Embed Size (px)

Citation preview

The Accounting Information System

CHAPTER

3

The Accounting Information The Accounting Information SystemSystem

• The system of:The system of:– Collecting and processing transaction dataCollecting and processing transaction data

– Communicating financial information to Communicating financial information to interested partiesinterested parties

Accounting EquationAccounting Equation

• Assets = Liabilities + Shareholders’ EquityAssets = Liabilities + Shareholders’ Equity

• The accounting equation must always The accounting equation must always balancebalance

Accounting TransactionsAccounting Transactions

• Transactions are events that must be Transactions are events that must be recorded in the financial statementsrecorded in the financial statements

• Transaction analysis determines impact Transaction analysis determines impact on the accounting equationon the accounting equation

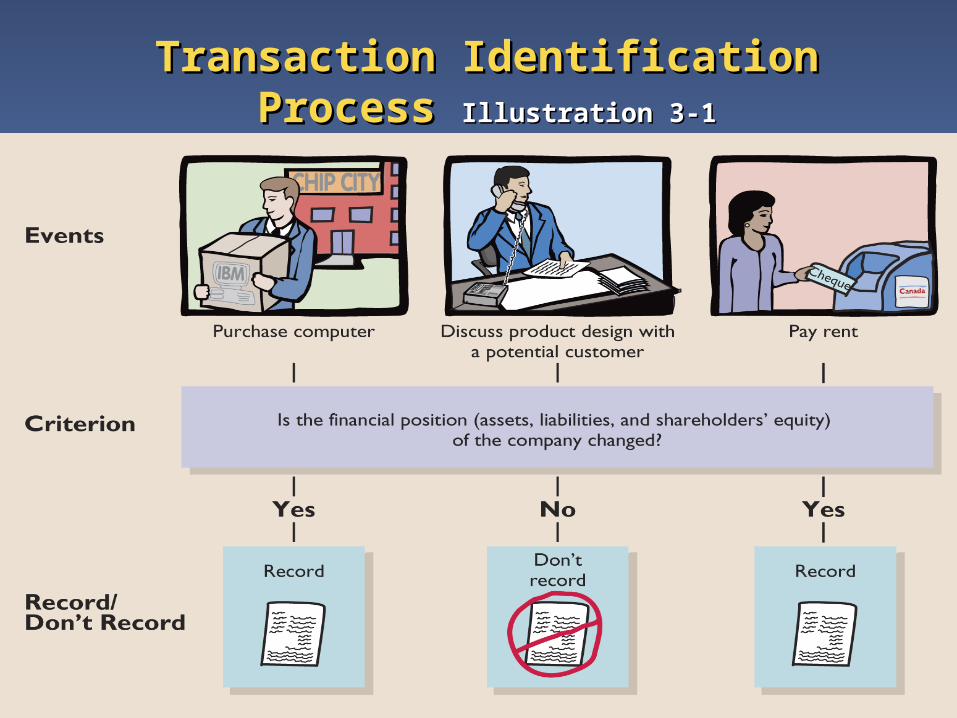

Transaction Identification Process Transaction Identification Process Illustration 3-1Illustration 3-1

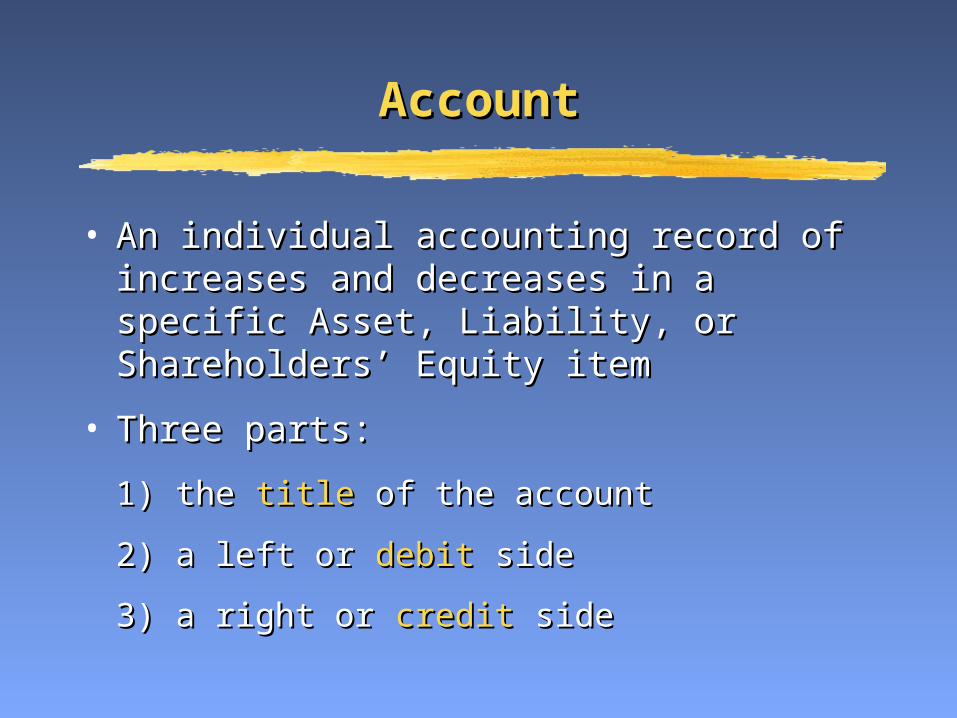

AccountAccount

• An individual accounting record of increases An individual accounting record of increases and decreases in a specific Asset, Liability, or and decreases in a specific Asset, Liability, or Shareholders’ Equity itemShareholders’ Equity item

• Three parts:Three parts:

1) the 1) the titletitle of the account of the account

2) a left or 2) a left or debitdebit side side

3) a right or 3) a right or creditcredit side side

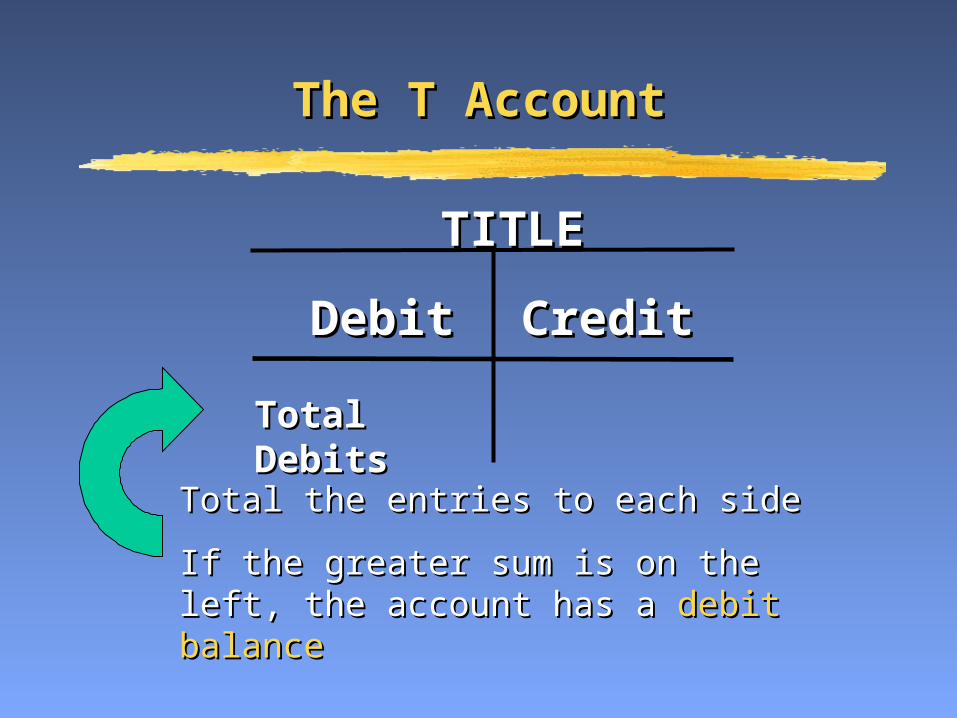

TITLETITLE

DEBITDEBIT CREDITCREDIT

The T AccountThe T Account

Total the entries to each sideTotal the entries to each side

If the greater sum is on the left, the account If the greater sum is on the left, the account has ahas a debit balancedebit balance

Total Total DebitsDebits

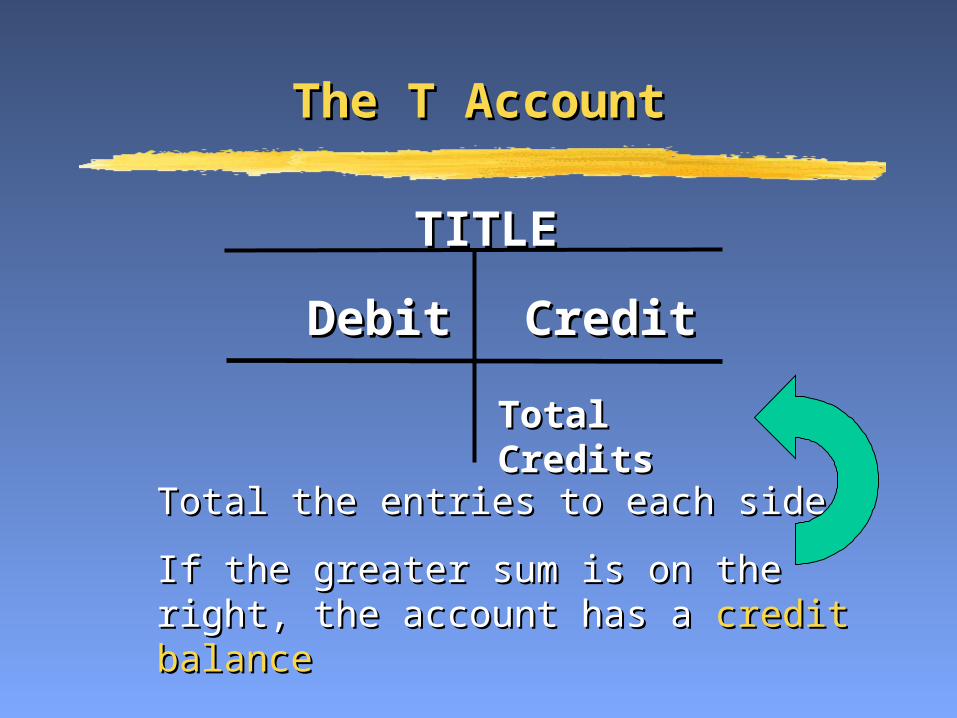

TITLETITLE

DebitDebit CreditCredit

The T AccountThe T Account

Total the entries to each sideTotal the entries to each side

If the greater sum is on the right, the If the greater sum is on the right, the account has aaccount has a credit balancecredit balance

Total CreditsTotal Credits

TITLETITLE

DebitDebit CreditCredit

The T AccountThe T Account

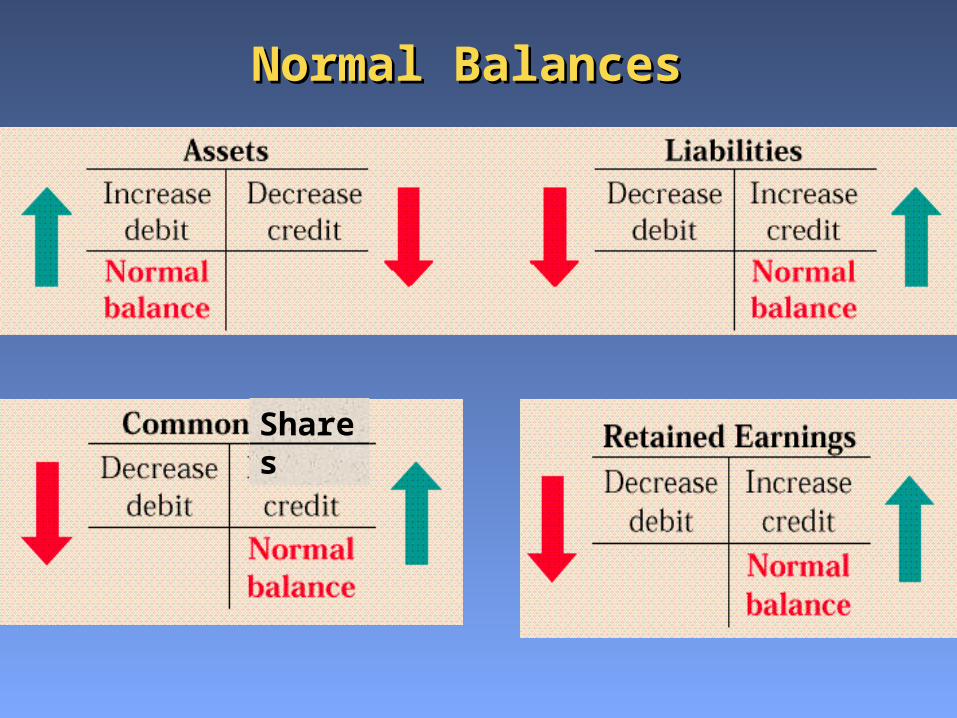

Normal BalancesNormal Balances

Shares

Normal BalancesNormal Balances

Expanded Accounting Equation Expanded Accounting Equation Illustration 3-10Illustration 3-10

Recording ProcessRecording ProcessIllustration 3-11Illustration 3-11

JournalJournal

• Accounting record where the transactions are Accounting record where the transactions are recorded in chronological orderrecorded in chronological order

• Types of journalsTypes of journals– Cash receiptsCash receipts– Cash disbursementsCash disbursements– SalesSales– PurchasesPurchases– GeneralGeneral

JournalsJournals

• Journals aid in the recording process by:Journals aid in the recording process by:– Disclosing in one place the complete effect of Disclosing in one place the complete effect of

a transactiona transaction– Providing a chronological record of Providing a chronological record of

transactionstransactions– Helping to prevent or locate errors as debit Helping to prevent or locate errors as debit

and credit amounts can be easily comparedand credit amounts can be easily compared

General LedgerGeneral Ledger

• Entire group of accounts maintained by a Entire group of accounts maintained by a companycompany

• Contains all the asset, liability, and Contains all the asset, liability, and shareholders’ equity accountsshareholders’ equity accounts

• Posting is the process of transferring Posting is the process of transferring information from the journals to the general information from the journals to the general ledger accountsledger accounts

Chart of AccountsChart of Accounts

• A listing of the company’s accountsA listing of the company’s accounts• The number of accounts in a company’s chart The number of accounts in a company’s chart

of accounts depends on the size, complexity, of accounts depends on the size, complexity, and type of business.and type of business.

• New accounts can be created at any time New accounts can be created at any time during the life of the companyduring the life of the company

• See sample chart of accounts on the See sample chart of accounts on the Toolkit Toolkit CDCD

PostingPosting

• The process of transferring journal entries to The process of transferring journal entries to ledger accountsledger accounts

• Posting should be done on a timely basisPosting should be done on a timely basis• This phase of the recording process This phase of the recording process

accumulates the effects of journalized accumulates the effects of journalized transactions in the individual accountstransactions in the individual accounts

Trial BalanceTrial Balance

• List of all the accounts and their balances List of all the accounts and their balances at a given timeat a given time

• Serves to prove the mathematical equality Serves to prove the mathematical equality of debits and credits after postingof debits and credits after posting

• Aids in the preparation of financial Aids in the preparation of financial statementsstatements

SIERRA CORPORATIONTrial Balance

October 31, 2004

DebitsDebits CreditsCredits

Cash Cash Advertising Advertising Supplies Supplies Prepaid Insurance Prepaid Insurance Office Equipment Office Equipment Notes Notes Payable Payable Accounts Accounts Payable Payable Unearned Unearned Service Revenue Service Revenue Common Common Shares Shares Dividends Dividends Service Revenue Service Revenue Salaries Expense Salaries Expense Rent ExpenseRent Expense

$15,200$15,2002,5002,500

6006005,0005,000

500500

4,0004,000900900

$28,700$28,700

$ 5,000$ 5,000

2,5002,500

1,2001,200

10,00010,000

10,00010,000

$28,700$28,700