Embed Size (px)

Citation preview

The Future of the Electric & Gas Industry

Bob Bellemare, P.E.

CEO

Energy Insurance Mutual’s

Risk Managers Information MeetingFebruary 24, 2004

2

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

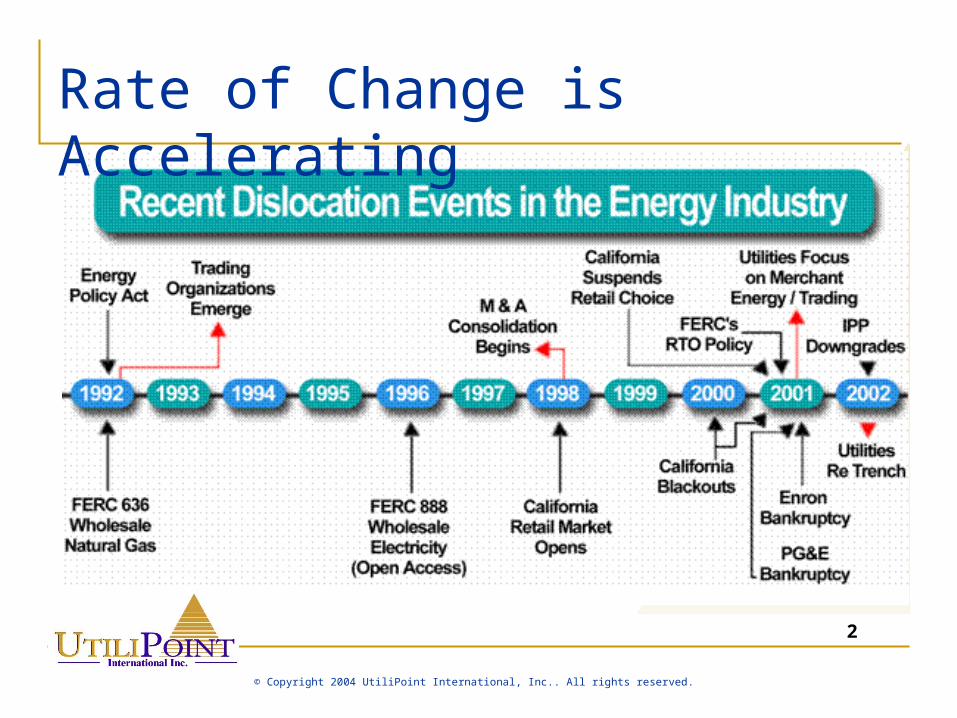

Rate of Change is Accelerating

3

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

Agenda

The Basics Generation/Fuels Wires Corporate & Regulatory New Technologies

Industry Basics

Unique Characteristics

5

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

Characteristics

Real-time product Lack of substitute products Long construction times - over 2 years The laws of physics can not be changed –

electrons are no respecters of political, state, or regulatory boundaries

6

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

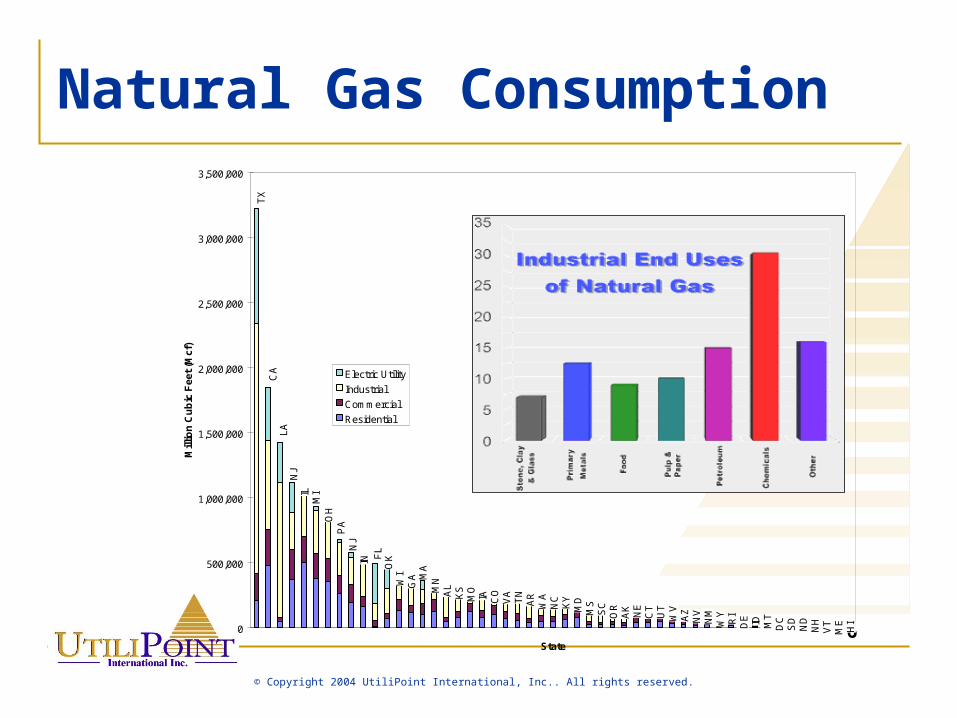

Natural Gas Consumption

IL

OH

IN

WI

GA

MN

AL

KS

MO

IA CO

VA

TN

AR

WA

NC

KY

MD

MS

SC

OR

AK

NE

CT

UT

WV

AZ

NV

NM

WY

RI

DE ID MT

DC

SD

ND

NH

VT

ME

HI

FL

OK

MA

NJ

LA

CA

TX

PA

NJ

MI

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

State

Mill

ion

Cu

bic

Fee

t (M

cf)

Electric Utility

Industrial

Commercial

Residential

7

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

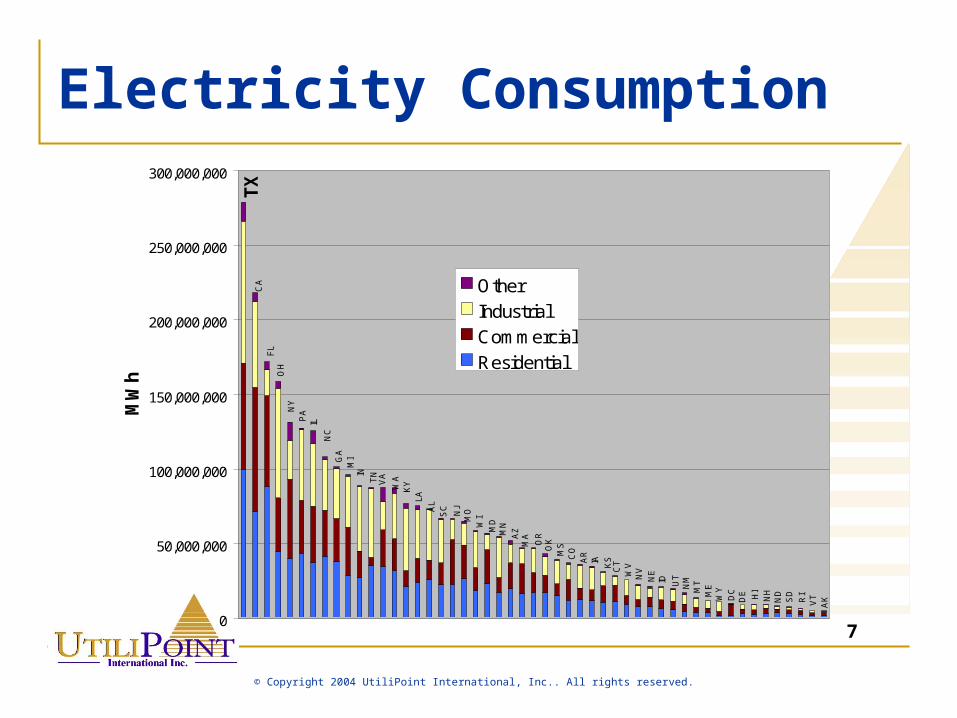

Electricity Consumption

AKVTRI

SD

ND

NHHI

DEDC

WYMEMTNMUTIDNENVW

VCTKSIAA

RCOMSOKO

R

MAA

ZMNMDW

IMONJ

SCA

LLA

WA

KYV

ATNIN

MIG

AN

C

PAN

YO

HF

L

TX

IL

CA

0

50,000,000

100,000,000

150,000,000

200,000,000

250,000,000

300,000,000

MW

h

Other

Industrial

Commercial

Residential

8

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

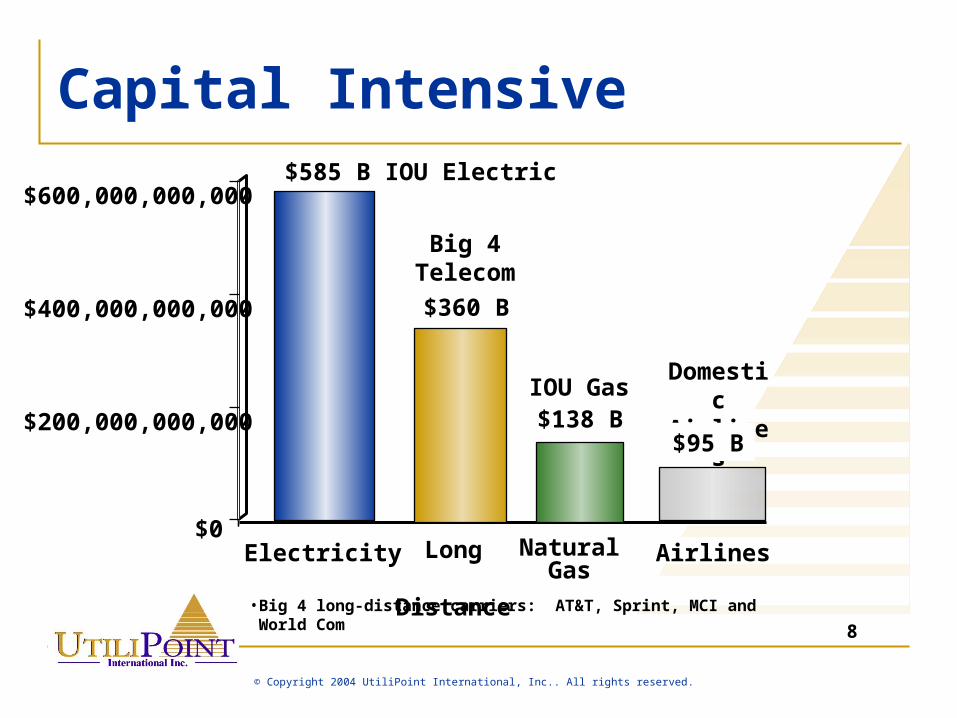

Capital Intensive

•Big 4 long-distance carriers: AT&T, Sprint, MCI and World Com

$200,000,000,000

$400,000,000,000

$600,000,000,000

Electricity Airlines$0

IOU Electric

Domestic

Airlines

$585 B

Long

Distance

Big 4Telecom

$360 B

NaturalGas

IOU Gas$138

B $95 B

9

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

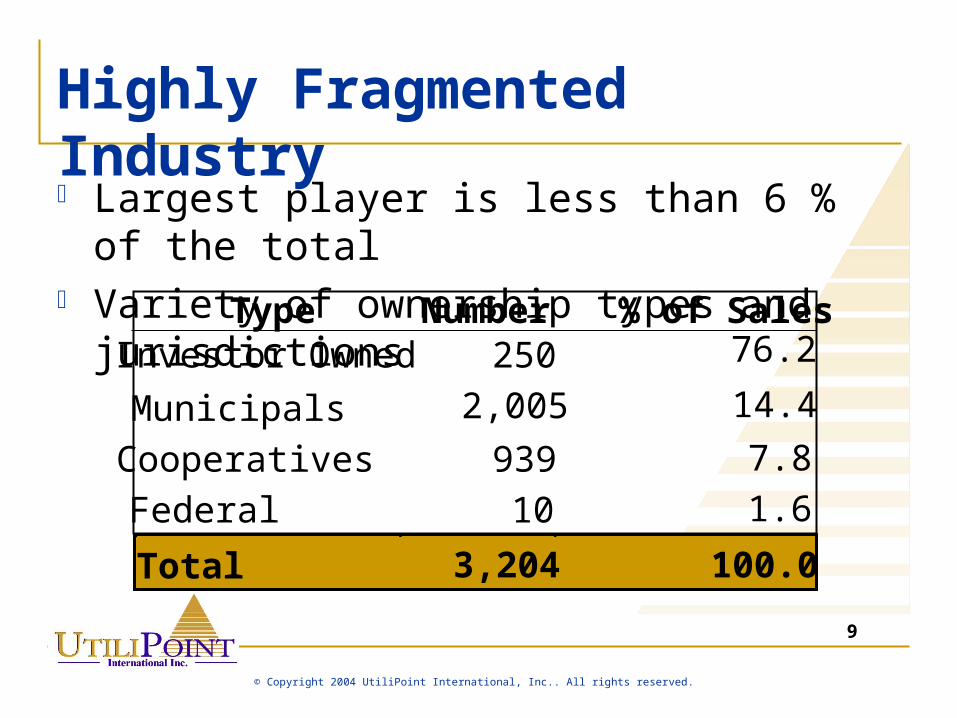

Highly Fragmented Industry Largest player is less than 6 % of the total Variety of ownership types and jurisdictions

Type Number % of SalesInvestor Owned 250

Municipals 2,005

Cooperatives 939

Federal 10

Total 3,204

76.2

14.4

7.8

1.6

100.0

10

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

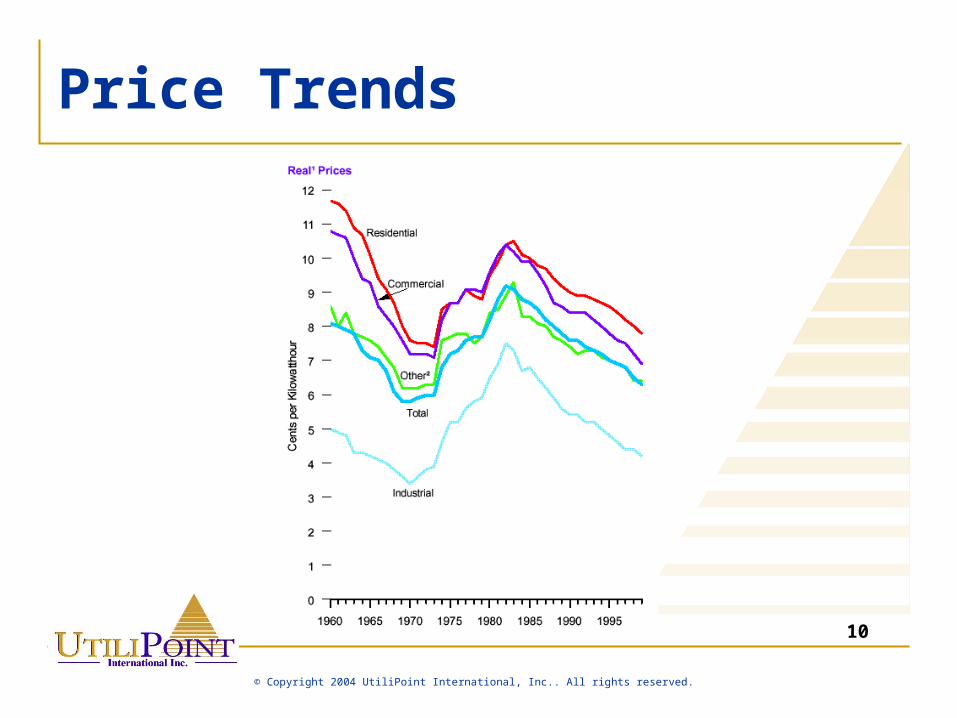

Price Trends

11

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

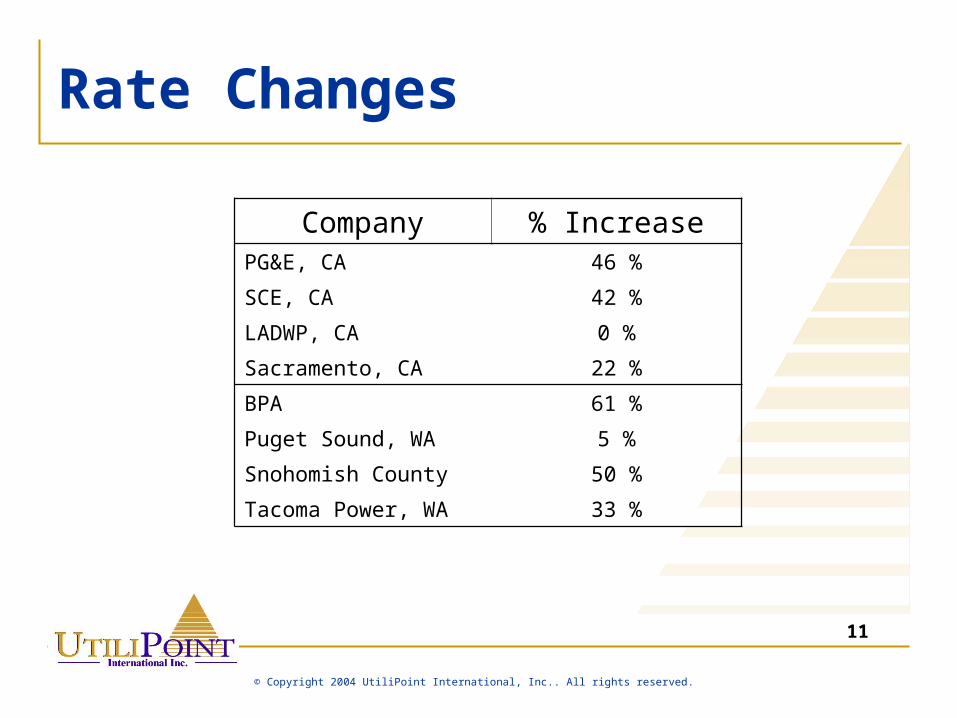

Rate Changes

Company % IncreasePG&E, CA 46 %

SCE, CA 42 %

LADWP, CA 0 %

Sacramento, CA 22 %

BPA 61 %

Puget Sound, WA 5 %

Snohomish County 50 %

Tacoma Power, WA 33 %

12

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

Risk Myth

“This is not a risky business”

GENERATION

History

Fuel

The Future

“After Nearly $5 Billion Loss, TXU Corp. to Concentrate

on Core Texas Business”

“Rising cost of power gives customers a jolt Bonneville”

14

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

19

49

19

52

19

55

19

58

19

61

19

64

19

67

19

70

19

73

19

76

19

79

19

82

19

85

19

88

19

91

19

94

19

97

20

00

20

03

Year

Ca

pa

cit

y (M

W)

Coal Gas Uranium

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

19

49

19

52

19

55

19

58

19

61

19

64

19

67

19

70

19

73

19

76

19

79

19

82

19

85

19

88

19

91

19

94

19

97

20

00

20

03

Year

Ca

pa

cit

y (M

W)

Coal Gas Uranium

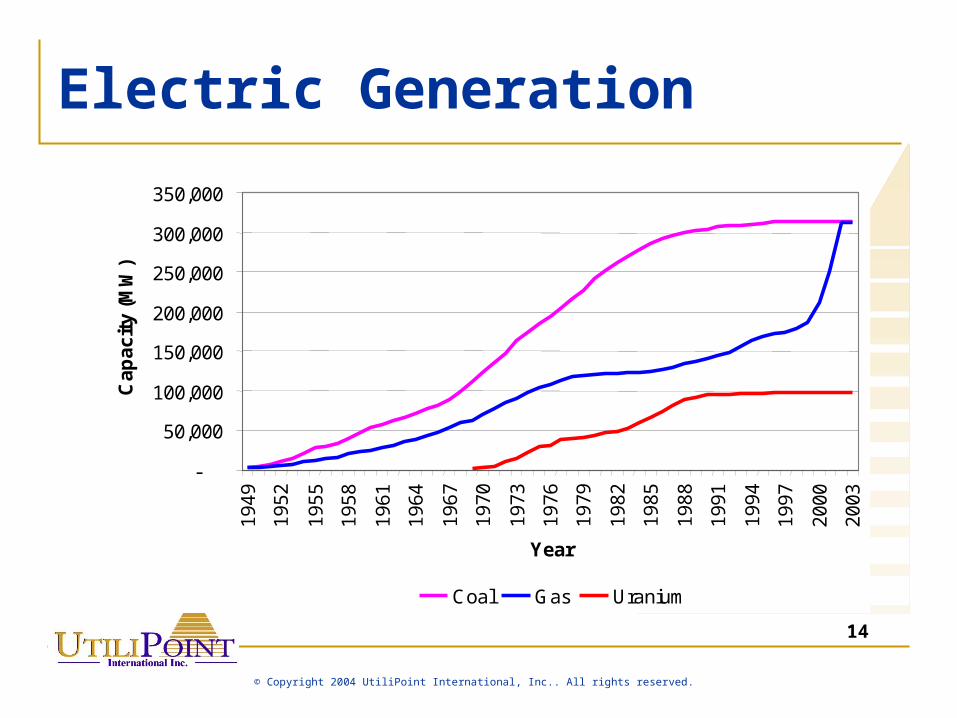

Electric Generation

15

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

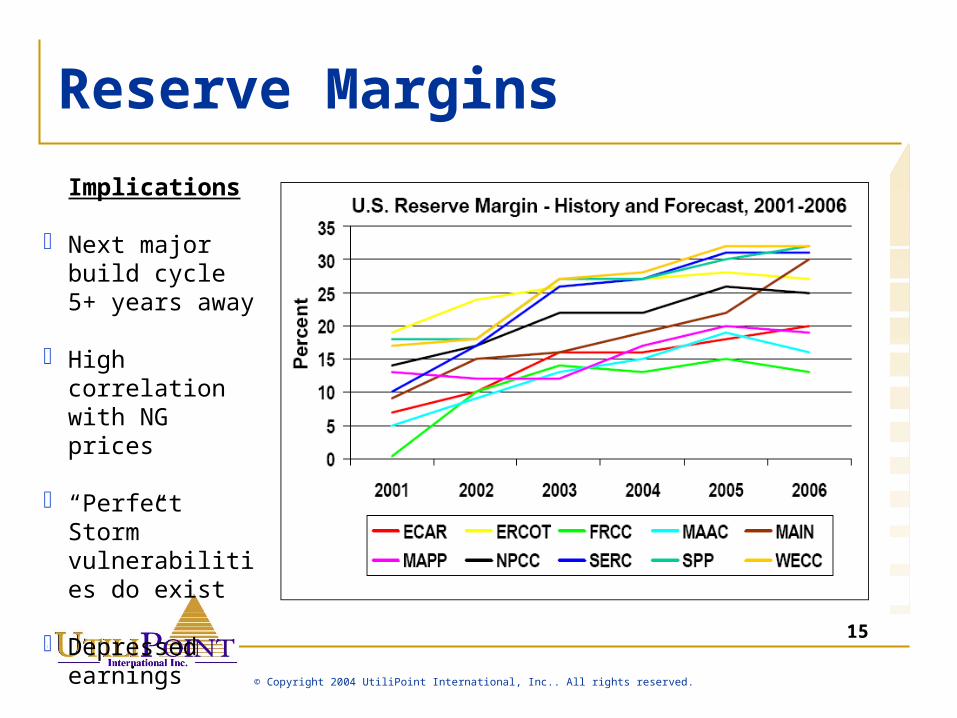

Reserve Margins

Implications

Next major build cycle 5+ years away

High correlation with NG prices

“Perfect Storm” vulnerabilities do exist

Depressed earnings

16

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

The Debt Problem

Sector has lost $100 B in market capitalization in the past 2 years

Energy merchants face nearly $65 billion of loans coming due by the end of 2010, says S&P. That’s out of a total debt burden of $125 billion

Divestitures and write-downs likely to continue

17

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

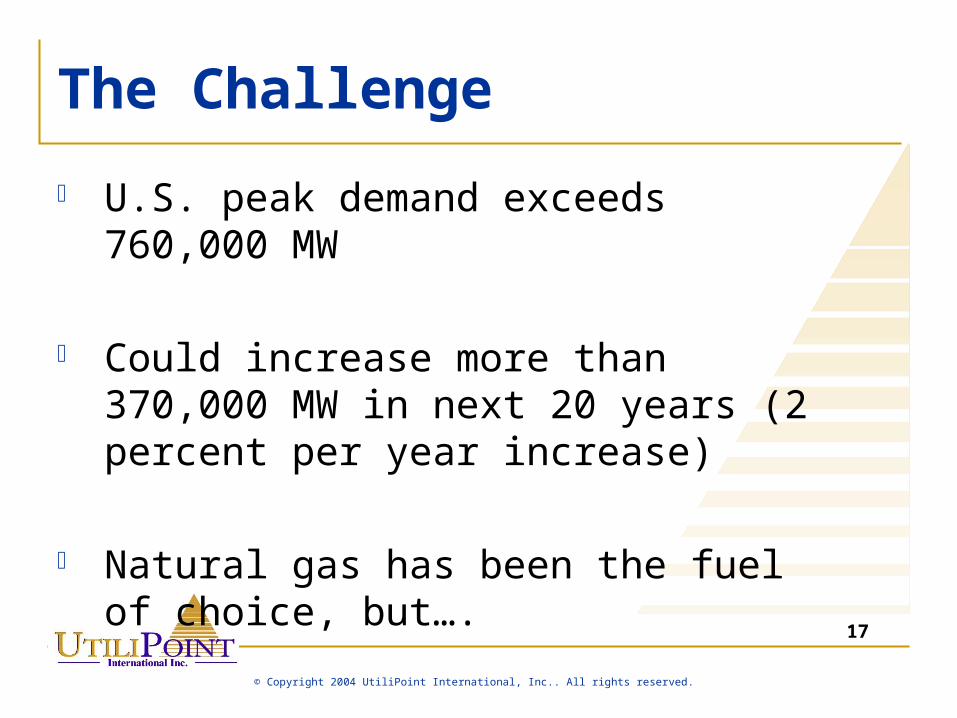

The Challenge

U.S. peak demand exceeds 760,000 MW

Could increase more than 370,000 MW in next 20 years (2 percent per year increase)

Natural gas has been the fuel of choice, but….

18

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

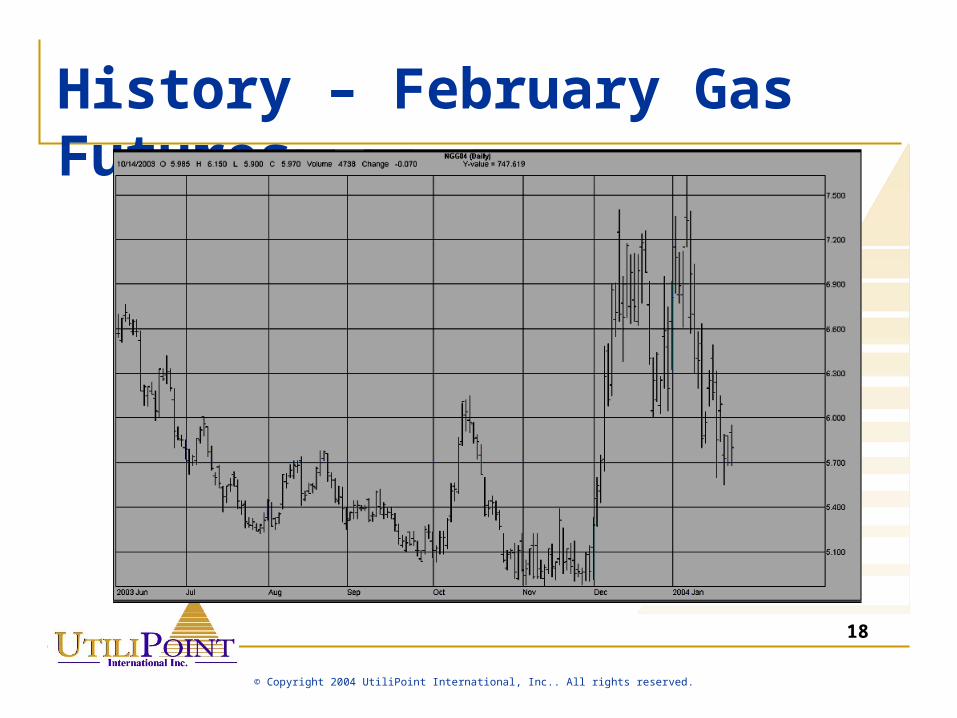

History – February Gas Futures

19

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

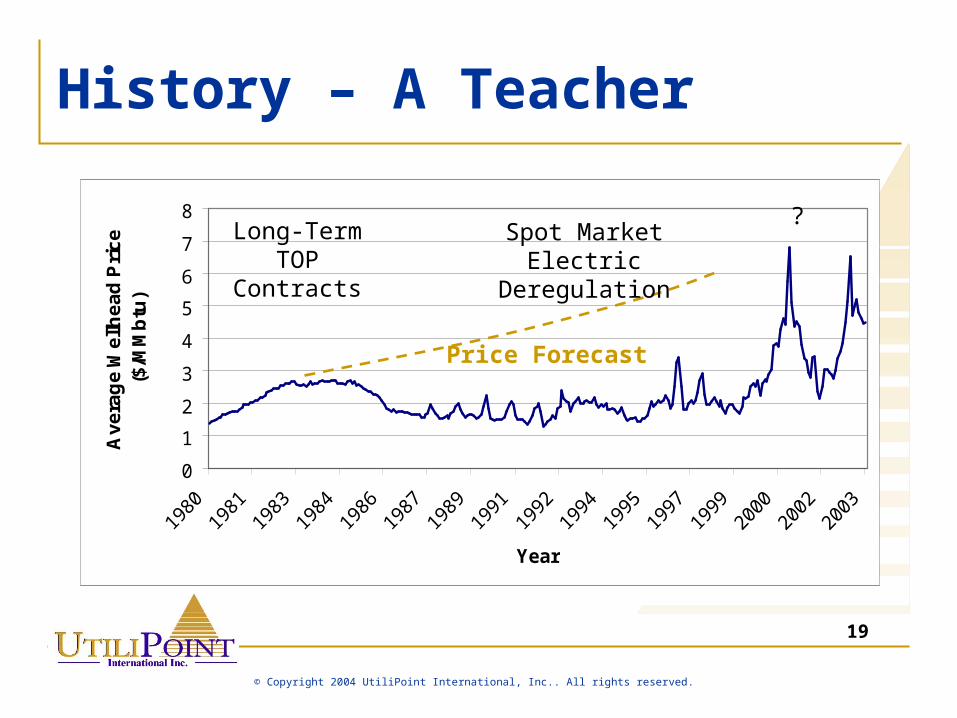

History – A Teacher

0

1

2

3

4

5

6

7

8

Year

Av

era

ge

We

llhe

ad

Pri

ce

($

/MM

btu

)

Long-TermTOP

Contracts

Spot MarketElectric

Deregulation

?

Price Forecast

20

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

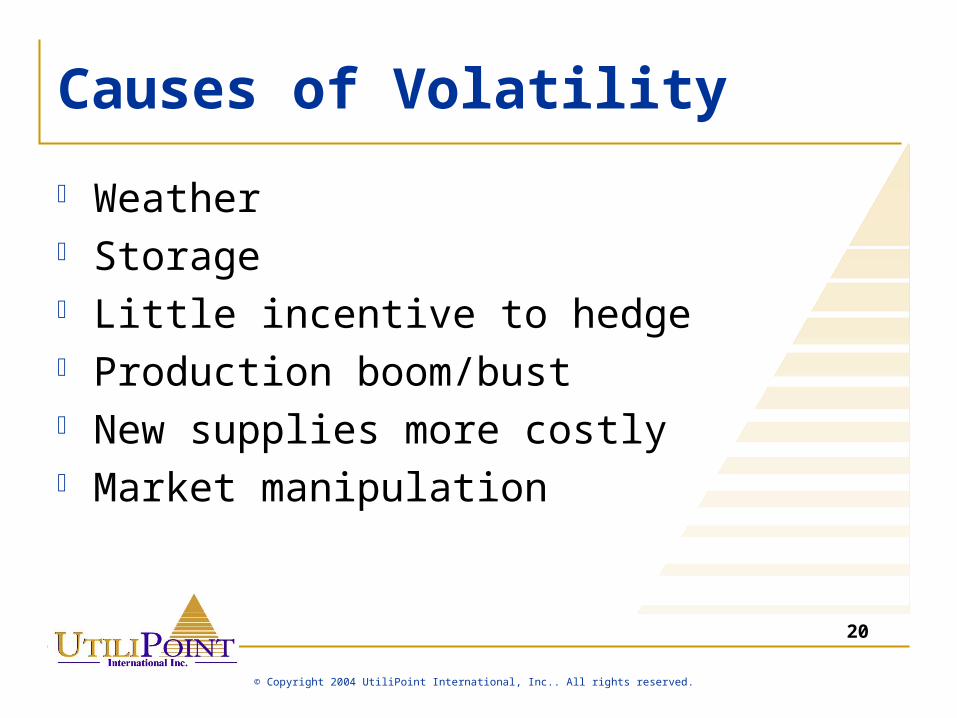

Causes of Volatility

Weather Storage Little incentive to hedge Production boom/bust New supplies more costly Market manipulation

21

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

Market Manipulation

Round-Trip Trades Withholding Production Serious Financial Impacts

BPA, Sierra-Pacific, Seattle, PG&E

Regardless: High prices will occur during

times of constraints

22

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

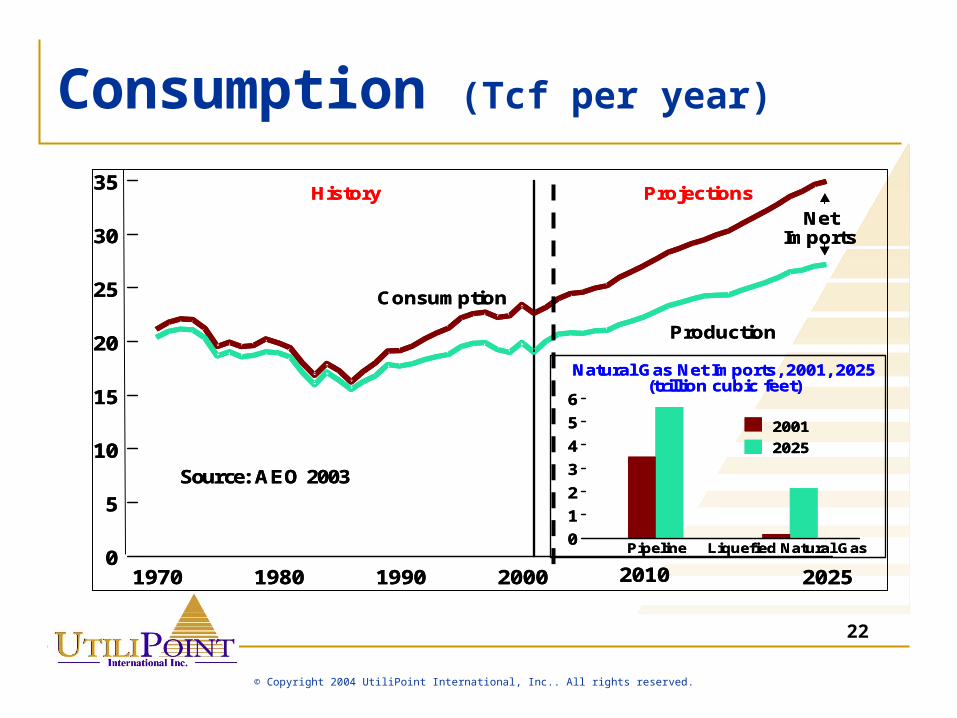

1970 1980 1990 2000 2010 20250

5

10

15

20

25

30

35 History Projections

Production

NetImports

Consumption

Pipeline Liquefied Natural Gas0

1

2

3

4

5

6

2001

2025

Natural Gas Net Imports, 2001, 2025(trillion cubic feet)

Source: AEO 2003

1970 1980 1990 2000 2010 20250

5

10

15

20

25

30

35 History Projections

Production

NetImports

Consumption

Pipeline Liquefied Natural Gas0

1

2

3

4

5

6

2001

2025

Natural Gas Net Imports, 2001, 2025(trillion cubic feet)

Source: AEO 2003

Consumption (Tcf per year)

23

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

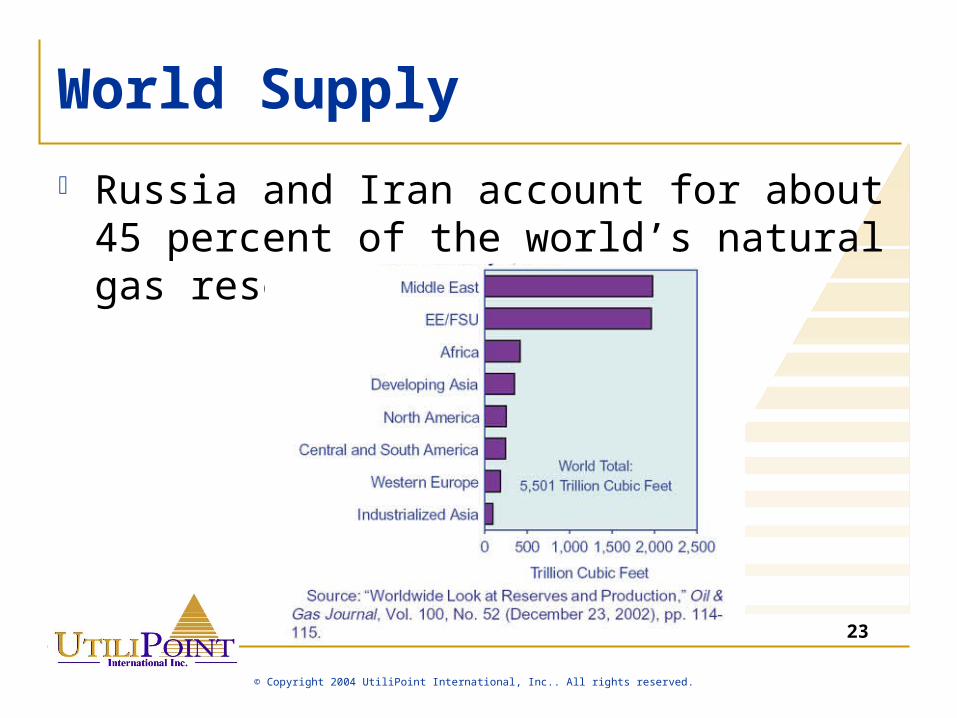

World Supply

Russia and Iran account for about 45 percent of the world’s natural gas reserves

24

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

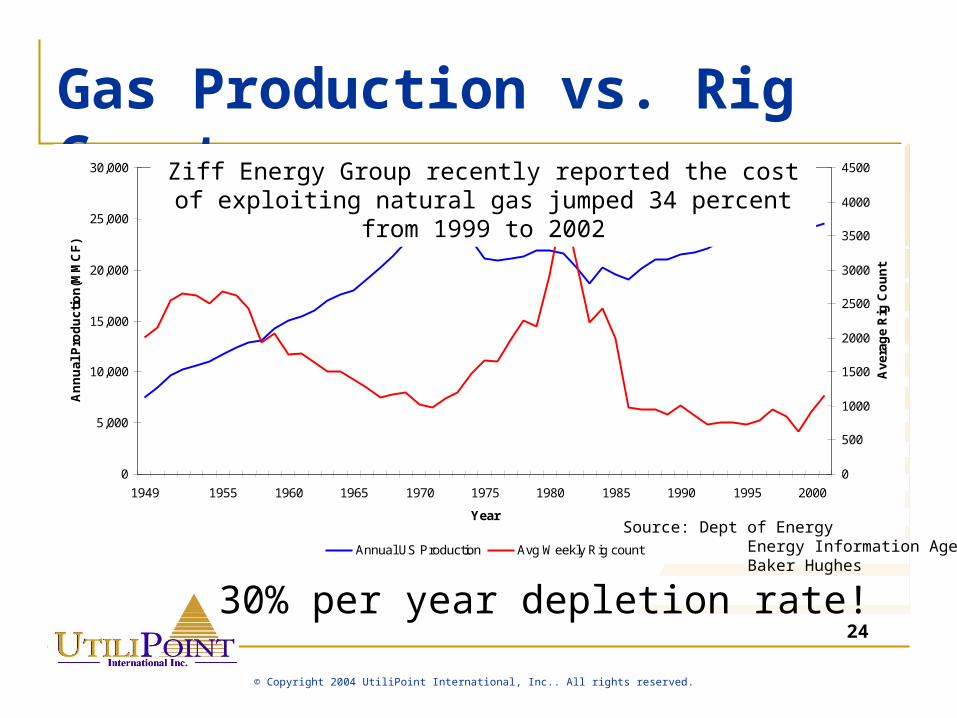

Gas Production vs. Rig Count

0

5,000

10,000

15,000

20,000

25,000

30,000

1949 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000

Year

An

nu

al P

rod

uct

ion

(MM

CF

)

0

500

1000

1500

2000

2500

3000

3500

4000

4500

Av

erag

e R

ig C

ou

nt

Annual US Production Avg Weekly Rig count

0

5,000

10,000

15,000

20,000

25,000

30,000

1949 1955 1960 1965 1970 1975 1980

0

5,000

10,000

15,000

20,000

25,000

30,000

1949 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000

Year

An

nu

al P

rod

uct

ion

(MM

CF

)

0

500

1000

1500

2000

2500

3000

3500

4000

4500

Av

erag

e R

ig C

ou

nt

Annual US Production Avg Weekly Rig count

Source: Dept of Energy Energy Information Agency Baker Hughes

Ziff Energy Group recently reported the cost of exploiting natural gas jumped 34 percent from 1999 to 2002

30% per year depletion rate!

25

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

Forecast

“An Unsustainable Trend is Exactly That”

26

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

The Coming “Train Wreck”

27

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

The Coming “Train Wreck” New electric generation additions = Gas

Coal and Nuclear produce over 70% of electricity currently

By 2010, 77% of coal units >30 years old and <300MW

New Coal takes 5 to 7 years to complete

28

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

LNG/Imports To The Rescue? To avoid shortages – Yes!

Price Stability - Means prices will likely exceed $4 per MMBtu

29

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

Renewables

Renewable programs on the increase Many utilities have implemented green

pricing programs States with portfolio requirements

AZ, CA, CT, HI, IL, IA, ME, MA, MN, NV, NJ, NM, PA, TX, WI

CA: September 12, 2002. Established the most aggressive renewable portfolio standard in the country by requiring utilities to purchase 20 percent of their electricity from renewable sources by 2017.

30

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

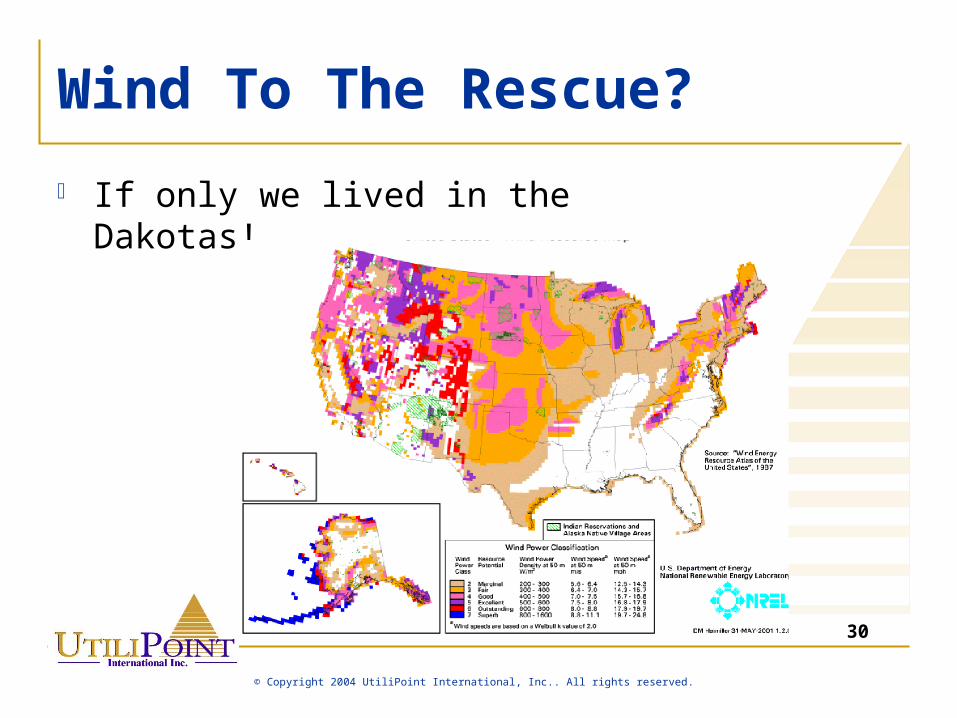

Wind To The Rescue?

If only we lived in the Dakotas!

31

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

Coal To The Rescue? US has 10 times more BTU’s

in the form of coal than oil and gas combined

Over 80 coal plants representing over 40 GW of power under consideration

Takes years to construct plant once permitted

Increasing emission regulations

32

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

Hydrogen To The Rescue? Made from Water, Methane,

Natural Gas Net Energy Loss Therefore effectively a

battery Decades away

33

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

Risk Myth

“We are not trading.”

Wires

Siting & Investment

Standard Market Design

“AEP receives final approval for Wyoming-Jacksons Ferry 765-kV project”

“Senate energy panel head criticizes FERC rules”

35

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

Reliability Standards

Blackout demonstrates potential liability exposure

Several entities violated NERC operating policies and planning standards

When it comes to reliability you cannot afford “reactionary” quality

36

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

Siting Issues

Lack of investment incentive

Multi-state, jurisdiction

Not In My Backyard!!

!

37

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

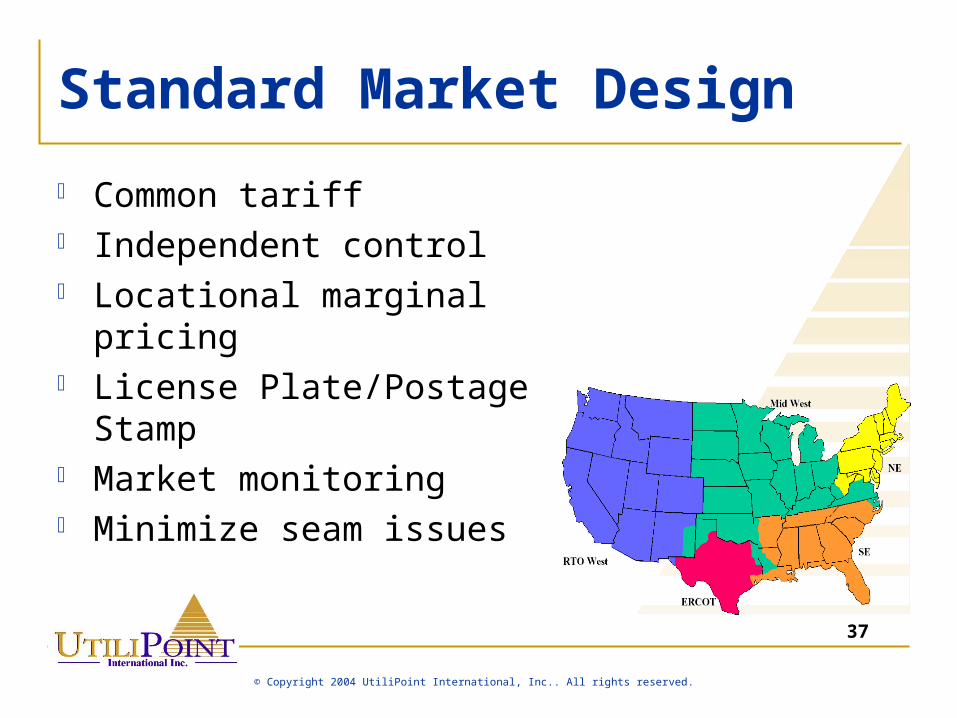

Standard Market Design

Common tariff Independent control Locational marginal pricing License Plate/Postage Stamp Market monitoring Minimize seam issues

38

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

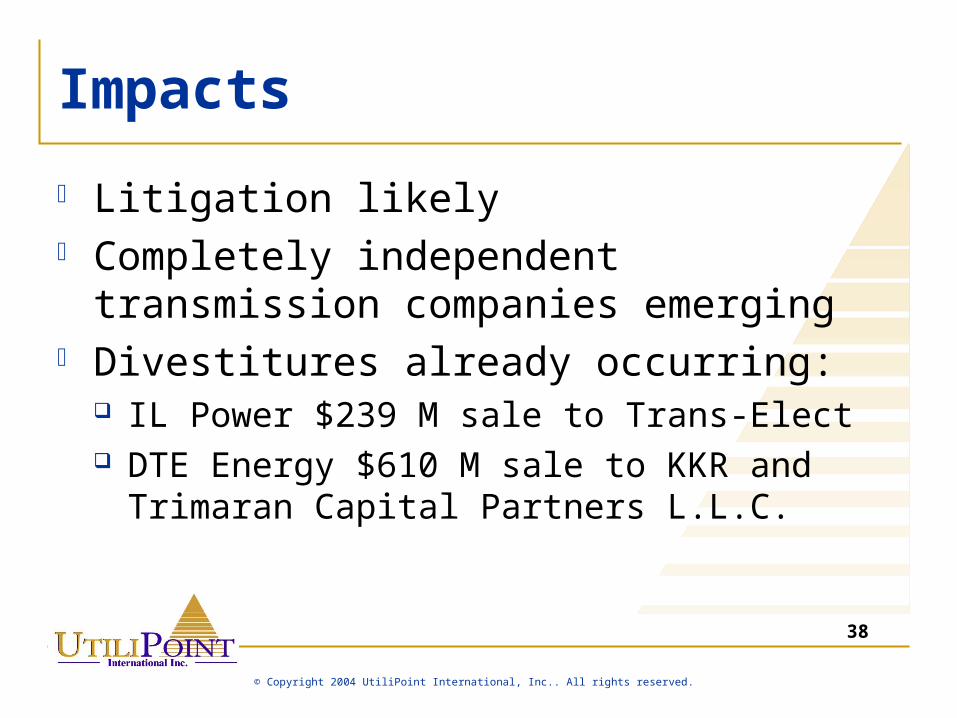

Impacts

Litigation likely Completely independent transmission

companies emerging Divestitures already occurring:

IL Power $239 M sale to Trans-Elect DTE Energy $610 M sale to KKR and Trimaran

Capital Partners L.L.C.

39

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

Risk Myth

“We can milk the wires business.”

Corporate and Regulatory

M&A

Energy Policy

41

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

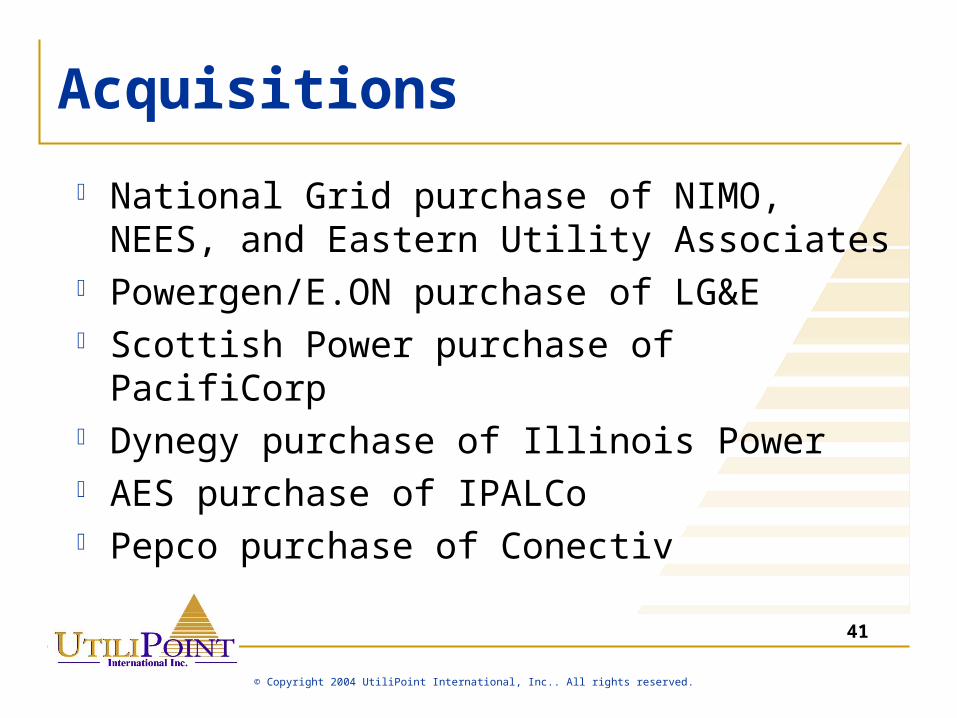

Acquisitions

National Grid purchase of NIMO, NEES, and Eastern Utility Associates

Powergen/E.ON purchase of LG&E Scottish Power purchase of PacifiCorp Dynegy purchase of Illinois Power AES purchase of IPALCo Pepco purchase of Conectiv

42

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

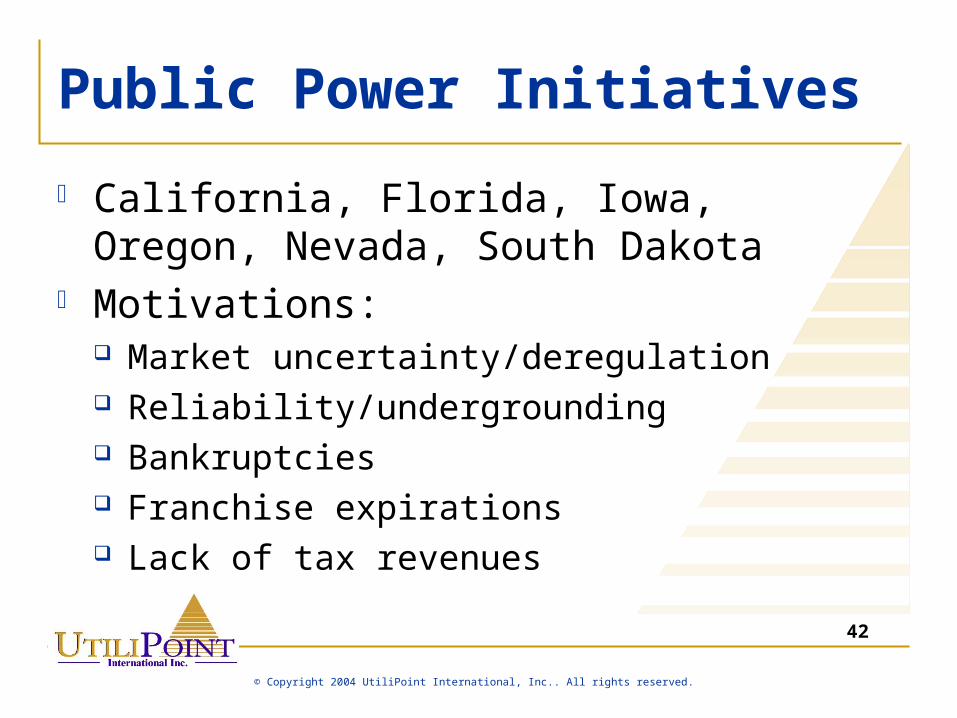

Public Power Initiatives

California, Florida, Iowa, Oregon, Nevada, South Dakota

Motivations: Market uncertainty/deregulation Reliability/undergrounding Bankruptcies Franchise expirations Lack of tax revenues

43

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

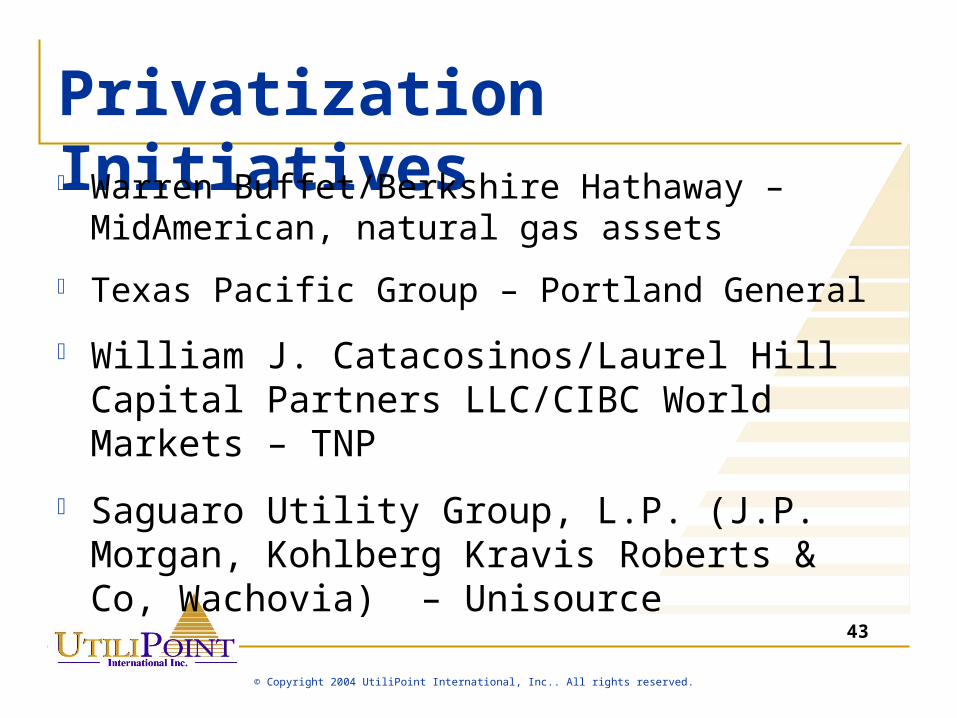

Privatization Initiatives Warren Buffet/Berkshire Hathaway –

MidAmerican, natural gas assets

Texas Pacific Group – Portland General

William J. Catacosinos/Laurel Hill Capital Partners LLC/CIBC World Markets – TNP

Saguaro Utility Group, L.P. (J.P. Morgan, Kohlberg Kravis Roberts & Co, Wachovia) – Unisource

44

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

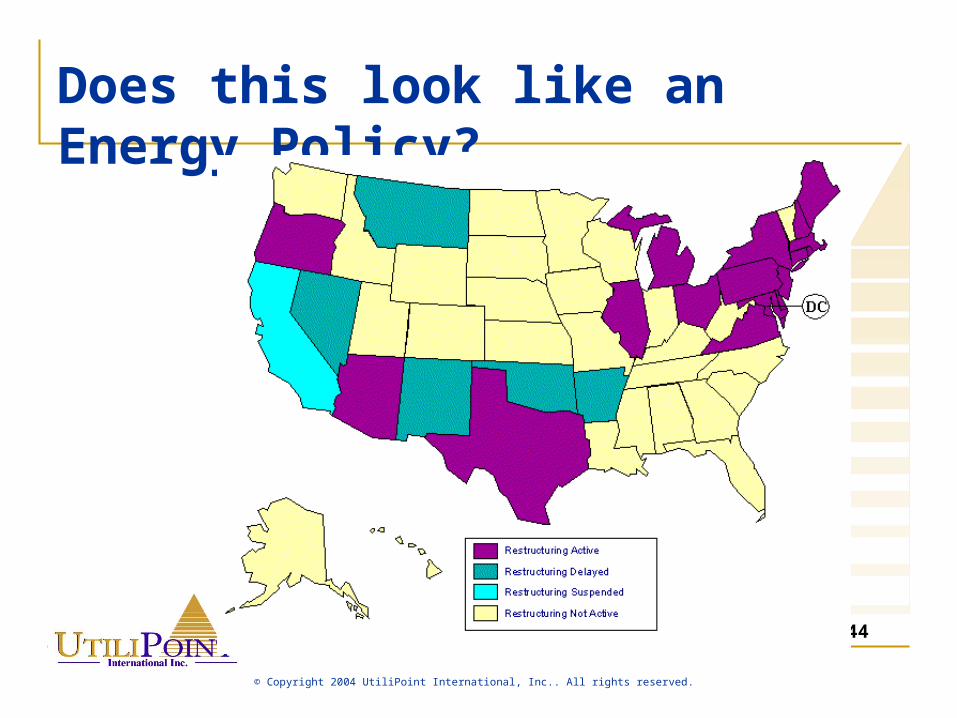

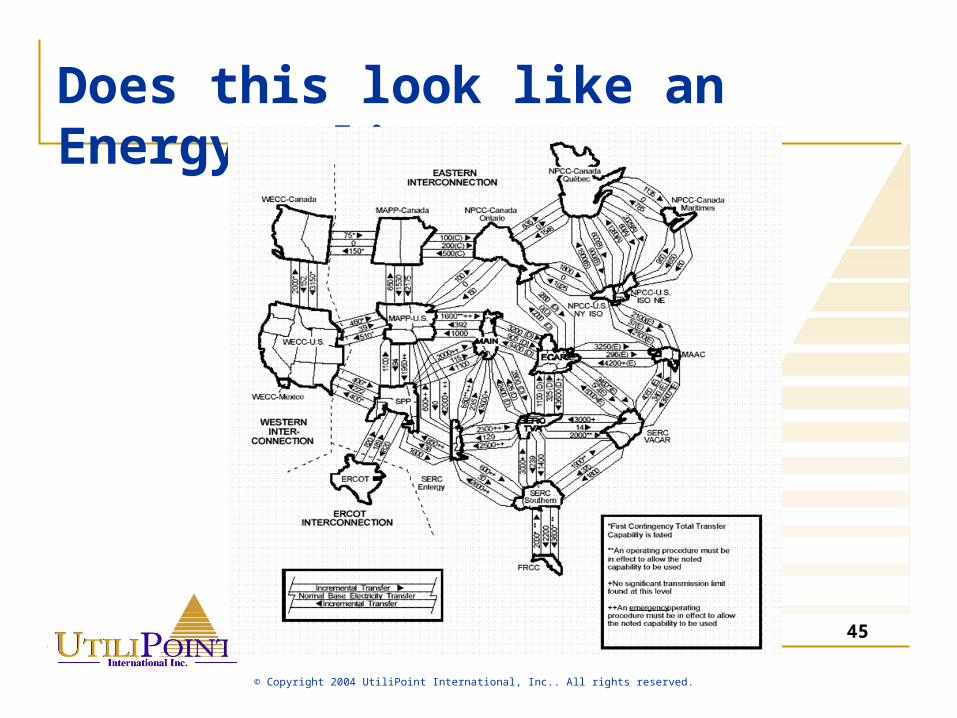

Does this look like an Energy Policy?

45

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

Does this look like an Energy Policy?

New Technologies

Energy Storage

Fuel Cells

Other

47

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

Venture Capital

R&D expenditures for 20 leading utilities have decreased by 62% from 1995 to 2000

Same utilities increased their subsidiary investments from $4.5 B (1995) to $15 B (2000)

Venture capital in the industry increased from near zero 6 years ago to over $1 billion in 2001

Venture capitalists in 2002 curtailed their fund raising for future investments to a 21-year low. While 108 venture capital funds raised a total of $6.9 billion during 2002, another 26 funds refunded $5 billion to investors.

48

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

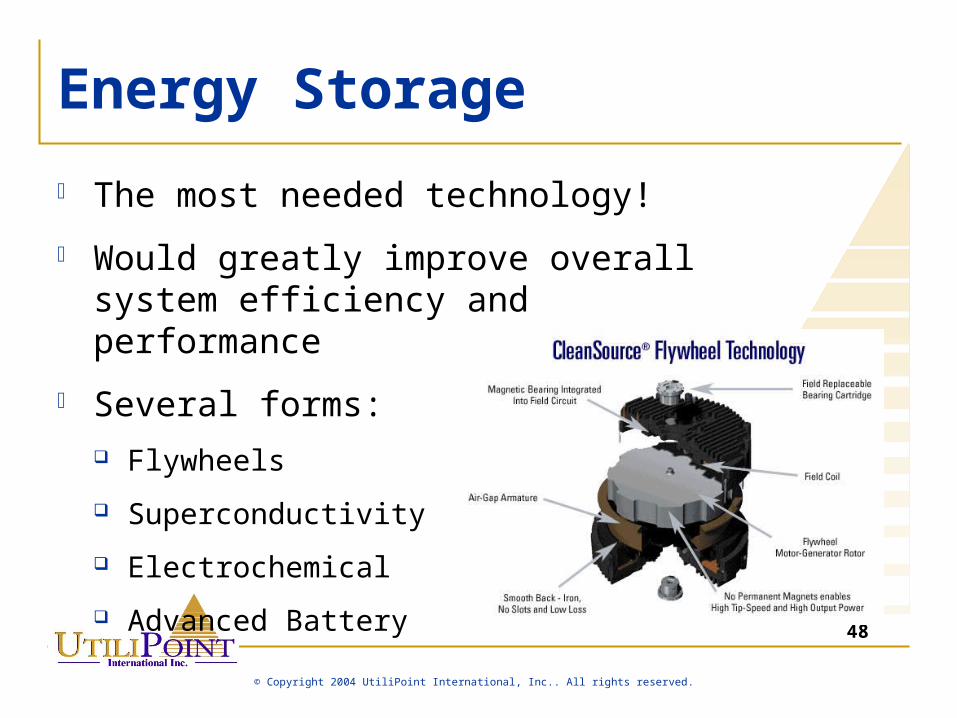

Energy Storage

The most needed technology!

Would greatly improve overall system efficiency and performance

Several forms: Flywheels

Superconductivity

Electrochemical

Advanced Battery

49

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

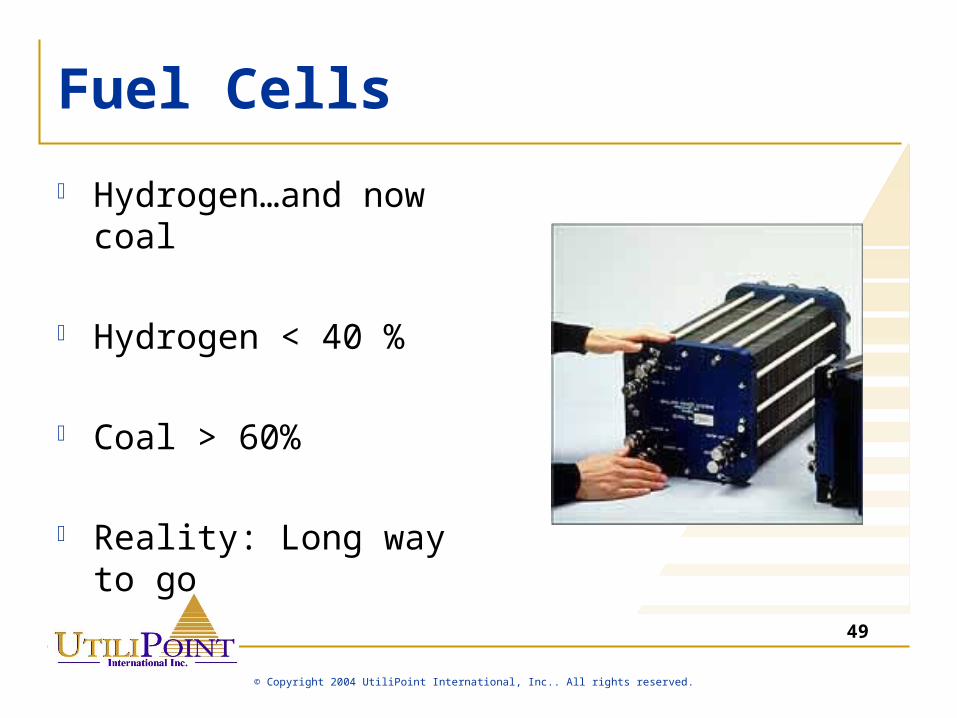

Fuel Cells

Hydrogen…and now coal

Hydrogen < 40 %

Coal > 60%

Reality: Long way to go

50

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

Makes Industry Better

Coal Gasification Clean Coal Pebble Bed Nuclear Reactor FACTS devices Advance metering and data

acquisition/management Power line carrier

51

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

Risk Myth

“This technology will revolutionize the business in 2 years”

52

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

Things we now know not to be true… $50+ billion in total assets, 5 million or

more customers to survive Deregulation means lower rates Asset-lite in trading Diversification is required We rely primarily on the spot market

53

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

Things we must commit to: Reliability is job one Doing what’s in the public and customer

interest is ultimately in the best interest of the company

Avoid speculation and diversifying into non-core areas

54

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

55

© Copyright 2004 UtiliPoint International, Inc.. All rights reserved.

Contact Information

Bob Bellemare

505.244.7612