Embed Size (px)

Citation preview

The EU’s CAP and the likely impact of a Doha Agreement

Lecture 24.

Economics of Food Markets

Alan Matthews

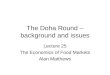

Why focus on Doha?Composition of operating surplus

in agriculture

Premia and arable aid

Market returns

Rural development payments

0

500

1000

1500

2000

2500

€ m

illi

on

Decoupling

WTO reduced protection

Rural development

Export Subsidies

• January 2003: EU initially offered to reduce aggregate expenditure limits by 45%– but in 2001/02 only used 35% of entitlement

• In July 2004 Framework Agreement, EU signed up conditionally to full elimination

• Importance of ‘credible date to be agreed’– Blair has called for end by 2010

• It may be that policy change will eliminate the commodity export surplus: but what about Non-Annex I goods, i.e. the food industry?

Domestic support – EU situation 2001 (before Mid-Term Review)

Amber Box US dollars

Bound AMS 65,383

Market Price Support 25,085

Direct Payments 12,117

less De Minimis 411

Current AMS 36,791

Degree of AMS Overhang 44%

Blue Box

$ Millions 21,262

% Value of Agricultural Production 7%

Green Box 19,452

Overall Distorting Support (ODS)

Bound ODS 87,056

Current ODS 58,464

Degree of ODS Overhang 33%

Market accessEffect on tariff cut on beef price

EU support price (basic intervention price)

€2,224

Estimated world market price €1,200

Current EU import tariff €1,922

Possible tariff cut which does not impact on EU market price (tariff overhang)

40%

Market accessEffect on tariff cut on beef price

EU market price €2,700

Estimated world market price €1,200

Current EU import tariff €1,922

Possible tariff cut which does not impact on EU market price (tariff overhang)

16%

Market accessEffect of tariff cuts on butter prices, €/tonne

Unfavourable world market

Favourable world

market

EU market price (2008) €2,247 €2,247

Estimated world market price

1,170 1,575

Current EU import tariff 1,896 1,896

Possible tariff cut which does not impact on EU market price (tariff overhang )

36% 54%

Market accessEffect of tariff cuts on SMP prices, €/tonne

Unfavourable world market

Favourable world market

EU market price (2008) 1,782 1,782

Estimated world market price

1,650 1,800

Current EU import tariff 1,118 1,118

Possible tariff cut which does not impact on EU market price (tariff overhang )

55% 64%

Effect of tariff cuts on white sugar price

EU support price (based on Commission July 2005 reform proposal)

€386

Estimated world market price €210

Current EU import tariff €419

Possible tariff cut which does not impact on EU market price (tariff overhang )

63%

Export Subsidies

• January 2003: EU initially offered to reduce aggregate expenditure limits by 45%– but in 2001/02 only used 35% of entitlement

• In July 2004 Framework Agreement, EU signed up conditionally to full elimination

• Hong Kong 2005 agreed to end date of 2013, with substantial progress in early years

• Only important now for dairy and sugar exports, but implications for Non-Annex I goods, i.e. the food industry?

The EU’s AVEs (ad valorem equivalents of specific rates), excluding sugar

Bands TariffLines

>100% 7480-99% 5160-79% 8240-59% 16620-39% 2800-19% 350Agra Europe, 22 July 2005

Note many of the highest tariffs are actually on processed foods (e.g. yogurt, whey) rather than bulk commodities

Comparison of EU banded offer with Swiss 60 formula

Market accessEffect on tariff cut on beef price

EU support price (basic intervention price)

€2,224

Estimated world market price €1,200

Current EU import tariff €1,922

Possible tariff cut which does not impact on EU market price (tariff overhang)

40%

Market accessEffect on tariff cut on beef price

EU market price €2,700

Estimated world market price €1,200

Current EU import tariff €1,922

Possible tariff cut which does not impact on EU market price (tariff overhang)

16%

Market accessEffect of tariff cuts on butter prices, €/tonne

Unfavourable world market

Favourable world

market

EU market price (2008) €2,247 €2,247

Estimated world market price

1,170 1,575

Current EU import tariff 1,896 1,896

Possible tariff cut which does not impact on EU market price (tariff overhang )

36% 54%

Market accessEffect of tariff cuts on SMP prices, €/tonne

Unfavourable world market

Favourable world market

EU market price (2008) 1,782 1,782

Estimated world market price

1,650 1,800

Current EU import tariff 1,118 1,118

Possible tariff cut which does not impact on EU market price (tariff overhang )

55% 64%

Effect of tariff cuts on white sugar price

EU support price (based on Commission July 2005 reform proposal)

€386

Estimated world market price €210

Current EU import tariff €419

Possible tariff cut which does not impact on EU market price (tariff overhang )

63%

Domestic support - EU situation 2001 (end Uruguay Round, before Mid-Term Review)

Amber Box US dollars

Bound AMS 65,383

Market Price Support 25,085

Direct Payments 12,117

less De Minimis 411

Current AMS 36,791

Degree of AMS Overhang 44%

Blue Box

$ Millions 21,262

% Value of Agricultural Production 7%

Green Box 19,452

Overall Distorting Support (ODS)

Bound ODS 87,056

Current ODS 58,464

Degree of ODS Overhang 33%

Fischler reforms (EU15):

• Switch 90%? of existing blue box expenditure into the green box

• Shift €4.2 billion (cotton, tobacco, etc.) from amber to blue/green

• Milk reforms strip €1.9 billion from amber box, and add (dairy premium) €0.4 billion to blue/green

• Sugar reforms strip €3.5 billion from amber box, and add €1.3 billion to blue/green (EU15 income support)

• Rice, fruit and vegetables…..

Commitments on blue and amber boxes:

• EU will make the biggest AMS cuts under the tiered formula – could afford up to 70%

• Blue box limited to 5% of value of agricultural production– achievable, provided most of the Single Payment is in

the green box

• Overall limit on all trade-distorting support (80% of base entitlement): achievable for EU15

• Product specific AMS limits

Source: Kutas, G. EU Negotiating Room in Domestic Support after the 2003 CAP Reform and Enlargement

Source: Kutas, G. EU Negotiating Room in Domestic Support after the 2003 CAP Reform and Enlargement

Source: Kutas, G. EU Negotiating Room in Domestic Support after the 2003 CAP Reform and Enlargement

Does the Single Payment fit in the green box?

• Restrictions on fruit and vegetables: see Upland Cotton

• Annex 2, 6(d): ‘The amount of such payments in any given year shall not be related to, or based on, the factors of production employed in any year after the base period’– But an annual claim on farmland in agricultural

production or kept in good environmental condition

Future challenges for Irish agriculture

Premia and arable aid

Market returns

Rural development payments

0

500

1000

1500

2000

2500

Premia and arable aid

€ m

illi

on

Decoupling

WTO reduced protection

Rural development