Embed Size (px)

Citation preview

THE ETHIOPIAN ECONOMY AND THE WAY FORWARD

BY Agerachinen Enadin/TG 12/30/2007 The Global economic context Ethiopia is in: The past 30 years have been remarkable for many developing countries while disappointing for countries such as Ethiopia. In the late 1970s China emerged from Cultural Revolution and embarked on reform. As a result more than 1 billion people – one fifth of earth’s population have experienced a period of sustained growth and poverty reduction that has no precedent in human history. In the 1980’s 400 million people in Central and Eastern Europe and the former Soviet Union embarked on transitions from Command economy towards democracy and market economy. India’s growth began to pick up in the 1980’s, and in the early 1990’s, it initiated far-reaching economic change. Today India is seeing growth and poverty reduction on a scale that would have been dismissed as highly improbable by many analysts in the 1970s and 1980s. Thirty years ago just one-third of the World’s countries could be described as democratic now that share is closer to two thirds. Remarkable too has been the improvement in leaving standards, including those related to health and education. In the past forty years the average life expectancy in developing countries increased from mid-forties to mid-sixties. Over the past thirty years, the share of illiterate people in the developing world declined from around one-half to one-quarter, with particular strong progress for girls and women. And in the last quarter - century the number of people living on less than $1 a day fell by about 200 millions. This decrease has occurred at a time when the population of the developing world rose by 1.5 billion.

While there is a tremendous global advancement in growth, production and productivity sadly, Ethiopia has not been a beneficiary of such progress. For Ethiopia the 1970s and 1980s are the lost decades where the country was engaged in bitter civil war, regional and sub regional conflicts and internal turmoil that consumed a whole generation of young people that the country

1

so heavily inverted in and led to a long time economic decline that led to famine, poverty and disease. Ethiopia’s growth remains determined by the rain-fed agriculture sector which is volatile. Most of the Ethiopian people are left out from the Global growth and benefits. In rich countries, mortality to children under age five is 7 deaths per 1,000 and in poor countries the average is 84 deaths per 1,000 in Sub-Saharan Africa 162 deaths per 1,000 while in Ethiopia it is a shocking 166 deaths per 1,000. Ethiopia’s human development Index (UNDP HDR - 2007) HDI is 0.406 which is much less than the average for developing countries 0.691 and Sub-Saharan Africa’s 0.493. Ethiopia is ranked 168 out of 177 countries in its HDI Index which is a clear indication of the level of underdevelopment. GDP (purchasing power parity) is $73.79 billion (Ministry of Finance and economic Planning 2006 est.) and GDP is $11.8 billion (EIU for 2006). And GDP per capita (PPP) is $834 (EIU FOR 2006). Population below poverty line (US$1 a day) is 40% (FY05/06) and 80% of the population live on less that US$2 a day. Household income and consumption by percentage share is lowest 10% is 3.9% and highest 10% is 25.5% (central Statistical Office -CSO 2000). Inflation is 13.5 % in 2006 and 20% in 2007 and rapidly climbing. Revenue was $2.614 billion and expenditure $3.201 billion, including capital expenditure of $788 million (2006). (some of the figures by the Ministry of Finance, Economist Intelligence Unit and the World Bank are not exactly similar due to different approaches and interpretations of statistical facts and statistical collections). Ethiopia is using 10.01% of its arable land unable to control deforestation, soil erosion, desertification and overgrazing. Ethiopia has 76,511,887 million people with the overwhelming majority being young and unemployed. There is no official unemployment rate, but youth unemployment, some experts reckon, may be as high as 70%. 47% of the population (male 16.6 million and female 16.54 million) are in the age bracket of 0 to 14 years. 53.8% (male 20.56million and female 20.64 million) are in the age bracket of 15 to 64. Only 2.7 % of the population (0.9 million male and 1.2 million female) are over 65 years old. This clearly shows that the population is young and if the issue of unemployment is not effectively addressed its consequences will not be pleasant to say the least. The mood of the young is often restless and despairing with resentment.

2

Since the current government has introduced Ethnicity as a major factor in the politics and economics of the nation, the ethnic mix clearly signals that the issue of governance, political representation, access to both economic and political power that leads to stability and economic prosperity needs to be fairly and squarely addressed. The ethnic mix shows that 32.1% Oromos, 30,1% Amharas, 6.2 million Tigreans, 5.9 Somalis, 4.3 Gurages, 3.5 Sidama, 2.4 Welaita, and others 15.4 (1994 ETC or 2002 GC census) . It is therefore, from this Global verses National context that we examine the Ethiopian economy. Economic Policy: Economic reform based on Liberalization, has been undertaken by the Government (in close cooperation with the Britton Woods Institutes) since it came to power in 1991. The economic reforms are relatively based on “local ownership” of the process to a certain degree. This means in some areas such as land tenure, Banking and Financial Sector, telecommunications etc. the Government Economic Team (formerly known as the Policy Framework Group- PFP group) held its ground against the advise of the IMF, the World Bank and the Donor community. The government has to be commended for its stand on some and is deadly wrong on others. The IMF suspended disbursement temporarily in 1997 because of disagreement over the pace and scope of financial-sector reforms, which still remains key areas of policy conflict. The official policy framework of economic reform in Ethiopia is provided by the sustainable development and poverty reduction programme (SDPRP), which ran from 2001/02 to 2005/06, and its successor, the plan for accelerated and sustained development to end poverty (PASDEP), which run from 2006/07 to 2010/11. The government strategy has several key components, including macroeconomic adjustment, structural reforms, better governance, food security, and a belief in “agricultural led industrialization”. The SDPRP and PASDEP, according to official lines, are also geared towards poverty alleviation and meeting Millennium Development Goals. Overall the strategy envisaged achieving the following:

• Sustained growth of 7% a year through massive investment in key anti poverty sector, rising to 10% a year at the end of the programme.

• A sustained rise in agricultural productivity and production, with crop output climbing from 15 million tones a year to 38 million tones, and

3

• A particular focus on textile, leather and floriculture industries in an effort to boost export.

The total investment under the programme is projected to be a massive Birr 342bn. (US$39.3bn), including Birr 233bn. in capital spending and Birr 109bn. in recurrent outlays. Donor funding will be sought to cover 30-40% of the amount, while private-sector participation will also be encouraged. The largest sectoral outlays are earmarked for education (19%), health (19%), agriculture (14%), roads (13%), water (12%), energy (12%), housing (5%), and telecommunications (5%). (Ministry Of Finance and Economic Development, MOFD, June 2007). The plan and strategy looks good on paper and looks reasonable with the Ethiopiain economic reality. However, it is overly ambitious and will not be realized given the circumstances the nation is finding itself in the areas of economics, political, military, regional and international issues. Such issues include tension and conflict with Eritrea (direct and through proxy); the war in Somalia; the continued instability in the Sudan and its possible direct and indirect impact; regional pressure on Djibouti to serve regional interest sometimes contrary to Ethiopia’s; internal division; political tension and ethnic conflicts; continued vulnerability to exogenous shocks like drought, commodity price fluctuation, growing oil price; growing uncertainty of donor funding and heavy dependency on external support.

The regions’ economic powers are growing

Ethiopia’s regional governments have a considerable degree of economic autonomy on paper under the constitution and the policy of decentralization, which theoretically limits the federal government’s influence on economic policy to monetary matters, land ownership, foreign trade and investment, interstate commerce and nationwide transport, and devolves all other economic powers to the regions, including taxation. In practice, however, the regions remain politically subservient to and financially dependent on the EPDRF government and off course the core TPLF leadership, and this autonomy worked only when TPLF wants it and does not go against its interest. They handle a growing share of the national budget and play a role in trying to attract investment, both local and foreign, and providing social services. However, the government’s party pararstatals and key TPLF officials are in total control operating behind the seen on what is going on and are more direct beneficiaries than the local population. The local

4

regional elected officials are total subservient to the politicians in power with very limited substantive skills and know how. Those with skills and know how are deliberately shunned and kept at arms length to secure behind the seen iron fist control by the core of TPLF.

The capital, Addis Ababa, remains the dominant economic city and the only one with a wide tax base. Dire Dawa is an important commercial centre and its proximity to the sea through Djibouti, and the rail road connection makes it an attractive investment area as long as there is security and stability. . Awassa is emerging as the growing business center in the South where there is a relatively less risk to private sector investment and less ethnically charged business atmosphere. Mekele is also growing as several critical investments are made along with the establishment of new institutions and industrial establishments and this should be seen as a positive development.

Highlights of the major activities in the economy in recent years and its challenges: Macro Economics: The economy has registered some positive results in the last few years in terms of growth. According to Government sources real GDP growth rate during 2005/6 stood at about 10% while skeptics think it is 5-6%. According to official statistics during the years 2000/01 to 2006/7, the economy registered average growth rate of 6.7% which is above the average of 5.8% realized in SSA. With some questioning of the government statistics, economists agree with the fact that there was growth but at a little lower rate than claimed by the government. Economists also argue that this rate of growth compared to many years of stagnation and negative growth cannot be exaggerated and more and higher growth is required to have a significant impact on the abject poverty prevalent in the country. According to official statistics, the agricultural sector registered growth rate of 11.2% during 2005/06 while it is expected to settle at 10.9% in 2006/07. In regard to industrial and service sector, during 200/06 growth rate of 7.4% and 9.2% has been registered respectively while in 2006/07 it is estimated to register rate of 10.9% and 9.6% respectively. (MOFD, 2007). Many economists and observers believe that the service sector is the one that grew faster and consistently since there are less political and bureaucratic interference as well as less party parastatals crowding out with unfair advantage.

5

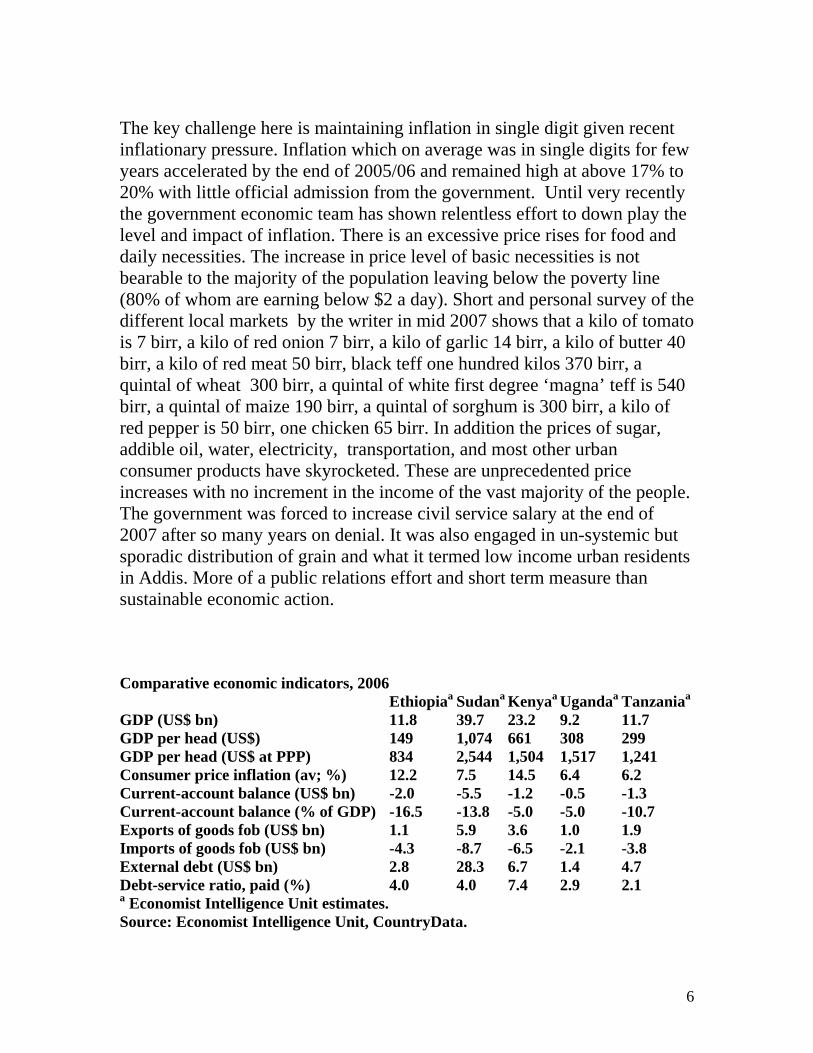

The key challenge here is maintaining inflation in single digit given recent inflationary pressure. Inflation which on average was in single digits for few years accelerated by the end of 2005/06 and remained high at above 17% to 20% with little official admission from the government. Until very recently the government economic team has shown relentless effort to down play the level and impact of inflation. There is an excessive price rises for food and daily necessities. The increase in price level of basic necessities is not bearable to the majority of the population leaving below the poverty line (80% of whom are earning below $2 a day). Short and personal survey of the different local markets by the writer in mid 2007 shows that a kilo of tomato is 7 birr, a kilo of red onion 7 birr, a kilo of garlic 14 birr, a kilo of butter 40 birr, a kilo of red meat 50 birr, black teff one hundred kilos 370 birr, a quintal of wheat 300 birr, a quintal of white first degree ‘magna’ teff is 540 birr, a quintal of maize 190 birr, a quintal of sorghum is 300 birr, a kilo of red pepper is 50 birr, one chicken 65 birr. In addition the prices of sugar, addible oil, water, electricity, transportation, and most other urban consumer products have skyrocketed. These are unprecedented price increases with no increment in the income of the vast majority of the people. The government was forced to increase civil service salary at the end of 2007 after so many years on denial. It was also engaged in un-systemic but sporadic distribution of grain and what it termed low income urban residents in Addis. More of a public relations effort and short term measure than sustainable economic action. Comparative economic indicators, 2006 Ethiopiaa Sudana Kenyaa Ugandaa Tanzaniaa

GDP (US$ bn) 11.8 39.7 23.2 9.2 11.7 GDP per head (US$) 149 1,074 661 308 299 GDP per head (US$ at PPP) 834 2,544 1,504 1,517 1,241 Consumer price inflation (av; %) 12.2 7.5 14.5 6.4 6.2 Current-account balance (US$ bn) -2.0 -5.5 -1.2 -0.5 -1.3 Current-account balance (% of GDP) -16.5 -13.8 -5.0 -5.0 -10.7 Exports of goods fob (US$ bn) 1.1 5.9 3.6 1.0 1.9 Imports of goods fob (US$ bn) -4.3 -8.7 -6.5 -2.1 -3.8 External debt (US$ bn) 2.8 28.3 6.7 1.4 4.7 Debt-service ratio, paid (%) 4.0 4.0 7.4 2.9 2.1 a Economist Intelligence Unit estimates. Source: Economist Intelligence Unit, CountryData.

6

Public Finance (Fiscal policy): Under the circumstances there has been a relatively reasonable fiscal management and stable macro economy in the last few years. During 2005/06, government revenue reached 19.5 billion Birr while total revenue including grants reached 24.3 billion Birr. The tax revenue amounted to 12.2% of GDP in 2005/06. Revenue from income tax is expected to increase. Domestic revenue mobilization efforts have been supplemented by increased external resource flows until the 2005 election, which has increased from US$693.6 million in 2002/03 to US$1.05 billion and US$1.5 billion in fiscal year 2004/05 and 2005/06, respectively. While these measures are recognized as reasonable, the technique used to implement them and how fairly and evenly applied to all regions based on acceptable universal rule is questionable.

There has also been a substantial increase in expenditure. Total government expenditure reached 29.3 billion Birr in 2005/06 (25.3% of the GDP). During 2005/06, 52% of the expenditure is allocated for recurrent cost while capital expenditure accounted for 48%. In general public spending management and its transparency needs to be improved and that domestic borrowing (to limit the inflationary consequences) be curbed. Domestic borrowing was much higher than expected in 2004/05, 3.5% of GDP, (MOFD and EUI). compared with a target of 1.5%, while the stock of domestic debt remained high at 35% of GDP. The risk is much higher in 2006/07 since the government resorted to heavy domestic borrowing since donors withheld some of their funds due to the political tension after the 2005 election ODA Disbursement: Including emergency aid and technical assistance, Ethiopia currently receives about US$1.1 billion per annum in aid. On per capita terms, this is equivalent to US$14.8 in 2005/06. The amount of ODA have risen sharply from the average of $500 million per annum in the mid-1990s to over US$1 billion per annum recently. Over the last five years (2001/02 – 2005.06), ODA has averaged at US$932.5 million per year. The contribution of bilateral donors to ODA over the five years period was on average, US$270.9 million per year (30%). Multilateral donors have been and still are the principal providers of external assistance. On average they altogether contributed US$661.6 million (70%) of total ODA to Ethiopia. There is tremendous volatility and unpredictability in ODA flows. In

7

addition the level of fund needed is significant. The level of official development assistance that Ethiopia currently receives in terms of per capita assistance (US$14.8) is considerably lower than that of other low income countries in SSA.

In general when we look at the public finance, the government is not prudent and transparent in its expenditure policy. Major criticism is the unequal and unfair expenditure through higher allocation to the favored region of the political leaders The business community complain that the system of taxation is aggressive and pointed at those that do not have political connection or that are not party parastatals. Some have even claimed that increasing tax has been used as a tactic of pressurizing and settling score on those suspected of supporting the opposition. The real problem and challenge here is that the revenue base is still very narrow and tax revenue has been increasing fast. Maintaining a prudent fiscal stance that addresses the development needs of the country while maintaining the deficit at a sustainable level in the medium term is critical. At the same time understanding the need to balance the tremendous demand of service and investment with the need for macroeconomic discipline, protecting the poor from inflation, maintaining economic stability needed for private sector growth to create jobs and income as well as expanding investment in education, health, infrastructure as fast as possible are the key challenges is a must.

Defense and security expenditure has naturally increased after the 2005 controversial election and the government violent crack down against the opposition as well as the Somalia invasion and the build up for growing confrontation with Eritrea. This will continue to put pressure on public finance.Therefore, the expenditure pattern has been drastically affected and will have a consequence on the growth and development patter in the coming years.

External Sector: Export registered growth in recent years, owing to both increase in volume and revival in the prices of major exports in international market. Ethiopia depended heavily on Coffee, its main export, but earnings are vulnerable to shifts in world prices. Coffee receipts crashed from a peak of US$420 million in 1997/98 (70% of total earning) to US$165 million in 2002/03 (34% of total earnings). However, income recovered strongly to US$335m in 2004/05, and an estimated US$354m in 2005/06 (35% of total

8

earnings), because of the rebound in world prices and higher production. Coffee may never regain its former prominence, however, as a result of rising exports of other goods. Oilseeds have emerged as the second most valuable export, because of high sales of sesame to China, with earnings from the sale of these up from US$114m in 2004/05 to US$200m in 2005/06. Khat/Chat (sold mainly to Djibouti and Somalia), is third in the earnings league, although sales edged down from US$100m in 2004/05 to US$89m in 2005/06. Other key exports include leather and leather products, gold, pulses, and live animals and meat. Exports of horticultural products (especially flowers) are growing rapidly from a small base, with sales rising from US$22.8m in 2004/05 to US$35.6m in 2005/06. Total exports have grown rapidly in recent years, reaching US$847m in 2004/05 and an estimated US$1bn in 2005/06, according to provisional data from the National Bank of Ethiopia (the Central Bank), spurred by rising coffee prices and increased sales of other commodities.

Imports also surged. Ethiopia’s import needs are vast and have risen rapidly—from US$1.6bn in 2001/02 to US$3.6bn in 2004/05, and a provisional US$4.4bn in 2005/06. The surge in imports reflects several factors, including higher purchases of capital equipment (for donor-backed projects and for new aircraft by Ethiopia Airlines), purchase by the party parastatals, private sector investment and consumption demand increases, the rapid rise in world oil prices and an overall increase in economic activity (as indicated by faster GDP growth). Trade deficit widened and reached 18% of GDP during the same period from 15% in 2001/02. As a result of export and import trends, Ethiopia has a large structural deficit on its merchandise trade account. This rose from US$1.2bn in 2001/02 to US$2.8bn in 2004/05 and an estimated US$3.4bn in 2005/06. The unparallel increase in imports of goods was reflected in a widening trade and current account deficit of the balance of payment which is a major challenge The external current account deficit (excluding official transfer) widened to 13% and 16% increase of GDP in 2004/05 and 2005/06, respectively from 11.3% of GDP in 2003/04. Exports of goods and non-factor services reached 15% of GDP while imports of goods and non-factor services have stabilized at about 33% of GDP by the end of 2005/06. (MOFD, EUI). As stated earlier, with the war in Somalia and Ogaden, the growing instability and building up the military for a possible deterrence or confrontation with Eritrea, growing internal security expenditure, the

9

external current account will definitely be much worse. This will be impacting negatively on the economy.

Financial Sector: There is a progressive and relative improvement and deepening of the financial sector reform though very slow with a lot of political interference.

The regime has approached financial liberalization extremely cautiously. The sector was nationalized following the 1974 revolution, giving the Commercial Bank of Ethiopia (CBE) a virtual monopoly on retail banking. Local private-sector banks have been allowed to operate since the mid-1990s, but foreign banks remain barred. The government has resisted IMF pressure to open up the sector, believing that local institutions are not yet strong enough to compete. The National Bank of Ethiopia (NBE, the central bank) was established in 1964. Since 1991 the NBE has held Treasury-bill auctions and has overseen the gradual liberalization of foreign-exchange markets. Moves to legalize market-determined foreign-exchange trading in private- and state-sector financial institutions began in 1997. Regular foreign-exchange auctions were replaced by an interbank market in October 2001an interbank market in October 2001.

The CBE dominates commercial banking

The CBE remains the dominant market player, but faced financial meltdown a few years ago as its level of non-performing loans (NPLs) passed the 50% mark, because of unregulated lending to state-owned companies, Party Parastatals and to people with political connections and connections with Bank officials. The lending to private individuals and part parastatals has resulted in internal fighting and corruption charges and imprisonment of several Bank Officials. Restructuring of the CBE was a key aspect of the IMF-backed reform programme in 2001-04. An independent audit was carried out in 2003 and a private management contract was awarded to the UK’s Royal Bank of Scotland for an initial two-year period. This was later extended by six months to February 2006. Other measures adopted included a timed programme to cut the share of NPLs to 20% of total loans, a rise in the capital-adequacy ratio, the establishment of an audit committee and the transfer of lending authority from the bank’s board to its management. As a result, the CBE has now returned to profitability and posted gross profits of Birr787m (US$91m) in 2004/05, about 60% higher than the previous year. However, NPLs remain high, at about one-third of total loans. (MOFED).

10

Six local private banks have been established since liberalization in the mid-1990s—Dashen, Awash, Abyssinia, Wegagen, NIB and United. They have taken an increasing share of business and accounted for about 30% of outstanding credit in 2005/06, up from 10% in 1999/2000, according to the NBE. A new bank, Lion International, formally opened on January 1st 2007—the first entrant since the minimum capital requirement for private banks was lifted to Birr75m (US$8.6m) in 1999 making the number of private banks seven. Three other banks are seeking registration.

Most of Ethiopia's six private banks recorded significant profit rises in the 2005/06 financial year (ending June 30th), reflecting a growing activities and growth in the economy, with Dashen Bank leading the pack. Dashen, which has 37 branches, earned a net profit of Birr133.6m (US$15.4m) in the 2005/06 financial year—a record for a private bank in Ethiopia and almost double the level in 2004/05. NPLs account for a relatively small 6.2% of the bank's loan portfolio. NIB also performed strongly in 2005/06 with net profits rising by 24% year on year, to Birr56.6m. NIB was also named "Ethiopian Bank of the Year 2006" by the Global Finance journal last November, and entered African Business magazine's list of Africa's 100 top banks in 2006, joining CBE and Dashen. However, access to precious foreign exchange remained challenging, given the dominant position of the state-run Commercial Bank of Ethiopia (CBE), especially in the foreign-exchange market

At the close of 2004/05, the number of bank branches increased by 31 to reach 389 branches; of which 174 (or about 44.7%) belonged to the Commercial Bank of Ethiopia, which is the largest public bank in the country. (MOFED).

During the same period, the number of private banks along with their branch offices registered a growth rate of 15% compared to 2003/04 and reached 157. Total capital budget of the banking system reached 3,486 million Birr by the end of June 2005; of which 1,979 million Birr (56.8%) was held by the three government-owned banks ( Commercial Bank of Ethiopia, Development Bank, and Construction and Business Bank). The market share of private banks has been steadily increasing in terms of all banking operations as well despite the complaint of unnecessary restrictions and interference by the government. The total capital of seven

11

private banks stood at 1,507 million Birr (43.2%). By the close of 2004/05, the share of private banks in total banking system deposits has reached 25.3% and accounted for 49.4% on new loan disbursements. Domestic credit increased by 31.5% by the end of 2004/05 and by 20.1% by the end of 2005/06 as claims on non-governmental sectors increased by 58.5% in 2004/05 and by 29.8% in 2005/06. The latter was largely attributed to the increase in claims of commercial banks on public and private enterprises. As a result, the 19.6% growth in broad money supply is partially attributed to the growth in domestic credit. The growth in domestic liquidity was 10.9% by close of 2004/05 and increased to 17.4% in 2005/06.

Despite these developments, however, commercial banks continue to face the problem of excess liquidity and this is the major challenge. Attaining relative price and exchange rate stability with major objectives of containing inflation within single digits as well as encourage saving and long-term investment is the main challenges. Credit to the private sector and expanding infrastructure development and capacity –building program to maintain the momentum of growth by the private sector is critical. Sectoral Economy:

Agriculture and Food Security: Agriculture is the main driver of the economy and the source of income for the majority of the population. The sector contributes about 50% to total GDP, generates about 90% of export earnings and supplies about 70% of the country’s raw material requirements for industries that are agro based. It employs 80% of the nation’s work force. Agricultural output in Ethiopia consists primarily of food crops. Food crops have performed poorly. Cereal yields are much less compared to other places such as South Africa, Zimbabwe, Asia and Latin America in general.

Ethiopia’s total land area is about 1.1 million square kilometers; of which about 73.6 million hectares (66%) is estimated to be potentially suitable for agricultural production. Out of the total land suitable for agriculture, the cultivated land is estimated to be 16.5 million hectares (22%). About 96% of the cultivated land area is under small holder farming while the remaining is used for commercial farming (both state and private owned). For over 80% of peasants, the average per capita land holding, including grazing land is less than 2 hectares. Per capita cultivated land holding averaged around 0.5

12

hectares. The number is even substantially less in some densely populated high land areas.

Some 80% of food production consists of cereals, mainly maize, teff, barley and sorghum. Pulses and oilseeds are also grown extensively. The sparsely populated southern and eastern regions are largely pastoral. The livelihood of pastoralists has been seriously damaged by successive droughts since the late 1990s and pastoralists have not benefited much from the better rains in the last three seasons, which fell largely on cropping areas. It is consistently claimed that agricultural output has grown in Ethiopia, but it is very difficult to trace and calculate a reliable growth rate because of wide variations across the regions. What is real is that the country continued to be food deficit relying on external food aid for millions of its citizens and substantial portion of its population malnourished. However, it is also true that some relative improvements are made in production and productivity by the relatively small portion of the peasant farmers through increasing the amount of land cultivated, increased usage of fertilizers and extension services in, promotion of agricultural exports etc. Most of the increased yields gains in food production in Ethiopia were produced primarily through the expansion of cultivated land.

The government claims that it is focusing on rural development. This means that the agricultural sector is subsumed within a broader rural focus which cannot be sustainably financed and technically supported. The technical skills needed to support agricultural development adequately have also declined overtime. The government’s limited capacity to address the constraints on agriculture has not been used strategically to meet the diverse needs of a sector that requires coordinated intervention across a range of activities.

Adoption of a single development strategy may not bring the best results as Ethiopia is characterized by differentiated agro-ecological zones, varying landscape, and agricultural production practice. Prioritization based on growth poles and surplus producing districts helps to promote rapid and sustainable growth, which integrates the agriculture sector with other off-farm activities. The main agro-ecological zones include: (i) regions with adequate rainfall where efforts have to be exerted to efficiently utilize available rainwater to bring about the maximum possible rate of agricultural development; (ii) moisture stress areas where enhancing food security and

13

increasing off-farm income opportunities are required and (iii) pastoral areas where special efforts are required to enhance specialization in livestock production and marketing through provision of water supply, improving quality, expansion of animal health services, water points, feed production, and developing the market infrastructure. In addition introduction of intensive irrigated farming with strong government support and mechanization can effectively address food security, export and domestic raw material supply.

The key challenges and instruments to achieve these include infrastructure investment especially roads, telecommunications and electric grids; irrigation equipments; strengthening the flow of development finance; improving management and administrative capacity; agro processing and health intervention for control of malaria and other human and animal diseases. Identifying marketable products, shift to high value crops, promoting high value export crops, facilitating the commercialization of agriculture, supporting large scale commercial agriculture, integrating farms with markets, opening up growth corridors, equity in access and access to agriculture inputs and technology, extension services, research and finally practical land tenure.

Food Security: Ethiopia is constantly dependent on international aid for 10% of its annual food needs. This figure at times reaches 25% in periods such as the drought years. This means that 5 million people are living in continuous risk of food shortage and their existence is directly related to external help. Another 10 million are constantly affected by shortage in drought years. This makes it 15 million. The country has a high percentage of persistent chronically undernourished population and vulnerability is a challenge. There is a general consensus among donors and UN agencies that the past decades of food aid assistance to Ethiopia have not improved the economic status of the chronically food insecure households for a variety of reasons. The various schemes such as food for work, employment generation and safety net programmes have failed to meet development objectives.

The challenge is to have an effective Food Security Program and deliberate plan to increase agricultural productivity and diversity to overcome it once and for all. Voluntary resettlement program is also a useful tool. It is the contention of many experts that, through the combined efforts of the people of Ethiopia, if the government has serious concerns and resolve, it should be

14

possible to eliminate famine and bring about significant reduction in all manifestations of food insecurity. Ethiopia could actually not only provide food security to its people but also to the entire horn of Africa and even beyond reaching out to the Middle East. God knows what percentage of the Ethiopian people eat three decent meals a day. It is clear that most of the urban population do not. I was shocked to see one bite of hotel left over (yetrefrafi gursha in Amharic) being sold for 15 to 25 Ethiopian cents in Merkato. The level of suffering, hunger and malnutrition can never be understood or taken into account in the calculations of the so called IMF and World Bank experts advise or governments who disregard their elementary responsibility of looking after the welfare of their own citizens.

The productive safety nets project:

Despite the recovery in agriculture since the 2002/03 drought, Ethiopia continues to suffer from a structural food deficit. The government has introduced plans to end reliance on food aid in the long term. As part of this process, about 5m of the 8m people needing assistance were switched to the new, productive safety nets programme (PSNP) in 2005 and 2006. This innovative approach involves a switch from direct food aid to a mixture of food and cash aid (either via direct grants or public works programmes), and will cost about US$200m a year over five years. This has already been tried and implemented in Tigray for the last few years. It is intended to stimulate the development of local markets and enable internal trading between surplus and deficit localities, facilitated by an expanding road network. In December 2006 the World Bank approved funding of US$150m for the second phase of the productive safety nets programme (PSNP), which started in 2007. One element of the programme is to build a portfolio of drought financing instruments, including an Ethiopia-specific contingency fund, a contingency credit with the World Bank/IMF, and weather-based insurance schemes. It is hoped that a combination of all of these will limit the need for annual emergency appeals to extreme circumstances only. It is noted that the government's original plan, for the PSNP to end food aid dependency after five years (2005-09), is too optimistic, and that the programme will need to run for at least ten years to have a chance of meeting its target. However, Ethiopia’s fundamental agricultural and food security issues can only be solved through radical transformation and intense public and private partnership and action.

15

Land certification programme as a partial land tenure reform

Ethiopia’s restrictive land tenure system is a major point of controversy. All land is owned by the state, giving farmers little incentive to invest in vital productivity improvements. However, the government continues to resist calls to allow private ownership on the grounds that it would lead to the sale of land to speculators and encourage rural-urban migration, which has been relatively constrained in Ethiopia. The government is seeking a compromise and, after successful trials, started to roll out a new “certification” programme in January 2005, granting specific leasehold rights. In theory, this will allow farmers to use land as collateral, but the impact of the scheme is hard to predict, particularly as traditional systems of land tenure are being threatened by increased urbanization and industrialization. The locally based Forum for Social Studies believes that the rights being conferred on farmers will not be sufficient to encourage investment, particularly as the government retains the ultimate authority to deal with any land as it sees fit, although a compensation scheme is also promised, to deal with cases of expropriation. However, practical experience shows that the peasantry has no confidence and trust on the compensation scheme since arbitrary decision and political intervention on land issues has always been a common practice by the government and its officials. The peasants know better.

Horticulture is a new boom sector

The export-based horticulture sector, consisting mainly of flowers, is growing rapidly in Ethiopia, attracted by good growing conditions and government investment incentives (including a five-year tax holiday and cheap land leases). Flower exports grew from US$13m in 2004/05 to US$23m in 2005/06 and could earn US$100m a year within the next few years, according to the Ethiopian Horticultural Producers and Exporters’ Association (EHPEA). Ethiopia now has about 40 flower producers—up from just three in 2001—including foreign investors from the Netherlands, Germany, India and Israel. Golden Rose, a private firm that is majority-owned by UK-based Rina Investment, is the largest flower producer. The sector has faced a shortage of storage facilities and air freight capacity, but the opening of new cargo terminal at Bole airport in 2006—and the acquisition of new freight planes—is helping to correct this problem. Other challenges in the sector include poor infrastructure (roads, power and

16

telecommunications), a shortage of construction materials, delays in securing crucial imports, and limited access to bank financing.

Livestock sector grows in importance

Ethiopia is the one of the largest livestock producers in Africa, with about 35m cattle, 25m sheep and 18m goats, according to a survey in 2003. The sector accounts for almost 10% of GDP and employs over 30% of the agricultural labor force. Activity has picked up since the government ended its monopoly on livestock trading in 1999, thereby encouraging local and foreign private investment in ranches, meat-processing companies and abattoirs. Livestock and livestock by-products are export earners: sales of leather and leather products jumped from US$44m in 2003/04 to US$75m in 2005/06, while exports of meat and live animals climbed even faster, from US$10m to US$46m over the same period. Saudi Arabia is the main market for meat and live animals, although sales to Egypt started in 2005 following investment in new and upgraded abattoirs.

The sector remains underexploited. According to the Livestock Marketing Authority, this sector will benefit from a 20-year development plan being implemented by the government and the African Development Bank. Apart from the challenge of low world prices for animal products and vulnerability to drought, the sector faces a number of other problems, including a high level of illegal cross border trade in live animals; periodic import bans imposed on health grounds by key Middle Eastern buyers; unreliable supplies because of weak links between buyers and pastoralists; a scarcity of bank credit; and poor transport infrastructure. Education: Improvement has been made by expanding access to all level. The challenge here is that improving and maintaining quality, regional equity, working systems, human resources and further expansion of access in emerging regions such as Afar, Somali and improving the quality of education across the country. To its credit the government has recently conducted a big push to increase primary school enrolments, including the promotion of universal free primary education. The number of children in primary schools increased (from 8.1 million in 2001/02 to 12.6 million in 2005/06 according to government sources). The government has increased spending on education, in construction of schools, and of text books. The real problem is also the proportinalization of investment in education according to the size of the population of the specific region and their

17

contribution to the national treasury. In addition the quality of education delivered is not even. Some get better quality and provided with more quantity than others. It is too obvious and visible to see. Health: There is a very high disease occurrences of food or waterborne diseases such as bacterial and protozoal diarrhea, hepatitis A and E, and typhoid fever; vectorborne disease such as malaria and respiratory diseases such as meningitis; animal contact diseases such as rabies, and water contact diseases such as schistosomiasis are common occurrences Ethiopia also experiences a heavy burden of diseases with growing prevalence of communicable and infectious diseases. It is estimated that 10 million families live in Malaria prone areas. About 1.3 million people have HIV AIDS, of which 765,803 are women and 155,371 are children below 15 years old. About 8.2 million are reported orphans that lost their parents due to HIV/AIDS (possibly a bit exaggerated). There is an attempt and effort to expand health services, to control malaria, HIV AIDS etc. According to government statistics 670 community health posts, 5 blood banks, 11 health centers were being constructed in 2005/06.

However, this is an area where the government has drastically failed. There are some private sector developments in this areas. The government should show more commitment and resolve to support the private sector in health services. Health service is becoming totally not affordable for the ordinary people. Continued chronic shortage of health professionals coupled with high rate of staff turner over and inadequate health service management, lack of resources have made it impossible to overcome basic hygienic related diseases leave alone the major diseases that afflict the Ethiopian people. With the current level of income of the majority of the population (less than two dollars a day), basic medical services and drugs are not affordable. Water Supply and Sanitation: There is an attempt to improve access both in rural and urban areas. The challenge here is failure of keeping the proportionally small rural systems operational and maintained leave alone adding new systems which are very much in demand.

There is a total failure of financing large upfront investment cost of cities and town schemes as well as rural schemes. With the availability of numerous rivers, springs and underground water the lack of dedicated effort and mobilization of the people and all social forces have resulted in Ethiopia

18

being one of the poorest country with extremely poor supply of water and sanitation to the people. Irrigation Development: This is also one of the areas where Ethiopia could do much better and could benefit a lot. Very poor effort. Government is limited to very low level of feasibility and designed studies, construction. Land suitable for irrigation is about 3.5 million hectares. According to the data obtained from the Ministry of Agriculture and Rural Development (MoARD) and the Ministry of Water Resources (MoWR), the total irrigated land in 2005/06 stood AT 603,359 hectares; of which traditional irrigation accounts for 479,049 hectares while 124,569 hectares of land is developed through modern irrigation on of few irrigation sites.

The challenge here includes low level implementation capacity, shortage of heavy machinery and equipment, lack of capable and efficient contractors and poor managerial experience, shortage of basic inputs such as cement, lack of commitment from the government etc. Roads: This is an area where progress is made even if Ethiopia has a long way to go to reach acceptable international standard and have a network that can effectively facilitate economic growth and development. Total network of the country has increased. Proportion of roads in good condition has increased. Road network density has increased. Total network of the country reached to 39,477 Km (excluding community roads) in 2006. Road network density has increased from 32.3 Km/1000 Km2 in 2001/02 to 35.9 Km/1000 Km2 by the end of 2005/06. The challenge here is that the country has a long way to go to have an acceptable level of road network and road infrastructure that will facilitate economic development.

Lack of resources for effective and satisfactory investment in the road sector, serious financial and managerial limitations of local contractors, skills gap in road project management and management of contractors. Telecommunication: The Government has a monopoly of state-run telecommunications and mobile phone operation and no plans to license others to compete wit it. Few decades ago Ethiopia was one of the few African countries with a relatively better telecommunications system and infrastructure in Africa. However, with the advance of technology and new investment as well as interventionist states that failed to catch up with the telecommunications revolution Ethiopia is regularly mentioned as one of the

19

poorest countries that has badly lagged behind. The latest data from the International Telecommunication Union (ITU) show that Ethiopia's per capita indicators remain among the world's lowest, based on total subscriber numbers of about 1.6m in 2006, although there is likely to have been a significant improvement in 2007, assuming that the new figures given by the transport minister are correct. Unreliable and slow internet connectivity is another problem in this area. In relative terms coverage has increased, old networks have expanded and new ones have been added and the telecommunication density has some how increased. However it still remains way behind by any standard, the disparity of distribution between Addis and other regions is huge. AUS$1.5bn, infrastructure programme is currently under way to be completed in 2010. The government aims to increase the number of fixed and mobile-phone subscribers from 3.6m at present to 10m by 2010. The problem is that the Ethiopian government seems very adamant about carrying out an unrealistic telecommunication and internet operations model based on complete government control and totally inconsistent with ICT technology practices that could not be affordable and manageable for a poor and developing country like Ethiopia. Power: Again power is also an area where Ethiopia needs huge leap forward. The country has a long way to go. Four major hydropower projects with varying capacities and new transmission grid are under construction. This is an updated and readjusted version of the previous government’s plan.

The challenge here is chronic lack of power, regional imbalances, especially in the less developed part of Ethiopia. In some cases the , provision of power infrastructure is not cost effective because of low population concentration, or the high cost of reaching remote areas. The Ethiopia Electric Power Corporation (EEPCo), the state-run monopoly provider, is pushing ahead with several major electricity projects, including new hydroelectric dams (to raise generating capacity) and new transmission lines (to increase national coverage and provide export outlets to neighbouring states). Electricity interconnections with Djibouti and Sudan are scheduled for completion by early 2009, and plans for a link to Kenya are also advancing. The World Bank board was due to meet in December to consider a US$41m loan for the Ethiopia-Sudan interconnector, including

20

US$32m for the construction of transmission lines from Bahir Dar to Meteme (to link with the Sudanese network at Gallabat) and US$8m for institutional and capacity building at EEPCo. The latter amount includes funds to develop Ethiopian expertise (both technical and commercial) in electricity trading and to conduct feasibility studies into other potential links, including to Yemen, Eritrea and Somalia. Work on the Ethiopia-Djibouti connection, costing about US$45m on the Ethiopian side (and mostly funded by the AfDB) is under way after EEPCo signed construction contracts in September. In addition, EEPCo secured a US$140m loan in October from the China National Machinery and Equipment Import and Export Corporation, to help to expand the national grid and link new generating and transmission facilities.

To cope with rising demand at home and abroad, EEPCo and chosen contractors are currently building four major dams, costing about US$1.5bn in total, that are due for completion by the end of 2008 or early 2009. These are Beles (460 mw), Gilgel Gibe II (420 mw), Tekeze (300 mw) and Amerti Neshi (100 mw). Testing is due to start on Gilgel Gibe II before the end of 2007. The four dams will raise national capacity from approximately 800 mw at present to over 2,000 mw. Next in line is the massive Gilgel Gibe III station (1,870 mw), costing up to US$2bn, which is due to open in 2011/12: work started in September. Italy's Salini is playing a key role (as contractor and co-financier) in Beles, Gilgel Gibe II and Gilgel Gibe III, while Chinese contractors are building Tekeze. Several other dams are at the pre-feasibility stage, including Mendia (2,400 mw), Kara Dobi (1,700 mw) and Border (1,600 mw), according to EEPCo in November. Latest data show that power supply rose by 12.3% year on year in 2005/06, to 2.9bn kwh, while generation climbed by about 15% year on year in the first three quarters of 2006/07.

Manufacturing and Industry Development: Production of leather and leather products, semi-processed hides and skins, production of cement, development of floriculture, expansion of sugar factories (3) has increased in relative terms and there are improvements in these areas and some others. Limited privatization has taken place under very nontransparent and questionable way leading to question about the legitimacy of the transfer of public resources to the party parastatals and politically connected corrupt individuals. Export volumes commodities have shown improvements in volume and revenue.

21

The challenge in this area is the sheer low level of industrial development, constraints in the production of suitable types or raw materials, interdependence between different types of production stages (such as in spinning, weaving, finishing, sewing and accessories), structural set up problems, foreign buyers not encouraging semi processes goods at most and not finished products (lower end products), etc

The manufacturing sector remains small

Manufacturing accounted for a relatively small 3.3% of GDP in 2005/06 (rising to 5.2% of GDP with the inclusion of small-scale and cottage industries), which is a similar level to previous years. The sector is dominated by food (especially flour products, vegetable oil, and sugar), beverages (soft drinks and beer) and textiles/garments. The bulk of production is concentrated in Addis Ababa—especially in the southern suburbs—followed by Dire Dawa in the east. A number of new factories have propped up in Tigray while few are dispersed in the different regions.

Ethiopia has four sugar refineries, at Wonji, Shoa, Metahara and Fincha, all owned by the state. Production totals about 275,000 tones/year (t/y), about 85% of domestic consumption. Fincha is the largest (85,000 t/y) and the newest (built in 1999) and produces the higher-quality sugar needed for the soft drinks sector. The government is seeking private involvement in the sugar sector and plans to increase production to fully satisfy local demand and generate a surplus for export. In 2006 the government unveiled an ambitious plan to invest Birr16bn (US$1.8bn) in the sugar sector over the next six years, with the aim of raising production of processed sugar to 1.5m tones a year, of which 1m tones would be earmarked for exports. (MOFED).

New developments in the non-food sector

In the non-food sector, Slovakia’s Matador (a large, family-owned firm) joined forces with the Ethiopian state-owned Addis Tyre Company (ATC) in mid-2004, taking a 61% stake in the new joint venture—Matador Addis Tyre (MAT)—and assuming management control. MAT produces tyres for trucks and small passenger vehicles, and aims to become the market leader in Ethiopia before diversifying into regional markets. Matador promised investment of US$23m to triple output, but acknowledges the long-standing problem of competition with illegal imports. In other recent ventures, the US$25m Ethio-Iran Aluminum Factory at Sululta, 25 km from Addis Ababa,

22

opened in December 2005, with the intention of making Ethiopia self-sufficient in aluminum, while India’s Kadila group opened a new US$9m pharmaceutical factory, 20 km south of Addis Ababa, in 2006, to produce medicines used in the treatment of tuberculosis and malaria

Leather production is important in Ethiopia, and export earnings rose by 11% year on year to US$75m in 2005/06. The sector was largely liberalized in the 1990s, and the private sector owns most of the 20 tanneries. Although most leather is exported, local processing (in the form of shoe manufacturing) is expanding. The government, with help from the UN Industrial Development Organization (UNIDO), plans to invest US$7m in new shoe factories over the next five years. Ethiopia produces some of the world’s finest leather (from the highland cabretta sheep), although most output is of much poorer quality. As with other sectors, the government seeks foreign expertise and investment, and in mid-2005 handed management of the largest state tannery, Ethiopia Tannery, to UK firm Pittards, a long-term buyer of Ethiopian leather, for a five-year period. New investment takes place in shoe manufacturing: There is hope to achieve a rapid rise in the production and export of shoes, helped by the planned opening of the country's largest shoe factory in mid-2008. The US$29m venture is being undertaken by Sheba Tannery (a subsidiary of the TPLF and state-sponsored Endowment Fund for the Rehabilitation of Tigray; Effort), and aims to produce 2m pairs a year, more than doubling national production from six existing plants (two state-owned and four private). Ethiopia has a natural advantage in shoe manufacturing because of abundant leather supplies, but shoe exports remain small, at about US$6m in 2006/07 (compared with US$90m for the wider leather sector). There has been minimal foreign investment in the shoe sector to date, although Germany's Ara Shoes is now sourcing shoes from Ethiopia and plans to start local manufacture within two years. Ethiopia’s garment sector has grown rapidly from small beginnings, spurred by duty-free access to US markets under the terms of the African Growth and Opportunity Act (AGOA), passed in 2001. Garment sales under AGOA rose from US$1.8m in 2003 to US$3.5m in 2005. Garment exports to the EU are of a similar amount. The government is seeking private and foreign investment to boost activity in the sector, and is also seeking buyers for state-owned garment factories, with mixed results. Better linkages between

23

the textile and cotton sectors are also required, according to an International Labour Organization (ILO) study in 2005. The recent discussion between the Prime Minster and the representatives of the private sector business in the garment industry clearly indicated a clear example of how the private sector and the government think in parallel. The Prime Minister articulates a business model and policy that indicated the government readiness to support to the garment industry to strictly enable it to be competitive and a shot term strategic intervention to build capacity of the sector to make it competitive but tactically ignored the privileges and blanket support the party parastatals got and still get from the government. On the other hand the private sector was indicating (at least indirectly) that it should be given support in all garment related areas such as cotton production, processing and textile manufacturing in order to be able to compete first with the party parastatals and also the need to create a level playing field and equal treatment to make them competitive on the international market and promote export. Motor vehicle assembly:Ethiopia's nascent automobile industry took a step forward in October as Holland Car, an Ethiopian-Dutch joint venture established in 2005, produced the country's first locally assembled saloon car in a tie-up with China's Lifan group. Holland Car started producing a small, compact car in 2006, but the infusion of new capital from Lifan is enabling expansion. The new vehicle, branded as "Abay" and retailing at Birr140,000 (US$15,730), is assembled using imported Chinese components. The venture aims to produce about 1,000 Abays in 2008, and is also developing plans for the assembly of small commercial vehicles and mini-buses. To facilitate development in the sector, the government agreed in October to lift the 10% surtax and 2% with-holding tax levied on imported components. The future for local production is bright, given rising demand and high import tariffs (up to 150%) on imported vehicles Mining: Based on the studies conducted by the previous government, the current government has increased geosciences data quality and coverage. Different minerals have continued to be exported with foreign currency earnings. The government has conducted a relatively better promotional activities but this sector has a long way to go with a very good potential.

24

Gold attracts foreign investment

Mining accounts for only 0.5% of GDP, mainly centered around the extraction and sale of gold. In 1997 the government awarded the license to operate the country’s largest existing gold deposit, at Lega Dembi, to a Sheik Mohammed Almoudi conglomerate, MIDROC, for US$175m. Production started in 1998, and reached about 4 tones in 2002. Total gold exports, including a small amount from artisan miners, have risen steadily in recent years, from US$35m in 2001/02 to a new peak of US$65m in 2005/06, partly as a result of the improvement in world prices. Several firms are engaged in exploration, and production could reach 20-30 tones/year with sufficient investment. In mid-2005 the National Bank of Ethiopia (NBE, the central bank) lifted a 28-year ban on gold trading in an attempt to boost small-scale production and curb smuggling and black-market trading. Under the new rules, the NBE will purchase gold from licensed traders and producers, at the world market rate, and re-sell it to retailers. The NBE also plans to offer loans to businessmen wishing to set up gold-exporting ventures.

Production of non-metallic minerals—such as limestone, clay and marble for the construction sector, and salt for household use and the leather tanning industry—is also important. Ethiopia is currently assessing the viability of coal reserves at Yaya, in Oromia with a view to the possible establishment of a US$300m coal-to-fertilizer complex. The government has long sought to develop the Yaya reserves—and first issued a tender for a feasibility study for a coal-to-fertilizer plant in 1997—but their viability has never been confirmed.

Construction :A building boom

The construction sector has seen rapid growth since 1991, including large state-driven projects and smaller private ones. Hundreds of commercial buildings have been constructed throughout Addis Ababa, and in provincial centers such as Dire Dawa, Mekelle, Bahir Dar and Awassa. Private firms with close links to the ruling party and the Sheik Mohammed Alamoudi conglomerate MIDROC have been particularly successful in winning contracts, as have Chinese outfits, leading to complaints by some European competitors of unfair competition—although the government denies that non-commercial considerations apply. The Chinese firm Sinohydro has been particularly prominent, winning the US$226m contract for the Tekeze dam

25

in 2002, in a joint venture with a local construction firm, Sur, which is owned by TPLF. In 2004 Sinohydro formed a US$100m joint venture with the Ministry of Defence-owned Lalibela Engineering, to carry out construction activities throughout the country. Chinese firms are also involved in the construction of the Addis Ababa ring road, and have won contracts in housing, water supply and telecommunications. Italian firm Salini is a key player in dam construction, carrying out works funded by the Italian government.

The building boom—including road construction, hydroelectric dams and housing—put pressure on cement supplies in 2006, leading to shortages and higher prices. Current production of 1.67m tonnes a year from three existing plants—Mugar (900,000 tonnes), Mesobo (700,000 tonnes) and Dire Dawa (72,000 tonnes)—is not enough to satisfy demand, which is estimated at 2.4m tonnes a year. Imports will fill the gap in the short-term, pending the development of new capacity. Several projects are in the pipeline.

Tourism and Hotels:

Ethiopia has enormous tourism potential, based on its wealth of historical and natural sites as well as being the diplomatic center hosting AU,ECA and other Regional Centers. Visitor numbers jumped by 23.5% in 2005, to 227,000, while tourism earnings climbed by 18%, to US$134.5m, according to the Ethiopia Tourism Commission. The rate of increase is surprising in view of the widespread unrest that took place after the disputed election in May 2005 (which led to a high number of cancellations, according to reports at the time), but reflects Ethiopia's strong attractions, good air links and the country's relative stability compared with the last three decades of the 20th century. It is likely that business and conference traffic to Addis Ababa accounts for the majority of arrivals—but the northern tourist route, taking in the famous rock-hewn Ethiopian Orthodox churches in Lalibela, continues to attract a rising number of visitors (18,000 in 2005).

Hotel construction, especially in the capital, is gathering pace. The Addis Sheraton (one of only two five-star hotels at present, along with the Addis Hilton) is adding capacity, while a joint venture between Kuwait’s Al-Kharafi construction group (60%) and French hotel group, Accor (40%), plans two hotels, a four-star Novotel and a three-star Ibis, in Addis Ababa’s Meskel Square: construction started in early 2007 after planning delays. The Strandwood Hotel Group of Ireland and local partners plan a new, four-star

26

hotel in the capital—the Emerald Addis Hotel—which is due to open in 2008. Ethiopia has high hopes for tourism, and aims to raise visitor numbers to 500,000 by 2010, and to become one of Sub-Saharan Africa's top-ten destinations by 2020. However, the sector remains constrained by a deficit in both the quantity and the quality of hotels and other tourism infrastructure and services, especially outside the capital. Regional instability along Ethiopia's borders and internal discontent also remains a deterrent.

The 2005 post election crisis, political repression and continued tension has increased uncertainty and is descending into some kind of ethnic tension which is discouraging for rapid growth of the Tourist Industry. Safety and security as well as political stability are preconditions for the growth of the Tourist Industry.

Foreign Direct Investment

Ethiopia started to liberalize its investment code in the mid-1990s, including a partial opening of the telecommunications and energy sectors, but initial efforts were undermined by the 1998-2000 war with Eritrea. Liberalization made a significant step forward in April 2003, with many restrictions on domestic and foreign investors being lifted, although the former benefited the most. All activities are now open to the domestic private sector, except three: the supply of electricity via the national grid; postal services (apart from couriers); and air transport using planes with more than 20 seats. Sectors newly opened to foreigners include air freight and the import of cooking gas, although several sectors remain closed, including banking and domestic wholesale and retail trade. Significantly, minimum investment by foreign firms was reduced from US$500,000 to US$100,000, or from US$300,000 to US$60,000 in the case of joint ventures. Minimum capital requirements were lifted entirely for investors exporting at least 75% of their output. The three-year tax holiday for agribusiness ventures that export at least 50% of their production was extended to five years

Growth of Foreign investment is not at the required level and pace: Foreign direct investment (FDI) inflows to Ethiopia fell by more than one-half in 2005, to US$205m (from a record US$545m in 2004), according to the latest World Investment Report from the UN Conference on Trade and Development (UNCTAD). The decline undoubtedly reflects the political turbulence that followed the disputed elections in May 2005. There is considerable uncertainty about levels of Ethiopian FDI. The IMF, for

27

example, records FDI of US$100m in 2003/04 and US$150m in 2004/05, rising to an estimated US$170m in 2005/06. It is not clear where UNCTAD's much higher figures come from, but the discrepancy partly reflects statistical weakness in Ethiopia. Notably, UNCTAD highlights that Ethiopia is a key recipient of FDI from the category of "developing and transition" economies, which accounted for 51% of FDI into Ethiopia in 2002-04. This flow FDI also illustrates the prominent role played by Saudi Arabia's Sheikh Mohamed Al-Moudi (who is acknowledged to be Ethiopia's largest foreign investor) and his Mohamed International Development Research Organization Companies (MIDROC). Ethiopia has also secured FDI from other non-traditional sources such as China, India, Turkey, Iran and Slovakia.

As part of the effort to boost FDI, the government established the National Foreign Investment Advisory Council in October 2006, including representatives from government ministries, the Ethiopian Investment Agency, the Privatization and State Enterprises Supervising Agency (PPESA) and private companies (both foreign and local). The council has been tasked with finding over 40 foreign investors in the 2006/07 financial year, including ten in agro-processing, ten in horticulture, 15 in textiles and garments, and the rest in shoes. The composition of the council is designed to offer expertise (and facilitate practical arrangements) in several key areas including land acquisition, financing and the provision of infrastructure. The council met for the first time in November 2006 and plans to convene every two months.

The political and governance condition, Ethiopia’s role in the sub region as well as stability and overall long term security plays a fundamental role in attracting FDI and making it part of the overall strategy for economic growth and prosperity. Under the circumstances and particularly with continued war, conflict, internal political repression and tension it is unlikely that Ethiopia can attract a reasonable and competitive FDI. IF we look at a comparative example in 2006 Turkey got US $20 billion, Saudi $18 billion, United Arab Emirates $8 billion, China $69 billion, Hong Kong $43 billion, India $17 billion, Africa in general $36 billion (Economy Today-issue No.39 November 2007). In addition Egypt got 45.3 billion, South Africa got $5.2 billion, Nigeria got $2 billion (Wporld Development Indicators database). Ethiopia with the current political situation and lack of long term political stability and deepening democracy, is unlikely to go near these

28

kinds of investments which will have a significant impact in alleviating poverty and bringing in regional stability and prosperity.

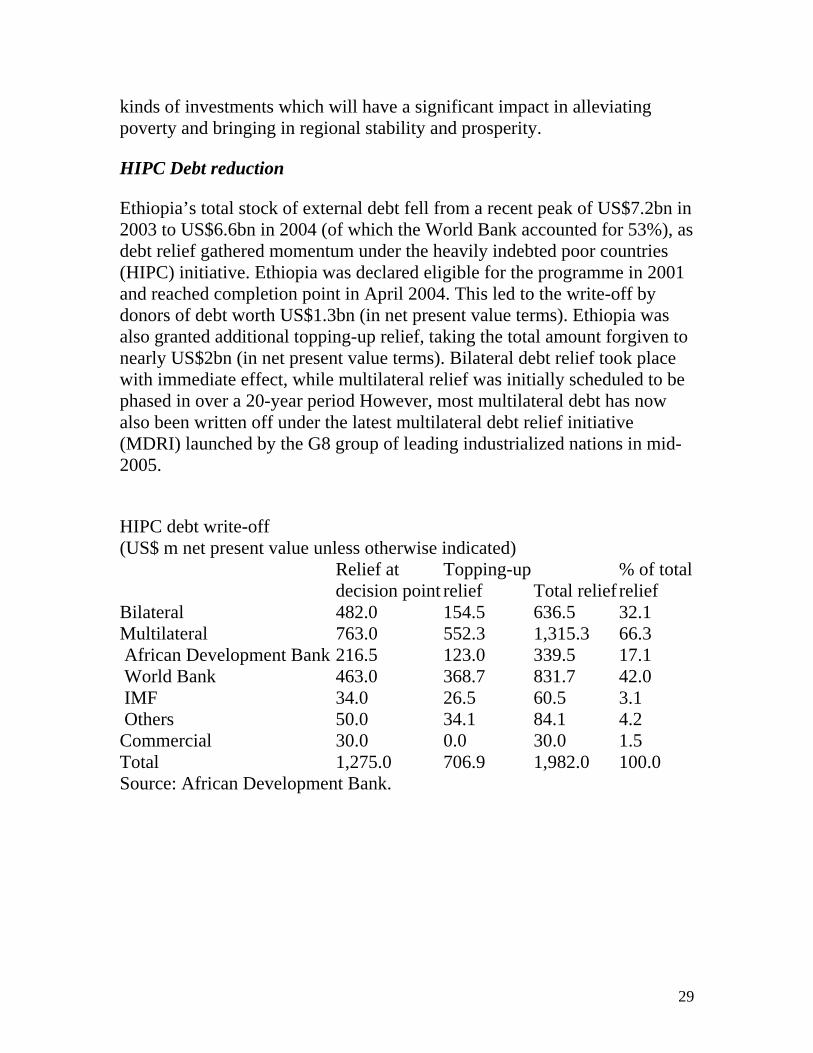

HIPC Debt reduction

Ethiopia’s total stock of external debt fell from a recent peak of US$7.2bn in 2003 to US$6.6bn in 2004 (of which the World Bank accounted for 53%), as debt relief gathered momentum under the heavily indebted poor countries (HIPC) initiative. Ethiopia was declared eligible for the programme in 2001 and reached completion point in April 2004. This led to the write-off by donors of debt worth US$1.3bn (in net present value terms). Ethiopia was also granted additional topping-up relief, taking the total amount forgiven to nearly US$2bn (in net present value terms). Bilateral debt relief took place with immediate effect, while multilateral relief was initially scheduled to be phased in over a 20-year period However, most multilateral debt has now also been written off under the latest multilateral debt relief initiative (MDRI) launched by the G8 group of leading industrialized nations in mid-2005.

HIPC debt write-off (US$ m net present value unless otherwise indicated) Relief at Topping-up % of total decision point relief Total relief relief Bilateral 482.0 154.5 636.5 32.1 Multilateral 763.0 552.3 1,315.3 66.3 African Development Bank 216.5 123.0 339.5 17.1 World Bank 463.0 368.7 831.7 42.0 IMF 34.0 26.5 60.5 3.1 Others 50.0 34.1 84.1 4.2 Commercial 30.0 0.0 30.0 1.5 Total 1,275.0 706.9 1,982.0 100.0 Source: African Development Bank.

29

Britton Woods Institutes cancelled Ethiopia’s debts

Ethiopia was named as one of the beneficiaries of the US$40bn MDRI agreed by the G8 at the Gleneagles summit in mid-2005. The G8 proposed a full write-off of all debts owed to the World Bank, the IMF and the African Development Bank for 18 poor countries that have reached completion point under the HIPC. In December 2005 the IMF agreed to write-off debts owed to the Fund by the 18 states—amounting to US$161m in Ethiopia’s case. The World Bank’s soft-arm loan, the International Development Association (IDA), made a similar decision in April 2006, which is having a much greater impact on Ethiopia. Reductions in debt-service costs are earmarked for poverty-reduction initiatives. As a result of debt relief, the Economist Intelligence Unit estimates that Ethiopian external debt fell to US$2.8bn at the end of 2006.

Soviet debt is cancelled

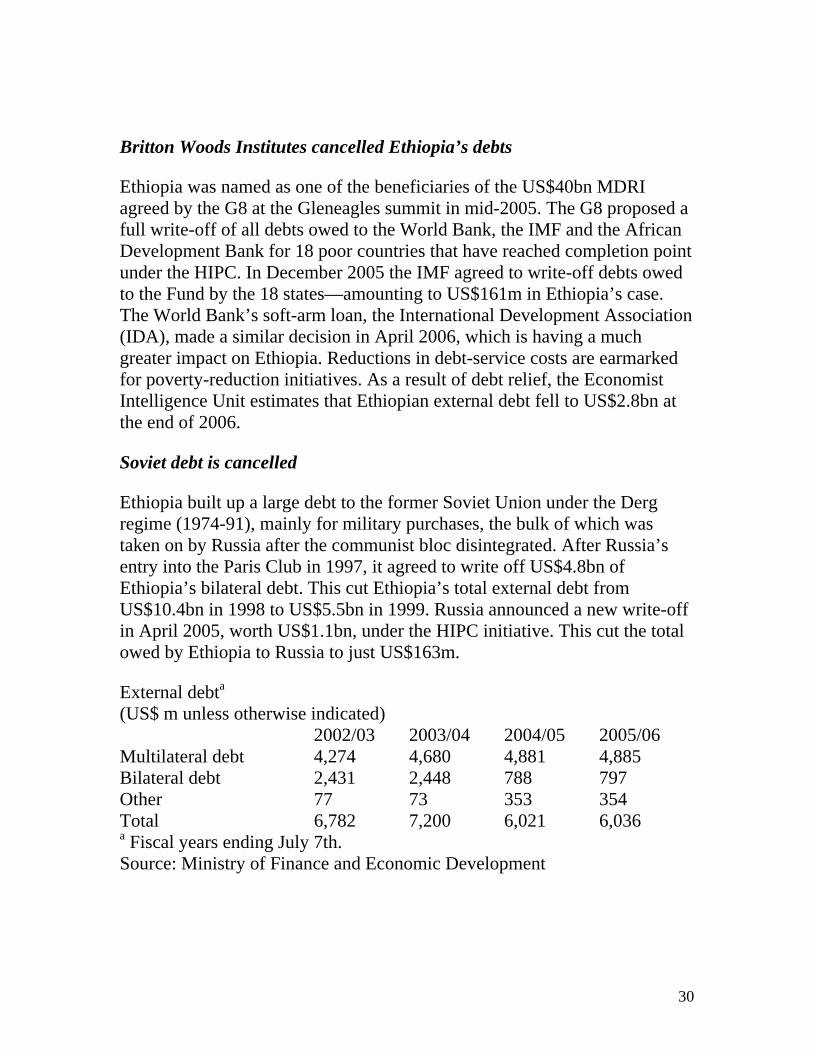

Ethiopia built up a large debt to the former Soviet Union under the Derg regime (1974-91), mainly for military purchases, the bulk of which was taken on by Russia after the communist bloc disintegrated. After Russia’s entry into the Paris Club in 1997, it agreed to write off US$4.8bn of Ethiopia’s bilateral debt. This cut Ethiopia’s total external debt from US$10.4bn in 1998 to US$5.5bn in 1999. Russia announced a new write-off in April 2005, worth US$1.1bn, under the HIPC initiative. This cut the total owed by Ethiopia to Russia to just US$163m.

External debta (US$ m unless otherwise indicated) 2002/03 2003/04 2004/05 2005/06 Multilateral debt 4,274 4,680 4,881 4,885 Bilateral debt 2,431 2,448 788 797 Other 77 73 353 354 Total 6,782 7,200 6,021 6,036 a Fiscal years ending July 7th. Source: Ministry of Finance and Economic Development

30

Foreign reserves and the exchange rate

Foreign-exchange reserves are under pressure

Ethiopia’s official foreign-exchange reserves declined steadily in the late 1990s, to US$306m in 2000, owing mainly to the costs of buying arms and munitions to prosecute the war with Eritrea. The return to normality, coupled with high levels of donor support, pushed reserves to an historic high of nearly US$1.5bn at the end of 2004, equivalent to a healthy five months of goods and services imports. However, reserves weakened from mid-2005 onwards, reaching US$756m in November 2006, because of rising imports (as a result of growth-driven demand and high oil prices) and reduced donor inflows following election-related unrest. Import cover is currently below the generally accepted standard of three months.

Progressive depreciation of the currency ( birr)

Ethiopia established an interbank foreign-exchange market in October 2001, replacing part-managed foreign-exchange auctions, as part of the move to a market-determined exchange rate. However, some restrictions on the movement of money persist. The foreign-exchange market remains dominated by the Commercial Bank of Ethiopia (CBE), although private banks are handling a rising share of remittances. Ethiopian policy favors a cautious depreciation of the birr, which gently subsided against the dollar, by 0.4% a year, from Birr8.57:US$1 in 2002 to Birr8.69:US$1 in 2006. However, the decline in foreign-exchange reserves in 2005 and 2006 has put greater pressure on the birr. This is reflected in a larger premium on the informal, parallel market and faster depreciation of the official rate, which slipped by 0.8% year on year in December 2006 to Birr8.75:US$1. The adjustment is not surprising, as the IMF has considered the birr to be overvalued, although we do not anticipate any major exchange-rate instability and Ethiopia should take these type of IMF advise with a grain of salt and not taken at their face value.

Private Sector development: Private industry is dominated by leading politicians

31

Fifteen years after the Ethiopian People’s Revolutionary Democratic Front (EPRDF) came to power, the private sector is dominated by two interlocking conglomerates: one set of companies is associated with the TPLF Party Prastatals, members of the ruling party or regional government bodies and the other with an Ethiopian-Saudi entrepreneur, Mohammed al-Moudi, . The predominance of party-owned companies in key sectors is bitterly resented by independent private entrepreneurs as well as the general population which sees this as Ethnic based deliberate systemic economic domination and exploitation . The World Bank and many internal as well as external observers as well as business people note that party-owned enterprises enjoy preferential access to contracts, access to capital, physical infrastructure and administrative services, tax breaks and other politically motivated privileged supports. In order to “level the playing field”, the government have to devise new competition policies and dismantle and privatize these party parastatals in a transparent way or this will have a long term consequence and loss of trust as well as confidence among the different political and economic contenders.

Ethiopia’s business environment has a number of failings. Ethiopia’s private sector has a low number of firms; small-sized firms; low labor productivity (50% lower than China, although local wages are only 30% lower); and little propensity to export (most private firms produce for the local market). Apart from the obvious problem of high transport costs, several related constraints are identifies to private-sector development, including:

• the dominant role of the state; • an absence of fair competition; • weak institutional support for business; • low skill levels in the private sector; and • a lack of external integration.

However, with some recognizable developments in the private sector, the government appear to have stalled Private sector reform by tampering in the privatization program and slowing down until it fits its party pararstatals strategic positioning to play a dominating role and position. IT and Telecommunications is the best example. These are areas where the party parastatls are weak and unable to compete and therefore the entire process of modernizing and increasing the role of the private sector is delayed until they catch up and are ready to be major players. There are also sustained

32