Embed Size (px)

Citation preview

Step-By-Step Guide to

Raising Venture Capital

Step-By-Step Guide to Raising Venture Capital Page 2

Legal Notices

All rights reserved. No part of this publication may be reproduced in any form or by any means

graphic, electronic or mechanical including recording, photocopying or by any other information

storage or retrieval system, without the written consent of the publisher.

This publication is sold as an educational reference only. While all attempts have been made to

verify information provided in this publication, neither the author nor the Publisher assumes any

responsibility for errors, omissions or contrary interpretation of the subject matter herein.

This publication is not intended for use as a source of legal or accounting advice. The Publisher

wants to stress that the information contained herein may be subject to varying state and/or local

laws or regulations. All users are advised to retain competent counsel to determine what state

and/or local laws or regulations may apply to the user’s particular business.

The purchaser or reader of this publication assumes responsibility for the use of these materials

and information. The author and Publisher assume no responsibility or liability whatsoever on

the behalf of any purchaser or reader of these materials. We expressly do not guarantee any

results you may or may not get as a result of following our recommendations.

Step-By-Step Guide to Raising Venture Capital Page 3

Table of Contents

Getting Started: Venture Capital 101.............................................. 5

Introduction.............................................................................................................................. 5

What is Venture Capital? ........................................................................................................ 5

The Difference Between Equity & Debt Capital ...................................................................... 6

The Pros & Cons of Equity Capital.......................................................................................... 8

The 5 Key Stages of Equity Investments ................................................................................ 9

The Difference Between Venture Capitalists and Angel Investors ....................................... 13

The Value that Venture Capitalists Offer............................................................................... 14

Strategic/Corporate Investors ............................................................................................... 14

Private Equity Firms .............................................................................................................. 15

Giving Up Equity in Your Company....................................................................................... 17

What Do Venture Capitalists Want?............................................. 19

How Venture Capital Firms Make Money.............................................................................. 19

Types of Companies That Venture Capital Firms Finance ................................................... 20

Market Sectors Where Venture Capital Firms Focus............................................................ 21

How Venture Capitalists Assess Companies ........................................................................ 22

Creating Your Venture Capital Marketing and Presentation

Materials......................................................................................... 23

The Presentation Materials You Need to Raise Venture Capital.......................................... 23

The High Concept Pitch ........................................................................................................ 23

The Elevator Pitch ................................................................................................................. 24

The Teaser Email .................................................................................................................. 25

The Business Plan ................................................................................................................ 28

Operations Plan/Risk Factors ............................................................................................... 31

The Executive Summary ....................................................................................................... 33

The Investor Slide Presentation ............................................................................................ 35

Identifying the Right Venture Capitalists..................................... 37

Factors to Consider when Seeking a Venture Capital Firm.................................................. 37

How to Create Your List of Potential Venture Capital Firms................................................. 39

Identifying the Right Partner at a Venture Capital Firm ........................................................ 40

Lead Investors vs. Syndicates/Co-Investors ......................................................................... 41

Step-By-Step Guide to Raising Venture Capital Page 4

Contacting Venture Capitalists..................................................... 43

The Three Ways to Contact Venture Capitalists................................................................... 43

1. Getting Introductions ......................................................................................................... 43

2. Meeting Venture Capitalists Online or Offline ................................................................... 47

3. Contacting Venture Capitalists Cold ................................................................................. 48

What Materials to Send – And in What Order....................................................................... 49

Meeting with Venture Capitalists.................................................. 52

Introduction............................................................................................................................ 52

Structure of Your VC Presentation........................................................................................ 53

What Not To Say in Your Presentation ................................................................................. 53

How to Properly Answer Common VC Questions................................................................. 55

How to Tell if a VC is Interested (or Not)............................................................................... 58

Post-Meeting Follow-Up Tips to Raise Venture Capital........................................................ 58

Legal & Negotiating Issues........................................................... 60

The Preferred Type of Incorporation ..................................................................................... 60

The Term Sheet's Role in Raising Venture Capital............................................................... 60

Legal Assistance: Do You Really Need a Lawyer for This?.................................................. 61

Key Venture Capital Negotiating Issues................................................................................ 62

Understanding Pre-Money vs. Post-Money Valuation .......................................................... 66

How to Maximize Your Valuation & Better Negotiate Terms ................................................ 67

Before You Sign a Term Sheet, Minimize Your Risk ............................................................ 68

The Importance of Understanding Liquidation Preference ................................................... 69

Preparing for Due Diligence .................................................................................................. 71

How to Protect Your Business Ideas When Presenting to Venture Capitalists .................... 72

Additional Venture Capital FAQs ................................................. 75

Venture Capitalist Follow-Up Strategies ............................................................................... 75

Approaching Multiple Investors at Once ............................................................................... 75

Contacting Associates and Venture Partners ....................................................................... 76

How to Position Yourself to Raise Your NEXT Round of Capital ......................................... 76

Assembling Your Advisory Board.......................................................................................... 77

Missing Management Team Members.................................................................................. 77

How Long Does It Really Take to Raise Venture Capital ..................................................... 78

Re-Cap: Action Plan for Raising Venture Capital........................ 79

Step-By-Step Guide to Raising Venture Capital Page 5

Getting Started: Venture Capital 101

Introduction

This in-depth report provides you with a complete roadmap for raising venture

capital, including:

• How to develop compelling investor materials

• Proven strategies and tactics to identify the “right” venture capitalists for

you, contact them, and make an effective pitch

• Guidelines for negotiating with venture capitalists

• Advice for long-term post-funding business success

But first things first…

In order to successfully raise venture capital, you must be familiar with the

broader funding landscape and the terminology surrounding venture capital.

What is Venture Capital?

Venture capital, also abbreviated as “VC”, is a sub-set of private equity, and

refers to institutional investments in early-stage, high-potential growth

companies (like yours).

Private equity refers to investing in shares in privately-held companies, rather

than publicly-traded stocks.

Step-By-Step Guide to Raising Venture Capital Page 6

And in this context, institutional means that venture capitalists are NOT

investing their own money, like “angel” investors do. (More on angel investors

later…). Instead, they are investing money on behalf of institutions, such as

pension funds and university endowments (as well as the collective funds of some

very wealthy individuals).

A venture capital firm is an investment company that regularly makes venture

capital investments.

The size of the venture capital fund is the specific amount of money the

venture capital firm has raised (from pension funds, etc.). Successful venture

capital firms regularly raise new funds to invest in promising new companies.

A venture capitalist is an individual who works at a venture capital firm, who

makes such investments.

To get a sense of the amount of money that venture capitalists invest, VCs

invested $28.3 billion in 3,808 companies in 2008 according to data from the

National Venture Capital Association, PricewaterhouseCoopers and Thomson

Reuters. This implies an average funding amount of $7.4 million per financing

transaction.

The Difference Between Equity & Debt Capital

As explained above, venture capital is a type of private equity capital. And private

equity is one type of equity capital.

Let’s take a moment to understand what exactly equity capital is, and what effect

equity capital will have on your business, versus other options – like debt capital.

Step-By-Step Guide to Raising Venture Capital Page 7

Equity capital, unlike debt capital, is when someone or some company invests in

a company in return for shares or stock in that company. Venture capital is such

an equity investment.

This money does NOT need to be paid back to the investor.

Rather, the investor generally gets paid when there is a liquidity event, which is

the event through which the company “cashes out” such as being sold to another

company or having an initial public offering or “IPO.” Note that a liquidity event

is also known as an “exit.”

As you might imagine, equity capital is much riskier to investors than debt

capital. With debt capital, lenders (typically banks) will receive interest and

principal payments from the businesses they lend to, and earn perhaps 10% on

their money with a relatively low risk profile. That is, due to their review process,

the lenders feel that there is a high likelihood that the company will be able to

repay the loan.

Equity capital is very different since the likelihood of a liquidity event is relatively

low. However, when liquidity events do happen, investors can receive 10 times,

100 times or even 1,000+ times their money back.

In one extreme example, the earliest equity investor made a 15,000X return on

his investment when he decided to make an early bet on Google. (More on that

story later – it’s a great one).

Note that with equity investments, investors also believe that there is a strong

likelihood that their investments will succeed, but they do understand that there

is more risk involved than with most debt investments.

Step-By-Step Guide to Raising Venture Capital Page 8

The Pros & Cons of Equity Capital

The key negative with equity capital is that you, the entrepreneur, generally need

to qualify by proving that your venture can grow quickly and be acquired (or have

an initial public offering) so that the investor can earn a return.

In addition, like everything else in business, real work is required to gain equity

capital. You need to create a strong business plan and know how to find and

present it to the right investors (all of which this report explains in detail). On the

other hand, finding a bank to give you a loan is much easier.

The other key negative is that equity investors, such as venture capitalists, take a

piece of your company, so that if you do eventually “exit” the company (through

an IPO, sale, etc.) you have to share the proceeds.

This may seem scary at first – but relax…

In our experience, a small piece of a big company is better than a large piece of a

small company. For example, a 10% piece of a $10 million company is twice as

valuable as 100% piece of a $500,000 company. This argument holds true if the

equity investor's money and advice can help you create the larger entity.

With their stake in your company, equity investors may often exert control,

particularly if they control the majority of the shares of your company. At the

least, they will probably take a seat on your Board of Directors. Generally,

however, these investors have the same goals as you -- to grow a successful

business and exit -- and thus, their control and advice does NOT harm your

company.

On the other hand, there are many key positives to equity capital. Many equity

investors have “deep pockets,” that is, they can offer significant dollars to help

Step-By-Step Guide to Raising Venture Capital Page 9

grow your business. In addition, most equity investors offer strategic assistance

and connections to help grow your business.

Also, equity investments are more accessible to early-stage companies than bank

loans which often require a multi-year operating history.

Finally, equity investments do not include periodic principal and interest

payments which allows you to focus more on growing your business and less on

short-term cash flow needs.

The 5 Key Stages of Equity Investments

To understand where venture capital fits in, it is important to understand the five

main sources of equity capital:

1. Friends and Family

2. Angel Investors

3. Venture Capital

4. Strategic/Corporate Investors

5. Private Equity Firms

For equity investments, the source of capital is, for the most part, tied to the

round of capital being raised. Read below to learn more.

Equity capital is raised in stages or rounds. The five main stages include the

following:

1. Pre-Seed Funding

2. Seed Funding

3. Early Stage Investment (Series A & B)

4. Later Stage Investment (Series C, D, etc.)

5. Mezzanine Financing

Step-By-Step Guide to Raising Venture Capital Page 10

Most companies that raise equity capital that are eventually acquired or go public

receive multiple rounds of financing. It is important to consider this when

negotiating deal terms on earlier stage financing rounds. That is, you don’t want

to include terms in early-stage financing agreements that limit your ability to

raise future rounds of capital.

Here are the five main stages of equity capital, in more detail:

1. Pre-Seed Funding

Pre-seed funding refers to the initial capital that a company brings in that comes

from friends and family members.

This round of financing typically can be as small as $5,000 and as high as $100K.

Not all companies raise a pre-seed round.

With this funding, the company often perfects its business plan and starts

building its management team in order to position itself for its next round of

funding. (Note that companies do not necessarily have to raise pre-seed or seed

funding in order to raise venture capital.)

2. Seed Funding

Seed funding or seed capital refers to the capital that a company brings in before

the first institutional round of funding (e.g., capital invested by a company or

institution such as a venture capital firm).

Seed funding typically ranges from $100K to $500K and is generated by angel

investors and even the rare early stage venture capital firm. In addition,

sometimes debt capital, like SBA loans and traditional bank loans, are used as a

Step-By-Step Guide to Raising Venture Capital Page 11

company’s seed funding -- yes, oftentimes companies raise both debt capital and

equity capital.

Seed investments are typically structured as convertible notes or common stock.

Convertible notes are loans which are made to a company at a fixed rate of

interest which can either be redeemed for cash (like traditional debt capital) OR

can be converted into stock (equity) at a predetermined date, usually upon the

next round of financing, or within a certain time period.

A key benefit of convertible notes is that you don’t need to negotiate valuation

since the valuation is tied to your Series A financing.

3. Early Stage Investment (Series A & B)

Series A is the term used to describe the first round of institutional funding for a

venture. The name “Series A” is derived from the class of preferred stock

investors receive in return for their capital.

The average Series A round is between $2 million and $5 million, with the

expressed goals of funding early stage business operations. Providing enough

capital for 6 months to 2 years of operations, funds obtained from the Series A

round can be used for the full gamut of needs -- from product development and

marketing to employee salaries.

Series B is the round that follows Series A in early stage financing. These rounds

generally raise $5 million to $10 million, but can sometimes generate up to $20

million in capital or more.

Series A and Series B rounds are usually obtained from venture capital firms

and/or strategic/corporate investors (more on strategic/corporate investors

later), and are best pursued once your company has completed its initial

Step-By-Step Guide to Raising Venture Capital Page 12

products, shows initial revenue, and/or demonstrates compelling growth (such as

fast and steadily increasing member growth).

To get from Series A to Series B, the primary challenge for your company is to

demonstrate market adoption of your venture (i.e., that customers really want to

buy your product or service).

Key point: If your company doesn't resonate with its target market or

demographic, you will have serious difficulty attracting additional funding.

4. Later Stage Investment (Series C, D, etc.)

Series C, D, etc. (some venture backed companies raise over 10 rounds of

financing) are further rounds of venture capital. Each round may raise between

$5 million and $20 million or more. This type of financing is provided to

companies that have demonstrated a high level of success, are approaching or

have reached a financial “break-even” point, and are looking to expand even

further.

Series C, D, etc. rounds are usually obtained from venture capital firms and/or

strategic/corporate investors.

5. Mezzanine Financing

Mezzanine capital is capital – provided either as equity, debt or a convertible note

– that is provided to a company just prior to its IPO.

Mezzanine investors generally take less risk, since the company is generally solid

and poised to “cash out” relatively quickly. However there is still some risk since

Step-By-Step Guide to Raising Venture Capital Page 13

sometimes companies cancel their IPOs, the valuation at the IPO event is lower

than anticipated, and/or the company loses value after its IPO.

Note that investors in pre-IPO companies often have to endure a “lock-up period”

which is the period of time after the IPO (often a year) in which they cannot sell

their shares of the public company.

Mezzanine capital is often provided by private equity firms.

The Difference Between Venture Capitalists and Angel Investors

As the previous section pointed out, venture capitalists differ from angel

investors in that they typically provide more money (generally at least $2 million)

and focus on companies that have achieved more operational milestones than

companies generally funded by angel investors.

Other key differences include the following:

• Professional vs. non-professional investors: Venture capitalists are

professional investors. That is what they do for a living. Angel investors do

not invest for a living. They often have other jobs or commitments to

attend to.

• Other people’s money vs. own money: Venture capitalists invest

other people’s money in ventures. This money comes from pension funds,

corporations and other sources. Conversely, angels invest their own

money. As a result, angel investments are not always based on the

potential return on investment (ROI) of the deal (the primary concern of

venture capitalists) but may result from other factors such as simply liking

the entrepreneur and wanting to help them out.

Step-By-Step Guide to Raising Venture Capital Page 14

• Board seat vs. no board seat: Angel investors may or may not want a

seat on the company’s Board of Directors. For venture capitalists, taking a

Board seat is the norm.

The Value that Venture Capitalists Offer

Venture capitalists often provide value beyond the actual dollars they invest in

your company. Venture capitalists often provide additional value via:

• Contacts that they have in their networks that can help your business

• Advice in running your business, based on deep experience in your

industry and in successfully growing ventures

• Contacts to additional sources of capital

Many VC firms are made up of entrepreneurs who have launched and grown their

own successful businesses. As such, they are often able to provide significant

strategic guidance and connections that can help your business grow.

Strategic/Corporate Investors

In addition to venture capital firms, venture capital is also disbursed by

“strategic” or “corporate” investors.

Strategic investors are generally corporations that invest in early stage companies

in order to 1) earn financial returns and 2) partially control ventures that could

effect or “disrupt”, that is cause a significant change to, their market(s) in the

future.

Step-By-Step Guide to Raising Venture Capital Page 15

Strategic investors can offer capital in amounts ranging from a few hundred

thousand dollars or less to several million dollars.

Some corporations, like Intel (via Intel Capital) and Siemens (via Siemens

Venture Capital), have formal venture capital arms that actively seek and invest

in emerging companies.

These corporations are often the ideal investors to contact should you have a

venture in their market space(s), since if they like your concept they could

provide value well beyond their capital contributions such as strategic advice,

industry connections, and distribution assistance.

Note that most corporations, even if they don't have formal venture capital arms,

do fund emerging ventures if they are properly presented to them. This is

specifically the case if the venture's management team clearly shows how their

venture could impact the industry and/or help the corporation further its

mission.

For example, if you have a product or technology that enables a corporation to

gain competitive advantage and thus increase profits, they might be extremely

receptive to providing funding. Most major U.S. corporations have provided

venture capital financing to emerging ventures.

Private Equity Firms

As the name implies, private equity (PE) is the process of investing in private

companies (those that are not listed on a public exchange) in return for shares of

those companies.

There are several subsets of private equity including:

Step-By-Step Guide to Raising Venture Capital Page 16

1. Venture capital, which focuses on investing in privately-held, young, fast

growing companies

2. Buyout investing

3. Recapitalizations

4. Mezzanine investing

While venture capital is technically a subset of private equity, it is generally

treated separately and the term “private equity” is generally thought of as buyout

and mezzanine investing, both of which focus on investments in mature

companies.

Private equity deal sizes are generally very large. While some deal range in the

millions of dollars, private equity deals often reach hundreds of millions if not

billions of dollars.

For example, private equity firm Cerberus Capital Management owns or has

financing stakes in massive firms including Chrysler, GMAC Financial Services

and Spyglass Entertainment.

From a risk/return perspective, private equity generally falls in between debt

capital, which is low risk/low return, and venture capital, which is high risk/high

return investing.

Private equity is generally not appropriate for early stage companies. However, it

is never to early to meet with private equity firms as they may introduce you to

earlier stage investors, and also track your performance so as to potentially

provide funding to your company in the future.

Step-By-Step Guide to Raising Venture Capital Page 17

Giving Up Equity in Your Company

Many entrepreneurs and business owners who seek venture capital or other

equity investments have concerns about giving up too much equity and/or losing

control of their companies.

You must understand, on some level, that raising capital is very important to your

business. Otherwise, you wouldn’t have purchased this report. But let me pause

for a moment at this point to explain exactly how important raising capital is to

the success of your business.

Raising capital is the MOST important thing to your business. In fact, running

out of capital is the reason why most businesses fail. And with capital, your

business gains massive competitive advantages such as:

• The ability to hire better personnel

• Access to better equipment and technology

• Access to better education and training

• The ability to get to and more quickly penetrate markets

• More inventory to serve customers faster

• The ability to plan and execute long-term. For example, how many more

lifetime customers might you be able to get if you offered products to first

time buyer at below cost.

• The ability to invest more in R&D

Having the appropriate funding is a KEY ingredient to success!

Even if you don't think you need capital, you probably do. Think about it, how

much could your business improve if you had more capital to invest in it? Or

Step-By-Step Guide to Raising Venture Capital Page 18

think about it the other way -- how bad would it be for you if your competitors

gained access to lots of capital and started an assault on you?

Now, in terms of giving up equity to investors, consider this important yet simple

mathematical fact: 100% of nothing is nothing.

And without the capital, your company may be worth nothing. As we explained

earlier, a small piece of a big company is better than a large piece of a small

company. For example, a 10% piece of a successful company (perhaps a $10

million company) is twice as great as 100% piece of a small company, perhaps a

$500,000 business. Plus, as mentioned, venture capital investors provide value

beyond the capital they provide, further improving your chances of success.

Yes, you don't want a venture capitalist to take the vast majority of your company

from you. But note that any savvy VC WON'T do this. They know that the

entrepreneur is only going to perform at his peak if he has a major carrot (with

the carrot being a big payday if the company succeeds). As such, the savvy

venture capitalist WANTS the entrepreneur to maintain a meaningful equity

piece.

Likewise, the savvy venture capitalist will want the company to maintain an

employee stock option plan so that all key company personnel are motivated to

make the company a success.

So, in summary, the key is to focus on raising capital. Focus less on retaining the

highest equity position. If your company succeeds, you will still make a ton of

money. And, then, if you want, you will have enough capital and connections to

launch a future business where you retain most or all of the equity.

Step-By-Step Guide to Raising Venture Capital Page 19

What Do Venture Capitalists Want?

How Venture Capital Firms Make Money

To recap, a venture capital firm is a financial institution that focuses on providing

capital, in the form of equity, to companies who offer them the prospects of

significant growth.

The partners and associates at venture capital firms are known as venture

capitalists. The term “VC” or “VCs” applies to both venture capital firms and

venture capitalists.

Unlike angel investors, VCs are professional institutions that invest other people's

money. VC firms raise capital for their own funds from sources which primarily

include pension funds, financial and insurance companies, endowments and

foundations, individuals and families, and corporations.

The VCs are then charged with finding high growth companies, making

investments in them at favorable terms, guiding and nurturing them, and

enacting a liquidity event (e.g., selling the company or having it complete an

initial public offering).

Because they are utilizing other people's money, and are judged and compensated

by the performance of their investments, venture capitalists are extremely

rigorous in their investment decision-making process.

VCs tend to invest in companies with significant market potential of $50 million,

$100 million or more. This is because even with all their relevant experience, the

average venture capital firm will lose money on half the companies they invest in

and only break even on a third.

Step-By-Step Guide to Raising Venture Capital Page 20

Where VCs make their money is on the approximately 20% of

companies they invest in that see explosive growth and provide

remarkable returns of 10 times to 100 times or more on their

investment.

Specifically, it is important to note that relatively few venture capital investments

produce large gains. In fact, industry insiders sometimes refer to the 2:6:2 rule.

This rule is that an average portfolio of ten investments will include two losses

(e.g., companies go bankrupt), six moderately performing companies (may break-

even on the investment or lose a little) and two very successful returns.

In fact, an analysis by Bygrave and Timmons of VC funding between 1969 and

1985 found that just 6.8% of investments returned ten times or more on the

invested capital. Conversely over 60% of investments lost money or failed to

exceed the amount of money earned if the capital had been put in an interest-

bearing bank account.

The result of this analysis is that typically a venture capitalist will want to see the

ability to get 10X their money back or more from investing in your company. As

such, if you are seeking $1 million from VCs, you must show them a realistic

scenario where you can turn that $1 million into $10 million.

Types of Companies That Venture Capital Firms Finance

Most venture capital firms invest between $1 million and $25 million in the

companies they fund. The amount they provide often reflects the size of their

funds. For example a VC with a billion dollar fund cannot manage 1,000 one-

million dollar investments and thus tends to offer more capital to each company

it funds.

Step-By-Step Guide to Raising Venture Capital Page 21

Virtually all VC firms have specific criteria that guide them such as the amount of

financing they give to a company, the stage at which they like to invest, the

sectors they are interested in, and the geographic area in which they will invest.

Also, venture capital firms have very strict criteria regarding scale, speed and

liquidity potential. They want to fund companies that can grow very quickly,

achieve significant revenues, and be sold or go public for many times the

company's current valuation. Typically, venture capital firms like to exit an

investment within 5 to 7 years.

As a result, VCs tend to fund technology companies that typically have scale,

speed and exit potential. Remember, they are looking for companies with the

potential to turn every $1 million they invest into $10 million.

Market Sectors Where Venture Capital Firms Focus

Venture capitalists tend to invest in the following sectors:

• Biotechnology

• Business Products and Services

• Computers and Peripherals

• Consumer Products and Services

• Electronics/Instrumentation

• Financial Services

• Healthcare Services

• Industrial/Energy

• IT Services

• Media and Entertainment

• Medical Devices and Equipment

• Networking and Equipment

• Retailing/Distribution

• Semiconductors

• Software

• Telecommunications

Step-By-Step Guide to Raising Venture Capital Page 22

How Venture Capitalists Assess Companies

As mentioned, venture capitalists primarily look for companies that can grow

really fast with an infusion of capital.

The other key thing that VCs look for is a quality management team. In fact,

many VCs say they rather bet on the jockey (i.e., the management team) than the

horse (i.e., the company’s products and/or services).

With regards to the management team, VCs look for the following:

• Management teams who can really execute, which often includes:

o Management teams who have successfully worked together in the

past.

o Management teams who have succeeded in prior positions.

• Management teams who really know their business/market, which often

means:

o They are known as experts in their industry.

o They have been working in their industries for a long time and

know all the ins and outs.

• A good fit with the founder(s) and management team:

o Entrepreneurs and venture capitalists are partners. That

is, they generally work very closely together to achieve a common

goal (growing a successful company and getting to an exit). As such,

it is critical that there be a good personality fit and ability to work

together between the VC and the company’s founder/management

team.

Step-By-Step Guide to Raising Venture Capital Page 23

Creating Your Venture Capital Marketing and Presentation Materials

The Presentation Materials You Need to Raise Venture Capital

In order to raise venture capital, you need to develop the following presentation

materials:

1. High concept pitch (if possible)

2. Elevator pitch

3. Teaser email

4. Business Plan (including financial projections)

5. Executive Summary

6. Slide Presentation

The High Concept Pitch

I originally learned of the term "High Concept Pitch" from Babak Nivi, an

entrepreneur and investor who also runs VentureHacks.com. A high concept

pitch is a single sentence that distills your company's vision.

Hollywood has used and perfected the art of the high concept pitch. For instance,

the movie Aliens was promoted as "Jaws in space!" And some smart emerging

companies have also used high concept pitches. For example, Dogster promotes

itself as "Friendster for dogs" while Bookswim describes itself as "Netflix for

books."

So, why are high concept pitches so critical? First, they allow others (consumers,

investors (including venture capitalists) and the media) to instantly understand

what your company does. For example, if you know what Netflix does (DVD

Step-By-Step Guide to Raising Venture Capital Page 24

rentals via the mail), you can instantly understand that Bookswim offers book

rentals via the mail.

As a result, the high concept pitch is the perfect tool for consumers/fans who are

spreading the word about your company. Venture capitalists use the pitch when

they tell their partners about your company. And the press uses the pitch when

they cover your company (which also allows their readers to quickly understand

your company).

Secondly, high concept pitch offer some proof to potential VCs that the business

model makes sense. For example, a VC might think, “well Netflix has been really

successful, so the Netflix business model works; so applying that same model to

books also makes intuitive sense and should be successful.”

The Elevator Pitch

An elevator pitch is a little different than a high concept pitch.

Specifically, an elevator pitch is a brief description of a business idea. It is termed

as such since it usually must be delivered within the time that you spend with an

investor in an elevator, or just a minute or two. If possible, the elevator pitch

should start with high concept pitch, and then discuss other key characteristics of

the business.

Entrepreneurs should incorporate the following three characteristics in their

elevator pitches when seeking venture capital:

1. Offering a concise definition of the benefits of the company's products

and/or services. No one really cares about how good a widget is; rather they

care what the benefits of the widget are to them.

Step-By-Step Guide to Raising Venture Capital Page 25

2. Using examples of other companies. New companies, particularly those

offering new products or new ways of doing things, often have a difficult

time explaining what they do since they focus too much on details of how

they do what they do.

Rather than describe these details, companies should start by mentioning a

well-known company that the venture capitalist knows. They should then

explain the positive differences between the well-known company and their

organization. This allows the prospective VC to quickly grasp what the

company does, the benefits it offers, and its advantages over others. (Note

that this characteristic may be solved with the use of the high concept pitch.)

3. Stressing competitive differentiation. A new company exists to fulfill an

unmet need. That unmet need is the result of competitors not providing an

adequate product or service to customers. In their elevator pitch, companies

should stress how they differ from competitors and how this allows them to

fulfill the unmet needs. Similarly, companies can discuss similarities

between competitors, since rarely are competitors all bad.

Because VCs are time constrained, and particularly if you meet a VC at an event

you may only have a minute of their time, perfecting your elevator pitch can have

a significant impact on your success in raising venture capital.

The Teaser Email

“Teaser” emails are emails that “tease” the VC into wanting to learn more about

your company.

The teaser email typically includes 5 to 6 bullets about the venture and is very

short (200 words or less). The goal of the email is simply to create a general

interest in your venture so the VC commits time and energy to learning more

about it (by requesting additional documents or setting up a meeting).

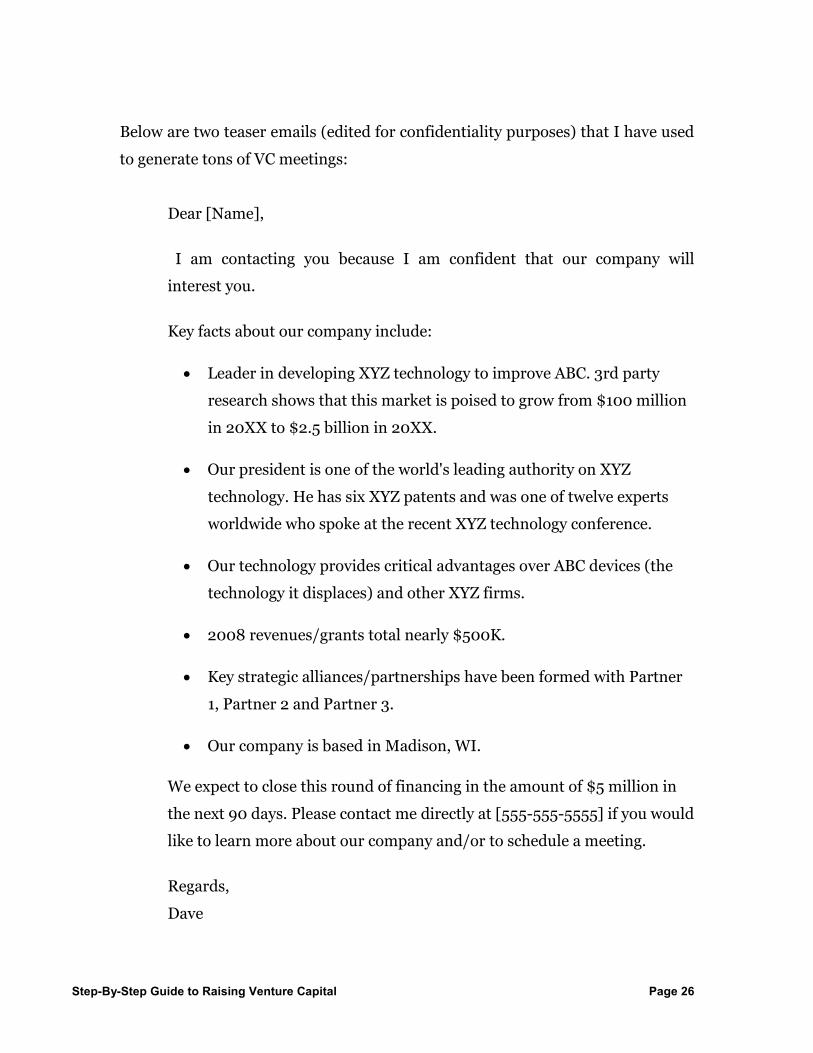

Step-By-Step Guide to Raising Venture Capital Page 26

Below are two teaser emails (edited for confidentiality purposes) that I have used

to generate tons of VC meetings:

Dear [Name],

I am contacting you because I am confident that our company will

interest you.

Key facts about our company include:

• Leader in developing XYZ technology to improve ABC. 3rd party

research shows that this market is poised to grow from $100 million

in 20XX to $2.5 billion in 20XX.

• Our president is one of the world's leading authority on XYZ

technology. He has six XYZ patents and was one of twelve experts

worldwide who spoke at the recent XYZ technology conference.

• Our technology provides critical advantages over ABC devices (the

technology it displaces) and other XYZ firms.

• 2008 revenues/grants total nearly $500K.

• Key strategic alliances/partnerships have been formed with Partner

1, Partner 2 and Partner 3.

• Our company is based in Madison, WI.

We expect to close this round of financing in the amount of $5 million in

the next 90 days. Please contact me directly at [555-555-5555] if you would

like to learn more about our company and/or to schedule a meeting.

Regards,

Dave

Step-By-Step Guide to Raising Venture Capital Page 27

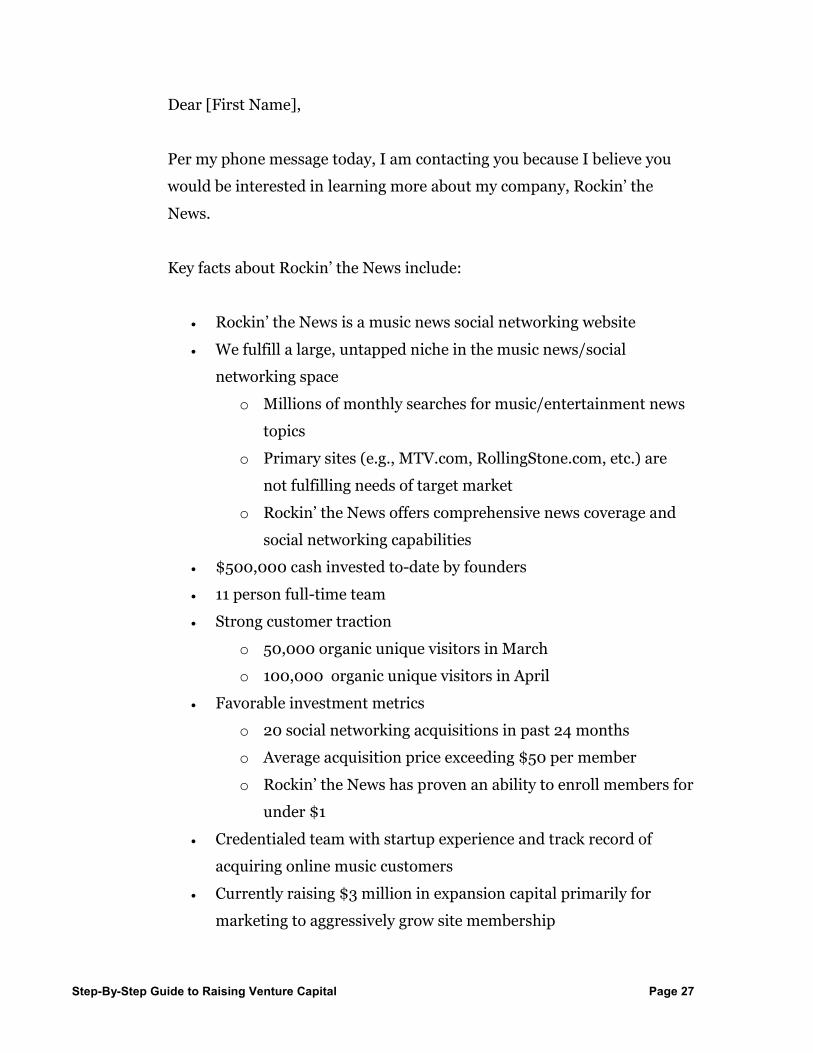

Dear [First Name],

Per my phone message today, I am contacting you because I believe you

would be interested in learning more about my company, Rockin’ the

News.

Key facts about Rockin’ the News include:

• Rockin’ the News is a music news social networking website

• We fulfill a large, untapped niche in the music news/social

networking space

o Millions of monthly searches for music/entertainment news

topics

o Primary sites (e.g., MTV.com, RollingStone.com, etc.) are

not fulfilling needs of target market

o Rockin’ the News offers comprehensive news coverage and

social networking capabilities

• $500,000 cash invested to-date by founders

• 11 person full-time team

• Strong customer traction

o 50,000 organic unique visitors in March

o 100,000 organic unique visitors in April

• Favorable investment metrics

o 20 social networking acquisitions in past 24 months

o Average acquisition price exceeding $50 per member

o Rockin’ the News has proven an ability to enroll members for

under $1

• Credentialed team with startup experience and track record of

acquiring online music customers

• Currently raising $3 million in expansion capital primarily for

marketing to aggressively grow site membership

Step-By-Step Guide to Raising Venture Capital Page 28

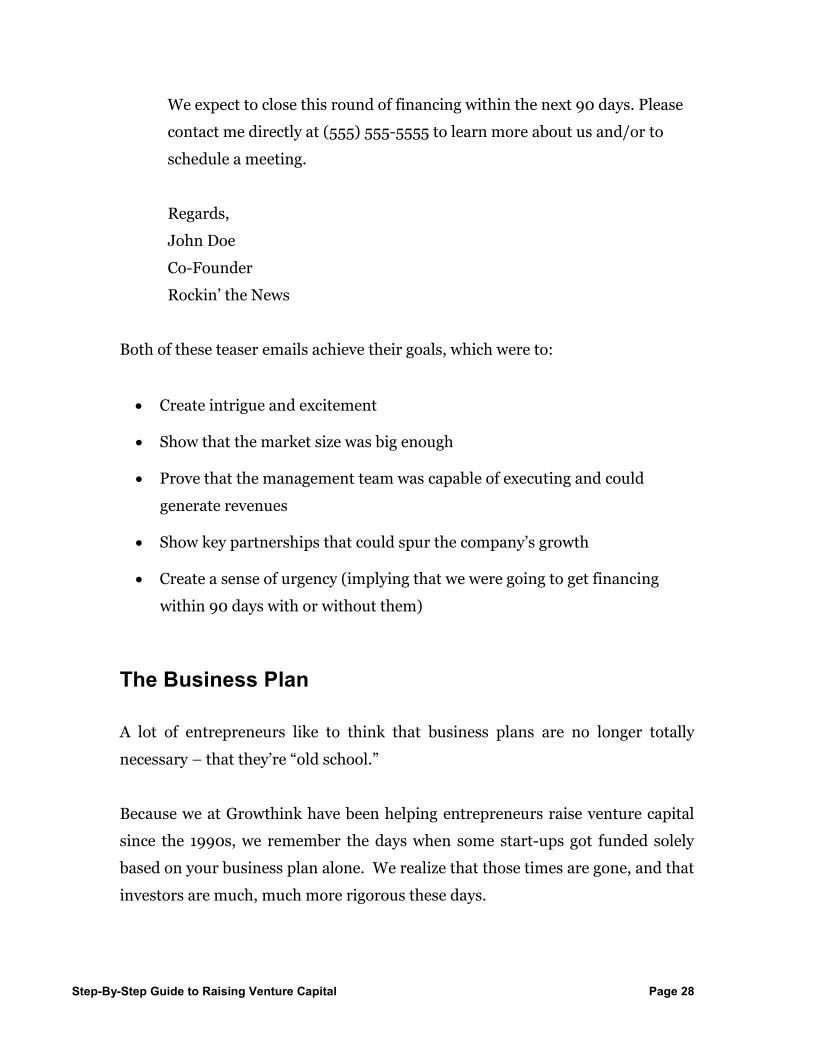

We expect to close this round of financing within the next 90 days. Please

contact me directly at (555) 555-5555 to learn more about us and/or to

schedule a meeting.

Regards,

John Doe

Co-Founder

Rockin’ the News

Both of these teaser emails achieve their goals, which were to:

• Create intrigue and excitement

• Show that the market size was big enough

• Prove that the management team was capable of executing and could

generate revenues

• Show key partnerships that could spur the company’s growth

• Create a sense of urgency (implying that we were going to get financing

within 90 days with or without them)

The Business Plan

A lot of entrepreneurs like to think that business plans are no longer totally

necessary – that they’re “old school.”

Because we at Growthink have been helping entrepreneurs raise venture capital

since the 1990s, we remember the days when some start-ups got funded solely

based on your business plan alone. We realize that those times are gone, and that

investors are much, much more rigorous these days.

Step-By-Step Guide to Raising Venture Capital Page 29

It’s also true that your business plan usually is NOT the first communication you

have with an investor. You shouldn’t just send your business plan around to

venture capitalists left and right. Instead, at the beginning of your dialogue with

a VC, you’re much better off sending a PowerPoint or an Executive Summary

rather than the whole business plan, unless the investor specifically requests to

see your business plan.

Nevertheless, business plans are the vehicle by which companies are scrutinized

by venture capitalists. It is critical that your company develop a strong business

plan if you seek financing from venture capitalists.

In other words, the more work you put into your business plan, the more

compelling you can make it; and the sounder its assumptions are, the better your

overall chances are for raising venture capital.

Let’s say you have a really well designed PowerPoint but you haven’t really done

your business planning homework. It’ll show. You’ll fall apart when venture

capitalists dig in with their tough questions when you meet in their office or

during the due diligence phase. They’ll begin to lose confidence in you and you

won’t get funded.

While a business plan may be “old school” in some respects, we strongly

recommend that you take the entire business planning process very seriously.

Your business plan is your strategic road map, helping to guide you as you build

your company. But it’s also a marketing document that still plays a very

important role in the capital raising process.

If you haven’t done so already, we recommend that you organize your business

plan into ten key sections as follows:

1. Executive Summary

2. Company Analysis

Step-By-Step Guide to Raising Venture Capital Page 30

3. Industry Analysis

4. Customer Analysis

5. Competitive Analysis

6. Marketing Plan

7. Operations Plan

8. Management Team

9. Financial Plan

10. Appendix

Next, to establish credibility with venture capitalists, it is critical that your

business plan avoids overestimating market sizes, underestimating competition,

or projecting results over-aggressively.

Instead, you must present a realistic game plan for achieving success.

The following are keys to a successful business plan:

• Highlighting past accomplishments: The best indicator of future success is

a company's past track record. The business plans of previously funded

companies must show what milestones they have achieved with those

funds. Your business plan must show how the past successes of your

management team will enable your company to overcome expected

challenges.

• Understanding and defining the “relevant market”: Improper sizing of a

company's target market is a telltale sign of a poorly reasoned business

plan. For example, although the U.S. healthcare market is a trillion dollar

market, there is no company that could reap $1 trillion in healthcare sales.

Rather, a more meaningful metric is the relevant market size, which equals

the company's sales if it were to capture 100% of its specific niche of the

market. Defining and communicating a credible relevant market size is far

more powerful than presenting generic industry figures.

Step-By-Step Guide to Raising Venture Capital Page 31

• Understanding and catering to customer needs: Investors have a laser

sharp focus on the relationship between a company and its customers. In

your business plan, you must clearly communicate how your products and

services meet specific customers' wants and needs – and then go further to

identify which target markets most exemplify these needs. Your business

plan must also outline an easy-to-follow and credible roadmap of how your

company plans to penetrate its customers.

• Proving barriers to entry: Your business plan must include strategies that

demonstrate that your company can and will build long-term barriers

around its customers. Claiming a “first mover advantage” is not enough.

• Developing realistic financial assumptions: You need to realize that many

investors skip straight to the financial section of your business plan.

Therefore, it is critical that the assumptions and projections in this section

be realistic. If your plan shows penetration, operating margin and revenues

per employee figures that are poorly reasoned, internally inconsistent or

simply unrealistic, this will seriously damage the credibility of your entire

business plan. In contrast, sober, well-reasoned financial assumptions and

projections communicate operational maturity and credibility.

Operations Plan/Risk Factors

While your Operations Plan is part of your business plan, the following is a

critical point which deserves its own section in this report.

Venture capitalists are essentially risk managers. They assess tons of business

plans and then invest in a portfolio of these companies knowing that several will

fail, but hopefully some will succeed big. So, they are constantly seeking to

minimize their risk by diversifying.

Step-By-Step Guide to Raising Venture Capital Page 32

They also seek to minimize risk within each company they invest in. Obviously a

company with existing customers and revenues is less risky than a company that

hasn’t even developed a prototype. However, the latter company may offer a

better return on investment (ROI) to the VC.

But, that pre-prototype company must prove to the VC that it will eventually

become a company with existing customers and significant revenues.

One of the best ways to prove this to VCs is for your company to create an

operations plan/milestone chart that identifies each key risk factor in your

business and when you expect to overcome that risk factor.

The following are sample risk factors:

• Prototype design

• Prototype development/working prototype

• Beta testing

• Product finalization

• Customer adoption/sales

• Partnerships secured

• Key management team members hired

• Revenues reach $X

So, it is critical for you to:

1. Map out your business’ risk factors

2. Create dates when you expect to accomplish each (and thus remove them

as risk factors)

3. Identify where your business currently is within the list of risk factors

A few more key thoughts regarding the importance of laying out your business’

risk factors:

Step-By-Step Guide to Raising Venture Capital Page 33

1. Addressing risk factors is a good sales technique. Master sales people

preach the need to proactively address customer objections in closing

sales. VCs are generally very smart; it’s not like they don’t realize the risk

factors in your business. By presenting the risk factors and then

addressing how you will overcome them, you are in a better position to

raise venture capital.

2. Figuring out where your company currently is on your risk factor chart will

help you find the right VC firm. As you will learn later, venture capitalists

often focus their investments by stage of development. So, the right

venture capital firm is often highly related to the number of risk factors

you have already overcome.

3. VCs like to take their time when investing. For instance, it’s not

uncommon for a VC to take 6 months from the time they meet an

entrepreneur until the time they write that entrepreneur a check.

Importantly, during that time period, the VC does not want to see the

entrepreneur/management team sitting idle. They want to see the team

accomplishing milestones and eliminating risk factors.

In fact, oftentimes, a VC will say they will invest once the team achieves

their next milestone/risk factor. Your ability to accomplish that milestone

mitigates the VC’s risk and proves the execution abilities of you and your

management team.

The Executive Summary

The next VC presentation material which you need is an Executive Summary. An

Executive Summary is a brief summary of your business plan that highlights the

Step-By-Step Guide to Raising Venture Capital Page 34

key factors that VCs need to know in order to determine if your company might

be a fit for them.

The Executive Summary is typically 1-3 pages in length and precedes the full

business plan. However, many VCs like to initially read just the Executive

Summary. As such, it should be prepared as a stand-alone document.

Your Executive Summary must included the following critical elements:

1. A concise explanation of your business

2. A description of the market size and market need for your business

3. A discussion of how your company is uniquely qualified to fulfill this need

• Virtually all Executive Summaries should include these seven words -

“We are uniquely qualified to succeed because” – followed by

supporting reasons.

In addition, your Executive Summary should often include summaries of each

essential elements of the business plan. This includes paragraphs addressing each

of the following:

• Customer Analysis: What specific customer segments the company is

targeting and their demographic profiles.

• Competition: Who the company's direct competitors are and the

company's key competitive advantages.

• Marketing Plan: How the company will effectively penetrate its target

market.

• Financial Plan: A summary of the financial projections of the

company, including how much capital you seek and your expected

P&L results.

• Management Team: Biographies of key management team and Board

members.

Step-By-Step Guide to Raising Venture Capital Page 35

Your Executive Summary is critically important. If it does not grab the investor's

attention, the investor will neither read nor request the full business plan. Nor

will they request a meeting. As such, spend time developing the best possible

Executive Summary.

The Investor Slide Presentation

The final piece of the presentation materials you need to raise venture capital is

your slide presentation, which is typically developed using Microsoft

PowerPoint®.

A well-crafted PowerPoint presentation will contain the highlights of your

business and financial plans, and should echo the clarity that is put forth in your

Executive Summary.

Specifically, your PowerPoint presentation should include answers to the

following TEN questions:

1. What does your company do?

o Answer this in 1 line

2. What is the status of your company?

o Age of venture, previous funding, customer traction, etc.

3. What are the key points that make your company unique?

o Management team, successes to date, patents, etc.

4. What pain does your solution solve?

o And how big is the pain?

o What is your unique selling proposition?

5. In what market(s) are you competing?

Step-By-Step Guide to Raising Venture Capital Page 36

o Market sizes, trends, etc.

6. How do you generate revenues?

7. Who is your competition?

o Strengths, weaknesses, etc.

8. Who is on your management team?

o Experience, track record, etc.

9. What is your timeline/roll-out plan/milestones?

10. How much capital are you seeking?

o Projections and uses of funds

When developing your investor PowerPoint presentation it is always good to try

to achieve VC and blogger Guy Kawasaki's 10/20/30 Rule of PowerPoint as

follows: a PowerPoint presentation should have ten slides, last no more than

twenty minutes, and contain no font smaller than thirty points.

Step-By-Step Guide to Raising Venture Capital Page 37

Identifying the Right Venture Capitalists

Factors to Consider when Seeking a Venture Capital Firm

Once you prepare your marketing and presentation materials, the next part of the

process of raising venture capital is to find the right venture capital firms. While

this may seem simple, it isn't. There are thousands of venture capital firms in the

United States alone, and going after the wrong ones is one of the most common

reasons why companies fail to raise the capital they need.

When seeking a venture capital firm, there are seven key variables to consider:

1. Location: Most venture capital firms only invest within 100 to 200 miles

of their office(s). By investing close to home, the firms are able to more

actively get involved with and add value to their portfolio companies.

2. Sector preference: Many venture capital firms focus on specific sectors

such as healthcare, information technology (IT), wireless technologies, etc.

In most cases, even if you have a great company, if you fall outside of the

VC's sector preference, they'll pass on the opportunity.

3. Stage preference: VCs tend to focus on different stages of ventures. For

instance, some VCs prefer early stage ventures, for example companies

with no revenues, where the risk is great, but so are the potential returns.

Conversely, some VCs focus on providing capital to firms to bridge capital

gaps before they go public.

4. Partners: Venture capital firms are comprised of individual partners.

These partners make investment decisions and typically take a seat on

Step-By-Step Guide to Raising Venture Capital Page 38

each portfolio company's Board. (Note that companies that VCs fund are

known as “portfolio companies.”)

Partners tend to invest in what they know, so finding a partner that has

past work experience in your industry is very helpful. This relevant

experience allows them to more fully understand your venture's value

proposition and gives them confidence that they can add value, thus

encouraging them to invest.

5. Portfolio: Just as you should seek venture capital firms whose partners

have experience in your industry, the ideal venture capital firm has

portfolio companies in your field as well.

In fact, a VC may ask the management teams of their portfolio companies

about your venture since these individuals are industry experts. In

addition, if your venture has potential synergies with a portfolio company,

this may significantly enhance the VC’s interest in your firm.

6. Assets: Most companies seeking venture capital for the first time will

require subsequent rounds of capital. As such, it is helpful if the VC has

“deep pockets,” that is, enough cash to participate in follow-on rounds.

This will save the company significant time and effort in raising future

funds.

7. Fit: As mentioned previously, entrepreneurs and venture capitalists are

partners. That is, they generally work very closely together to achieve a

common goal (growing a successful company and getting to an exit). As

such, it is critical that there be a good personality fit and ability to work

together between the VC and the founder/management team.

Finding the right venture capital firm is absolutely critical to companies seeking

venture capital. Success yields you both the capital your company requires and

Step-By-Step Guide to Raising Venture Capital Page 39

significant assistance in growing your venture. Conversely, failing to find the

right firm often results in raising no capital at all and being unable to grow your

company.

How to Create Your List of Potential Venture Capital Firms

If you talk to an experienced direct marketer, they will tell you that “The list is

everything.” If you don't have the right list, you are wasting your marketing

dollars. The right list is ten times as important as whatever you put in the mailing

envelope, or whatever offer you include in your outbound telemarketing script.

The same holds true for your list of prospective venture capital firms. That is, if

you are going after the wrong VCs, no matter how good your company is, you

probably won't get funding.

There are three steps to creating a killer VC list.

1. Develop a list of VC funds. You can do this either by purchasing a list or

database access from a firm such as Growthink Research or by going to the

National Venture Capital Association's website (which lists NVCA member

organizations).

2. Narrow your list. VCs invest primarily based on:

• Market sector

• Stage of development

• Geographic location

The other factors presented in the last section, mainly partners, portfolio, assets,

and fit, become more important after you create your initial list.

Step-By-Step Guide to Raising Venture Capital Page 40

Virtually all VCs have websites that make this information readily available. Find

investors that are a fit with your company for all three of these areas. For

instance, if you are a pre-revenue software company based in Chicago, your best

bet is to find a venture capital firm within 200 miles of Chicago that has

experience funding pre-revenue software companies. Sites like Growthink

Research allow you automatically filter your lists by these criteria.

3. Make sure the VC is active. Go to the press release section of the VC's

website and/or search Google News to see how active the VC is. If the VC has not

done a deal in a year, they probably are not actively investing in new deals and

may not be worth contacting.

What you will be left with is a list of VCs that are actively seeking companies like

yours. Once you have this list, you need to identify the right partner at that firm

to contact.

Identifying the Right Partner at a Venture Capital Firm

As mentioned above, venture capital firms are comprised of individual partners

(and associates that assist them). These partners make investment decisions and

typically take a seat on each portfolio company's Board.

Partners tend to invest in what they know, so finding a partner that has past work

experience in your industry is very helpful. This relevant experience allows them

to more fully understand your venture's value proposition and gives them

confidence that they can add value, thus encouraging them to invest.

Fortunately, most venture capital firm websites list their partners with great

pride. Each partner typically has a bio that includes their educational credentials,

business accomplishments and investments that they have made. In identifying

the right venture capital partner to contact for your company, try to find the

Step-By-Step Guide to Raising Venture Capital Page 41

partner that, from their background, will truly grasp the opportunity and can

really add value.

Once you have identified the most appropriate venture capital partner, it is

important to figure out how to contact them. As partners are often inundated

with business plans, having a personal connection and/or introduction is often

the difference between getting heard and not getting heard.

For instance, if you attended the same university or worked at a company that

they did, call or email them and use this as the introduction. If not, it is important

to network. Call people that may have been associated with the partner and ask

for an introduction.

Getting the partner's attention is the first key hurdle in raising venture capital.

The second hurdle is getting them to believe in the opportunity, and finally,

giving them the enthusiasm and information needed to convince other partners

in their firm that investing in your venture represents a sound investment.

Lead Investors vs. Syndicates/Co-Investors

When raising venture capital, it is important to note that many venture capital

financing events are “syndicated.” In other words, multiple venture capital firms

participate in the financing round.

The entrepreneur or business owner's mission is to find the “lead investor” – the

investor who will fund at least 50% of the financing round, and who often helps

in finding the other syndicates/co-investors as needed.

Note that if investors tell you that they are interested in investing but that you

must first find a lead, this is pretty close to them saying “No.” The lead investor is

Step-By-Step Guide to Raising Venture Capital Page 42

the one who really takes the risk in learning about your company, conducting due

diligence, and providing the most capital to your firm.

Find the lead, and the rest should follow.

Step-By-Step Guide to Raising Venture Capital Page 43

Contacting Venture Capitalists

The Three Ways to Contact Venture Capitalists

To recap, at this point, you should have a list of venture capital firms who seem to

be a good fit for your company with regards to their geographic, sector and stage

foci. In addition, you have reviewed their websites to make sure they are actively

investing, and you have identified the ideal partner at their firm to contact. Now,

let’s talk about how to most effectively contact these partners.

There are three main ways to contact partners at VC firms:

1. Get an introduction

2. Meet them online or offline

3. Contact them cold

I have listed these in descending order of preference, meaning that the most

effective contact method is via an introduction. Cold contacting is the least

effective; however it still works time and time again.

1. Getting Introductions

Getting an introduction is the easiest way to getting a VC’s attention. Because VCs

are inundated with pitches from entrepreneurs, they simply lack the time to meet

with everyone. An introduction gives you priority over other entrepreneurs who

contact the VCs.

There are six key types of individuals who can introduce you to the venture

capitalist you are seeking.

Step-By-Step Guide to Raising Venture Capital Page 44

1. Entrepreneurs whom the investor has previously backed or is

currently backing.

Venture capitalists place significant value on the opinions of the

entrepreneurs they are currently backing (they obviously believed in them

enough to write them large checks). As such, getting an introduction from

these entrepreneurs carries a lot of weight.

Better yet, VCs have an even higher opinion of entrepreneurs they have

funded that have made them a lot of money (i.e., entrepreneurs who have

successful grown and exited companies giving the VC major returns).

Getting introductions from these entrepreneurs is even better.

Even if you don’t currently know such entrepreneurs, finding them can be

quite easy. Growthink Research maintains a database with the contact

information of nearly 100,000 entrepreneurs who are, or have been, on

the management teams of venture backed companies.

A great story of leveraging other entrepreneurs to get VC contacts is the

story of Ryan Allis, the CEO of iContact. Ryan raised $5 million in venture

capital for his North Carolina-based company at the age of 22. He did this

by finding a nearby entrepreneur who had successfully raised venture

capital and getting him to agree to be his mentor. The entrepreneur

introduced Ryan to several venture capitalists, advised him on many of the

capital-raising issues, and ultimately led to his financing success.

2. Other investors with whom the investor has co-invested.

If you have connections to other venture capitalists, particularly those who

have co-invested with the venture capitalist you are seeking, ask them to

introduce you.

Step-By-Step Guide to Raising Venture Capital Page 45

Likewise, whenever you speak with a potential investor, find out who else

they know that could be a good fit and ask for an introduction to them.

3. Market, product, and technology experts such as senior

executives at dominant companies or lauded professors.

Venture capitalists follow industries. For example, if a venture capitalist

focuses on software, you can bet that they are reading the software trade

journals, attending software conferences, following public software

companies, etc.

As such, the venture capitalists generally know, or at least know by name,

executives at dominant companies or professors in the space. Finding

these individuals and asking them to introduce you to the appropriate

venture capitalists is often very effective.

Key Point – assembling your Board of Advisors: Oftentimes you

should first solicit these individuals to become a member of your Board of

Advisors. A Board of Advisors is an informal version of your Board of

Directors. They generally have no voting privileges, but provide value in

the form of advice, know-how and contacts. Typically, Advisors are

compensated with equity. Industry executives, successful entrepreneurs,

and professors make great Advisors.

If you don’t have an Advisory Board, you should get one as they are

relatively easy and cost no money to create. In fact, SCORE (go to

score.org) offers a free service to help you build your Advisory Board.

Step-By-Step Guide to Raising Venture Capital Page 46

4. Lawyers, accountants, consultants and other industry people.

Lawyers, accountants, and consultants are the trusted advisors of venture

capital firms, and VCs pay them large sums of money each year to provide

their services. As trusted advisors, venture capitalists give great merit to

entrepreneurs which they introduce to them.

While top law firms may charge significant dollars to set up legal

agreements, entrepreneurs should consider the benefits they may provide

with regards to introductions to venture capitalists. The same holds true

for many accountants and consultants.

5. Angel Investors and Board Members.

As mentioned above members of your Advisory Board often have

connections to venture capitalists. Likewise members of your Board of

Directors, if you have one, are often well-connected. Finally, if you have

angel investors, they often have relationships with venture capitalists or

are can contact friends who do.

6. The venture capitalist’s online social networking colleagues.

Many venture capitalists participate in online social networks such as

LinkedIn, Spoke, or Facebook. On networks such as LinkedIn, you can ask

other individuals who are connected with the venture capitalist you seek to

introduce you to them. If you are not yet a member of LinkedIn, join it (at

LinkedIn.com). It’s free and doesn’t take too much time to get real value

from it.

Successful entrepreneurs oftentimes leverage several of these sources of

introductions. As mentioned above, each time you meet a venture capitalist or

other established individual, don’t hesitate to ask for an introduction. Oftentimes

the random introduction leads to a financing transaction.

Step-By-Step Guide to Raising Venture Capital Page 47

One example of using multiple introductions was the story behind Google’s

financing. Google founder's Page and Brin discussed their concept with their

computer science professor David R. Cheriton. Cheriton then introduced them to

his friend Andy Bechtolsheim.

Bechtolsheim then wrote Google a check for $100,000.

And then, Google raised more money from friends and family.

And through their rapidly growing network of investors and advisors, they met

and received angel investments from Ram Shriram, a former Netscape executive,

and Ron Conway and Bob Bozeman, partners in Angel Investors.

And later these angel investors introduced Google to the right venture capitalists

who wrote Google even larger financing checks.

2. Meeting Venture Capitalists Online or Offline

As mentioned above, many venture capitalists participate in online social

networks through which you can get introductions to them.

You can also create relationships yourself with VCs through the online medium.

For example, you can find out if the venture capitalists has a blog (many do). If

so, read their blog to learn more about them and what excites them. It is also

smart to post comments on their blog. Oftentimes they’ll reply to your comments,

and before you know it, you have established a relationship with them.

Step-By-Step Guide to Raising Venture Capital Page 48

You might also see if the VC is active on Twitter (many are). If so, follow them on

Twitter and see what they’re posting about. See if there are opportunities to start

a dialogue.

And all the while, think of these online interactions just as if they were offline in

the “real world.” Act just like you’d act as if you were meeting them in person at a

cocktail party.

While meeting venture capitalists virtually/online may be simpler and easier,

meeting them offline is also highly effective. In order to stay abreast of the

happenings in their markets, venture capitalists attend lots of events. They attend

capital conferences, pitching events (where entrepreneurs pitch VCs or angel

investors), trade shows, etc.

Oftentimes you can read on their blog about the events they will be attending. It

is a good idea to attend these same events and meet the venture capitalists there.

You can then discuss the event with them and establish yourself as a credible

industry insider.

As an example of the power of offline events, note the story of Ron Feldman, CEO

of Kwiry. Ron met a venture capitalist at a University alumni event he attended;

that VC eventually funded his company.

Finally, when you are seeking venture capital, you need to let your network know

about it. Tell your contacts on Facebook and/or email your friends. You never

know who has connections to potential investors.

3. Contacting Venture Capitalists Cold

The final way to contact venture capitalists is “cold” – that is, without an

introduction and without meeting them at an event or conference or online.

Step-By-Step Guide to Raising Venture Capital Page 49

While this method is the most challenging, since you need to get through the VC’s

filters, it can be highly effective.

The best strategy for contacting venture capitalists “cold” is to email them. Note

that calling them is much less effective as you will nearly always get their voice

message and rarely if ever will you receive a call back.

With regards to emailing the venture capitalist, usually the email address of each

partner is listed on the VC’s website. If not, call the VC firm to find out the

partner's email address.

It’s critical that you NEVER email a generic email address (such as

[email protected] or [email protected]). These

types of email addresses are like “black holes” – you’ll generally never see a

response.

In the email, ideally you can make a connection to them via their blog or research

(e.g., I read how you are involved with this and that. Based on that, I think you

might be interested in my venture…).

In your email, do NOT send them your business plan. Realize that VCs are

inundated with business plans. They are NOT going to read your business plan if

you send it to them in the initial email. Rather, send them your “teaser email” as

discussed earlier.

What Materials to Send – And in What Order