Embed Size (px)

Citation preview

Proceedings of the International Conference on Tourism, Hospitality and Marketing

(IC16Mauritius Conference) ISBN - 978-1-943579-19-8

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M624

1 www.globalbizresearch.org

The Banking Sector in Mauritius:

An Assessment of Service Quality from Customer Perspective

Jugurnath. B,

Department of Accounting and Finance,

Faculty of Law and Management,

University of Mauritius, Mauritius.

E-mail: [email protected]

Nowbutsing. J,

University of Mauritius, Mauritius.

Ramen. M,

Department of Accounting and Finance,

Faculty of Law and Management,

University of Mauritius, Mauritius.

__________________________________________________________________________________

Abstract In this paper, we study whether Mauritian banks are using service quality as a weapon to

compete on the market to satisfy customers. The goal set is to identify the interrelationships

between service quality, customer satisfaction and customer loyalty in the retail banking

sector in Mauritius. The study also aims to find out the most important attributes of service

quality in retail banks, which can be used to evaluate the characteristics of banking service

quality as perceived by customers. The study consists of a sample of 147 respondents. The

results indicate that the perceptions of the Mauritian banking customers far exceed their

expectations regarding the five dimensions of SERVQUAL model, which is a good indication.

At the same time, the findings show that responsiveness, assurance and empathy are the

important dimensions considered by the customers while assessing the quality of services

rendered by the Mauritian banks. The major contribution of the study is that it extends the

usage of SERVQUAL model. This study, fully focused on service quality issues, will help to

understand service dimensions issues for the banking sector in Mauritius.

__________________________________________________________________________

Key Words: SERVQUAL, Service Quality, Customer Satisfaction, Banking Sector in

Mauritius

Proceedings of the International Conference on Tourism, Hospitality and Marketing

(IC16Mauritius Conference) ISBN - 978-1-943579-19-8

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M624

2 www.globalbizresearch.org

1. Introduction

The Banking sector has always been dynamic and resilient with high levels of

competition. Banks use various strategies to protect their existing portfolio of customers and

build upon new ones so as to ensure business growth. Quality and marketing tools are the

essential factors that can contribute to the bank’s inner corporate objectives. In Mauritius,

there has been a continual propagation of banks through time, where only a few commercial

banks existed prior to its independence. At present, there are 21 banks, out of which 7 are

local banks, 8 are foreign-owned subsidiaries, 1 is a joint-venture and 5 are branches of

foreign banks. These banks are allowed to conduct banking transactions both onshore and

offshore. The banks in Mauritius are licensed and regulated by the Bank of Mauritius (BOM),

mandated by law as Central Bank to administer a strong regulatory framework. In order to

create a harmonization in the Mauritian banking industry, BOM has issued guidelines under

the name of Bank of Mauritius Act (2004), Banking Act (2004) and a series of rules that

oversee the daily operations of banks. The banking sector has played a key function in the

development of the Mauritian economy as they are expected to play in any other modern free-

orientated economy. This industry employs more than 5,000 professionals, contributing to

around 6% of GDP. For this study, only five of the most popular banks have been selected for

this paper, namely the state bank of Mauritius (SBM) ltd, the Mauritius Commercial Bank

(MCB) LTD, Barclays Bank Mauritius Limited, hongkong&shanghai bank cooperation

(HSBC) ltd and bramer banking corporation ltd. Service Quality has become a substantial

component of the banking industry – at least as a competitive tool. It becomes useful to

measure the effectiveness of service quality correctly. Hence, this study assesses the service

quality offered by commercial banks in Mauritius - from a customer’s perspective with

emphasis on what customers expect on the level of quality presently offered and from their

past experience. This study also examines the relationship between demographic factors of

bank customers and service quality using the SERVQUAL model.

2. SERVQUAL

Derived from two words namely service and quality, SERVQUAL is among the most

popular instruments used to measure service quality from a customer’s perspective.

SERVQUAL is a multi-scale instrument developed by Parasuraman, Berry and Zeithmal in

1985 and refined in 1991. Also known as the gap model, SERVQUAL is said to be one of the

best ways to measure service quality by many researchers. According to Brown et al (1993),

this service evaluation method has been proven consistent and reliable. The model is made up

of five dimensions, namely:

Tangibility – relates to the physical aspect related to the service. For instance a

bank’s physical appearance and the quality of the pamphlets it provides.

Proceedings of the International Conference on Tourism, Hospitality and Marketing

(IC16Mauritius Conference) ISBN - 978-1-943579-19-8

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M624

3 www.globalbizresearch.org

Reliability – refers to the potential of the providing efficiently and professionally the

promised service.

Responsiveness – concerns with the enthusiasm to assist customers and provide

prompt service.

Assurance – relate to the knowledge, competency, courtesy and ability of the

personnel delivering the service as well as the extent to which the system being used is

secured and credible

Empathy – refers to the extent to which the service provider cares for its customers

and its ability to provide for personalized service

Based on the above, it is crucial that banks assess the 5 dimensions in order to identify the

gaps in service quality by looking at the difference between customer expectations and

perceptions. Through these gaps bankers can recognize their shortfalls and consequently

address them in order to increase their competitive edge on the market.

3. Theoretical Framework

3.1 Service and Service Quality

A review of the existing literatures shows that there is quite a wide disparity in definitions

related to service. Proomprow (2003) came up with a very interesting play of words for

SERVICE which goes as S for Satisfaction, E for Expectation, R for Readiness , V for

Value, I for Interest, C for Courtesy and E for Efficiency. Many researches are of the view

that services cannot be counted nor tested prior to delivery thus businesses “find it difficult to

understand how customers perceive their services and evaluate them” (Parasuraman et al,

1985). The study pursue with the quality of service as a company’s business health is

reflected by the quality of service it provides. As underlined by (Parasuraman et al, 1992, p5)

“if the service quality is mediocre, the company is mediocre”. However, there is no single

definition for service quality. It varies from people to people and from situation to situation.

Service quality is a term used to express achievement obtained in a service. Parasuraman et al

(1985) viewed service quality as the degree and direction of discrepancy between customers’

service perception and expectations. They argued that service quality involves not only the

outcome but also the delivery process. Moreover, in a one of his researches conducted in

1988, these authors maintained that service quality is a function of the difference between

service expected and customers, perceptions of the actual service delivered. On his part,

Zeithaml (1987) described service quality as the consumer's judgment about an entity's

overall excellence or superiority. It is a form of attitude, and results from a comparison of

expectations to perceptions of performance received. Lewis (1989) defined service quality as

meeting customers’ needs, requirements and how well the service delivered meets customers’

expectations. Also, Lewis and Mitchell (1990) pointed out that service quality is linked to the

Proceedings of the International Conference on Tourism, Hospitality and Marketing

(IC16Mauritius Conference) ISBN - 978-1-943579-19-8

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M624

4 www.globalbizresearch.org

concepts of perceptions and expectations and that it is a requisite for the durability and

development of any company. Through these elements, it can easily be recognized that

service quality is one of the key drivers for a business to grow. Banks’policy makers have to

understand that for an eventual increase in profits they will have to secure a better position on

the market and to ensure customer loyalty, they need to use service quality as a competitive

approach.

3.2 Customer Satisfaction

Customer satisfaction relates to the customer’s feeling of fulfilment or disappointment

resulting from comparing a product’s perceived performance in relation to his to her

expectations (Kotler, 2000).From this definition, it is evident that to be able to satisfy

customer needs, customer expectations have to be known. Service providers, in particular

banks, have to provide the required products and services to match with customer needs. In

today’s competitive market if banks fail to plan their marketing strategy with customers in the

matrix, it is simply an eventual plan for their own failure. Customers are therefore among the

main parameters for successful business. As mentioned by Mittal & Kamakura (2001)

customer satisfaction is a key factor in formation of customer’s desires for future purchase.

According to Zeithaml et al. (1990), customer satisfaction is the result of a customers’

perception of the service quality relative to the expectation. Moreover, Looy et al. (2003)

defines customer satisfaction as the customer’s feeling regarding the gap between his or her

expectations towards a company, product or service and the perceived performance of the

company, product or service. Later on, Zeithaml et al (2009) stressed on customer

expectations as beliefs about a service that serves as standards or reference points to which

the performance of the service is judged. It was further affirmed by the same researcher that

knowing what the customer expects is the first and possibly most critical factor in delivering

quality service. ForJohnson et al , (1996) customer satisfaction can be interpreted as an

overall evaluation of service quality attributes or service attribute performance.

In order to combine the important elements pertaining to customer satisfaction, it seemed

necessary to drawn up a chain of cyclic reactions.

Proceedings of the International Conference on Tourism, Hospitality and Marketing

(IC16Mauritius Conference) ISBN - 978-1-943579-19-8

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M624

5 www.globalbizresearch.org

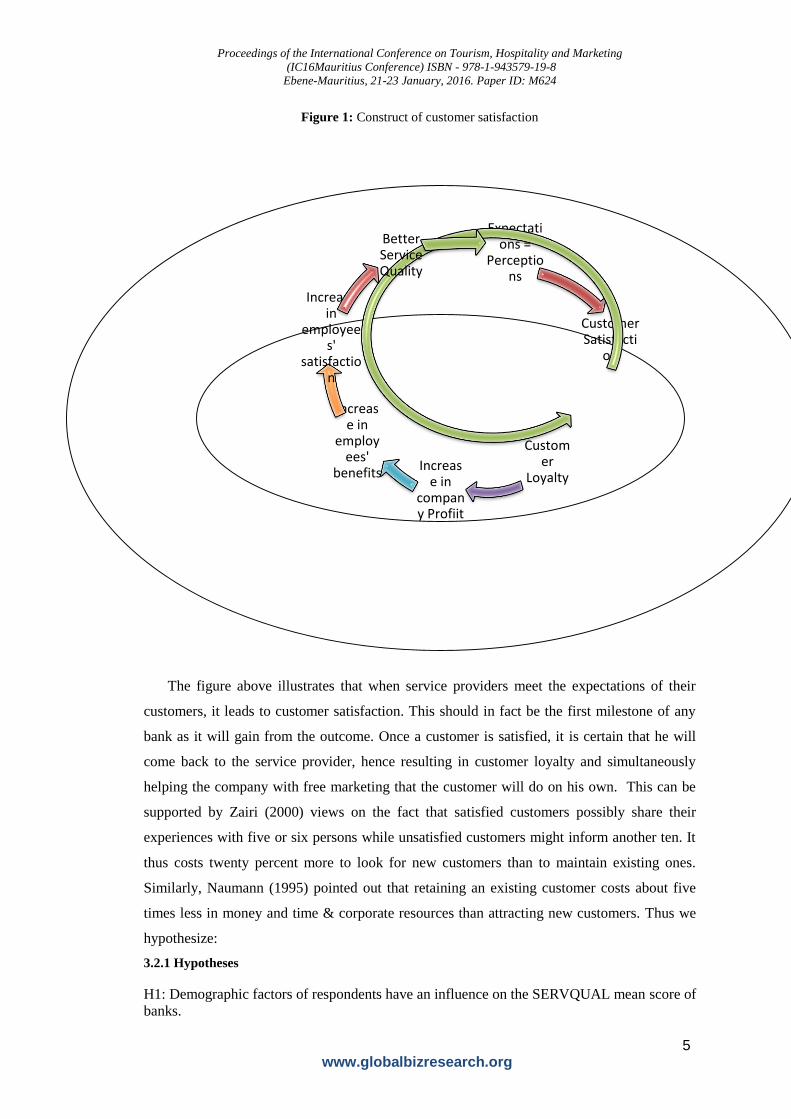

Figure 1: Construct of customer satisfaction

The figure above illustrates that when service providers meet the expectations of their

customers, it leads to customer satisfaction. This should in fact be the first milestone of any

bank as it will gain from the outcome. Once a customer is satisfied, it is certain that he will

come back to the service provider, hence resulting in customer loyalty and simultaneously

helping the company with free marketing that the customer will do on his own. This can be

supported by Zairi (2000) views on the fact that satisfied customers possibly share their

experiences with five or six persons while unsatisfied customers might inform another ten. It

thus costs twenty percent more to look for new customers than to maintain existing ones.

Similarly, Naumann (1995) pointed out that retaining an existing customer costs about five

times less in money and time & corporate resources than attracting new customers. Thus we

hypothesize:

3.2.1 Hypotheses

H1: Demographic factors of respondents have an influence on the SERVQUAL mean score of

banks.

Expectations =

Perceptions

Customer Satisfacti

on

Customer

LoyaltyIncreas

e in company Profiit

Increase in

employees'

benefits

Increase in

employees'

satisfaction

Better Service Quality

Proceedings of the International Conference on Tourism, Hospitality and Marketing

(IC16Mauritius Conference) ISBN - 978-1-943579-19-8

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M624

6 www.globalbizresearch.org

3.3 Customer Perception and Expectation of Service Quality

The main objective of delivering high service quality is to satisfy customers and as seen

in Figure1 the ideal point resulting in customer satisfaction is where customer expectations

equal to customer perceptions. The major challenge of service providers is the constant and

ever changing expectations of their customers.According to Zeithamlet al (2009), customer

expectations are beliefs about a service that serves as standards or reference points to which

the performance of the service is judged. Knowing what the customer expects is the first and

possibly most critical factor in delivering quality service. Getting what customers want

wrong, can result in losing a customer to another company who meets the target, expending

money and resources in wrong places and not surviving in a fiercely competitive market.

Together with customer expectations come customer perceptions. It is another focal point of

service quality on which service providers have to ponder on. Customer perception refers to

the way in which customers feel about the services being provided. It is actually this element

that shapes customers’ expectations from the company. Parasuraman et al (1985) believed

that perception and expectation are strongly relative concepts. Berry et al.(1988) and

Parasuramanet al. (1985) viewed quality as the customers’ perception of service excellence.

This implies that customers shape their perception of the quality of service based on their past

experience, word of mouth and even their closed ones experience. Moreover, Schneider and

White (2004) stated that perceive service quality and service qualities are two concepts that

deal together in the concept of marketing. Zeithaml et al., (2006) considered perceived service

quality as a scale for firm to measure how much they were successful to cover their customer

purpose. In the publication of Parasuraman et al., (1985) service quality was conceptualized

as a gap between consumers’ expectations and perceptions.Thus service providers that are not

able to meet their customer’s expectation will most probably experience a decline in customer

retention and unfavourable corporate image. Thus we hypothesize:

3.3.1 Hypotheses

H2: There is a significant difference between customer perceptions and expectations

3.4 Impact of Service Quality and Customer Satisfaction on Banks

As documented by Wang et al., (2003) and cited by Ahmad (2010) quality service and

products to the customer, is essential for success and survival in today's global and highly

competitive banking environment. Bloemer et al. (1998) wrote that bank customer satisfaction

can be regarded as a bank fully meeting its customers’ expectations. To support this

statement, Jamal et al (2002) defined bank customer satisfaction as a feeling or attitude

formed by bank customers after service, which directly links to the various purchasing

behaviours. Moreover, providing a high level of service to customers is the marketing weapon

that banks can use to differentiate themselves on the market. It is a known fact that nearly all

Proceedings of the International Conference on Tourism, Hospitality and Marketing

(IC16Mauritius Conference) ISBN - 978-1-943579-19-8

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M624

7 www.globalbizresearch.org

banks provide the same products to customers and that it takes only some days for new

products to be copied. However the only additional effort on which they can clearly

demarcate themselves is in providing an excellent service quality which would be impossible

for competitors to copy. According to Roth and Van Der Velde (1991) there is a positive

relationship between service quality level and financial performance implying that an

enhancement of the service quality provided by organisations will result in an improved the

financial status of the company. Bennet (1992) supported this by adding that the outcome of

developed service quality is positive financial performance. The quality of the service being

offered to a customer is actually a defining moment for the banks. As documented by Bitner

et al.(1990) delivering high service quality results in customer satisfaction and loyalty, greater

willingness to recommend to someone else, reduction in customer complaints, and improved

customer retention rates. Thus we hypothesize:

3.4.1 Hypotheses

H3: There is a relationship between service quality and customer satisfaction in the Mauritian

banking industry.

It can be concluded that in this era of high competition, it is a must for banks to provide a

high quality of service to satisfy their customers. Hence, for banks to know where they stand

on the market, they have to constantly measure the quality of service that they offer. But due

to the intangibility aspect of service, it is quite difficult to measure the quality of service being

delivered to customers. Thus, a number of instruments have been devised by prior researchers

and for the purpose of this study SERVQUAL will be used, one of the most famous and well

appreciated models in the service industry. In this review, the importance of this model has

been elaborated.

4. Methodology

For the purpose of this study, the quantitative approach has been used through self-

administered questionnaire. The questionnaire comprises of three sections. Section A and B

each comprises of a set of 22 questions. These questions are used to measure the five different

SERVQUAL dimensions of service quality namely five questions to measure Reliability and

Empathy and Four questions to measure Tangibility, Responsiveness and Assurance.

Secondary data has been extracted from available research papers, dissertations, journal, and

articles from Ebsco, Emerald, magazines and Internet. In order to determine the sample size, a

number of similar past studies done has been taken into consideration; whereby it has

concluded that a sample size of 200 is suffice for the purpose of this study. Moreover, the

banks considered were mainly the 5 banks whose services are perceived to be commonly

utilised by Mauritians. They are namely MCB SBM, HSBC, BBC and Barclays Bank.

Proceedings of the International Conference on Tourism, Hospitality and Marketing

(IC16Mauritius Conference) ISBN - 978-1-943579-19-8

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M624

8 www.globalbizresearch.org

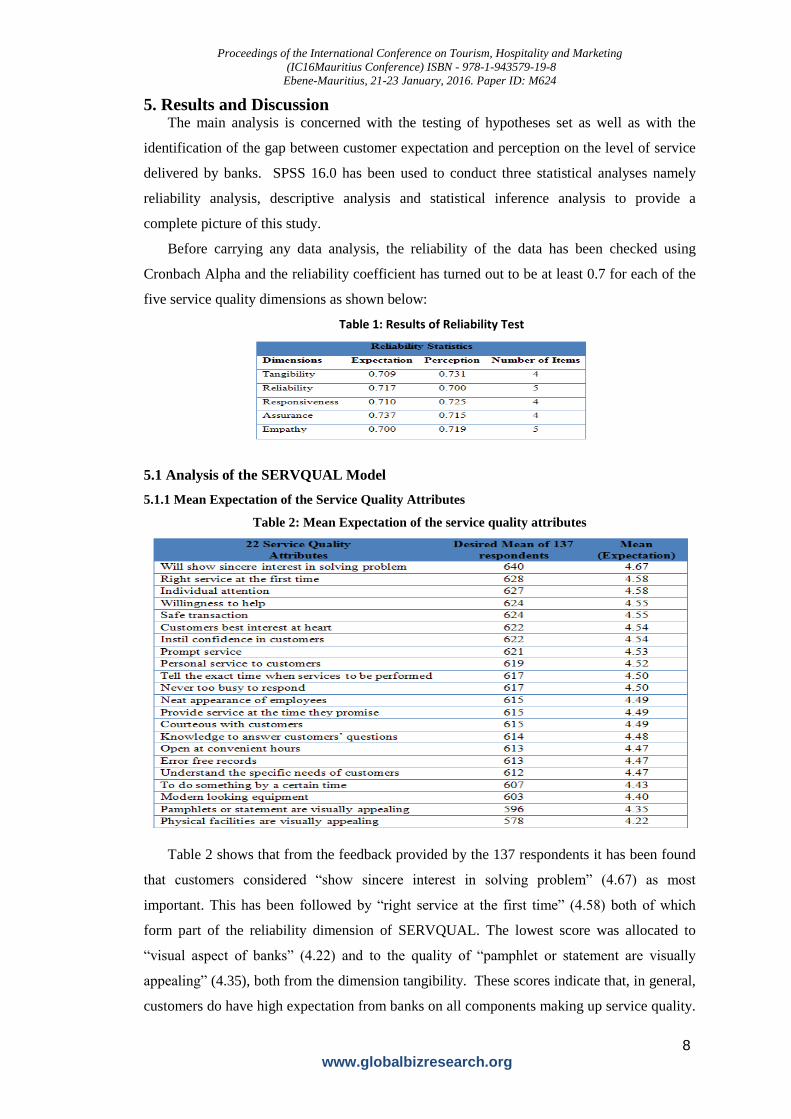

5. Results and Discussion The main analysis is concerned with the testing of hypotheses set as well as with the

identification of the gap between customer expectation and perception on the level of service

delivered by banks. SPSS 16.0 has been used to conduct three statistical analyses namely

reliability analysis, descriptive analysis and statistical inference analysis to provide a

complete picture of this study.

Before carrying any data analysis, the reliability of the data has been checked using

Cronbach Alpha and the reliability coefficient has turned out to be at least 0.7 for each of the

five service quality dimensions as shown below:

Table 1: Results of Reliability Test

5.1 Analysis of the SERVQUAL Model

5.1.1 Mean Expectation of the Service Quality Attributes

Table 2: Mean Expectation of the service quality attributes

Table 2 shows that from the feedback provided by the 137 respondents it has been found

that customers considered “show sincere interest in solving problem” (4.67) as most

important. This has been followed by “right service at the first time” (4.58) both of which

form part of the reliability dimension of SERVQUAL. The lowest score was allocated to

“visual aspect of banks” (4.22) and to the quality of “pamphlet or statement are visually

appealing” (4.35), both from the dimension tangibility. These scores indicate that, in general,

customers do have high expectation from banks on all components making up service quality.

Proceedings of the International Conference on Tourism, Hospitality and Marketing

(IC16Mauritius Conference) ISBN - 978-1-943579-19-8

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M624

9 www.globalbizresearch.org

Thus, their expectations, though vary from attribute to attribute, are near to the maximum

score of 5 on the 5-likert scale used. In fact these findings are consistent with Parasuraman et

al (1988, 1990) findings. Berry and Parasuraman (1991) pointed out that the tangibility

dimension is of least importance to customers as compared to other attributes. However,

Gronroos (2007) believed that the tangibility aspects of banks help to ensure that customers

get a satisfactory quality of service. It is also worth noting that the mean value of all of the 22

attributes is above 4 over a maximum of 5 points, implying that even if an attribute is

perceived as less important customers do have a high level of expectation on same.

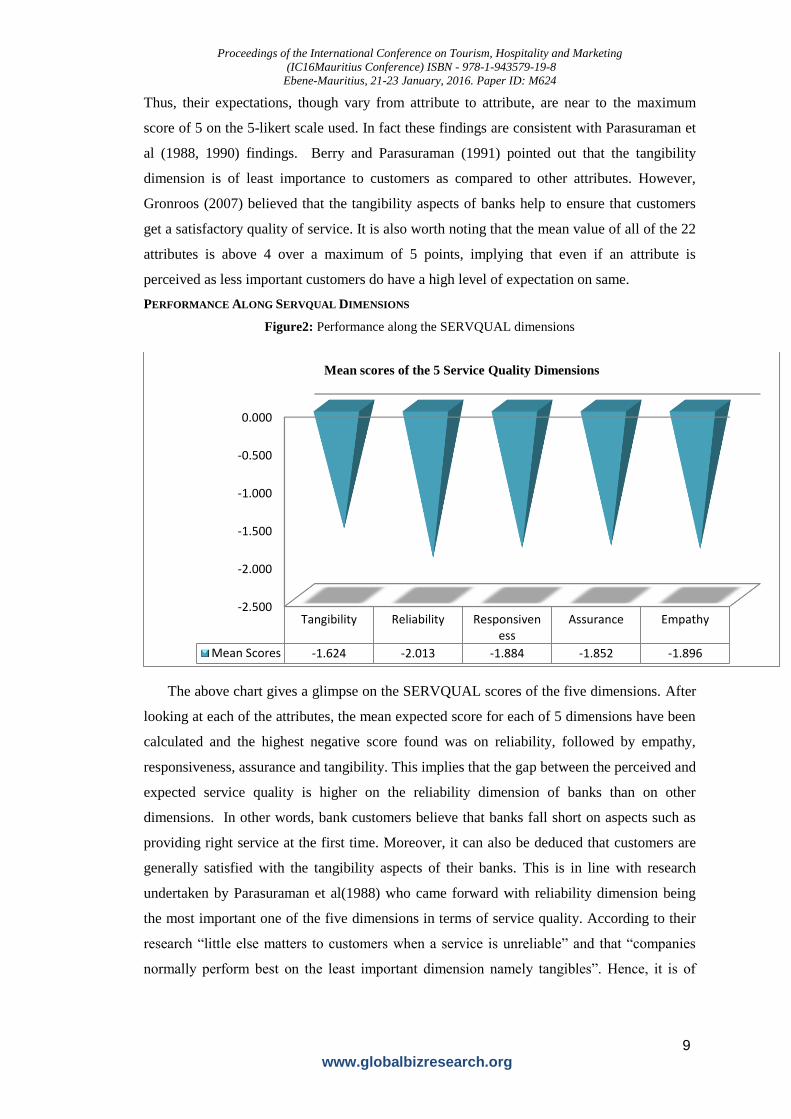

PERFORMANCE ALONG SERVQUAL DIMENSIONS

Figure2: Performance along the SERVQUAL dimensions

The above chart gives a glimpse on the SERVQUAL scores of the five dimensions. After

looking at each of the attributes, the mean expected score for each of 5 dimensions have been

calculated and the highest negative score found was on reliability, followed by empathy,

responsiveness, assurance and tangibility. This implies that the gap between the perceived and

expected service quality is higher on the reliability dimension of banks than on other

dimensions. In other words, bank customers believe that banks fall short on aspects such as

providing right service at the first time. Moreover, it can also be deduced that customers are

generally satisfied with the tangibility aspects of their banks. This is in line with research

undertaken by Parasuraman et al(1988) who came forward with reliability dimension being

the most important one of the five dimensions in terms of service quality. According to their

research “little else matters to customers when a service is unreliable” and that “companies

normally perform best on the least important dimension namely tangibles”. Hence, it is of

-2.500

-2.000

-1.500

-1.000

-0.500

0.000

Tangibility Reliability Responsiveness

Assurance Empathy

Mean Scores -1.624 -2.013 -1.884 -1.852 -1.896

Mean scores of the 5 Service Quality Dimensions

Proceedings of the International Conference on Tourism, Hospitality and Marketing

(IC16Mauritius Conference) ISBN - 978-1-943579-19-8

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M624

10 www.globalbizresearch.org

high importance that bank management strives hard to improve all the dimensions of service

quality in order to increase customer satisfaction

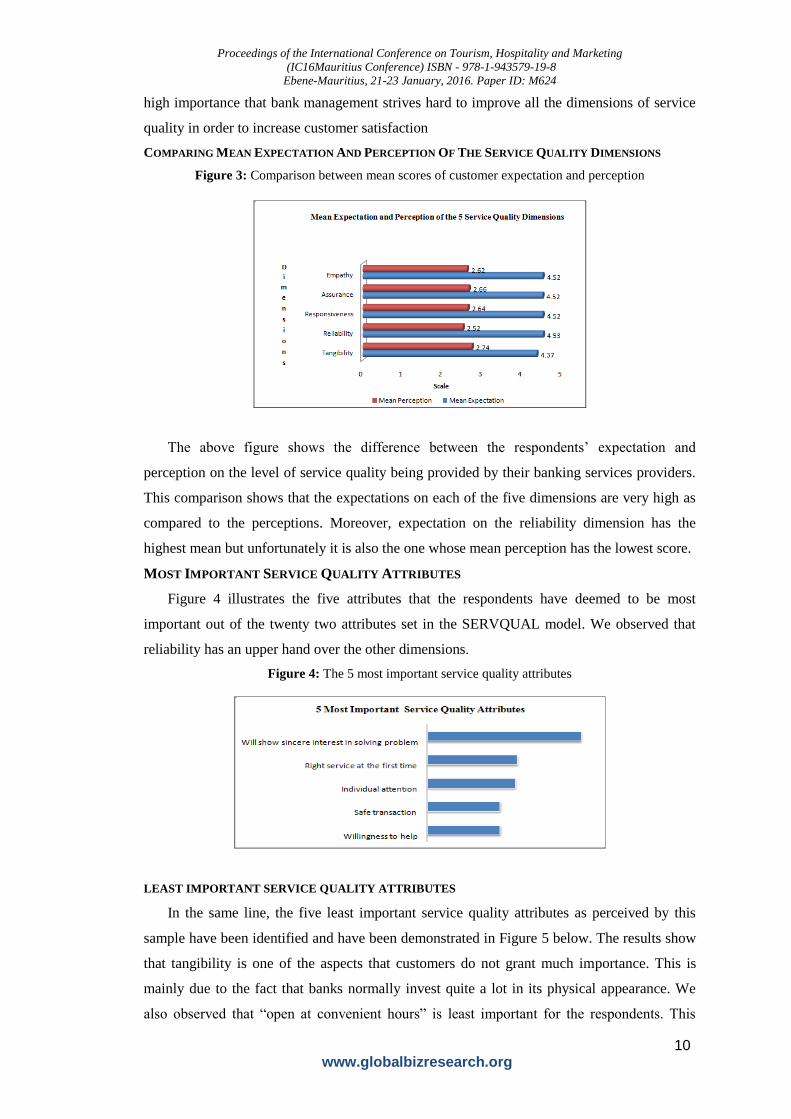

COMPARING MEAN EXPECTATION AND PERCEPTION OF THE SERVICE QUALITY DIMENSIONS

Figure 3: Comparison between mean scores of customer expectation and perception

The above figure shows the difference between the respondents’ expectation and

perception on the level of service quality being provided by their banking services providers.

This comparison shows that the expectations on each of the five dimensions are very high as

compared to the perceptions. Moreover, expectation on the reliability dimension has the

highest mean but unfortunately it is also the one whose mean perception has the lowest score.

MOST IMPORTANT SERVICE QUALITY ATTRIBUTES

Figure 4 illustrates the five attributes that the respondents have deemed to be most

important out of the twenty two attributes set in the SERVQUAL model. We observed that

reliability has an upper hand over the other dimensions.

Figure 4: The 5 most important service quality attributes

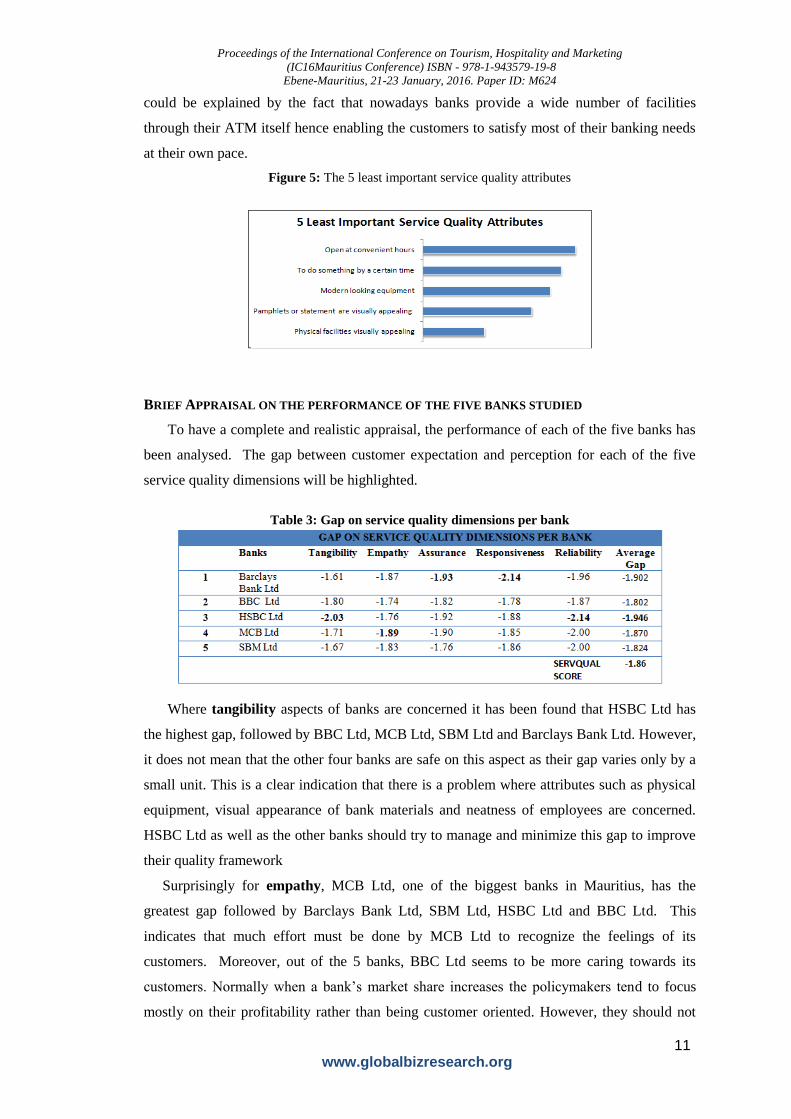

LEAST IMPORTANT SERVICE QUALITY ATTRIBUTES

In the same line, the five least important service quality attributes as perceived by this

sample have been identified and have been demonstrated in Figure 5 below. The results show

that tangibility is one of the aspects that customers do not grant much importance. This is

mainly due to the fact that banks normally invest quite a lot in its physical appearance. We

also observed that “open at convenient hours” is least important for the respondents. This

Proceedings of the International Conference on Tourism, Hospitality and Marketing

(IC16Mauritius Conference) ISBN - 978-1-943579-19-8

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M624

11 www.globalbizresearch.org

could be explained by the fact that nowadays banks provide a wide number of facilities

through their ATM itself hence enabling the customers to satisfy most of their banking needs

at their own pace.

Figure 5: The 5 least important service quality attributes

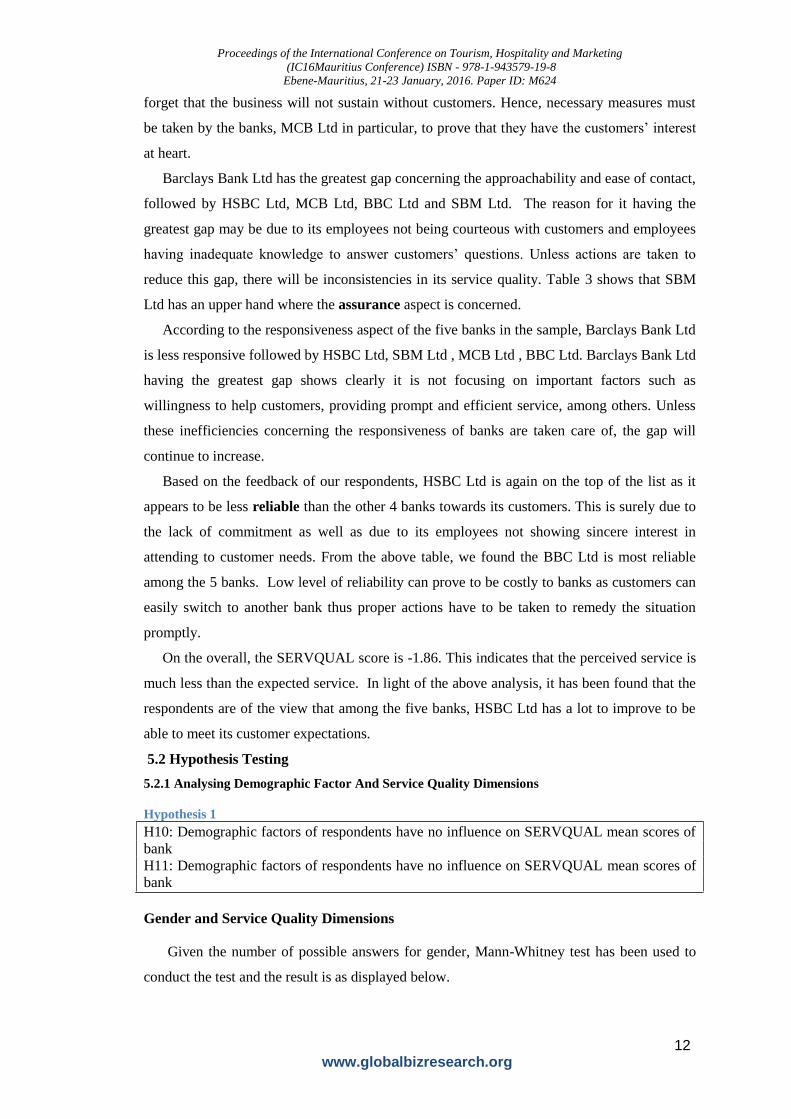

BRIEF APPRAISAL ON THE PERFORMANCE OF THE FIVE BANKS STUDIED

To have a complete and realistic appraisal, the performance of each of the five banks has

been analysed. The gap between customer expectation and perception for each of the five

service quality dimensions will be highlighted.

Table 3: Gap on service quality dimensions per bank

Where tangibility aspects of banks are concerned it has been found that HSBC Ltd has

the highest gap, followed by BBC Ltd, MCB Ltd, SBM Ltd and Barclays Bank Ltd. However,

it does not mean that the other four banks are safe on this aspect as their gap varies only by a

small unit. This is a clear indication that there is a problem where attributes such as physical

equipment, visual appearance of bank materials and neatness of employees are concerned.

HSBC Ltd as well as the other banks should try to manage and minimize this gap to improve

their quality framework

Surprisingly for empathy, MCB Ltd, one of the biggest banks in Mauritius, has the

greatest gap followed by Barclays Bank Ltd, SBM Ltd, HSBC Ltd and BBC Ltd. This

indicates that much effort must be done by MCB Ltd to recognize the feelings of its

customers. Moreover, out of the 5 banks, BBC Ltd seems to be more caring towards its

customers. Normally when a bank’s market share increases the policymakers tend to focus

mostly on their profitability rather than being customer oriented. However, they should not

Proceedings of the International Conference on Tourism, Hospitality and Marketing

(IC16Mauritius Conference) ISBN - 978-1-943579-19-8

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M624

12 www.globalbizresearch.org

forget that the business will not sustain without customers. Hence, necessary measures must

be taken by the banks, MCB Ltd in particular, to prove that they have the customers’ interest

at heart.

Barclays Bank Ltd has the greatest gap concerning the approachability and ease of contact,

followed by HSBC Ltd, MCB Ltd, BBC Ltd and SBM Ltd. The reason for it having the

greatest gap may be due to its employees not being courteous with customers and employees

having inadequate knowledge to answer customers’ questions. Unless actions are taken to

reduce this gap, there will be inconsistencies in its service quality. Table 3 shows that SBM

Ltd has an upper hand where the assurance aspect is concerned.

According to the responsiveness aspect of the five banks in the sample, Barclays Bank Ltd

is less responsive followed by HSBC Ltd, SBM Ltd , MCB Ltd , BBC Ltd. Barclays Bank Ltd

having the greatest gap shows clearly it is not focusing on important factors such as

willingness to help customers, providing prompt and efficient service, among others. Unless

these inefficiencies concerning the responsiveness of banks are taken care of, the gap will

continue to increase.

Based on the feedback of our respondents, HSBC Ltd is again on the top of the list as it

appears to be less reliable than the other 4 banks towards its customers. This is surely due to

the lack of commitment as well as due to its employees not showing sincere interest in

attending to customer needs. From the above table, we found the BBC Ltd is most reliable

among the 5 banks. Low level of reliability can prove to be costly to banks as customers can

easily switch to another bank thus proper actions have to be taken to remedy the situation

promptly.

On the overall, the SERVQUAL score is -1.86. This indicates that the perceived service is

much less than the expected service. In light of the above analysis, it has been found that the

respondents are of the view that among the five banks, HSBC Ltd has a lot to improve to be

able to meet its customer expectations.

5.2 Hypothesis Testing

5.2.1 Analysing Demographic Factor And Service Quality Dimensions

Hypothesis 1

H10: Demographic factors of respondents have no influence on SERVQUAL mean scores of

bank

H11: Demographic factors of respondents have no influence on SERVQUAL mean scores of

bank

Gender and Service Quality Dimensions

Given the number of possible answers for gender, Mann-Whitney test has been used to

conduct the test and the result is as displayed below.

Proceedings of the International Conference on Tourism, Hospitality and Marketing

(IC16Mauritius Conference) ISBN - 978-1-943579-19-8

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M624

13 www.globalbizresearch.org

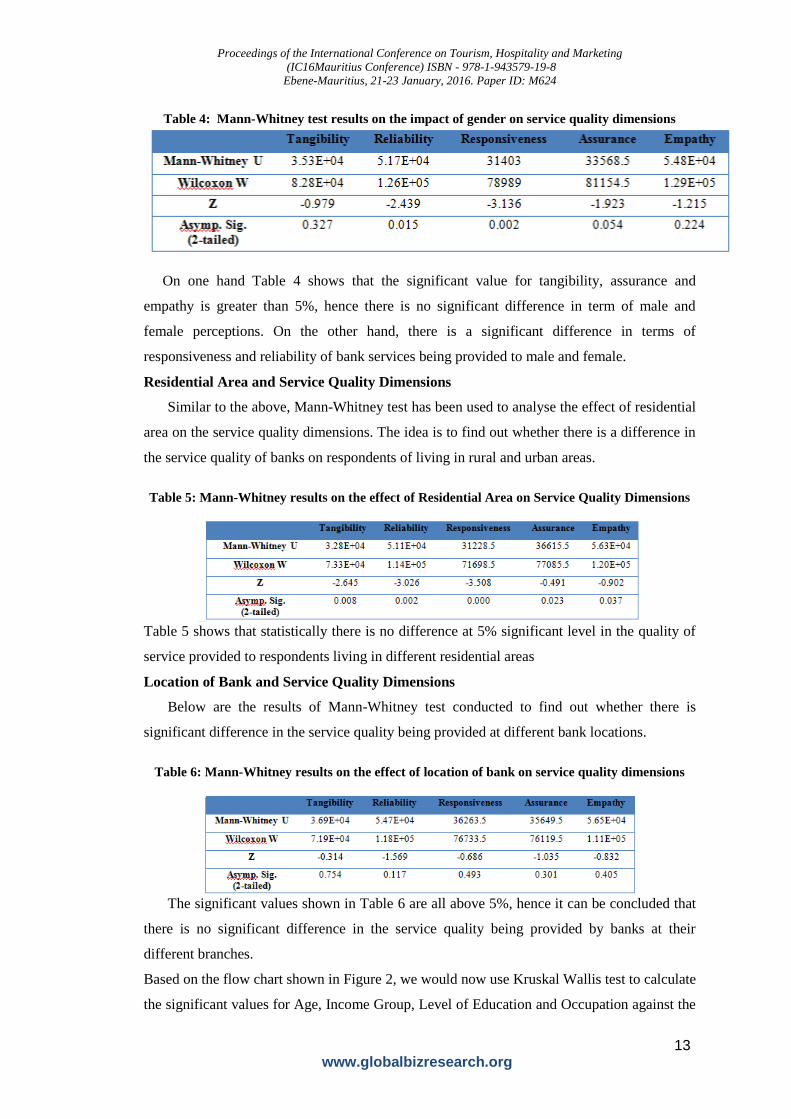

Table 4: Mann-Whitney test results on the impact of gender on service quality dimensions

On one hand Table 4 shows that the significant value for tangibility, assurance and

empathy is greater than 5%, hence there is no significant difference in term of male and

female perceptions. On the other hand, there is a significant difference in terms of

responsiveness and reliability of bank services being provided to male and female.

Residential Area and Service Quality Dimensions

Similar to the above, Mann-Whitney test has been used to analyse the effect of residential

area on the service quality dimensions. The idea is to find out whether there is a difference in

the service quality of banks on respondents of living in rural and urban areas.

Table 5: Mann-Whitney results on the effect of Residential Area on Service Quality Dimensions

Table 5 shows that statistically there is no difference at 5% significant level in the quality of

service provided to respondents living in different residential areas

Location of Bank and Service Quality Dimensions

Below are the results of Mann-Whitney test conducted to find out whether there is

significant difference in the service quality being provided at different bank locations.

Table 6: Mann-Whitney results on the effect of location of bank on service quality dimensions

The significant values shown in Table 6 are all above 5%, hence it can be concluded that

there is no significant difference in the service quality being provided by banks at their

different branches.

Based on the flow chart shown in Figure 2, we would now use Kruskal Wallis test to calculate

the significant values for Age, Income Group, Level of Education and Occupation against the

Proceedings of the International Conference on Tourism, Hospitality and Marketing

(IC16Mauritius Conference) ISBN - 978-1-943579-19-8

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M624

14 www.globalbizresearch.org

5 service quality dimensions. Kruskal Wallis test is a non-parametric test used to compare 3

or more groups of data. It is in fact an extension of the Mann-Whitney test.

Age and Service Quality Dimensions

The feedback of the 137 respondents based on their age range using Kruskal Wallis test

and the results are tabulated below.

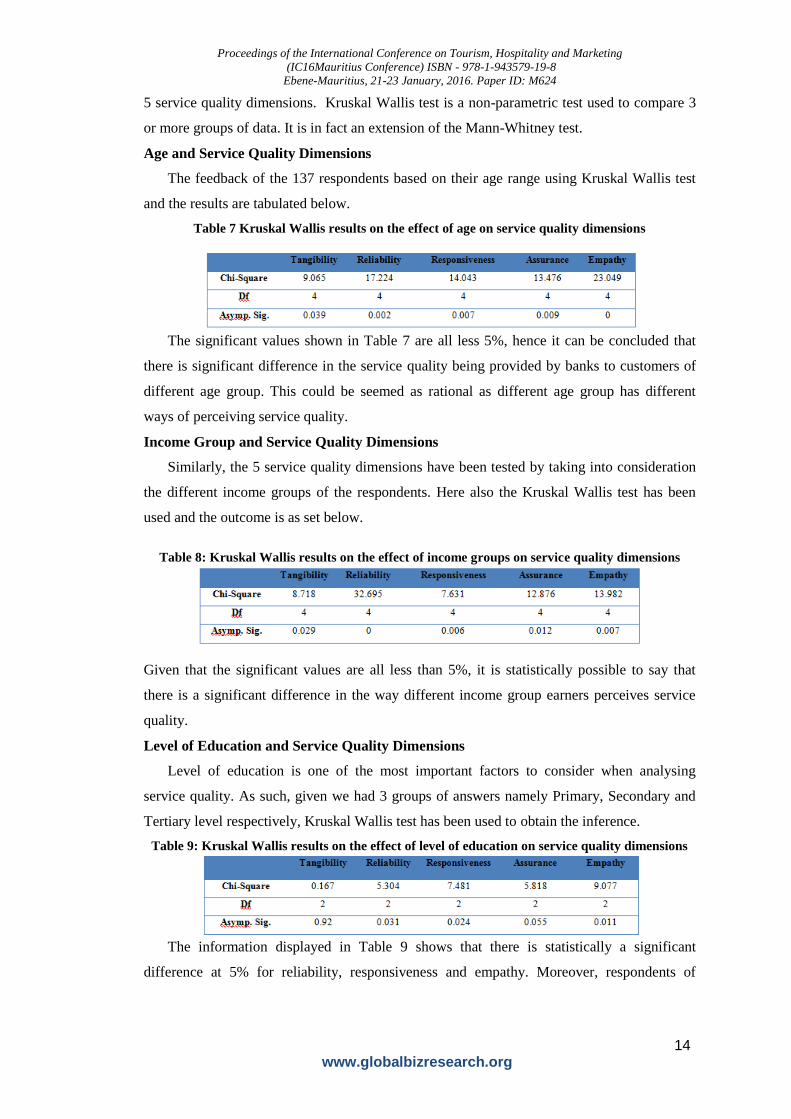

Table 7 Kruskal Wallis results on the effect of age on service quality dimensions

The significant values shown in Table 7 are all less 5%, hence it can be concluded that

there is significant difference in the service quality being provided by banks to customers of

different age group. This could be seemed as rational as different age group has different

ways of perceiving service quality.

Income Group and Service Quality Dimensions

Similarly, the 5 service quality dimensions have been tested by taking into consideration

the different income groups of the respondents. Here also the Kruskal Wallis test has been

used and the outcome is as set below.

Table 8: Kruskal Wallis results on the effect of income groups on service quality dimensions

Given that the significant values are all less than 5%, it is statistically possible to say that

there is a significant difference in the way different income group earners perceives service

quality.

Level of Education and Service Quality Dimensions

Level of education is one of the most important factors to consider when analysing

service quality. As such, given we had 3 groups of answers namely Primary, Secondary and

Tertiary level respectively, Kruskal Wallis test has been used to obtain the inference.

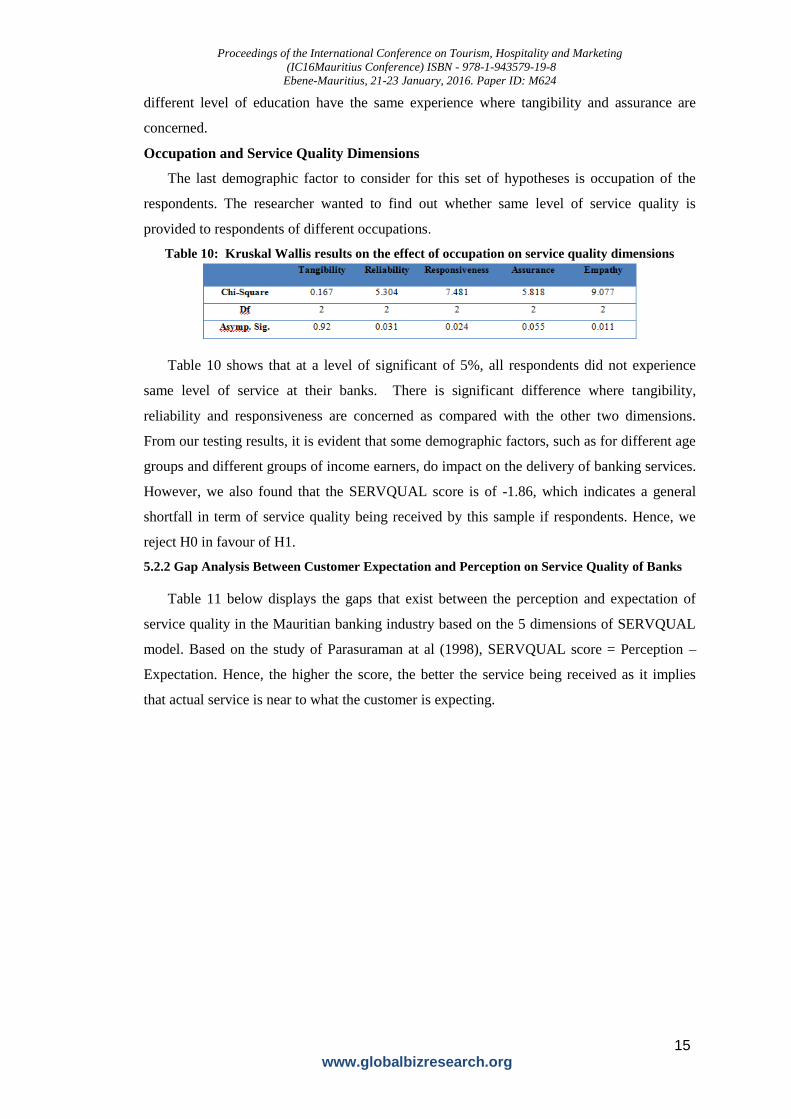

Table 9: Kruskal Wallis results on the effect of level of education on service quality dimensions

The information displayed in Table 9 shows that there is statistically a significant

difference at 5% for reliability, responsiveness and empathy. Moreover, respondents of

Proceedings of the International Conference on Tourism, Hospitality and Marketing

(IC16Mauritius Conference) ISBN - 978-1-943579-19-8

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M624

15 www.globalbizresearch.org

different level of education have the same experience where tangibility and assurance are

concerned.

Occupation and Service Quality Dimensions

The last demographic factor to consider for this set of hypotheses is occupation of the

respondents. The researcher wanted to find out whether same level of service quality is

provided to respondents of different occupations.

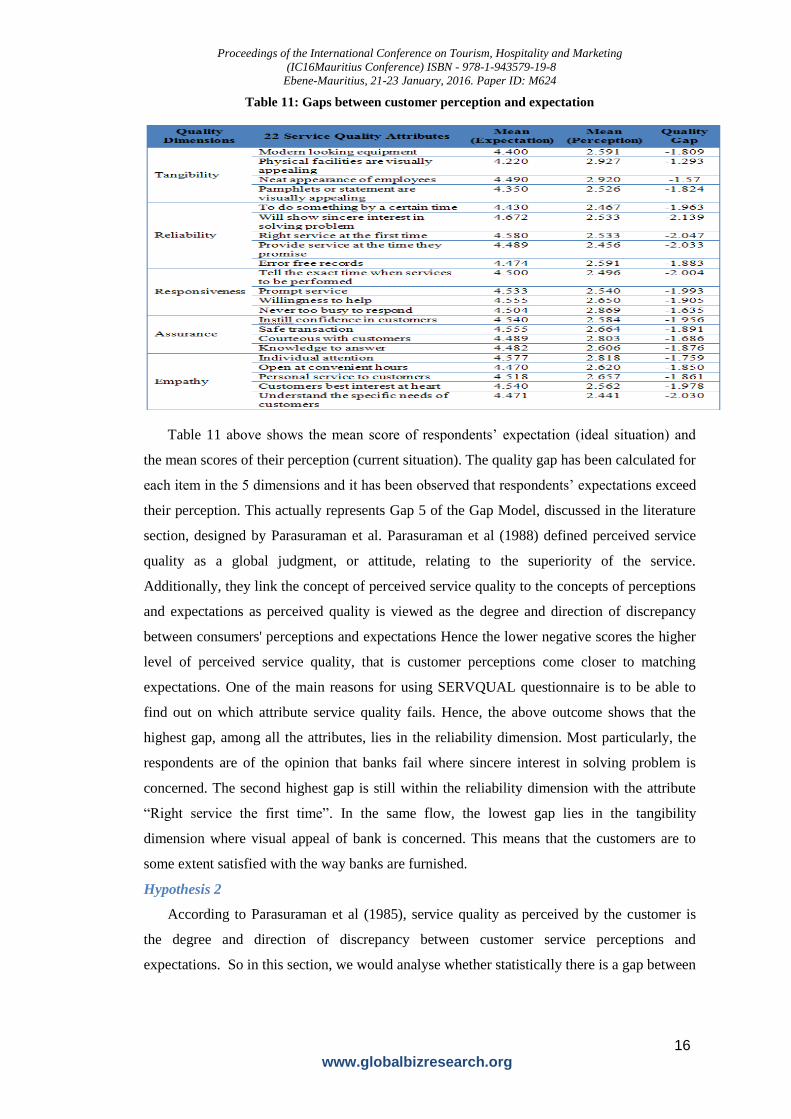

Table 10: Kruskal Wallis results on the effect of occupation on service quality dimensions

Table 10 shows that at a level of significant of 5%, all respondents did not experience

same level of service at their banks. There is significant difference where tangibility,

reliability and responsiveness are concerned as compared with the other two dimensions.

From our testing results, it is evident that some demographic factors, such as for different age

groups and different groups of income earners, do impact on the delivery of banking services.

However, we also found that the SERVQUAL score is of -1.86, which indicates a general

shortfall in term of service quality being received by this sample if respondents. Hence, we

reject H0 in favour of H1.

5.2.2 Gap Analysis Between Customer Expectation and Perception on Service Quality of Banks

Table 11 below displays the gaps that exist between the perception and expectation of

service quality in the Mauritian banking industry based on the 5 dimensions of SERVQUAL

model. Based on the study of Parasuraman at al (1998), SERVQUAL score = Perception –

Expectation. Hence, the higher the score, the better the service being received as it implies

that actual service is near to what the customer is expecting.

Proceedings of the International Conference on Tourism, Hospitality and Marketing

(IC16Mauritius Conference) ISBN - 978-1-943579-19-8

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M624

16 www.globalbizresearch.org

Table 11: Gaps between customer perception and expectation

Table 11 above shows the mean score of respondents’ expectation (ideal situation) and

the mean scores of their perception (current situation). The quality gap has been calculated for

each item in the 5 dimensions and it has been observed that respondents’ expectations exceed

their perception. This actually represents Gap 5 of the Gap Model, discussed in the literature

section, designed by Parasuraman et al. Parasuraman et al (1988) defined perceived service

quality as a global judgment, or attitude, relating to the superiority of the service.

Additionally, they link the concept of perceived service quality to the concepts of perceptions

and expectations as perceived quality is viewed as the degree and direction of discrepancy

between consumers' perceptions and expectations Hence the lower negative scores the higher

level of perceived service quality, that is customer perceptions come closer to matching

expectations. One of the main reasons for using SERVQUAL questionnaire is to be able to

find out on which attribute service quality fails. Hence, the above outcome shows that the

highest gap, among all the attributes, lies in the reliability dimension. Most particularly, the

respondents are of the opinion that banks fail where sincere interest in solving problem is

concerned. The second highest gap is still within the reliability dimension with the attribute

“Right service the first time”. In the same flow, the lowest gap lies in the tangibility

dimension where visual appeal of bank is concerned. This means that the customers are to

some extent satisfied with the way banks are furnished.

Hypothesis 2

According to Parasuraman et al (1985), service quality as perceived by the customer is

the degree and direction of discrepancy between customer service perceptions and

expectations. So in this section, we would analyse whether statistically there is a gap between

Proceedings of the International Conference on Tourism, Hospitality and Marketing

(IC16Mauritius Conference) ISBN - 978-1-943579-19-8

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M624

17 www.globalbizresearch.org

customer perceptions and expectations in the quality of service being provided by banks in

the Mauritian banking industry. The hypothesis set for this analyse is as follows:

H2i0: There is no significant difference between customer perceptions and expectations

related to dimension i

H2i1: There is a significant difference between customer perceptions and expectations to

dimension i

(wherei = a, b, c, d, e for tangibility, reliability, responsiveness, assurance and empathy

respectively)

In the view of conducting this analysis, a very powerful statistical tool named Wilcoxon

signed rank test would be used to detect if statistically there is significant difference between

a paired set of data. Crichton (1997) supported that Wilcoxon Sign test is a statistical

comparison of the average of two dependent samples. Also, the differences are approximately

symmetric and that the data are measured on an ordinal, interval, or ratio scale. This is

therefore appropriate for this study as our model used likert scale to capture respondents’

opinion.

Moreover, according to Crichton et al (1997), paired data means that the values in the two

groups being compared are naturally linked, and usually arise from individuals being

measured more than once. This fits well for this part of our study as the difference between

the scores received for perception and those for expectation would be clearly seen. So here,

the respondents’ opinions on their perception and expectation would be considered as a set of

paired data. Thus, given there are five service quality dimensions, we would be having 5 sets

of paired data.

The results of the test conducted have been stated below.

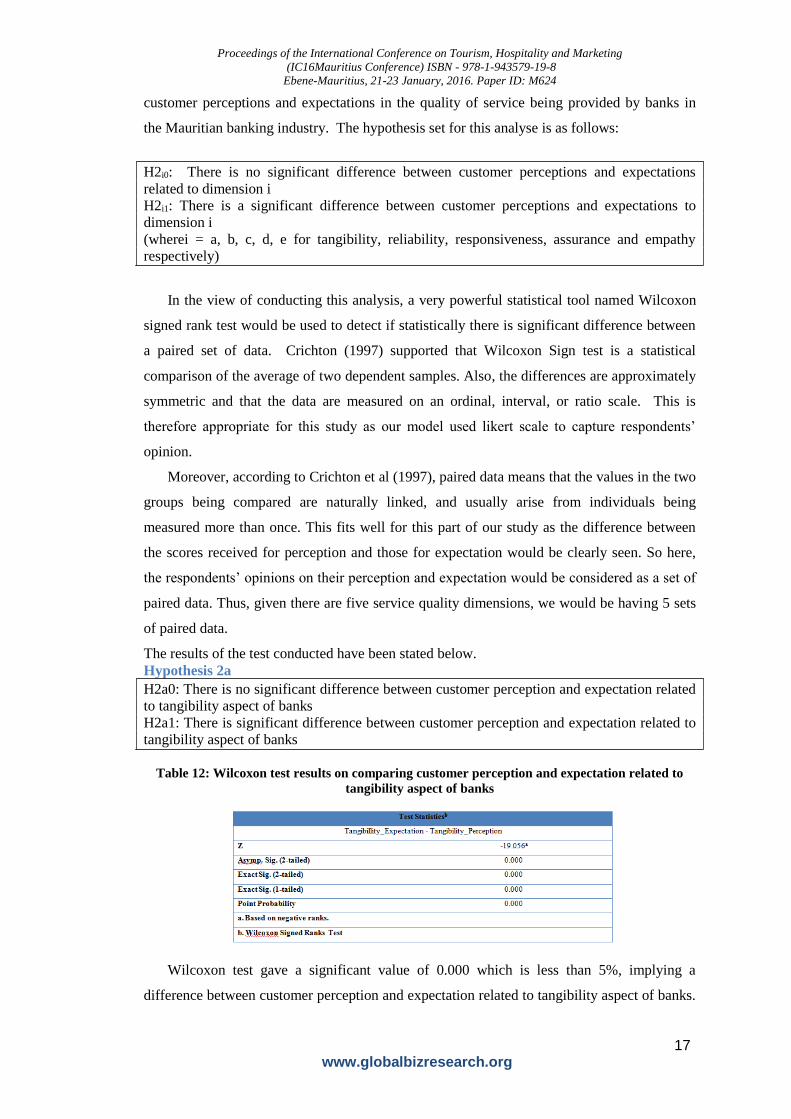

Hypothesis 2a

H2a0: There is no significant difference between customer perception and expectation related

to tangibility aspect of banks

H2a1: There is significant difference between customer perception and expectation related to

tangibility aspect of banks

Table 12: Wilcoxon test results on comparing customer perception and expectation related to

tangibility aspect of banks

Wilcoxon test gave a significant value of 0.000 which is less than 5%, implying a

difference between customer perception and expectation related to tangibility aspect of banks.

Proceedings of the International Conference on Tourism, Hospitality and Marketing

(IC16Mauritius Conference) ISBN - 978-1-943579-19-8

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M624

18 www.globalbizresearch.org

Moreover, this result is in line with Table 11 where we found that the mean expectation for

tangibility is 4.37 which is higher than the mean perception of 2.74 hence showing the gap

between customers’ expectation and perception on tangibility. As such, we can reject H2a0in

favour of H2a1.

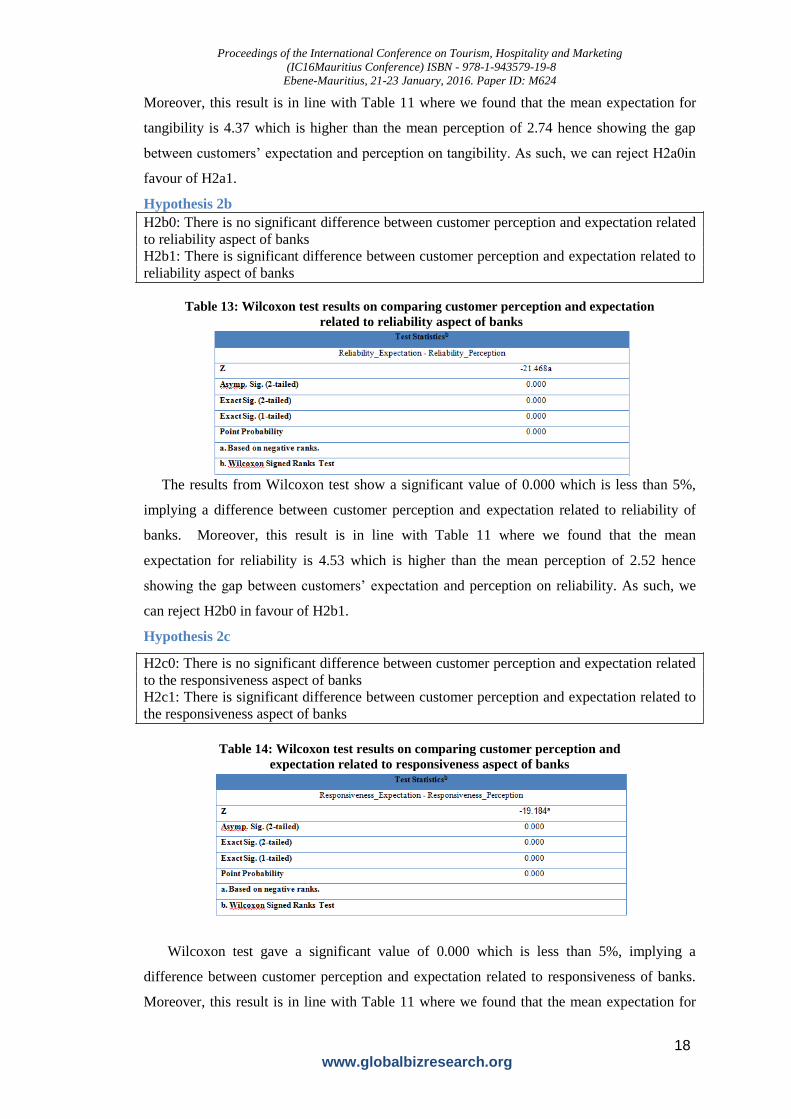

Hypothesis 2b

H2b0: There is no significant difference between customer perception and expectation related

to reliability aspect of banks

H2b1: There is significant difference between customer perception and expectation related to

reliability aspect of banks

Table 13: Wilcoxon test results on comparing customer perception and expectation

related to reliability aspect of banks

The results from Wilcoxon test show a significant value of 0.000 which is less than 5%,

implying a difference between customer perception and expectation related to reliability of

banks. Moreover, this result is in line with Table 11 where we found that the mean

expectation for reliability is 4.53 which is higher than the mean perception of 2.52 hence

showing the gap between customers’ expectation and perception on reliability. As such, we

can reject H2b0 in favour of H2b1.

Hypothesis 2c

H2c0: There is no significant difference between customer perception and expectation related

to the responsiveness aspect of banks

H2c1: There is significant difference between customer perception and expectation related to

the responsiveness aspect of banks

Table 14: Wilcoxon test results on comparing customer perception and

expectation related to responsiveness aspect of banks

Wilcoxon test gave a significant value of 0.000 which is less than 5%, implying a

difference between customer perception and expectation related to responsiveness of banks.

Moreover, this result is in line with Table 11 where we found that the mean expectation for

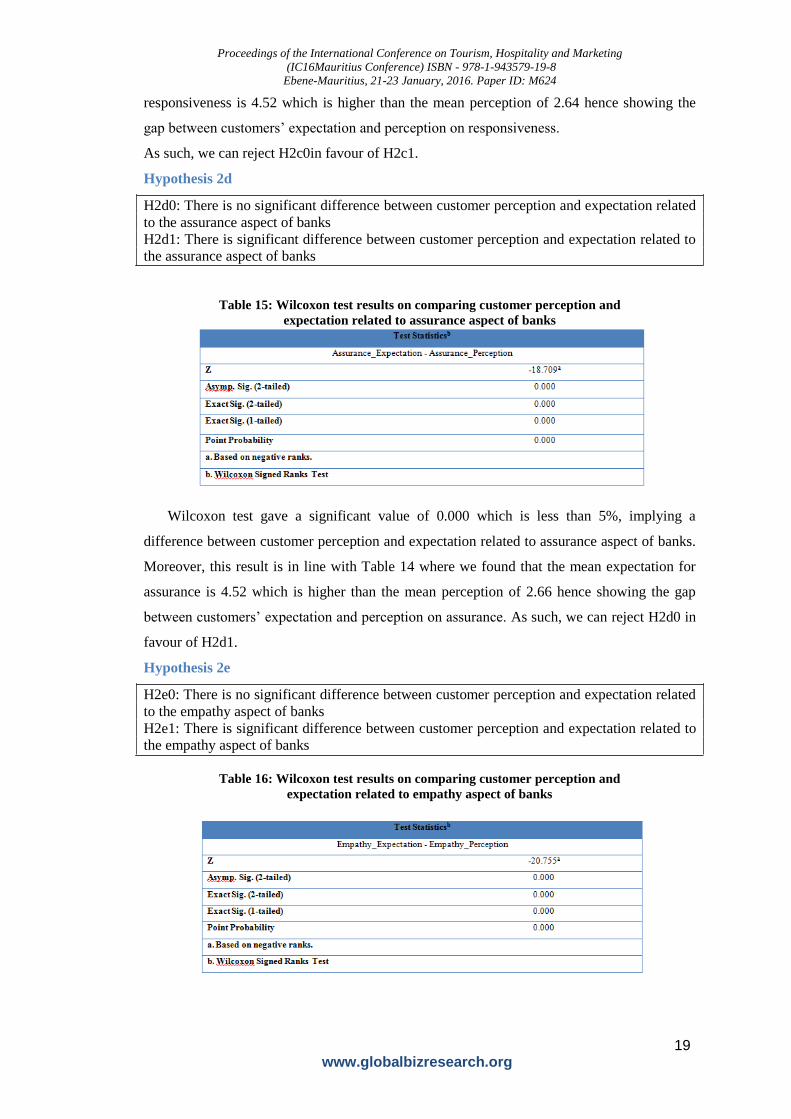

Proceedings of the International Conference on Tourism, Hospitality and Marketing

(IC16Mauritius Conference) ISBN - 978-1-943579-19-8

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M624

19 www.globalbizresearch.org

responsiveness is 4.52 which is higher than the mean perception of 2.64 hence showing the

gap between customers’ expectation and perception on responsiveness.

As such, we can reject H2c0in favour of H2c1.

Hypothesis 2d

H2d0: There is no significant difference between customer perception and expectation related

to the assurance aspect of banks

H2d1: There is significant difference between customer perception and expectation related to

the assurance aspect of banks

Table 15: Wilcoxon test results on comparing customer perception and

expectation related to assurance aspect of banks

Wilcoxon test gave a significant value of 0.000 which is less than 5%, implying a

difference between customer perception and expectation related to assurance aspect of banks.

Moreover, this result is in line with Table 14 where we found that the mean expectation for

assurance is 4.52 which is higher than the mean perception of 2.66 hence showing the gap

between customers’ expectation and perception on assurance. As such, we can reject H2d0 in

favour of H2d1.

Hypothesis 2e

H2e0: There is no significant difference between customer perception and expectation related

to the empathy aspect of banks

H2e1: There is significant difference between customer perception and expectation related to

the empathy aspect of banks

Table 16: Wilcoxon test results on comparing customer perception and

expectation related to empathy aspect of banks

Proceedings of the International Conference on Tourism, Hospitality and Marketing

(IC16Mauritius Conference) ISBN - 978-1-943579-19-8

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M624

20 www.globalbizresearch.org

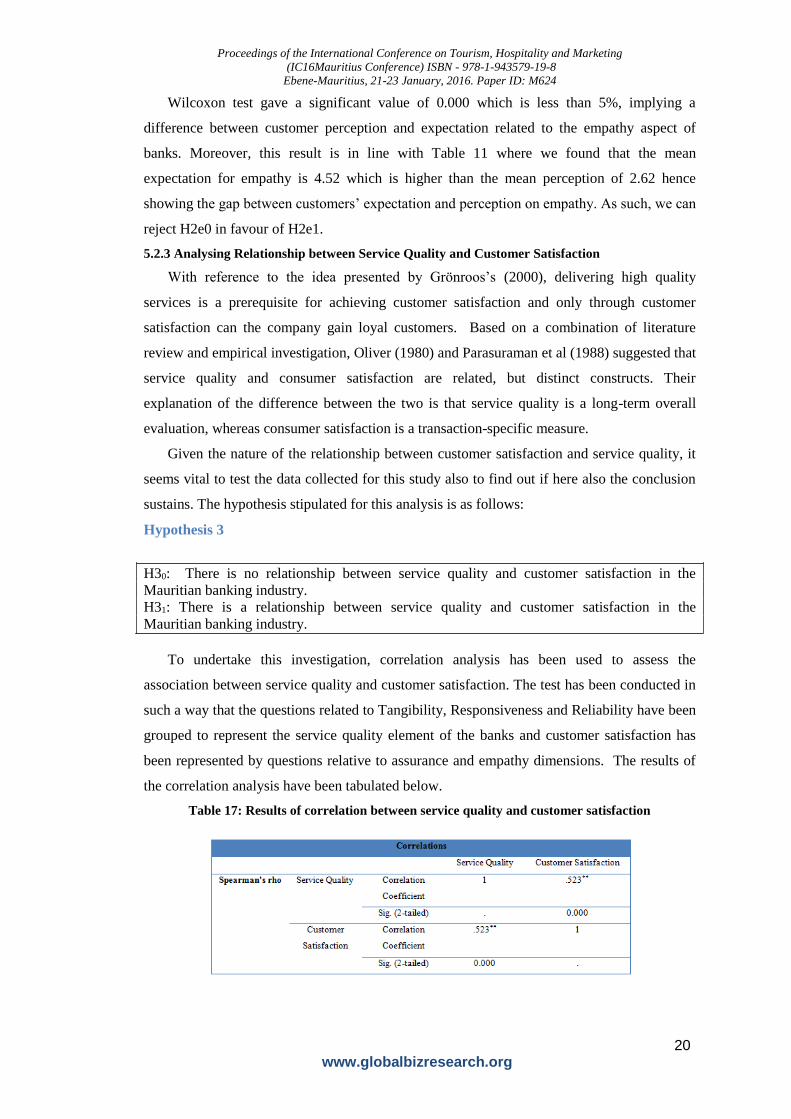

Wilcoxon test gave a significant value of 0.000 which is less than 5%, implying a

difference between customer perception and expectation related to the empathy aspect of

banks. Moreover, this result is in line with Table 11 where we found that the mean

expectation for empathy is 4.52 which is higher than the mean perception of 2.62 hence

showing the gap between customers’ expectation and perception on empathy. As such, we can

reject H2e0 in favour of H2e1.

5.2.3 Analysing Relationship between Service Quality and Customer Satisfaction

With reference to the idea presented by Grönroos’s (2000), delivering high quality

services is a prerequisite for achieving customer satisfaction and only through customer

satisfaction can the company gain loyal customers. Based on a combination of literature

review and empirical investigation, Oliver (1980) and Parasuraman et al (1988) suggested that

service quality and consumer satisfaction are related, but distinct constructs. Their

explanation of the difference between the two is that service quality is a long-term overall

evaluation, whereas consumer satisfaction is a transaction-specific measure.

Given the nature of the relationship between customer satisfaction and service quality, it

seems vital to test the data collected for this study also to find out if here also the conclusion

sustains. The hypothesis stipulated for this analysis is as follows:

Hypothesis 3

H30: There is no relationship between service quality and customer satisfaction in the

Mauritian banking industry.

H31: There is a relationship between service quality and customer satisfaction in the

Mauritian banking industry.

To undertake this investigation, correlation analysis has been used to assess the

association between service quality and customer satisfaction. The test has been conducted in

such a way that the questions related to Tangibility, Responsiveness and Reliability have been

grouped to represent the service quality element of the banks and customer satisfaction has

been represented by questions relative to assurance and empathy dimensions. The results of

the correlation analysis have been tabulated below.

Table 17: Results of correlation between service quality and customer satisfaction

Proceedings of the International Conference on Tourism, Hospitality and Marketing

(IC16Mauritius Conference) ISBN - 978-1-943579-19-8

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M624

21 www.globalbizresearch.org

The significant value is 0.000 which shows that there is a significant difference between

customer satisfaction and service quality at 5% significant level. Hence, rejecting the null

hypothesis. Moreover, there is a positive relationship between these two variables such that an

increase of 1% in reliability, responsiveness and tangibility will lead to an increase of 52.3%

in customer satisfaction.

6. Conclusion and Further Research

It is very important that bank managers understand that service quality is made up of

different dimensions and it being intangible makes it difficult to assess. All the service quality

dimensions have a positive relationship with the way bank employees behave. Therefore, the

staff needs to have ample knowledge, communication skills, and eagerness to help in giving

quick services efficiently. Bank managers should realize the fact that training to employees is

an investment, not an expense. Training of staffs with regards to service quality and

knowledge in service quality dimensions should be regularly conducted in order for the staffs

to feel more at ease, professional and confident while delivering the required service to

customers. Business drivers can use the five dimensions discussed in this study to evaluate the

level of service being delivered to their customers. Thus, enabling them to analyse their

current situation and convert weaknesses into strengths to have a sharper competitive edge on

the market. Bank staffs should keep in mind that customers evaluate service quality by

comparing the quality of service they expected to receive against the quality of service they

actually experience.

Further research can be carried out to solely appraise the reliability dimension of banks. It

would also certainly add value to the banking industry to find out about the financial impact

on banks when more emphasis is laid on service quality. Finally, it would be interesting to

assess service quality from the employees’ perspective as well.

References

Berry, L. L. (1995). Relationship marketing of services—growing interest, Emerging Perspectives.

Journal of the Academy of Marketing Science, 23(4), 236-245.

Bitner, M. J., Booms, B .H. & Tetreault, M .S. (1990). The service Encounter: Diagnosing Favorable

and Unfavorable Indents. Journal of Marketing, 54(1), 71-84.

Bloemer, J., de-Ruyter, K. & Wetzels, M. (1999). Linking perceived service quality and service

loyalty: A multi- dimensional perspective. European Journal of Marketing, 33(11/12), 1082–1106.

Carman, J.M. (1990), “Consumer perceptions of service quality: an assessment of the SERVQUAL

dimensions”, Journal of Retailing, Vol. 66, pp. 33-5.

Choudhury, K. (2008), “Service quality: insights from the Indian banking scenario”, Australasian

Marketing Journal, Vol. 16 No. 1, pp. 48-61.

Jamal, A. and Naser, K. (2002), “Customer satisfaction and retail banking: an assessment of some of

the key antecedents of customer satisfaction in retail banking”, International Journal of Bank

Marketing, Vol. 20 No. 4, pp. 146-60.

Jamal, A. and Naser, K. (2003), “Factors influencing customer satisfaction in the retail banking sector

in Pakistan”, International Journal of Commerce & Management, Vol. 13 No. 2, p. 29.

Proceedings of the International Conference on Tourism, Hospitality and Marketing

(IC16Mauritius Conference) ISBN - 978-1-943579-19-8

Ebene-Mauritius, 21-23 January, 2016. Paper ID: M624

22 www.globalbizresearch.org

Ladhari, R. (2008), “Alternative measure of service quality: a review”, Journal of Managing Service

Quality, Vol. 18 No. 1, pp. 65-86.

Oliver, R .L. (1980). A Cognitive Model of the Antecedents and Consequences of Satisfaction

decisions. Journal of marketing research, 17(4), 460-469.

Parasuraman, A. & Grewal, D. (2000). The Impact of Technology on the Quality Value Loyalty Chain.

A Research Agenda. Journal of Academy of Marketing science, 28(1), 168-174.

Parasuraman, A., Berry, L.L. and Zeithaml, V.A. (1988), “SERVQUAL: a multiple-item scale for

measuring consumer perceptions of service quality”, Journal of Retailing, Vol.64 No. 1, p. 12.

Parasuraman, A. (1991). Refinement and reassessment of the SERVQUAL scale. Journal of Retailing,

67(4), 420-450.

Parasuraman, A., Berry, L. L. & Zeithaml, V. A. (1991). Understanding Customer Expectations of

Service. Sloan Management Review, 32(3), 39-48.

Zeithaml, V.A. and Bitner, M.J. (1996), Services Marketing, International edition,McGraw-

Hill,London

http://www.google.com

https://www.bom.mu

www.sbmgroup.mu

www.mcb.mu/