Embed Size (px)

Citation preview

The evolving political, economic and business landscape

12 March 2019

Citrus Growers Association

What we will be covering today…?

1. SA Political Outlook…

2. SA Economic Outlook…

3. How Global Business is evolving…

4. How Standard Bank is evolving…

What we will be covering today…?

2

1. Pres. Rampahosa replaced Jacob Zuma as state leader in February 2018.

2. Signals of future accountability.

3. New boards at State Owned Enterprises.

4. No further ratings downgrades.

5. Nuclear plans shelved, and signed a ZAR56bn contract with 27 independent renewable energy power producers.

6. Economic stimulus and recovery plan announced, together with USD100bn investment target.

7. Wide changes across State Security and Police structures.

Stage one: stabilisation of the institutions most harmed

during the Zuma era

3

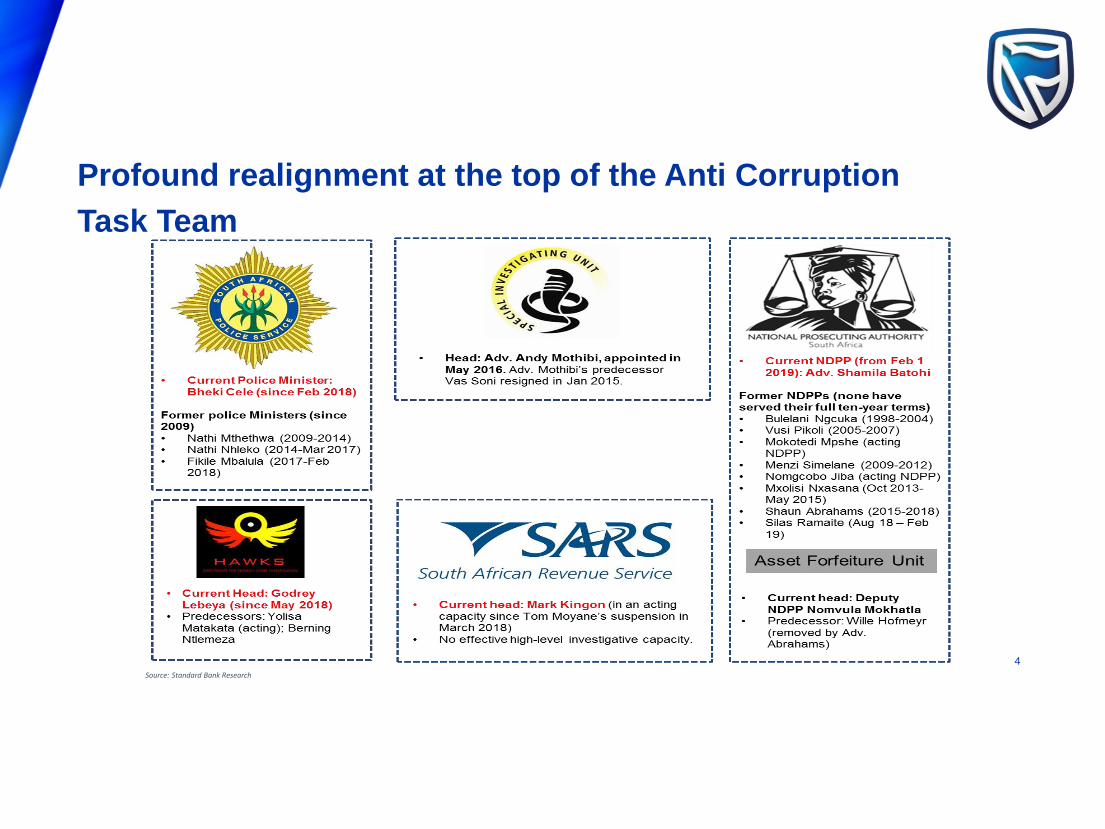

Source: Standard Bank Research

Profound realignment at the top of the Anti Corruption

Task Team

4

Percent

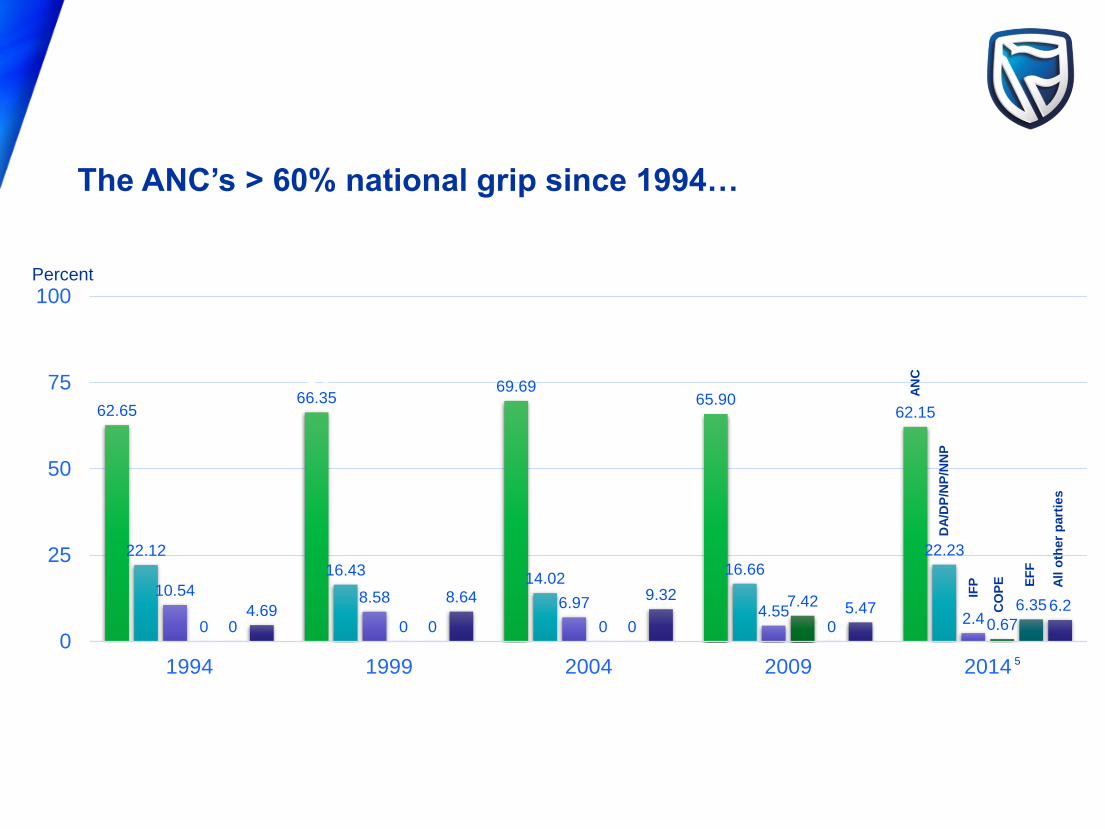

62.6566.35

69.6965.90

62.15

22.12

16.4314.02

16.66

22.23

10.54 8.58 6.974.55 2.4

0 0 0

7.42

0.670 0 0 0

6.354.698.64 9.32

5.47 6.2

0

25

50

75

100

1994 1999 2004 2009 2014

AN

C

DA

/DP

/NP

/NN

P

IFP

CO

PE EF

F

All o

ther

part

ies

The ANC’s > 60% national grip since 1994…

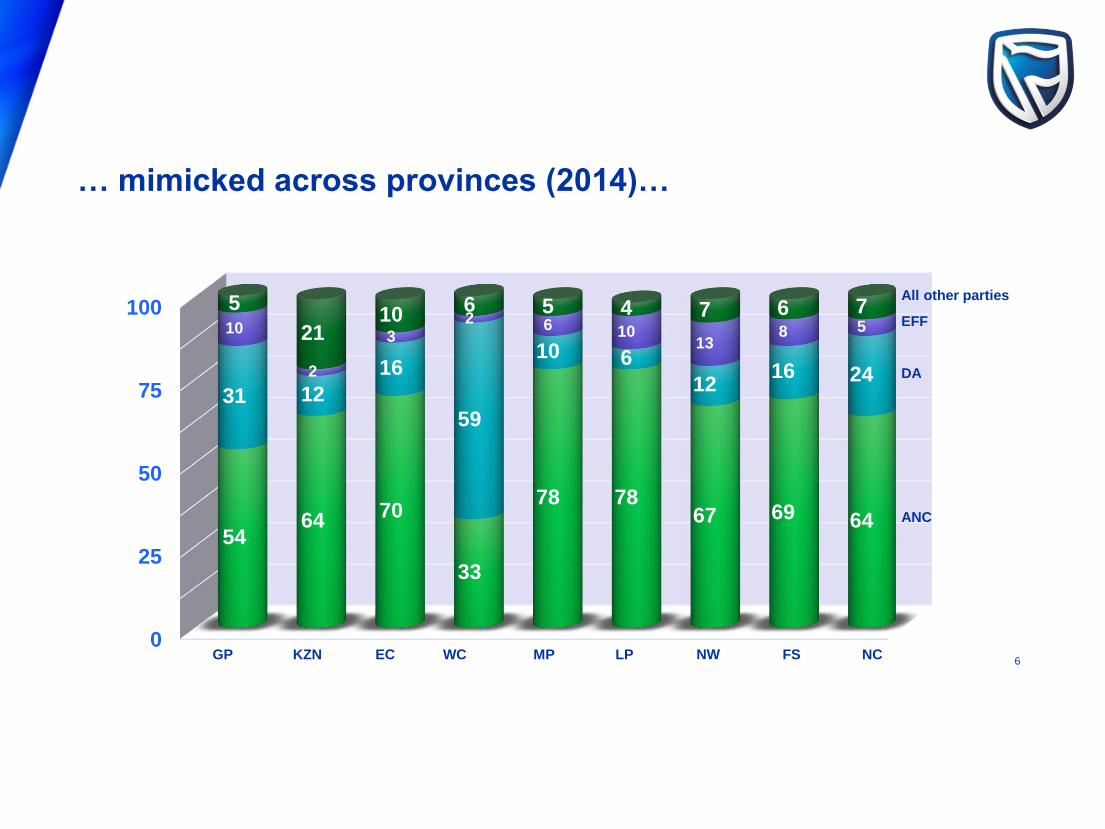

5

0

25

50

75

100

5464 70

33

78 7867 69 64

31 12

16

59

10 6

1216 24

10

2

32 6 10

138 5

5

2110 6 5 4 7 6 7

ANC

GP KZN EC

DA

EFF

All other parties

WC MP LP NW FS NC

… mimicked across provinces (2014)…

6

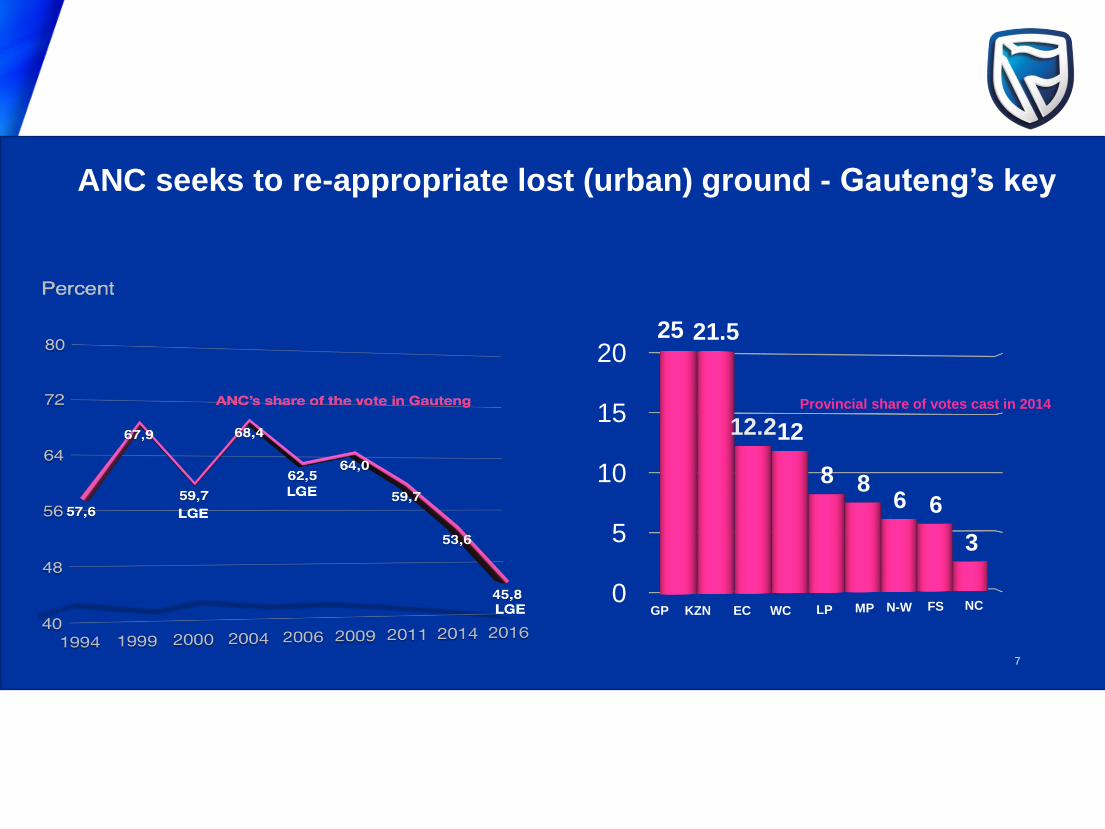

Percent

0

5

10

15

2025 21.5

12.212

8 86 6

3

GP KZN EC WC LP MP N-W FS NC

Provincial share of votes cast in 2014

ANC seeks to re-appropriate lost (urban) ground - Gauteng’s key

7

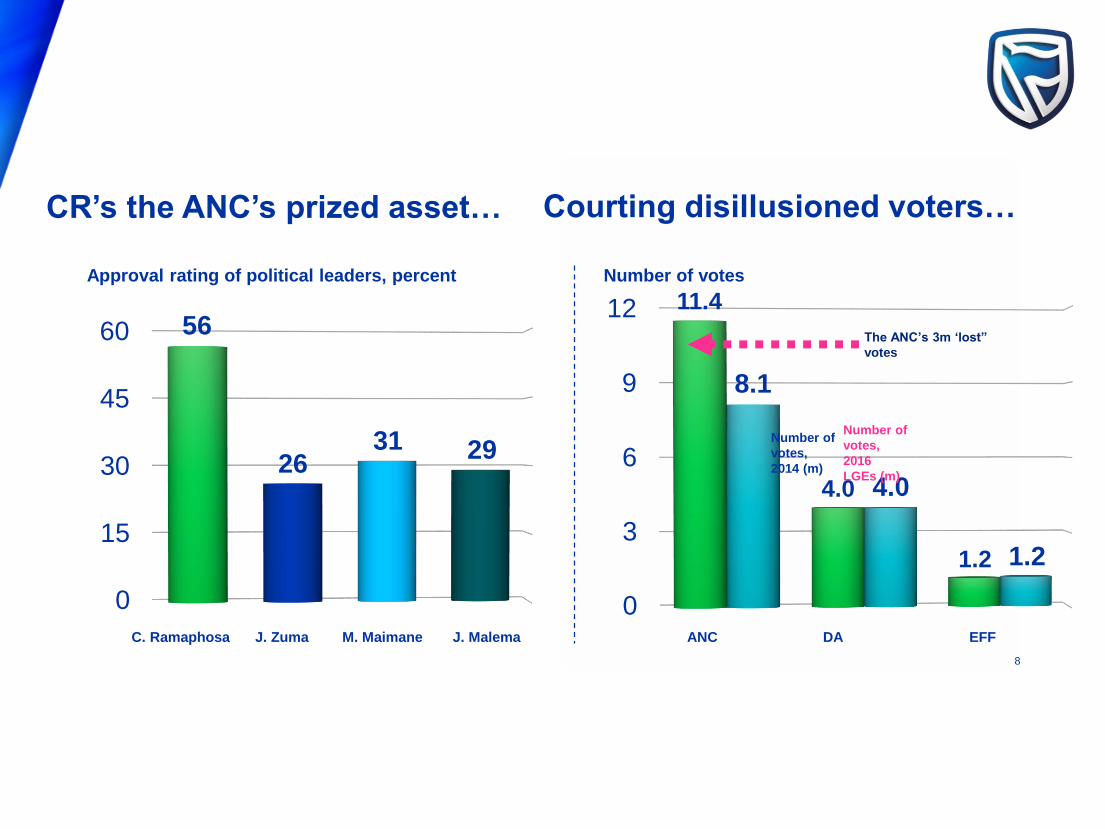

Approval rating of political leaders, percent Number of votes

0

15

30

45

60 56

2631 29

J. Zuma M. MaimaneC. Ramaphosa J. Malema

0

3

6

9

12 11.4

4.0

1.2

8.1

4.0

1.2

Number of

votes,

2016

LGEs (m)

Number of

votes,

2014 (m)

DA EFFANC

The ANC’s 3m ‘lost”

votes

CR’s the ANC’s prized asset… Courting disillusioned voters…

8

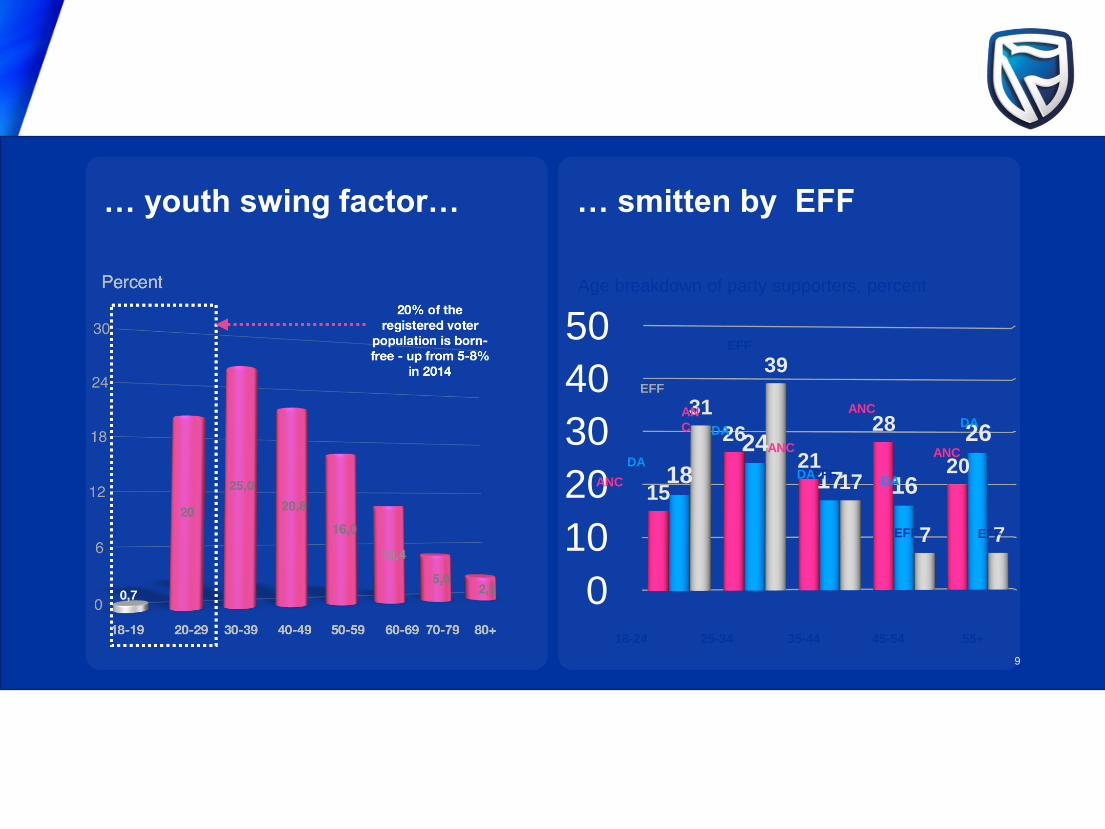

… youth swing factor… … smitten by EFF

Age breakdown of party supporters, percent

0

10

20

30

40

50

15

26

21

28

2018

24

17 16

2631

39

17

7 7

18-24 25-34 35-44 45-54 55+

EFF

DAANC

EFF

DA

ANC

EFFDA

AN

C

EFF

DAANC

EFF

DAANC

9

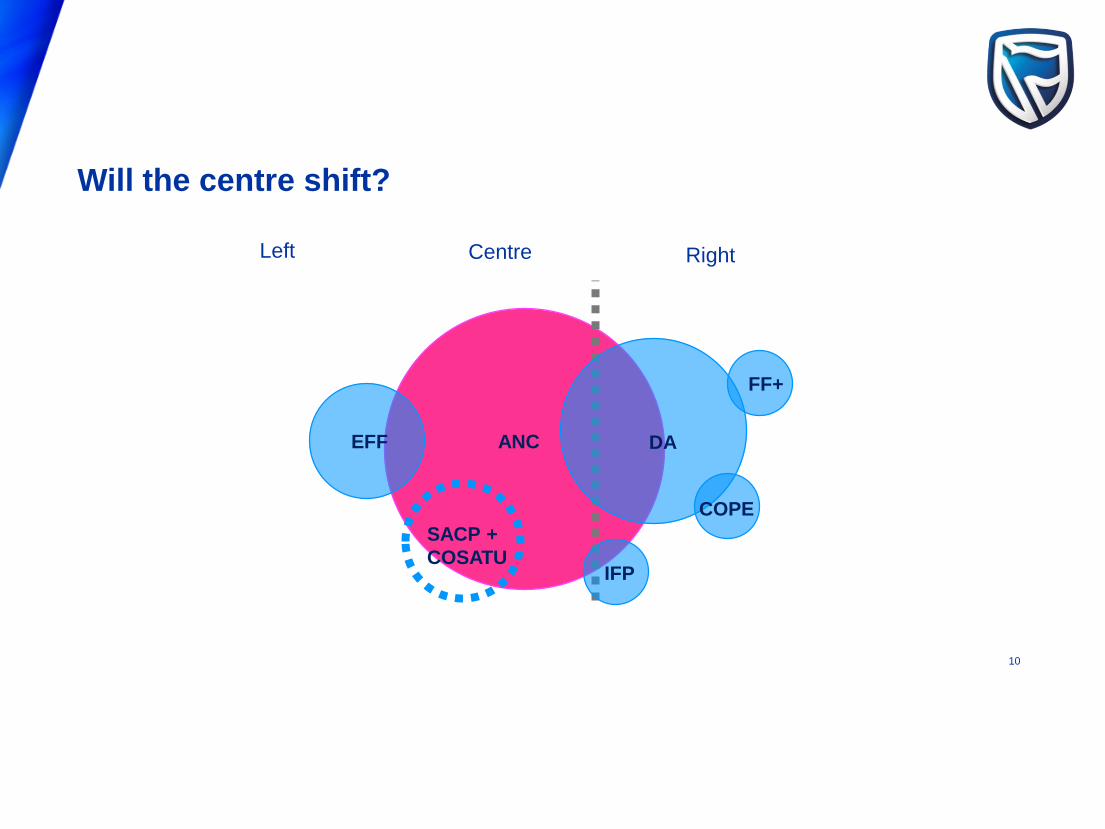

Left RightCentre

ANC

SACP +

COSATU

EFF

FF+

COPE

IFP

DA

Will the centre shift?

10

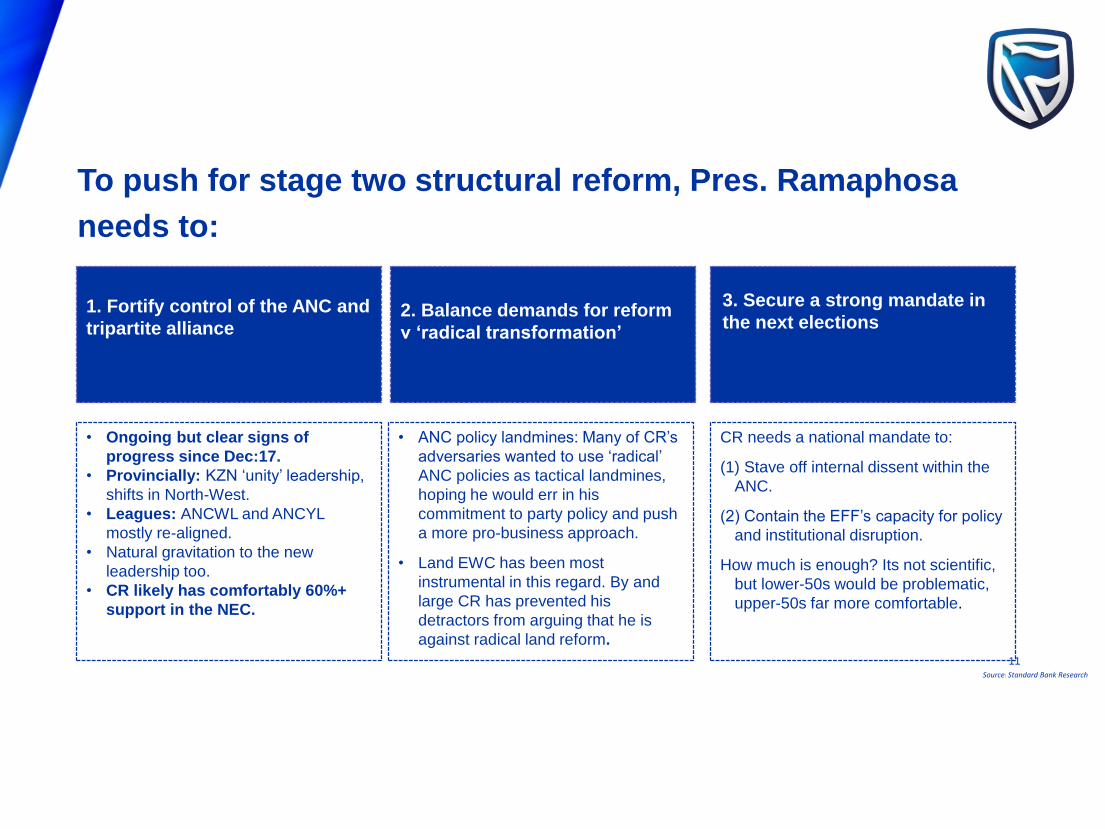

1. Fortify control of the ANC and

tripartite alliance 2. Balance demands for reform

v ‘radical transformation’

3. Secure a strong mandate in

the next elections

• Ongoing but clear signs of

progress since Dec:17.

• Provincially: KZN ‘unity’ leadership,

shifts in North-West.

• Leagues: ANCWL and ANCYL

mostly re-aligned.

• Natural gravitation to the new

leadership too.

• CR likely has comfortably 60%+

support in the NEC.

• ANC policy landmines: Many of CR’s

adversaries wanted to use ‘radical’

ANC policies as tactical landmines,

hoping he would err in his

commitment to party policy and push

a more pro-business approach.

• Land EWC has been most

instrumental in this regard. By and

large CR has prevented his

detractors from arguing that he is

against radical land reform.

CR needs a national mandate to:

(1) Stave off internal dissent within the

ANC.

(2) Contain the EFF’s capacity for policy

and institutional disruption.

How much is enough? Its not scientific,

but lower-50s would be problematic,

upper-50s far more comfortable.

Source: Standard Bank Research

To push for stage two structural reform, Pres. Ramaphosa

needs to:

11

If CR’s grip on the

ANC weakens…

… if the economy

does not expand,

and transform…

… but if CR

succeeds, the

political economy

can re-centre

12

SA Economic Outlook

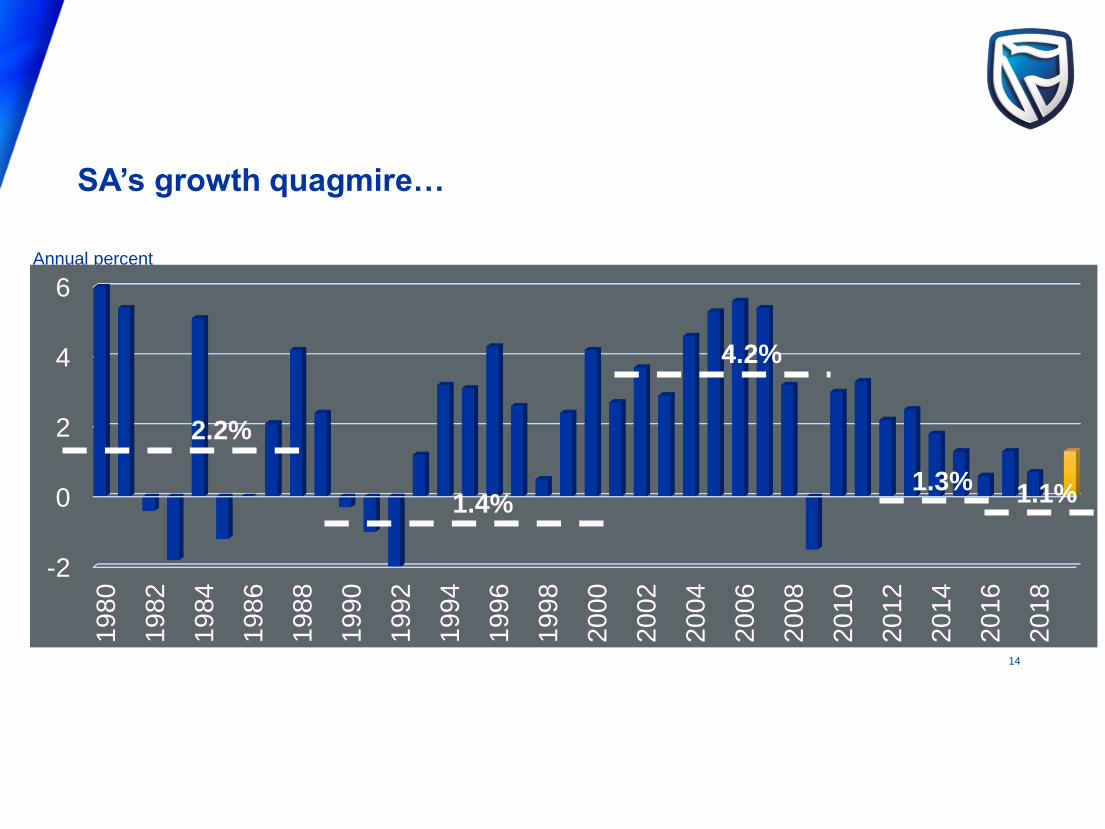

13

Annual percent

-2

0

2

4

6

19

80

19

82

19

84

1986

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

20

12

20

14

20

16

20

18

2.2%

1.4%

4.2%

1.3% 1.1%

SA’s growth quagmire…

14

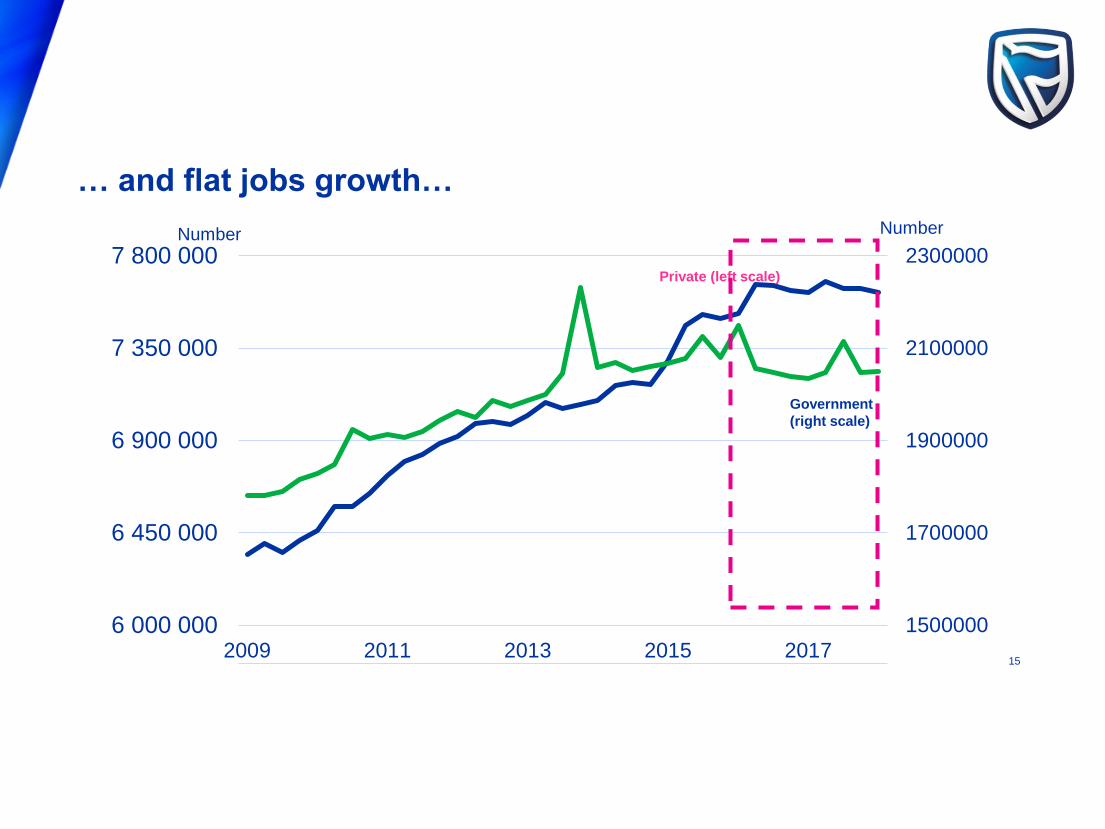

Number

1500000

1700000

1900000

2100000

2300000

6 000 000

6 450 000

6 900 000

7 350 000

7 800 000

2009 2011 2013 2015 2017

Government

(right scale)

Private (left scale)

Number

… and flat jobs growth…

15

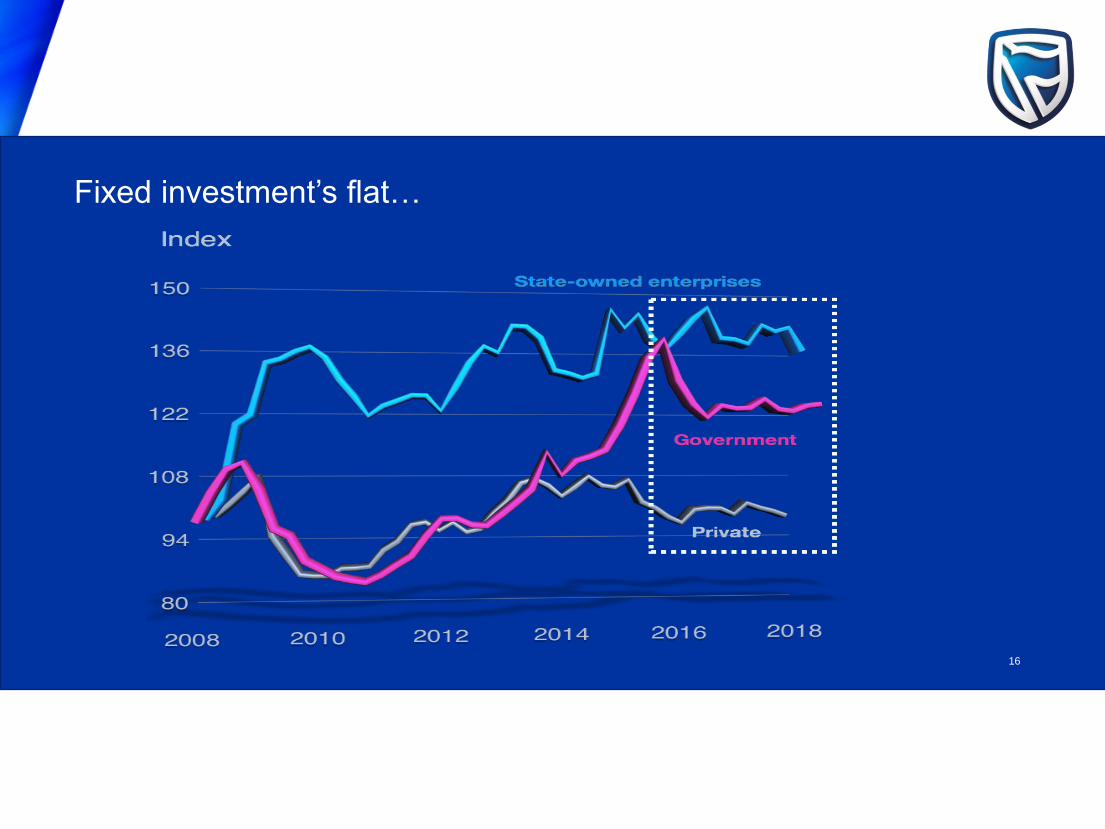

Fixed investment’s flat…

16

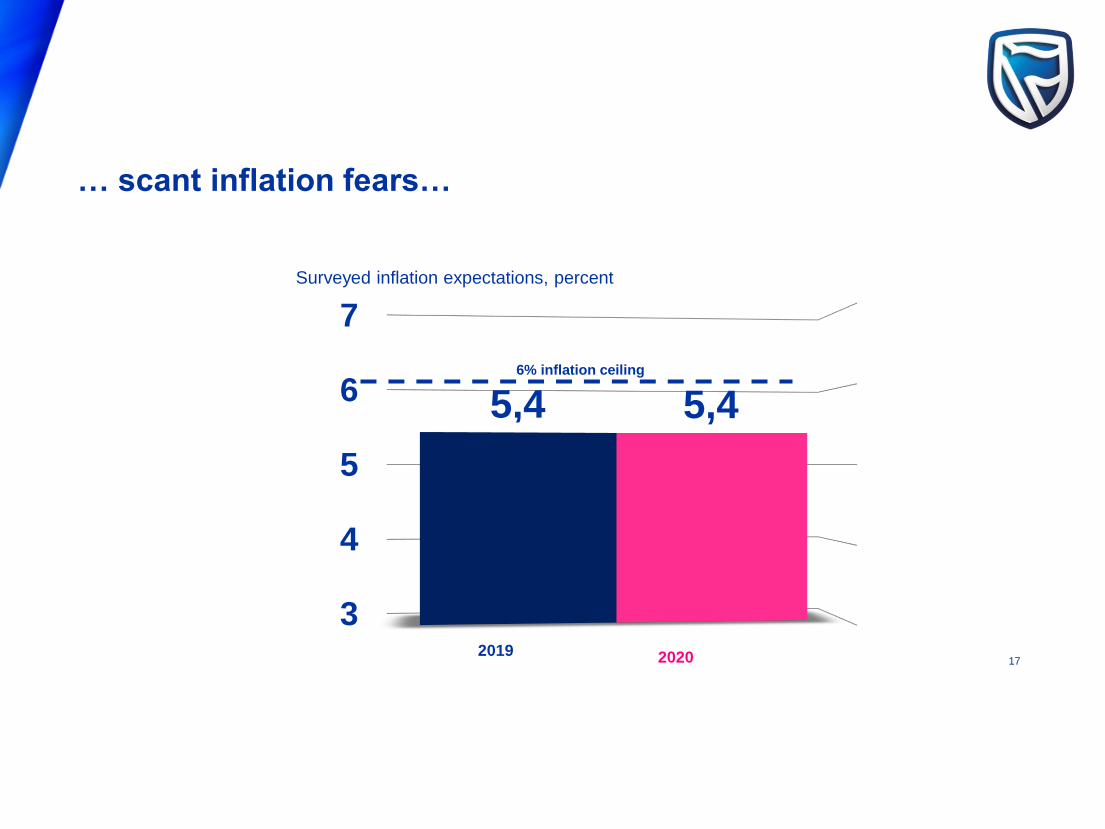

Surveyed inflation expectations, percent

3

4

5

6

7

5,4 5,4

20202019

6% inflation ceiling

… scant inflation fears…

17

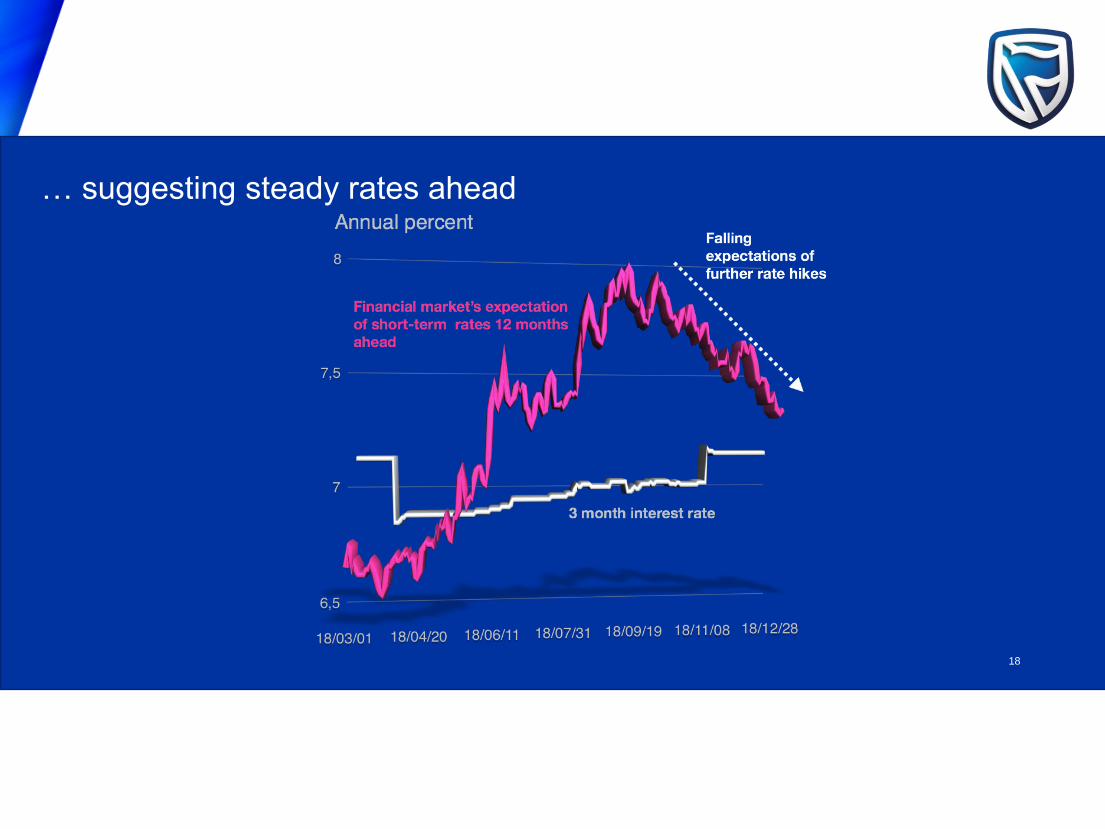

… suggesting steady rates ahead

18

0

14

28

42

56

70

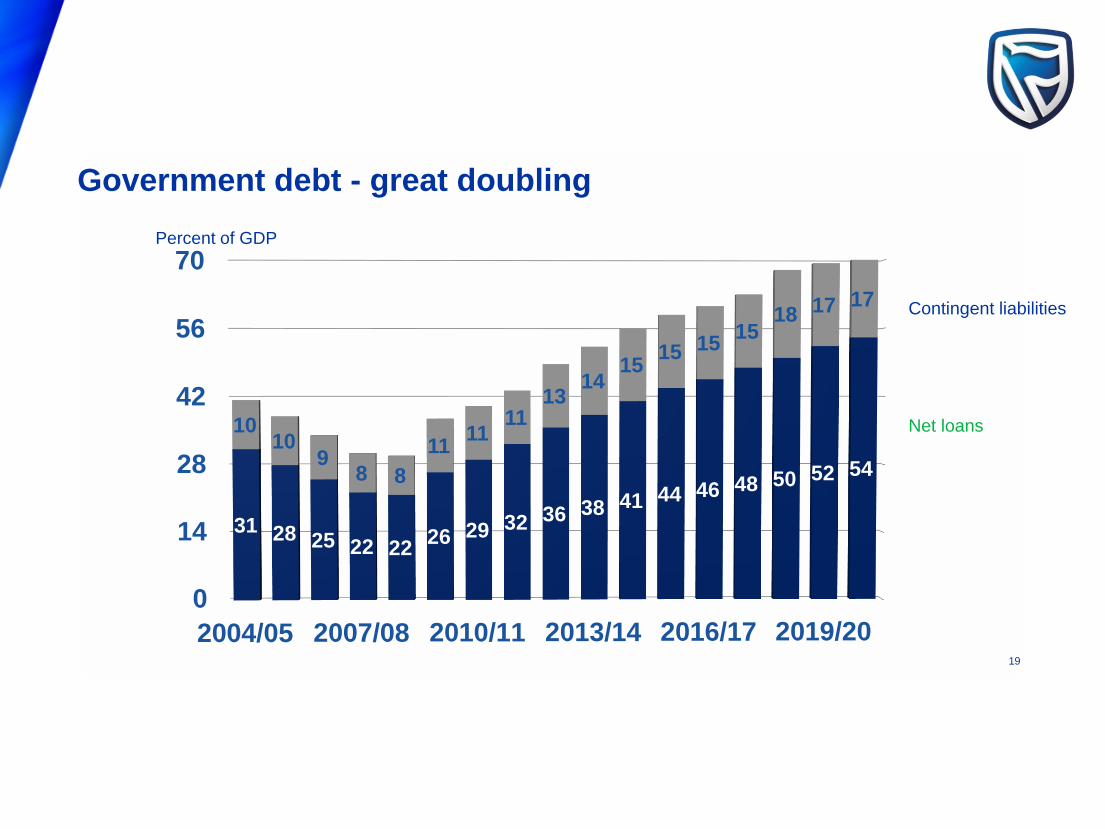

2004/05 2007/08 2010/11 2013/14 2016/17 2019/20

31 28 25 22 2226 29 32 36 38 41 44 46 48 50 52 54

1010

98 8

1111

1113

1415

15 1515

18 17 17

Percent of GDP

Contingent liabilities

Net loans

Government debt - great doubling

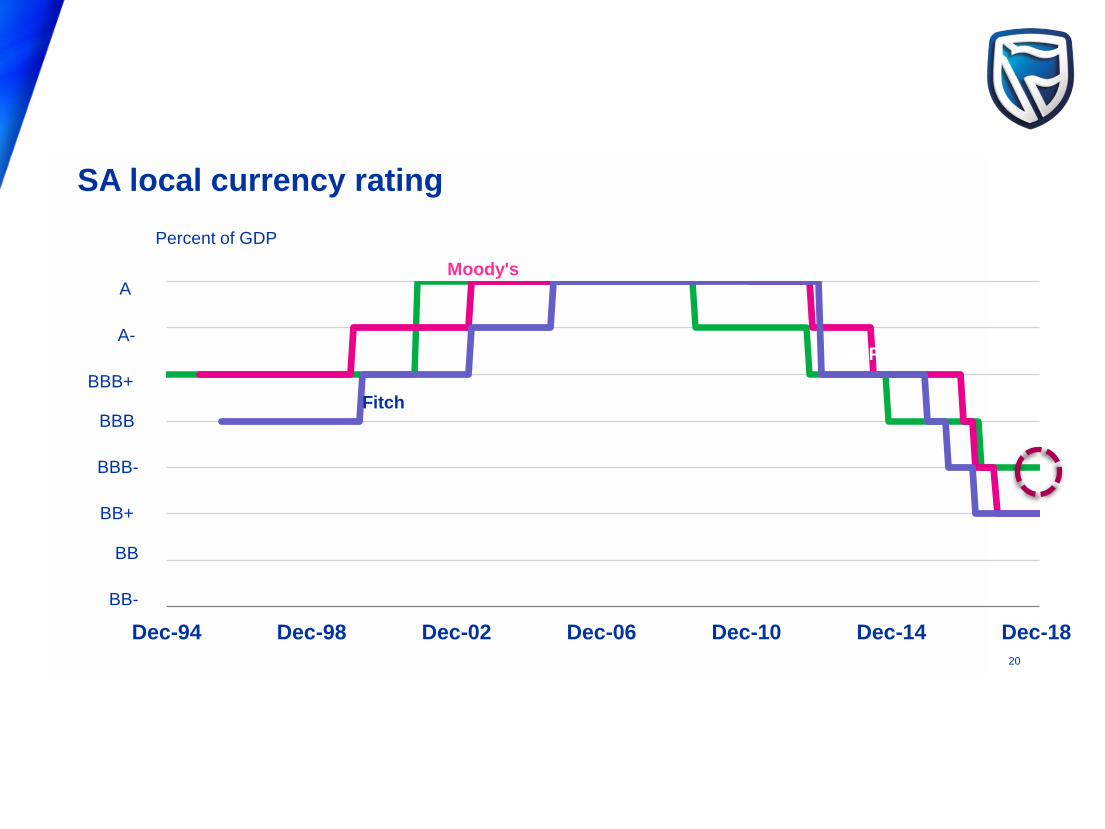

19

Dec-94 Dec-98 Dec-02 Dec-06 Dec-10 Dec-14 Dec-18

Percent of GDP

S&P

Moody's

Fitch

BB

BB+

BBB-

BBB

BBB+

A-

A

BB-

SA local currency rating

20

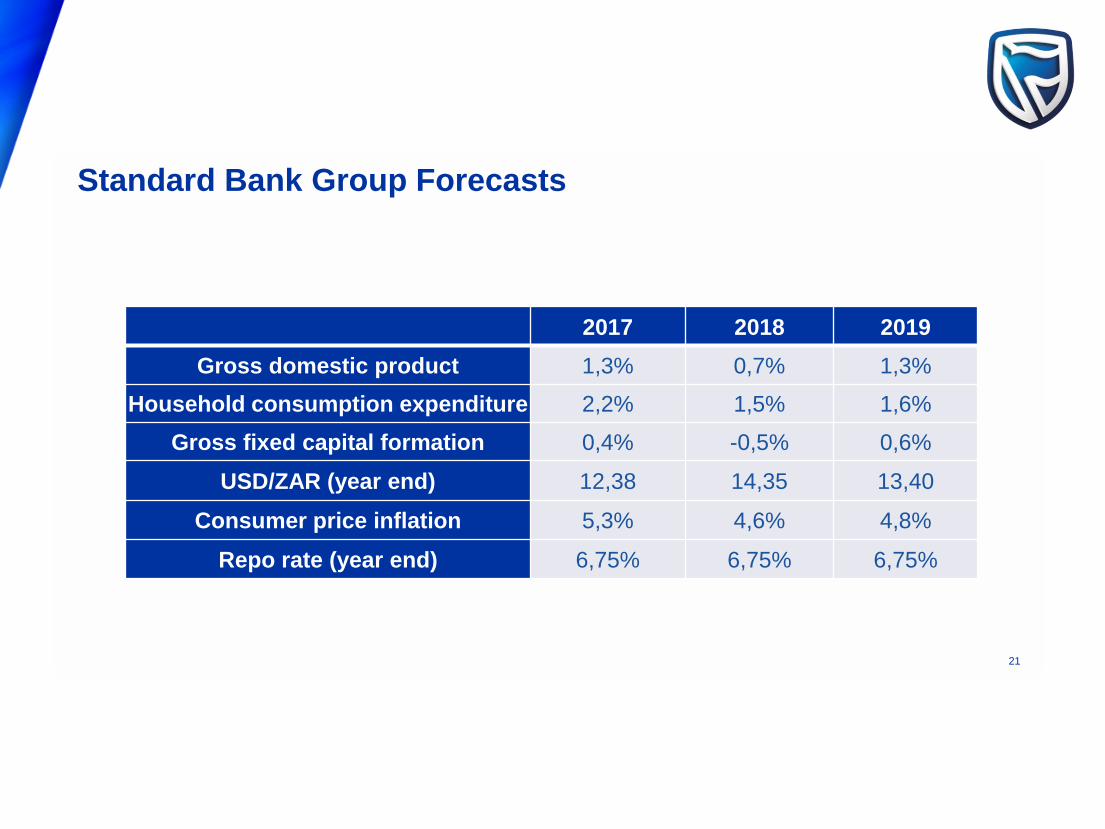

2017 2018 2019

Gross domestic product 1,3% 0,7% 1,3%

Household consumption expenditure 2,2% 1,5% 1,6%

Gross fixed capital formation 0,4% -0,5% 0,6%

USD/ZAR (year end) 12,38 14,35 13,40

Consumer price inflation 5,3% 4,6% 4,8%

Repo rate (year end) 6,75% 6,75% 6,75%

Standard Bank Group Forecasts

21

• IMF projects 2019 global growth slowing to 3,5% for 2019; from 3,7% in 2018.

• Slowing US economy off the back of reduced stimulus and delayed effect of tightening monetary

policy.

• Chinese economy slowing and impact of trade wars.

• Eurozone anticipating slower growth.

• Brexit remains a huge unknown…

• Overall growth economic backdrop remains worrying, with greater risk to global growth deceleration

– which would adversely impact SA as a commodity exporter…

Global growth concerns to add to SA uncertainty

22

HOW BUSINESS IS EVOLVING…

23

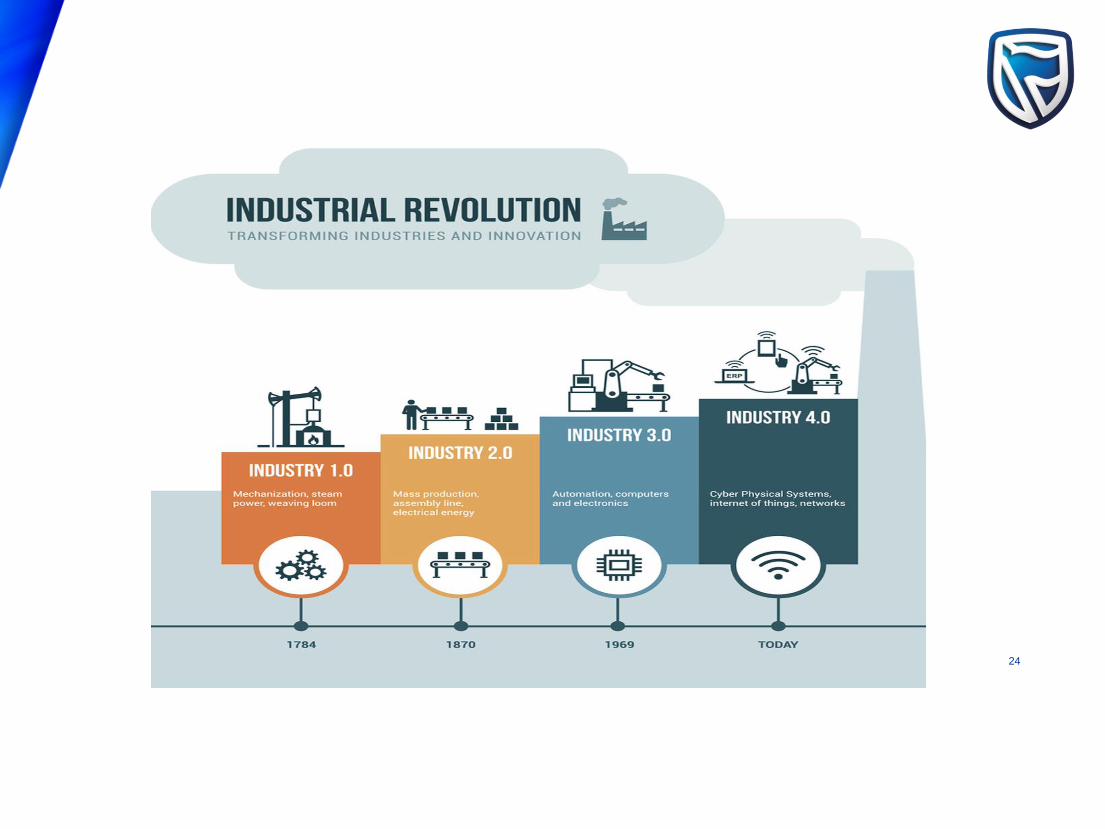

Image Place Holder

24

The rise and rise of dominant Digital giants

THE LARGEST COMPANIES BY MARKET CAPITALISATION

SOURCE: HTTP://WWW.VISUALCAPITALIST.COM/CHART-LARGEST-COMPANIES-MARKET-CAP-15-YEARS/\

25

Megatrends driving the Digital Revolution

Mature WWW

Software as a Service

Ubiquitous Smart Mobile Devices

Internet of Things26

Megatrends driving the Digital Revolution

Artificial Intelligence

Cloud

Data Analytics

Social Media27

HOW STANDARD BANK IS EVOLVING…

28

• Core Banking replacements

• Process Automation

• Online everything

• Automated Decisioning

• Biometric Authentication

• Data Analytics

• Personalisation

*120*2345#

Harnessing the power of Technology to improve customer

experience and inclusivity…..

29

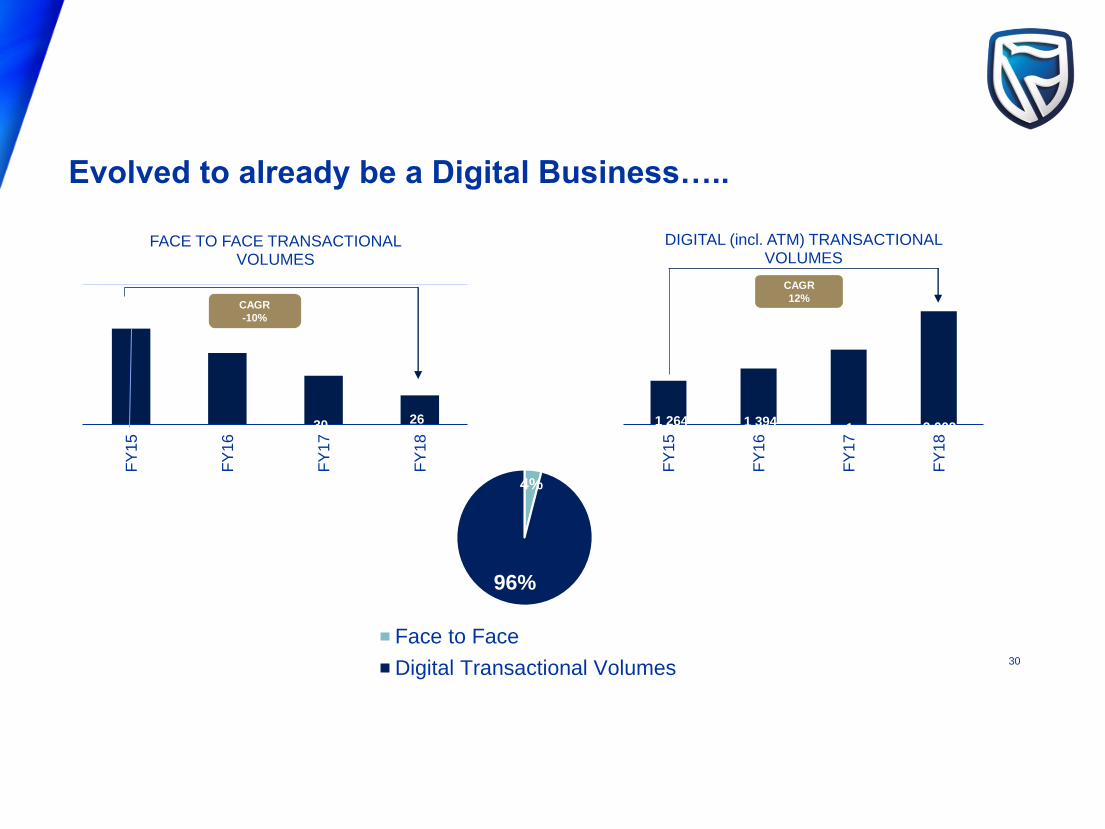

Evolved to already be a Digital Business…..

41 35 30 26

FY

15

FY

16

FY

17

FY

18

FACE TO FACE TRANSACTIONAL VOLUMES

CAGR

-10%

1 264 1 394 1 … 2 002

FY

15

FY

16

FY

17

FY

18

DIGITAL (incl. ATM) TRANSACTIONAL VOLUMES

CAGR

12%

4%

96%

Face to Face

Digital Transactional Volumes30

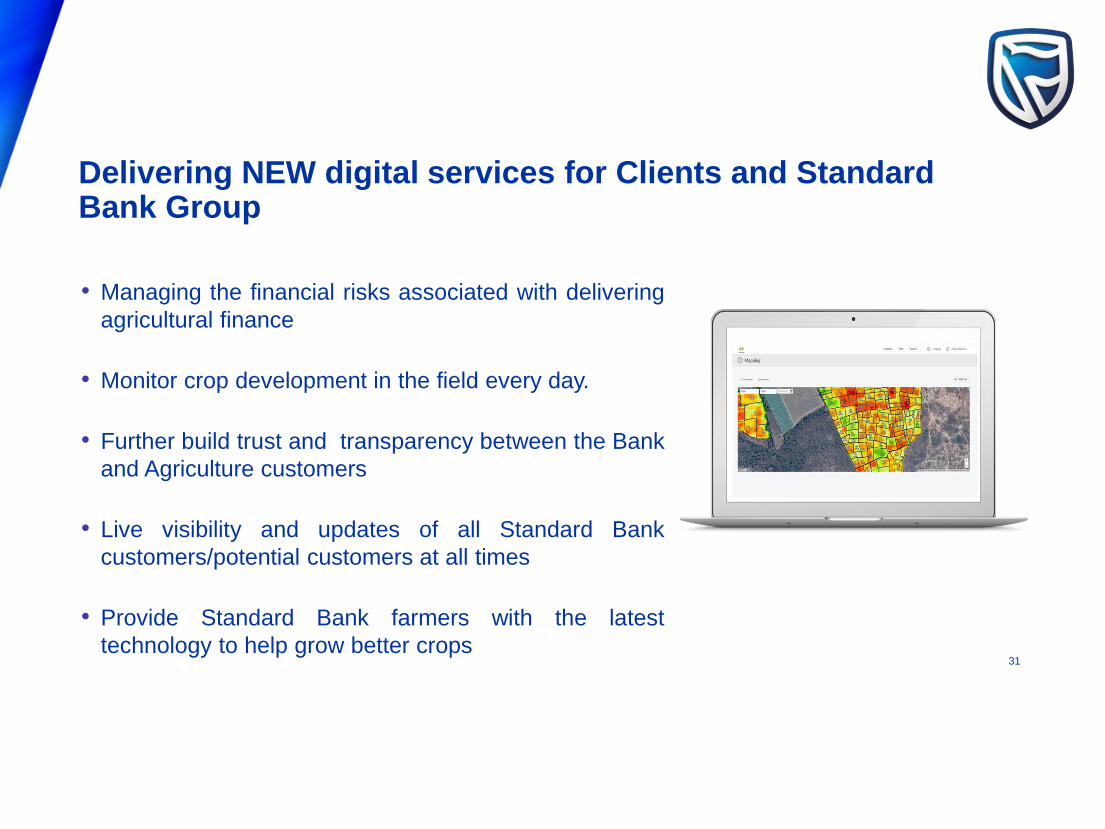

• Managing the financial risks associated with delivering

agricultural finance

• Monitor crop development in the field every day.

• Further build trust and transparency between the Bank

and Agriculture customers

• Live visibility and updates of all Standard Bank

customers/potential customers at all times

• Provide Standard Bank farmers with the latest

technology to help grow better crops

Delivering NEW digital services for Clients and Standard Bank Group

31

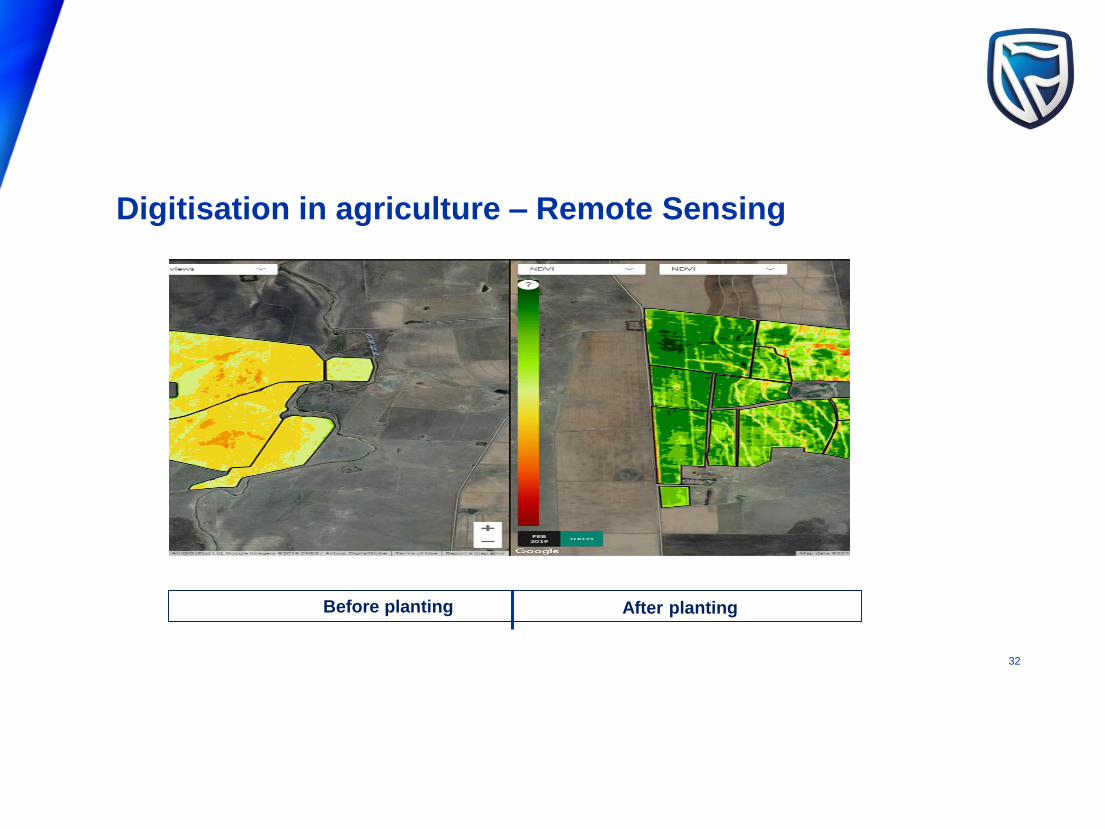

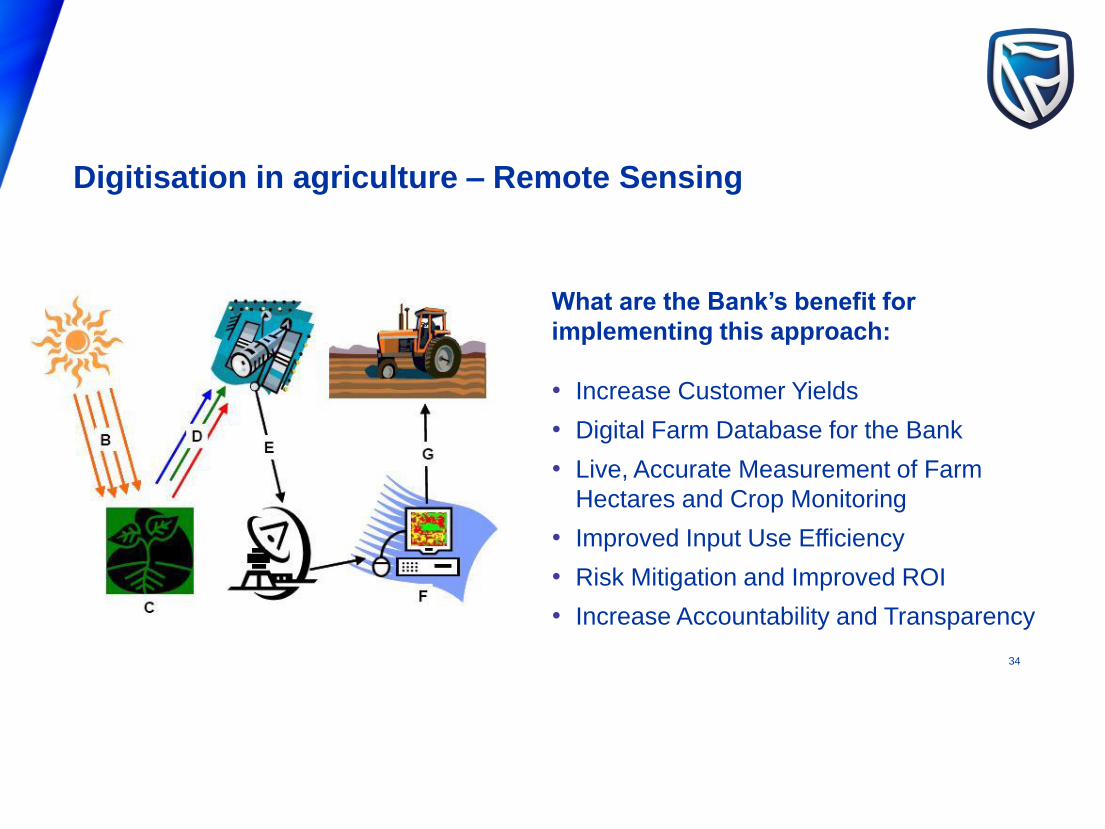

Digitisation in agriculture – Remote Sensing

After plantingBefore planting

32

Remote sensing from far and close…..

33

Digitisation in agriculture – Remote Sensing

What are the Bank’s benefit for

implementing this approach:

• Increase Customer Yields

• Digital Farm Database for the Bank

• Live, Accurate Measurement of Farm

Hectares and Crop Monitoring

• Improved Input Use Efficiency

• Risk Mitigation and Improved ROI

• Increase Accountability and Transparency

34

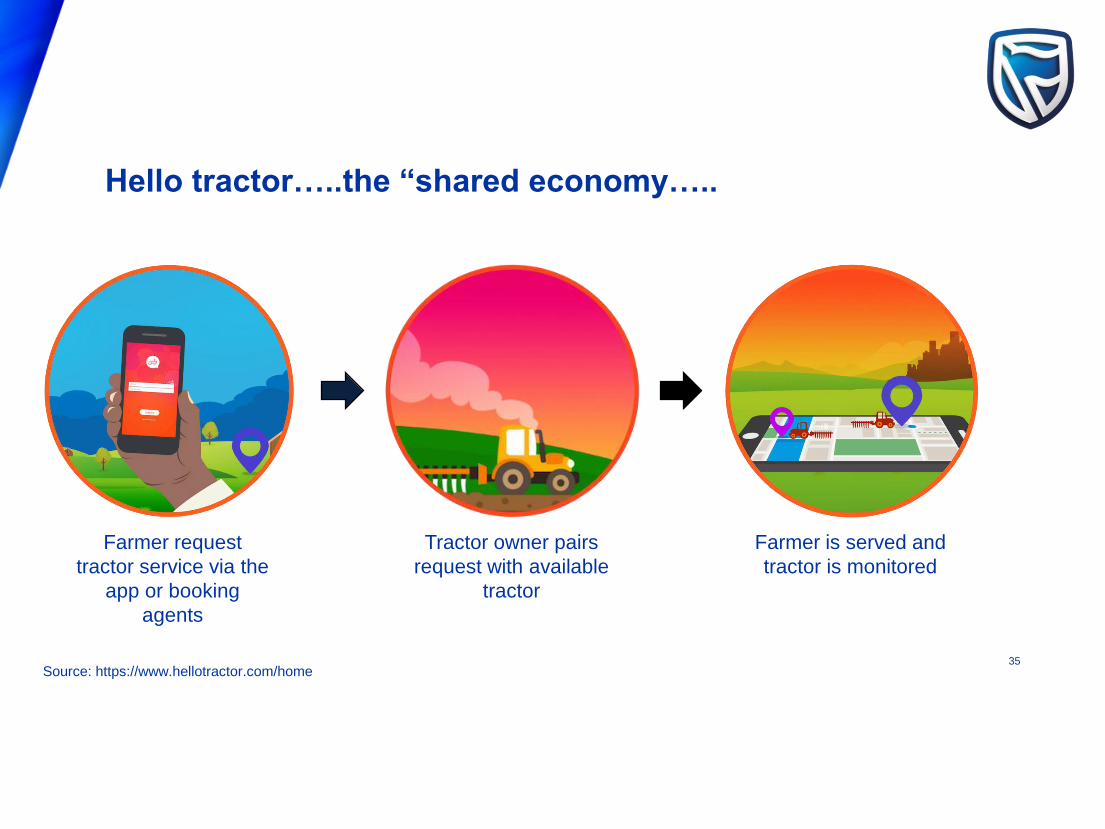

Hello tractor…..the “shared economy…..

Farmer request

tractor service via the

app or booking

agents

Tractor owner pairs

request with available

tractor

Farmer is served and

tractor is monitored

Source: https://www.hellotractor.com/home35

Learn more about new markets

and easily research any industry in

any country

Explore new markets

Curated 200000 pages of content

on trade in 190 countries

Standard Bank Trade Club will help businesses grow

Connect with trusted suppliers

and clients

Meet new local and international

businesses by responding to

opportunities, through introductions

suggested by our artificial intelligence

matching engine, the community

manager or at events

Join us now! tradeclub@standardb

ank.co.za

First 25 businesses

who apply and bank

with Standard Bank

will be granted

“Friends Of The

Programme” status

and be given the

opportunity to find

you new markets

through our

International Trade

Alliance network.

Receive orders and trade

Option to load your stock and price

lists so that interested importers can

place orders and trade

36

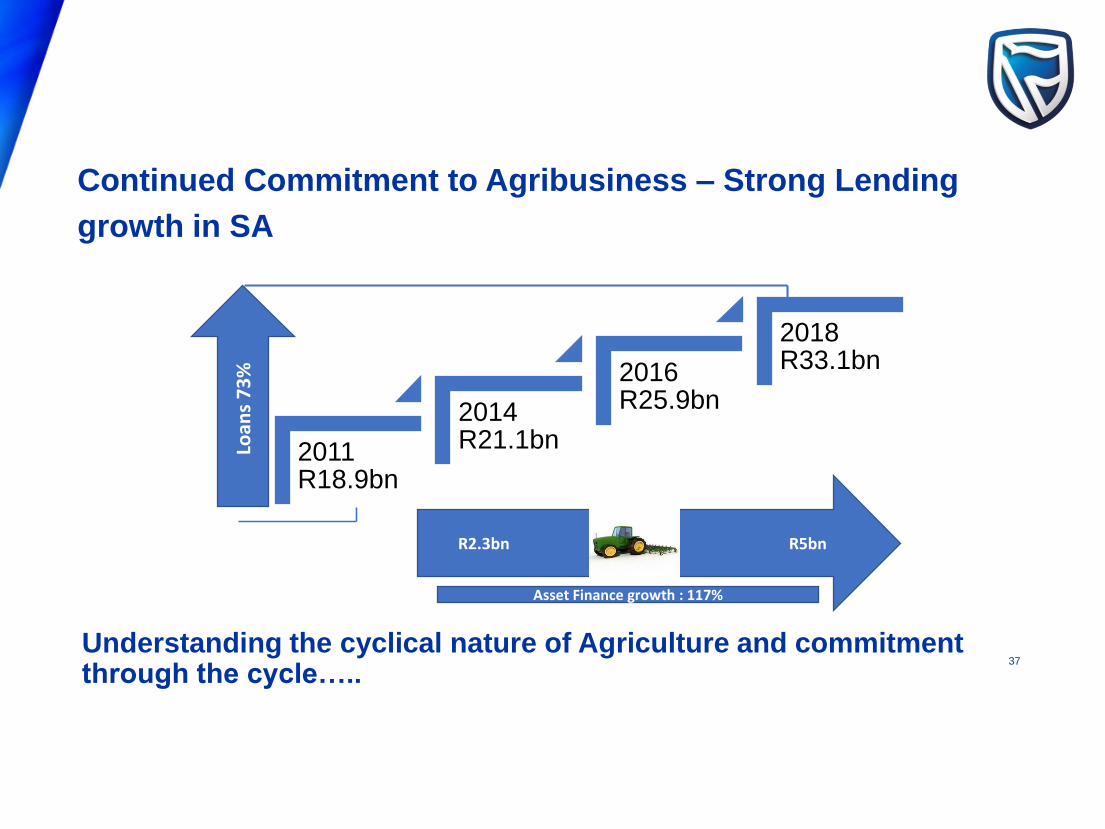

2011 R18.9bn

2014 R21.1bn

2016 R25.9bn

2018 R33.1bn

Loan

s 7

3%

R2.3bn R5bn

Asset Finance growth : 117%

Understanding the cyclical nature of Agriculture and commitment through the cycle…..

Continued Commitment to Agribusiness – Strong Lending

growth in SA

37

38

Building name Street number Street Name City 0000 / PO Box 00000 City Name 0000 Country Name

Tel +00 (0)00 000 0000 Fax +00 (0)00 000 0000 / [email protected]

standardbank.com