Embed Size (px)

Citation preview

Sustainable development, corporate social responsibility &

accounting

Prof. Jan BebbingtonCentre for Social & Environmental Accounting Research

St Andrews Sustainability InstituteVice-Chair (Scotland), Sustainable Development Commission

Where I am going …

• Mixture of:– Ideas from academia– Application of these in applied research settings– With awareness of policy context

• Key concepts– Accounting & accountability– Sustainable development– Governance/governmentality

• Played out via accounting for sustainable development example

We all think we know about accountability …

but do we?

and if it were ‘easy’ why does it seem so hard?

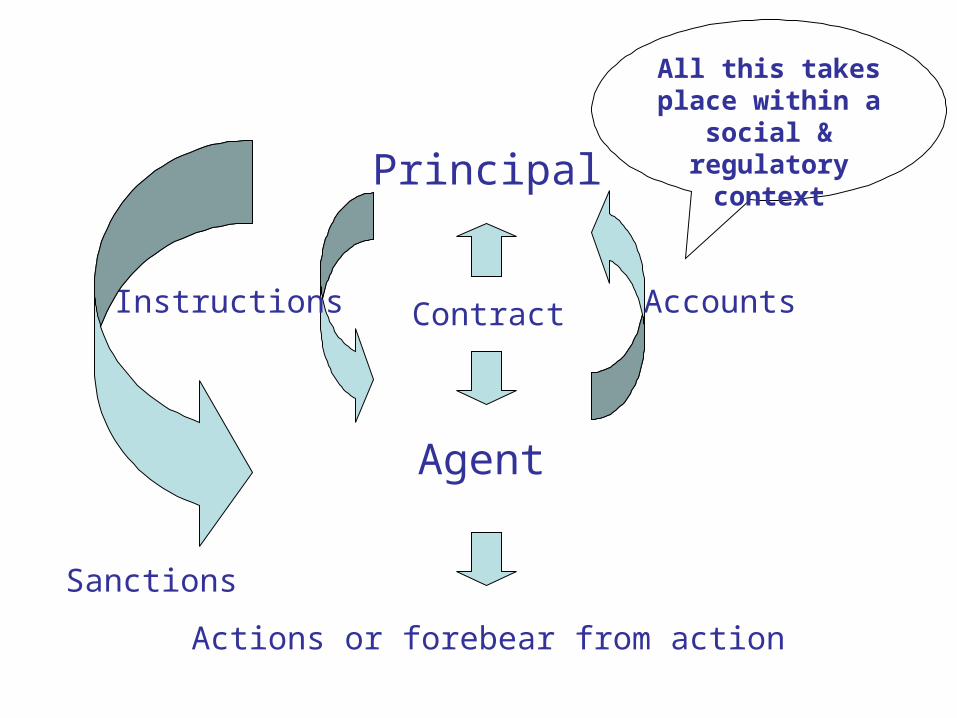

A possible definition

“The duty to provide an account (by no means necessarily a financial account) or reckoning of those actions for which one is

responsible”

Gray, Owen & Adams (1996)

Principal

Agent

Instructions

Actions or forebear from action

AccountsContract

Sanctions

All this takes place within a

social & regulatory

context

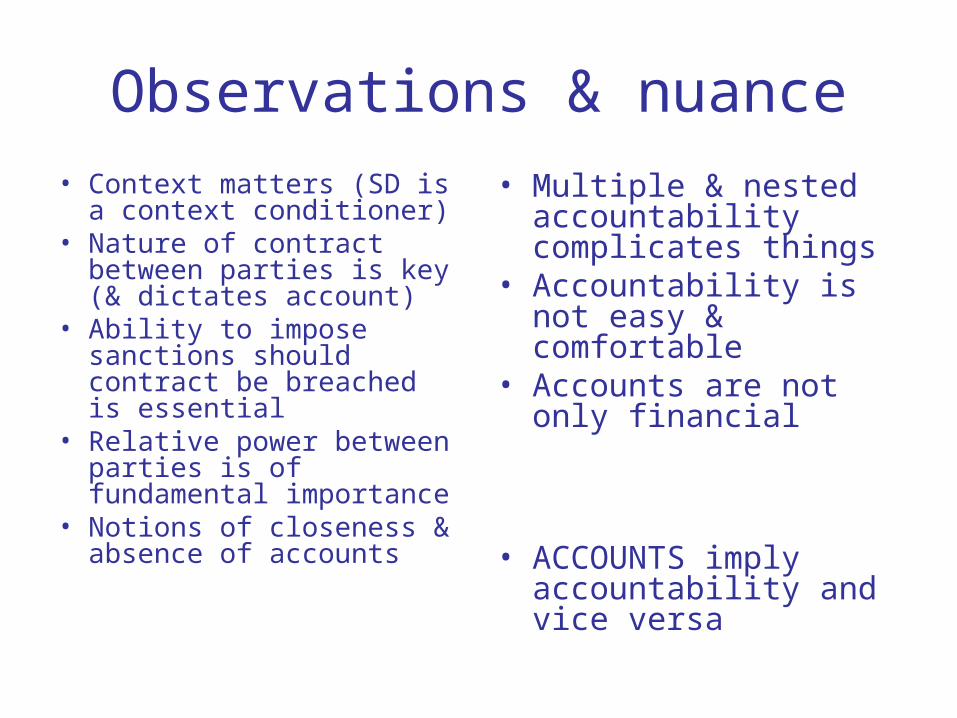

Observations & nuance

• Context matters (SD is a context conditioner)

• Nature of contract between parties is key (& dictates account)

• Ability to impose sanctions should contract be breached is essential

• Relative power between parties is of fundamental importance

• Notions of closeness & absence of accounts

• Multiple & nested accountability complicates things

• Accountability is not easy & comfortable

• Accounts are not only financial

• ACCOUNTS imply accountability and vice versa

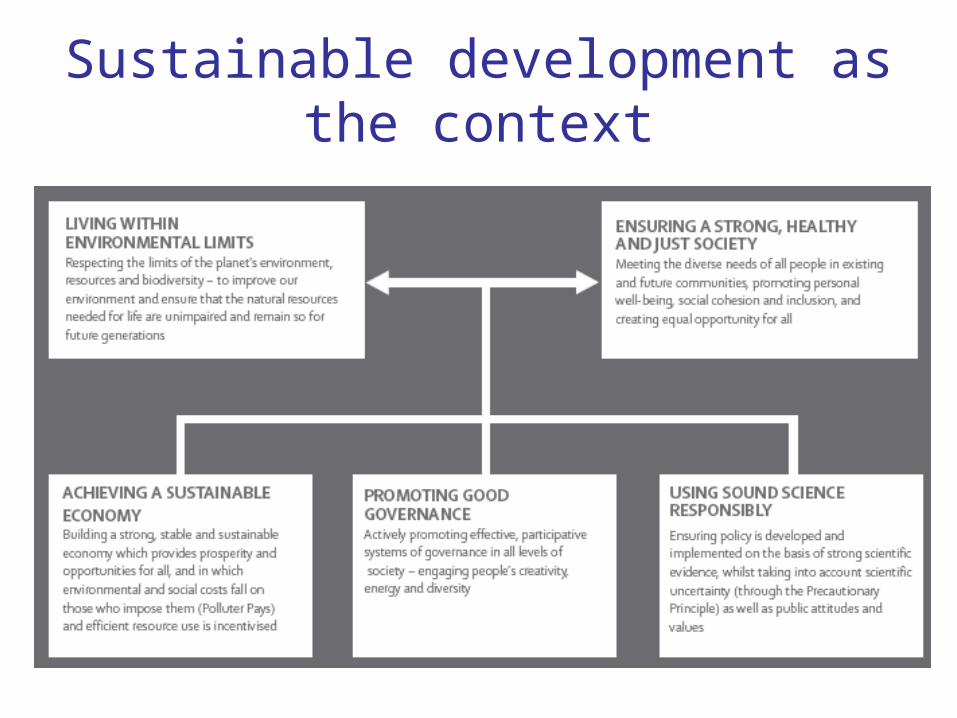

Sustainable development as the context

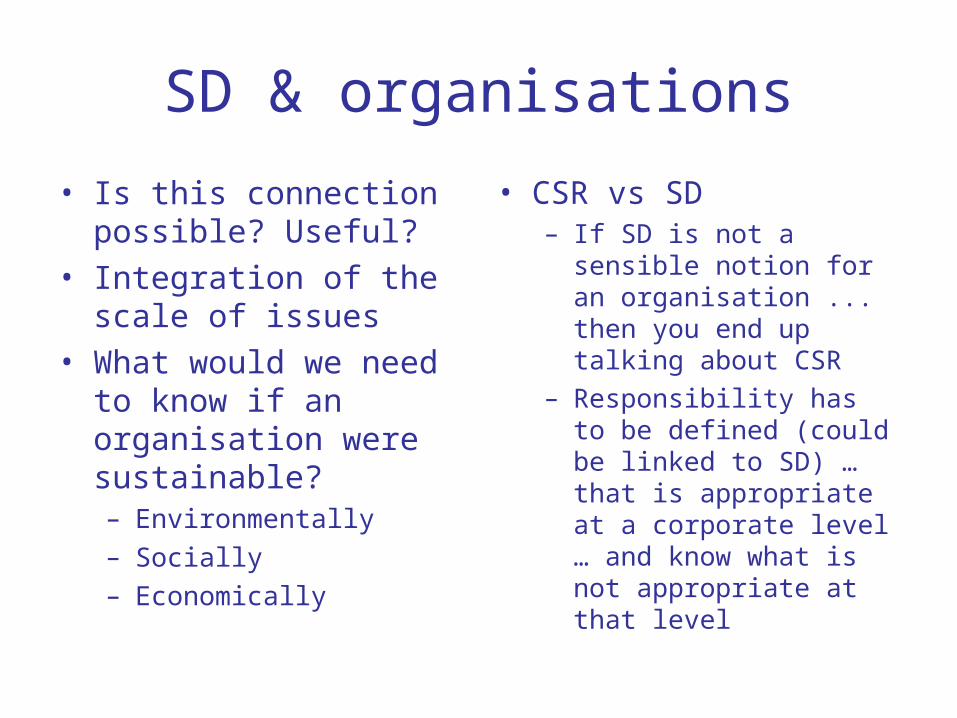

SD & organisations

• Is this connection possible? Useful?

• Integration of the scale of issues

• What would we need to know if an organisation were sustainable?– Environmentally– Socially– Economically

• CSR vs SD– If SD is not a sensible

notion for an organisation ... then you end up talking about CSR

– Responsibility has to be defined (could be linked to SD) … that is appropriate at a corporate level … and know what is not appropriate at that level

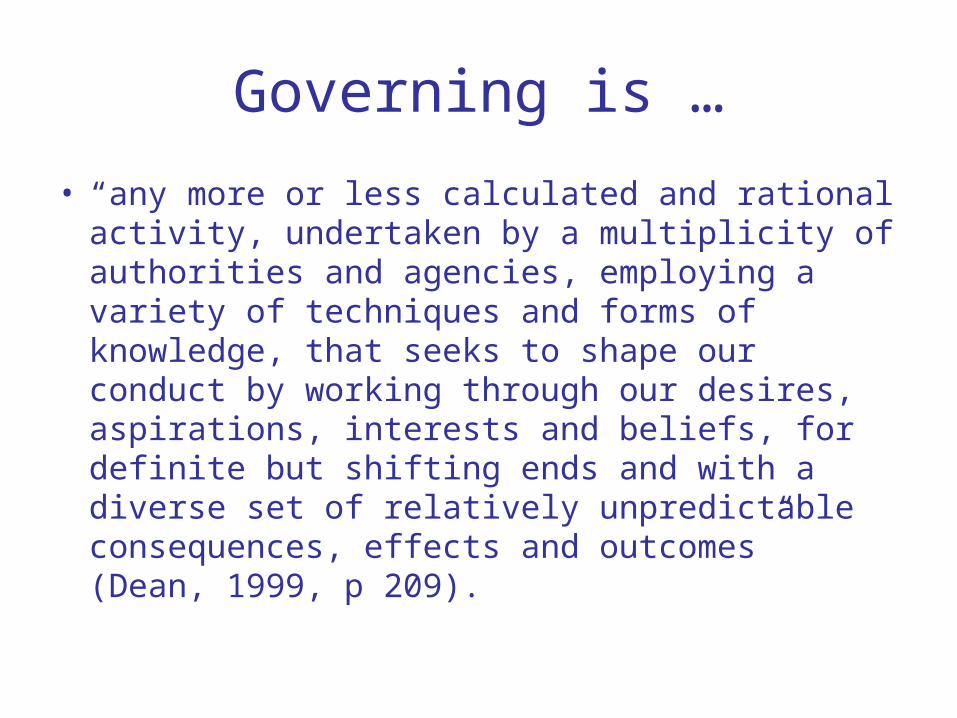

Governing is …

• “any more or less calculated and rational activity, undertaken by a multiplicity of authorities and agencies, employing a variety of techniques and forms of knowledge, that seeks to shape our conduct by working through our desires, aspirations, interests and beliefs, for definite but shifting ends and with a diverse set of relatively unpredictable consequences, effects and outcomes” (Dean, 1999, p 209).

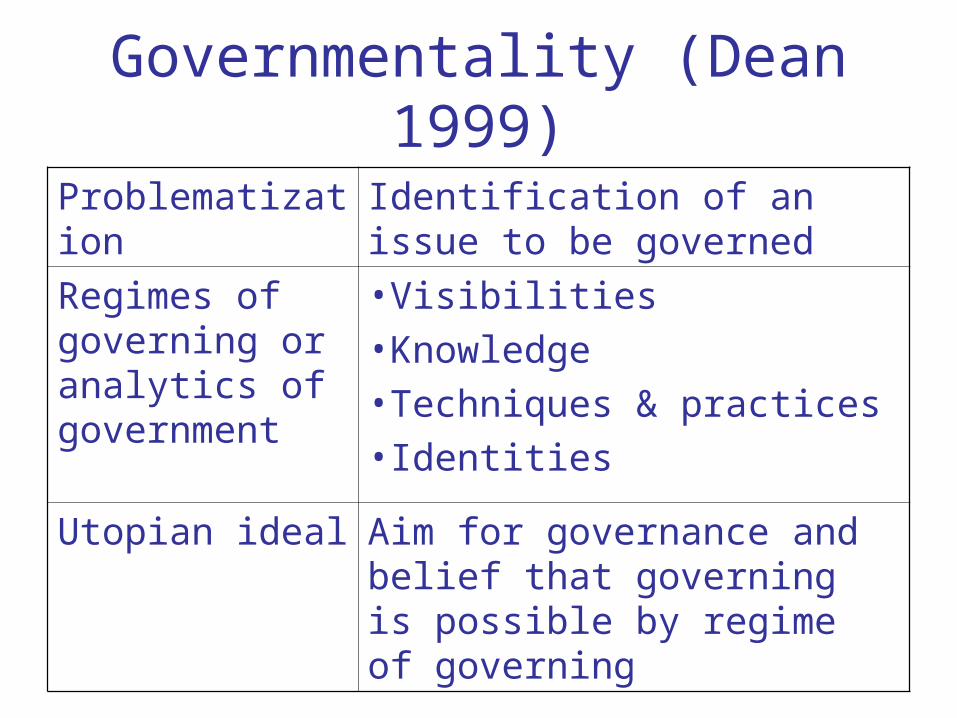

Governmentality (Dean 1999)

Problematization Identification of an issue to be governed

Regimes of governing or analytics of government

•Visibilities•Knowledge•Techniques & practices•Identities

Utopian ideal Aim for governance and belief that governing is possible by regime of governing

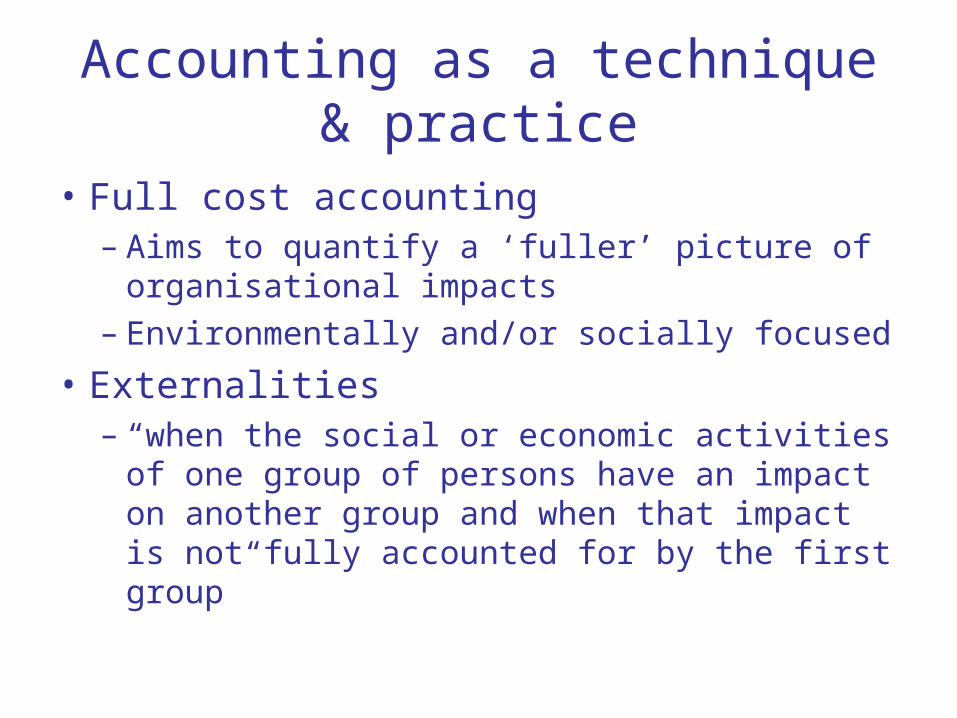

Accounting as a technique & practice

• Full cost accounting– Aims to quantify a ‘fuller’ picture of

organisational impacts– Environmentally and/or socially focused

• Externalities– “when the social or economic activities of one

group of persons have an impact on another group and when that impact is not fully accounted for by the first group”

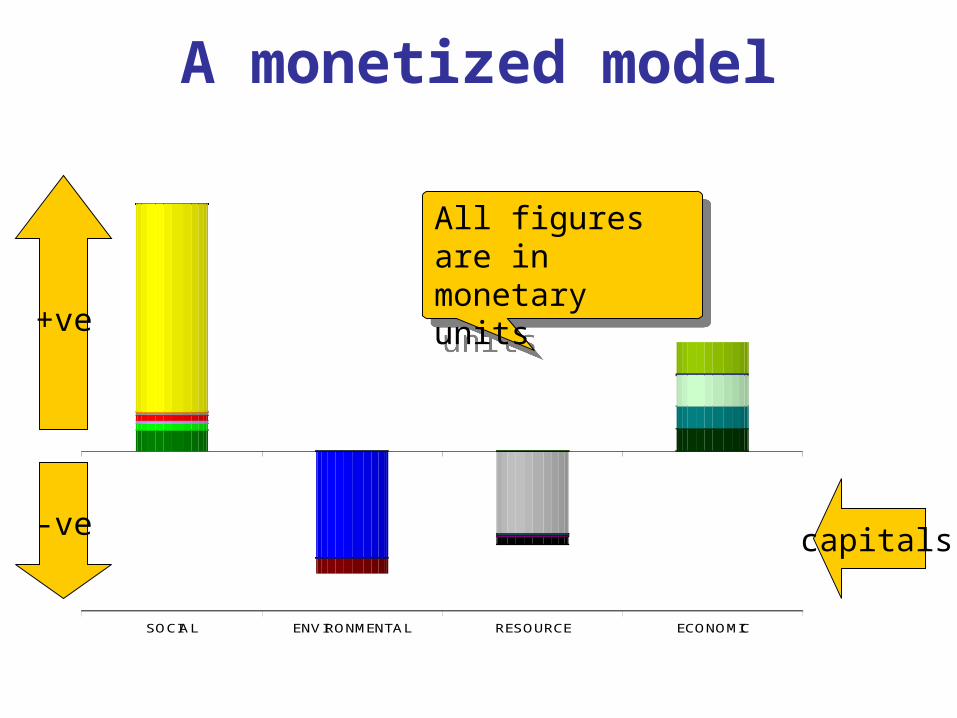

A monetized model

SOCIAL ENVIRONMENTAL RESOURCE ECONOMIC

capitals

+ve

-ve

All figures are in monetary units

All figures are in monetary units

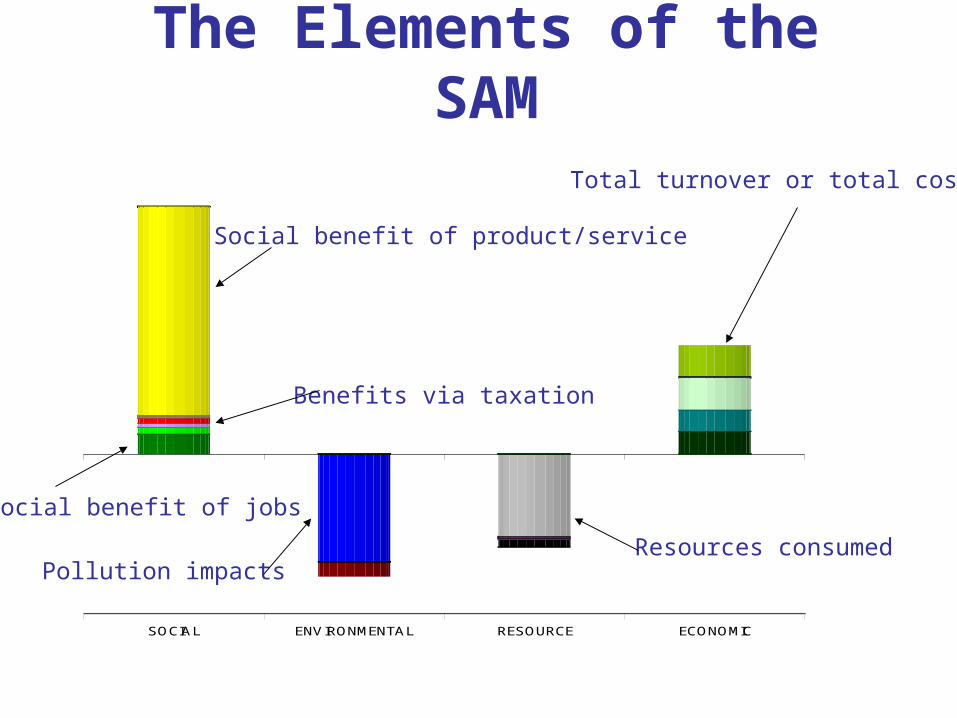

The Elements of the SAM

SOCIAL ENVIRONMENTAL RESOURCE ECONOMIC

Total turnover or total cost

Resources consumedPollution impacts

Social benefit of jobs

Benefits via taxation

Social benefit of product/service

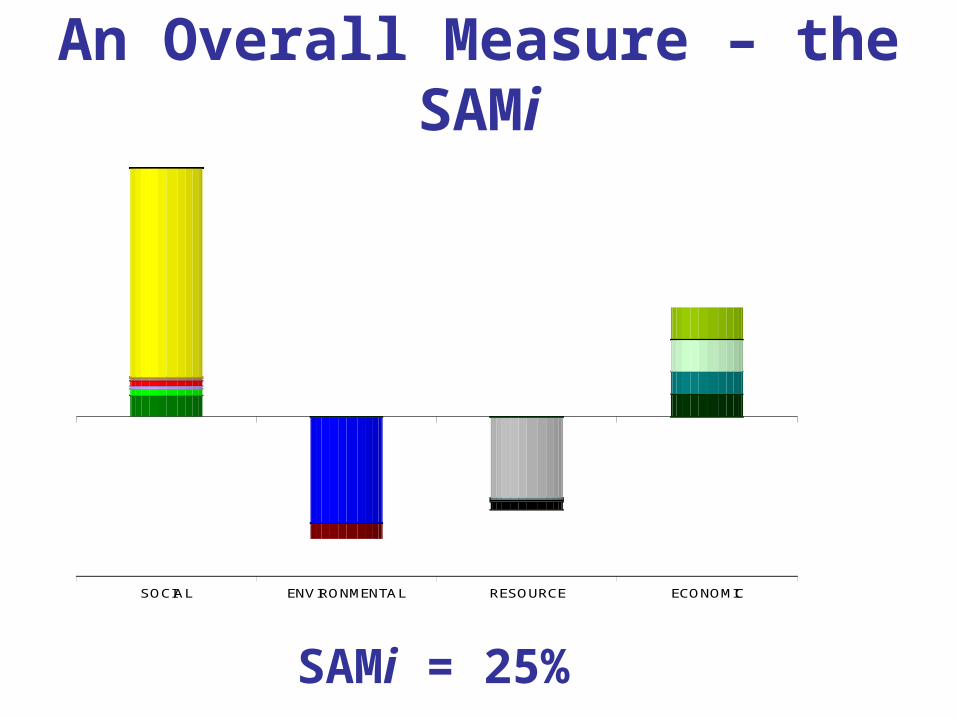

An Overall Measure – the SAMi

SOCIAL ENVIRONMENTAL RESOURCE ECONOMIC

SAMi = 25%

Summary

• Accounting– Discharging accountability– Negotiation about responsibility

• Sustainable development as a set of aspirations

• Governance– Full cost accounting is one technique– Implies a great deal