Embed Size (px)

DESCRIPTION

taxtaxtax

Citation preview

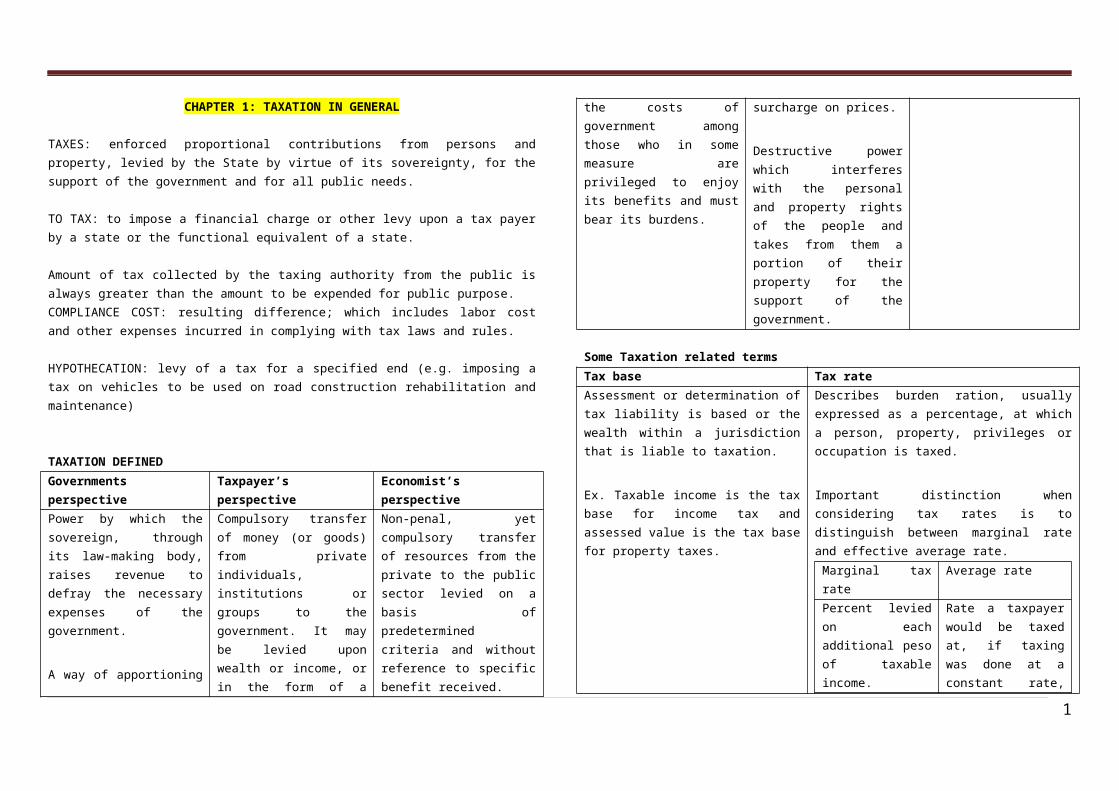

CHAPTER 1: TAXATION IN GENERAL

TAXES: enforced proportional contributions from persons and property, levied by the State by virtue of its sovereignty, for the support of the government and for all public needs.

TO TAX: to impose a financial charge or other levy upon a tax payer by a state or the functional equivalent of a state.

Amount of tax collected by the taxing authority from the public is always greater than the amount to be expended for public purpose. COMPLIANCE COST: resulting difference; which includes labor cost and other expenses incurred in complying with tax laws and rules.

HYPOTHECATION: levy of a tax for a specified end (e.g. imposing a tax on vehicles to be used on road construction rehabilitation and maintenance)

TAXATION DEFINEDGovernments perspective Taxpayer’s perspective Economist’s perspective

Power by which the sovereign, through its law-making body, raises revenue to defray the necessary expenses of the government.

A way of apportioning the costs of government among those who in some measure are privileged to enjoy its benefits and must bear its burdens.

Compulsory transfer of money (or goods) from private individuals, institutions or groups to the government. It may be levied upon wealth or income, or in the form of a surcharge on prices.

Destructive power which interferes with the personal and property rights of the people and takes from them a portion of their property for the support of the government.

Non-penal, yet compulsory transfer of resources from the private to the public sector levied on a basis of predetermined criteria and without reference to specific benefit received.

Some Taxation related termsTax base Tax rate

Assessment or determination of tax liability is based or the wealth within a jurisdiction that is liable to taxation.

Ex. Taxable income is the tax base for income tax and assessed value is the tax base for property taxes.

Describes burden ration, usually expressed as a percentage, at which a person, property, privileges or occupation is taxed.

Important distinction when considering tax rates is to distinguish between marginal rate and effective average rate.

Marginal tax rate Average rate

Percent levied on each additional peso of taxable income.

Marginal tax rate rises as income increases.

Rate a taxpayer would be taxed at, if taxing was done at a constant rate, instead of progressively.

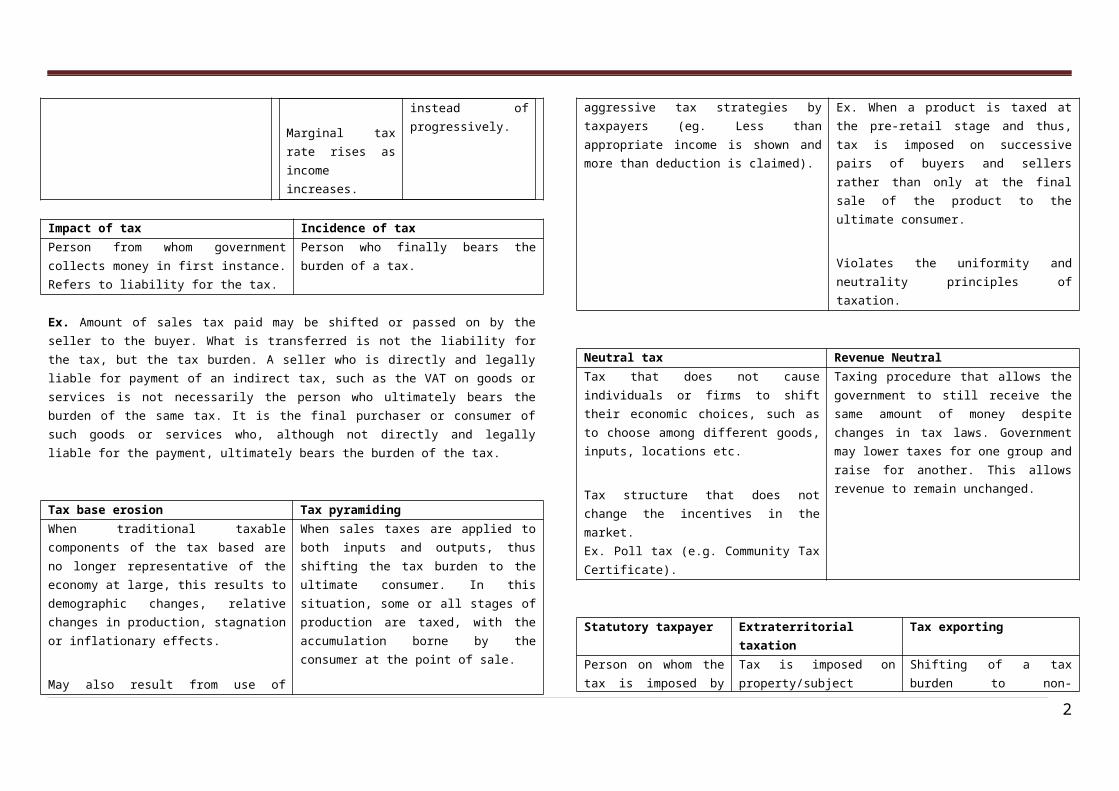

Impact of tax Incidence of tax

Person from whom government collects money in first instance. Refers to liability for the tax.

Person who finally bears the burden of a tax.

Ex. Amount of sales tax paid may be shifted or passed on by the seller to the buyer. What is transferred is not the liability for the tax, but the tax burden. A seller who is directly and legally liable for payment of an indirect tax, such as the VAT on goods or services is not necessarily the person who ultimately bears the burden of the same tax. It is the final purchaser or consumer of such goods or services who, although not directly and legally liable for the payment, ultimately bears the burden of the tax.

Tax base erosion Tax pyramiding

When traditional taxable components of the tax based are no longer representative of the economy at large, this results to demographic changes, relative changes in production, stagnation or inflationary effects.

When sales taxes are applied to both inputs and outputs, thus shifting the tax burden to the ultimate consumer. In this situation, some or all stages of production are taxed, with the accumulation borne by the consumer at the point of sale.

1

May also result from use of aggressive tax strategies by taxpayers (eg. Less than appropriate income is shown and more than deduction is claimed).

Ex. When a product is taxed at the pre-retail stage and thus, tax is imposed on successive pairs of buyers and sellers rather than only at the final sale of the product to the ultimate consumer.

Violates the uniformity and neutrality principles of taxation.

Neutral tax Revenue Neutral

Tax that does not cause individuals or firms to shift their economic choices, such as to choose among different goods, inputs, locations etc.

Tax structure that does not change the incentives in the market.Ex. Poll tax (e.g. Community Tax Certificate).

Taxing procedure that allows the government to still receive the same amount of money despite changes in tax laws. Government may lower taxes for one group and raise for another. This allows revenue to remain unchanged.

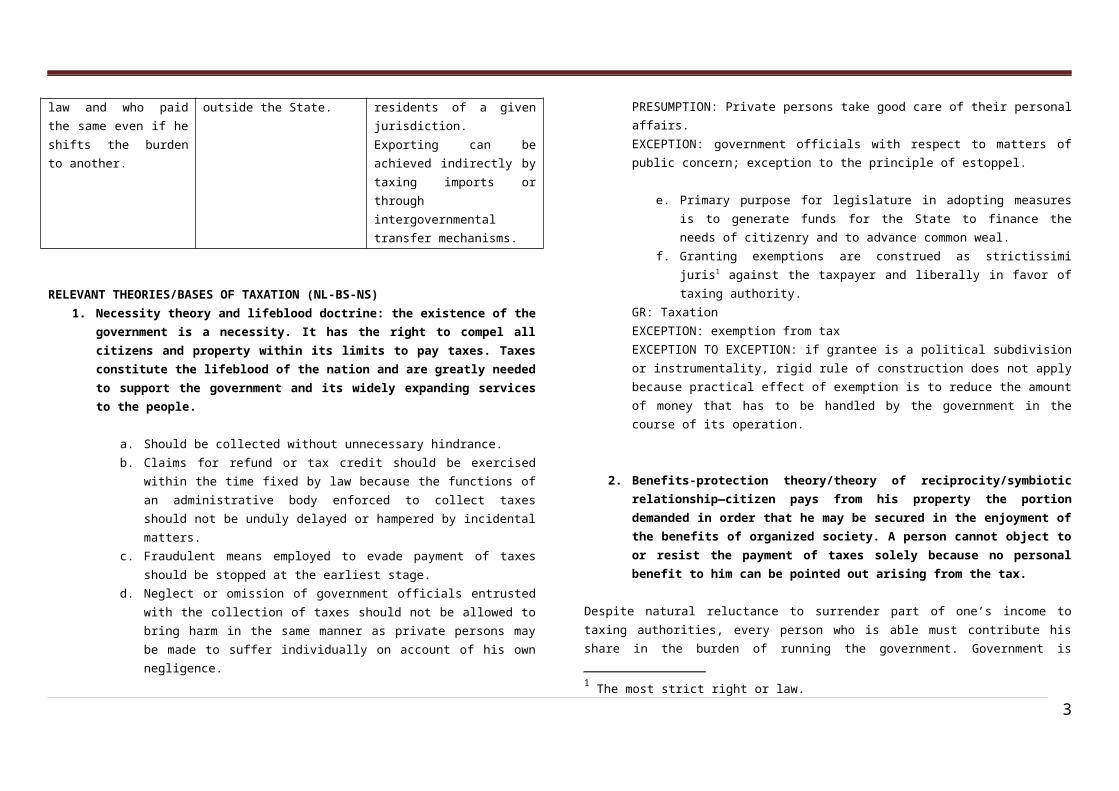

Statutory taxpayer Extraterritorial taxation Tax exporting

Person on whom the tax is imposed by law and who paid the same even if he shifts the burden to another.

Tax is imposed on property/subject outside the State.

Shifting of a tax burden to non-residents of a given jurisdiction. Exporting can be achieved indirectly by taxing imports or through intergovernmental transfer mechanisms.

RELEVANT THEORIES/BASES OF TAXATION (NL-BS-NS)1. Necessity theory and lifeblood doctrine: the existence of the government is a

necessity. It has the right to compel all citizens and property within its limits to pay taxes. Taxes constitute the lifeblood of the nation and are greatly

needed to support the government and its widely expanding services to the people.

a. Should be collected without unnecessary hindrance.b. Claims for refund or tax credit should be exercised within the time fixed by

law because the functions of an administrative body enforced to collect taxes should not be unduly delayed or hampered by incidental matters.

c. Fraudulent means employed to evade payment of taxes should be stopped at the earliest stage.

d. Neglect or omission of government officials entrusted with the collection of taxes should not be allowed to bring harm in the same manner as private persons may be made to suffer individually on account of his own negligence.

PRESUMPTION: Private persons take good care of their personal affairs.EXCEPTION: government officials with respect to matters of public concern; exception to the principle of estoppel.

e. Primary purpose for legislature in adopting measures is to generate funds for the State to finance the needs of citizenry and to advance common weal.

f. Granting exemptions are construed as strictissimi juris1 against the taxpayer and liberally in favor of taxing authority.

GR: TaxationEXCEPTION: exemption from taxEXCEPTION TO EXCEPTION: if grantee is a political subdivision or instrumentality, rigid rule of construction does not apply because practical effect of exemption is to reduce the amount of money that has to be handled by the government in the course of its operation.

2. Benefits-protection theory/theory of reciprocity/symbiotic relationship—citizen pays from his property the portion demanded in order that he may be secured in the enjoyment of the benefits of organized society. A person cannot object to or resist the payment of taxes solely because no personal benefit to him can be pointed out arising from the tax.

1 The most strict right or law.

2

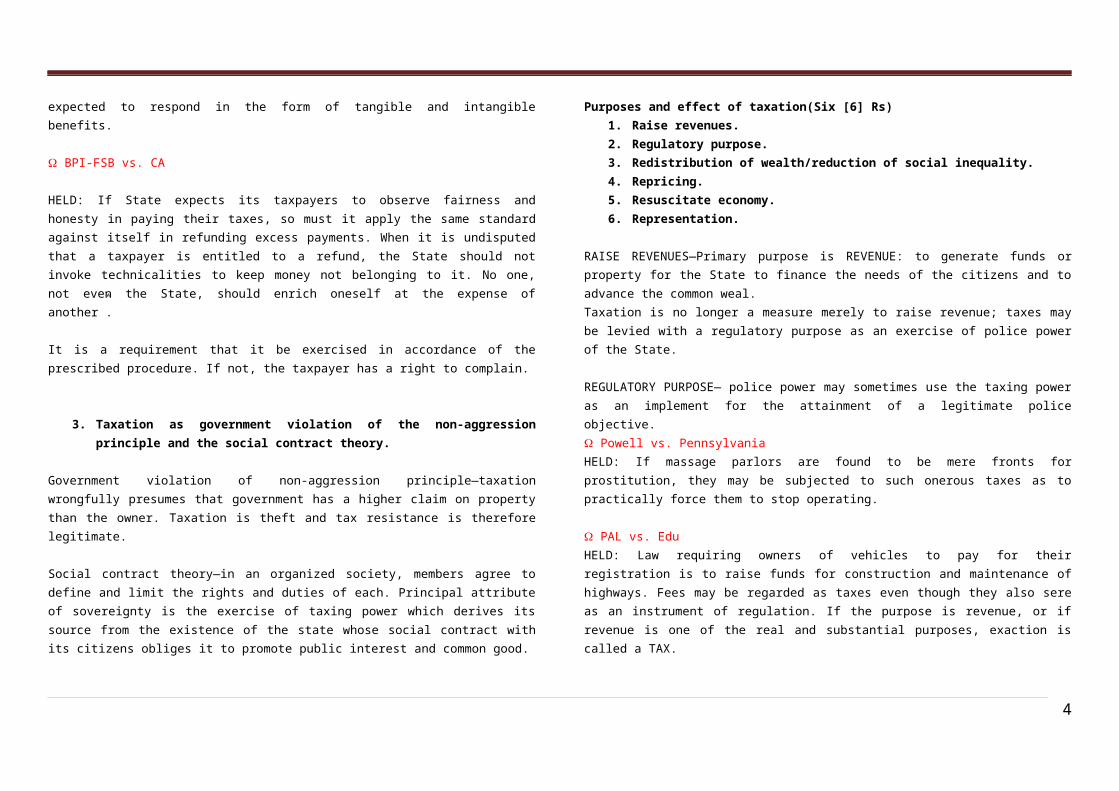

Despite natural reluctance to surrender part of one’s income to taxing authorities, every person who is able must contribute his share in the burden of running the government. Government is expected to respond in the form of tangible and intangible benefits.

BPI-FSB vs. CA

HELD: If State expects its taxpayers to observe fairness and honesty in paying their taxes, so must it apply the same standard against itself in refunding excess payments. When it is undisputed that a taxpayer is entitled to a refund, the State should not invoke technicalities to keep money not belonging to it. No one, not even the State, should enrich oneself at the expense of another”.

It is a requirement that it be exercised in accordance of the prescribed procedure. If not, the taxpayer has a right to complain.

3. Taxation as government violation of the non-aggression principle and the social contract theory.

Government violation of non-aggression principle—taxation wrongfully presumes that government has a higher claim on property than the owner. Taxation is theft and tax resistance is therefore legitimate.

Social contract theory—in an organized society, members agree to define and limit the rights and duties of each. Principal attribute of sovereignty is the exercise of taxing power which derives its source from the existence of the state whose social contract with its citizens obliges it to promote public interest and common good.

Purposes and effect of taxation(Six [6] Rs)1. Raise revenues.2. Regulatory purpose.3. Redistribution of wealth/reduction of social inequality.4. Repricing.5. Resuscitate economy.6. Representation.

RAISE REVENUES—Primary purpose is REVENUE: to generate funds or property for the State to finance the needs of the citizens and to advance the common weal. Taxation is no longer a measure merely to raise revenue; taxes may be levied with a regulatory purpose as an exercise of police power of the State.

REGULATORY PURPOSE— police power may sometimes use the taxing power as an implement for the attainment of a legitimate police objective. Powell vs. PennsylvaniaHELD: If massage parlors are found to be mere fronts for prostitution, they may be subjected to such onerous taxes as to practically force them to stop operating.

PAL vs. EduHELD: Law requiring owners of vehicles to pay for their registration is to raise funds for construction and maintenance of highways. Fees may be regarded as taxes even though they also sere as an instrument of regulation. If the purpose is revenue, or if revenue is one of the real and substantial purposes, exaction is called a TAX.

SUMPTUARY PURPOSE OF TAXATION: non-revenue or regulatory purpose of taxation.

REDISTRIBUTION OF WEALTH/REDUCITON OF SOCIAL INEQUALITY—there is an effort to apportion the costs of government among the people which in a way thwarts the undue concentration of wealth in the hands of a few individuals.

PROGESSIVITY: those who are able to pay more should shoulder the bigger portion of tax burden. Taxation is now being used as an implement for exercise of the power of eminent domain. Full reimbursement (peso for peso basis) is not necessary when the State uses taxation as an implement of eminent domain.Ex. Tax deduction does not offer full reimbursement of the senior citizen discount because it only shaves money off the taxable income resulting to a partial recovery unlike a tax credit which reduces the tax to be paid by the amount of discount. As such, it does not meet the definition of just compensation. However, amendment to the law granting senior citizen discount providing for tax deduction instead credit is not unconstitutional since the State can impose upon private establishments the burden of partly subsidizing a government program.

REPRICING— taxes may be levied to address externalities.

3

EXTERNALITIES: cost or benefit that is not transmitted through prices and is incurred by a party who was not involved as either a buyer or seller of the goods or services causing the cost or benefit.

External cost External benefit

Negative externality/cost of an externality Positive/benefit of an externality

Ex: Imposition of Pigovian Tax

PIGOVIAN TAX: tax levied on a market activity to correct the market outcome, if there are negative externalities associated with market activity. If there are negative externalities, social cost is not covered by the private cost of the activity which may lead to over-consumption of the product. To correct this, Pigouvian tax may be imposed (effective means to reduce incidence of bad behavior is to tax it).If there are positive externalities (public benefits from a market activity), those who receive the benefit do not pay for it and the market may under-supply the product. To correct this, Pigouvian subsidy may be given.

Illustration:A tax may be imposed on cigarettes—vs. negative externality of second-hand smoke.Pollution tax—factories emitting smoke.

Taxes may be used to modify consumption or employment by making some classes of transaction attractive or to protect local industries or consumers.

Ex: Levying of special duties on importation1. Dumping duty;2. Countervailing duty;3. Marking duty; and4. Discriminatory or retaliatory duty.

RESUSCITATE ECONOMY— tax may be imposed as a first aid measure to resuscitate an economy in distress.Ex: PD 1956: AD VALOREM TAX on manufactured oils and other fuel oils—for the purpose of minimizing frequent price changes by exchange rate adjustments and/or increase in world market prices of crude oil and imported petroleum products.

Tax exemptions may be granted to entice investments. Reduced tax collection redounds by enticing more business investments and employment opportunities.

FISCAL POLICY: taxes used to influence macroeconomic performance.

REPRESENTATION—“no taxation without representation”; no taxes should be imposed on the people but with their consent, personally or by representatives.

CONSTI: all bills for raising revenue shall originate in House of Representative on theory that they are more sensitive to local needs and problems.

Characteristics and requisites of taxesCharacteristics

1. An enforced contribution.2. Exacted pursuant to legislative authority.3. Contribution being in form of money.4. Imposed, levied and collected for the purpose of raising revenue.5. To be used for public or governmental purposes.6. Levied by authority which has jurisdiction over the person, property, transaction,

rights and privileges.

Requisites (JAPUN)1. Person or property taxed should be within jurisdiction of taxing authority.2. A ssessment and collection of certain kinds of taxes guarantee against injustice to

individuals, especially by providing notice and opportunity for hearing.3. For public purpose.4. Rule of taxation shall be uniform and equitable.5. Tax must not impinge on the inherent and constitutional limitation on power of

taxation.

An enforced contribution—does not depend on the will or acquiescence of the taxpayer.Exacted pursuant to legislative authority—GR: power is exercised only by the legislative department except in case of valid delegations of power or when there is constitutional grant.

Contribution in the form of money—there is no law prohibiting payment in some other form of property.

4

However, State could determine in what manner taxes should be discharged.1. Notes of legal tender do not apply to involuntary contributions exacted by a State

buy only to debts (obligations for payment of money founded on contracts, whether express or implied).

2. Statute requiring payment to be collected in gold and silver coins was sustained on 2 grounds:

a. Right of each state to collect its taxes in such material as it might deem expedient. Mode in which it should be exercised, were all equally within the discretion of its legislature, except as restrained by its own constitution; and

b. Legal tender act had no reference to taxes imposed by State authority, but only to debts arising out of simple contracts or contracts of specialty, which include judgments or recognizances.

Imposed, levied and collected for purpose of raising revenue—taxes may have regulatory or economic purpose other than to generate funds.

To be used for public or governmental purpose—it cannot be used for private purposes.

Levied by authority which has jurisdiction over the person, property, transaction, rights and privileges—jurisdictional limitation has 2 questions:

1. Is there a sufficient relationship between the State exercising tax power and the object of the exercise of that power?

2. Is the degree of contact sufficient to justify the state’s imposition of a particular obligation?

Nature of taxing power1. It is inherent and legislative.

Inherent Legislative

GR: power to tax is an incident of sovereignty and is unlimited in its range, acknowledging in its very nature no limits, so that security against its abuse is to be found only in the responsibility of this legislature which imposes the tax on the constituency who are to pay it.

Legislature lies the discretion to determine the nature, object, extent, coverage and situs of taxation. It has the authority to prescribe a certain tax at a specific rate for a particular public purpose.

Scopes of legislative power:1. Purposes provided they are lawful

Rule of taxation shall be uniform and equitable and Congress shall evolve a progressive system of taxation.

The following are manifestation of this inherent nature

1. It can be imposed even in the absence of a constitutional grant

2. Injunction is not generally available to enjoin collection of taxes

3. Taxes cannot be set-off or compensated

4. It is an unlimited or plenary power5. It is inherent in the power to tax

that State be free to select the subjects of taxation

Taxing power of LGUs is not inherent because they are not sovereign units. LGU is merely an agency of the State for carrying out the objects of the government. Thus, constitutional or legislative grant is necessary before it can exercise taxing power.

and public2. Person, property, privileges or

occupation to be taxed3. Amount or rate4. Kind of tax5. Apportionment of tax (whether tax

shall be of general application or limited to a particular locality, partly general and partly local)

6. Situs7. Mode or method of collection

Power to tax is primarily vested in Congress; however it may be exercised by local legislative bodies pursuant to direct authority conferred by SEC 5, ART 10 CONSTI.

TAX FARMING: principle of assigning the responsibility for tax revenue collecting to private citizens or grounds was once used by other countries.

2. Power is not granted in the Constitution.3. It is not a contract between the State and its citizens.4. It is not political in nature.5. Taxes are personal.6. It is unlimited in range.7. It is imprescriptible.

Power is not granted in the Constitution—it merely constitutes limitations upon a power which would be impractical without itSEC 28(3), ART 6 CONSTI. Charitable institutions, churches and parsonages or convents appurtenant thereto, mosques, nonprofit cemeteries and all lands, buildings and

5

improvements, actually, directly and exclusively used for religion, charitable or educational purposes shall be exempt from taxation.

It is not a contract between the State and its citizens—it operates in invitum, which means that it is in no way depend on the will or contractual assent, expressed or implied, of the person taxed.Taxes are obligations arising from law and not from contracts because of lack of consent or choice.

It is not political in nature—Co Kim Chan vs. Valdes Tan KehHELD: Internal revenue laws were continued in force during the period of enemy occupation and in effect were enforced by the occupation government. As a matter of fact, income tax returns were filed during that period and income tax payment were effected and considered valid and legal. Such tax laws are deemed to be the laws of occupied territory and not of the occupying enemy.

Tax are personal—liability cannot be shifted. Rights are transmissible but obligations are not. Thus, heirs cannot be held liable beyond what they inherited for delinquent taxes of a decedent. Corporation’s tax delinquency cannot be enforced against its stockholders or related entities. A corporation is vested by law with a separate and distinct personality. However, stockholders may be held liable for the unpaid taxes of a dissolved corporation if it appears that corporate assets have been passed into their hands. Same is true if stockholders have unpaid subscriptions pursuant of the trust fund doctrine.

In case of indirect taxes, shifting of the burden to tax from the seller to the buyer is not incompatible with the principle that taxes are personal liabilities. When seller passes on the tax to his buyer, he is only shifting the tax burden, but not the liability, to the buyer as part of the cost of the goods sold or services rendered.

It is unlimited in range—it is not subject to any restrictions except in the discretion of the authority which exercises it. Security against its abuse is to be founded only in the responsibility of the legislature which imposes the tax on the constituency who pay it.

McCulloch vs. MarylandHELD: Power to tax involves the power to destroy.

Panhandle vs. MississippiHELD: Debunked the ruling in McCullock vs. Maryland where it is held that "power to tax is not the power to destroy while this court sits”. The power to tax may include the power to destroy if it is used as an implement of the police power in discouraging and in effect ultimately prohibiting certain things or enterprises inimical to public welfare. But where the power to tax is used solely for the purpose of raising revenues, modern view is that it cannot be allowed to confiscate or destroy.

It is imprescriptible—without exception, taxes being the lifeblood of the government. However, statutes may provide for prescriptive periods for the collection of particular kinds of taxes when government has not by express statutory provision, provided a limitation upon its right to assess unpaid taxes, such right is imprescriptible.

HELD: The government is not bound by any statute of limitations, unless Congress has clearly manifested its intention that it should be so bound.

Aspects of taxation1. Aspects (LAP)

a. Levy2

b. Assessment and Collection3

c. Payment and/or exercise of remedies4

2. Grant of exemption is an exercise of power of taxation—power to tax includes power to exempt

Sound Tax System (ECCEPSD)1. Canons of taxation.

a. Equity.b. Certainty.c. Convenience.

2 Determination of persons, property or exercises to be taxed, amount to be raised, rate to be imposed and the manner of implementation; this is exercised by the Legislature.3 Manner of enforcing the obligation of taxes already levied upon the taxpayer; act of administration and implementation by Executive Department.4 Compliance and/or resistance by the taxpayer; through Executive or Legislature (through suffrage or initiative/referendum) and ultimately through Judiciary.

6

d. Economy.e. Productivity.f. Elasticity.g. Simplicity.h. Diversity.

Equity—every person should pay to the government depending upon his ability to pay.Certainty—must not be arbitrary; taxpayer should know in advance how much tax he has to pay, at what time and in what form.Convenience—mode and timing must be convenient to tax payers.Economy—cost of tax collection should be lower than amount of tax collected.

Productivity—tax when levied should produce sufficient revenue to the government.Elasticity—tax system should be fairly elastic so that if at any time the government is in need of more funds, it should increase its financial resources without incurring any additional cost of collection.Simplicity—tax system should be fairly simple, plain, and intelligible to the taxpayer.Diversity—system should include a large number of taxes which are economical; government should collect revenue by levying direct and indirect taxes.

2. Basic principles of Sound Tax System(FAT).a. Fiscal adequacy.b. Administrative feasibility.c. Theoretical justice.

Fiscal adequacy—sources of revenues must be adequate to meet government expenditures and their variations; violation of this principle will make the law unsound but still valid and not unconstitutional.

Administrative feasibility--- taxes should be capable of being effectively enforced; tax policy that costs government and taxpayers more to collect that taxes generated is inherently flawed. Violation of this principle will make the law unsound but still valid and not unconstitutional.

Theoretical justice—taxed must be based on the taxpayer’s ability to pay and proportional to the relative value of the property; it must be uniform and equitable and that State must evolve a progressive system of taxation. It is progressive when its rate goes up depending

on the resources of peron affected. Violation of this principle will make the law unsound, invalid and unconstitutional.

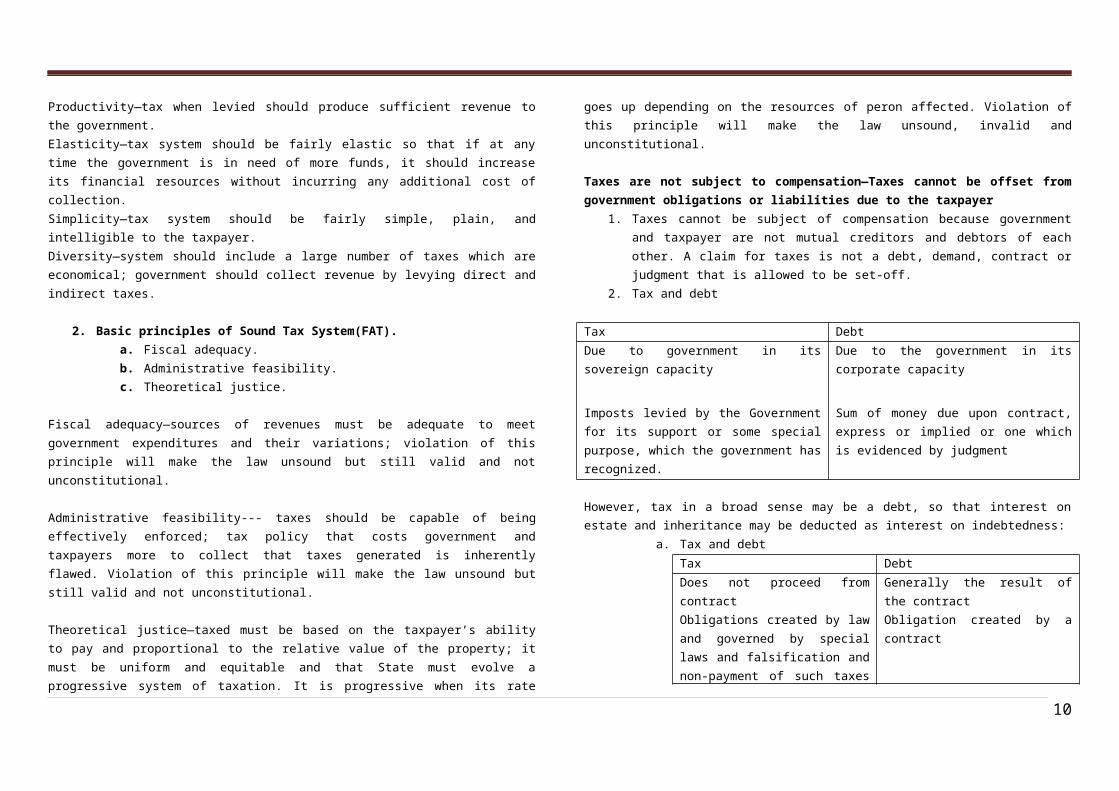

Taxes are not subject to compensation—Taxes cannot be offset from government obligations or liabilities due to the taxpayer

1. Taxes cannot be subject of compensation because government and taxpayer are not mutual creditors and debtors of each other. A claim for taxes is not a debt, demand, contract or judgment that is allowed to be set-off.

2. Tax and debt

Tax Debt

Due to government in its sovereign capacity

Imposts levied by the Government for its support or some special purpose, which the government has recognized.

Due to the government in its corporate capacity

Sum of money due upon contract, express or implied or one which is evidenced by judgment

However, tax in a broad sense may be a debt, so that interest on estate and inheritance may be deducted as interest on indebtedness:

a. Tax and debtTax Debt

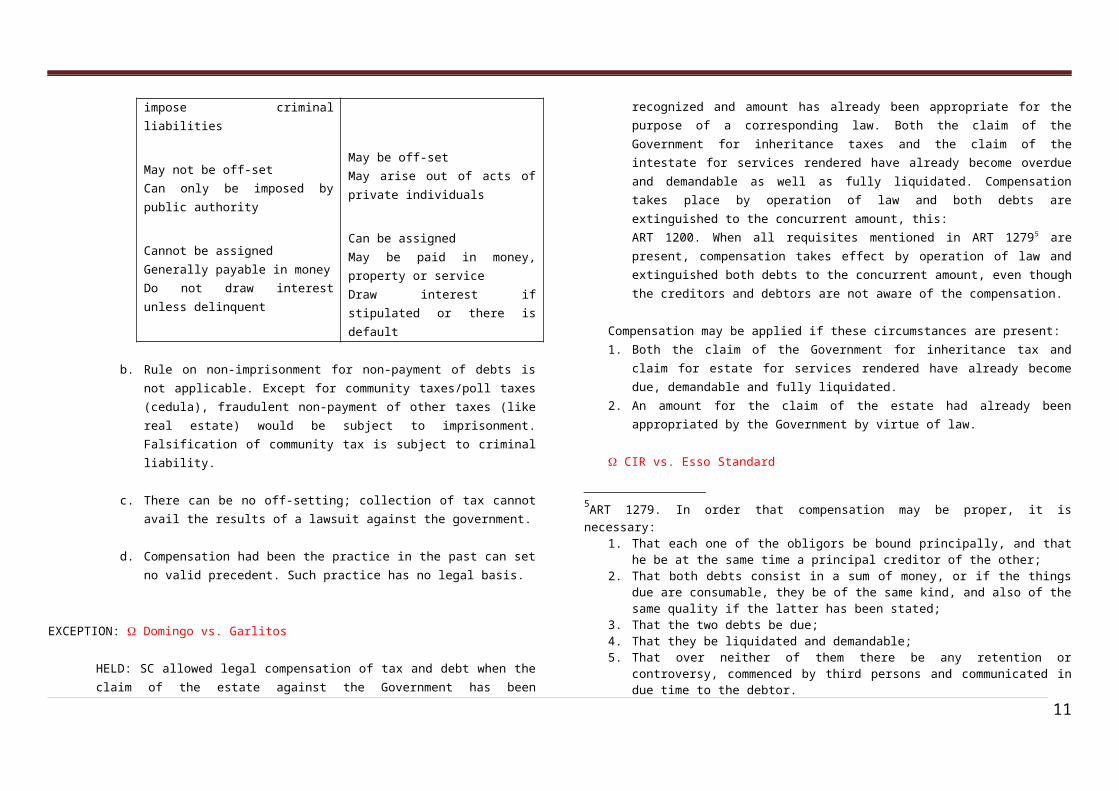

Does not proceed from contractObligations created by law and governed by special laws and falsification and non-payment of such taxes impose criminal liabilities

May not be off-setCan only be imposed by public authority

Cannot be assignedGenerally payable in moneyDo not draw interest unless delinquent

Generally the result of the contractObligation created by a contract

May be off-setMay arise out of acts of private individuals

Can be assignedMay be paid in money, property or serviceDraw interest if stipulated or there is default

7

b. Rule on non-imprisonment for non-payment of debts is not applicable. Except for community taxes/poll taxes (cedula), fraudulent non-payment of other taxes (like real estate) would be subject to imprisonment. Falsification of community tax is subject to criminal liability.

c. There can be no off-setting; collection of tax cannot avail the results of a lawsuit against the government.

d. Compensation had been the practice in the past can set no valid precedent. Such practice has no legal basis.

EXCEPTION: Domingo vs. Garlitos

HELD: SC allowed legal compensation of tax and debt when the claim of the estate against the Government has been recognized and amount has already been appropriate for the purpose of a corresponding law. Both the claim of the Government for inheritance taxes and the claim of the intestate for services rendered have already become overdue and demandable as well as fully liquidated. Compensation takes place by operation of law and both debts are extinguished to the concurrent amount, this:ART 1200. When all requisites mentioned in ART 12795 are present, compensation takes effect by operation of law and extinguished both debts to the concurrent amount, even though the creditors and debtors are not aware of the compensation.

Compensation may be applied if these circumstances are present:1. Both the claim of the Government for inheritance tax and claim for estate for

services rendered have already become due, demandable and fully liquidated.

5ART 1279. In order that compensation may be proper, it is necessary:1. That each one of the obligors be bound principally, and that he be at the same time a

principal creditor of the other;2. That both debts consist in a sum of money, or if the things due are consumable, they be of

the same kind, and also of the same quality if the latter has been stated;3. That the two debts be due;4. That they be liquidated and demandable;5. That over neither of them there be any retention or controversy, commenced by third

persons and communicated in due time to the debtor.

2. An amount for the claim of the estate had already been appropriated by the Government by virtue of law.

CIR vs. Esso Standard

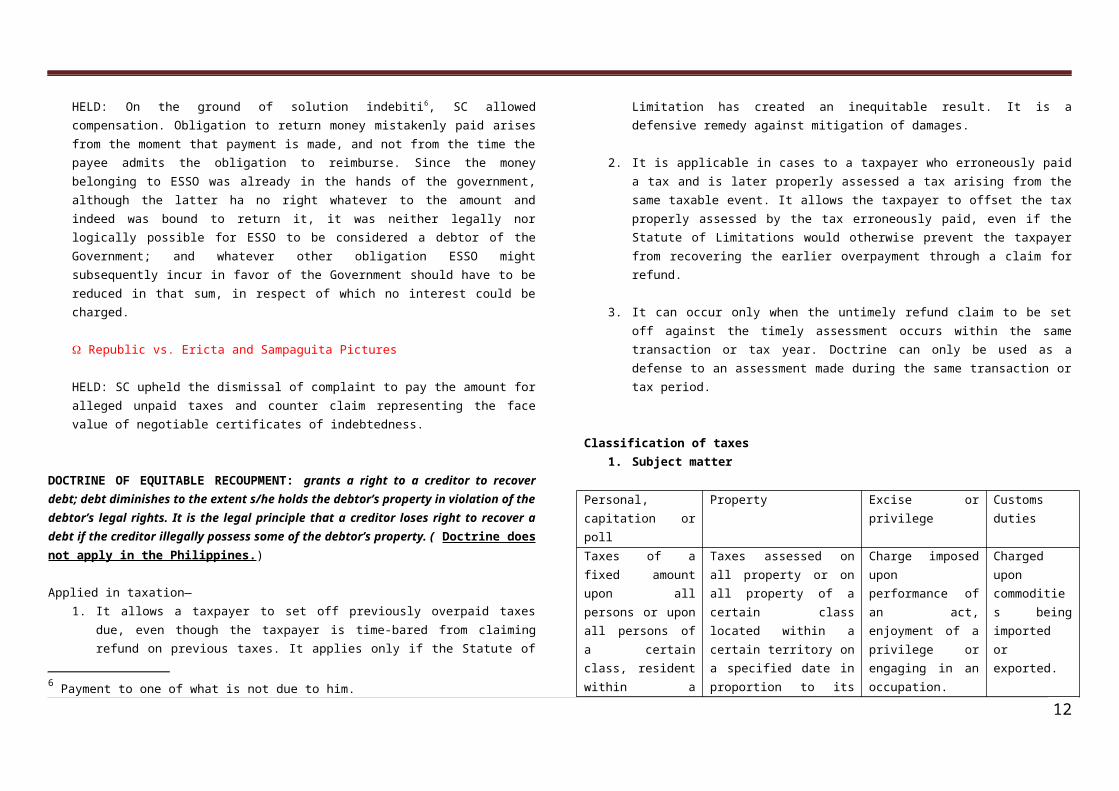

HELD: On the ground of solution indebiti6, SC allowed compensation. Obligation to return money mistakenly paid arises from the moment that payment is made, and not from the time the payee admits the obligation to reimburse. Since the money belonging to ESSO was already in the hands of the government, although the latter ha no right whatever to the amount and indeed was bound to return it, it was neither legally nor logically possible for ESSO to be considered a debtor of the Government; and whatever other obligation ESSO might subsequently incur in favor of the Government should have to be reduced in that sum, in respect of which no interest could be charged.

Republic vs. Ericta and Sampaguita Pictures

HELD: SC upheld the dismissal of complaint to pay the amount for alleged unpaid taxes and counter claim representing the face value of negotiable certificates of indebtedness.

DOCTRINE OF EQUITABLE RECOUPMENT: grants a right to a creditor to recover debt; debt diminishes to the extent s/he holds the debtor’s property in violation of the debtor’s legal rights. It is the legal principle that a creditor loses right to recover a debt if the creditor illegally possess some of the debtor’s property. ( Doctrine does not apply in the Philippines.)

Applied in taxation—1. It allows a taxpayer to set off previously overpaid taxes due, even though the

taxpayer is time-bared from claiming refund on previous taxes. It applies only if the Statute of Limitation has created an inequitable result. It is a defensive remedy against mitigation of damages.

2. It is applicable in cases to a taxpayer who erroneously paid a tax and is later properly assessed a tax arising from the same taxable event. It allows the taxpayer to offset the tax properly assessed by the tax erroneously paid, even if the Statute

6 Payment to one of what is not due to him.

8

of Limitations would otherwise prevent the taxpayer from recovering the earlier overpayment through a claim for refund.

3. It can occur only when the untimely refund claim to be set off against the timely assessment occurs within the same transaction or tax year. Doctrine can only be used as a defense to an assessment made during the same transaction or tax period.

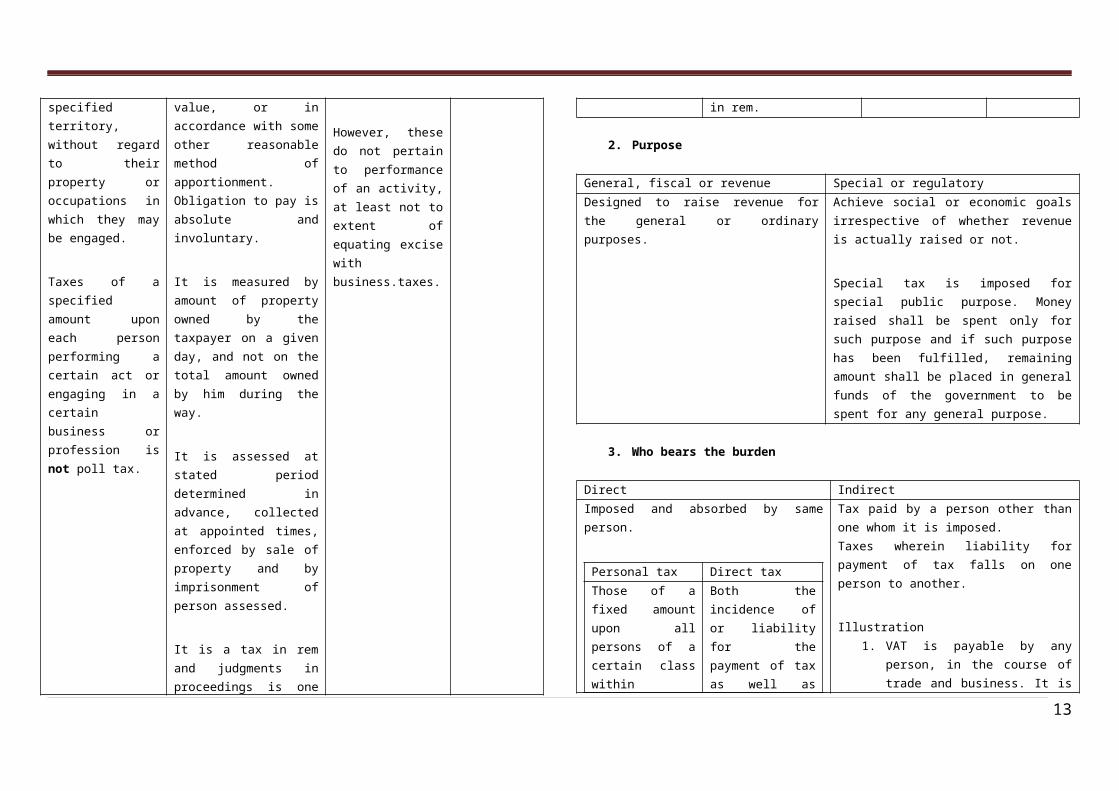

Classification of taxes1. Subject matter

Personal, capitation or poll

Property Excise or privilege Customs duties

Taxes of a fixed amount upon all persons or upon all persons of a certain class, resident within a specified territory, without regard to their property or occupations in which they may be engaged.

Taxes of a specified amount upon each person performing a certain act or engaging in a certain business or profession is not poll tax.

Taxes assessed on all property or on all property of a certain class located within a certain territory on a specified date in proportion to its value, or in accordance with some other reasonable method of apportionment. Obligation to pay is absolute and involuntary.

It is measured by amount of property owned by the taxpayer on a given day, and not on the total amount owned by him during the way.

It is assessed at stated period determined in advance, collected at appointed times, enforced by sale of property and by

Charge imposed upon performance of an act, enjoyment of a privilege or engaging in an occupation.

However, these do not pertain to performance of an activity, at least not to extent of equating excise with business.taxes.

Charged upon commodities being imported or exported.

imprisonment of person assessed.

It is a tax in rem and judgments in proceedings is one in rem.

2. Purpose

General, fiscal or revenue Special or regulatory

Designed to raise revenue for the general or ordinary purposes.

Achieve social or economic goals irrespective of whether revenue is actually raised or not.

Special tax is imposed for special public purpose. Money raised shall be spent only for such purpose and if such purpose has been fulfilled, remaining amount shall be placed in general funds of the government to be spent for any general purpose.

3. Who bears the burden

Direct Indirect

Imposed and absorbed by same person.

Personal tax Direct tax

Those of a fixed amount upon all persons of a certain class within jurisdiction of the taxing power without regard to the amount of their property.

Both the incidence of or liability for the payment of tax as well as impact or burden of tax falls on same person and cannot be shifted.

Ex. Franchise tax: a

Tax paid by a person other than one whom it is imposed.Taxes wherein liability for payment of tax falls on one person to another.

Illustration1. VAT is payable by any person, in

the course of trade and business. It is applied to each stage of production. Burden of paying the amount may be shifted on to the buyer, transferee or lessee of goods, properties or services.

2. Contractor’s tax—payable by

9

percentage tax imposed on franchise holders is a direct liability of the franchise grantee.

Those that are exacted from the very person ho, it is intended or desired, should pay them; they are impositions for which a taxpayer is directly liable on the transaction or business he is engaged in.

Ex. Income tax—taxes an individual’s ability to pay based on his income or net wealth.

contractor but it is the owner of the building that shoulders the burden.

3. Excise tax—liability for payment may fall from a person other than the one who actually bears the burden.

Those that are demanded, from or are paid by, one person in the expectation and intention that he can shift the burden to someone else.

Ex. VAT—substantial portion of consumer expenditures.

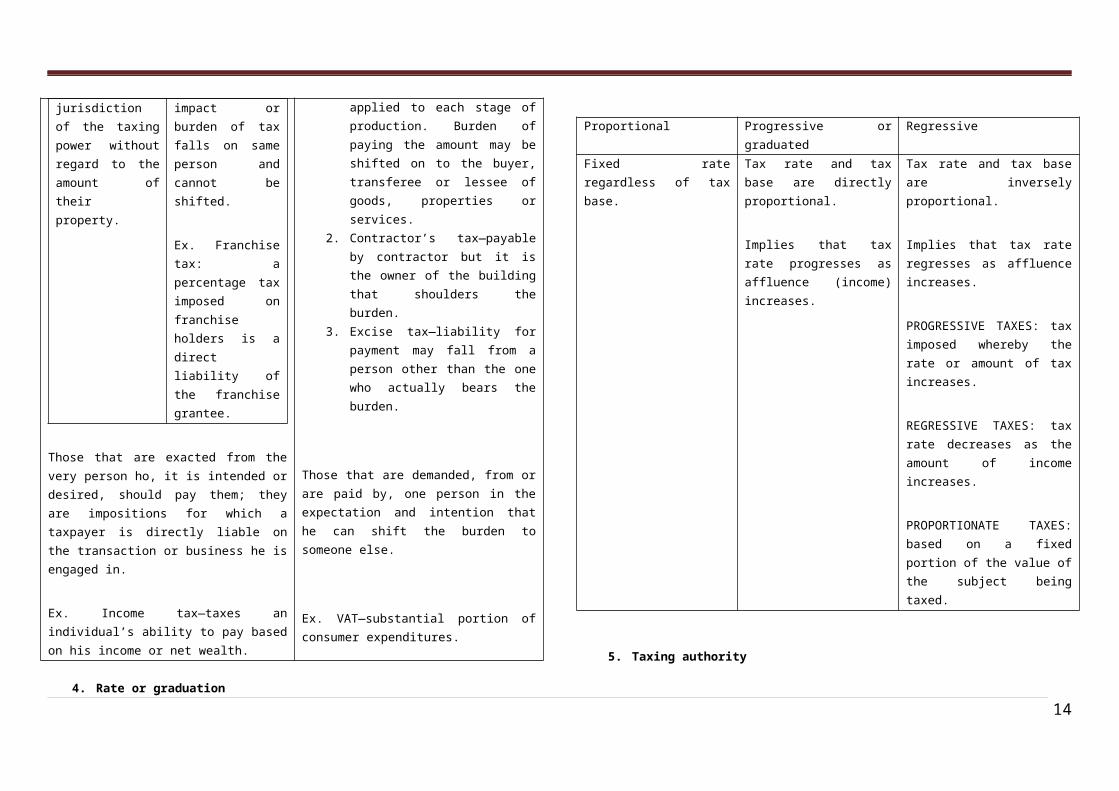

4. Rate or graduation

Proportional Progressive or graduated Regressive

Fixed rate regardless of tax base.

Tax rate and tax base are directly proportional.

Implies that tax rate progresses as affluence (income) increases.

Tax rate and tax base are inversely proportional.

Implies that tax rate regresses as affluence increases.

PROGRESSIVE TAXES: tax imposed whereby the rate or amount of tax increases.

REGRESSIVE TAXES: tax rate decreases as the amount of income increases.

PROPORTIONATE TAXES: based on a fixed portion of the value of the subject being taxed.

5. Taxing authority

National Local/municipal

Imposed by Congress imposed by local legislative bodies

6. Scope

General Specific

Imposed throughout the state or civil division for raising revenue for general purposes on the ground of general public interests.

Levied for a special purpose for the benefit of a part of a body politic resting upon the supposition that a portion of the public is specially benefited in the increase of the value of property.

7. Basis of amount

Specific Ad valorem (value)

Fixed amount by head or number or by some standard of weight or measurement.

Specific Excise

Imposes a specific sum by the head or number or by some standard of weight or measurement and which requires no assessment beyond a listing and classification of the subject to be taxed.

Privilege tax laid upon the manufacture, sale or consumption of commodities within the country .

Fixed proportion of value of property with respect to which taxes are assessed and require the intervention of assessors or appraisers to estimate the value of such property.

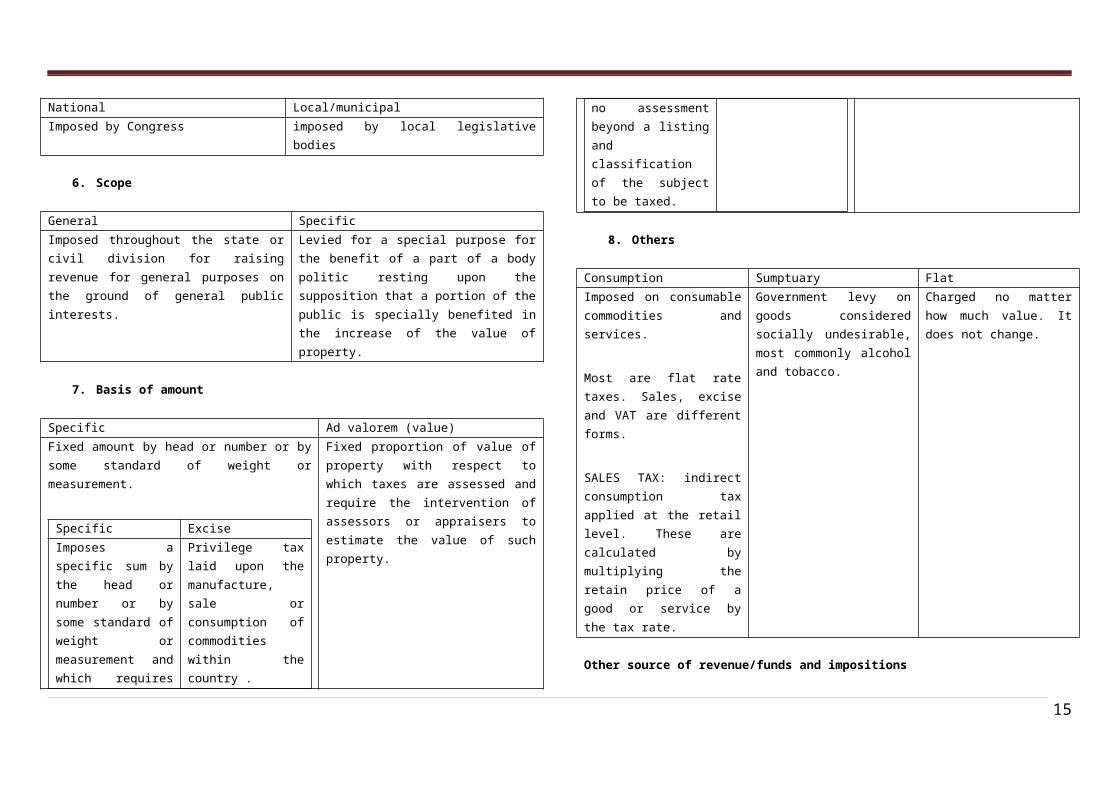

8. Others

Consumption Sumptuary Flat

10

Imposed on consumable commodities and services.

Most are flat rate taxes. Sales, excise and VAT are different forms.

SALES TAX: indirect consumption tax applied at the retail level. These are calculated by multiplying the retain price of a good or service by the tax rate.

Government levy on goods considered socially undesirable, most commonly alcohol and tobacco.

Charged no matter how much value. It does not change.

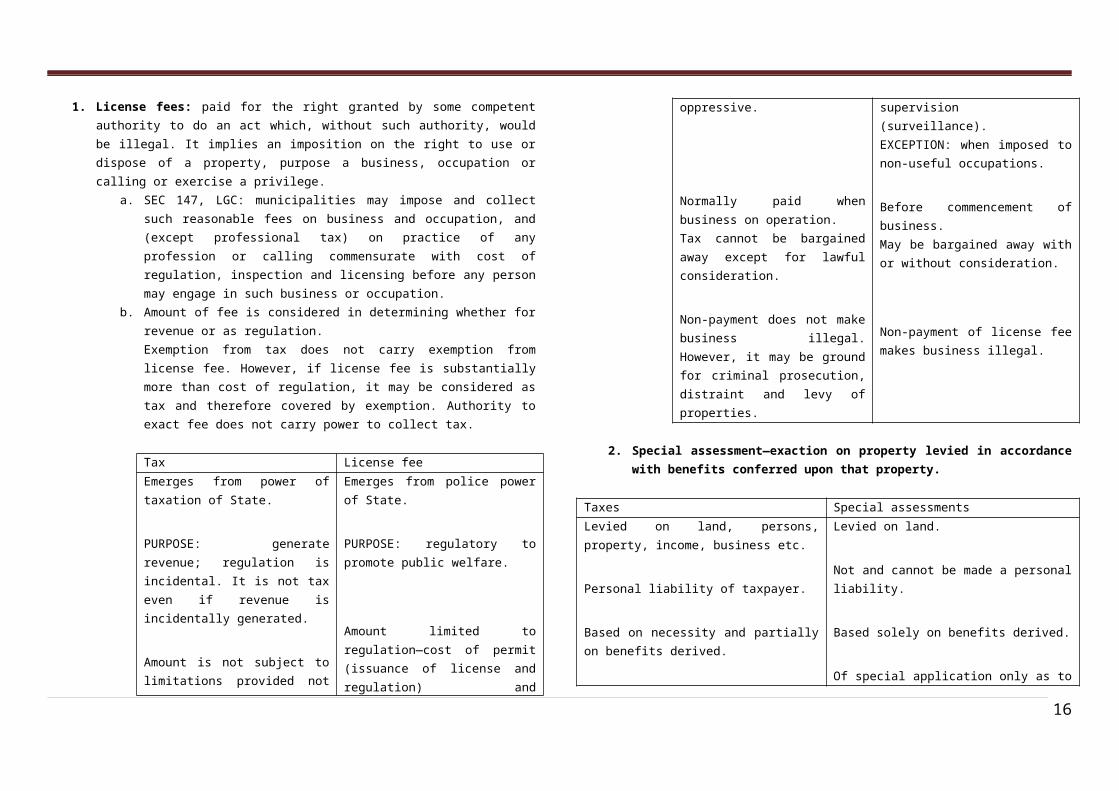

Other source of revenue/funds and impositions1. License fees: paid for the right granted by some competent authority to do an act

which, without such authority, would be illegal. It implies an imposition on the right to use or dispose of a property, purpose a business, occupation or calling or exercise a privilege.

a. SEC 147, LGC: municipalities may impose and collect such reasonable fees on business and occupation, and (except professional tax) on practice of any profession or calling commensurate with cost of regulation, inspection and licensing before any person may engage in such business or occupation.

b. Amount of fee is considered in determining whether for revenue or as regulation.Exemption from tax does not carry exemption from license fee. However, if license fee is substantially more than cost of regulation, it may be considered as tax and therefore covered by exemption. Authority to exact fee does not carry power to collect tax.

Tax License fee

Emerges from power of taxation of State.

PURPOSE: generate revenue; regulation is incidental. It is not tax even if revenue is incidentally

Emerges from police power of State.

PURPOSE: regulatory to promote public welfare.

generated.

Amount is not subject to limitations provided not oppressive.

Normally paid when business on operation.Tax cannot be bargained away except for lawful consideration.

Non-payment does not make business illegal. However, it may be ground for criminal prosecution, distraint and levy of properties.

Amount limited to regulation—cost of permit (issuance of license and regulation) and supervision (surveillance).EXCEPTION: when imposed to non-useful occupations.

Before commencement of business.May be bargained away with or without consideration.

Non-payment of license fee makes business illegal.

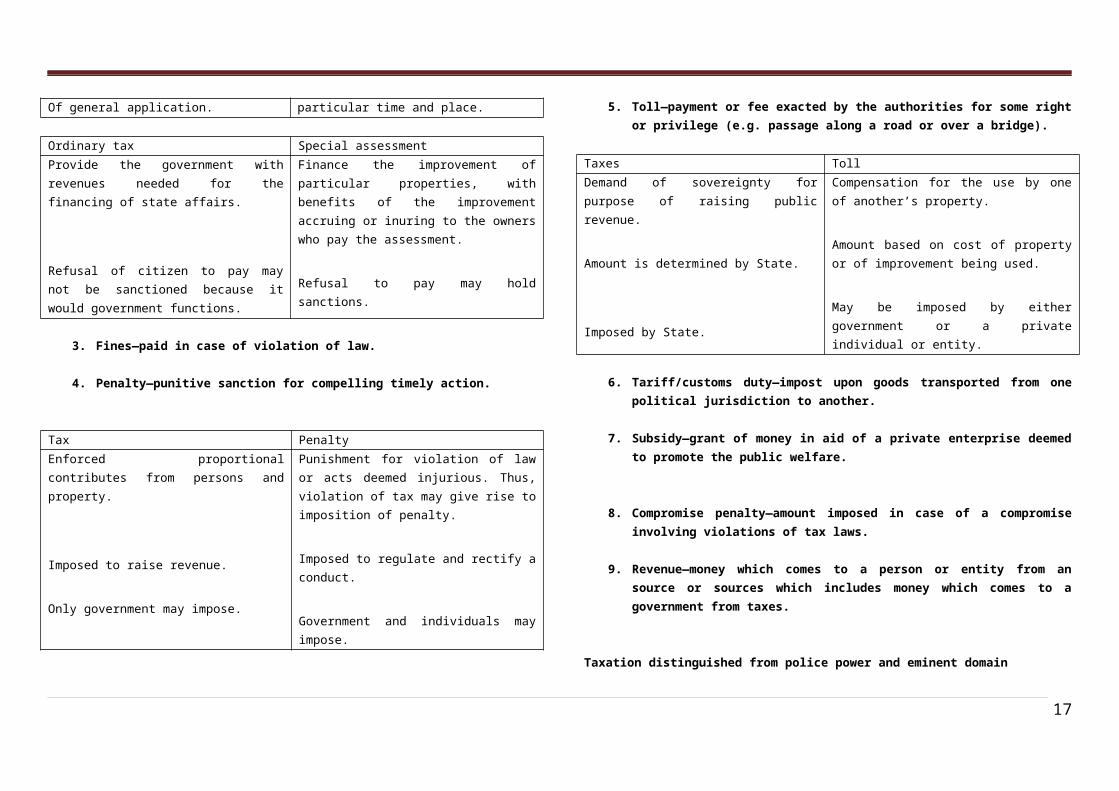

2. Special assessment—exaction on property levied in accordance with benefits conferred upon that property.

Taxes Special assessments

Levied on land, persons, property, income, business etc.

Personal liability of taxpayer.

Based on necessity and partially on benefits derived.

Of general application.

Levied on land.

Not and cannot be made a personal liability.

Based solely on benefits derived.

Of special application only as to particular time and place.

Ordinary tax Special assessment

Provide the government with revenues needed for the financing of state affairs.

Refusal of citizen to pay may not be sanctioned because it would government

Finance the improvement of particular properties, with benefits of the improvement accruing or inuring to the owners who pay the assessment.

11

functions. Refusal to pay may hold sanctions.

3. Fines—paid in case of violation of law.

4. Penalty—punitive sanction for compelling timely action.

Tax Penalty

Enforced proportional contributes from persons and property.

Imposed to raise revenue.

Only government may impose.

Punishment for violation of law or acts deemed injurious. Thus, violation of tax may give rise to imposition of penalty.

Imposed to regulate and rectify a conduct.

Government and individuals may impose.

5. Toll—payment or fee exacted by the authorities for some right or privilege (e.g. passage along a road or over a bridge).

Taxes Toll

Demand of sovereignty for purpose of raising public revenue.

Amount is determined by State.

Imposed by State.

Compensation for the use by one of another’s property.

Amount based on cost of property or of improvement being used.

May be imposed by either government or a private individual or entity.

6. Tariff/customs duty—impost upon goods transported from one political jurisdiction to another.

7. Subsidy—grant of money in aid of a private enterprise deemed to promote the public welfare.

8. Compromise penalty—amount imposed in case of a compromise involving violations of tax laws.

9. Revenue—money which comes to a person or entity from an source or sources which includes money which comes to a government from taxes.

Taxation distinguished from police power and eminent domain

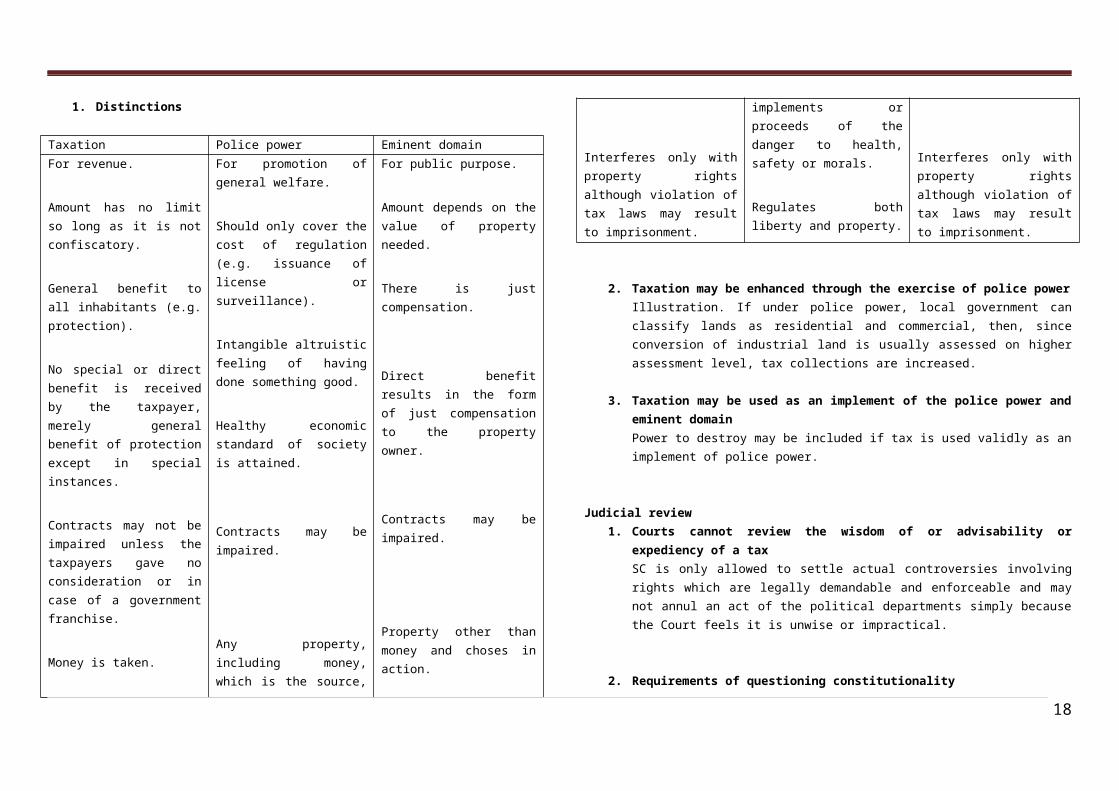

1. Distinctions

Taxation Police power Eminent domain

For revenue.

Amount has no limit so long as it is not confiscatory.

General benefit to all inhabitants (e.g. protection).

No special or direct benefit is received by the taxpayer, merely general benefit of protection except in special instances.

Contracts may not be impaired unless the taxpayers gave no consideration or in case of a government franchise.

Money is taken.

Interferes only with property rights although violation of

For promotion of general welfare.

Should only cover the cost of regulation (e.g. issuance of license or surveillance).

Intangible altruistic feeling of having done something good.

Healthy economic standard of society is attained.

Contracts may be impaired.

Any property, including money, which is the source, implements or proceeds of the danger to health, safety or morals.

Regulates both liberty and

For public purpose.

Amount depends on the value of property needed.

There is just compensation.

Direct benefit results in the form of just compensation to the property owner.

Contracts may be impaired.

Property other than money and choses in action.

Interferes only with property rights although violation of tax laws may result to imprisonment.

12

tax laws may result to imprisonment.

property.

2. Taxation may be enhanced through the exercise of police powerIllustration. If under police power, local government can classify lands as residential and commercial, then, since conversion of industrial land is usually assessed on higher assessment level, tax collections are increased.

3. Taxation may be used as an implement of the police power and eminent domainPower to destroy may be included if tax is used validly as an implement of police power.

Judicial review1. Courts cannot review the wisdom of or advisability or expediency of a tax

SC is only allowed to settle actual controversies involving rights which are legally demandable and enforceable and may not annul an act of the political departments simply because the Court feels it is unwise or impractical.

2. Requirements of questioning constitutionalitya. There must be actual controversy falling for exercise of judicial review;b. Question before Court must be ripe for adjudication;c. Locus standi7of a private citizen questioning the act;d. Question of constitutionality must be raised at the earlier opportunity; ande. Issue of constitutionality must be the lis mota of the case.

7 Party’s personal and substantial interest in a case such that he has sustained or will sustain direct injury as a result of the governmental act being challenged; Right of appearance in a court of justice on a given question; in private suits, standing is governed by real parties in interest (SEC 2, RULE 3);

REAL PARTY: party who stands to be benefited or injured by the judgment in the suit or the party entitled to the avails of the suit. INTEREST: material interest in an issue affected by the decree.MERE INTEREST: mere interest in the question involved or mere incidental interest.

A private person is allowed to raise constitutional questions only if he can show that he has personally suffered some actual or threatened injury as a result of the allegedly illegal conduct of the government, injury is fairly traceable to the challenged action and injury is likely to be redressed by a favorable action.

Party must show not only that law or act is invalid butalso that he has imminent danger of sustaining some direct injury as a result of its enforcement and not merely that he suffers in some indefinite way.

3. Moot and academic caseGR: Courts decline jurisdiction on the ground of mootnessEXCEPTION: Not moot and academic if:

a. There is a grave violation of the Constitution;b. Exceptional character of the situation and the paramount public interest is

involved;c. When constitutional issue raised requires formulation of controlling

principles to guide the bench, the bar and the public; andd. Case is capable of repetition yet evading review.

4. Judicial proceedings not requiredCollection of taxes levied should be summary and interfered with as little as possible. However, taxpayers and State are not prohibited from seeking remedies from courts.

5. Quantum of evidence: preponderance of evidencePREPONDERANCE OF EVIDENCE: weight, credit and value of the aggregate on either side; testimony adduced by one side is more credible and conclusive than that of the other.

6. No estoppel against the governmentGovernment is not estopped by mistakes or errors of its agents.Erroneous application of the law by public officers do not bar the subsequent correct application of statutes. Principle of Estoppel does not apply when State acts to rectify mistakes, errors, irregularities or illegal acts of its officials and agents. Rule holds true even if rectification prejudices parties who had meanwhile received benefits. This is particularly true in collection of legitimate taxes due where collection has to be made whether or not there is error, complicity or plain neglect on part of collecting agents.

13

However, this rule may be relaxed in the interest of justice and fair play, as where injustice will result to the taxpayer.

Taxpayer’s suit

Citizen and taxpayer suitsPlaintiff in a taxpayer’s suit Plaintiff in citizen’s suit

Plaintiff is affected by the expenditure of public funds.

Right a citizen and a taxpayer to maintain an action in courts to restrain the unlawful use of public funds to his injury cannot be denied

He is but the mere instrument of public concern.

In a matter of mere public right, people are real parties. It is the right, if not the duty, of every citizen to interfere and see that public offense be properly pursued and punished and that public grievance be remedied

DIRECT INJURY TEST: for a private individual to invoke judicial power in determining the validity of an executive or legislative action, he must have sustained direct injury and it is not sufficient that he has general interest common to all members in public.

Brushing aside technicalitiesRequirement of locus standi may be waived in the exercise of court discretion, where transcendental importance prompted the Court to act liberally.

Requirements1. Cases involve constitutional issues;2. For taxpayers, there must be a claim of illegal disbursement of public funds or that

tax measure is unconstitutional;3. For voters, there must be a showing of obvious interest in the validity of election

law in question;4. For concerned citizens, there must be a showing that issues raised are for

transcendental importance which must be settled early; and5. For legislators, there must be a claim that official action complained of infringes

upon their prerogatives as legislators.

Decision to entertain a taxpayer’s suit is discretionary upon court.

Questioning the validity and constitutionality of statutes by a taxpayerGR: Locus standi must be presentEXCEPTION: Misapplication of funds

GR: Not only persons individually affected, taxpayers must have sufficient interest in preventing the illegal expenditure of moneys raised by taxation and they may, therefore, question the constitutionality of statutes requiring expenditure of public moneys.To justify the suit, it is necessary that public funds should be involved.

Requisites of taxpayer’s suit1. Tax money is being extracted and spent in violation of specific Constitutional

protections against abuses of legislative power;2. Public money is being deflected to any improper purpose; and3. Petitioner seeks to restrain respondents from wasting public funds through

enforcement of an invalid or unconstitutional law.

Expenditure of public funds by an officer of the State for the purpose of executing an unconstitutional act constitutes a misapplication of such funds.

Taxpayer need not be a party to the contract to challenge its validity. As long as taxes are involved, people have the right to question contracts entered into by the government.

Transcendental importanceDeterminants

1. Character of funds or other assets involved in the case;2. Presence of a clear case of disregard of a constitutional or statutory prohibition by

the public respondent agency or instrumentality of the government; and3. Lack of any other party with a more direct and specific interest in raising the

questions being raised.

It is not proper to implead the President as respondentGR: The President, during his actual incumbency, may not be sued in any civil or criminal case.

14

EXCEPTION: He remains accountable to the people but he may be removed from office only by impeachment.

CHAPTER 2: INHERENT LIMITATIONS ON THE POWER OF TAXATION

A. THE POWER TO TAX HAS LIMITS The power to tax is an inherent power but such power must still be exercised in

accordance with the inherent and constitutional limitations If there exists conflicting interest between the taxing authorities and taxpayers, it

must be resolved in favor of the real purpose of taxation, which is, promotion of common good.

2 Kinds of Limitations:o Constitutional Limitation – those provided for in the Constitution

o Inherent Limitations – restrictions to the power to tax attached to its

nature

B. THE INHERENT LIMITATIONS (Le-N-T-Ex-Ice)1. (Le) Levied for a public purpose2. (N) Non-delegability of the taxing power3. (T) Territoriality or situs of taxation4. (Ex) Tax exemptions of the Government5. (Ice) International Comity

Violation of any or all of the above is a. equal to taking without due processb. infringement of the general principles of int’l law which form part of the law

of the land

C. LEVIED FOR A PUBLIC PURPOSE Amount raised must

o Inure to the benefit of the public

o Used for

Support of the state Some recognized object of the Government Public service

You cannot use public funds to promote an individual’s interest, even if it may incidentally result to the benefit of the public

Rationale: tax can be levied against one class of individuals in favor of another class; you can ruin one class while favoring the other

If it is for a private purpose, it is robbery because government takes property of another and then gives it in favor of another person.

“public purpose” includes “indirect public advantage”o if an individual directly enjoys the tax, it is still valid as long as there is a

link to public purpose

Test to determine existence of Public Purposeo Duty test – if it is the duty of the government to provide such thing

o Promotion of General Welfare Test – if proceeds will directly promote

the public’s welfare

Purposes of levying tax: o regulatory purpose

o raise government revenue

o support government existence

o rehabilitate/stablize a threatened industry, which is affected with public

interest

If purpose of the tax is not stated, it is presumed that it is created for a public purpose

Examples (presumption of public purpose)o Pensions of war veterans assurance that a person’s patriotism will be

acknowledged and rewardedo Unemployment relief

o Support for the handicapped

o Care for the aged

o Scholarships for poor but deserving citizens

o Tax on sugar

o Oil Price Stabilization Fund oil industry is imbued with public interest,

and a dramatic increase in oil prices will result to economic crisis

The public purpose must exist at the time the law was enacted.o Government may only use public funds for a public purpose

15

o The existence of public purpose determines its validity, not the incidental

benefit to the public

D. NON DELEGABILITY OF TAXING POWER

Source of Power People Delegation Transferred from the people to Congress Basis: delegata potestas non potest delegari.

Theories that justify the delegation:o Power to fill up the details- subjects of less interest in which general

provision may be made, thus those who are to act under such general provision, has the power to fill up the details.

o Power of Contingent Legislation- what is delegated is the task of

ascertaining the facts that bring its declared policy into operation.

Delegable Powers: (Ta-Em-Trea-LIA)a. (Ta) Tariff Powers-reason for its delegation is necessity.b. (Em) Emergency Power- President can exercise this power in times of war or

other national emergency, as authorized by Congress through law. (Sec23(2) ArtVI, 1987 Constitution)

c. (Trea) Treaty and Executive Agreement Powers-Power of President to enter in to executive agreements, and to ratify treaties. (Sec21, ArtVII, 1987 Constitution)

d. (L) Local taxing power- Theory of non-delegation of legislative power does not apply in local units. Reason- LGU not sovereign entities.

e. (I) Initiative and Referendum- o Initiative- power of the people to propose and enact legislation

without action by the legislature.o Referendum- power of the people to approve or reject any act of the

legislature, and also to approve or reject legislation that the legislature has referred to them.

f. (A) Administrative Matters: o Valid as regards:

i. Valuation of property pursuant to fixed rulesii. Equalization of assessments by a central bodyiii. Collection of taxes

Test to determine permissible delegation: a. Completeness test- The law must be complete in itself, setting forth therein

the policy to be executed, carried out, or implemented by the delegateb. Sufficiency standard test -The law must fix a standard. The limits of which are

sufficiently determinate and determinable to which the delegate must conform in the performance of his functions.

Non-Delegable Powers:a. Selection of property or transaction to be taxedb. Determination of purposesc. Rate of taxationd. Rules of taxation

Prohibition on Executive Legislation and Judicial Legislationo Based on separation of powers of state.

o Law-making power-legislative branch

o Law-executing power- executive branch

o Law-interpreting power- judicial branch

E. TERRITORIALITY OR SITUS OF TAXATION

General rule: A state may not tax property lying outside its borders or lay an excise or privilege tax upon the exercise or enjoyment of a right or privilege derived from the laws of another state and therein exercised or enjoyed.

Taxation is an act of sovereignty which could only be exercised within state’s territorial boundaries.

Taxes are paid for the protection and services provided by the taxing authority which could not be provided outside the territorial limits of the taxing power.

Situs of taxation: situs is latin term which means “situation,” “location or place.”

Determination of situs: (S-NCR-L)o (S) Subject matter of the tax- Situs may depend on what is being taxed:

excise/privilege, business, occupation, person, act or activity.o (N) Nature/kind/ classification of the tax- situs may depend on what tax is

being levied: income tax, import duty, sales tax or real property tax. o (C) Citizenship of the tax payer- situs may depend on which state the taxpayer

is a citizen of, or probably an alien, dual citizen, stateless or refugee.

16

o (R) Residenxe of the taxpayer- situs may depend on the residence of the

taxpayer: resident, non- resident. o (L) Location of the property- situs may depend on the palce the thing or

property is located: within the Philippines or outside the Philippines.

F. GOVERNMENT EXEMPTION

It is a matter of public policy. o Property belonging to the State or any of its political division intended for

government use and purposes is generally exempt from taxation.o express provision of law needed to satisfy the rule.

Always remember that “Exemption is the rule and taxation is the exception.”

Reasons for exemption (A-Nore-So-Re)o (A) Avoid transferring money from one pocket to another.

o (Nore) No revenue.

o (So) So as not to unduly impede govt functions.

o (Re) Reduce amount of money to be handled.

Exception to the (General Rule) Exemption o The rule on the exemption of government is not absolute.

o The government may tax itself. Clearly, exemption applies only to

government entities which immediately and directly exercise its government powers.

o GOCCs, agencies, or instrumentalities are subject to taxation under

the NIRC and LGC. However, only income from proprietary activities and not from essential governmental functions are taxable.

Definition of Termso RP (Republic of the Philippines) – corporate government entity through

which the functions of government are exercised throughout the Philippines.

o NG (National Government) – entire machinery of the central government

as distinguished from different forms of local governmento GOCC (Government-Owned and Controlled Corporations) – any

agency organized as a stock or non-stock corporation

o GA (Government Agency) – any of the various units of the government

including a department, bureau, office, instrumentality, or GOCC, or LGU or a distinct unit therein.

G. INTERNATIONAL COMITY

DSE (Doctrine of Sovereign Equality) o In par parem non habet imperium or “as between equals there is no

sovereign”o Foreign sovereign does not subject itself to another.

DSI (Doctrine of Sovereign Immunity)o The State cannot be sued without its consent.

o The State can do no wrong.

o Based on practicality because of the difficulty of enforcing tax laws.

IC (Incorporation Clause)o The Philippines adopts the generally accepted principles on international

law as part of the law of the land.o The Philippines adheres to the policy of peace, equality, justice, freedom,

cooperation, and amity with all nations.

CHAPTER III: CONSTITUTIONAL LIMITATIONS

The power to tax involves the power to destroy.8 These were the famous words penned by the great Chief Justice Marshall in 1819. As discussed in the preceding chapters, the power to tax is the strongest of all the inherent powers of the State. As being unlimited in its range, the 1987 Constitution has vested this power to the people who pay it, through their representatives, the Legislature.9 Though the taxing power is characterized as such an awesome power, it is not unconfined.10

8 McCulloch v. Maryland, 17 U.S. 4 Wheat. 316 316 (1819). 9 MCIAA v. Marcos, 330 Phil. 392, 404 (1996).

17

In the previous chapter, we have already discussed that taxing power, although plenary in nature, is still subject to certain limitations. Some of these limitations are not to be found in any statute, thus the term inherent limitations. In this chapter, we are now to discuss the second type of limitations of the taxing power of the State – The Constitutional Limitations on Taxation. The 1987 Philippine Constitution provides the following limitations:

1. Due process;2. Equal protection;3. Freedom of speech and of the press;4. Non – infringement of religious freedom and worship;5. Non – impairment of contracts;6. Non – imprisonment for dent or non – payment of poll tax;7. Appropriations, revenue, and tariff b ills shall originate exclusively originate

from the house of representatives;8. Uniformity, equitability, and progressivity of taxation;9. Power of Congress to delegate to the President the authority to fix tariff rates,

import and export quotas, etc.;10. Veto power of the President;11. Tax exemption of properties actually, directly, and exclusively used for

religious, charitable, and educational purposes;12. Voting requirement in connection with the legislative grant of tax exemption13. Non – impairment of the jurisdiction of the Supreme court in tax cases;14. Exemption from taxes of the revenues and assets of educational institutions,

including grants, endowments, donations and contributions

DUE PROCESS

No person shall be deprived of life, liberty, or property without due process of law , nor shall any person be denied the equal protection of the laws. (Sec. 1, Art III, 1987 Phil. Constitution)

10 Dizon, E. (2013). THE CONSTITUTIONAL LIMITATIONS OF TAXATION. In Taxation Law Compendium (2013 ed., Vol. 1). Rex Book Store.

In order that a tax statute may be validly imposed on the people, it must be lawful. In other words, a tax law passed by the Congress of the Philippines must first be constitutional. Under Section one (1) of the Bill of Rights (Art. III, 1987 Philippine Constitution), the tax law must undergo due process for it amounts to an individual’s property (though minimal) being deprived from him. The due process clause is a constitutional safeguard of the people from the government, which is the taxing authority. If so proved that the tax law is violative of this constitutionally protected right, under the principle of ubi jus ibi remedium, it shall be struck down. As in the words of Justice Bradley, “In judging what is ‘due process of law’, respect must be had to the cause and object of the taking, whether under the taxing power, the power of eminent domain, or the power of the assessment fir local improvements, or some of these; and, if found to be suitable or admissible in the special case, it will be adjudged to be ‘due process of law’, but if found arbitrary, oppressive, and unjust, it may be declared to be not ‘due process of law’.” 11

ASPECTS OF DUE PROCESS

There are two aspects under the due process clause – substantive and procedural. Substantive Due Process is the aspect which prohibits the State from encroaching on the fundamental liberties provided for by the constitution. Simply put, in order that a tax statute be constitutional, it must be reasonable, fair and just, and not be harsh nor oppressive. In the event that taxes collected, or to be collected, are confiscatory in nature, such obligation enforced upon the tax payer is violative of the due process principle, and is therefore unconstitutional.12

Procedural due process, on the other hand refers to the procedural limitations placed on the manner in which a law is administered, applied or enforced.13 It is but elementary in democratic forms of government that laws, especially those which impose a tax obligation on its citizenry, be exercised in accordance with the prescribed procedure. This is mandatory. To do otherwise shall give rise to a right which the taxpayer may use to ask the Courts its succor. The tax collector may be stopped if the taxpayer can demonstrate

11 Davidson v. New Orleans, 96 US 97 (1878).12 Reyes, et al. v. Almanzor, et al., G.R. Nos. 49839 – 46, 26 APR 1991.13 Dizon, E. (2013). THE CONSTITUTIONAL LIMITATIONS OF TAXATION. In Taxation Law Compendium (2013 ed., Vol. 1). Rex Book Store.

18

that the law has not been observed.14 In a case decided by the Supreme Court, it held that due process was not observed when the trial court classified certain properties of the Roman Catholic Church were tax – exempt under the 1973 constitution where no court hearing was conducted thereon.15

RULES OF DUE PROCESS IN TAXATION

The exercise of the State of its inherent power to tax its constituency must conform to the following rules:

a.) It must be for a public purpose;b.) Operates uniformly to all who are under its purview;c.) Exercised only within the jurisdiction of the duly authorized taxing authorityd.) In the assessment and collection of taxes, notice and hearing shall be

provided the taxpayer to guarantee against injusticee.) Publication is not merely directory, but mandatory;f.) There must be a right to appeal given to the taxpayer in cases where it is

proper, being a statutory, and not a natural right.16

It is good to take note, that although the taxpayer is granted the right to have due notice and hearing, such is only guaranteed when the tax to be imposed shall substantially affect him. In other words, when the tax to be imposed by the government is not one which could be changed by hearing the taxpayer, its absence does not violate the constitutional safeguard. A person’s right to due process is therefore not invaded. However, if such tax would be in the nature of an ad valorem tax which utilizes the use of assessors to ascertain the proper value of a taxable item or property, such act is considered as judicial in nature. Thus, due process is satisfied by giving the opportunity to the taxpayer to be heard respecting such assessment.17

14 Commissioner of Internal Revenue v. Algue, Inc., G.R. No. L – 28896, 17 FEB 1988.15 Province of Abra v. Hernando, etc., et al., G.R. No. L – 49336, 31 AUG 1981. 16 Bello v. Francisco, 4 SCRA 134; Rodriguez v. Director of Prisons, 47 SCRA 153.17 Dizon, E. (2013). THE CONSTITUTIONAL LIMITATIONS OF TAXATION. In Taxation Law Compendium (2013 ed., Vol. 1). Rex Book Store.

PROCEEDINGS IN TAX CASES

Due process in taxation does not mean nor require that a full blown judicial proceeding be done. Generally, such cases are settled summarily and must be interfered with as little as possible.18 As government projects are mainly fueled by the revenue generated by taxes paid by individual taxpayers, the delay which is normally present in judicial proceedings are not required in the enforcement of taxes and assessments and are frowned upon.19 No government could exist if all litigants were permitted to delay the collection of its taxes.20

PRESUMPTION OF VALIDITY OF TAX LAWS; RETROACTIVITY

The courts of law will not declare a statute, passed in accordance with the manner set out by the Constitution, unconstitutional for being in violation of the due process clause on mere allegations by the taxpayer.21 Every statute passed by the Congress enjoys the presumption of validity, including tax laws. The burden of proving that the law is unconstitutional shall be borne by the taxpayer in accordance with our rules on evidence. Also, the mere fact that a tax statute is expressed to be retroactive in its application is not proof in itself that the law is unconstitutional.

EQUAL PROTECTION

No person shall be deprived of life, liberty, or property without due process of law, nor shall any person be denied the equal protection of the laws. (Sec. 1, Art III, 1987 Phil. Constitution)

18 Churchill and Tait v. Rafferty, 32 Phil. 580, 585, 21 DEC 1915.19 Dizon, E. (2013). THE CONSTITUTIONAL LIMITATIONS OF TAXATION. In Taxation Law Compendium (2013 ed., Vol. 1). Rex Book Store.20 Lorenzo v. Posadas, 64 Phil. 353, 368 18 JUN 1937.21 Dizon, E. (2013). THE CONSTITUTIONAL LIMITATIONS OF TAXATION. In Taxation Law Compendium (2013 ed., Vol. 1). Rex Book Store.

19

The second (2nd) constitutional limitation is found under the same provision of the 1987 Constitution as the due process clause. Aptly stated, not person shall be denied of the equal protection of laws. The equal protection clause requires that persons similarly situated should be treated alike, both as to rights conferred and responsibilities imposed.22 It does not, however, require equal treatment of all persons, regardless of their situation. The Constitutional safeguard merely requires that all persons who are within the ambit of the statute shall be treated alike, under like circumstances and conditions, both with respect to the privileges acquired and liabilities imposed.23

The power of the State to classify, in relation to taxation, property and persons to be taxed, the rates of such taxes, as well as the methods of assessment, valuation, and collection is unquestioned, but is not absolute.24 Such classification must be based upon real and substantial differences between the persons, property or privileges, and those not taxed must bear some reasonable relation to the object or purpose of legislation or to some permissible governmental policy or legitimate end of governmental action.25Thus, the equality of taxation rule is not violated if classifications or distinctions made are based on substantial and reasonable differences.26

GOALS IN DISTRIBUTION

Two different goals in distribution arise when “fairness” or “equality” are looked at, vertical and horizontal. The latter refers to the fair treatment of tax payers with the like ability to pay. It prohibits the discrimination on the grounds such as race, gender, occupation, etc.27 Stated differently, those similarly situated shall be similarly taxed.28 Meanwhile, the former

22 Ichong v. Hernandez, 101 Phil. 1155.23 Sison, jr. v. Ancheta, G.R. No. 59431, 25 JUL 1984. 24 Aban, B. (1994). Law of Basic Taxation in the Philippines (2001 ed.). National Book Store.25 See Thomas P. Matic, Jr., Taxation in the Philippines (Vol. I, pp. 79 – 80).26 Aban, B. (1994). Law of Basic Taxation in the Philippines (2001 ed.). National Book Store.27 Dizon, E. (2013). THE CONSTITUTIONAL LIMITATIONS OF TAXATION. In Taxation Law Compendium (2013 ed., Vol. 1). Rex Book Store.28 See AICPA Guiding Principles for Tax Equity and Fairness (2007), p. 3.

refers to the relative tax burden of tax paying units with different abilities to pay. Vertical equity seeks to tax in a proportional or progressive way.29

DIMENSIONS OF TAX EQUITY AND FAIRNESS

Aside from the aforementioned goals, it has been recommended that the following dimensions be considered in determining tax equity and fairness

a.) Exchange Equity and Fairness – Taxpayers must, over the long run, receive the appropriate value for the taxes they pay;

b.) Process Equity and Fairness – Taxpayers have a voice within the tax system, are given due process and are treated with respect by the tax administrators;

c.) Time – Related Equity and Fairness – Taxes are not unduly distorted when income or wealth levels fluctuate over time;

d.) Inter – Group Equity and Fairness – No group of taxpayers is favored to the detriment of another without good cause; and,

e.) Compliance Equity and Fairness – All tax payers pay what they owe on a timely basis.30

REQUIREMENTS OF VALID CLASSIFICATION OR DISTINCTION

As stated earlier, the State may validly classify or discriminate among its subjects so long as such is based on a rational basis. “The equal protection clause does not require the universal application of the laws, that is, that it operates on all people without distinction. Such an effect might in fact sometimes result in unequal protection.”31 Thus, in order that a classification to be a valid one, it must conform to the following:

a.) That it must be based on substantial distinctions;b.) It must be germane it the purpose of the law;c.) It must not be limited to the preexisting conditions; and,d.) It must apply equally to all members of the class.32

29Dizon, E. (2013). THE CONSTITUTIONAL LIMITATIONS OF TAXATION. In Taxation Law Compendium (2013 ed., Vol. 1). Rex Book Store.30 Ibid.31 Cruz, I. (2000). Constitutional law (2000 ed., p. 125). Quezon City, Metro Manila, Philippines: Central Lawbook Pub.32 Ormoc Sugar Co. Inc. v. Treasurer of Ormoc City, et al., L – 23794, 17 FEB 1968.

20

FREEDOM OF SPEECH AND OF THE PRESS

No law shall be passed abridging the freedom of speech, of expression, or of the press,or the right of the people peaceably to assemble and petition the government for redress of grievances (Section 4, Article III, 1987 Constitution)

There are four (4) primary reasons why freedom of expression, which encompasses speech, the press, assembly and petition, is essential to a free society. First, the self – expression of an individual enables him to realize his full potential as a human being. Second, enlightened judgment is possible if one considers all the facts and ideas and test’s one’s own against it. It is vital to the attainment and advancement of knowledge. Third, it is necessary to our system of governance. Democratic Societies’ development and advancement is largely dependent on how well – informed its citizenry is for if it would be otherwise, the result would be tyranny and oppression. Lastly, it serves as a safeguard system of the public, developing a system of “checks and balances” against the possible corrupt practices of the State.33

The provision of the constitution necessarily includes the liberty of the press which is principally, although not exclusively, immunity from prior restraint and/or subsequent censorship.34 To discuss further, it is not the censorship of the press per se which is the evil sought to be prevented. It refers to any action of the government by means of which it might prevent such free and general discussion of public matters as seems absolutely essential to prepare the people for an intelligent exercise of their rights as citizens.35

CURTAILMENT OF FREEDOM

Briefly put, immunity is granted to the press so as to help promote and develop an informed citizenry. They exist as a vital source of public information. It sheds more light on

33 Dizon, E. (2013). THE CONSTITUTIONAL LIMITATIONS OF TAXATION. In Taxation Law Compendium (2013 ed., Vol. 1). Rex Book Store.34 Near v. Minnesota, 283 U.S. 697, 283 U.S. 707.35 Cooley’s Constitutional Limitations, 8th ed. P. 866

the public and business affairs of the nation than any other instrumentality of publicity. Public opinion, as the most potent of all restraints against the corrupt actions and practices of the government, is afforded protection by nothing less than the constitution itself. A free press stands as one of the great interpreters between the government and the people. To treat it otherwise, as to subject it to taxes, would amount to suppression and abridgement of publicity results to the curtailment of press freedom and freedom of speech and of expression.36

It has been held though that although granted immunity from certain taxes, they can still be subject to general taxes. However, taxes that may still be validly imposed upon them must be fair, reasonable, and just, and in accordance with the person’s right to the equal protection of laws. It must not be used as a tool to abridge the freedom of press under the guise of valid tax, as when it is exercised by the state arbitrarily and capriciously, singling out the press from other businesses or if such taxes are imposed only on a select few press members. In such case, the Supreme Court has acknowledged the potential for abuse is present in differential taxation of the press.37

RELIGIOUS FREEDOM

No law shall be made respecting an establishment of religion or prohibiting the free exercise thereof. The free exercise and enjoyment of religious profession and worship without discrimination or preference shall forever be allowed. No religious test shall be required for the free exercise of civil or political rights (Sec 5, Art. III, 1987 Philippine Constitution)

In accordance with the above stated provision, our Constitution and laws provide an exemption from taxation properties which are devoted exclusively for religious purposes. This grant of immunity of the fundamental law of the land and other tax laws were made to

36 Ibid.37 Robert M. Howie, Leathers v. Medlock: The Supreme Court Changes Course on Taxing the Press, 49 Wash. & Lee L. Rev. 1053 (1992), citing Minneapolis Tribune Co. v. Minnesota Commissioner of Revenue, 460 U.S. 575 (1983)

21

further realize the declared principle of the State which is The Separation of the Church and the State.38

The Constitutional provision, like Sec. 1 of the Bill of Rights, can be further divided in to 2 clauses: (a) the Non – Establishment clause; and (b) the Free Exercise clause.

NON – ESTABLISHMENT CLAUSE

The non – establishment clause, in general, merely prohibits the State, or any of its instrumentalities and political subdivisions, from setting up a church. Necessarily, it includes prohibitions such as:

a.) The State cannot pass a law which aid nor discriminate a religion;b.) It cannot force a person, nor influence him, to join, remain, or to leave a

church or religious sect;c.) It cannot, openly or secretively, participate in the affairs of any religion or

church; and,d.) No tax in any amount, large or small, can be levied to support any religious

activities or institutions, whatever they may be called, or whatever form they may adopt to teach or practice religion.39

REQUISITES FOR CONSTITUTIONALITY

The wall of separation that must be maintained between church and state “is a blurred, distinct, and variable barrier depending upon the circumstances of a particular relationship.”40 The case of Lemon v. Kurtzman41 enunciated in a three – part test to assess whether a law violates the Establishment clause:

1.) Does the law have a secular purpose?2.) Is the Primary effect either to advance religion or to inhibit religion?3.) Does the law foster an excessive governmental entanglement with religion?

38 Sec. 6, Art II, 1987 Philippine Constitution39 see Everson v. Board of Education40 Dizon, E. (2013). THE CONSTITUTIONAL LIMITATIONS OF TAXATION. In Taxation Law Compendium (2013 ed., Vol. 1). Rex Book Store.41 403 U.S. 602 (1970)

If any of these questions are answered in the negative, then the law becomes unconstitutional as it violates the Establishment Clause

FREE EXERCISE CLAUSE

The Free Exercise clause, on the other hand, withdraws from the legislative power, state and federal, the extortion of any restraint on the free exercise of religion. It bars “governmental regulation of religious beliefs as such, prohibiting the misuse of secular governmental programs “to impede the observance of one or all religions even though the burden may be characterized as being only indirect.42

RELIGIOUS GROUPS ARE EXEMPT TO PAY TAXES

Generally, religious groups, sects, and like organizations are exempt from paying taxes like Income tax, license fees, and similar taxes as it imposes a burden on the free exercise of religion. Albeit, like the press, religious groups may still be subject to general taxes depending upon the circumstances.

Properties Actua PROHIBITION AGAINST IMPAIRMENT OF OBLIGATION OF CONTRACTS

No law impairing the obligation of contracts shall be passed. [Section 10, Article III, Constitution]