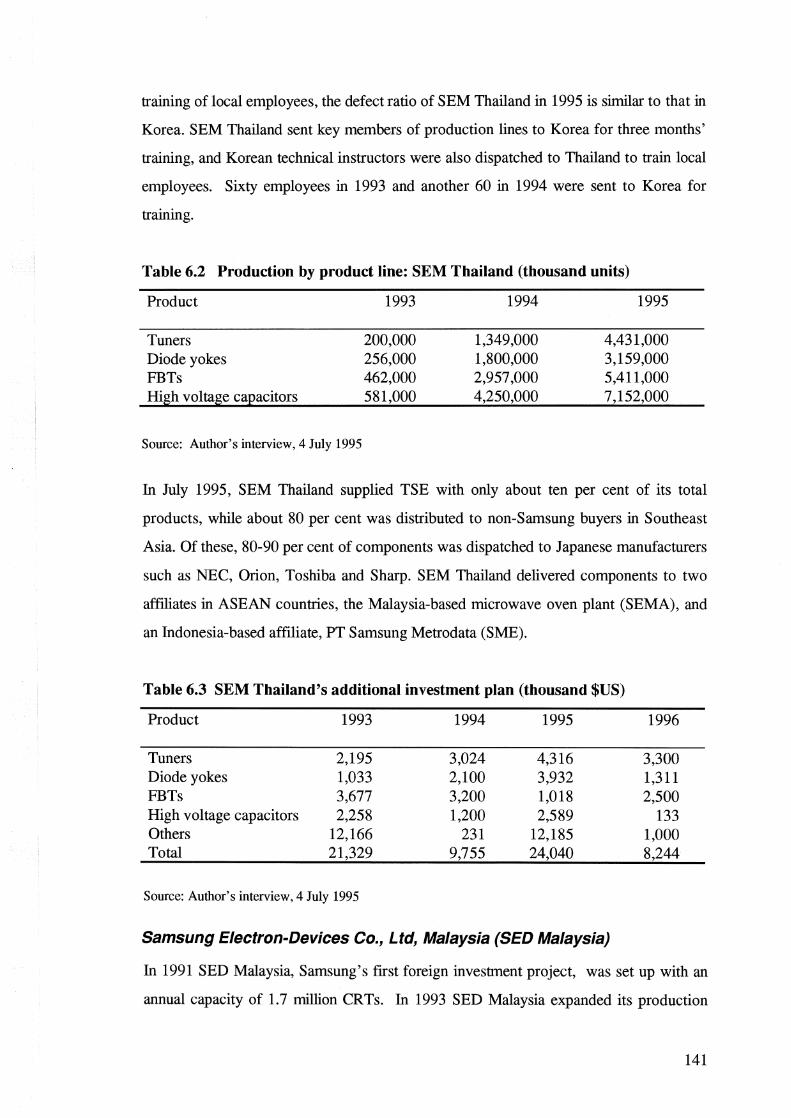

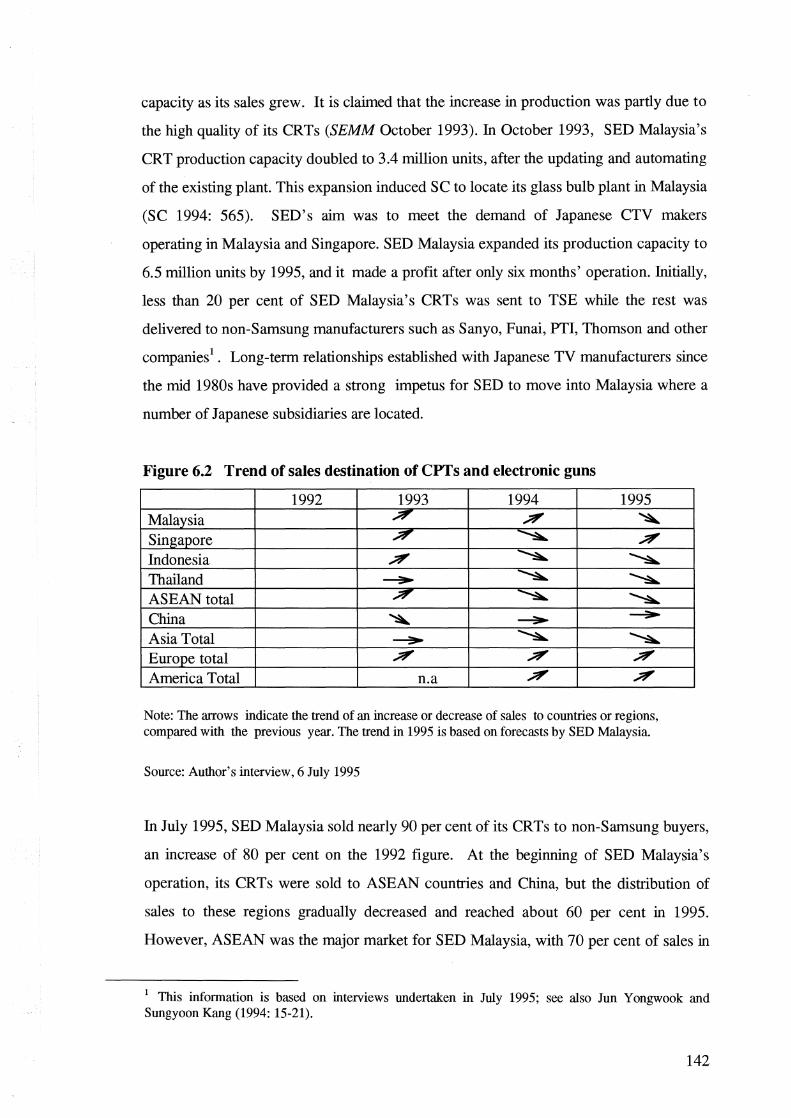

Embed Size (px)

Citation preview

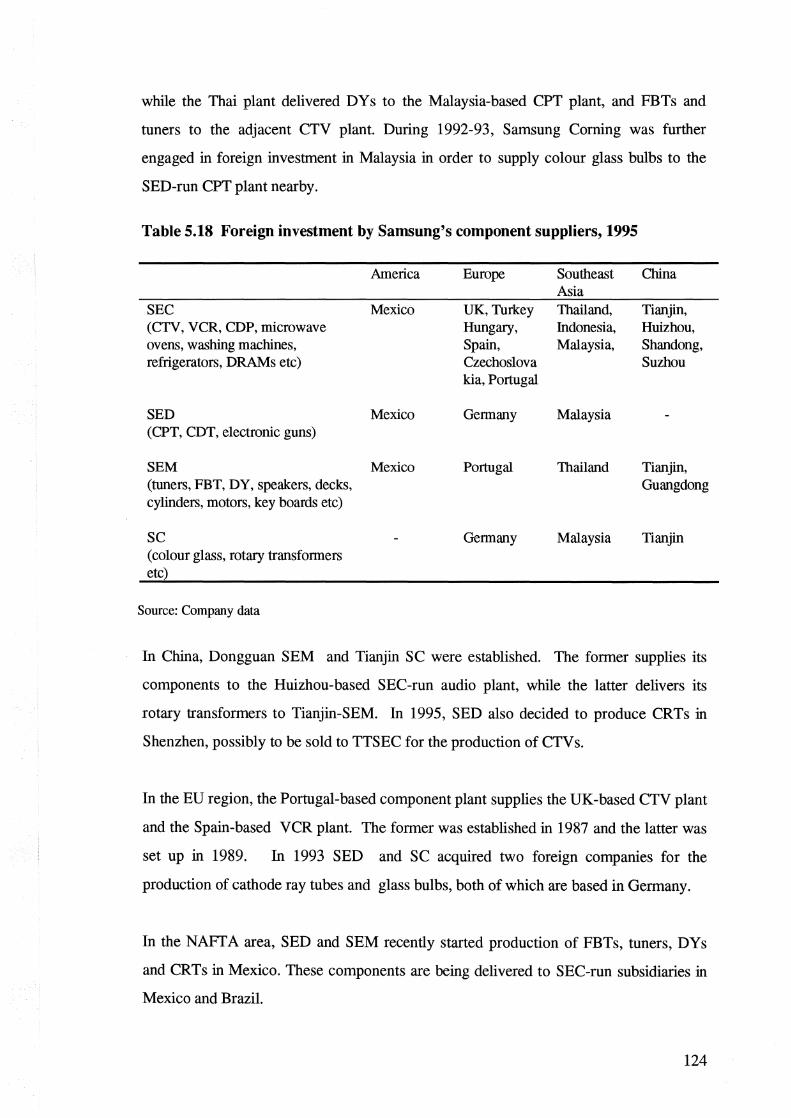

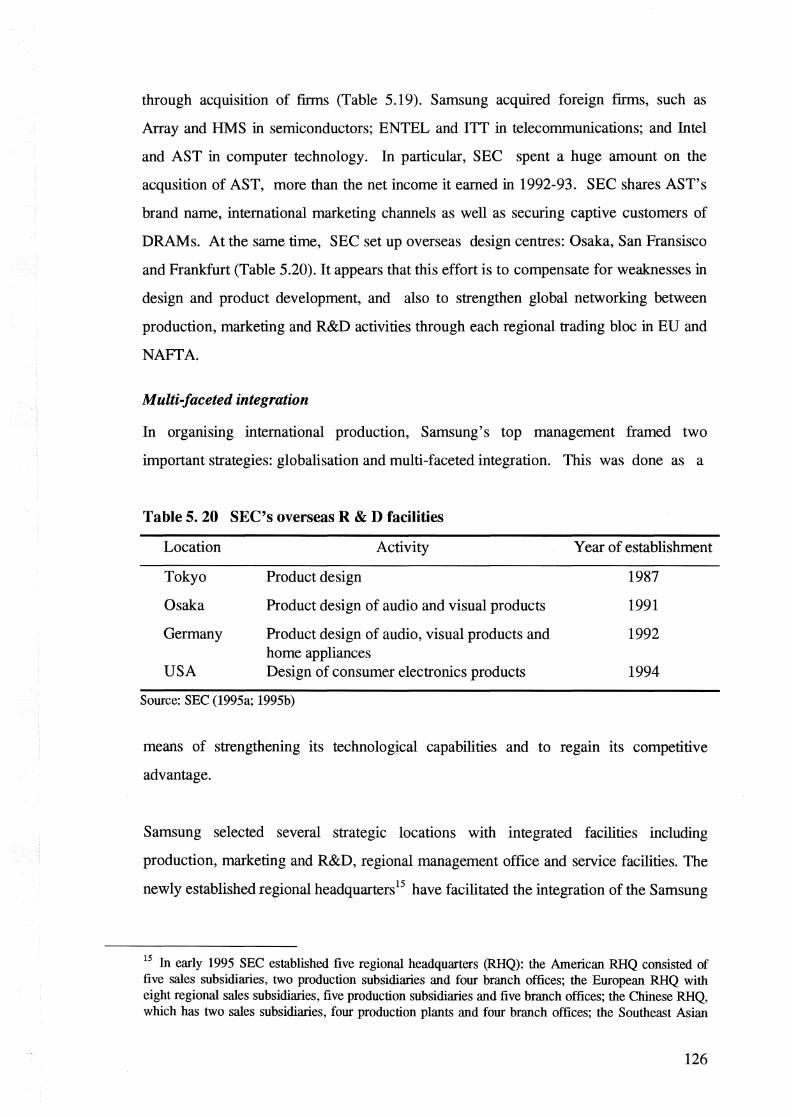

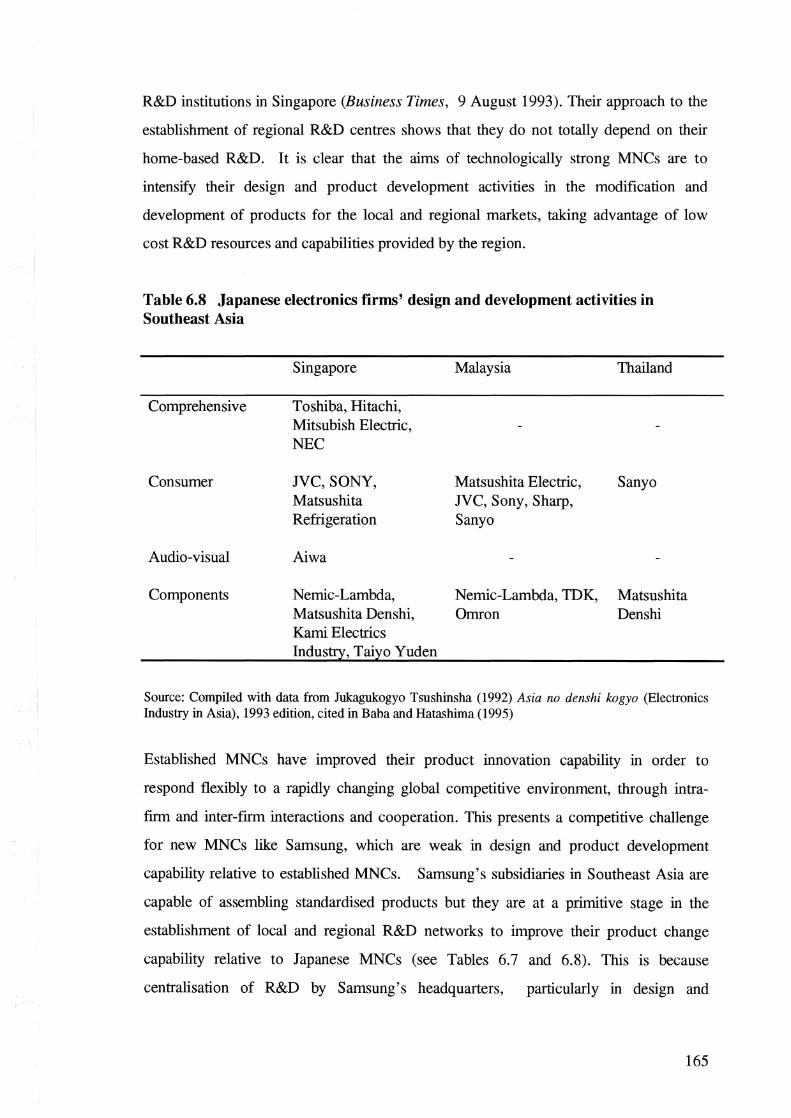

Technological Capabilities and Samsung's International Production

Strategies in East Asia

Young-Soo Kim

A thesis submitted for the degree of Doctor of Philosophy at the Australian National University

April1997

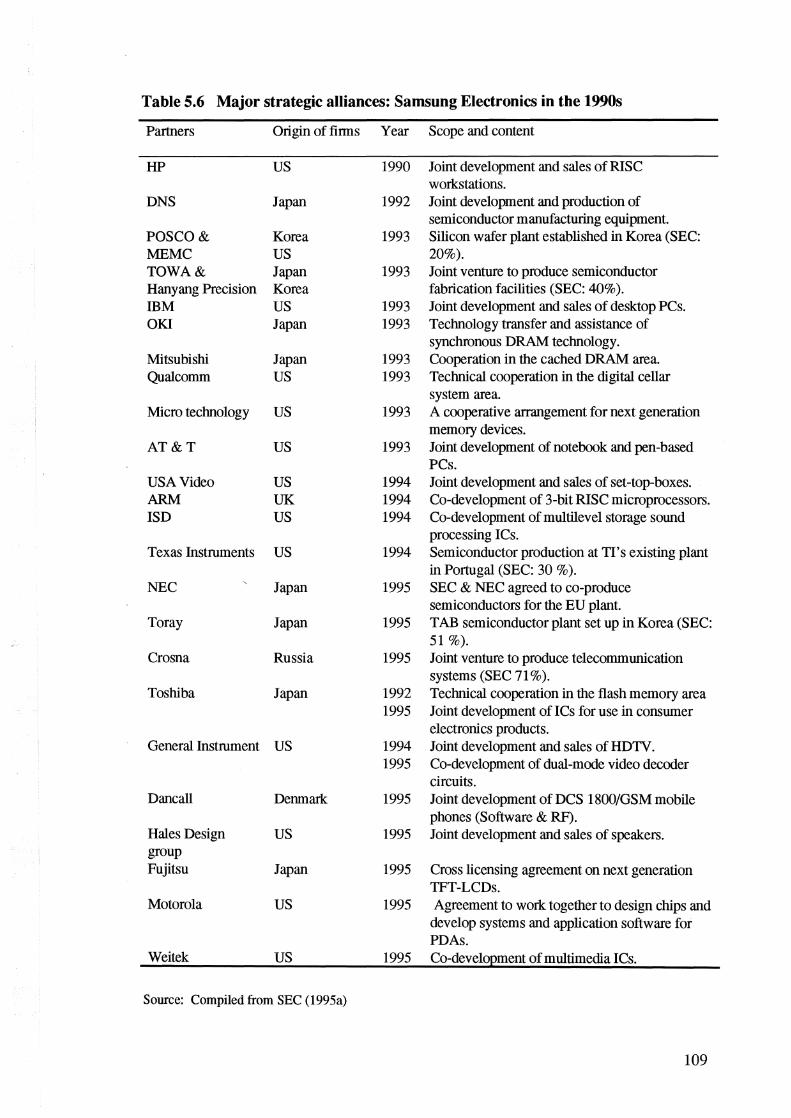

4 DRAM, OEM and international production in the mid and late 1980s

Despite criticism that was openly expressed within the group due to the expensive and

risky nature of Samsung' s investment in the DRAM business, the late chairman Lee

Byung-Chull remained strongly committed to the DRAM project until his death in 1988.

Samsung's success in DRAM production partly derived from Lee Byung-Chull's

enterprenuership.

Another aspect of DRAM production that affected, directly or indirectly, the

development of Samsung's technological capabilities and internationalisation was

connected with its original equipment manufacturer (OEM) arrangements. OEM

production benefits technologically weak firms by reducing the need for capital

investment in the establishment of international marketing and distribution channels, as

well as reducing the need for in-house design and new product development capacity.

OEM thus was a most attractive mechanism, allowing Samsung to allocate a large

proportion of the group's resources and capabilities to the DRAM sector. For nearly a

decade, according to Business Korea (March 1992), many Samsung affiliates were

starved of cash because of the size of investment directed towards the DRAM project.

In 1984-87 Samsung established two foreign production plants, one in the United States

and one in the United Kingdom, where cheap labour was not available. Jun (1987)

argues that conventional theories fail to explain this type of foreign investment, and calls

for the development of a new theory. In 1988-89 foreign investment by Samsung was

extended to low labour cost economies in Asia, America and Europe. During this

period, the export market was increasingly characterised by protectionism. Significant

features of Samsung's internationalisation in the 1980s were the strength of Samsung's

production capability on the one hand, as well as weakness in product change, strategic

marketing and international management on the other.

65

This chapter examines (1) OEM and foreign licensing which significantly influenced

Samsung's technological development; (2) innovation activities and systems; (3)

production capability and product-market position; and (4) the relationship between

international production and technological capabilities.

OEM and foreign licences

OEM and foreign licences were the most significant factors in the technological

development of Korean firms during the 1980s. They also mark a feature of the process

of internationalisation during the period. During the 1970s the source of foreign

technology in the electronics sector in Korea was mainly foreign direct investment from

Japan and the United States. In the 1980s, Korean manufacturers, with upgraded

assembling capability, shifted from being subcontractors of foreign technology suppliers

to OEM suppliers for major distributors in the United States, and for Japanese buyers

who had established their own sales channels and brand names internationally.

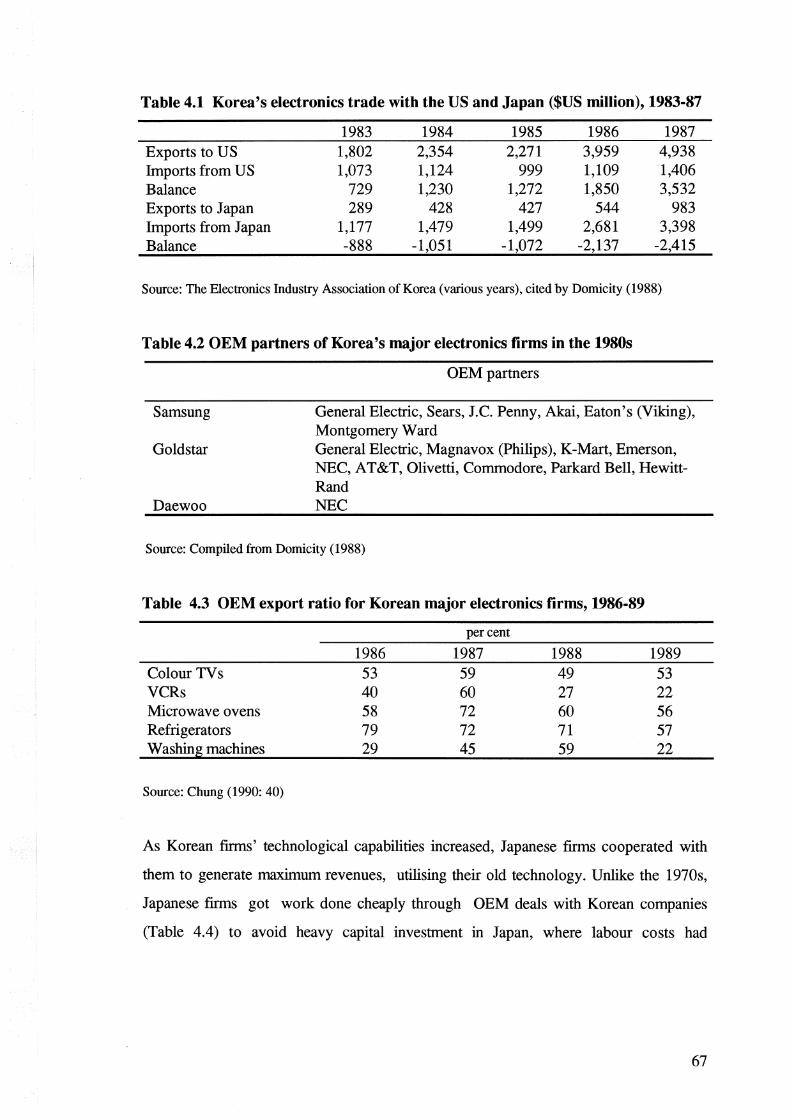

Korean firms could not operate efficiently in the export market without their Japanese

counterparts. Korean frrms, being final assemblers, needed a large proportion of

imported components from Japan. Table 4.1 indicates a typical feature of the Korean

electronics industry's trade: a huge bilateral trade surplus with the United States,

coupled with a huge deficit with Japan.

The leading Japanese consumer electronics companies were no longer in need of US

partners as a source of OEM buyers because they had established their own superior

sales channels and value-added products sold under their brand names (Domicity 1988:

8-7). By contrast Korean firms needed US partners. Their OEM partners fell into two

categories: traditional electronics companies, such as General Electric, RCA, Sunbeam

and Emerson Radio; and diversified retail outlets, such as J.C. Penny and Sears

(Domicity 1988: 8-7). All three major Korean firms (Samsung, Daewoo and Goldstar)

were heavily dependent on OEM exports during the 1980s and export ratios in most

products did not significantly change over time (see Tables 4.1 and 4.3).

66

Table 4.1 Korea's electronics trade with the US and Japan ($US million), 1983-87

Exports to US Imports from US Balance Exports to Japan Imports from Japan Balance

1983 1,802 1,073

729 289

1,177 -888

1984 2,354 1,124 1,230

428 1,479

-1,051

1985 2,271

999 1,272

427 1,499

-1,072

1986 3,959 1,109 1,850

544 2,681

-2,137

1987 4,938 1,406 3,532

983 3,398

-2,415

Source: The Electronics Industry Association of Korea (various years), cited by Domicity (1988)

Table 4.2 OEM partners of Korea's major electronics firms in the 1980s

OEM partners

Samsung General Electric, Sears, J.C. Penny, Akai, Eaton's (Viking), Montgomery Ward

Gold star

Daewoo

General Electric, Magnavox (Philips), K-Mart, Emerson, NEC, AT&T, Olivetti, Commodore, Parkard Bell, HewittRand NEC

Source: Compiled from Domicity (1988)

Table 4.3 OEM export ratio for Korean major electronics firms, 1986-89

percent

1986 1987 1988 1989 Colour TVs 53 59 49 53 VCRs 40 60 27 22 Microwave ovens 58 72 60 56 Refrigerators 79 72 71 57 Washing machines 29 45 59 22

Source: Chung (1990: 40)

As Korean firms' technological capabilities increased, Japanese firms cooperated with

them to generate maximum revenues, utilising their old technology. Unlike the 1970s,

Japanese firms got work done cheaply through OEM deals with Korean companies

(Table 4.4) to avoid heavy capital investment in Japan, where labour costs had

67

gradually increased (Domicity 1988). In doing so, technology licences1 were negotiated

with arrangements under which OEMs were tied to foreign component supply. In

addition, export restrictions were placed on VCRs, microwave ovens and compact disc

players (Bloom 1992: 77). For example, NC placed restrictions on Samsung for

overseas export when it licensed VCR technology in the early 1980s. When Japanese

firms began to issue licences for CDP technology, Korean firms remained dependent on

the Japanese firms for deck mechanisms (Bloom 1992: 78).

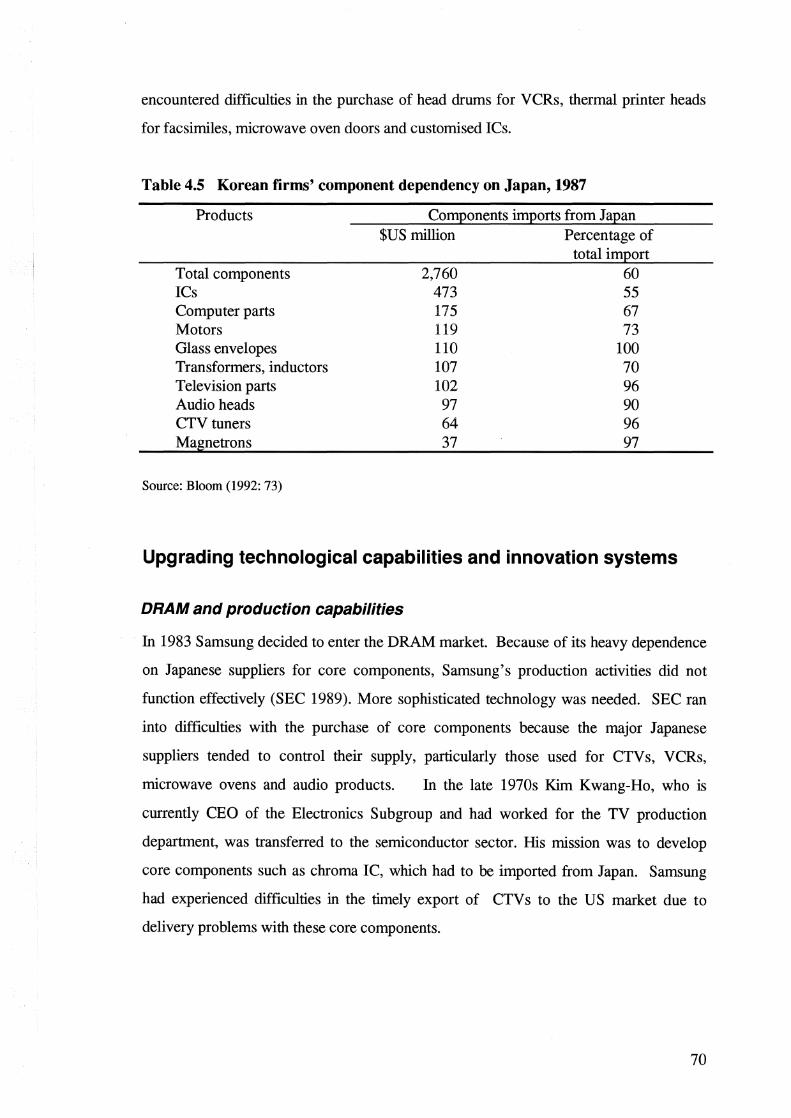

As a result, a large proportion of components had to be imported from Japanese firms.

The average import dependency on Japan was 60 per cent in 1987, but the proportion

for more sophisticated components such as magnetrons and TV tuners audio heads was

much higher (Table 4.5). As for Samsung, imports from Japan accounted for 35 per

cent of the value of its VCRs in 1987, 40 per cent for facsimile machines, 50 per cent for

computer terminals and audio cassette players, and over 60 per cent for personal

computers and computer printers (Management Today, April1987: 90).

Imported components need sophisticated high value-added technology and therefore

represent a high proportion of cost. This leads to smaller profit margins for Korean

firms. When Korean currency appreciates or wage rates increase, Korean products

become more vulnerable to foreign competition. Heavy dependence on OEM sales

makes it more difficult for Korean firms to lessen their reliance on Japanese component

suppliers due to their lack of design capability (Bloom 1992: 82) because product life

cycles require faster new product development.

As Korean firms' exports increased, Japanese firms protected the manufacture of their

core components which were essential to the assembly of final products. Bloom

(1992:81-82) identifies two strategies employed by Japanese firms in competing against

Korean counterparts which were catching up in technology. Firstly, Japanese firms, in

order to reduce the potential competition in the higher value-added and higher quality

1 Japanese firms changed their strategies in this regard. For instance, Japanese firms used semiknockdown kits that were ready for assembly as a first defence against reverse engineering. This gave competitors what they needed, but did not allow them to truly manufacture it. This applied to TV s, stereos and compact disc players (Domicity 1988).

68

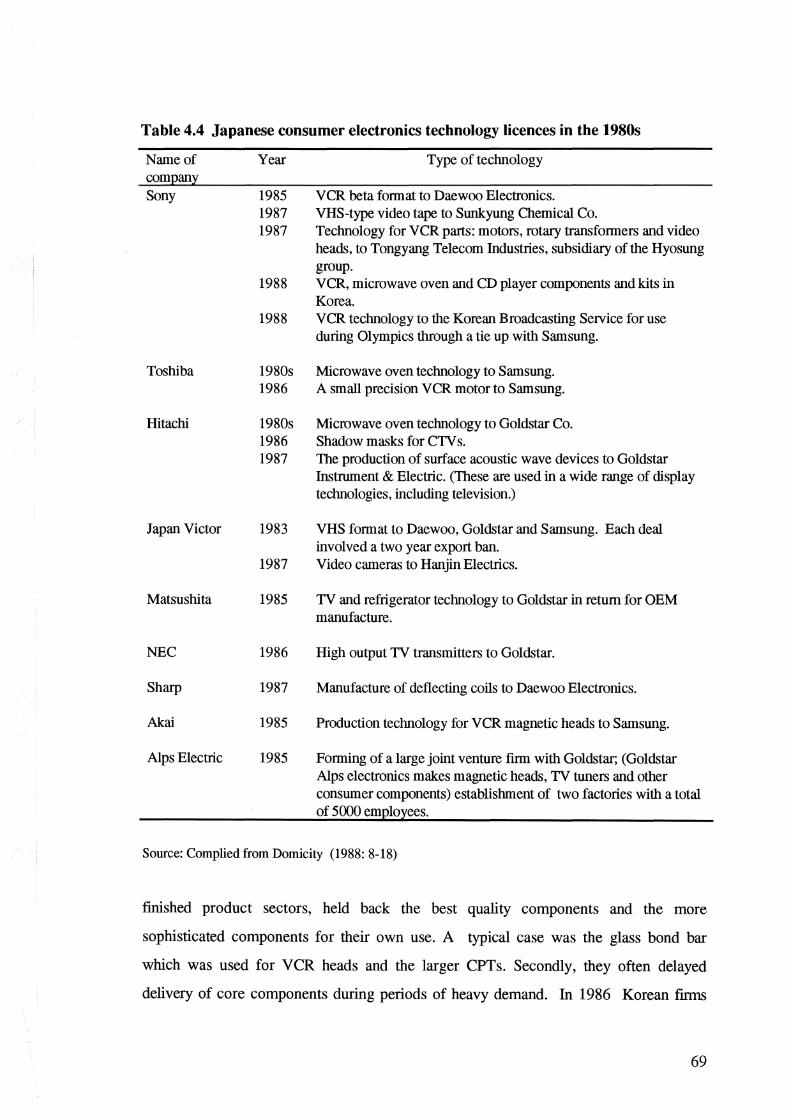

Table 4.4 Japanese consumer electronics technology licences in the 1980s

Name of company Sony

Toshiba

Hitachi

Japan Victor

Matsushita

NEC

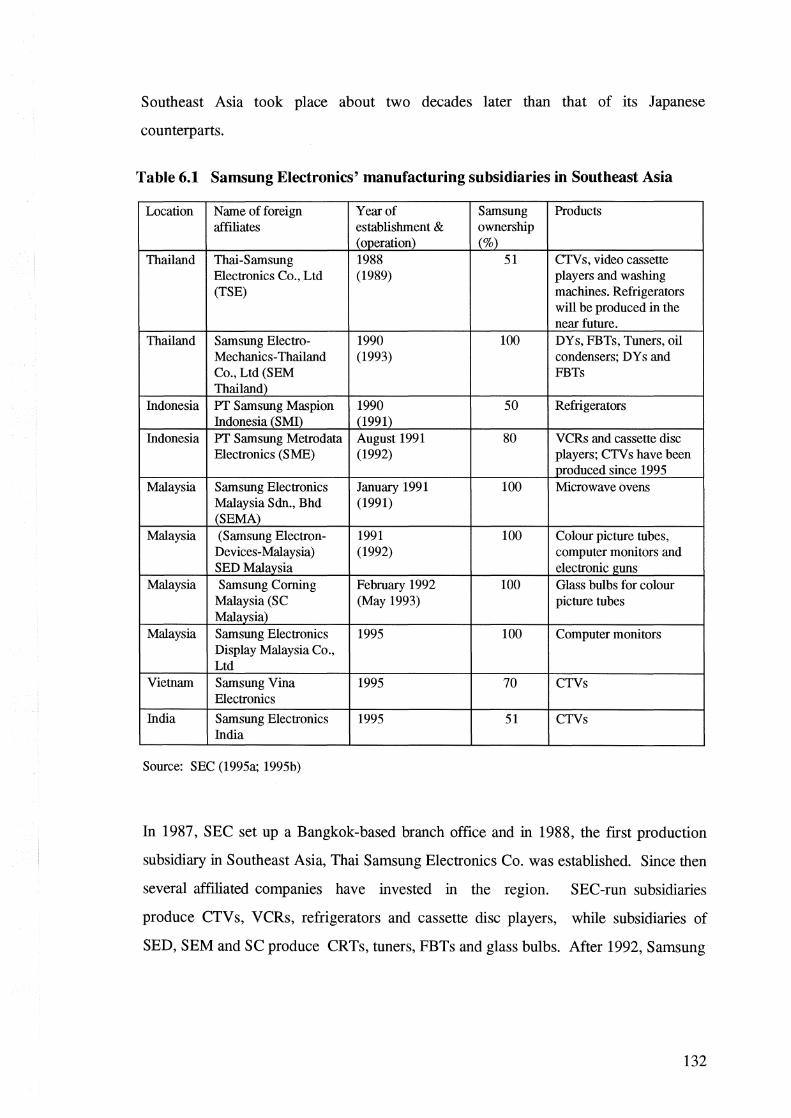

Sharp

Akai

Alps Electric

Year

1985 1987 1987

Type of technology

VCR beta format to Daewoo Electronics. VHS-type video tape to Sunkyung Chemical Co. Technology for VCR parts: motors, rotary transformers and video heads, to Tongyang Telecom Industries, subsidiary of the Hyosung group.

1988 VCR, microwave oven and CD player components and kits in Korea.

1988 VCR technology to the Korean Broadcasting Service for use during Olympics through a tie up with Samsung.

1980s 1986

1980s 1986 1987

1983

1987

1985

1986

1987

1985

1985

Microwave oven technology to Samsung. A small precision VCR motor to Samsung.

Microwave oven technology to Goldstar Co. Shadow masks for CTV s. The production of surface acoustic wave devices to Goldstar Instrument & Electric. (These are used in a wide range of display technologies, including television.)

VHS format to Daewoo, Goldstar and Samsung. Each deal involved a two year export ban. Video cameras to Hanjin Electrics.

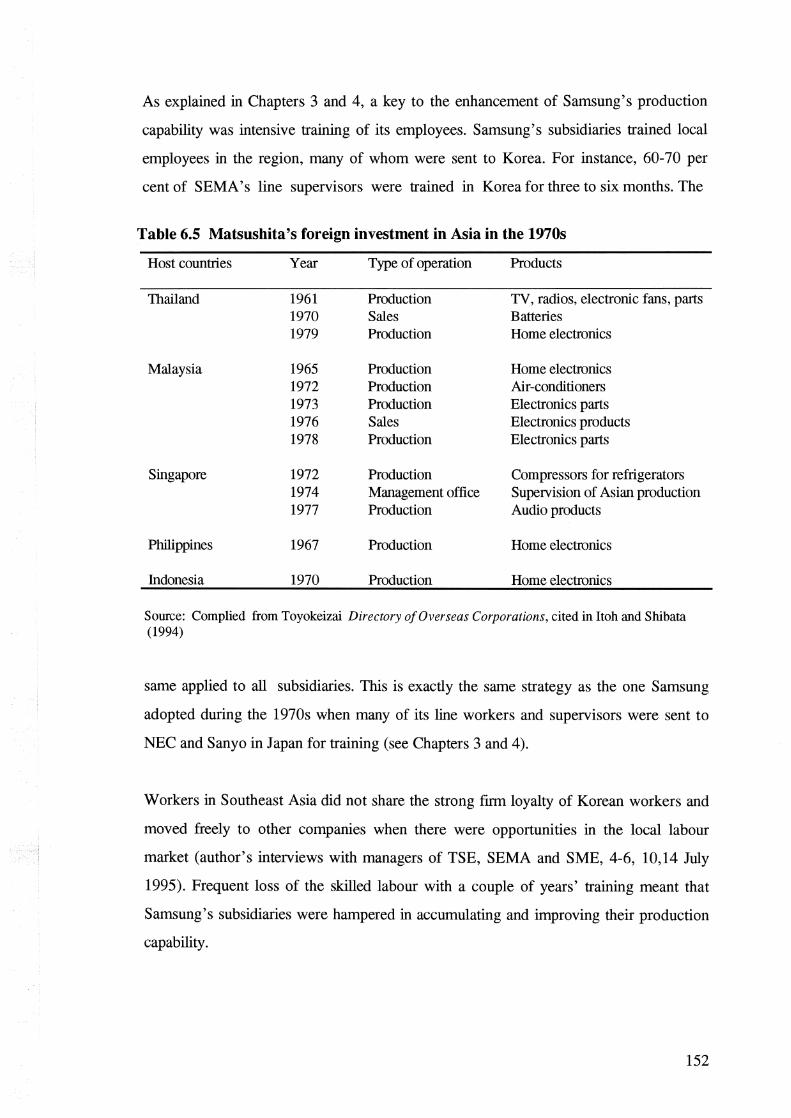

TV and refrigerator technology to Goldstar in return for OEM manufacture.

High output TV transmitters to Goldstar.

Manufacture of deflecting coils to Daewoo Electronics.

Production technology for VCR magnetic heads to Samsung.

Forming of a large joint venture firm with Goldstar; (Goldstar Alps electronics makes magnetic heads, TV tuners and other consumer components) establishment of two factories with a total of 5000 employees.

Source: Complied from Domicity (1988: 8-18)

finished product sectors, held back the best quality components and the more

sophisticated components for their own use. A typical case was the glass bond bar

which was used for VCR heads and the larger CPTs. Secondly, they often delayed

delivery of core components during periods of heavy demand. In 1986 Korean finns

69

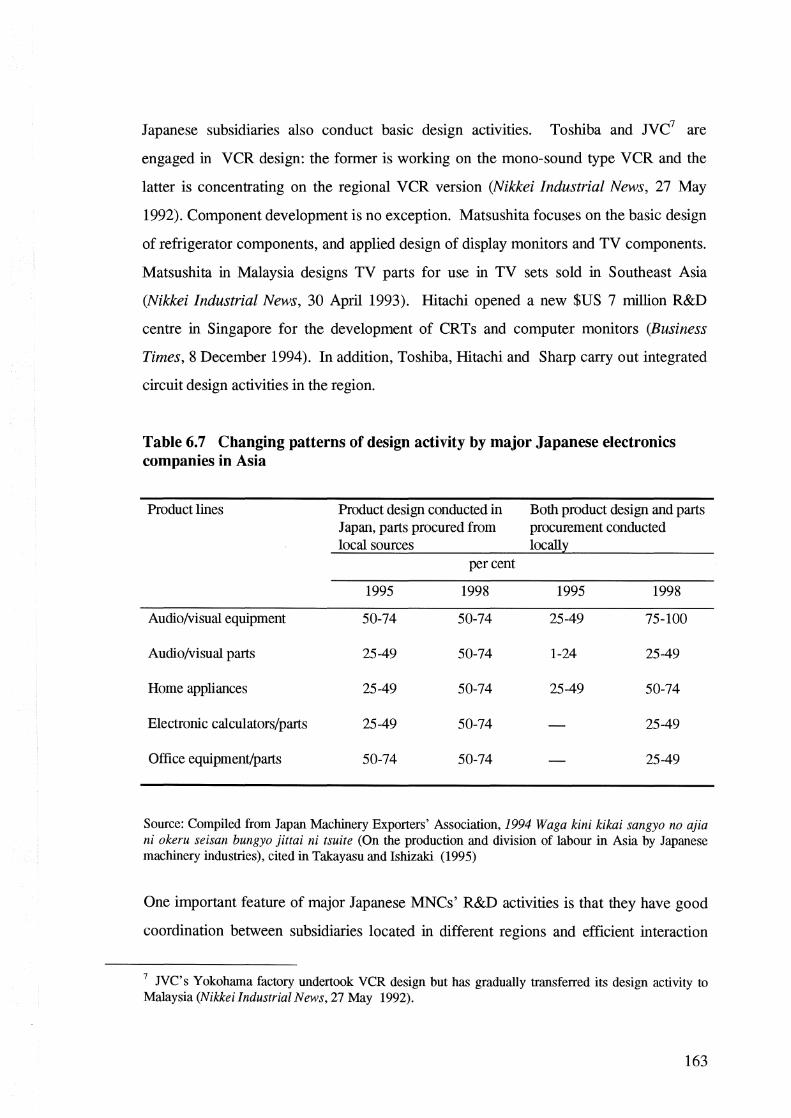

encountered difficulties in the purchase of head drums for VCRs, thermal printer heads

for facsimiles, microwave oven doors and customised ICs.

Table 4.5 Korean firms' component dependency on Japan, 1987

Products Components imports from Japan $US million Percentage of

Total components ICs Computer parts Motors Glass envelopes Transformers, inductors Television parts Audio heads CTVtuners Magnetrons

Source: Bloom (1992: 73)

2,760 473 175 119 110 107 102 97 64 37

total import 60 55 67 73

100 70 96 90 96 97

Upgrading technological capabilities and innovation systems

DRAM and production capabilities

In 1983 Samsung decided to enter the DRAM market. Because of its heavy dependence

on Japanese suppliers for core components, Samsung's production activities did not

function effectively (SEC 1989). More sophisticated technology was needed. SEC ran

into difficulties with the purchase of core components because the major Japanese

suppliers tended to control their supply, particularly those used for CTVs, VCRs,

microwave ovens and audio products. In the late 1970s Kim Kwang-Ho, who is

currently CEO of the Electronics Subgroup and had worked for the TV production

department, was transferred to the semiconductor sector. His mission was to develop

core components such as chroma IC, which had to be imported from Japan. Samsung

had experienced difficulties in the timely export of CTV s to the US market due to

delivery problems with these core components.

70

Samsung's chip production capability originally stemmed from the mass production of

watch chips that began in the early 1970s. Its capability had improved considerably by

the early 1980s. In 1983 Samsung announced its entry into DRAM production when the

Korean government enforced the 'Semiconductor Industry Promotion Plan' which was

to provide firms with tax incentives and substantial loans (Ernst 1994b: 77). Previous

experience gained through the production of watch chips motivated Samsung to enter

the DRAM business. The late Chairman also had a strong desire to expand into the

high technology sector.

In May 1983 Samsung set up its first foreign R&D institute- Samsung Semiconductor

Inc (SSI)- in Silicon Valley. Samsung's first objective was to develop 64K and 256K

DRAMs, and SSI became a means for the collection of information about up-to-date

technology and markets as well as being a training post for headquarters' R&D

personnel. Samsung was also able to recruit several Korean DRAM experts who were

educated in the US, and later played an important role in developing and

commercialising DRAMs. In June 1983, Samsung licensed DRAM design from Micron

Technology2 , a medium-sized US DRAM producer. Micron was the only possible

technology source, given Samsung's consistent but unsuccessful attempts to acquire

foreign technology from TI, Advanced MOS, Motorola, NEC, and Toshiba. For the

process technology development of the 64K DRAM, Samsung had access to

technological information from Sharp3 , which was the only source of process

technology such as 16K SRAM and 256K ROM. In November 1983, the 64K DRAM

was developed, and in mid 1984, mass production started.

Samsung shortened its learning process by a variety of interactions with foreign

technology sources. In particular, it put more importance on informal learning and

training in addition to the purchase of foreign technology. This enabled SEC to master

2 Micron Technology entered into the licence agreement because it desperately needed cash to establish a low-cost second source, enabling Micron to keep its own investment at a minimum. (Ernst 1994b:79).

3 Sharp's contribution to Samsung's DRAM success was significant. Dr Sasaki, who worked for Sharp and had a close relationship with the top management of Samsung, played an important role in the transfer of semiconductor process technology to Samsung. See Ernst (1994a) for the strategic differences between Sharp and other Japanese semiconductor competitors.

71

tacit knowledge as well as the technical information from imported patents. This

provided Samsung with an opportunity to overcome problems whenever critical

situations occurred.4 For instance, Japanese technology advisers who had maintained a

relationship with the ex-chairman, Lee Byung-Chull, advised on semiconductor

technology and market trends. Similarly, the new Chairman Lee Kun-Hee's informal

networks with technology sources were useful when the 4M DRAM was developed.

For the development of the 256K DRAM, Micron's design was submitted to extensive

'reverse engineering' (Ernst 1994b: 81). This is similar to the way VCRs and microwave

ovens were developed in the late 1970s. Samsung adopted a dual strategy in order to

accelerate the process of development. Two teams, one in Silicon Valley and the other

in a Korea-based laboratory, worked simultaneously. In October 1984, the Korea-based

team developed a 256K DRAM model and in early 1985 the Silicon Valley team

developed a model. The model developed in Silicon Valley was adopted for mass

production (Ernst 1994b). Samsung had trouble with mass production of this model,

however, and it was not until April 1986 that mass production of the 256K DRAM

started. Subsequently, Samsung was able to develop advanced DRAM products: 1M

DRAM (July 1986), 4M DRAM (February 1988), and 16M DRAM (September. 1990).

This shows the innovative way in which Samsung created a new capability by quickly

combining new knowledge and information from foreign sources with its own

accumulated capabilities.

Due to the technological spillover driven as a result of the development of the 256K

DRAM in July 1985, Samsung accelerated development of key microchips. Various

kinds of microelectronic chips were made during the late 1980s, ranging from

consumer electronics to industrial and telecommunications products. In October 1984

the 64K DRAM was exported to the United States and Europe. Samsung, however,

4 Sarnsung (SST 1987: 203) states, 'of the 309 individual manufacturing process steps, it succeeded in managing all the steps except eight key process steps by the application of its accumulated chip production technology .... as for the eight key process steps, it managed to overcome difficulties by the recruitment of three experts who had participated in the project of 64K DRAM in the US and been trained at Micron Technology'.

72

suffered from a huge loss because DRAM prices fell drastically from US$ 3 in 1984 to

20 cents in 1985. This fall continued until the end of the 1980s.

Samsung's production capability improved rapidly in the 1980s, in particular due to

improvements in DRAM process technology. In November 1981 SST was able to

develop the chroma IC, one of the most important components of CTV sets (SEC

1989).5 This was followed by the motor drive IC in 1982 and the image signal IC and

the playback IC in 1984.6 These components were used for TVs and VCRs, and only

produced by Japanese and US firms (SEC 1989).

Samsung accelerated its development of key microchips: ICs for multiple voice TV,

which combined six functions in one chip, in September (SMM September 1985); and

voice synthesis ICs in 1989 for use in robots, automobiles, microwave ovens,

refrigerators, washing machines and electronic toys. This spread to the

telecommunications sector. In March 1987, SST was able to produce 61 kinds of

telecommunications IC, which were core components of information processing systems

such as key phones, computers, electronic private automatic branch exchanges

(EPABXs) and facsimile machines.7 Various kinds of microelectronic chip were

developed during the late 1980s, ranging from consumer electronics to industrial and

telecommunications products.

By January 1987, before moving its international production to Thailand, SEC could

produce a total of 37 kinds of VCR IC. It is claimed that Samsung was able to supply

all the core microelectronic chips used in VCR sets (SMM January 1987). This lessened

the dependency on Japanese suppliers for core components. In 1988 SEC developed 2

micron bipolar process technology (SMM June 1988). From 1988 to 1989 it achieved

5 In the 1980s, the head of the semiconductor sector was Kim Kwang-Ho, who is a current CEO of SEC and the Samsung electronic business sector in charge of SED, SEM, SC, SDS, etc.

6 These were technologically sophisticated components which contain both analog and digital functions in one chip (SEC 1989).

7 These telecommunications ICs were not only for Samsung's internal use, but also for the export market. Exports were expected to increase up to US$ 350 million in 1987-92 (SMM March 1987).

73

several technological breakthroughs by developing a range of core components. These

were VCR motor control ICs, which improved the quality of the picture and the sound

of VCRs (SMM March 1989); communication ASICs used in personal computers

(SMM April1989); and dolby ICs (SMM September 1989).

Apart from microelectronic chips used in TV s, VCRs and telecommunications products,

several other memory devices were also developed in the 1980s. In December 1983,

Sarnsung developed the 64K DRAM, and then the 16K electrically erasable

programmable read only memory (EEPROM) in July 1984. As the speed of

technological improvement was accelerating in the late 1980s, Samsung achieved a

technological breakthrough by developing several microelectronic chips: the 256K

EEPROM equivalent to the 1M DRAM (December 1988); 1M SRAM equivalent to the

technology level of the 4M DRAM; 4M mask ROM (May 1989); and 0.6 micron

process technology equivalent to ultra large scale integration (ULSI) level technology

(December 1989). In June 1989, the 3-inch gallium arsenide (GaAs) wafer was

developed by an in-house R&D institute, Samsung Advanced Technology Institute

(SATI), and SC was in charge of producing the wafer. Subsequently, SEC planned to

manufacture light emitting diodes and the GaAs IC.8 In September 1989, Samsung

developed the laser diode.

DRAM production had both positive and negative effects on Samsung's technological

capabilities. One of the most significant contributions was the spillover effect of DRAM

technology on its production process capability in manufacturing sophisticated

components. This improved the quality of end products, particularly digitalised rather

than analog products. Major benefits went to the development of components for

telecommunication equipment, computers and semiconductors. Due to a favourable

external market environment, Samsung has generated huge profits since 1992, and the

exchange of its own DRAM technology contributed to the development of strategic

alliances with firms possessing complementary technology.

8 Gallium arsenide is superior to silicon for use in semiconductors. Unlike silicon, GaAs can convert from laser to electricity, and from electricity to laser. The GaAs chip is five times as fast as the silicon chip. It is used for high-frequency communications where silicon semiconductors cannot be used (SMM September 1989).

74

On the other hand, due to the fact that huge financial resources were poured into the

DRAM sector for almost a decade, investment in the improvement of design and

product development, as well as foreign market development, was postponed. As a

result, both consumer and industrial products were unable to achieve sustainable

competitiveness. One negative effect of this concentration on DRAM production was

SEC Korea's failure to transfer product change capability to its US-based subsidiary.

This meant that the subsidiary did not adequately meet changing customer needs with a

high end product mix.

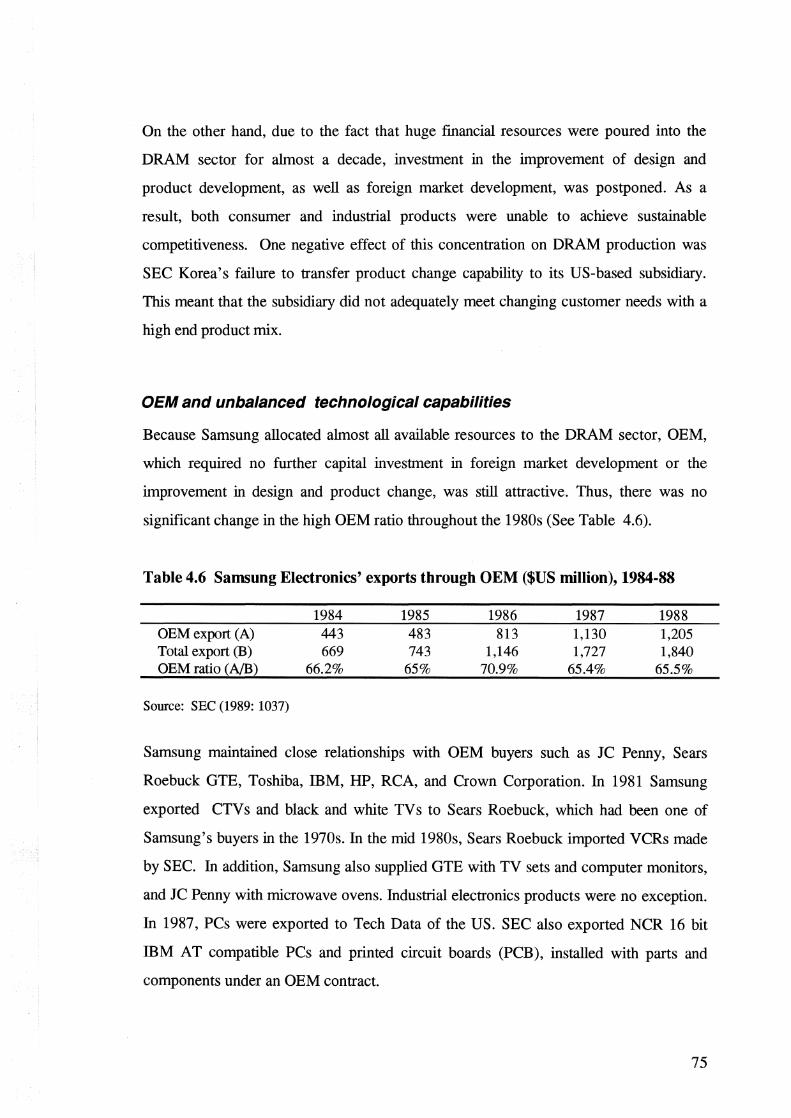

OEM and unbalanced technological capabilities

Because Samsung allocated almost all available resources to the DRAM sector, OEM,

which required no further capital investment in foreign market development or the

improvement in design and product change, was still attractive. Thus, there was no

significant change in the high OEM ratio throughout the 1980s (See Table 4.6).

Table 4.6 Samsung Electronics' exports through OEM ($US million), 1984-88

1984 1985 1986 1987 1988 OEM export (A) 443 483 813 1,130 1,205 Total export (B) 669 743 1,146 1,727 1,840 OEM ratio (AlB) 66.2% 65% 70.9% 65.4% 65.5%

Source: SEC (1989: 1037)

Samsung maintained close relationships with OEM buyers such as JC Penny, Sears

Roebuck GTE, Toshiba, IBM, HP, RCA, and Crown Corporation. In 1981 Samsung

exported CTV s and black and white TV s to Sears Roebuck, which had been one of

Samsung's buyers in the 1970s. In the mid 1980s, Sears Roebuck imported VCRs made

by SEC. In addition, Samsung also supplied GTE with TV sets and computer monitors,

and JC Penny with microwave ovens. Industrial electronics products were no exception.

In 1987, PCs were exported to Tech Data of the US. SEC also exported NCR 16 bit

IBM AT compatible PCs and printed circuit boards (PCB), installed with parts and

components under an OEM contract.

75

I

In order to maintain the three strategic products (CTVs, VCRs and microwave ovens) at

profitable levels, Samsung continuously improved production capability by the

acquisition of foreign technology, mostly from Japan. In order to access broad ranges of

technologies, Samsung extended its links with several technology suppliers in the

1980s, from Sanyo and NBC, to Matsushita, Toshiba, Sony and Sharp. SEC entered

into transactions with Sanyo, Toshiba, Matsushita, and Design and Manufacturing of the

US for microwave oven technology (Bloom 1992; SEC 1989). Multiple technology

sources allowed Samsung to master foreign technology quickly and as necessary. As

had been the case in the 1970s, Samsung had technical assistance agreements with

foreign licensors, mostly for the training of employees (SEC 1989: 286-90, 461-62) .

SEC particularly strengthened its relations with Toshiba. In 1982 it bought production

technology for facsimile machines, and acquired licences for more sophisticated

technology: air-conditioners over a five year period (1983), for which Toshiba sent

technical experts to SEC to train 450 technicians; cellular mobile phones, word

processors and washing machines (1984); air-conditioners, facsimile machines and

mobile phones (1985); hi-fi VCRs over a period of three years (1987), for which

Toshiba sent SEC technical advisers (SEC 1989).

SEC also developed its relations with Sanyo, Samsung's first joint venture partner. SEC

concluded a licensing agreement with Sanyo for microwave oven technology over a five

year period (December 1984), for which Sanyo sent technical experts to train SEC's

employees (SEC 1989). In May 1985, SEC also negotiated a five year licensing

agreement with Matsushita for magnetron production technology (a core component of

microwave ovens), for which Matsushita dispatched technical experts to SEC and SEC

sent its technical personnel to Matsushita Japan for training (SEC 1989:371). In

August 1983, Sony licensed Samsung to produce VHS-VCRs over a five year period

and, in February 1987, broadcasting cameras and VCRs. Samsung also linked with

Ikegami in September 1984 and with Shibasoku in May 1986 to produce broadcasting

colour monitors. Both firms also trained SEC technical personnel (SEC 1989).

76

SEC's technology acquisition was closely related to its OEM arrangements, supporting

the strategic export of profitable products. In this way, SEC accumulated improved

production capability through assembly of consumer electronics goods such as CTV s,

VCRs and microwave ovens.

On the other hand, OEM was negatively associated with upgrading product change

capability, which needs a relatively long period of investment in design and product

development because it is characterised as 'difficult-to-imitate technology'. This was no

problem in the early period when SEC freely purchased it. However, problems

developed when the technology market turned into a seller's market. The concept of

'low-cost with high volume', established during the OEM production period, was

embedded in Samsung' s organisational culture. This became a constraint on learning

and improving capabilities in international marketing and design and product

development where longer term investment was required.

Research and development, and innovation systems

SEC incrementally increased the number of its own foreign sales affiliates, while

maintaining its relationship with OEM buyers. Typically, Samsung first set up a foreign

branch office, and then it turned into a sales subsidiary when it had accumulated a

certain degree of foreign market knowledge.

Under the export led strategy, however, foreign sales channels that usually sold products

made in Korea did not closely interact with Korea-based production sites due to

Samsung's hierarchical multi-divisional organisation structure. Feedback from foreign

distribution channels to production functions in Korea was rare. Strategic marketing had

a long way to go, partly due to the lack of coordination between key value-added

activities.

The acquisition of information about changing customer needs and the need to forecast

future trends can lead to the development of new products with a competitive

advantage. This is difficult when there is a lack of coordination between manufacturing

77

and marketing. These organisational weaknesses lasted until the early 1990s and

directly resulted in low performance in the export market in the 1990s when the

electronics market became more complex and consumers' needs become diverse, with

regional variations.

At the same time, mismanagement of the 'profit centre' system (see Jun and Han 1994)

often resulted in unproductive competition between different departments and/or

divisions as well as different affiliates. One exemplar case was the brand conflict which

occurred between SEC and SED, both of which were producing the same CRT products

and competing with each other in the CRT export market, where the products were

being sold under the same Samsung brand name. In May 1986, SEC officially notified

SED to stop using the Samsung brand name for exports of CRT products. Finally, the

conflict was resolved when SEC withdrew its previous prohibition and allowed SED to

use the Samsung brand name again. Given the fact that competition with SEC was

unavoidable because SED had to continue CRT exports, however, SED eventually

decided to take on a new brand name, SAMTRON, which has been used since January

1988 (SED 1990: 338-39).

In the early 1980s, three of Samsung's affiliates, Korea Semiconductor, Korea

Telecommunications and Samsung-GTE, merged to form Samsung Semiconductor

and Telecommunications Co. Ltd (SST). It is thought that the objective of the merger

was to share semiconductor technology with the industrial and telecommunication

sectors (SMM October 1982), shifting concentration from consumer electronics to

industrial electronics.

The second stage of the merger between SEC and SST occurred in 1988. Samsung

aimed to share with SST its technological capability in the semiconductor sector and in

SEC-owned cross-border marketing channels for electronic products (SMM May

1988). In May 1988 a range of business functions including consumer electronics,

information and telecommunications, and semiconductor production was undertaken by

SEC. It appears that a hidden objective of this merger was to improve SEC's financial

78

position, since profitability continued to decrease in 1983-87. This will be discussed

later.

What SST got out of the merger was a diversification of microchips for consumer

electronics products. Before the merger, the development of microchips for consumer

electronics such as CTVs and VCRs was not a strategic priority for SST (SMM May

1988). Indeed, SEC was able to share telecommunications, computer and

semiconductors technologies. Kang Jin-Ku, who was the CEO of SST, was appointed

CEO of the new organisation of SEC (SMM September 1988).

As for R&D activities, there were three aspects to building technological capabilities:

increasing Korean-based R&D centres where Samsung was involved in the assimilation

and development of acquired foreign technology; establishing foreign-based R&D

centres which could provide it with new technologies, and up-to-date information; and

training for Korea-based R&D personnel.

SEC's newly established R&D centres in Korea during the 1980s were: the Suwon R&D

laboratory for audio and video products (1980); the Kiheung R&D laboratory for

memory devices (1982); and the two Kiheung R&D laboratories for telecommunications

systems (1983 and 1987). Samsung also established the Techno-College which offered

telecommunications and computer technology courses. From the late 1980s, Samsung

needed to integrate intra-group R&D activities. In 1987, an integrated R&D

organisation, Samsung Advanced Institute of Technology (SAlT) which linked with

several affiliates was established, concentrating particularly on chemistry, electronics and

aerospace technologies (Koh 1992). The Samsung Advanced Technology Training

Institute (SA TTl) was also set up in 1989 to provide vocational training in electronics

related technologies such as software, computer-aided design (CAD), computer-aided

manufacturing (CAM), micro processors and semiconductors (Koh 1992).

In addition, Samsung started to establish its own R&D organisations overseas. In 1987

it formed the Santa Clara Semiconductor R&D centre within the existing branch office

which had opened in 1983 and had been producing silicon wafers since 1985, employing

300 engineers. The strategic goal for this R&D centre was to seek frontier technologies

79

in the computing, office equipment and telecommunications fields. SEC's Tokyo Design

Centre also opened in 1987 to develop product design skills in consumer electronics and

robots (Koh 1992). In 1988 SEC acquired the Micro Five Corporation of the US to

complement its technological capability in the computer sector, and set up Samsung

Software America (SSA) in Boston. The objective was to acquire advanced software

technologies and to establish a US marketing base for computer exports. In October

1989 SEC established Samsung Information Systems America Inc. (SISA) in San Jose,

California, to support export activities and gather further technology for information and

telecommunications products (Koh 1992).

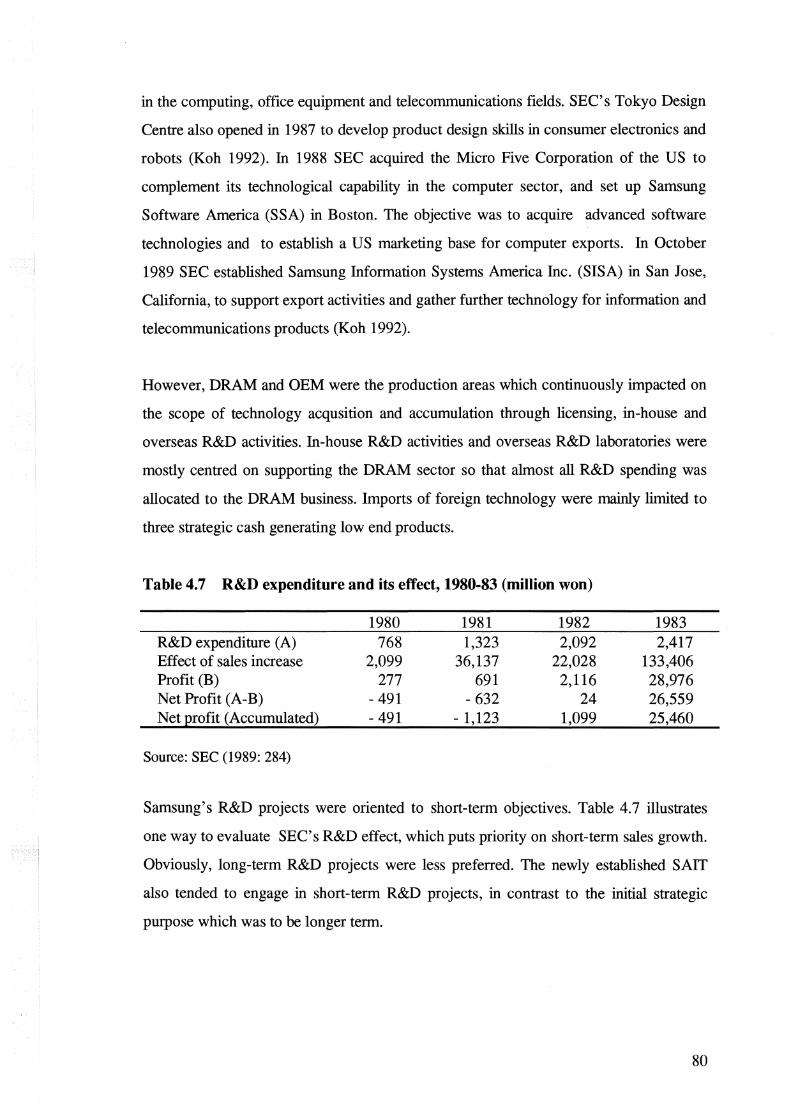

However, DRAM and OEM were the production areas which continuously impacted on

the scope of technology acqusition and accumulation through licensing, in-house and

overseas R&D activities. In-house R&D activities and overseas R&D laboratories were

mostly centred on supporting the DRAM sector so that almost all R&D spending was

allocated to the DRAM business. Imports of foreign technology were mainly limited to

three strategic cash generating low end products.

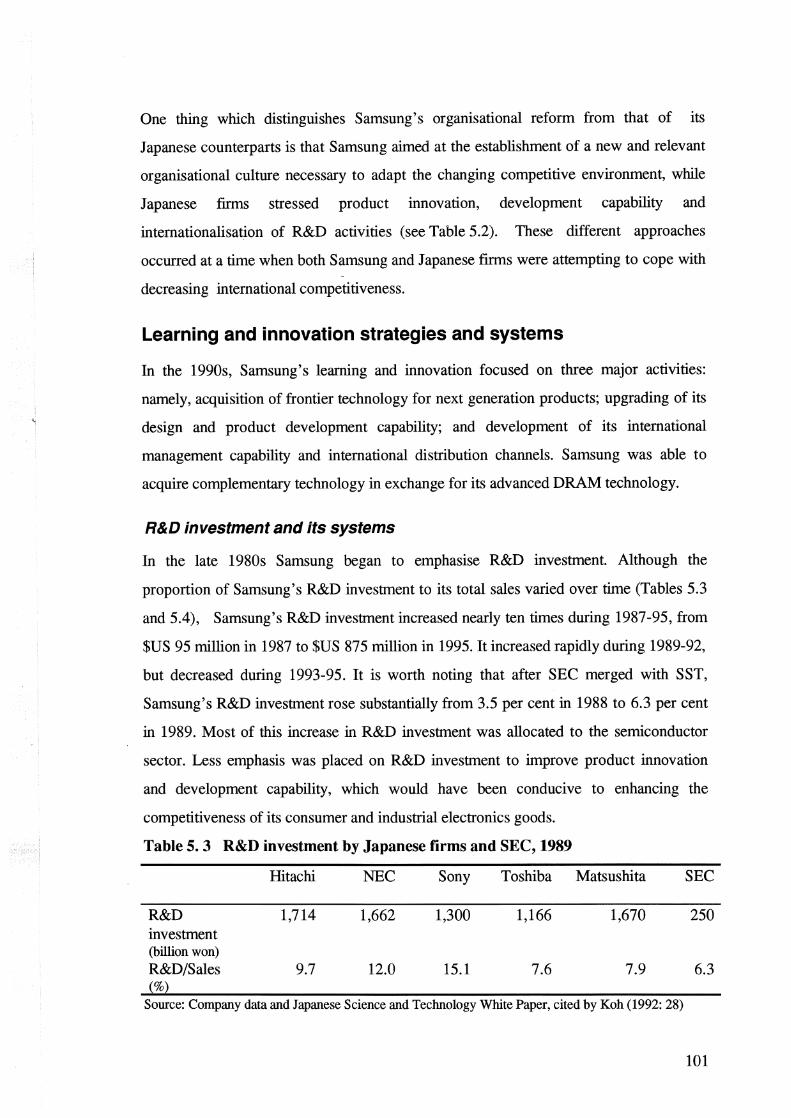

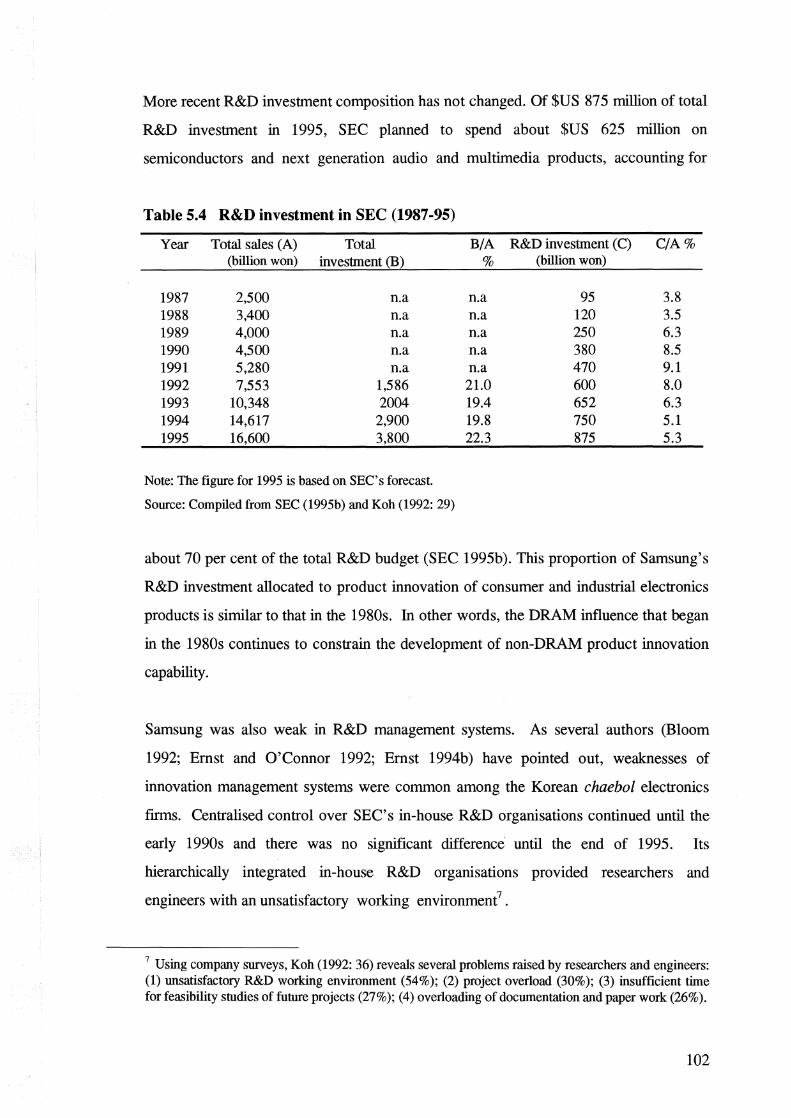

Table 4.7 R&D expenditure and its effect, 1980-83 (million won)

1980 1981 1982 1983 R&D expenditure (A) 768 1,323 2,092 2,417 Effect of sales increase 2,099 36,137 22,028 133,406 Profit (B) 277 691 2,116 28,976 Net Profit (A-B) -491 -632 24 26,559 Net profit (Accumulated) -491 - 1,123 1,099 25,460

Source: SEC (1989: 284)

Samsung's R&D projects were oriented to short-term objectives. Table 4.7 illustrates

one way to evaluate SEC's R&D effect, which puts priority on short-term sales growth.

Obviously, long-term R&D projects were less preferred. The newly established SAlT

also tended to engage in short-term R&D projects, in contrast to the initial strategic

purpose which was to be longer term.

80

The new chairman Lee Kun-Hee criticised the employee evaluation system which

focused on the evaluation of short-term performance as having negative impact on the

implementation of long-term strategies (Samsung 1993). However, this system

continued until the early 1990s. In addition to the concentration on DRAM production

and OEM arrangements, Samsung's human resources evaluation system was another

element working against upgrading design and product development capabilities.

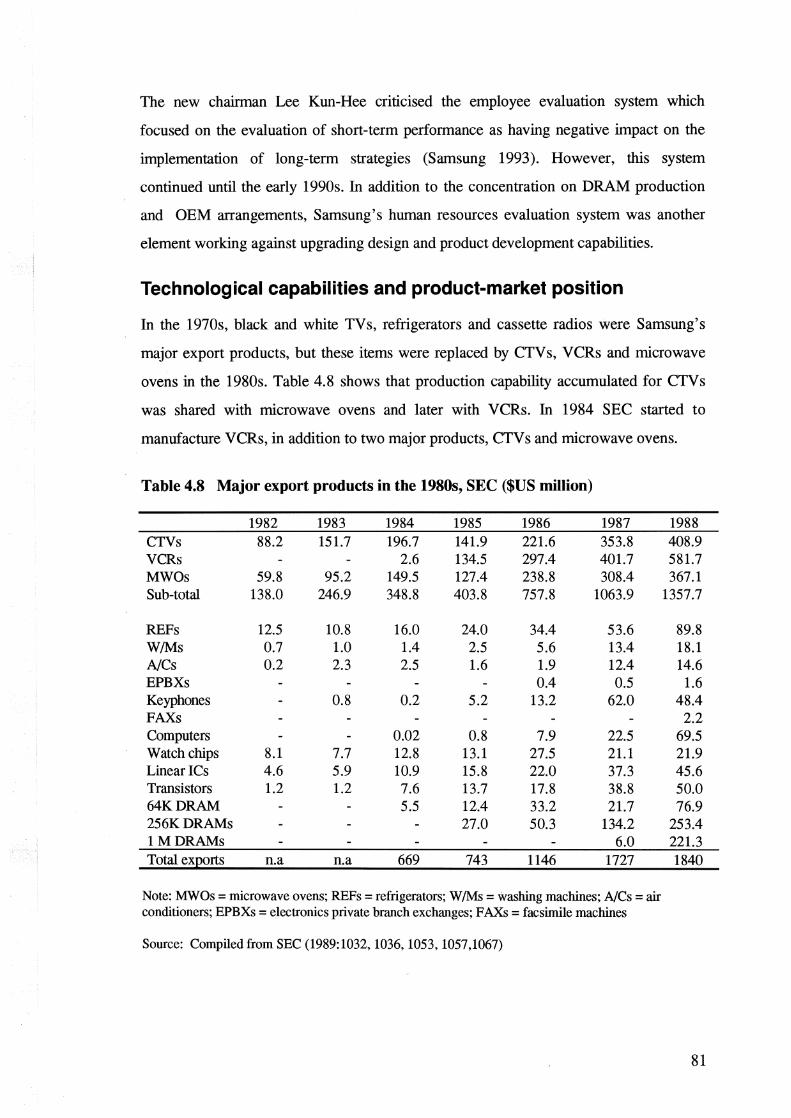

Technological capabilities and product-market position

In the 1970s, black and white TVs, refrigerators and cassette radios were Samsung's

major export products, but these items were replaced by CTV s, VCRs and microwave

ovens in the 1980s. Table 4.8 shows that production capability accumulated for CTVs

was shared with microwave ovens and later with VCRs. In 1984 SEC started to

manufacture VCRs, in addition to two major products, CTVs and microwave ovens.

Table 4.8 Major export products in the 1980s, SEC ($US million)

1982 1983 1984 1985 1986 1987 CTVs 88.2 151.7 196.7 141.9 221.6 353.8 VCRs 2.6 134.5 297.4 401.7 MWOs 59.8 95.2 149.5 127.4 238.8 308.4 Sub-total 138.0 246.9 348.8 403.8 757.8 1063.9

REFs 12.5 10.8 16.0 24.0 34.4 53.6 W/Ms 0.7 1.0 1.4 2.5 5.6 13.4 NCs 0.2 2.3 2.5 1.6 1.9 12.4 EPBXs 0.4 0.5 Keyphones 0.8 0.2 5.2 13.2 62.0 FAXs Computers 0.02 0.8 7.9 22.5 Watch chips 8.1 7.7 12.8 13.1 27.5 21.1 LineariCs 4.6 5.9 10.9 15.8 22.0 37.3 Transistors 1.2 1.2 7.6 13.7 17.8 38.8 64KDRAM 5.5 12.4 33.2 21.7 256KDRAMs 27.0 50.3 134.2 1MDRAMs 6.0 Total ex12orts n.a n.a 669 743 1146 1727

Note: MWOs =microwave ovens; REFs= refrigerators; W/Ms =washing machines; NCs =air conditioners; EPBXs =electronics private branch exchanges; FAXs =facsimile machines

Source: Compiled from SEC (1989:1032, 1036, 1053, 1057,1067)

1988 408.9 581.7 367.1

1357.7

89.8 18.1 14.6

1.6 48.4

2.2 69.5 21.9 45.6 50.0 76.9

253.4 221.3 1840

81

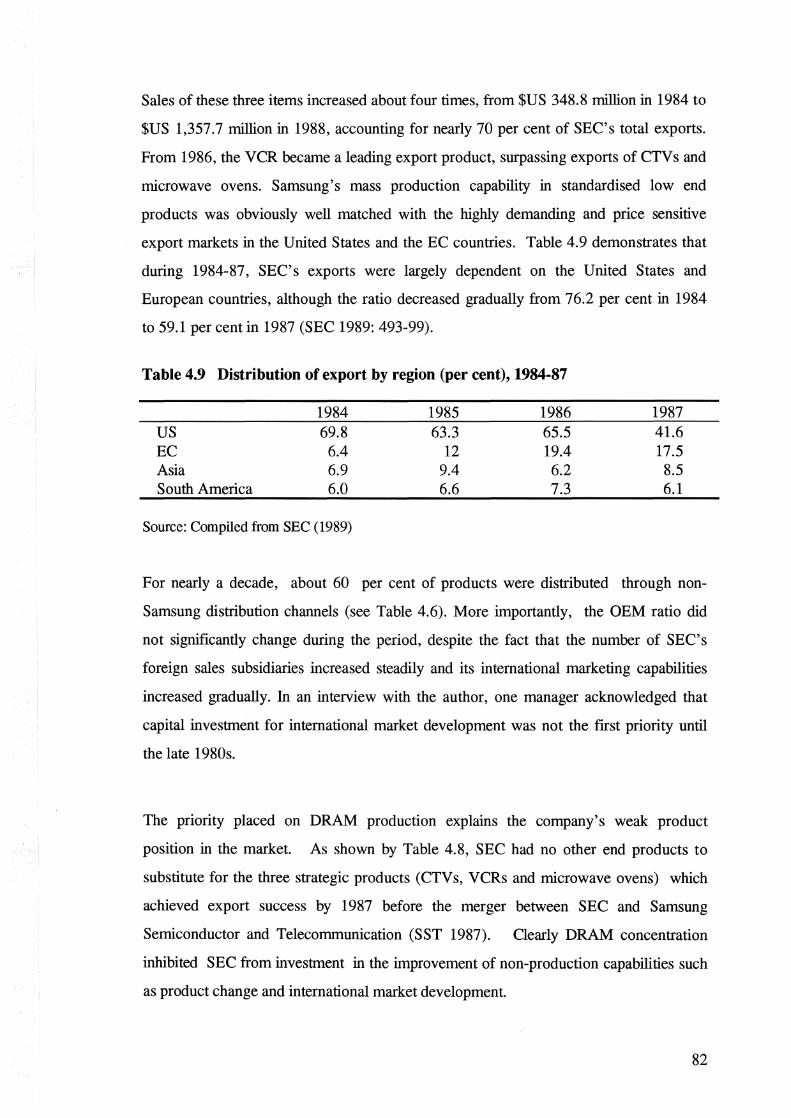

Sales of these three items increased about four times, from $US 348.8 million in 1984 to

$US 1,357.7 million in 1988, accounting for nearly 70 per cent of SEC's total exports.

From 1986, the VCR became a leading export product, surpassing exports of CTVs and

microwave ovens. Samsung 's mass production capability in standardised low end

products was obviously well matched with the highly demanding and price sensitive

export markets in the United States and the EC countries. Table 4.9 demonstrates that

during 1984-87, SEC's exports were largely dependent on the United States and

European countries, although the ratio decreased gradually from 76.2 per cent in 1984

to 59.1 per cent in 1987 (SEC 1989: 493-99).

Table 4.9 Distribution of export by region (per cent), 1984-87

1984 1985 1986 1987 us 69.8 63.3 65.5 41.6 EC 6.4 12 19.4 17.5 Asia 6.9 9.4 6.2 8.5 South America 6.0 6.6 7.3 6.1

Source: Compiled from SEC (1989)

For nearly a decade, about 60 per cent of products were distributed through non

Samsung distribution channels (see Table 4.6). More importantly, the OEM ratio did

not significantly change during the period, despite the fact that the number of SEC's

foreign sales subsidiaries increased steadily and its international marketing capabilities

increased gradually. In an interview with the author, one manager acknowledged that

capital investment for international market development was not the frrst priority until

the late 1980s.

The priority placed on DRAM production explains the company's weak product

position in the market. As shown by Table 4.8, SEC had no other end products to

substitute for the three strategic products (CTVs, VCRs and microwave ovens) which

achieved export success by 1987 before the merger between SEC and Samsung

Semiconductor and Telecommunication (SST 1987). Clearly DRAM concentration

inhibited SEC from investment in the improvement of non-production capabilities such

as product change and international market development.

82

DRAM production and profitability

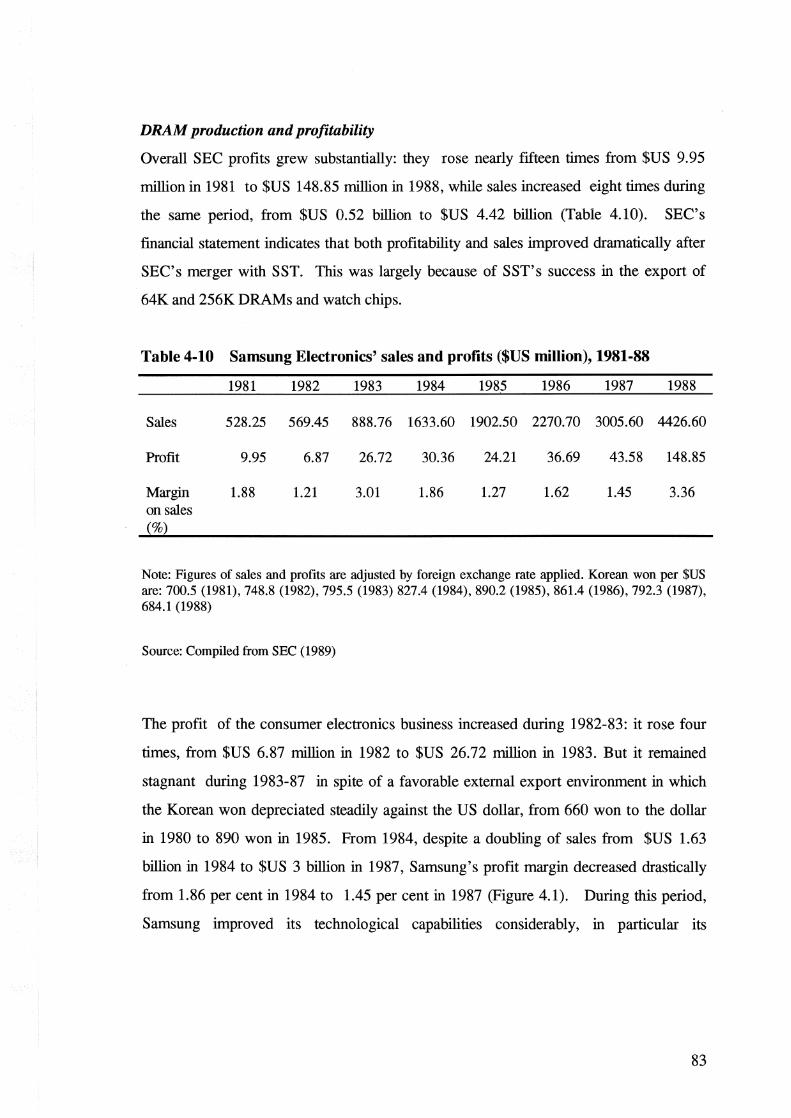

Overall SEC profits grew substantially: they rose nearly fifteen times from $US 9.95

million in 1981 to $US 148.85 million in 1988, while sales increased eight times during

the same period, from $US 0.52 billion to $US 4.42 billion (Table 4.10). SEC's

financial statement indicates that both profitability and sales improved dramatically after

SEC's merger with SST. This was largely because of SST's success in the export of

64K and 256K DRAMs and watch chips.

Table 4-10 Samsung Electronics' sales and profits ($US million), 1981-88

1981 1982 1983 1984 1985 1986 1987 1988

Sales 528.25 569.45 888.76 1633.60 1902.50 2270.70 3005.60 4426.60

Profit 9.95 6.87 26.72 30.36 24.21 36.69 43.58 148.85

Margin 1.88 1.21 3.01 1.86 1.27 1.62 1.45 3.36 on sales (%)

Note: Figures of sales and profits are adjusted by foreign exchange rate applied. Korean won per $US are: 700.5 (1981), 748.8 (1982), 795.5 (1983) 827.4 (1984), 890.2 (1985), 861.4 (1986), 792.3 (1987), 684.1 (1988)

Source: Compiled from SEC (1989)

The profit of the consumer electronics business increased during 1982-83: it rose four

times, from $US 6.87 million in 1982 to $US 26.72 million in 1983. But it remained

stagnant during 1983-87 in spite of a favorable external export environment in which

the Korean won depreciated steadily against the US dollar, from 660 won to the dollar

in 1980 to 890 won in 1985. From 1984, despite a doubling of sales from $US 1.63

billion in 1984 to $US 3 billion in 1987, Samsung' s profit margin decreased drastically

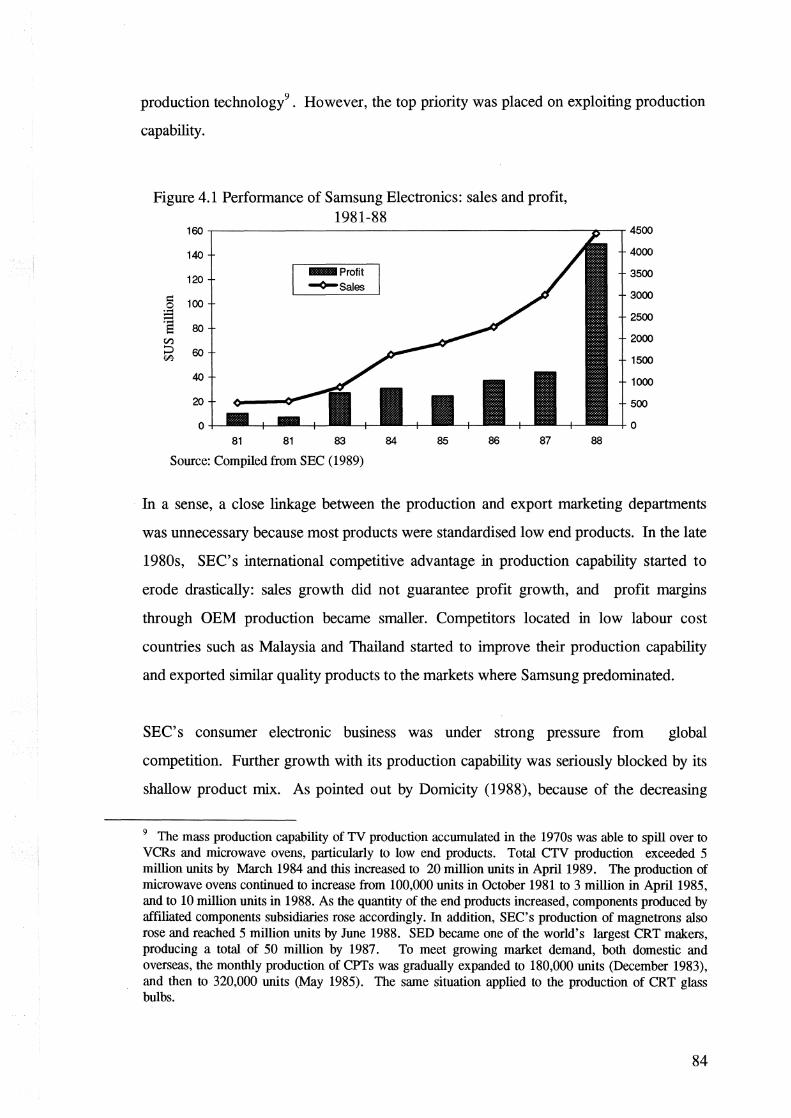

from 1.86 per cent in 1984 to 1.45 per cent in 1987 (Figure 4.1). During this period,

Samsung improved its technological capabilities considerably, in particular its

83

production technology9 • However, the top priority was placed on exploiting production

capability.

Figure 4.1 Performance of Samsung Electronics: sales and profit, 1981-88

160

140

120 -Profit ~Sales

§ ;.::I - 100

·s 80 tr.l :::::> 60 """'

40

20

0 81 81 83 84 85 86 87

Source: Compiled from SEC (1989)

4500

4000

3500

3000

2500

2000

1500

1000

500

0 88

In a sense, a close linkage between the production and export marketing departments

was unnecessary because most products were standardised low end products. In the late

1980s, SEC's international competitive advantage in production capability started to

erode drastically: sales growth did not guarantee profit growth, and profit margins

through OEM production became smaller. Competitors located in low labour cost

countries such as Malaysia and Thailand started to improve their production capability

and exported similar quality products to the markets where Samsung predominated.

SEC's consumer electronic business was under strong pressure from global

competition. Further growth with its production capability was seriously blocked by its

shallow product mix. As pointed out by Domicity (1988), because of the decreasing

9 The mass production capability of TV production accumulated in the 1970s was able to spill over to VCRs and microwave ovens, particularly to low end products. Total CTV production exceeded 5 million units by March 1984 and this increased to 20 million units in April 1989. The production of microwave ovens continued to increase from 100,000 units in October 1981 to 3 million in April1985, and to 10 million units in 1988. As the quantity of the end products increased, components produced by affiliated components subsidiaries rose accordingly. In addition, SEC's production of magnetrons also rose and reached 5 million units by June 1988. SED became one of the world's largest CRT makers, producing a total of 50 million by 1987. To meet growing market demand, both domestic and overseas, the monthly production of CPTs was gradually expanded to 180,000 units (December 1983), and then to 320,000 units (May 1985). The same situation applied to the production of CRT glass bulbs.

84

profitability of its three strategic products, SEC as a holding company in the electronic

business required new products for further sales growth. Computers and DRAM

products suited SEC's requirements as their export growth was just beginning (as

shown in Table 4.9). Following the merger with SST, SEC was able to improve its

profitability.

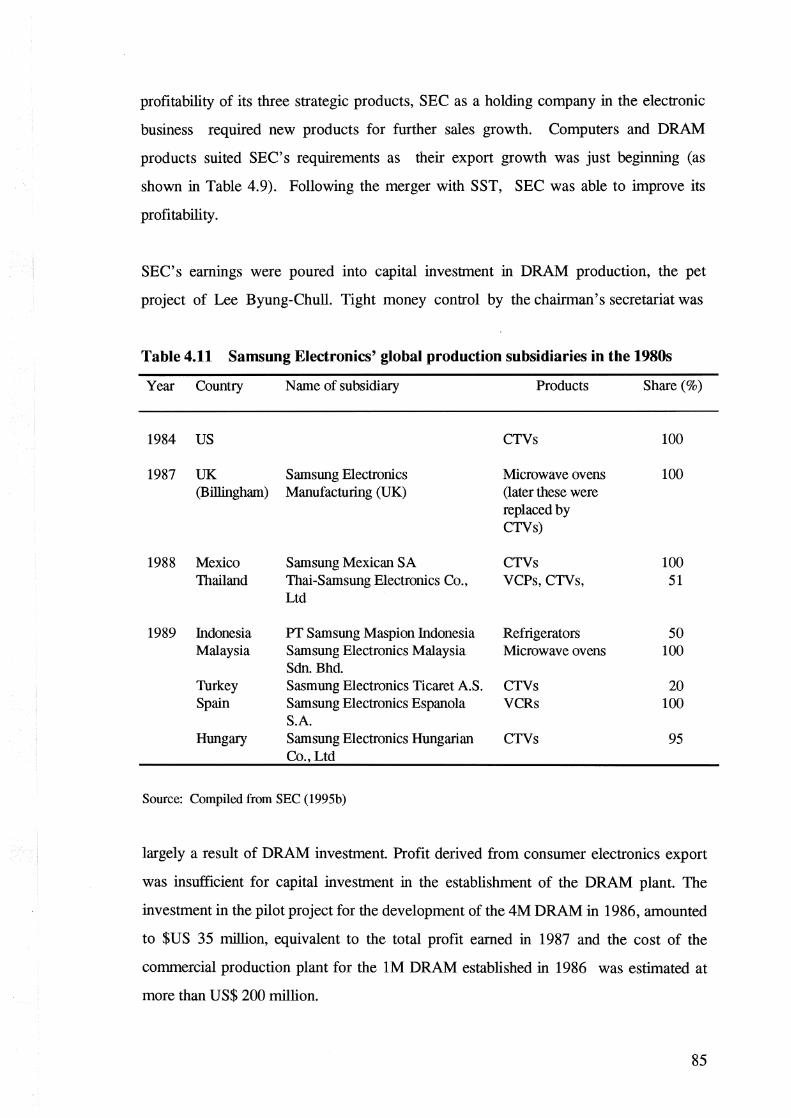

SEC's earnings were poured into capital investment in DRAM production, the pet

project of Lee Byung-Chull. Tight money control by the chairman's secretariat was

Table 4.11 Samsung Electronics' global production subsidiaries in the 1980s

Year Country Name of subsidiary Products Share(%)

1984 us CTVs 100

1987 UK Sarnsung Electronics Microwave ovens 100 (B illingharn) Manufacturing (UK) (later these were

replaced by CTVs)

1988 Mexico Sarnsung Mexican SA CTVs 100 Thailand Thai-Sarnsung Electronics Co., VCPs, CTVs, 51

Ltd

1989 Indonesia PT Sarnsung Maspion Indonesia Refrigerators 50 Malaysia Sarnsung Electronics Malaysia Microwave ovens 100

Sdn. Bhd. Turkey Sasmung Electronics Ticaret A.S. CTVs 20 Spain Sarnsung Electronics Espanola VCRs 100

S.A. Hungary Sarnsung Electronics Hungarian CTVs 95

Co., Ltd

Source: Compiled from SEC (1995b)

largely a result of DRAM investment. Profit derived from consumer electronics export

was insufficient for capital investment in the establishment of the DRAM plant. The

investment in the pilot project for the development of the 4M DRAM in 1986, amounted

to $US 35 million, equivalent to the total profit earned in 1987 and the cost of the

commercial production plant for the 1M DRAM established in 1986 was estimated at

more than US$ 200 million.

85

SEC only directed a small proportion of its sales profits towards R&D: 3.8 per cent in

1987 and 3.5 per cent in 1988. This was far below the R&D investment of its Japanese

counterparts, whose ratios amounted to 7.9 per cent for Matsushita in 1989 and 7.6 per

cent for Toshiba in the same year (Koh 1992). The postponement of improving product

change capability in the 1980s because of concentration on the DRAM burdened SEC and

this has continued to be a constraint on expansion through international production and

foreign subsidiaries' performance in the late 1980s and 1990s. This will be discussed in

Chapters 6 and 7.

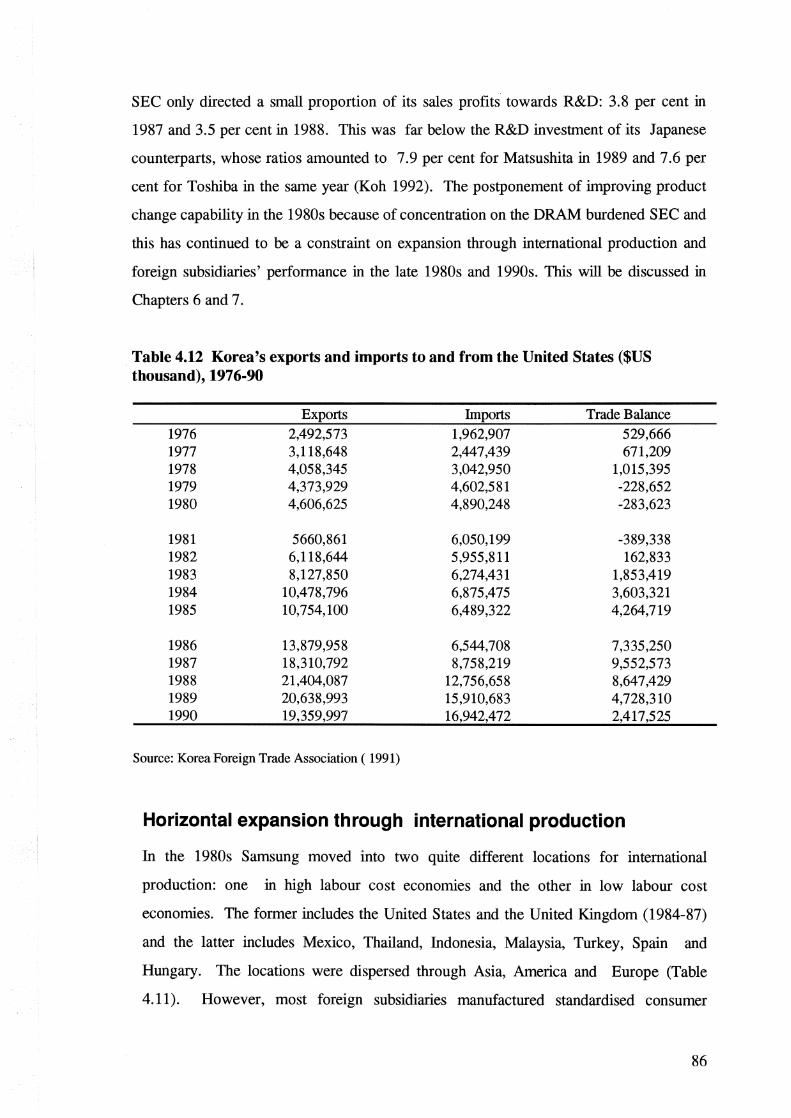

Table 4.12 Korea's exports and imports to and from the United States ($US thousand), 1976-90

Exports Imports Trade Balance 1976 2,492,573 1,962,907 529,666 1977 3,118,648 2,447,439 671,209 1978 4,058,345 3,042,950 1,015,395 1979 4,373,929 4,602,581 -228,652 1980 4,606,625 4,890,248 -283,623

1981 5660,861 6,050,199 -389,338 1982 6,118,644 5,955,811 162,833 1983 8,127,850 6,274,431 1,853,419 1984 10,478,796 6,875,475 3,603,321 1985 10,754,100 6,489,322 4,264,719

1986 13,879,958 6,544,708 7,335,250 1987 18,310,792 8,758,219 9,552,573 1988 21,404,087 12,756,658 8,647,429 1989 20,638,993 15,910,683 4,728,310 1990 19,359,997 16,942,472 2,417,525

Source: Korea Foreign Trade Association ( 1991)

Horizontal expansion through international production

In the 1980s Samsung moved into two quite different locations for international

production: one in high labour cost economies and the other in low labour cost

economies. The former includes the United States and the United Kingdom (1984-87)

and the latter includes Mexico, Thailand, Indonesia, Malaysia, Turkey, Spain and

Hungary. The locations were dispersed through Asia, America and Europe (Table

4.11). However, most foreign subsidiaries manufactured standardised consumer

86

products such as CTV s, microwave ovens and VCRs, for which Samsung had

accumulated technological capabilities since the late 1970s. This type of foreign

investment is a kind of horizontal diversification overseas.

Increasing trade barriers in the US and the EC

The second oil shock and domestic political umest in the late 1970s caused Korea to incur

. a bilateral trade deficit with the United States for three consecutive years (1979-81)

(Table 4.12). After 1982, Korea's trade surplus increased more than ten times, from

$US 0.16 billion in 1982, to $US 18.5 billion in 1983. At the same time Korea's CTV

exports to the United States rose rapidly, from 630,000 sets to 1,900,000 sets during the

same period. As the voluntary export restraint was lifted, they grew more than three

times during 1982-83 (Table 4.13).

As a consequence, in May 1983 dumping charges were filed on Korean made CTVs by

General Electric, and preliminary anti-dumping duties were imposed on three electronics

companies: 3.87 per cent for Goldstar, 3.05 per cent for Samsung and 1.77 per cent for

Daewoo. In February 1984 these duties suddenly increased to an average of 13.9 per

cent, and in September they rose further to 32.5 per cent, although they eventually settled

at 10.65 per cent in December (Park 1986).

Table 4.13 Korean CTV exports (thousand units), 1980-85

1980 1981 1982 1983 1984 1985 Total (A) n.a n.a 1,107 2,499 2,959 2,826 US market(B) 381 553 630 1,933 2,002 1,705 B/A% 60 77 68 60

Source: Electronics Industry Association of Korea, various years

Subsequently, the US trade barriers were further extended to CTV components such as

colour picture tubes and printed circuit boards. In November 1986, the US government

imposed anti-dumping tariffs on all CPTs and PCB products that had been imported

from January 1984. Samsung and Goldstar referred this to the Court of International

Trade, but they eventually failed in their efforts against the US measure (EIAK 1989:

249).

87

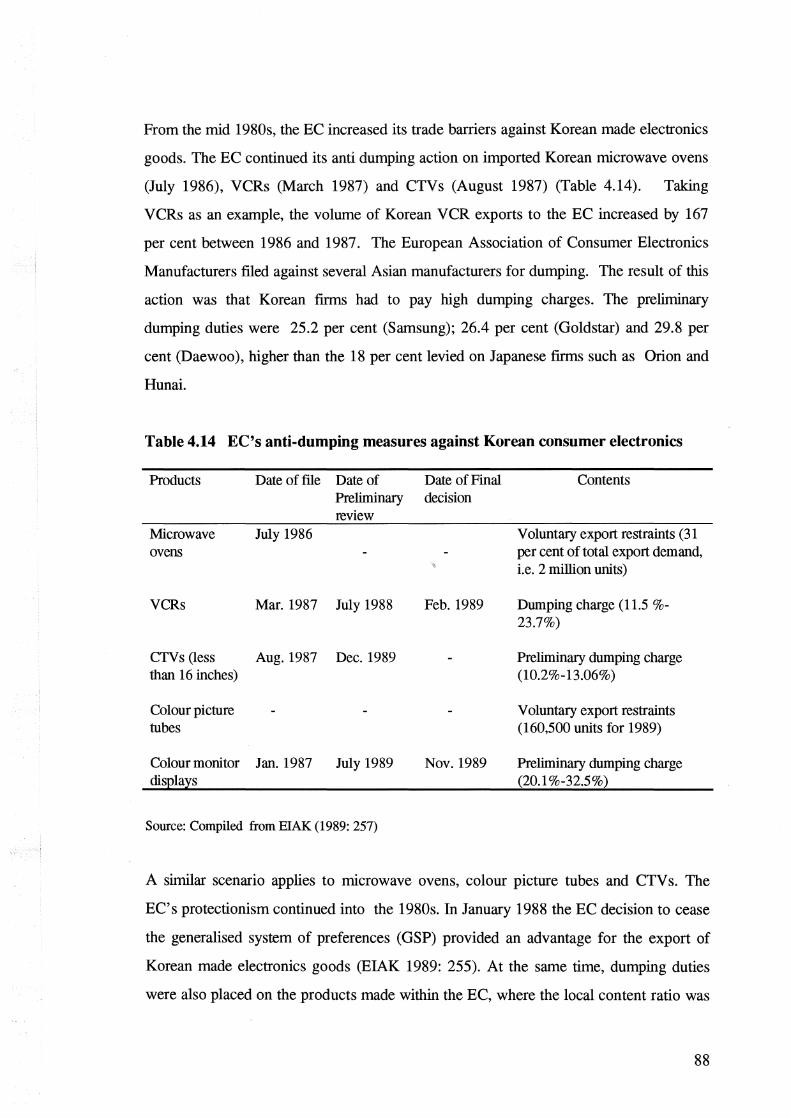

From the mid 1980s, the EC increased its trade barriers against Korean made electronics

goods. The EC continued its anti dumping action on imported Korean microwave ovens

(July 1986), VCRs (March 1987) and CTVs (August 1987) (Table 4.14). Taking

VCRs as an example, the volume of Korean VCR exports to the EC increased by 167

per cent between 1986 and 1987. The European Association of Consumer Electronics

Manufacturers filed against several Asian manufacturers for dumping. The result of this

action was that Korean firms had to pay high dumping charges. The preliminary

dumping duties were 25.2 per cent (Samsung); 26.4 per cent (Goldstar) and 29.8 per

cent (Daewoo), higher than the 18 per cent levied on Japanese firms such as Orion and

Hunai.

Table4.14 EC's anti-dumping measures against Korean consumer electronics

Products Date of :file Date of Date of Final Contents Preliminary decision review

Microwave July 1986 Voluntary export restraints (31 ovens per cent of total export demand, .,.

i.e. 2 million units)

VCRs Mar. 1987 July 1988 Feb. 1989 Dumping charge (11.5 %-23.7%)

CTVs (less Aug. 1987 Dec. 1989 Preliminary dumping charge than 16 inches) (10.2%-13.06%)

Colour picture Voluntary export restraints tubes (160,500 units for 1989)

Colour monitor Jan. 1987 July 1989 Nov. 1989 Preliminary dumping charge displays (20.1 %-32.5%)

Source: Compiled from EIAK (1989: 257)

A similar scenario applies to microwave ovens, colour picture tubes and CTV s. The

EC's protectionism continued into the 1980s. In January 1988 the EC decision to cease

the generalised system of preferences (GSP) provided an advantage for the export of

Korean made electronics goods (EIAK 1989: 255). At the same time, dumping duties

were also placed on the products made within the EC, where the local content ratio was

88

less than 40 per cent (Japan Economic Journal 28 January 1989). Thus, the so-called

'screw driver' type of international production was under strong pressure. As a

consequence, the UK based Samsung production subsidiary, established in 1987 and

mostly dependent on imported components from Korea, encountered serious problems.

SEC had to protect its existing export markets mostly in the US and EC.10

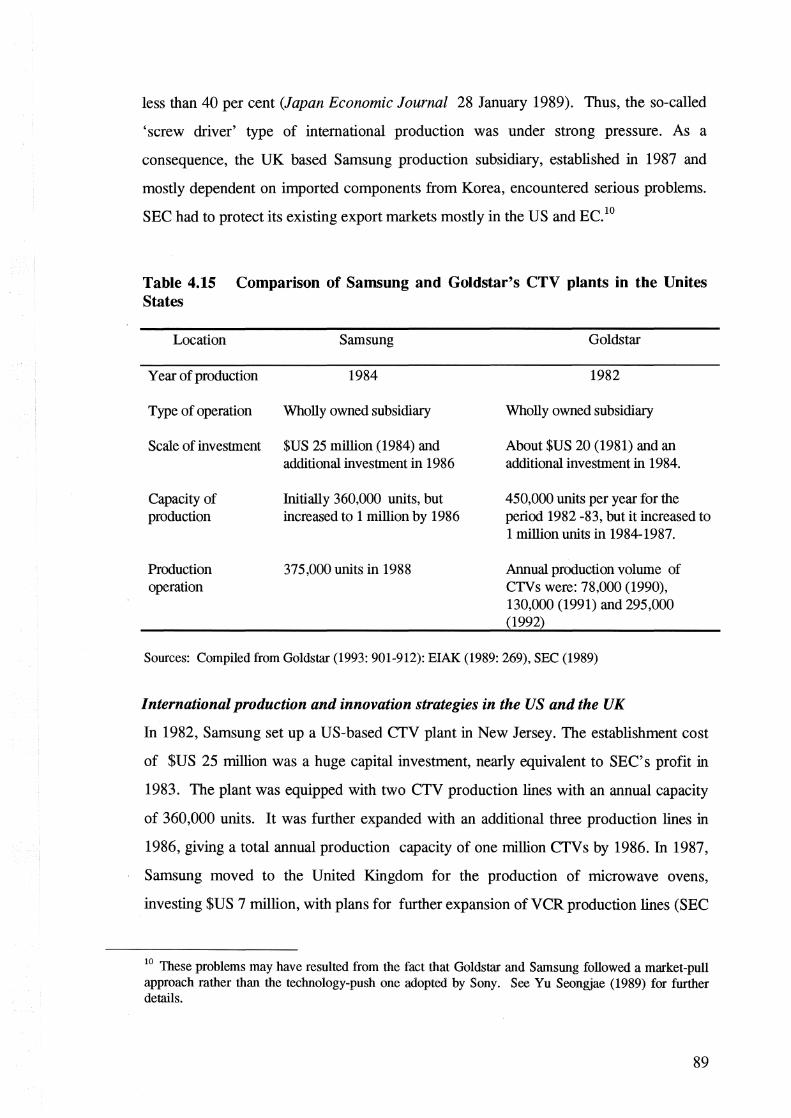

Table 4.15 Comparison of Samsung and Goldstar's CTV plants in the Unites States

Location

Year of production

Type of operation

Scale of investment

Capacity of production

Production operation

Sam sung

1984

Wholly owned subsidiary

$US 25 million .(1984) and additional investment in 1986

Initially 360,000 units, but increased to 1 million by 1986

375,000 units in 1988

Golds tar

1982

Wholly owned subsidiary

About $US 20 (1981) and an additional investment in 1984.

450,000 units per year for the period 1982 -83, but it increased to 1 million units in 1984-1987.

Annual production volume of CTVs were: 78,000 (1990), 130,000 (1991) and 295,000 (1992)

Sources: Compiled from Goldstar (1993: 901-912): EIAK (1989: 269), SEC (1989)

International production and innovation strategies in the US and the UK

In 1982, Samsung set up a US-based CTV plant in New Jersey. The establishment cost

of $US 25 million was a huge capital investment, nearly equivalent to SEC's profit in

1983. The plant was equipped with two CTV production lines with an annual capacity

of 360,000 units. It was further expanded with an additional three production lines in

1986, giving a total annual production capacity of one million CTVs by 1986. In 1987,

Samsung moved to the United Kingdom for the production of microwave ovens,

investing $US 7 million, with plans for further expansion of VCR production lines (SEC

10 These problems may have resulted from the fact that Goldstar and Samsung followed a market-pull approach rather than the technology-push one adopted by Sony. See Yu Seongjae (1989) for further details.

89

1989: 515). In October 1987, it started production with a capacity of 150,000 per

annum.

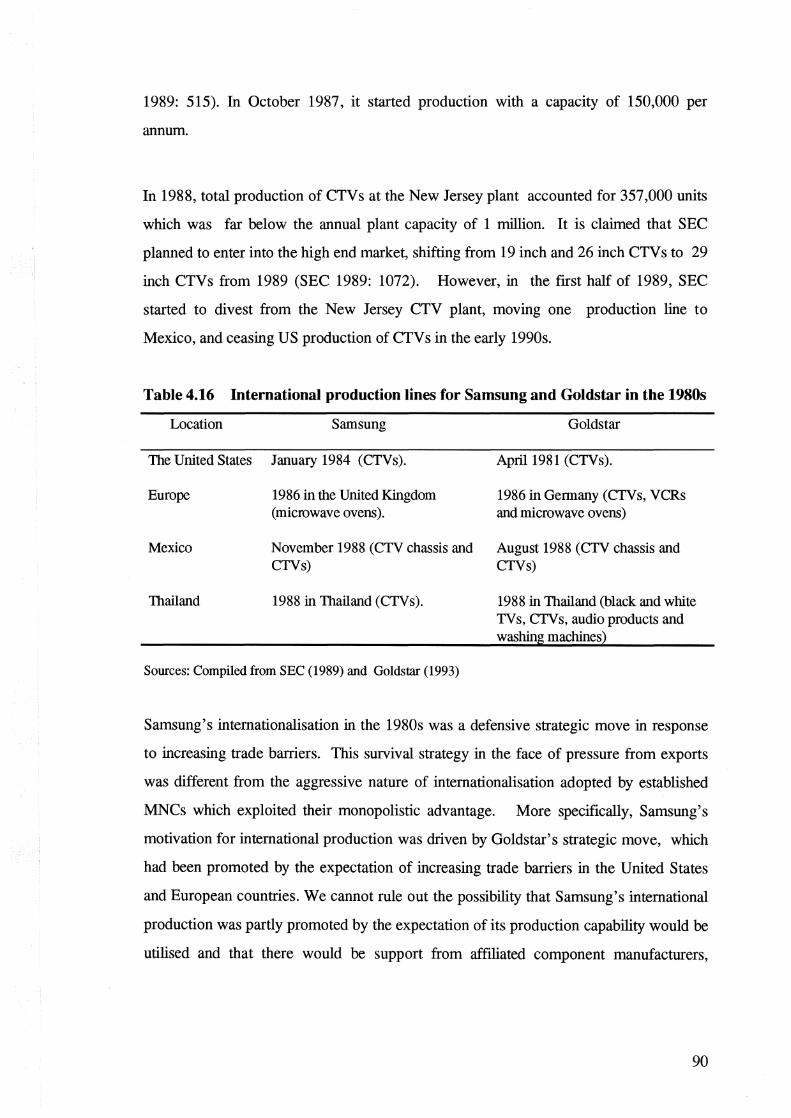

In 1988, total production of CTVs at the New Jersey plant accounted for 357,000 units

which was far below the annual plant capacity of 1 million. It is claimed that SEC

planned to enter into the high end market, shifting from 19 inch and 26 inch CTVs to 29

inch CTVs from 1989 (SEC 1989: 1072). However, in the first half of 1989, SEC

started to divest from the New Jersey CTV plant, moving one production line to

Mexico, and ceasing US production of CTV s in the early 1990s.

Table 4.16 International production lines for Samsung and Goldstar in the 1980s

Location Samsung

The United States January 1984 (CTVs).

Europe 1986 in the United Kingdom (microwave ovens).

Mexico November 1988 (CTV chassis and CTVs)

Thailand 1988 in Thailand (CTVs).

Sources: Compiled from SEC (1989) and Goldstar (1993)

Golds tar

April1981 (CTVs).

1986 in Germany (CTVs, VCRs and microwave ovens)

August 1988 (CTV chassis and CTVs)

1988 in Thailand (black and white TVs, CTVs, audio products and washing machines)

Samsung's internationalisation in the 1980s was a defensive strategic move in response

to increasing trade barriers. This survival strategy in the face of pressure from exports

was different from the aggressive nature of internationalisation adopted by established

MNCs which exploited their monopolistic advantage. More specifically, Samsung's

motivation for international production was driven by Goldstar' s strategic move, which

had been promoted by the expectation of increasing trade barriers in the United States

and European countries. We cannot rule out the possibility that Samsung's international

production was partly promoted by the expectation of its production capability would be

utilised and that there would be support from affiliated component manufacturers,

90

whose production capability would provide SEC with low price and relatively good

quality standardised components.

Moreover, Samsung's organisational culture, that of the calculated risk-taker, also

influenced the way it organised foreign investment projects. The investment in the

United States was undertaken after a certain degree of international management

experience had been gained through the Portugal-based CTV joint venture. It should

also be remembered that Golds tar's operation in Alabama had started production in

1982 and had begun to be profitable from 1983. At the last minute, Samsung set up a

US-based CTV plant in 1984, soon after a dumping charge was filed on CTVs imported

from Korean plants.

Samsung's scale of investment was similar to Goldstar's (see Table 4.15). In 1987

similar strategic behaviour drove the firm's investment in the United Kingdom. In late

1986, in the expectation of increasing EC protectionism, Goldstar moved to Germany to

produce CTVs and VCRs. A couple of months later, Samsung established aUK-based

microwave oven plant

Samsung set up the New Jersey-based CTV plant under technologically critical

conditions. Its technological capabilities were very vulnerable, and it had to cope with

external pressure from the United States. Moreover, the failure to establish affiliated

component suppliers inhibited SEC from local component sourcing. There was a plan in

which SED would set up a CPT plant in the United States (SEC 1989), but this was not

realised.

The competitiveness of Samsung's CTV products in the United States decreased

drastically. The real cost of production in the United States was higher than in Korea.

The only benefit was the saving in import tax. Samsung's competitiveness was based on

mass production of easily imitated products. Samsung's products had not been

supported by 'difficult-to-imitate capability' such as product change capability. Neither

was SEC-Korea, the parent company, able to assist with product change capability.

Samsung' s major concern at that time was to ensure the success of its DRAM business.

91

SEC-Korea was more centred on the exploitation of production capability, that is, the

commercialisation of its manufacturing capability in VCR and microwave oven

production, than on improving capabilities in product change, strategic marketing,

international management and linkage with local component suppliers. Sarnsung's

international venture was apparently successful for the first two years of operation, so,

like Goldstar, SEC expanded its plant with additional capacity. The subsidiary could not

survive, however, with the payment of anti-dumping tariffs on CPTs and PCBs.

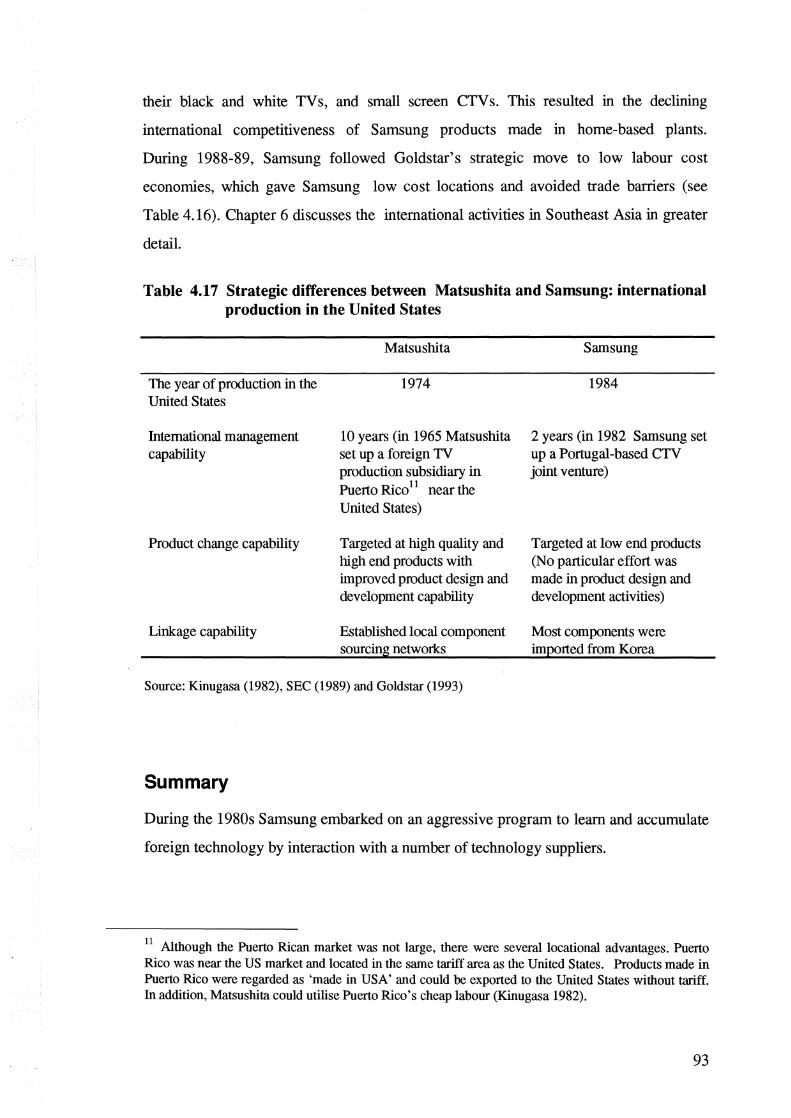

Samsung 's strategy for the process of building capabilities was different from

Matsushita's. Matsushita had strengthened its product change capability before

launching its US-based CTV project in 1974. Matsushita's objective was to serve its

US customers with high end and high quality products (Kinugasa 1982), while

Samsung' s prime objective was to sell low end and low quality products to the US

market in contrast to Matsushita (Table 4.17). Matsushita could quickly transfer its

accumulated product development capability to the US plant. Similarly, local links with

component suppliers were forged at the right time.

Investment during 1988-89

Following the unsuccessful operation of Sarnsung's two plants in the United States and

the United Kingdom, Samsung looked for other locations for international

production. At the same time SEC encountered cost pressures due to the appreciation of

the Korean won and wage increases from the mid 1980s.

Accordingly, profitability gradually decreased. In the late 1980s Samsung, one of the

world's biggest producers of TV sets, microwave ovens, VCRs and colour picture

tubes, was under continuous pressure at the low end of its market from Japanese

offshore plants in Southeast Asia Japanese firms were developing better products and

manufacturing them in lower wage Southeast Asian countries (Far Eastern Economic

Review 30 May 1991).

The quality and price of products made in the Southeast Asia was better than Korean

made goods. Even Chinese manufacturers started to enter the television market, with

92

their black and white TV s, and small screen CTV s. This resulted in the declining

international competitiveness of Samsung products made in home-based plants.

During 1988-89, Samsung followed Goldstar's strategic move to low labour cost

economies, which gave Samsung low cost locations and avoided trade barriers (see

Table 4.16). Chapter 6 discusses the international activities in Southeast Asia in greater

detail.

Table 4.17 Strategic differences between Matsushita and Samsung: international production in the United States

The year of production in the United States

International management capability

Product change capability

Linkage capability

Matsushita

1974

10 years (in 1965 Matsushita set up a foreign TV production subsidiary in Puerto Rico11 near the United States)

Targeted at high quality and high end products with improved product design and development capability

Established local component sourcing networks

Source: Kinugasa (1982), SEC (1989) and Goldstar (1993)

Summary

Sam sung

1984

2 years (in 1982 Samsung set up a Portugal-based CTV joint venture)

Targeted at low end products (No particular effort was made in product design and development activities)

Most components were imported from Korea

During the 1980s Samsung embarked on an aggressive program to learn and accumulate

foreign technology by interaction with a number of technology suppliers.

11 Although the Puerto Rican market was not large, there were severallocational advantages. Puerto Rico was near the US market and located in the same tariff area as the United States. Products made in Puerto Rico were regarded as 'made in USA' and could be exported to the United States without tariff. In addition, Matsushita could utilise Puerto Rico's cheap labour (Kinugasa 1982).

93

Adopting a slightly different approach, Samsung learnt more sophisticated DRAM

technology in the 1980s than it had in the 1970s. This was a dynamic technological

capability building process, which capitalised on the previously accumulated production

capability in the 1970s. Samsung established foreign-based technology laboratories to

seek information, recruit overseas Korean scientists and train home-based scientists,

while simultaneously learning and developing technological capabilities through in-house

R&D institutes in Korea.

Samsung's strength lay in its mass production capability, but its weaknesses were a lack

of product change capability requiring improved design and product development, as

well as international management and strategic marketing capabilities. These weaknesses

directly or indirectly derived from a high dependency on OEM arrangements as well as a

concentration on DRAM production.

As Samsung's overall technological capabilities improved (mostly in mass production

capability), international production was geographically diverse, from Portugal to the

United States, the United Kingdom, Thailand and Mexico. Externally, increasing trade

barriers in the United States and Europe continuously pushed Samsung toward

internationalisation despite its immature technological capabilities. International

production by Samsung followed Goldstar' s lead in an attempt to defend its established

export markets. This also reflected the risk-averse nature of Samsung's established

organisational culture. Thus, internationalisation proceeded reluctantly featuring a

process of transferring and exploiting production capability - which only provided a

temporary competitive advantage.

This temporary competitive advantage in production capability was an 'easy-to-imitate

capability' which was short-lived in the foreign locations in which Samsung operated. In

addition, Samsung failed to establish a strong production network position through

local linkages with affiliated component suppliers of SEM and SED. These eventually

led to Samsung's failure in its international operations in the United States and the

United Kingdom during the 1980s.

94

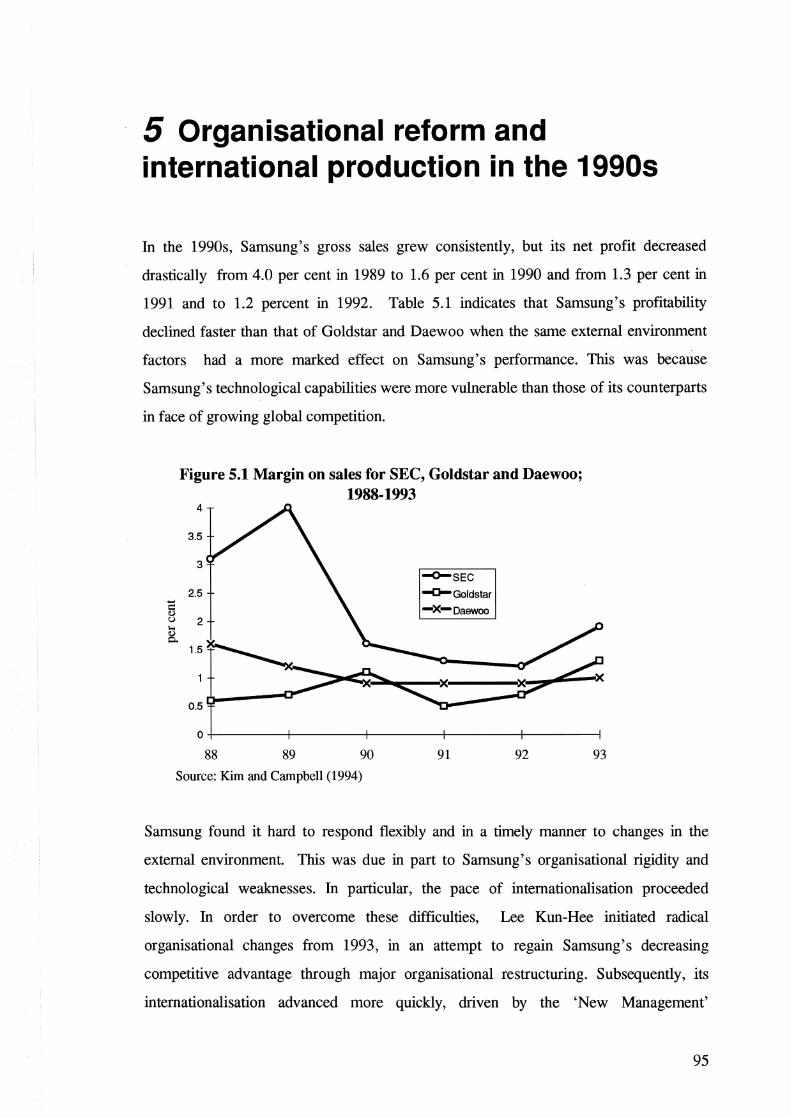

5 Organisational reform and international production in the 1990s

In the 1990s, Samsung's gross sales grew consistently, but its net profit decreased

drastically from 4.0 per cent in 1989 to 1.6 per cent in 1990 and from 1.3 per cent in

1991 and to 1.2 percent in 1992. Table 5.1 indicates that Samsung's profitability

declined faster than that of Goldstar and Daewoo when the same external environment

factors had a more marked effect on Samsung' s performance. This was because

Samsung's technological capabilities were more vulnerable than those of its counterparts

in face of growing global competition.

..... 5 (.)

as p,

Figure 5.1 Margin on sales for SEC, Goldstar and Daewoo; 1988-1993

4

3.5

3 ~SEC

2.5 ~Goldstar

-x-oaewoo 2

1.5

0.5

0+--------r------~--------+--------r------~

88 89 90 91 92 93

Source: Kim and Campbell (1994)

Samsung found it hard to respond flexibly and in a timely manner to changes in the

external environment. This was due in part to Samsung's organisational rigidity and

technological weaknesses. In particular, the pace of internationalisation proceeded

slowly. In order to overcome these difficulties, Lee Kun-Hee initiated radical

organisational changes from 1993, in an attempt to regain Samsung's decreasing

competitive advantage through major organisational restructuring. Subsequently, its

internationalisation advanced more quickly, driven by the 'New Management'

95

!

movement. This chapter focuses on the relationship between Samsung' s organisational

reform and its accumulation and improvement of technological capabilities as well as its

international production process during the 1990s.

Table 5.1 Performance of Korean electronics companies, 1988-93

1988 1989 1990 1991 1992

Gross sales Sam sung 4,595 6,063 6,353 6,500 7,600 ($US million) Go1dstar 4,139 3,836 4,201 5023 4,787

Daewoo 1,621 1,765 1,846 2,357 2,182

Net profit Sam sung 148.8 233.4 102.8 106.8 94.4 ($US million) Go1dstar 26.6 26.5 47.4 25.2 33.4

Daewoo 26.0 20.5 18.2 18.5 20.9

Margin on Samsung 3.1 4.0 1.6 1.3 1.2 sales(%) Go1dstar 0.6 0.7 1.1 0.5 0.7

Daewoo 1.6 1.2 0.9 0.9 0.9

Return on Sam sung 6.2 6.5 2.4 1.7 1.8 investment Goldstar 1.0 -1.8 2.4 1.2 1.9 (%) Daewoo 1.8 1.4 0.9 0.9 0.9

Source: Company documents, cited by Kim and Campbell (1994)

A new competitive environment and major organisational change

Changes in the competitive environment

1993

10,100 5,337 2,473

190.8 81.0 47.8

1.9 1.3 1.0

5.6 3.0 1.4

Korean electronics firms have been aggressively involved in learning and knowledge

accumulation over the past two decades. They have continued to improve their

capabilities through learning-by-doing. In this way, Korean electronics products were

able to maintain a competitive advantage until the late 1980s. In the 1990s, some

significant changes occurred in the global electronics market. Demand growth in

markets in the United States and Europe slowed down remarkably while price

competition continues to play an important role (Ernst and O'Connor 1992). In

addition, access to foreign technology has become extremely difficult and the speed of

technological obsolescence has accelerated.

96

In particular, latecomer electronics firms found it more difficult to get access to frontier

technology, the access to technology discussed by Ernst (1997)1 and Ernst and

O'Connor (1992). Their competitiveness decreased remarkably except for components

such as DRAMs.

As explained in the Chapter 4, Samsung's technological capability was marked by an

imbalance between product and production. It had a relatively high capability in mass

production, but was very weak in product design and development. This is a legacy of

Samsung 's OEM production style in which product designs were provided by OEM

partners. When major global electronics firms entered the low end market where

latecomer electronics firms like Samsung had predominated nearly a decade,

competition was unavoidable between Samsung' s own brand products and those by

firms from industrialised countries.

During the early 1990s, Samsung's international competitiveness m consumer and

industrial electronics goods decreased. In spite of a good external climate characterised

by an appreciation of the yen and a depreciation of the won against US currency,

Samsung's competitive advantage in production capability gradually waned. In

particular, consumer and industrial electronics products incurred a huge loss in

international operations. This was in contrast to Samsung' s high performance in the

1970s and 1980s.

Major organisational change under 'New Management' movement

Samsung's new Chairman, Lee Kun-Hee perceived the need for change. In order to

respond to a rapidly changing external environment, two problems were perceived in the

management of Samsung: the use of central planning and internal auditing as a

mechanism to control the group affiliates, a problem which had been embedded in

1 Ernst (1997) observes that developing countries are confronted with a twofold challenge. It is difficult to acquire the public knowledge element of technology due to aggressive intellectual property right strategies and the proliferation of 'high-tech neo-mercantilism'. For Korean and Taiwanese firms, access to the public knowledge element of foreign technology has become increasingly difficult and costly, especially for new product designs and key components.

97

organisational culture during the late chairman, Lee Byung-Chull' s period; and a rigid

and bureaucratic organisational system on the topic of organisational culture (Choi

1995). Choi (1995 : 78) states that,

... the late Chairman recognised that importance of nurturing capable and hard-driving managers. In fact it was his philosophy that the survival of a company depends, most of all, on the quality of its managers. Sarnsung, thus, was the first private company in Korea to recruit employees by entrance examination in 1957. He also set up the chairman' secretariat to develop long-term plans and conduct internal audits. The company also monitored subsidiary performance very closely and encouraged good performers, but descended heavily on bad ones. To enhance the status of the best new recruits... he demanded absolute loyalty from them and guaranteed them a sure career path within the company in return.

Lee Kun-Hee believed that a 'volume-oriented growth' strategy, which was derived

from production capability with minor changes of product, production process and

organisational systems, was unlikely to be effective due to rapid changes of technology

and international market. Organisational reform in Samsung would entail major changes

because the 50-year-old organisational culture of the group which had grown under the

'profit centre' system encouraged a narrow, short-term approach.

The new chairman often raised with managers and senior executives the problems that

critically impeded Samsung from high performance and growth. At the same time, SEC

introduced minor changes in its organisation. For instance, in 1991, SEC set up a

strategic management section undertaking planning, intemationalisation and strategic

technology management in order to manage its complex organisations efficiently and

effectively (SEMM, August 1991). In December 1992, SEC integrated its multi

divisional business sectors, and appointed Kim Kwang-Ho as head of Samsung

Electronics (SMM, December 1992).

Although changes were imperative under the new competitive circumstances, the new

Chairman soon realised that employees became resistant to change and too reluctant to

take risky initiatives (Choi 1995). Lee Kun-Hee believed that it was not easy for the

habits of 50 years to be changed immediately, thus, unprecedented measures were used

to dislodge them. Changes were: the working hours of Samsung employees were

changed from 9 am to 7 pm, to 7 am to 4 pm; any worker at a production site was

98

empowered to stop the entire line if a defect was found; senior executives were asked

to spend at least half of their six-day week at factories, meeting suppliers and customers

instead of remaining behind their desks. In January 1993, SEC restructured its

organisation again because SEC needed to increase coordination between different

organisations in response to a rapidly changing international environment. The audio and

video business sectors were integrated and a technology management division was

newly established. (SEMM, January 1993).

From the beginning of 1993, Samsung began a radical organisational reform2 of its

management along the lines of its major Japanese counterparts (Table 5.3). In October

1994, Kim Kwang-Ho was appointed as head of the electronics sector, which includes

SEC and its subsidiaries including SED, SEM and SC. This was the first fully integrated

organisational structure since 1969 when Samsung entered the electronics industry.

Through the 'Frankfurt Declaration' in 1993, Lee Kun-Hee showed Samsung's senior

executive managers how much Samsung products lagged behind in terms of product

quality and international marketing3 • Explicitly, Lee Kun-Hee urged all Samsung

employees to reevaluate their roles. 'Change yourself first' became the prime slogan of

the 'New Management' movement. The New Management philosophy encompasses

the three major guiding principles of quality management4 , multifaceted integration5 and

globalisation6 •

2 The reform was initiated by Lee Kun-Hee, who was called the Samsung group's chief visionary officer and Kim Kwang-Ho, who supplied the vision and set the strategic goals (Business Times 19 February 1994).

3 Over a two month period, 850 senior executives were summoned in London, Los Angeles, Tokyo, Osaka, and Fukuoka in groups of 20 to 40 (Choi 1995: 79).

4 Samsung committed itself to producing high quality products. It adopted the line stop system in order to reduce the defect ratio of its products, based on a sense of individual responsibility and initiative (Samsung Homepage, WWW 1996).

5 Samsung aims to apply this concept to every field on many levels, including infrastructure, facilities, technology and information management. The objective is to maximise competitiveness and efficiency through consolidation of different elements. Samsung claims that unlike a traditional departmental configuration, multi-faceted integration brings organisations, people, infrastructure and facilities together (Samsung Homepage, WWW 1996).

6 Samsung's global strategy emphasises the expansion of overseas production facilities by means of joint ventures and foreign acquisition. Samsung claims that true globalisation requires mental, physical and cultural adaptation to the local environment (Samsung Homepage, WWW 1996).

99

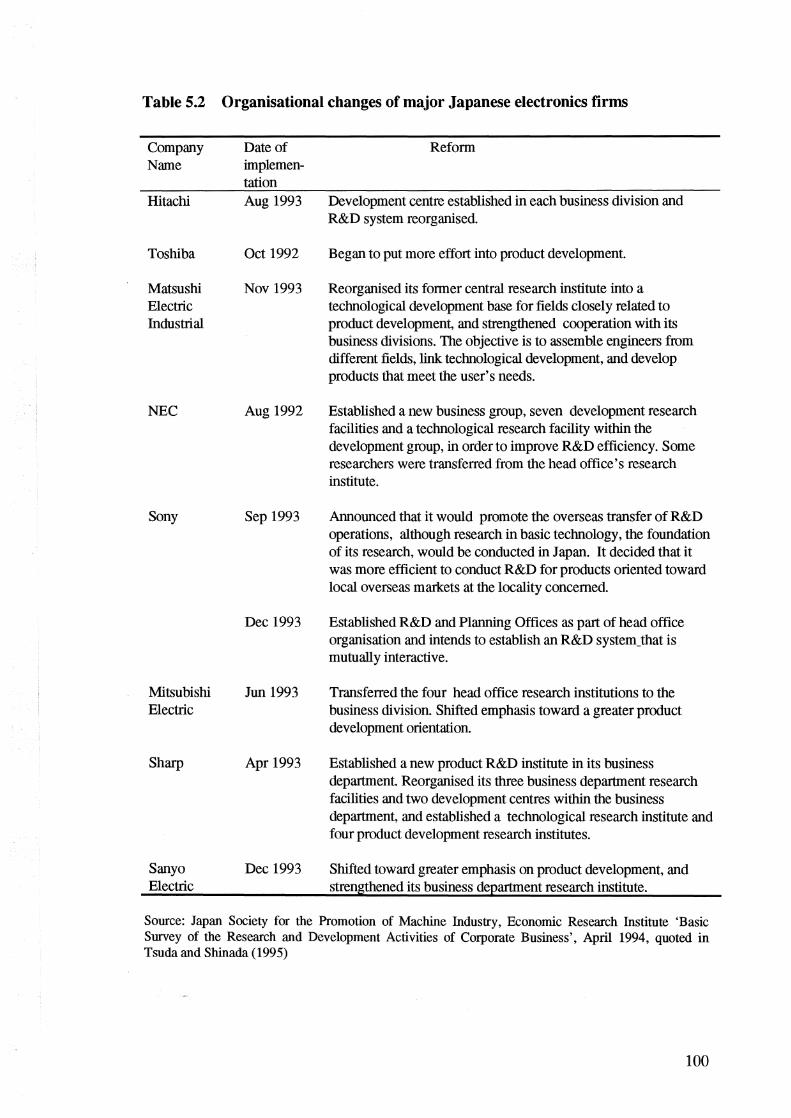

Table 5.2 Organisational changes of major Japanese electronics firms

Company Name

Hitachi

Toshiba

Matsushi Electric Industrial

NEC

Sony

Mitsubishi Electric

Sharp

Sanyo Electric

Date of implementation Aug 1993

Oct 1992

Nov 1993

Aug 1992

Sep 1993

Dec 1993

Jun 1993

Apr 1993

Dec 1993

Reform

Development centre established in each business division and R&D system reorganised.

Began to put more effort into product development.

Reorganised its former central research institute into a technological development base for fields closely related to product development, and strengthened cooperation with its business divisions. The objective is to assemble engineers from different fields, link technological development, and develop products that meet the user's needs.

Established a new business group, seven development research facilities and a technological research facility within the development group, in order to improve R&D efficiency. Some researchers were transferred from the head office's research institute.

Announced that it would promote the overseas transfer of R&D operations, although research in basic technology, the foundation of its research, would be conducted in Japan. It decided that it was more efficient to conduct R&D for products oriented toward local overseas markets at the locality concerned.

Established R&D and Planning Offices as part of head office organisation and intends to establish an R&D system_ that is. mutually interactive.

Transferred the four head office research institutions to the business division. Shifted emphasis toward a greater product development orientation.

Established a new product R&D institute in its business department. Reorganised its three business department research facilities and two development centres within the business department, and established a technological research institute and four product development research institutes.

Shifted toward greater emphasis on product development, and strengthened its business department research institute.

Source: Japan Society for the Promotion of Machine Industry, Economic Research Institute 'Basic Survey of the Research and Development Activities of Corporate Business', April 1994, quoted in Tsuda and Shinada (1995)

100

One thing which distinguishes Samsung's organisational reform from that of its

Japanese counterparts is that Samsung aimed at the establishment of a new and relevant

organisational culture necessary to adapt the changing competitive environment, while

Japanese firms stressed product innovation, development capability and

internationalisation of R&D activities (see Table 5.2). These different approaches

occurred at a time when both Samsung and Japanese firms were attempting to cope with