Embed Size (px)

Citation preview

1 1 1

KBank Capital Markets Perspectives 29 February 2016

Thailand’s economy steadied in February, though domestic demand decelerated

slightly from January after government’s stimulus measure concluded.

Foreigners’ demand to visit Thailand improved more broadly.

The increase in public servant salary and investment by state-enterprises helped

sustain the economic momentum.

The BoT revised down most of the economic indicators, as risks to growth remain

tilted towards the downside.

The economy is expected to be supported by public spending and the tourism

sector.

Domestic demand is expected to slow down to 1.8% against an earlier forecast of

2.8%.

Exports are expected to contract by 2%, as opposed to earlier forecast of 0%

growth.

Large current account surplus and weak domestic demand will keep Thailand’s

current account surplus afloat, hence, supporting for THB rise.

In the press conference, the BoT spokesperson said the MPC could lower rates

further if warranted.

As such, we expect the BoT to cut policy rate by 25bps in Q2/15 to 1.25%.

Disclaimer: For private circulation only. The foregoing is for informational purposes only and not to be considered as an offer to buy or sell, or a solicitation of an offer to buy or sell any security. Although the information herein was obtained from sources we believe to be reliable, we do not guarantee its accuracy nor do we assume responsibility for any error or mistake contained herein. Further information on the securities referred to herein may be obtained upon request.

Thailand Economic Monitor and BoT Forecast : March 2016

Nattariya Wittayatanaseth [email protected]

Anchali Singh [email protected]

2.8 2.9 3.0 3.2 3.4 3.53.2

-0.50.00.51.01.52.02.53.03.54.04.5

1Q14 3Q14 1Q15 3Q15 1Q16* 3Q16* 1Q17*

Real GDP (%YoY) Sep- 15 projection Dec- 15 projection Mar- 16 projection

% YoY

The BoT revised down GDP forecast

2

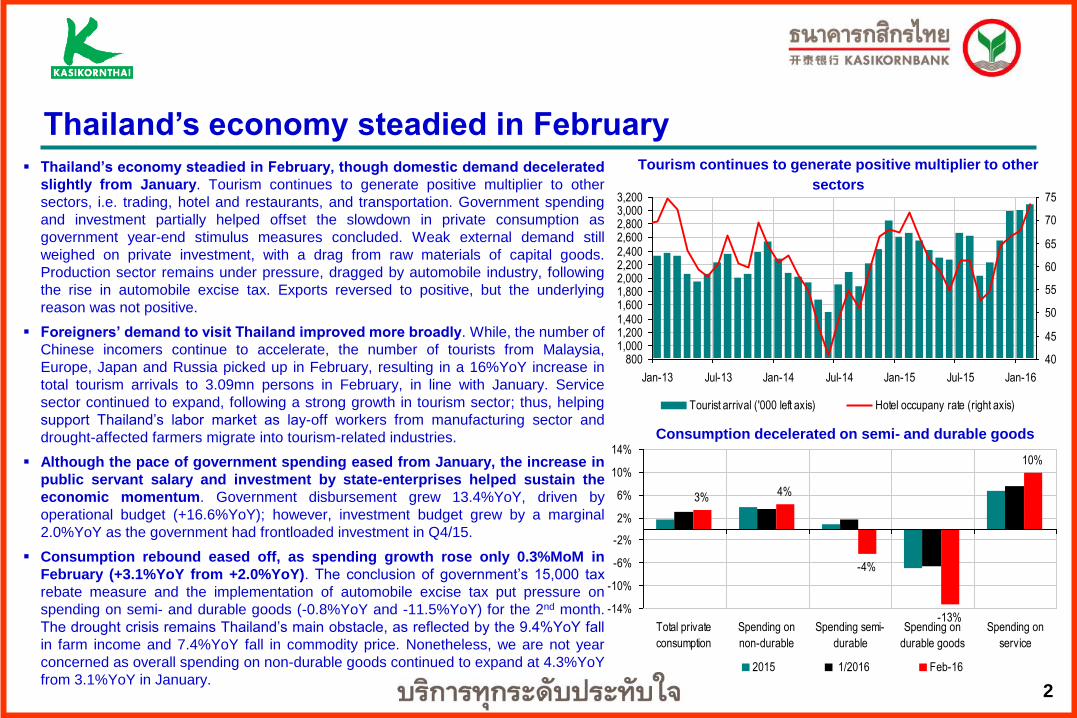

Thailand’s economy steadied in February, though domestic demand decelerated

slightly from January. Tourism continues to generate positive multiplier to other

sectors, i.e. trading, hotel and restaurants, and transportation. Government spending

and investment partially helped offset the slowdown in private consumption as

government year-end stimulus measures concluded. Weak external demand still

weighed on private investment, with a drag from raw materials of capital goods.

Production sector remains under pressure, dragged by automobile industry, following

the rise in automobile excise tax. Exports reversed to positive, but the underlying

reason was not positive.

Foreigners’ demand to visit Thailand improved more broadly. While, the number of

Chinese incomers continue to accelerate, the number of tourists from Malaysia,

Europe, Japan and Russia picked up in February, resulting in a 16%YoY increase in

total tourism arrivals to 3.09mn persons in February, in line with January. Service

sector continued to expand, following a strong growth in tourism sector; thus, helping

support Thailand’s labor market as lay-off workers from manufacturing sector and

drought-affected farmers migrate into tourism-related industries.

Although the pace of government spending eased from January, the increase in

public servant salary and investment by state-enterprises helped sustain the

economic momentum. Government disbursement grew 13.4%YoY, driven by

operational budget (+16.6%YoY); however, investment budget grew by a marginal

2.0%YoY as the government had frontloaded investment in Q4/15.

Consumption rebound eased off, as spending growth rose only 0.3%MoM in

February (+3.1%YoY from +2.0%YoY). The conclusion of government’s 15,000 tax

rebate measure and the implementation of automobile excise tax put pressure on

spending on semi- and durable goods (-0.8%YoY and -11.5%YoY) for the 2nd month.

The drought crisis remains Thailand’s main obstacle, as reflected by the 9.4%YoY fall

in farm income and 7.4%YoY fall in commodity price. Nonetheless, we are not year

concerned as overall spending on non-durable goods continued to expand at 4.3%YoY

from 3.1%YoY in January.

Thailand’s economy steadied in February

Consumption decelerated on semi- and durable goods

Tourism continues to generate positive multiplier to other

sectors

8001,0001,2001,4001,6001,8002,0002,2002,4002,6002,8003,0003,200

Jan-13 Jul-13 Jan-14 Jul-14 Jan-15 Jul-15 Jan-16

40

45

50

55

60

65

70

75

Tourist arrival ('000 left axis) Hotel occupany rate (right axis)

3% 4%

-4%

-13%

10%

-14%

-10%

-6%

-2%

2%

6%

10%

14%

Total private

consumption

Spending on

non-durable

Spending semi-

durable

Spending on

durable goods

Spending on

service

2015 1/2016 Feb-16

3

Private investment decelerated to 2.0%YoY in February from 3.1%YoY, as car sales

declined 5.1%YoY. Nonetheless, the drag was completely offset by 4G infrastructure

investment in telecommunication sector. Government investment projects also

benefitted construction material which managed to grow 1.7%YoY for the first time since

2015. However, we have not seen clear sign of private investment recovery due to weak

domestic demand and low business confidence. Moreover, credit standards have

become tightened over recent periods, both for corporate and SMEs.

Weak demand and a slowdown in automobile production pushed production back

into negative territory. The MPI index declined 1.6%YoY following a 3.5%YoY fall in

January. Apart from waning automobile production, production of textile and garments,

and hard-disk drivers remained negative due to a shift in consumer demand towards

solid-state drive. The bright star for production was probably rubber as sellers

frontloaded exports before the agreement between Thailand, Malaysia, and Indonesia,

to limit rubber exports comes into effect in August.

The 6.2% rise in February exports was boosted by gold and jewelry in response to

Hong Kong International Jewellery Show and the sharp rise in gold price. However,

stripping off the impact of gold export which totaled to as much as USD 1.89bn, overall

exports contracted 4.0%YoY. Most products witnessed slower demand, especially

petroleum-related items, i.e. petrochemical and chemicals. The only products that saw

material improvement was sugar. Sugar demand surged as ASEAN countries who

expect the drought crisis will shore up sugar price.

Imports continued to post a double-digit drop, falling 16.3%YoY from a 17.8%YoY

fall with across the board weakness observed. The most concerning point was imports

of raw materials and intermediate goods fell sharply, suggesting that recovery in exports

remains dampened.

Current account surplus rose to a record high at USD 7.4bn, driven by trade

surplus, totaling USD 6.0bn in February. This resulted in net positive balance of

payment which partially explained THB strength in February; USD/THB averaged 35.16

in February from 36.15 in January.

Current account surplus rose to a record high Current account surged to record high due to trade surplus

Thailand’s February economic momentum steadied

-3.5

2.0 3.1

-9.3

-17.8

-1.6

3.1 2.0

6.2

-16.3

-24

-20

-16

-12

-8

-4

0

4

8

Manufacturing Consumption Investment Exports (USD) Imports (USD)

Nov-15 Dec-15 Jan-16 Feb-16

% YoY

1.8

-0.7

1.6

-0.6

0.40.9

1.5

-0.6

0.9

2.6

-0.5

2.3

0.3

1.5

0.4

2.6

1.91.4

2.3

0.4

3.3

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

Jun-14 Sep-14 Dec-14 Mar-15 Jun-15 Sep-15 Dec-15

Trade balance Trade balance, excluding gold

USD, bn

4

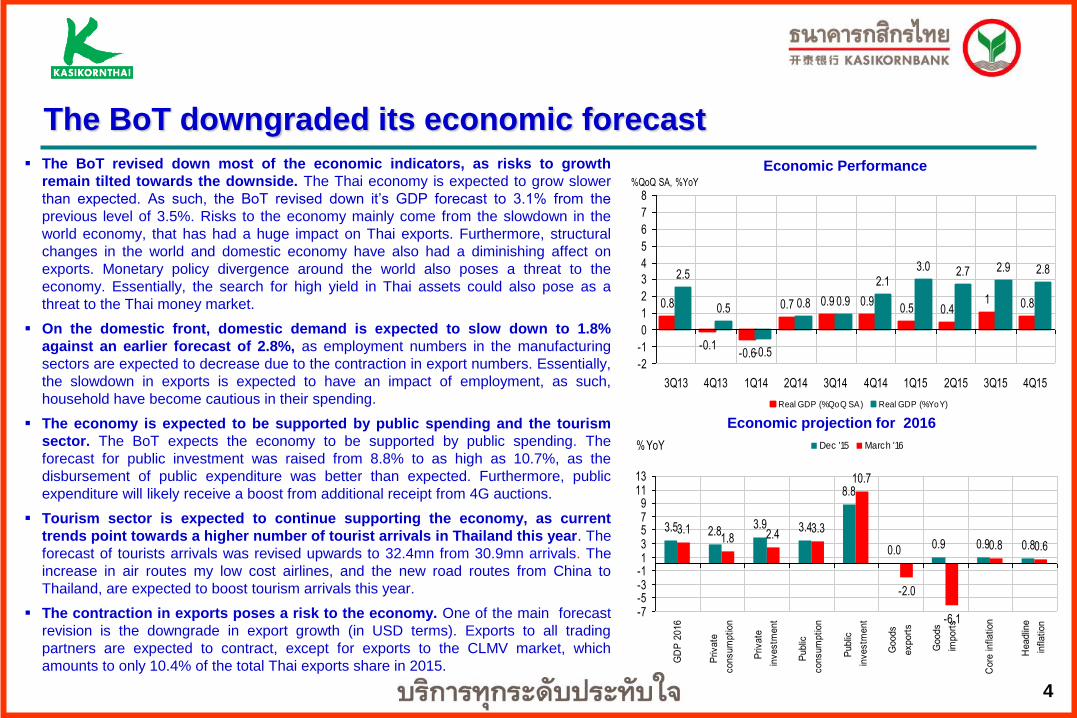

The BoT revised down most of the economic indicators, as risks to growth

remain tilted towards the downside. The Thai economy is expected to grow slower

than expected. As such, the BoT revised down it’s GDP forecast to 3.1% from the

previous level of 3.5%. Risks to the economy mainly come from the slowdown in the

world economy, that has had a huge impact on Thai exports. Furthermore, structural

changes in the world and domestic economy have also had a diminishing affect on

exports. Monetary policy divergence around the world also poses a threat to the

economy. Essentially, the search for high yield in Thai assets could also pose as a

threat to the Thai money market.

On the domestic front, domestic demand is expected to slow down to 1.8%

against an earlier forecast of 2.8%, as employment numbers in the manufacturing

sectors are expected to decrease due to the contraction in export numbers. Essentially,

the slowdown in exports is expected to have an impact of employment, as such,

household have become cautious in their spending.

The economy is expected to be supported by public spending and the tourism

sector. The BoT expects the economy to be supported by public spending. The

forecast for public investment was raised from 8.8% to as high as 10.7%, as the

disbursement of public expenditure was better than expected. Furthermore, public

expenditure will likely receive a boost from additional receipt from 4G auctions.

Tourism sector is expected to continue supporting the economy, as current

trends point towards a higher number of tourist arrivals in Thailand this year. The

forecast of tourists arrivals was revised upwards to 32.4mn from 30.9mn arrivals. The

increase in air routes my low cost airlines, and the new road routes from China to

Thailand, are expected to boost tourism arrivals this year.

The contraction in exports poses a risk to the economy. One of the main forecast

revision is the downgrade in export growth (in USD terms). Exports to all trading

partners are expected to contract, except for exports to the CLMV market, which

amounts to only 10.4% of the total Thai exports share in 2015.

The BoT downgraded its economic forecast

Economic projection for 2016

3.5 2.83.9 3.4

8.8

0.0 0.9 0.9 0.8

3.11.8 2.4 3.3

10.7

-2.0

-6.1

0.8 0.6

-7-5-3-113579

1113

GD

P 2

016

Priva

te

co

nsu

mp

tio

n

Priva

te

inve

stm

en

t

Pub

lic

co

nsu

mp

tio

n

Pub

lic

inve

stm

en

t

Goo

ds

exp

ort

s

Goo

ds

imp

ort

s

Co

re in

fla

tio

n

He

adlin

e

infla

tio

n

Dec '15 March '16% YoY

0.8

-0.1-0.6

0.7 0.9 0.90.5 0.4

1 0.8

2.5

0.5

-0.5

0.8 0.9

2.13.0 2.7 2.9 2.8

-2

-1

0

1

2

3

4

5

6

7

8

3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15

Real GDP (%QoQ SA) Real GDP (%YoY)

%QoQ SA, %YoY

Economic Performance

5

Risk to growth is tilted to the downside

Policy Rate Forecast by KBank model

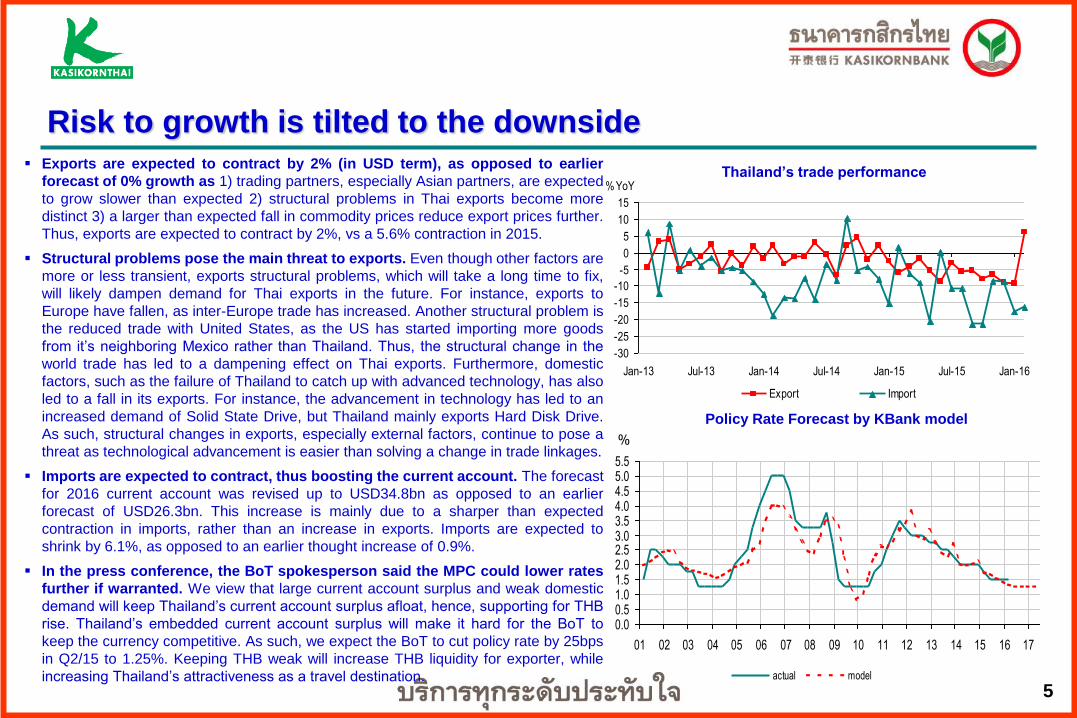

Thailand’s trade performance Exports are expected to contract by 2% (in USD term), as opposed to earlier

forecast of 0% growth as 1) trading partners, especially Asian partners, are expected

to grow slower than expected 2) structural problems in Thai exports become more

distinct 3) a larger than expected fall in commodity prices reduce export prices further.

Thus, exports are expected to contract by 2%, vs a 5.6% contraction in 2015.

Structural problems pose the main threat to exports. Even though other factors are

more or less transient, exports structural problems, which will take a long time to fix,

will likely dampen demand for Thai exports in the future. For instance, exports to

Europe have fallen, as inter-Europe trade has increased. Another structural problem is

the reduced trade with United States, as the US has started importing more goods

from it’s neighboring Mexico rather than Thailand. Thus, the structural change in the

world trade has led to a dampening effect on Thai exports. Furthermore, domestic

factors, such as the failure of Thailand to catch up with advanced technology, has also

led to a fall in its exports. For instance, the advancement in technology has led to an

increased demand of Solid State Drive, but Thailand mainly exports Hard Disk Drive.

As such, structural changes in exports, especially external factors, continue to pose a

threat as technological advancement is easier than solving a change in trade linkages.

Imports are expected to contract, thus boosting the current account. The forecast

for 2016 current account was revised up to USD34.8bn as opposed to an earlier

forecast of USD26.3bn. This increase is mainly due to a sharper than expected

contraction in imports, rather than an increase in exports. Imports are expected to

shrink by 6.1%, as opposed to an earlier thought increase of 0.9%.

In the press conference, the BoT spokesperson said the MPC could lower rates

further if warranted. We view that large current account surplus and weak domestic

demand will keep Thailand’s current account surplus afloat, hence, supporting for THB

rise. Thailand’s embedded current account surplus will make it hard for the BoT to

keep the currency competitive. As such, we expect the BoT to cut policy rate by 25bps

in Q2/15 to 1.25%. Keeping THB weak will increase THB liquidity for exporter, while

increasing Thailand’s attractiveness as a travel destination.

0.00.51.01.52.02.53.03.54.04.55.05.5

01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17

actual model

%

-30

-25

-20

-15

-10

-5

0

5

10

15

Jan-13 Jul-13 Jan-14 Jul-14 Jan-15 Jul-15 Jan-16

%YoY

Export Import

6

-5

0

5

10

15

20

12 13 14 15 16

60

65

70

75

80

85

90

Consumer Confidence (right) Private Consumption (PII)

%YoY Diffusion (Neutral =100)

Thailand’s economic momentum in picture

Consumer confidence dampened in line with spending Trade performance received temporary support

Chinese tourists buoyed tourism sector, while arrivals from

other countries grew more broad-based

0%

5%

10%

15%

20%

25%

30%

China Europe U.S. Japan ASEAN (ex

CLMV)

CLMV

Revenue share in 2015 Arrivals share in 2015

53.2

49.2 48.4 48.046.1

43.5

53.351.2

45.4 45.3 46.244.6

35

40

45

50

55

60

Investment Employment Production

Cost

Production Domestic

Order Books

Foreign Order

Books

Dec-15 Jan-16 Feb-16

Diffusion Index (50 = no change from previous month)

Business confidence remained mix in February

4.4

19.0

-6.2 -4.0 -1.9

0.3

-19.7 -19.9

-9.4

-35

-25

-15

-5

5

15

25

35

Rubber

(2%)

Jewellery

(3%)

Computer

(7%)

IC

(4%)

Auto

(21%)

Rice

(2%)

Rubber

(2%)

Tapioca

(1%)

Petroleum

&

Chemical

(10%)

Jan-16 Feb-16%YoY

7

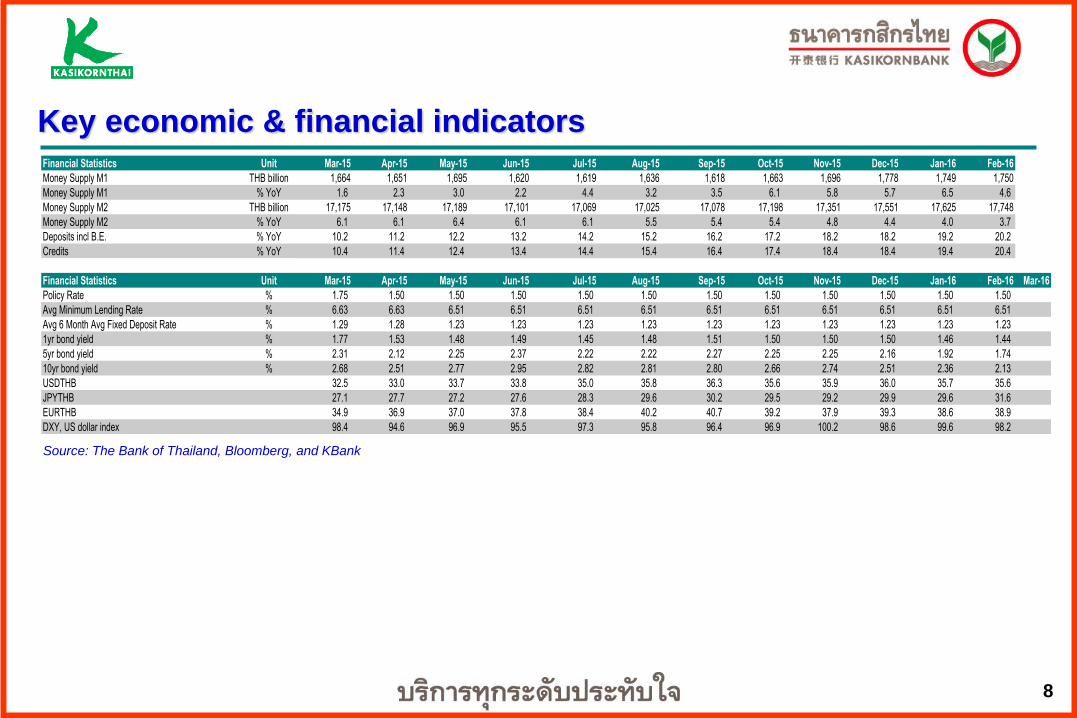

Key economic & financial indicators

Source: The Bank of Thailand, Bloomberg, and KBank

Real Sector Unit Mar-15 Apr-15 May-15 Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 Nov-15 Dec-15 Jan-16 Feb-16

Manufacturing Production Index, % YoY % YoY -1.0 -0.1 -0.1 -0.6 2.6 0.5 -0.3 -0.8 0.3 1.4 -3.5 -1.6

Capacity Utilization Index, non-seasonally adjusted level 70.8 57.9 64.0 64.8 65.3 62.7 64.9 63.8 63.6 62.9 63.8 65.7

Retail Sales % YoY -4.6 -3.3 -6.0 -0.8 -1.8 -0.3 -3.9 -0.2 2.9 6.0 #N/A N/A #N/A N/A

Car Sales Units 74,117 54,058 56,942 60,322 60,863 61,991 61,869 67,910 76,426 101,426 51,821 57,093

Net Capital Goods Imports USD million 127,071 148,077 133,487 159,072 143,540 160,350 148,688 187,912 166,442 147,136 N/A N/A

CPI All Items % YoY -0.57 -1.04 -1.27 -1.07 -1.05 -1.19 -1.07 -0.77 -0.97 -0.85 -0.53 -0.50

CPI Food % YoY 1.3 0.6 0.1 0.5 1.1 1.3 1.3 1.8 0.9 0.8 0.8 1.3

CPI Non Food % YoY (1.5) (1.9) (2.0) (1.9) (2.2) (2.5) (2.4) (2.1) (2.0) (1.8) (1.3) (1.5)

Core Price % YoY 1.31 1.02 0.94 0.94 0.94 0.89 0.96 0.95 0.9 0.68 0.59 0.68

Producer Prices % YoY (5.0) (5.4) (4.8) (3.7) (3.8) (3.8) (3.6) (3.1) (3.1) (2.7) (2.4) (3.0)

External Sector Unit Mar-15 Apr-15 May-15 Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 Nov-15 Dec-15 Jan-16 Feb-16

Foreign Trade Merchandise Exports USD million 18,758 16,744 18,226 17,679 18,113 17,587 18,524 18,288 17,006 16,958 15,560 18,120

Foreign Trade Merchandise Exports % YoY -4.3 -1.8 -5.5 -8.9 -3.1 -5.6 -5.4 -8.0 -6.6 -9.1 -9.3 6.2

Foreign Trade Merchandise Imports USD million 15,277 15,041 14,066 15,682 15,405 14,680 14,523 13,957 14,920 13,739 12,924 12,142

Foreign Trade Merchandise Imports % YoY -6.4 -9.1 -20.4 0.3 -10.6 -10.8 -21.3 -21.3 -8.5 -8.7 -17.8 -16.3

BOP Current Account Balance USD million 2,292 1,768 2,796 1,555 2,326 2,817 1,723 4,220 2,038 3,924 4,066 7,401

TotalTourist Arrivals persons 2,533,000 2,290,000 2,309,000 2,283,000 2,643,000 2,600,000 2,031,000 2,229,000 2,549,000 2,987,000 3,001,000 3,001,001

Overall Balance of Payments (BOP) USD million 1,096 1,808 116 1,402 -1,746 -1,187 550 2,441 -849 -661 4,544 6,071

Total International Foreign Reserves USD billion 157.4 160.1 158.5 160.3 156.9 155.8 155.7 158.3 155.7 157.4 160.1 167.7

International Reserves, Net Forward Position USD billion 19.6 17.9 19.1 18.2 17.6 14.8 13.2 12.1 11.9 11.4 9.2 10.2

8

Key economic & financial indicators

Source: The Bank of Thailand, Bloomberg, and KBank

Financial Statistics Unit Mar-15 Apr-15 May-15 Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 Nov-15 Dec-15 Jan-16 Feb-16

Money Supply M1 THB billion 1,664 1,651 1,695 1,620 1,619 1,636 1,618 1,663 1,696 1,778 1,749 1,750

Money Supply M1 % YoY 1.6 2.3 3.0 2.2 4.4 3.2 3.5 6.1 5.8 5.7 6.5 4.6

Money Supply M2 THB billion 17,175 17,148 17,189 17,101 17,069 17,025 17,078 17,198 17,351 17,551 17,625 17,748

Money Supply M2 % YoY 6.1 6.1 6.4 6.1 6.1 5.5 5.4 5.4 4.8 4.4 4.0 3.7

Deposits incl B.E. % YoY 10.2 11.2 12.2 13.2 14.2 15.2 16.2 17.2 18.2 18.2 19.2 20.2

Credits % YoY 10.4 11.4 12.4 13.4 14.4 15.4 16.4 17.4 18.4 18.4 19.4 20.4

Financial Statistics Unit Mar-15 Apr-15 May-15 Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 Nov-15 Dec-15 Jan-16 Feb-16 Mar-16

Policy Rate % 1.75 1.50 1.50 1.50 1.50 1.50 1.50 1.50 1.50 1.50 1.50 1.50

Avg Minimum Lending Rate % 6.63 6.63 6.51 6.51 6.51 6.51 6.51 6.51 6.51 6.51 6.51 6.51

Avg 6 Month Avg Fixed Deposit Rate % 1.29 1.28 1.23 1.23 1.23 1.23 1.23 1.23 1.23 1.23 1.23 1.23

1yr bond yield % 1.77 1.53 1.48 1.49 1.45 1.48 1.51 1.50 1.50 1.50 1.46 1.44

5yr bond yield % 2.31 2.12 2.25 2.37 2.22 2.22 2.27 2.25 2.25 2.16 1.92 1.74

10yr bond yield % 2.68 2.51 2.77 2.95 2.82 2.81 2.80 2.66 2.74 2.51 2.36 2.13

USDTHB 32.5 33.0 33.7 33.8 35.0 35.8 36.3 35.6 35.9 36.0 35.7 35.6

JPYTHB 27.1 27.7 27.2 27.6 28.3 29.6 30.2 29.5 29.2 29.9 29.6 31.6

EURTHB 34.9 36.9 37.0 37.8 38.4 40.2 40.7 39.2 37.9 39.3 38.6 38.9

DXY, US dollar index 98.4 94.6 96.9 95.5 97.3 95.8 96.4 96.9 100.2 98.6 99.6 98.2

9

The Bank of Thailand’s new economic forecasts

(unit : % YoY or otherwise indicated)

Forecast as of June 2015 2015 2016 (F) 2017 (F) Actual Dec '15 March '16 March'16

GDP 2.8 3.5 3.1 3.3 Core inflation 1.1 0.9 0.8 1.1 Headline inflation -0.9 0.8 0.6 2.2 Domestic demand 2.8 3.5 2.8 2.9 - Private consumption 2.1 2.8 1.8 2.4 - Private investment -2.0 3.9 2.4 4.0 - Public consumption 2.2 3.4 3.3 2.8 - Public investment 29.8 8.8 10.7 4.5 Current account ($ bn)* 34.8 26.3 34.8 32.7 - Exports of goods (f.o.b) -5.6 0.0 -2.0 0.1 - Imports of goods (f.o.b.)* -11.3 0.9 -6.1 3.6 Source: Bank of Thailand, * changes according to IMF’s BPM6 effective from August 2011 Full Report (Thai) can be found at https://www.bot.or.th/Thai/MonetaryPolicy/MonetPolicyComittee/MPR/DocLib/MPR_March2559_BVS59.pdf

10