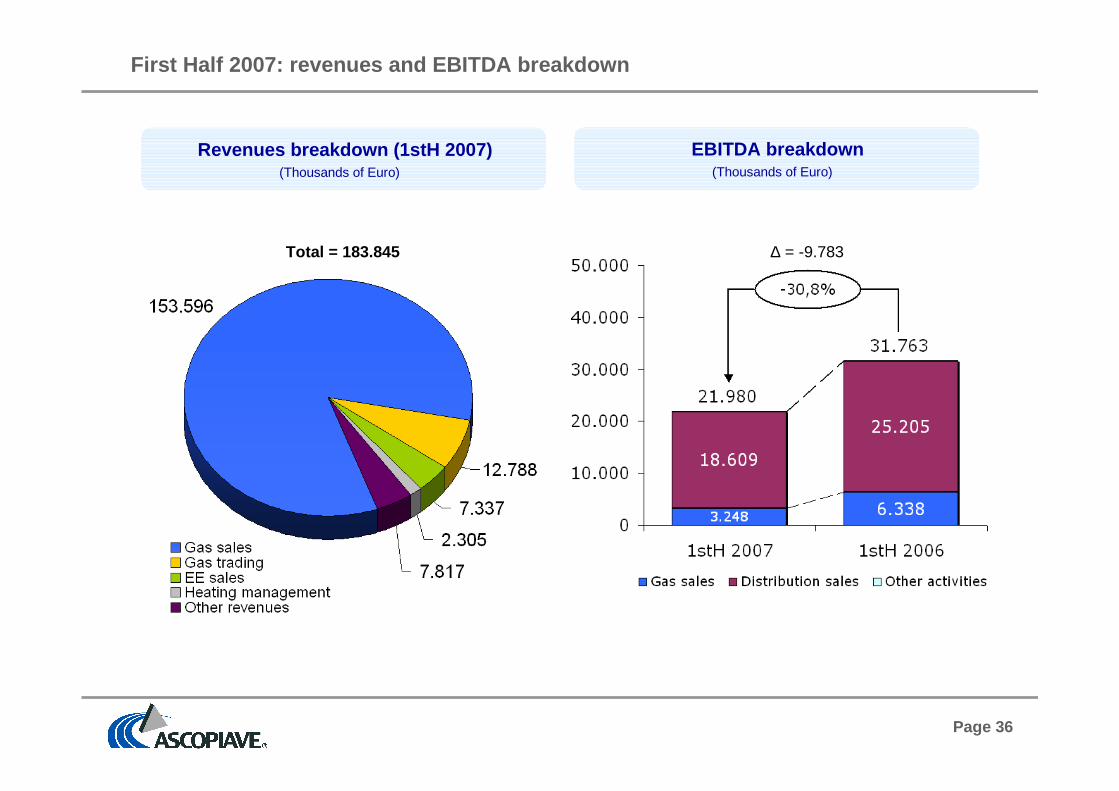

Revenues 318.105 279.307 38.797 13,9% 183.845 188.325 (4.4 80) -2,4%

EBITDA 40.405 56.194 (15.789) -28,1% 21.980 31.763 (9.783) -30,8%

EBIT 29.150 45.137 (15.987) -35,4% 16.312 26.243 (9.932) -37,8%

EBT 27.286 41.705 (14.419) -34,6% 17.272 25.024 (7.751) -31,0%

Net income 16.239 24.522 (8.283) -33,8% 10.360 15.322 (4.9 62) -32,4%

Decrease of margins are mainly due to:

p low gas consumption for mild climate conditions

p tariffs up-dating by the Electricity and Gas Authority

Page 33

Financial highlights: balance sheet

(Thousand of Euro)

*Negative values of the Net Financial Position indicate that the Group has a positive liquidity balance

31/12/06 31/12/05 Chg Chg % 30/06/07 31/12/06 Chg Chg %

Capital employed 281.361 284.574 (3.213) -1,1% 306.924 281.361 25.563 9,1%

Shareholders equity 368.902 194.586 174.316 89,6% 365.708 368.902 (3.194) -0,9%

Net financial position* (87.541) 89.988 (177.529) -197,3% (58.784) (87.541) 28.757 -32,9%

Page 34

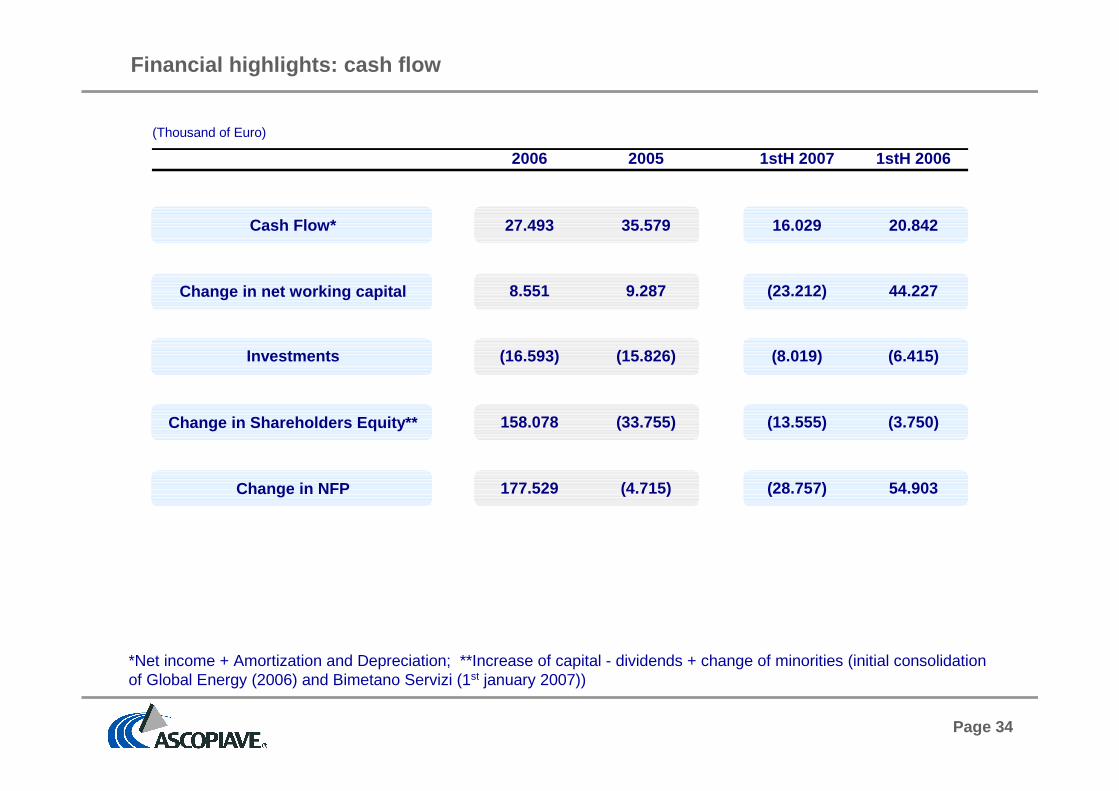

Financial highlights: cash flow

*Net income + Amortization and Depreciation; **Increase of capital - dividends + change of minorities (initial consolidationof Global Energy (2006) and Bimetano Servizi (1st january 2007))

(Thousand of Euro)

2006 2005 1stH 2007 1stH 2006

Cash Flow* 27.493 35.579 16.029 20.842

Change in net working capital 8.551 9.287 (23.212) 44.227

Investments (16.593) (15.826) (8.019) (6.415)

Change in Shareholders Equity** 158.078 (33.755) (13.555) (3.750)

Change in NFP 177.529 (4.715) (28.757) 54.903

Page 35

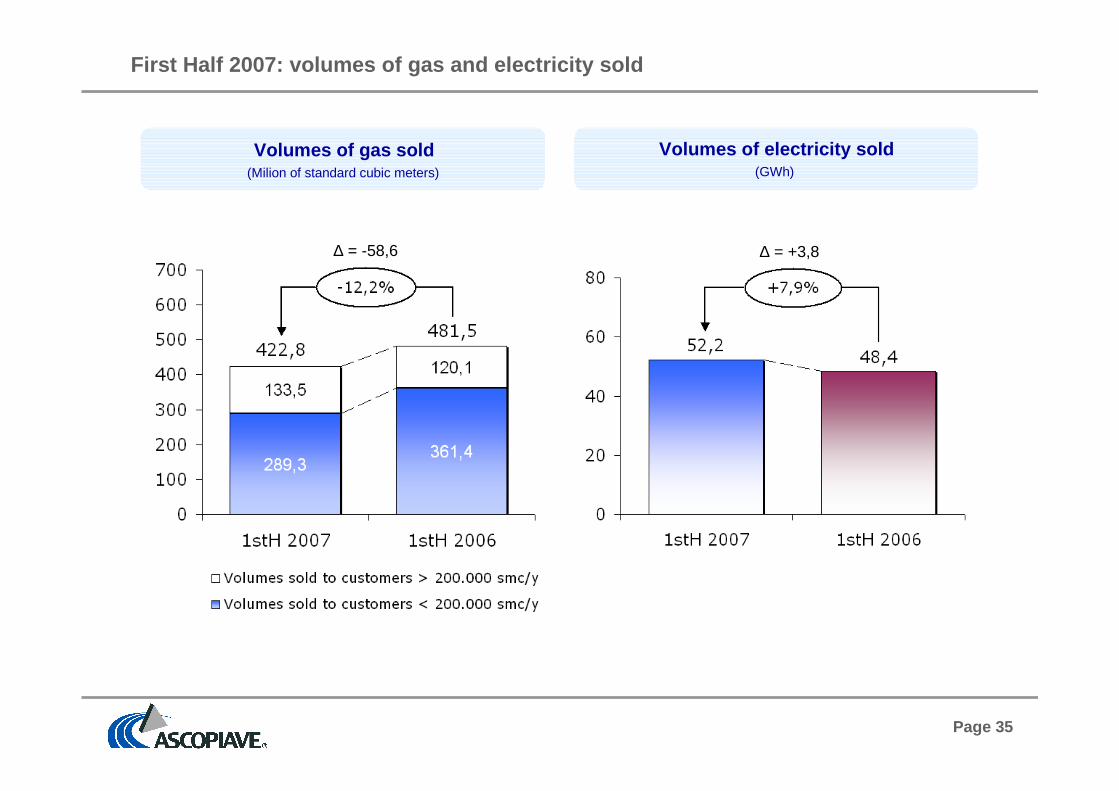

First Half 2007: volumes of gas and electricity sol d

Volumes of gas sold(Milion of standard cubic meters)

Volumes of electricity sold(GWh)

∆ = -58,6 ∆ = +3,8

Page 36

First Half 2007: revenues and EBITDA breakdown

EBITDA breakdown(Thousands of Euro)

Revenues breakdown (1stH 2007)(Thousands of Euro)

Total = 183.845 ∆ = -9.783

Page 37

First Half 2007 EBITDA bridge

∆ = -9.783

EBITDA bridge(Thousands of Euro)

Change in grossmargin on gas sales

and distribution

Page 38

Business Overview

Strategy

Financial highlights

Dividends

Annexes

CONTENTS

Page 39

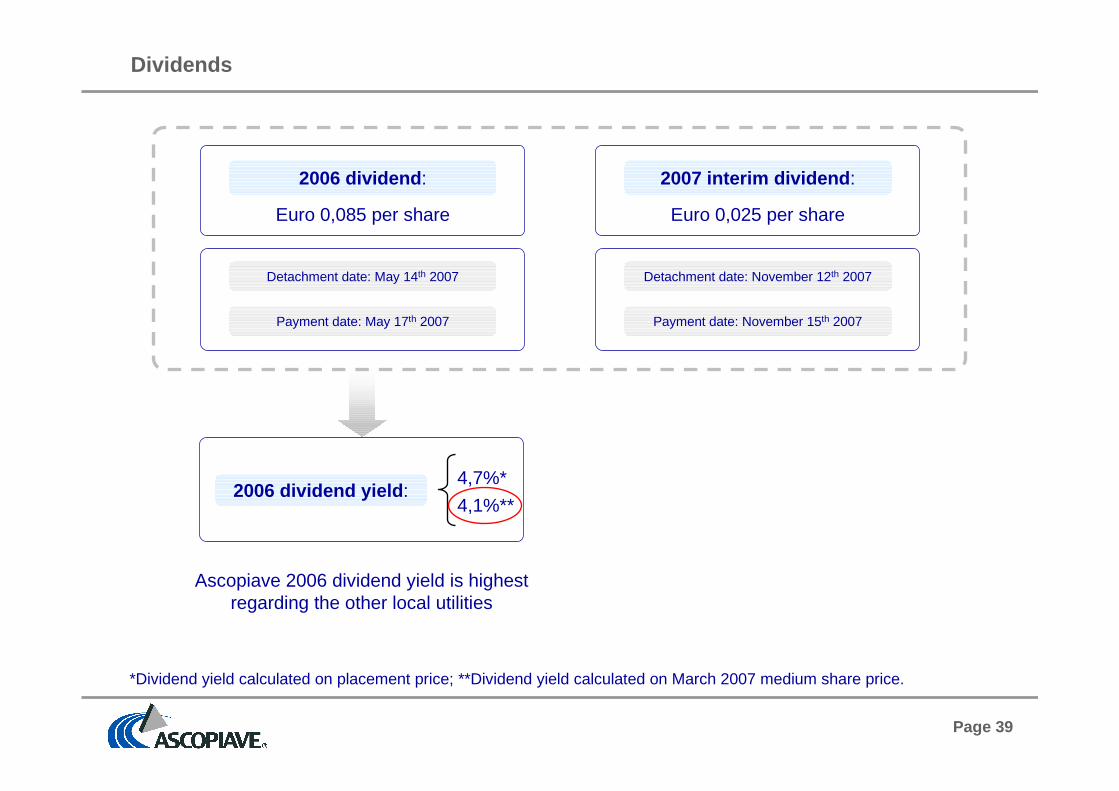

Dividends

*Dividend yield calculated on placement price; **Dividend yield calculated on March 2007 medium share price.

2006 dividend yield :4,7%*

4,1%**

2006 dividend :

Euro 0,085 per share

Detachment date: May 14th 2007

Payment date: May 17th 2007

2007 interim dividend :

Euro 0,025 per share

Detachment date: November 12th 2007

Payment date: November 15th 2007

Ascopiave 2006 dividend yield is highestregarding the other local utilities

Page 40

Business Overview

Strategy

Financial highlights

Dividends

Annexes

CONTENTS

Page 41

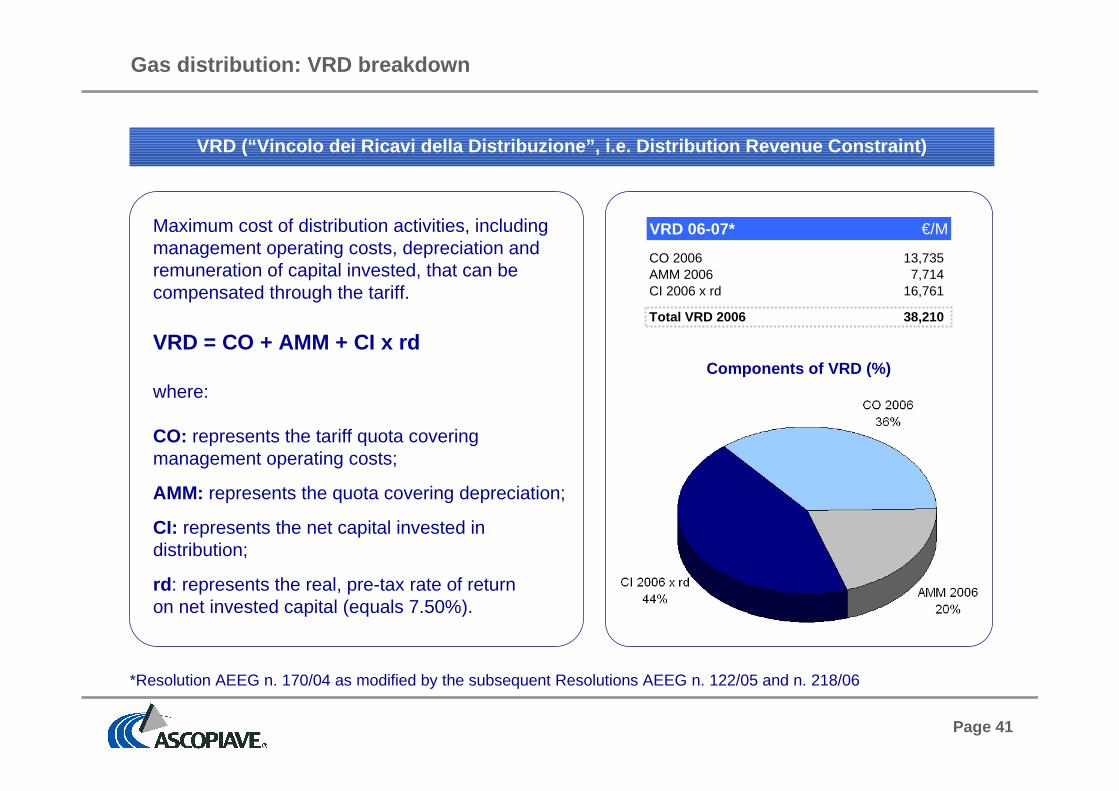

Gas distribution: VRD breakdown

Maximum cost of distribution activities, includingmanagement operating costs, depreciation andremuneration of capital invested, that can becompensated through the tariff.

VRD = CO + AMM + CI x rd

where:

CO: represents the tariff quota coveringmanagement operating costs;

AMM: represents the quota covering depreciation;

CI: represents the net capital invested indistribution;

rd : represents the real, pre-tax rate of returnon net invested capital (equals 7.50%).

*Resolution AEEG n. 170/04 as modified by the subsequent Resolutions AEEG n. 122/05 and n. 218/06

Components of VRD (%)

VRD (“Vincolo dei Ricavi della Distribuzione”, i.e. Distribution Revenue Constraint)

VRD 06-07* €/M

CO 2006 13,735AMM 2006 7,714CI 2006 x rd 16,761

Total VRD 2006 38,210

Page 42

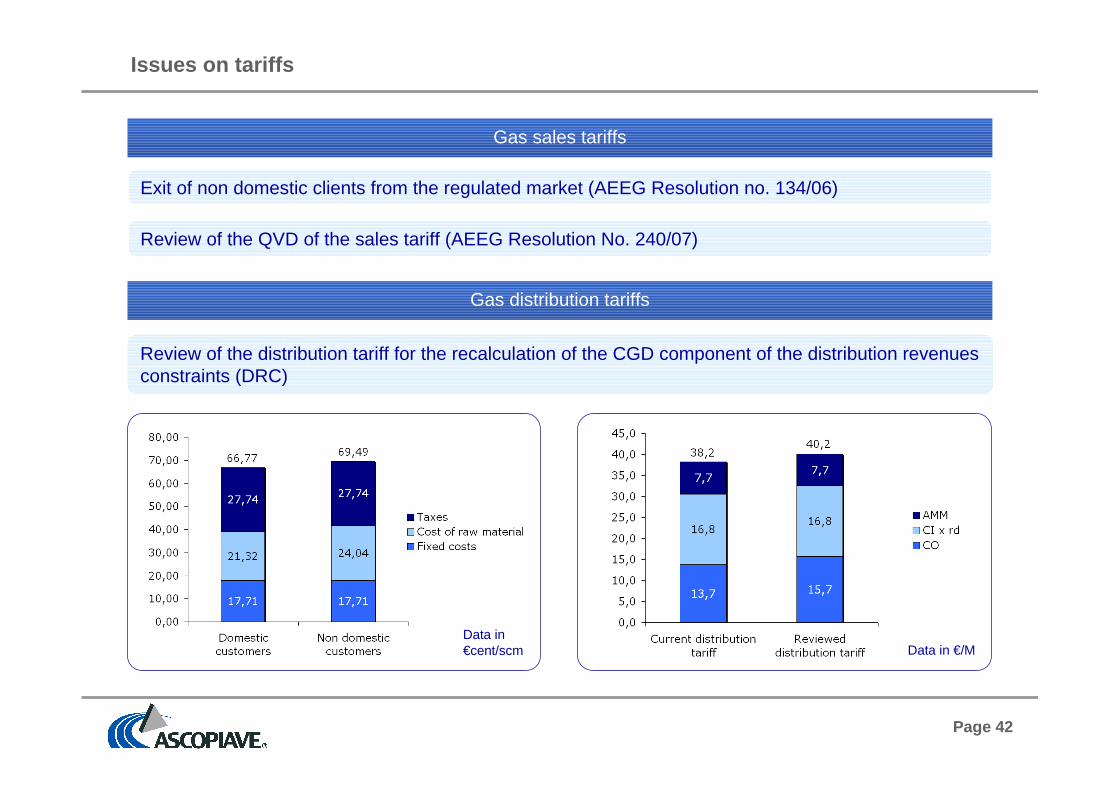

Issues on tariffs

Gas sales tariffs

Exit of non domestic clients from the regulated market (AEEG Resolution no. 134/06)

Review of the QVD of the sales tariff (AEEG Resolution No. 240/07)

Gas distribution tariffs

Review of the distribution tariff for the recalculation of the CGD component of the distribution revenuesconstraints (DRC)

Data in€cent/scm Data in €/M

Page 43

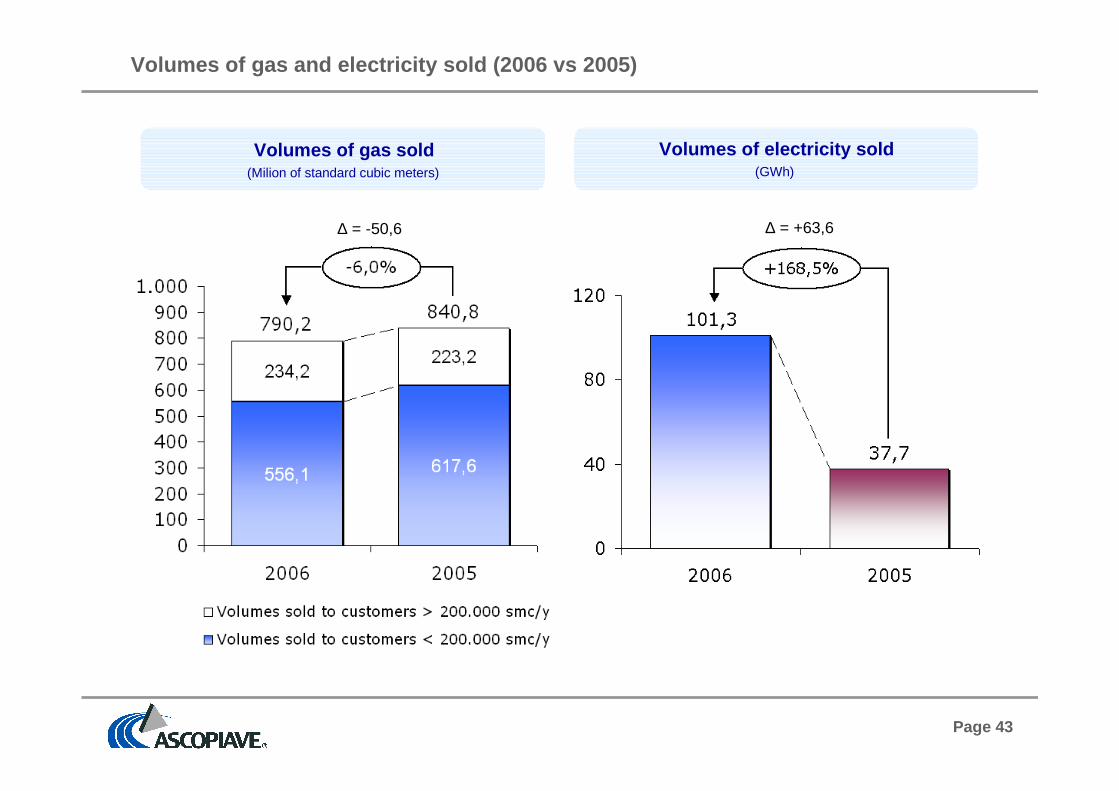

Volumes of gas and electricity sold (2006 vs 2005)

Volumes of gas sold(Milion of standard cubic meters)

∆ = -50,6

Volumes of electricity sold(GWh)

∆ = +63,6

Page 44

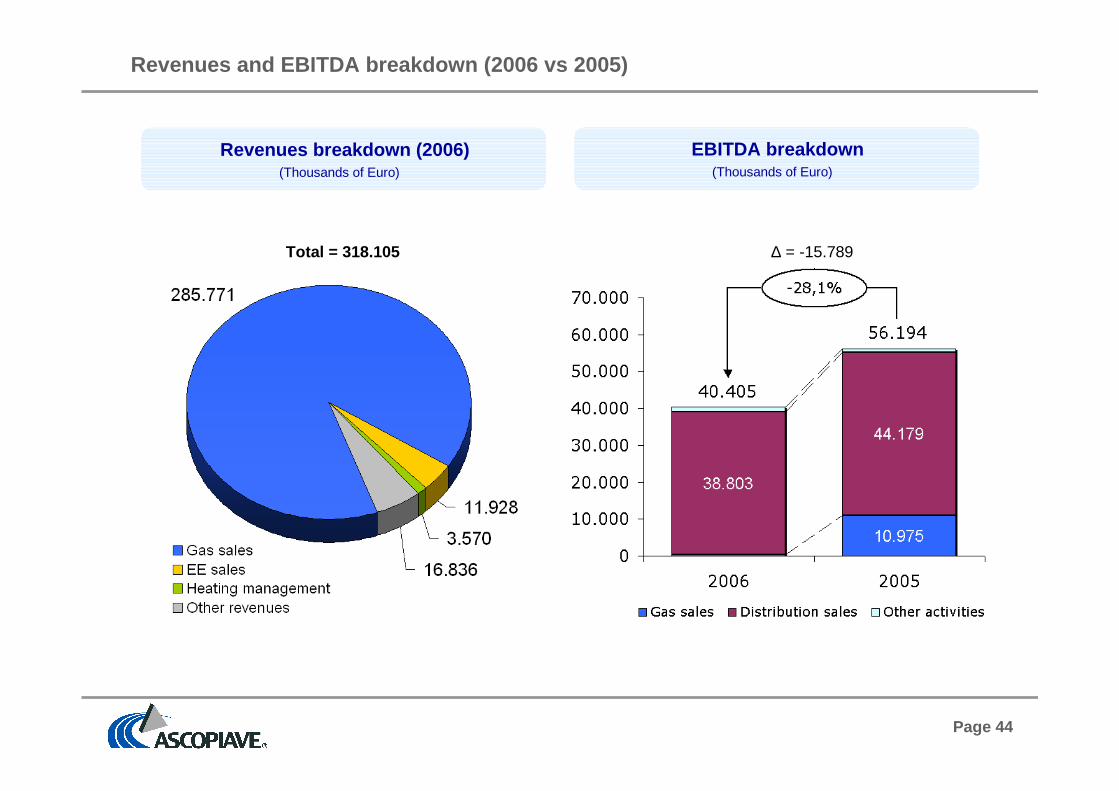

Revenues and EBITDA breakdown (2006 vs 2005)

EBITDA breakdown(Thousands of Euro)

∆ = -15.789

Revenues breakdown (2006)(Thousands of Euro)

Total = 318.105

Page 45

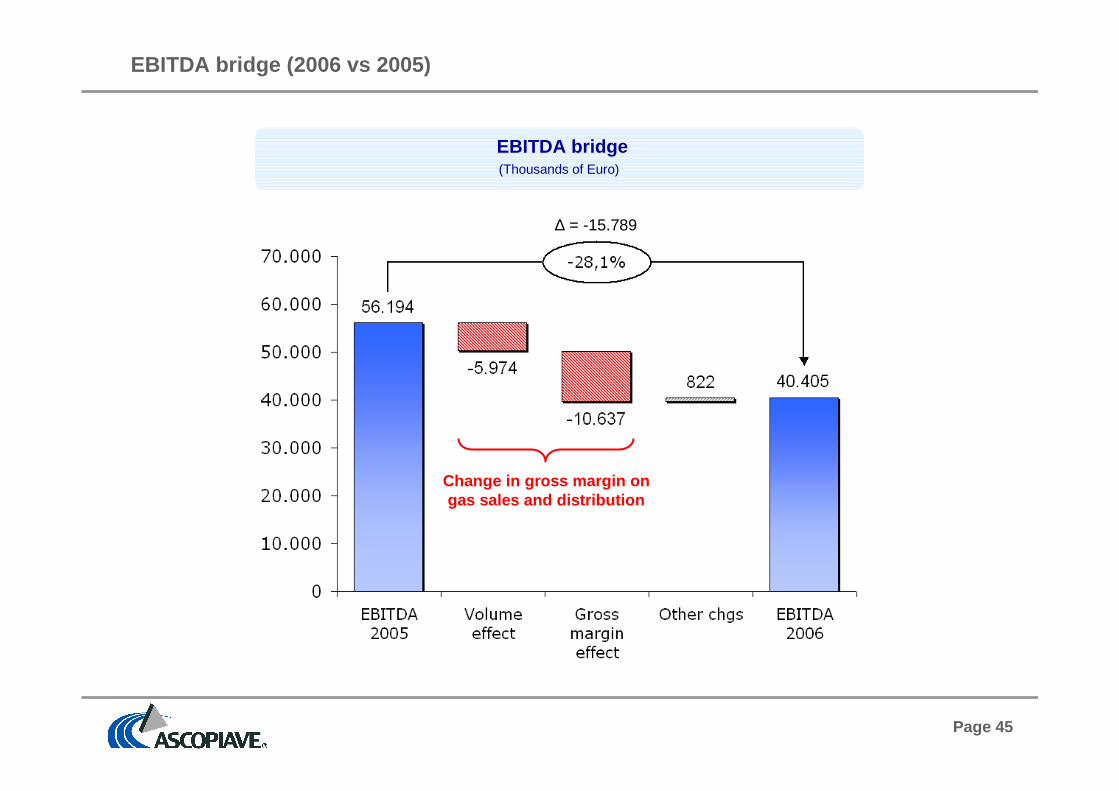

EBITDA bridge (2006 vs 2005)

∆ = -15.789

EBITDA bridge(Thousands of Euro)

Change in gross margin ongas sales and distribution