Embed Size (px)

Citation preview

State Taxation Acts Further Amendment Act 2016 No. 66 of 2016

TABLE OF PROVISIONSSection Page

Part 1—Preliminary 1

1 Purposes 12 Commencement 2

Part 2—Amendment of Land Tax Act 2005 3

3 Definitions 34 Taxable value of land 35 Land tax for absentee trusts surcharge rate 4

Part 3—Amendment of Payroll Tax Act 2007 5

6 Motor vehicle allowances 57 Statute law revision 5

Part 4—Amendment of Planning and Environment Act 1987 6

8 Definitions 69 Excluded subdivisions of land 610 Imposition of growth areas infrastructure contribution 611 New section 201SGA inserted 712 When and to whom the GAIC is payable 813 Liability to pay deferred GAIC in relation to subsequent

dutiable transactions 814 New section 201SOC inserted 815 Deferred GAIC and interest must be paid to Commissioner by

due date 916 New section 201SPAA inserted 917 Default on payment of deferred GAIC 1118 Deferred GAIC becomes a charge on the land 1119 Approval by Minister for staged payment of GAIC for

subdivisions or building works 1220 Certificate of partial release 1221 Notice to Registrar regarding registration of subdivision or

transfer of land 1322 Commissioner to pay GAIC into Consolidated Fund 1323 Exemption from paying GAIC for land dealings involving

public authorities and councils 13

1

24 New section 222 inserted 1325 Statute law revision 14

Part 5—Amendment of Valuation of Land Act 1960 15

26 Definitions 1527 Late nomination of valuation authority 1528 Notice of valuation 16

Part 6—Repeal of amending Act 17

29 Repeal of amending Act 17═══════════════

Endnotes 18

1 General information 18

State Taxation Acts Further Amendment Act 2016†

No. 66 of 2016

[Assented to 15 November 2016]

The Parliament of Victoria enacts:

Part 1—Preliminary1 Purposes

The main purposes of this Act are—

(a) to amend the Land Tax Act 2005—

(i) to make further provision in relation to the date for the determination of the taxable value of land that is not rateable land or non-rateable leviable land; and

Victoria

1

(ii) to correct one of the surcharge rates of land tax for absentee trusts; and

(b) to amend the Payroll Tax Act 2007 to change the way the exempt rate used in the calculation of the exempt component of motor vehicle allowances is determined; and

(c) to amend the Planning and Environment Act 1987 to make further provision in relation to the imposition, payment and apportionment of the growth areas infrastructure contribution in certain circumstances; and

(d) to amend the Valuation of Land Act 1960—

(i) to make further provision in relation to the meaning of a general valuation under that Act; and

(ii) to permit the Valuer-General to accept a late nomination from a collection agency to be the valuation authority for the purpose of valuing land for the fire services property levy; and

(iii) to require notices of valuation to show the Australian Valuation Property Classification Code (AVPCC) allocated to relevant land.

2 Commencement

(1) This Act (except Part 2 and sections 6 and 28) comes into operation on the day after the day on which this Act receives the Royal Assent.

(2) Part 2 comes into operation on 1 January 2017.

(3) Section 6 is taken to have come into operation on 1 July 2016.

(4) Section 28 comes into operation on 1 July 2018.

Section Page

2

Part 2—Amendment of Land Tax Act 20053 Definitions

In section 3(1) of the Land Tax Act 2005 insert the following definitions—

"general valuation means a general valuation within the meaning of the Valuation of Land Act 1960 made under section 11(a), 12, 13H(a) or 13I of that Act;

non-rateable non-leviable land has the same meaning as in the Valuation of Land Act 1960;".

4 Taxable value of land

For section 19(2) of the Land Tax Act 2005 substitute—

"(2) The relevant date is—

(a) for land that is rateable land or non-rateable leviable land—

(i) subject to subparagraph (ii), the date as at which that land was valued for the purposes of the last general valuation returned to the valuation authority before 1 January in the tax year; or

(ii) if that land has been valued for the purposes of a supplementary valuation after the return date of the last general valuation referred to in subparagraph (i) but before 1 January in the tax year, the return date of the supplementary valuation; and

Part 6—Repeal of amending Act

State Taxation Acts Further Amendment Act 2016No. 66 of 2016

3

(b) for land that is non-rateable non-leviable land—

(i) subject to subparagraph (ii), the date as at which rateable land or non-rateable leviable land was valued for the purposes of the last general valuation referred to in paragraph (a)(i); or

(ii) the date as at which the land was valued for and on behalf of the Commissioner before 1 January in the tax year by the Valuer-General or a valuer nominated by the Valuer-General.".

5 Land tax for absentee trusts surcharge rate

In Table 5.2 in Schedule 1 to the Land Tax Act 2005, in item 3, for "2·0575%" substitute "2·075%".

Part 6—Repeal of amending Act

State Taxation Acts Further Amendment Act 2016No. 66 of 2016

4

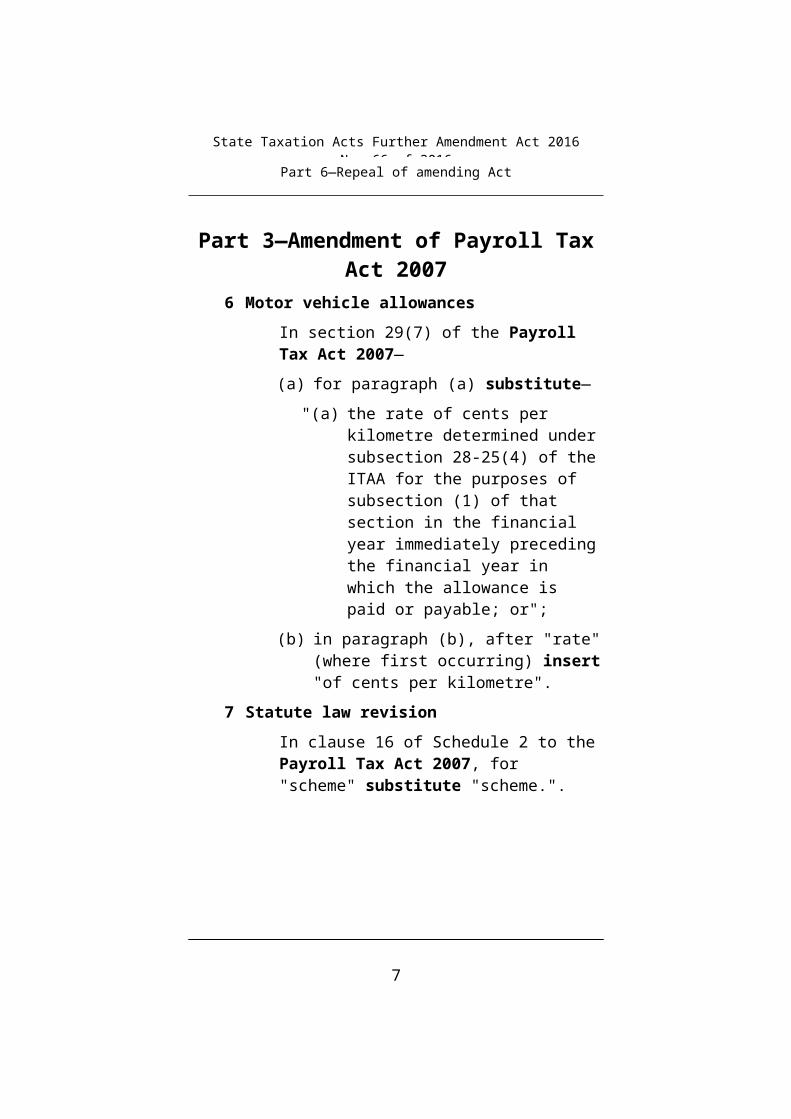

Part 3—Amendment of Payroll Tax Act 20076 Motor vehicle allowances

In section 29(7) of the Payroll Tax Act 2007—

(a) for paragraph (a) substitute—

"(a) the rate of cents per kilometre determined under subsection 28-25(4) of the ITAA for the purposes of subsection (1) of that section in the financial year immediately preceding the financial year in which the allowance is paid or payable; or";

(b) in paragraph (b), after "rate" (where first occurring) insert "of cents per kilometre".

7 Statute law revision

In clause 16 of Schedule 2 to the Payroll Tax Act 2007, for "scheme" substitute "scheme.".

Part 6—Repeal of amending Act

State Taxation Acts Further Amendment Act 2016No. 66 of 2016

5

Part 4—Amendment of Planning and Environment Act 1987

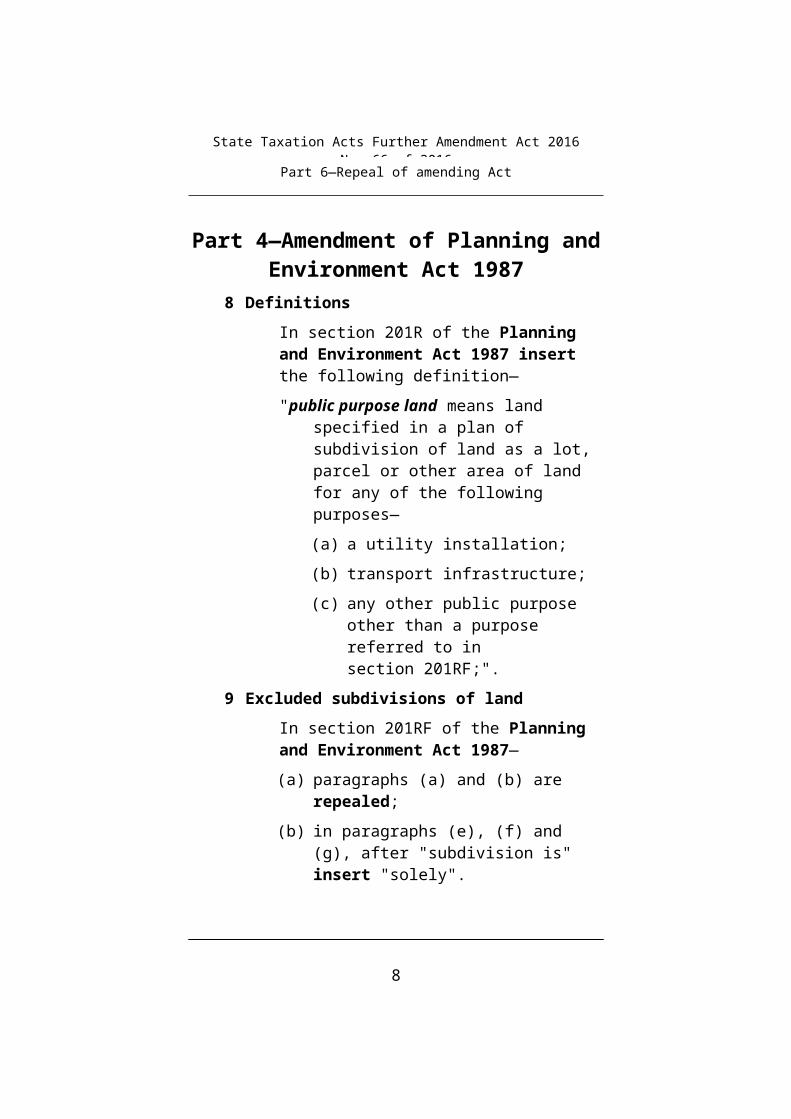

8 Definitions

In section 201R of the Planning and Environment Act 1987 insert the following definition—

"public purpose land means land specified in a plan of subdivision of land as a lot, parcel or other area of land for any of the following purposes—

(a) a utility installation;

(b) transport infrastructure;

(c) any other public purpose other than a purpose referred to in section 201RF;".

9 Excluded subdivisions of land

In section 201RF of the Planning and Environment Act 1987—

(a) paragraphs (a) and (b) are repealed;

(b) in paragraphs (e), (f) and (g), after "subdivision is" insert "solely".

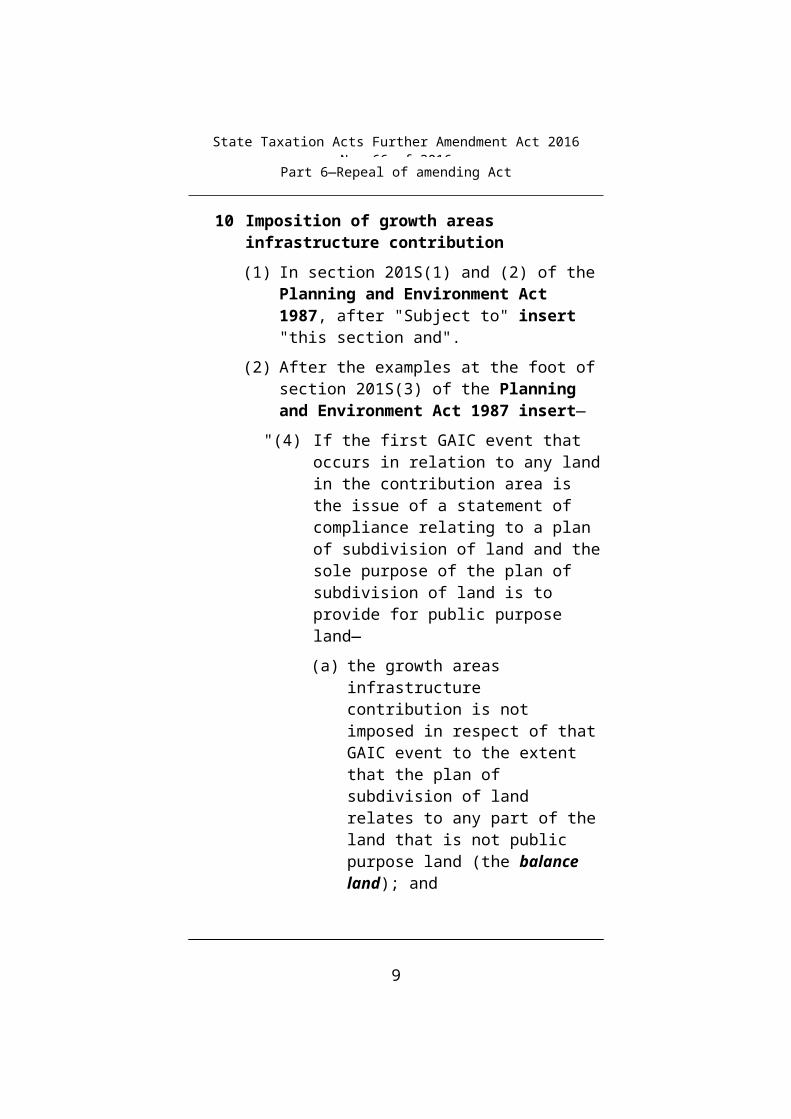

10 Imposition of growth areas infrastructure contribution

(1) In section 201S(1) and (2) of the Planning and Environment Act 1987, after "Subject to" insert "this section and".

(2) After the examples at the foot of section 201S(3) of the Planning and Environment Act 1987 insert—

"(4) If the first GAIC event that occurs in relation to any land in the contribution area is the issue of a statement of compliance relating to

Part 6—Repeal of amending Act

State Taxation Acts Further Amendment Act 2016No. 66 of 2016

6

a plan of subdivision of land and the sole purpose of the plan of subdivision of land is to provide for public purpose land—

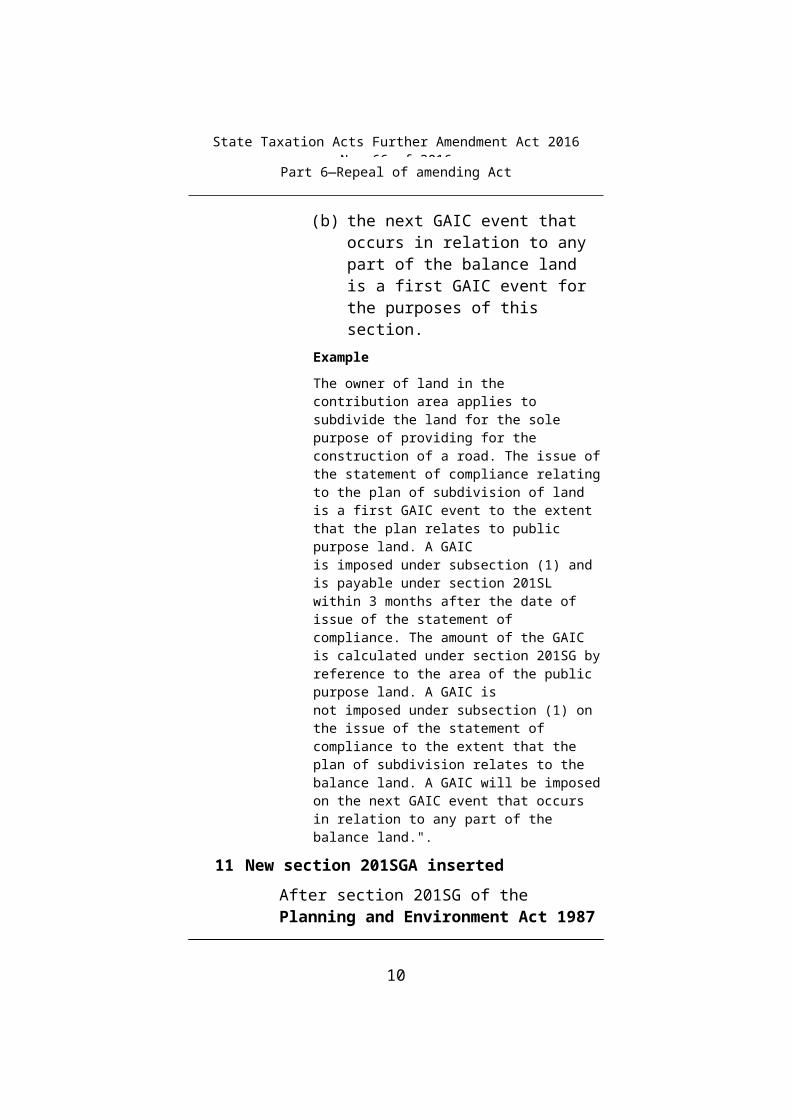

(a) the growth areas infrastructure contribution is not imposed in respect of that GAIC event to the extent that the plan of subdivision of land relates to any part of the land that is not public purpose land (the balance land); and

(b) the next GAIC event that occurs in relation to any part of the balance land is a first GAIC event for the purposes of this section.

Example

The owner of land in the contribution area applies to subdivide the land for the sole purpose of providing for the construction of a road. The issue of the statement of compliance relating to the plan of subdivision of land is a first GAIC event to the extent that the plan relates to public purpose land. A GAIC is imposed under subsection (1) and is payable under section 201SL within 3 months after the date of issue of the statement of compliance. The amount of the GAIC is calculated under section 201SG by reference to the area of the public purpose land. A GAIC is not imposed under subsection (1) on the issue of the statement of compliance to the extent that the plan of subdivision relates to the balance land. A GAIC will be imposed on the next GAIC event that occurs in relation to any part of the balance land.".

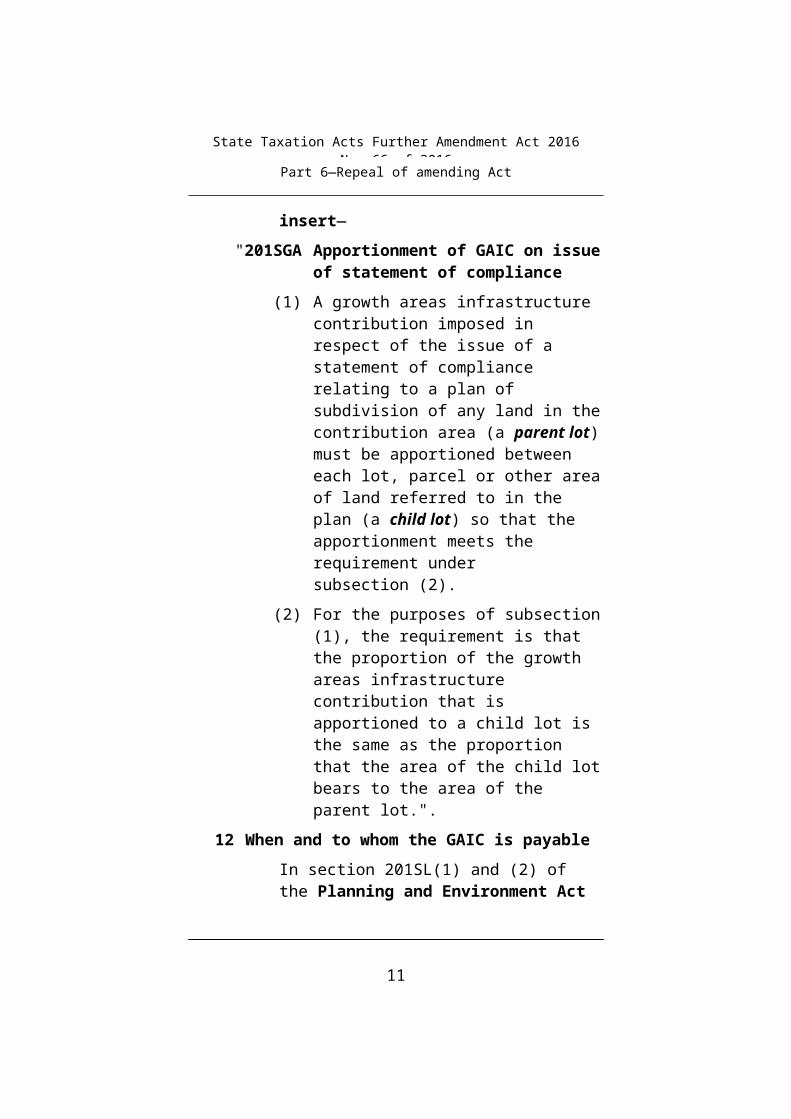

11 New section 201SGA inserted

After section 201SG of the Planning and Environment Act 1987 insert—

"201SGA Apportionment of GAIC on issue of statement of compliance

(1) A growth areas infrastructure contribution imposed in respect of the issue of a statement of compliance relating to a plan of

Part 6—Repeal of amending Act

State Taxation Acts Further Amendment Act 2016No. 66 of 2016

7

subdivision of any land in the contribution area (a parent lot) must be apportioned between each lot, parcel or other area of land referred to in the plan (a child lot) so that the apportionment meets the requirement under subsection (2).

(2) For the purposes of subsection (1), the requirement is that the proportion of the growth areas infrastructure contribution that is apportioned to a child lot is the same as the proportion that the area of the child lot bears to the area of the parent lot.".

12 When and to whom the GAIC is payable

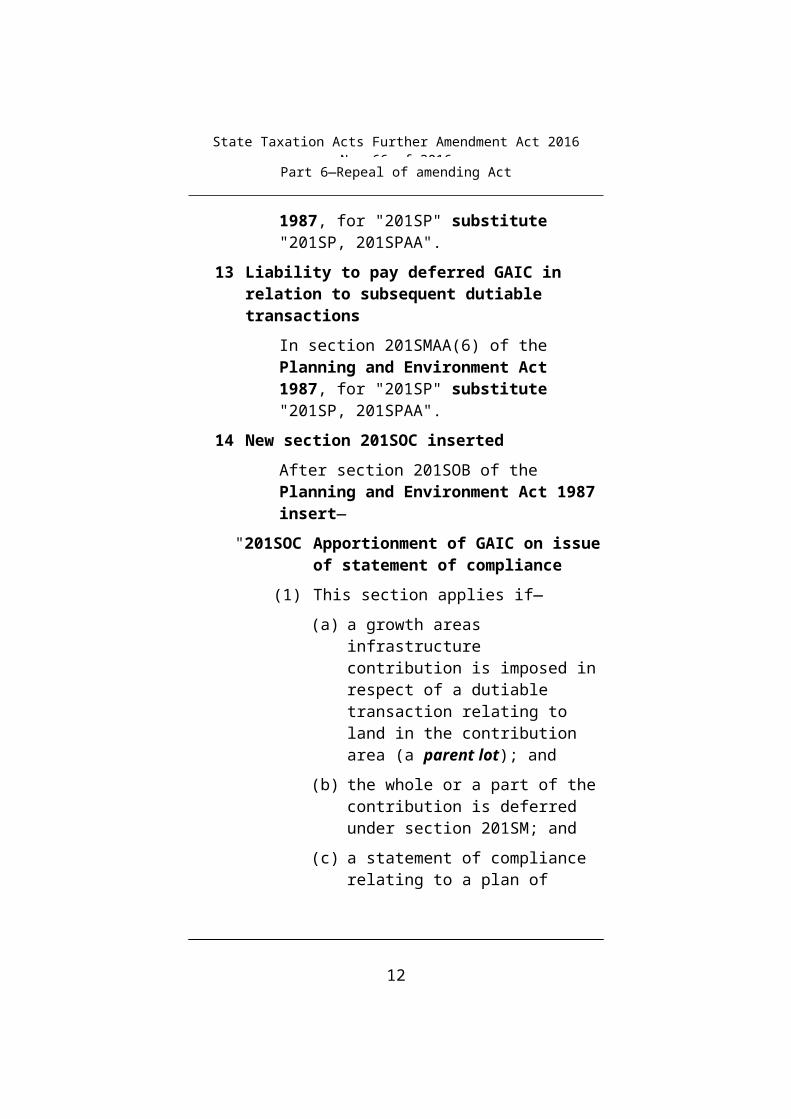

In section 201SL(1) and (2) of the Planning and Environment Act 1987, for "201SP" substitute "201SP, 201SPAA".

13 Liability to pay deferred GAIC in relation to subsequent dutiable transactions

In section 201SMAA(6) of the Planning and Environment Act 1987, for "201SP" substitute "201SP, 201SPAA".

14 New section 201SOC inserted

After section 201SOB of the Planning and Environment Act 1987 insert—

"201SOC Apportionment of GAIC on issue of statement of compliance

(1) This section applies if—

(a) a growth areas infrastructure contribution is imposed in respect of a dutiable transaction relating to land in the contribution area (a parent lot); and

(b) the whole or a part of the contribution is deferred under section 201SM; and

Part 6—Repeal of amending Act

State Taxation Acts Further Amendment Act 2016No. 66 of 2016

8

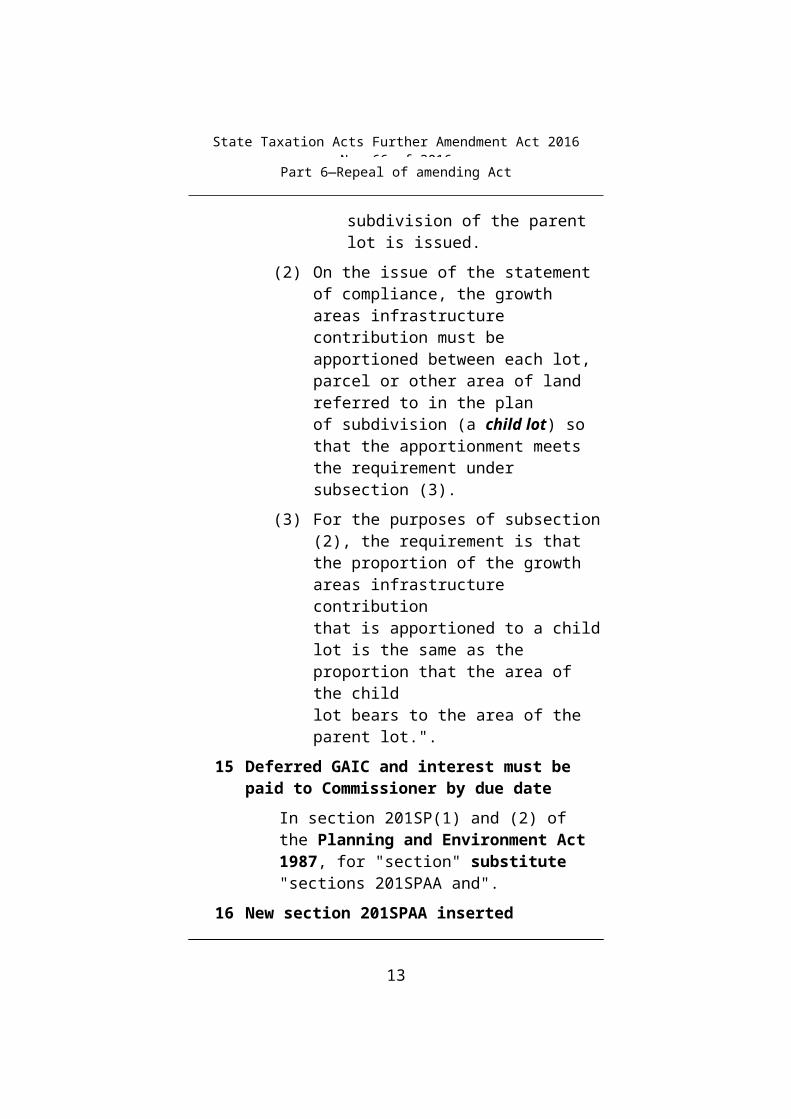

(c) a statement of compliance relating to a plan of subdivision of the parent lot is issued.

(2) On the issue of the statement of compliance, the growth areas infrastructure contribution must be apportioned between each lot, parcel or other area of land referred to in the plan of subdivision (a child lot) so that the apportionment meets the requirement under subsection (3).

(3) For the purposes of subsection (2), the requirement is that the proportion of the growth areas infrastructure contribution that is apportioned to a child lot is the same as the proportion that the area of the child lot bears to the area of the parent lot.".

15 Deferred GAIC and interest must be paid to Commissioner by due date

In section 201SP(1) and (2) of the Planning and Environment Act 1987, for "section" substitute "sections 201SPAA and".

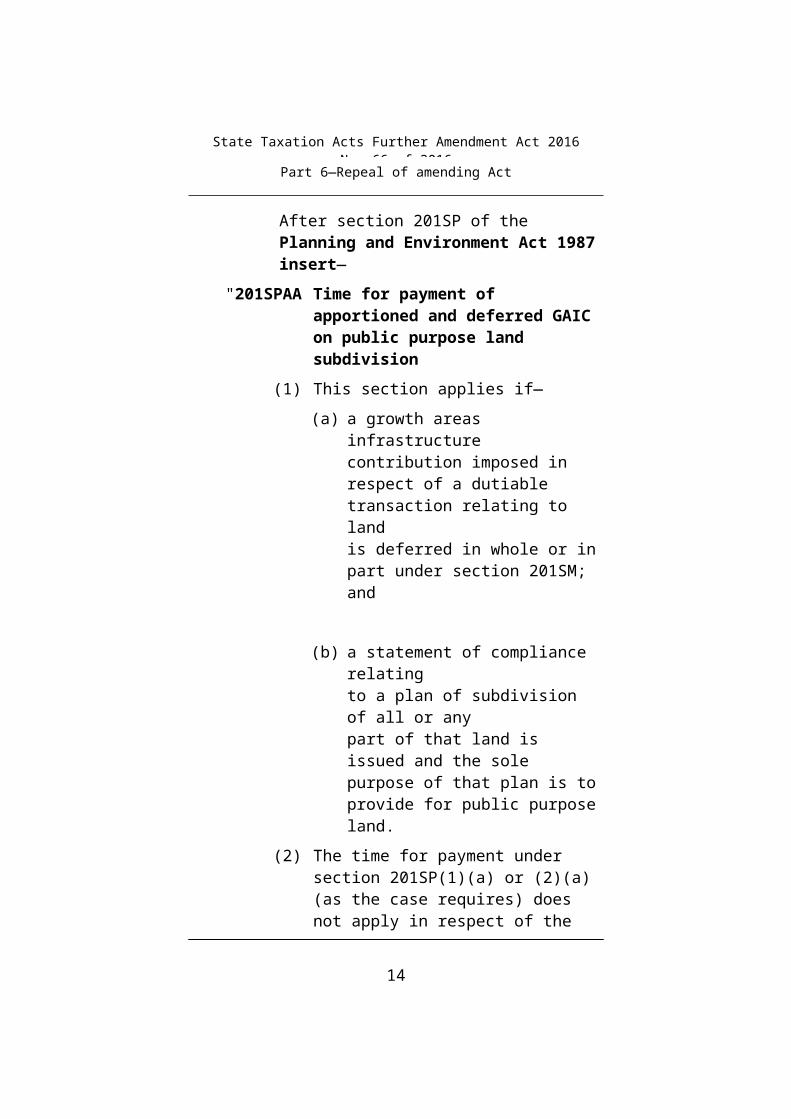

16 New section 201SPAA inserted

After section 201SP of the Planning and Environment Act 1987 insert—

"201SPAA Time for payment of apportioned and deferred GAIC on public purpose land subdivision

(1) This section applies if—

(a) a growth areas infrastructure contribution imposed in respect of a dutiable transaction relating to land is deferred in whole or in part under section 201SM; and

Part 6—Repeal of amending Act

State Taxation Acts Further Amendment Act 2016No. 66 of 2016

9

(b) a statement of compliance relating to a plan of subdivision of all or any part of that land is issued and the sole purpose of that plan is to provide for public purpose land.

(2) The time for payment under section 201SP(1)(a) or (2)(a) (as the case requires) does not apply in respect of the whole or part of the growth areas infrastructure contribution deferred under section 201SM.

(3) In addition—

(a) the proportion of the growth areas infrastructure contribution that is apportioned under section 201SOC to public purpose land (a PPL proportion) must be paid within 3 months after the day on which the statement of compliance is issued; and

(b) the proportion of the growth areas infrastructure contribution that is apportioned under section 201SOC to any part of the land that is not public purpose land continues to be a deferred contribution (a deferred proportion).

(4) For the purposes of subsection (3)—

(a) a reference in this Subdivision (other than section 201SM or 201SP) to a growth areas infrastructure contribution that is deferred in whole or in part under section 201SM includes a reference to a PPL proportion; and

Part 6—Repeal of amending Act

State Taxation Acts Further Amendment Act 2016No. 66 of 2016

10

(b) a reference in this Subdivision (other than section 201SM) to a growth areas infrastructure contribution that is deferred in whole or in part under section 201SM includes a reference to a deferred proportion.

Example

ABC Pty Ltd purchases 15 hectares of land in the contribution area in June 2017. The dutiable transaction in relation to the land is the first GAIC event in relation to the land and a GAIC is imposed. ABC Pty Ltd is liable to pay the GAIC and elects under section 201SM to defer 100% of the amount payable. In December 2017, ABC Pty Ltd applies to subdivide the land for the sole purpose of providing 1·5 hectares of land for the construction of a road. On the issue of the statement of compliance relating to the plan of subdivision of land, the GAIC is apportioned between the two child lots based on the area of land each child lot bears to the parent lot. Accordingly, 10% of the GAIC is apportioned to the public purpose land (the PPL proportion). This amount, as indexed under section 201SMA, and any accrued interest on this amount is payable within 3 months after the date of the issue of the statement of compliance. The remaining 90% is apportioned to the balance land (the deferred proportion) and this amount continues to be deferred and subject to indexation and interest under section 201SMA until the amount becomes payable under this Subdivision.".

17 Default on payment of deferred GAIC

(1) In section 201SPA of the Planning and Environment Act 1987, after "201SP" insert "or 201SPAA".

(2) In the note at the foot of section 201SPA of the Planning and Environment Act 1987, after "201SP" insert "or 201SPAA".

18 Deferred GAIC becomes a charge on the land

In section 201SQ of the Planning and Environment Act 1987, after "201SP" insert "or 201SPAA".

Part 6—Repeal of amending Act

State Taxation Acts Further Amendment Act 2016No. 66 of 2016

11

19 Approval by Minister for staged payment of GAIC for subdivisions or building works

(1) In section 201SR(1) and (2) of the Planning and Environment Act 1987, for "A person" substitute "Subject to subsection (8), a person".

(2) After section 201SR(7) of the Planning and Environment Act 1987 insert—

"(8) If the sole purpose of a plan of subdivision of land to which a statement of compliance referred to in subsection (1)(a) or (2)(a) relates is to provide for public purpose land, a person cannot apply to the Minister for approval of the staged payment of the proportion of the growth areas infrastructure contribution that is apportioned under section 201SGA or 201SOC (as the case requires) to public purpose land.".

20 Certificate of partial release

At the end of section 201SZB of the Planning and Environment Act 1987 insert—

"(2) The Commissioner must issue to a person who is or may be liable to pay a PPL proportion within the meaning of section 201SPAA(3)(a) a certificate of partial release of that liability if—

(a) the person has applied in accordance with section 201SX; and

(b) the Commissioner is satisfied that the person has paid the PPL proportion,

any interest under Subdivision 3 relating to the PPL proportion and any applicable interest or penalty tax imposed under Part 5 of the Taxation Administration Act 1997.".

Part 6—Repeal of amending Act

State Taxation Acts Further Amendment Act 2016No. 66 of 2016

12

21 Notice to Registrar regarding registration of subdivision or transfer of land

After section 201SZG(1)(a) of the Planning and Environment Act 1987 insert—

"(ab) a certificate of partial release issued under section 201SZB(2);".

22 Commissioner to pay GAIC into Consolidated Fund

In section 201SZJ of the Planning and Environment Act 1987, for "201SP" substitute "201SP, 201SPAA".

23 Exemption from paying GAIC for land dealings involving public authorities and councils

Section 201TC(2) of the Planning and Environment Act 1987 is repealed.

24 New section 222 inserted

After section 221 of the Planning and Environment Act 1987 insert—

"222 Transitional provisions—State Taxation Acts Further Amendment Act 2016

(1) Part 9B, as in force immediately before the commencement day, applies in respect of a plan of subdivision of land that has been submitted for certification under the Subdivision Act 1988 before 12 October 2016 and for which a statement of compliance is issued on or after that date.

(2) Part 9B, as in force immediately before the commencement day, applies in respect of a plan of subdivision of land that has been submitted for certification under the Subdivision Act 1988 on or after 12 October 2016 but before the commencement day and for which a statement of compliance is issued before the commencement day.

Part 6—Repeal of amending Act

State Taxation Acts Further Amendment Act 2016No. 66 of 2016

13

(3) In this section—

commencement day means the day on which section 10 of the State Taxation Acts Further Amendment Act 2016 comes into operation.".

25 Statute law revision

In section 201SMAA(3) of the Planning and Environment Act 1987, for "extinguished;" substitute "extinguished.".

Part 6—Repeal of amending Act

State Taxation Acts Further Amendment Act 2016No. 66 of 2016

14

Part 5—Amendment of Valuation of Land Act 1960

26 Definitions

In section 2(1) of the Valuation of Land Act 1960, for the definition of general valuation substitute—

"general valuation means—

(a) a valuation of all the rateable land under Part II for which a rating authority is responsible—

(i) in the area of the rating authority; or

(ii) in any one or more subdivisions of an area of the rating authority; or

(b) a valuation of all the non-rateable leviable land under Part IIA for which a rating authority is responsible for valuing whether or not the land is in the area of the rating authority; or

(c) a valuation of all of the land described in paragraphs (a) and (b);".

27 Late nomination of valuation authority

(1) For section 13G(2) of the Valuation of Land Act 1960 substitute—

"(2) On the making of a nomination under subsection (1) within the time specified in subsection (3)(b) or the acceptance of a nomination by the valuer-general as provided under subsection (3A), the valuer-general has the power to cause—

Part 6—Repeal of amending Act

State Taxation Acts Further Amendment Act 2016No. 66 of 2016

15

(a) a valuation of all non-rateable leviable land in the municipal district of the council which has made the nomination; or

(b) a valuation in respect of non-rateable leviable land in respect of which the council has been directed to be the collection agency.".

(2) After section 13G(3) of the Valuation of Land Act 1960 insert—

"(3A) Despite subsection (3)(b), the valuer-general may accept a nomination from a collection agency to be the valuation authority after the day specified in that subsection if the valuer-general considers it appropriate to do so.".

(3) In section 13G(4) of the Valuation of Land Act 1960, after "subsection (1)" insert "that was made within the time specified in subsection (3)(b), or a nomination that was accepted as provided under subsection (3A),".

(4) In section 13G(5) of the Valuation of Land Act 1960, after "subsection (1)" insert "that was made within the time specified in subsection (3)(b), or a nomination that was accepted as provided under subsection (3A),".

28 Notice of valuation

After section 15(6)(b) of the Valuation of Land Act 1960 insert—

"(ba) show the AVPCC allocated to the land; and".

Part 6—Repeal of amending Act

State Taxation Acts Further Amendment Act 2016No. 66 of 2016

16

Part 6—Repeal of amending Act29 Repeal of amending Act

This Act is repealed on 1 July 2019.Note

The repeal of this Act does not affect the continuing operation of the amendments made by it (see section 15(1) of the Interpretation of Legislation Act 1984).

═══════════════

Part 6—Repeal of amending Act

State Taxation Acts Further Amendment Act 2016No. 66 of 2016

17

Endnotes1 General information

See www.legislation.vic.gov.au for Victorian Bills, Acts and current authorised versions of legislation and up-to-date legislative information.

Endnotes

State Taxation Acts Further Amendment Act 2016No. 66 of 2016

18

† Minister's second reading speech—

Legislative Assembly: 12 October 2016

Legislative Council: 8 November 2016

The long title for the Bill for this Act was "A Bill for an Act to amend the Land Tax Act 2005, the Payroll Tax Act 2007, the Planning and Environment Act 1987 and the Valuation of Land Act 1960 and for other purposes."

![Arnold and Commissioner of Taxation (Taxation) … and Commissioner of Taxation (Taxation) [2017] AATA 1318 PAGE 2 OF 26 CATCHWORDS TAXATION AND REVENUE – appeal …](https://img.pdfslide.net/doc/110x75/5af2c9387f8b9ac2469120bc/arnold-and-commissioner-of-taxation-taxation-and-commissioner-of-taxation.jpg)