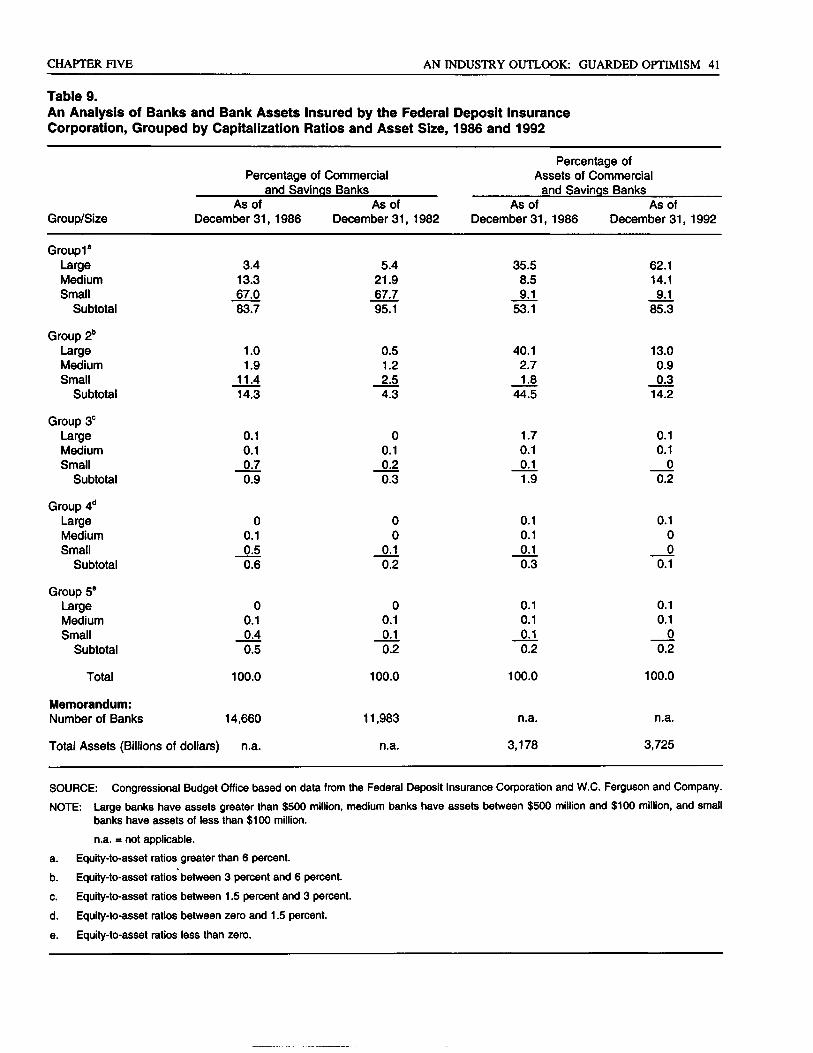

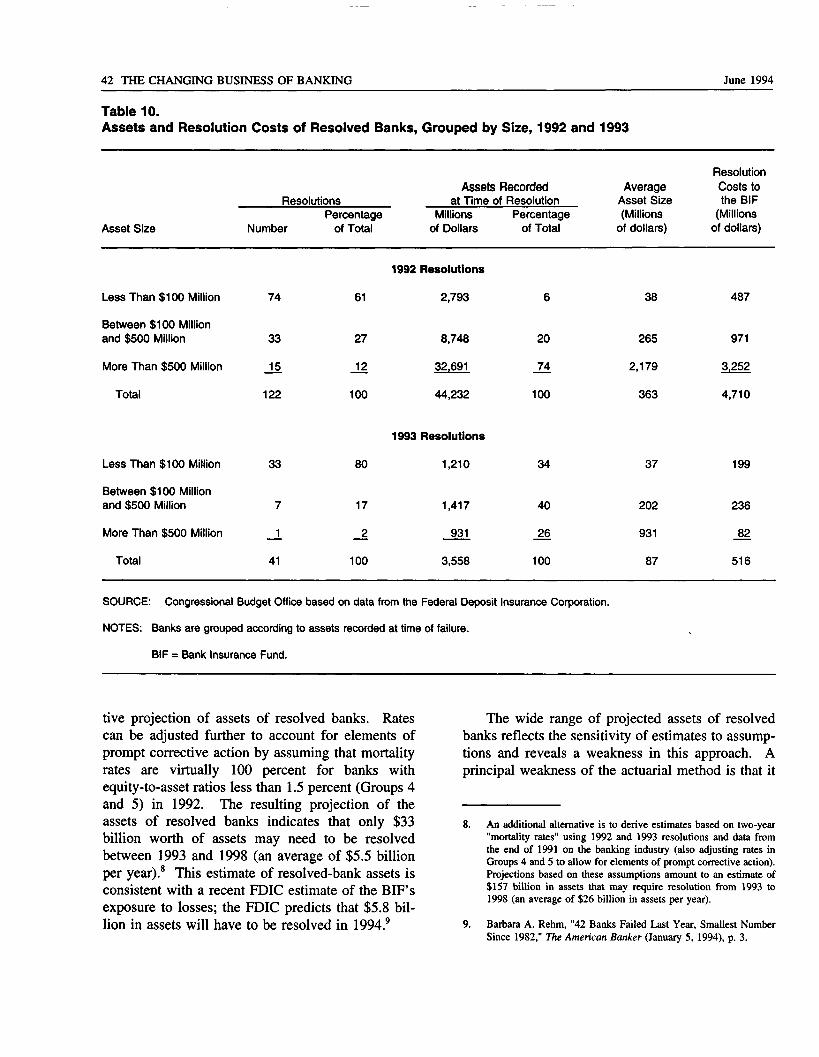

Embed Size (px)

Citation preview

CONGRESS OF THE UNITED STATESCONGRESSIONAL BUDGET OFFICE

S T U D Y

THE CHANGING BUSINESS OF BANKING:A STUDY OF FAILED BANKS

FROM 1987 TO 1992

The Congress of the United StatesCongressional Budget Office

NOTES

Numbers in the text and tables may not add to totals because of rounding.

Cover photo shows a run on a bank in New York City in 1987 (The BettmannArchive).

Preface

S ince the Banking Act of 1933 established the Federal Deposit Insurance Corpo-ration, the FDIC has resolved about 2,000 banks. More than 1,000 of these reso-lutions occurred in the six years between 1987 and 1992. The dramatic increase

in the number and costs of resolutions in this period, coming on the heels of the savingsand loan crisis, raises questions about the long-term condition of the banking industryand the Bank Insurance Fund.

This study, which was prepared in response to a request from the Senate Commit-tee on Banking, Housing, and Urban Affairs, examines major factors contributing tobank failures during this six-year period and why these failures resulted in such extraor-dinary resolution costs. It examines bank-specific factors such as asset quality andportfolio composition, as well as more general structural and economic conditions affect-ing the industry. In keeping with the mandate of the Congressional Budget Office(CBO) to provide objective analysis, this study makes no recommendations.

Patrice L. Gordon and Thomas Lutton (currently at the Office of the Comptrollerof the Currency, Bank Research Division) wrote the study, under the supervision of JanPaul Acton and Elliot Schwartz of CBO's Natural Resources and Commerce Division.Aaron Zeisler, Michael Crider, and Veronica French provided research assistance. KimKowalewski, Bruce Vavrichek, Robin Seiler, Jim Hearn, Mark Booth, and Ron Feldmanof CBO offered comments and helpful suggestions. The authors wish to thank GeorgeKaufman, George French, James Thompson, James Earth, R. Dan Brumbaugh, RobertLitan, Philip F. Bartholomew, Larry Mote, Harold A. Black, and Haluk Unal for theirconstructive comments.

Sherwood D. Kohn edited the manuscript, and Christian Spoor provided editorialassistance. Gwen Coleman and Angela Z. McCollough produced the numerous drafts.With the assistance of Regina Washington and Martina Wojak-Piotrow, KathrynQuattrone prepared the study for publication.

Robert D. ReischauerDirector

June 1994

Contents

ONE

TWO

THREE

FOUR

FIVE

SUMMARY

INTRODUCTION

Bank Resolutions in HistoricalPerspective 2

The Economic Costs of BankFailures 6

THE STRUCTURAL TRENDS AND ECONOMICCONDITIONS UNDERLYINGBANK RESOLUTIONS

Enhanced Competition andFinancial Innovation 8

Macroeconomic Conditions, RegionalDisparities, and Asset Losses 14

THE ROLE OF MANAGEMENT ANDINSTITUTION-SPECIFIC FACTORSASSOCIATED WITH RESOLUTIONS

XI

1

19

Management and Bank FailureA Comparison of Resolved and

Surviving Banks 22

19

BANK RESOLUTIONS AND THE COSTSOF RESOLUTION

Resolution Costs as Estimatesof BIF Losses 27

Resolution Costs andRegulatory Effectiveness 29

FDICIA and Prompt Corrective Action 34

AN INDUSTRY OUTLOOK: GUARDEDOPTIMISM

The Exposure of the Bank InsuranceFund to Losses from Bank Resolutions 37

Reforms in FDICIA and SomeRemaining Policy Issues 43

21

31

vi THE CHANGING BUSINESS OF BANKING June 1994

APPENDIXES

A Methods of Evaluating the FinancialCondition of Banks 49

B Types of Resolutions: Data on ResolutionCosts and Bank Resolutions 53

C A Simulation of Embedded Costs 63

CONTENTS vii

TABLES

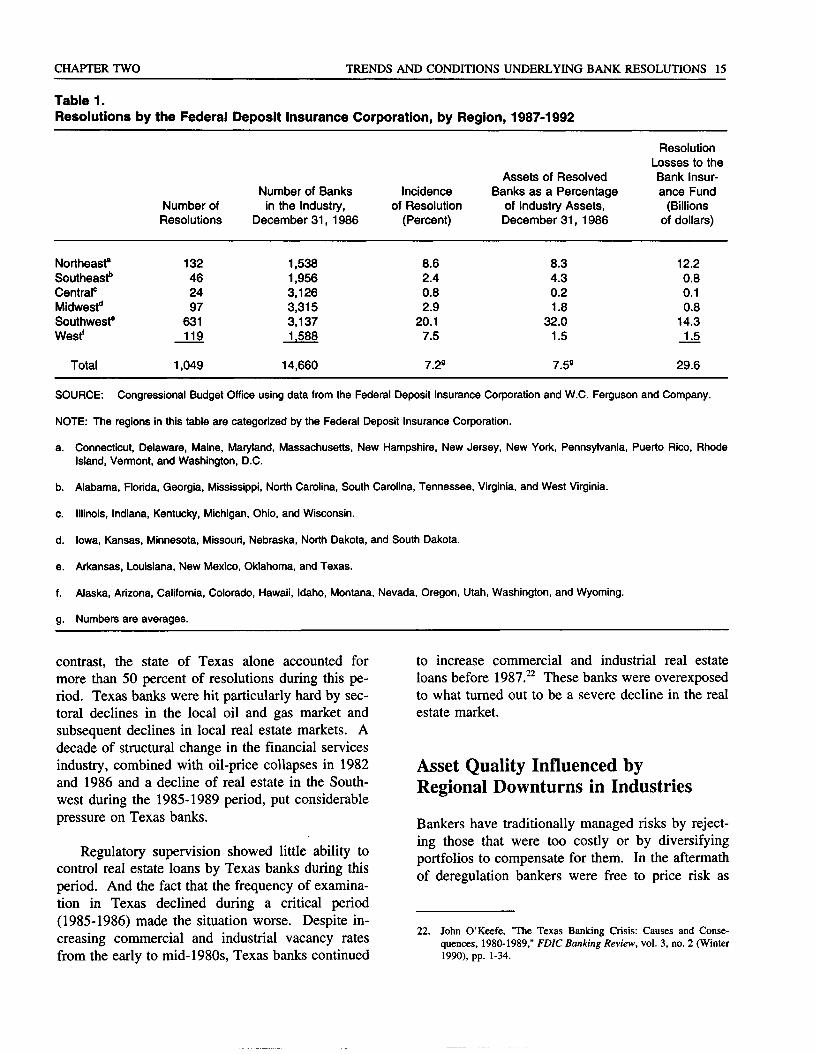

1. Resolutions by the Federal Deposit InsuranceCorporation, by Region, 1987-1992 14

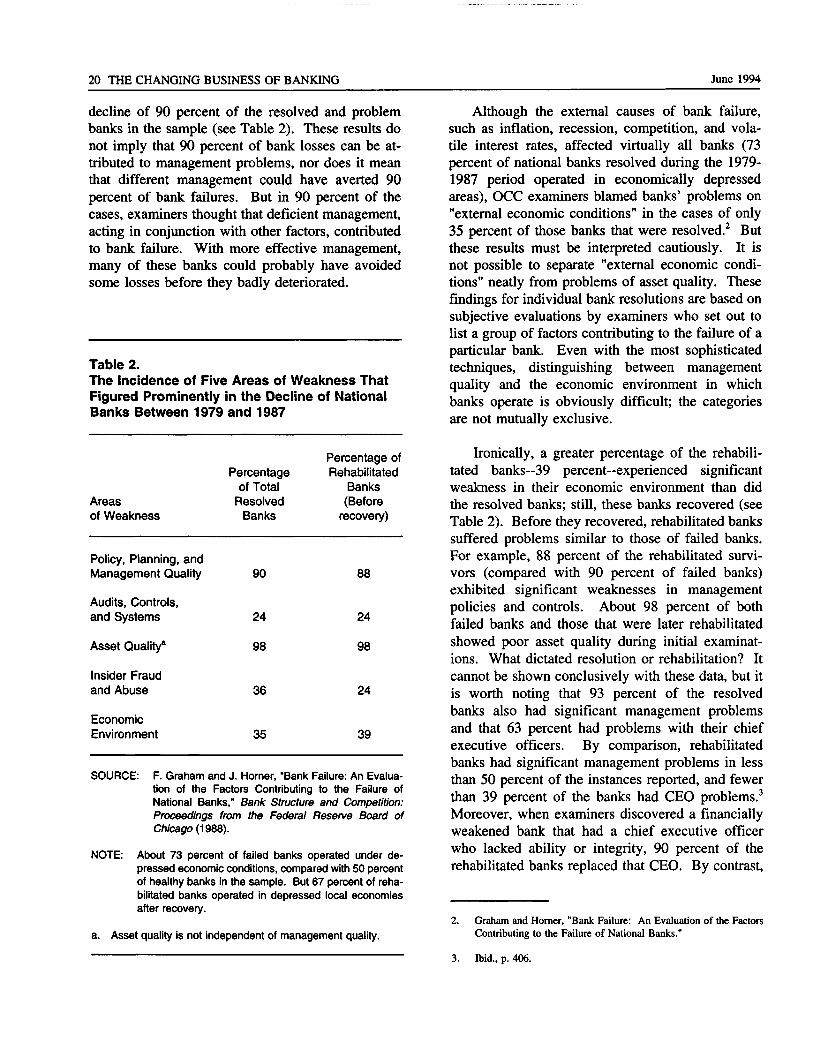

2. The Incidence of Five Areas of Weakness ThatFigured Prominently in the Decline ofNational Banks Between 1979 and 1987 20

3. Internal Management Factors Contributing tothe Failure of National Banks ResolvedBetween 1979 and 1987 21

4. A Comparison of Portfolio Characteristicsof Small Resolved and Surviving Banks,1987-1989 22

5. Assets, Capitalization, and Profitability: AComparison of Historical Characteristics ofSmall Resolved and Surviving Banks, 1987-1989 23

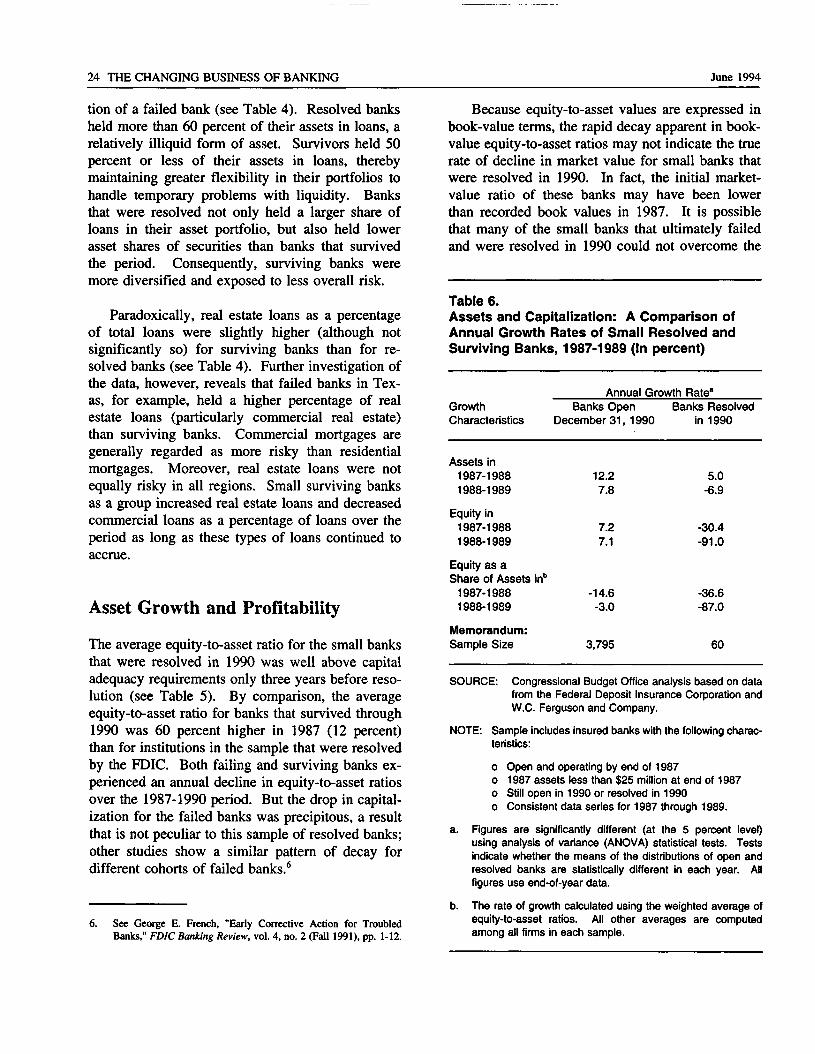

6. Assets and Capitalization: A Comparison ofAnnual Growth Rates of Small Resolved andSurviving Banks, 1987-1989 24

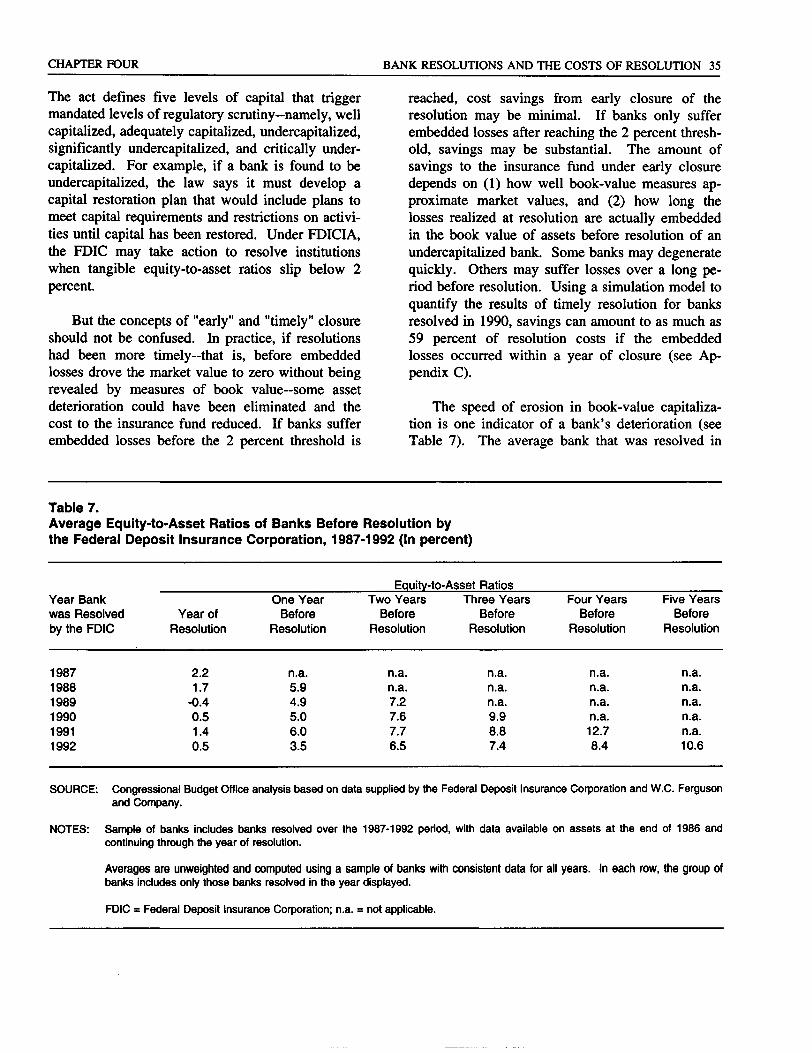

7. Average Equity-to-Asset Ratios of BanksBefore Resolution by the Federal DepositInsurance Corporation, 1987-1992 35

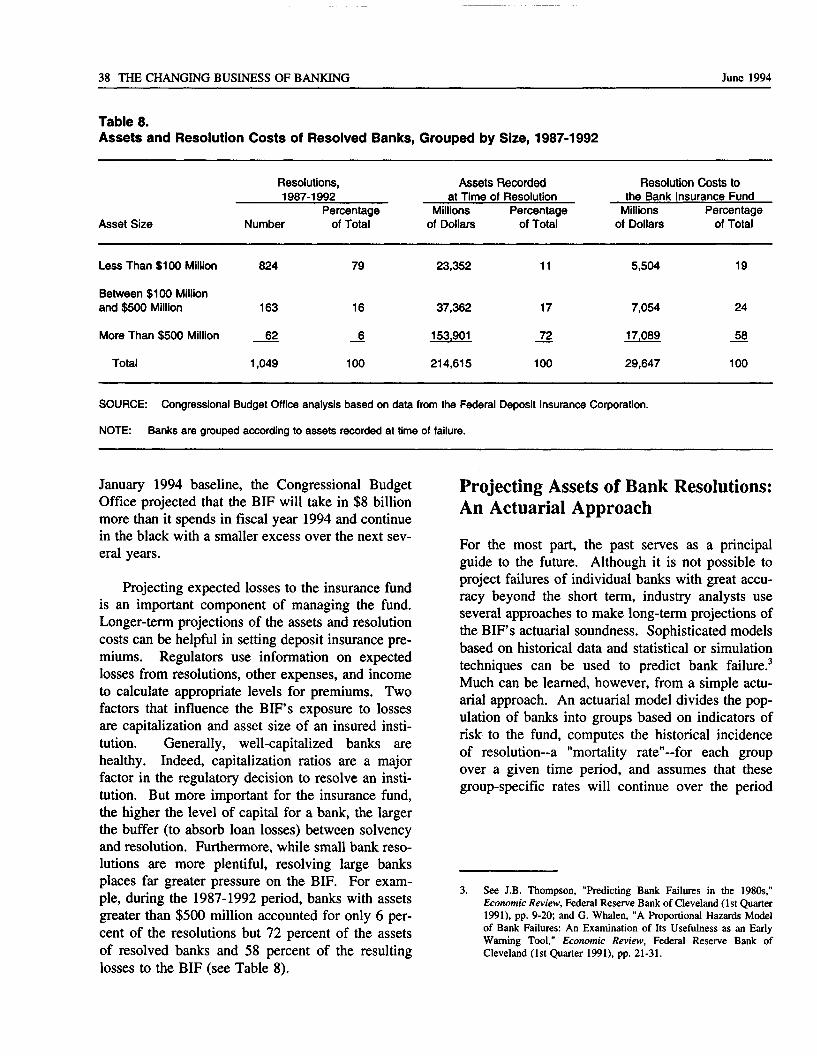

8. Assets and Resolution Costs of ResolvedBanks, Grouped by Size, 1987-1992 38

9. An Analysis of Banks and Bank AssetsInsured by the Federal Deposit InsuranceCorporation, Grouped by CapitalizationRatios and Asset Size, 1986 and 1992 41

10. Assets and Resolution Costs of ResolvedBanks, Grouped by Size, 1992 and 1993 42

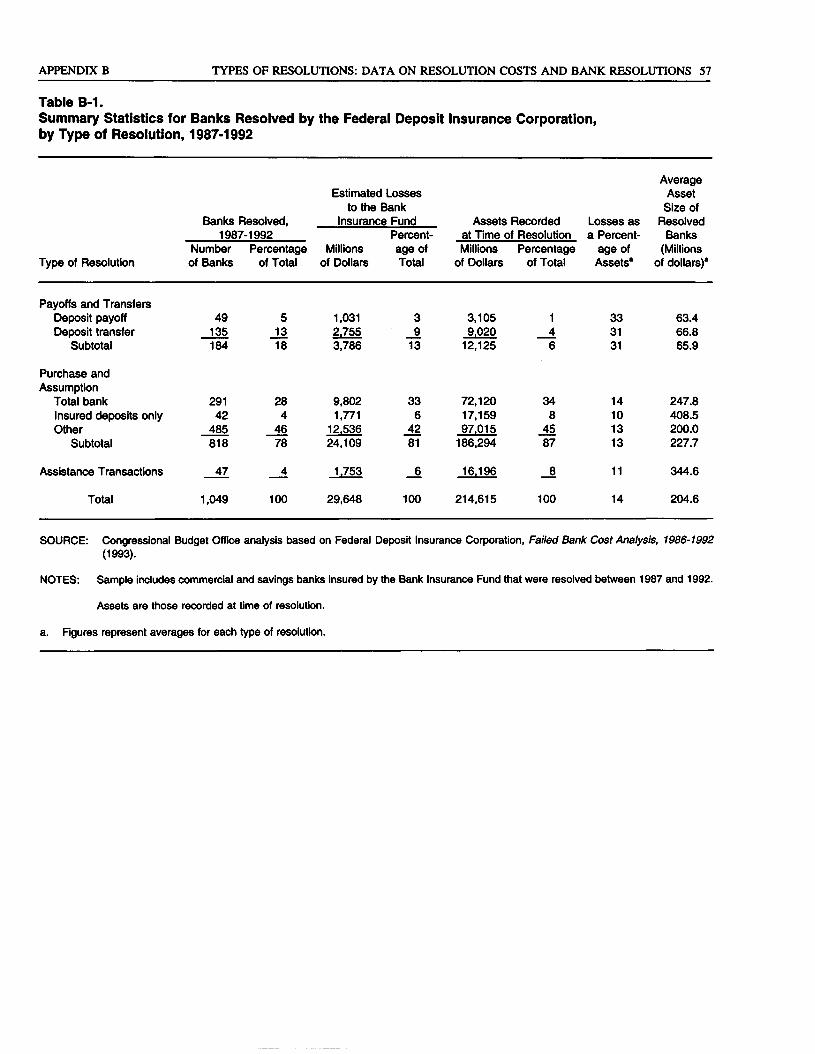

B-l. Summary Statistics for Banks Resolved by theFederal Deposit Insurance Corporation, byType of Resolution, 1987-1992 57

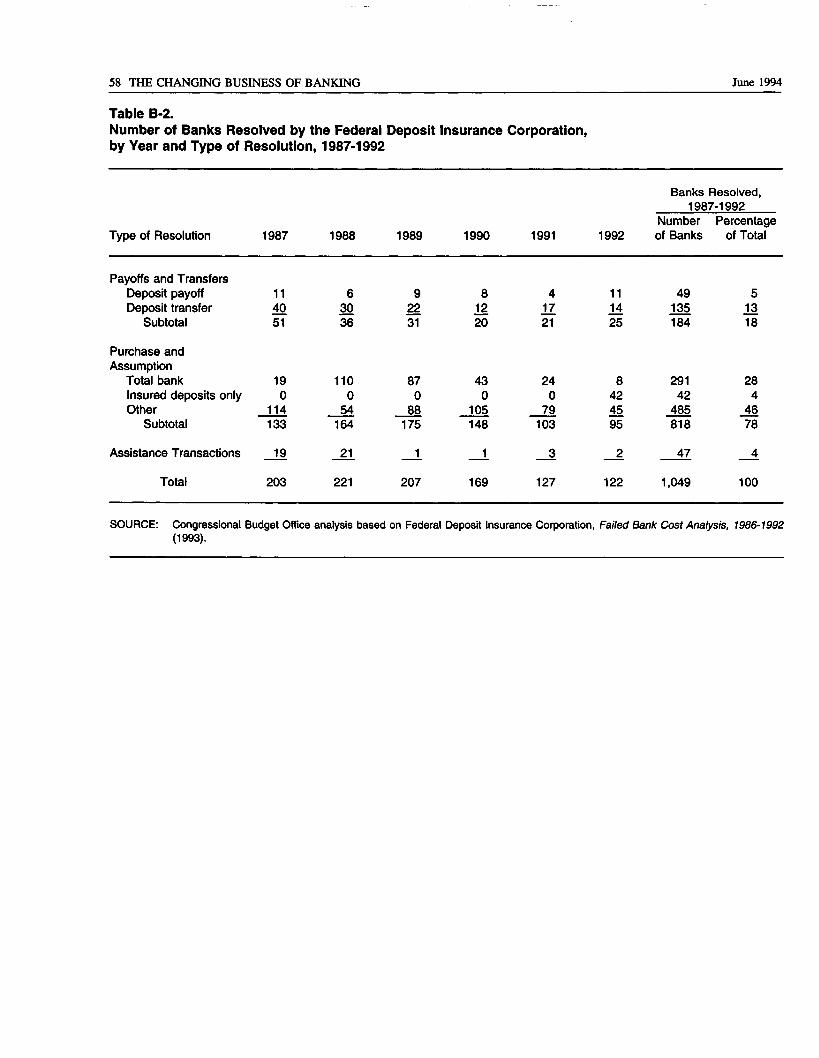

B-2. Number of Banks Resolved by the Federal DepositInsurance Corporation, by Year and Type ofResolution, 1987-1992 58

viii THE CHANGING BUSINESS OF BANKING June 1994

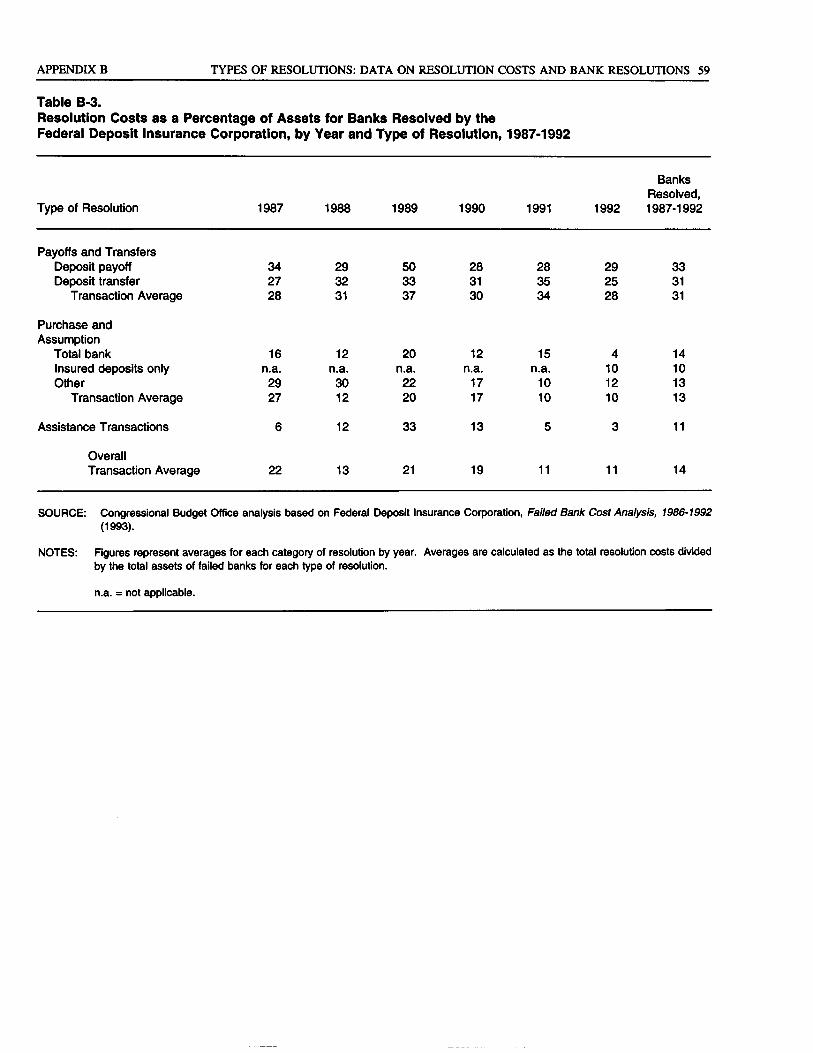

B-3. Resolution Costs as a Percentage of Assetsfor Banks Resolved by the Federal DepositInsurance Corporation, by Year and Typeof Resolution, 1987-1992 59

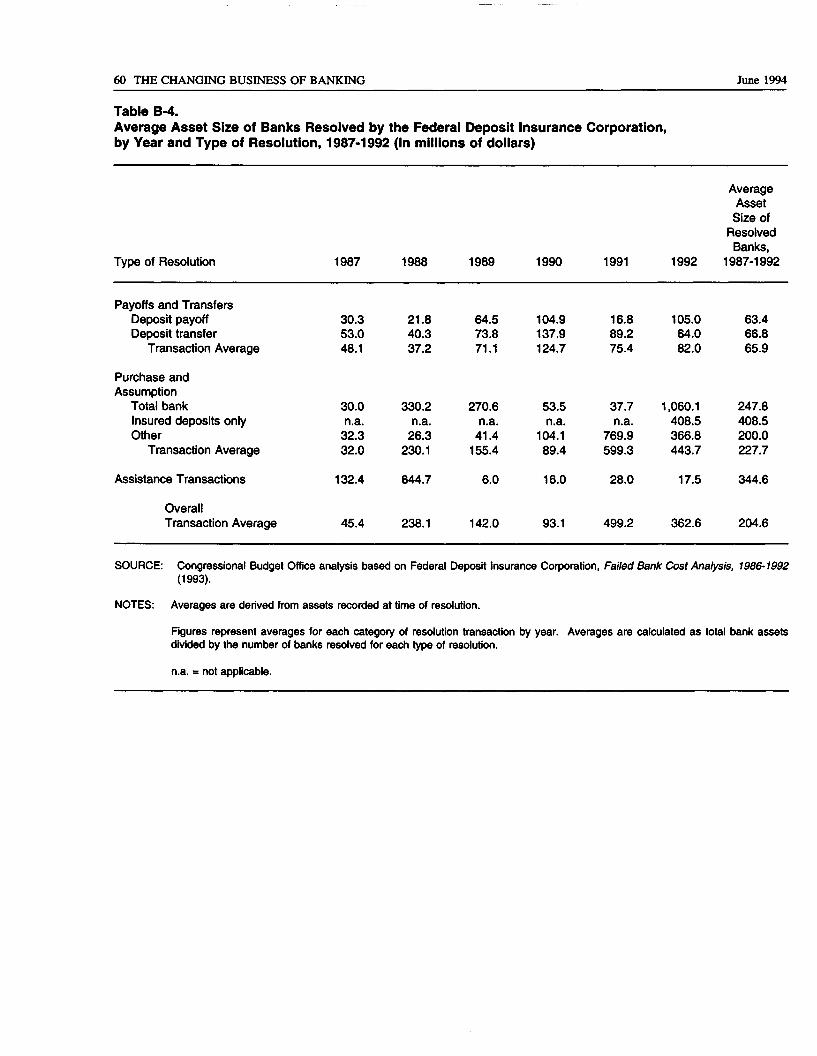

B-4. Average Asset Size of Banks Resolved by theFederal Deposit Insurance Corporation, byYear and Type of Resolution, 1987-1992 60

B-5. Total Assets of Banks Resolved by the FederalDeposit Insurance Corporation, by Year andType of Resolution, 1987-1992 61

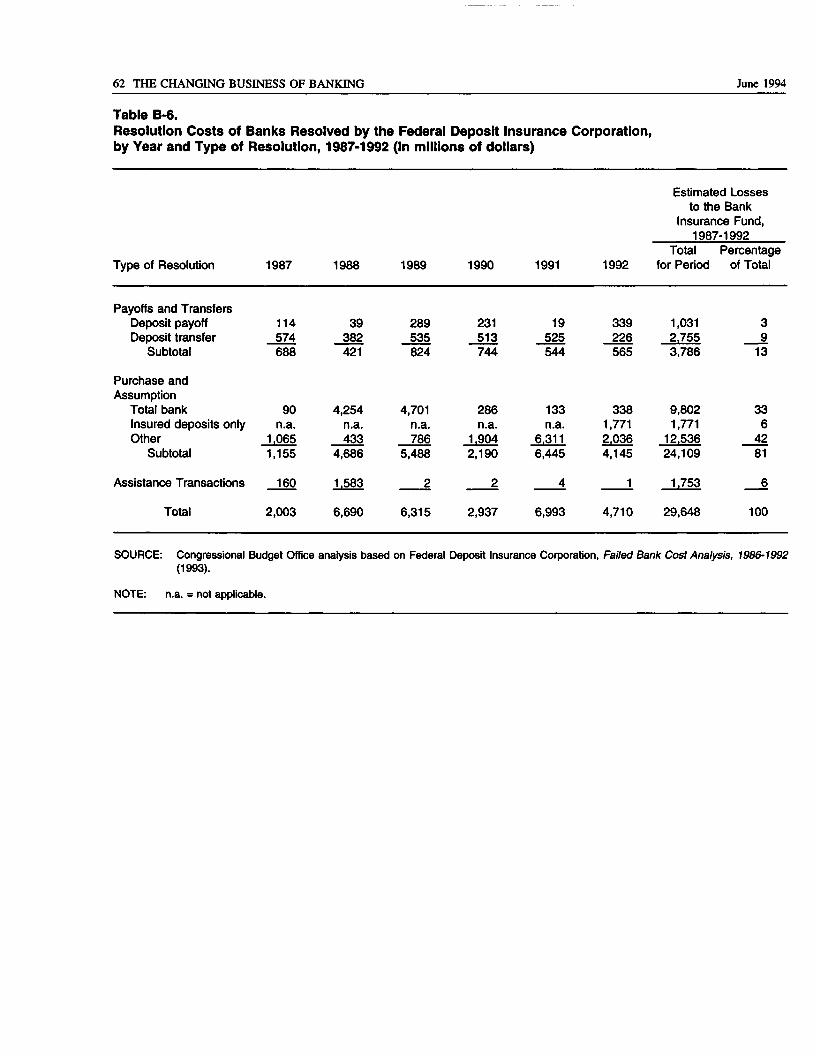

B-6. Resolution Costs of Banks Resolved by the FederalDeposit Insurance Corporation, by Year and Typeof Resolution, 1987-1992 62

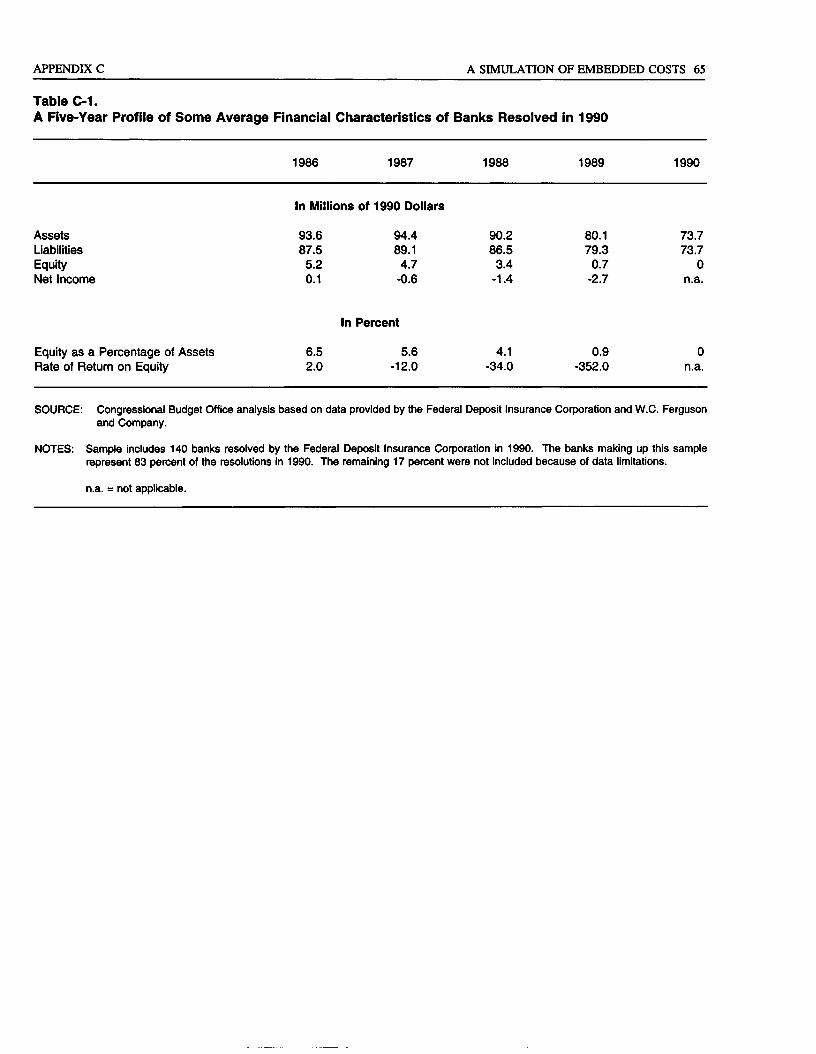

C-l. A Five-Year Profile of Some Average FinancialCharacteristics of Banks Resolved in 1990 65

C-2. Resolution Costs and Estimated Embedded LossesUsing Average Characteristics of 1990Resolutions 66

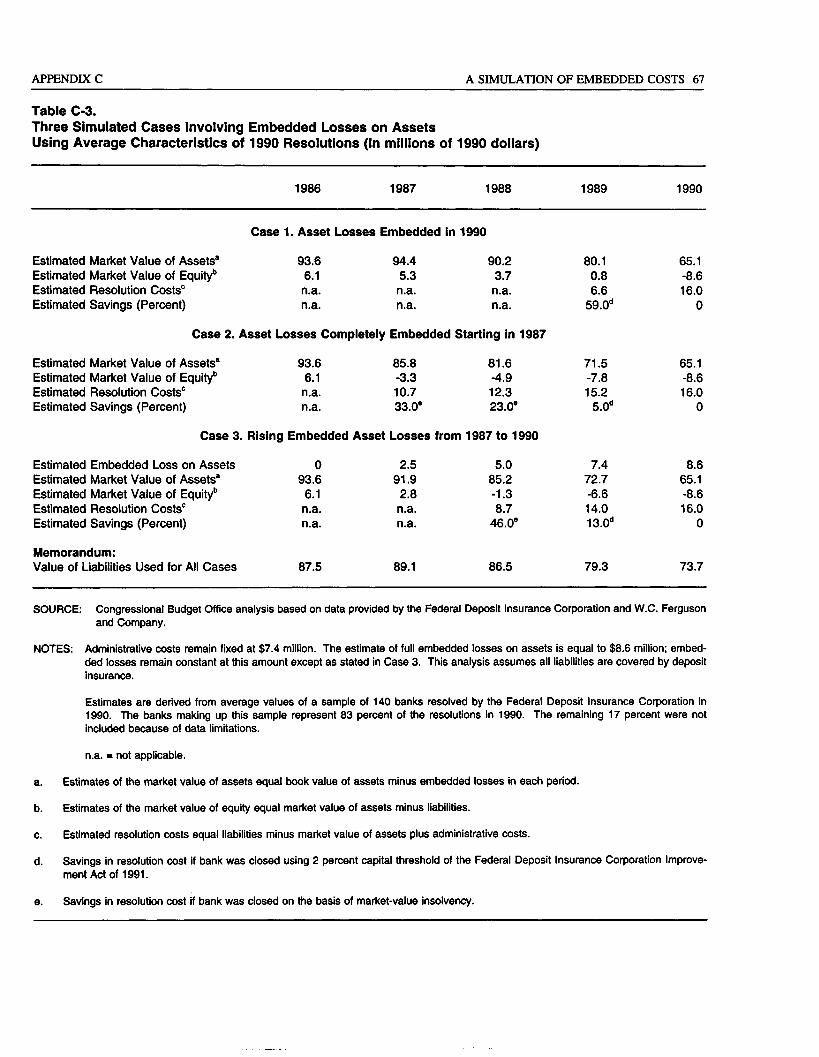

C-3. Three Simulated Cases Involving Embedded Losseson Assets Using Average Characteristics of1990 Resolutions 67

FIGURES

1. Average Annual Number of Bank Failures forSelected Periods Between 1900 and 1992 2

2. Number of Bank Resolutions, 1934-1992 4

3. Average Resolution Costs for Resolved Banks,1934-1992 4

4. Composition of Commercial and Savings BankLiabilities, 1960-1992 9

5. Composition of Commercial and Savings BankLoans and Leases, 1960-1992 10

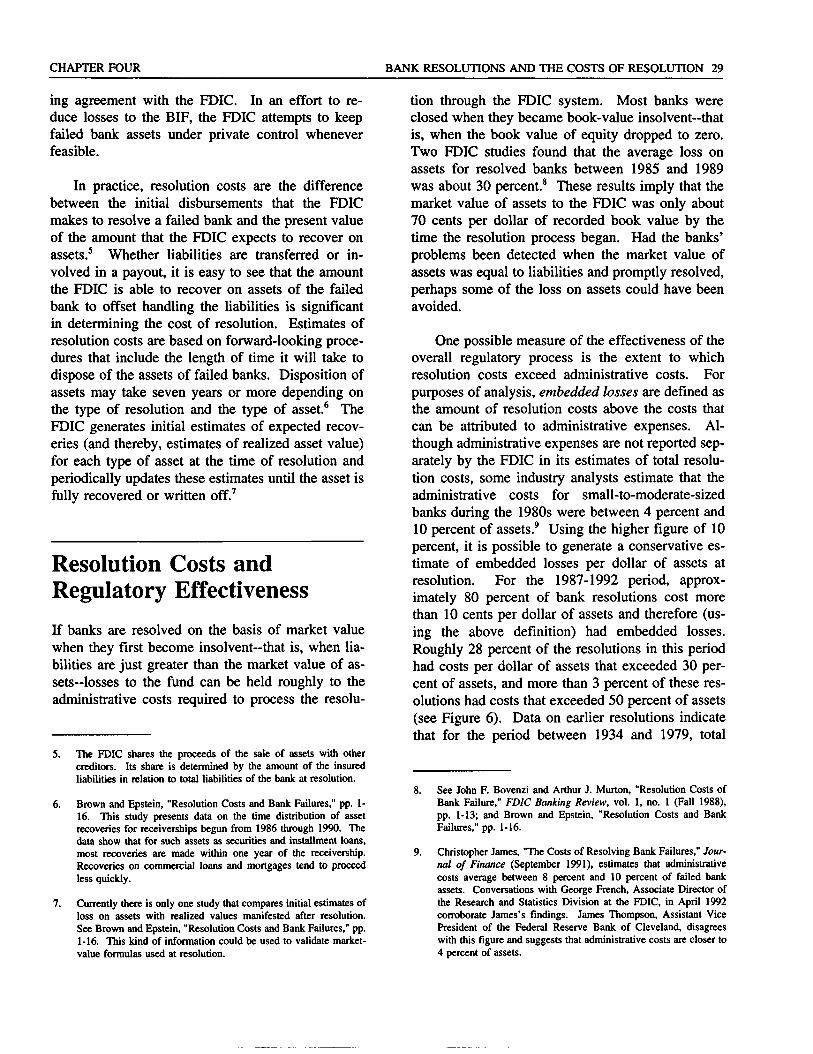

6. Distribution of Resolved Banks Grouped byRatios of Resolution Costs to Bank Assets,1987-1992 30

CONTENTS ix

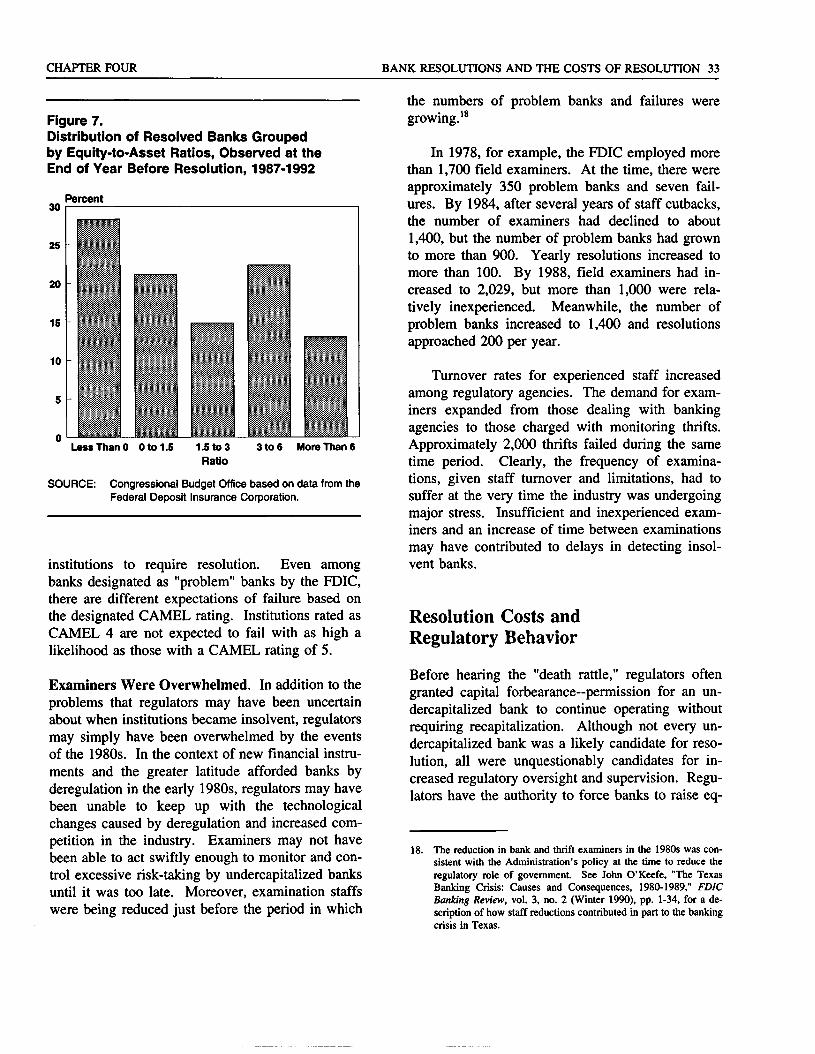

7. Distribution of Resolved Banks Grouped byEquity-to-Asset Ratios, Observed at the Endof Year Before Resolution, 1987-1992 33

BOXES

1. The Basics of Bank Regulation and Examination 31

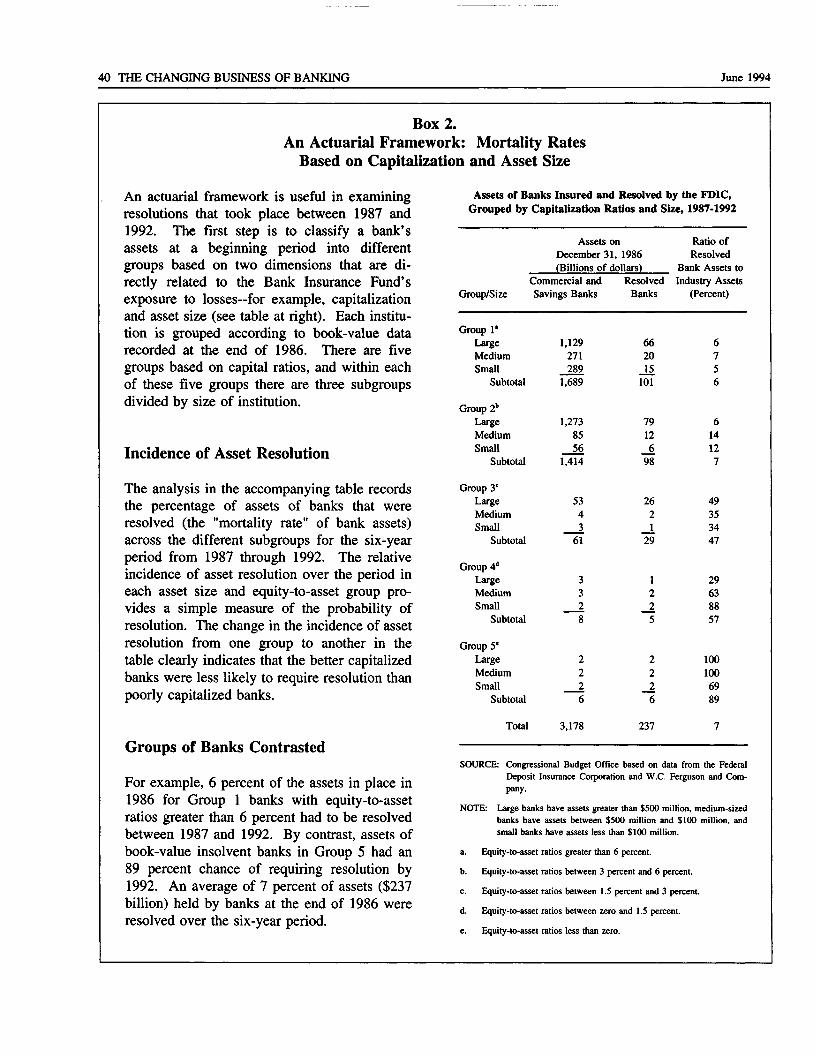

2. An Actuarial Framework: Mortality RatesBased on Capitalization and Asset Size 40

Summary

T he history of banking in the United States islike a volatile stock market, characterizedby wide fluctuations in profitability and

decline. In the 35 years between 1885 and 1920,the number of U.S. banks tripled from 10,000 to30,000. It took only five years-from 1929 through1933-for the number of banks in the industry toshrink by one-half. This period of rapid declinewas associated with deteriorating industries, de-pressed regions, and to some extent with runs onbanks. Concern about the soundness of the industrywas a catalyst for the Banking Acts of 1933 and1934. These acts restricted competition and estab-lished the deposit insurance system.

The 1980s was also a turbulent decade for theU.S. banking industry. It ushered in intense domes-tic and international competition in financial mar-kets. A peculiar confluence of economic forces,technical innovation, and deregulation contributed toan unprecedented number of bank failures and sub-sequent resolutions during the late 1980s and early1990s. During the six years from 1987 through1992, more than 1,000 bank resolutions (commercialand savings banks) cost the Bank Insurance Fund(BIF) about $30 billion, exhausting an $18 billionreserve in the deposit insurance system. The sheernumber of bank failures and the extensive losses tothe deposit insurance fund during the 1987-1992period dwarfed the experience of the previous fivedecades. In conjunction with a crisis in the thriftindustry, the bank failures and losses caused by thebanks' resolutions brought about the first real chal-lenge to the deposit insurance system.

The banking crisis may indeed be over. Butwhat were the underlying causes of the failures, and

why were the costs of resolving these banks somuch higher than those in previous periods? Someof the factors associated with bank failures occur-ring over this six-year period could reemerge andonce again expose some banks to increased risk ofloss. Evidence from this turbulent period may bevaluable in assessing the condition of the industryas it undergoes continued structural change andconsolidation.

Why Did Banks Fail?

Banks failed for many reasons. Local market andmacroeconomic influences, the regulatory environ-ment, and management performance all contributedto the tendency of banks to fail and to the size ofassociated losses. Surveys reveal that fraud andabuse also contributed to failure, but those factorswere primary causes in only 25 percent of the cases.Most banks failed because a significant portion oftheir asset portfolios defaulted; in other words, thesebanks made what turned out to be bad loans.

Many of the problems with loans that becameapparent after the mid-1980s probably originated inthe late 1970s and early 1980s. Two dramaticsurges in inflation during the 1970s changed thebusiness of banking. Both inflationary periods ledto sharp rises in commodity prices, mercurial stockand bond prices, and particularly volatile interestrates. Initially, market interest rates climbed whileregulated interest rates on deposits remained cappedat 5.25 percent. Although ceilings on deposit inter-est rates had been in place for decades, banks had

xii THE CHANGING BUSINESS OF BANKING June 1994

still been able to attract depositors. But once mar-ket interest rates exceeded the caps, depositors be-gan to look elsewhere. By the early 1980s, disinter-mediation—the diversion of savings from accountshaving low interest rates to direct investment inhigh-yielding instruments-had become a problem.

The double-digit interest rates available onmoney market mutual funds, Treasury securities,and other nondepository financial instruments madethem popular alternatives to banks and thrifts.Banks could not legally compete with the productsor rates offered by other financial institutions. Afteran outcry from banks and thrifts, regulated interestrate ceilings were phased out over a six-year period,starting in 1980 with the Depository InstitutionsDeregulation and Monetary Control Act of 1980(DIDMCA). Banks were also permitted to offer abroader array of financial products. AfterDIDMCA, banks were better able to compete withother financial intermediaries for depository funds,but much of the damage was already done. At thebeginning of the 1980s banks were in a weakenedstate.

Advances in computers, telecommunications,and other forms of technology greatly improved thedissemination and flow of financial information.Competition by other banks, thrifts, money marketfunds, and other nonbank financial institutions in-tensified. Bank earnings and rates of return fromtraditional activities suffered throughout the 1980s.By the end of the 1980s, new financial instrumentsproliferated. Banks became more dependent on off-balance sheet activities such as interest rate swaps,loan commitments, and future markets for exchangerates for income. Shares of assets of nonbank fi-nancial institutions grew dramatically. Meanwhile,the share of financial assets held by banks decreasedsteadily throughout the 1980s.

Competition took many forms, but banks—espe-cially big banks with assets greater than $10 billion—lost ground in major markets, including that forlarge industrial borrowers with excellent creditratings. These "blue-chip borrowers," formerly themainstays of bank lending, defected for more favor-able lending rates in commercial paper markets.Banks had to adjust their asset portfolios. Theycould no longer look to less risky commercial and

industrial loans to bolster their earnings; the devel-opment of the commercial paper market had madethese loans more difficult to obtain. As a result,commercial and industrial loans declined as a per-centage of bank portfolios.

Faced with fewer investment alternatives, somebanks sought refuge in higher-risk assets, includingloans to developing countries and energy invest-ments in the 1970s and 1980s. When oil prices felland defaults on loans to developing countries in-creased in the 1980s, banks that had not properlydiversified lost large portions of their asset portfo-lios. In some cases, banks turned to highly lever-aged transactions and junk bonds in an effort tobolster sagging earnings. The subsequent softeningof these markets resulted in substantial losses inbank earnings and equity. Rates of return for manybanks dropped far below past averages. Bad loansbegan to surface, and provisions for bad loans be-gan to overwhelm the income on good loans. Re-turns on equity in some of the largest banks wereless than returns on government bonds.

Analysis of industry data reveals a strong pat-tern of higher-than-average bank failure associatedwith regions experiencing temporary economicdifficulties. Banks tied to regional markets sufferedfrom economic declines in energy, real estate, andagriculture. For example, bank failures in theSouthwestern states can be attributed in part toregional collapses in oil and real estate prices.Texas banks were hit particularly hard by sectoraldeclines in the local oil and gas market and subse-quent slumps in local real estate markets. Real-estate-related difficulties spread to the Northeast, theSoutheast, and finally the West Coast. Bank fail-ures in the West and Midwest regions can be linkedto a downturn in the agriculture sector during themid-1980s.

Although many of the problems that beset bankswere externally induced, the primary responsibilityfor bank failures rests squarely on the shoulders ofbank managers and boards of directors. This re-sponsibility does not negate ineffective regulation orunforeseen economic developments as causes offailure, but the bank manager is the agent whoreacts to economic conditions and the regulatoryenvironment. Some managers made mistakes be-

SUMMARY Xlll

cause they reacted incorrectly to a barrage of un-usual factors. In some cases, managers simplyfailed to diversify asset portfolios and boards ofdirectors did not insist on reasonable loan practices.Managers of failed banks often pursued aggressiveloan policies without reasonable precautions againstdefault. As a result, many bank managers whofailed to deal effectively with increased competitionand adverse economic shocks presided over thedemise of their institutions.

A comparison of the financial characteristics ofbanks that failed and banks that survived is reveal-ing. It shows that some of the traits that distinguishresolved and surviving banks began appearing in theinstitutions' balance sheets years before they failed.Industry data show that surviving banks were morelikely to have higher equity-to-asset ratios (mea-sured by book value) and lower loan-to-assets ratiosthan resolved banks had even three years beforetheir resolution. Even with the limited data avail-able, it is possible to infer that those banks thatsurvived this period did so by holding more liquidassets, managing modest growth in diversified as-sets, maintaining a suitable buffer of capital, andcomplying with regulatory requirements. Banks thatfailed and were resolved experienced dramaticlosses in book-value equity-to-asset ratios withinone year of resolution—a relatively short period oftime. Whatever caused the book-value equity ratiosto fall so rapidly, the event has implications forregulatory efficiency in recognizing losses on assetsand carrying out timely closure.

All resolutions were marked by one importantregulatory decision—banks that were resolved couldnot raise capital. Regulators did not resolve a bankif it proved that it was capable of raising capital.Capital is simply defined as the difference betweenassets and liabilities—the equity held at book value.The act of raising additional capital is an act ofvalidation—a market affirmation of the continuedexistence of a bank. Weakly capitalized banks mayraise capital either by increasing income for retainedearnings or by otherwise raising capital in the equitymarket. Surviving banks generated positive incomeand raised capital when it was required; failed bankswere unable to do so.

Why Did ResolutionsCost So Much?

During the 1980s, regulators faced not only anincrease in the number of bank failures requiringresolution, but also an increase in the average costof resolving a bank. The cost to the BIF of resolv-ing a bank depends on the value of liabilities cov-ered by deposit insurance and the value of assetsthat can be recovered during the resolution process.Covered liabilities mostly include insured deposits.A major factor determining the cost of resolution isthe loss on assets-that is, the difference between thebook value of assets at the time of resolution andthe net value that can be recovered if the assets aresold. As the recoverable value of assets decreases,the cost of resolving an institution increases. Ifbanks are resolved when they first become insolventon the basis of market value—that is, when liabilitiesare just greater than the market value of assets-losses to the fund can be held roughly to the admin-istrative costs required to process the resolutionthrough the FDIC system.

The average loss on assets for resolved banks inthe late 1980s was about 30 percent. In the 1980s,most banks were closed when they became book-value insolvent-that is, when the book value oftheir equity dropped to zero. When asset values aredeclining, banks will generally be insolvent on amarket-value basis before they display book-valueinsolvency. Because there was such a drain on theinsurance fund, recognition of bank insolvency anda timely exit policy for insolvent institutions becamea critical part of regulatory effectiveness.

The fact that losses were, on average, higher inthe 1980s than they were in the previous periodmay indicate diminished regulatory effectiveness.Two factors could have contributed to diminishedeffectiveness. First, examiners may not have beenable to identify potential failures early enough topermit regulators to avoid additional losses. Al-though bank examiners can usually determine whichbanks are financially distressed, judging when abank first becomes insolvent is very difficult.

xiv THE CHANGING BUSINESS OF BANKING June 1994

Also, during this interval an extraordinary numberof banks failed over a short period of time. Second,examiners may have identified severely undercapi-talized banks, but either practiced a policy of for-bearance or were unable to elicit compliancethrough supervision.

The process of classifying a bank as economi-cally incapable of surviving before it reaches bookvalue insolvency is fraught with uncertainty. Regu-lators can make two kinds of errors in classifying abank as insolvent. First, they may classify a bankthat is really functional as insolvent. In the secondcase, regulators may classify a bank that is reallyinsolvent as functional.

In the history of the insurance fund, the twoerrors have not been equally important. Since 1934,regulators have rarely resolved a bank that wassolvent by book-value measures. During the 1980s,regulators usually preferred to err on the side ofleaving a financially distressed bank operating ratherthan close a functional bank. The costs associatedwith behaving as though a bank is functional whenit is not can appear eventually as embedded coststhat show up as relatively high resolution costs perdollar of assets. Regulators also faced legal andeconomic pressures to avoid closing a bank before itbecame book-value insolvent. To close such institu-tions meant that the regulators would have had toendure immediate vocal disapproval from thosedirectly affected-owners of banks, boards of direc-tors, local communities, and their representatives.Beneficiaries of timely closures were conspicuouslysilent and typically unaware of the costs of regula-tory delay.

Along with the problem that regulators mayhave been uncertain about when an institution be-came insolvent, regulators may have been simplyoverwhelmed by the events of the 1980s. In thecontext of new financial instruments and the greaterlatitude afforded banks by deregulation in the early1980s, regulators may have been unable to keep upwith the technological changes caused by deregula-tion and increased competition in the industry. On-site examinations, conducted to assess the financialhealth of an institution, were less frequent (as aresult in part of budget cutbacks) at a time whenfinancial markets were changing faster than at virtu-

ally any other point in the nation's history. Withoutrelatively current assessments from examiners, regu-lators had to rely solely on quarterly call reportsbased on book-value data. Book-value data basedon past transactions can overstate the current marketvalue of a financially weak institution. Whenevents in the market affect the value of an institu-tion, book-value accounting does not reflect achange in value. Without data based on examina-tion and the true value of assets, regulators couldnot easily recognize asset losses and bank in-solvency.

A policy of forbearance gives economicallyfunctional banks—those that may be undergoingshort-term difficulties—a window of time in whichto adjust to market conditions without enforcingotherwise applicable bank regulations. Althoughnot every undercapitalized bank is a likely candidatefor resolution, all are unquestionably candidates forincreased regulatory oversight and supervision.Regulators have the authority to force banks to raiseequity, suspend dividends, reduce assets, issue newstock, force divestiture of affiliates, remove direc-tors or managers, demand increased allowances forloan losses, or charge off uncollectible loans. En-forcing such actions on these undercapitalized banksmay have resulted in even more failures. In somecases, regulators decided to forgo enforcement ofsupervisory actions—in particular, enforcing capitalrequirements-presumably because they felt thatthese banks would be more likely to survive ratherthan fail.

Post-FDICIA: An Outlook ofGuarded Optimism for theBanking Industry

The Congress intended the deposit insurance systemto be self-sustaining. Revenues collected frompremium assessments paid by insured banks areused to cover the costs of resolving insolvent banks.For almost 50 years, the fund's revenues exceededits costs. But the expense of resolving banks in thelate 1980s drained the Bank Insurance Fund. By1991, there was increasing concern about the num-bers and losses of bank resolutions.

SUMMARY xv

The financial condition of the banking industryand the ability of the federal deposit insurance fundto cover losses from the alarming number of resolu-tions in the 1980s were major motivating factors forpassage of the Federal Deposit Insurance Corpora-tion Improvement Act of 1991 (FDICIA). Alongwith recapitalizing the BIF (the FDIC is to recapi-talize the insurance fund by 2005), a major themeof this legislation is to foster "safety and soundness"in the banking industry.

Because only little more than two years haveelapsed since its passage, it is difficult to evaluatefully the effects of FDICIA. Nevertheless, thereforms put in place by this act appear to haveaddressed directly some of the major problemsidentified during the 1980s-a period that put con-siderable stress on the regulatory and deposit insur-ance systems. The FDICIA authorized the FederalDeposit Insurance Corporation to take prompt cor-rective action (or intervene earlier) to limit insur-ance losses. That is, bank regulators must employregulatory constraints depending on whether a bankmeets minimum prescribed capital levels. The actrequires prompt closure of severely undercapitalizedbanks. In FDICIA, the Congress also charged theFDIC with the responsibility of putting into place arisk-based capital system and developing a risk-based premium system. Properly designed risk-based premiums will provide increased insurancefunds to cover heightened risk in bank portfolios.A system of risk-based capital requirements, alongwith the mandated yearly on-site examinations, mayprovide a better buffer (to absorb losses on assets)between assets that default in a risky bank portfolioand bank insolvency that requires resolution.

After several years of poor performance, thebanking industry earned record profits in 1992 and1993. The average return on assets for commercialbanks was 1.21 percent in 1993, a year in which thereturn on assets in each quarter surpassed averagespreviously reported by the industry. At the sametime, the average annual return on equity for theindustry exceeded 15 percent. Several factors con-tribute to the improved health of the banking indus-try even as the industry undergoes continued struc-tural change and consolidation. In particular, favor-able interest rate conditions and a growing economyhave enabled banks to prosper. Banks have been

able to take advantage of the fact that they can payless for their liabilities and receive greater returnson assets. Moreover, the growing economy hashelped to reduce the amount of troubled assets—noncurrent loans declined in all regions of the coun-try and across all major loan categories—whichmeans that banks do not have to set aside as muchmoney to cover potential bad loans.

The outlook for the Bank Insurance Fund hasimproved as the banking industry continues to earnrecord profits. After incurring positive outlays from1988 to 1992, the fund is now in the black. Thefund's balance (net worth) rebounded to $6.8 billionin the second quarter of 1993, from a negative $100million at the end of 1992 and a negative $7 billionat the end of 1991. In its January 1994 baseline,the Congressional Budget Office projected that theBIF will take in $8 billion more than it spends infiscal year 1994 and continue in the black with asmaller excess in the next several years.

At the close of 1993, only 41 banks had beenresolved through the BIF, the fewest resolutions inany year since 1982, when there were 42. Theassets of banks resolved by the FDIC have beenfalling from a record $63.4 billion in 1991 to $44.2billion in 1992 and only $3.6 billion in 1993. As arule, larger banks are more costly to resolve. Theaverage size of a resolved bank in 1993 was $87million, down from $363 million in 1992.

The record profits in the two years followingFDICIA tend to obscure the fact that the bankingindustry has been losing ground to other types offinancial services. To some degree, however, banksare earning profits by taking advantage of low inter-est rates, which exposes them to increased interest-rate risk. Although favorable conditions for interestrates have allowed banks to increase profits andreplenish their capital, their increased exposure tointerest rate risk warrants a posture of guardedoptimism. When economic conditions change sothat the returns based on interest rate spreads nar-row, it could expose some banks to increased risk offailure. Given the possibility that the industry maybe susceptible to such periodic crises because ofchanging economic conditions, policymakers areexamining the need for further structural reform inthe banking industry. In particular, there is continu-

xvi THE CHANGING BUSINESS OF BANKING June 1994

ing interest in legislative reform that would enable bill currently under consideration by the Congressbanks to diversify, either geographically or through would permit banks to diversify their loan portfoliosvarious product offerings. An interstate branching across state lines.

Chapter One

Introduction

P roblems in the banking industry proliferateddramatically during the 1980s, and thenumber of bank resolutions reached levels

not seen since the Great Depression. Since theBanking Act of 1933 established the Federal De-posit Insurance Corporation (FDIC), more than2,000 troubled commercial and savings banks havebeen resolved. Banks resolved by the FDIC haveeither failed, requiring regulatory involvement intheir exit from the industry, or needed some finan-cial assistance to remain open. Between 1980 and1992, the FDIC resolved almost three times as manybanks (1,505 banks) as it resolved in the first 46years of its existence (at many times the cost to theinsurance fund). During the peak years between1987 and 1992, the FDIC resolved more than 1,000banks, seriously depleting the Bank Insurance Fund(BIF).

Before 1980, the solvency of the insurance fundwas never an issue. Until the mid-1980s, revenuesto the insurance fund, primarily derived from semi-annual assessments of premiums, invariably ex-ceeded losses. Regulators assessed premiums at thesame flat rate used since the creation of the fund-8.3 cents per $100 of insured deposits. At the time,the FDIC (with Congressional authorization) com-monly provided rebates of up to one-third of theoverall annual premium assessments to avoid gener-ating what was commonly thought of as an "exces-sive" insurance fund surplus.1 Regulators consid-ered the fund reserves more than sufficient to han-dle recognized fund losses, feeling that it was not

necessary to increase premiums. In 1987, the BIFhad an $18 billion reserve. But by 1991, the recordnumber of resolutions had caused such a drain oninsurance fund reserves that the General AccountingOffice pronounced the Bank Insurance Fund insol-vent.2

The dramatic increase in the number and costsof resolutions in the late 1980s, coming on the heelsof the savings and loan crisis, brought into questionthe long-term condition of the deposit insurancefund. Taxpayers have paid dearly for the savingsand loan insurance losses, a financial hemorrhagethat may cost more than $150 billion (expressed in1990 dollars) before it is finished.3 Speculation thattaxpayers would again have to come to the rescueof another ailing insurance fund sparked Congres-sional debate.

In addition to the immediate problem of lossesto the Bank Insurance Fund, industry analysts werealso concerned about the broad economic effects ofbank failures. The average loss in asset value ofbanks and thrifts resolved during the 1980s was un-precedented in the history of deposit insurance.These losses were symptomatic of poor decisions bymany depositories and weaknesses in the regulatorysystem of monitoring and supervision. Another

William E. Gibson, "Deposit Insurance in the United States: Eval-uation and Reform," Journal of Financial and Quantitative Analy-sis (March 1972), pp. 1575-1594.

2. General Accounting Office, "Financial Audit: Bank InsuranceFund's 1991 and 1990 Financial Statements" (report to the Boardof Directors, Federal Deposit Insurance Corporation, Washington,D.C., May 11, 1992). The insurance fund is insolvent when thereare not sufficient reserves on hand to manage bank failures. Tech-nically, however, the fund is never illiquid because the FDIC hasthe ability to borrow funds (up to $30 billion as of 1991) from theU.S. Treasury to handle resolutions and maintain working capital.

3. See Congressional Budget Office, The Economic and BudgetOutlook: Fiscal Years 1995-1999 (January 1994), p. 44.

2 THE CHANGING BUSINESS OF BANKING June 1994

cause of concern is that bad investments made withfunds from depository institutions may have contrib-uted to an overvalued capital stock and poor growthof productivity in the United States during the1980s.

The alarming increase in the number of bank(and thrift) resolutions revealed the necessity forbank reform legislation. The Financial InstitutionsReform, Recovery, and Enforcement Act of 1989and the Federal Deposit Insurance Corporation Im-provement Act of 1991 (FDICIA) were responses tothe pressure put on the deposit insurance system be-cause of the costs of resolving these institutions. Asa result of these legislative actions and an increasein banking industry profits in 1992 that continuedinto 1993, concerns have abated somewhat. Amongthe most interesting questions remaining are whythere was such an increase in bank failures and sub-sequent resolutions in the late 1980s and early1990s. Also, why did the costs to the governmentof resolving failed banks increase so dramatically,depleting the BIF in just a few years?

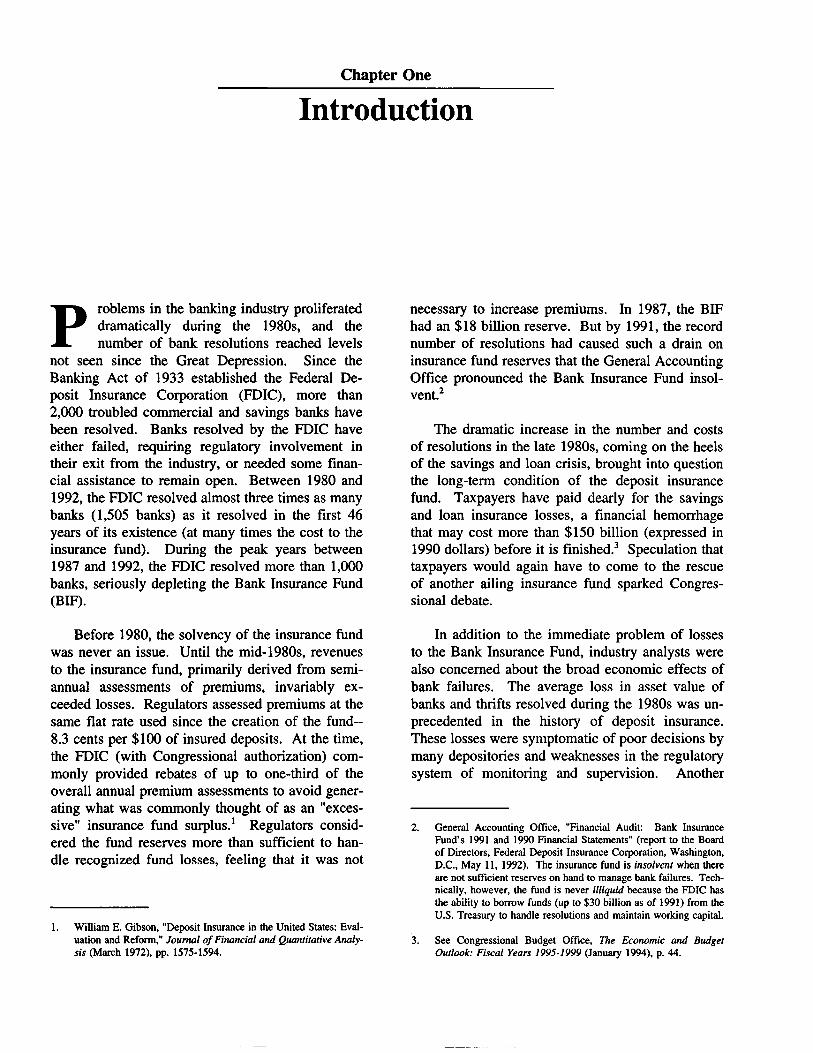

Figure 1.Average Annual Number of Bank Failures forSelected Periods Between 1900 and 1992

Years

1900-1920

1921-1929

1930

1931

1932

1933

1934-1940

1941-1980

1981-1986

1987-1992

1

•:ir:7T.:i: :. , ;;;,j: -.: :. j; "~1J " ;;

ji i i i i0 1,000 2,000 3,000 4,000

Number of Banks

SOURCE: Congressional Budget Office based on data from theFederal Deposit Insurance Corporation.

Bank Resolutions inHistorical Perspective

In the early history of the U.S. banking industry,from 1870 to 1919, banks failed at a rate slightlylower than that of firms in other sectors of theeconomy.4 In fact, the industry grew rapidly duringthis period. The number of commercial banks tri-pled in 35 years, growing from 10,000 in 1885 to30,000 in 1920. Almost 500 banks failed in 1893,but from 1900 to 1920 the average rate of failurewas less than 100 a year.5 Circumstances began tochange, however, in the 1920s.

4. George Kaufman, "Banking Risk in Historical Perspective," Re-search in Financial Services: Private and Public Policies, vol. 1(Chicago: JAI Press Inc., 1989), pp. 151-164.

5. George Benston and George Kaufman, "Risks and Failures inBanking: Overview, History, and Evaluation," in George G.Kaufman and Roger C. Kormendi, eds., Deregulation of FinancialServices: Public Policy in Flux (Cambridge, Mass.: BallingerPress, 1986).

During the 1920s, the banking industry began tocontract. As many as 5,400 banks suspended opera-tions and more than 4,000 never reopened. Nearly700 banks failed every year during the 1920s (seeFigure 1). A recession hit the agricultural sector inthe late 1920s, accounting for the failure of manysmall rural banks. The Great Depression struck theentire economy in the early 1930s, causing recordnumbers of bank failures.

Between 1930 and 1933, the average number ofannual bank failures reached an incredible 2,274.Within the five years from 1929 through 1933, thenumber of banks in the United States was cut al-most in half, to about 14,700. Even during thesecrisis years, annual losses to depositors rarely ex-ceeded 1 percent of total deposits at all banks.Losses at many of these banks were generallylimited to less than 10 cents on the dollar.6

James S. Lawrence, "What is the Average Recovery of Deposi-tors?" American Bankers Association Journal (February 1931), pp.655-656, 722-723.

CHAPTER ONE INTRODUCTION 3

During this period, in the absence of a systemof deposit guarantees, banks were declared legallyinsolvent and closed by their creditors much morequickly than they were after deposit insurance.7

Liquidity was much more costly in early financialmarkets because funds moved slowly through thesystem. If banks could not meet liquidity require-ments, they would often voluntarily suspend opera-tions. Bank examiners would then determinewhether a bank had sufficient capital to reopen.The fact that banks were closed fairly quickly in aliquidity crisis helped to limit depositors' losses.

It is popularly supposed that many of thesefailed banks had fallen victim to deposit runs. Butfrom 1865 to 1929, fewer than 15 percent of allbank failures occurred as a result of depositor runs.8

Surprisingly few solvent banks were drawn intofailure as depositors reacted in panic to losses atother insolvent banks.9 Although there were severesystemwide runs in the early 1930s, a large propor-tion of the banks that failed were insolvent. Banksthat the Federal Reserve supported (in the role oflender of last resort) tended to survive.10

Banking After the Depression

After the banking crisis of the early 1930s, theBanking Acts of 1933 and 1934 created the FDIC.

7. Kaufman, "Banking Risk in Historical Perspective," pp. 151-164.

8. George Thorndyke, "Fiction and Fact on Bank Runs," AmericanBankers Association Journal (June 1929), p. 1,269.

9. Kaufman, "Banking Risk in Historical Perspective," p. 152.

10. See Allan H. Meltzer, "Financial Failures and Financial Policies,"in George G. Kaufman and Roger C. Kormendi, eds., Deregula-tion of Financial Services: Public Policy in Flux (Cambridge,Mass.: Ballinger Press, 1986). Meltzer states that the FederalReserve in the role of a lender of last resort should act to preventilliquid but solvent banks from being forced to close by makingloans to them when they face heavy deposit withdrawals.

See also Milton Friedman and Anna J. Schwartz, A MonetaryHistory of the United States, 1867-1960 (Princeton, N.J.: PrincetonUniversity Press, 1963). The authors state that during the 1930sthe Federal Reserve did not provide sufficient liquidity, whetherthrough the discount window or open-market operations, andthousands of banks were forced to liquidate their assets simulta-neously in depressed markets.

These acts made the FDIC responsible for resolvingbanks when the state or federal chartering agencydeclared them insolvent, and for maintaining an in-surance fund to protect depositors. Deposit insur-ance was supposed to immunize the system as awhole against a contagious response to individualbank failures, but in so doing it transferred the bur-den of monitoring individual institutions from thecreditors of depositories to regulators. Before thedeposit insurance system put guarantees in place,several parties, including investors and depositors,were interested in reducing their risk of loss. Therisk of losing depositors and shareholders (in thecase of national banks) generally influenced banksto keep their portfolio risk low. Depositors alsopressured banks to hold more capital because thegreater the amount, the more losses the bank couldwithstand before becoming insolvent and forcinglosses on depositors.

The Post-Depression Incidence of Bank Resolu-tions. From 1934 onward, bank runs were virtuallynonexistent. The average annual rate of banks re-solved by the FDIC dropped well below preinsur-ance levels (see Figure 1). From 1934 to 1940, theaverage annual number of bank resolutions droppeddramatically to 64. During the next 40 years, from1941 to 1981, the average number of resolutions fellto only five banks a year. Bank resolutions beganto rise again in the 1980s as changes in financialmarkets, lingering inflation, regulatory reform, andnational and regional economic shocks contributedto an environment of structural change for financialinstitutions.

More than 100 banks had to be resolved everyyear between 1985 and 1992. The peak year duringthis period was 1989, when the FDIC resolved 207banks. In an industry composed of between 11,000and 12,000 commercial banks, even 200 resolutionsin any one year may seem slight-a failure rate ofless than 2 percent. But the number of resolutionsin any one year is not as significant as the trendover several years. Between 1980 and 1992, thenumber of commercial banks in the industry shrankby more than 16 percent. This period saw the high-est number of resolutions and the first significantchallenge to the deposit insurance system in the his-tory of the FDIC.

4 THE CHANGING BUSINESS OF BANKING June 1994

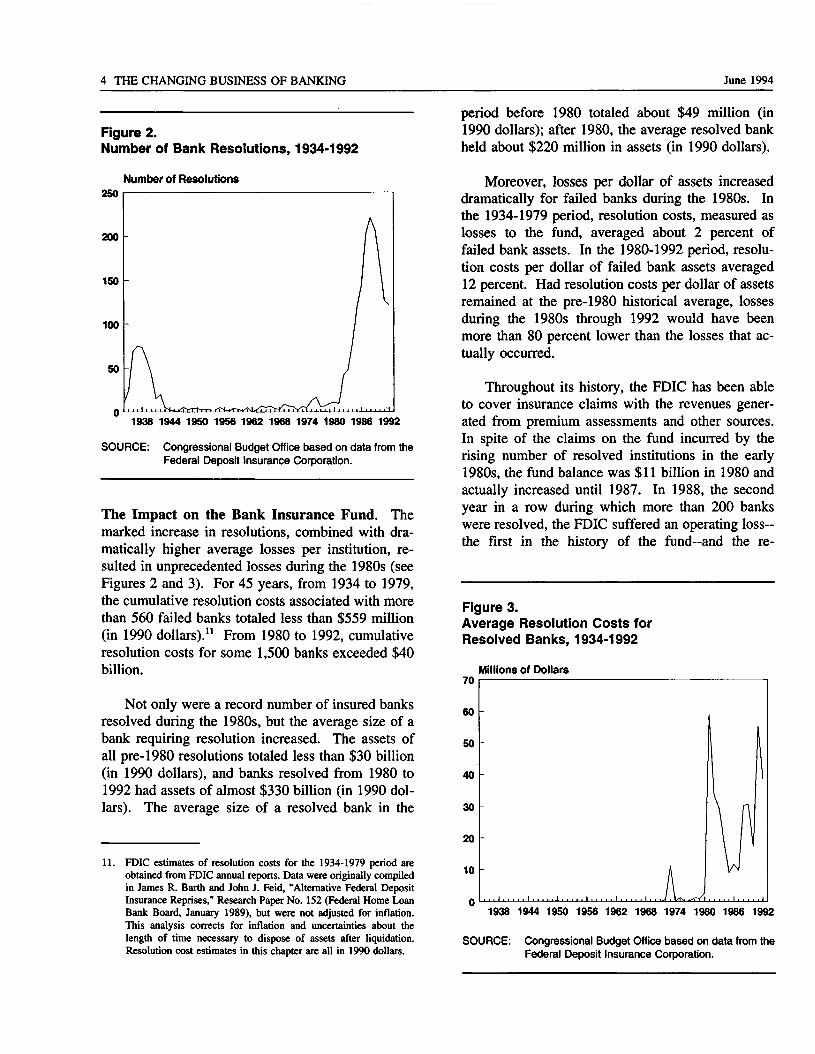

Figure 2.Number of Bank Resolutions, 1934-1992

Number of Resolutions250

200

1938 1944 1950 1956 1962 1968 1974 1980 1986 1992

SOURCE: Congressional Budget Office based on data from theFederal Deposit Insurance Corporation.

The Impact on the Bank Insurance Fund. Themarked increase in resolutions, combined with dra-matically higher average losses per institution, re-sulted in unprecedented losses during the 1980s (seeFigures 2 and 3). For 45 years, from 1934 to 1979,the cumulative resolution costs associated with morethan 560 failed banks totaled less than $559 million(in 1990 dollars).11 From 1980 to 1992, cumulativeresolution costs for some 1,500 banks exceeded $40billion.

Not only were a record number of insured banksresolved during the 1980s, but the average size of abank requiring resolution increased. The assets ofall pre-1980 resolutions totaled less than $30 billion(in 1990 dollars), and banks resolved from 1980 to1992 had assets of almost $330 billion (in 1990 dol-lars). The average size of a resolved bank in the

11. FDIC estimates of resolution costs for the 1934-1979 period areobtained from FDIC annual reports. Data were originally compiledin James R. Earth and John J. Feid, "Alternative Federal DepositInsurance Reprises," Research Paper No. 152 (Federal Home LoanBank Board, January 1989), but were not adjusted for inflation.This analysis corrects for inflation and uncertainties about thelength of time necessary to dispose of assets after liquidation.Resolution cost estimates in this chapter are all in 1990 dollars.

period before 1980 totaled about $49 million (in1990 dollars); after 1980, the average resolved bankheld about $220 million in assets (in 1990 dollars).

Moreover, losses per dollar of assets increaseddramatically for failed banks during the 1980s. Inthe 1934-1979 period, resolution costs, measured aslosses to the fund, averaged about 2 percent offailed bank assets. In the 1980-1992 period, resolu-tion costs per dollar of failed bank assets averaged12 percent. Had resolution costs per dollar of assetsremained at the pre-1980 historical average, lossesduring the 1980s through 1992 would have beenmore than 80 percent lower than the losses that ac-tually occurred.

Throughout its history, the FDIC has been ableto cover insurance claims with the revenues gener-ated from premium assessments and other sources.In spite of the claims on the fund incurred by therising number of resolved institutions in the early1980s, the fund balance was $11 billion in 1980 andactually increased until 1987. In 1988, the secondyear in a row during which more than 200 bankswere resolved, the FDIC suffered an operating loss-the first in the history of the fund—and the re-

Figure 3.Average Resolution Costs forResolved Banks, 1934-1992

70

60

50

40

30

20

10

Millions of Dollars

1938 1944 1950 1956 1962 1968 1974 1980 1986 1992

SOURCE: Congressional Budget Office based on data from theFederal Deposit Insurance Corporation.

CHAPTER ONE INTRODUCTION 5

serve ratio was less than 1 percent. The ratio of theinsurance fund reserves to total insured deposits is ameasure of the overall health of the fund. At thetime the law required the FDIC to maintain the in-surance fund at a minimum ratio of 1.16 percent.The reserve ratio continued to fall for the next threeyears and by the end of 1991 the fund had a nega-tive balance.

The Congress enacted special legislation toprovide the FDIC with sufficient funds to closeinsolvent banks and recapitalize the insurance fund.The Federal Deposit Insurance Corporation Im-provement Act of 1991 gives the BIF authority toborrow up to $30 billion from the U.S. Treasury tocover the losses from bank resolutions.12 FDICIAalso enables the BIF to borrow additional funds forworking capital~up to 90 percent of the value of theassets acquired from failed banks held by the FDIC—from the Federal Financing Bank (also a part ofthe U.S. Treasury). To recapitalize the BIF,FDICIA requires that the FDIC set assessment ratesthat will achieve a designated ratio of insurancefund reserves to total insured deposits of 1.25 per-cent by 2005. A minimum rate of 23 cents per$100 of insured deposits is required until the targetratio is achieved. In January 1993, the FDIC putinto effect a "risk-based" premium structure withaverage premiums of approximately 25 cents per$100 of qualified deposits.

Banking Industry Changes and Consolidation. Inone sense, industry analysts view the bank reso-lutions of the 1980s as the inevitable consequenceof an industry undergoing fundamental changeswhile moving toward greater competitiveness andefficiency. Bank failures, like failures in any otherbusiness, can occur as unfortunate by-products of anindustry experiencing intensive competition, deregu-lation, and structural change.

The deregulation of banking began in 1980 withthe removal of statutory interest rate caps. Suchindustries as railroads, trucking, airlines, petroleum,and natural gas experienced consolidation and firm

failures following deregulation. So, too, the bank-ing industry underwent a period of consolidationand failures. Less efficient banks fell into insol-vency as other banks and nonbank financial institu-tions competed to serve consumers in financial mar-kets.

The numbers and costs of bank resolutionsduring the last decade, however, carry more onerousimplications than a simple movement toward en-hanced efficiency might suggest. The banking sec-tor, despite partial deregulation, still operates underthe supervision of state and federal chartering agen-cies and FDIC regulators. It is therefore importantthat regulators have an efficient exit policy for in-solvent institutions because the longer an insolventbank is permitted to operate, the greater the poten-tial loss to the insurance fund. By the time regula-tors declared many failed banks legally insolventduring the 1980s, the value of assets had deterior-ated so much that the cost of resolution greatly ex-ceeded administrative costs. A bank is economic-ally insolvent when the market value of its liabilitiesexceeds the market value of its assets. Without reg-ulatory intervention, an insolvent bank can continueto operate independently until it cannot meet cashobligations; in other words, until insolvency be-comes clearly noticeable. The large margin of loss-es over administrative costs is one indication thatthese banks had operated in an insolvent state forsome time before they were resolved. Empiricalanalyses of the savings and loan crisis suggest thatinsolvent institutions that are closed earlier cost lessto resolve.13

The high resolution costs of the 1980s broughtinto question the efficiency of regulatory supervi-sion and the process of removing insolvent banksfrom the system. Regulators depended on tradi-tional book-value methods of accounting thatmasked potentially insolvent banks until resolutioncosts became extraordinary. Unanticipated resolu-

12. Section 101 of the Federal Deposit Insurance Corporation Im-provement Act of 1991, 12 U.S.C. 1824, 105 Stat. 2236.

13. R. Dan Brumbaugh, Jr., and Robert E. Litan, "A Critique of theFinancial Institutions Recovery, Reform and Enforcement Act(FIRREA) of 1989 and the Financial Strength of CommercialBanks," in James Barth and R. Dan Brumbaugh, eds., The Reformof Federal Deposit Insurance (New York: Harper Business, 1992).See also Congressional Budget Office, "The Cost of ForbearanceDuring the Thrift Crisis," CBO Staff Memorandum (June 1991).

6 THE CHANGING BUSINESS OF BANKING June 1994

tions raise fundamental concerns about the ability ofregulators to limit future losses. In addition, allow-ing insolvent banks to continue operating can hurthealthy banks in the same market. Insolvent banksthat remain open can increase the cost of doingbusiness as they bid for potential customers.

The Economic Costsof Bank Failures

The primary function of the nation's financial sys-tem is to facilitate the efficient allocation of re-sources in the economy. As an important compo-nent of the financial system, banks provide mecha-nisms for facilitating transactions, transmitting mon-etary policy, and transferring funds between saversand borrowers—a principal ingredient of economicgrowth. Banks have been a primary credit conduit,especially for such information-intensive borrowersas small businesses.

The most frequently stated goal of bankingregulation is to maintain the safety and soundness(or stability) of the financial system. As an impor-tant part of that system, banks provide a vital ser-vice to the economy and to society as a whole.Conditions that impede the ability of banks to oper-ate efficiently affect the allocation of resources. Ifbank closings create a shortage in the amount ofcredit available, society bears the cost of lost invest-ment opportunities and therefore lower economicgrowth. Circumstances that affect the stability ofbanking can also affect monetary policy.

The Direct and Indirect Costsof Bank Resolutions

The cost of bank failures involves more than justthe losses that the FDIC reports to the insurancefund. Most failures throw bank employees out of

work, causing them at least a temporary loss of fullwages. But on the whole, bank resolutions duringthe last decade did not cause a major loss of jobs inthe industry. Bank employment actually increasedduring most of the decade. Despite the reduction inthe number of banks providing financial services,the number of branches did not decrease over theperiod. It was not until the early 1990s that severalinstitutions started to contract and lay off workers,causing employment in the industry to fall slightly.

There may be, however, substantial indirectlosses, particularly in those regions where there arelarger numbers of resolved banks. Excessive bankfailures in a particular region can temporarily in-crease the difficulty and costs of obtaining credit forsmall-to-middle-sized firms in the area. These firmsusually depend on banks for commercial and indus-trial loans. Economic losses associated with bankresolutions can carry over to other industries ifcreditworthy businesses find it excessively costly toobtain credit as a result of a high rate of bank fail-ures in a region.

In addition to indirect losses suffered by otherbusinesses after bank failures, real economic lossescan occur even before a bank fails and is resolved.Most financially weakened banks get that way be-cause they lose money on poor-quality assets--mostly bad loans. For example, excessive invest-ment in commercial real estate throughout the 1980stook the place of other, potentially more valuable,investments. Bad loans, which eventually show upas relatively high losses on an asset, equate to mis-allocated investment and lower economic growth.Many economists believe that the lack of productiv-ity during the 1980s was, in part, the result of insuf-ficient investment in productive resources. A Con-gressional Budget Office study of the failures ofsome 1,000 savings and loans suggests that theopportunity costs of misdirected investment byfailed thrifts was substantial.14

14. See Congressional Budget Office, The Economic Effects of theSavings & Loan Crisis (January 1992).

Chapter Two

The Structural Trends and EconomicConditions Underlying

Bank Resolutions

B anks confronted significant changes in theeconomic and institutional environment inthe 1970s and 1980s, contributing to a

dramatic increase in the rate of failures. Regula-tions that were applied just after the Great Depres-sion limited the activities of most depository institu-tions for more than four decades. Regulators setprices and costs of doing business and limited com-petition; banks and thrifts usually earned profits andrelatively few failed. Banking in those days was amuch easier enterprise; markets were insulated andinflation was low.

Two dramatic surges in inflation during the1970s fundamentally changed the business of bank-ing. One occurred in the mid-1970s as a result of aspike in food and oil prices. The other occurred in1979 when oil prices surged again as a result ofevents tied to the revolution in Iran. These twoprice shocks, combined with an apparently overheat-ing economy, were primarily responsible for thesurges in the inflation rate. Both inflationary per-iods led to dramatic rises in commodity prices, mer-curial stock and bond prices, and particularly vola-tile interest rates.

Interest rate volatility, coupled with advances ininformation processing, changed bank competitionand depositor behavior fundamentally and irrevers-ibly. Volatile inflation raised market interest rateswell above regulated interest rate ceilings by theend of the 1970s. As a result, depositors withdrewfunds from banks (and thrifts) to invest in instru-

ments that promised to earn a higher rate of return.The draw of double-digit interest rates available onmoney market mutual funds and Treasury securitiesmade them popular alternatives to banks and thrifts.

Profitability in the banking industry, measuredby return on assets, increased moderately during thetwo decades before 1970.1 The return on assetsstarted to decline after 1979. Banks entered the1980s facing a set of structural and economic condi-tions that had weakened their position in relation toother financial intermediaries both here and abroad.In response to these pressures and the increased rateof bank failures in the latter half of the 1980s, theCongress and state legislators enacted major regula-tory changes by the end of the 1980s. Deregulationof depository institutions in the 1980s included alifting of interest rate ceilings on deposits, an expan-sion of product lines, and the spread of interstatebanking.2 The regulatory changes were intended toallow banks to compete better with nonbank finan-cial intermediaries. As a result, banks now operatein competitive rather than insulated markets.

1. Information on bank profitability throughout this chapter comesfrom the Federal Reserve Bulletin.

2. The Depository Institutions Deregulation and Monetary ControlAct of 1980 (DIDMCA) mandated the phasing out of depositinterest rate ceilings and allowed interest payment on transactionsaccounts; the Depository Institutions Act of 1982 (Garn-StGermain) allowed interstate mergers between banks and savingsand loans; and the Competitive Equality in Banking Act of 1987(CEBA) limited the growth of so-called nonbank banks.

8 THE CHANGING BUSINESS OF BANKING June 1994

Enhanced Competition andFinancial Innovation

Banks as a group lost ground to open-market creditsources and nondepository financial institutions interms of funds advanced in U.S. credit markets.Open-market credit increased dramatically duringthe 1980s, caused by growth in commercial paperand junk bonds. Finance companies led nonbankmediation of credit. Moreover, nondepository finan-cial institutions compete with banks in markets forassets and liabilities. Nonbanks now offer creditcards, residential mortgages, consumer and commer-cial loans, and transaction accounts. By 1990,subsidiaries of such retailers as Sears Roebuck andsuch manufacturers as the Ford Motor Company andGeneral Electric were financing one-third of con-sumer credit and one-quarter of commercial loans.3

Although the assets of the financial servicesindustry (including banks) have continued to grow,the share of domestic financial assets held by U.S.commercial and savings banks decreased from about50 percent in 1950 to 22 percent in 1991. Over thesame period, pension and mutual funds grew fromabout 5 percent to 30 percent of financial assets.Assets held by finance companies doubled duringthis period, accounting for 7 percent of assets in1991. Other depositories, life insurance firms, andnondepository institutions, including automobilecompanies, retail department stores, and telephonecompanies, make up the remaining share of assets.4

Increased competition and financial innovationmade banking less stable in the 1980s. Continuingadvances in computer technology, which increasethe speed and volume of information processing,have helped to popularize new kinds of financialassets, especially off-balance-sheet instruments. En-hanced technology also facilitated the development

3. See Roger Vaughan and Edward Hill, Banking on the Brink(Washington, D.C.: Washington Post Company, 1992), p. 19.

4. Herbert L. Baer and Larry R. Mote, The U.S. Financial System(Chicago: Federal Reserve Bank, December 1990). See alsoRobert E. Litan, "The Revolution in U.S. Finance: Past, Presentand Future" (paper presented as a Frank M. Engle lecture, TheAmerican College, Bryn Mawr, Pa., April 30, 1991).

of an increasingly international market for financialassets. Each day, global banking transactionsamount to more than $1 trillion. International com-petition continues to threaten the domestic bankingindustry's ability to vie for both deposits and assets.Many of the resulting changes in financial marketsdirectly contributed to falling revenues from interestincome.

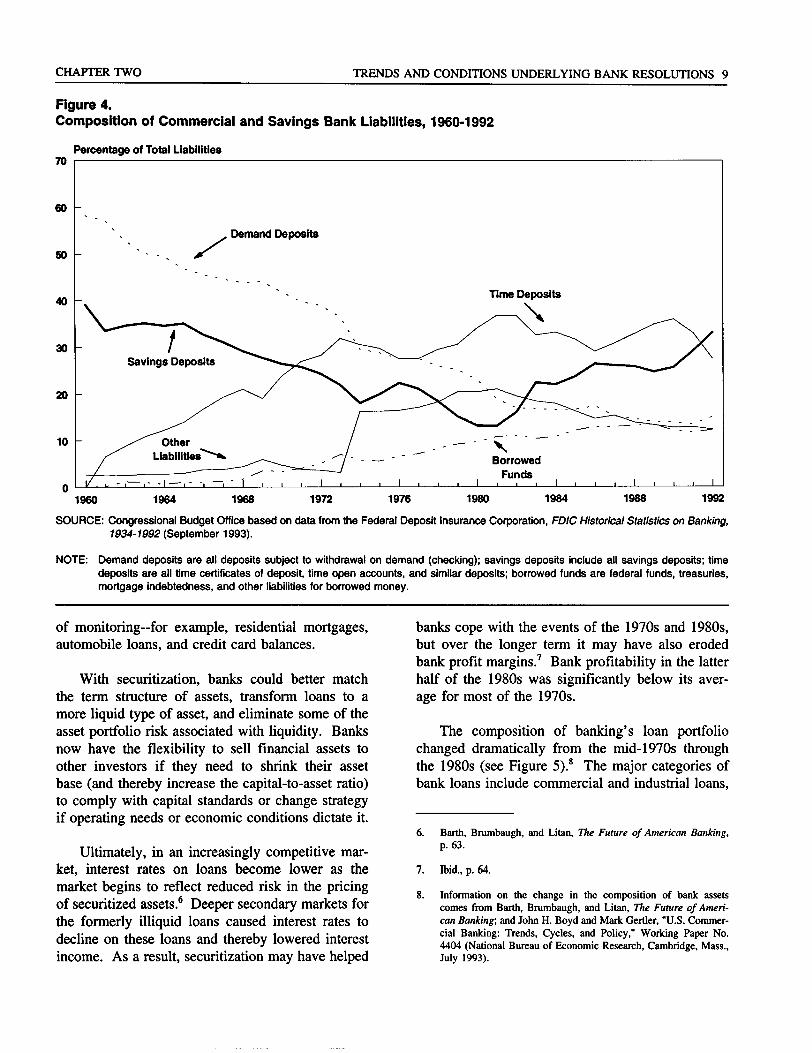

The Changing Compositionof Bank Balance Sheets

The composition of bank liabilities has changeddrastically since the 1970s (see Figure 4). Thetrend shows a decline in checkable deposits (mostlydemand deposits and NOW accounts) in favor ofinterest-bearing liabilities. Two of the more popularforms of liabilities are certificates of deposit andmoney market instruments. Demand for both ofthese financial instruments is sensitive to move-ments in the market interest rate. Now, when short-term market rates move adversely, depositorsrespond by shifting their investments to the financialinstrument with the highest return. Banks areforced to offer competitive returns to keep custom-ers. The increased competition puts a downwardpressure on interest income and increasingly ex-poses banks to liquidity risk.5

As the effects of inflation eroded the value oflong-term loans, liquidity became important. Aidedby improvements in data processing, the phenome-non of securitization of finance became a popularmeans for banks to increase their liquidity in thelate 1980s. Many banks sought to turn away from astrictly buy-and-hold management strategy in whichthey collect funds from customers, then invest themin financial assets held until maturity. Securitizationinvolves the pooling of a large number of individualloans into bundles that can be sold as some form ofsecurity on secondary markets. Loans for securiti-zation have fairly uniform features, are usually wellcollateralized, and do not require a high level of

5. James Earth, R. Dan Brumbaugh, Jr., and Robert E. Litan, TheFuture of American Banking (New York: M.E. Sharpe, Inc.,1992), p. 63.

CHAPTER TWO TRENDS AND CONDITIONS UNDERLYING BANK RESOLUTIONS 9

Figure 4.Composition of Commercial and Savings Bank Liabilities, 1960-1992

Percentage of Total Liabilities

1960 1964 1968 1972 1976 1980 1984 1988 1992

SOURCE: Congressional Budget Office based on data from the Federal Deposit Insurance Corporation, FDIC Historical Statistics on Banking,1934-1992 (September 1993).

NOTE: Demand deposits are all deposits subject to withdrawal on demand (checking); savings deposits include all savings deposits; timedeposits are all time certificates of deposit, time open accounts, and similar deposits; borrowed funds are federal funds, treasuries,mortgage indebtedness, and other liabilities for borrowed money.

of monitoring—for example, residential mortgages,automobile loans, and credit card balances.

With securitization, banks could better matchthe term structure of assets, transform loans to amore liquid type of asset, and eliminate some of theasset portfolio risk associated with liquidity. Banksnow have the flexibility to sell financial assets toother investors if they need to shrink their assetbase (and thereby increase the capital-to-asset ratio)to comply with capital standards or change strategyif operating needs or economic conditions dictate it.

Ultimately, in an increasingly competitive mar-ket, interest rates on loans become lower as themarket begins to reflect reduced risk in the pricingof securitized assets.6 Deeper secondary markets forthe formerly illiquid loans caused interest rates todecline on these loans and thereby lowered interestincome. As a result, securitization may have helped

banks cope with the events of the 1970s and 1980s,but over the longer term it may have also erodedbank profit margins.7 Bank profitability in the latterhalf of the 1980s was significantly below its aver-age for most of the 1970s.

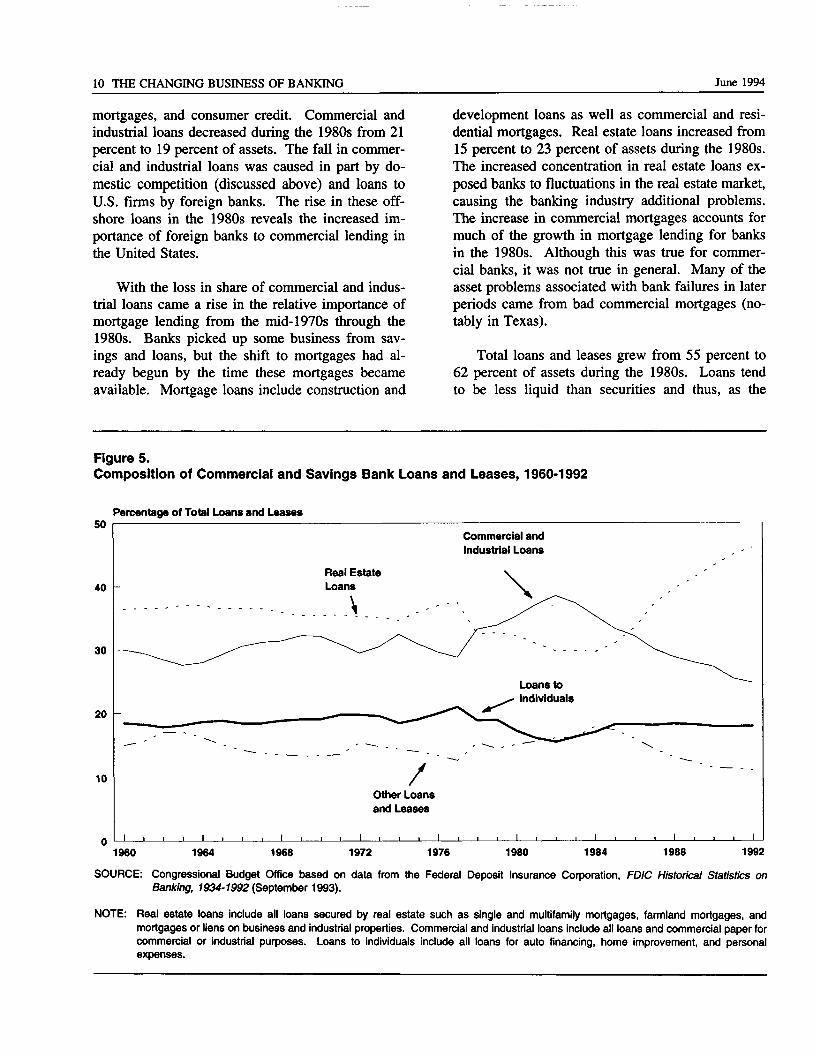

The composition of banking's loan portfoliochanged dramatically from the mid-1970s throughthe 1980s (see Figure 5).8 The major categories ofbank loans include commercial and industrial loans,

6. Earth, Brumbaugh, and Litan, The Future of American Banking,p. 63.

7. Ibid., p. 64.

8. Information on the change in the composition of bank assetscomes from Earth, Brumbaugh, and Litan, The Future of Ameri-can Banking', and John H. Boyd and Mark Gertler, "U.S. Commer-cial Banking: Trends, Cycles, and Policy," Working Paper No.4404 (National Bureau of Economic Research, Cambridge, Mass.,July 1993).

10 THE CHANGING BUSINESS OF BANKING June 1994

mortgages, and consumer credit. Commercial andindustrial loans decreased during the 1980s from 21percent to 19 percent of assets. The fall in commer-cial and industrial loans was caused in part by do-mestic competition (discussed above) and loans toU.S. firms by foreign banks. The rise in these off-shore loans in the 1980s reveals the increased im-portance of foreign banks to commercial lending inthe United States.

With the loss in share of commercial and indus-trial loans came a rise in the relative importance ofmortgage lending from the mid-1970s through the1980s. Banks picked up some business from sav-ings and loans, but the shift to mortgages had al-ready begun by the time these mortgages becameavailable. Mortgage loans include construction and

development loans as well as commercial and resi-dential mortgages. Real estate loans increased from15 percent to 23 percent of assets during the 1980s.The increased concentration in real estate loans ex-posed banks to fluctuations in the real estate market,causing the banking industry additional problems.The increase in commercial mortgages accounts formuch of the growth in mortgage lending for banksin the 1980s. Although this was true for commer-cial banks, it was not true in general. Many of theasset problems associated with bank failures in laterperiods came from bad commercial mortgages (no-tably in Texas).

Total loans and leases grew from 55 percent to62 percent of assets during the 1980s. Loans tendto be less liquid than securities and thus, as the

Figure 5.Composition of Commercial and Savings Bank Loans and Leases, 1960-1992

50

40

30

20

10

Percentage of Total Loans and Leases

Commercial andIndustrial Loans

Real EstateLoans

Other Loansand Leases

1960 1964 1968 1972 1976 1980 1984 1988 1992

SOURCE: Congressional Budget Office based on data from the Federal Deposit Insurance Corporation, FDIC Historical Statistics onBanking, 1934-1992 (Septemberl 993).

NOTE: Real estate loans include all loans secured by real estate such as single and multifamily mortgages, farmland mortgages, andmortgages or liens on business and industrial properties. Commercial and industrial loans include all loans and commercial paper forcommercial or industrial purposes. Loans to individuals include all loans for auto financing, home improvement, and personalexpenses.

CHAPTER TWO TRENDS AND CONDITIONS UNDERLYING BANK RESOLUTIONS 11

share of these assets increases, they increase the ex-posure of a portfolio to liquidity risk. The ratio ofloan losses to total industry loans has been risingsince 1960. Loan losses decreased moderately in1992, but the ratio of loan losses is still high com-pared with periods before 1960. During the 1980sbanks also reduced liquidity as cash, and cash duefrom other depositories, fell by one-half from 18percent of assets in 1980 to 9 percent in 1990.

Incentives for IncreasedRisk in Investments

Corporate borrowers had long been the mainstays ofcommercial bank lending and provided a goodsource of income. Banks typically charged theseborrowers 100 basis points (1 percentage point) overthe cost of funds. Blue-chip corporations with su-perior credit ratings soon found that uninsured in-vestment banks could provide them with access tothe commercial paper market—borrowers could at-tend to their short-term credit needs through corpo-rate bonds. As a result, corporate bonds increaseddramatically during the 1970s. By the end of the1970s, corporations had obtained $124 billionthrough debt financing. In addition, investmentbanks gave corporate borrowers more access tocommercial paper. They began to offer borrowersmedium-term notes and other sources of credit, aswell as making available to firms the ability to in-sure against large changes in equity value.

Rapid gains in telecommunications and comput-ers helped blue-chip borrowers seek credit else-where. During the 1980s, the volume of commer-cial paper tripled. Between 1960 and 1989, the pro-portion of nonbank commercial paper issued bycommercial firms grew from 10 percent to morethan 75 percent. Banks had little choice but to con-sider alternative types of assets to replace the lostbusiness.

As many of the high-quality assets moved offbank balance sheets, banks were left with fewerlow-risk customers. Moreover, bank profit marginswere challenged on both the asset and liability sidesof the balance sheet through increases in interestexpenses and downward pressures on interest in-

come. These challenges to bank operations movedbanks to pursue riskier management strategies in aneffort to augment returns.9 Before partial deregula-tion in the 1980s, regulations limited the incentiveand ability of banks to pursue excessively high-riskactivities. When regulations relaxed, it becameincreasingly important that regulators monitor banksafety, soundness, and risk and supervise banks thatposed a risk of loss to the Bank Insurance Fund.

Usually, if investors anticipate that the returnson an investment will vary, they will not lend un-less the expected return is high enough to compen-sate for the risk. It has long been recognized, how-ever, that a fixed-rate deposit insurance system canpose a moral hazard by encouraging excessive risktaking.10 Banks had an extra incentive to increasereturns through riskier instruments since, in effect,any increase in risk was subsidized by the depositguarantee system. The deposit insurance systemsubsidized risk taking by banks because during thisperiod insurance premiums were unrelated to risk offailure. (The Federal Deposit Insurance CorporationImprovement Act of 1991 mandates that insurancepremium rates take into account the risk of loss tothe insurance fund.)

Evidence of Increased RisksAssociated with Returns to Banks

Investment risk is defined as potential variation inexpected returns to the investor. The variance (astatistical measure of variation) of both the returnon assets and return on equity of banks increasedthroughout the 1980s, indicating the increased riski-ness associated with bank capital. The popular per-ception that the 1980s were marked by a dramaticincrease in banking risks is reinforced by an exami-

9. See Frederick T. Furlong and Michael C. Keeley, "Capital Regula-tion and Bank Risk-Taking: A Note," Journal of Banking andFinance (November 1989), pp. 883-891.

10. See Michael C. Keeley, "Deposit Insurance, Risk and MarketPower in Banking," American Economic Review (December 1990),pp. 1183-1200. Keeley concludes that the recent increase in bankfailures can be attributed to a rise in competition (resulting fromderegulation), causing franchise value to decline and creating anincentive for increased risk taking.

12 THE CHANGING BUSINESS OF BANKING June 1994

nation of the total variance of bank stock returns.11

From 1979 to 1990, the average return on bankstocks of a sample of 84 large bank holding compa-nies fell in relation to a sample of nonfinancialstocks and government bonds; at the same time, thevariance of stock returns increased.

Many banks began to seek returns in this com-petitive and fast-moving environment from whatproved to be not only risky but ill-advised invest-ments. At a time when competition was escalating,large banks, hit hardest by the loss of blue-chip cus-tomers, may have been tempted to pursue riskierforms of investment. The evidence shows that non-performing loans constituted about 2 percent of as-sets for the largest banks (banks with assets greaterthan $10 billion) through 1985 and rose to 2.5 per-cent on average for the last half of the decade. Bycontrast, banks with assets of less than $100 billionhad 1.5 percent of their assets invested in nonper-forming loans, falling to 1 percent by 1990. Twoexamples of investments that caused significantlosses—primarily for big banks with the technologyand access to these markets-were loans to develop-ing countries and junk bonds.12

Debt in Developing Countries. Mexico, Brazil,Chile, Argentina, and other developing countriesborrowed tens of billions of dollars from U.S. banksto finance social programs and oil imports in the1970s. These loans were fueled in part by the largeamount of money placed in international banks byoil-exporting countries after the oil-price rises in the1970s.13 U.S. banks required little or no collateralfor these loans. Many were based on tenuous as-sumptions about economic growth in developingcountries and as a gesture of international coopera-tion.

Banks clearly misread the borrowers' ability torepay. As time passed, the burden of debt repay-

11. Jonathan A. Neuberger, "Bank Stock Risk and Return," FederalReserve Bank of San Francisco Weekly Letter, no. 91-38 (Novem-ber 1, 1991).

12. See Vaughan and Hill, Banking on the Brink, p. 33.

13. David S. Holland, "The Bank and Thrift Crises-A Retrospective,"FDIC Banking Review, vol. 6, no. 1 (Spring/Summer 1993).

ment as a percentage of national income climbedsteadily. In the early 1980s, U.S. banks began tolend more funds to these countries in an effort tosalvage what would have been a guaranteed default.In 1982, Mexico, Brazil, and Argentina demandedrescheduling of their payments. By the mid-1980s,developing countries owed foreign investors ap-proximately $400 billion. U.S. money center banks—those holding more than $10 billion in assets withaccess to international markets—held about $50 bil-lion of Third-World debt. In 1987, at the request ofbank regulators, U.S. banks wrote off as lossesabout $40 billion in loans to developing countries.Compensation for these debt losses was especiallynoticeable because the return on assets for the bank-ing industry fell from 0.61 percent in 1986 to 0.09percent in 1987. By the early 1990s, the debt bur-den for many developing countries had been easedthrough debt restructuring, thereby reducing theproblem for U.S. banks.

Junk Bonds. So-called "junk" bonds are high-yielding but low-rated corporate debt securities.These bonds carry ratings of BB or lower, becausethey are judged to be of above-average default risk.In the 1980s, many companies issued them to fi-nance corporate acquisitions or to repay debt obliga-tions. Banks traditionally played an important rolein the financing of leveraged buyouts (LBOs) be-cause client information gave them an advantage.14

By requiring access to a client's cash flow and anadequate valuation of assets, traditional investmentsin LBOs were less risky than those that took placeduring the 1980s. Commercial credit companieswilling to take greater risks by allowing lower creditstandards began to compete very successfully withbanks. Equity yields of 35 percent to 50 percentand subordinated debt yields of 25 percent to 40percent were not uncommon for these investmentsin the early 1980s. With such high returns avail-able, this financial instrument grew enormously. Infact, the volume of junk bonds grew from $1.6 bil-lion to more than $300 billion before the collapse ofthe junk bond market in 1989.

14. Traditionally, banks had an advantage over virtually all otherintermediaries in information-intensive lending.

CHAPTER TWO TRENDS AND CONDITIONS UNDERLYING BANK RESOLUTIONS 13

Banks fueled this expansion by encouraginghigh interest rates and fees that amounted to 1 per-cent or 2 percent of principal. Concerns about cred-itworthiness began to erode. Loan officers foundthat they could more than double their banks' earn-ings by concentrating on LBOs rather than lendingto investment-grade (more creditworthy) firms.15

The subsequent downturn in this market imposedheavy losses on banks participating in these deals.

The Growth of Off-Balance-Sheet Activities: A SignificantSectoral Trend

The business of banking has changed considerablyover the last two decades. An increasing amount ofthe business done by banks does not show up aseither assets or liabilities—that is, it is not recordedon balance sheets. In fact, many of the traditionalactivities of commercial banking have moved offthe balance sheet. For example, a standby letter ofcredit is a financial instrument in which a bankguarantees a loan made by some third party, ratherthan funding the loan with depositor funds. Eventhough the loan does not appear on the asset side ofthe bank's balance sheet, the risk of loss is virtuallythe same as if it did.

Other examples of major off-balance-sheet ac-tivities include securitization (discussed above), loancommitments, and the rapidly growing category ofderivative instruments (primarily swaps and op-tions). Banks use loan commitments essentially likea line of credit to fund planned investments. Firmsanticipating needs for funds will arrange for a loancommitment. Derivative instruments involve thetrading (swapping) of risks. A common example ofa derivative security is an interest rate swap inwhich two parties exchange sequences of interestpayments. A foreign exchange contract involvingthe exchange of a sequence of interest paymentsamong different currencies is another derivative in-strument. Option contracts give the purchaser theright to buy or sell a specified amount of a financialasset at a particular price on or before a future dateof expiration.

In 1989, off-balance-sheet items accounted forapproximately four times the volume of balance-sheet items.16 Income from off-balance-sheet activi-ties (fee income) as a percentage of total income be-fore operating costs grew from 20 percent in 1979to 33 percent in 1991. Despite having a decreasedshare of industry assets on their balance sheets,banks remain important for originating information-intensive lending. Commercial banks remain in-volved (directly or indirectly) in the lending ofshort-term working capital and therefore continue toprovide an important service to businesses.17

Some regulators have expressed particular con-cern about the risk exposure of commercial banksoperating in the market for derivative instruments.18

These markets are largely unregulated, and as theyevolve and technology advances, new types of secu-rities continue to be developed at a rapid pace.There is also uneasiness that activity in derivativesis concentrated among a small group of very largecommercial banks. Substantial losses on trading inderivatives could force a large bank into insolvency,which could affect derivatives markets unfavorablyand perhaps damage money and exchange rate mar-kets as well.19 The data on derivative instrumentsare still preliminary and several agencies are evalu-ating these concerns.20

In addition to the recent structural changes inthe financial sector and the incentives to increasereturns by investing in riskier ventures, a series ofadverse economic events put more stress on the fi-nancial system. Not only did interest rates risesharply and the junk bond market collapse in the1980s, but the economy underwent periods of reces-sion, rapid inflation and deflation of energy prices,

15. Vaughan and Hill, Banking on the Brink.

16. Eileen Maloney and George Gregorash, "Banking 1989: Not Quitea Twice Told Tale," Economic Perspectives, Federal Reserve Bankof Chicago (July-August 1990).

17. Boyd and Gertler, "U.S. Commercial Banking."

18. E. Gerald Corrigan, "The Risk of a Financial Crisis," in MartinFeldstein, ed., The Risk of Economic Crisis (Chicago: Universityof Chicago Press, 1991), pp. 44-53.

19. Boyd and Gertler, "U.S. Commercial Banking," pp. 12-14.

20. General Accounting Office, Financial Derivatives: Actions Neededto Protect the Financial System (May 18, 1994).

14 THE CHANGING BUSINESS OF BANKING June 1994

and a stock market "break." Banks tied to regionalmarkets suffered from declines in agriculture, en-ergy, and real estate.

Macroeconomic Conditions,Regional Disparities,and Asset Losses

General economic conditions affect the financialcondition of bank customers and therefore influencebank profitability. The 1970s and 1980s share simi-lar business cycle patterns. Both decades beganwith modest recessions that grew more serious andwere followed by booms. The similarities in termsof lost production and unemployment are striking.But the recession of the 1980s was marked by moresevere regional dislocations than that of the 1970s.Some macroeconomists have characterized the eco-nomic environment of the 1980s as one big rollingregional recession hitting different geographic areasat different times over the decade. Lost steel pro-duction in the early 1980s preceded the oil and farmsector problems of the middle 1980s, which pre-ceded the economic problems in New England andCalifornia in the late 1980s.

There were periods in the 1980s when the valueof the dollar was high in relation to other curren-cies, export trade suffered, and industries such asagriculture, which rely heavily on exports, declined.During these periods, foreign competition increasedagainst some of the more labor-intensive industriesin which lower labor costs gave foreign firms acomparative advantage. In addition, changes inworld prices affected the demand for the products ofsome important domestic industries. For example,the steel and energy industries were hit by a price-induced decline in consumer demand for thosegoods.

Regional Variation in Bank Failure

During the 1987-1992 period, the FDIC resolvedsome 7 percent of those banks in existence at thebeginning of 1987, or 1,049 in all (see Table 1).