Embed Size (px)

Citation preview

Journal of International Money and Finance21 (2002) 295–350

www.elsevier.com/locate/econbase

The dynamics of emerging market equity flows

G. Bekaerta,d, C.R. Harveyb,d,∗, R.L. Lumsdainec,d

a Columbia University, New York, 10027 USAb Duke University, Durham, NC 27708, USA

c Deutsche Bank, London, EC2N 2DB UKd National Bureau of Economic Research, Cambridge, MA 02138, USA

Abstract

We study the interrelationship between capital flows, returns, dividend yields and worldinterest rates in 20 emerging markets. We estimate a vector autoregression with these variablesto measure the degree to which lower interest rates contribute to increased capital flows andshocks in flows affect the cost of capital among other dynamic relations. We precede the VARanalysis by a detailed examination of endogenous break points in capital flows and the othervariables. These structural breaks are traced to the liberalization of emerging equity markets.Our evidence of structural breaks calls into question past research which estimates VAR mod-els over the full sample. After a liberalization, we find that equity flows increase by 1.4% ofmarket capitalization. We also show that shocks in equity flows initially increase returns whichis consistent with a price pressure hypothesis. While the effect is diminished over time, therealso appears to be a permanent impact. This is consistent with our finding that our proxy forthe cost of capital, the dividend yield, decreases. Finally, our analysis of the transition dyna-mics from pre-liberalization to post-liberalization suggests that when capital leaves, it leavesfaster than it came in. These results may help us understand the dynamics of the recent crisesin Latin America and East Asia. 2002 Published by Elsevier Science Ltd.

JEL classification: F3; F4; G1; E4

∗ Corresponding author. Tel.:+1-919-660-7768; fax:+1-919-660-8030.E-mail address: [email protected] (C.R. Harvey).

0261-5606/02/$ - see front matter 2002 Published by Elsevier Science Ltd.PII: S0261 -5606(02 )00001-3

Journal of International Money and FinancePublished in:

COLUMBIA BUSINESS SCHOOL 1

296 G. Bekaert et al. / Journal of International Money and Finance 21 (2002) 295–350

1. Introduction

With a number of recent crises in emerging markets, the role of foreign capitalin developing countries is under intense scrutiny once again. One country, Malaysia,imposed capital controls on October 1, 1998, in an effort to thwart the perceiveddestabilizing actions of foreign speculators. After a decade of capital market liberaliz-ations and increased portfolio flows into developing countries, this process may nowbe stalled or even reversed. The goal of this paper is to explore the dynamics, causesand consequences of capital flows in 20 emerging markets over the last 20 years.Importantly, we explicitly investigate the role of the recent financial liberalizationprocess in these dynamics.

Our work is related to two literatures. First, there is a growing body of researchthat studies the joint dynamics of capital flows and equity returns [see for example,Warther, 1995; Choe et al., 1999, Froot et al., 2001; Clark and Berko, 1997; Edelenand Warner, 1999; Stulz, 1999]. The first hypothesis of interest is whether foreigninvestors are “return chasers”, in the terms of Bohn and Tesar (1996), that is, areflows caused by changes in expected returns? A related hypothesis is that inter-national investors are momentum investors, leading to a positive relation betweenpast returns and flows. The second set of hypotheses focuses on the effect of flowson returns. Both Froot et al. (focusing on 28 emerging markets) and Clark and Berko(focusing on Mexico) find that increases in capital flows raise stock market prices,but the studies disagree on whether the effect is temporary or permanent. If theincrease in prices is temporary, it may be just a reflection of “price pressure”, whichhas also been documented for mutual fund flows and stock indices [Warther, 1995;Shleifer, 1986]. If the price increase is permanent, it may reflect a long-lastingdecrease in the cost of equity capital associated with the risk sharing benefits ofcapital market openings in emerging markets.

Our work is also related to a second literature on capital market liberalizationsand the integration process in emerging markets [see Bartolini and Drazen, 1997;Bekaert and Harvey, 1995, 2000a,b; Henry, 2000a,b; Kim and Singal, 2000]. Duringthe sample period, many emerging markets removed capital controls, which oftenwent hand in hand with other reforms in the domestic financial system, trade lib-eralization, macro-economic stabilization programs (especially in Latin-America)and large scale privatizations [see Bekaert and Harvey, 2000b for detailed time lineson important structural changes in emerging countries]. These structural changescomplicate any empirical analysis of emerging markets during this period, since theycould cause permanent or at least long-lasting changes in the data-generating pro-cesses. In Bekaert et al. (2002), we use the structural break methodology of Bai,Lumsdaine, and Stock (hereafter BLS) (1998) to “date” when market integrationoccurred and document structural changes in a number of financial and economictime-series.1

1 Kawakatsu and Morey (1999) also use endogenous break point techniques to date stock marketopenings and examine stock market efficiency before and after the opening.

COLUMBIA BUSINESS SCHOOL 2

297G. Bekaert et al. / Journal of International Money and Finance 21 (2002) 295–350

The main tool of analysis in this paper is a vector-autoregressive (VAR) frame-work as in Froot et al. (2001), but with a number of differences. First, we add twovariables to the bivariate set-up of returns and equity flows in Froot et al.: the worldinterest rate and local dividend yields. The low level of US interest rates has oftenbeen cited as one of the major reasons for increased capital flows to emerging mar-kets in 1993 [see World Bank, 1997; as well as Calvo et al. (1993, 1994) and Fernan-dez-Arias, 1996] and our framework will allow us to trace out the effects of anunexpected reduction in world interest rates on capital flows to emerging markets.We are ultimately interested in the effects of structural reforms in emerging marketson local returns and particularly, on the local cost of capital. The inclusion of theworld interest rate helps in that endeavor in that it removes the effect of exogenousglobal determinants of capital flows. We add dividend yields to the VAR as our costof capital measure, since they capture potential permanent price effects induced byincreased foreign capital after liberalizations better than average returns [see Bekaertand Harvey, 2000a] and they also serve as an indicator of expected returns allowingdifferentiation of the ‘return chasing’ and ‘momentum investing’ hypotheses.

Second, we precede our VAR analysis with a detailed endogenous break pointanalysis of our three main time series (net equity flows as a proportion of localmarket capitalization, log returns and the log dividend yield) using the novel tech-niques in BLS (1998) and Bai and Perron (1998a,b). This analysis helps pin downa relevant time-period over which to conduct the VAR analysis but is also interestingin its own right. For example, we study the transition dynamics of some of ourvariables around the break points. Such analysis is particularly important given thatrecent events in South-East Asia indicate that the integration process may now behalted and reversed. Studying capital flow dynamics and their impact on the localmarket may therefore yield predictions for the likely effects of the recent re-impo-sition of capital controls in some countries. Also, if capital market liberalizationsinduce one-time portfolio rebalancing on the part of global investors, one may expectnet flows to increase substantially after a liberalization and then to decrease again[see Bachetta and van Wincoop (2000) for a formal model generating such dynam-ics]. The Bai-Perron statistics look for multiple breaks in a time series and mayuncover such dynamics. We also test this prediction directly.

Third, although equity flows are our main focus, we also investigate how theyrelate to bond flows. For example, increased equity flows may substitute fordecreased bond flows or both may increase simultaneously as a result of a generalfinancial liberalization package.

We find that equity capital flows increase after liberalization but level out threeyears after their liberalization. This provides evidence that foreign investors rebalancetheir portfolios towards the newly available emerging market assets. Our analysis ofthe transition dynamics suggests that the movement of equity capital is much fasterwhen it leaves than when it enters. In general, we find sharply different results ifour models are estimated over the entire sample—which ignores a fundamental non-stationarity in the data—versus a post-break (liberalization) sample. One of our mainfindings is that unexpected equity flows are indeed associated with strong short-livedincreases in returns. However, we also find that they lead to permanent reductions

COLUMBIA BUSINESS SCHOOL 3

298 G. Bekaert et al. / Journal of International Money and Finance 21 (2002) 295–350

in dividend yields. As we explain later, the dividend yield change may reflect achange in the cost of capital. Hence, the reduction in the dividend yield suggeststhat additional flows reduce the cost of capital and that the actual return effect isnot a pure price pressure effect.

The paper is organized as follows. The second section presents the vector autore-gressive empirical model that we use to interpret the relation between expectedreturns, dividend yields and capital flows. The third section explores the methodsthat we use to establish structural breaks in the time-series of interest. The fourthsection describes the data. The results are presented in the fifth and sixth sections.The final section offers some concluding remarks.

2. The econometric framework

2.1. Variables and main hypotheses

Since there is currently no well-accepted model of transition dynamics around aliberalization, we conduct our empirical analysis in the context of vector autore-gressions (VARs). For part of our analysis, these VARs are reduced-form represen-tations of an unspecified structural model, but some of the empirical hypotheses wewant to test require a structural interpretation of the VARs. In our primary empiricalsystem, we generalize the set-up of Froot et al. (2001), who run a bivariate VARon the ratio of net capital flows to market capitalization and market returns. Theirmain identifying structural restriction is that the shock to flows may affect returnsbut not vice versa. In addition, past returns only affect current returns through theireffects on flows. Two interesting questions can be investigated in this framework:

1. What is the effect of an unexpected shock to capital flows on current returns andwhat are its dynamics (that is, does it die out or is it permanent)? The dynamiceffects of the shock serve to distinguish the price pressure hypothesis from thepermanent change in the cost of capital hypothesis.

2. Do past returns affect current capital flows? In particular, Bohn and Tesar (1996)argue that capital flows are motivated by capital “chasing” high expected returns,rather than portfolio rebalancing motives. One issue here is that high past returnsneed not signal high future returns, unless momentum is an important determinantof expected return (see Bohn and Tesar (1997). In our framework, we will beable to distinguish the expected return-updating hypothesis from the momentumhypothesis.

In contrast to previous work, our primary VAR will contain four variables. LetYt � [it,nft,dyt,rt]�, whereit is the world interest rate,nft is the net equity capital flowdivided by market capitalization,dyt is the log-dividend yield andrt is the loggedequity return.

The presence of the world interest rate allows a more subtle testing of the hypoth-eses in (1). It has often been argued that the emerging markets received a lot of US

COLUMBIA BUSINESS SCHOOL 4

299G. Bekaert et al. / Journal of International Money and Finance 21 (2002) 295–350

capital in 1993 because investors were chasing higher yielding assets with interestrates in the US reaching historical lows. It should be mentioned that there may begood reasons for an inverse link between US interest rates and capital flows to emerg-ing markets. For example, the low US interest rates may have increased the Amer-icans’ wealth and therefore increased their risk tolerance, leading them to rebalancetowards riskier emerging market securities. Whatever the reason, our framework willallow a direct test of the magnitude and dynamics of a decrease in the world interestrate on capital flows to emerging markets.

With the world interest rate in the system, we can now divide the effect of highercapital flows on returns into two components. Capital flow increases induced bylower world interest rates may, for example, be less likely to lead to permanent priceincreases than capital flow increases that are not caused by world factors, but alsomay reflect portfolio rebalancing after a capital market liberalization.

The addition of the log-dividend yield is motivated by the work of Bekaert andHarvey (2000a). They argue that the extreme volatility in emerging market returnsimplies that changes in the cost of capital can be better assessed by investigatingchanges in dividend yields. In any rational pricing model, dividend yields will bedecreasing in the growth rate of dividends (cash flows) and increasing in the discountrate. Because of their low variability, dividend yields will capture permanent priceeffects induced by cost of capital changes more accurately than average returns.Bekaert and Harvey document that liberalizations tend to lead to small drops individend yields. One problem is that a lower dividend yield may also reflect animprovement in growth opportunities. Nevertheless, our set-up will allow us to testthe effect of a change in the world interest rate, and/or capital flows on the dividendyield in emerging markets and contrast that with the effect on returns. In addition,given that the dividend yield is a good proxy for expected returns, which is alsoborne out in the predictability tests for emerging markets by Harvey (1995), itsinclusion allows for a proper test of the Bohn-Tesar hypotheses mentioned above.

To perform tests of the main hypotheses, we use impulse response analysis basedon a structural interpretation of the VAR. Consider, without loss of generality, afirst-order VAR, suppressing the constant:

Yt � AYt�1 � et, (1)

with all eigenvalues ofA having moduli less than one so that the VAR is stationary.We compute impulse responses,IR(i,j,k) � ∂e�iYt�k /∂e∗t,j, wheree∗t,j are the “struc-

tural” shocks andei is an indicator variable selecting theith variable, e.g.e1 =[1,0,0,0]. We look at one standard deviation shocks. The structural shocks,e∗

t,j, aredetermined by the ordering in the VAR, that is,et � P�e∗t , whereP is an upper-triangular matrix ande∗t are uncorrelated structural shocks, such that� �E[et e�t] � P�P.

The ordering of the variables is as defined above, with the world interest ratecoming first. Hence, the world interest residual is implicitly assumed not to be affec-ted by the other shocks in the system. As in Froot et al. (2001), we order flowsbefore returns, but we insert the dividend yield in the middle. Dividend yields andreturns are contemporaneously negatively correlated, but a shock to the dividend

COLUMBIA BUSINESS SCHOOL 5

300 G. Bekaert et al. / Journal of International Money and Finance 21 (2002) 295–350

yield may reflect a near-permanent price change due to the liberalization process ora change in expected returns, and it is therefore natural to order dividend yieldsbefore returns. We are interested in:

1. the effects of the world interest rate, it, on the ratio of net capital flows to marketcapitalization, returns and dividend yields,

2. the impact of flows on returns and dividend yields to test the price pressure versuspermanent impact hypotheses, and

3. the effect of past returns and dividend yields on flows to test ‘return chasing’ and‘momentum investing’.

For this last response, our setup removes the contemporaneous correlation betweenreturns or dividend yields and flows, ascribed potentially to price pressure effects,because flows are ordered before these two variables. For example, a shock to thedividend yield not contemporaneously correlated with capital flows may reflect achange in growth opportunities or a change in expected returns which may affectfuture foreign capital inflows.

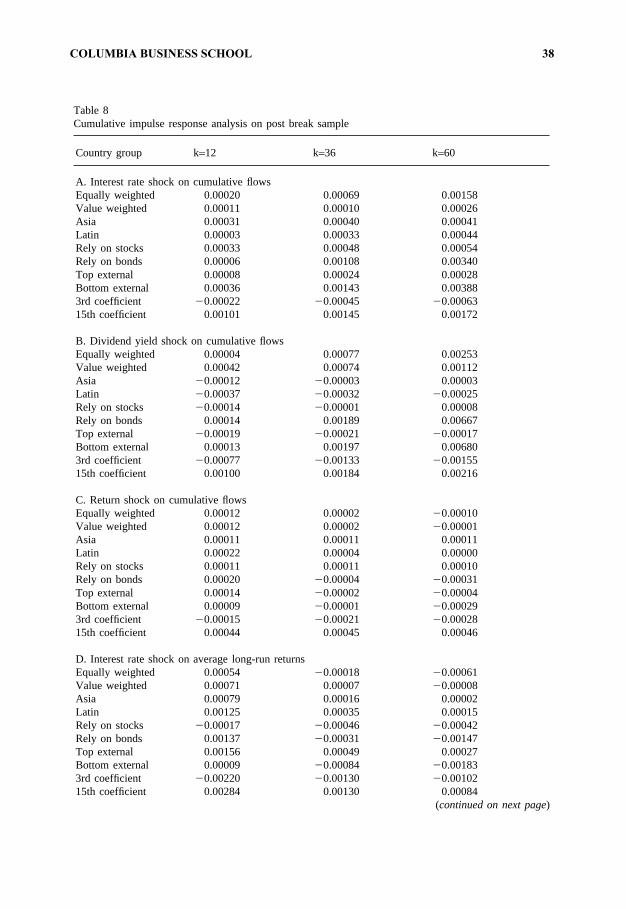

We also report impulse responses of shocks to the world interest rate, currentcapital flows, returns, and dividend yields on two cumulative variables: the averagelong-run return and the change in US holdings.

First, we definert�k,k � 1k�k�1

i � 0 rt�1�i as the per period cumulative long-horizon

return. Next, consider the definition of net capital flows to capitalization:

nft �ft

mcapt

,

where ft is the net capital flow andmcapt is the equity market capitalization. Thecumulative capital flow to market capitalization is:

cft,t+k � �k

i � 1

nf t+i

�ft+1

mcapt+1

� % �ft+k

mcapt+k

�1

mcapt+k�ft+1 ×

mcapt+k

mcapt+1

� % � ft+k�.

So,cft,t+k accumulates the flows occurring betweent andt+k and allows each flowto change value as a result of the market return.

Now consider the definition of the cumulative holdings in the local market:

COLUMBIA BUSINESS SCHOOL 6

301G. Bekaert et al. / Journal of International Money and Finance 21 (2002) 295–350

ht � ��t

i�0

fimcapt

mcapi� 1

mcapt

� �t

i�0

fimcapi

� �t

i�0

nfi.

So holdings accumulate the flows from the beginning of time (notice the counterbegins ati = 0) allowing for the market return and express them as a proportion ofcurrent market capitalization. From this analysis, it is immediate that

cft,t+k � ht+k�ht,

is the change in holdings. Whereas impulse responses on the VAR variables die outin any stationary VAR, these cumulative effects represent the permanent effect onreturns and capital flows when we letk go to infinity.

2.2. VAR dynamics

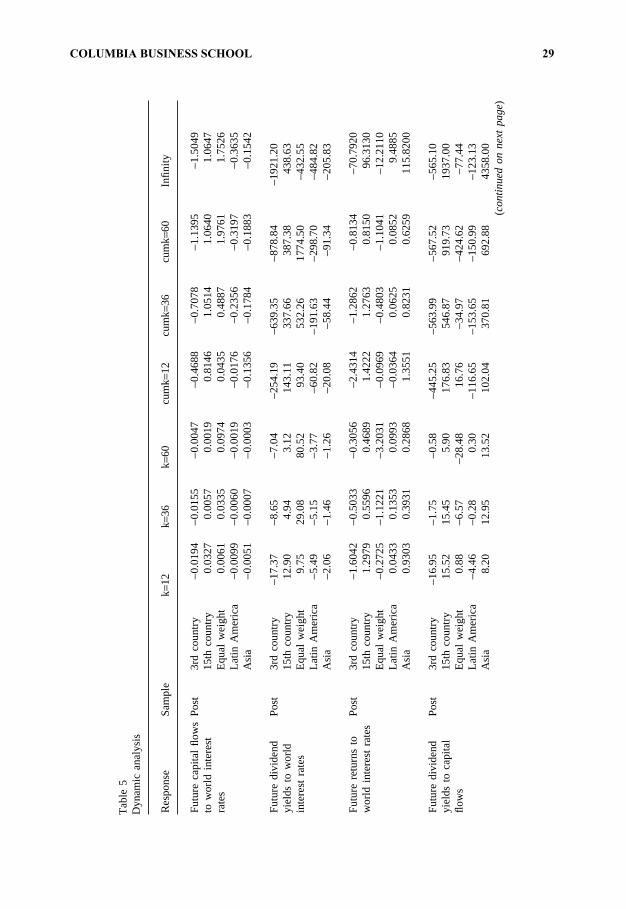

Before we test the main hypotheses, we document the information in the VARsregarding the dynamic relations between our four variables using two different stat-istics.

First, we investigate dynamic regression coefficients between the various variables,for example, what is the correlation between world interest rates today and capitalflows or returns in the future? Formally, we investigate:

bi,j,k �Cov [e�iYt+k, e�jYt]

Var[e�jYt], (2)

whereei are indicator vectors, e.g.e1 = [1,0,0,0].Given that the VAR is stationary, Var[Yt] = C(0) can be computed as

Vec[C(0)] � [I�A�A]�1vec(�), (3)

where � � E[et e�t] and I is the identity matrix. The VAR fully summarizes theshort-run and long-run dynamics ofYt ; e.g.

E[YtYt�k] � C(k) � AkC(0). (4)

With this information, projection coefficients at all horizons can be computed.With the long-run variables introduced above, changes in holdings and long-run

returns, we can investigate the relation between these variables on the one hand andworld interest rates and capital flows on the other hand. For example, we compute:

COLUMBIA BUSINESS SCHOOL 7

302 G. Bekaert et al. / Journal of International Money and Finance 21 (2002) 295–350

gk �Cov [rt+k,k, nft]

Var[nft]

�

1ke�4[I � A � % � Ak�1]C(0)e�2

e�2C(0)e2,

(5)

wheree2 (e4) are indicator variables selecting flows (returns). Also, [I+A+%+Ak�1]= [I�Ak][I�A]�1. We can also letk go to infinity here. Analogously, we can investi-gate the long-run beta of changes in holdings with respect to current interest rates,returns and dividend yields.

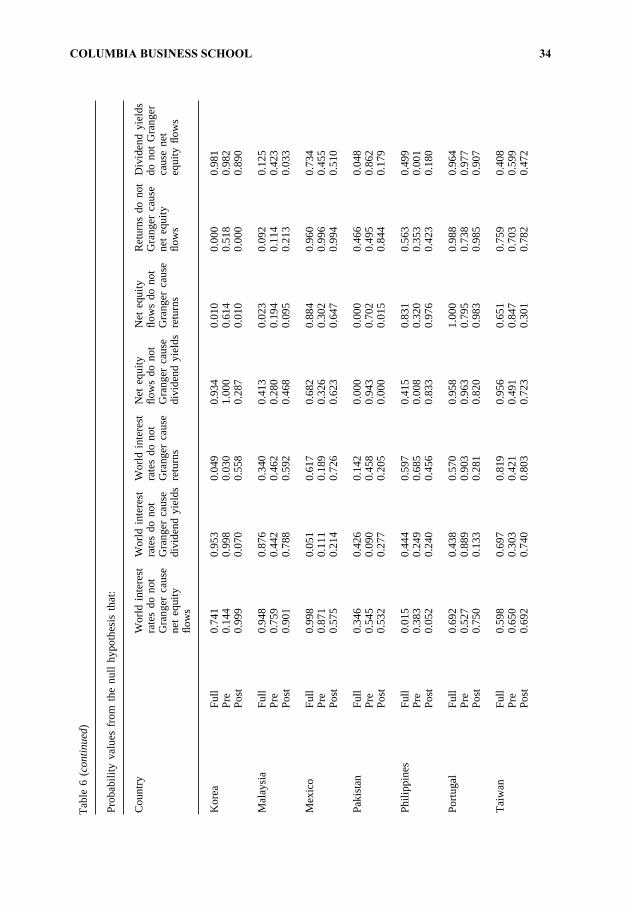

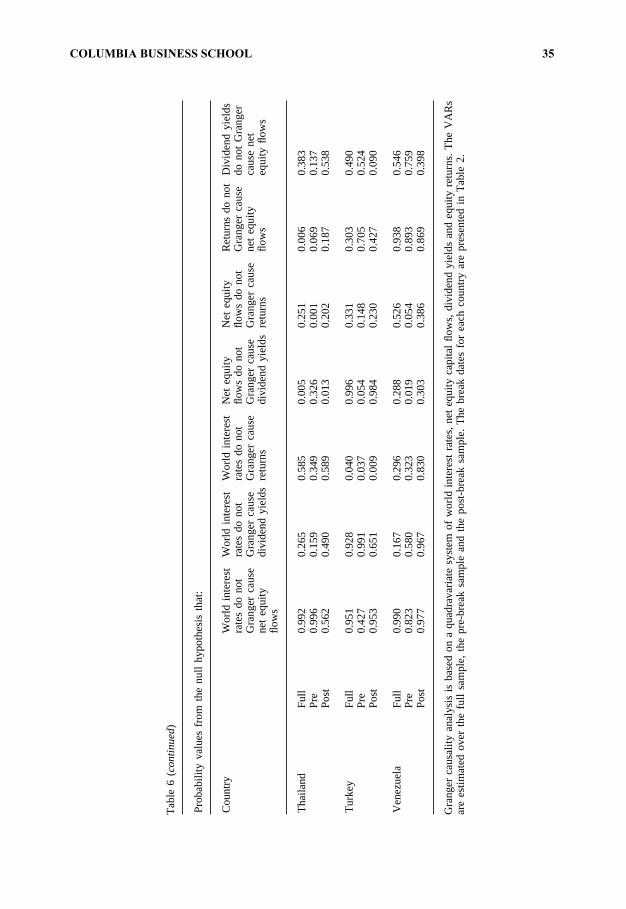

Second, whereas the regression coefficients provide useful summary information,they are univariate relations that may hide intricate dynamic patterns. For example,there may be a positive relation between current capital flows and future returns, butpart of this correlation may come indirectly through the effect of world interest rateson capital flows. It would be interesting to see whether there is still a relation betweencapital flows and future returns, controlling for the world interest rate effect. Simi-larly, are capital flows mostly predictable by external variables like world interestrates, or by internal variables (returns and dividend yields) that may proxy forexpected returns for example? This question has been addressed before [see Calvoet al., 1993, 1994; and Fernandez-Arias, 1996], but in the context of our VAR it isparticularly simple to implement. We conduct a series of Granger-causality tests,testing whether world interest rates Granger-cause the other variables, and whetherreturns and dividend yields Granger-cause capital flows or vice versa. If liberalizationis a gradual process and is pre-announced, dividend yields may decrease and returnstemporarily increase before flows pick up. In this case, returns and dividend yieldsmay Granger-cause flows. Hence, it may be hard to distinguish this effect frommomentum investing (positive feedback trading), since this would also imply thatpositive returns predict higher flows.

2.3. The dynamics of capital flows and breaks

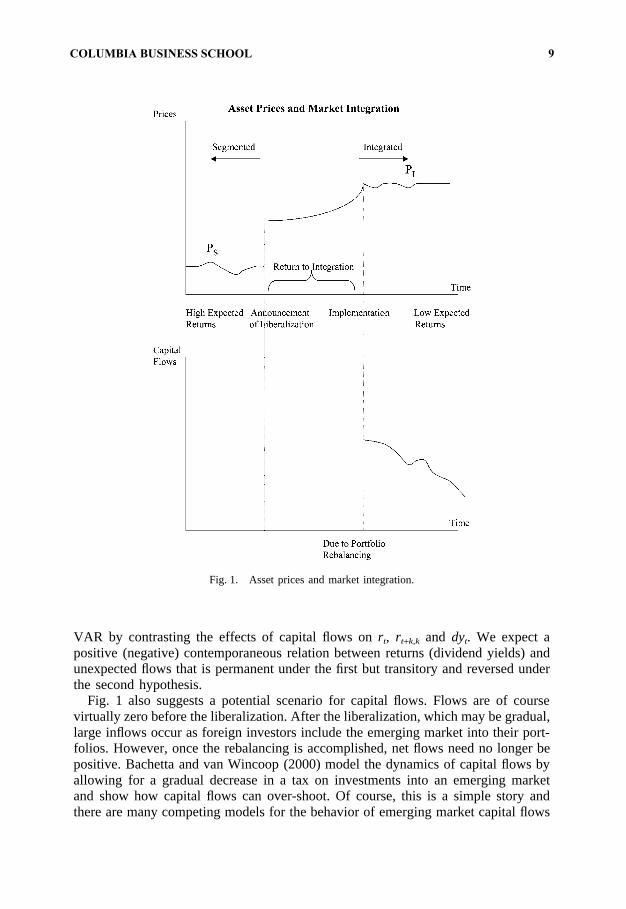

It does not make much sense to conduct this analysis over the full sample of data,given that many of the markets that we study may have undergone an integrationprocess somewhere in the middle of the sample. If the market truly went from seg-mented to integrated, the dynamics of all the variables in our VAR except the worldinterest rate would be affected. Consider Fig. 1 which sketches what a standardmodel of risk sharing [see the description in Bekaert et al., 2002] would predict,namely “a permanent change in prices leading to a new regime of lower expectedreturns”. Interestingly, this process is associated with short-term increases in returns(the return to integration) and long-run decreases in expected returns, plus a perma-nent decrease in dividend yields. This pattern would more generally result from“investor base broadening”, the spreading of risks among more investors (see Stulz,1999, for a summary of the scarce evidence to date on this). If flows drive pricestemporarily away from fundamentals, the price effect ought to be temporary (“theprice pressure hypothesis”). This behavior can be examined in the context of our

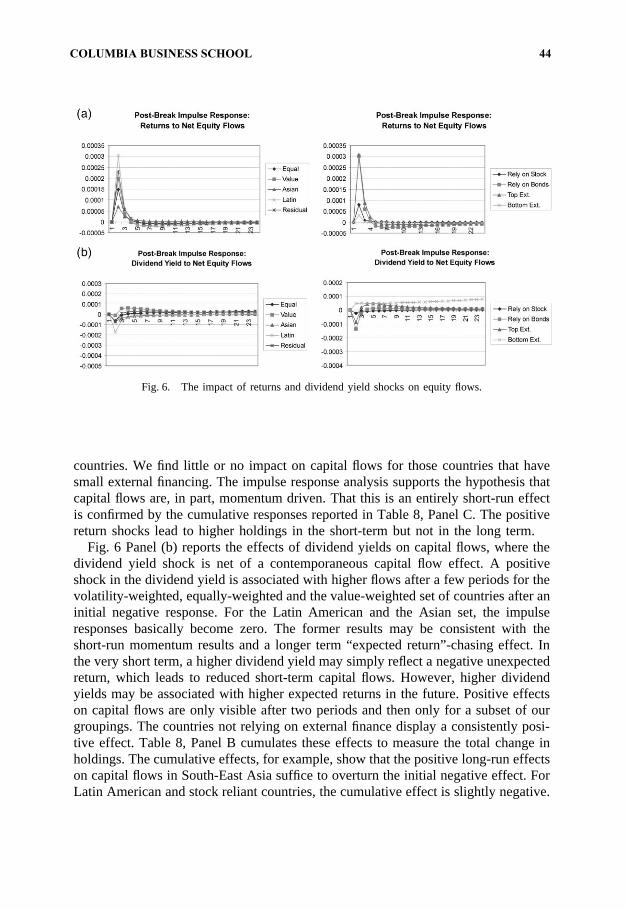

COLUMBIA BUSINESS SCHOOL 8

303G. Bekaert et al. / Journal of International Money and Finance 21 (2002) 295–350

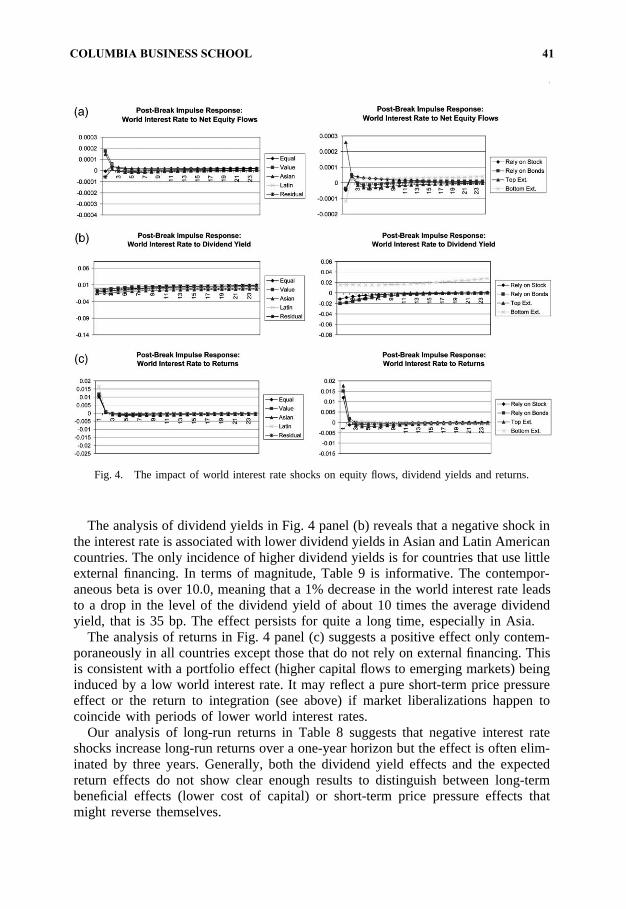

Fig. 1. Asset prices and market integration.

VAR by contrasting the effects of capital flows onrt, rt+k,k and dyt. We expect apositive (negative) contemporaneous relation between returns (dividend yields) andunexpected flows that is permanent under the first but transitory and reversed underthe second hypothesis.

Fig. 1 also suggests a potential scenario for capital flows. Flows are of coursevirtually zero before the liberalization. After the liberalization, which may be gradual,large inflows occur as foreign investors include the emerging market into their port-folios. However, once the rebalancing is accomplished, net flows need no longer bepositive. Bachetta and van Wincoop (2000) model the dynamics of capital flows byallowing for a gradual decrease in a tax on investments into an emerging marketand show how capital flows can over-shoot. Of course, this is a simple story andthere are many competing models for the behavior of emerging market capital flows

COLUMBIA BUSINESS SCHOOL 9

304 G. Bekaert et al. / Journal of International Money and Finance 21 (2002) 295–350

including models that predict a foreign lending boom followed by the inevitablecrash! [see, for example, Calvo and Mendoza, 1998.]

To deal with this problem, we apply the most recent methodology on break dateinference. We first apply the methodology developed in BLS to all of our univariateseries, and also use it to determine a break date for the joint system. This breakpoint analysis then determines the post-break period to which we will apply ourVAR analysis described above. The break point analysis also reveals a period oftransitions and the transition dynamics are of interest in their own right.

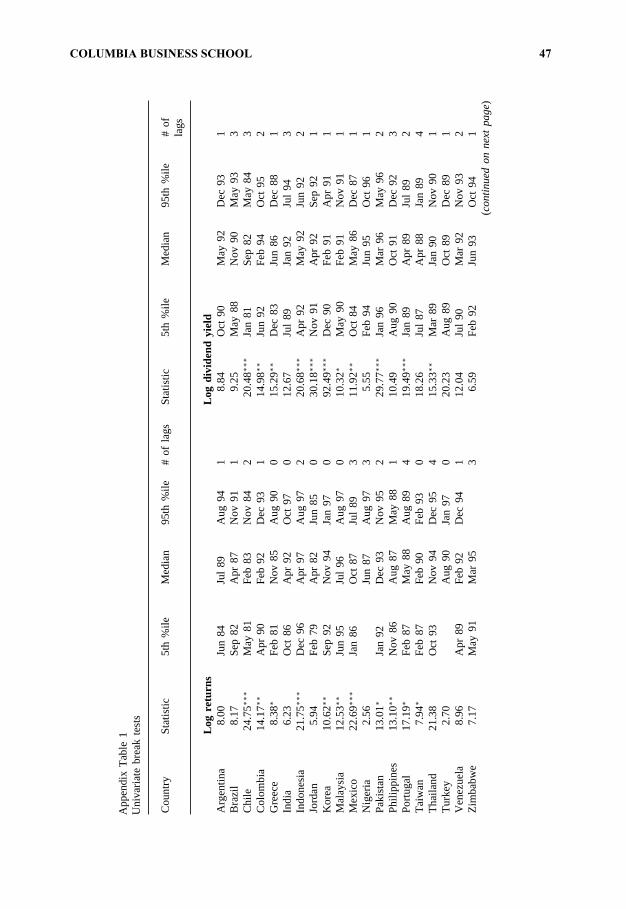

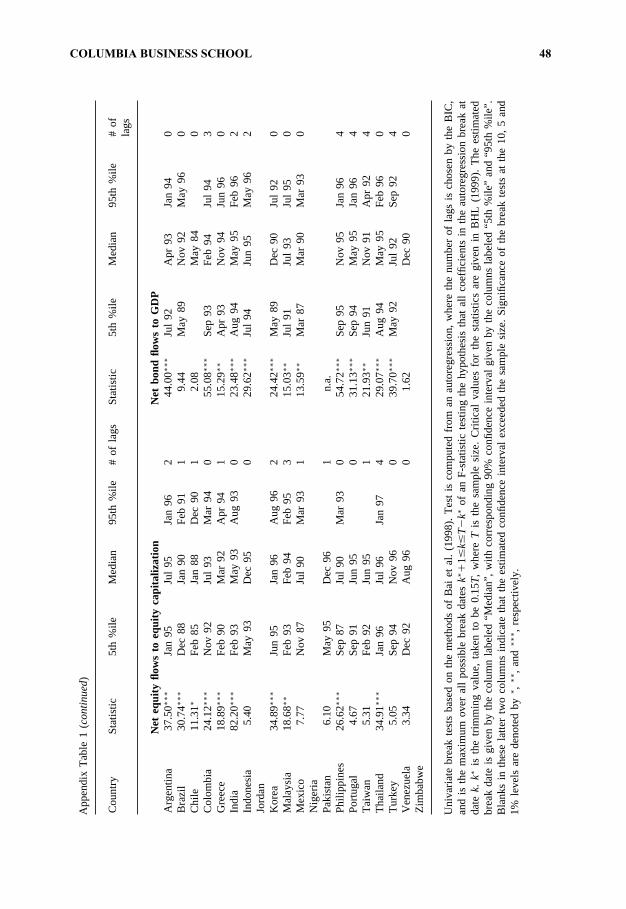

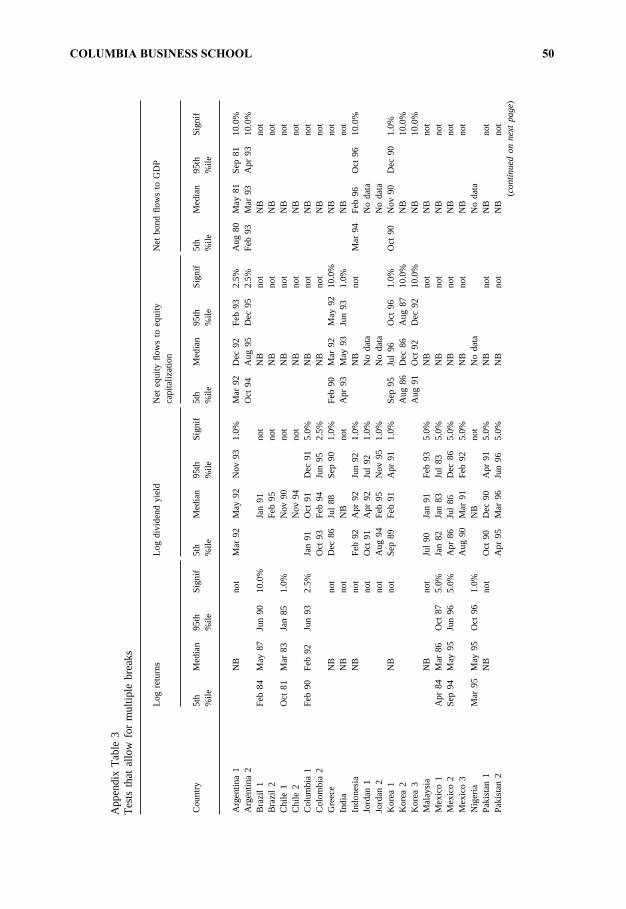

A disadvantage of the BLS methodology is that it only allows for one break. Thereare a number of reasons why there may be more than one break especially in thenet flows series. As indicated above, flows may be temporarily high to effect aportfolio rebalancing after capital market integration. There may be a second breakat the end of this process. Recently, we have seen a reversal of capital flows witha number of well-publicized crises in Mexico 1994–1995, and in South-East Asiain 1997–98. Even much before this, the debt crisis may have caused some LatinAmerican markets to become effectively segmented from the rest of the world,although capital flows before then were small. Therefore we also apply the techniquesof Bai and Perron (1998a,b) which allow for multiple breaks, but only apply tounivariate series. Additional details are presented in the econometrics section.

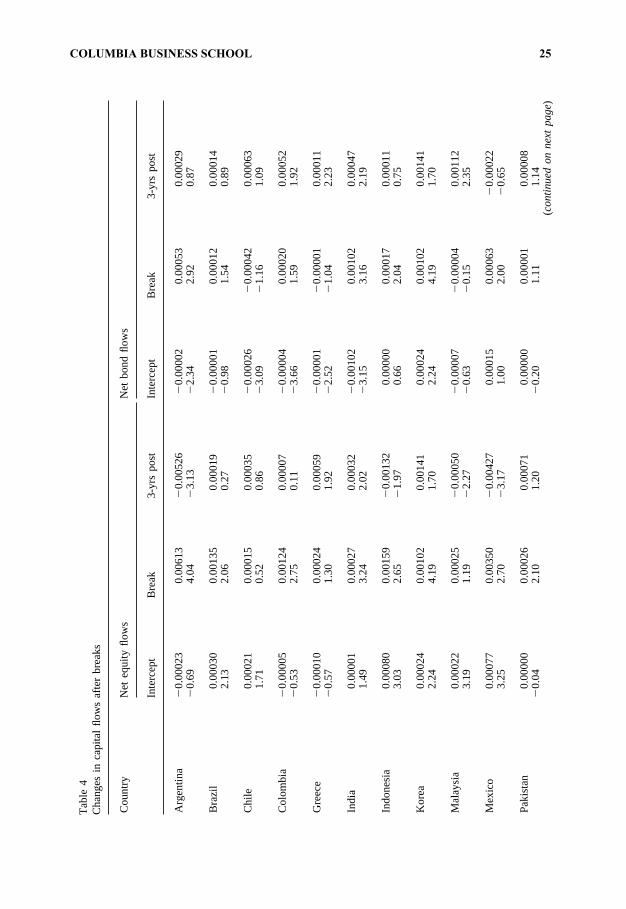

We also investigate the dynamics of capital flows around a potential liberalizationbreak using a very simple regression procedure. If the capital flow story of Fig. 1is accurate, mean equity flows should be higher after the break than before, butdecrease again after portfolio re-balancing is completed. In other words, letD1t bea dummy that comes on after the break andD2t the dummy that comes on threeyears after the break, then in the regression

nft � a � bD1t � cD2t � et, (6)

we would findb to be positive, andc to be negative. We choose three years becauseof the time it takes from announcement to effective implementation of a marketliberalization. Bekaert and Harvey (2000a) provide evidence that liberalizations areoften gradual.

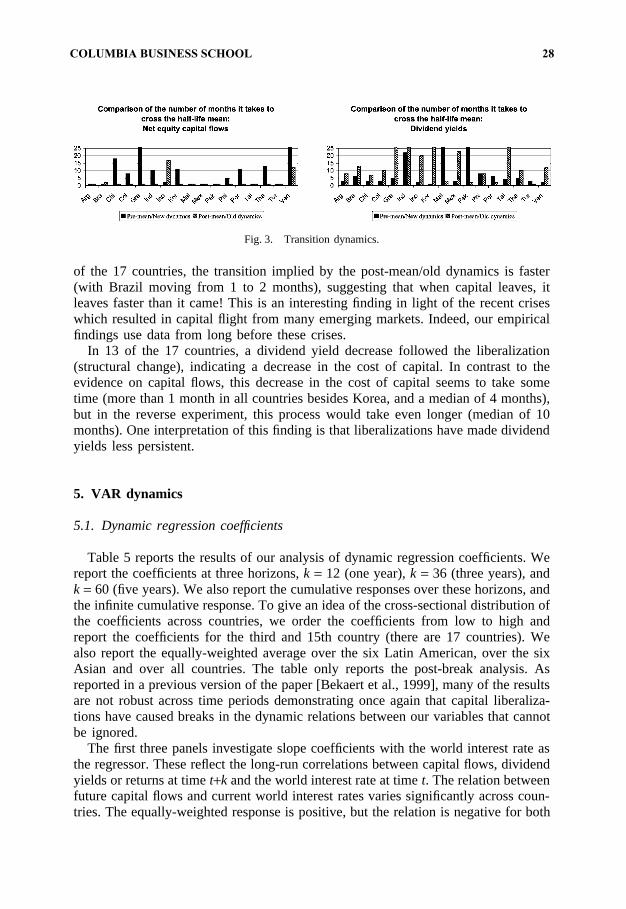

Finally, to examine the transition dynamics, we compute a statistic we call the“transition half-life statistic” (THL). The THL statistic is measured as follows. Con-sider the point in time at which the break occurs and imagine the current realizationof the variable is at the unconditional meanbefore the break. Now consider fore-castingk periods in the future using the new dynamics. If the VAR is stationary,eventually the forecasts will reach the new unconditional mean. How fast they willget there depends on the persistence of the system and how far away the post-breakmean is from the starting point (pre-break mean). Our THL statistic records the timeit takes (in months) to reach half the distance between old and new mean. We canalso reverse the computation. That is, we compute the THL statistic starting fromthe new mean going to the old mean using the pre-break dynamics. Comparing thetwo statistics is informative about the different dynamics before and after the break.We will compute this statistic for capital flows and dividend yields. For capital flows,a bold interpretation of the pre-break THL statistic is that it reveals something about

COLUMBIA BUSINESS SCHOOL 10

305G. Bekaert et al. / Journal of International Money and Finance 21 (2002) 295–350

how capital flows will react when the integration process is reversed, as is recentlyhappening in a few countries. We do not compute the THL statistic for returns,because we conjecture that the measurement of mean returns is too noisy to makethe computation valuable.

3. Data

Our data consists of capital flows, interest rates, dividend yields, and returns. Oursource of monthly data on capital flows is the US Treasury International Capital(TIC) reporting system.2 For the 20 emerging markets we study, we are able tocalculate the net US flows for stocks and bonds for 17 countries. The Treasury doesnot track data on Jordan, Nigeria, and Zimbabwe. We use the International FinanceCorporation’s Emerging Markets Database as a source of the US dollar returns andthe dividend yields. The world interest rate is constructed as a GDP weighted averageof the short-term government Treasury bills in the G-7 countries.3 The interest rateand GDP data are from Datastream.

With so many countries and relatively small sample periods, a country by countryanalysis may both lack power and prevent us from presenting the results in an intelli-gible way. Therefore we present most of our results using country groupings. Weuse three different types of groupings. The first set is aimed primarily at noisereduction. We aggregate results over all countries with three weighting schemes:equally weighted, value weighted (using the market capitalization of the equity mar-ket from the IFC) and volatility weighted. The volatility weighting constructs weightsusing the inverse of the sum of squared residuals of all the regressions in the VARfor a particular country relative to the inverse sum of the squared residuals overall countries. Hence, the “noisiest” VARs are down-weighted. Before applying thisprocedure, we re-scaled the residuals, so that at a global, all-country level, capitalflows accounted for 40% of the total variance, returns and dividend yields each 25%,and interest rates, 10%. If the coefficients (like impulse responses) are independentacross countries, this aggregation would lead to a reduction of the typical country-specific standard error by a factor of over four, since there are 17 countries in oursample. Hence, even if the country-specific standard errors are double the size ofthe coefficients, we would obtain significance.

The second grouping is geographical. We contrast the results for six Latin Amer-ican countries (Argentina, Brazil, Chile, Colombia, Mexico and Venezuela) and sixAsian countries (Indonesia, Korea, Malaysia, the Philippines, Taiwan and Thailand).Although these results may be sensitive to country-specific outliers, the contrastsbetween the development models of Latin-America and South-East Asia and therecent crises in both areas make this grouping meaningful.

2 See Tesar and Werner (1994, 1995) for a description and analysis of these data.3 See the data appendix for additional details on the construction of the dividend yields and the world

interest rate.

COLUMBIA BUSINESS SCHOOL 11

306 G. Bekaert et al. / Journal of International Money and Finance 21 (2002) 295–350

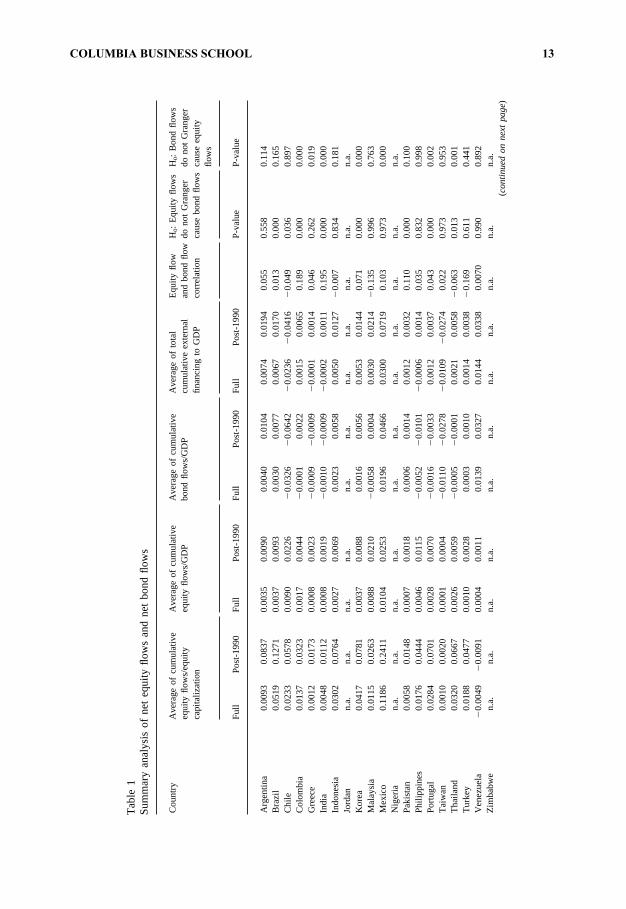

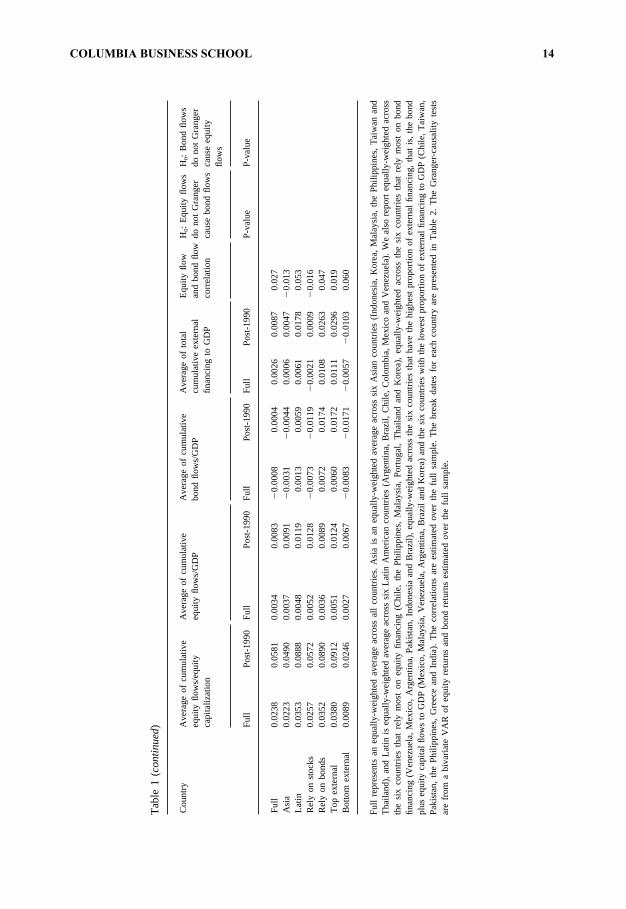

Our last groupings focus on the characteristics of capital flows. Table 1 summar-izes some of the characteristics we use in the selection process. First, we investigatethe magnitude of equity and bond flows. We calculate the return-adjusted cumulativeequity flows divided by market capitalization. This is a measure of US ownershipin the country. We present average ownership over the full sample as well as the1990s. The largest average ownership is found for Mexico (since 1990) followed byBrazil and Argentina. The country with the largest average ownership in Asia isThailand in the 1990s. To allow comparison with bond flows, where return adjust-ments and market capitalizations are not available, we also calculate the cumulativeequity flows to GDP without return adjustments. In this analysis, Mexico, Chile andMalaysia have the largest cumulative U.S. equity flows to GDP. Bond flows to GDPare presented in the next column. The highest averages of the cumulative bond flowsto GDP are found in Mexico, Venezuela and Argentina. Clearly, cumulative net bondflows are much smaller than equity flows. By adding cumulative equity and bondflows, we obtain a measure of total external financing through portfolio capital. Wealso report sample averages and averages in the 1990s. There are two countries withnet negative external financing, Chile and Taiwan, both, not surprisingly, countrieswith stringent capital controls. Mexico, Venezuela and Malaysia have the highestexternal financing to GDP. Generally, both equity and bond flows are larger in thenineties than for the full sample, and total external financing is larger in the ninetiesfor 15 out of 17 countries.

We now consider different groups of countries based on this information for the1990s sample. First, we rank the countries according to the importance of externalfinance. In addition to the three countries previously mentioned (Mexico, Venezuelaand Malaysia), we add Argentina, Brazil and Korea to the top group. The bottomsix countries are, in addition to Chile and Taiwan, India, Greece, the Philippines andPakistan, all with less than 0.35% of GDP in external financing through US bondand equity flows.

Finally, we want to select countries that primarily rely on equity capital and coun-tries that primarily rely on fixed income. This is not trivial to do, since for somecountries the absolute flows may be very small and, in particular, for bonds, theymay be negative. Our approach was to rank countries based on the difference betweenthe average cumulative post-1989 equity and bond flows to GDP. The bottom sixcountries are deemed bond-reliant, the top six equity reliant. We exclude countrieswhen they do not place in the top 10 ranked according to cumulative bond flows orcumulative equity flows to GDP, respectively. The countries relying primarily onequity are Chile, the Philippines, Malaysia, Portugal, Thailand and Korea. Weexcluded Taiwan because of its insignificant absolute equity flows. Although Mexico,Brazil and Argentina are top countries in terms of equity flows to GDP, they appearin the fixed income group because of their substantial positive fixed income flows.The other three countries are Venezuela, Pakistan, and Indonesia. Because of therelative non-importance of bond flows in general, it is possible that countries groupedin the “rely on bonds” category receive more equity than bond capital.

At the bottom of the table, we present country groupings. We find that LatinAmerican countries tend to have high US equity ownership. Asian countries have

COLUMBIA BUSINESS SCHOOL 12

307G. Bekaert et al. / Journal of International Money and Finance 21 (2002) 295–350

Tab

le1

Sum

mar

yan

alys

isof

net

equi

tyflo

ws

and

net

bond

flow

s

Cou

ntry

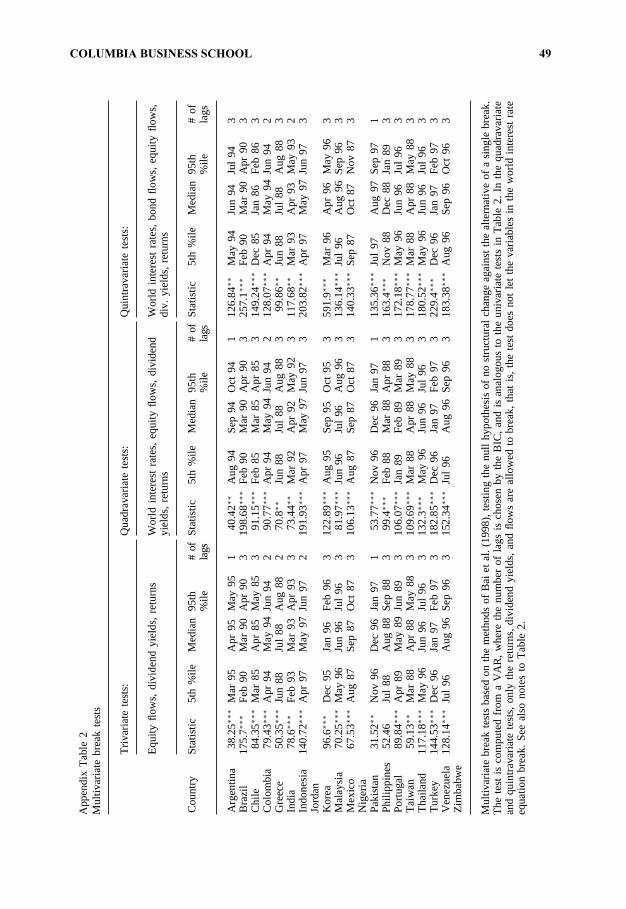

Ave

rage

ofcu

mul

ativ

eA

vera

geof

cum

ulat

ive

Ave

rage

ofcu

mul

ativ

eA

vera

geof

tota

lE

quity

flow

H0:

Equ

ityflo

ws

H 0:

Bon

dflo

ws

equi

tyflo

ws/

equi

tyeq

uity

flow

s/G

DP

bond

flow

s/G

DP

cum

ulat

ive

exte

rnal

and

bond

flow

dono

tG

rang

erdo

not

Gra

nger

capi

taliz

atio

nfin

anci

ngto

GD

Pco

rrel

atio

nca

use

bond

flow

sca

use

equi

tyflo

ws

Ful

lP

ost-

1990

Ful

lP

ost-

1990

Ful

lP

ost-

1990

Ful

lP

ost-

1990

P-v

alue

P-v

alue

Arg

entin

a0.

0093

0.08

370.

0035

0.00

900.

0040

0.01

040.

0074

0.01

940.

055

0.55

80.

114

Bra

zil

0.05

190.

1271

0.00

370.

0093

0.00

300.

0077

0.00

670.

0170

0.01

30.

000

0.16

5C

hile

0.02

330.

0578

0.00

900.

0226

�0.

0326

�0.

0642

�0.

0236

�0.

0416

�0.

049

0.03

60.

897

Col

ombi

a0.

0137

0.03

230.

0017

0.00

44�

0.00

010.

0022

0.00

150.

0065

0.18

90.

000

0.00

0G

reec

e0.

0012

0.01

730.

0008

0.00

23�

0.00

09�

0.00

09�

0.00

010.

0014

0.04

60.

262

0.01

9In

dia

0.00

480.

0112

0.00

080.

0019

�0.

0010

�0.

0009

�0.

0002

0.00

110.

195

0.00

00.

000

Indo

nesi

a0.

0302

0.07

640.

0027

0.00

690.

0023

0.00

580.

0050

0.01

27�0.

007

0.83

40.

181

Jord

ann.

a.n.

a.n.

a.n.

a.n.

a.n.

a.n.

a.n.

a.n.

a.n.

a.n.

a.K

orea

0.04

170.

0781

0.00

370.

0088

0.00

160.

0056

0.00

530.

0144

0.07

10.

000

0.00

0M

alay

sia

0.01

150.

0263

0.00

880.

0210

�0.

0058

0.00

040.

0030

0.02

14�

0.13

50.

996

0.76

3M

exic

o0.

1186

0.24

110.

0104

0.02

530.

0196

0.04

660.

0300

0.07

190.

103

0.97

30.

000

Nig

eria

n.a.

n.a.

n.a.

n.a.

n.a.

n.a.

n.a.

n.a.

n.a.

n.a.

n.a.

Pak

ista

n0.

0058

0.01

480.

0007

0.00

180.

0006

0.00

140.

0012

0.00

320.

110

0.00

00.

100

Phi

lippi

nes

0.01

760.

0444

0.00

460.

0115

�0.

0052

�0.

0101

�0.

0006

0.00

140.

035

0.83

20.

998

Por

tuga

l0.

0284

0.07

010.

0028

0.00

70�

0.00

16�

0.00

330.

0012

0.00

370.

043

0.00

00.

002

Tai

wan

0.00

100.

0020

0.00

010.

0004

�0.

0110

�0.

0278

�0.

0109

�0.

0274

0.02

20.

973

0.95

3T

haila

nd0.

0320

0.06

670.

0026

0.00

59�

0.00

05�

0.00

010.

0021

0.00

58�

0.06

30.

013

0.00

1T

urke

y0.

0188

0.04

770.

0010

0.00

280.

0003

0.00

100.

0014

0.00

38�0.

169

0.61

10.

441

Ven

ezue

la�

0.00

49�

0.00

910.

0004

0.00

110.

0139

0.03

270.

0144

0.03

380.

0070

0.99

00.

892

Zim

babw

en.

a.n.

a.n.

a.n.

a.n.

a.n.

a.n.

a.n.

a.n.

a.n.

a.n.

a.(c

onti

nued

onne

xtpa

ge)

COLUMBIA BUSINESS SCHOOL 13

308 G. Bekaert et al. / Journal of International Money and Finance 21 (2002) 295–350

Tab

le1

(cont

inue

d)

Cou

ntry

Ave

rage

ofcu

mul

ativ

eA

vera

geof

cum

ulat

ive

Ave

rage

ofcu

mul

ativ

eA

vera

geof

tota

lE

quity

flow

H0:

Equ

ityflo

ws

H 0:

Bon

dflo

ws

equi

tyflo

ws/

equi

tyeq

uity

flow

s/G

DP

bond

flow

s/G

DP

cum

ulat

ive

exte

rnal

and

bond

flow

dono

tG

rang

erdo

not

Gra

nger

capi

taliz

atio

nfin

anci

ngto

GD

Pco

rrel

atio

nca

use

bond

flow

sca

use

equi

tyflo

ws

Ful

lP

ost-

1990

Ful

lP

ost-

1990

Ful

lP

ost-

1990

Ful

lP

ost-

1990

P-v

alue

P-v

alue

Ful

l0.

0238

0.05

810.

0034

0.00

83�

0.00

080.

0004

0.00

260.

0087

0.02

7A

sia

0.02

230.

0490

0.00

370.

0091

�0.

0031

�0.

0044

0.00

060.

0047

�0.

013

Latin

0.03

530.

0888

0.00

480.

0119

0.00

130.

0059

0.00

610.

0178

0.05

3R

ely

onst

ocks

0.02

570.

0572

0.00

520.

0128

�0.

0073

�0.

0119

�0.

0021

0.00

09�

0.01

6R

ely

onbo

nds

0.03

520.

0890

0.00

360.

0089

0.00

720.

0174

0.01

080.

0263

0.04

7T

opex

tern

al0.

0380

0.09

120.

0051

0.01

240.

0060

0.01

720.

0111

0.02

960.

019

Bot

tom

exte

rnal

0.00

890.

0246

0.00

270.

0067

�0.

0083

�0.

0171

�0.

0057

�0.

0103

0.06

0

Ful

lre

pres

ents

aneq

ually

-wei

ghte

dav

erag

eac

ross

all

coun

trie

s.A

sia

isan

equa

lly-w

eigh

ted

aver

age

acro

sssi

xA

sian

coun

trie

s(I

ndon

esia

,K

ore

a,M

alay

sia,

the

Phi

lippi

nes,

Tai

wan

and

Tha

iland

),an

dLa

tinis

equa

lly-w

eigh

ted

aver

age

acro

sssi

xLa

tinA

mer

ican

coun

trie

s(A

rgen

tina,

Bra

zil,

Chi

le,

Col

ombi

a,M

exic

oan

dV

enez

uela

).W

eal

sore

port

equa

lly-w

eigh

ted

acro

ssth

esi

xco

untr

ies

that

rely

mos

ton

equi

tyfin

anci

ng(C

hile

,th

eP

hilip

pine

s,M

alay

sia,

Por

tuga

l,T

haila

ndan

dK

orea

),eq

ually

-wei

ghte

dac

ross

the

six

coun

trie

sth

atre

lym

ost

onbo

ndfin

anci

ng(V

enez

uela

,M

exic

o,A

rgen

tina,

Pak

ista

n,In

done

sia

and

Bra

zil),

equa

lly-w

eigh

ted

acro

ssth

esi

xco

untr

ies

that

have

the

high

est

prop

ort

ion

ofex

tern

alfin

anci

ng,

that

is,

the

bond

plus

equi

tyca

pita

lflow

sto

GD

P(M

exic

o,M

alay

sia,

Ven

ezue

la,

Arg

entin

a,B

razi

land

Kor

ea)

and

the

six

coun

trie

sw

ithth

elo

wes

tpr

opor

tion

ofex

tern

alfin

anci

ngto

GD

P(C

hile

,T

aiw

an,

Pak

ista

n,th

eP

hilip

pine

s,G

reec

ean

dIn

dia)

.T

heco

rrel

atio

nsar

ees

timat

edov

erth

efu

llsa

mpl

e.T

hebr

eak

date

sfo

rea

chco

untr

yar

epr

esen

ted

inT

able

2.T

heG

rang

er-c

ausa

lity

test

sar

efr

oma

biva

riate

VA

Rof

equi

tyre

turn

san

dbo

ndre

turn

ses

timat

edov

erth

efu

llsa

mpl

e.

COLUMBIA BUSINESS SCHOOL 14

309G. Bekaert et al. / Journal of International Money and Finance 21 (2002) 295–350

had sharply negative bond outflows in the 1990s perhaps due in part to the Asiancrisis. Latin American countries tend to rely more on equity financing than Asiancountries. The countries grouped in the “relying on bonds” category are generallycountries that heavily rely on external portfolio capital, including equity capital. Asa proportion of market capitalization, these countries have higher U.S. holdings thanthe “stock reliant” countries.

Table 1 presents some additional information on the relation between bond andstock flows. Given that our analysis focuses on equity flows, it is important to knowwhether bond flows are substitutes for equity flows. We present the correlation ofthe net capital flows which is, in general, small. The highest correlation is found forIndia and Colombia. The largest negative correlations are found for Turkey andMalaysia. In the majority of the countries, the correlation is positive, and of the fivenegative correlations, three are in South-East Asian countries.

We also present Granger-causality tests based on a bivariate system of stock flowsto market capitalization and bond flows to GDP. We can reject the hypothesis at the5% level that equity flows do not Granger-cause bond flows in Brazil, Chile, Colom-bia, India, Korea, Pakistan, Portugal and Thailand. We can reject the hypothesis atthe 5% level that bond flows do not Granger-cause equity flows in Colombia, Greece,Indonesia, Korea, Mexico, Portugal and Thailand. Hence, there are five countries forwhich there are significant predictive relations in both directions, potentially suggest-ing the effect of a third variable on general capital flows or persistence in capitalflows after a capital market liberalization. There is no support for a consistent patternwhere bonds always lead equity (or vice versa) or where bonds and equity areclear substitutes.

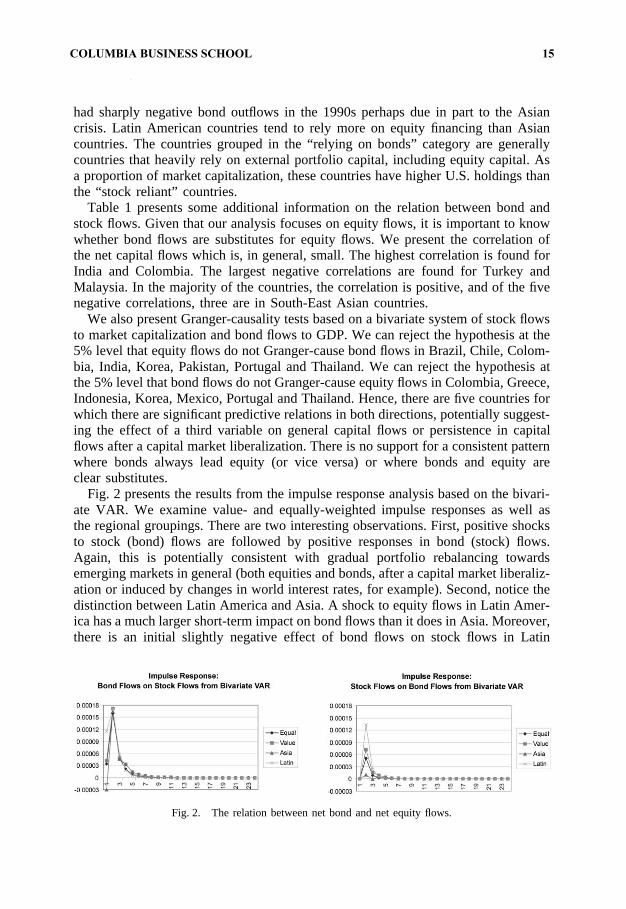

Fig. 2 presents the results from the impulse response analysis based on the bivari-ate VAR. We examine value- and equally-weighted impulse responses as well asthe regional groupings. There are two interesting observations. First, positive shocksto stock (bond) flows are followed by positive responses in bond (stock) flows.Again, this is potentially consistent with gradual portfolio rebalancing towardsemerging markets in general (both equities and bonds, after a capital market liberaliz-ation or induced by changes in world interest rates, for example). Second, notice thedistinction between Latin America and Asia. A shock to equity flows in Latin Amer-ica has a much larger short-term impact on bond flows than it does in Asia. Moreover,there is an initial slightly negative effect of bond flows on stock flows in Latin

Fig. 2. The relation between net bond and net equity flows.

COLUMBIA BUSINESS SCHOOL 15

310 G. Bekaert et al. / Journal of International Money and Finance 21 (2002) 295–350

America whereas the effect in Asia is positive. From the second period onwards,the effects are positive and very similar in magnitude across the two regions. Fromboth graphs, it is clear that the effects die out within six months. We also conducteda break point analysis of bond and equity flows. In the countries that experiencedsignificant breaks in equities and bond capital flows, the break in bonds precededthe break in equities in four countries (Argentina, Korea, Malaysia and Thailand).The break in equities preceded the break in bonds in five countries (Brazil, Colombia,Greece, India and the Philippines). With the exception of one country, the Philip-pines, the equity and bond breaks are clustered closely in time for all of thesecountries.4

Taken together, our results suggest that bond and equity flows are not substitutesbut both increased in the nineties with the liberalization process.

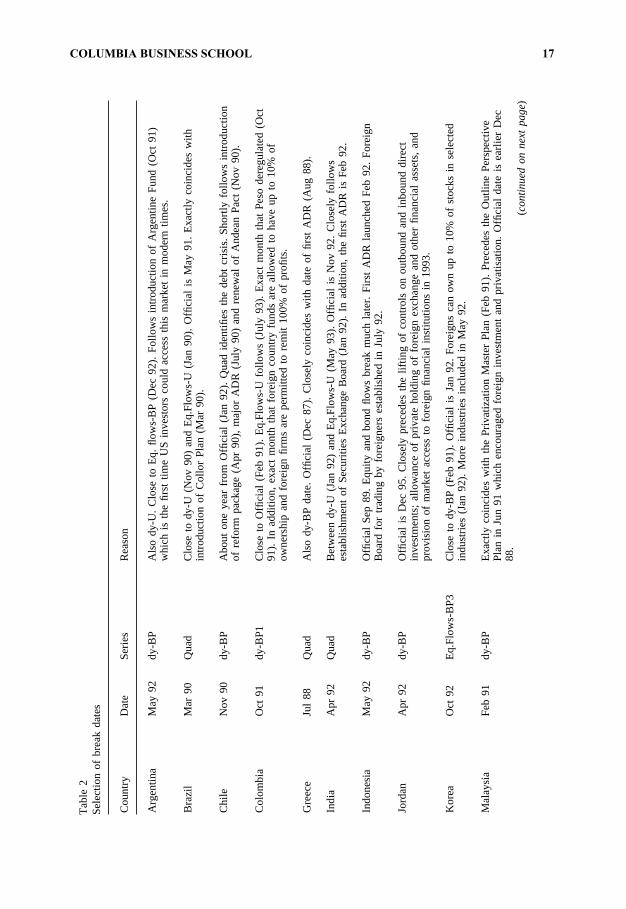

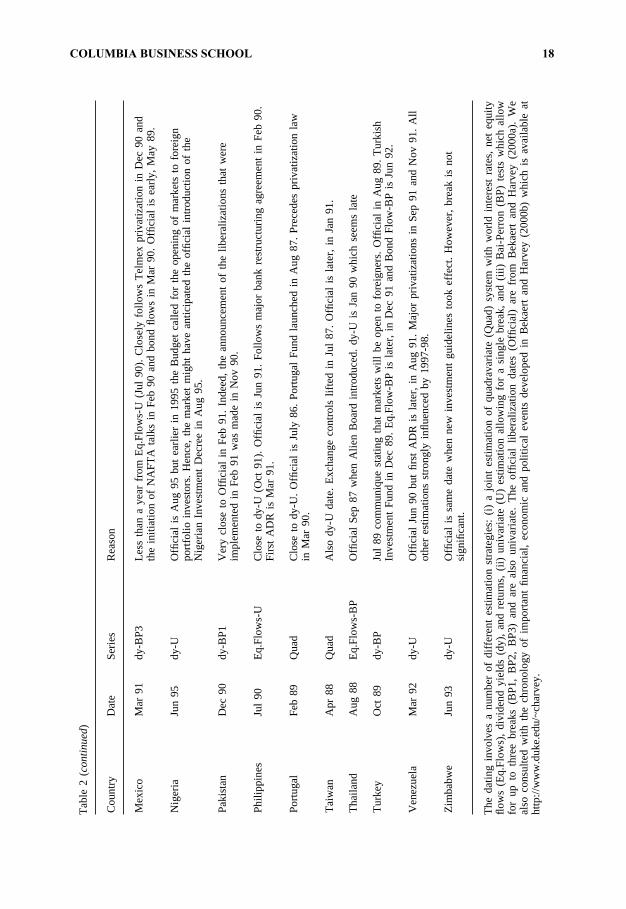

4. Breaks and initial pre and post-break analysis

4.1. Break analysis

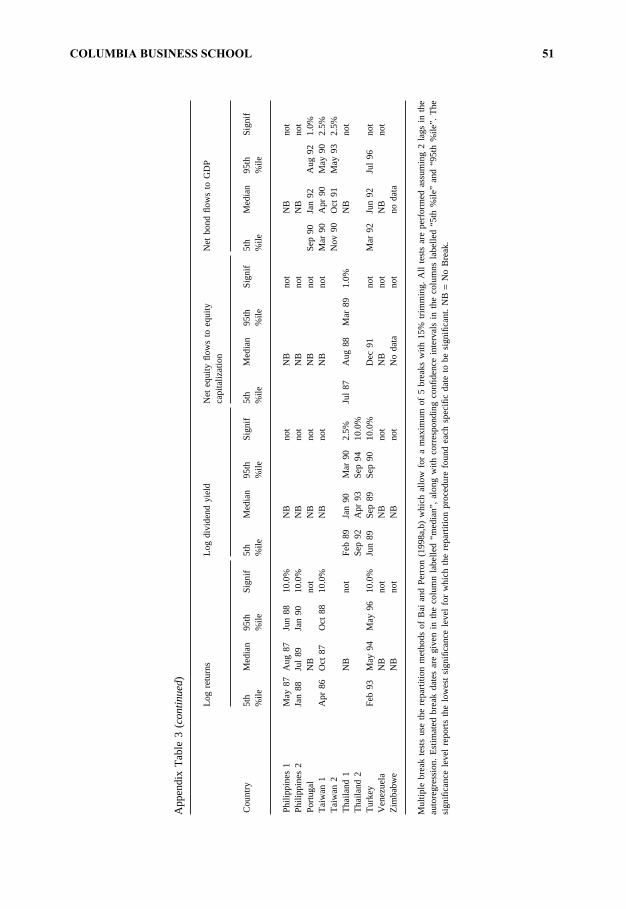

To select an appropriate break date for use in subsequent analysis, we rely onseveral pieces of information. First, we use the results of the univariate break analysisfor three series: returns, dividend yields and net equity flows. We compute themedian break date, the 90% confidence interval for the date in months as well as astatistic that provides a test of the null hypothesis that no break occurred. Detailedresults on all break tests are reported in Appendix Tables 1–3.

Second, we conduct a multivariate analysis of breaks using the BLS framework.We investigate three specifications. The first is a trivariate system with equity capitalflows, dividend yields and returns. The second specification is a quadravariate systemthat includes an equation for the world interest rate. However, the coefficients in theworld interest rate equation are not allowed to break in the estimation but the depen-dence of the other variables in the system on the world interest rate may break. Thethird specification adds the bond capital flows to the system of equations to see ifthe breaks we find are affected by this addition. For 13 of the 17 countries, themultivariate breaks fall within the range of the univariate breaks for either bond orequity flows. For four countries, (Greece, Mexico, Portugal and Taiwan), the breakdates correspond to the break dates in dividend yields or returns, but the confidenceintervals for the breaks are always tighter in the multivariate estimation consistentwith what the theory would predict. Finally, the break dates from the three multivari-ate systems are very close to each other.

Third, we conduct the Bai-Perron tests that allow for multiple breaks. In a numberof countries more than one break occurs. For example, in the dividend yield esti-mation for Mexico there are three significant breaks: January 1983, July 1986 andMarch 1991. The first date closely follows the onset of the Latin American debt

4 See Appendix Table 1.

COLUMBIA BUSINESS SCHOOL 16

311G. Bekaert et al. / Journal of International Money and Finance 21 (2002) 295–350

crisis. The second date closely follows the abolition of the official exchange rateand coincides with major debt restructuring. The final date closely follows the privat-ization of Telmex and the beginning of the NAFTA negotiations. For the flows esti-mation, we find little evidence in favor of multiple breaks, although this may be dueto low power. Argentina shows two breaks in equity flows, with the second onebeing detected in the BLS tests. There are three breaks for equity flows in Korea,partially reflecting the gradual lifting of foreign ownership. Finally, there are twobreak dates for bond flows in Taiwan, one preceding and one following the liberaliz-ation plan of January 1991. Hence, there appears to be a pattern in the multiplebreak analysis that is linked to important events tied to either deliberalization orliberalization of capital markets.

Finally, we link the statistical breaks to the economic events detailed in Bekaertand Harvey (2000b). The end-result is presented in Table 2, where we also brieflyindicate the motivation for each break date. All the dates we choose are dates foundby one of the break analyses we conducted, but the final choice uses exogenousinformation on regulatory reforms to make sure we use a relevant break date. Werely heavily on the break dates that arise from the quadravariate system as well asthe Bai-Perron breaks for dividend yields and equity flows. For example, the Bai-Perron break for equity capital flows in Thailand is August 1988. This closely corre-sponds to the opening of the market to foreigners by the creation of the Alien Boardfor trading in late 1987. The quadravariate and quintravariate date for Taiwan isApril 1988. This closely corresponds to the lifting of exchange controls. Pakistan isparticularly interesting. Most consider the official liberalization to be February 1991.The Bai-Perron break in dividend yields is earlier, in December 1990. However,an examination of the chronology shows that the liberalization was announced inNovember 1990.5

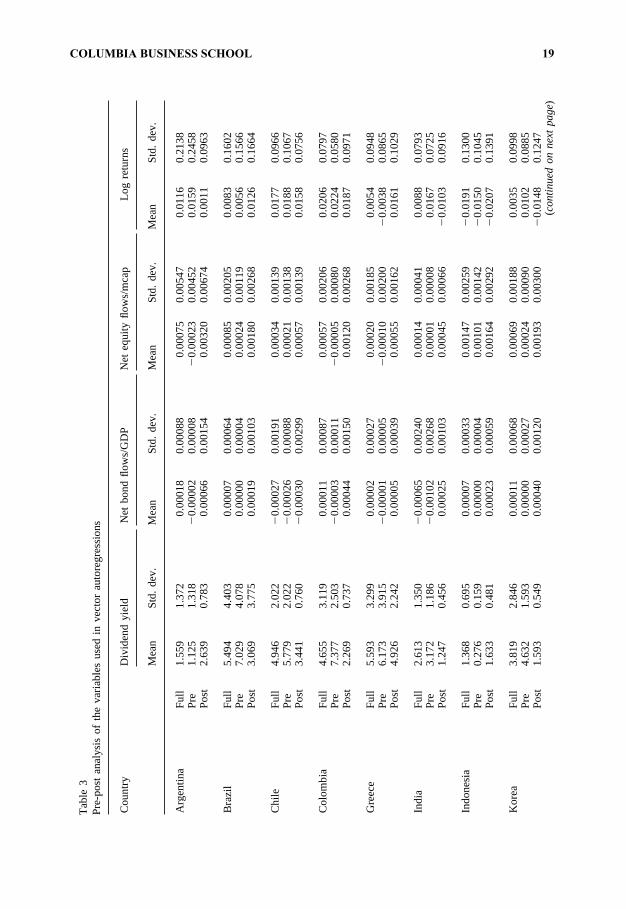

4.2. The impact of breaks on unconditional means

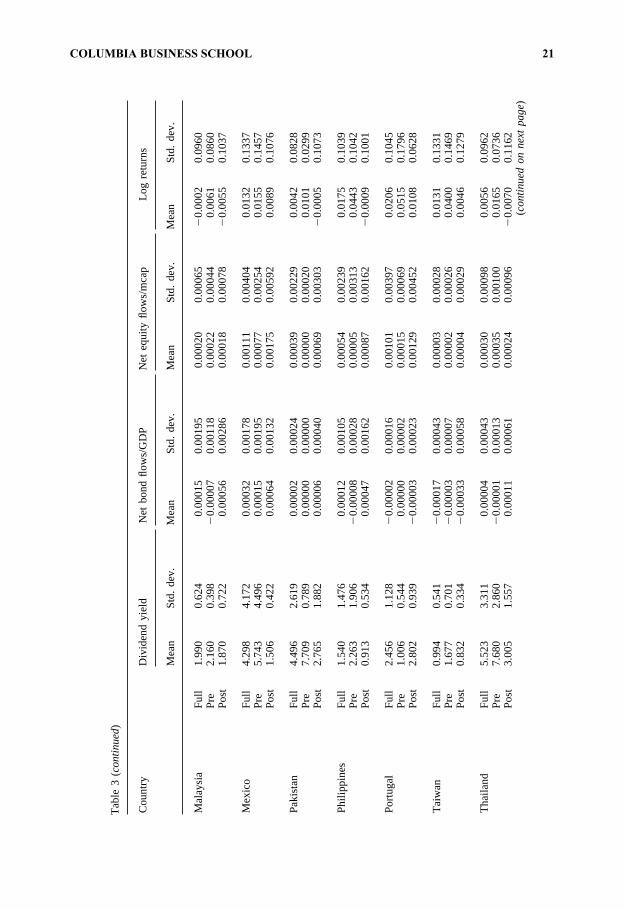

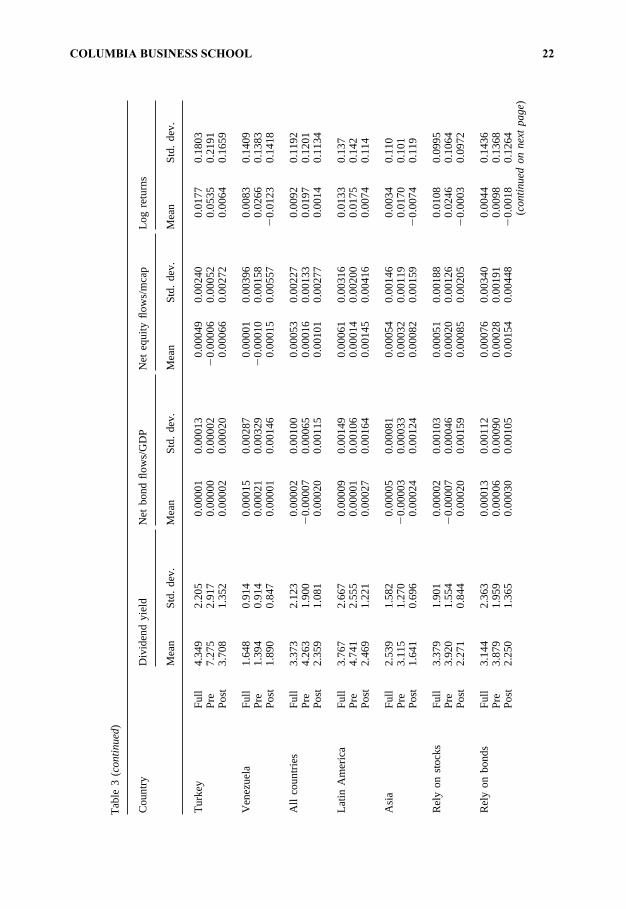

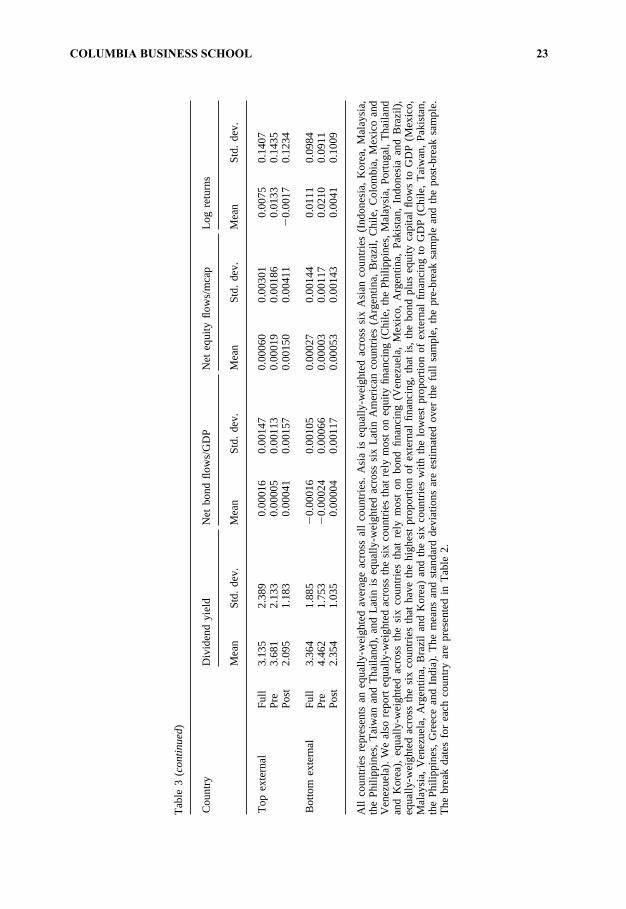

Table 3 presents an analysis of both the means and standard deviations of the fourcountry-specific variables that we study in the VARs: dividend yields, log returns,net bond flows to GDP and net equity flows to equity market capitalization. Individ-ual country results and results for our country groupings are presented for the fullsample, as well as the pre- and post-break periods using the dates in Table 2.

There are a number of interesting differences between the pre-break and post-break periods. The dividend yields are sharply lower on average (2.5 in post-breakand 4.7 in pre-break). The yields decrease in 13 of 17 countries. This is consistentwith the idea that expected returns decrease after a liberalization. Although returnsare much noisier than dividend yields, we also observe that the average return

5 We also closely examined the results of estimations with a smaller trimming factor, which suggestedbreaks near the end of the sample that are associated with the Asian crisis. Since these dates are verymuch near the end of our sample, we did not exclude post-break observations.

COLUMBIA BUSINESS SCHOOL 17

312 G. Bekaert et al. / Journal of International Money and Finance 21 (2002) 295–350T

able

2S

elec

tion

ofbr

eak

date

s

Cou

ntry

Dat

eS

erie

sR

easo

n

Arg

entin

aM

ay92

dy-B

PA

lso

dy-U

.C

lose

toE

q.flo

ws-

BP

(Dec

92).

Fol

low

sin

trod

uctio

nof

Arg

entin

eF

und

(Oct

91)

whi

chis

the

first

time

US

inve

stor

sco

uld

acce

ssth

ism

arke

tin

mod

ern

times

.

Bra

zil

Mar

90Q

uad

Clo

seto

dy-U

(Nov

90)

and

Eq.

Flo

ws-

U(J

an90

).O

ffici

alis

May

91.

Exa

ctly

coin

cide

sw

ithin

trod

uctio

nof

Col

lor

Pla

n(M

ar90

).

Chi

leN

ov90

dy-B

PA

bout

one

year

from

Offi

cial

(Jan

92).

Qua

did

entifi

esth

ede

btcr

isis

.S

hort

lyfo

llow

sin

trod

uctio

nof

refo

rmpa

ckag

e(A

pr90

),m

ajor

AD

R(J

uly

90)

and

rene

wal

ofA

ndea

nP

act

(Nov

90).

Col

ombi

aO

ct91

dy-B

P1

Clo

seto

Offi

cial

(Feb

91).

Eq.

Flo

ws-

Ufo

llow

s(J

uly

93).

Exa

ctm

onth

that

Pes

ode

regu

late

d(O

ct91

).In

addi

tion,

exac

tm

onth

that

fore

ign

coun

try

fund

sar

eal

low

edto

have

upto

10%

ofow

ners

hip

and

fore

ign

firm

sar

epe

rmitt

edto

rem

it10

0%of

profi

ts.

Gre

ece

Jul

88Q

uad

Als

ody

-BP

date

.O

ffici

al(D

ec87

).C

lose

lyco

inci

des

with

date

offir

stA

DR

(Aug

88).

Indi

aA

pr92

Qua

dB

etw

een

dy-U

(Jan

92)

and

Eq.

Flo

ws-

U(M

ay93

).O

ffici

alis

Nov

92.

Clo

sely

follo

ws

esta

blis

hmen

tof

Sec

uriti

esE

xcha

nge

Boa

rd(J

an92

).In

addi

tion,

the

first

AD

Ris

Feb

92.

Indo

nesi

aM

ay92

dy-B

PO

ffici

alS

ep89

.E

quity

and

bond

flow

sbr

eak

muc

hla

ter.

Firs

tA

DR

laun

ched

Feb

92.

For

eign

Boa

rdfo

rtr

adin

gby

fore

igne

rses

tabl

ishe

din

July

92.

Jord

anA

pr92

dy-B

PO

ffici

alis

Dec

95.

Clo

sely

prec

edes

the

liftin

gof

cont

rols

onou

tbou

ndan

din

boun

ddi

rect

inve

stm

ents

;al

low

ance

ofpr

ivat

eho

ldin

gof

fore

ign

exch

ange

and

othe

rfin

anci

alas

sets

,an

dpr

ovis

ion

ofm

arke

tac

cess

tofo

reig

nfin

anci

alin

stitu

tions

in19

93.

Kor

eaO

ct92

Eq.

Flo

ws-

BP

3C

lose

tody

-BP

(Feb

91).

Offi

cial

isJa

n92

.F

orei

gns

can

own

upto

10%

ofst

ocks

inse

lect

edin

dust

ries

(Jan

92).

Mor

ein

dust

ries

incl

uded

inM

ay92

.

Mal

aysi

aF

eb91

dy-B

PE

xact

lyco

inci

des

with

the

Priv

atiz

atio

nM

aste

rP

lan

(Feb

91).

Pre

cede

sth

eO

utlin

eP

ersp

ectiv

eP

lan

inJu

n91

whi

chen

cour

aged

fore

ign

inve

stm

ent

and

priv

atis

atio

n.O

ffici

alda

teis

earli

erD

ec88

.(c

onti

nued

onne

xtpa

ge)

COLUMBIA BUSINESS SCHOOL 17

313G. Bekaert et al. / Journal of International Money and Finance 21 (2002) 295–350T

able

2(co

ntin

ued)

Cou

ntry

Dat

eS

erie

sR

easo

n

Mex

ico

Mar

91dy

-BP

3Le

ssth

ana

year

from

Eq.

Flo

ws-

U(J

ul90

).C

lose

lyfo

llow

sT

elm

expr

ivat

izat

ion

inD

ec90

and

the

initi

atio

nof

NA

FT

Ata

lks

inF

eb90

and

bond

flow

sin

Mar

90.

Offi

cial

isea

rly,

May

89.

Nig

eria

Jun

95dy

-UO

ffici

alis

Aug

95bu

tea

rlier

in19

95th

eB

udge

tca

lled

for

the

open

ing

ofm

arke

tsto

fore

ign

port

folio

inve

stor

s.H

ence

,th

em

arke

tm

ight

have

antic

ipat

edth

eof

ficia

lin

trod

uctio

nof

the

Nig

eria

nIn

vest

men

tD

ecre

ein

Aug

95.

Pak

ista

nD

ec90

dy-B

P1

Ver

ycl

ose

toO

ffici

alin

Feb

91.

Inde

ed,

the

anno

unce

men

tof

the

liber

aliz

atio

nsth

atw

ere

impl

emen

ted

inF

eb91

was

mad

ein

Nov

90.

Phi

lippi

nes

Jul

90E

q.F

low

s-U

Clo

seto

dy-U

(Oct

91).

Offi

cial

isJu

n91

.F

ollo

ws

maj

orba

nkre

stru

ctur

ing

agre

emen

tin

Feb

90.

Firs

tA

DR

isM

ar91

.

Por

tuga

lF

eb89

Qua

dC

lose

tody

-U.

Offi

cial

isJu

ly86

.P

ortu

gal

Fun

dla

unch

edin

Aug

87.

Pre

cede

spr

ivat

izat

ion

law

inM

ar90

.

Tai

wan

Apr

88Q

uad

Als

ody

-Uda

te.

Exc

hang

eco

ntro

lslif

ted

inJu

l87

.O

ffici

alis

late

r,in

Jan

91.

Tha

iland

Aug

88E

q.F

low

s-B

PO

ffici

alS

ep87

whe

nA

lien

Boa

rdin

trod

uced

.dy

-Uis

Jan

90w

hich

seem

sla

te

Tur

key

Oct

89dy

-BP

Jul

89co

mm

uniq

uest

atin

gth

atm

arke

tsw

illbe

open

tofo

reig

ners

.O

ffici

alin

Aug

89.

Tur

kish

Inve

stm

ent

Fun

din

Dec

89.

Eq.

Flo

w-B

Pis

late

r,in

Dec

91an

dB

ond

Flo

w-B

Pis

Jun

92.

Ven

ezue

laM

ar92

dy-U

Offi

cial

Jun

90bu

tfir

stA

DR

isla

ter,

inA

ug91

.M

ajor

priv

atiz

atio

nsin

Sep

91an

dN

ov91

.A

llot

her

estim

atio

nsst

rong

lyin

fluen

ced

by19

97-9

8.

Zim

babw

eJu

n93

dy-U

Offi

cial

issa

me

date

whe

nne

win

vest

men

tgu

idel

ines

took

effe

ct.

How

ever

,br

eak

isno

tsi

gnifi

cant

.

The

datin

gin

volv

esa

num

ber

ofdi

ffere

ntes

timat

ion

stra

tegi

es:

(i)a

join

tes

timat

ion

ofqu

adra

varia

te(Q

uad)

syst

emw

ithw

orld

inte

rest

rate

s,ne

teq

uity

flow

s(E

q.F

low

s),

divi

dend

yiel

ds(d

y),

and

retu

rns,

(ii)

univ

aria

te(U

)es

timat

ion

allo

win

gfo

ra

sing

lebr

eak,

and

(iii)

Bai

-Per

ron

(BP

)te

sts

whi

ch

allo

wfo

rup

toth

ree

brea

ks(B

P1,

BP

2,B

P3)

and

are

also

univ

aria

te.

The

offic

ial

liber

aliz

atio

nda

tes

(Offi

cial

)ar

efr

omB

ekae

rtan

dH

arve

y(2

000a

).W

eal

soco

nsul

ted

with

the

chro

nolo

gyof

impo

rtan

tfin

anci

al,

econ

omic

and

polit

ical

even

tsde

velo

ped

inB

ekae

rtan

dH

arve

y(2

000b

)w

hich

isav

aila

ble

at

http

://w

ww

.duk

e.ed

u/~

char

vey.

COLUMBIA BUSINESS SCHOOL 18

314 G. Bekaert et al. / Journal of International Money and Finance 21 (2002) 295–350T

able

3P

re-p

ost

anal

ysis

ofth

eva

riabl

esus

edin

vect

orau

tore

gres

sion

s

Cou

ntry

Div

iden

dyi

eld

Net

bond

flow

s/G

DP

Net

equi

tyflo

ws/

mca

pLo

gre

turn

s

Mea

nS

td.

dev.

Mea

nS

td.

dev.

Mea

nS

td.

dev.

Mea

nS

td.

dev.

Arg

entin

aF

ull

1.55

91.

372

0.00

018

0.00

088

0.00

075

0.00

547

0.01

160.

2138

Pre

1.12

51.

318

�0.

0000

20.

0000

8�

0.00

023

0.00

452

0.01

590.

2458

Pos

t2.

639

0.78

30.

0006

60.

0015

40.

0032

00.

0067

40.

0011

0.09

63

Bra

zil

Ful

l5.

494

4.40

30.

0000

70.

0006

40.

0008

50.

0020

50.

0083

0.16

02P

re7.

029

4.07

80.

0000

00.

0000

40.

0002

40.

0011

90.

0056

0.15

66P

ost

3.06

93.

775

0.00

019

0.00

103

0.00

180

0.00

268

0.01

260.

1664

Chi

leF

ull

4.94

62.

022

�0.

0002

70.

0019

10.

0003

40.

0013

90.

0177

0.09

66P

re5.

779

2.02

2�

0.00

026

0.00

088

0.00

021

0.00

138

0.01

880.

1067

Pos

t3.

441

0.76

0�

0.00

030

0.00

299

0.00

057

0.00

139

0.01

580.

0756

Col

ombi

aF

ull

4.65

53.

119

0.00

011

0.00

087

0.00

057

0.00

206

0.02

060.

0797

Pre

7.37

72.

503

�0.

0000

30.

0001

1�

0.00

005

0.00

080

0.02

240.

0580

Pos

t2.

269

0.73

70.

0004

40.

0015

00.

0012

00.

0026

80.

0187

0.09

71

Gre

ece

Ful

l5.

593

3.29

90.

0000

20.

0002

70.

0002

00.

0018

50.

0054

0.09

48P

re6.

173

3.91

5�

0.00

001

0.00

005

�0.

0001

00.

0020

0�

0.00

380.

0865

Pos

t4.

926

2.24

20.

0000

50.

0003

90.

0005

50.

0016

20.

0161

0.10

29

Indi

aF

ull

2.61

31.

350

�0.

0006

50.

0024

00.

0001

40.

0004

10.

0088

0.07

93P

re3.

172

1.18

6�

0.00

102

0.00

268

0.00

001

0.00

008

0.01

670.

0725

Pos

t1.

247

0.45

60.

0002

50.

0010

30.

0004

50.

0006

6�

0.01

030.

0916

Indo

nesi

aF

ull

1.36

80.

695

0.00

007

0.00

033

0.00

147

0.00

259

�0.

0191

0.13

00P

re0.

276

0.15

90.

0000

00.

0000

40.

0010

10.

0014

2�

0.01

500.

1045

Pos

t1.

633

0.48

10.

0002

30.

0005

90.

0016

40.

0029

2�

0.02

070.

1391

Kor

eaF

ull

3.81

92.

846

0.00

011

0.00

068

0.00

069

0.00

188

0.00

350.

0998

Pre

4.63

21.

593

0.00

000

0.00

027

0.00

024

0.00

090

0.01

020.

0885

Pos

t1.

593

0.54

90.

0004

00.

0012

00.

0019

30.

0030

0�

0.01

480.

1247

(con

tinu

edon

next

page

)

COLUMBIA BUSINESS SCHOOL 19

315G. Bekaert et al. / Journal of International Money and Finance 21 (2002) 295–350

Tab

le3

(cont

inue

d)

Cou

ntry

Div

iden

dyi

eld

Net

bond

flow

s/G

DP

Net

equi

tyflo

ws/

mca

pLo

gre

turn

s

Mea

nS

td.

dev.

Mea

nS

td.

dev.

Mea

nS

td.

dev.

Mea

nS

td.

dev.

Mal

aysi

aF

ull

1.99

00.

624

0.00

015

0.00

195

0.00

020

0.00

065

�0.

0002

0.09

60P

re2.

160

0.39

8�

0.00

007

0.00

118

0.00

022

0.00

044

0.00

610.

0860

Pos

t1.

870

0.72

20.

0005

60.

0028

60.

0001

80.

0007

8�

0.00

550.

1037

Mex

ico

Ful

l4.

298

4.17

20.

0003

20.

0017

80.

0011

10.

0040

40.

0132

0.13

37P

re5.

743

4.49

60.

0001

50.

0019

50.

0007

70.

0025

40.

0155

0.14

57P

ost

1.50

60.

422

0.00

064

0.00

132

0.00

175

0.00

592

0.00

890.

1076

Pak

ista

nF

ull

4.49

62.

619

0.00

002

0.00

024

0.00

039

0.00

229

0.00

420.

0828

Pre

7.70

90.

789

0.00

000

0.00

000

0.00

000

0.00

020

0.01

010.

0299

Pos

t2.

765

1.88

20.

0000

60.

0004

00.

0006

90.

0030

3�

0.00

050.

1073

Phi

lippi

nes

Ful

l1.

540

1.47

60.

0001

20.

0010

50.

0005

40.

0023

90.

0175

0.10

39P

re2.

263

1.90

6�

0.00

008

0.00

028

0.00

005

0.00

313

0.04

430.

1042

Pos

t0.

913

0.53

40.

0004

70.

0016

20.

0008

70.

0016

2�

0.00

090.

1001

Por

tuga

lF

ull

2.45

61.

128

�0.

0000

20.

0001

60.

0010

10.

0039

70.

0206

0.10

45P

re1.

006

0.54

40.

0000

00.

0000

20.

0001

50.

0006

90.

0515

0.17

96P

ost

2.80

20.

939

�0.

0000

30.

0002

30.

0012

90.

0045

20.

0108

0.06

28

Tai

wan

Ful

l0.

994

0.54

1�

0.00

017

0.00

043

0.00

003

0.00

028

0.01

310.

1331

Pre

1.67

70.

701

�0.

0000

30.

0000

70.

0000

20.

0002

60.

0400

0.14

69P

ost

0.83

20.

334

�0.

0003

30.

0005

80.

0000

40.

0002

90.

0046

0.12

79

Tha

iland

Ful

l5.

523

3.31

10.

0000

40.

0004

30.

0003

00.

0009

80.

0056

0.09

62P

re7.

680

2.86

0�

0.00

001

0.00

013

0.00

035

0.00

100

0.01

650.

0736

Pos

t3.

005

1.55

70.

0001

10.

0006

10.

0002

40.

0009

6�

0.00

700.

1162

(con

tinu

edon

next

page

)

COLUMBIA BUSINESS SCHOOL 21

316 G. Bekaert et al. / Journal of International Money and Finance 21 (2002) 295–350

Tab

le3

(cont

inue

d)

Cou

ntry

Div

iden

dyi

eld

Net

bond

flow

s/G

DP

Net

equi

tyflo

ws/

mca

pLo

gre

turn

s

Mea

nS

td.

dev.

Mea

nS

td.

dev.

Mea

nS

td.

dev.

Mea

nS

td.

dev.

Tur

key

Ful

l4.

349

2.20

50.

0000

10.

0001

30.

0004

90.

0024

00.

0177

0.18

03P

re7.

275

2.91

70.

0000

00.

0000

2�

0.00

006

0.00

052

0.05

350.

2191

Pos

t3.

708

1.35

20.

0000

20.

0002

00.

0006

60.

0027

20.

0064

0.16

59

Ven

ezue

laF

ull

1.64

80.

914

0.00

015

0.00

287

0.00

001

0.00

396

0.00

830.

1409

Pre

1.39

40.

914

0.00

021

0.00

329

�0.

0001

00.

0015

80.

0266

0.13

83P

ost

1.89

00.

847

0.00

001

0.00

146

0.00

015

0.00

557

�0.

0123

0.14

18

All

coun

trie

sF

ull

3.37

32.

123

0.00

002

0.00

100

0.00

053

0.00

227

0.00

920.

1192

Pre

4.26

31.

900

�0.

0000

70.

0006

50.

0001

60.

0013

30.

0197

0.12

01P

ost

2.35

91.

081

0.00

020

0.00

115

0.00

101

0.00

277

0.00

140.

1134

Latin

Am

eric

aF

ull

3.76

72.

667

0.00

009

0.00

149

0.00

061

0.00

316

0.01

330.

137

Pre

4.74

12.

555

0.00

001

0.00

106

0.00

014

0.00

200

0.01

750.

142

Pos

t2.

469

1.22

10.

0002

70.

0016

40.

0014

50.

0041

60.

0074

0.11

4

Asi