Embed Size (px)

Citation preview

January 30, 2013

Avoiding the Inferno: Making Import and Export Issues Predictable in the Year of the Dragon

Avoiding the Inferno: Making Import and Export Issues Predictable in the Year of the Dragon

Three PanelsThree Panels

1. Foreign Corrupt Practices Act;

2. U.S. Trade and Customs Law; and

3. False Claims Act – Civil and Criminal Customs Actions.

2

Dr. Graeme Hunter – NERA

Peter J. Bradford, Managing Director – KPMG LLP

Tom Gorman, J Jackson and Beth Forsythe – Dorsey & Whitney LLP

Foreign Corrupt Practices ActForeign Corrupt Practices Act

33

4

This Resource Guide “aims to provide businesses and individuals with information to help them This Resource Guide “aims to provide businesses and individuals with information to help them

•

“abide by the law

•

“detect and prevent FCPA violations, and

•

“implement effective compliance programs.”

5

The Joint Resource GuideThe Joint Resource Guide

•

What is it?

•

Does it accomplish its goals?

•

How can we effectively use it?

6

Introduction Introduction

•

The Guide is an effort to provide guidance to the market place re FCPA

•

It comes in the wake of calls for clarification by the OECD

•

It also follows intense lobbying by business groups for reform that lead to Congressional hearings

7

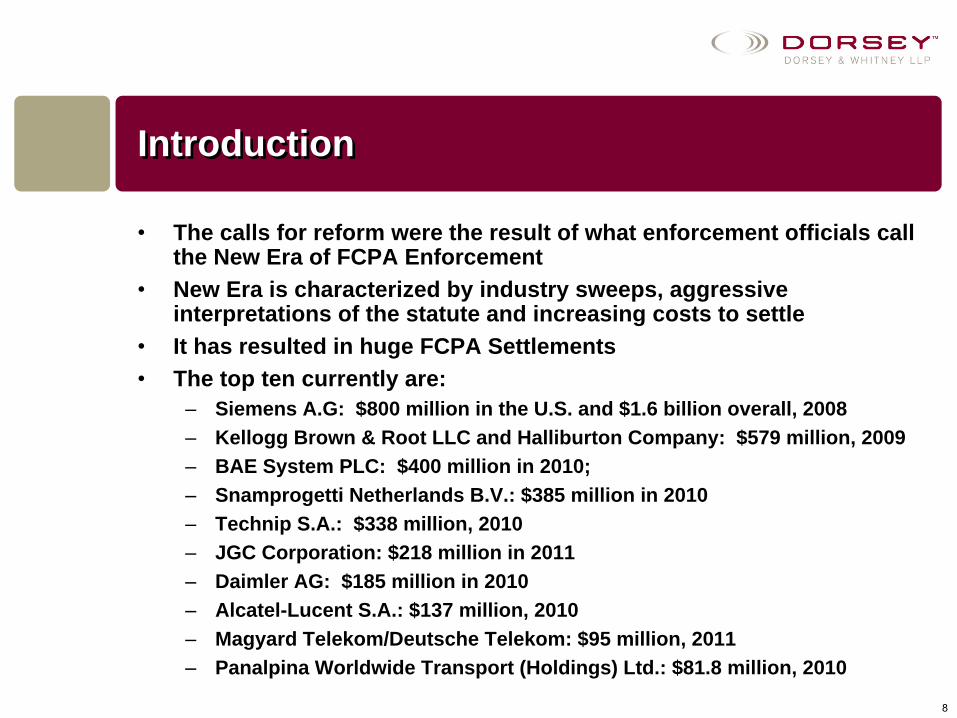

Introduction Introduction

•

The calls for reform were the result of what enforcement officials call the New Era of FCPA Enforcement

•

New Era is characterized by industry sweeps, aggressive interpretations of the statute and increasing costs to settle

•

It has resulted in huge FCPA Settlements•

The top ten currently are: –

Siemens A.G: $800 million in the U.S. and $1.6 billion overall, 2008–

Kellogg Brown & Root LLC and Halliburton Company: $579 million, 2009–

BAE System PLC: $400 million in 2010; –

Snamprogetti Netherlands B.V.: $385 million in 2010–

Technip S.A.: $338 million, 2010–

JGC Corporation: $218 million in 2011–

Daimler AG: $185 million in 2010–

Alcatel-Lucent S.A.: $137 million, 2010–

Magyard Telekom/Deutsche Telekom: $95 million, 2011–

Panalpina Worldwide Transport (Holdings) Ltd.: $81.8 million, 2010

8

The GuideThe Guide

•

The Guide is a comprehensive review of the FCPA and related enforcement issues

•

It covers–

Origin of the statutes

–

The anti-bribery provisions–

The accounting provisions

–

Related U.S. statutes–

Guiding principles of enforcement

–

Resolutions and sanctions

9

The GuideThe Guide

•

Essentially a restatement of the views of enforcement officials

•

Many of its citations are to charging documents from New Era cases

•

It does not respond to the issues raised by business groups or Congress re:–

Definition of foreign official

–

Successor liability –

Compliance defense

10

The GuideThe Guide

•

It does define the key principles for a compliance program–

Tone at the top–

Code of conduct –

Responsibility–

Risk assessment –

Training and updating–

Incentives and disciplinary measures–

Third party due diligence–

Confidential reporting

•

If properly utilized these can be used to fashion the compliance defense called for by business groups

11

© 2011, KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarksof KPMG International. 24506KCG

FCPA Risk Influencing Business Decisions

12

A Dow Jones report released in 2012 shows that:

The survey shows a rise in the use of anti-corruption programs, with 83% of companies reporting in-place programs versus 74% in 2011.

Those surveyed believe regulation has created greater fairness across industries (66%), saved them money (62%) and improved business-partner relationships due to scrutiny (57%).

Emerging markets continue to present businesses with new risks and challenges.

The incidence of companies losing business to unethical competitors is on the rise, with 44% of compliance professionals suspecting they have lost contracts to unethical competitors.

Companies are still struggling with due diligence despite its growing importance in a more heavily regulated environment, and as a result only half feel very confident in their programs.

Source: “Dow Jones State of Anti-Corruption Compliance Survey.” Published 2012.

© 2011, KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarksof KPMG International. 24506KCG

Where to Start?

13

Understand where your company does business

Countries with historically poor records around bribery and corruption of government officials

Countries that have nationalized industriesUnderstand the nature and ownership of your partners

Companies that are state controlled or have government ties or partial ownership

Companies that are intermediaries between foreign-based companies and local governments (agents, brokers, distributors)

Customers should be evaluated on the same criteria as agencies and vendors−

Management should understand the composition of their organizations as well and institute some due diligence around customers and distributors

Understand where your business interacts with government agencies

Sales, entertainment, and purchasing are more commonly attributed areas

Tax, customs, logistics, environmental compliance, facilities are other areas to consider

© 2011, KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarksof KPMG International. 24506KCG

Consultants/Third Parties

Unions/Labor Groups

Customs/Logistics

Procurement Sales

Emissions (Air, Water)/Regulators

Waste/Hazardous MaterialsRemoval

Tax, VAT

Government Touch Points

14

© 2011, KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarksof KPMG International. 24506KCG

Continuous Monitoring

15

Prevention

Roles and Responsibilities –

for the program, Board oversight, corporate tone, and culture

Risk Assessment –

has a FCPA/ABC

risk assessment been conducted, evaluate scope and completeness of assessment

Policies and Procedures –

has P&P

been implemented, are they reasonably designed and updated

Due Diligence –

employees and third parties

Communication –

has compliance communication been communicated

Training –

has training been delivered to directors, officers, employees, and third-

party agents

Certification –

have certifications of compliance been obtained from appropriate personnel (e.g., sales management, agents)

© 2011, KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarksof KPMG International. 24506KCG

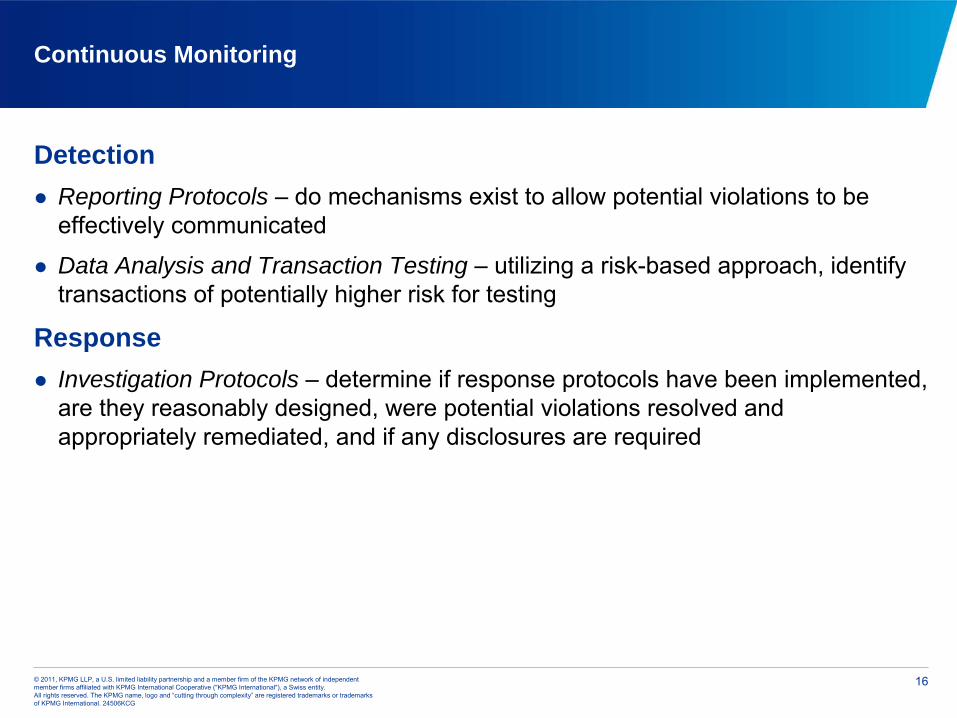

Continuous Monitoring

16

Detection

Reporting Protocols –

do mechanisms exist to allow potential violations to be effectively communicated

Data Analysis and Transaction Testing –

utilizing a risk-based approach, identify transactions of potentially higher risk for testing

Response

Investigation Protocols –

determine if response protocols have been implemented, are they reasonably designed, were potential violations resolved

and appropriately remediated, and if any disclosures are required

© 2011, KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarksof KPMG International. 24506KCG

Anti-bribery and Corruption Framework

PreventionPrevention DetectionDetection ResponseResponseBoard/audit committee oversight

Executive and line management functions

Internal audit, compliance, and monitoring functions

Fraud and misconduct risk assessment

Code of conduct and related standards

Employee and third-party due diligence

Communication and training

Process-specific fraud risk controls

Hotlines and whistle-

blower mechanisms

Auditing and monitoring

Proactive forensic data analysis

Internal investigation protocols

Enforcement and accountability protocols

Disclosure protocols

Remedial action protocols

© 2011, KPMG LLP, a U.S. limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarksof KPMG International. 24506KCG

Since the maturity of the anti-bribery control structures and processes at each location may vary, use a “tiered”

approach

The main focus is to apply appropriate assessment procedures based on the control readiness of each location

Such an approach would likely reduce the risk of potential disclosure issues

An upfront evaluation of the degree of control readiness for each location would be necessary

FCPA

Control MaturityImmature Advanced

Site Level Assessments

18

Internal Investigations: Triggers and Guiding Principles Internal Investigations: Triggers and Guiding Principles

•

Triggers–

Government investigation

–

Internal source of information •

whistleblower •

accounting irregularity

•

Resource Guide encourages self-reporting–

For public companies, generally the only option

–

Think before picking up the phone to call DOJ or SEC

–

Guiding principle: How will the government view the way this investigation is being conducted?

19

Internal Investigations: Critical Steps Internal Investigations: Critical Steps

•

Determine what happened –

Does it amount to a violation?–

What is the scope of the problem? •

Take immediate remedial measures (e.g. termination, place hold on account)

•

Understand how it happened–

Control environment–

Company structure–

Common theme: Lack of sufficient understanding of how business is being conducted on company’s behalf

•

Sales agents•

Third parties•

Begin developing longer term remedial measures–

Use Resource Guide to inform this process20

Internal Investigations: Complications Internal Investigations: Complications

•

Maintaining ability to conduct investigation on your terms–

Whistleblowers

–

Privilege issues

•

Working with employees whose activities are being scrutinized

•

Third parties–

Access to documents

–

Access to people–

Access to public information in foreign countries

21

22

Bribery and Economics

How does bribery alter the probability of securing the project?

What is the “economic profit”

of the project change from bribery?

Other types of claims

23

FCPA and Economics

Example:

TSKJ

paid $182 million in bribes and received contracts worth more than $6 billion in relation to a Nigerian Liquefied Natural Gas (LNG) plant

Combined, the four TSKJ

settlements are the largest FPCA

enforcement set of actions ($1.5

billion)

Notes and Sources:The TSKJ

name was taken from the joint venture participants: Technip, Snamprogetti, Kellogg Brown & Root and JGC

Corporation. “The New Era of FCPA

Enforcement”, Gorman and McGrath, Securities Regulation Law Journal, Vol. 40:4 (2012) and The FCPA

Blog.

24

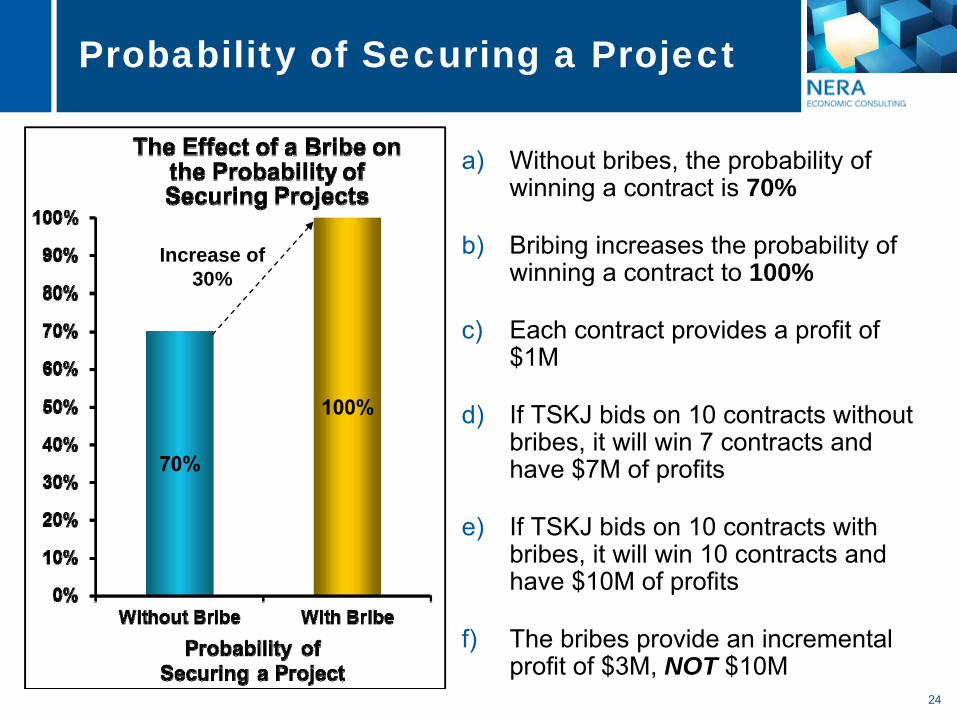

Probability of Securing a Project

a)

Without bribes, the probability of winning a contract is 70%

b)

Bribing increases the probability of winning a contract to

100%

c)

Each contract provides a profit of $1M

d)

If TSKJ

bids on 10 contracts without bribes, it will win 7 contracts and have $7M of profits

e)

If TSKJ

bids on 10 contracts with bribes, it will win 10 contracts and have $10M of profits

f)

The bribes provide an incremental profit of $3M, NOT $10M

Increase of30%

25

Economic Profit An Example from The Guidelines

“Pecuniary gain" … means the additional before tax profit to the defendant resulting from the relevant conduct of the offense. Gain can result from either additional revenue or cost savings.

For example, an offense involving odometer tampering can produce additional revenue. In such a case, the pecuniary gain is the additional revenue received because the automobiles appeared to have less mileage, i.e., the difference between the price received or expected for the automobiles with the apparent mileage and the fair market value of the automobiles with the actual mileage.

26

Economic Profit from Revenue Changes (Alternative Sales)

Example: TSKJ

had a $6B project obtained through bribes

TSKJ

was offered an alternative $5B project (with the same costs)

TSKJ

had to turn down the alternative $5B project it because it was at capacity

The economic profit of the bribe would be $1B

$5B $5B

$1B $1

billion

27

Economic Profit From Cost Changes (No Project)

Let’s say TSKJ

builds equipment for multiple LNG

plants each year

Each identical set of LNG

equipment can be built at

TSKJ’s

Spain high-cost factory for $15M…

Or, at TSKJ’s

South Africa low-cost factory for $10M

The LNG

equipment for the Nigerian contract was built

in low-cost South Africa for $10M

If the Nigerian contract was not acquired, TSKJ

would

have lost the revenue, but would also have lower costs

Let’s say the Nigerian contract provided $50M of revenue and had $30M of costs, including $10M for equipment

28

Economic Profit From Cost Changes (No Project)

Together with the Nigerian contract, all TSKJ

projects

combined have:

$100M of revenues,

$70M of costs

and thus $30M of profits

The Nigerian contract alone has:

$50M of revenues,

$30M of costs ($10M equipment)

and thus $20M of profits

29

Economic Profit From Cost Changes (No Project)

Without the Nigerian contract, TSKJ

loses $50M of revenue

Costs are reduced by $30M…

And, TSKJ

reduces production at the high-cost plant, while maintaining production at the low-

cost plant

This reduces costs by $35M in total

($30M + $5M from high-cost reduction)

Profit falls by only $15M, not the $20M profits earned on the Nigeria project

TSKJ

maintains production at the low-cost plant and uses the equipment in its other projects

Former Congressman Don Bonker – APCO

William Perry and Emily Lawson – Dorsey & Whitney LLP

U.S. Trade and Customs LawU.S. Trade and Customs Law

30

Trade and Customs ProblemsTrade and Customs Problems•

The problem–Millions of dollars retroactive AD duties missing

•

$800 million In AD Duties on Just Four Products – mushrooms, garlic, crawfish and honey.

•

Total missing AD duties well over $1 billion•

Intense Political Pressure by Congress on Customs to Enforce AD and CVD orders

•

Attempts to Get Around Antidumping and Countervailing Duty Orders – Circumvention

•

Customs Issues and Criminal Problems•

337 Year Long IP Investigation at the ITC – Exclusion Order

31

Overview of AD and CVD LawOverview of AD and CVD Law

•

To win an antidumping or countervailing duty case, the Petitioner(s), usually the US Industry:–

Must prove dumping or subsidization at the Commerce Department

–

Injury or Threat of Material Injury at the U.S. International Trade Commission (“ITC”) – Entire Domestic Industry

–

Year long Proceeding –

Jurisdiction – In Rem

–

Expanding Scope – Aluminum Extrusions

32

What is Dumping?What is Dumping?

•

Market economy – US Sales below Normal Value – home market prices or Fully Allocated Cost of Production

•

China–Nonmarket Economy Country – Do not Use Actual Prices and Costs in China

•

Construct Cost – Factors of Production•

Surrogate Values from Surrogate Country – India, Thailand, Indonesia, Philippines or Ukraine

•

Wood Flooring – Indonesia or Philippines•

Solar Cells – India or Thailand

•

Inherently arbitrary and capricious •

2016 – 15 Years after WTO Agreement

33

Countervailing Duty – To offset subsidies Given by the Chinese government Countervailing Duty – To offset subsidies Given by the Chinese government

•

On March 30, 2007 Commerce applied the US CVD law to imports from China in Coated Free Sheet Paper case.

•

CVD Duties are Not Small–615% Circular Welded Pipes from China

•

CVD Duties to Countervail a subsidy, a benefit, money, given by the government to a Chinese company for exporting products OR to a specific industry

•

Commerce looks at benchmark in foreign company to determine size of subsidy

•

Dirty factory land in China looks at land in Thailand for a shopping center

•

Mandatory Respondents, Separate Rate Companies and PRC Wide Rate

34

Critical Dates for Importers in AD Investigation Critical Dates for Importers in AD Investigation

•

160-210 Days DOC Preliminary AD Determination•

CVD Earlier – 65-150 days

•

Day Liability Begins to run – require a bond or cash deposit

•

Critical Circumstances – Solar Cells•

7 Days After ITC Final Injury Determination – AD CVD Order

•

ITC Final Injury Publication Date Retroactive Liability Begins

•

AD and CVD orders stay in place 5-30 years

35

ANNUAL REVIEW INVESTIGATIONSANNUAL REVIEW INVESTIGATIONS

•

If request, new review investigation every year

•

Every year dumping and countervailing duty margins change.

•

Every year for the importer of record new roll of the dice.

•

Review Investigation Starts – Anniversary Month

•

Takes Year and a Half

•

But Review Investigations Can Lead to Exclusive Distributorships

•

Saccharin, Sebacic, Indigo and Aspirin

•

Sunset Reviews – Injury battle at the ITC, but in China cases ITC refused to Lift Order if DI fights to keep it in place

36

CASH DEPOSITS NOT DUTIESCASH DEPOSITS NOT DUTIES

•

Dumping rates and CVD rates in initial investigation, not dumping duty – cash deposit rate

•

Actual Dumping and CVD Duties Determined in Review Investigations

•

Retroactive Nature of AD Law

Importer of Record Liable for difference PLUS INTEREST

Furniture 16-216%, Steel Nails 21-118%, Ironing Tables

0 to 157%

No Reimbursement of Dumping or Countervailing Duties

•

Dumping Margin or CVD rate Determined in Review Will be cash deposit for subsequent Review period.

37

Protection and PoliticsProtection and Politics

•

Do not be the importer of record, consider a coalition•

Do not say this is the foreign exporter’s problem. Importer is liable, not the foreign exporter

•

Political Problem – Many importers have abandoned the political field in Washington DC in AD and CVD cases.

•

The worst political situation in Washington DC on China – GPX case December 2011-March 8, 2012

•

Trade War – Tip of the Iceberg – 337/IP, Customs, Antitrust, Securities, Products Liability

•

Chinese Government Retaliation – US Exports of Polysilicon, Cellulose Pulp, Chemicals in Varnishes and Paints

•

We have a trade war•

Politics of China Trade – How can we change the dialogue38

Insure That U.S. Officials And Congress Remain “Upright” on Trade Rulings

•

Most Countries have legal mechanisms to address unfair trade practices, but often they are applied equally and fairly.

•

In the U.S., public interest is not being served if application of trade laws are politicized or unfairly applied.

•

U.S. –

China trade –

recent government rulings are proving discriminatory and certainly damaging to both:

Chinese producers being shut out of the U.S. market.

American importers who pay the prohibitive tariffs.

End-users compelled to pay higher tariffs, often threatening cost-effectives of projects (solar plants).

•

In the long term Congress must revise our trade laws to insure that the DofC

and ITC (and yes, CFIUS) rulings are balanced.

Currently one-sided favoring U.S. companies that may be “injured”

by imports.

Must take into account U.S. importers who are also “injured”

when prohibitive tariffs are applied.

39

Insure That U.S. Officials And Congress Remain “Upright” on Trade Rulings

•

In the short term, Chinese producers/U.S. importers/end-users must collaborate to counter the political activity that is affecting their businesses and could well prompt a trade war with China.

•

A “collaborative”

approach is what is giving the other side an advantage on these

government rulings. Examples:

Coalition for American Solar Manufacturing (CASM).

The Wind Tower Trade Coalition.

American Wind Industry Association.

•

What makes them effective?

It gives them collective clout on single cases.

Rally support on Capitol Hill.

Mobilize others (trade associations, local public and private leaders, media) to strengthen their case.

Arouse concerns over Chinese imports/economic dominance to sparking a reaction from China-basher Congressmen.

40

Insure That U.S. Officials And Congress Remain “Upright” on Trade Rulings

•

What should the U. S. import side do?

Create a similar coalition (China producers, U.S. importers and end-users (pool resources).

Adopt strategies (coordinate with law firm) that will provide stronger, more effective representation on the import side.

Prepare/distribute info on economic effects or potential injury when punitive tariffs are imposed.

Mobilize regional/local public support (letters to Congressmen) about the economic impacts of rulings.

Proactively fashion awareness on traditional media outlets and today’s social media to match what competitors are posting on Google and other internet venues.

•

Purpose and Objectives:

Insure that U.S. officials and Congressmen remain “upright”

(hear both sides) when presiding over trade and CFIUS

cases.

Build closer and reliable networks on Capitol Hill and officials

in Washington.

Convey message to China producers of effort to insure equal and fair treatment by the U.S. government.

41

U.S. Customs ComplianceU.S. Customs Compliance

•

U.S. Customs & Border Protection (“CBP”)

•

The Customs Modernization Act or “Mod Act” (enacted in 1993)

•

Concepts of “informed compliance” and “shared responsibility”Burden on importers (“importer of record”) to provide CBP correct and accurate information and apply applicable laws when making entryObligation of CBP to inform importers of legal duties

CBP has prepared a number of Informed Compliance publications on import topics available at: http://www.cbp.gov/xp/cgov/trade/legal/informed_compliance_pubs/

42

U.S. Customs ComplianceU.S. Customs Compliance

•

Reasonable Care:

The importer is “responsible for using reasonable care to enter, classify and determine the value of imported merchandise and to provide any other information necessary to enable U.S. Customs . . . to properly assess duties, collect accurate statistics, and determine whether other applicable legal requirements, if any, have been met.” 19 U.S.C. § 1484.

43

U.S. Customs ComplianceU.S. Customs Compliance

•

Reasonable Care (A Checklist for Compliance)–

Merchandise description & tariff classification (rate of duty)

–

Valuation (including assists, and related party transactions)

–

Country of origin/marking/quota –

Intellectual property rights

–

Duty reduction preferences (e.g., NAFTA and Generalized System of Preferences); and

–

Textiles and apparel –

Merchandise transshipment

–

Antidumping/countervailing duty 44

U.S. Customs ComplianceU.S. Customs Compliance

•

What is Reasonable Care? –

The drafting Committee of the Mod Act stated that an importer should consider utilizing the following aids:

•

Seeking guidance from CBP through the pre-importation or formal ruling program;

•

Consulting with a customs broker, customs consultant, a public accountant or an attorney;

•

Using in-house employees such as counsel, a customs administrator, or if valuation is an issue, a corporate controller, who have experience and knowledge of customs laws, regulations and procedures.

H. Rep. No. 103-361 at 120, 1993 U.S.C.C.A.N. 2670 (1993).

45

U.S. Customs ComplianceU.S. Customs Compliance

•

What is Reasonable Care? (cont.)

CBP defines negligence as a violation that results from an act or acts done through the failure to exercise the degree of reasonable care and competence expected from a person in the same circumstances. 19 C.F.R. Pt. 171, App. B(C)(1).

46

U.S. Customs ComplianceU.S. Customs Compliance

•

Under CBP’s standard for “reasonable care” importers are expected to have documented and demonstrable internal procedures and controls that are audited.

•

Policies and procedures–

Importers must have written policies

–

Must explain application of procedures in practice

47

U.S. Customs ComplianceU.S. Customs Compliance

•

Record Keeping & Documenting Reasonable Care–

5 years and beyond

–

Are import recordkeeping requirements established in the company records retention program?

48

U.S. Customs ComplianceU.S. Customs Compliance

•

Customs Compliance Program –

Evaluation of company’s customs operations

•

Are you a large or small importer? •

Are your imports high risk materials? •

Who are your trading partners? Are they from high risk countries?

•

Evaluate the number, types, and complexity of classification of imports

–

Are they specifically provided for in the HTS? •

Do you use special duty programs like FTA’s (Free Trade Agreements) or GSP (Generalized System of Preference)?

–

Can the company substantiate use of the program through documentation?

49

U.S. Customs ComplianceU.S. Customs Compliance

•

Customs Compliance Program (cont.)–

Have your imports increased or decreased significantly?

–

What other government agencies have jurisdiction over your goods and what requirements must be met? (EPA, FDA, etc.)

•

CBP works with 47 other government agencies to mitigate threats through enforcement strategies

–

What is your valuation methodology?

50

Presented By:William Perry, Ed Magarian and Emily LawsonDorsey & Whitney LLP

False Claims Act – Civil and Criminal Customs Action False Claims Act – Civil and Criminal Customs Action

51

U.S. Customs ViolationsU.S. Customs Violations

•

Civil Enforcement Methods

•

Focus on actions of importer of record

•

Importers must demonstrate reasonable care in entering merchandise–

Classification of goods

–

Valuation of goods–

Origin of goods

52

U.S. Customs ViolationsU.S. Customs Violations

•

Failure to comply with Customs laws may result in a civil penalty proceeding under 19 U.S.C. § 1592. Section 1592 provides for penalties against any person who:

•

By fraud (i.e., voluntarily and intentionally), gross negligence (i.e., with actual knowledge or wanton disregard), or negligence (i.e., fails to exercise reasonable care);

•

Enters or introduces (or attempts to enter or introduce) any merchandise into the commerce of the U.S.;

•

By means of any document or electronically transmitted data or information, written or oral statement, or act which is material and false, or any omission which is material (i.e., the falsity has the potential to alter the classification, appraisement, or admissibility of merchandise, or the liability for duty or if it tends to conceal an unfair trade practice under the antidumping, countervailing duty or similar statute, or an unfair act involving patent or copyright infringement).

53

U.S. Customs ViolationsU.S. Customs Violations

•

Penalty exposure in § 1592 case based on level of culpability (maximum):

Negligence – 2 times the loss of lawful duties, taxes, and fees or 20% of the dutiable value if the violation did not affect the assessment of duties (not to exceed the domestic value of the merchandise)

Gross Negligence – 4 times the loss of lawful duties, taxes, and fees, or the domestic value or, if the violation did not affect the assessment of duties 40% of the dutiable value (not to exceed the domestic value of the merchandise)

Fraud – The domestic value of the merchandise

•

Mitigation – Customs and Border Protection (CBP) offers opportunities to reduce any penalty through petition

54

U.S. Customs ViolationsU.S. Customs Violations

•

CBP Priority Trade Issues (PTIs)

•

PTIs drive investment of CBP resources and enforcement

List of PTIs in alphabetical order:–

Agriculture Program–

Antidumping and Countervailing Duties–

Import Safety–

Intellectual Property Rights –

Penalties –

Revenue–

Textiles–

Trade Agreements (FTAs or GSP) 55

U.S. Customs ViolationsU.S. Customs Violations

•

The U.S. has criminal laws as well as civil laws enforcing customs violations

•

CBP is referring more cases to the Department of Justice for criminal investigation and prosecution

•

Additional potential defendants (foreign-based companies; consignees)–

Corporate as well as personal exposure

–

Additional theories of culpability and liability (e.g., conspiracy)

–

Additional sanctions, including potential for prison sentence and penalties

56

U.S. Customs ViolationsU.S. Customs Violations

•

Criminal statutes for Customs prosecution: –

18 U.S.C. § 541 (Entry of Goods by Means of False Statements)

–

18 U.S.C. § 542 (Entry of Goods by Means of False Statements)

–

18 U.S.C. § 545 (Smuggling Goods into the U.S.)–

18 U.S.C. §1519 (Destruction, Alteration, or Falsification of Records)

–

18 U.S.C. § 371 (Conspiracy)

57

U.S. Customs ViolationsU.S. Customs Violations

•

United States v. Wolff, et al. – Evasion of Antidumping Duties for Honey from China Imports

•

Criminal charges alleging conspiracy to evade nearly $80 million in antidumping duties by way of transshipping Chinese honey through third countries−

Antidumping duties have been in place on imports of honey from China since 2001

•

Defendants, including executives and companies allegedly falsified, in part, U.S. Customs entry forms and sales documents

58

59

False Claims ActFalse Claims Act

•

False Claims Act, 31 USC 3729(a)(1)(G), can be used by Private Parties to Police Customs Fraud

•

Reverse False Claims– knowingly makes a false record or statement to avoid or decrease an obligation to pay or transmit money or property to the Government

•

Relator in the Shoes of Government – Individual Whistleblower or Competitor

•

FCA Complaint Filed in Secret and Served on Govt – DOJ and US Attorney

•

US Govt has 60 days to decide to intervene but will often extend to do a complete investigation

•

Remedy Triple Damages Plus Attorney’s Fees Relator with government intervention 15-25% of any recovery of US government

•

If US government chooses not to intervene, Relator can prosecute the case by itself receive up to 30% of any recovery

•

US Government Can Go Back and Look at 6-10 years of Past Imports

60

FCA Cases Will IncreaseFCA Cases Will Increase

•

Pervasive Evasion of US Antidumping and Countervailing Duty Laws

•

Google type in "antidumping china and transshipment" 100s Companies Advertising

•

Transshipment is a crime•

The Customs Trade Facilitation and Enforcement Act of 2012

•

FCA Cases Useful •

Feedback from US Government to US producers and competitors

•

Govt Must Tell Them – E-Allegation – No Feedback•

Relatively cheap to bring FCA case because Government Prosecutes – Very expensive to defend

61

Recent FCA Cases – Evasion AD CVD Duties Recent FCA Cases – Evasion AD CVD Duties

•

Violet Pigment, United States ex rel. Dickson v. Toyo Ink Manufacturing Co., Ltd., et al., No. 09-CV- 438 (W.D.N.C.). December 17, 2012

•

Brought by Competitor $45 million dollar payment Settlement $7,875,000 to Relator

•

Doe v. Staples, Inc., et al., No. 08-cv-00846-RJL (D.D.C.) – Qui Tam Action against Target, Office Max, Staples Pencils Transshipped through other countries to avoid AD duties

•

Govt Chose Not to Intervene – Difficult Case for Relator•

United States v. Bank of China (S.D.N.Y. 2003)•

Mushroom importers transshipped Chilean mushrooms through Canada to avoid antidumping and customs duties

•

Bank of China , which financed the operations, also named as defendant

•

Bank settled for $5.25 million, Denying all Liability

62

Why Me or My Company Why Me or My Company

•

Current or Former Employees

•

Competitor

•

Ongoing civil or criminal investigation of others

•

Government monitoring, investigations, audits

•

Hotlines: E.g. 866-DHS-2-ICE

•

Media stories

•

Rumors

63

Whistleblower ProcessWhistleblower Process

•

Qui Tam relator discloses Information

•

Qui Tam relator files suit under seal and provides written statement

•

Government decides whether to intervene–

Government Has 60 days to decide, unless extended

–

Government investigates

•

If government intervenes, government takes control of the case. (prosecute, settle, dismiss)

•

If government does not intervene, plaintiff can go forward on behalf of the United States

64

False Claims Act in Import CasesFalse Claims Act in Import Cases

•

Any person who (1) knowingly presents, causes to be presented, to an officer or employee of the United States Government or member of the Armed Forces of the United States a false or fraudulent claim for payment or approval; . . . . or (7) knowingly makes, uses, or causes to be made or used, a false record or statement to conceal, avoid or decrease an obligation to pay or transmit money or property to the Government.

65

KnowledgeKnowledge

•

Means actual knowledge; acting in deliberate ignorance of the truth or falsity of the information; or acting in reckless disregard of the truth or falsity of the information.

66

Penalties Penalties

•

Damages

•

Treble damages

•

Penalties per claim

•

Costs of litigation

67

What Can You Do to Mitigate RiskWhat Can You Do to Mitigate Risk

•

Know your business partners – especially those from whom you import products

•

Understand your transactions

•

Examine your practices

•

Institute an effective compliance program

•

When issues arise, execute on that program.

68

Effective Compliance ProgramEffective Compliance Program

•

Establish standards and controls to reduce the likelihood of criminal conduct

•

High level oversight•

Due care in delegating authority

•

Effectively communicate standards and procedures•

Take reasonable steps to achieve compliance

•

Custom design your program to your business•

Punish crime and encourage compliance

•

Consistently enforce standards•

Respond appropriately and timely to offense

69

Avoiding the Inferno: Making Import and Export Issues Predictable in the Year of the Dragon

Avoiding the Inferno: Making Import and Export Issues Predictable in the Year of the Dragon

70

Thank you for attending!