Embed Size (px)

Citation preview

1

Supply-side Reform & China’s Steel Industry --Darkness before Dawn

12th Annual Platts Steel Markets Asia Conference

Nov 17th, 2016, Mumbai, India

JIANG Li

Baosteel, China

2

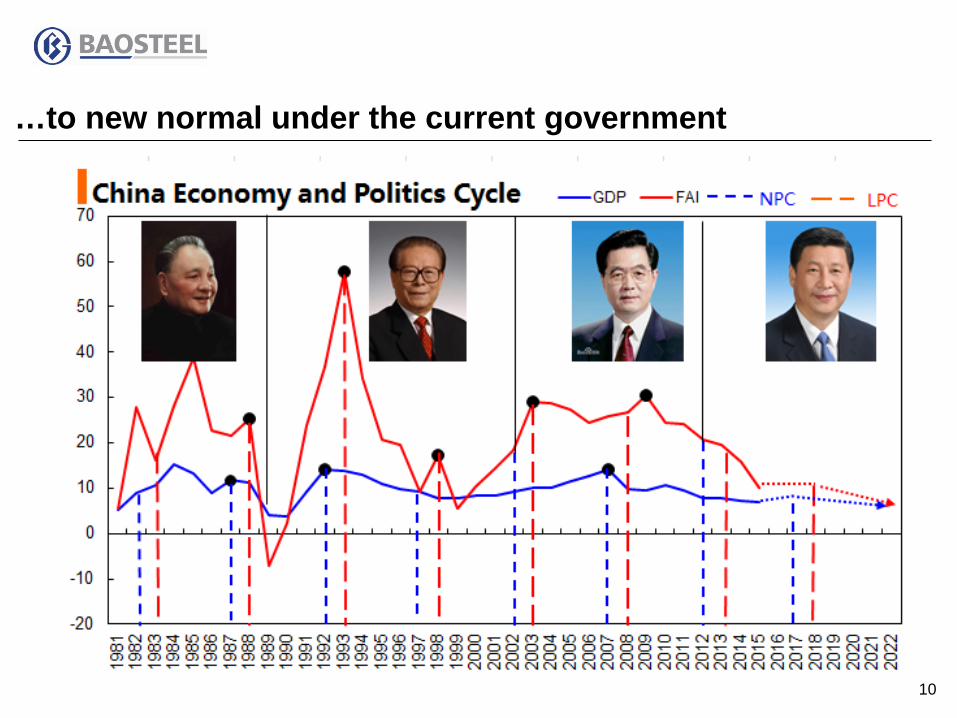

Current & Future China Steel Market

Supply-side Reform & China Steel Industry

BAOSTEEL & WISCO

Conclusion

Agenda

3

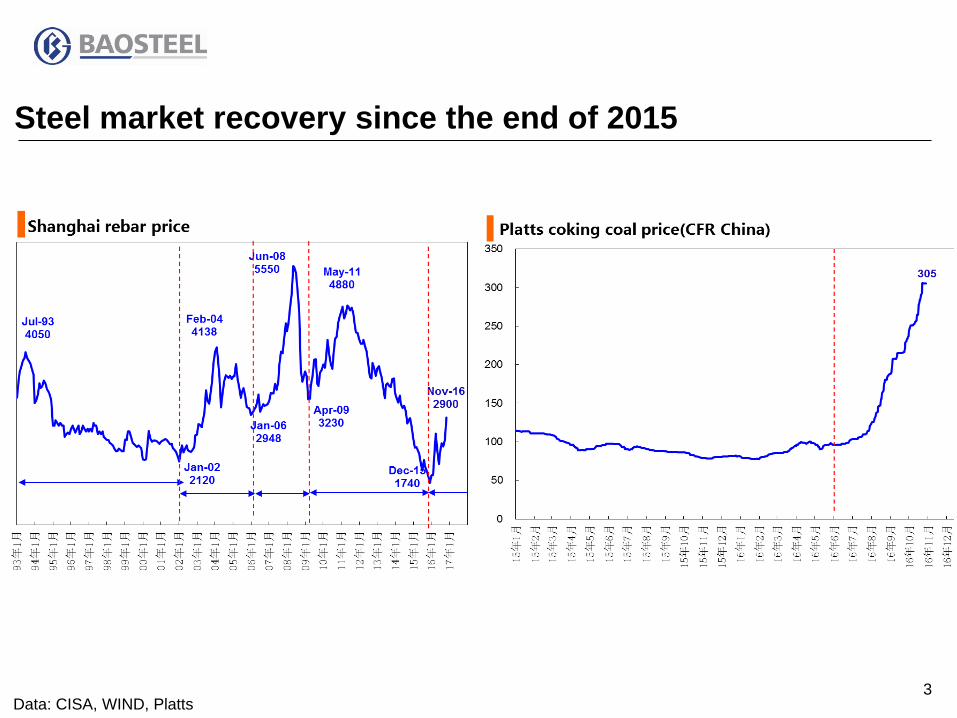

Steel market recovery since the end of 2015

Data: CISA, WIND, Platts

4

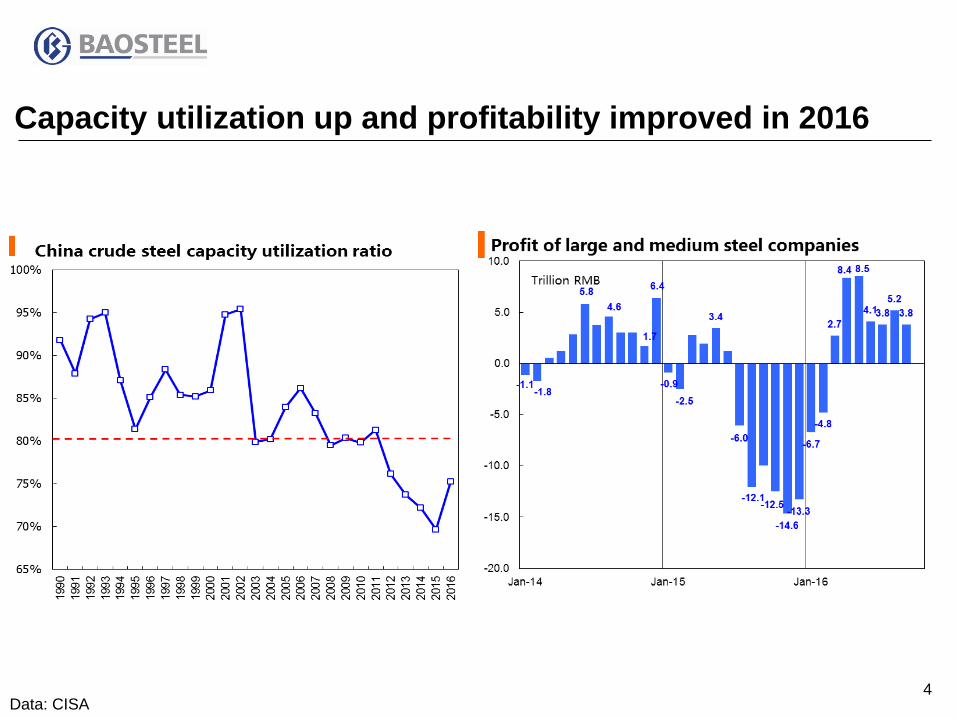

Capacity utilization up and profitability improved in 2016

Data: CISA

5

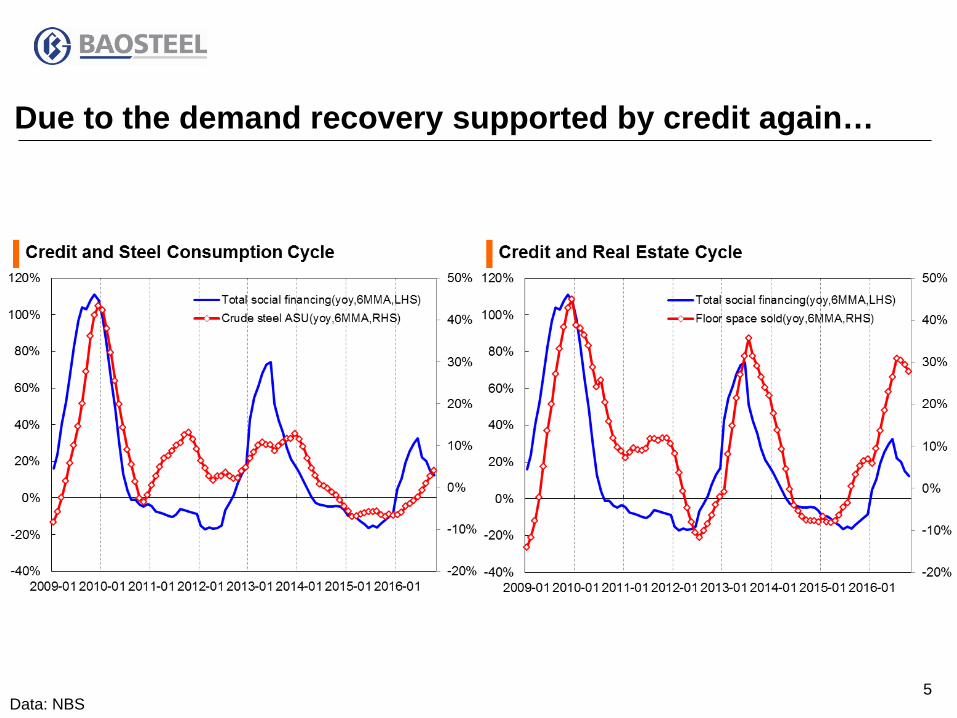

Due to the demand recovery supported by credit again…

Data: NBS

6

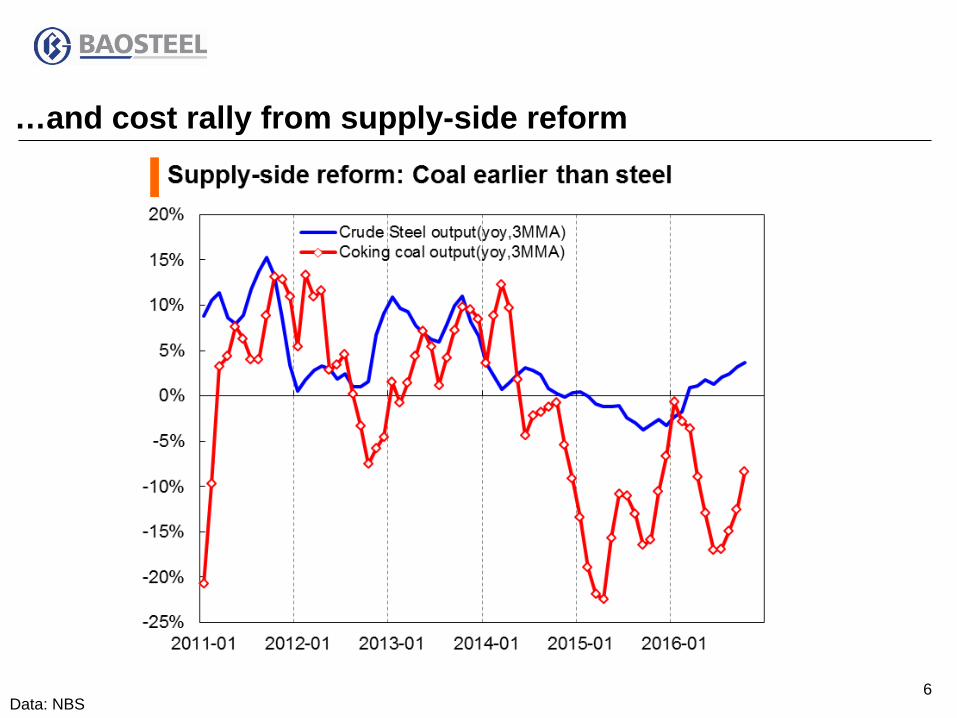

…and cost rally from supply-side reform

Data: NBS

7

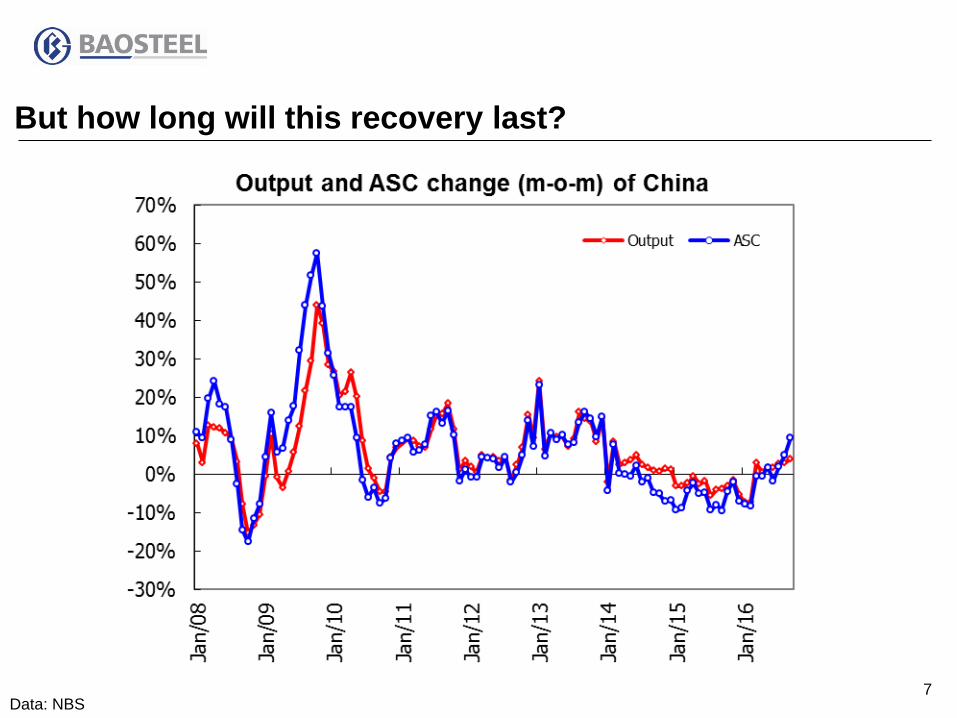

But how long will this recovery last?

Data: NBS

8

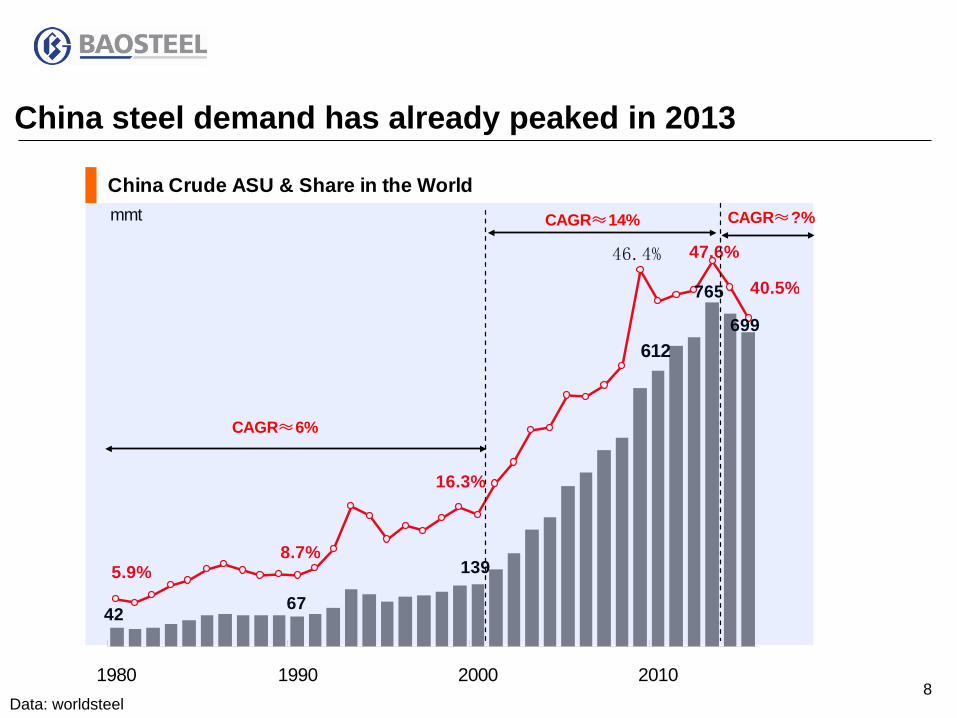

China steel demand has already peaked in 2013

Data: worldsteel

China Crude ASU & Share in the World

765

612

139

6742

699

47.6%46.4%

16.3%

8.7%5.9%

40.5%

1980 1990 2000 2010

mmt

CAGR≈6%

CAGR≈14% CAGR≈?%

9

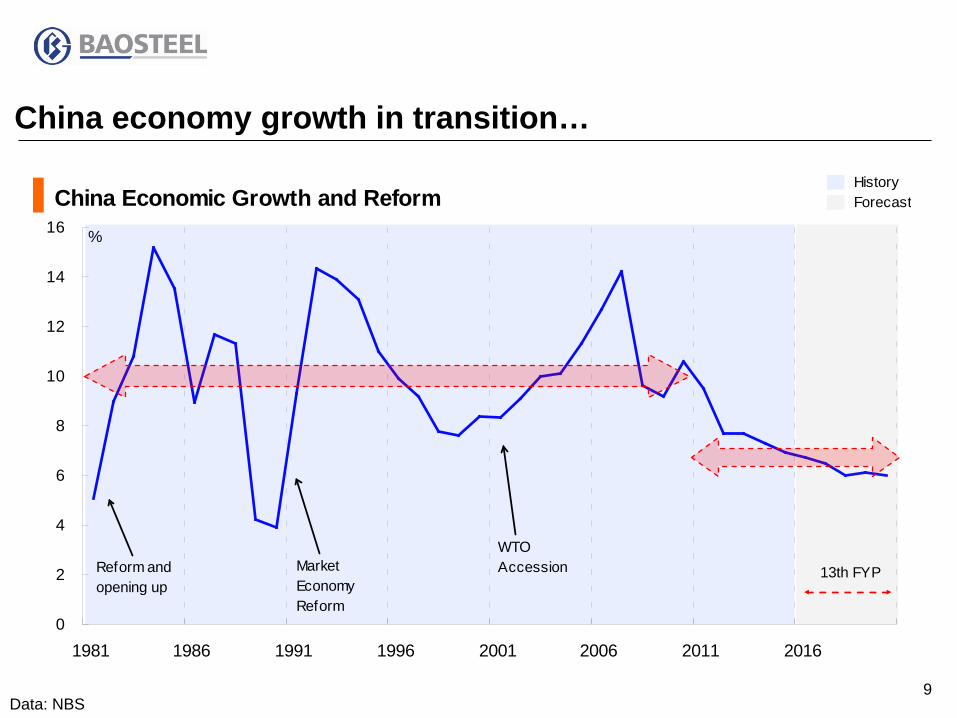

China economy growth in transition…

Data: NBS

China Economic Growth and Reform

0

2

4

6

8

10

12

14

16

1981 1986 1991 1996 2001 2006 2011 2016

%

Reform andopening up

MarketEconomyReform

WTOAccession

HistoryForecast

13th FYP

10

…to new normal under the current government

11

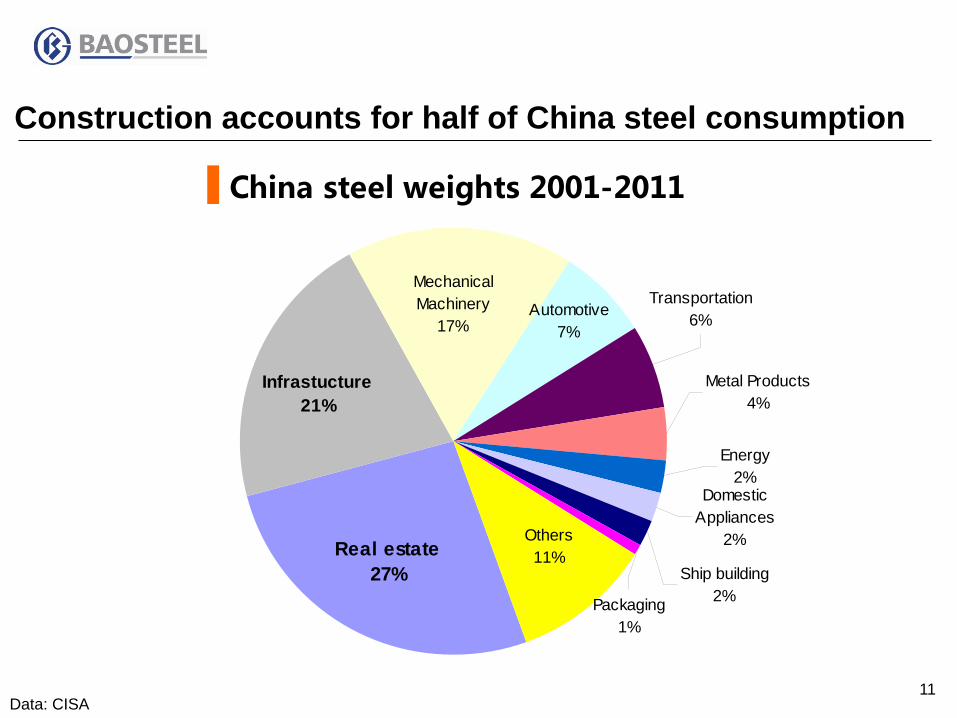

Construction accounts for half of China steel consumption

Data: CISA

China steel weights 2001-2011

Energy2%

Metal Products4%

DomesticAppliances

2%

Ship building2%Packaging

1%

Others11%Real estate

27%

Infrastucture21%

MechanicalMachinery

17%Automotive

7%

Transportation6%

12

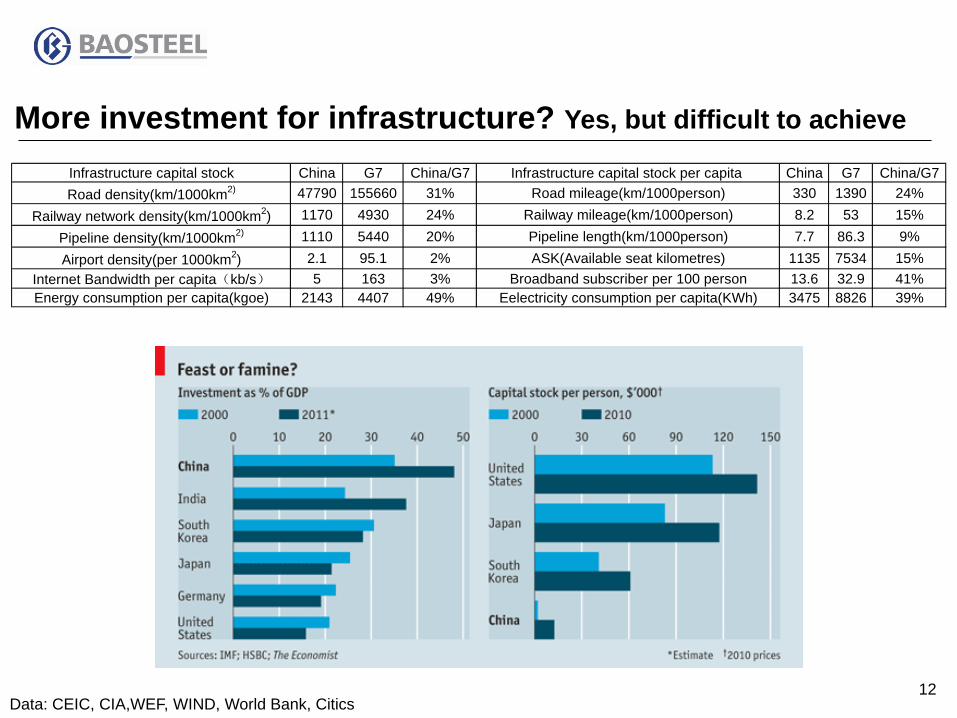

More investment for infrastructure? Yes, but difficult to achieve

Data: CEIC, CIA,WEF, WIND, World Bank, Citics

Infrastructure capital stock China G7 China/G7 Infrastructure capital stock per capita China G7 China/G7Road density(km/1000km2) 47790 155660 31% Road mileage(km/1000person) 330 1390 24%

Railway network density(km/1000km2) 1170 4930 24% Railway mileage(km/1000person) 8.2 53 15%Pipeline density(km/1000km2) 1110 5440 20% Pipeline length(km/1000person) 7.7 86.3 9%Airport density(per 1000km2) 2.1 95.1 2% ASK(Available seat kilometres) 1135 7534 15%

Internet Bandwidth per capita(kb/s) 5 163 3% Broadband subscriber per 100 person 13.6 32.9 41%Energy consumption per capita(kgoe) 2143 4407 49% Eelectricity consumption per capita(KWh) 3475 8826 39%

13 Data: WIND, NBS

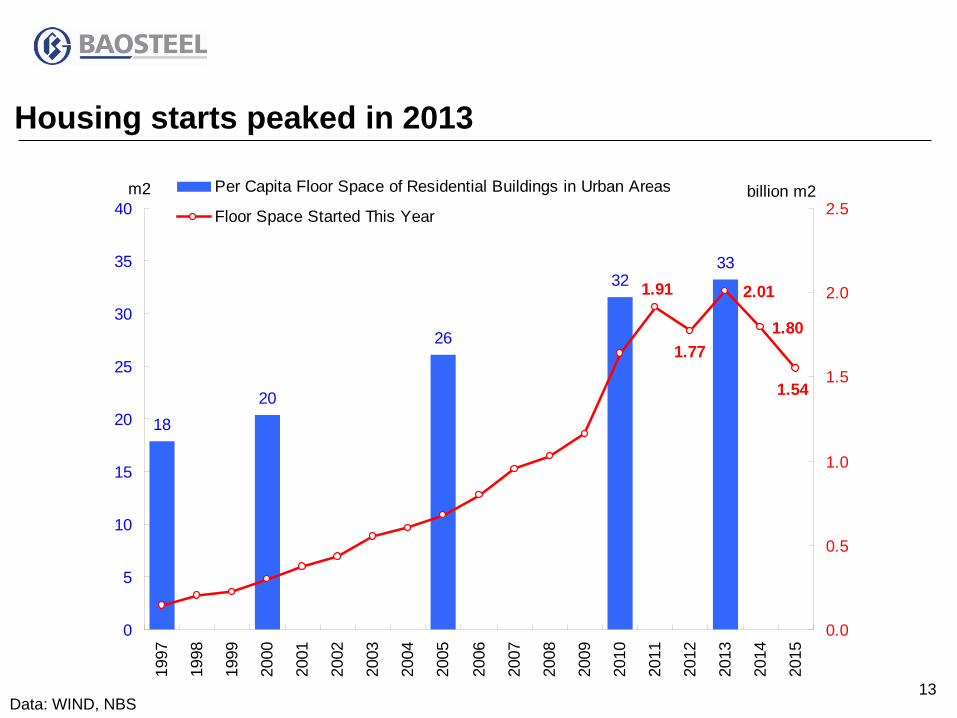

Housing starts peaked in 2013

1820

26

3233

1.801.77

1.91

1.54

2.01

0

5

10

15

20

25

30

35

40

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

0.0

0.5

1.0

1.5

2.0

2.5Per Capita Floor Space of Residential Buildings in Urban Areas

Floor Space Started This Yearbillion m2m2

14

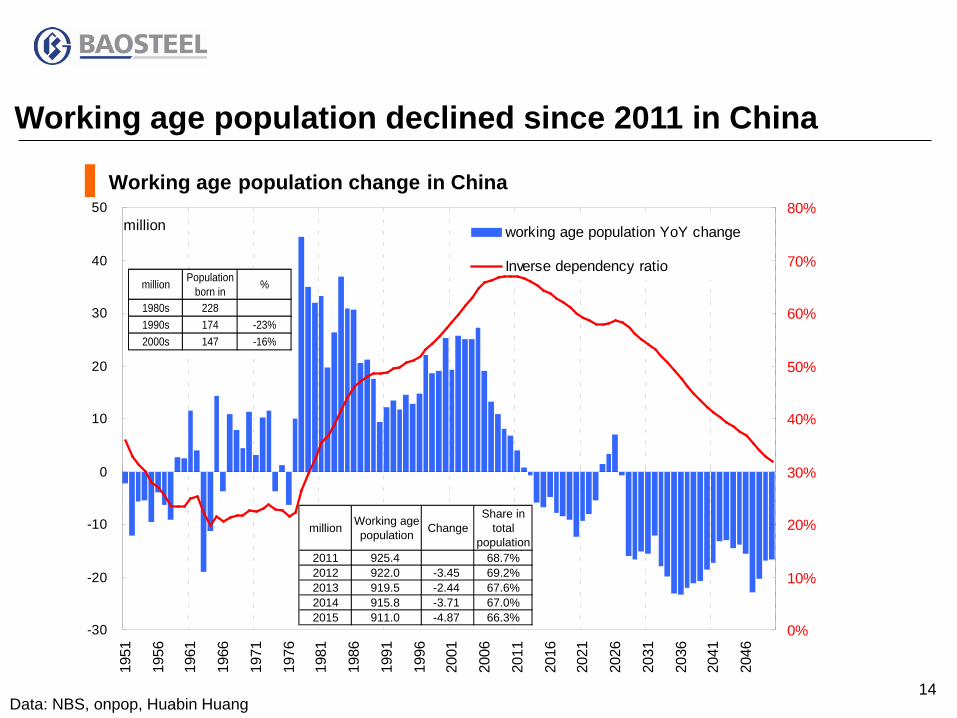

Working age population declined since 2011 in China

Data: NBS, onpop, Huabin Huang

Working age population change in China

-30

-20

-10

0

10

20

30

40

50

1951

1956

1961

1966

1971

1976

1981

1986

1991

1996

2001

2006

2011

2016

2021

2026

2031

2036

2041

2046

0%

10%

20%

30%

40%

50%

60%

70%

80%working age population YoY change

Inverse dependency ratio

million

million Populationborn in %

1980s 2281990s 174 -23%2000s 147 -16%

million Working agepopulation Change

Share intotal

population2011 925.4 68.7%2012 922.0 -3.45 69.2%2013 919.5 -2.44 67.6%2014 915.8 -3.71 67.0%2015 911.0 -4.87 66.3%

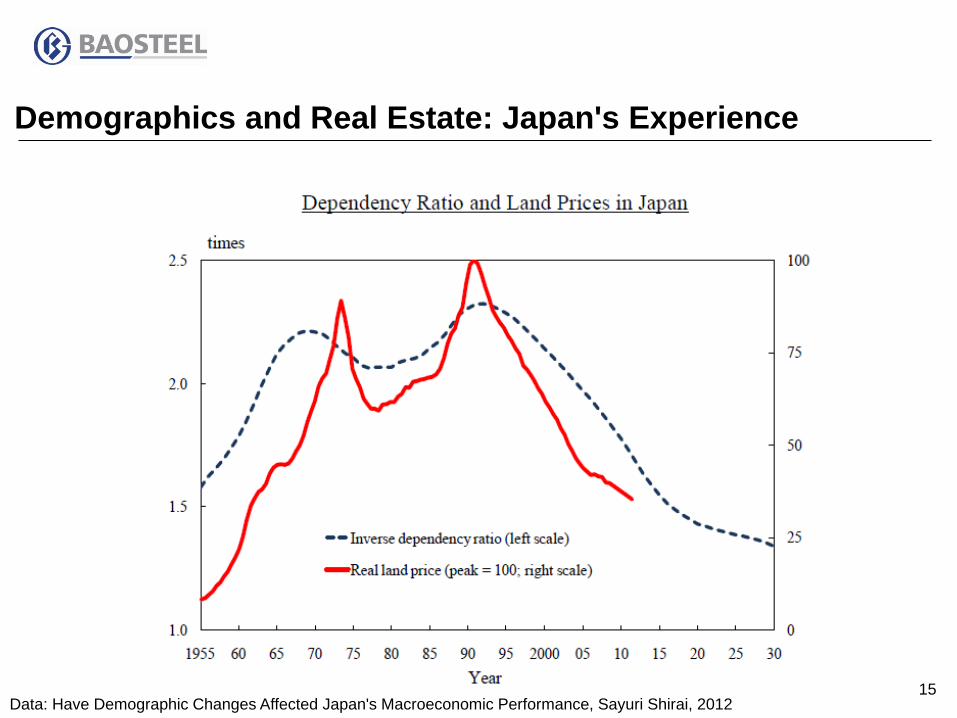

15 Data: Have Demographic Changes Affected Japan's Macroeconomic Performance, Sayuri Shirai, 2012

Demographics and Real Estate: Japan's Experience

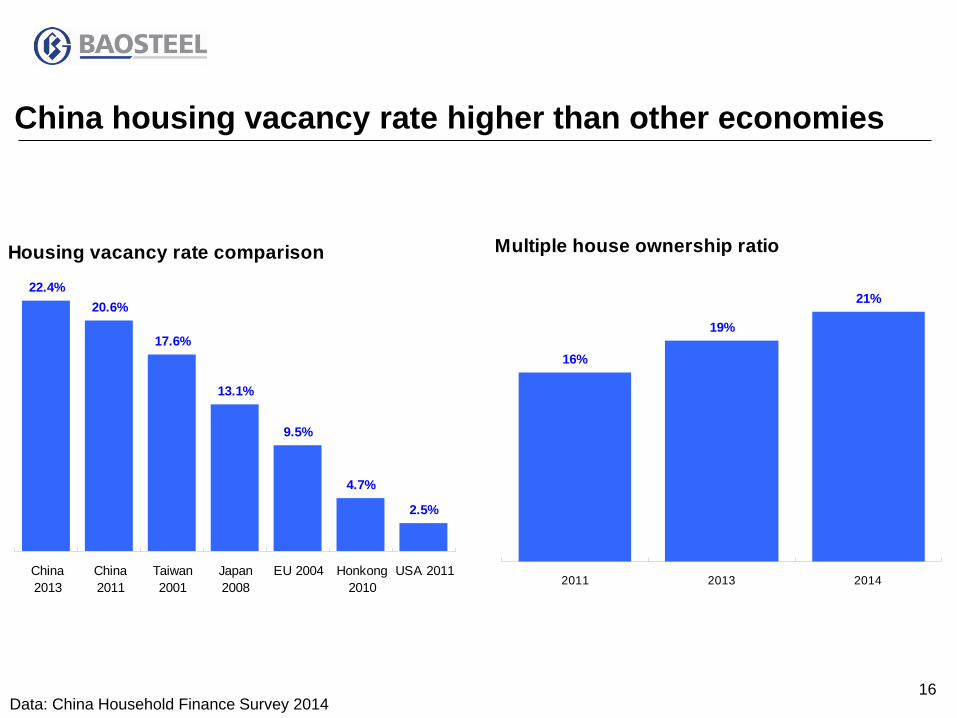

16 Data: China Household Finance Survey 2014

China housing vacancy rate higher than other economies

Housing vacancy rate comparison22.4%

20.6%

17.6%

13.1%

9.5%

4.7%

2.5%

China2013

China2011

Taiwan2001

Japan2008

EU 2004 Honkong2010

USA 2011

Multiple house ownership ratio

16%

19%

21%

2011 2013 2014

17 Data: NBS

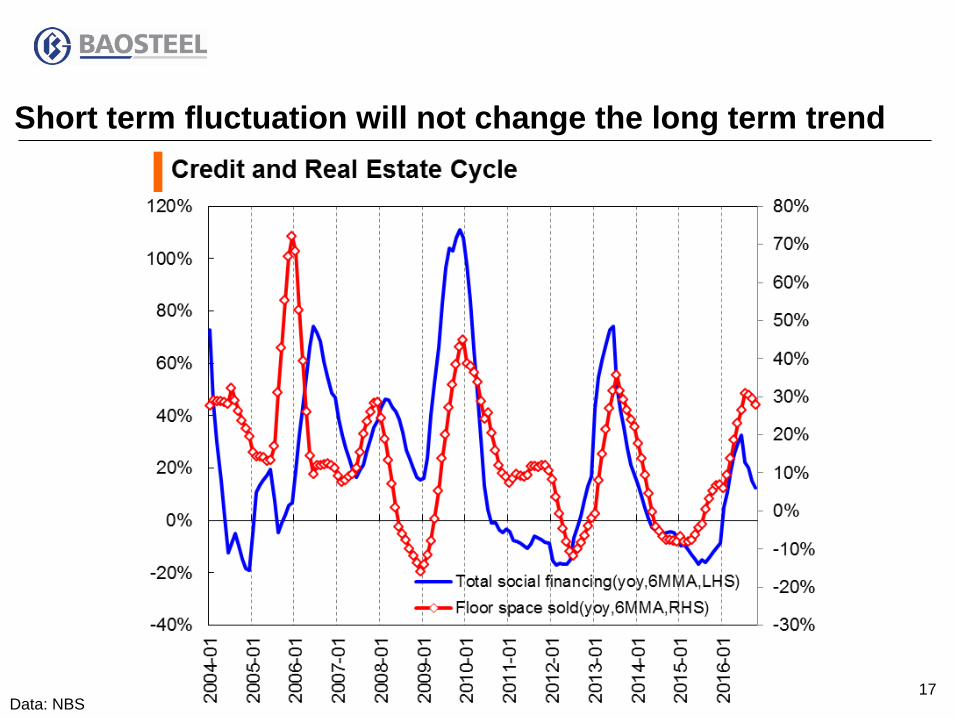

Short term fluctuation will not change the long term trend

18 Data: worldsteel

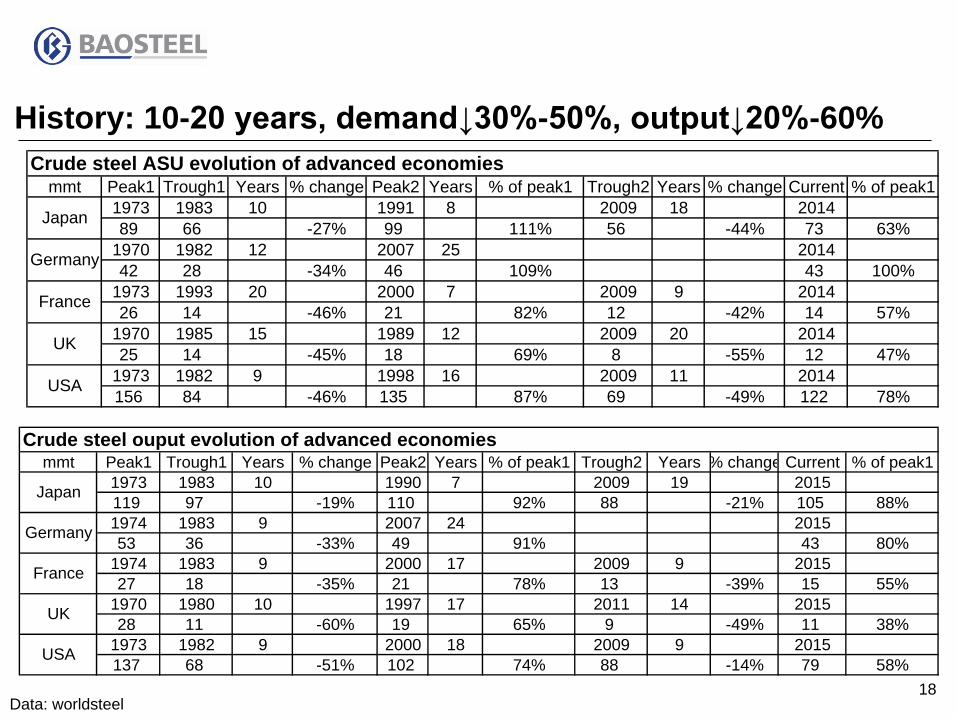

History: 10-20 years, demand↓30%-50%, output↓20%-60%

mmt Peak1 Trough1 Years % change Peak2 Years % of peak1 Trough2 Years % change Current % of peak11973 1983 10 1991 8 2009 18 201489 66 -27% 99 111% 56 -44% 73 63%

1970 1982 12 2007 25 201442 28 -34% 46 109% 43 100%

1973 1993 20 2000 7 2009 9 201426 14 -46% 21 82% 12 -42% 14 57%

1970 1985 15 1989 12 2009 20 201425 14 -45% 18 69% 8 -55% 12 47%

1973 1982 9 1998 16 2009 11 2014156 84 -46% 135 87% 69 -49% 122 78%USA

Crude steel ASU evolution of advanced economies

Japan

Germany

France

UK

mmt Peak1 Trough1 Years % change Peak2 Years % of peak1 Trough2 Years % change Current % of peak11973 1983 10 1990 7 2009 19 2015119 97 -19% 110 92% 88 -21% 105 88%1974 1983 9 2007 24 201553 36 -33% 49 91% 43 80%

1974 1983 9 2000 17 2009 9 201527 18 -35% 21 78% 13 -39% 15 55%

1970 1980 10 1997 17 2011 14 201528 11 -60% 19 65% 9 -49% 11 38%

1973 1982 9 2000 18 2009 9 2015137 68 -51% 102 74% 88 -14% 79 58%USA

Crude steel ouput evolution of advanced economies

Japan

Germany

France

UK

19

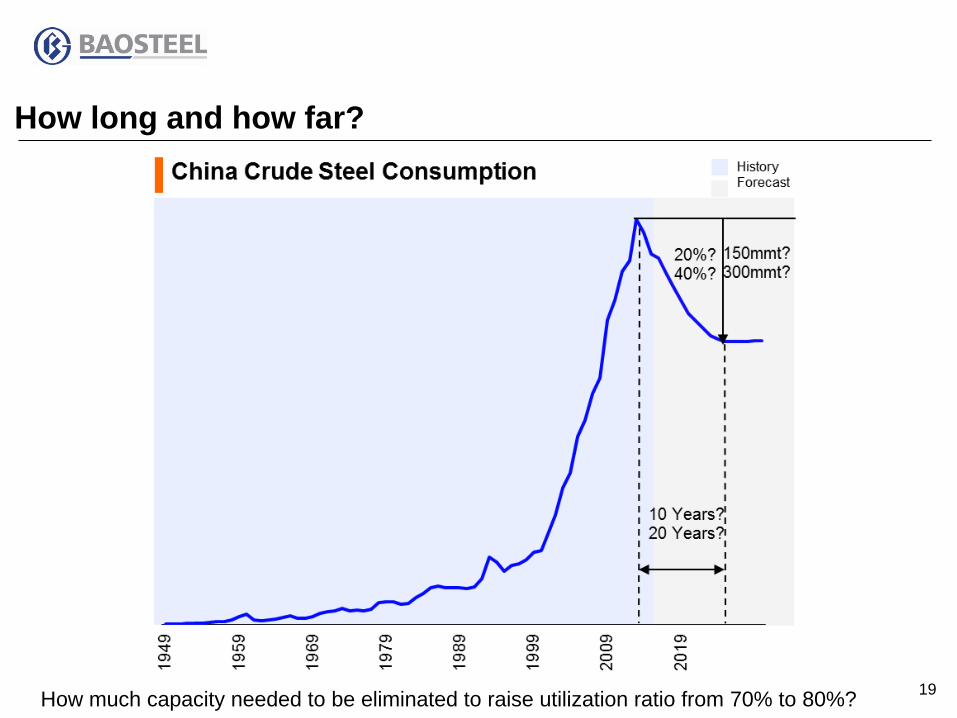

How long and how far?

How much capacity needed to be eliminated to raise utilization ratio from 70% to 80%?

20

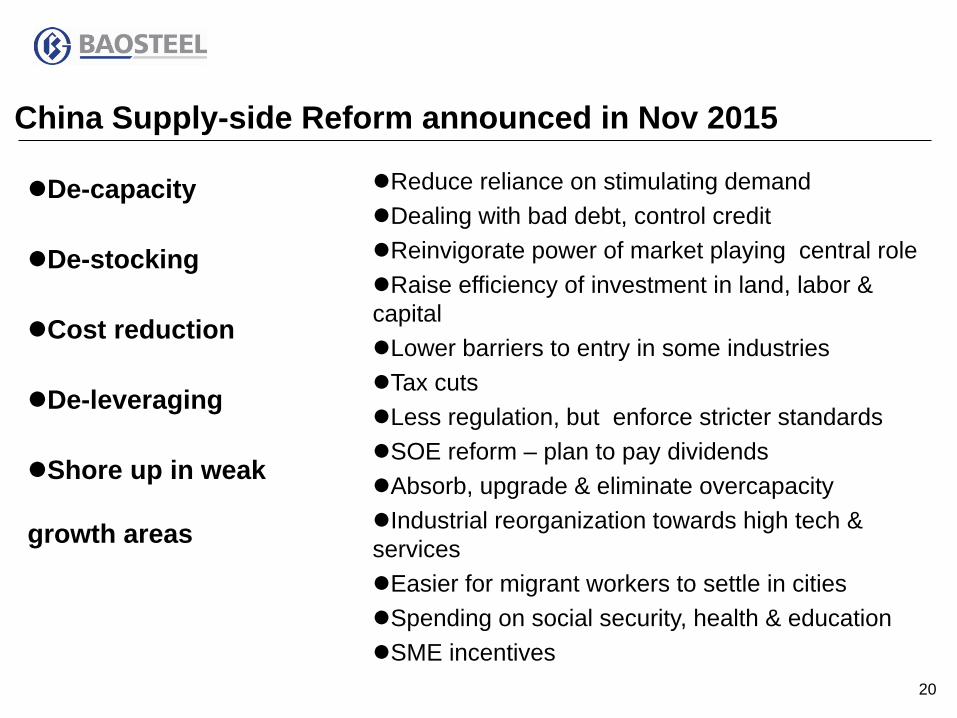

China Supply-side Reform announced in Nov 2015

De-capacity

De-stocking

Cost reduction

De-leveraging

Shore up in weak

growth areas

Reduce reliance on stimulating demand Dealing with bad debt, control credit Reinvigorate power of market playing central role Raise efficiency of investment in land, labor & capital Lower barriers to entry in some industries Tax cuts Less regulation, but enforce stricter standards SOE reform – plan to pay dividends Absorb, upgrade & eliminate overcapacity Industrial reorganization towards high tech & services Easier for migrant workers to settle in cities Spending on social security, health & education SME incentives

21

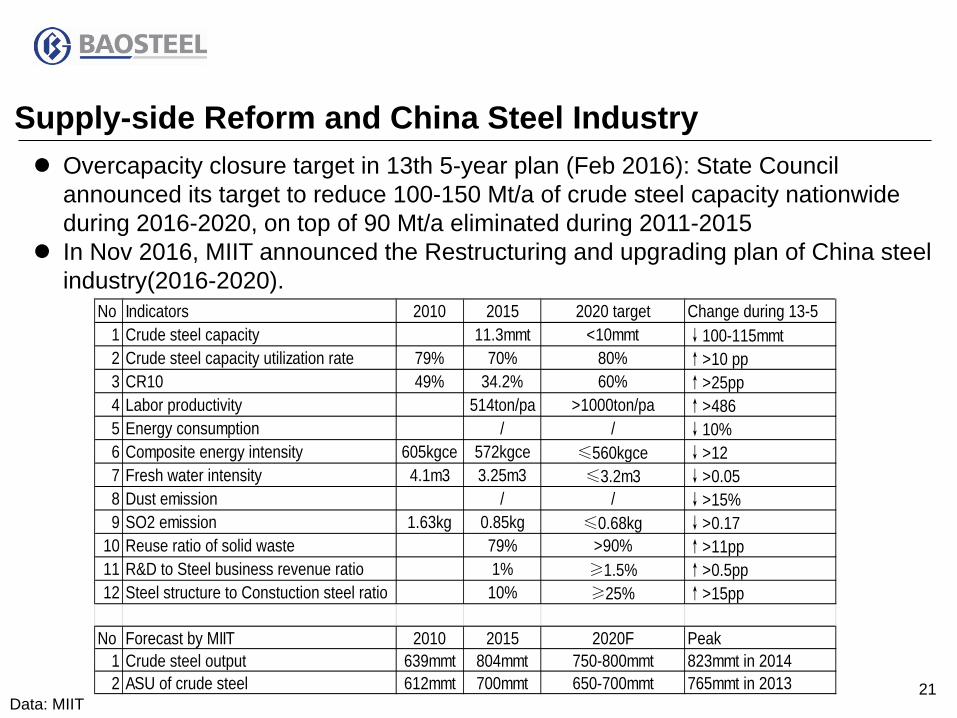

Supply-side Reform and China Steel Industry

Data: MIIT

No Indicators 2010 2015 2020 target Change during 13-51 Crude steel capacity 11.3mmt <10mmt ↓100-115mmt2 Crude steel capacity utilization rate 79% 70% 80% ↑>10 pp3 CR10 49% 34.2% 60% ↑>25pp4 Labor productivity 514ton/pa >1000ton/pa ↑>4865 Energy consumption / / ↓10%6 Composite energy intensity 605kgce 572kgce ≤560kgce ↓>127 Fresh water intensity 4.1m3 3.25m3 ≤3.2m3 ↓>0.058 Dust emission / / ↓>15%9 SO2 emission 1.63kg 0.85kg ≤0.68kg ↓>0.17

10 Reuse ratio of solid waste 79% >90% ↑>11pp11 R&D to Steel business revenue ratio 1% ≥1.5% ↑>0.5pp12 Steel structure to Constuction steel ratio 10% ≥25% ↑>15pp

No Forecast by MIIT 2010 2015 2020F Peak1 Crude steel output 639mmt 804mmt 750-800mmt 823mmt in 20142 ASU of crude steel 612mmt 700mmt 650-700mmt 765mmt in 2013

Overcapacity closure target in 13th 5-year plan (Feb 2016): State Council announced its target to reduce 100-150 Mt/a of crude steel capacity nationwide during 2016-2020, on top of 90 Mt/a eliminated during 2011-2015

In Nov 2016, MIIT announced the Restructuring and upgrading plan of China steel industry(2016-2020).

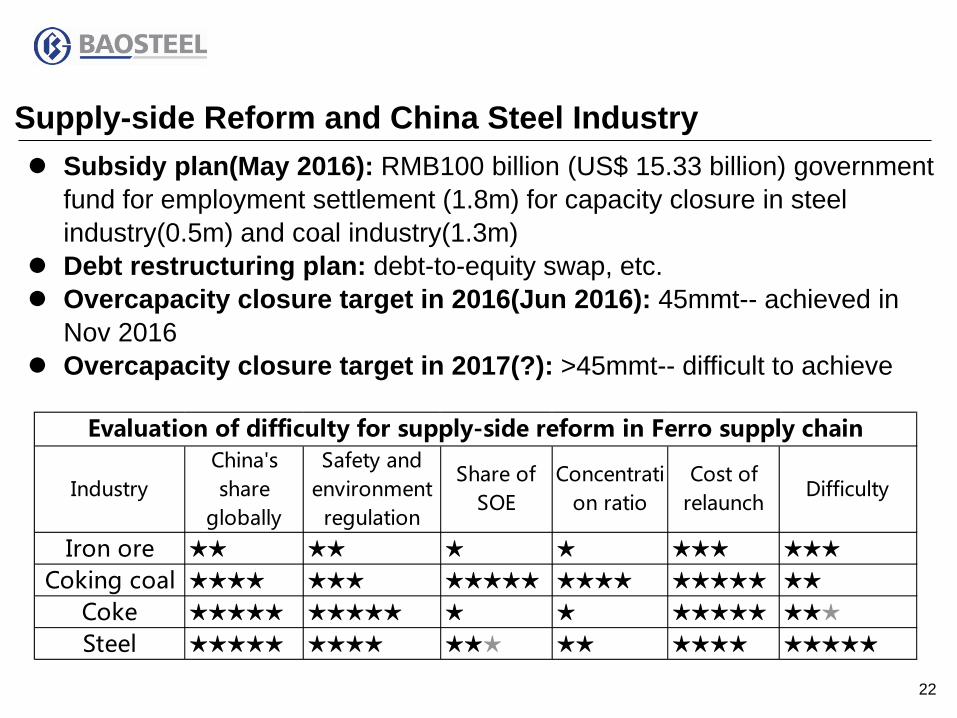

22

Supply-side Reform and China Steel Industry Subsidy plan(May 2016): RMB100 billion (US$ 15.33 billion) government

fund for employment settlement (1.8m) for capacity closure in steel industry(0.5m) and coal industry(1.3m)

Debt restructuring plan: debt-to-equity swap, etc. Overcapacity closure target in 2016(Jun 2016): 45mmt-- achieved in

Nov 2016 Overcapacity closure target in 2017(?): >45mmt-- difficult to achieve

IndustryChina'sshare

globally

Safety andenvironment

regulation

Share ofSOE

Concentration ratio

Cost ofrelaunch

Difficulty

Iron ore ★★ ★★ ★ ★ ★★★ ★★★Coking coal ★★★★ ★★★ ★★★★★ ★★★★ ★★★★★ ★★

Coke ★★★★★ ★★★★★ ★ ★ ★★★★★ ★★★Steel ★★★★★ ★★★★ ★★★ ★★ ★★★★ ★★★★★

Evaluation of difficulty for supply-side reform in Ferro supply chain

23

Key drivers of potential success of de-capacity-1

Data: CISA

Overcapacity has become more severe as steel demand peaked in 2013 and has to be addressed

Profitability of China steel industry has deteriorated since 2012 which lead to rising debt and NPLs at banks

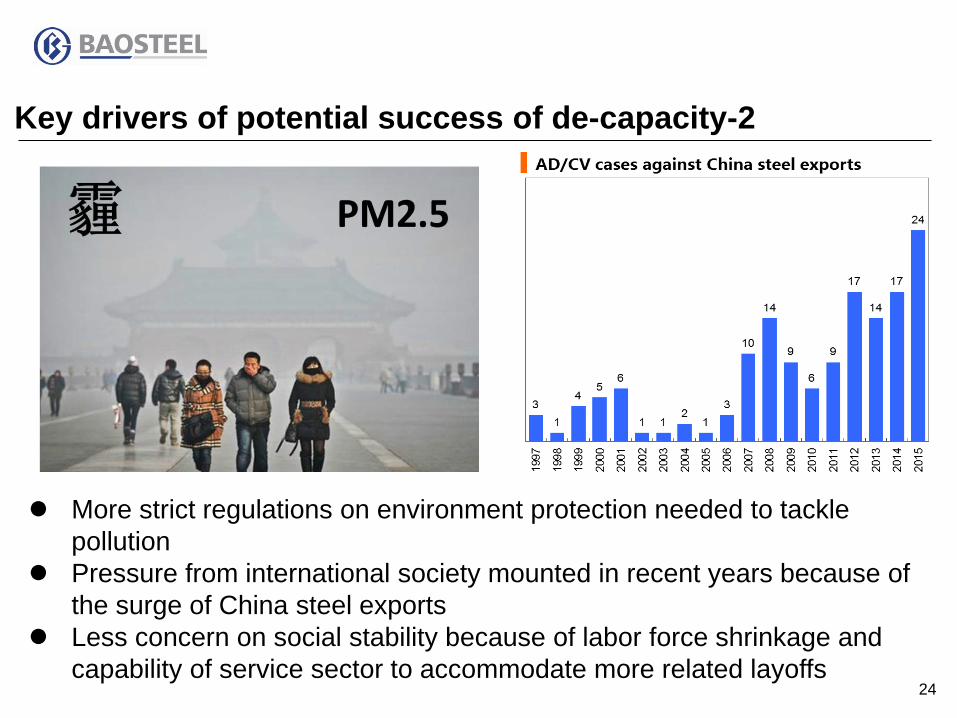

24

More strict regulations on environment protection needed to tackle pollution

Pressure from international society mounted in recent years because of the surge of China steel exports

Less concern on social stability because of labor force shrinkage and capability of service sector to accommodate more related layoffs

Key drivers of potential success of de-capacity-2

25

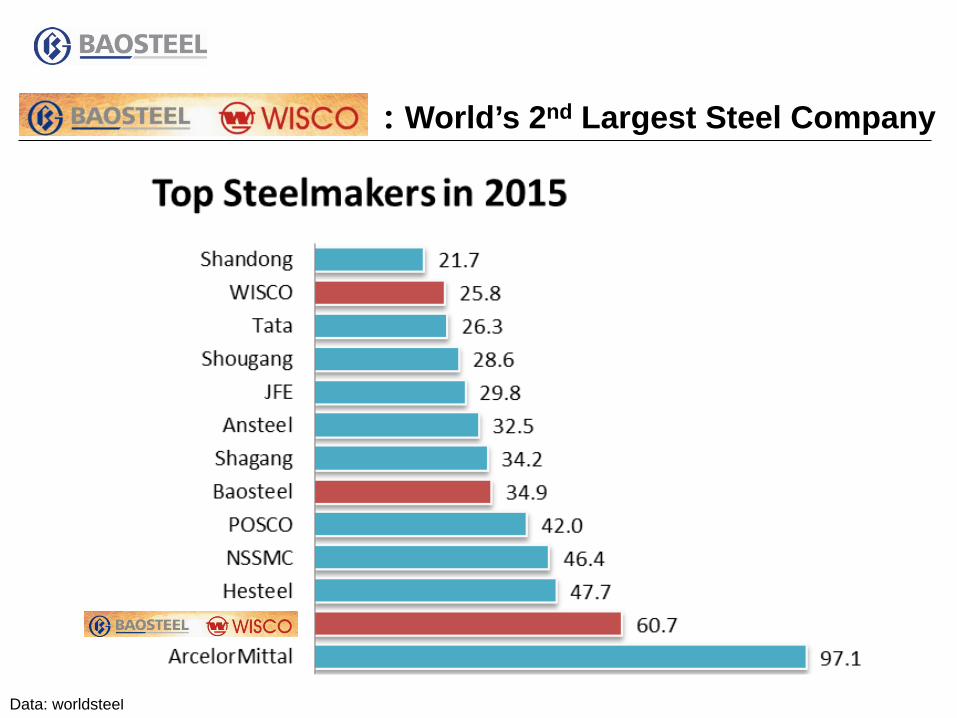

:World’s 2nd Largest Steel Company

Data: worldsteel

26

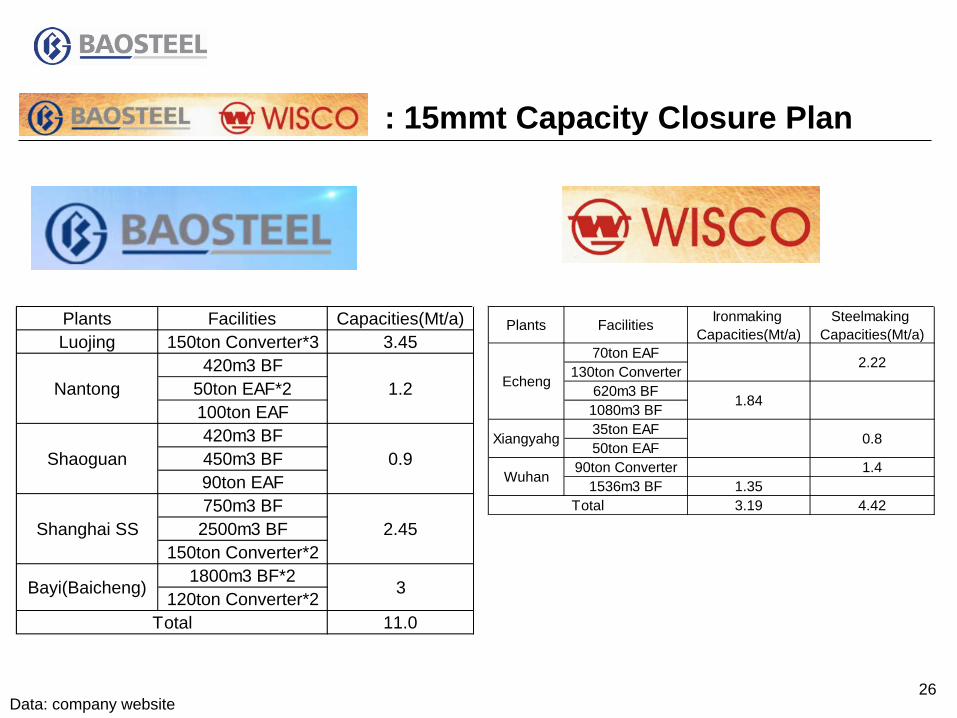

: 15mmt Capacity Closure Plan

Data: company website

Plants Facilities Capacities(Mt/a)Luojing 150ton Converter*3 3.45

420m3 BF50ton EAF*2100ton EAF420m3 BF450m3 BF90ton EAF750m3 BF2500m3 BF

150ton Converter*21800m3 BF*2

120ton Converter*211.0

1.2

0.9

2.45

3

Total

Nantong

Shaoguan

Shanghai SS

Bayi(Baicheng)

Plants Facilities Ironmaking Capacities(Mt/a)

Steelmaking Capacities(Mt/a)

70ton EAF130ton Converter

620m3 BF1080m3 BF35ton EAF50ton EAF

90ton Converter 1.41536m3 BF 1.35

3.19 4.42

Echeng2.22

0.8Xiangyahg

Wuhan

Total

1.84

27 Data: company report

Wuhan Qinghshan

Nanjing Meishan

Zhanjiang Dongshan

Shanghai Baoshan

R&D Procurement Marketing

&Sales Production Strategy Planning

4 production sites

Shanghai Baoshan • Yangtze river delta,

eastern coast, overseas Nanjing Meishan • eastern China Zhanjing Dongshan • Pearl River Delta,

southern China, overseas Wuhan Qingshan • Midwest, upper and

middle Yangtze River

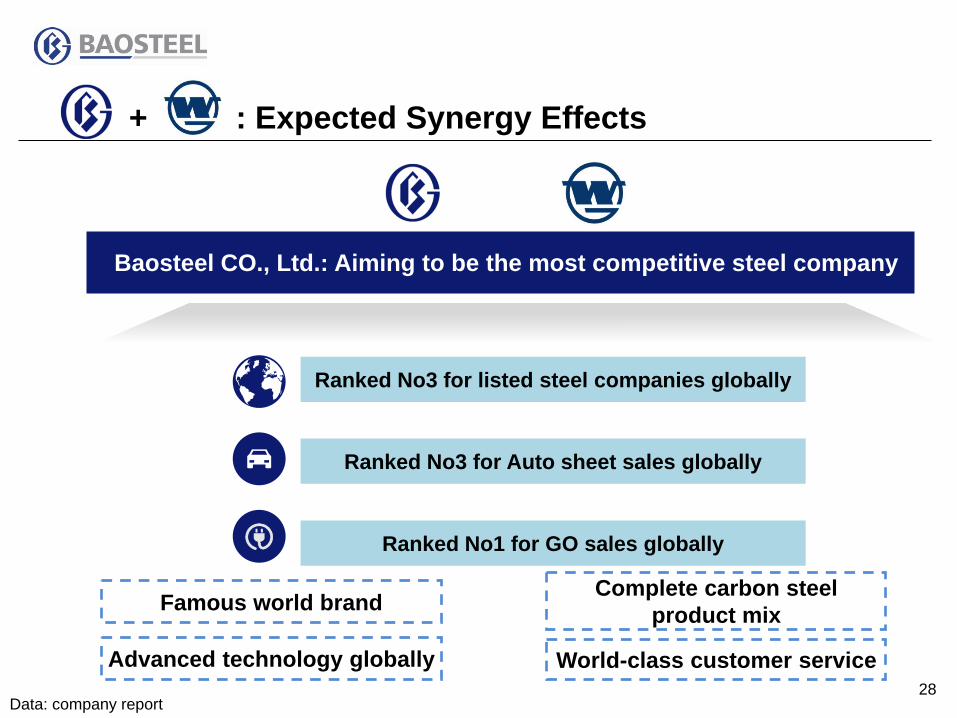

+ : Expected Synergy Effects

Baosteel CO., Ltd.

28 Data: company report

Baosteel CO., Ltd.: Aiming to be the most competitive steel company

Ranked No3 for Auto sheet sales globally

Ranked No3 for listed steel companies globally

Ranked No1 for GO sales globally

Famous world brand

World-class customer service

Complete carbon steel product mix

Advanced technology globally

+ : Expected Synergy Effects

29

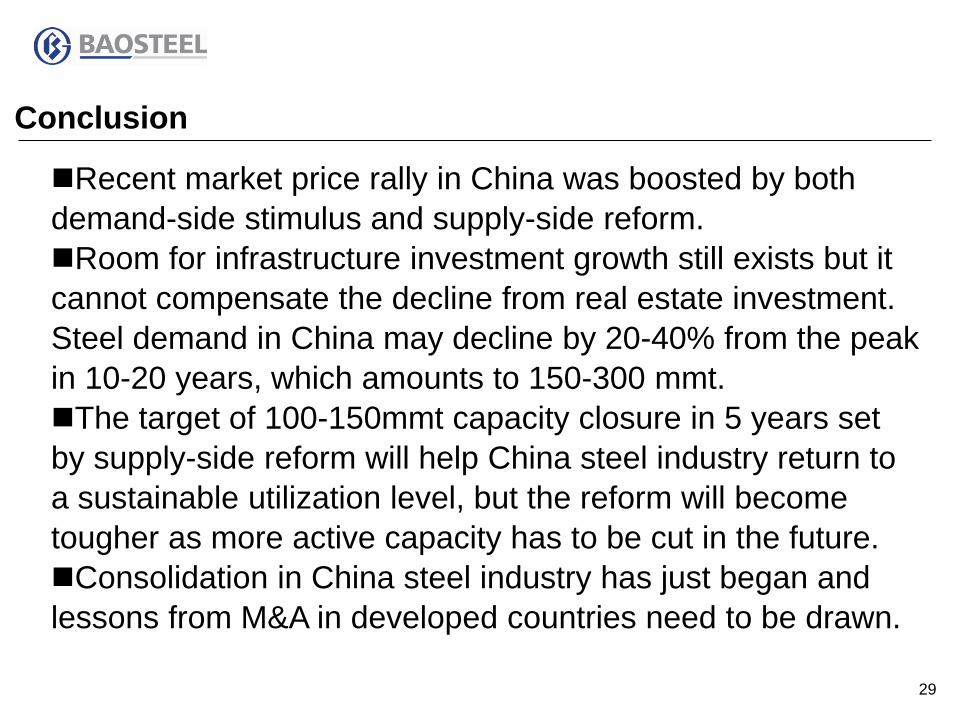

Recent market price rally in China was boosted by both demand-side stimulus and supply-side reform. Room for infrastructure investment growth still exists but it cannot compensate the decline from real estate investment. Steel demand in China may decline by 20-40% from the peak in 10-20 years, which amounts to 150-300 mmt. The target of 100-150mmt capacity closure in 5 years set by supply-side reform will help China steel industry return to a sustainable utilization level, but the reform will become tougher as more active capacity has to be cut in the future. Consolidation in China steel industry has just began and lessons from M&A in developed countries need to be drawn.

Conclusion

30

Thank you

JIANG, Li Email: [email protected]

Disclaimer: The views expressed here are solely those of the author and do not represent the official views of the company.

![SK하이닉스 (000660)file.mk.co.kr/imss/write/20190401130910__00.pdf · 29 기업분석[sk하이닉스] 재무상태표 포괄손익계산서 (십억원) 2016 2017 2018 2019f 2020f](https://img.pdfslide.net/doc/110x75/5e22072f213d79460e3f6c1d/ske-000660filemkcokrimsswrite2019040113091000pdf-29-eeske.jpg)