Embed Size (px)

Citation preview

The Company Secretary, The Board and Stakeholder

Expectations

Joel Wolpert CA (SA) FCMA FCIS

Chartered Secretaries Southern Africa 5 April 2013, New Delhi

What Stakeholders Expect from Directors

1. Hallmarks of Corporate Governance 2. Corporate governance institutional environment 3. Role of the board 4. Stakeholder relationships 5. Current issues in corporate governance

• Integrated reporting • Social media considerations • Executive remuneration • Anti-corruption business ethics

6. Company secretary’s role 7. Future issues for corporate governance

1. Hallmarks of Corporate Governance

1. Hallmarks of Corporate Governance Corporate Responsibility 1. Society grants companies important rights and

freedoms – such as the privilege of limited liability – and in return expects companies to fulfil certain obligations. Corporate responsibility is the foundation of successful commercial relationships in the corporate/business ecosystem.

1. Hallmarks of Corporate Governance

Value Creation 2. Pressure is growing for companies to adhere to such

principles not only because of legal or regulatory compliance, but because they create value for the enterprise.

This development has led to heightened interest in corporate governance and other aspects of the non-financial drivers of value, with the result that recent thinking on corporate governance is moving towards an approach that goes beyond the traditional financial bottom line. In a civilised society, the market needs to be tempered by moral values based on duty and obligation to something beyond self-interest.

1. Hallmarks of Corporate Governance

Principles 3. Commonly accepted principles of Corporate Governance

include: • Rights of and equitable treatment of shareholders • Respect for interests of other stakeholders • Role and responsibilities of the board • Integrity and ethical behaviour • Disclosure and transparency

1. Hallmarks of Corporate Governance

Activities 4. Certain fundamental activities lie at the heart of Corporate Governance. They

include: • Sound economic, social and environmental – triple bottom line

(sustainability) performance; • Effective financial management; integrated risk management processes; • Systems and processes for effective decision making; • Organisational integrity; • Effective monitoring and controls; • Independent auditing and verification; • Accountability and responsibility; and • Adequate sustainability reporting and transparency. • Ensure there is a company code of ethics for employees and management.

Ethical behaviour is reinforced when top management shows through its own actions, that questionable behaviour will not be tolerated. The credibility of any code is measured by the degree of enforcement.

1. Hallmarks of Corporate Governance

Risk and Accountability 5. Corporate Governance has expanded in scope since its early

focus on the financial aspects of business direction, so that it now embraces new areas of corporate accountability, including those of corporate social responsibility and the environment. A new area of concern is the range of risks and uncertainties which may threaten a company.

As a result of the above, companies have been facing increasing levels of legal, regulatory, and economic reporting requirements, with a resultant obligation to improve their governance principles, policies and standards.

1. Hallmarks of Corporate Governance

Accountability/Reporting/Assurance 6. The interests of investors and other stakeholders are

usually protected by a two-tier system. At one level is the company’s internal governance code. At the other end is the reporting system regulated by public and private institutions which subject public companies to accounting and disclosure standards as well as implement auditing surveillance.

1. Hallmarks of Corporate Governance

Codes 7. Internationally, various codes on corporate governance

have been developed over the last two decades. South African companies are regulated by the King Code on Corporate Governance for South Africa (King III) 1994 – King I 2002 – King II 2009 – King III

2. CORPORATE GOVERNANCE CODES

2. Corporate Governance Codes

The Comply-or-Explain Approach • Having a voluntary code as the basis of a corporate

governance regime is popular in many countries. At the heart of such an approach is the concept of “comply or explain”. (King III – Apply or Explain)

• The use of this concept is designed to permit flexibility in companies and it is in response to the fact that one size does not fit all as far as companies are concerned, as they are all different and should not be subject to rigid rules.

2. Corporate Governance Codes The Comply-or-Explain Approach • It is incumbent on the markets generally and the company’s

shareholders specifically to determine whether the response of the company to Code provisions does enough, and then to take some action in order to force companies either to conform with the provisions (if they have not) or to explain why they have failed to do so.

• The aim of the comply or explain principle is to empower shareholders to make an informed evaluation as to whether non-compliance is justified, given the company’s circumstances. (eg SAB/CEO/Chairman Role)

2. Corporate Governance Environment

1. Corporate entity structure resulted in a split between ownership and management: This split results in agency risk – which is the raison-de-etre of corporate governance.

2. “Corporate governance is concerned with holding the balance between economic and social goals and between individual and communal goals. The governance framework is there to encourage the efficient use of resources and equally to require accountability for stewardship of these resources. The aim is to align as nearly as possible the interests of individuals, corporations and society”.

3. Corporate Governance, then is essentially about the responsible and ethical leadership of companies. This is leadership that is transparent, answerable and accountable towards the company’s identified stakeholders.

2. Corporate Governance – Implementation Corporate Governance in a business enterprise is primarily a function of three things: 1. Direction and leadership (the quality of the organisation’s strategy, the

calibre of executive management charged with developing and implementing the strategy, and the calibre of the board charged with supervision and overseeing).

2. Risk management and control (the processes in place to identify, evaluate, monitor and control risks associated with the successful delivery of strategic and operational objectives which ensure sustainability).

3. Accountability and reporting (the provision of a true, fair and accurate account of the stewardship of the enterprise, in a transparent manner, to relevant stakeholders).

• Governance has two drivers – Structure and Behaviour

Governance

Performance Conformance

Value Crea1on Resource u1lisa1on

Strategy

Accountability Assurance Compliance

Opportuni1es

Risks

2. Key Focus Areas of Corporate Governance

2. Corporate Governance - RSA - Overview King 3

1. Pillars of Corporate Governance 1. Leadership – Effective in meeting business goals 2. Sustainability – Moral/Economic imperative of 21st century 3. Corporate Citizenship – Inclusivity of stakeholders

2. Principles of King III 1. Responsibility 2. Accountability 3. Fairness 4. Transparency

3. Behaviours for Directors (per King III) 1. Inclusivity – society at large is silent partner incorporate governance 2. Conscience – intellectual honesty / independence 3. Commitment – dedication / effort 4. Courage – take risks with integrity 5. Competence – knowledge and skills (development of behavioural, governance,

technical)

3. ROLE OF THE BOARD

3. Role of the Board

Board of Directors The key corporate organ responsibility for implementing corporate governance is the Board of Directors, the “directing mind of the company”. Usually the Board would be responsible for: • Oversight of the company, including its control and accountability

systems • Input into and final approval of managements’ development of corporate

strategy and performance objectives • Reviewing and ratifying systems of risk management and internal

compliance and control, codes of conduct, and legal compliance • Monitoring senior management’s performance and implementation of

strategy, and ensuring appropriate resources are available

3. Role of the Board

Board of Directors • Approving and monitoring the progress of major capital expenditure,

capital management, and acquisitions and divestments • Approving and monitoring financial and other reporting • Board appointments, removals, succession planning and executive

remuneration

3. Role of the Board RSA COMPANIES ACT 71/2008 POWERS OF THE BOARD S66 – The business and affairs of a company must be managed by or under the direction of the board, which has the authority to exercise all the powers and perform any of the functions of the company, except to the extent that this Act or the company’s MOI provides otherwise

ENLARGEMENT OF BOARD POOL S66/Reg 38 – has extended rights, duties and liabilities of directors to prescribed officers who are persons who despite not being a director – exercise control or participate to a material degree in exercise of general executive control/management over the whole or significant portion of business/activities of company

3. Board Role in Corporate Governance

Strategy formulation – outward looking/future focused Policy making – inward looking/future focused Monitoring and supervising – inward looking/past and present focused Providing accountability – outward looking/past and present focused Performance

– Strategy formulation – Policy making

Conformance – Monitoring and supervising – Providing accountability

3. Features of Boardroom Dynamics

1. Culture: Values: Ethics: Tone at the top 2. Composition: Qualifications, experience, diversity,

independence, time 3. Roles: Responsibilities: Committees 4. Agendas: Tools: Secretarial Support

6. Risk Awareness/oversight 7. Talent development and reward, succession planning,

remuneration policy/mix and currency of skills

5. Information and Reporting/Stakeholder Awareness/Sensitivity - Communication

4. STAKEHOLDER EXPECTATIONS RE DIRECTORS DUTIES

4. Stakeholder Expectations Re Directors Duties

1. Compliance and Loyalty • Honest exercise of powers and for proper purpose • Lawful actions in accordance with MOI • Good faith – best interests of company (not only shareholders – must consider

stakeholders) 2. Independence of Judgement

• Unfettered judgement • Intellectual honesty • Business judgement rule

3. Conflict of Interest

• Recusal • Full Disclosure • Confidentiality of Information • No secret profits (fiduciary duty)

4. Stakeholder Expectations Re Directors Duties

4. Fairness

• Balance competing interests (minority)

5. Care Skill & Diligence • Reasonable diligence • High standard of professionalism

4. Characteristics of Best Practice Boardroom Behaviour

1. Board members must have clear understanding of role of Board (Cosec as Mentor)

2. An appropriate deployment of knowledge, skills, experience, judgement

3. Independent thought leadership 4. Questioning of assumptions/established orthodoxy 5. Challenge – Constructive confident, principled, rational, proportionate 6. Debate to be rigorous 7. Supportive decision making environment (NB: to be managed by

Company Secretary) 8. Common vision 9. Systematic closure on each item of board business

(Cosec to manage action list)

4. Corporate Governance – Board/Directors “Business Judgement Rule”

Section 76 of New Companies Act Directors Check-List for Decision Making by Directors Relative to Good Corporate Governance – as proposed by Judge Mervyn King • Do I have any conflict in this matter? If so, I must disclose it. • Am I basing my decision on all relevant facts, or on assumption and conjecture?

If the latter, I must wait until the facts are in hand. • Is this a rational business decision based on the facts I have at this time? • Is this decision in the best interests of the company? • How will I communicate this decision to shareholders? • Is this decision socially responsible? • And, finally, would I or the board be embarrassed if this decision and its

motivations appeared on the front page of a prominent newspaper?

4. Board Communication Skills Requirements of Directors

Consciousness of detail Insists that sufficiently detailed and reliable information is taken account of, and reported as necessary

Eclecticism

Systematically seeks all possible relevant information from a variety of sources

Numeracy

Assimilates numerical and statistical information accurately, understands its derivation and makes sensible, sound interpretations

Problem recognition

Identifies problems and identifies possible or actual causes

4. RSA King III – Governing Stakeholder Relationships

P8.1 The board should appreciate that stakeholders perceptions affect corporate reputation

• Reputation is relevant to economic value of company • Legitimate interests/expectations of stakeholders • Reputation is critical board agenda item • Board must identify its stakeholders • Reputation part of risk management • Annual review of stakeholder impact

4. RSA King III – Governing Stakeholder Relationships

P8.2 The board should delegate to management to proactively deal with stakeholder relationships

• Develop strategy/policies • Publish identified stakeholders • Mechanism for constructive engagement with stakeholders • Encourage shareholder participation in AGM • Stakeholders also have responsibility • Risk of disclosure of price sensitive information • Communicate stakeholder engagement, policies/practices in

integrated report

4. RSA King III – Governing Stakeholder Relationships

P8.3 The board should strive to achieve the appropriate balance between its various stakeholder groupings, in the best interests of the company

• Differing degrees of significance • Constructive engagement requires co-operation of

stakeholders • Stakeholders must subscribe to good governance principles

P8.4 Companies should ensure the equitable treatment of shareholders

NB: Protection of minorities

4. RSA King III – Governing Stakeholder Relationships

P8.5 Transparent and effective communication with stakeholders is essential for building and maintaining their trust and confidence

• Timely, complete, accurate, relevant, honest and accessible

information • Clear and simple language – channels to be accessible to

stakeholders • Communication guidelines to be adopted by board • Confidentiality and privilege P8.6 The board should ensure disputes are resolved as effectively

efficiently and expeditiously as possible

NB: Alternative dispute resolution (ADR)

5. RSA KING III – INTEGRATED REPORTING AND DISCLOSURE

• The board should ensure the integrity of the company’s integrated report – Holistic and integrated representation of finances and sustainability – Operations, sustainability issues, financial results, results of its operations

and cash flows: complete, timely, relevant, accurate, honest, accessible, comparable with past performance and forward-looking

• Sustainability reporting and disclosure should be integrated with the company’s financial reporting

– How money was made: positive and negative effects on stakeholders and future plans on how positives will be improved and negatives eradicated

– Transparency in sustainability reporting is critical – G3 guidelines to be considered

• Sustainability reporting and disclosure should be independently assured

5. RSA King III: Integrated reporting and disclosure

5. Stakeholders: The Importance of Integrated Reporting

1. It is critical that the board as a whole has a clear understanding of its mandate, which should include the purpose of the business of the company, its main value drivers, and the main stakeholders.

2. The board should have ongoing strategic communication with those stakeholders to understand their legitimate needs, interests and expectations. Thus informed, the board can make better decisions, and management can implement a more effective strategy.

3. The board must understand how the sustainability issues that are material to the business of the company have been embedded into the long-term strategy so that stakeholders, particularly the providers of capital, can make an informed assessment as to whether the company’s business will sustain value creation.

4. Integrated thinking and integrated management, requires the collective mind of the board to be applied to understanding how the financial performance affects the nonfinancial and vice versa.

5. Stakeholders: The Importance of Integrated Reporting

5. The two great challenges of the 21st century – financial stability and sustainability – are interconnected. Financial markets do not operate in isolation.

6. The collective mind of the board must articulate in clear and understandable language the financial and sustainability issues material to the business of the company and show that the business will be able to sustain value creation.

7. Companies need a complete understanding of the needs, interests and expectations of stakeholders, to take these into account in the decision-making process. But they also need to be guided by what is in the best interests of the company for maximisation of its total economic value.

8. During the reporting period, the corporation can use the better understanding of stakeholders’ needs, interests, and expectations to build a pathway of knowledge to prepare its integrated report.

5. Executive Remuneration Defining the Problem

1. High executive pay levels in absolute terms have been an issue for many years, but in recent years this issue has become more acute given the increasing differentials between the highest and lowest pay levels.

2. This has involved voting against annual pay arrangements and, in some cases, seeking enhanced power over such packages.

3. The question will be raised as to whether there has been market failure in international and national executive pay levels, and what are the policy implications of the answer to this question.

4. It is important that boards define the explicit rationale for their compensation arrangements. They should also take account of the way in which such compensation awards will be viewed by outside stakeholders. In the current highly – charged political environment, compensation transparency is an important aspect of retaining legitimacy in the eyes of stakeholders, regulators and the wider public.

5. Remuneration Problem of 2008 – Global Financial Crisis

5. There were flaws in the remuneration practices in the investment banking sector. Bonus driven remuneration structures encouraged reckless/excessive risk taking. The design of bonus schemes was not aligned with shareholders interests nor long term sustainability of banks.

6. Remuneration policies and practices were not at arms’ length – board did not exercise objective judgment – conflict of interest – dilemma of risk taking and remuneration structure – during boom, the board was less independent in monitoring remuneration and more accommodating in their bargaining.

7. Remuneration schemes were not transparent – they did not measure consequences – transparency must be improved by disclosure in non-technical terms.

5. Remuneration Current Perspectives

8. Weak link between performance and remuneration – need to determine long term KPI’s – ensure that generous incentives must be matched by strong risk management systems.

9. Big problem is ratio of CEO remuneration to that of average employee. “Say on Pay” must be implemented – shareholder resolution in respect of director’s remuneration.

10. Having regard to the government’s interest in the stability of the financial system is intervention in pay structures as legitimate as the traditional forms of financial regulation?

11. Risk of “Rewards for Failure”

11. MYTH OF INDISPENSABLE CEO • MYTH OF GLOBAL TALENT POOL [publication February 2013 by HIGH PAY

CENTRE UK]: The alleged existence of a global talent pool is cited as one of the reasons for the sharp rate of increase in executive pay over the past decade.

• This myth assumes that top executives are prepared to emigrate at short notice for a bigger package.

• It is the belief that the culture of bonus incentivisation was one of the causes of

the global financial crisis (2008). • It is the supposed scarcity of talent, and what is claimed to be the highly

competitive market for that talent, which is principally responsible for the surge in executive pay levels.

5. Remuneration

Indispensable CEO continued • The survey found that companies do not feel they need to search far and wide for

their next CEO. • The survey found that most companies do NOT have to scour the world for talent

but are able to recruit locally/internally. This debunks the heavily exaggerated and self –serving myth of the competitiveness of the international market for CEOs which is said to drive up executive pay.

5. Remuneration

5. Remuneration – Future Scenario

12. The focus on corporate governance is likely to concentrate on those activities of the Nomination and Remuneration Committees whose work stream cannot rely on the luxury of the “check-list driven” Audit, Risk and Social & Ethics Committees, but must deal inter alia, with the arcane art of the recruitment and reward of senior executives of the ilk of Bob Diamond of Barclays (2012 Libor Scandal).

13. The “arms race” in executive pay, aided and abetted, many believe, by the advice of external remuneration consultants (cynically referred to as “friends with benefits”), has unfortunately created a corporate elite (“celebrity CEO’s”) that is remote from its own workforce and the rest of the economy.

14. Key message to stakeholders – simplify, quantify, justify.

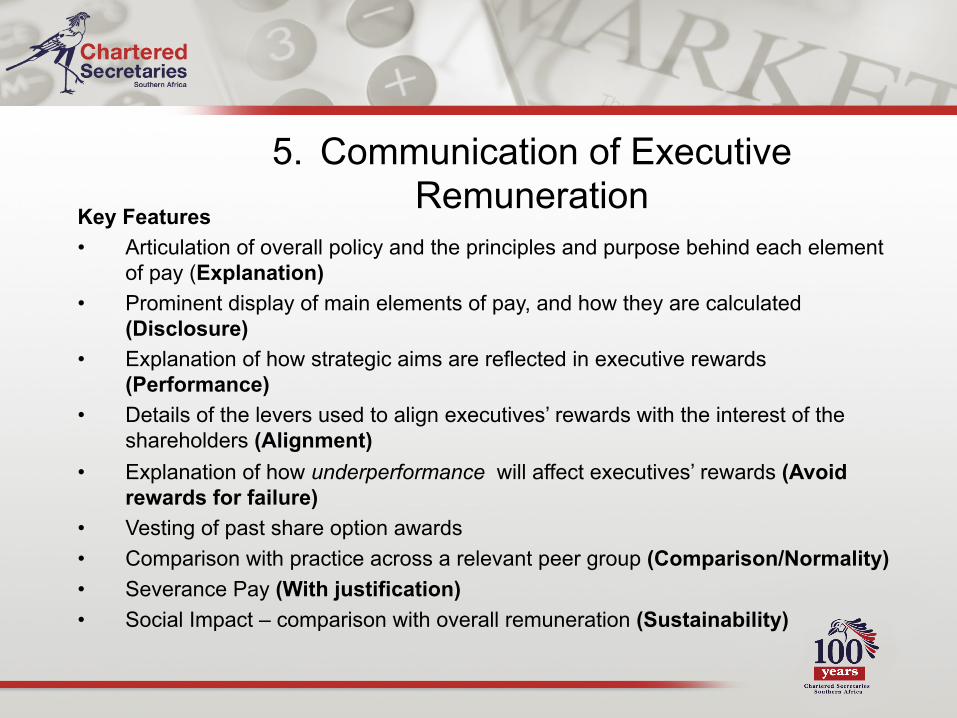

5. Communication of Executive Remuneration

Key Features • Articulation of overall policy and the principles and purpose behind each element

of pay (Explanation) • Prominent display of main elements of pay, and how they are calculated

(Disclosure) • Explanation of how strategic aims are reflected in executive rewards

(Performance) • Details of the levers used to align executives’ rewards with the interest of the

shareholders (Alignment) • Explanation of how underperformance will affect executives’ rewards (Avoid

rewards for failure) • Vesting of past share option awards • Comparison with practice across a relevant peer group (Comparison/Normality) • Severance Pay (With justification) • Social Impact – comparison with overall remuneration (Sustainability)

5. Remuneration South African Protocols

1. Non-executive directors fees must be approved by shareholders’ special resolution (Companies Act – S66)

2. Overall remuneration policy must be put to “advisory vote” at AGM (King III recommendation)

3. Companies encouraged to prepare remuneration report (Per King III)

5. Board Governance of Social Media

Knowledge Management 1. Avoiding social medial is no longer an option. Widespread use of

social media has potential to transform corporate agendas. 2. The first and most important social media question board directors

need to ask themselves is whether they have the knowledge necessary to understand these changes and new technologies.

3. Individual directors must educate themselves about social media – from technology to terminology. Directors and managers must understand social media technologies, the ethos of social media users, the dynamics of how “conversations” occur and people “engage” with one another, and the tools used to monitor and analyse social media activities.

4. Board need to investigate how all the various stakeholders the company affects, are using social media.

5. Board Governance of Social Media

Risk Management 5. The very existence of social media generates unavoidable risks for

companies – even when they choose not to be engaged in social media. Shareowners/Stakeholders with the most insignificant stakes can now stir wide rebellion at negligible cost.

6. Social media makes it more difficult for organisations to control information. A message spread by social media is seen to reflect the opinion of the general public, regardless of whether it actually does so, affecting the decision making of people in power

7. All stakeholders can now demand accountability. Ethics, working conditions, and company culture take on new importance as employees become de facto examiners and raters of the company, putting the company in the public spotlight.

5. Board Governance of Social Media

Risk Management – (continued) 8. Companies’ representatives – their employees – have the potential

to generate legal and other liabilities. Employees might unintentionally reveal trade secrets, blow the whistle on their employer or fellow employees, reveal business strategy, or provide insider information

9. A social media crisis could arise without warning – on a weekend or even on the other side of the globe while it is night-time at the company’s headquarters.

5. Board Governance of Social Media

Opportunities 10. Potential opportunities and advantages

• New level of transparency • Empowered stakeholders • Rise of e-lobbying and e-advocacy • Immediacy of social media

11. Companies can us social media channels creatively to improve stakeholder loyalty: and can develop new means of constructive dialogue with different constituencies.

12. Social media can be used to keep stakeholders informed, taking advantage of speed and reach of the reaction, company loyalty, around-the-clock availability, and person-to-person influence

13. Companies must develop social media policies for all employees, and include training on these policies

5. Ethics and Anti-Corruption

1. Anti-corruption, business ethics and the sustainability agenda are at

the forefront of good corporate governance. 2. Business leadership is responsible for setting the course by which

business operations succeed or fail in meeting the moral expectations of society and the financial goals of investors.

3. Leadership, via actions ,commitment and examples, sets the moral tone at the top, translating ethical principles into concrete behaviour. Business leaders must meet the ethical challenge in the context of fierce global competition and not fall into the corruption trap.

5. Ethics and Anti-Corruption

4. An important factor in dealing with corruption is the establishment of strong public and private regulating institutions. The rise of worldwide democracy, accountability and transparency have reduced the tolerance for corrupt behaviour and raised governance standard for both companies and nations as a whole.

5. Business is often perceived to be the cause of corruption. Business ethics is a means of ensuring behaviour consistent with the rule of law and other principles underpinning market economies and democratic governance.

6. Ethics and moral norms now set a new benchmark for appropriate business behaviour. The increased regulatory framework demands on disclosure, reporting and compliance are not enough to guard against corruption.

5. Ethics and Anti-Corruption

7. A proven anti–corruption tool is corporate governance which introduces standards and mechanisms of transparency ,accountability and compliance which should expose bribery and illegal behaviour, thus making corporate corruption unsustainable .

8. Ethics provide the moral compass of corporate governance. Stakeholders need to feel that they are treated fairly and honestly.

9. The board of directors bears the ultimate responsibility for the moral ethics and integrity standards that underpin culture of how a company conducts business.

10. To an ethical organisation, ethics is about doing business right, not merely compliance box-ticking. The board must establish and maintain a corporate ethics programme.

11. Ethics is a set of principles and values by which a company defines its

raison–de–etre , guiding its behaviour, conduct , commitment and communication.

5. Ethics and Anti-Corruption

6. CORPORATE GOVERNANCE HOW DOES THE COMPANY SECRETARY

HELP?

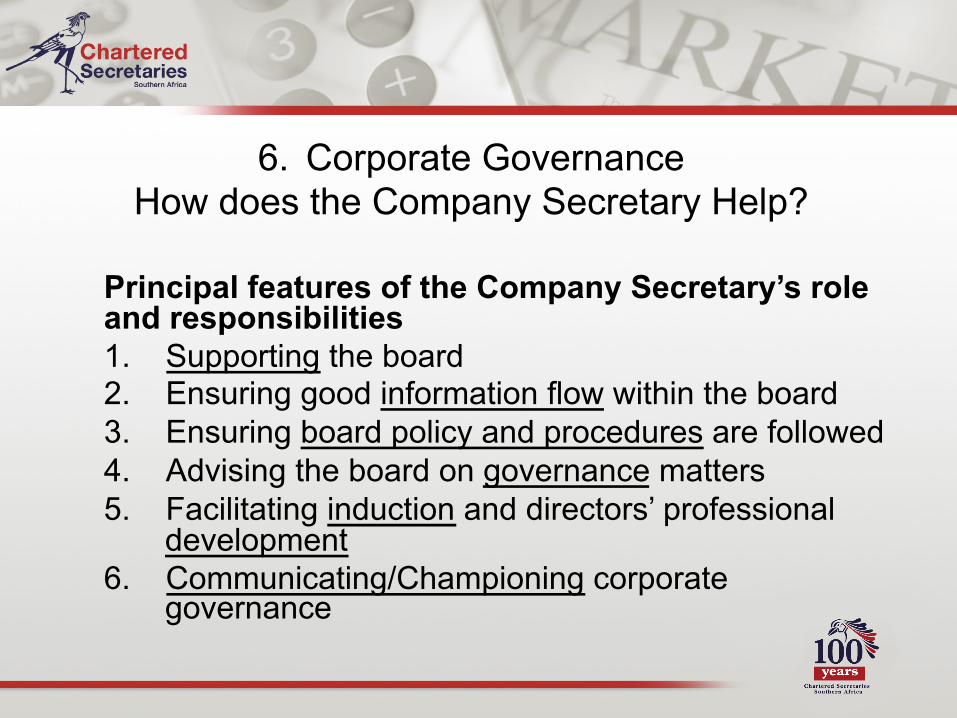

6. Corporate Governance How does the Company Secretary Help?

Principal features of the Company Secretary’s role and responsibilities 1. Supporting the board 2. Ensuring good information flow within the board 3. Ensuring board policy and procedures are followed 4. Advising the board on governance matters 5. Facilitating induction and directors’ professional

development 6. Communicating/Championing corporate

governance

6. The Role of the Company Secretary

Company Secretary’s Corporate Governance Role

1. Focus on Board Effectiveness/Independence (Nominations Committee)

2. Social Productivity: Ethical culture/compliance culture/Executive Pay GAP

3. Ensure Board / Committees are evaluated – Ensure succession planning

4. Maintain/Strengthen Ethics/Values – culture audit: Board’s working style, handling recession/downturn

5. Improve Shareholder communications – communicate governance practices in integrated report

6. Manage conflicts of interest 7. Watching brief on whether board is acting in best interests of

company

6. The Company Secretary and Board Communication

8. Shareholders/Investment Community

• To communicate with the stakeholders as appropriate and to ensure that due regard is paid to their interests.

• Primary point of contact for institutional and other

shareholders, especially with regard to matters of Corporate Governance. Assist in Investor Relations process.

6. Role of the Company Secretary - Conclusion

The Secretary’s administrative role is integral to the effective operation of a board. The Secretary is the conduit for information to the board. In particular the Secretary serves as an “enhancer” to the effectiveness of the board in the following ways. • The provision of concise and accurate board papers (meeting packages) • Timing and regularity of board meetings • Obtaining board approval of policies on administrative processes • Ensuring timely decision making by the board • Recording policies and decisions • Keeping the board informed – raising pertinent current issues • Conscience of the company – custodian of corporate governance • Board evaluation process

7. BUSINESS, SOCIETY AND CORPORATE GOVERNANCE

7. Business, Society and Corporate Governance

1. Values culture and ethics are cornerstones of business integrity and good governance practice. They must be embedded into the corporate DNA.

2. Raising standards or corporate governance cannot be achieved by structure/process/check-lists alone. Governance is not only a compliance exercise.

3. We see the emergence of new sense of entrepreneurship, called responsible capitalism. Business must combine sustainability with the profit motive.

4. Business must have a purpose in society – in fulfilling that purpose, they are expected to earn a fair profit return.

Conclusion What do Stakeholders Really Expect?

1. Business leaders need to understand that prosperity of organisations depend upon prosperity of people and other sectors of the economy.

2. Most stakeholders need pride, hope, wealth and power, dignity and respect together with a satisfying return on their investment and efforts.

3. The supreme goal of business should not be shareholder wealth creation but rather profitable business which delivers good value services to customers. The future philosophy of capitalism requires a new morality – a socio-economic approach which does not rely only on the market. The value of business activity should not be completely delineated by the market.

4. The value of business is dependent on values with which we do business. Society cannot regulate business behaviour only by legislation and regulations. The culture of moral values must encompass corporate governance processes.

Features of Fit for Purpose Governance: The Key Dozen

Conclusion

Culture Vision Values

Transparency Accountability Disclosure

Trust Confidence

Integrity Independence Competence

Ethics

Thank you

Question and Answers?

![[Organisation’s Title] Environmental Management System](https://img.pdfslide.net/doc/110x75/56812bd4550346895d903d0a/organisations-title-environmental-management-system.jpg)