Embed Size (px)

Citation preview

The Definitive Guide for ImprovingInsurance Persistency in India

Customer retention is critical to any insurance business – as important as new policy sales. While new policy sales are often achieved through expensive marketing and business development costs, retaining existing customers offers a more profitable avenue.

The persistency ratio broadly measures customer retention by a life insurance company calculated basis the percentage of policyholders paying renewal premiums at the end of one year, or more years depending on the tenure of the policy.

Persistency ratio has been a concern for life insurers in India. Even reporting of persistency ratio numbers has been debated upon.

1

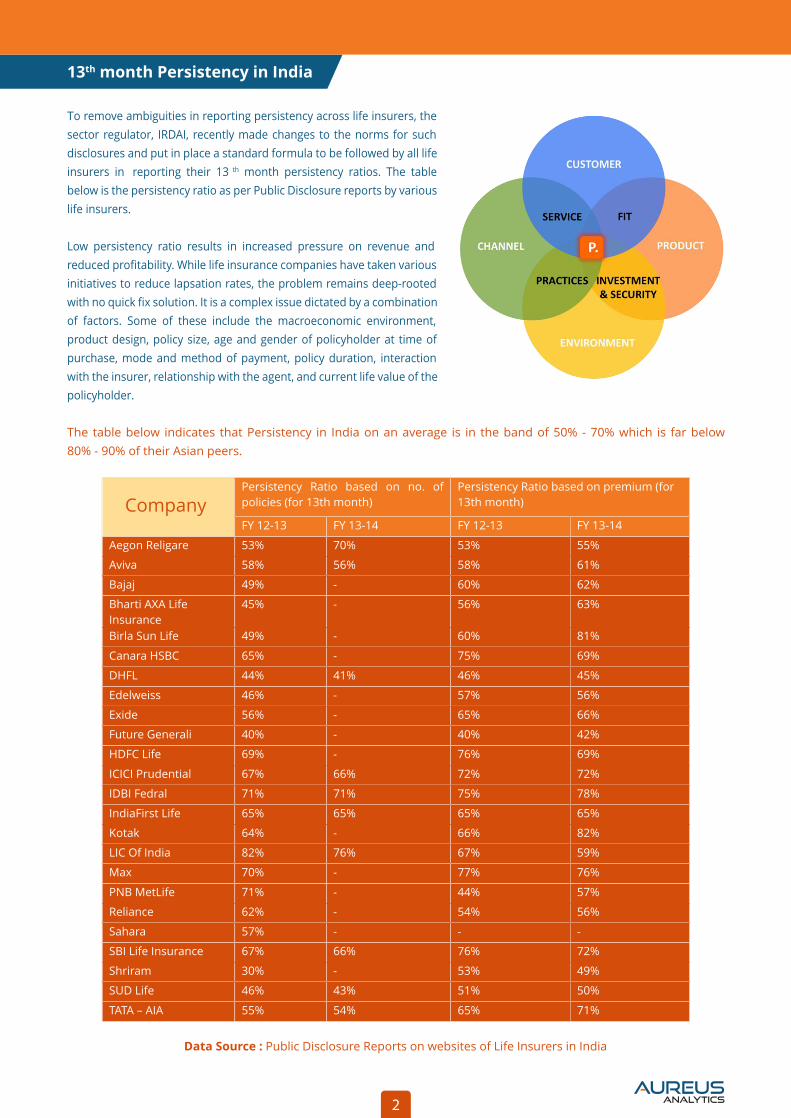

The table below indicates that Persistency in India on an average is in the band of 50% - 70% which is far below

80% - 90% of their Asian peers.

Company Persistency Ratio based on no. of

policies (for 13th month)

Persistency Ratio based on premium (for

13th month)

FY 12-13 FY 13-14 FY 12-13 FY 13-14

Aegon Religare 53% 70% 53% 55%

Aviva 58% 56% 58% 61%

Bajaj 49% - 60% 62%

Bharti AXA Life

Insurance

45% - 56% 63%

Birla Sun Life 49% - 60% 81%

Canara HSBC 65% - 75% 69%

DHFL 44% 41% 46% 45%

Edelweiss 46% - 57% 56%

Exide 56% - 65% 66%

Future Generali 40% - 40% 42%

HDFC Life 69% - 76% 69%

ICICI Prudential 67% 66% 72% 72%

IDBI Fedral 71% 71% 75% 78%

IndiaFirst Life 65% 65% 65% 65%

Kotak 64% - 66% 82%

LIC Of India 82% 76% 67% 59%

Max 70% - 77% 76%

PNB MetLife 71% - 44% 57%

Reliance 62% - 54% 56%

Sahara 57% - - -

SBI Life Insurance 67% 66% 76% 72%

Shriram 30% - 53% 49%

SUD Life 46% 43% 51% 50%

TATA – AIA 55% 54% 65% 71%

Data Source : Public Disclosure Reports on websites of Life Insurers in India

th13 month Persistency in India

To remove ambiguities in reporting persistency across life insurers, the

sector regulator, IRDAI, recently made changes to the norms for such

disclosures and put in place a standard formula to be followed by all life

insurers in reporting their 13 th month persistency ratios. The table

below is the persistency ratio as per Public Disclosure reports by various

life insurers.

Low persistency ratio results in increased pressure on revenue and

reduced profitability. While life insurance companies have taken various

initiatives to reduce lapsation rates, the problem remains deep-rooted

with no quick fix solution. It is a complex issue dictated by a combination

of factors. Some of these include the macroeconomic environment,

product design, policy size, age and gender of policyholder at time of

purchase, mode and method of payment, policy duration, interaction

with the insurer, relationship with the agent, and current life value of the

policyholder.

2

Factors that impact lapsation

There are several factors that lead to policy lapsation. All or some of these could be impacting persistency of a life

insurer at any given point of time.

The major factors that impact persistency of life insurance policies, as per work done by

Aureus Analytics in this area, include:

1. Policy Returns (ROI) promised at time of sale versus actual returns received by policyholder

2. Poor need gap assessment at the time of sale

3. Customer service and complaints management experience

4. Churning of channels

5. New product options

6. Ignorance of policyholder specifically on policy terms and conditions

7. Lack of adequate checks at time of financial underwriting

8. Financial crisis of policyholder or adverse market performance

The role of the sales person in life insurance business has always remained key in emerging markets; and accordingly,

it would not be out of place to look at various aspects of business wherein the distributor can play an important part in

arresting the discontinuance of policy contracts. One gets to hear very often that a policyholder has discontinued

payment of premium in dissatisfaction as he or she was sold the wrong product different from what was explained at

the time of entering into the contract.

Impact of lapsation In addition to the insurer, policy lapse impacts multiple other stakeholders as well:

3

Insurers do provide for policy lapses even while designing the policy. The challenge is to accurately

predict the lapse rate for a particular product and for a particular block of policies. For fixed premium

policies, insurer actuaries have to be accurate as possible. If lapse rates are higher than predicted,

insurer stands the risk of losing his margins.

Reducing policy lapse and increasing persistency benefits the field force a lot. If a customer lapses a

policy, not only does the agent lose his renewal commissions, it also becomes tough to sell another

policy to that customer as the losses on his first policy would have created a negative customer

perception.

Policy lapse affects the customers in three ways:

On lapse, policyholder loses the insurance coverage and more often than not, the insuranceneed is

acute at the times of lapse (one example is where the insured is out of work due to illness and hence

unable to pay premiums).

Customer get a reduced return if any; from the lapsed policy as discount factors tend to get applied

to the paid-up value.

As a class, customers will be affected by higher lapse rates as the cost gets passed on to them by way

of higher premiums (in future product pricing) or lower bonuses

a.

b.

c.

Customer

Insurers

Intermediaries

1

Regularizing the sales

process; digitization

and monitoring of the

sourcing channels by

the insurer. This will

also help in providing

c o n t i n u o u s

knowledge building of

the existing field force

so that the exact

target segment a

product is designed

for and should be

instructed to sell only

to them.

2

Ensuring the customer

has a better

understanding of the

product nature. If the

customer understands a

product well, it will be

that much easier to map

the needs gap. And the

realization by the

customer of his needs

that the product is

meeting, will ensure that

the customer keeps the

policy in force.

3

Alignment of product design

to a typical Indian person’s

life cycle. Time bound

factors which impact policy

renewal premium paying

ability – education expenses,

marriage expenses, and

retirement – should be

addressed via product

design. This would yield in

better prediction of

“in-danger-of-lapse” policies

and result in sharper focus

on renewing them.

4

Perceived Present values

of insurance contracts

are not controllable after

issue. Rather product

feature design has to

take care of embedding

features which get high

returns. The popularity

of unit linked products is

a pointer to this. Better

positioning of the

product can mitigate the

effect of return rates on

lapse rates.

Suggestions to counter Policy Lapsation

The Indian Life Insurance market can therefore be said to operate in a very ordinary persistency range as an industry. To

leapfrog from this level of persistency to that of other Asian markets such as Singapore, which has a 99% persistency,

the following key areas need to be addressed:

AUPERA from Aureus

The need to address each of the above aspects are to a great extent appreciated by Life Insurers. However the key

disconnect occurs in using the underlying information effectively and in real time. Data analytics, specifically that which

incorporates both structured and unstructured data and combine customer and distribution level interaction has the

potential to impact persistency. AUPERA from Aureus is an advanced persistency control and management framework

which leverage complex algorithms to arrest lapsation significantly by addressing underlying customer and product

issues. Based on policy risk scoring, AUPERA helps insurers reach out to ‘ about to lapse’ customers beforehand and

initiate retention campaigns.

For a demo of AUPERA, contact us now.

![[Our Redemption] Doctrines of Grace: Definitive Atonement](https://img.pdfslide.net/doc/110x75/61934b65b86f4e773a2b24f5/our-redemption-doctrines-of-grace-denitive-atonement.jpg)