Embed Size (px)

Citation preview

The 1st International Conference on Accounting Research and Education

(iCARE 2014)

Accounting Profession, Research and Education:

Bridging the Gap and Shaping the Future

2nd – 3rd September 2014

Casuarina @ Meru, Ipoh, Perak, Malaysia

Jointly Organized by:

Faculty of Accountancy UiTM

MYAA

ARI

MAREF

UnSyiah Kuala

Copyright Faculty of Accountancy Universiti Teknologi MARA Malaysia 2014

All rights reserved. No part of this book may be reproduced or utilized in any form or by any

means, electronic or mechanical, including photography regarding, or by any information

storage and retrieval system, without permission in writing to publisher.

For information:

Secretariat of iCARE2014

Faculty of Accountancy

UniversitiTeknologi MARA (PERAK)

32610 Bandar Baru Seri ISkandar

Perak, MALAYSIA

Tel No: (+605) 374 2381

Fax No: (+605) 374 2635 or (+605) 374 2277

e-mail: [email protected]

Website: http://perak.uitm.edu.my/icare2014/

ISBN No.: 978-967-5741-23-4

Disclaimer The views and recommendations expressed by the authors are entirely their own and do not

necessarily reflect the views of the editors, the school or the university. While every attempt has

been made to ensure consistency of the format and the layout of the proceedings, the editors

are not responsible for the content of the papers appearing in the proceedings.

Perpustakaan Negara Malaysia Cataloging in Publication Data International Conference on Accounting Research and Education (iCARE 2014) – Accounting Profession, Research and Education: Bridging the Gap and Shaping the Future / Editors : Dr.Wan Razazila Wan Abdullah, Irda Syahira Khair Anwar, Mohd Taufik Mohd Suffian, Noor Saatila Mohd Isa, Siti Nabilah Mohd Shaari; Amizahanum Adam, Mohd Shahril Abdul Rashid, Haslinawati Che Hasan, Liyana Ab Rahman, Nurfarizan Mazhani Mahmud, Wan Roshaini Wan Ali, Nooriha Mansor and Azlan Zainal.

ISBN 978-967-5741-23-4 Financial Accounting & Reporting; Islamic Accounting & Finance; Public Sector Accounting; Accounting Education; Corporate Social Responsibility; Finance & Capital Market; Corporate Governance & Accountability; Accounting & Governance for Non-Profit Sector; Ethics; Taxation; Management Accounting; Auditing; Forensic Accounting; Risk & Earnings Management; Intellectual Capital; Others. All rights reserved. © 2014 Faculty of Accountancy, (UiTM Perak) ISBN 978-967-5741-23-4

TABLE OF CONTENTS

Accounting Students’ Perception And Experience On Blended Learning Erlane K Ghani, Kamaruzzaman Muhammad and Salina Salleh

1-12

The Impact of Economic Transformation Programme on Business Model of a Malaysian Agriculture Company: An Organisational Change Perspective Kamaruzzaman Muhammad, Nor‘Azam Mastuki and Faezah Darus

13-25

Are accounting students apprehensive about oral communication? Badriyah Minai, Zaharah Hamzah and Mazlina Mustapha

26-34

Sources of Funds and Funding Trends of Public Universities in Malaysia: Preliminary Analysis Ibrahim Kamal Abdul Rahman, Syed Noh Syed Ahmad, Kalsom Salleh and Noor Hasniza Haron

35-45

Accounting Educators’ Assessment of Quality Assurance Inputs for the Teaching of NCE Accounting Education in Colleges of Education in South-East and South-South Nigeria Odo, Samuel N.

46-59

Exploring The Competency Assessment System By Malaysian Institute Of Accountants Azleen Shabrina Mohd Nor and Nor Aziah Abu Kasim

60-72

Real Earnings Management And Firm’s Value: Empirical Evidence From Malaysia Mohd Taufik Mohd Suffian, Zuraidah Mohd Sanusi and Nor‘Azam Mastuki

73-87

The Effect of Ethical Climate on Organizational Commitment: The Mediating Role of Job Satisfaction Norliana Omar and Liyana Ab Rahman

88-100

Determinants of Dividend Payout: A Comparative Study between Trading and Industrial Companies in Malaysia Maslina Musa, Mohd Taufik Mohd Suffian and Ganisen Sinnasamy

101-115

A Study of Audit Disclaimers among Malaysian Listed Companies Hashanah Ismail and Shum Yin Peng

116-125

Management Accounting: Research Assumptions and Empirical Studies Findings Ahmed Abdullah Saad Al-Dhubaibi, Ibrahim Kamal Abdul Rahman, Mohd Nizal Haniff and Zuraidah Mohd Sanusi

126-136

Effect of Industrial Training on Academic Performance: Evidence from Malaysia Putri Nor Suad Megat Mohd Nor and Suhaiza Ismail

137-145

Assessing The Effect Of Bureaucratic Organization Culture In Implementation Of Internal Control In Malaysian Public School Siti Noorzainah Sahat and Kalsom Salleh

146-160

CEO Duality and Dividend Policy: Empirical Evidence on Oil and Gas Companies in Malaysia Yip Pick Schen and Mohd Taufik Mohd Suffian

161-174

Fraud Financial Indicators and Earnings Management: Evidence from Malaysia and Thailand Nor Farhana Selahudin, Nor Balkish Zakaria, Zuraidah Mohd Sanusi and Pornanong Budsaratragoon

175-191

Institutional Level Factors Impacting Accounting Ethics Education In Malaysia Marzlin Marzuki, Nava Subramaniam and Barry J. Cooper

192-206

Integrating Target Costing Indicators within the Balanced Scorecard Model in Malaysian Automotive Industry: A Rasch Analysis Hussein H. Sharaf-Addin, Normah Omarb and Suzana Sulaiman

207-223

Green Human Capital, Green Innovation Capital and Firms’ Competitive Advantage Naimah Ahmad Yahya, Roshayani Arshad and Amrizah Kamaluddin

224-234

Academic Integrity Among Accounting Students In Malaysia: Some Preliminary Evidence Hairul Suhaimi Nahar, Bakhtiar Alrazi and Mohd Nazli Mohd Nor

235-256

Can Size Influence Firm’s Performance Of Manufacturing Firms In Nigeria? Nuraddeen Usman Miko

257-262

Malaysian Accountant’s Propensity to Whistleblow Saadon Mydinsa, Azizah Abdullah and Nafsiah Mohamed

263-277

The Contribution Of Board Of Directors’ Commitment To The Timely Submission Of The Annual Financial Report Of Agricultural Co-Operative Societies In The State Of Perak Hatta Hj Sapwan

278-288

Future Direction Of Enterprise Risk Management Research Enny Nurdin Sutan Maruhun, Siti Haliza Asat and Ruhaya Atan

289-302

The Role Of Taxation In Developing Waqf Mohd Rizal Palil, Mohamad Abdul Hamid, Noor Inayah Ya‘akub, Aryani Abdullah and Nor Hazila Mohd Zain

303-308

The Contribution Of Board Of Directors’ Integrity To The Timely Submission Of The Annual Financial Report Of Agricultural Co-Operative Societies In The State Of Perak. Md Lehan Parimon and Hatta Hj. Sapwan

309-319

R&D And Market Valuation: Empirical Evidence From Malaysian Listed Firms Sunarti Binti Halid, Amizahanum Binti Adam, Marina Binti Ibrahim and Masetah Binti Ahmad Tarmizi

320-355

Applying Stakeholder Approach In Developing Accountability Indicators For Tahfiz Centers Hamidah Bani, Maheran Katan, Abd Halim Mohd Noor and Muhammad Mukhlis Abdul Fatah

356-366

Risk Management Committee (RMC) And Performance Of Malaysian Firms Roslida Ramlee and Normah Ahmad

367-377

The Influence Of Organizational Culture On Auditor’s Job Satisfaction And Turnover Intention Norul Akma Mansor, Irda Syahira Khair Anwar and Mohd Amran Mahat

378-392

Public Sector Multiple Accountabilities And Current Public Sector Reform In Malaysia: A Literature Review Ang Li Ling, Dayana Jalaludin and A.K Siti-Nabiha

393-405

Managing The Outcome: The Case Of Poverty Eradication Program In Malaysia SangitaJeyaram, A.K Siti-Nabiha and DayanaJalaludin

406-416

The Relationship Between Agency Problems and Firm Performance On Family Firms : Case In Small And Medium Entreprise In Indonesia D. Agus Harjito and Arif Singapurwoko

417-427

Factors Influence The Level Of Compliance Of Shariah Responsibility Disclosure In Malaysian Islamic Banks Nuruu Ain Binti Fauzi and Mohamad Hafiz Bin Rosli

428-443

Innovation, Integrity and Management Accounting Practices as Catalyst on Small Medium Enterprises Performances in Malaysia Nor Azlina Ab.Rahman; Bello Lawal Danbatta; Normah Omar and Aliza Ramli

444-455

Enhancing Shariah Compliance: The Role Of Shariah Committee And Shariah Auditing Rosnadzirah Ismail and Nawal Kasim

456-465

The Relationship Between Managerial Ownership And Company Performances Using Extended Agency Theory Mohd Abdullah Jusoh and Ayoib Che Ahmad

466-476

Corporate Governance Characteristics And Firm Performance Among Shariah And Non-Shariah Approved Companies In Malaysia Hanim Norza Baba and Mohd Ariff bin Mustafa

477-490

Factors That Affect The Practice Of Risk Disclosures Among Non-Profit Organizations In Malaysia - A Preliminary Study Nawal Afifah Khairuddin and Mohd Shatari Abd Ghafar

491-509

Combating Money Laundering And Terrorism Financing In Non-Profit Organisations In Malaysia: Risk-Based Approach Perspectives Wan Ainul Asyiqin Wan Mohd Razali and Roshayani Arshad

510-518

Predicting Fraudulent Financial Reporting using Artificial Neural Network in Malaysian’s Shariah Government Link Companies (GLCs) Normah Omar and Zulaikha Amirah Johari

519-539

Trade Based Money Laundering: An Overview Normah Omar, Salwa Zolkaflil, and Roshayani Arshad

540-548

Corporate Governance Reforms And Good Practices In Malaysia: What Have We Learned So Far? Azmi Abd Hamid, Rozainun Abdul Aziz and Normah Hj Omar

549-559

Enterprise Risk Management (ERM) Of The Housing Developers In Malaysia Siti Haliza Asat, Enny Nurdin Sutan Maruhun, Hasnah Haron and Mastura Jaafar

560-569

The Influence of Financing Structure to Insolvency Risk In Islamic Bank Listed in Bank Indonesia Evi Mutia and Nabila Rifa

570-582

The Effect Of Profitability, Liquidity, And Free Cash Flow On Cash Dividend And Its Impact On Firm Value (Studies At Banking Companies Listed In Indonesia Stock Exchange) Islahuddin and Yunita Sahputri

583-592

The Impacts Of Capital Expenditure And Fixed Assets On Maintenance Expenditures (A Study Of Aceh Government Agencies) Dewi Safitri and Islahuddin

593-602

Determinants of Accounting Students' Academic Performance Siti Nabilah, M. S., Nurfarizan Mazhani, M., Suryani, A. R and Nik Nurul Aswani, N. K

603-613

Waqf Management And Accounting: An Overview Nurfarizan Mazhani Mahmud, Wan Roshaini Wan Ali, Maizura Meor Zawawi and Naimah Zaini

614-621

The Evolution Of The Malaysian Islamic Capital Market: 1996 To 2013 Wan Razazila Wan Abdullah, Jamal Roudaki and Murray B Clark

622-634

Corporate Governance Mechanism And Fraudulent Financial Reporting: Evidence From Malaysian Listed Companies Mahanum Sulaiman and Hasnah Haron

635

The Impact of Enterprise Resource Planning (ERP) System on User Performance: a Critical Review Norzarina Noordin, Zaini Ahmad and Erlane K Ghani

636

The Impact of IFRS on the Value Relevance of Book Values, Earnings and Cash Flow: Study on the Malaysian Market Shazerinna bt. Zainal Osman Shah, Louise Macniven, Nooriha Mansor, and Nor Asyiqin Salleh

637

Mitigation Of Reputation Problems: Level Of Hotel Quality Management Program And Environmental Management Practices Towards Performance. Siti Anis Nadia Abu Bakar, Zuraidah Mohd Sanusi, Rani Diana Othman and Nurul Zamratul Asyikin Ahmad

638-642

Proceedings of International Conference on Accounting Research & Education 2014 ISBN 978-967-5741-23-4

593

The Impacts Of Capital Expenditure And Fixed Assets On Maintenance Expenditures

(A Study Of Aceh Government Agencies)

Dewi Safitri Islahuddin

Abstract

This paper measures the impacts of capital expenditure and fixed assets on the maintenance

expenditures in budget allocation and realization at Aceh government agencies. The research

method used in this research is causal research method. The independent variables of the

research are capital expenditure and fixed assets while the dependent variables are the

budgeted maintenance expenditure and the actual maintenance expenditure. This paper uses

merely secondary data collected from financial statements of 33 Aceh government agencies. The

data includes actual budget reports and balance sheet for the period of 2008 – 2012 obtained

from Aceh Department of Finance. The results are the capital expenditure and the fixed assets

simultaneously and partially have significant impacts on both budgeted and actual maintenance

expenditures. However, partially, capital expenditure had a lower effect on the dependent

variables than the fixed assets. Capital expenditure has negative effect on budgeted and actual

maintenance expenditures, while the fixed assets have positive effect on budgeted and actual

maintenance expenditures.

Keywords: capital expenditure, fixed assets, government agencies, maintenance expenditures

1. INTRODUCTION The allocation of maintenance expenditures for fixed assets obtained from capital

expenditure is closely related to a long term financial planning, in the context of regional financial management. It is contextually because the fixed assets are assets that can be utilized for more than one year. Financing the asset maintenance expenditure is very essential to ensure that the assets can always be used in accordance with their functions and estimated life.

Budget for mantenance in accounting perspective calculated based on the length of time

and the using period of fixed asset as in the calculation of the depreciation for the fixed asset (Abdullah and Halim, 2006). However, in reality the maintenance expenditure is often neglected. According to research in many developed countries such as Africa and Latin America (IMF, 2007; World Bank, 2008), the phenomena so called ghost expenditures, that could not be accounted is a usual matter. Allocation for maintenance expenditures is always budgeted incrementally although some assets have been left unused or lost.

Prior to this research, little research on maintenance expenditures in Aceh has been

done although the financial condition in Aceh after the implementation of special autonomy, earthquake and tsunami disasters recovery program have created a significant increase in the capital expenditure and fixed assets. Basically, the fixed assets are not only obtained from the budged realization capital expenditure but may also from the third parties (grant).

___________________ Corresponding Authors: Islahuddin, Faculty of Economics, SYiah Kuala University, Indonesia.

Proceedings of International Conference on Accounting Research & Education 2014 ISBN 978-967-5741-23-4

594

Meanwhile, the government of Aceh province until 2012 was still granted the category of ―reasonable with exceptions‖ or qualified opinion for its financial statement. One of the exceptions was the balance off the fixed assets for the period of December 31, 2012, i.e. 13.786 trillion rupiah, which was considered unreasonable. It was due to the lack internal control for the fixed asset, inventory, and the improvement for the fixed asset management system.

This research investigated the impact of capital expenditure and fixed assets on maintenance budget at Aceh government agencies in Aceh province government. The data used for this research were the data from financial statements prepared by Aceh government agencies for the five-year periods, from 2008 until 2012. It is expected that this research can be used as a recommendation in establishing the policies of maintenance budget for Aceh Province government.

2. LITERATURE REVIEW Budget and Regional Budgeting

Budget is a statement of working estimation in the form of monetary measure. In public sector organization, budget is an accountability instrument for public financial management and the implementation of programs financed by public funds (Mahsun et al., 2011:65).

According to Law Number 32 of 2004, Articles 184, budgeting process is a consecutives

activities which includes planning, compiling, implementing, reporting, and evaluation. This process is known as budget cycle. This cycle is not implemented in sequence but simultaneously. When the budget is still used and the report has not been completed, the planning and compiling should have been arranged.

Local Government Accountability Report

Thhe guideline on local government financial management (Regulation of Minister of Internal Affairs Number 13 of 2006) mentions that local government agencies are government agencies which use the public budget. The agencies propose their budget in Work Plan and Budget of Local Government Agency. It is used later in designing local government regulation regarding local government budget and regulation of government head regarding outline of local government budget.

According to Law Number 32 of 2004, Article 184, reporting is draft of local government

regulation, prepared by Head of the Government regarding accountability for local government budget implementation to Local Government Representative Assembly. This draft is a financial statement which has been audited by Audit Board. The report should include actual spending report of local government budget, balance sheet, cash flow statement, and notes for the financial statement, with the attachment of Local Government Own Enterprise financial report.

Maintenance Expenditure

Maintenance is an activity or action that utilizes the properties of local government to keep them in usable. These properties are all the goods purchased or obtained by using local government budget or other approved funding (Regulation of Minister of Internal Affairs Number 17 of 2007 on Technical Guide of Local Property Management, Article 1).

According to Law Number 17 of 2003, maintenance expenditure is a expenditure to

maintain the condition of existing fixed assets or other assets regardless of the amount of fund, such as the maintenance of lands, buildings, government institution houses, official vehicles, and other facilities related to the government operation. Maintenance expenditure is a regular spending that involved in all working units or local government which has an

Proceedings of International Conference on Accounting Research & Education 2014 ISBN 978-967-5741-23-4

595

asset. Therefore, the amount of annual budgeted maintenance expenditure depends on the number of assets owned by every corresponding working unit or local government.

The national capital expenditure should consider the amount of fund required for operation and maintenance of public works related to government fund based on the programs, project types, and regions. The reserve of capital expenditure creates a demand for funding the operational and maintenance activities. Even in some states such as Cincinnati, Ohio, and Waco, and Texas, they do not consider forming a new capital expenditure before obtaining guarantee for operational and maintenance funding to avoid the suspension. Therefore, there should be no more any expression of ―build then forget‖ in government administrative style (Choate, 1981:25)

Capital Expenditure

Halim (2002:72) defines capital expenditure as the spending of budget for a period of more than one year and it adds asset or property to local government, leading to the addition in routine expenditure such as for maintenance. The capital budget is divided into two types, namely public budget and budget for civil servants.

In accordance with Government Regulation Number 24 of 2005 on the Standard of

Government Accounting, the statement number 2 on government report on budget outcomes defines capital expenditures as budget spending to obtain fixed assets and other assets which give benefit for one accounting period. Capital expenditure includes the spending to obtain land, building, tools and other intangible assets. Fixed Assets

Government Regulation Number 24 of 2005 states that an asset is a resource owned by the government as a result of past activities and where the government obtain economic or social benefits for the future, either by the government or society, and it can be measured with money, including non-financial resource to provide services for public and conserved resources for historic and cultural reasons. Fixed assets are tangible assets which give benefit for the period of more than 12 months used for government activities or by members of public.

Hypothesis Hypothesis of this research were: Hypothesis 1 = capital expenditure and fixed assets simultaneously influenced the budgeted

maintenance expenditure. Hypothesis 2 = capital expenditure influenced the budgeted maintenance expenditure. Hypothesis 3 = fixed assets influenced budgeted maintenance expenditure. Hypothesis 4 = capital expenditure and fixed assets simultaneously influenced the

realization maintenance expenditure. Hypothesis 5 = capital expenditure influenced the realization maintenance expenditure. Hypothesis 6 = fixed assets influenced the realization maintenance expenditure. 3. RESEARCH METHODOLOGY

The research method used in this research is a causal research method. The objective of this research is to analyze the influence of independent variables on dependent variables through a hypothesis test.

The population in this research is all Aceh Government Agencies between and the

study period is between 2008 and 2012. The objects investigated in this research are the Government Realization Report and the Balance Sheets from Aceh Government Agencies. The sample was selected by using a purposive sampling technique for which the SKPA used were the regular SKPA in the observed periods. Based on these criteria, 33 Aceh government agencies have been selected as the research sample.

Proceedings of International Conference on Accounting Research & Education 2014 ISBN 978-967-5741-23-4

596

The data collected for this research are quantitative data, i.e. secondary data obtained from financial statements prepared by the Aceh Government Agencies. The collected documents are Government Realization Report and the Balance Sheets prepared by Aceh Government Agencies. The documents were collected from Department of Finance of Aceh. The collected data are presented in the following: 1. Capital expenditure in year t-1 (one year before the concerned year) and fixed assets in

year t-1 for the period of 4 years, 2008 – 2011. 2. Budgeted maintenance expenditure and actual maintenance expenditure from 2009 until

2012. Operationalization of Variables Independent variables 1. Capital expenditure is an expense to purchase/procure or construct tangible fixed

assets which give benefits for more than 12 months to be used for government activities. The data for capital expenditure were collected from Government Realization Report prepared by Aceh Government Agencies for prior year (t – 1), presented in Indonesian rupiah.

2. Fixed assets are tangible assets which give benefits for the period of more than 12 months to be used for government activities. The data for capital expenditure were collected from Balance Sheet prepared by Aceh Government Agencies for year t – 1 in rupiah.

Dependent variables 1. Budgeted maintenance expenditure in this research is defined as a budget allocated

by Aceh Government Agencies to maintain assets owned by the agencies in the proper condition. The amount of budgeted maintenance expenditure was taken from budgeted maintenance expenditure in a certain year in the Government Realization Report prepared by Aceh Government Agencies in rupiah.

2. Realization of maintenance expenditure in this research is defined as the realization expenditure by Aceh Government Agencies to maintain assets owned by the agencies in proper condition. The amount of realization maintenance expenditure was taken from the actual maintenance expenditure in a certain year from Government Realization Report prepared by Aceh Government Agencies in rupiah.

Technique of Data Analysis

A classical assumption test was conducted before the data were analyzed to test the hypotheses. The hypotheses were tested by using t-test and F-test formulas. The relationship between two variables was determined by using multiple regression equation, as presented in the following:

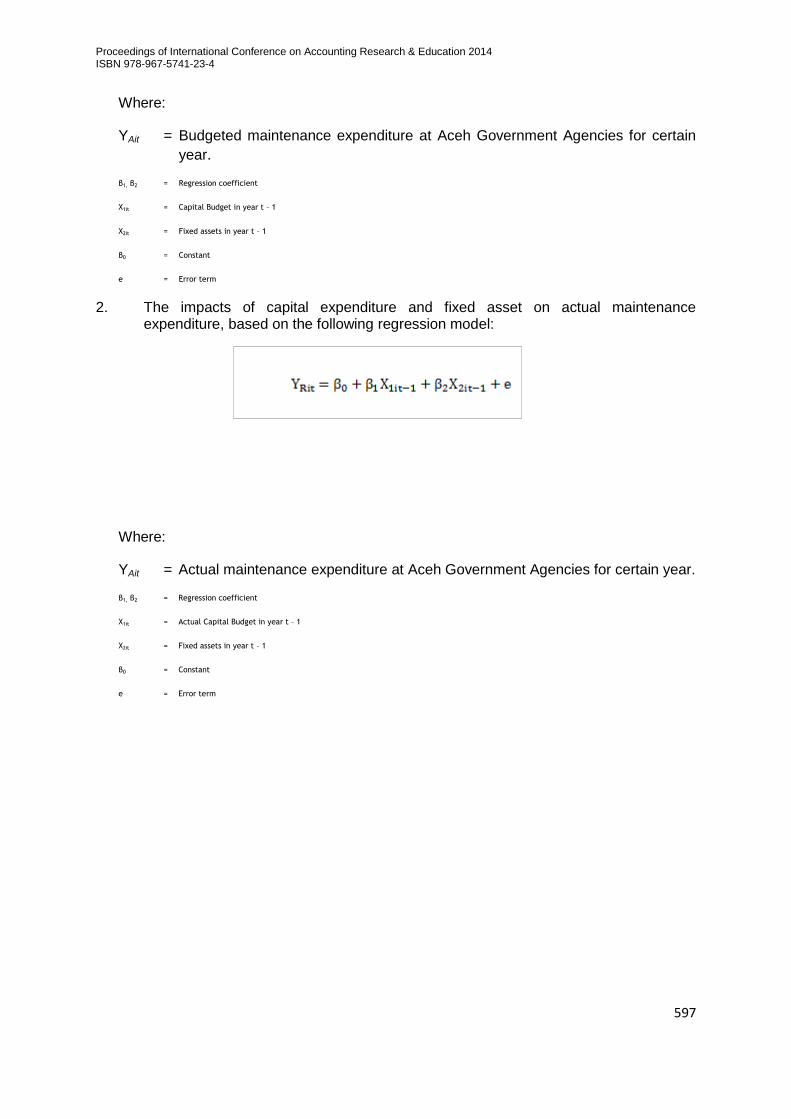

1. The impacts of capital expenditure and fixed asset on budgeted maintenance

expenditure, based on the following regression model:

Proceedings of International Conference on Accounting Research & Education 2014 ISBN 978-967-5741-23-4

597

Where:

YAit = Budgeted maintenance expenditure at Aceh Government Agencies for certain

year.

β1, β2 = Regression coefficient

X1it = Capital Budget in year t – 1

X2it = Fixed assets in year t – 1

β0 = Constant

e = Error term

2. The impacts of capital expenditure and fixed asset on actual maintenance expenditure, based on the following regression model:

Where:

YAit = Actual maintenance expenditure at Aceh Government Agencies for certain year.

β1, β2 = Regression coefficient

X1it = Actual Capital Budget in year t – 1

X2it = Fixed assets in year t – 1

β0 = Constant

e = Error term

Proceedings of International Conference on Accounting Research & Education 2014 ISBN 978-967-5741-23-4

598

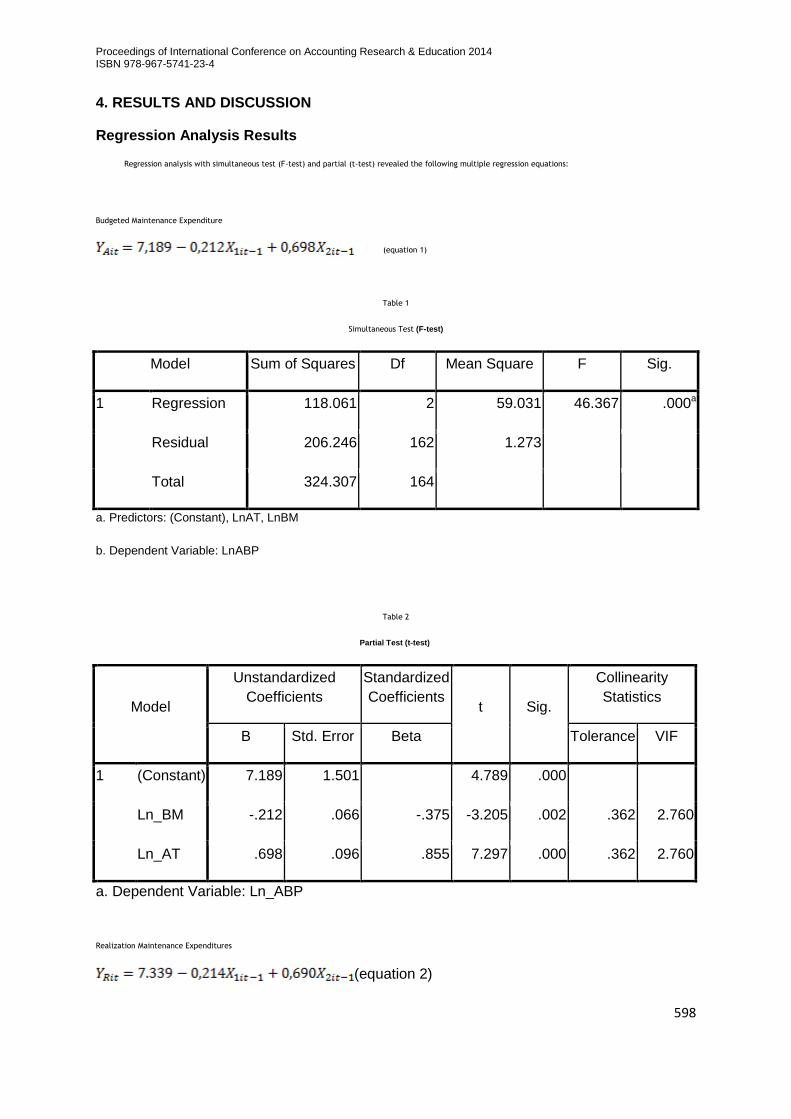

4. RESULTS AND DISCUSSION

Regression Analysis Results

Regression analysis with simultaneous test (F-test) and partial (t-test) revealed the following multiple regression equations:

Budgeted Maintenance Expenditure

(equation 1)

Table 1

Simultaneous Test (F-test)

Model Sum of Squares Df Mean Square F Sig.

1 Regression 118.061 2 59.031 46.367 .000a

Residual 206.246 162 1.273

Total 324.307 164

a. Predictors: (Constant), LnAT, LnBM

b. Dependent Variable: LnABP

Table 2

Partial Test (t-test)

Model

Unstandardized

Coefficients

Standardized

Coefficients t Sig.

Collinearity

Statistics

B Std. Error Beta Tolerance VIF

1 (Constant) 7.189 1.501 4.789 .000

Ln_BM -.212 .066 -.375 -3.205 .002 .362 2.760

Ln_AT .698 .096 .855 7.297 .000 .362 2.760

a. Dependent Variable: Ln_ABP

Realization Maintenance Expenditures

(equation 2)

Proceedings of International Conference on Accounting Research & Education 2014 ISBN 978-967-5741-23-4

599

Table 3

Simultaneous Test (F-test)

Model Sum of Squares Df Mean Square F Sig.

1 Regression 86.312 2 43.156 35.967 .000a

Residual 154.785 129 1.200

Total 241.098 131

a. Predictors: (Constant), Ln_AT, Ln_BM

b. Dependent Variable: Ln_RBP

Table 4

Partial Test (t-test)

Model

Unstandardized

Coefficients

Standardized

Coefficients

T Sig.

Collinearity

Statistics

B Std. Error Beta Tolerance VIF

1 (Constant) 7.339 1.479 4.963 .000

Ln_BM -.214 .065 -.385 -3.283 .001 .362 2.760

Ln_AT .690 .094 .859 7.329 .000 .362 2.760

a. Dependent Variable: Ln_RBP

DISCUSSION

The Impacts of Capital Expenditure and Fixed Assets on Budgeted Maintenance

Expenditure

Based on the table 1, the impacts of capital expenditure and fixed assets on budgeted maintenance expenditure can be seen from the value of F, i.e. 46.367 with the significance level of 0.000, which is lower than regression significance, i.e. 0.05. Based on this result, it can be concluded that the first hypothesis was empirically accepted, which means that capital expenditure and fixed assets simultaneously influenced the budgeted maintenance expenditure.

Proceedings of International Conference on Accounting Research & Education 2014 ISBN 978-967-5741-23-4

600

The Impacts of Capital Expenditure on Budgeted Maintenance Expenditure Based on the table 2, the level of significance for capital expenditure is 0.002, which

was lower than the regression significance, i.e. 0.05. It is indicated that the capital budget of t – 1 significantly effect on the budgeted maintenance expenditure. The regression coefficient for capital budget is negative, i.e. -0.212, which means that the higher the capital expenditure, the lower the budgeted maintenance expenditure. Therefore, if the coefficient was constant, for every one Rupiah of increase in capital expenditure, there is Rp 0,212 decrease in budgeted maintenance expenditure. In conclusion, the second hypothesis is empirically accepted; therefore, capital expenditure significantly influenced the budgeted maintenance expenditure.

From the discussion above, the results of this research were different from the

research conducted by Kamensky (1984:14) who discovered that 57 percent of the cities in the United States are not influenced by the maintenance or repair cost of a project. Therefore that managers in public sectors had to learn more comprehensively about the total cost from capital expenditure beside restrict the expenditure merely on construction and procurement.

The Impacts of Fixed Assets on Fixed Maintenance Expenditure

Based on the table 2, the analysis results show that the significance level for fixed assets is 0.000, which is lower than regression significance, i.e. 0.05, reveals that the fixed assets gave an impact on budgeted maintenance expenditure. The regression coefficient for fixed assets is positive, i.e. 0.698, which means that the more expensive the fixed assets, the higher the budgeted maintenance expenditure. This suggested that if the coefficient remained constant, every Rp1 increased in fixed asset price boosted the budgeted maintenance expenditure by 0,698 Rupiah. Therefore, it can be concluded that the third hypothesis which stated that fixed assets influenced budgeted maintenance expenditure was empirically accepted.

This result is supported by the results of a research conducted by Sinaga and

Sidaburat (2012) which concluded that the variable of asset price gave direct and positive impacts on maintenance expenditure. This suggested that the budgeted maintenance expenditure had been adjusted to the fixed asset value. The Simultaneous Impacts of Capital Expenditure and Fixed Assets on Actual Maintenance Expenditure

Based on the table 3, the value of F is 35,967 with the significant of 0.0000, which is lower than the significant regression, namely 0.05. It again reveals that the forth hypothesis supported empirically that the capital expenditure and fixed asset simultaneously give the impact on realization maintenance expenditure

The Impacts of Capital Expenditureon Realization Maintenance Expenditure

Based on the table 4, te significance level for capital expenditure, i.e 0.009, is lower than regression significance, i.e. 0.05. It suggests that the capital expenditure gave an impact on realization maintenance expenditure. In addition, regression coefficient for capital expenditure is negative, i.e. -0.214 indicated that the higher the capital expenditure, the lower the realization maintenance expenditure. These results reveal that for every one rupiah increase in capital expenditure, there is 0.214 Rupiah increase in realization maintenance expenditure, if the coefficient remained constant. Therefore, it can be concluded that the fifth hypothesis which stated that capital expenditure influenced realization maintenance expenditure is empirically accepted.

Proceedings of International Conference on Accounting Research & Education 2014 ISBN 978-967-5741-23-4

601

The Impacts of Fixed Assets on Realization Maintenance Expenditure Based on the table 4, the significance level of fixed assets of 0.000, which was lower

than regression significance, i.e. 0.05, shows that fixed assets significantly influenced the realization maintenance expenditure. The regression coefficient for fixed assets was positive, i.e. 0.690, meaning that the higher the fixed asset value, the higher the realization maintenance expenditure. This result suggested that if the coefficient remained constant, the increase in fixed asset value as much as 1 (one) rupiah increase, the realization maintenance expenditure will increase as much as 0.69 Rupiah. Therefore, it can be concluded that the sixth hypothesis i.e assets influenced realization maintenance expenditure was empirically accepted.

Comparison of Both Regression Test Results

The comparison of both regression test results (coefficient of β1 and β2 ) show that the comparison of coefficients for independent variables, i.e. X1it-1 (capital expenditure) and X2it-1(fixed assets) for maintenance expenditure and realization maintenance expenditure, presented as follows.

β1YAit (0.212) <β1YRit (0.214) β2YAit (0.698) >β2YRit(0.690) β1 <β2 The coefficient for capital expenditure (β1) which influenced the budgeted

maintenance expenditure (YAit) is lower than the coefficient for capital expenditure (β1) which also influenced the realization maintenance expenditure (YRit). These results show that the capital expenditure could predict realization maintenance expenditure better than it did to budgeted maintenance expenditure. The coefficient for fixed assets (β2) which is the influenced budgeted maintenance expenditure (YAit) is higher than the coefficient for fixed assets (β2), namely the influenced realization maintenance expenditure (YRit). These results show that fixed assets could predict budgeted maintenance expenditure better than capital expenditure. The coefficient for capital expenditure (β1) is lower than the coefficient for fixed assets (β2). This suggested that the fixed assets could predict the impacts of capital and maintenance expenditure than capital expenditure. Maintenance expenditure is only budgeted to ensure that fixed assets worked well as the functions. Therefore, the policy on allocation maintenance budget based on the fixed asset value is supported by this research.

The obstacles often occurred are that the local government did not have sufficient

information regarding the total of their fixed assets. It was proved from audit reports issued by National Audit Board (BPK) for Financial Statements prepared by Aceh Government for the year of 2011. The National Audit Board responded ―Reasonable with Exception‖ for that financial statement. The exceptions included balance for the assets, which was considered so unreasonable that the Aceh government was not able to obtain ―Reasonable without Exception‖ from National Audit Board (BPK) for its financial statements.

CONCLUSIONS AND SUGGESTIONS Conclusions 1) Budgeted and realization maintenance expenditure is affected negatively by the

capital expenditure. It means that an increase in capital budget is followed by a decrease in maintenance expenditure. It also suggests that funding for asset maintenance was not predicted when capital expenditure was budgeted.

2) Budgeted and actual maintenance expenditure is positively impact by the fixed asset. It suggests that an increase in fixed asset value was followed by an increase in maintenance expenditure.

3) Capital expenditure and fixed assets simultaneously and partially gave impacts on budgeted and realization maintenance expenditure. However, the capital expenditure

Proceedings of International Conference on Accounting Research & Education 2014 ISBN 978-967-5741-23-4

602

gave lower impact partially, instead of simultaneously. 4) The impacts of capital expenditure on budgeted maintenance expenditure were

smaller than on realization maintenance expenditure. 5) Fixed assets gave more impacts on budgeted maintenance expenditure than on

realization maintenance expenditure. Suggestions 1) Considering the capital expenditure transferred to the third party is separated from

capital expenditure of Government Agencies as a result of the implementation of Permendagri No.37/2010, the following research shall use the data for capital expenditure of Government Agencies since 2011 and add the local government income to analyze Aceh government's capability in funding operational and maintenance costs.

2) To simplify the responsibility, capital expenditure from special autonomy fund is recommended to be transferred to third parties (district/city/society) not in the corresponding year, and allocated separately from capital expenditure for Aceh government agencies.

3) It has to be noted that physical development by Aceh government agencies by utilizing special autonomy fund, which has been planned to be handed to district or municipality government is less effective if it is budgeted in capital expenditure of Aceh government agencies. Therefore, further research need to include the grant and other financial assistance in Aceh government policies.

4) To find out whether there is an increase in maintenance expenditure, further research should separate fixed assets purchased or procured by Aceh government agency‘s fund and those from capital expenditure and special autonomy fund.

REFERENCES Abdullah, Syukriydan Abdul Halim. 2006. Studi atas Belanja Modal pada Anggaran

Pemerintah Daerah dalam Hubungannya dengan Belanja Pemeliharaan dan Sumber Pendapatan. Jurnal Akuntansi Pemerintah (Vol. 2 No. 2): 17-32.

Choate, Pat. 1981. The Case for a National Capital Budget. Public Budgeting and Finance (Winter): 21-26

Halim, Abdul. 2002. Akuntansi Keuangan Daerah. Jakarta: Salemba Empat. Indriantoro, N. 1999. Metodologi Penelitian Bisnis: Untuk Akuntansi dan Manajemen.

Yogyakarta: BPFE. Kamensky, John M. 2004. Budgeting for State and Local Infrastructure: Developing a

Strategy. Public Budgeting and Finance (Autumn): 3-17. Mahsun, Moh, Firma Sulistiyowati, & Heribertus A. Purwanugraha. 2011. Akuntansi Sektor

Publik. Yogyakarta: BPFE. Sidabutar, Rimbun C. D dan Timbul Sinaga (2012). Pengaruh Belanja Kendaraan Dinas

dan Nilai Kendaraan Dinas terhadap Belanja Pemeliharaan Kendaraan Dinas pada Dinas Provinsi Jawa Barat. JurnalEkonomidanBisnis (Vol. 3 No.1): 11-22.

_______, Peraturan Menteri Dalam Negeri Nomor 13 Tahun 2006 Tentang Pedoman Pengelolaan Keuangan Daerah.

_______, Peraturan Menteri Dalam Negeri Nomor 17 Tahun 2007 Tentang Pedoman Teknis Pengelolaan Barang Milik Daerah

_______, Peraturan Pemerintah Nomor 24 Tahun 2005 Tentang Standar Akuntansi Pemerintah.

_______, Undang-Undang Republik Indonesia Nomor 17 Tahun 2003 Tentang Keuangan Negara.

_______, Undang-Undang Republik Indonesia Nomor 32 Tahun 2004 Tentang Pemerintah Daerah