Embed Size (px)

Citation preview

Sustainable Industrial

Development?

Learning from the BRICS

Jomo Kwame Sundaram

Assistant Director-General

Food and Agriculture Organization

of the United Nations

Vienna, 20 November 2012

Outline

• BRICS pattern, model to emulate?

• Any lessons from BRICS?

• Do developing countries need

industrial policy?

• Implications of global economic

slowdown and other crises for

industrialization efforts?

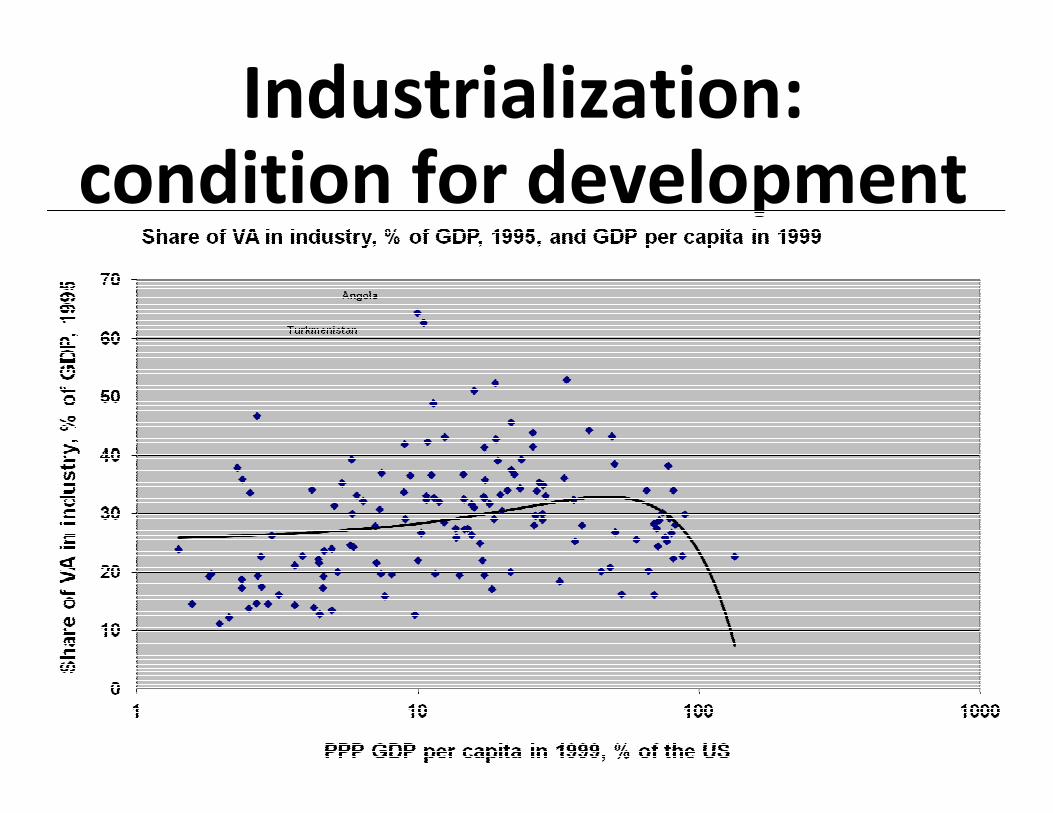

Industrialization: condition for development

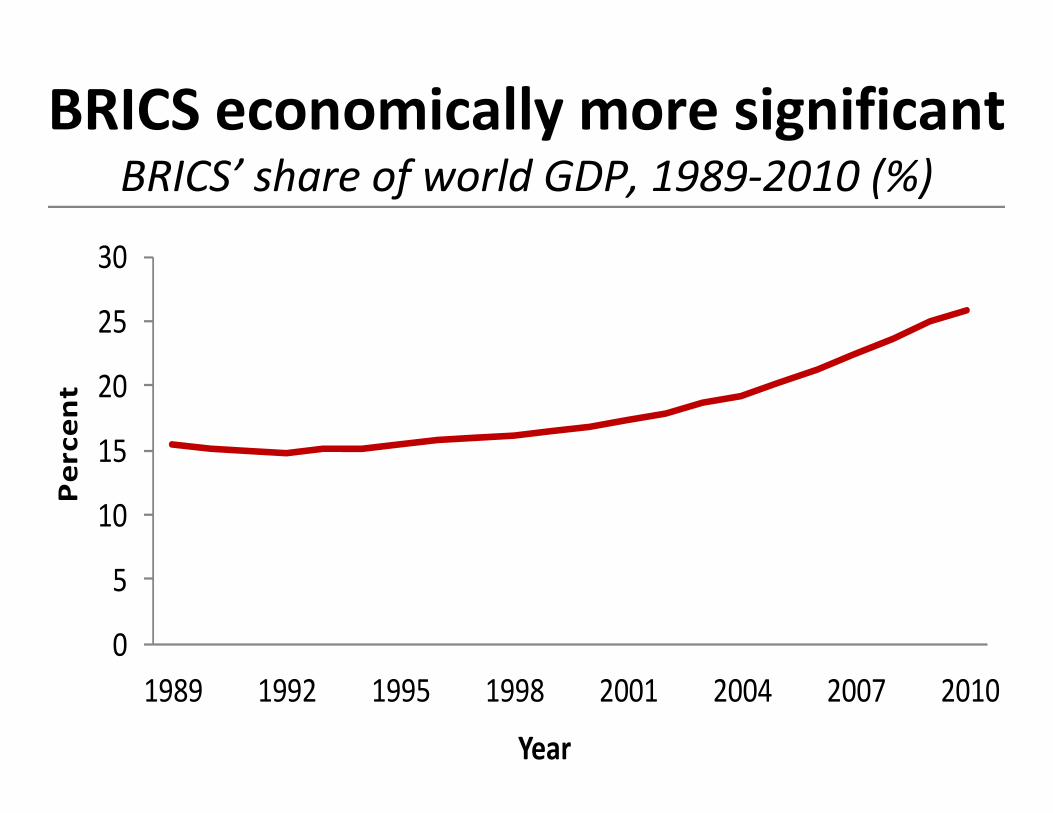

BRICS economically more significantBRICS’ share of world GDP, 1989-2010 (%)

0

5

10

15

20

25

30

1989 1992 1995 1998 2001 2004 2007 2010

Pe

rce

nt

Year

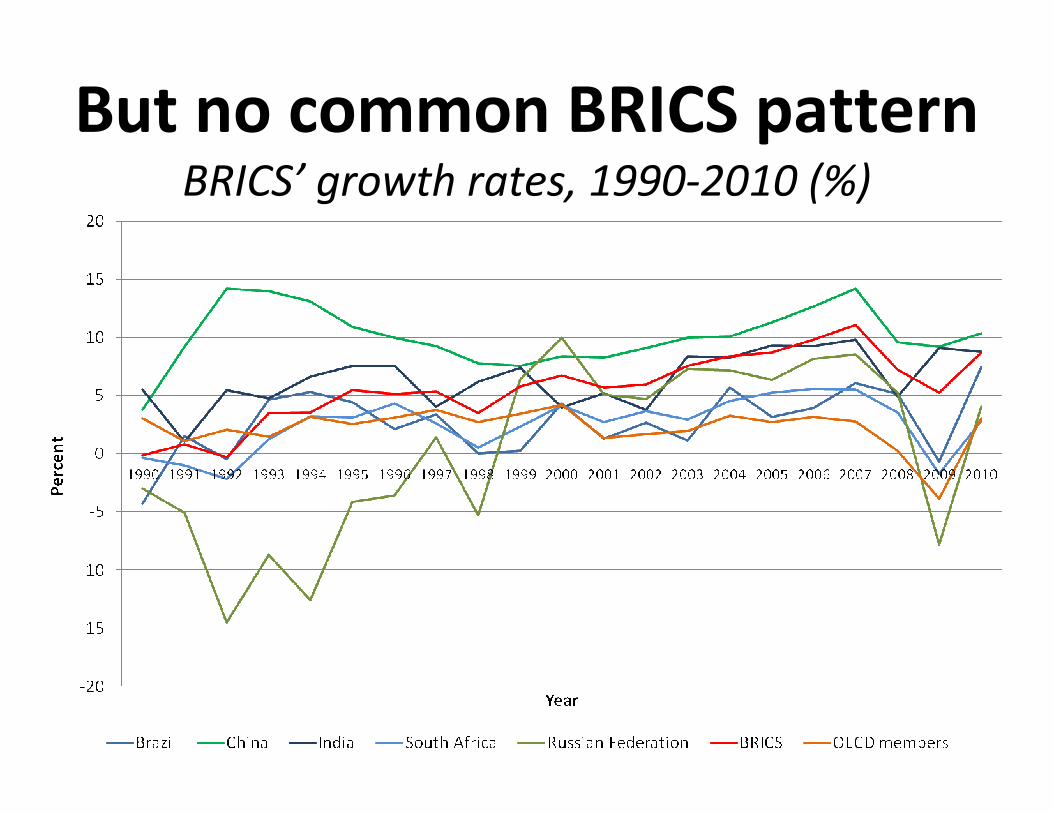

But no common BRICS patternBRICS’ growth rates, 1990-2010 (%)

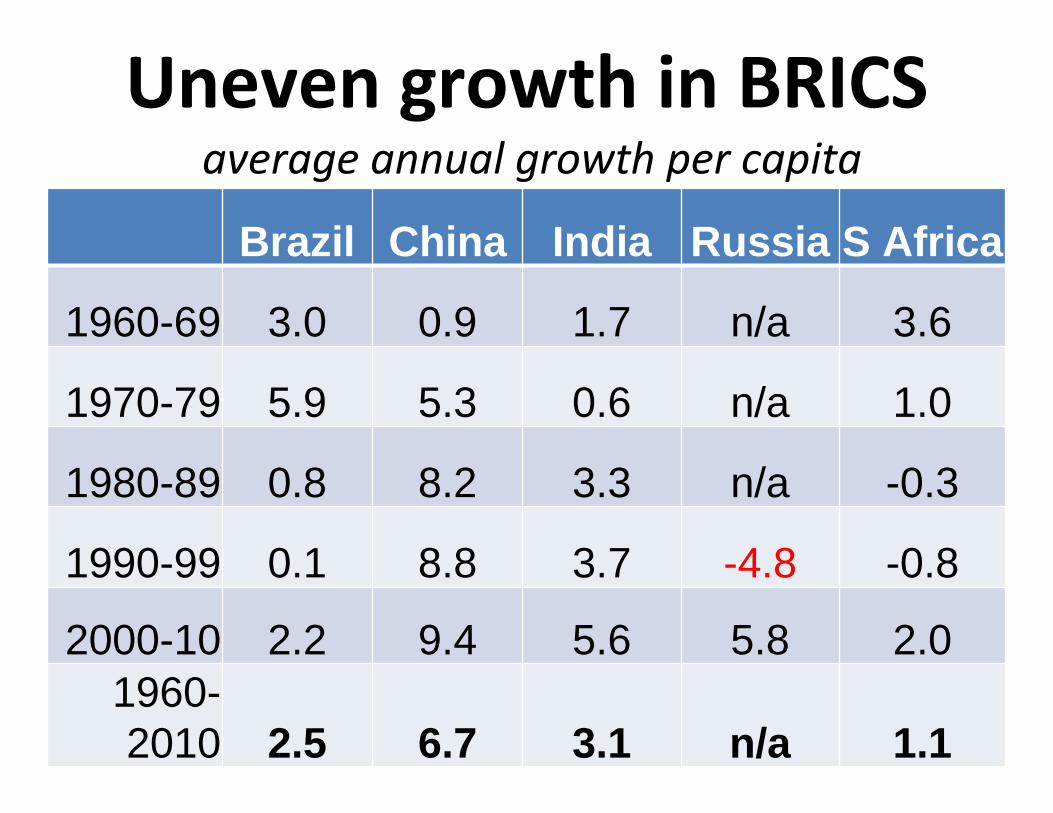

Uneven growth in BRICS average annual growth per capita

Brazil China India Russia S Africa

1960-69 3.0 0.9 1.7 n/a 3.6

1970-79 5.9 5.3 0.6 n/a 1.0

1980-89 0.8 8.2 3.3 n/a -0.3

1990-99 0.1 8.8 3.7 -4.8 -0.8

2000-10 2.2 9.4 5.6 5.8 2.01960-2010 2.5 6.7 3.1 n/a 1.1

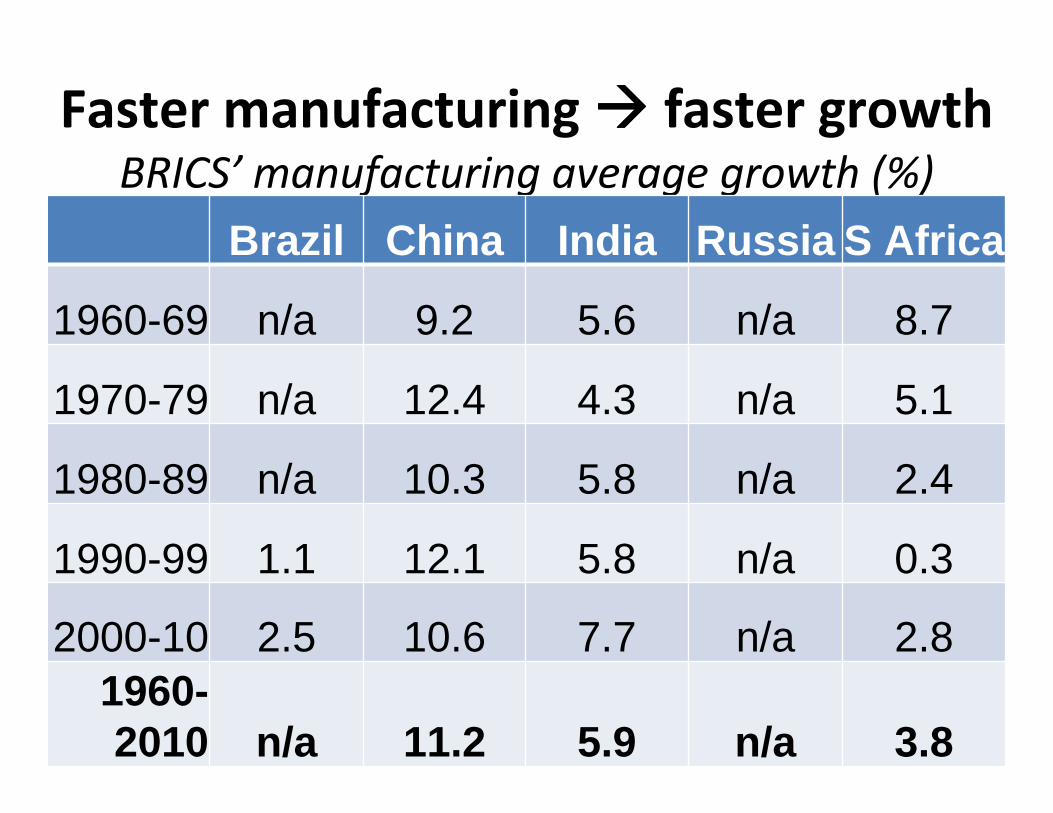

Faster manufacturing ���� faster growth BRICS’ manufacturing average growth (%)

Brazil China India Russia S Africa

1960-69 n/a 9.2 5.6 n/a 8.7

1970-79 n/a 12.4 4.3 n/a 5.1

1980-89 n/a 10.3 5.8 n/a 2.4

1990-99 1.1 12.1 5.8 n/a 0.3

2000-10 2.5 10.6 7.7 n/a 2.81960-2010 n/a 11.2 5.9 n/a 3.8

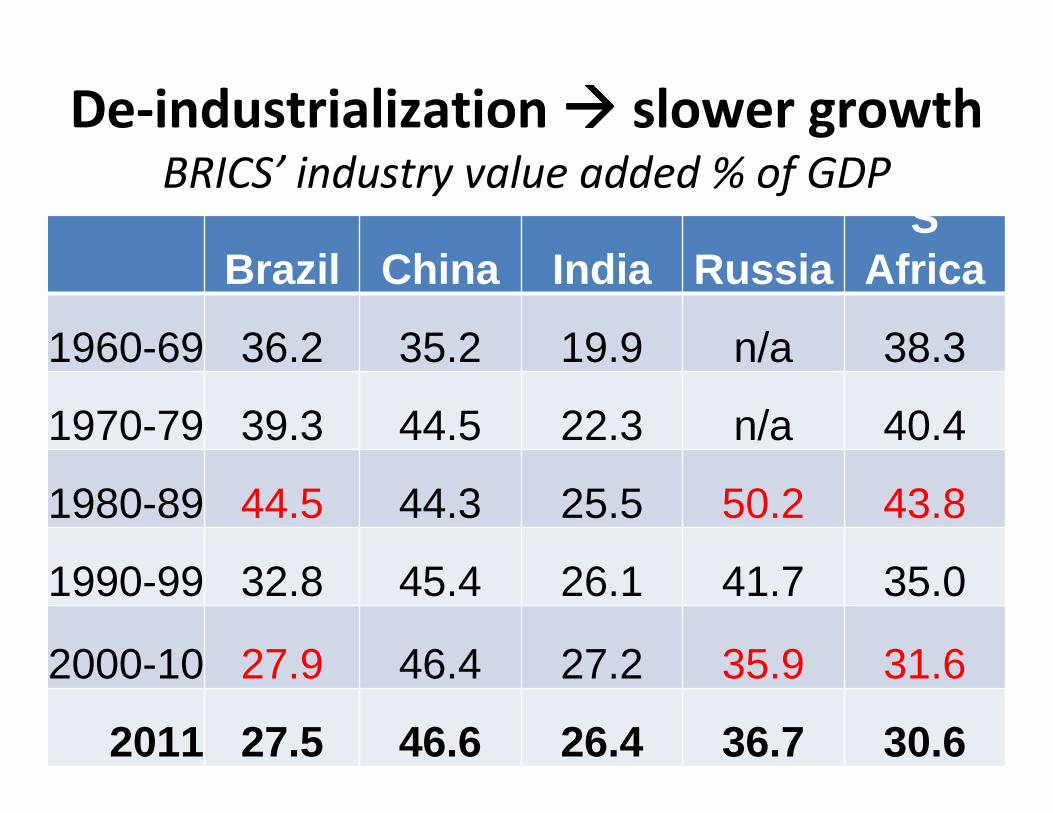

De-industrialization ���� slower growthBRICS’ industry value added % of GDP

Brazil China India RussiaS

Africa

1960-69 36.2 35.2 19.9 n/a 38.3

1970-79 39.3 44.5 22.3 n/a 40.4

1980-89 44.5 44.3 25.5 50.2 43.8

1990-99 32.8 45.4 26.1 41.7 35.0

2000-10 27.9 46.4 27.2 35.9 31.6

2011 27.5 46.6 26.4 36.7 30.6

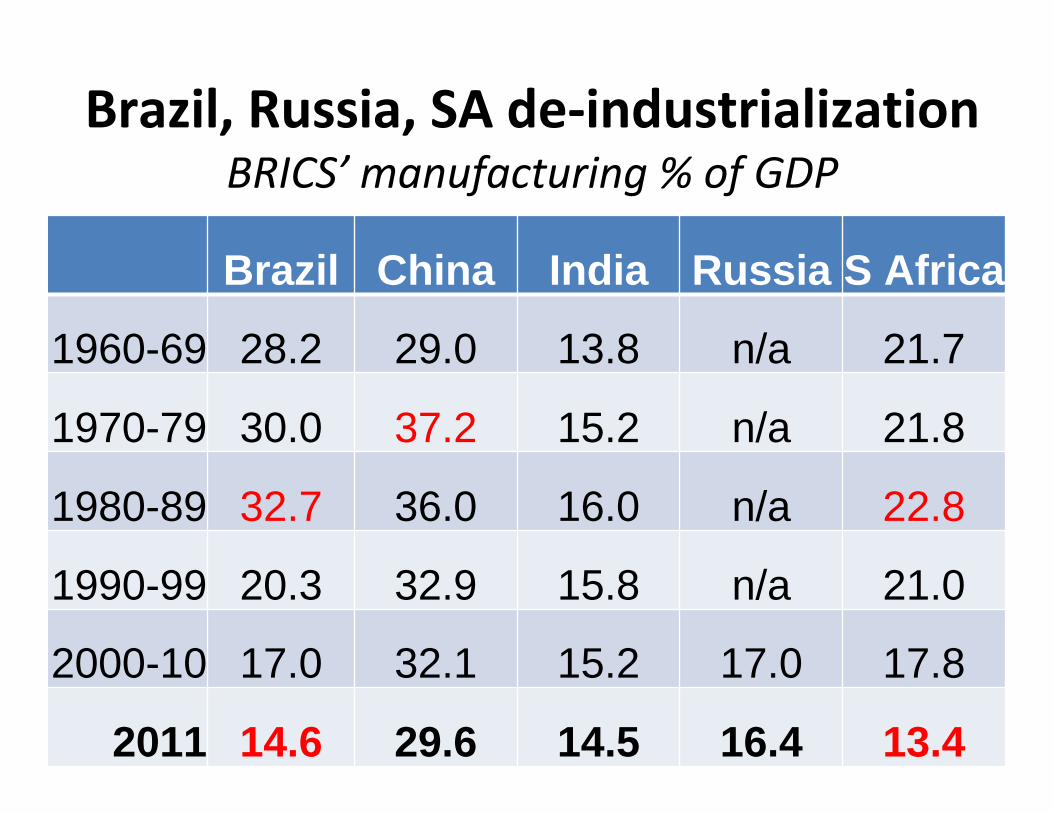

Brazil, Russia, SA de-industrialization BRICS’ manufacturing % of GDP

Brazil China India Russia S Africa

1960-69 28.2 29.0 13.8 n/a 21.7

1970-79 30.0 37.2 15.2 n/a 21.8

1980-89 32.7 36.0 16.0 n/a 22.8

1990-99 20.3 32.9 15.8 n/a 21.0

2000-10 17.0 32.1 15.2 17.0 17.8

2011 14.6 29.6 14.5 16.4 13.4

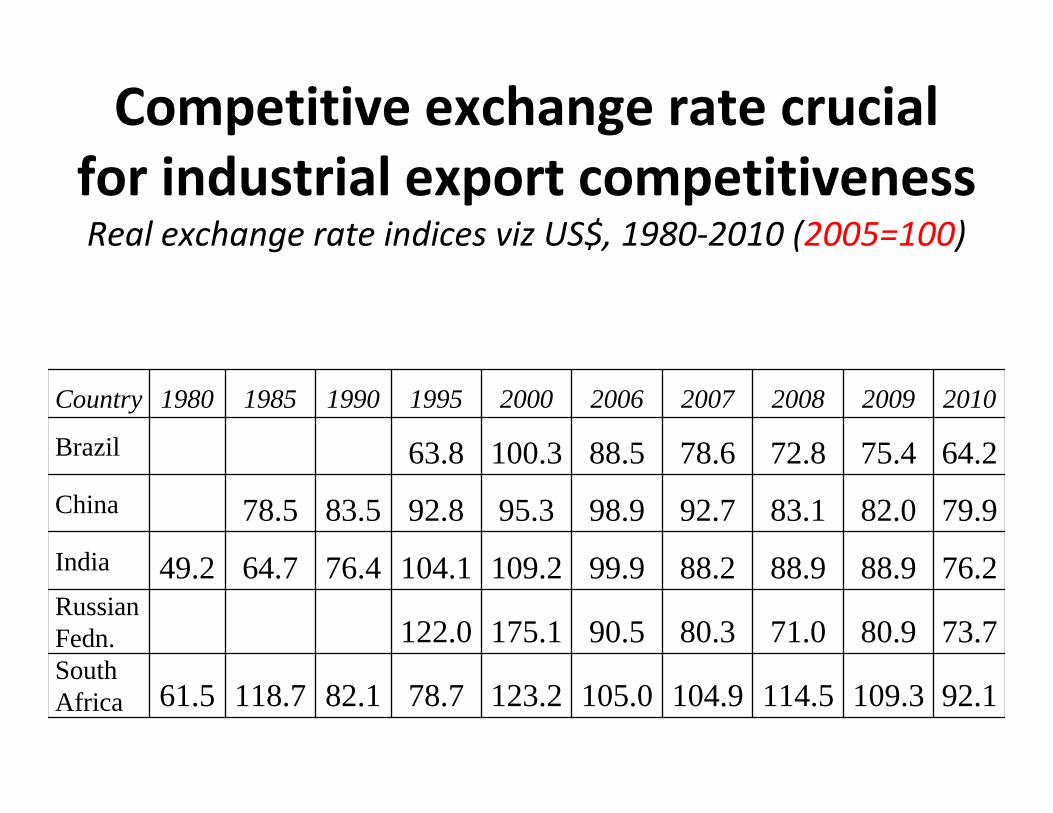

Competitive exchange rate crucial

for industrial export competitivenessReal exchange rate indices viz US$, 1980-2010 (2005=100)

Country 1980 1985 1990 1995 2000 2006 2007 2008 2009 2010

Brazil 63.8 100.3 88.5 78.6 72.8 75.4 64.2

China 78.5 83.5 92.8 95.3 98.9 92.7 83.1 82.0 79.9

India 49.2 64.7 76.4 104.1 109.2 99.9 88.2 88.9 88.9 76.2Russian Fedn. 122.0 175.1 90.5 80.3 71.0 80.9 73.7South Africa 61.5 118.7 82.1 78.7 123.2 105.0 104.9 114.5 109.3 92.1

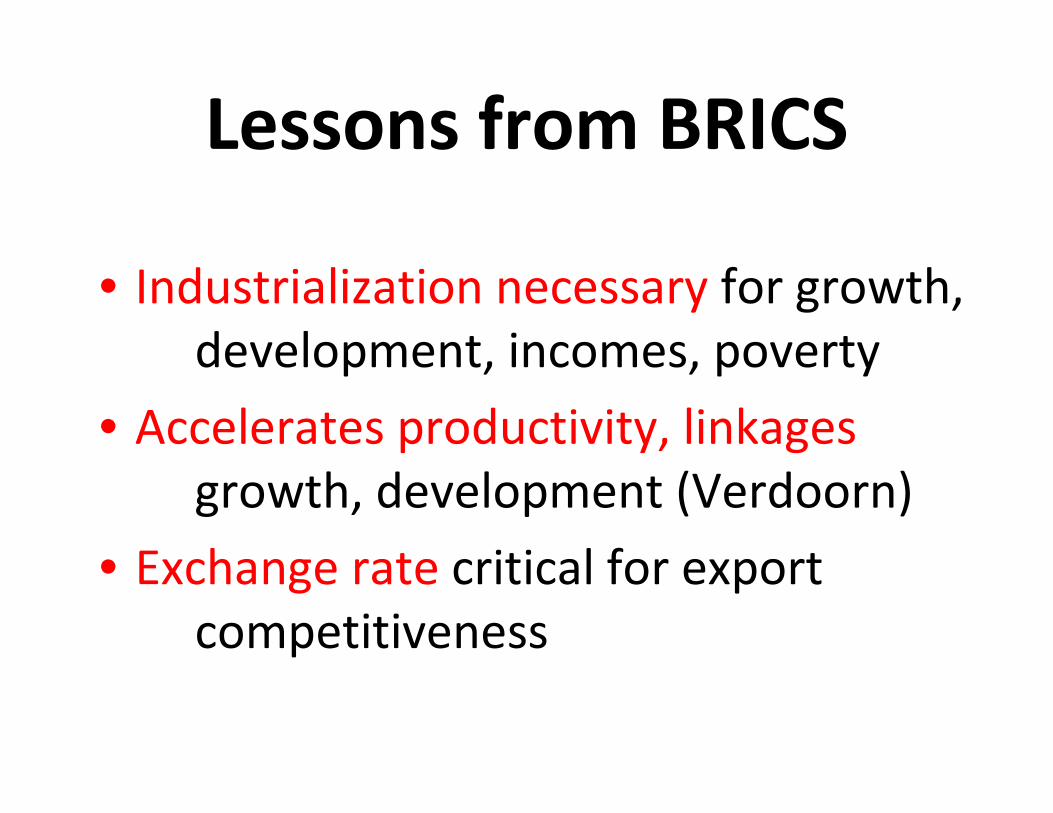

Lessons from BRICS

• Industrialization necessary for growth,

development, incomes, poverty

• Accelerates productivity, linkages

growth, development (Verdoorn)

• Exchange rate critical for export

competitiveness

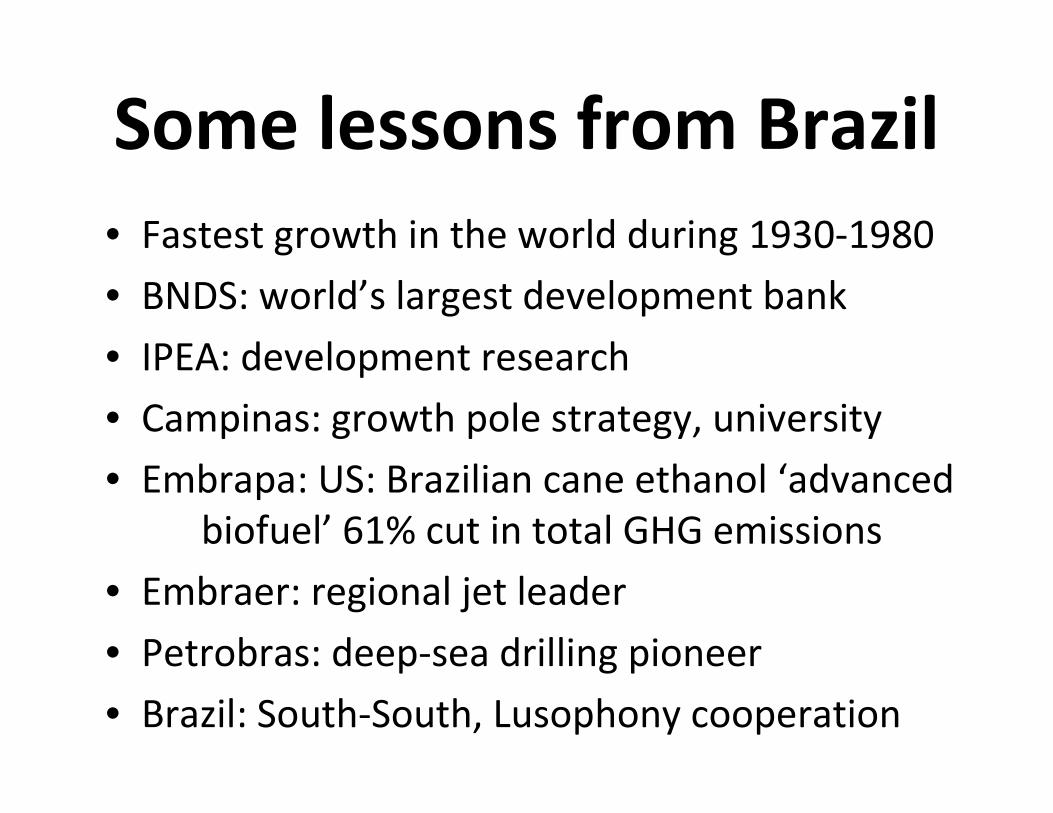

Some lessons from Brazil

• Fastest growth in the world during 1930-1980

• BNDS: world’s largest development bank

• IPEA: development research

• Campinas: growth pole strategy, university

• Embrapa: US: Brazilian cane ethanol ‘advanced

biofuel’ 61% cut in total GHG emissions

• Embraer: regional jet leader

• Petrobras: deep-sea drilling pioneer

• Brazil: South-South, Lusophony cooperation

Brazil: rapid growth,

industrialization, 1930-1980

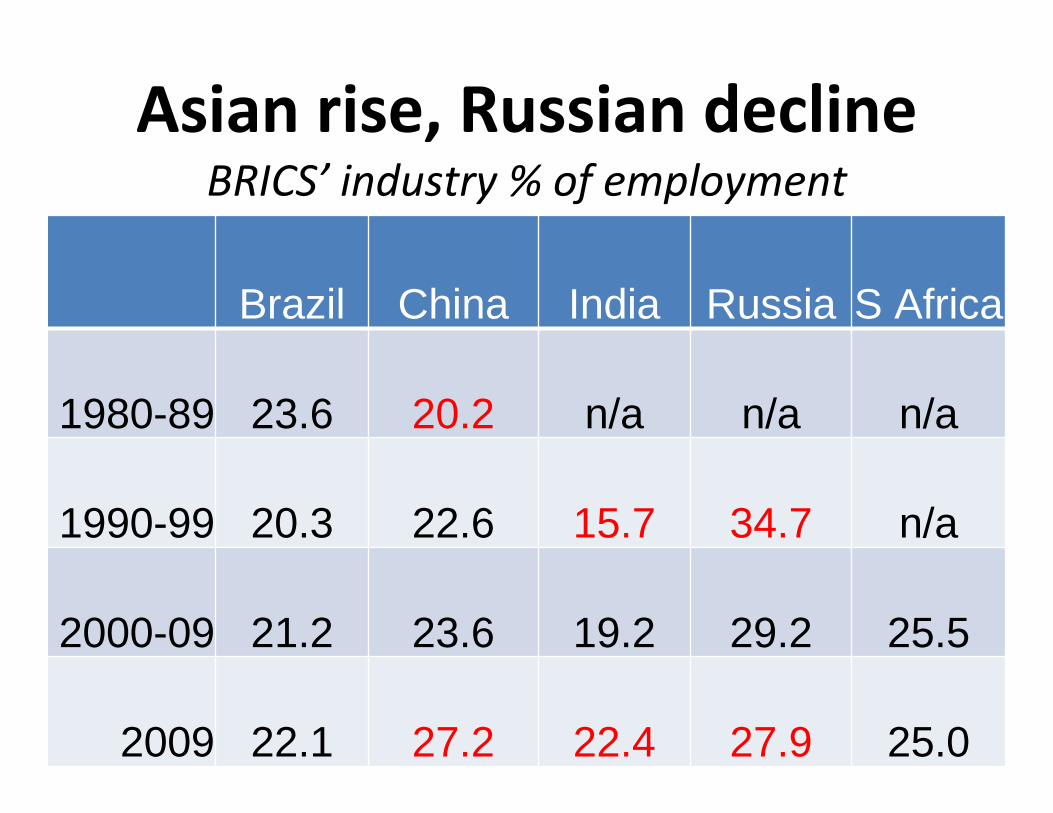

Asian rise, Russian declineBRICS’ industry % of employment

Brazil China India Russia S Africa

1980-89 23.6 20.2 n/a n/a n/a

1990-99 20.3 22.6 15.7 34.7 n/a

2000-09 21.2 23.6 19.2 29.2 25.5

2009 22.1 27.2 22.4 27.9 25.0

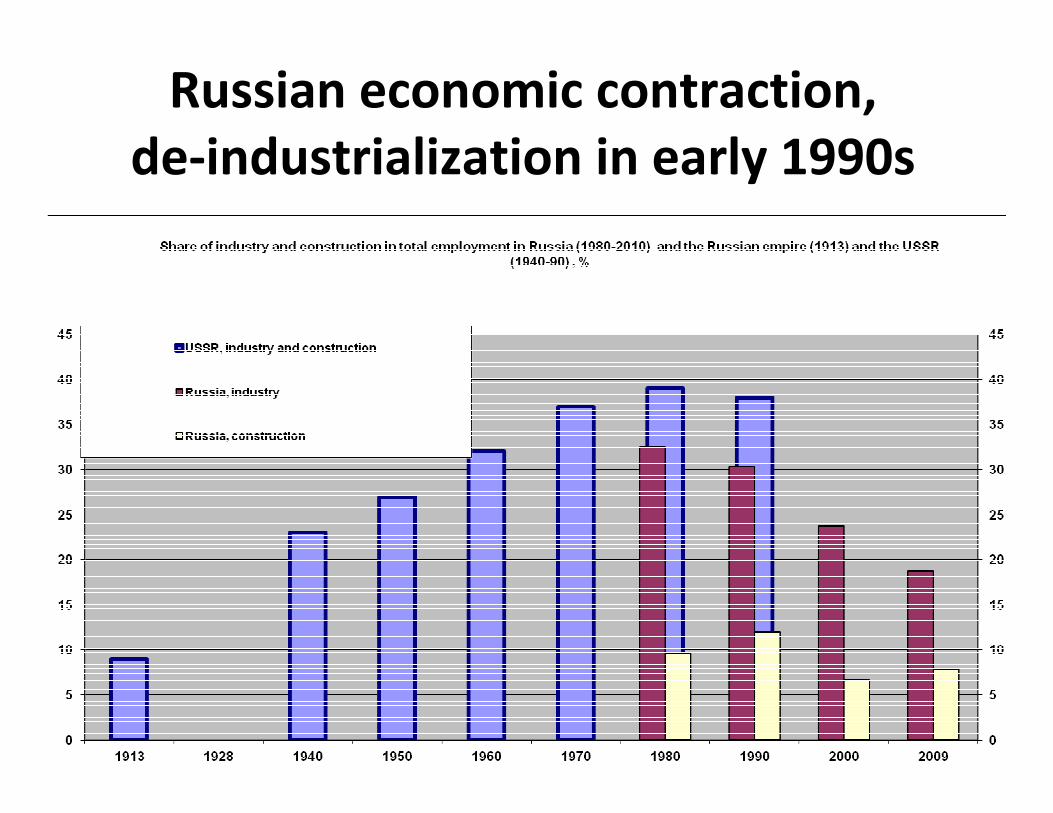

Russian economic contraction,

de-industrialization in early 1990s

Some lessons from Russia

• Rapid industrialization, growth, 1930s-1960s

despite wars

• University technical education

• Aero-space program

• Military industries: MIGs, Tupolev,

Kalashnikov

• Gazprom

• Rusnano: the ‘conversion’ of Anatoly Chubais

• Science/technology programs’ mixed records

Some lessons from India

• University technology education: world

standard -- Indian Institute of Technology

• Popular science movements

• Dissemination of grassroots innovation

• Tata: pioneer of ‘Fordism’

• Hindustan Machine Tools

• India’s ‘white revolution’: cooperative

pasteurization – phyto-sanitary standards

(Verghese Kurien)

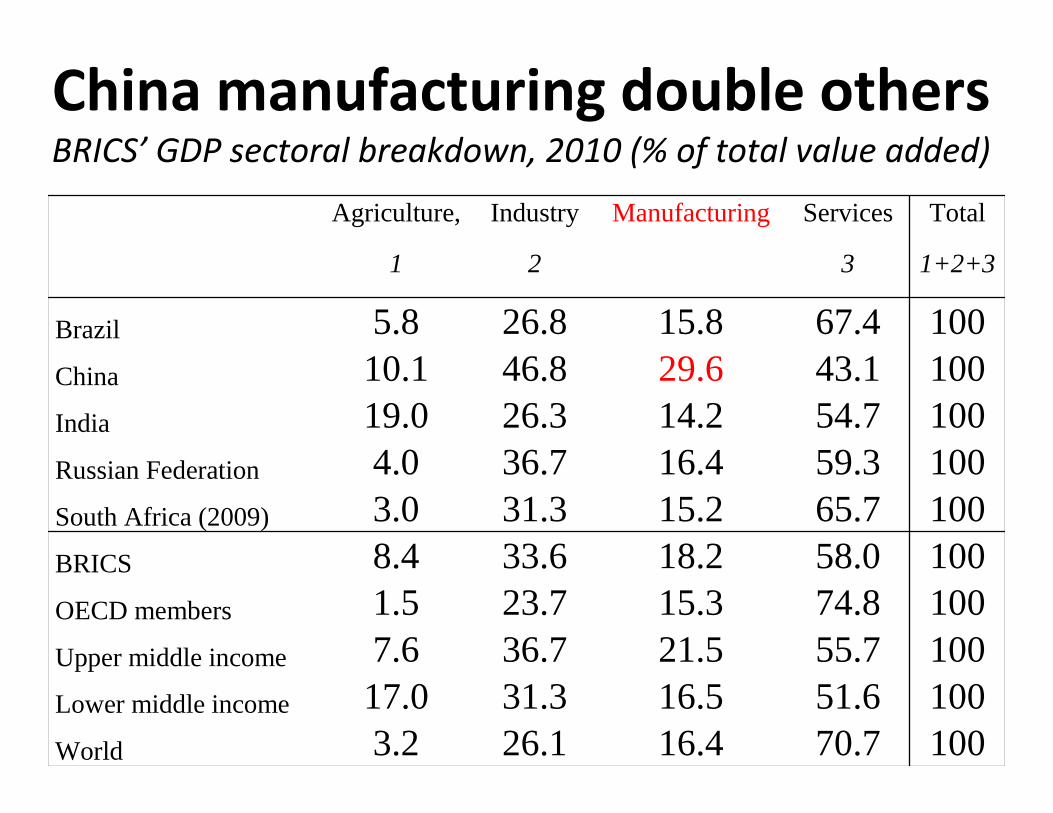

China manufacturing double othersBRICS’ GDP sectoral breakdown, 2010 (% of total value added)

Agriculture, Industry Manufacturing Services Total

1 2 3 1+2+3

Brazil 5.8 26.8 15.8 67.4 100China 10.1 46.8 29.6 43.1 100India 19.0 26.3 14.2 54.7 100Russian Federation 4.0 36.7 16.4 59.3 100South Africa (2009) 3.0 31.3 15.2 65.7 100BRICS 8.4 33.6 18.2 58.0 100OECD members 1.5 23.7 15.3 74.8 100Upper middle income 7.6 36.7 21.5 55.7 100Lower middle income 17.0 31.3 16.5 51.6 100World 3.2 26.1 16.4 70.7 100

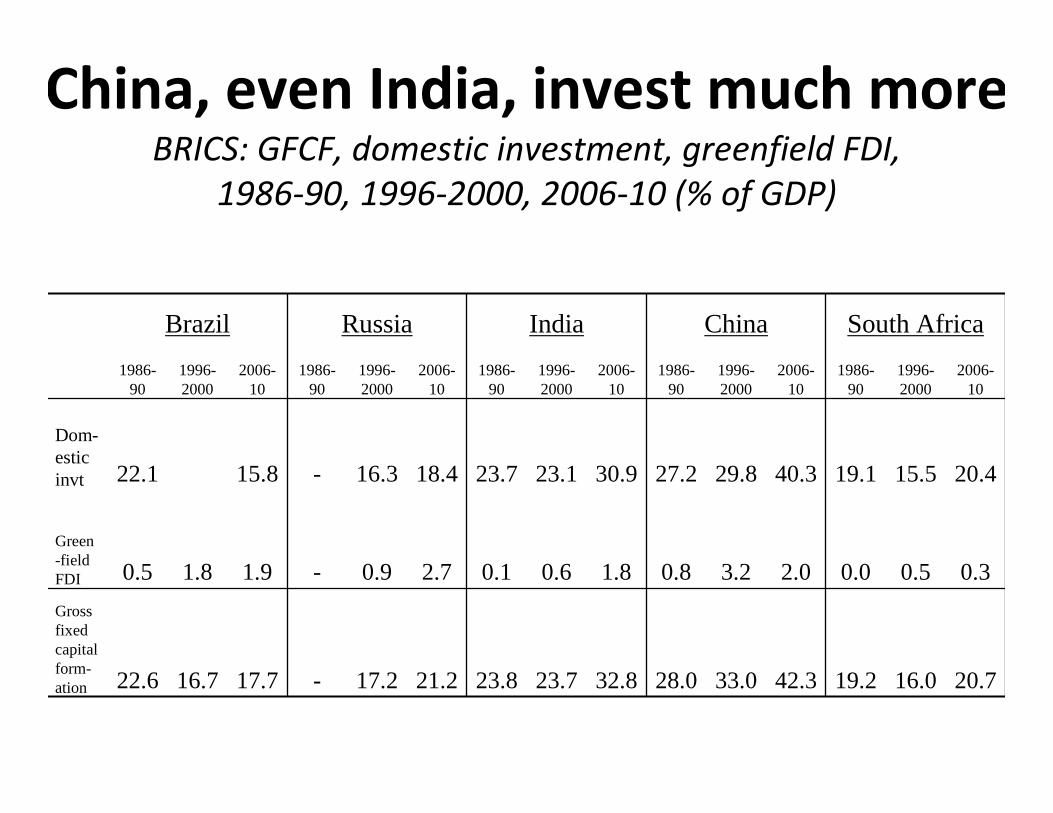

China, even India, invest much moreBRICS: GFCF, domestic investment, greenfield FDI,

1986-90, 1996-2000, 2006-10 (% of GDP)

Brazil Russia India China South Africa

1986-90

1996-2000

2006-10

1986-90

1996-2000

2006-10

1986-90

1996-2000

2006-10

1986-90

1996-2000

2006-10

1986-90

1996-2000

2006-10

Dom-estic invt 22.1 15.8 - 16.3 18.4 23.7 23.1 30.9 27.2 29.8 40.3 19.1 15.5 20.4

Green-field FDI 0.5 1.8 1.9 - 0.9 2.7 0.1 0.6 1.8 0.8 3.2 2.0 0.0 0.5 0.3

Gross fixed capitalform-ation 22.6 16.7 17.7 - 17.2 21.2 23.8 23.7 32.8 28.0 33.0 42.3 19.2 16.0 20.7

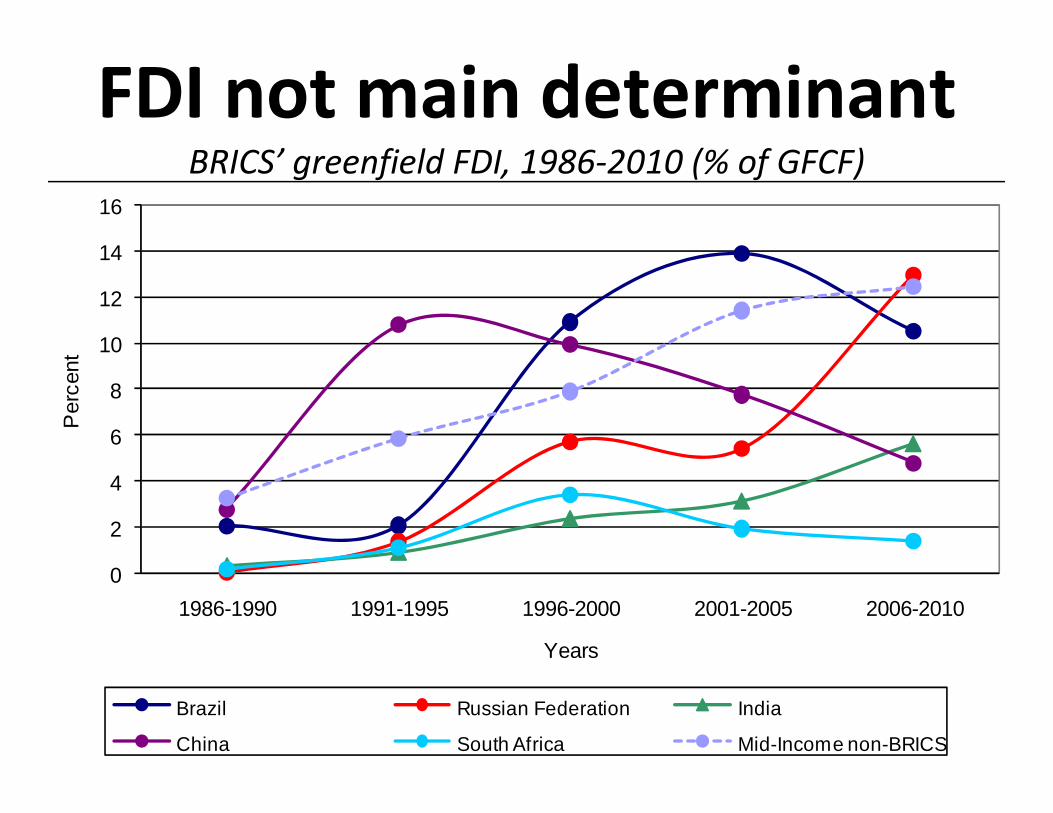

FDI not main determinantBRICS’ greenfield FDI, 1986-2010 (% of GFCF)

0

2

4

6

8

10

12

14

16

1986-1990 1991-1995 1996-2000 2001-2005 2006-2010

Per

cent

Years

Brazil Russian Federation India

China South Africa Mid-Income non-BRICS

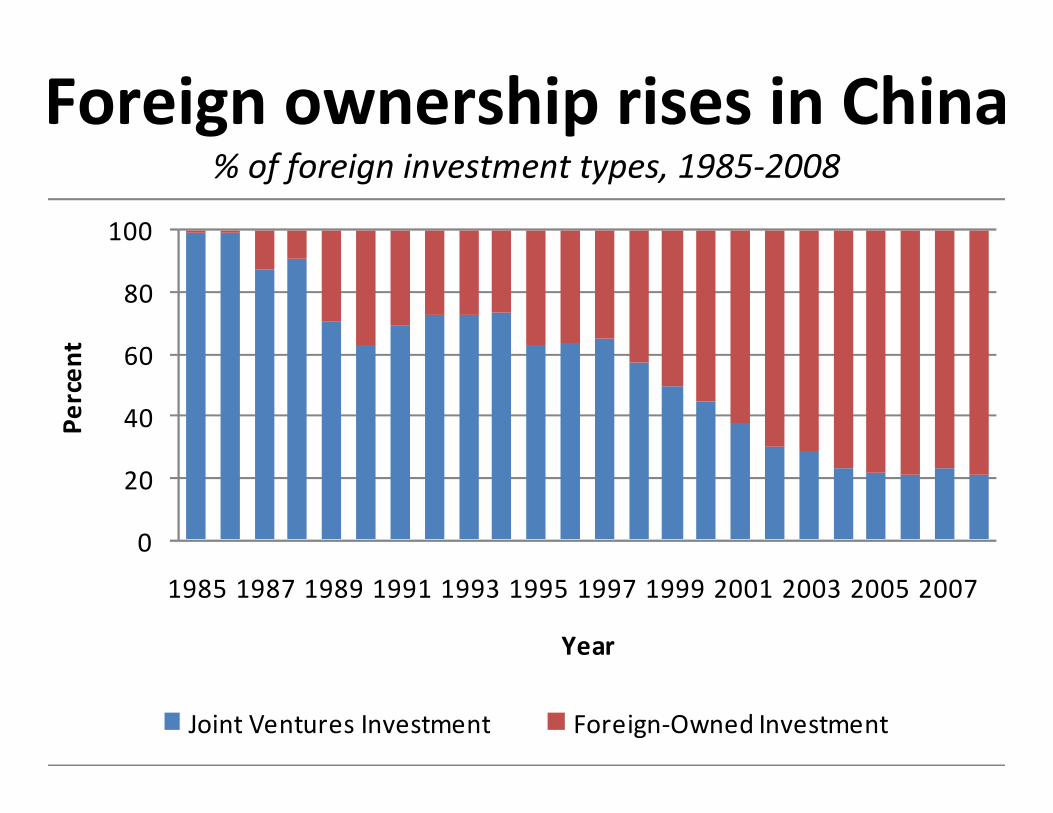

Foreign ownership rises in China % of foreign investment types, 1985-2008

0

20

40

60

80

100

1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007

Pe

rce

nt

Year

Joint Ventures Investment Foreign-Owned Investment

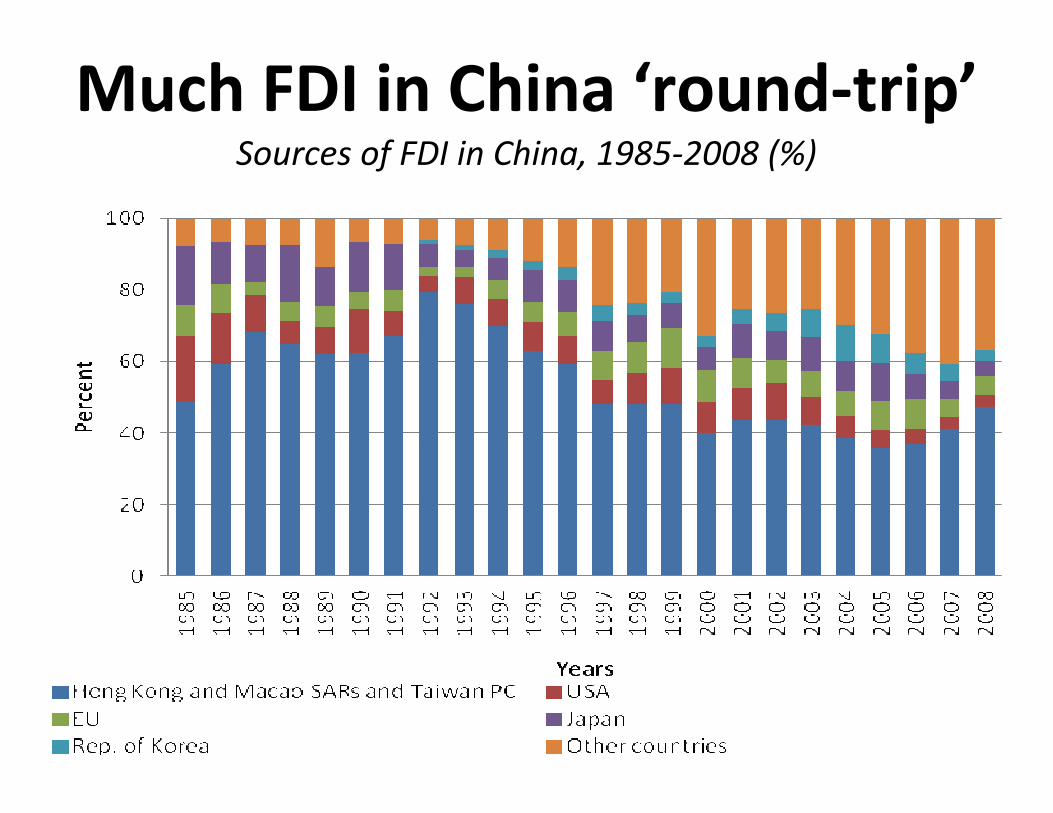

Much FDI in China ‘round-trip’Sources of FDI in China, 1985-2008 (%)

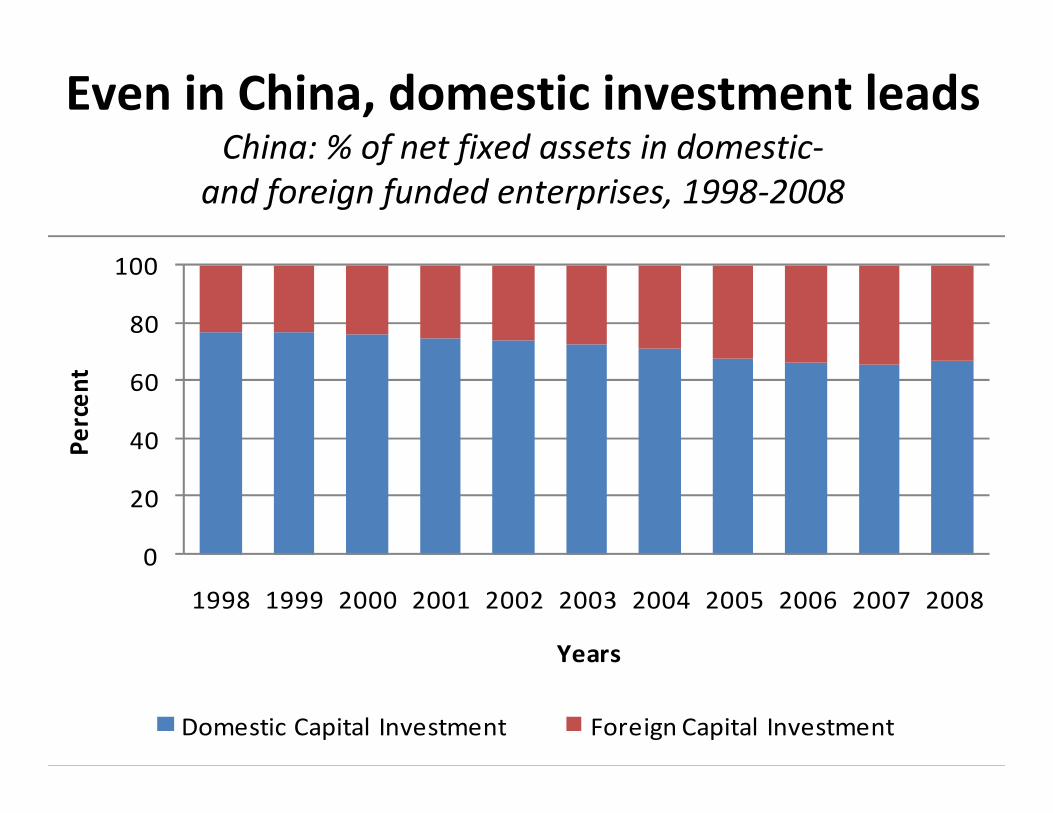

Even in China, domestic investment leadsChina: % of net fixed assets in domestic-

and foreign funded enterprises, 1998-2008

0

20

40

60

80

100

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Pe

rce

nt

Years

Domestic Capital Investment Foreign Capital Investment

Some lessons from China

• Heavier reliance on FDI

• Chinese overtakes US: steel, cars, beer, cotton,

coal, tobacco, hi-tech products, including

solar cells, wind turbines, ‘organic’ plastic,

new pharmaceutical drugs,

• China Development Bank

• Major South-South investor

• Bao Steel: most efficient steel producer (SOE)

• Manufacturing exports slowdown hurts SE Asia

coal,

Some lessons from S Africa

• Industrial Development Corporation (IDC): SA

industrialization -- apartheid era sanctions

• Southern African Development Bank (SADB)

transformed role

• Nuclear program abandoned post-Apartheid

• Recent reconsideration of pebble bed nuclear

technology

• Southern hemisphere appreciation of

Montreal protocol on CFCs: common but

differentiated responsibility for climate

Why industrialize?

International terms of trade have moved against developing countries

1. Primary commodities vs manufactures (Singer-Prebisch)

2. Tropical vs temperate agriculture (W A Lewis)

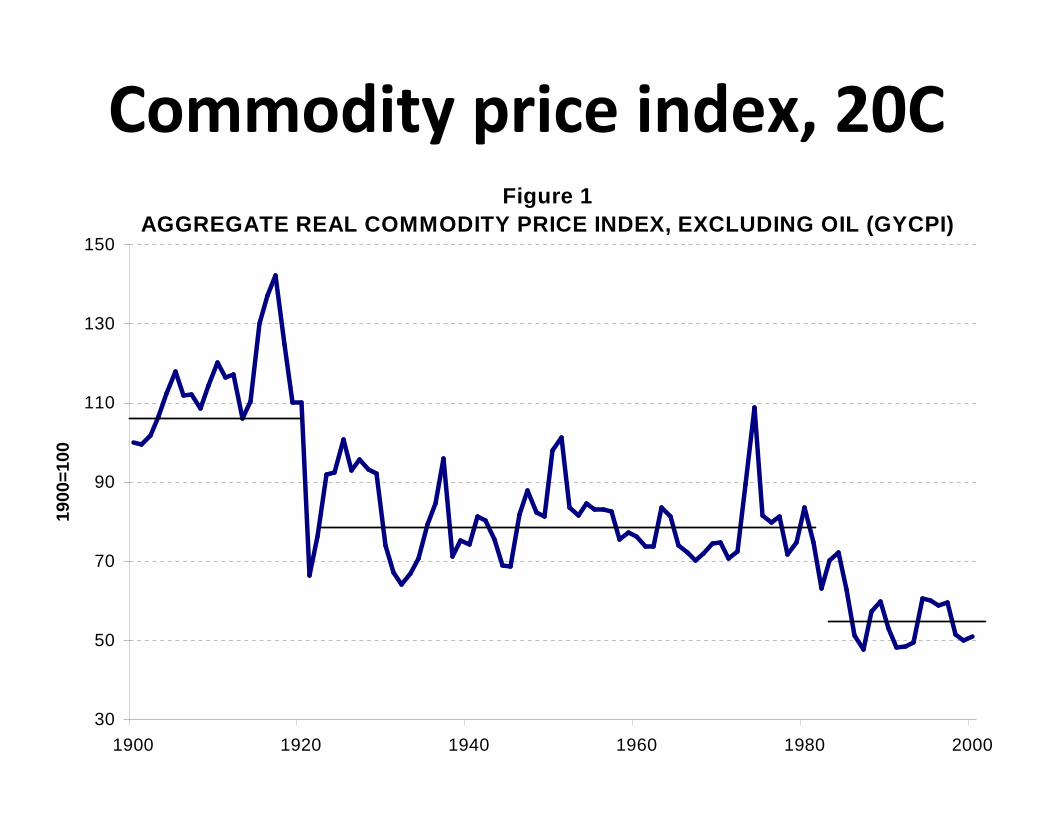

Commodity price index, 20CFigure 1

AGGREGATE REAL COMMODITY PRICE INDEX, EXCLUDING OIL (GYCPI)

30

50

70

90

110

130

150

1900 1920 1940 1960 1980 2000

1900

=100

Why industrialize?International terms of trade have moved

against developing countries

1. Primary commodities vs manufactures

2. Tropical vs temperate agriculture

3. South vs North manufactured Xs

� productivity gains lost by producers to consumers unless supply monopolistic (e.g. with IPRs)

South vs North manufacturedexports’ terms of trade

Unit value of manufactures exported by developing countries relative to manufactures exported by developed countries

90

95

100

105

110

115

120

125

130

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2001

2002

2000

=10

0

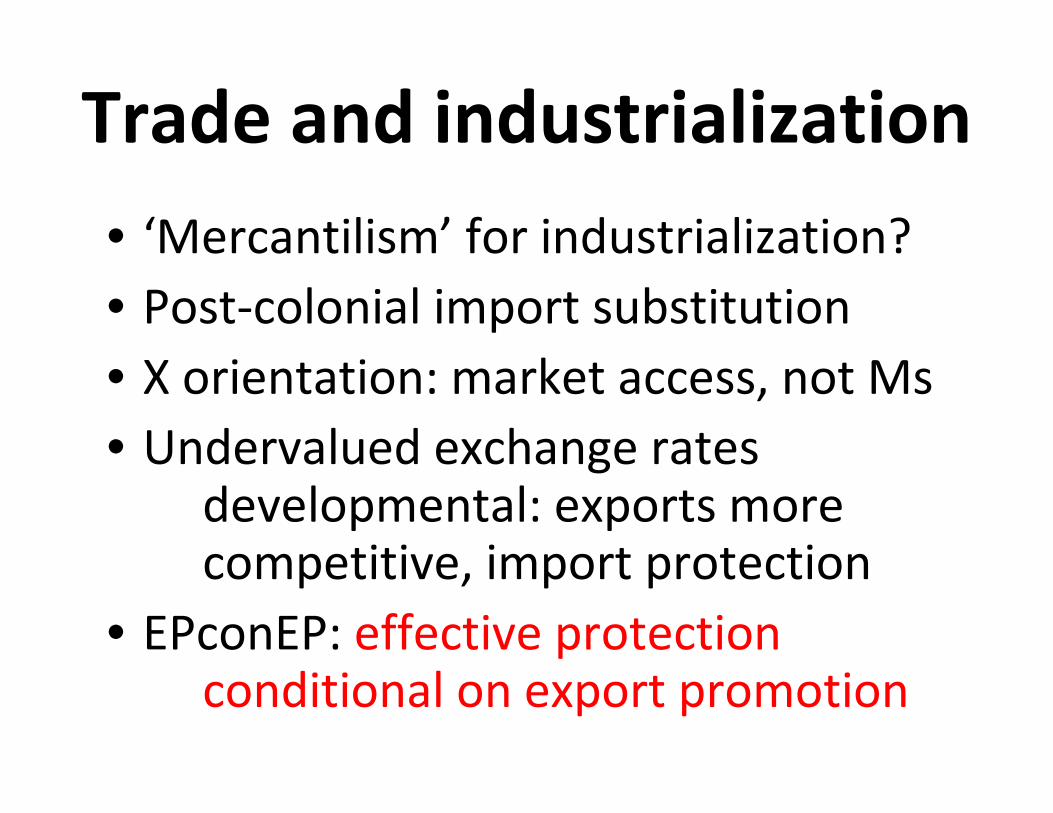

Trade and industrialization

• ‘Mercantilism’ for industrialization?

• Post-colonial import substitution

• X orientation: market access, not Ms

• Undervalued exchange rates developmental: exports morecompetitive, import protection

• EPconEP: effective protection conditional on export promotion

Industrial policy?

1. Evaluate potential competitiveness of

industries, branches, components

2. Support learning by doing; critical

support for potentially successful

3. Carefully use selective industrial

policy tools

Crafting industrial policyIdentify:

• national priorities for investment,

technology policy

• critical constraints, bottlenecks

Consider:

• existing economic sectors + sub-sectors

• Backward, forward linkages

• national priorities (employment growth,

wage growth, export earnings, etc.)

32

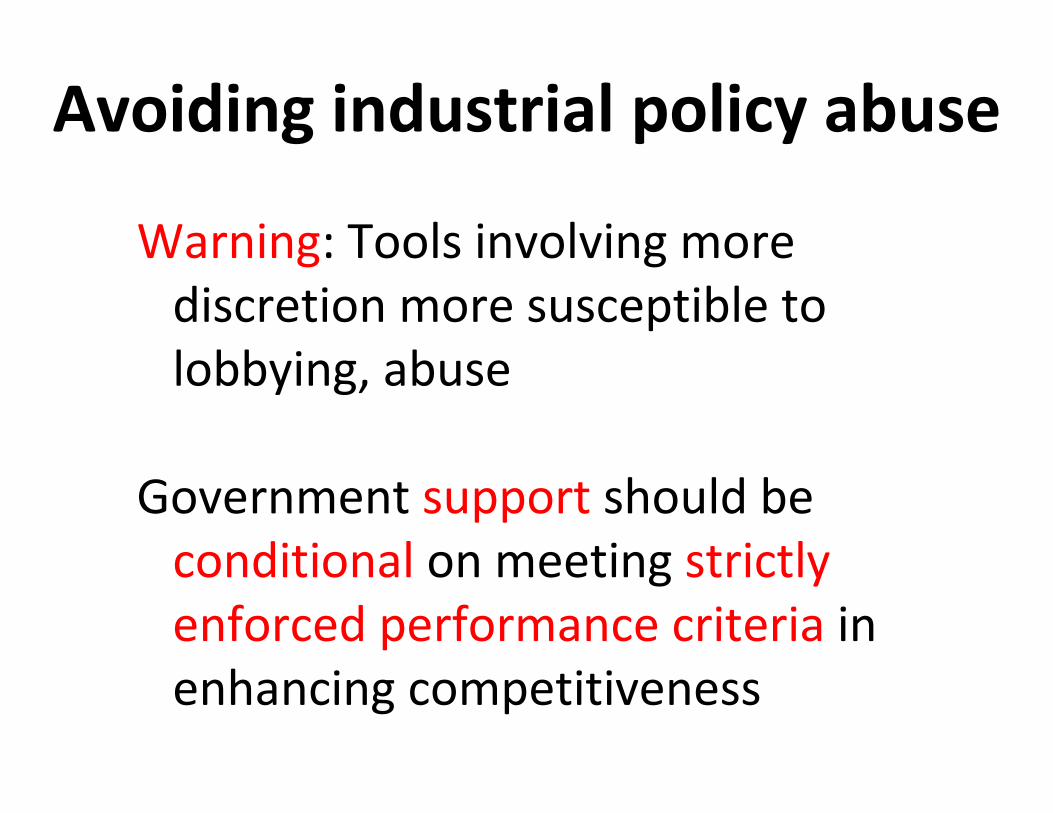

Avoiding industrial policy abuse

Warning: Tools involving more

discretion more susceptible to

lobbying, abuse

Government support should be

conditional on meeting strictly

enforced performance criteria in

enhancing competitiveness

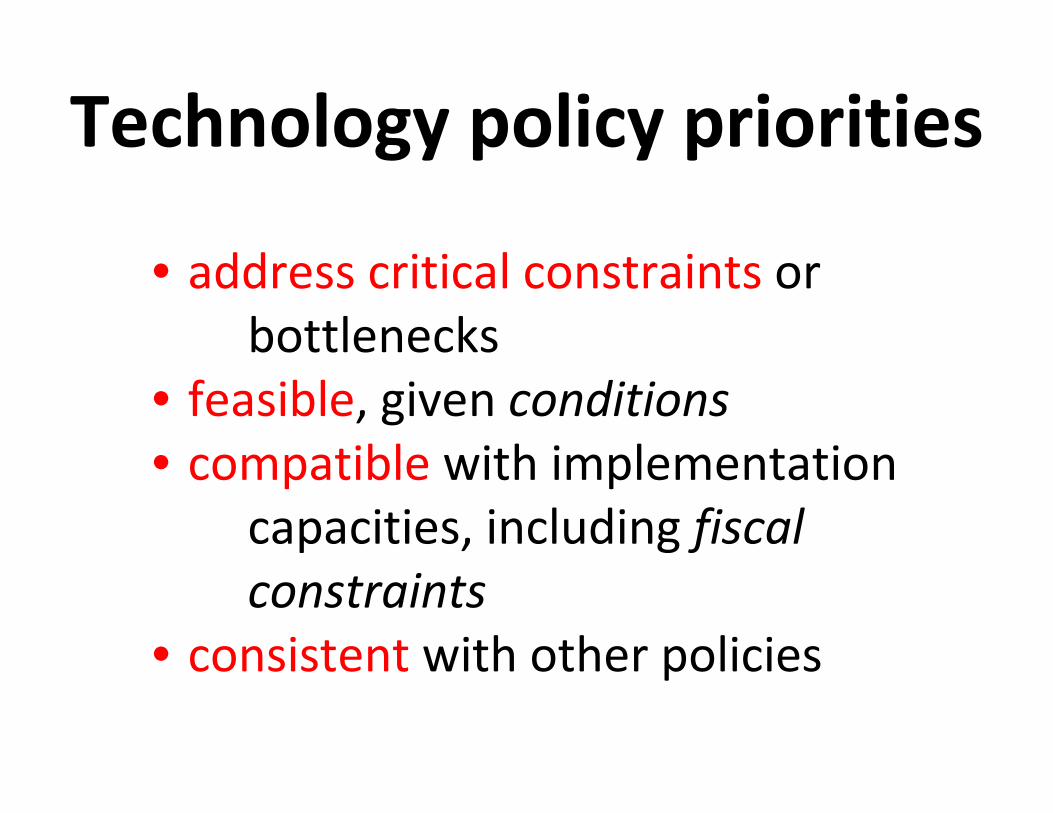

Technology policy priorities

• address critical constraints or

bottlenecks

• feasible, given conditions

• compatible with implementation

capacities, including fiscal

constraints

• consistent with other policies

Pre-crisis over-investment has impeded recovery

Cheap credit � over-investment

� under-utilized capacity

� private sector reluctant to invest

� need cross-subsidized public

investments, incentives to induce

private investments in renewable

energy, smallholder food agriculture

Global Green New Deal

Addressing crises together? – Financial– Food– Climate – Jobs – Development

New Deal? recovery, jobsGreen? food, climateGlobal? inequality, development

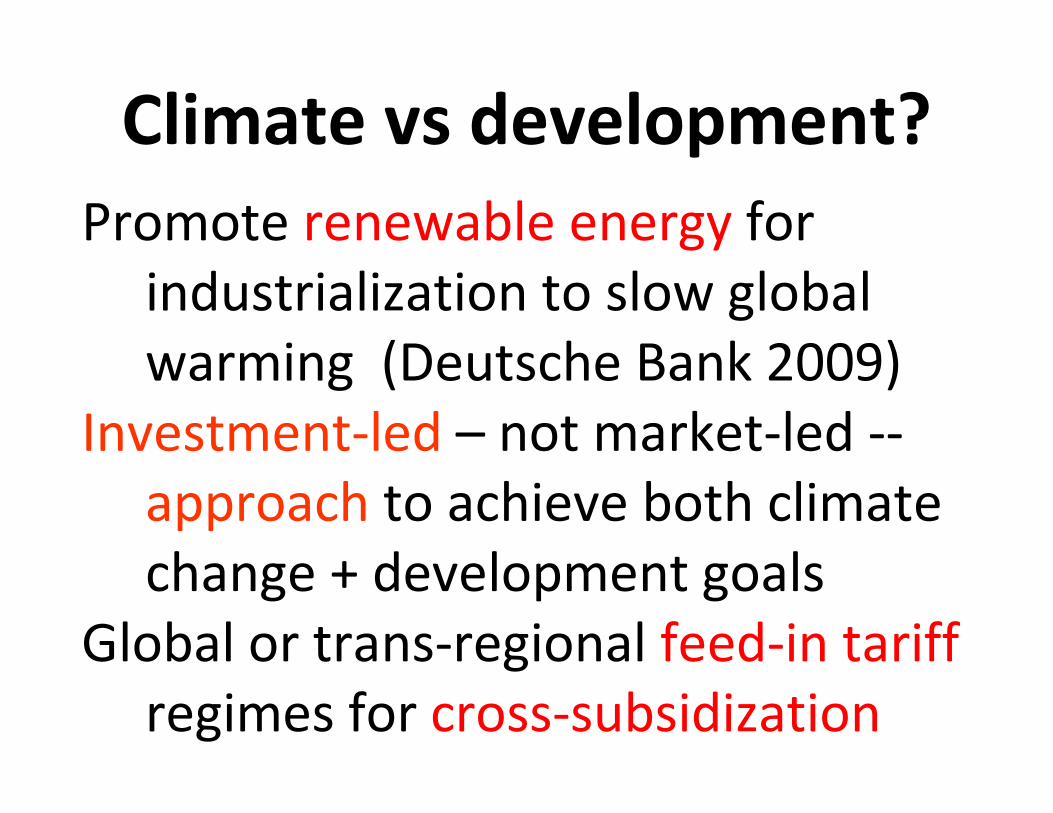

Climate vs development?

Promote renewable energy for

industrialization to slow global

warming (Deutsche Bank 2009)

Investment-led – not market-led --

approach to achieve both climate

change + development goals

Global or trans-regional feed-in tariff

regimes for cross-subsidization

Policy implications

Investments must be front-loaded, given danger of lock-in and importance of scale, learning economies for technology leapfrogging

Public investment to crowd-inprivate investment to sustain new development pathway

Significant transfers (finance, technology) required for big push

Summary

• No BRICS pattern, model

• Many lessons from BRICS nonetheless

• Appropriate industrial (investment,

technology) policies crucial

• Technical cooperation crucial: need

coherence, complementariness

• GGND: investment-led promotion of

renewable energy for sustainable

industrialization, overcome poverty

40

Thank youSome relevant publications:

Manufacturing Competitiveness in Asia

Technology, Competitiveness and the State

Globalization and Development in Sub-Saharan Africa

Reforming the International Financial System for

Development

Poor Poverty: The Impoverishment of Analysis,

Measurement and Policies

Growth Divergences: Explaining differences in economic

performance

Policy Matters: Economic and Social Policies To Sustain

Equitable Development

The New Development Economics

![[AW]policy BRICS - ITD · กลุ่มประเทศ brics จะก่อให้เกิดประโยชน์ทางเศรษฐกิจกับไทย”](https://img.pdfslide.net/doc/110x75/5eb6589d95ac763ff45c6af5/awpolicy-brics-aaaaaaaaaaa-brics-aaaaaafaaaaaaaaaaaaaaoeaaaaaaaaaaaaaaaaaa.jpg)