Embed Size (px)

Citation preview

STRATEGY

Research Analysts:

Learning from corporate failure

Prashant Mittal, [email protected]

March 2016

Complacency

to

competition

Complacent

capital

allocation

Complacency

to business

environment

CDRRocks

Top

Quality

Company

Saurabh Mukherjea, [email protected]: +91 22 3043 3174

Consultant: Anupam [email protected]

Ritesh Gupta, [email protected]

Parita Ashar, [email protected]

Ashvin Shetty, [email protected]

Paresh Dave, [email protected]

Strategy

March 23, 2016 Ambit Capital Pvt. Ltd. Page 2

CONTENTS

Learnings from corporate failure…………………………………………………… 3

Section 1: A framework for identifying failure ……………………………………4

Section 2 – Analysis of corporate failure …………………………………………10

- Case Study 1: Tata Steel (bottom slider) vs JSW Steel (top half) …………15

- Case Study 2: M&M (bottom slider) vs Tata Motors (top half) …………….19

- Case Study 3: Indian Oil Corporation (IOC; bottom slider) ……………...24 vs Bharat Petroleum Corporation (BPCL; top half)

- Case Study 4: GSK Pharma (bottom slider) vs Sun Pharma (top half) …..28

Section 3 – Spotting corporate failure on a prospective basis ………………..33

Appendix 1 ……………………………………………………………………………40

Ambit Capital and / or its affiliates do and seek to do business including investment banking with companies covered in its research reports. As a result, investors should be aware that Ambit Capital may have a conflict of interest that could affect the objectivity of this report. Investors should not consider this report as the only factor in making their investment decision.

Learning from corporate failure

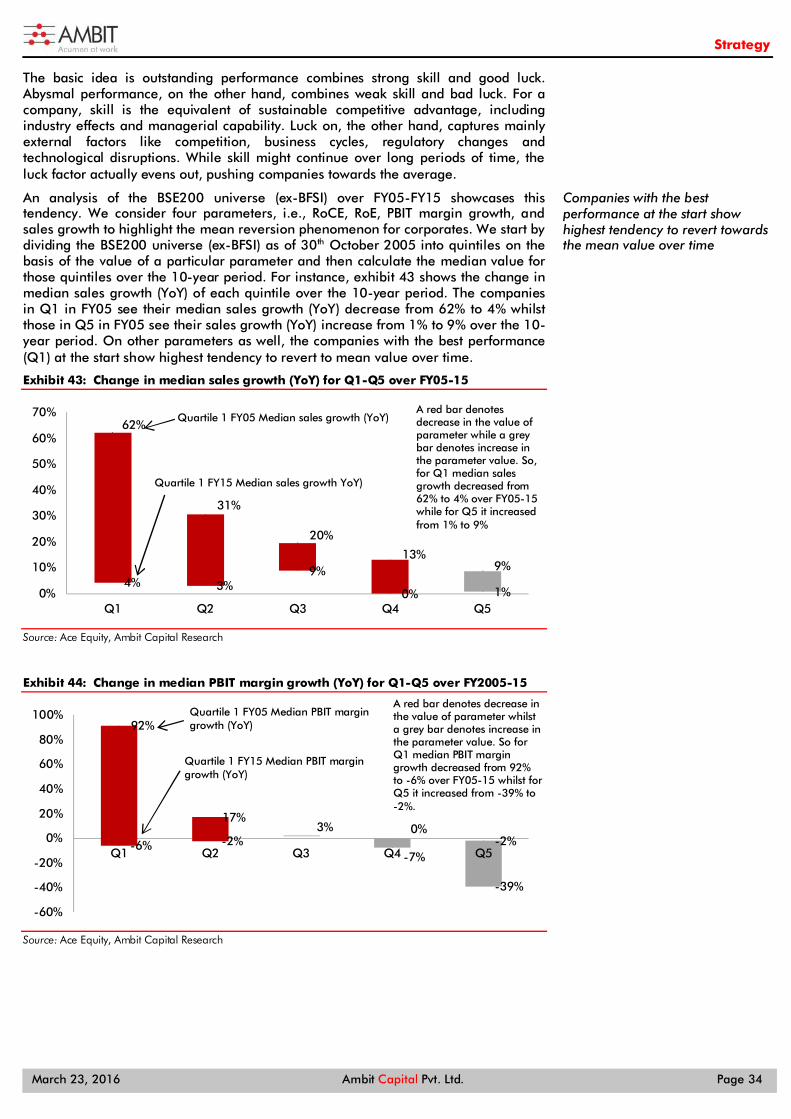

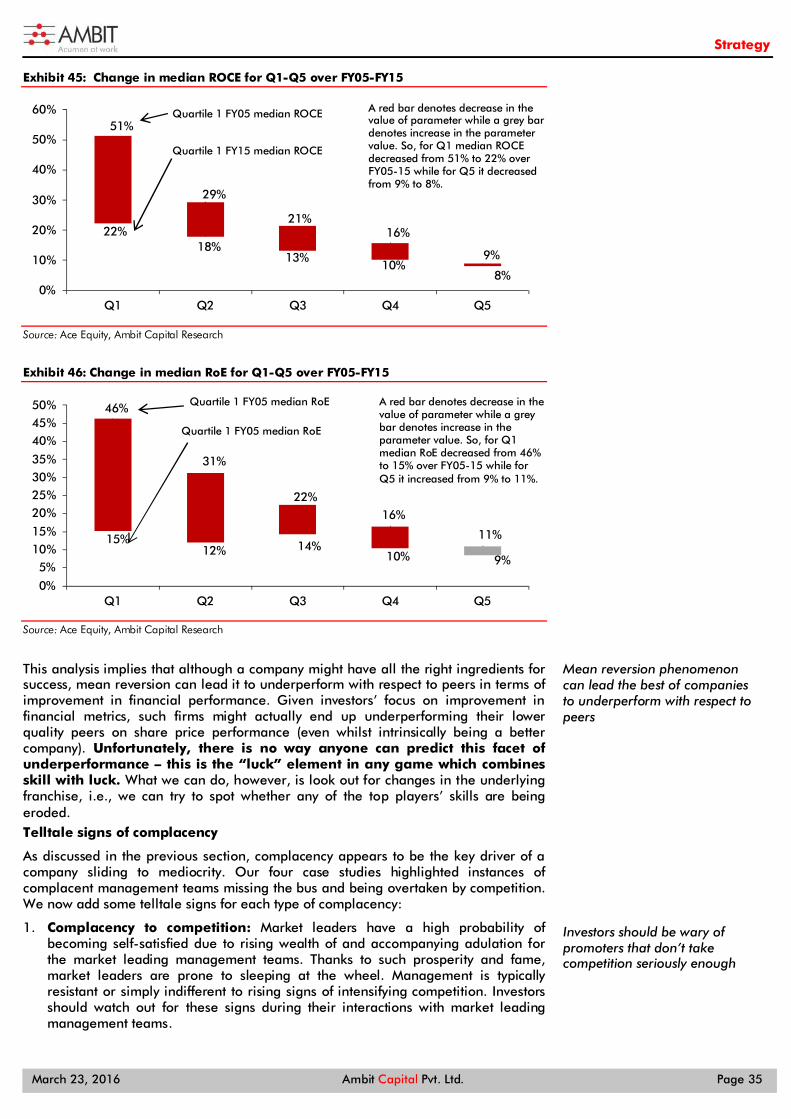

64% of BSE200 companies (ex-Financial Services) that were “great” in FY05 slid to mediocrity by FY15. However, our analysis shows that secular (i.e., non-cyclical) companies have a much higher probability than cyclical companies of remaining great (i.e., delivering superior results over long periods of time). That said, even with secular companies, investors should watch out for promoters sleeping at the wheel, i.e., complacency to competition, to the business environment and to capital allocation; these remain the biggest reasons for failure. Leading businesses are prone to fail but provide enough red flags before sliding.

Identifying corporate failure Our 'Greatness Framework', unveiled in 2012, has a strong track record of identifying companies that allocate capital sensibly over long periods of time. Not much, however, is known about companies that have failed to do so. Hence, we now use the same framework to identify failure – companies that were once great, but have slipped over the past decade (FY05-FY15). Secular companies outgun cyclicals along different dimensions We ran our Greatness Filter on the BSE200 Index (ex-Financials) as it stood on 30th Oct 2005 and classified the companies into quartiles (with Q1 being the top quartile). Our analysis revealed that 64% of all Q1 companies as of FY05 end up in Q3 or Q4 by FY15. However, 50% of the FY05 secular companies stay in the top half (Q1+Q2) even as 71% of cyclical companies slide to the bottom half (Q3+Q4) over FY05-15. Expectedly, secular Q1 companies (in FY05) that remain in the top half (in FY15) provide the best stock price performance, beating cyclicals and the BSE200 (ex-BFSI) over FY05-15. Surprisingly, the few cyclical companies that managed to sustain their financial performance over FY05-15 delivered lower stock price returns than the secular companies which slid. Why do companies fail? Complacency is a key factor It is easy to blame the economy, the worsening of commodity cycle, etc., for the travails of companies that slid to the bottom half. We posit that the real reason is simpler: complacency in the face of rising competition and in light of a deteriorating business environment resulting in sub-optimal capital allocation. We provide four pairs of case studies - M&M v/s Tata Motors, Tata Steel v/s JSW Steel, IOC v/s BPCL and GSK Pharma v/s Sun Pharma – to highlight how amongst similar businesses, one slides to the bottom and the other does not. The red flags that signal an imminent slide to mediocrity Are companies that have stayed in Q1/Q2 over FY05-FY15 at risk of sliding to mediocrity going forward? We provide investors with a list of red flags. Watch out for complacent promoters who miss shifts in the market and changes in the business environment, and make excessively bold bets risking their balance sheet. Investors who avoid these companies can make more returns on their investment than promoters of those companies will make on their capital.

THEMATIC March 23, 2016

Strategy

Quartile 1 stocks in FY05 that stayed in Quartile 1 or 2 in FY15

Name

Secular companies (Magic Box)

Cyclical companies

Sun Pharma BPCL

Tata Motors GAIL (India)

Bosch JSW Steel

Nestle India Essar Ports

Sanofi India GE Shipping Co

Ipca Labs Monsanto India

Gujarat Alkalies

Quartile 1 stocks in FY05 that fell to Quartile 3 or 4 in FY15

Name Secular companies Cyclical companies

M & M IOCL

Hero MotoCorp Hindustan Zinc

GSK Pharma Siemens

Jubilant Life Ambuja Cements

SKF India Tata Steel

Asahi India Glass Bharat Electronics

BHEL

Vedanta

ACC

A B B

SAIL

Thermax

BEML Ltd

Chennai Petro. Corp

JP Associates

Gujarat NRE Coke

Bajaj Hindusthan

THIS NOTE CANNOT BE USED BY THE MEDIA IN ANY SHAPE OR FORM WITHOUT PRIOR CONSENT FROM AMBIT CAPITAL.

Research Analysts Saurabh Mukherjea, CFA +91 22 3043 3174 [email protected]

Prashant Mittal, CFA +91 22 3043 3218 [email protected]

Consultant Anupam Gupta [email protected]

“Magic Box” - Secular companies that remain great over FY05-15

Source: Company, Ambit Capital research

Strategy

March 23, 2016 Ambit Capital Pvt. Ltd. Page 4

Section 1: A framework for identifying failure "Every institution is vulnerable, no matter how great. No matter how much you've achieved, no matter how far you've gone, no matter how much power you've garnered, you are vulnerable to decline. There is no law of nature that the most powerful will inevitably remain at the top. Anyone can fall and most eventually do."

- Jim Collins, How the mighty fall (2009)

Given the efficacy of our “Greatness” framework in delivering market-beating returns (by identifying corporates which allocate capital sensibly over extended periods of time), we use the framework to identify corporate failures. In this section, we identify companies that were great in FY05 but slipped to mediocrity by FY15. Our analysis leads us to three startling conclusions:

(a) 64% of all Quartile 1 companies in the BSE200 (ex–BFSI) universe as of FY05 ended up in the bottom half (i.e., Quartile 3 and Quartile 4) by FY15, suggesting that great companies have a high tendency to slide to mediocrity.

(b) Secular (i.e., non-cyclical) companies are more resilient than cyclical ones; 50% of the secular companies in Quartile 1 in FY05 remain in the top half (i.e., Quartile 1 and Quartile 2) in FY15;

(c) Amongst the cyclical companies that were in Quartile 1 in FY05, only 29% remained in the top half in FY15 (implying that 71% of the FY05 Q1 cyclicals slid to mediocrity); and

(d) Secular companies that remained in the top half have posted much better total stock returns (median 25% CAGR) than cyclical companies that remained in the top half (median 15% CAGR) over FY05-FY15.

Our “Greatness” framework works

We had unveiled the ‘Greatness Framework’ on 19th January 2012 with the first iteration of the “Tomorrow’s ten baggers” report (click here). This framework quantifies a firm’s structural strengths by focusing not on absolutes but on improvements in capital allocation (as per the flow diagram given below) and corporate performance over long periods of time and the consistency of those improvements.

Exhibit 1: The ‘greatness’ framework

Source: Ambit Capital Research

More than half of the companies in Q1 in FY05 slide to the bottom half by FY15

Capital allocation lies at the core of our Greatness Framework

b. Conversion of investment to sales (asset turnover, sales)

c. Pricing discipline (PBIT margin)

d. Balance sheet discipline (D/E, cash ratio)

a. Investment (gross block)

e. Cash generation (CFO)

Strategy

March 23, 2016 Ambit Capital Pvt. Ltd. Page 5

Capital allocation lies at the core of our Greatness Framework; in the 10 years from FY05 to FY15, the stock price of BSE200 (ex-BFSI) companies with ROCE of more than 15% beat the BSE200 index by 7.7% on a CAGR basis. The Greatness Framework is reproduced in Appendix 1.

Since 2012, our Greatness Framework has held us in good stead, providing us with the quantitative approach for the ten-bagger portfolio (see our 19 Jan 2016 iteration here). As can be seen in the exhibit below, the ten-bagger portfolio has consistently beaten the BSE500 index since the inception of the portfolio in 2012.

Exhibit 2: Our ten-bagger portfolio has consistently beaten the BSE500 index since initiation

Source: Bloomberg, Ambit Capital Research

Identifying failure

Our three-step exercise begins with identifying companies that have slid to mediocrity on the basis of our Greatness Framework, comparing their total stock returns performance over the past ten years, and, finally, assigning probabilities of success and failure to a particular company in today’s top quartile.

Identifying the companies

We now use our Greatness Framework in reverse. While the ten-bagger portfolio identified stocks that have sustained and/or improved their financial performance, we now apply the greatness filter to identify companies whose financial performance has deteriorated in the past decade. The methodology is as follows:

Step 1: We start with the BSE200 Index, excluding banking and financial services industry (BFSI) stocks, as on 30th October 2005. The sample set consists of 161 companies.

Step 2: We apply the Greatness Framework (outlined in Appendix 1) on these companies for FY05-FY15 (10 years). In other words, we run our Greatness Framework on the selected 161 companies as at FY05-end and at FY15-end.

Step 3: We use quartiles to rank the sample set of 161 companies. Quartile 1 consists of the highest ranked companies in the Greatness Framework and Quartile 4 has the worst ranked companies. We use the term ‘top half’ to describe companies in Quartile 1 and Quartile 2 and ‘bottom half’ to describe companies in Quartile 3 and Quartile 4.

Step 4: We use the term ‘bottom slider’ to denote companies that slid from Quartile 1 in FY05 to the bottom half (Q3 or Q4) in FY15.

Step 5: We define as secular as any sector (mainly IT, Pharma, FMCG, Autos and Consumer Discretionary) that is not cyclical. As a result, 67% of the companies in Quartile 1 as at FY05-end are cyclical whilst 33% are secular.

6.7 9.8

43.4 52.6 53.3

(10) - 10 20 30 40 50 60 70 80

2012 2013 2014 2015 2016

Ret

urn

(%)

Ten-bagger iteration return index return cumulative alpha

We use our Greatness Framework in reverse to identify failures

Strategy

March 23, 2016 Ambit Capital Pvt. Ltd. Page 6

Applying the above methodology, we get the following results:

41 companies start in Quartile 1 (top quartile) of the BSE200 ex-Financials. We exclude five companies (Mylan Lab, Ranbaxy, Kochi Refineries, Bongaigaon Refineries and Sterlite Industries) that were delisted or merged over FY05-15. That leaves us with 36 companies in Quartile 1. Of these, 23 (i.e. 64%) slide to the bottom half by FY15, while 13 remain in the top half ten years hence.

Of the 23 bottom sliders, 17 are cyclical and 6 are secular. We highlight that the high share of cyclicals (17 out of 23 companies, or 74%) is much higher than the percentage of cyclicals (67%) in Quartile 1 at FY05-end (implying that cyclical companies are over-represented amongst the bottom-sliders).

Of the 13 top winners (i.e. companies that were Q1 in FY05 and remained in either Q1 or Q2 in FY15), 6 are secular and 7 are cyclical. Here, we highlight the high share of secular companies (6 out of the 13 top winners, or 46%) which is significantly higher than the seculars’ share of 33% in Quartile 1 at FY05-end (implying that secular companies are over-represented amongst the top winners).

The secular companies which started in Quartile 1 in FY05 and are in the top half in FY15 constitute the “Magic Box”. In other words, these are the companies which have the benefit of both being secular in nature, thus having higher probability of ending up in the top half in FY15 (~59%; computed as ‘1- probability of sliding to the bottom half (41%)’ as seen in exhibit 3 below), and being the best of that lot as well. Exhibit 3 below shows the number of secular and cyclical companies sliding from Q1 to the bottom half over three 10-year instances i.e. FY03-13, FY04-14 and FY05-15 and computes the probability of a secular or cyclical company sliding to the bottom half over a 10-year period.

Exhibit 3: Secular companies have a higher probability of ending up in the top half after a decade

Firms

in Q1

# of secular firms in

Q1

# of cyclical firms in

Q1

# of total firms

after a decade in

% of firms moving to

bottom half

# of secular firms after a

decade in

# of cyclical firms after a

decade in

% Seculars moving to

bottom half

% Cyclicals moving to

bottom half

Top half Bottom half Top

half Bottom

half Top half

Bottom half

FY03-13 41 23 18 18 23 56% (i.e. 23/41) 14 9 4 14 39%(i.e. 9/23) 78% (i.e. 14/18)

FY04-14 37 17 20 18 19 51% (i.e. 19/37) 11 6 7 13 35% (i.e. 6/17) 65% (i.e. 13/20)

FY05-15 36 12 24 13 23 64%(i.e. 23/36) 6 6 7 17 50% (i.e. 6/12) 71% (i.e. 17/24)

Average 57% 41% 71%

Source: Ambit Capital Research, Bloomberg

We summarize our findings in the exhibit below.

Exhibit 4: Magic Box – 6 secular stocks that beat their cyclical peers and the benchmark over FY05-15

Source: Ambit Capital research, Bloomberg.

The list of FY05 Q1 companies in the top half and the bottom half in FY15 are as follows:

Of the 36 companies in Q1, 13 remain in the top half till FY15 while 23 slide to the bottom half

Magic Box consists of six stocks that have beaten cyclical peers and the BSE200 (ex-BFSI) index

13 top half companies vs 23 bottom half companies

Strategy

March 23, 2016 Ambit Capital Pvt. Ltd. Page 7

Exhibit 5: Separating the winners from the bottom sliders

Remained in top half (FY05 to FY15) Slid to bottom half (FY05 to FY15)

Secular companies (10-year share price CAGR, 10-year EPS CAGR) Secular companies (10-year share price CAGR, 10-year EPS CAGR)

1 Nestle India (22%, 17%) 1 Hero MotoCorp (14%, 11%)

2 Bosch (25%, 14%) 2 Jubilant Life (7%, N/A)

3 Sanofi India (13%, 5%) 3 M & M (21%, 13%)

4 Tata Motors (16%, 19%) 4 Glaxosmithkline Pharma (14%, 6%)

5 Ipca Labs. (26%, 13%) 5 SKF India (19%, 12%)

6 Sun Pharma (32%, 26%) 6 Asahi India Glass (9%, -9%)

Cyclical companies (10-year share price CAGR, 10-year EPS CAGR) Cyclical companies (10-year share price CAGR, 10-year EPS CAGR)*

1 BPCL (17%, 10%) 1 Tata Steel (-2%, N/A)

2 GE Shipping Co (11%, 1%) 2 Gujarat NRE Coke (-20%, N/A)

3 JSW Steel (16%, 1%) 3 Vedanta (8%, N/A)

4 GAIL (India) (7%, 4%) 4 Bharat Electronics (18%, 10%)

5 Essar Ports (14%, -5%) 5 Siemens (19%, 13%)

6 Monsanto India (11%, 3%) 6 Thermax (18%, 12%)

7 Gujarat Alkalies (2%, 5%) 7 BEML Ltd (4%, -30%)

8 A B B (14%, 4%)

9 JP Associates (-10%, N/A)

10 BHEL (6%, 4%)

11 ACC (12%, 11%)

12 Hindustan Zinc (22%, 29%)

13 CPCL (Chennai Petroleum Corporation) (-1%, N/A)

14 IOCL (Indian Oil) (6%, -1%)

15 Ambuja Cements (12%, 10%)

16 SAIL (0%, -11%)

17 Bajaj Hindusthan (-19%, N/A)

Source: Ambit Capital research, Bloomberg. Note: 10-year share price CAGR computed from 31st Oct’05 to 30th Oct’15. * There are several “N/A” signs here as these companies did not make a profit in FY15.

Comparing total stock returns over FY05-15

We tracked the total stock returns of the above companies over a 10-year period from 31st October 2005 to 30th October 2015. One striking find was that secular companies in the top half gave the best returns (median returns of 25% CAGR versus 15% CAGR for the top half cyclical companies and 14% CAGR for the BSE200 (ex-BFSI)) over the 10-year period.

Cyclical companies in the bottom half gave the worst returns (median returns of 9% CAGR versus 17% CAGR for secular bottom half companies and 14% CAGR for the BSE200 universe (ex-BFSI)) over the 10-year period. Even more interestingly, cyclical companies who stayed in the top half gave 10-year share price returns similar to the broader market (15%) suggesting that even if one invests in the best cyclical companies AND even if these companies stay in the top half ten years hence, the shareholders in these names still won’t outperform the benchmark!

In order to make sure that our FY05-15 data run is not an anomaly, we have also performed similar data runs on FY03-13 and FY04-14. Our results for the three 10-year periods FY03-13, FY04-14 and FY05-15 are in the exhibit below.

Secular companies in the top half gave the best returns, while cyclical companies in the bottom half underperformed

Strategy

March 23, 2016 Ambit Capital Pvt. Ltd. Page 8

Exhibit 6: Secular companies in the top half in the tenth year contains the best performing stocks*

Median returns (CAGR)

Secular companies Cyclical companies BSE200

(ex-BFSI) returns

In top half in 10th year (The Magic Box)

In bottom half in 10th year

In top half in 10th year

In bottom half in 10th year

Over the ten years

FY03-13 16.4% 9.2% 12.2% 11.7% 13.7%

FY04-14 25.2% 17.2% 17.8% 16.5% 17.6%

FY05-15 24.9% 16.9% 14.5% 8.8% 13.7%

Average 22.2 % 14.5% 14.8% 12.3% 15.0%

Source: Ambit Capital research, Bloomberg. * The returns given above are total stock returns i.e. these returns take dividend payments into account and assume that dividends are reinvested on the ex-dividend date.

Probability of great companies sliding to mediocrity

We calculated the probability of a company in the top quartile now sliding to the bottom half over the next decade by looking at data from three 10-year data sets, i.e., FY03-13, FY04-14 and FY05-15. The results are as follows:

1) 23 of 36 great companies (in Quartile 1) slide to mediocrity over FY05-15 (implying a probability of 64% of sliding to mediocrity). Considering all the three 10-year data sets, the implied probability of a Q1 company ending up in the bottom half after a decade is 57% (computed using the proportion of companies sliding from Q1 to the bottom half as shown in exhibit 3 above).

2) However, given that it is already known at the beginning of the 10-year period if a company is secular or cyclical, we should look at this probability for secular and cyclical companies separately. Our analysis reveals that the chances of a Q1 secular company sliding to the bottom half is 41%, while the chances of a Q1 cyclical company sliding to the bottom half is higher, at 71% (as shown in exhibit 3 above).

3) Conversely, the chances of a Q1 secular company remaining in the top half is high (59%), while the chances of a Q1 cyclical company remaining in the top half is low (29%). It is worth reflecting on the latter finding for a minute – even if one invests in the best cyclical companies, history suggests that ten years hence, 71% of them would have slid to mediocrity (with obvious adverse implications for shareholders’ returns).

To ensure that these 10-year results do not give us anomalous findings, we ran the same exercise (i.e., applying the greatness filter on BSE200 ex-BFSI companies) over a five-year period for eight instances (shown in the exhibit below) and found that these findings are broadly in line with those of the 10-year data run. The chance of a Q1 secular company staying in the top half five years hence is 59%, while the chance of a Q1 cyclical company staying in the top half five years hence is only 39%. It is worth reflecting on the latter finding for a minute – even if one invests in the best cyclical companies, history suggests that in as little as five years, 61% of them would have slid to mediocrity (with obvious adverse implications for shareholders’ returns).

The chance of a Q1 secular company staying in the top half is high over a decade (at 59%) as well as over a five year period (at 59%)

Strategy

March 23, 2016 Ambit Capital Pvt. Ltd. Page 9

Exhibit 7: Secular companies have a higher probability of retaining top position even on a shorter time frame of 5 years*

5-year period

Secular companies Cyclical companies

Top half in 5th year (The Magic Box)

Bottom half in 5th year

Top half in 5th year

Bottom half in 5th year

FY03-08 50% 50% 41% 59%

FY04-09 47% 53% 57% 43%

FY05-10 57% 43% 36% 64%

FY06-11 47% 53% 48% 52%

FY07-12 67% 33% 28% 72%

FY08-13 50% 50% 46% 54%

FY09-14 70% 30% 36% 64%

FY10-15 86% 14% 20% 80%

Average 59% 41% 39% 61%

Source: Ambit Capital research, Bloomberg. *The above table depicts movement of secular and cyclical companies from Q1 to top/bottom half (basis greatness framework) over a 5 year timeframe.

The ‘cyclicals’ myth debunked

With 23 of 36 companies falling to the bottom half from top quartile (Q1) over FY05-15, our analysis tells us that great stocks have a very high tendency of sliding to mediocrity over a decade. However, the implications for cyclicals are even more damaging. As we have highlighted in our macro-economic research, investors are awaiting a recovery in the Indian economy, which we believe is unlikely anytime soon (we expect FY17 GDP growth of 6.8%, flat over FY16- (click here) for our 26 Oct 2015 note). This extended hope of economic recovery has led to a rising wave of investor fondness for cyclicals. We believe this fondness is not grounded in facts.

Firstly, cyclical companies are more vulnerable to a slide to mediocrity (falling to the bottom half from Quartile 1) over both 5-year period (61% chance) and 10-year period (71% chance).

Secondly, in terms of stock price performance over a decade, even those cyclical companies that remained in the top half (average return of 15% on CAGR basis) underperformed their secular counterparts in the top half (average return of 22% on CAGR basis). To put this more bluntly – by investing in cyclicals, investors carry too much risk for much lower return. The probability of the best cyclical companies sliding to mediocrity is high (see Exhibit 3) and even for those cyclical companies that stay in the top half, the decadal shareholder returns are only in-line with the benchmark (see Exhibit 6).

The case for investing in secular companies remains strong

The tendency of Q1 secular companies to slide to mediocrity is not just lower than that of cyclical ones, it is also much lower than 50%. Further, not only are secular companies much more likely to stay in the top half on a 5-year (59%) and 10-year (59%) basis, they also posted much better share price returns over the 10-year period. Q1 secular companies that stay in the top half a decade hence gave the best stock price performance over a decade (22% CAGR, compared to 15% for their cyclical counterparts in the top half and 15% for BSE200 ex-BFSI).

These findings raise two issues that the remainder of this report will investigate, namely:

Why do successful Indian companies slide to mediocrity so systematically? [see section 2]; and

Are secular companies currently in the Magic Box (Q1 in 2005 and the top half in 2015) a source of future outperformance or a death trap? [see Section 3]

By investing in cyclicals, investors carry too much risk for much lower return.

The tendency of secular companies to slide to mediocrity is not just lower than cyclical companies, it is also much lower than 50%.

Strategy

March 23, 2016 Ambit Capital Pvt. Ltd. Page 10

Section 2 – Analysis of corporate failure "I like to study failure, actually. My partner says, "I want to know where I'll die so I'll never go there." We want to see what has caused businesses to go bad. The biggest thing that kills them is complacency. ... The danger would always be that you rest on your laurels." - Warren Buffett's Top 10 Rules For Success1

“Success breeds complacency. Complacency breeds failure. Only the paranoid survive.” - Andy Grove, Only the Paranoid Survive (1996)

The list of FY05-15 bottom sliders contains some of India’s largest companies like Tata Steel, Vedanta and Hero MotoCorp. Why do these companies slide to mediocrity? It is tempting to ascribe the failure to simplistic reasons such as volatility in commodity prices and weakness in overall economic growth. However, we believe the biggest reason for this failure is complacency at the promoter level. In this section, we use case studies to show how complacency to competition, complacency to business environment and complacency to capital allocation sow the seeds of failure.

Revisiting corporate failure

While corporate success is celebrated, failure – and its important lessons – are ignored. This is our second major study of corporate failure. Our first report was titled “Why do great Indian companies self-destruct?” (click here) and published in June 2013. The central thesis of that report is that a great company’s slide to mediocrity is led by poor strategic decision-making fuelled by ’hubris and arrogance‘. Such faulty strategic decisions usually result in poor capital allocation, which destroys RoCE and creates financial stress. In that report, we created a 5-step framework to mark various phases in a great company’s slide to mediocrity. The framework was based on the works of respected authors like Jim Collins (How the mighty fall) and William Thorndike (The Outsiders). A recap of the five steps highlighted in our 2013 note:

Stage 1 - Hubris and arrogance: The company is on top of its game. Operating margins, RoCE, growth, valuation multiples, etc., are at all-time highs. Captivated by the success in its core business, the management starts believing its own press. Success and adulation intoxicate the top brass. Arrogance sets in. The company loses sight of the factors which made it successful in the first place.

Stage 2 – Unbridled expansion: In search of more growth and more adulation, management begins an expansion drive, often inorganic. The firm ’overreaches‘ into new geographies and product lines where it has no real experience or expertise. Sub-par capital allocation begins.

Stage 3 – Stuck in a rut: Often, cost discipline and/or product excellence erode and prices are then increased. Profits, return multiples and valuation multiples start sliding. Company politics thrives. The leader becomes increasingly autocratic and announces 'recovery plans' that are not based on accumulated experience.

Stage 4 – Grasping for solutions: The company thrashes around and looks for a solution even as profits and financial strength continue to slide. Senior management jobs are on the line. Often a new leader comes in and sometimes he tries to fire silver bullets (e.g., a 'transformative' acquisition, a blockbuster product, a cultural revolution, etc.). However, a new leader (ideally someone from inside) who takes a long, hard look at the facts and then acts calmly to put in place a measured recovery strategy with sensible use of cash and capital at its centre could be the saviour.

Stage 5a – Capitulation: The firm is sold or fades into insignificance or, and this happens rarely, shuts down.

Or Stage 5b – Recovery: The firm turns the corner and begins the long, slow climb to recovery.

Tata Steel is a good example of how the above process works.

1 https://www.youtube.com/watch?v=iEgu6p_frmE

The biggest reason for this failure is complacency at the promoter level

Our 2013 report had a 5-step chronology, marking a great company’s slide to mediocrity

Strategy

March 23, 2016 Ambit Capital Pvt. Ltd. Page 11

Exhibit 8: The five-stage framework

Source: Ambit Capital research, From the book ’How the Mighty Fall’.

Exhibit 9: Tata Steel's journey through the five stages Stage Remarks

Hubris and arrogance Superb financial performance through FY01-05

(FY01-05) Feted as the lowest-cost steel producer globally by World Steel Dynamics

Won the Deming prize

Company started believing it had insulated itself from steel price cycles

Unbridled expansion Evaluates alternative businesses to enter, including telecom, BPO, etc.

(FY06-08) Bids for Corus in 2006 and completes the acquisition in 2007 after a bidding war with CSN

Corus acquisition was at a value of US$12bn when the company’s net worth was US$2bn

Corus did not measure up to the criteria that the company had enunciated in its annual reports for growth/acquisition

Stuck in a rut After initial strong performance, Corus goes into the red

(FY09 - present) Domestic expansion plans get delayed

Company saddled with huge debt

Downturn in global steel cycle exacerbates the situation

Grasping for solutions Restructuring at Corus by mothballing capacities and disposing assets

(FY09 - present) Debt refinancing and equity raising

Enhances raw material security

Change of leadership at Corus

Capitulation or Recovery? Write-down of goodwill - acknowledgement that the acquisition is not working

(FY09 - present) Plans to sell off underperforming and inefficient assets of Corus

Accelerates expansion plans in India to improve the competitive structure of the entire company

Source: Company, Ambit Capital research

Later in this section, we look at a case study comparing Tata Steel and JSW Steel (a cyclical company that has remained in the top half over the past decade).

Corporate failure is ubiquitous

Clearly, different businesses fall apart for different reasons and these reasons are so varied that it is difficult to establish a neat categorisation or taxonomy. Moreover, most businesses in India struggle – evident from the fact that over the past 20 years, 75% of Indian stocks have delivered returns lower than the rate of inflation. Hence studying failure is a never ending task because the vast majority of Indian businesses have ‘failed’ insofar as the failed to even protect the value of shareholders’ money. Since our 2013 report (“Why do great Indian companies self-destruct?”; click here) we have found several of investors to be just as interested in understanding corporate failure better as they are in understanding the drivers of greatness. This prompted us to revisit our 2013 work on this complex topic.

Vast majority of Indian businesses have ‘failed’ insofar as they can’t even protect the value of their shareholders’ money

Strategy

March 23, 2016 Ambit Capital Pvt. Ltd. Page 12

Complacency, not arrogance, is the key culprit

We posit that the main source of greatness lost is staying still as the world changes, i.e., great companies lose their greatness not so much because they have a mighty fall but because they remain at a standstill in a changing world. To use an analogy from driving, great companies’ fall from grace is due to their falling asleep at the wheel and then crashing into the sidings as the road bends.

Exhibit 10: The list of bottom-slider companies

Slid to the bottom half (FY05 to FY15) FY05-15

Share price CAGR

FY05-15 EPS CAGR

FY05-15 cum. CFO /

cum. EBITDA

FY05-15 ROCE

change

Secular companies

1 Hero MotoCorp 14% 11% 96% -26%

2 Jubilant Life 7% N/A 86% -18%

3 M & M 21% 13% 29% -9%

4 GSK Pharma 14% 6% 100% -20%

5 SKF India 19% 12% 94% -10%

6 Asahi India Glass 9% -9% 87% -3%

7 Bajaj Hindusthan -19% N/A 52% -27%

Cyclical companies

1 Tata Steel -2% N/A 102% -56%

2 Gujarat NRE Coke -20% N/A 6% N/A

3 Vedanta 8% N/A 96% -102%

4 Bharat Electronics 18% 10% 88% -30%

5 Siemens 19% 13% 87% -33%

6 Thermax 18% 12% 97% -8%

7 BEML Ltd 4% -30% 40% -36%

8 ABB 14% 4% 70% -22%

9 JP Associates -10% N/A 66% -9%

10 BHEL 6% 4% 92% -21%

11 ACC 12% 11% 103% -4%

12 Hindustan Zinc 22% 29% 100% -15%

13 CPCL (Chennai Petroleum Corporation) -1% N/A 75% -30%

14 IOCL (Indian Oil) 6% -1% 49% -12%

15 Ambuja Cements 12% 10% 100% 0%

16 SAIL 0% -11% 87% -64%

Source: Bloomberg, Ace Equity, Ambit Capital Research. Note: 10-year share price CAGR computed from 31st Oct’05 to 30th Oct’15

Of the 23 names in the list shown above, none are over-aggressive except Tata Steel, which did an oversized acquisition. The 5-step Jim Collins framework does not appear to apply to them. So why did they fail? We believe that complacency lies at the heart of this failure, as follows:

1. Complacency to competition: One way to identify this complacency is when a company becomes used to staying at #1 and ignores competition catching up and eventually overtaking it. M&M stands out on this front given that it missed the shift in trend towards compact, urban sports utility vehicles (SUVs) – a market that was eventually captured by Ford’s Ecosport and Renault’s Duster. When M&M acquired Ssangyong Motors in 2010, Pawan Goenka, Executive Director M&M justified it, saying2, “There is an opportunity to introduce a premium portfolio of SUVs in the Indian market, providing a new growth avenue for SsangYong and further strengthen our dominant position in the UV segment.” After four years, when this premium SUV market failed to materialise, Mr. Goenka had this to say

2 http://www.business-standard.com/article/companies/mahindra-buys-70-in-ssangyong-110112400046_1.html

The main source of greatness lost is staying still as the world changes

M&M missed out on the shift in trend towards compact SUVs

Strategy

March 23, 2016 Ambit Capital Pvt. Ltd. Page 13

in a 2014 press interview3 when asked if M&M failed to spot the market preference for compact SUVs: “We didn’t miss the trend but we delayed it by about a year. We would have been more comfortable if new products had been launched this year rather than the next. The change or impetus for compact SUVs happened a year sooner than we thought. That’s the way I would put it.”

2. Complacency to the business environment: Changes in macro-environment – such as a slowdown in economic growth, collapse in commodity cycles – are difficult to predict. However, when such an event does occur, a complacent management does not react in time and by the time it does, it is too late. The smarter management teams ensure that their balance sheets are prepared to absorb these shocks. Tata Steel stands out as an example of excesses done during the peak of the cycle, like the acquisition of Corus, which landed them in trouble when the commodity cycle turned. As we wrote in our June 2013 thematic report (click here), “Why do great Indian companies self-destruct?”:

Leaving aside the acquisition price for Corus and leaving aside the recession that the world economy entered after September 2008, Tata Steel simply did not have the management bandwidth to run an ailing European steel manufacturer. While the intentions were noble, the organisation was completely unprepared. Instead of improving communication channels with the leadership team across units, insiders said Dr. Karl Köhler (Managing Director and CEO, Tata Steel Europe) surrounded himself with ‘yes men’. An executive from Tata Steel Europe, who declined to be named, said Köhler surrounded himself with former colleagues from ThyssenKrupp: “There is no British executive in the top management.” Thus, this was the first really large deal for a company; its earlier biggest challenge was operational in nature and internally focused – restructuring and modernisation. To top everything, the global financial crisis came soon after and demand in Europe is yet to recover to its pre-crisis levels.

3. Complacency to capital allocation: This happens when companies throw good money after bad and bet the balance sheet on ill-thought-out plans. Once again, M&M stands out for its forays into two-wheelers and trucks. While these ventures had no impact on their balance sheet, it is revealing that management chose to use acquisitions to foray into highly competitive sectors with little chance of meaningful success. M&M is also no stranger to global ambitions considering: a) it bid for European tractor maker Valtra in 2003 and was interested in bidding for JLR in 2007; b) acquired majority stakes in Korea’s Ssangyong Motors for US$463m in 2011and Italy’s Pininfarina for €25m in 2015. The Ssangyong acquisition took its toll on M&M’s financials even as it missed the compact SUV segment. As seen in the exhibit below, capital employed in M&M’s automotive segment shot up in FY11 and RoCE fell due to the acquisition. M&M’s 10% RoCE in FY15 is a far cry from peak levels in FY05.

3 http://www.thehindu.com/business/Industry/every-industry-has-to-innovate-disruptions-pawan-goenka/article6158306.ece

Tata Steel’s Corus acquisition stretched its balance sheet inordinately

M&M’s investments in trucks and two-wheelers had little impact on its overall profitability

Strategy

March 23, 2016 Ambit Capital Pvt. Ltd. Page 14

Exhibit 11: Investment in Ssangyong and loss of share in UVs have hit M&M’s automotive business RoCE

Source: Company, Ambit Capital research

We now delve into detailed case studies that highlight these issues. In all of them, we compare a bottom slider company with a top half company (i.e., one that stayed in the top half of our Greatness Framework over a 10-year period). The exhibit below lists these companies and their key financials and reasons for difference in performance over the last decade.

Exhibit 12: Key financials and differences between the four case study companies Case study company

FY05-15 Share price

CAGR

FY05-15 EPS CAGR

FY05-15 cum. CFO/

cum. EBITDA

FY05-15 ROCE

change Key differences

Tata Steel -2% N/A 102% -56% Acquired Corus putting balance sheet at risk

JSW Steel 16% 1% 80% -19% Focused on cost efficiencies in Indian operations

M & M 21% 13% 29% -9% Missed shift towards compact SUVs, invested outside UVs, tractors

Tata Motors 16% 19% 102% -13% Focused and filled product gaps in JLR portfolio, raised presence in China

IOCL (Indian Oil) 6% -1% 49% -12% Bureaucratic functioning has slowed network efficiencies compared to BPCL

BPCL 17% 10% 106% -6% Used branding initiatives, invested in upstream assets and gas ventures

GSK Pharma 14% 6% 100% -20% Impacted by drug price control order

Sun Pharma 32% 26% 80% 3% Turned around acquired companies effectively without impacting profitability

Source: Bloomberg, Ace Equity, Ambit Capital Research Note: 10-year share price CAGR computed from 31st Oct’05 to 30th Oct’15

0%

10%

20%

30%

40%

50%

60%

FY07 FY08 FY09 FY10 FY11` FY12 FY13 FY14 FY15

Share of automotive business in M&M's total capital employed

Average RoCE of automotive business

Strategy

March 23, 2016 Ambit Capital Pvt. Ltd. Page 15

Case Study 1: Tata Steel (bottom slider) vs JSW Steel (top half) Parita Ashar, CFA, [email protected], +91 22 3043 3223

Background: Tata Steel began operations in 1907 at its steel plant in Jamshedpur, which it developed into an industrial city. The plant was Asia's first integrated steel mill since Tata Steel had captive iron ore and coal mines near the factory. In 2004, Tata Steel acquired NatSteel Singapore, and in 2005, it acquired Millennium Steel Thailand. In 2008, Tata Steel acquired Corus for US$12bn – the largest acquisition by an Indian company. Currently, Tata Steel also has one new greenfield project underway in Odisha. JSW Steel is the flagship company of the Sajjan Jindal Group. The Jindals set up Jindal Iron & Steel Company in 1982, which was eventually merged with Jindal Vijaynagar Steel in 2005 to form JSW Steel. In Dec 2010, JSW Steel acquired Ispat Industries. Starting off as cold-rolled mill near Mumbai in 1982, JSW Steel now has six manufacturing locations in India (four in Maharashtra and one each in Karnataka and Tamil Nadu). As of end-FY15, JSW Steel had capacity of 14.3mt in India, compared to Tata Steel's 9.7mt. On a consolidated global level, however, Tata Steel is much larger with total capacity of ~30mt.

JSW Steel’s ability to stay in the top half of our Greatness Framework from FY05 to FY15 can be attributed to Sajjan Jindal’s reputation as a turnaround specialist. JSW Steel emerged successfully from a Corporate Debt Restructuring (CDR) scheme with IDBI Bank in the early 2000s. From there, JSW Steel acquired two debt-laden, ailing companies (Southern Iron and Steel Company in 2002 and Ispat Industries in 2010) and turned both of them around. In comparison, Tata Steel was likely a victim of its own ambitions of becoming a global steel superpower by acquiring Corus. Following the acquisition, Tata Steel struggled with integration issues since it simply did not have enough management bandwidth to run an ailing European steel manufacturer. More recently, while both companies have been hit by the slump in iron ore and steel prices (which began in 2011), JSW Steel has been better off due to its well-known cost-efficient operations in India, while Tata Steel has borne the brunt of the Corus acquisition.

We provide a snapshot comparison of the companies in the exhibit below:

Exhibit 13: Tata Steel vs JSW Steel Financial information (FY15) Tata Steel JSW Steel

Consolidated Sales (`bn) 1,395 530

Consolidated PAT (̀ bn) (3.3) 18

Pre-tax ROCE (%) 6.1% 10.3%

Total Assets (`bn) 1,214 590

Market cap (`bn) 291 290

FY05-15 stock price CAGR 3.2% 16.3%

Other information Number of subsidiaries 287 45

Peak ROCE between FY05-15 FY05: 61.6% FY05: 29.1%

Lowest ROCE between FY05-15 FY15: 6.1% FY09: 10.2%

Source: Company, Bloomberg, Ambit Capital research

JSW Steel has focused on cost efficiencies in its India operations, whereas Tata Steel’s global ambitions have weighed on stock price performance

Strategy

March 23, 2016 Ambit Capital Pvt. Ltd. Page 16

Exhibit 14: Tata Steel vs JSW Steel - stock price comparison

Source: Bloomberg, Ambit Capital research. Note: In the above chart, prices are indexed to 100 from 1st Jan 2004

Complacency to competition: Within India, JSW Steel’s rapid expansion has put it ahead of Tata Steel. Tata Steel’s balance sheet was stretched due to the Corus acquisition, which is likely to have resulted in the company going slow in the Indian market, allowing JSW Steel to race past. While Tata Steel did have global ambitions with the Corus acquisition, it does not feature in the Top 10 steel producers4 of the world. ArcelorMittal is the #1 player with production of 98mt in 2014, while Tata Steel comes in at #11 with 26mt.

Exhibit 15: Market share – JSW Steel has overtaken Tata Steel in India

Source: Company, Ambit Capital research

Complacency to business environment: Between the two, JSW Steel has remained focused on its Indian operations while Tata Steel has gone global. The Indian business environment for the steel industry has remained less volatile. The key factor, however, is how both companies handled the global business environment. Tata Steel’s acquisition of Corus raised a few issues. Corus did not have raw material security and would not be able to leverage on the low-cost production base in India. The Corus acquisition was not consistent with the company’s stated vision, as seen in the Management Discussion and Analysis (MDA) of its FY05 annual report: "In the near term, the industry cost structure is likely to remain high due to shortage of coking coal and iron ore. These structural deficiencies in the steel value chain are unlikely to be resolved in the near future... the company believes that the maximum value can be created by making semi-finished products (slabs/ billets) at locations where raw

4 https://www.worldsteel.org/statistics/top-producers.html

50

150

250

350

450

550

650

Jan-

04

May

-04

Sep-

04

Jan-

05M

ay-0

5

Sep-

05

Jan-

06M

ay-0

6Se

p-06

Jan-

07M

ay-0

7

Sep-

07

Jan-

08M

ay-0

8

Sep-

08Ja

n-09

May

-09

Sep-

09

Jan-

10M

ay-1

0

Sep-

10Ja

n-11

May

-11

Sep-

11

Jan-

12M

ay-1

2

Sep-

12

Jan-

13M

ay-1

3Se

p-13

Jan-

14M

ay-1

4

Sep-

14

Jan-

15M

ay-1

5Se

p-15

Jan-

16

Tata Steel

Sensex

JSW Steel

Tata Steel: Rising commodity demand and prices coupled with low cost of raw materials drive unbridled expansion

Tata Steel: 2009 demand meltdown sharply hits European profitability

Tata Steel: Declining commodity prices work adversely for an integrated player as domestic margins shrink; European margins never recovered, whereas acquisition debt burdened the balance sheet

02468

10121416

FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15

Tata Steel JSW Steel

Market share (%)

Within India, JSW Steel overtook Tata Steel as India’s largest steel player in the past decade

The Corus acquisition was not consistent with Tata Steel’s stated vision

Strategy

March 23, 2016 Ambit Capital Pvt. Ltd. Page 17

materials are available (or can be competitively assembled), and by finishing them at locations where customers/ markets currently exists or will grow in future."

The acquisition could have partly been driven by the then prevalent wisdom in the steel sector about consolidation, with Mittal Steel (LNM Group) showing the path. But LNM was consistently following the strategy of having primary manufacturing in countries which had cheap energy or availability of raw material or both. The other reason, and the less flattering one, could be that Tata Steel was driven by hubris into making a large acquisition to match the chairman’s vision of taking the group global. In Corus, Tata Steel saw the chance to become one of the largest steel producers in the world. In its FY07 annual report, Chairman Ratan Tata wrote to shareholders: "Undoubtedly the most notable event during the year was the company's public offer to acquire 100% of the shares of Corus group plc... the acquisition of Corus has transformed Tata Steel from a domestic producer to an international steel company with global scale."

Compare this with Sajjan Jindal's statement in the corresponding FY07 annual report for JSW Steel: "The company has adopted a dual strategy. One, expanding crude steel capacity significantly, with a multi-locational presence to capitalise on the India advantage. Two, evaluating inorganic opportunities for value-added facilities in the developed economies. With this intent, we have created a subsidiary and signed a share purchase agreement to take over a Service Center in UK with a proposed investment of £3.75million.

Complacency to capital allocation: With captive iron ore mines, Tata Steel had a natural advantage over JSW Steel. Although Tata Steel and JSW Steel’s cost heads are not strictly comparable as Tata Steel records expenses on iron ore royalty, employee expenses of the mining division, etc. in other expenses whereas for JSW Steel, these form are likely to form a part of their raw material costs, there still exists a wide difference between overhead and other costs for both the companies. As the exhibit below shows, JSW Steel has an edge on other costs such as power and fuel, employee and overhead costs (due to strong focus on efficiency and conversion costs). To be fair to Tata Steel, its overheads are also high because it maintains an industrial city off its books. However, the recent collapse in iron ore prices has significantly eroded Tata Steel’s raw material integration benefits. We also highlight that in FY12 (when both companies had added brownfield capacities), JSW Steel’s capex costs, at US$545/tonne, were less than half those of Tata Steel (US$1,116/tonne), primarily due to contribution from in house staff and efficient spends by JSW Steel.

Exhibit 16: Tata Steel has lower raw material costs…

Source: Company, Ambit Capital Research

Exhibit 17: …but JSW Steel has lower overhead costs

Source: Company, Ambit Capital Research. Note: in the above chart, overheads include employee costs, power and fuel and other costs.

-

5,000

10,000

15,000

20,000

25,000

30,000

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

Tata Steel JSW Steel

`/tonne

-

5,000

10,000

15,000

20,000

25,000

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

Tata Steel JSW Steel

`/tonne

JSW Steel has an edge over Tata Steel on overhead costs

Strategy

March 23, 2016 Ambit Capital Pvt. Ltd. Page 18

Both companies have seen their RoCE shrink significantly in the past decade, as can be seen in the exhibit below. However, JSW Steel has remained in the top half of our greatness filter, while Tata Steel has slipped to the bottom half. We highlight that this is mainly because JSW Steel performs better on our Greatness Framework filters such as Gross Block, Net Sales and FA turnover & CFO, whereas Tata Steel performs badly on most of these parameters, mainly due to Corus’s high cost of operations.

Exhibit 18: RoCE of both companies has come off sharply from peaks

Source: Company, Ambit Capital research.

0%

10%

20%

30%

40%

50%

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

Tata Steel JSW Steel

Tata Steel's RoCEs were higher as its raw material integration benefited the company in a bullish commodity price environment

Tata Steel's RoCE's decline sharply due to European acquisition

Muted RoCEs for JSW Steel as well as Tata Steel as falling iron ore prices gradually wipe off Tata Steel's raw material integration benefits

Strategy

March 23, 2016 Ambit Capital Pvt. Ltd. Page 19

Case Study 2: M&M (bottom slider) vs Tata Motors (top half) Ashvin Shetty, CFA, [email protected], +91 22 3043 3285

Background: M&M is India’s largest manufacturer of utility vehicles (UVs) and tractors. Tata Motors is India’s largest manufacturer of commercial vehicles, the fourth-largest in cars and the eighth-largest in utility vehicles. Following its 2008 acquisition of Jaguar-Land Rover (JLR) for US$2.3bn, Tata Motors is also an international major in the luxury passenger cars. Both companies are among India’s oldest and largest automobile companies with multiple subsidiaries and joint ventures. Both companies are known for the professional management that runs their major divisions. The main reason why Tata Motors has stayed in the top half of great companies is its success in making the high-priced JLR acquisition work in its favor even as it retained its dominance in the Indian truck industry. M&M, on the other hand, has seen its dominance of the UV industry decline, while its multiple ventures in other auto-related areas haven’t had meaningful impact. We note that on a 10-yr basis M&M’s stock price has outperformed Tata Motors stock price. However, we believe that the JLR acquisition was a major turning point for Tata Motors. Consequently, from Jan 2009 onwards –just after the JLR acquisition in late 2008 –Tata Motors’ stock price (60% CAGR from Jan 2009 to March 2015) has beaten M&M's stock price (39% CAGR), as can be seen in Exhibit 20.

We provide a snapshot comparison of the companies in the exhibit below:

Exhibit 19: A comparative snapshot of M&M and Tata Motors

M&M Tata Motors

Financial Information (FY15) Consolidated Sales (`bn) 719,486 2,627,963

Consolidated PAT (̀ bn) 23,178 141,710

ROCE (%) 12.6% 15.8%

Total Assets (`bn) 704,791 1,289,156

Market cap (`bn) 744 1,176

FY05-15 stock price CAGR 25% 21%

Other information Major Divisions Automotive, Farm Equipment Domestic CVs, PVs and

global luxury cars Number of subsidiaries 113 76

Non-auto businesses IT, Holidays, real estate, etc. None

Peak ROCE between FY05-15 FY10: 27% FY12: 33%

Lowest ROCE between FY05-15 FY15: 13% FY09: -3%

Source: Ambit Capital research, Bloomberg. Note: RoCE is pre-tax.

While Tata Motors has turned around JLR, M&M missed out on the shift to compact SUVs

Strategy

March 23, 2016 Ambit Capital Pvt. Ltd. Page 20

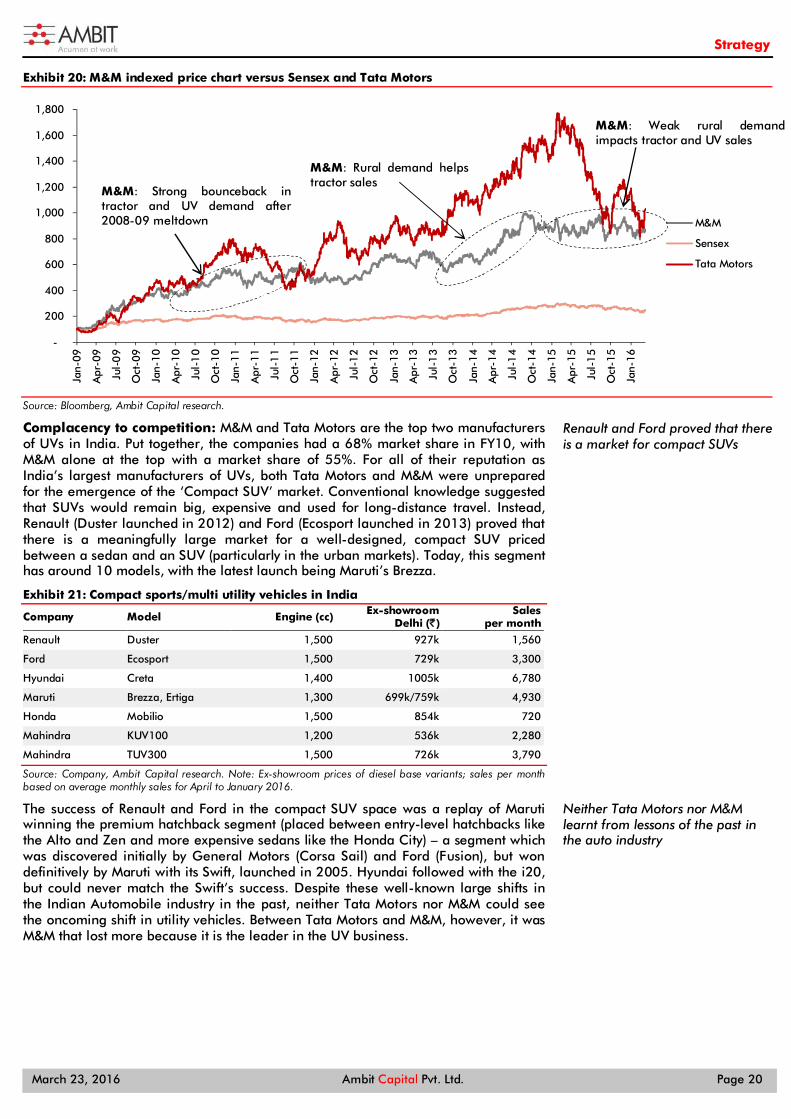

Exhibit 20: M&M indexed price chart versus Sensex and Tata Motors

Source: Bloomberg, Ambit Capital research.

Complacency to competition: M&M and Tata Motors are the top two manufacturers of UVs in India. Put together, the companies had a 68% market share in FY10, with M&M alone at the top with a market share of 55%. For all of their reputation as India’s largest manufacturers of UVs, both Tata Motors and M&M were unprepared for the emergence of the ‘Compact SUV’ market. Conventional knowledge suggested that SUVs would remain big, expensive and used for long-distance travel. Instead, Renault (Duster launched in 2012) and Ford (Ecosport launched in 2013) proved that there is a meaningfully large market for a well-designed, compact SUV priced between a sedan and an SUV (particularly in the urban markets). Today, this segment has around 10 models, with the latest launch being Maruti’s Brezza.

Exhibit 21: Compact sports/multi utility vehicles in India

Company Model Engine (cc) Ex-showroom Delhi (`)

Sales per month

Renault Duster 1,500 927k 1,560

Ford Ecosport 1,500 729k 3,300

Hyundai Creta 1,400 1005k 6,780

Maruti Brezza, Ertiga 1,300 699k/759k 4,930

Honda Mobilio 1,500 854k 720

Mahindra KUV100 1,200 536k 2,280

Mahindra TUV300 1,500 726k 3,790

Source: Company, Ambit Capital research. Note: Ex-showroom prices of diesel base variants; sales per month based on average monthly sales for April to January 2016.

The success of Renault and Ford in the compact SUV space was a replay of Maruti winning the premium hatchback segment (placed between entry-level hatchbacks like the Alto and Zen and more expensive sedans like the Honda City) – a segment which was discovered initially by General Motors (Corsa Sail) and Ford (Fusion), but won definitively by Maruti with its Swift, launched in 2005. Hyundai followed with the i20, but could never match the Swift’s success. Despite these well-known large shifts in the Indian Automobile industry in the past, neither Tata Motors nor M&M could see the oncoming shift in utility vehicles. Between Tata Motors and M&M, however, it was M&M that lost more because it is the leader in the UV business.

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Jan-

09

Apr

-09

Jul-

09

Oct

-09

Jan-

10

Apr

-10

Jul-

10

Oct

-10

Jan-

11

Apr

-11

Jul-

11

Oct

-11

Jan-

12

Apr

-12

Jul-

12

Oct

-12

Jan-

13

Apr

-13

Jul-

13

Oct

-13

Jan-

14

Apr

-14

Jul-

14

Oct

-14

Jan-

15

Apr

-15

Jul-

15

Oct

-15

Jan-

16

M&M

Sensex

Tata Motors

Renault and Ford proved that there is a market for compact SUVs

Neither Tata Motors nor M&M learnt from lessons of the past in the auto industry

M&M: Strong bounceback in tractor and UV demand after 2008-09 meltdown

M&M: Rural demand helps tractor sales

M&M: Weak rural demand impacts tractor and UV sales

Strategy

March 23, 2016 Ambit Capital Pvt. Ltd. Page 21

Exhibit 22: M&M's falling share in UVs

Source: Company, Ambit Capital research.

For Tata Motors, focus had shifted to the international business, where – to be fair – it is doing a far better job of reading the changing market. For example, Tata Motors’ JLR has plugged product gaps with the launch of the Range Rover Evoque and Jaguar XE. JLR has also been successful in China, where it has raised sales to 25% of JLR volumes in FY15 from 9.7% in FY10.

Exhibit 23: China has contributed significantly to JLR’s volume growth

Source: Company, Ambit Capital research

Complacency to business environment: Despite its various branding exercises and the success of subsidiaries (Tech Mahindra, Mahindra Holidays), M&M continues to be perceived as a 'rural' brand. This is because of its dominance in tractors and the success of its rural UVs like Bolero and Scorpio. With rural, diesel-run engines, M&M missed the shift towards petrol-run, urban SUVs. M&M's tie-up with SsangYong Motors (Korea) didn't help since SsangYong's models were expensive. Neither Renault nor Ford has a large market share in the passenger car segment and yet both beat M&M to the urban, compact SUV market.

In comparison, Tata Motors has retained its dominance of the commercial vehicle (CV) industry in India (CVs, including LCVs, account for ~75% of Tata Motor’s India revenues). It has kept pace with shifts in tonnage in the medium and heavy commercial vehicle (M&HCV) segment and led the change in the light commercial vehicle (LCV) segment. In the past, with the launch of the Ace in May 2005, Tata Motors took the sub-1 tonne market away from three-wheelers. In the car segment, Tata Motors has seen more success in the international markets (Evoque and Jaguar XE) than in the domestic segment.

30%

35%

40%

45%

50%

55%

60%

FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15

M&M's share in utility vehicles (UVs)

4.7%

9.7%11.3%

17.3%

21.4%24.2% 25.4%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

FY09 FY10 FY11 FY12 FY13 FY14 FY15

China vols (nos) - LHS China as % of total JLR

M&M’s perception as a rural brand likely made an impact on its urban market share

Strategy

March 23, 2016 Ambit Capital Pvt. Ltd. Page 22

Complacency to capital allocation: Both M&M and Tata Motors have had big ambitions and both have approached these ambitions differently. M&M has taken many small bets, while Tata Motors has taken one massive bet. Incidentally, M&M was also in the race to acquire JLR, but dropped out early.

M&M has always wanted to have a presence across the automobile industry. Thus, it ventured into highly competitive and heavily consolidated industries like commercial vehicles (top 3 players control 87% market share), cars (top 3 players control 73% market share) and two-wheelers (top 3 players control 79% market share). None of these ventures have really worked and eventually, M&M has exited from some of these, such as the car ventures with Ford and Renault and the truck venture with Navistar.

Exhibit 24: M&M's history of joint ventures Company Reason/purpose Year of JV Year of exit

Ford Ford escort car 1995 2005

Renault Logan car 2005 2010

Navistar Trucks 2005 2012

Navistar Engines 2007 2012

Jiangling Tractor Company of China Entry in China 2005 Jiangsu Yueda Yancheng Tractor Manufacturing Co. Ltd

Consolidate its position in China 2009

BAE Systems Plc Defence land systems products 2010

Source: Ambit Capital research, Company

M&M is also the holding company for its myriad investments in businesses as diverse as Information Technology and holiday packages. As a result, M&M’s investment in its subsidiaries/associates accounted for a whopping 45% of its standalone + MVML assets and about 43% of market cap.

Exhibit 25: M&M subsidiary details

Name of entity FY15 book value (̀ mn) as % of net

worth (SA + MVML) Equity Preference L&As Total

Subsidiaries Mahindra Two Wheelers 18,621 - - 18,621 9.4%

Mahindra Navistar 5,134 - - 5,134 2.6%

Mahindra Engine & Chemical 4,368 - - 4,368 2.2%

Ssangyong 21,339 - - 21,339 10.7%

Bristlecone Ltd 193 469 1,134 1,795 0.9% Mahindra Overseas Investments (Mauritius) 5,058 - 769 5,826 2.9%

Mahindra Reva Electric Vehicles 3,802 - - 3,802 1.9%

Mahindra Aerospace 2,899 50 - 2,949 1.5%

Mahindra Lifespace Developers 2,769 - - 2,769 1.4% Mahindra & Mahindra Financial Services 1,509 - - 1,509 0.8%

Mahindra Sanyo Special Steel 2,143 - - 2,143 1.1%

Others 8,581 - 87 8,668 4.4%

Associates Tech Mahindra 10,040 - - 10,040 5.1%

Mahindra CIE 5,315 - - 5,315 2.7%

Others 35 54 - 89 0.0%

Other companies 157 181 - 338 0.2% Provision for diminution in value of investments (4,325) - - (4,325) -2.2%

Total 87,639 753 1,989 90,381 45.5%

Source: Company, Ambit Capital Research.

M&M has taken many small bets, while Tata Motors has taken one massive bet

M&M has a history of forming and exiting JVs

Strategy

March 23, 2016 Ambit Capital Pvt. Ltd. Page 23

Tata Motors has also had its fair share of ambitious, expensive forays. Its investment and persistence in passenger cars in India, beginning with the Indica in the 1990s until the Nano in 2008, have not worked in dislodging Maruti as the leader. Tata Motors’ international bet, on the other hand, has worked much better. Admittedly, the JLR acquisition was too large – the price tag of US$2.3bn was equal to its shareholder equity in FY08. However, in the eight years since, Tata Motors has worked hard at making this large acquisition work in its favour. JLR revenues have registered a 28% CAGR and profits have improved to GBP2.0bn in FY15 (vs loss of GBP0.4bn in FY09). In 9MFY16, JLR’s profits were `90bn vs consolidated profits of `85.7bn. Investors have ascribed an exponentially higher value to Tata Motors’ international business compared to its more cyclical, trucks-led Indian business – thus proving, with the huge benefit of hindsight, that the JLR acquisition was worth it.

Exhibit 26: Fall in UV sales has hit M&M’s consolidated RoCE

Source: Company, Ambit Capital Research

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

0%

10%

20%

30%

40%

50%

60%

70%

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

Capital employed turnover (x) RoCE (post-tax)

Despite persistent investment in cars, Tata Motors has not dislodged Maruti as #1

Weak UV sales, increase in input costs, commodity pricing pressure impacts margins

RoCE expansion led by strong margin expansion in both tractor & UV segment

Strong UV & tractor sales offset by lower margin (commodity price increase)

Market share loss in UV; slowdown in tractor sales

Strategy

March 23, 2016 Ambit Capital Pvt. Ltd. Page 24

Case Study 3: Indian Oil Corporation (IOC; bottom slider) vs Bharat Petroleum Corporation (BPCL; top half) Ritesh Gupta, CFA, [email protected], +91 22 3043 3242

Background: Formed in 1959, Indian Oil Corporation (IOC) is India's largest oil refining and marketing company. IOC has nearly 50% market share of sale of petroleum products and 35% share of refining capacity. It owns and operates 11 of India's 23 refineries with combined refining capacity of 80.7MMTPA. Bharat Petroleum Corporation Limited (BPCL) was formed when the Indian Government nationalised Burmah-Shell Refineries in 1976. BPCL has a 21% market share in petroleum products and a 14% share of refining capacity. BPCL owns four refineries with total refining capacity of 30.5mtpa. The key difference between IOC and BPCL lies in their legacy – IOC was formed by the Indian Government to be the country’s 'national oil company', while BPCL was taken over in 1976 from multinational, Mumbai-based, Burmah-Shell (then a consortium between Royal Dutch, Shell and Rothschild). While both companies are run professionally today, BPCL started off as an MNC that was nationalised. As a result, between the two, BPCL was better at focusing on customers and had a stronger internal architecture (for example, delegation of authority).

We provide a snapshot comparison of the companies in the exhibit below:

Exhibit 27: A comparative snapshot of IOC and BPCL Financial Information (FY15) IOC BPCL

Consolidated sales (`bn) 4,501 2,426

Consolidated PAT (̀ bn) 49 48

ROCE (%) 4% 12%

Total assets (`bn) 1,313 481

Market cap (`bn) 925 582

FY05-15 stock price CAGR 5% 16%

Other information Major divisions Refining and Marketing Refining , marketing and E&P

Number of subsidiaries 9 7

Non-OMC businesses Petchem business, JV for nuclear power, Wind power, E&P

E&P, city gas distribution, Petchem expansion at Kochi

Peak ROCE between FY05-15 FY07: 13% FY05: 25%

Lowest ROCE between FY05-15 FY15: 4% FY09: 6%

Source: Company, Ambit Capital research

IOC was formed by the Indian Government to be India's 'national oil company', while BPCL was taken over in 1976 from multinational, Mumbai-based Burmah-Shell

Strategy

March 23, 2016 Ambit Capital Pvt. Ltd. Page 25

Exhibit 28: Stock price evolution for IOC vs BPCL

Source: Bloomberg, Ambit Capital research

Complacency to competition: IOC, BPCL and Hindustan Petroleum (HPCL) dominate the marketing of petroleum products in India. Their market shares have broadly been in the ratio of 46%, 29% and 26% respectively. While the sector was opened to competition, private players like Reliance and Essar have early single digit market share. Thus, oil refining and marketing remains a closed play between three state-run oil marketing companies (OMCs). BPCL has been more proactive than IOC and HPCL. For example, since 1997, BPCL has aggressive vision-based plans to provide direction. Project Cusecs, in 1997, focused on ‘customer service customer satisfaction’ and Project Destiny, in 2005, aimed at doubling turnover and quadrupling profits in the next five years. In comparison, Delhi-based IOC has been more bureaucratic, focusing on the Government’s larger objectives of expanding in rural areas, providing employment, etc. While all three OMCs have expanded their petrol pump network at a similar pace (see exhibit 29 below), BPCL has more pumps in higher-yielding urban areas (17% compared to IOC’s 9%).

Exhibit 29: Pump expansions by OMCs

Source: Company, Ambit Capital research.

IOC’s refineries are also smaller in capacity and located inland compared to BPCL’s larger refineries in coastal locations. As a result, IOC’s gross refining margins (GRMs) are more volatile than BPCL’s, but IOC also benefits from inventory gains when crude prices go up as it carries the highest inventory among the three OMCs.

0

100

200

300

400

500

600

Apr-05 Apr-06 Apr-07 Apr-08 Apr-09 Apr-10 Apr-11 Apr-12 Apr-13 Apr-14 Apr-15

IOC Brent BPCL

BPCL: Re-rating on the back of diesel deregulation

BPCL: Petrolderegulated in June 2010

IOCL: Strong GRM outlook and increasedmarketing margins

Brent: 2009 global meltdown led to crude crash beneficial for OMCs

Brent: High crude prices leading to higher under recoveries

BPCL: E&P discoveries drive valuations

BPCL: Crash in crude lead to E&P valuationsdecline

0

5,000

10,000

15,000

20,000

25,000

30,000

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

BPCL

HPCL

IOC

(Number of petrol pumps)

BPCL has been more proactive than IOC and HPCL in responding to competition

IOC’s gross refining margins (GRMs) are more volatile than those of BPCL

Strategy

March 23, 2016 Ambit Capital Pvt. Ltd. Page 26

Exhibit 30: IOC benefits from inventory gains; BPCL has less volatile GRMs

Source: Company, Ambit Capital research.

Complacency to business environment: The business environment for OMCs is tightly controlled by the Government, from subsidy sharing to expansion of marketing network and pricing of products. While subsidy on petrol and diesel was stopped in 2010 and 2014, it continues in LPG and kerosene. Within such an environment, BPCL has a better track record. When oil marketing was opened to competition in 2005, BPCL was already ready with unique branding initiatives. It was the first OMC that ran a branding campaign (Pure for Sure in early 2000s) and also the first to introduce a loyalty card (Petrocard which was, incidentally, a chip-based card as far back as 1999). At the petrol pump level, some of its customer-focused ideas include free health check-ups for the public (aimed at truck drivers who drive into the pump), with the health report being given only at the petrol pump.

Internally, too, BPCL has looked at ways to improve cost efficiencies (since revenues were determined by Government policies and crude prices). BPCL introduced computers as far back as 1981, bought its own VSAT network in 1999, and was the first OMC to arm its fuel tankers with GPS devices in 2008. By switching from SAIL to Tata Steel as suppliers for its LPG cylinders, BPCL saved `1.5bn in 2008. As a result of these efforts, BPCL is No. 2 in terms of volume market share (29%) despite having the lowest market share in terms of network (25%).

Exhibit 31: ‘Network efficiency’ of BPCL vs IOC (based on volume share/fuel pump share)

Source: Company

All those efforts speak of a culture in BPCL with a clear boundary between the company’s day-to-day operational performance and occasional interference from the Government. IOC is a Maharatna PSU and BPCL a Navratna PSU (i.e. one rung lower) and between the two, BPCL has done a better job than IOC at maintaining this boundary line.

0123456789

10

FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15

$/bbl

IOC

BPCL

1.10

1.02

1.10 1.12

1.17 1.13

1.17 1.14 1.15 1.14 1.14

0.92

0.86 0.87 0.89 0.91

0.94 0.96 0.96 0.95 0.95 0.95

0.80

0.85

0.90

0.95

1.00

1.05

1.10

1.15

1.20

FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15

BPCL IOC

BPCL has a better track record than IOC of branding and customer focus

BPCL has better network efficiency than IOC

Strategy

March 23, 2016 Ambit Capital Pvt. Ltd. Page 27

Complacency to capital allocation: Despite operating in a tight, regulated sector, BPCL’s capital allocation decisions have been superior to those of IOC. This is evident in RoCE trends in the backdrop of crude price movement (see exhibit below). Both companies saw a decline in ROCE as crude prices rose, but over the long term, lower fluctuation in GRMs has helped BPCL more than it did IOC.

Exhibit 32: RoCE trends – IOC vs BPCL

Source: Company, Ambit Capital research.

However, there are three key areas where BPCL has trumped IOC on the capital allocation front despite both companies being PSUs:

BPCL has been more aggressive in acquiring upstream assets (Bharat Petro Resources, which has 18 assets across 6 countries since it was incorporated in 2006). In comparison, IOC’s biggest upstream investment is its ownership in ONGC, which hasn’t yielded much;

BPCL built a cost-efficient refinery at Bina, Madhya Pradesh, in collaboration with Oman Oil in 2011. While IOC followed up with the Paradip Refinery, the benefits of this investment have yet to play out;

BPCL has made aggressive inroads in the gas sector with investments in Indraprastha Gas (22.5% stake) and Petronet LPG (12.5% stake); with these investments BPCL is better positioned than IOC to play India’s gas consumption story.

2%4%6%8%

10%12%14%16%18%

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

BPCL

IOCL

IOCL, BPCL: Rising underecoveries due to costlier brent bloated the capital emloyed

BPCL’s capital allocation decisions have been superior to that of IOC

BPCL’s investments in IGL and Petronet position it better than IOC to play the gas consumption story in India

IOCL generated higher GRMs, driven by inventory gains on the back of rising crude and reduced under recoveries due to petrol deregulation

Steadier GRMs for BPCL led to the RoCE growth, IOCL suffered due to higher inventory losses and investing in the Paradip refinery

Strategy

March 23, 2016 Ambit Capital Pvt. Ltd. Page 28

Case Study 4: GSK Pharma (bottom slider) vs Sun Pharma (top half) Paresh Dave, CFA, [email protected], +91 22 3043 3212

Background: GSK Pharma is among India’s oldest and largest MNC pharma companies and a subsidiary of GlaxoSmithKline UK. GSK Pharma is a leader in dermatology, vaccines and anti-parasitics. Its four largest selling products are Augmentin, Calpol, ZInetac and Eltroxin. In vaccines, GSK Pharma is the largest in India; its leading brands include Varilrix, Havrix, Rotarix, Synflorix, Cervarix and Infanrix. Sun Pharma was formed in 1983 and, from the 1990s to date, has made 19 acquisitions, the largest being Ranbaxy (US$4bn) in 2014 and Taro (~US$330mn) in 2010. Today, it is India’s largest pharma company and the fifth-largest specialty generics company in the world with the US accounting for ~50% of revenues. In India, Sun Pharma specialises in CNS, CVS, anti-infective and gastroenterology, and its main brands include Gemer, Pantocid and Susten. In the US, Sun Pharma leads in generic dermatology with a presence in anti-fungal medicines and steroids. Sun Pharma invests 6-7% of its total revenue in R&D with a primary focus on specialty generics. Apart from specialty projects, Sun is working on development of innovative projects like NCEs and NDDS (e.g., Tildrkizumab in collaboration with Merck).

While GSK Pharma is an MNC focused on India, Sun Pharma is an Indian company with a large global revenue base – to that extent, perhaps both aren’t comparable in the way we have discussed the other three case studies in this report. We highlight that the primary reason for GSK Pharma to feature in the bottom sliders (i.e., fall from the top quartile (Q1) of our greatness filter in FY05 to the bottom half in FY15; see Section 1) was deterioration in financials over FY13-FY15 following the impact of the drug price control order in May 2013. That led to deterioration on other greatness filters like improvement in net sales and PBIT margin relative to the universe median. In comparison, Sun Pharma has made its acquisitions work for it, sustaining strong financials and its position in the top half of our greatness filters over FY05-FY15.

We provide a snapshot comparison of the companies in the exhibit below:

Exhibit 33: GSK Pharma vs Sun Pharma - a snapshot GSK Pharma Sun Pharma

Financial information (FY15) Consolidated sales (`bn) 33,629 274,334

Consolidated PAT (̀ bn) 4,764 45,394

ROCE (%) 39 25

Total assets (`bn) 4,764 81,933

Market cap (`bn) 285 2000

FY05-15 stock price CAGR 15.6% 33.2%

Other information Major Products Augmentin, Calpol, ZInetac

and Eltroxin Gemer, Pantocid and

Susten Peak ROCE between FY05-15 FY05: 54% FY08: 36%

Lowest ROCE between FY05-15 FY10: 45% FY10: 19%

Source: Company, Bloomberg, Ambit Capital research

Strategy

March 23, 2016 Ambit Capital Pvt. Ltd. Page 29

Exhibit 34: GSK Pharma and Sun Pharma stock price evolution over FY05-15

Source: Bloomberg, Ambit Capital research

Complacency to competition: GSK Pharma has fared better than other MNC pharma companies (AstraZeneca, Merck, Pfizer and Sanofi) on this parameter. While other MNCs have held back new product launches, GSK Pharma kept launching products, including five patented ones from its parent, GSK UK. It has also committed to investing in a `10bn manufacturing facility in Karnataka. Thus, the parent company is fully committed to the listed entity and to the Indian market. Meanwhile, Sun Pharma scores over competition in India on better sales-force productivity, led by its strategy of efficiently using medical representatives.

Exhibit 35: Sun Pharma’s sales productivity has remained high

Source: Company, Ambit Capital research

In the US, Sun has identified complex and niche products dermatology and CNS, which face limited competition, and offers the flexibility to raise prices.

Exhibit 36: Expansion in EBITDA margin led by price increases and improvement in sales force efficiencies

Source: Company, Ambit Capital research

0

500

1000

1500

2000

2500

Jan-

05

Jun-

05

Nov

-05

Apr

-06

Sep-

06

Feb-

07

Jul-

07

Dec

-07

May

-08

Oct

-08

Mar

-09

Aug

-09

Jan-

10

Jun-

10

Nov

-10

Apr

-11

Sep-

11

Feb-

12

Jul-

12

Dec

-12

May

-13

Oct

-13

Mar

-14

Aug

-14

Jan-

15

Jun-

15

Nov

-15

10-year stock price movement

Sun Pharma

GSK Pharma

Sensex

GSK: Buyback of shares at 25% premium to CMP