Embed Size (px)

DESCRIPTION

‘Working for Desirable Future’ : Transparency and participation in electricity sector planning in Thailand. Suphakit Nuntavorakarn Healthy Public Policy Foundation, THAILAND 26th September 2011 FESTI International Conference, Bishkek. Installed Capacity by Type of Producers, April 2011. - PowerPoint PPT Presentation

Citation preview

‘Working for Desirable Future’:Transparency and participation

in electricity sector planning in ThailandSuphakit Nuntavorakarn

Healthy Public Policy Foundation, THAILAND26th September 2011 FESTI International Conference, Bishkek

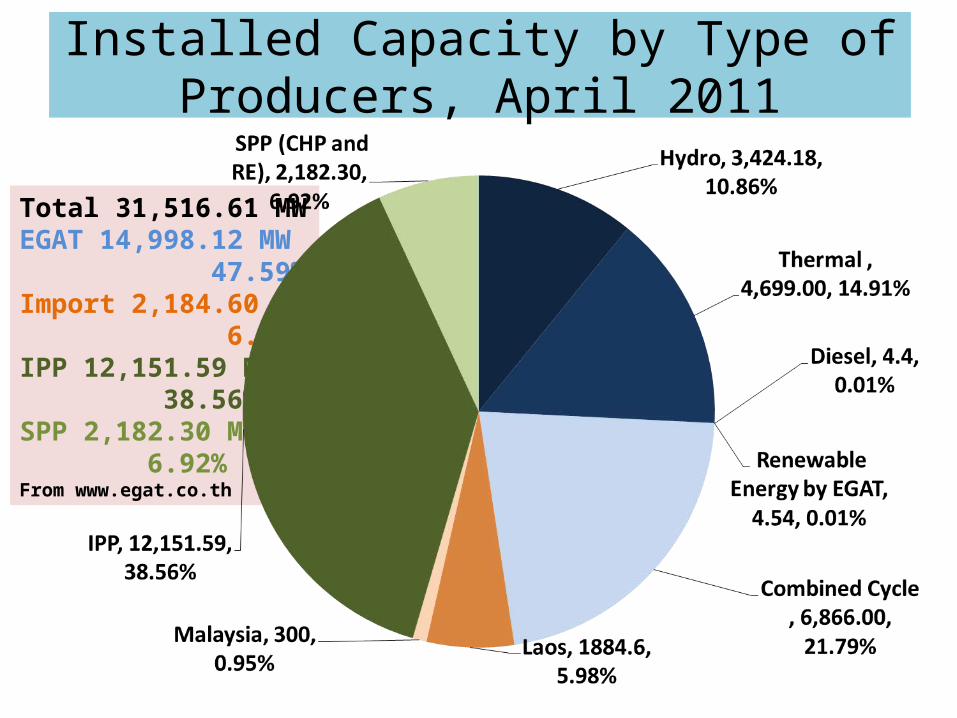

Installed Capacity by Type of Producers, April 2011

Total 31,516.61 MWEGAT 14,998.12 MW 47.59%Import 2,184.60 MW 6.93%IPP 12,151.59 MW 38.56%SPP 2,182.30 MW 6.92%From www.egat.co.th

Power Development Plan (PDP)• PDP is the long-term strategic plan of the Thai power

sector (15-20 years timeframe)• PDP determines the future investment on power

generation - how many and which types of power plant – and the transmission network.

– For example, total investment of PDP2010 120 billion USD

• So PDP also determines the future impacts of the power sector, including environmental, economic, social, and health impacts

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

55,000

60,000

65,000

70,000

2553 2554 2555 2556 2557 2558 2559 2560 2561 2562 2563 2564 2565 2566 2567 2568 2569 2570 2571 2572 2573

ดีเซล พลังงานหมุนเวียน น้ำ�า มันเตา ซื� อต่างประเทศก๊าซ ธรรมชาติ ถ่านหินน้ำา เข้า ลิกไ นต์ นิวเคลียร์ พลังน้ำ�า

MWMW

ปีปี

45%45%

49%49%

54%54%

61%61%64%64%68%68% 64%64%65%65% 66%66% 67%67% 63%63% 60%60%57%57%

51%51%51%51%

47%47%45%45%

44%44% 43%43% 43%43% 42%42%

5%5% 7%7% 7%7% 7%7% 7%7% 7%7% 7%7% 7%7% 7%7% 8%8% 8%8% 9%9% 9%9% 12%12% 11%11% 11%11% 13%13% 13%13% 15%15% 15%15% 17%17%

7%7% 7%7% 6%6% 6%6% 5%5% 5%5% 5%5% 5%5% 5%5% 5%5% 5%5% 5%5% 4%4% 4%4% 4%4%

5%5% 5%5% 6%6% 6%6% 7%7% 7%7% 7%7%7%7% 8%8%

8%8% 8%8% 8%8%

4%4% 4%4% 6%6% 8%8% 7%7% 7%7% 8%8% 8%8% 8%8%4%4%

6%6% 8%8% 10%10% 11%11% 12%12% 13%13% 14%14% 15%15% 15%15% 15%15% 16%16% 17%17%17%17%

6%6%7%7%7%7%

11%11% 10%10% 10%10% 9%9% 9%9% 9%9% 8%8% 9%9% 9%9% 9%9% 9%9% 8%8% 8%8% 8%8% 7%7% 7%7% 7%7% 7%7% 6%6% 6%6% 6%6%

18%18%18%18%

18%18%18%18%7%7%

7%7%7%7%

8%8%

7%7%

5%5%

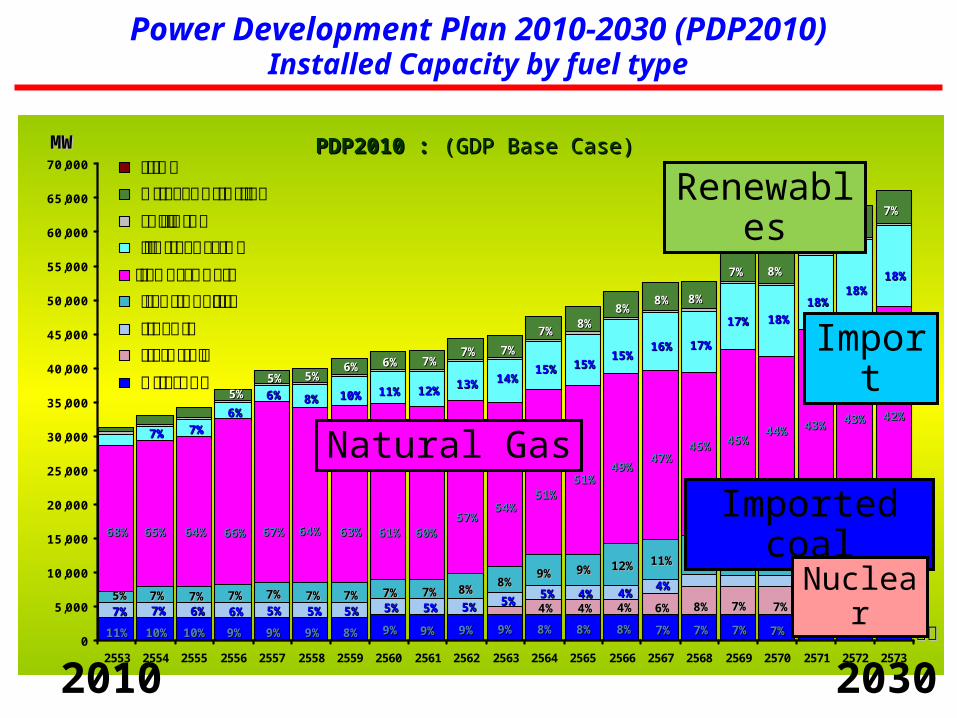

PDP2010 :PDP2010 : ( (GDP Base CaseGDP Base Case))

Power Development Plan 2010-2030 (PDP2010)Installed Capacity by fuel type

Renewables

Import

Natural GasImported coal

Nuclear

2010 2030

Drivers and institutional improvements on PDP

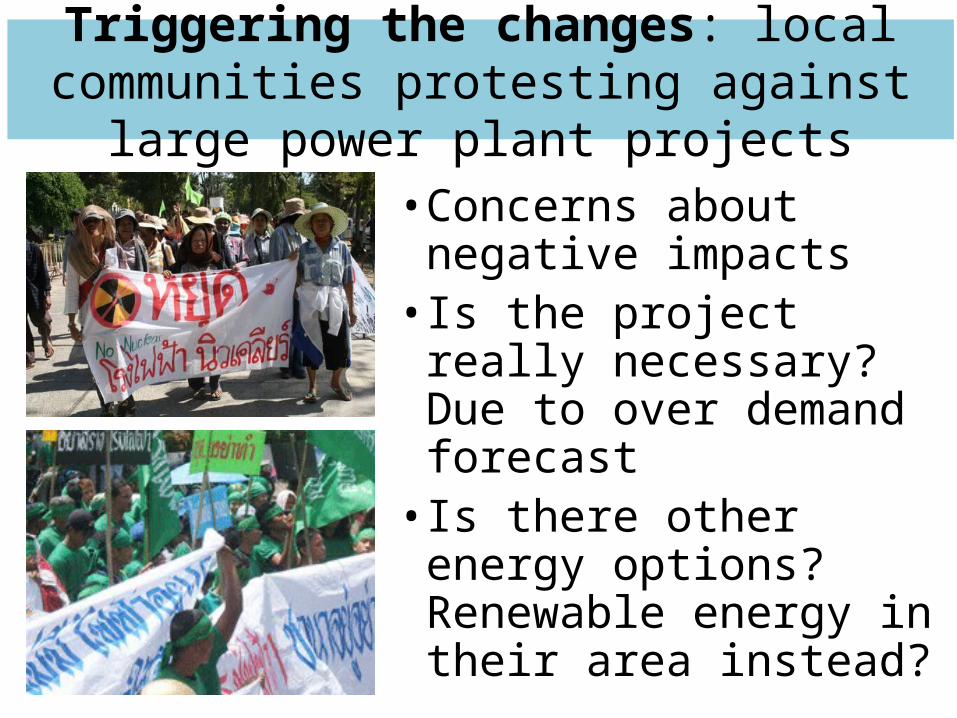

Triggering the changes: local communities protesting against large power plant projects

• Concerns about negative impacts

• Is the project really necessary? Due to over demand forecast

• Is there other energy options? Renewable energy in their area instead?

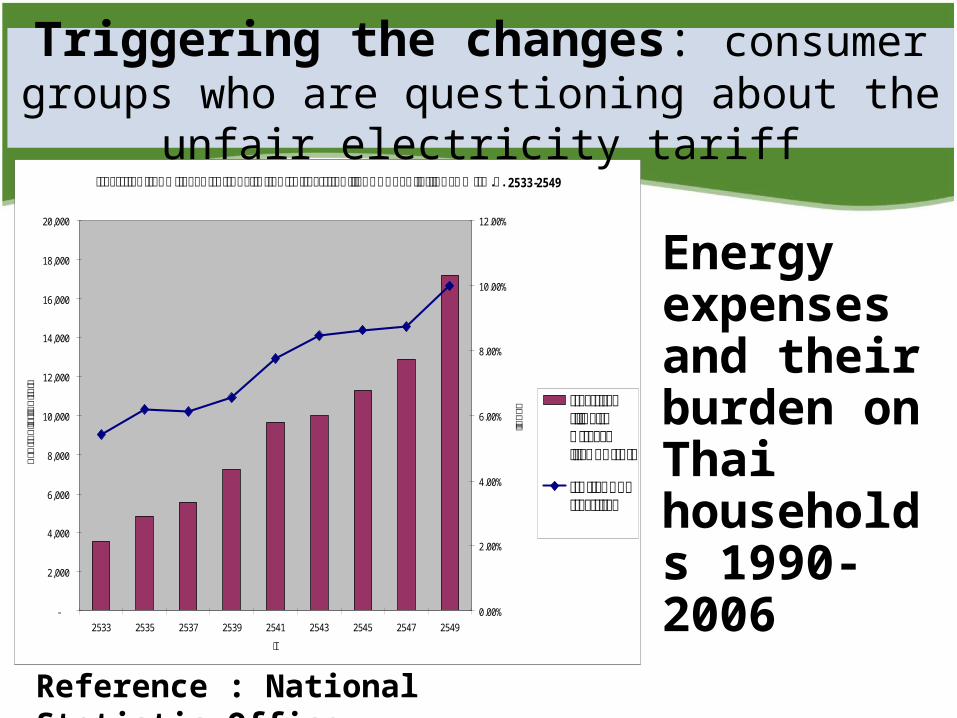

ค่า ใ ช้ จ่ายด้านพลังงา นต่อปีและ สัดส่วนต่อค่า ใ ช้ จ่ายท้ั งหมดของครัวเรือนไ ทย ปีพ.ศ. 2533-2549

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

2533 2535 2537 2539 2541 2543 2545 2547 2549

ปี

บาทต่

อครัว

เรือน

ต่อปี

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

ร้อยล

ะ ค่าใ ช้จ่ายเก่ียวกับพลังงานทั� งหมดต่อปี

สัดส่วนของค่าใ ช้จ่าย

Reference : National Statistic Office

Energy expenses and their burden onThai households 1990-2006

Triggering the changes: consumer groups who are questioning about the unfair electricity tariff

Academic contributions andpublic communication

• Information and analysis on the electricity sector- to create basic understanding for different social sector and

to get their attentions on various issues about PDP

• Development and impact assessment on Alternative Power Development Plans

- to create ‘Choice Awareness’ on many energy options andthese can be discuss deliberately as a social learning process

• Electricity Governance Assessment- focus on transparency, public participation, and accountability in the

Thai power sector

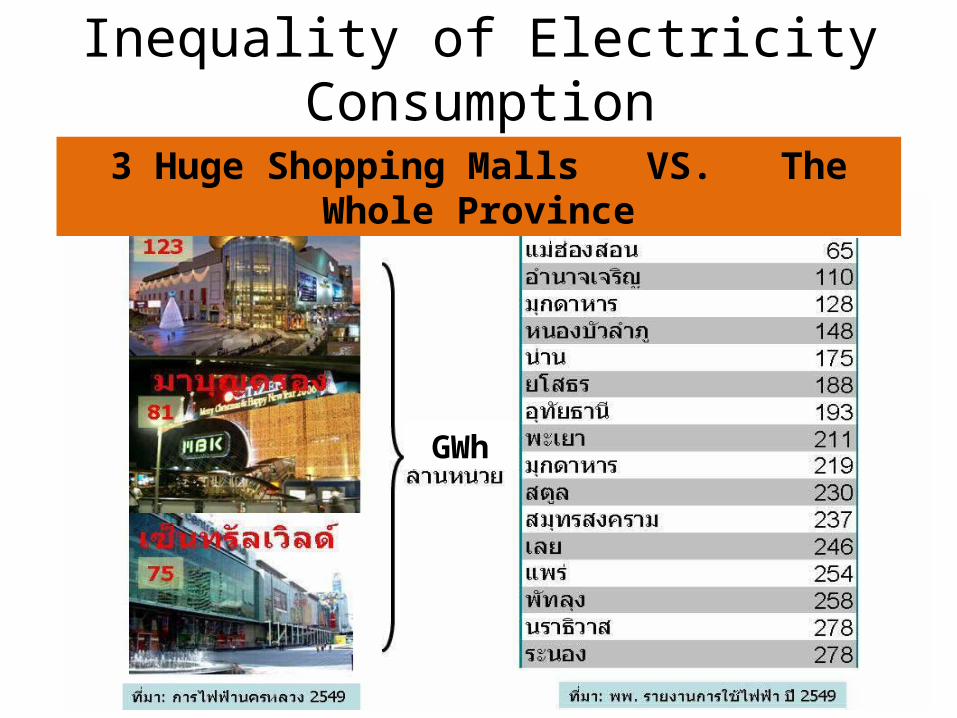

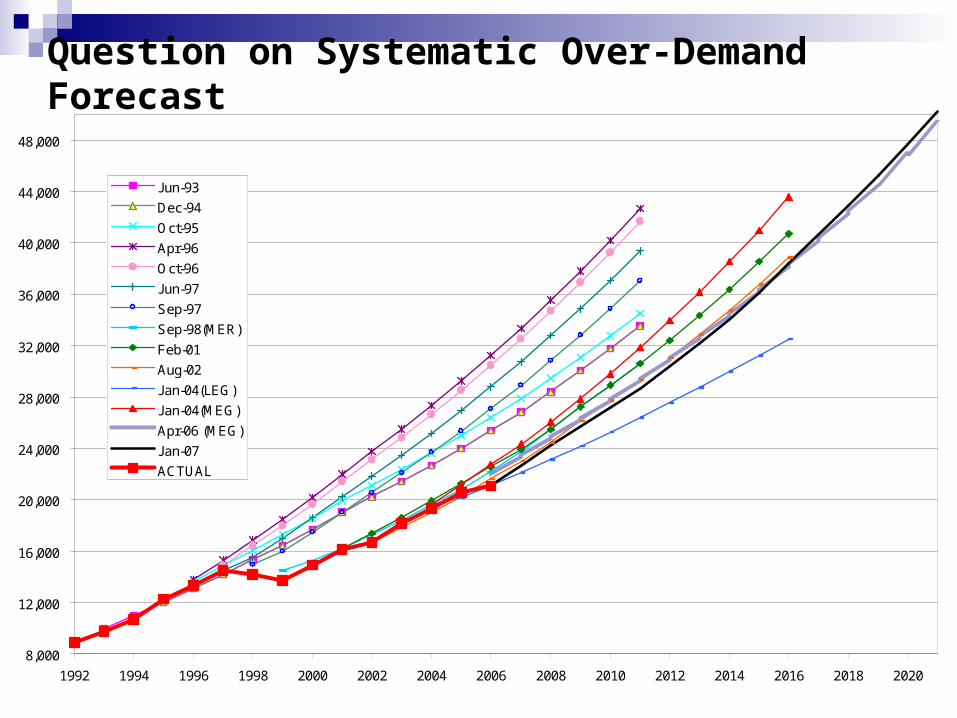

GWh

GWh3 Huge Shopping Malls VS. The Whole Province

Inequality of Electricity Consumption

8,000

12,000

16,000

20,000

24,000

28,000

32,000

36,000

40,000

44,000

48,000

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Jun-93Dec-94Oct-95Apr-96Oct-96Jun-97Sep-97Sep-98(MER)Feb-01Aug-02Jan-04(LEG)Jan-04(MEG)Apr-06 (MEG)Jan-07ACTUAL

Question on Systematic Over-Demand Forecast

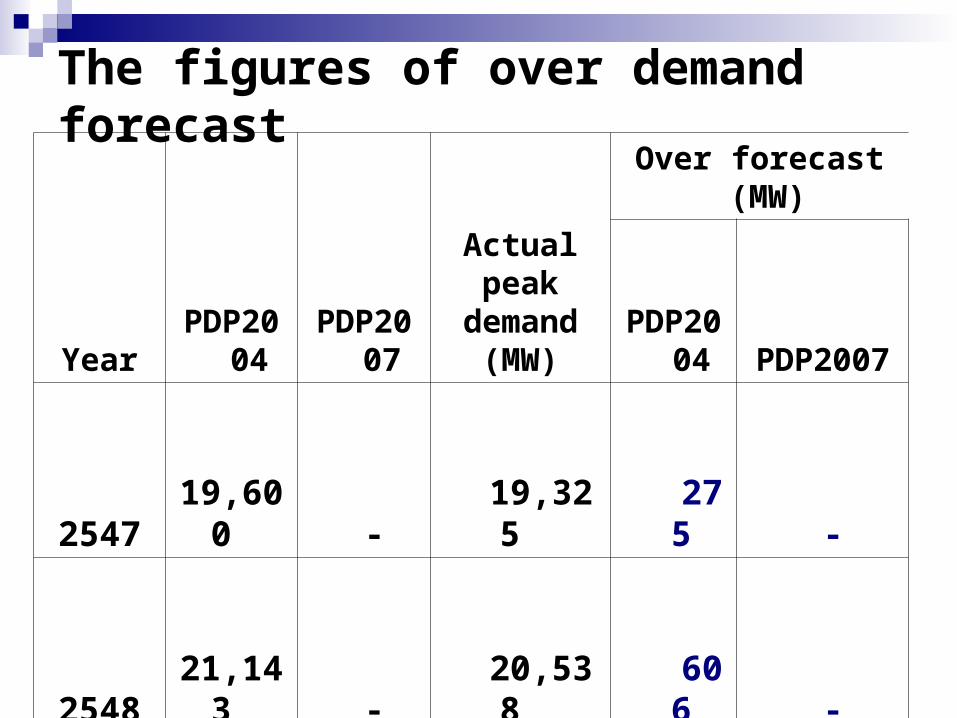

The figures of over demand forecast

YearPDP2

004PDP2

007

Actual peak

demand (MW)

Over forecast (MW)

PDP2004

PDP2007

2547

196,

00 -

1932

5

27

5 -

2548

211,

43 -

2053,

8

60

6 -

2549

227,

38 -

2106,

4

1,67

4 -

2550

243,

44

225,

86

2258,

6

1,75

8 -

2551

260,

48

2395

7

2256,

8

3,48

0

1,38

9

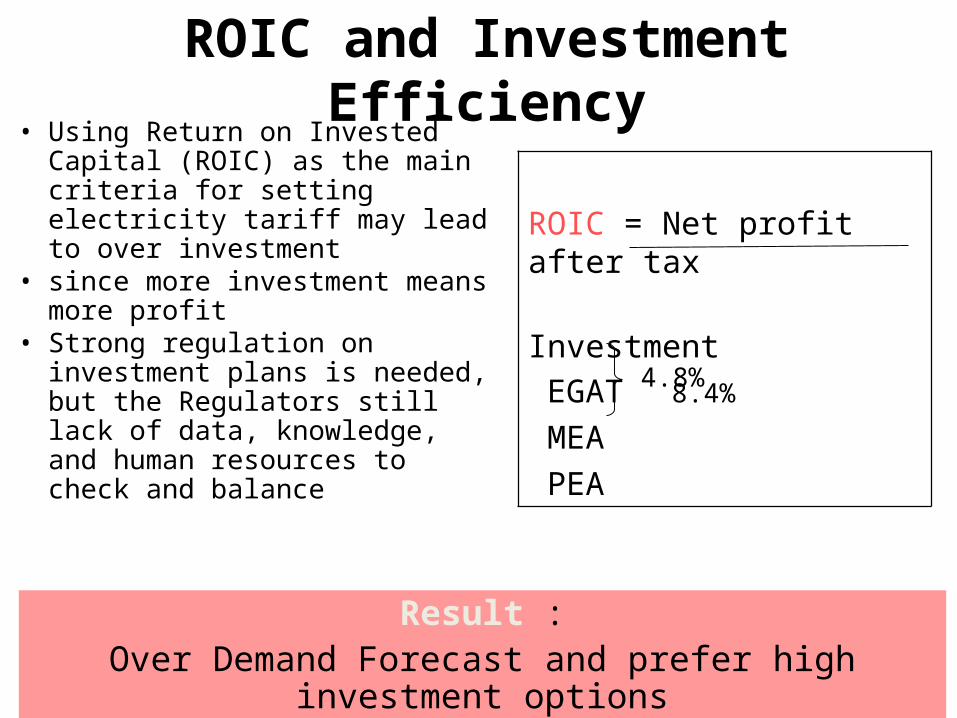

• Using Return on Invested Capital (ROIC) as the main criteria for setting electricity tariff may lead to over investment

• since more investment means more profit

• Strong regulation on investment plans is needed, but the Regulators still lack of data, knowledge, and human resources to check and balance

ROIC and Investment Efficiency

ROIC = Net profit after tax Investment EGAT 84. % MEA PEA

48.%

Result :Over Demand Forecast and prefer high investment

options

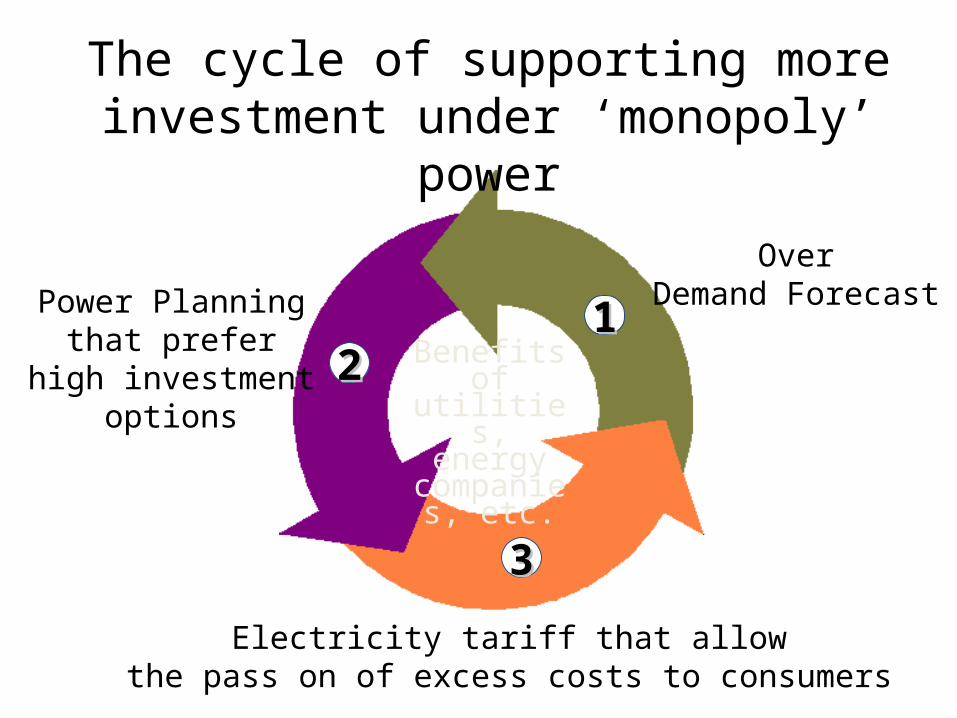

The cycle of supporting more investment under ‘monopoly’ power

OverDemand ForecastPower Planning

that preferhigh investment

options

Electricity tariff that allowthe pass on of excess costs to consumers

Benefits of utilities, energy companies, etc.

1122

33

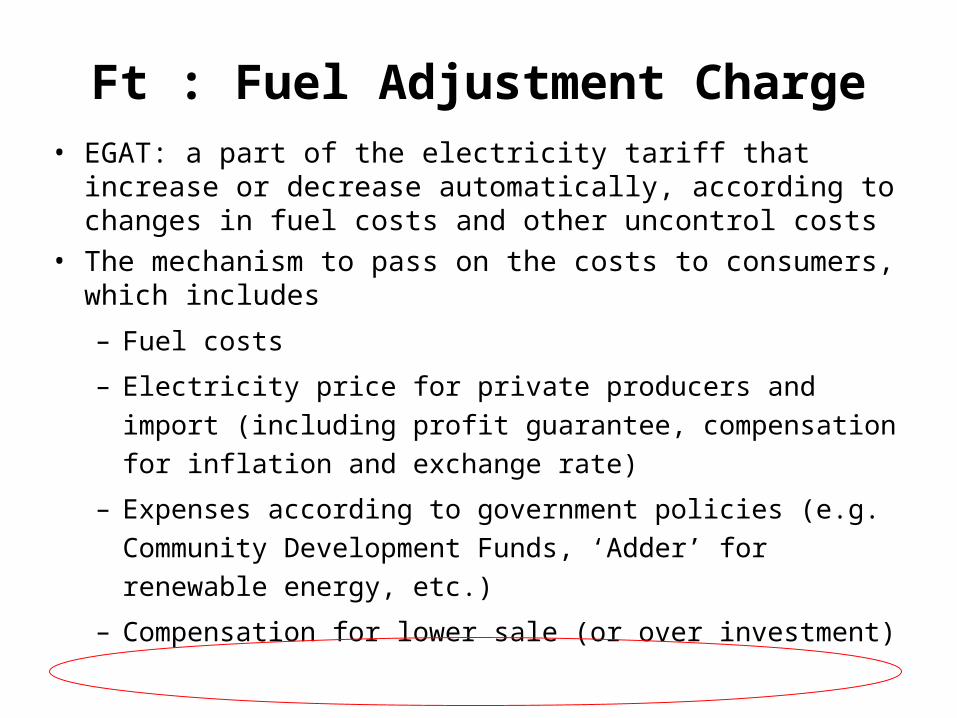

Ft : Fuel Adjustment Charge• EGAT: a part of the electricity tariff that increase or

decrease automatically, according to changes in fuel costs and other uncontrol costs

• The mechanism to pass on the costs to consumers, which includes– Fuel costs– Electricity price for private producers and import

(including profit guarantee, compensation for inflation and exchange rate)

– Expenses according to government policies (e.g. Community Development Funds, ‘Adder’ for renewable energy, etc.)

– Compensation for lower sale (or over investment)

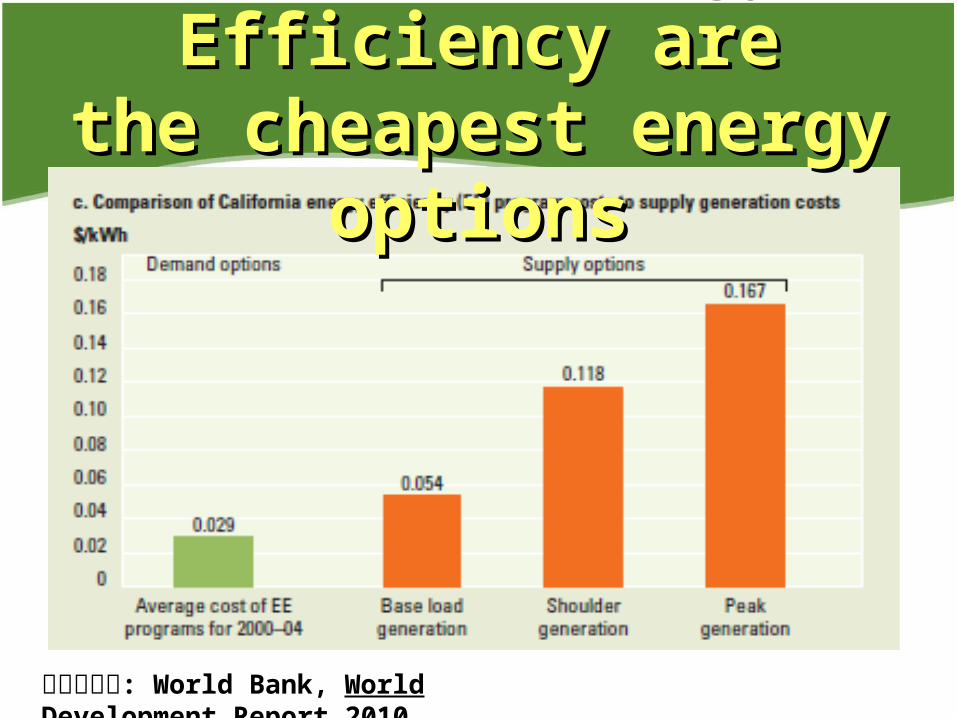

DSM and Energy DSM and Energy Efficiency areEfficiency are

the cheapest energy the cheapest energy optionsoptions

ท่ีมา: World Bank, World Development Report 2010

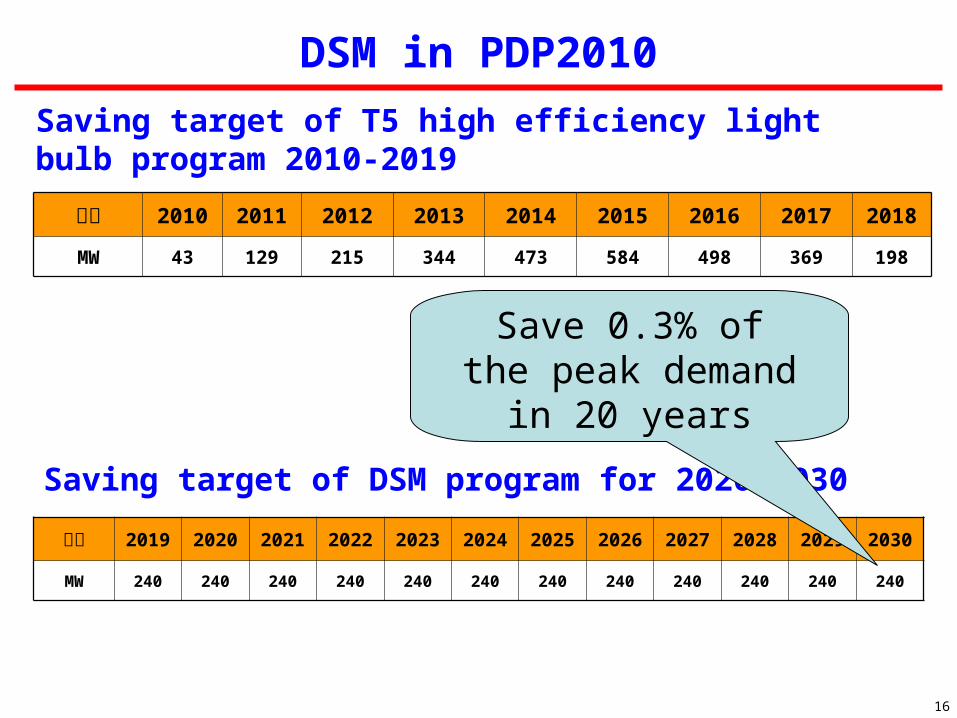

16

DSM in PDP2010

ปี 2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

MW 240 240 240 240 240 240 240 240 240 240 240 240

Saving target of T5 high efficiency light bulb program 2010-2019

ปี 2010 2011 2012 2013 2014 2015 2016 2017 2018MW 43 129 215 344 473 584 498 369 198

Saving target of DSM program for 2020-2030

Save 0.3% ofthe peak demand in

20 years

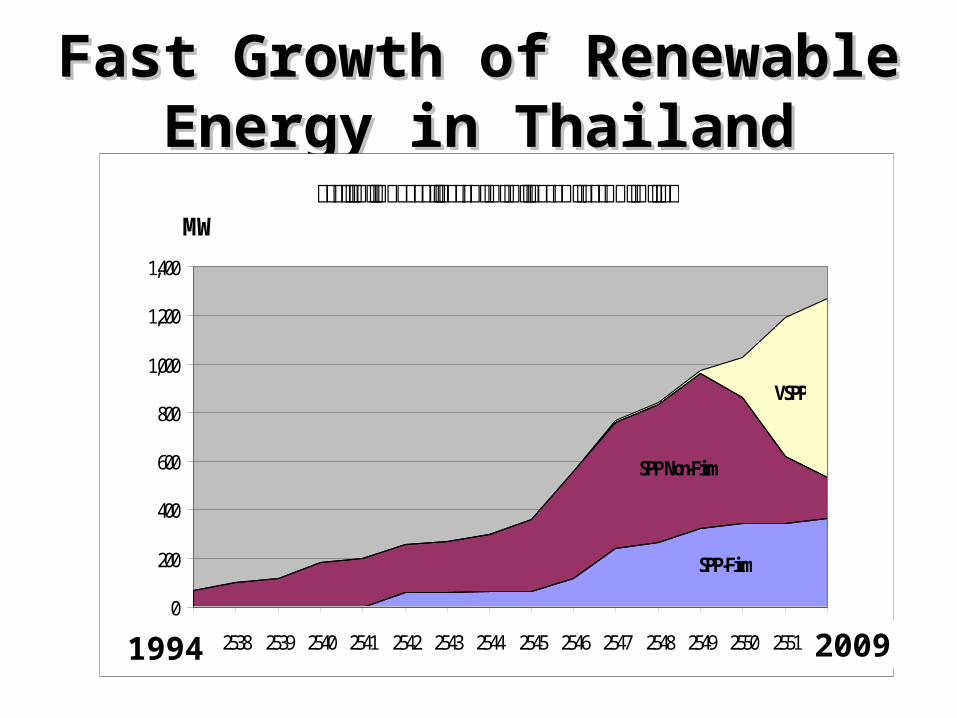

Fast Growth of Fast Growth of Renewable Energy in Renewable Energy in

ThailandThailandการเพ่ิมข้ึนของกำาลังการผลิตติดต้ังจากพลังงานหมุนเวียน

SPP-Firm

SPP Non-Firm

VSPP

0

200

400

600

800

1,000

1,200

1,400

2537 2538 2539 2540 2541 2542 2543 2544 2545 2546 2547 2548 2549 2550 2551 2552

MW

1994 2009

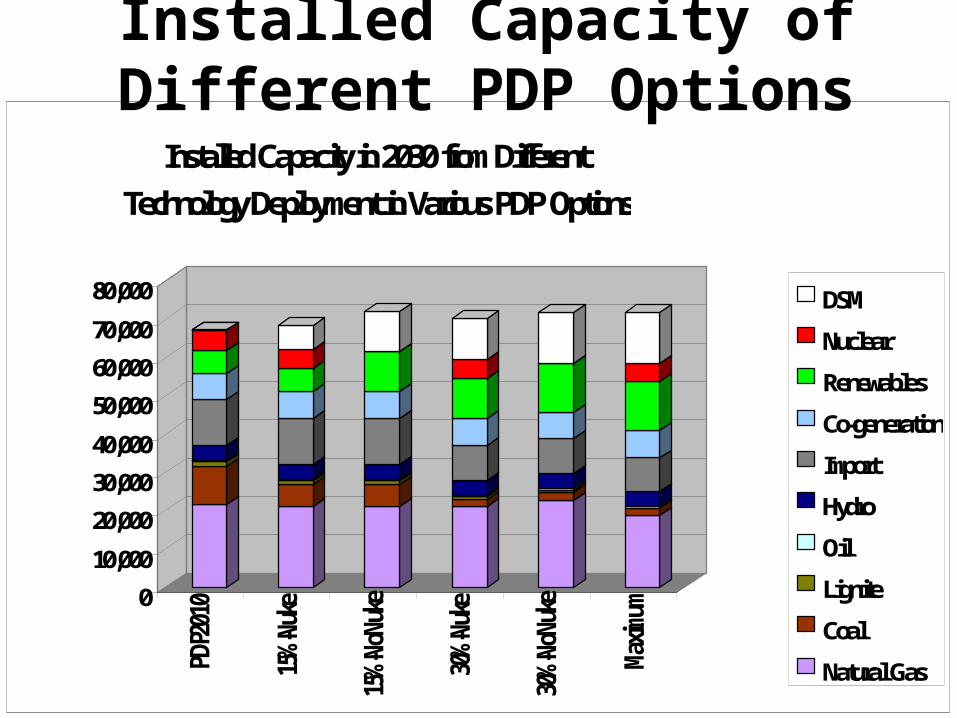

Example of PDP-Alternative

010,00020,00030,00040,00050,00060,00070,00080,000

PDP20

10

15%-Nu

ke

15%-No

Nuke

30%-Nu

ke

30%-No

Nuke

Maxim

um

Installed Capacity in 2030 from Different Technology Deployment in Various PDP Options

DSMNuclearRenewablesCo-generationImportHydroOilLigniteCoal Natural Gas

Installed Capacity of Different PDP Options

32.3

14.5

17.910.78.87.50.4

30.5

8.4

17.510.58.67.39.3

29.0

8.0

16.69.914.4-14.7

29.8

2.912.810.214.87.115.1

31.4

2.812.510.017.7-18.5

25.72.812.510.017.77.018.4

-

20.0

40.0

60.0

80.0

100.0

PDP20

10

15%-Nu

ke

15%-No

Nuke

30%-Nu

ke

30%-No

Nuke

Maxim

um

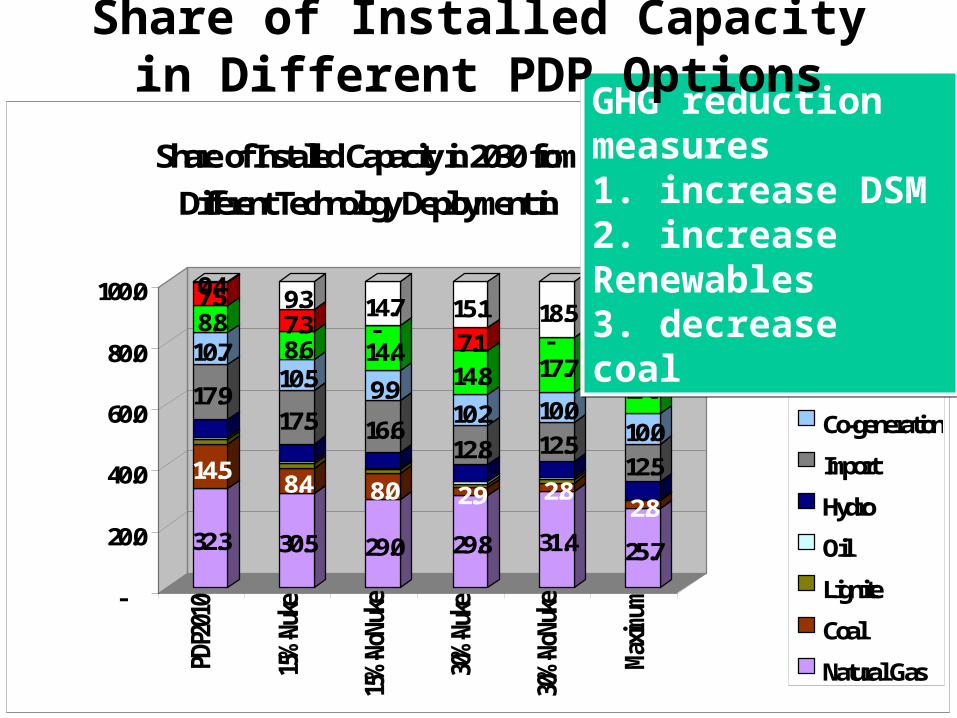

Share of Installed Capacity in 2030 from Different Technology Deployment in

DSMNuclearRenewablesCo-generationImportHydroOilLigniteCoal Natural Gas

GHG reduction measures1 . increase DSM2. increase Renewables3. decrease coal

Share of Installed Capacity in Different PDP Options

050,000

100,000150,000200,000250,000300,000350,000400,000

PDP20

10

15%-Nu

ke

15%-No

Nuke

30%-Nu

ke

30%-No

Nuke

Maxim

um

Energy Generations from Different Technology Deployment in Various PDP Options

DSMNuclearRenewablesCo-generationImportHydroOilLigniteCoal Natural Gas

Energy Generation in Different PDP Options

Comparative Impact Assessment on various

Alternative PDPsEconomics

Environment Social

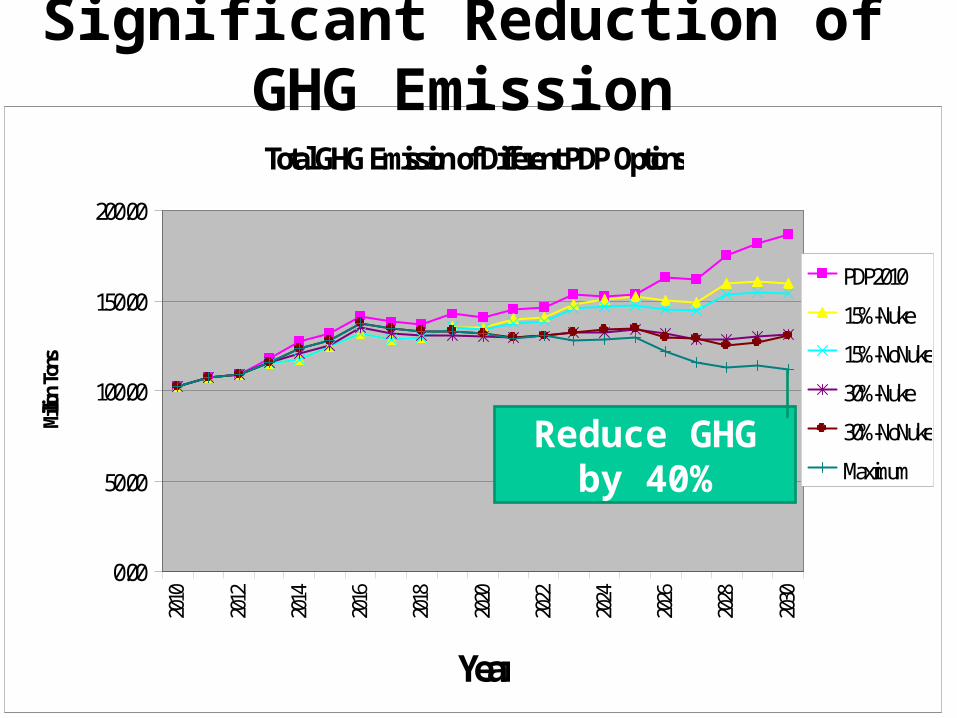

Total GHG Emission of Different PDP Options

0.00

50.00

100.00

150.00

200.00201

0

2012

2014

2016

2018

2020

2022

2024

2026

2028

2030

Year

Million

Tons

PDP201015%-Nuke15%-NoNuke30%-Nuke30%-NoNukeMaximum

Reduce GHG by 40%

Significant Reduction of GHG Emission

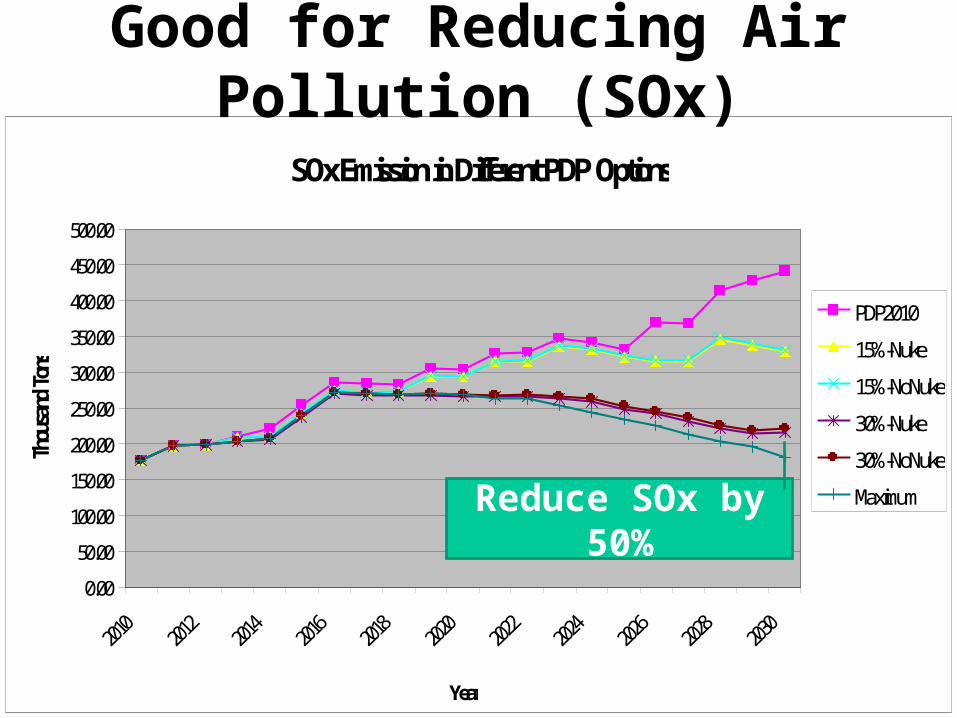

SOx Emission in Different PDP Options

0.0050.00

100.00150.00200.00250.00300.00350.00400.00450.00500.00

Year

Thousa

nd Ton

s

PDP201015%-Nuke15%-NoNuke30%-Nuke30%-NoNukeMaximumReduce SOx by

50%

Good for Reducing Air Pollution (SOx)

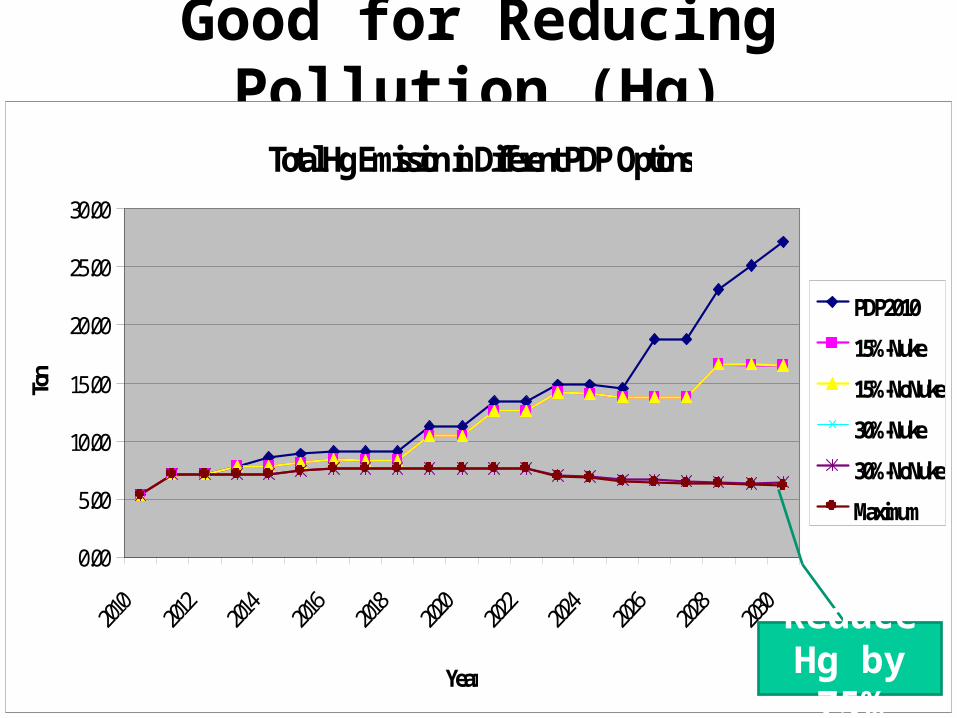

Good for Reducing Pollution (Hg)Total Hg Emission in Different PDP Options

0.00

5.00

10.00

15.00

20.00

25.00

30.00

Year

Ton

PDP201015%-Nuke15%-NoNuke30%-Nuke30%-NoNukeMaximum

Reduce Hg by 75%

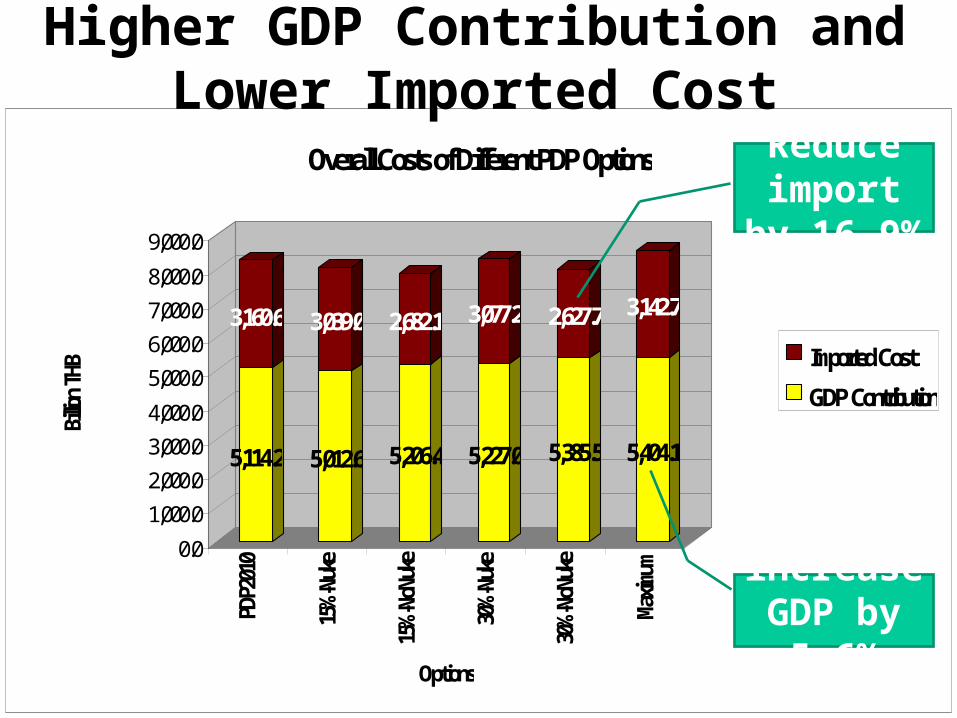

5,114.2

3,160.6

5,012.6

3,039.0

5,206.4

2,682.1

5,227.0

3,077.2

5,385.5

2,627.7

5,404.1

3,142.7

0.01,000.02,000.03,000.04,000.05,000.06,000.07,000.08,000.09,000.0

Billion

THB

PDP20

10

15%-Nu

ke

15%-No

Nuke

30%-Nu

ke

30%-No

Nuke

Maxim

umOptions

Overall Costs of Different PDP Options

Imported CostGDP Contribution

increase GDP by 5.6%

Reduce import

by 16.9%

Higher GDP Contribution and Lower Imported Cost

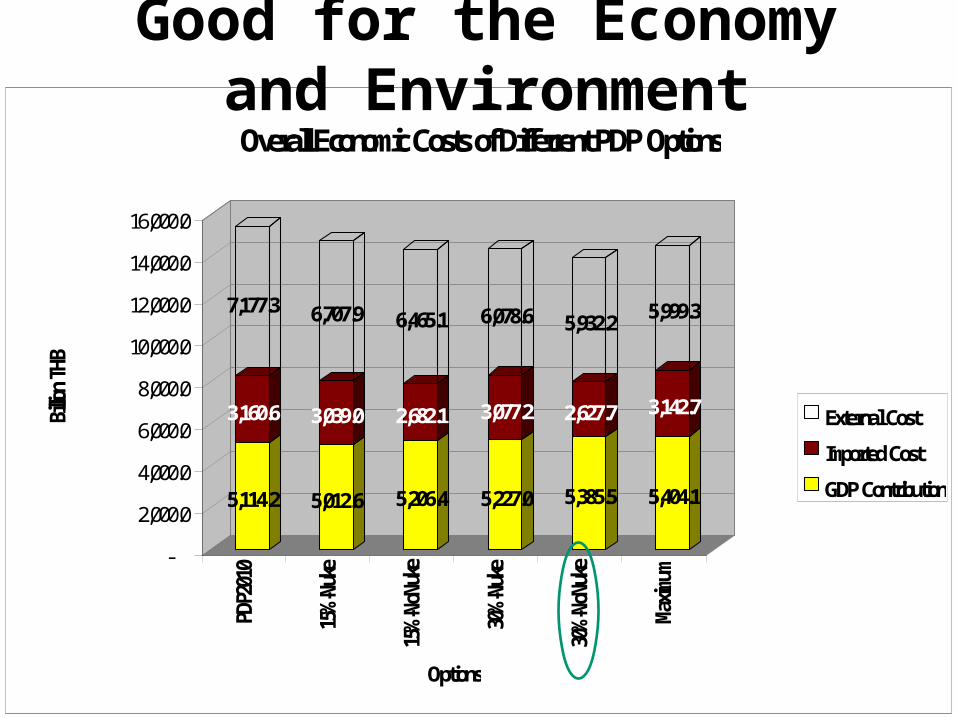

5,114.2

3,160.6

7,177.3

5,012.6

3,039.0

6,707.9

5,206.4

2,682.1

6,465.1

5,227.0

3,077.2

6,078.6

5,385.5

2,627.7

5,932.2

5,404.1

3,142.7

5,999.3

-2,000.04,000.06,000.08,000.0

10,000.012,000.014,000.016,000.0

Billion

THB

PDP20

10

15%-Nu

ke

15%-No

Nuke

30%-Nu

ke

30%-No

Nuke

Maxim

umOptions

Overall Economic Costs of Differrent PDP Options

External CostImported CostGDP Contribution

Good for the Economy and Environment

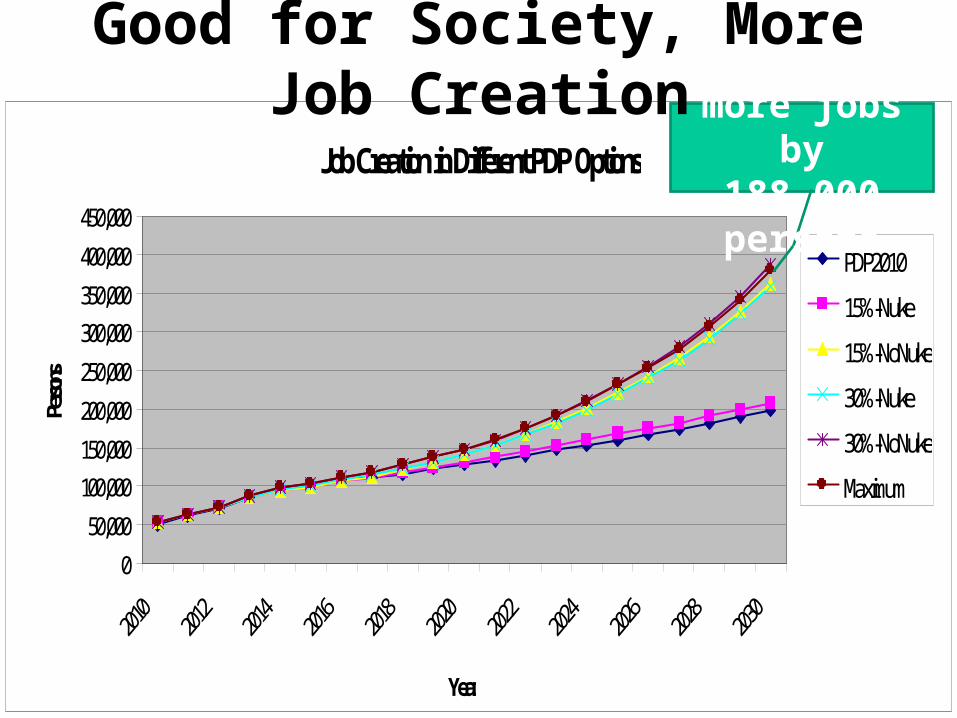

Job Creation in Different PDP Options

050,000

100,000150,000200,000250,000300,000350,000400,000450,000

Year

Perso

ns

PDP201015%-Nuke15%-NoNuke30%-Nuke30%-NoNukeMaximum

Create more jobs

by18800

0 persons

Good for Society, More Job Creation

Institutional Improvements on PDP:The policy network

• Expanding from mainly local communities against projects, NGOs, and some academics

• To different parts of the society, for example, consumer networks, community energy movement, National Human Rights Commission, several Ministries, Senate committee, the regulators, as well as EGAT and Ministry of Energy

• The network itself was transformed from ‘physical’ network to ‘coordinate by contents’ and more open aiming at social learning process on PDP

Institutional Improvements on PDP:The role of private sector

• The group on renewable energy, SPP and VSPP, was rather active, but conservative on pushing for change.

• The large power companies, IPP, have been passive to push for changes.

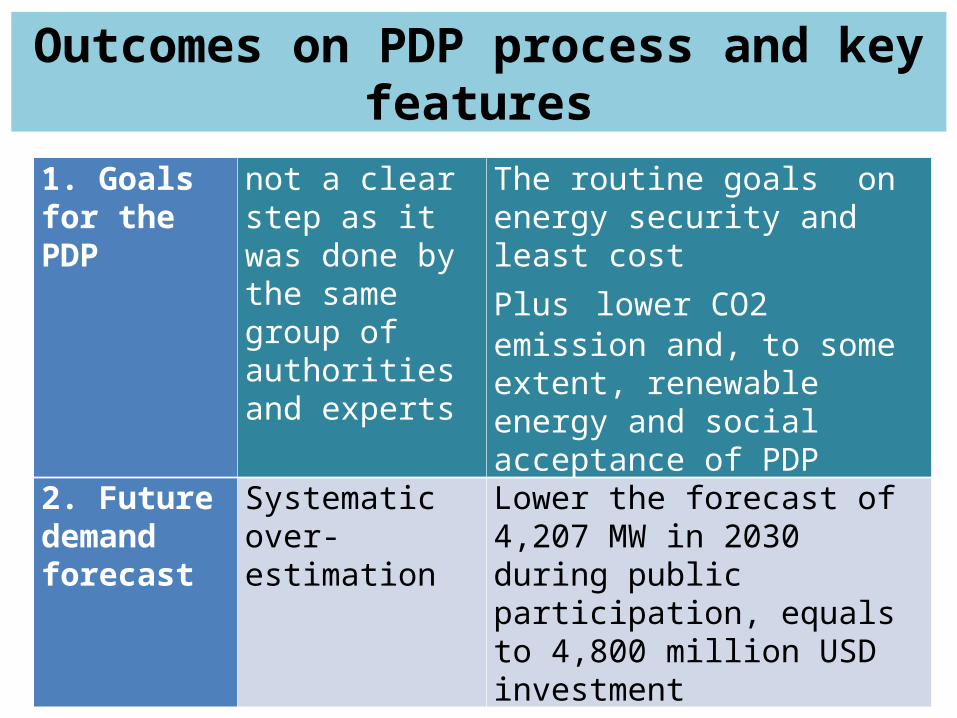

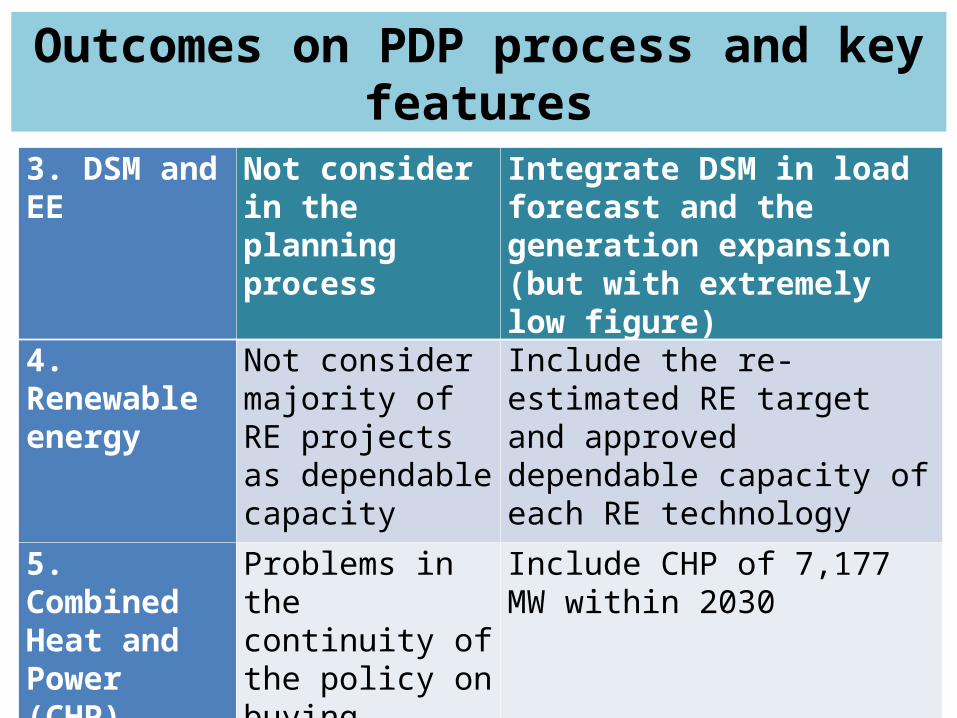

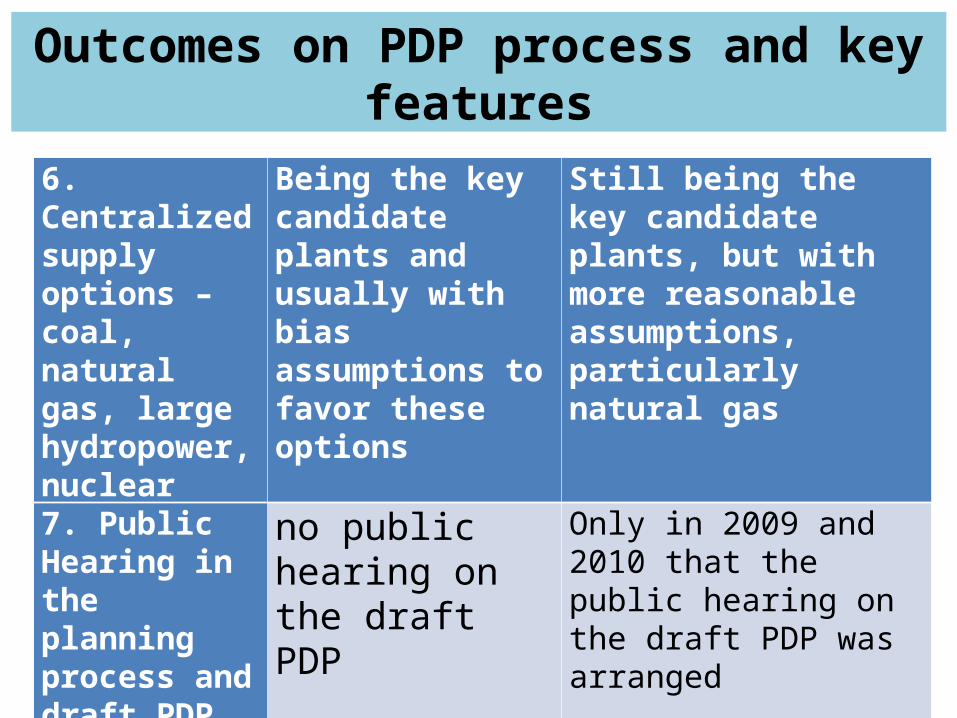

Outcomes on PDP process and key features

1. Goals for the PDP

not a clear step as it was done by the same group of authorities and experts

The routine goals on energy security and least costPlus lower CO2 emission and, to some extent, renewable energy and social acceptance of PDP

2. Future demand forecast

Systematic over-estimation

Lower the forecast of 4,207 MW in 2030 during public participation, equals to 4,800 million USD investment

Outcomes on PDP process and key features

3. DSM and EE Not consider in the planning process

Integrate DSM in load forecast and the generation expansion (but with extremely low figure)

4. Renewable energy

Not consider majority of RE projects as dependable capacity

Include the re-estimated RE target and approved dependable capacity of each RE technology

5. Combined Heat and Power (CHP)

Problems in the continuity of the policy on buying electricity from new CHP projects

Include CHP of 7,177 MW within 2030

Outcomes on PDP process and key features

6. Centralized supply options – coal, natural gas, large hydropower, nuclear

Being the key candidate plants and usually with bias assumptions to favor these options

Still being the key candidate plants, but with more reasonable assumptions, particularly natural gas

7. Public Hearing in the planning process and draft PDP

no public hearing on the draft PDP

Only in 2009 and 2010 that the public hearing on the draft PDP was arranged

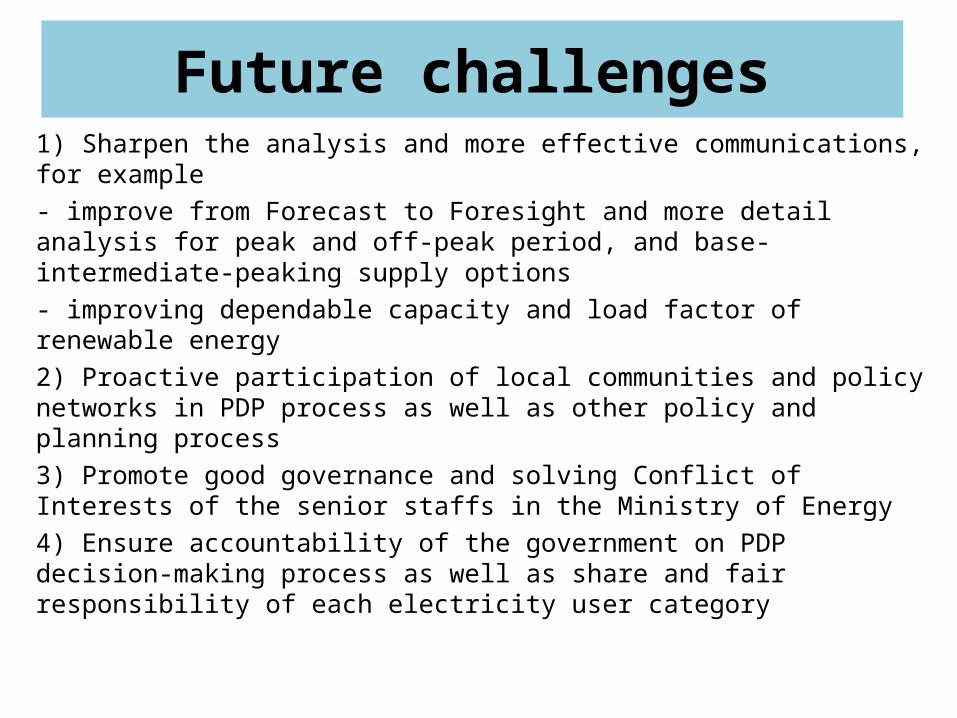

Future challenges1) Sharpen the analysis and more effective communications,for example- improve from Forecast to Foresight and more detail analysis for peak and off-peak period, and base-intermediate-peaking supply options- improving dependable capacity and load factor of renewable energy2) Proactive participation of local communities and policy networks in PDP process as well as other policy and planning process3) Promote good governance and solving Conflict of Interests of the senior staffs in the Ministry of Energy4) Ensure accountability of the government on PDP decision-making process as well as share and fair responsibility of each electricity user category

Thank youThank youfor your attentionfor your attention

35