Embed Size (px)

Citation preview

Master Thesis Investment Analysis

The Added Value of Structured Products as

a Portfolio

BsC FJP Heesters

University of Tilburg

amp

Van Lanschot Bankiers

July 2011

Master- student at University of Tilburg the Netherlands

2 | P a g e

Abstract

The financial service industry knows an area which has grown exceptionally fast in recent years namely

structured products These products more and more form a core business for both end consumers and product

manufacturers like banks One of the products developed en maintained by lsquoF van Lanschot Bankiersrsquo concerns

the Index Guarantee Contract (hereafter lsquoIGCrsquo) The product is held by a significant group of lsquoVan Lanschotsrsquo

clients as being part of a certain portfolio consisting of multiple financial instruments Not offered to the clients

though is a portfolio consisting entirely out of (a) structured product(s) Regarding the degree of specification

of this research the structured product of concern will be one specific IGC launched by lsquoVan Lanschot

Bankiersrsquo In order to realize a portfolio as such research needs to be conducted on the possible added value of

this portfolio relative to certain benchmarks This added value subsequently should be expressed in (a) certain

value(s) upon which specific conclusions can be drawn in historical- and in future perspective Once this added

value is determined translation is preferred to offer potential practical solutions These are the main issues

which are conducted in this research in order to give answer to the main research question What is the added

value of structured products as a portfolio

3 | P a g e

Introduction 4

1 Structured products and their Characteristics 5

11 Explaining Structured Products 5

12 Categorizing the Structured product 5

13 The Characteristics 6

14 Structured products in Time Perspective 7

15 Important Properties of the IGC 11

16 Valuing the IGC 14

17 Chapter Conclusion 16

2 Expressing lsquoadded valuersquo 17

21 General 17

22 The (regular) Sharpe Ratio 19

23 The Adjusted Sharpe Ratio 21

24 The Sortino Ratio 21

25 The Omega Sharpe Ratio 22

26 The Modified Sharpe Ratio 23

27 The Modified GUISE Ratio 24

28 Ratios vs Risk Indications 25

29 Chapter Conclusion 28

3 Historical Analysis 29

31 General 29

32 The performance of the IGC 29

33 The Benchmarks 30

34 The Influence of Important Features 31

35 Chapter Conclusion 33

4 Scenario Analysis 34

41 General 34

42 Base of Scenario Analysis 34

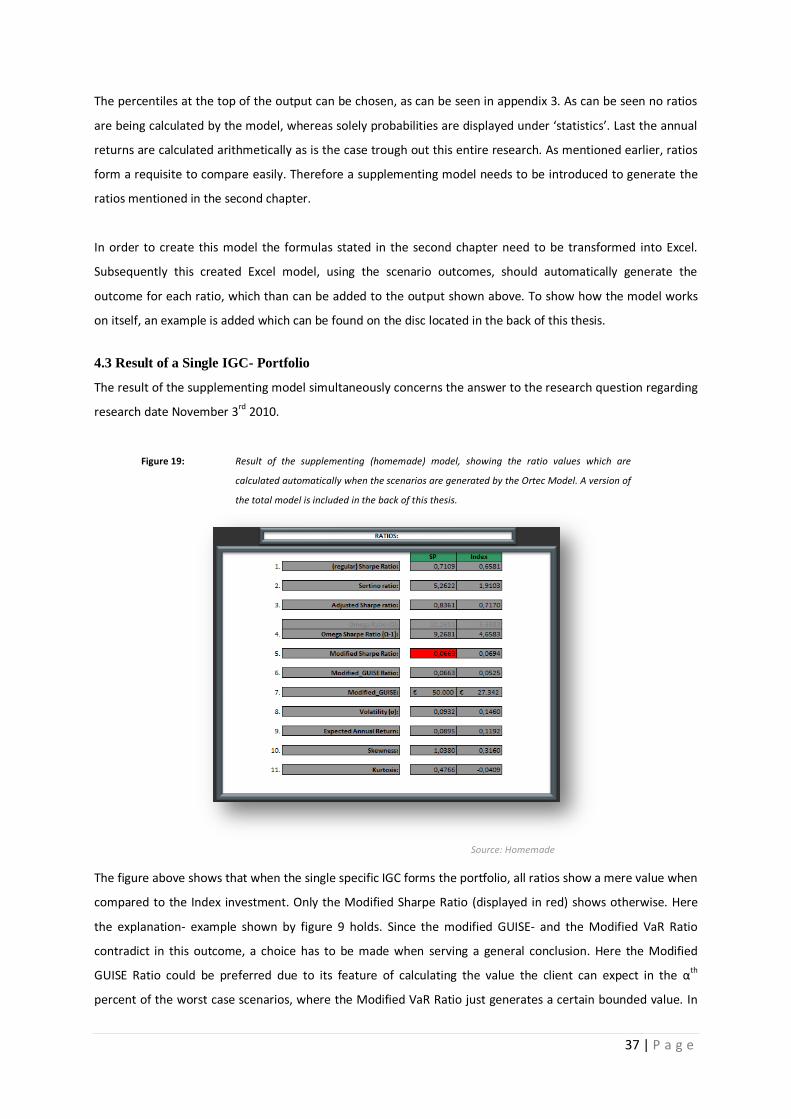

43 Result of a Single IGC- Portfolio 37

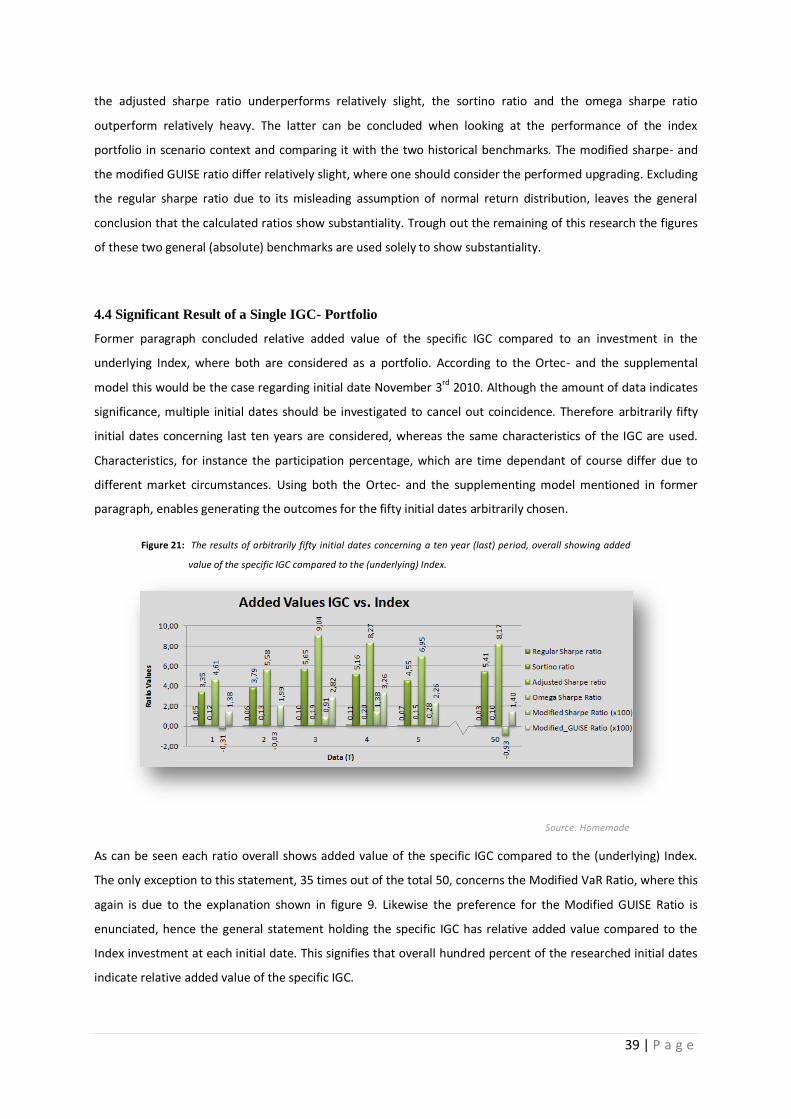

44 Significant Result of a Single IGC- Portfolio 39

45 Chapter Conclusion 40

5 Scenario Analysis multiple IGC- Portfolio 41

51 General 4141

52 The Diversification Effect 41

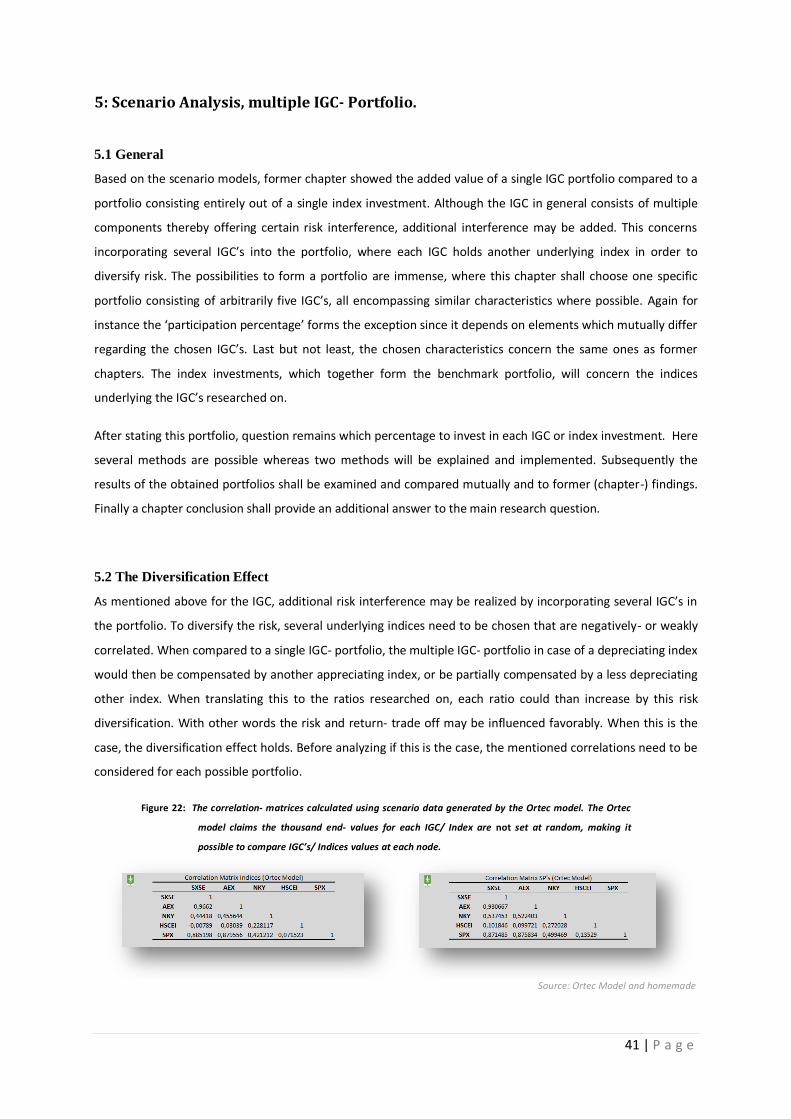

53 Optimizing Portfolios 42

54 Results of a multi- IGC Portfolio 44

55 Chapter Conclusion 45

6 Practical- solutions 46

61 General 46

62 A Bank focused solution 46

63 Chapter Conclusion 49

7 Conclusion 50

Appendix 52

References 76

4 | P a g e

Introduction

The financial service industry knows an area which has grown exceptionally fast in recent years namely

structured products These products more and more form a core business for both end consumers and product

manufacturers like banks One of the products developed en maintained by lsquoF van Lanschot Bankiersrsquo concerns

the lsquoIndex Guarantee Contractrsquo (hereafter lsquoIGCrsquo) The product is held by a significant group of lsquoVan Lanschotsrsquo

clients as being part of a certain portfolio consisting of multiple financial instruments Not offered to the clients

though is a portfolio consisting entirely out of (a) structured product(s) Regarding the degree of specification

of this research the structured product of concern will be one specific IGC launched by lsquoVan Lanschot

Bankiersrsquo In order to realize an IGC- portfolio as such research needs to be conducted on the possible added

value of this portfolio relative to certain benchmarks This leads to the main research question What is the

added value of structured products as a portfolio Current research shows that the added value of structured

products as a portfolio is that it can generate more return per unit risk for the owner of the portfolio Here

several ratios are consulted to express this added value whereas each ratio holds the return per unit risk Due

to different risk indications by holders of portfolios several are incorporated by the research each basically

embracing another ratio which best suits Current research historically shows that despite itsrsquo small sample

size altering the important determinant lsquoprovisionrsquo can result in the IGC- portfolio generating an added value

when compared to (some of) the fictitious portfolios containing stock - and government bond trackers

Furthermore current research shows that the same occurs when placing the IGC- portfolio in a future context

the underlying stock index being the benchmark Similar ratios are calculated to express this added value

Additionally a portfolio is introduced in future context which incorporates multiple IGCrsquos where each holds

another underlying stock index The diversification effect here shows the added value can be regarded as even

larger when compared to a single IGC portfolio Last serves as base to conduct future research on the matter

At the end current research provides possible practical solutions which may ameliorate some of the banksrsquo

(daily) businesses Before exercising these tough further research forms a requisite

5 | P a g e

1 Structured products and their Characteristics

11 Explaining Structured Products

In literature structured products are defined in many ways One definition and metaphoric approach is that a

structured product is like building a car1 The car represents the underlying asset and the carrsquos (paid for)

options represent the characteristics of the product An additional example to this approach Imagine you want

to drive from Paris to Milan for that purpose you buy a car You may think that the road could be long and

dangerous so you buy a car with an airbag and anti-lock brake system With these options you want to enlarge

the probability of arrival In the equity market buying an airbag and anti-lock brake system would be equal to

buying a capital guarantee on top of your stock investment This rather simple action combining stock

exposure with a capital guarantee would already form a structured product

As partially indicated by this example the overall purpose of a structured product is to actively influence the

reward for taking on risk which can be adjusted towards the financial needs and goals of the specific investor

Translated towards lsquoVan Lanschot Bankiersrsquo the financial needs of the specific investor are the possible

financial goals set by the bank and its client when consulted

Structured products come in many flavours regarding different components and characteristics In following

chapter the structured product chosen will be categorised characteristics and properties of the product will be

treated the valuation of each component of the product will be treated and the specific structured product

researched on shall be chosen

12 Categorizing the Structured product

The structured product researched on in this thesis concerns the lsquoIndex Guarantee Contractrsquo (hereafter lsquoIGCrsquo)

issued by lsquoVan Lanschot Bankiersrsquo in the Netherlands As partially indicated by name this specific structured

product falls under the category lsquoCapital Protectionrsquo as stated in the figure on the next page

Figure 1 All structured products can be divided into different categories taking the expected return and the risk as determinants

Source European Structured Investment Products Association (EUSIPA)

1 A Bluumlmke (2009) lsquoHow to invest in Structured products A guide for Investors and Asset Managers rsquo ISBN 978-0-470-74679

6 | P a g e

Therefore it can be considered a relatively safe product when compared to other structured products Within

this category differences of risk partially appear due to differences in fill ups of each component of the

structured product Generally a structured product which falls under the category lsquocapital protectionrsquo

incorporates a derivative part a bond part and provision Thus the derivative and the bond used in the product

partially determine the riskiness of the product The derivative used in the IGC concerns a call option whereas

the bond concerns a zero coupon bond issued by lsquoVan Lanschot Bankiersrsquo At the main research date

(November 3rd 2010) the bond had a long term rating of A- (lsquoStandard amp Poorrsquosrsquo) The lower this credit rating

the higher the probability of default of the specific fabricator Thus the credit rating of the fabricator of the

component of the structured product also determines the level of risk of the product in general For this risk

taken the investor though earns an additional return in the form of credit spread In case of default of the

fabricator the amount invested by the client can be lost entirely or can be recovered partially up to the full

Since in future analysis it is hard to assume a certain recovery rate one assumption made by this research is

that there is no probability of default This means when looking at future research that ceteris paribus the

higher the credit spread the higher the return of the product since no default is possible An additional reason

for the assumption made is that incorporating default fades some characterizing statistical measures of the

structured product researched on These measures will be treated in the first paragraph of second chapter

Before moving on to the higher degree of specification regarding the structured product researched on first

some characteristics (as the car options in the previous paragraph) need to be clarified

13 The Characteristics

As mentioned in the car example to explain a structured product the car contained some (paid for) options

which enlarged the probability of arrival Structured products also (can) contain some lsquopaid forrsquo characteristics

that enlarge the probability that a client meets his or her target in case it is set After explaining lsquothe carrsquo these

characteristics are explained next

The Underlying (lsquothe carrsquo)

The underlying of a structured product as chosen can either be a certain stock- index multiple stock- indices

real estate(s) or a commodity Focusing on stock- indices the main ones used by lsquoVan Lanschotrsquo in the IGC are

the Dutch lsquoAEX- index2rsquo the lsquoEuroStoxx50- index3rsquo the lsquoSampP500-index4rsquo the lsquoNikkei225- index5rsquo the lsquoHSCEI-

index6rsquo and a world basket containing multiple indices

The characteristic Guarantee Level

This is the level that indicates which part of the invested amount is guaranteed by the issuer at maturity of the

structured product This characteristic is mainly incorporated in structured products which belong to the

2 The AEX index Amsterdam Exchange index a share market index composed of Dutch companies that trade on Euronext Amsterdam

3 The EuroStoxx50 Index is a share index composed of the 50 largest companies in the Eurozone

4 The Standardamppoorrsquos500 is the leading index for Americarsquos share market and is composed of the largest 500 American companies 5 The Nikkei 225(NKY) is the leading index for the Tokyo share market and is composed of the largest 225 Japanese companies

6 The Hang Seng (HSCEI) is the leading index for the Hong Kong share market and is composed of the largest 45 Chinese companies

7 | P a g e

capital protection- category (figure 1) The guaranteed level can be upmost equal to 100 and can be realized

by the issuer through investing in (zero- coupon) bonds More on the valuation of the guarantee level will be

treated in paragraph 16

The characteristic The Participation Percentage

Another characteristic is the participation percentage which indicates to which extend the holder of the

structured product participates in the value mutation of the underlying This value mutation of the underlying

is calculated arithmetic by comparing the lsquocurrentrsquo value of the underlying with the value of the underlying at

the initial date The participation percentage can be under equal to or above hundred percent The way the

participation percentage is calculated will be explained in paragraph 16 since preliminary explanation is

required

The characteristic Duration

This characteristic indicates when the specific structured product when compared to the initial date will

mature Durations can differ greatly amongst structured products where these products can be rolled over into

the same kind of product when preferred by the investor or even can be ended before the maturity agreed

upon Two additional assumptions are made in this research holding there are no roll- over possibilities and

that the structured product of concern is held to maturity the so called lsquobuy and hold- assumptionrsquo

The characteristic Asianing (averaging)

This optional characteristic holds that during a certain last period of the duration of the product an average

price of the underlying is set as end- price Subsequently as mentioned in the participation percentage above

the value mutation of the underlying is calculated arithmetically This means that when the underlying has an

upward slope during the asianing period the client is worse off by this characteristic since the end- price will be

lower as would have been the case without asianing On the contrary a downward slope in de asianing period

gives the client a higher end- price which makes him better off This characteristic is optional regarding the last

24 months and is included in the IGC researched on

There are more characteristics which can be included in a structured product as a whole but these are not

incorporated in this research and therefore not treated Having an idea what a structured product is and

knowing the characteristics of concern enables explaining important properties of the IGC researched on But

first the characteristics mentioned above need to be specified This will be done in next paragraph where the

structured product as a whole and specifically the IGC are put in time perspective

14 Structured products in Time Perspective

Structured products began appearing in the UK retail investment market in the early 1990rsquos The number of

contracts available was very small and was largely offered to financial institutions But due to the lsquodotcom bustrsquo

8 | P a g e

in 2000 and the risk aversion accompanied it investors everywhere looked for an investment strategy that

attempted to limit the risk of capital loss while still participating in equity markets Soon after retail investors

and distributors embraced this new category of products known as lsquocapital protected notesrsquo Gradually the

products became increasingly sophisticated employing more complex strategies that spanned multiple

financial instruments This continued until the fall of 2008 The freezing of the credit markets exposed several

risks that werenrsquot fully appreciated by bankers and investors which lead to structured products losing some of

their shine7

Despite this exposure of several risks in 2008 structured product- subscriptions have remained constant in

2009 whereas it can be said that new sales simply replaced maturing products

Figure 2 Global investments in structured products subdivided by continent during recent years denoted in US billion Dollars

Source Structured Retail Productscom

Apparently structured products have become more attractive to investors during recent years Indeed no other

area of the financial services industry has grown as rapidly over the last few years as structured products for

private clients This is a phenomenon which has used Europe as a springboard8 and has reached Asia Therefore

structured products form a core business for both the end consumer and product manufacturers This is why

the structured product- field has now become a key business activity for banks as is the case with lsquoF van

Lanschot Bankiersrsquo

lsquoF van Lanschot Bankiersrsquo is subject to the Dutch market where most of its clients are located Therefore focus

should be specified towards the Dutch structured product- market

7 httpwwwasiaonecomBusiness

8 httpwwwpwmnetcomnewsfullstory

9 | P a g e

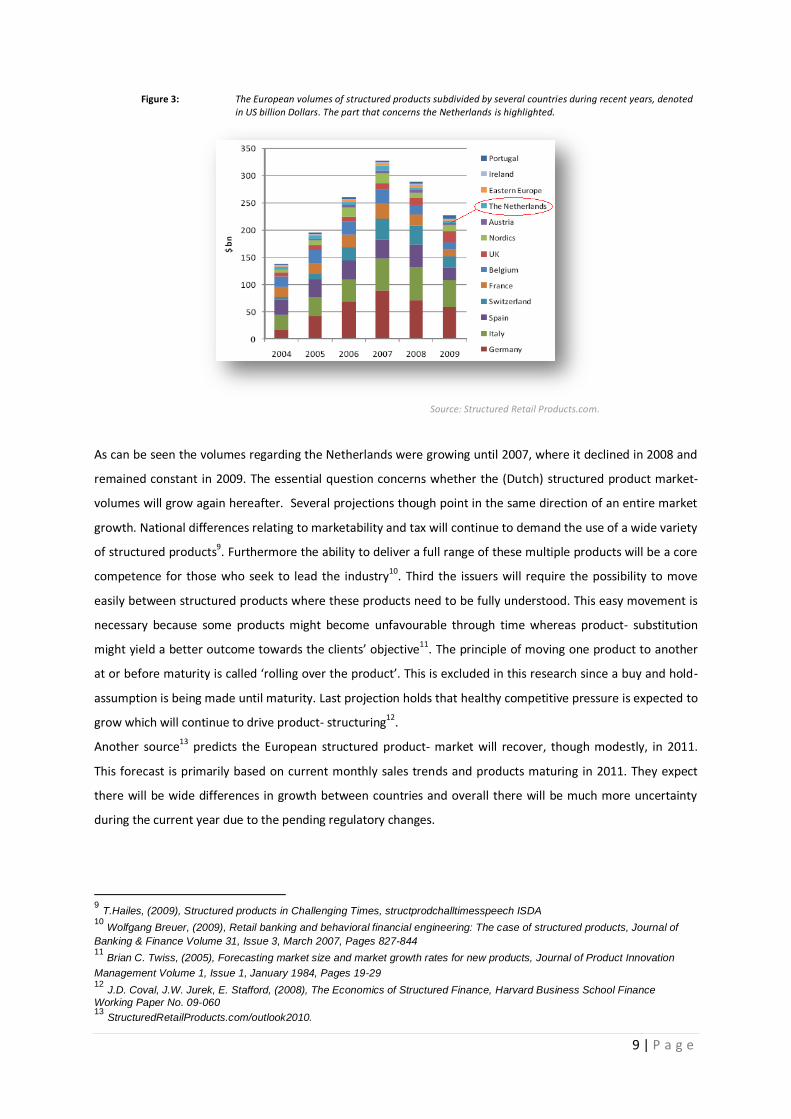

Figure 3 The European volumes of structured products subdivided by several countries during recent years denoted in US billion Dollars The part that concerns the Netherlands is highlighted

Source Structured Retail Productscom

As can be seen the volumes regarding the Netherlands were growing until 2007 where it declined in 2008 and

remained constant in 2009 The essential question concerns whether the (Dutch) structured product market-

volumes will grow again hereafter Several projections though point in the same direction of an entire market

growth National differences relating to marketability and tax will continue to demand the use of a wide variety

of structured products9 Furthermore the ability to deliver a full range of these multiple products will be a core

competence for those who seek to lead the industry10 Third the issuers will require the possibility to move

easily between structured products where these products need to be fully understood This easy movement is

necessary because some products might become unfavourable through time whereas product- substitution

might yield a better outcome towards the clientsrsquo objective11

The principle of moving one product to another

at or before maturity is called lsquorolling over the productrsquo This is excluded in this research since a buy and hold-

assumption is being made until maturity Last projection holds that healthy competitive pressure is expected to

grow which will continue to drive product- structuring12

Another source13 predicts the European structured product- market will recover though modestly in 2011

This forecast is primarily based on current monthly sales trends and products maturing in 2011 They expect

there will be wide differences in growth between countries and overall there will be much more uncertainty

during the current year due to the pending regulatory changes

9 THailes (2009) Structured products in Challenging Times structprodchalltimesspeech ISDA

10 Wolfgang Breuer (2009) Retail banking and behavioral financial engineering The case of structured products Journal of

Banking amp Finance Volume 31 Issue 3 March 2007 Pages 827-844 11 Brian C Twiss (2005) Forecasting market size and market growth rates for new products Journal of Product Innovation

Management Volume 1 Issue 1 January 1984 Pages 19-29 12

JD Coval JW Jurek E Stafford (2008) The Economics of Structured Finance Harvard Business School Finance

Working Paper No 09-060 13

StructuredRetailProductscomoutlook2010

10 | P a g e

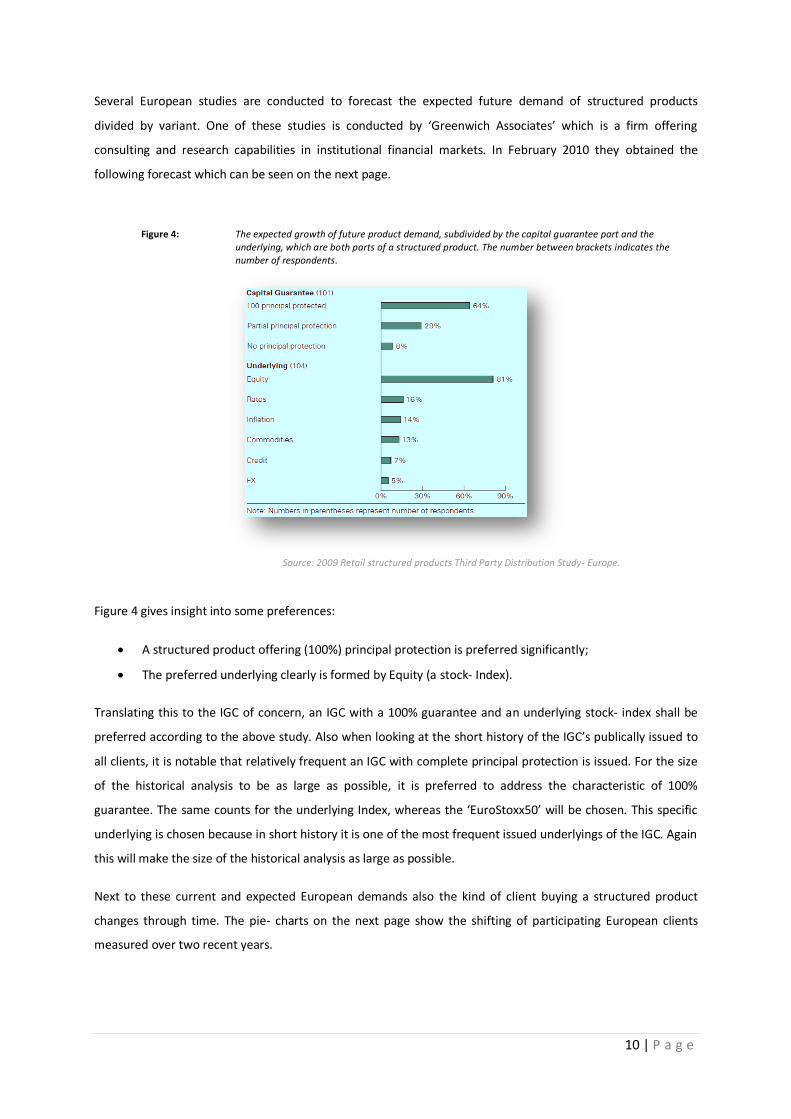

Several European studies are conducted to forecast the expected future demand of structured products

divided by variant One of these studies is conducted by lsquoGreenwich Associatesrsquo which is a firm offering

consulting and research capabilities in institutional financial markets In February 2010 they obtained the

following forecast which can be seen on the next page

Figure 4 The expected growth of future product demand subdivided by the capital guarantee part and the underlying which are both parts of a structured product The number between brackets indicates the number of respondents

Source 2009 Retail structured products Third Party Distribution Study- Europe

Figure 4 gives insight into some preferences

A structured product offering (100) principal protection is preferred significantly

The preferred underlying clearly is formed by Equity (a stock- Index)

Translating this to the IGC of concern an IGC with a 100 guarantee and an underlying stock- index shall be

preferred according to the above study Also when looking at the short history of the IGCrsquos publically issued to

all clients it is notable that relatively frequent an IGC with complete principal protection is issued For the size

of the historical analysis to be as large as possible it is preferred to address the characteristic of 100

guarantee The same counts for the underlying Index whereas the lsquoEuroStoxx50rsquo will be chosen This specific

underlying is chosen because in short history it is one of the most frequent issued underlyings of the IGC Again

this will make the size of the historical analysis as large as possible

Next to these current and expected European demands also the kind of client buying a structured product

changes through time The pie- charts on the next page show the shifting of participating European clients

measured over two recent years

11 | P a g e

Figure5 The structured product demand subdivided by client type during recent years

Important for lsquoVan Lanschotrsquo since they mainly focus on the relatively wealthy clients

Source 2009 Retail structured products Third Party Distribution Study- Europe

This is important towards lsquoVan Lanschot Bankiersrsquo since the bank mainly aims at relatively wealthy clients As

can be seen the shift towards 2009 was in favour of lsquoVan Lanschot Bankiersrsquo since relatively less retail clients

were participating in structured products whereas the two wealthiest classes were relatively participating

more A continuation of the above trend would allow a favourable prospect the upcoming years for lsquoVan

Lanschot Bankiersrsquo and thereby it embraces doing research on the structured product initiated by this bank

The two remaining characteristics as described in former paragraph concern lsquoasianingrsquo and lsquodurationrsquo Both

characteristics are simply chosen as such that the historical analysis can be as large as possible Therefore

asianing is included regarding a 24 month (last-) period and duration of five years

Current paragraph shows the following IGC will be researched

Now the specification is set some important properties and the valuation of this specific structured product

need to be examined next

15 Important Properties of the IGC

Each financial instrument has its own properties whereas the two most important ones concern the return and

the corresponding risk taken The return of an investment can be calculated using several techniques where

12 | P a g e

one of the basic techniques concerns an arithmetic calculation of the annual return The next formula enables

calculating the arithmetic annual return

(1) This formula is applied throughout the entire research calculating the returns for the IGC and its benchmarks

Thereafter itrsquos calculated in annual terms since all figures are calculated as such

Using the above technique to calculate returns enables plotting return distributions of financial instruments

These distributions can be drawn based on historical data and scenariorsquos (future data) Subsequently these

distributions visualize return related probabilities and product comparison both offering the probability to

clarify the matter The two financial instruments highlighted in this research concern the IGC researched on

and a stock- index investment Therefore the return distributions of these two instruments are explained next

To clarify the return distribution of the IGC the return distribution of the stock- index investment needs to be

clarified first Again a metaphoric example can be used Suppose there is an initial price which is displayed by a

white ball This ball together with other white balls (lsquosame initial pricesrsquo) are thrown in the Galton14 Machine

Figure 6 The Galton machine introduced by Francis Galton (1850) in order to explain normal distribution and standard deviation

Source httpwwwyoutubecomwatchv=9xUBhhM4vbM

The ball thrown in at top of the machine falls trough a consecutive set of pins and ends in a bar which

indicates the end price Knowing the end- price and the initial price enables calculating the arithmetic return

and thereby figure 6 shows a return distribution To be more specific the balls in figure 6 almost show a normal

14

Francis Galton inventor of the lsquoQuincunxrsquo also known as the Galton board thereby explaining normal distribution and the

standard deviation (1850)

13 | P a g e

return distribution of a stock- index investment where no relative extreme shocks are assumed which generate

(extreme) fat tails This is because at each pin the ball can either go left or right just as the price in the market

can go either up or either down no constraints included Since the return distribution in this case almost shows

a normal distribution (almost a symmetric bell shaped curve) the standard deviation (deviation from the

average expected value) is approximately the same at both sides This standard deviation is also referred to as

volatility (lsquoσrsquo) and is often used in the field of finance as a measurement of risk With other words risk in this

case is interpreted as earning a return that is different than (initially) expected

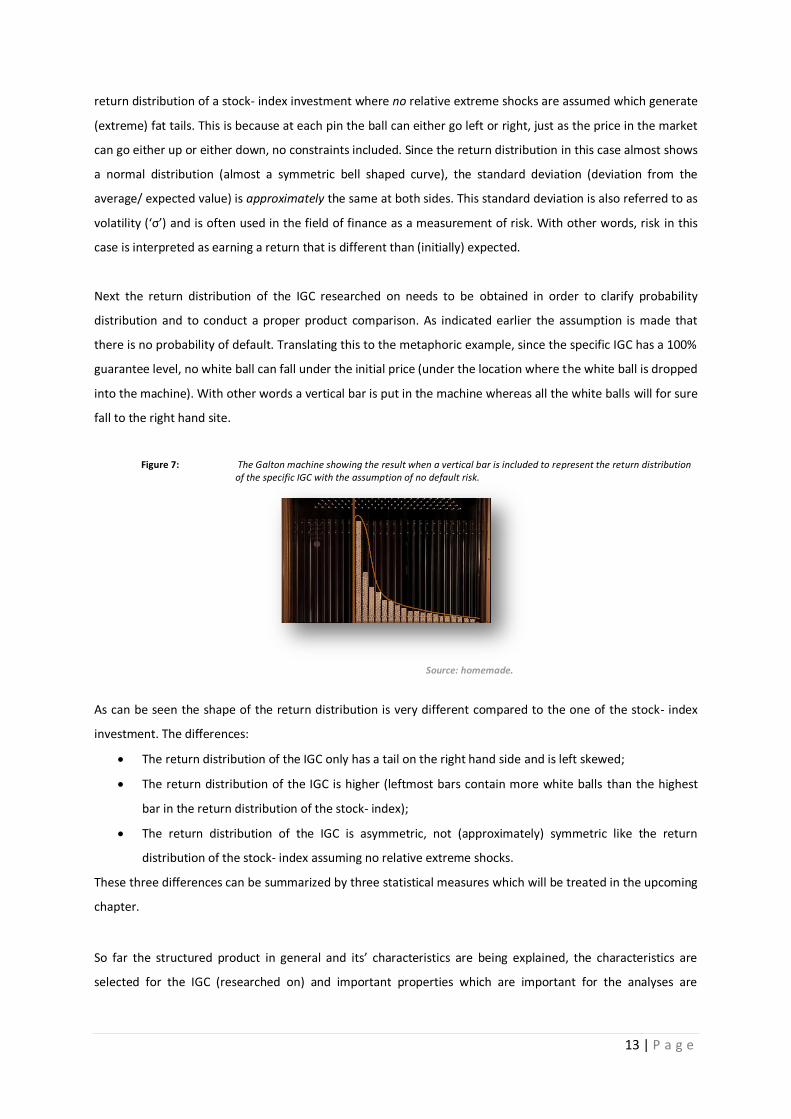

Next the return distribution of the IGC researched on needs to be obtained in order to clarify probability

distribution and to conduct a proper product comparison As indicated earlier the assumption is made that

there is no probability of default Translating this to the metaphoric example since the specific IGC has a 100

guarantee level no white ball can fall under the initial price (under the location where the white ball is dropped

into the machine) With other words a vertical bar is put in the machine whereas all the white balls will for sure

fall to the right hand site

Figure 7 The Galton machine showing the result when a vertical bar is included to represent the return distribution of the specific IGC with the assumption of no default risk

Source homemade

As can be seen the shape of the return distribution is very different compared to the one of the stock- index

investment The differences

The return distribution of the IGC only has a tail on the right hand side and is left skewed

The return distribution of the IGC is higher (leftmost bars contain more white balls than the highest

bar in the return distribution of the stock- index)

The return distribution of the IGC is asymmetric not (approximately) symmetric like the return

distribution of the stock- index assuming no relative extreme shocks

These three differences can be summarized by three statistical measures which will be treated in the upcoming

chapter

So far the structured product in general and itsrsquo characteristics are being explained the characteristics are

selected for the IGC (researched on) and important properties which are important for the analyses are

14 | P a g e

treated This leaves explaining how the value (or price) of an IGC can be obtained which is used to calculate

former explained arithmetic return With other words how each component of the chosen IGC is being valued

16 Valuing the IGC

In order to value an IGC the components of the IGC need to be valued separately Therefore each of these

components shall be explained first where after each onesrsquo valuation- technique is explained An IGC contains

following components

Figure 8 The components that form the IGC where each one has a different size depending on the chosen

characteristics and time dependant market- circumstances This example indicates an IGC with a 100

guarantee level and an inducement of the option value trough time provision remaining constant

Source Homemade

The figure above summarizes how the IGC could work out for the client Since a 100 guarantee level is

provided the zero coupon bond shall have an equal value at maturity as the clientsrsquo investment This value is

being discounted till initial date whereas the remaining is appropriated by the provision and the call option

(hereafter simply lsquooptionrsquo) The provision remains constant till maturity as the value of the option may

fluctuate with a minimum of nil This generates the possible outcome for the IGC to increase in value at

maturity whereas the surplus less the provision leaves the clientsrsquo payout This holds that when the issuer of

the IGC does not go bankrupt the client in worst case has a zero return

Regarding the valuation technique of each component the zero coupon bond and provision are treated first

since subtracting the discounted values of these two from the clientsrsquo investment leaves the premium which

can be used to invest in the option- component

The component Zero Coupon Bond

This component is accomplished by investing a certain part of the clientsrsquo investment in a zero coupon bond A

zero coupon bond is a bond which does not pay interest during the life of the bond but instead it can be

bought at a deep discount from its face value This is the amount that a bond will be worth when it matures

When the bond matures the investor will receive an amount equal to the initial investment plus the imputed

interest

15 | P a g e

The value of the zero coupon bond (component) depends on the guarantee level agreed upon the duration of

the IGC the term structure of interest rates and the credit spread The guaranteed level at maturity is assumed

to be 100 in this research thus the entire investment of the client forms the amount that needs to be

discounted towards the initial date This amount is subsequently discounted by a term structure of risk free

interest rates plus the credit spread corresponding to the issuer of the structured product The term structure

of the risk free interest rates incorporates the relation between time-to-maturity and the corresponding spot

rates of the specific zero coupon bond After discounting the amount of this component is known at the initial

date

The component Provision

Provision is formed by the clientsrsquo costs including administration costs management costs pricing costs and

risk premium costs The costs are charged upfront and annually (lsquotrailer feersquo) These provisions have changed

during the history of the IGC and may continue to do so in the future Overall the upfront provision is twice as

much as the annual charged provision To value the total initial provision the annual provisions need to be

discounted using the same discounting technique as previous described for the zero coupon bond When

calculated this initial value the upfront provision is added generating the total discounted value of provision as

shown in figure 8

The component Call Option

Next the valuation of the call option needs to be considered The valuation models used by lsquoVan Lanschot

Bankiersrsquo are chosen indirectly by the bank since the valuation of options is executed by lsquoKempenampCorsquo a

daughter Bank of lsquoVan Lanschot Bankiersrsquo When they have valued the specific option this value is

subsequently used by lsquoVan Lanschot Bankiersrsquo in the valuation of a specific structured product which will be

the specific IGC in this case The valuation technique used by lsquoKempenampCorsquo concerns the lsquoLocal volatility stock

behaviour modelrsquo which is one of the extensions of the classic Black- Scholes- Merton (BSM) model which

incorporates the volatility smile The extension mainly lies in the implied volatility been given a term structure

instead of just a single assumed constant figure as is the case with the BSM model By relaxing this assumption

the option price should embrace a more practical value thereby creating a more practical value for the IGC For

the specification of the option valuation technique one is referred to the internal research conducted by Pawel

Zareba15 In the remaining of the thesis the option values used to co- value the IGC are all provided by

lsquoKempenampCorsquo using stated valuation technique Here an at-the-money European call- option is considered with

a time to maturity of 5 years including a 24 months asianing

15 Pawel M Zareba (2010) Local Volatility Model paper for internal use only KempenampCo

16 | P a g e

An important characteristic the Participation Percentage

As superficially explained earlier the participation percentage indicates to which extend the holder of the

structured product participates in the value mutation of the underlying Furthermore the participation

percentage can be under equal to or above hundred percent As indicated by this paragraph the discounted

values of the components lsquoprovisionrsquo and lsquozero coupon bondrsquo are calculated first in order to calculate the

remaining which is invested in the call option Next the remaining for the call option is divided by the price of

the option calculated as former explained This gives the participation percentage at the initial date When an

IGC is created and offered towards clients which is before the initial date lsquovan Lanschot Bankiersrsquo indicates a

certain participation percentage and a certain minimum is given At the initial date the participation percentage

is set permanently

17 Chapter Conclusion

Current chapter introduced the structured product known as the lsquoIndex Guarantee Contract (IGC)rsquo a product

issued and fabricated by lsquoVan Lanschot Bankiersrsquo First the structured product in general was explained in order

to clarify characteristics and properties of this product This is because both are important to understand in

order to understand the upcoming chapters which will go more in depth

Next the structured product was put in time perspective to select characteristics for the IGC to be researched

Finally the components of the IGC were explained where to next the valuation of each was treated Simply

adding these component- values gives the value of the IGC Also these valuations were explained in order to

clarify material which will be treated in later chapters Next the term lsquoadded valuersquo from the main research

question will be clarified and the values to express this term will be dealt with

17 | P a g e

2 Expressing lsquoadded valuersquo

21 General

As the main research question states the added value of the structured product as a portfolio needs to be

examined The structured product and its specifications were dealt with in the former chapter Next the

important part of the research question regarding the added value needs to be clarified in order to conduct

the necessary calculations in upcoming chapters One simple solution would be using the expected return of

the IGC and comparing it to a certain benchmark But then another important property of a financial

instrument would be passed namely the incurred lsquoriskrsquo to enable this measured expected return Thus a

combination figure should be chosen that incorporates the expected return as well as risk The expected

return as explained in first chapter will be measured conform the arithmetic calculation So this enables a

generic calculation trough out this entire research But the second property lsquoriskrsquo is very hard to measure with

just a single method since clients can have very different risk indications Some of these were already

mentioned in the former chapter

A first solution to these enacted requirements is to calculate probabilities that certain targets are met or even

are failed by the specific instrument When using this technique it will offer a rather simplistic explanation

towards the client when interested in the matter Furthermore expected return and risk will indirectly be

incorporated Subsequently it is very important though that graphics conform figure 6 and 7 are included in

order to really understand what is being calculated by the mentioned probabilities When for example the IGC

is benchmarked by an investment in the underlying index the following graphic should be included

Figure 8 An example of the result when figure 6 and 7 are combined using an example from historical data where this somewhat can be seen as an overall example regarding the instruments chosen as such The red line represents the IGC the green line the Index- investment

Source httpwwwyoutubecom and homemade

In this graphic- example different probability calculations can be conducted to give a possible answer to the

specific client what and if there is an added value of the IGC with respect to the Index investment But there are

many probabilities possible to be calculated With other words to specify to the specific client with its own risk

indication one- or probably several probabilities need to be calculated whereas the question rises how

18 | P a g e

subsequently these multiple probabilities should be consorted with Furthermore several figures will make it

possibly difficult to compare financial instruments since multiple figures need to be compared

Therefore it is of the essence that a single figure can be presented that on itself gives the opportunity to

compare financial instruments correctly and easily A figure that enables such concerns a lsquoratiorsquo But still clients

will have different risk indications meaning several ratios need to be included When knowing the risk

indication of the client the appropriate ratio can be addressed and so the added value can be determined by

looking at the mere value of IGCrsquos ratio opposed to the ratio of the specific benchmark Thus this mere value is

interpreted in this research as being the possible added value of the IGC In the upcoming paragraphs several

ratios shall be explained which will be used in chapters afterwards One of these ratios uses statistical

measures which summarize the shape of return distributions as mentioned in paragraph 15 Therefore and

due to last chapter preliminary explanation forms a requisite

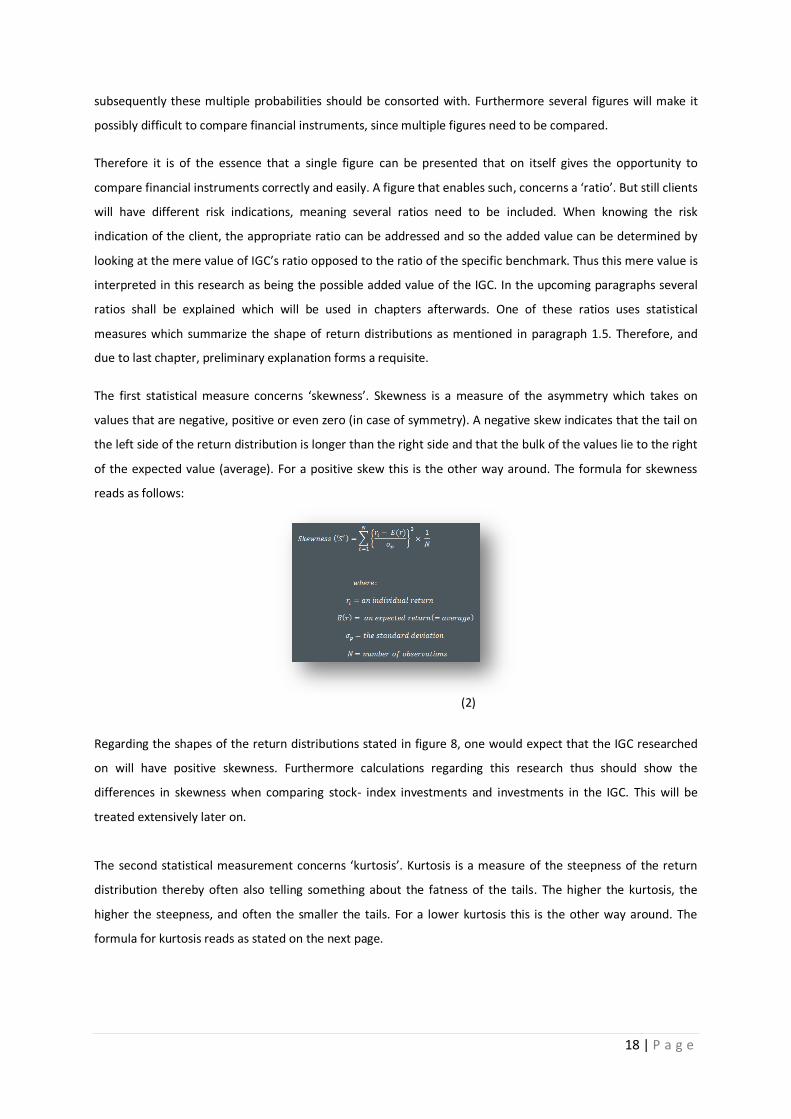

The first statistical measure concerns lsquoskewnessrsquo Skewness is a measure of the asymmetry which takes on

values that are negative positive or even zero (in case of symmetry) A negative skew indicates that the tail on

the left side of the return distribution is longer than the right side and that the bulk of the values lie to the right

of the expected value (average) For a positive skew this is the other way around The formula for skewness

reads as follows

(2)

Regarding the shapes of the return distributions stated in figure 8 one would expect that the IGC researched

on will have positive skewness Furthermore calculations regarding this research thus should show the

differences in skewness when comparing stock- index investments and investments in the IGC This will be

treated extensively later on

The second statistical measurement concerns lsquokurtosisrsquo Kurtosis is a measure of the steepness of the return

distribution thereby often also telling something about the fatness of the tails The higher the kurtosis the

higher the steepness and often the smaller the tails For a lower kurtosis this is the other way around The

formula for kurtosis reads as stated on the next page

19 | P a g e

(3) Regarding the shapes of the return distributions stated earlier one would expect that the IGC researched on

will have a higher kurtosis than the stock- index investment Furthermore calculations regarding this research

thus should show the differences in kurtosis when comparing stock- index investments and investments in the

IGC As is the case with skewness kurtosis will be treated extensively later on

The third and last statistical measurement concerns the standard deviation as treated in former chapter When

looking at the return distributions of both financial instruments in figure 8 though a significant characteristic

regarding the IGC can be noticed which diminishes the explanatory power of the standard deviation This

characteristic concerns the asymmetry of the return distribution regarding the IGC holding that the deviation

from the expected value (average) on the left hand side is not equal to the deviation on the right hand side

This means that when standard deviation is taken as the indicator for risk the risk measured could be

misleading This will be dealt with in subsequent paragraphs

22 The (regular) Sharpe Ratio

The first and most frequently used performance- ratio in the world of finance is the lsquoSharpe Ratiorsquo16 The

Sharpe Ratio also often referred to as ldquoReward to Variabilityrdquo divides the excess return of a financial

instrument over a risk-free interest rate by the instrumentsrsquo volatility

(4)

As (most) investors prefer high returns and low volatility17 the alternative with the highest Sharpe Ratio should

be chosen when assessing investment possibilities18 Due to its simplicity and its easy interpretability the

16 Wiliam FSharpe(1966) The sharpe Ratio the best of the journal of finance page 169-215 17 Adrian Blundell-Wignall (2007) An Overview of Hedge Funds and Structured products Issues in Leverage and Risk ISSN 0378-651X 18 RC Scott PAHorvath (1980) On The Directionof Preference for Moments of Higher Order Than The variance The journal of finance vol XXXV no4

20 | P a g e

Sharpe Ratio has become one of the most widely used risk-adjusted performance measures19 Yet there is a

major shortcoming of the Sharpe Ratio which needs to be considered when employing it The Sharpe Ratio

assumes a normal distribution (bell- shaped curve figure 6) regarding the annual returns by using the standard

deviation as the indicator for risk As indicated by former paragraph the standard deviation in this case can be

regarded as misleading since the deviation from the average value on both sides is unequal To show it could

be misleading to use this ratio is one of the reasons that his lsquograndfatherrsquo of all upcoming ratios is included in

this research The second and main reason is that this ratio needs to be calculated in order to calculate the

ratio which will be treated next

23 The Adjusted Sharpe Ratio

This performance- ratio belongs to the group of measures in which the properties lsquoskewnessrsquo and lsquokurtosisrsquo as

treated earlier in current chapter are explicitly included Its creators Pezier and White20 were motivated by the

drawbacks of the Sharpe Ratio especially those caused by the assumption of normally distributed returns and

therefore suggested an Adjusted Sharpe Ratio to overcome this deficiency This figures the reason why the

Sharpe Ratio is taken as the starting point and is adjusted for the shape of the return distribution by including

skewness and kurtosis

(5)

The formula and the specific figures incorporated by the formula are partially derived from a Taylor series

expansion of expected utility with an exponential utility function Without going in too much detail in

mathematics a Taylor series expansion is a representation of a function as an infinite sum of terms that are

calculated from the values of the functions derivatives at a single point The lsquominus 3rsquo in the formula is a

correction to make the kurtosis of a normal distribution equal to zero This can also be done for the skewness

whereas one could read lsquominus zerorsquo in the formula in order to make the skewness of a normal distribution

equal to zero With other words if the return distribution in fact would be normally distributed the Adjusted

Sharpe ratio would be equal to the regular Sharpe Ratio Substantially what the ratio does is incorporating a

penalty factor for negative skewness since this often means there is a large tail on the left hand side of the

expected return which can take on negative returns Furthermore a penalty factor is incorporated regarding

19 L R GoacutemeP Berrone MFranco Santos (2005) Compensation and Organisational Performance theory research and practice ISBN 978-0-7656-2251-8 20 JPeacutezier AWhite (2006) The Relative Merits of Investable Hedge Fund Indices and of Funds of Hedge Funds in Optimal Passive Portfolios ICMA Centre Discussion Papers in Finance DP 2006-10

21 | P a g e

excess kurtosis meaning the return distribution is lsquoflatterrsquo and thereby has larger tails on both ends of the

expected return Again here the left hand tail can possibly take on negative returns

24 The Sortino Ratio

This ratio is based on lower partial moments meaning risk is measured by considering only the deviations that

fall below a certain threshold This threshold also known as the target return can either be the risk free rate or

any other chosen return In this research the target return will be the risk free interest rate

(6)

One of the major advantages of this risk measurement is that no parametric assumptions like the formula of

the Adjusted Sharpe Ratio need to be stated and that there are no constraints on the form of underlying

distribution21 On the contrary the risk measurement is subject to criticism in the sense of sample returns

deviating from the target return may be too small or even empty Indeed when the target return would be set

equal to nil and since the assumption of no default and 100 guarantee is being made no return would fall

below the target return hence no risk could be measured Figure 7 clearly shows this by showing there is no

white ball left of the bar This notification underpins the assumption to set the risk free rate as the target

return Knowing the downward- risk measurement enables calculating the Sortino Ratio22

(7)

The Sortino Ratio is defined by the excess return over a minimum threshold here the risk free interest rate

divided by the downside risk as stated on the former page The ratio can be regarded as a modification of the

Sharpe Ratio as it replaces the standard deviation by downside risk Compared to the Omega Sharpe Ratio

21

C Keating WFShadwick (2002) A Universal Performance Measure The Finance Development Centre Jan2002 22

FASortino Rvan der Meer (1991) Sortino Ratio The Journal of Portfolio Management 17(4) 27-31

22 | P a g e

which will be treated hereafter negative deviations from the expected return are weighted more strongly due

to the second order of the lower partial moments (formula 6) This therefore expresses a higher risk aversion

level of the investor23

25 The Omega Sharpe Ratio

Another ratio that also uses lower partial moments concerns the Omega Sharpe Ratio24 Besides the difference

with the Sortino Ratio mentioned in former paragraph this ratio also looks at upside potential rather than

solely at lower partial moments like downside risk Therefore first downside- and upside potential need to be

stated

(8) (9)

Since both potential movements with as reference point the target risk free interest rate are included in the

ratio more is indicated about the total form of the return distribution as shown in figure 8 This forms the third

difference with respect to the Sortino Ratio which clarifies why both ratios are included while they are used in

this research for the same risk indication More on this risk indication and the linkage with the ratios elected

will be treated in paragraph 28 Now dividing the upside potential by the downside potential enables

calculating the Omega Ratio

(10)

Simply subtracting lsquoonersquo from this ratio generates the Omega Sharpe Ratio

23 Poddig Dichtl amp Petersmeier (2003) Understanding the Effect of Risk aversion p 135 24

C Keating WFShadwick (2002) A Universal Performance Measure The Finance Development Centre Jan2002

23 | P a g e

26 The Modified Sharpe Ratio

The following two ratios concern another category of ratios whereas these are based on a specific α of the

worst case scenarios The first ratio concerns the Modified Sharpe Ratio which is based on the modified value

at risk (MVaR) The in finance widely used regular value at risk (VaR) can be defined as a threshold value such

that the probability of loss on the portfolio over the given time horizon exceeds this value given a certain

probability level (lsquoαrsquo) The lsquoαrsquo chosen in this research is set equal to 10 since it is widely used25 One of the

main assumptions subject to the VaR is that the return distribution is normally distributed As discussed

previously this is not the case regarding the IGC through what makes the regular VaR misleading in this case

Therefore the MVaR is incorporated which as the regular VaR results in a certain threshold value but is

modified to the actual return distribution Therefore this calculation can be regarded as resulting in a more

accurate threshold value As the actual returns distribution is being used the threshold value can be found by

using a percentile calculation In statistics a percentile is the value of a variable below which a certain percent

of the observations fall In case of the assumed lsquoαrsquo this concerns the value below which 10 of the

observations fall A percentile holds multiple definitions whereas the one used by Microsoft Excel the software

used in this research concerns the following

(11)

When calculated the percentile of interest equally the MVaR is being calculated Next to calculate the

Modified Sharpe Ratio the lsquoMVaR Ratiorsquo needs to be calculated Simultaneously in order for the Modified

Sharpe Ratio to have similar interpretability as the former mentioned ratios namely the higher the better the

MVaR Ratio is adjusted since a higher (positive) MVaR indicates lower risk The formulas will clarify the matter

(12)

25

wwwInvestopediacom

24 | P a g e

When calculating the Modified Sharpe Ratio it is important to mention that though a non- normal return

distribution is accounted for it is based only on a threshold value which just gives a certain boundary This is

not what the client can expect in the α worst case scenarios This will be returned to in the next paragraph

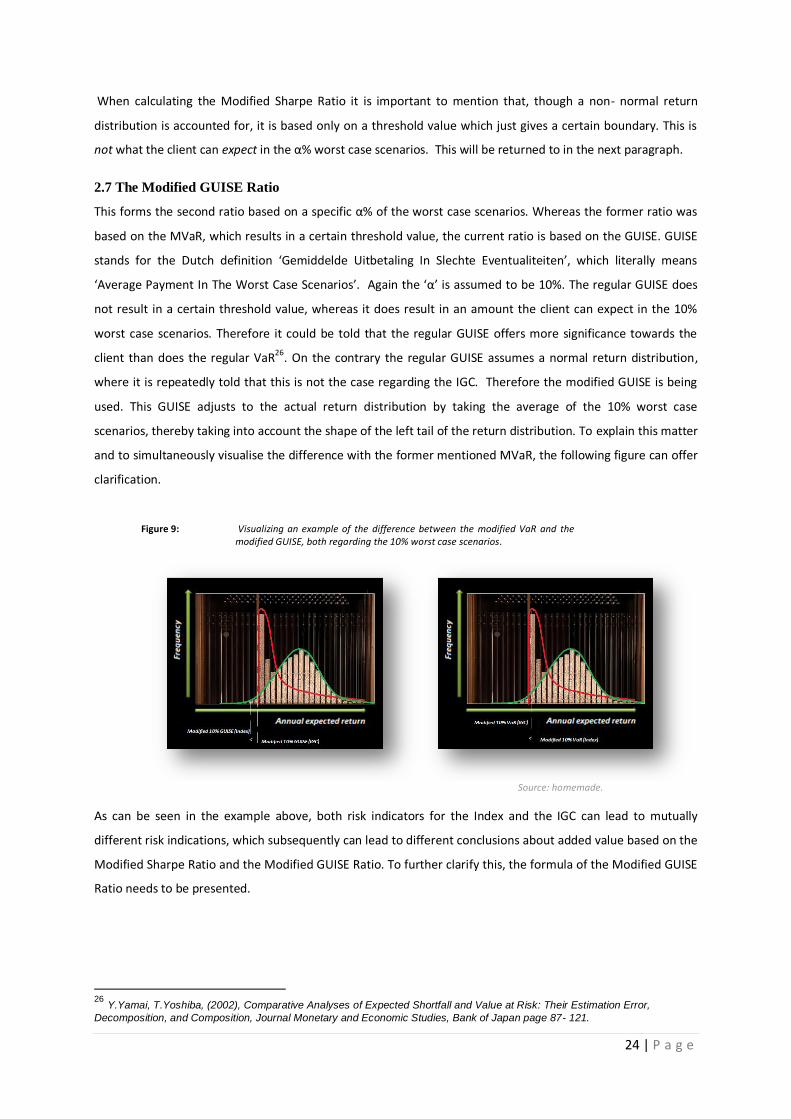

27 The Modified GUISE Ratio

This forms the second ratio based on a specific α of the worst case scenarios Whereas the former ratio was

based on the MVaR which results in a certain threshold value the current ratio is based on the GUISE GUISE

stands for the Dutch definition lsquoGemiddelde Uitbetaling In Slechte Eventualiteitenrsquo which literally means

lsquoAverage Payment In The Worst Case Scenariosrsquo Again the lsquoαrsquo is assumed to be 10 The regular GUISE does

not result in a certain threshold value whereas it does result in an amount the client can expect in the 10

worst case scenarios Therefore it could be told that the regular GUISE offers more significance towards the

client than does the regular VaR26 On the contrary the regular GUISE assumes a normal return distribution

where it is repeatedly told that this is not the case regarding the IGC Therefore the modified GUISE is being

used This GUISE adjusts to the actual return distribution by taking the average of the 10 worst case

scenarios thereby taking into account the shape of the left tail of the return distribution To explain this matter

and to simultaneously visualise the difference with the former mentioned MVaR the following figure can offer

clarification

Figure 9 Visualizing an example of the difference between the modified VaR and the modified GUISE both regarding the 10 worst case scenarios

Source homemade

As can be seen in the example above both risk indicators for the Index and the IGC can lead to mutually

different risk indications which subsequently can lead to different conclusions about added value based on the

Modified Sharpe Ratio and the Modified GUISE Ratio To further clarify this the formula of the Modified GUISE

Ratio needs to be presented

26

YYamai TYoshiba (2002) Comparative Analyses of Expected Shortfall and Value at Risk Their Estimation Error

Decomposition and Composition Journal Monetary and Economic Studies Bank of Japan page 87- 121

25 | P a g e

(13)

As can be seen the only difference with the Modified Sharpe Ratio concerns the denominator in the second (ii)

formula This finding and the possible mutual risk indication- differences stated above can indeed lead to

different conclusions about the added value of the IGC If so this will need to be dealt with in the next two

chapters

28 Ratios vs Risk Indications

As mentioned few times earlier clients can have multiple risk indications In this research four main risk

indications are distinguished whereas other risk indications are not excluded from existence by this research It

simply is an assumption being made to serve restriction and thereby to enable further specification These risk

indications distinguished amongst concern risk being interpreted as

1 lsquoFailure to achieve the expected returnrsquo

2 lsquoEarning a return which yields less than the risk free interest ratersquo

3 lsquoNot earning a positive returnrsquo

4 lsquoThe return earned in the 10 worst case scenariosrsquo

Each of these risk indications can be linked to the ratios described earlier where each different risk indication

(read client) can be addressed an added value of the IGC based on another ratio This is because each ratio of

concern in this case best suits the part of the return distribution focused on by the risk indication (client) This

will be explained per ratio next

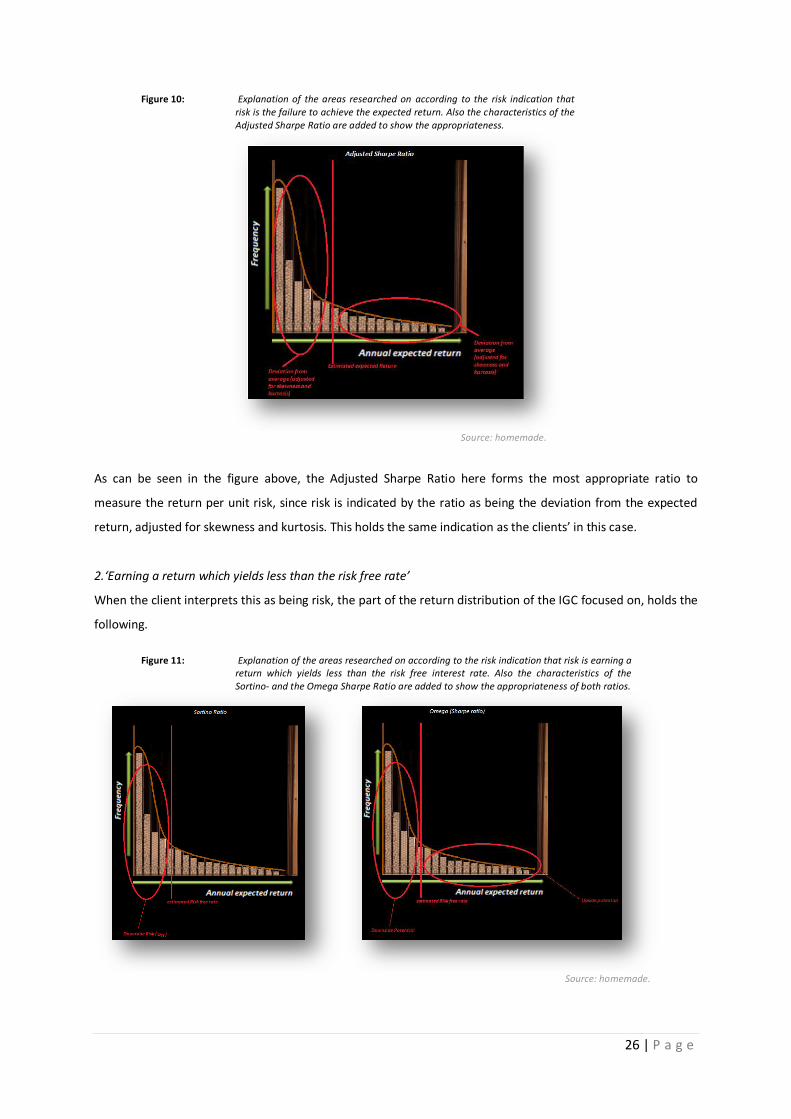

1lsquoFailure to achieve the expected returnrsquo

When the client interprets this as being risk the following part of the return distribution of the IGC is focused

on

26 | P a g e

Figure 10 Explanation of the areas researched on according to the risk indication that risk is the failure to achieve the expected return Also the characteristics of the Adjusted Sharpe Ratio are added to show the appropriateness

Source homemade

As can be seen in the figure above the Adjusted Sharpe Ratio here forms the most appropriate ratio to

measure the return per unit risk since risk is indicated by the ratio as being the deviation from the expected

return adjusted for skewness and kurtosis This holds the same indication as the clientsrsquo in this case

2lsquoEarning a return which yields less than the risk free ratersquo

When the client interprets this as being risk the part of the return distribution of the IGC focused on holds the

following

Figure 11 Explanation of the areas researched on according to the risk indication that risk is earning a return which yields less than the risk free interest rate Also the characteristics of the Sortino- and the Omega Sharpe Ratio are added to show the appropriateness of both ratios

Source homemade

27 | P a g e

These ratios are chosen most appropriate for the risk indication mentioned since both ratios indicate risk as

either being the downward deviation- or the total deviation from the risk free interest rate adjusted for the

shape (ie non-normality) Again this holds the same indication as the clientsrsquo in this case

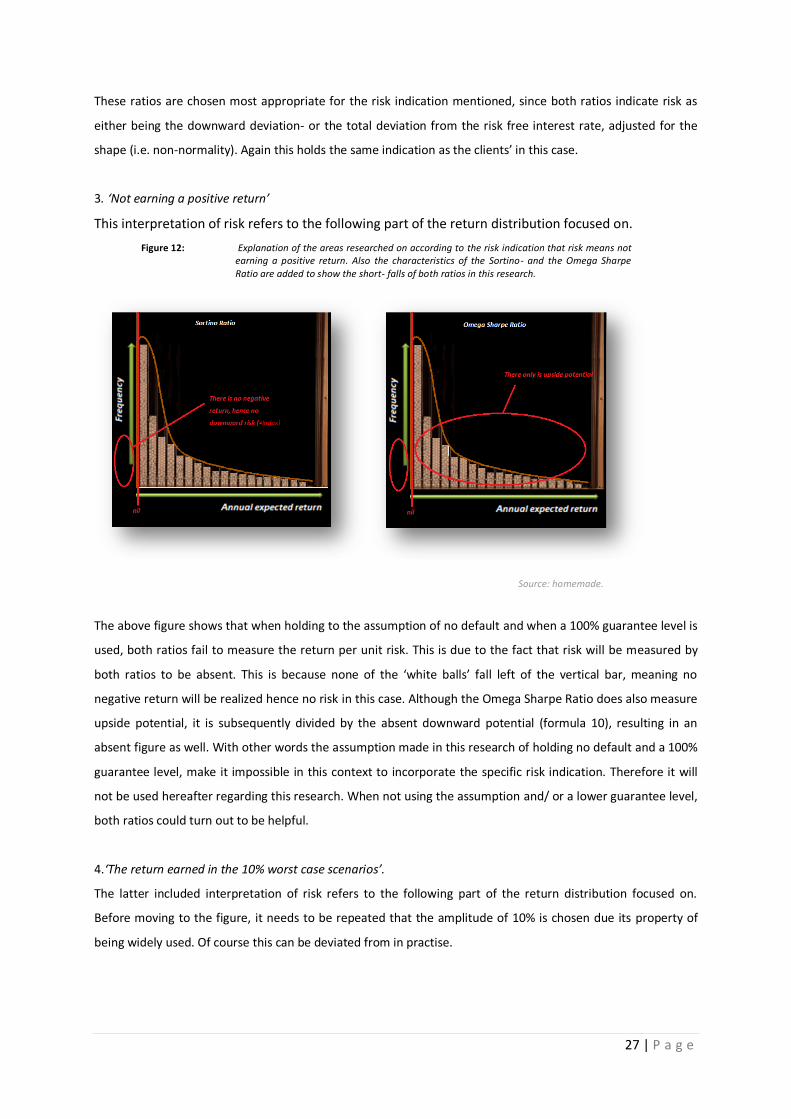

3 lsquoNot earning a positive returnrsquo

This interpretation of risk refers to the following part of the return distribution focused on

Figure 12 Explanation of the areas researched on according to the risk indication that risk means not earning a positive return Also the characteristics of the Sortino- and the Omega Sharpe Ratio are added to show the short- falls of both ratios in this research

Source homemade

The above figure shows that when holding to the assumption of no default and when a 100 guarantee level is

used both ratios fail to measure the return per unit risk This is due to the fact that risk will be measured by

both ratios to be absent This is because none of the lsquowhite ballsrsquo fall left of the vertical bar meaning no

negative return will be realized hence no risk in this case Although the Omega Sharpe Ratio does also measure

upside potential it is subsequently divided by the absent downward potential (formula 10) resulting in an

absent figure as well With other words the assumption made in this research of holding no default and a 100

guarantee level make it impossible in this context to incorporate the specific risk indication Therefore it will

not be used hereafter regarding this research When not using the assumption and or a lower guarantee level

both ratios could turn out to be helpful

4lsquoThe return earned in the 10 worst case scenariosrsquo

The latter included interpretation of risk refers to the following part of the return distribution focused on

Before moving to the figure it needs to be repeated that the amplitude of 10 is chosen due its property of

being widely used Of course this can be deviated from in practise

28 | P a g e

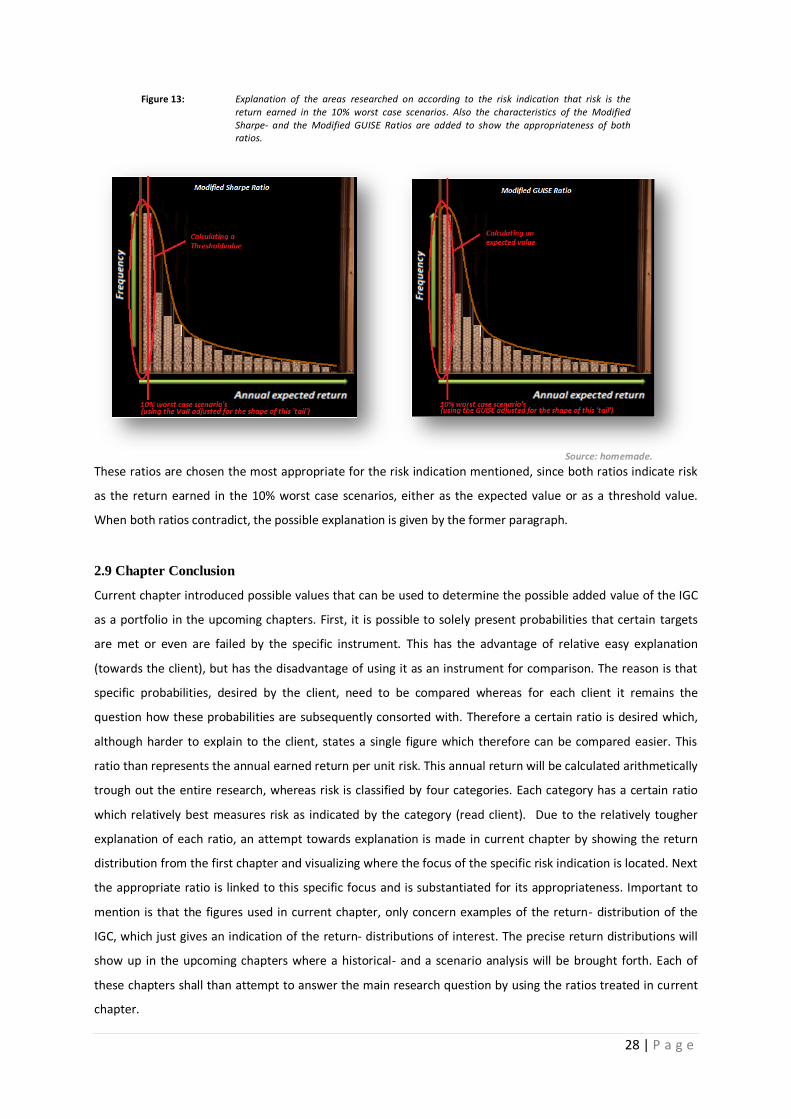

Figure 13 Explanation of the areas researched on according to the risk indication that risk is the return earned in the 10 worst case scenarios Also the characteristics of the Modified Sharpe- and the Modified GUISE Ratios are added to show the appropriateness of both ratios

Source homemade

These ratios are chosen the most appropriate for the risk indication mentioned since both ratios indicate risk

as the return earned in the 10 worst case scenarios either as the expected value or as a threshold value

When both ratios contradict the possible explanation is given by the former paragraph

29 Chapter Conclusion

Current chapter introduced possible values that can be used to determine the possible added value of the IGC

as a portfolio in the upcoming chapters First it is possible to solely present probabilities that certain targets

are met or even are failed by the specific instrument This has the advantage of relative easy explanation

(towards the client) but has the disadvantage of using it as an instrument for comparison The reason is that

specific probabilities desired by the client need to be compared whereas for each client it remains the

question how these probabilities are subsequently consorted with Therefore a certain ratio is desired which

although harder to explain to the client states a single figure which therefore can be compared easier This

ratio than represents the annual earned return per unit risk This annual return will be calculated arithmetically

trough out the entire research whereas risk is classified by four categories Each category has a certain ratio

which relatively best measures risk as indicated by the category (read client) Due to the relatively tougher

explanation of each ratio an attempt towards explanation is made in current chapter by showing the return

distribution from the first chapter and visualizing where the focus of the specific risk indication is located Next

the appropriate ratio is linked to this specific focus and is substantiated for its appropriateness Important to

mention is that the figures used in current chapter only concern examples of the return- distribution of the

IGC which just gives an indication of the return- distributions of interest The precise return distributions will

show up in the upcoming chapters where a historical- and a scenario analysis will be brought forth Each of

these chapters shall than attempt to answer the main research question by using the ratios treated in current

chapter

29 | P a g e

3 Historical Analysis

31 General

The first analysis which will try to answer the main research question concerns a historical one Here the IGC of

concern (page 10) will be researched whereas this specific version of the IGC has been issued 29 times in

history of the IGC in general Although not offering a large sample size it is one of the most issued versions in

history of the IGC Therefore additionally conducting scenario analyses in the upcoming chapters should all

together give a significant answer to the main research question Furthermore this historical analysis shall be

used to show the influence of certain features on the added value of the IGC with respect to certain

benchmarks Which benchmarks and features shall be treated in subsequent paragraphs As indicated by

former chapter the added value shall be based on multiple ratios Last the findings of this historical analysis

generate a conclusion which shall be given at the end of this chapter and which will underpin the main

conclusion

32 The performance of the IGC

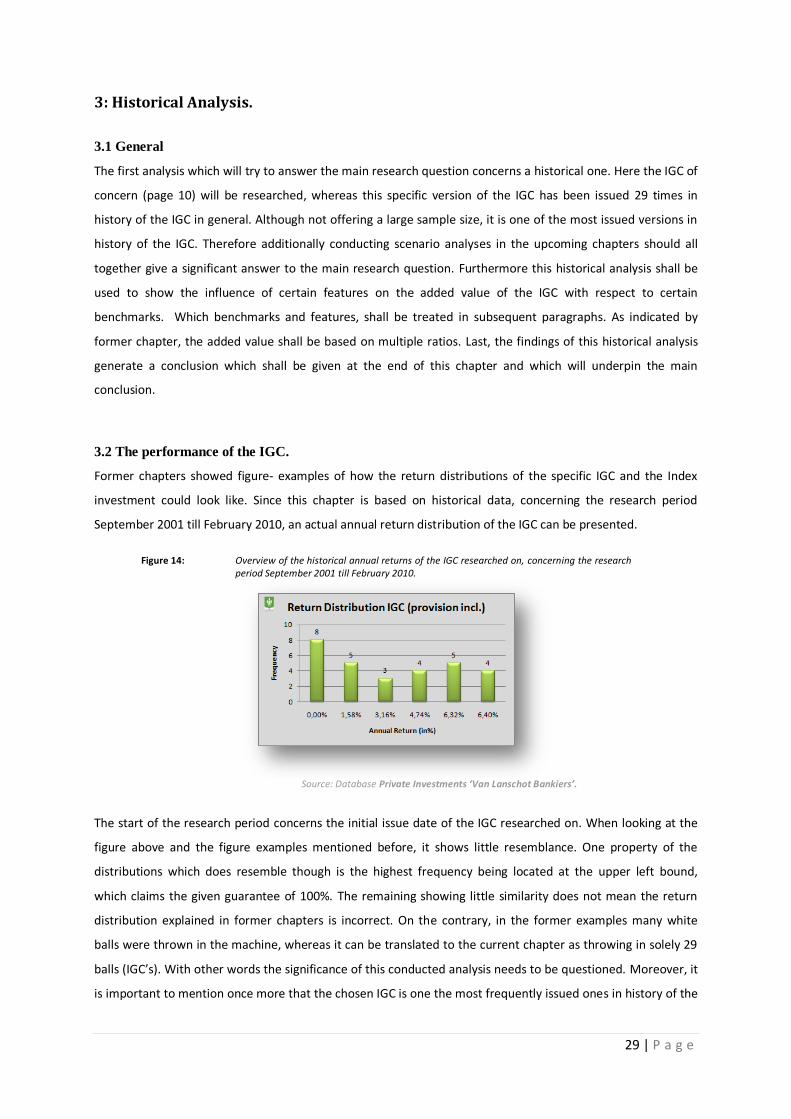

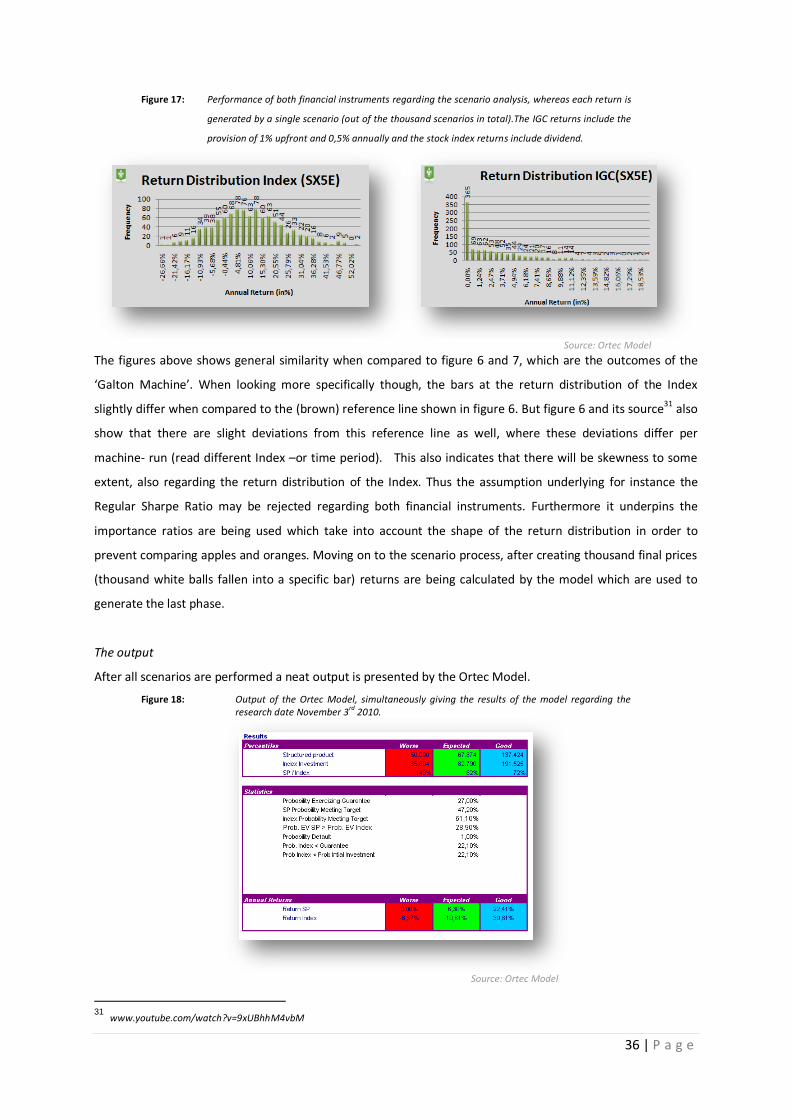

Former chapters showed figure- examples of how the return distributions of the specific IGC and the Index

investment could look like Since this chapter is based on historical data concerning the research period

September 2001 till February 2010 an actual annual return distribution of the IGC can be presented

Figure 14 Overview of the historical annual returns of the IGC researched on concerning the research period September 2001 till February 2010

Source Database Private Investments lsquoVan Lanschot Bankiersrsquo

The start of the research period concerns the initial issue date of the IGC researched on When looking at the

figure above and the figure examples mentioned before it shows little resemblance One property of the

distributions which does resemble though is the highest frequency being located at the upper left bound

which claims the given guarantee of 100 The remaining showing little similarity does not mean the return

distribution explained in former chapters is incorrect On the contrary in the former examples many white

balls were thrown in the machine whereas it can be translated to the current chapter as throwing in solely 29

balls (IGCrsquos) With other words the significance of this conducted analysis needs to be questioned Moreover it

is important to mention once more that the chosen IGC is one the most frequently issued ones in history of the

30 | P a g e

IGC Thus specifying this research which requires specifying the IGC makes it hard to deliver a significant

historical analysis Therefore a scenario analysis is added in upcoming chapters As mentioned in first paragraph

though the historical analysis can be used to show how certain features have influence on the added value of

the IGC with respect to certain benchmarks This will be treated in the second last paragraph where it is of the

essence to first mention the benchmarks used in this historical research

33 The Benchmarks

In order to determine the added value of the specific IGC it needs to be determined what the mere value of

the IGC is based on the mentioned ratios and compared to a certain benchmark In historical context six

fictitious portfolios are elected as benchmark Here the weight invested in each financial instrument is based

on the weight invested in the share component of real life standard portfolios27 at research date (03-11-2010)

The financial instruments chosen for the fictitious portfolios concern a tracker on the EuroStoxx50 and a

tracker on the Euro bond index28 A tracker is a collective investment scheme that aims to replicate the

movements of an index of a specific financial market regardless the market conditions These trackers are

chosen since provisions charged are already incorporated in these indices resulting in a more accurate

benchmark since IGCrsquos have provisions incorporated as well Next the fictitious portfolios can be presented

Figure 15 Overview of the fictitious portfolios which serve as benchmark in the historical analysis The weights are based on the investment weights indicated by the lsquoStandard Portfolio Toolrsquo used by lsquoVan Lanschot Bankiersrsquo at research date 03-11-2010

Source weights lsquostandard portfolio tool customer management at Van Lanschot Bankiersrsquo

Next to these fictitious portfolios an additional one introduced concerns a 100 investment in the

EuroStoxx50 Tracker On the one hand this is stated to intensively show the influences of some features which

will be treated hereafter On the other hand it is a benchmark which shall be used in the scenario analysis as

well thereby enabling the opportunity to generally judge this benchmark with respect to the IGC chosen

To stay in line with former paragraph the resemblance of the actual historical data and the figure- examples

mentioned in the former paragraph is questioned Appendix 1 shows the annual return distributions of the

above mentioned portfolios Before looking at the resemblance it is noticeable that generally speaking the

more risk averse portfolios performed better than the more risk bearing portfolios This can be accounted for

by presenting the performances of both trackers during the research period

27

Standard Portfolios obtained by using the Standard Portfolio tool (customer management) at lsquoVan Lanschotrsquo 28

EFFAS Euro Bond Index Tracker 3-5 years

31 | P a g e

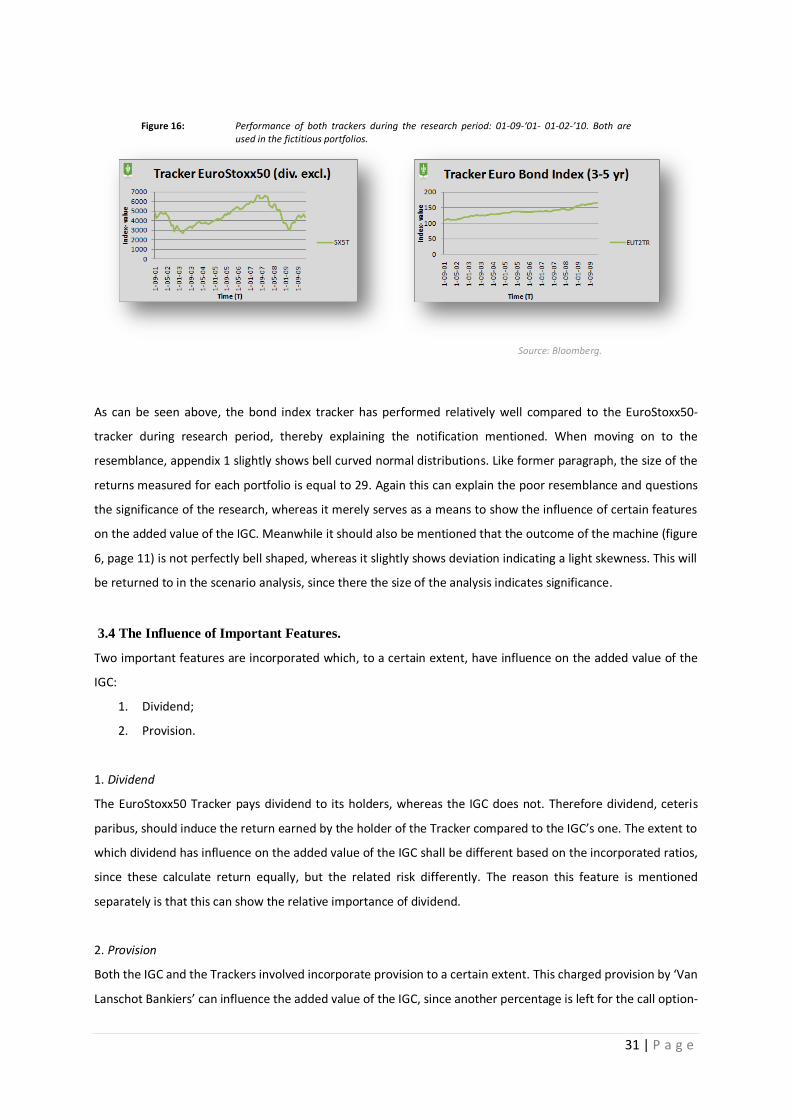

Figure 16 Performance of both trackers during the research period 01-09-lsquo01- 01-02-rsquo10 Both are used in the fictitious portfolios

Source Bloomberg

As can be seen above the bond index tracker has performed relatively well compared to the EuroStoxx50-

tracker during research period thereby explaining the notification mentioned When moving on to the

resemblance appendix 1 slightly shows bell curved normal distributions Like former paragraph the size of the

returns measured for each portfolio is equal to 29 Again this can explain the poor resemblance and questions

the significance of the research whereas it merely serves as a means to show the influence of certain features

on the added value of the IGC Meanwhile it should also be mentioned that the outcome of the machine (figure

6 page 11) is not perfectly bell shaped whereas it slightly shows deviation indicating a light skewness This will

be returned to in the scenario analysis since there the size of the analysis indicates significance

34 The Influence of Important Features

Two important features are incorporated which to a certain extent have influence on the added value of the

IGC

1 Dividend

2 Provision

1 Dividend

The EuroStoxx50 Tracker pays dividend to its holders whereas the IGC does not Therefore dividend ceteris

paribus should induce the return earned by the holder of the Tracker compared to the IGCrsquos one The extent to

which dividend has influence on the added value of the IGC shall be different based on the incorporated ratios

since these calculate return equally but the related risk differently The reason this feature is mentioned

separately is that this can show the relative importance of dividend

2 Provision

Both the IGC and the Trackers involved incorporate provision to a certain extent This charged provision by lsquoVan

Lanschot Bankiersrsquo can influence the added value of the IGC since another percentage is left for the call option-

32 | P a g e

component (as explained in the first chapter) Therefore it is interesting to see if the IGC has added value in

historical context when no provision is being charged With other words when setting provision equal to nil

still does not lead to an added value of the IGC no provision issue needs to be launched regarding this specific

IGC On the contrary when it does lead to a certain added value it remains the question which provision the

bank needs to charge in order for the IGC to remain its added value This can best be determined by the

scenario analysis due to its larger sample size

In order to show the effect of both features on the added value of the IGC with respect to the mentioned

benchmarks each feature is set equal to its historical true value or to nil This results in four possible

combinations where for each one the mentioned ratios are calculated trough what the added value can be

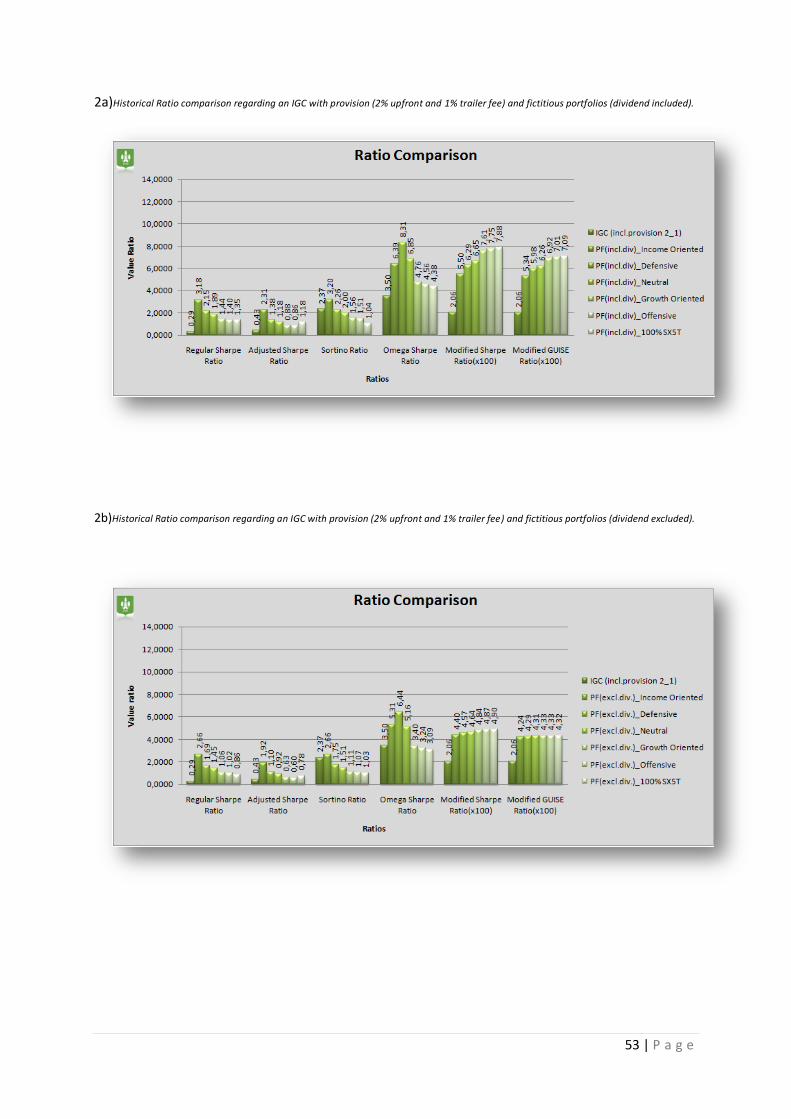

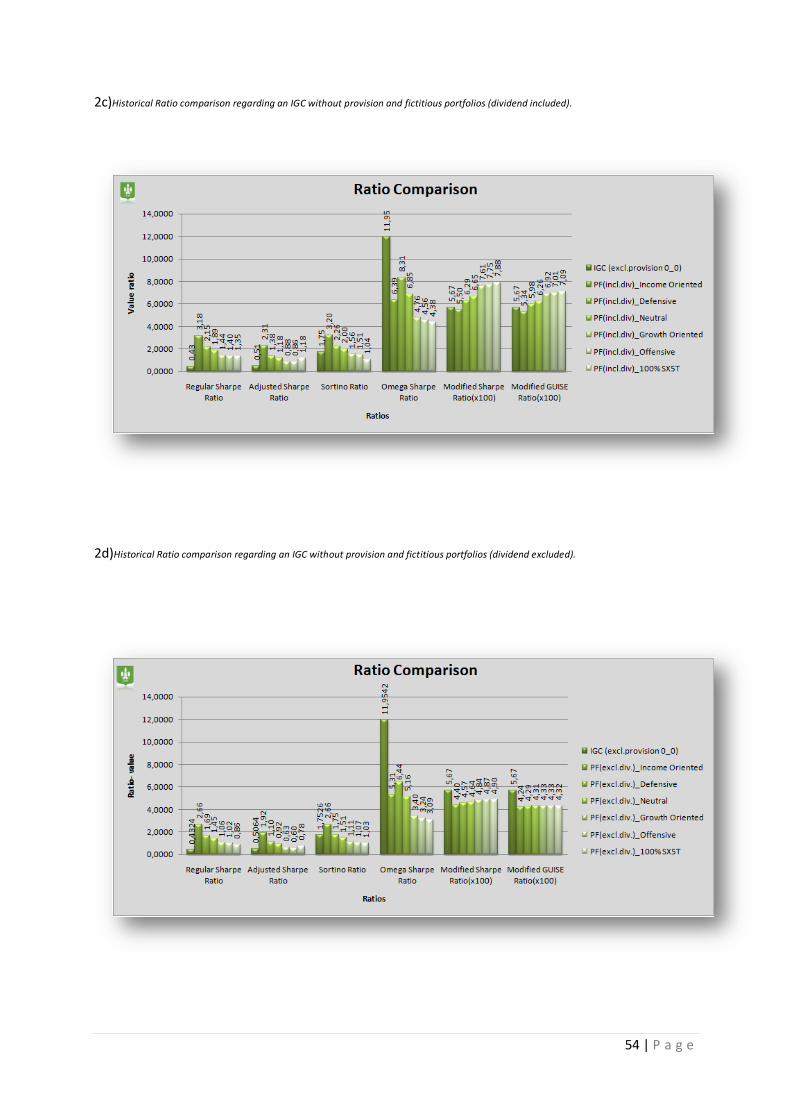

determined An overview of the measured ratios for each combination can be found in the appendix 2a-2d

From this overview first it can be concluded that when looking at appendix 2c setting provision to nil does

create an added value of the IGC with respect to some or all the benchmark portfolios This depends on the

ratio chosen to determine this added value It is noteworthy that the regular Sharpe Ratio and the Adjusted

Sharpe Ratio never show added value of the IGC even when provisions is set to nil Especially the Adjusted

Sharpe Ratio should be highlighted since this ratio does not assume a normal distribution whereas the Regular

Sharpe Ratio does The scenario analysis conducted hereafter should also evaluate this ratio to possibly confirm

this noteworthiness

Second the more risk averse portfolios outperformed the specific IGC according to most ratios even when the

IGCrsquos provision is set to nil As shown in former paragraph the European bond tracker outperformed when

compared to the European index tracker This can explain the second conclusion since the additional payout of

the IGC is largely generated by the performance of the underlying as shown by figure 8 page 14 On the

contrary the risk averse portfolios are affected slightly by the weak performing Euro index tracker since they

invest a relative small percentage in this instrument (figure 15 page 39)

Third dividend does play an essential role in determining the added value of the specific IGC as when

excluding dividend does make the IGC outperform more benchmark portfolios This counts for several of the

incorporated ratios Still excluding dividend does not create the IGC being superior regarding all ratios even

when provision is set to nil This makes dividend subordinate to the explanation of the former conclusion

Furthermore it should be mentioned that dividend and this former explanation regarding the Index Tracker are

related since both tend to be negatively correlated29

Therefore the dividends paid during the historical

research period should be regarded as being relatively high due to the poor performance of the mentioned

Index Tracker

29 K Bhanot SAMansi JK Wald (2008) Takeover risk and the correlation between stocks and bonds Journal of Emperical

Finance Volume 17 Issue 3 June 2010 pages 381-393

33 | P a g e

35 Chapter Conclusion

Current chapter historically researched the IGC of interest Although it is one of the most issued versions of the

IGC in history it only counts for a sample size of 29 This made the analysis insignificant to a certain level which

makes the scenario analysis performed in subsequent chapters indispensable Although there is low

significance the influence of dividend and provision on the added value of the specific IGC can be shown

historically First it had to be determined which benchmarks to use where five fictitious portfolios holding a

Euro bond- and a Euro index tracker and a full investment in a Euro index tracker were elected The outcome

can be seen in the appendix (2a-2d) where each possible scenario concerns including or excluding dividend

and or provision Furthermore it is elaborated for each ratio since these form the base values for determining

added value From this outcome it can be concluded that setting provision to nil does create an added value of

the specific IGC compared to the stated benchmarks although not the case for every ratio Here the Adjusted

Sharpe Ratio forms the exception which therefore is given additional attention in the upcoming scenario

analyses The second conclusion is that the more risk averse portfolios outperformed the IGC even when

provision was set to nil This is explained by the relatively strong performance of the Euro bond tracker during

the historical research period The last conclusion from the output regarded the dividend playing an essential

role in determining the added value of the specific IGC as it made the IGC outperform more benchmark

portfolios Although the essential role of dividend in explaining the added value of the IGC it is subordinated to

the performance of the underlying index (tracker) which it is correlated with

Current chapter shows the scenario analyses coming next are indispensable and that provision which can be

determined by the bank itself forms an issue to be launched

34 | P a g e

4 Scenario Analysis

41 General

As former chapter indicated low significance current chapter shall conduct an analysis which shall require high

significance in order to give an appropriate answer to the main research question Since in historical

perspective not enough IGCrsquos of the same kind can be researched another analysis needs to be performed

namely a scenario analysis A scenario analysis is one focused on future data whereas the initial (issue) date

concerns a current moment using actual input- data These future data can be obtained by multiple scenario

techniques whereas the one chosen in this research concerns one created by lsquoOrtec Financersquo lsquoOrtec Financersquo is

a global provider of technology and advisory services for risk- and return management Their global and

longstanding client base ranges from pension funds insurers and asset managers to municipalities housing

corporations and financial planners30 The reason their scenario analysis is chosen is that lsquoVan Lanschot

Bankiersrsquo wants to use it in order to consult a client better in way of informing on prospects of the specific

financial instrument The outcome of the analysis is than presented by the private banker during his or her

consultation Though the result is relatively neat and easy to explain to clients it lacks the opportunity to fast

and easily compare the specific financial instrument to others Since in this research it is of the essence that

financial instruments are being compared and therefore to define added value one of the topics treated in

upcoming chapter concerns a homemade supplementing (Excel-) model After mentioning both models which

form the base of the scenario analysis conducted the results are being examined and explained To cancel out

coincidence an analysis using multiple issue dates is regarded next Finally a chapter conclusion shall be given

42 Base of Scenario Analysis

The base of the scenario analysis is formed by the model conducted by lsquoOrtec Financersquo Mainly the model

knows three phases important for the user

The input

The scenario- process

The output

Each phase shall be explored in order to clarify the model and some important elements simultaneously

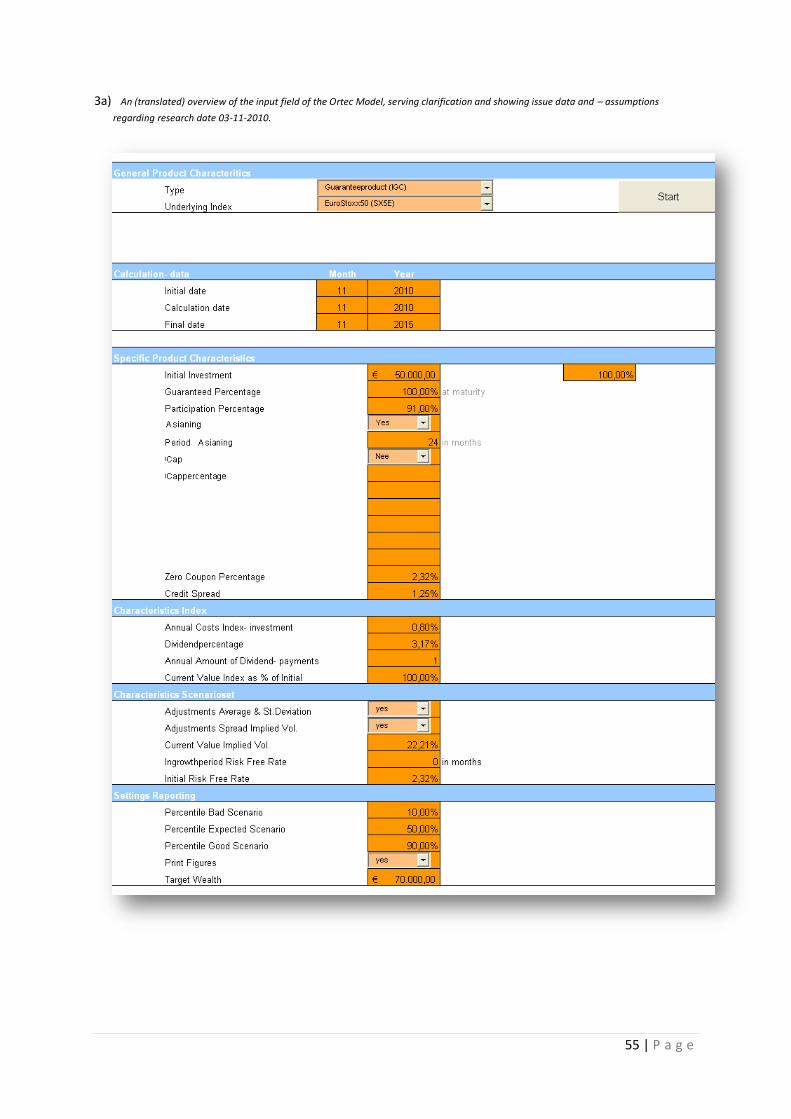

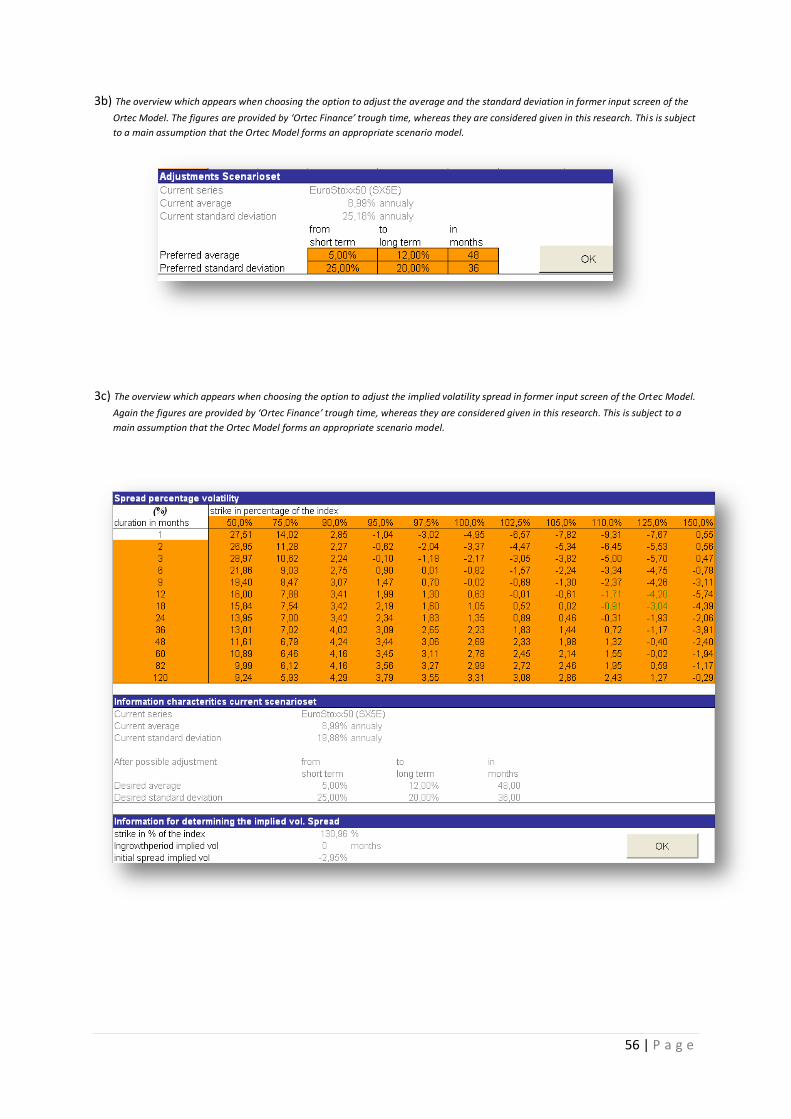

The input

Appendix 3a shows the translated version of the input field where initial data can be filled in Here lsquoBloombergrsquo

serves as data- source where some data which need further clarification shall be highlighted The first

percentage highlighted concerns the lsquoparticipation percentagersquo as this does not simply concern a given value

but a calculation which also uses some of the other filled in data as explained in first chapter One of these data

concerns the risk free interest rate where a 3-5 years European government bond is assumed as such This way

30

wwwOrtec-financecom

35 | P a g e

the same duration as the IGC researched on can be realized where at the same time a peer geographical region

is chosen both to conduct proper excess returns Next the zero coupon percentage is assumed equal to the

risk free interest rate mentioned above Here it is important to stress that in order to calculate the participation

percentage a term structure of the indicated risk free interest rates is being used instead of just a single

percentage This was already explained on page 15 The next figure of concern regards the credit spread as

explained in first chapter As it is mentioned solely on the input field it is also incorporated in the term

structure last mentioned as it is added according to its duration to the risk free interest rate This results in the

final term structure which as a whole serves as the discount factor for the guaranteed value of the IGC at

maturity This guaranteed value therefore is incorporated in calculating the participation percentage where