Embed Size (px)

DESCRIPTION

The global firm’s profit. We have the two equations : R' = C' + I' flow (1) 100 = 60 + 40 R' = C + S m reflux (2) 100 = 80 + 20 So the global firm’s profit : = C – C' = I' - S m = 20 (3) et (4). The global firm’s accounts. Desagregation of global firm in two sectors. - PowerPoint PPT Presentation

Citation preview

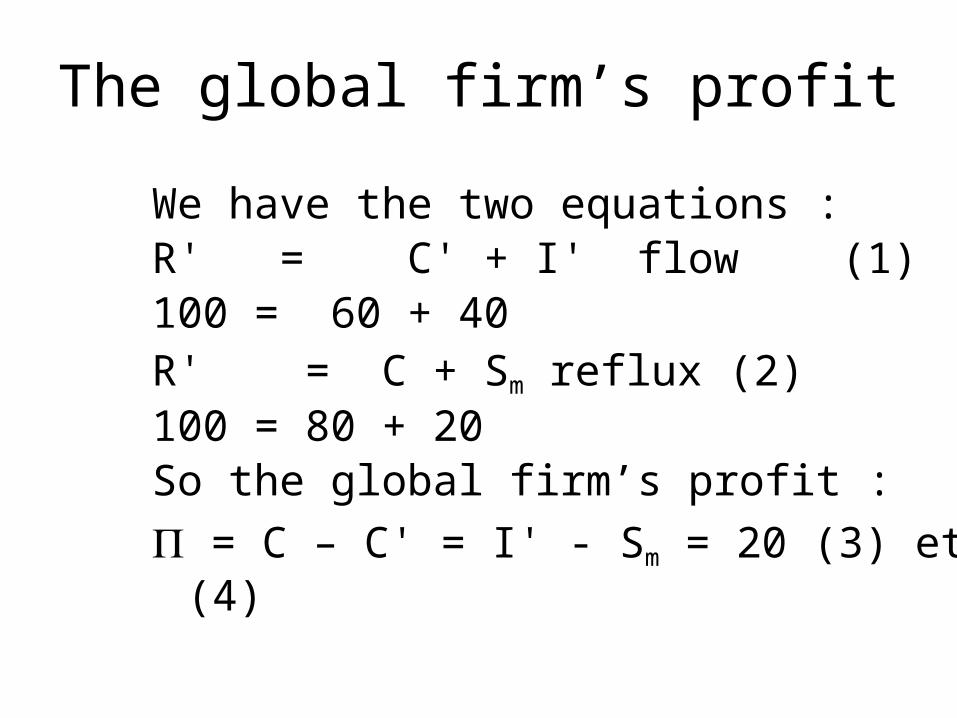

The global firm’s profit

We have the two equations :R' = C' + I' flow (1)100 = 60 + 40R' = C + Sm reflux (2)100 = 80 + 20So the global firm’s profit :

= C – C' = I' - Sm = 20 (3) et (4)

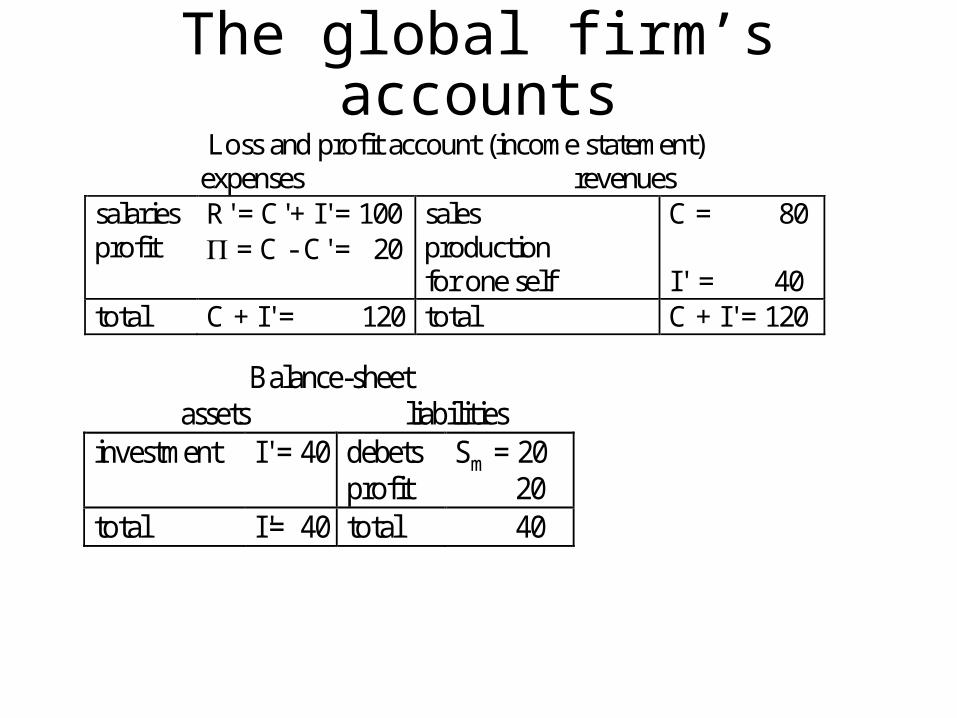

The global firm’s accountsLoss and profit account (income statement)

expenses revenues salaries profit

R' = C' + I' = 100 = C - C' = 20

sales production for one self

C = 80

I' = 40

total C + I' = 120 total C + I' = 120

Balance-sheet assets liabilities

investment I' = 40

debets profit

Sm = 20 20

total I'= 40 total 40

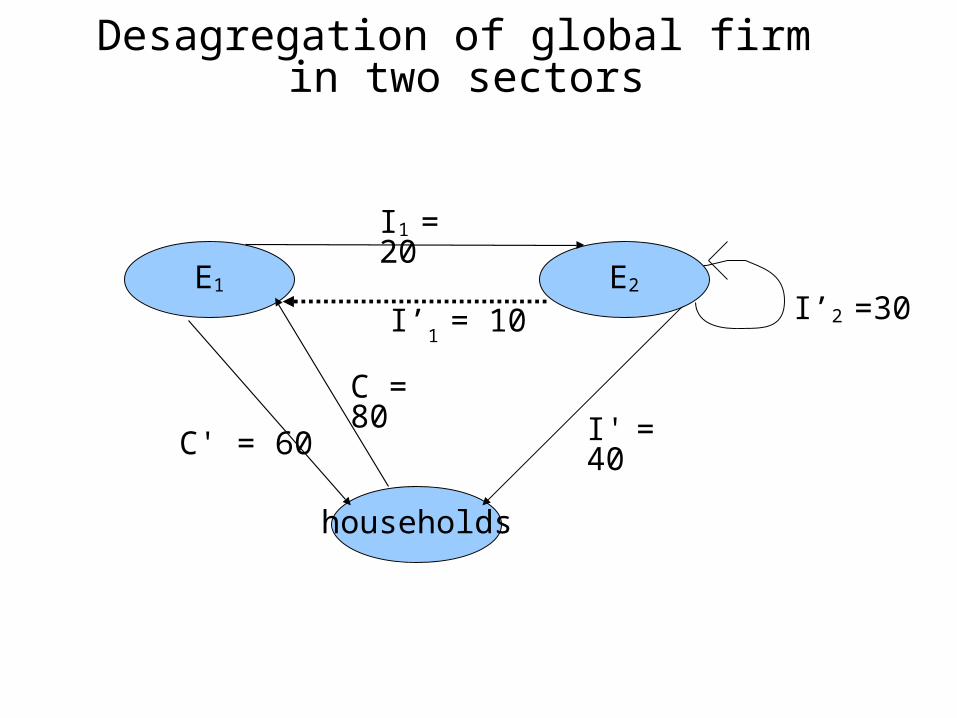

Desagregation of global firm in two sectors

households

E1

I’2 =30E2

I’1 = 10

I1 = 20

I' = 40C' = 60

C = 80

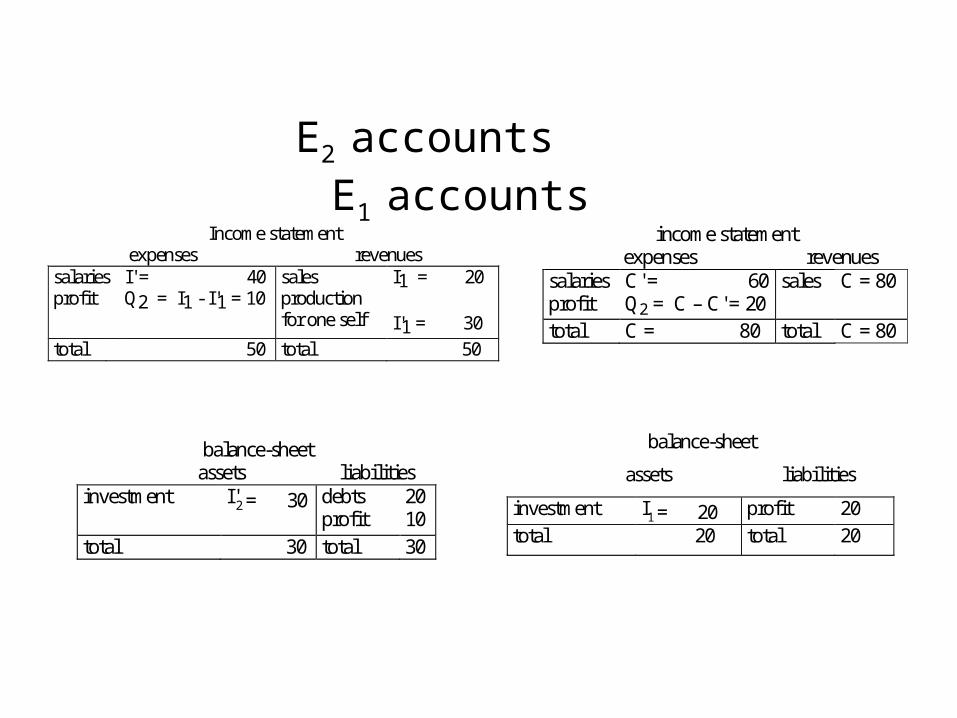

E2 accounts E1 accounts

c o m p t e d e r é s u l t a t c h a r g e s p r o d u i t s s a l a i r e s p r o f i t I ' = 4 0 Q 1 = I 2 - I ' 2 = 3 0 v e n t e s p r o d u c t i o n i m m o b i l i s é e I 2 = = 6 0 I ' 1 = 1 0 t o t a l I ' 1 + I 2 = 7 0 t o t a l I ' 1 + I 2 = 7 0

Income statement expenses revenues

salaries profit

I' = 40 Q2 = I1 - I'1 = 10

sales production for one self

I1 = 20 I'1 = 30

total 50 total 50

income statement expenses revenues

salaries profit

C' = 60 Q2 = C – C' = 20

sales

C = 80

total C = 80 total C = 80

balance-sheet assets liabilities

investment

I'2 = 30

debts profit

20 10

total 30 total 30

balance-sheet

assets liabilities

investment I1 = 20 profit 20

total 20 total 20

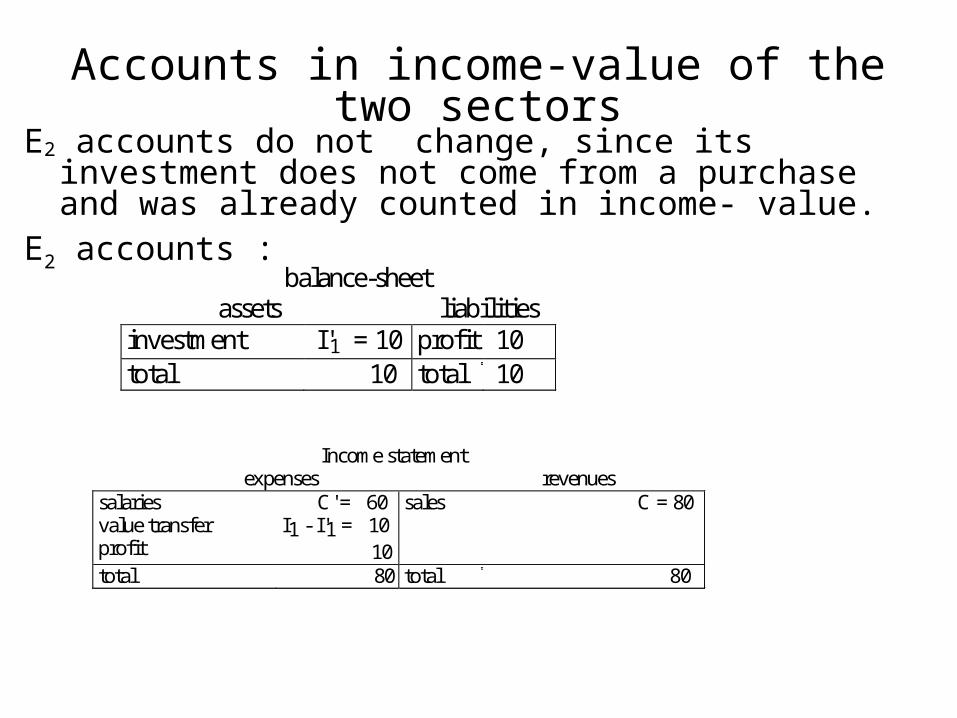

Accounts in income-value of the two sectorsE2 accounts do not change, since its investment does not come

from a purchase and was already counted in income- value.E2 accounts :

v a r i a t i o n d u b i l a n v a r . d e l ' a c t i f v a r . d u p a s s i f I m m o b i l i s a t i o n s P e r t e I ' 2 = 3 0 1 0 d e t t e s 4 0 t o t a l 4 0 t o t a l 4 0 v a r i a t i o n d u b i l a n v a r . d e l ' a c t i f v a r . d u p a s s i f I m m o b i l i s a t i o n s P e r t e I ' 2 = 3 0 1 0 d e t t e s 4 0 t o t a l 4 0 t o t a l 4 0 v a r i a t i o n d u b i l a n v a r . d e l ' a c t i f v a r . d u p a s s i f I m m o b i l i s a t i o n s P e r t e I ' 2 = 3 0 1 0 d e t t e s 4 0 t o t a l 4 0 t o t a l 4 0 v a r i a t i o n d u b i l a n v a r . d e l ' a c t i f v a r . d u p a s s i f I m m o b i l i s a t i o n s P e r t e I ' 2 = 3 0 1 0 d e t t e s 4 0 t o t a l 4 0 t o t a l 4 0

v a r i a t i o n d u b i l a n v a r . d e l ' a c t i f v a r . d u p a s s i f I m m o bi l i s a t i o n s P e r t e I ' 2 = 3 0 1 0 de t t e s 4 0 t o t a l 4 0 to t a l 4 0

balance-sheet assets liabilities investment I'1 = 10 profit 10 total 10 total 10

Income statement expenses revenues

salaries value transfer profit

C' = 60 I1 - I'1 = 10 10

sales C = 80

total 80 total 80

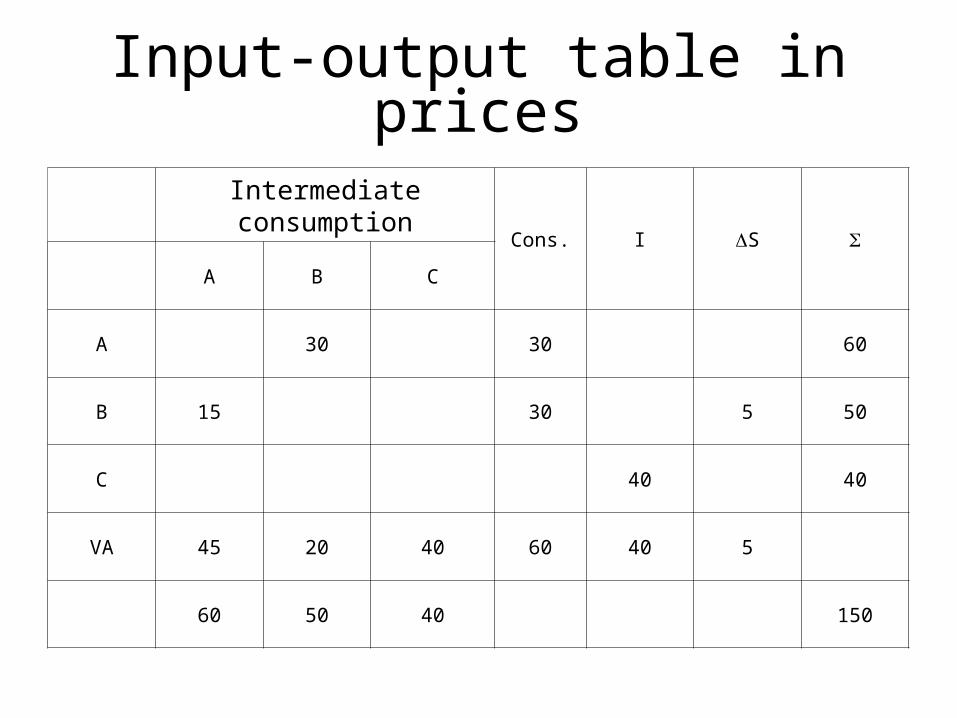

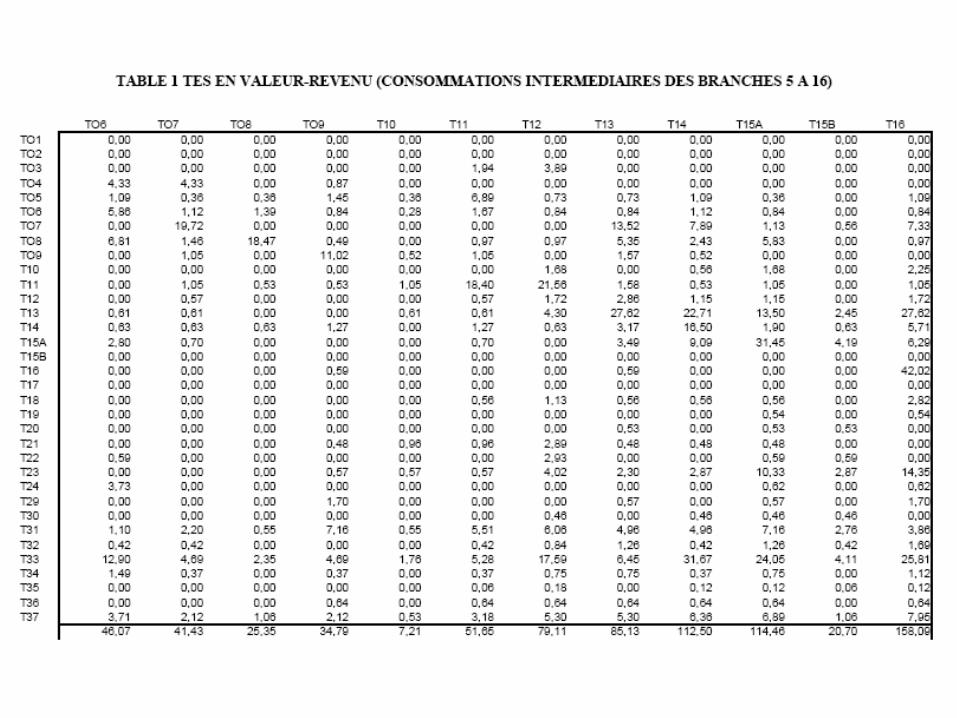

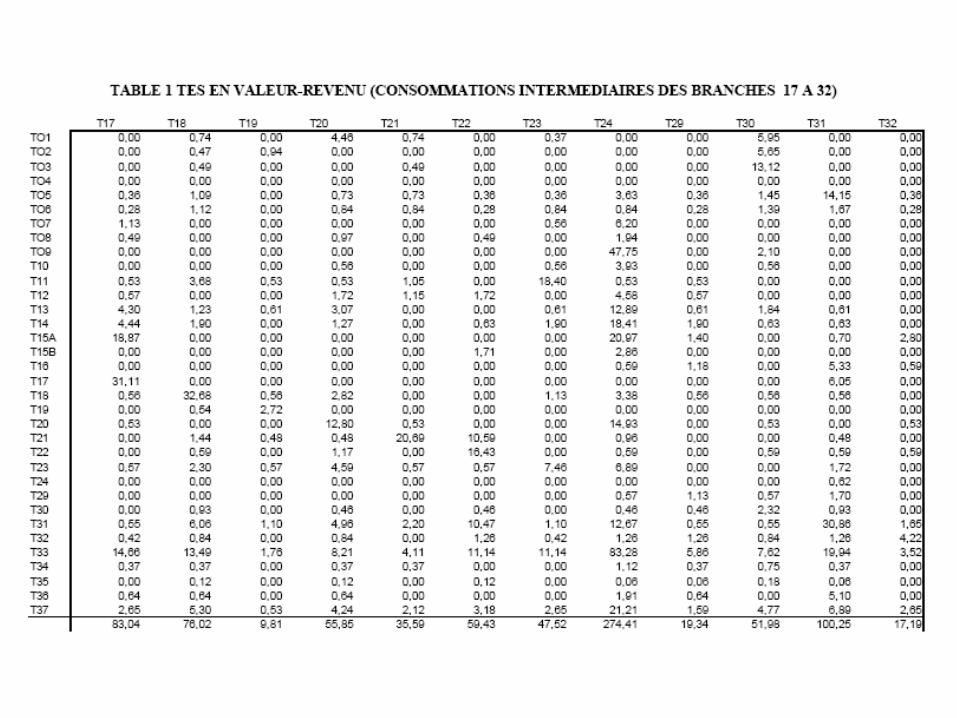

Input-output table in prices

iron corn

iron qipi piI i

corn qcpc pcC c

vai vac

i c

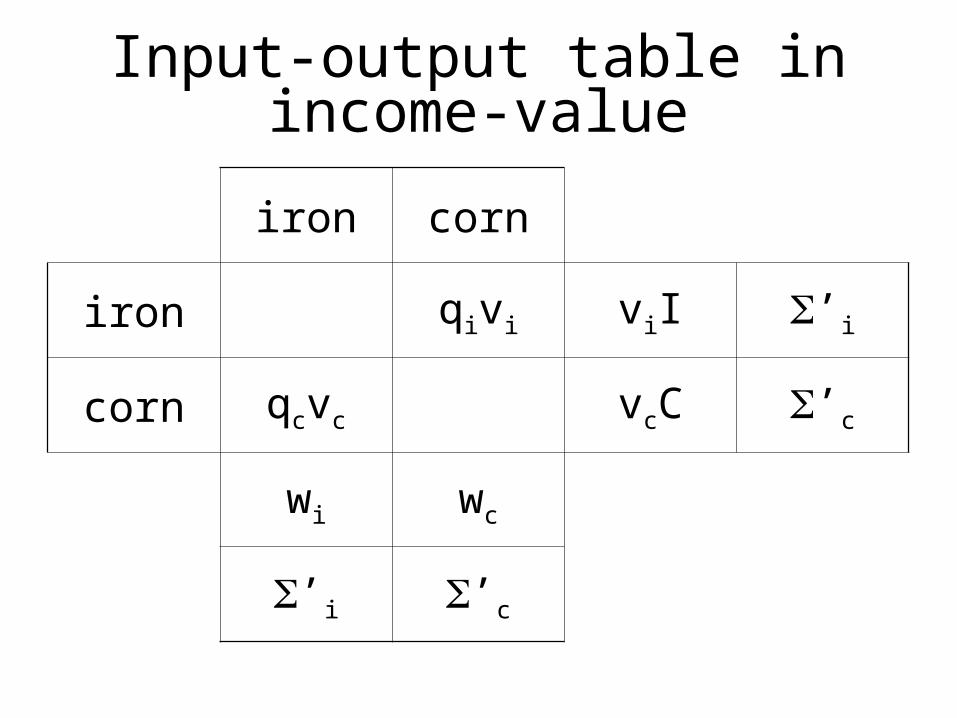

Input-output table in income-value

iron corn

iron qivi viI ’i

corn qcvc vcC ’c

wi wc

’i ’c

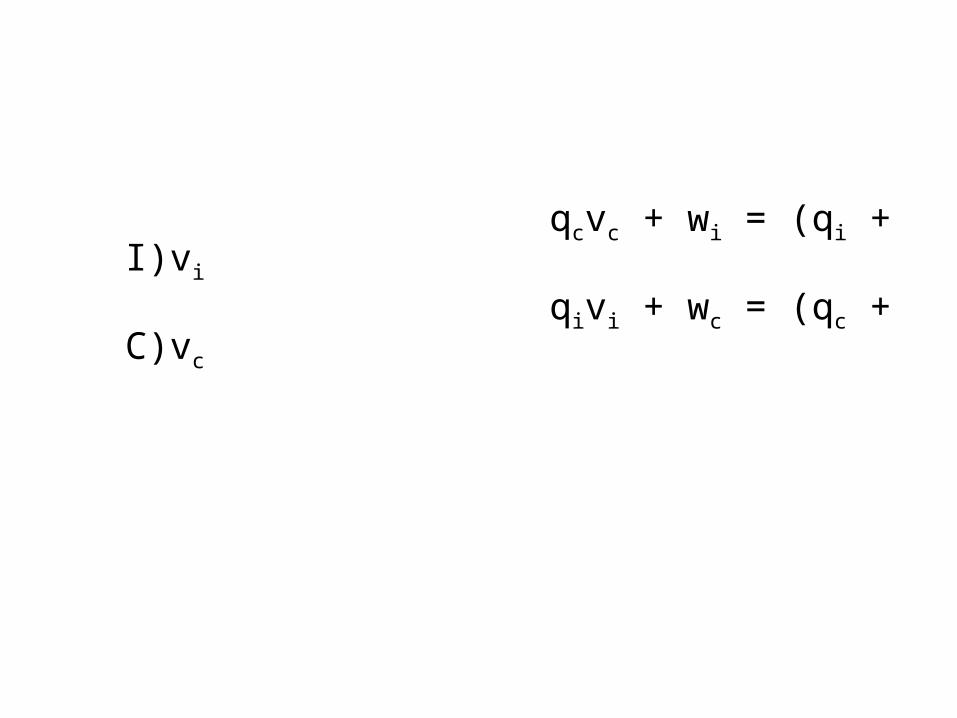

qcvc + wi = (qi + I)vi qivi + wc = (qc + C)vc

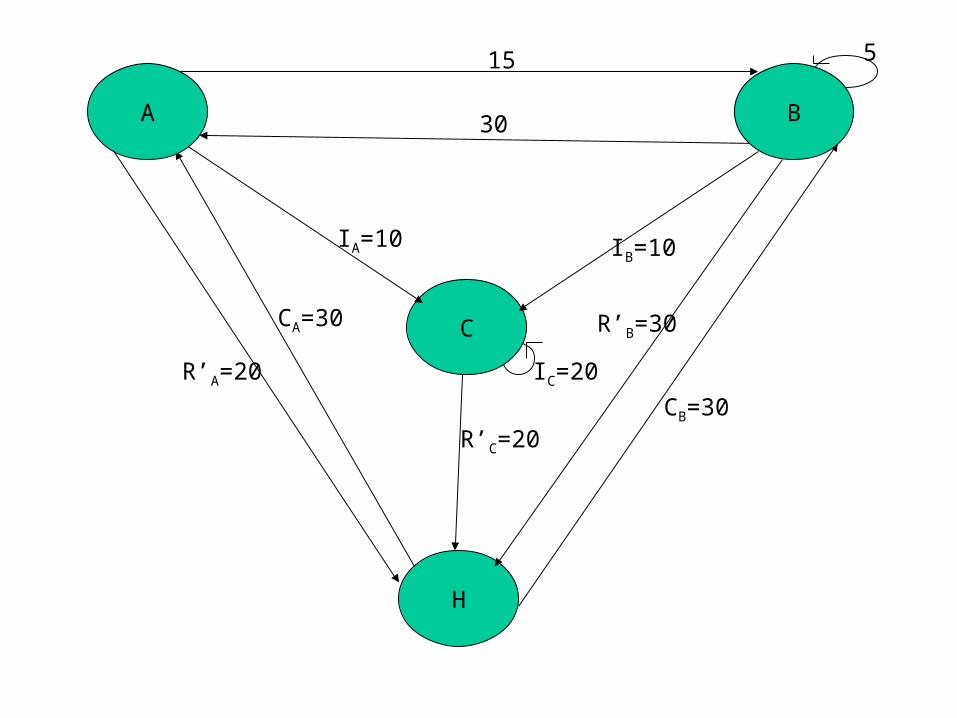

C

H

A B

15

30

IB=10

CB=30

R’B=30

R’C=20

R’A=20

CA=30

IA=10

IC=20

5

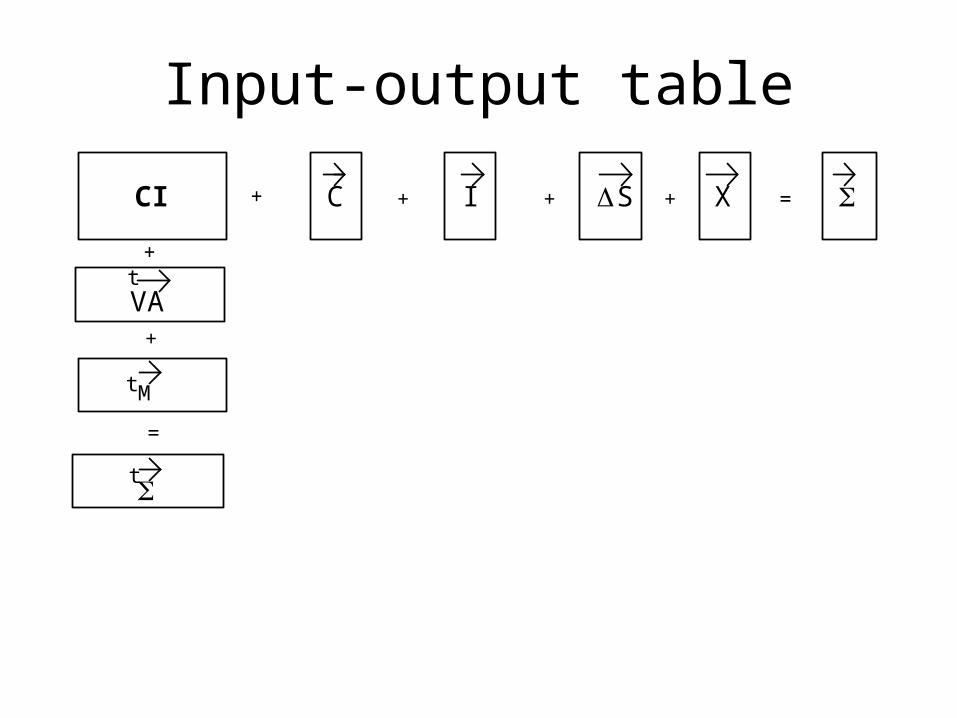

Input-output table

+CI + C + I + S X =

+tVA

+

t M

=

t

Input-output table in prices

Intermediate consumptionCons. I S

A B C

A 30 30 60

B 15 30 5 50

C 40 40

VA 45 20 40 60 40 5

60 50 40 150

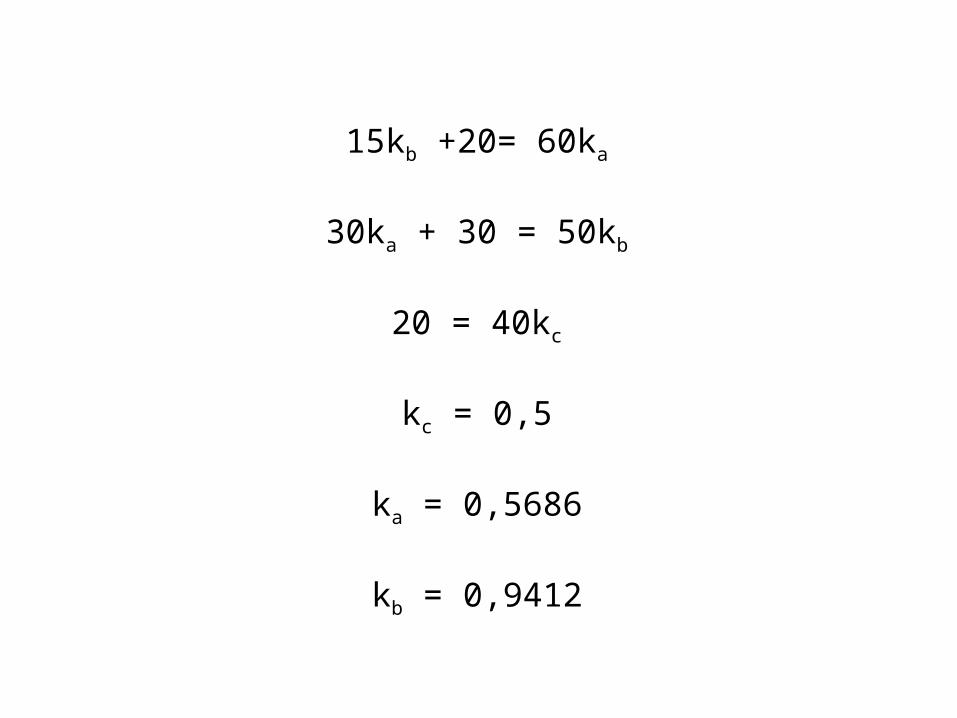

15kb +20= 60ka

30ka + 30 = 50kb

20 = 40kc

kc = 0,5

ka = 0,5686

kb = 0,9412

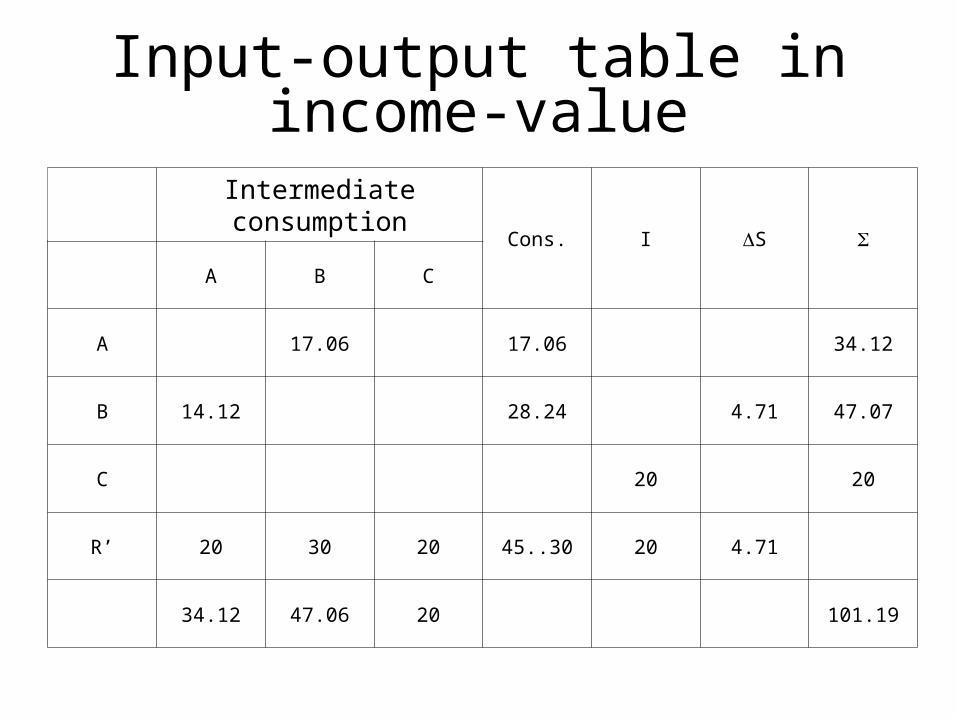

Input-output table in income-value

Intermediate consumptionCons. I S

A B C

A 17.06 17.06 34.12

B 14.12 28.24 4.71 47.07

C 20 20

R’ 20 30 20 45..30 20 4.71

34.12 47.06 20 101.19

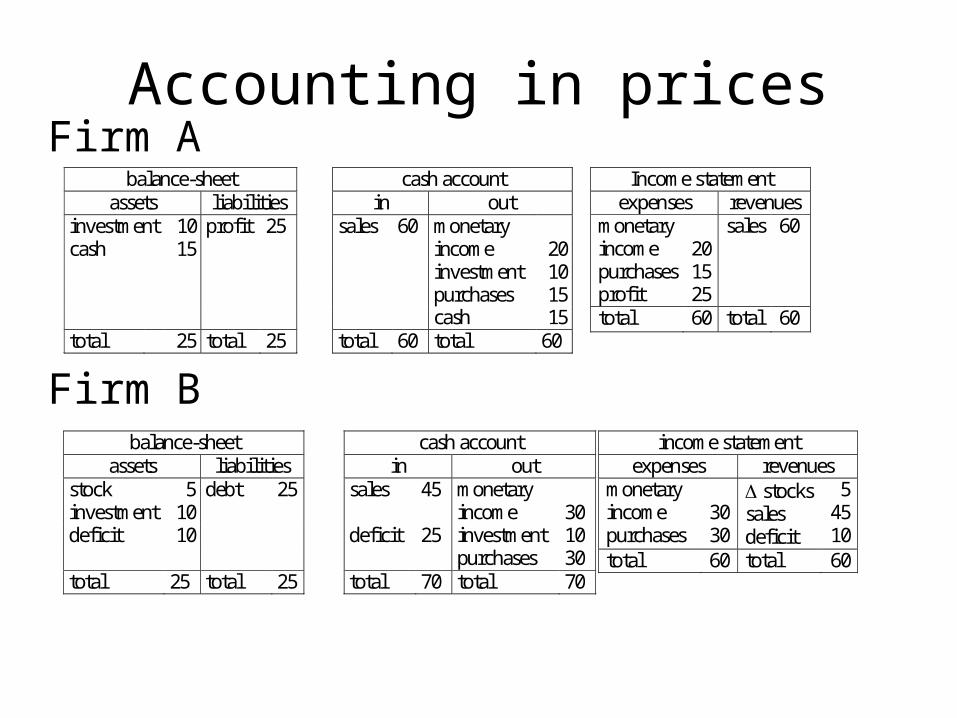

Accounting in pricesFirm A

Firm B

balance-sheet cash account assets liabilities

in out

investment cash

1015

profit 25 sales 60 monetary income

20

investment 10 purchases 15 cash 15 total 25 total 25 total 60 total 60

Income statement expenses revenues

monetary income purchases profit

20 15 25

sales

60

total 60 total 60

balance-sheet cash account assets liabilities in out

stock investment

5 10

debt 25 sales 45 monetary income

30

deficit 10 deficit 25 investment 10 purchases 30 total 25 total 25 total 70 total 70

income statement expenses revenues

monetary income purchases

30 30

stocks sales deficit

5 45 10

total 60 total 60

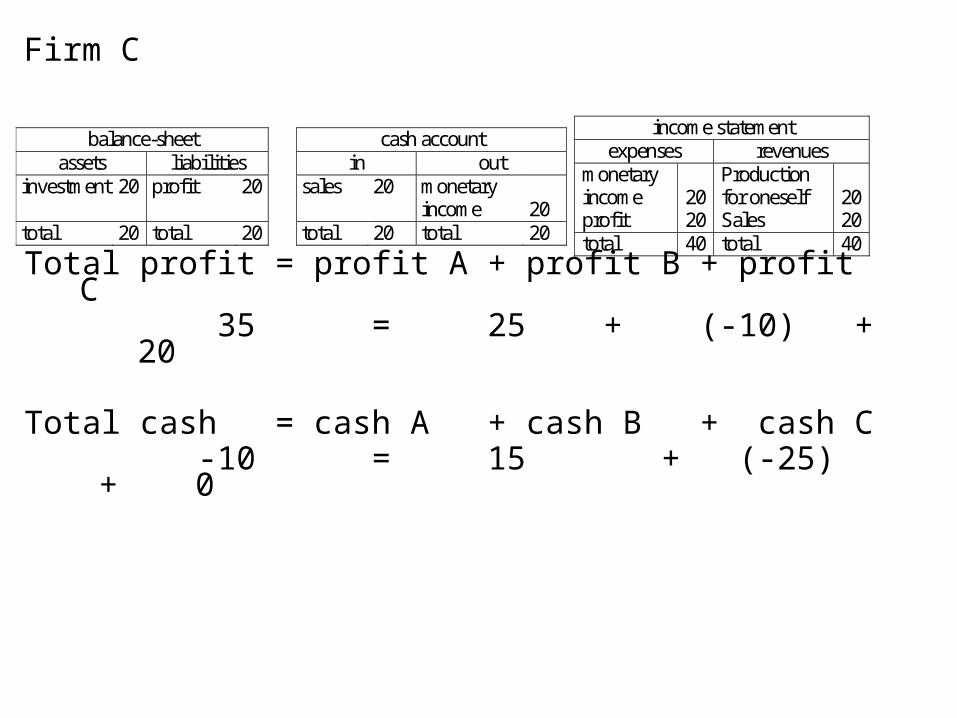

Firm C

Total profit = profit A + profit B + profit C 35 = 25 + (-10) + 20

Total cash = cash A + cash B + cash C -10 = 15 + (-25) + 0

balance-sheet cash account assets liabilities in out

investment 20 profit 20 sales 20 monetary income

20

total 20 total 20 total 20 total 20

income statement expenses revenues

monetary income profit

20 20

Production for oneself Sales

20 20

total 40 total 40

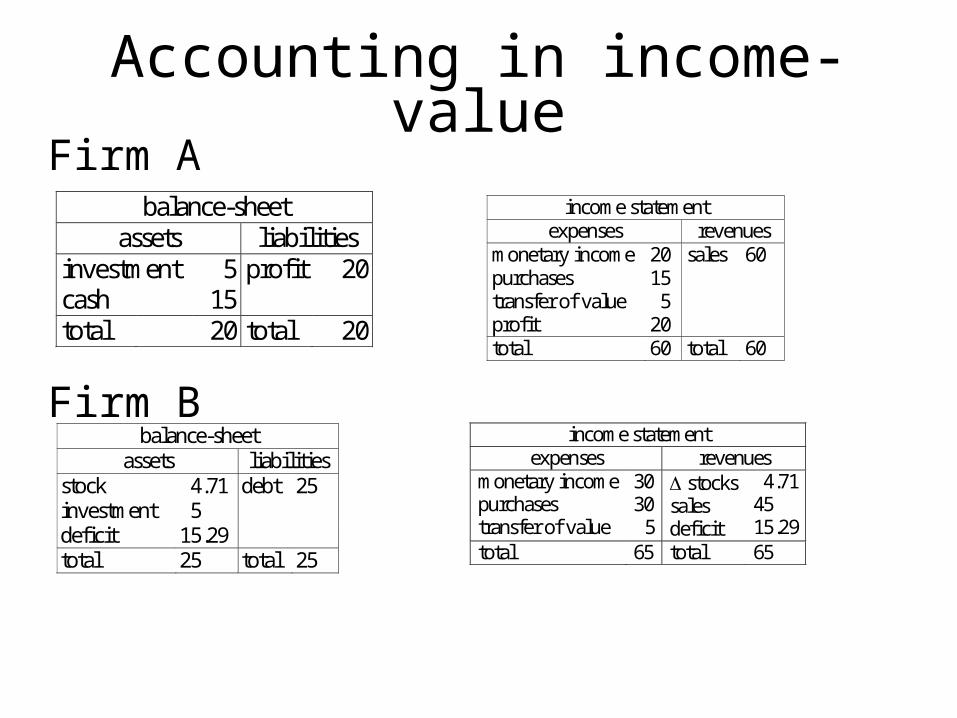

Accounting in income-valueFirm A

Firm B

income statement expenses revenues

monetary income purchases transfer of value profit

20 15 5 20

sales

60

total 60 total 60

balance-sheet assets liabilities

investment cash

5 15

profit 20

total 20 total 20

balance-sheet assets liabilities

stock investment

4.71 5

debt 25

deficit 15.29 total 25 total 25

income statement expenses revenues

monetary income purchases transfer of value

30 30 5

stocks sales deficit

4.71 45 15.29

total 65 total 65

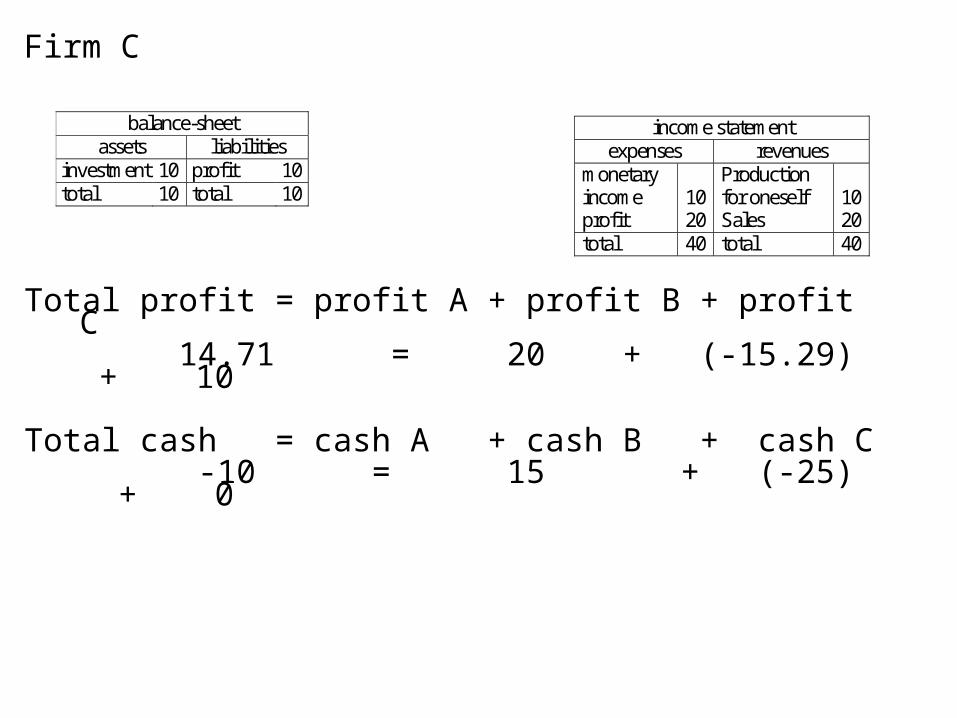

Firm C

Total profit = profit A + profit B + profit C 14.71 = 20 + (-15.29) + 10

Total cash = cash A + cash B + cash C -10 = 15 + (-25) + 0

balance-sheet assets liabilities

investment 10 profit 10 total 10 total 10

income statement expenses revenues

monetary income profit

10 20

Production for oneself Sales

10 20

total 40 total 40

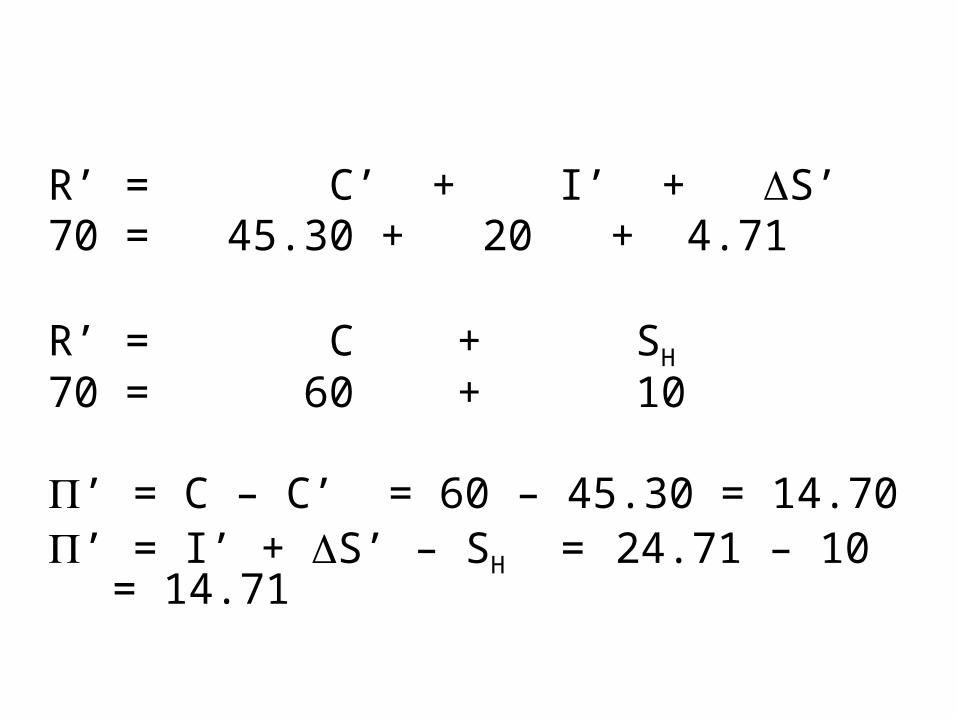

R’ = C’ + I’ + S’70 = 45.30 + 20 + 4.71

R’ = C + SH

70 = 60 + 10

’ = C – C’ = 60 – 45.30 = 14.70’ = I’ + S’ – SH = 24.71 – 10 = 14.71

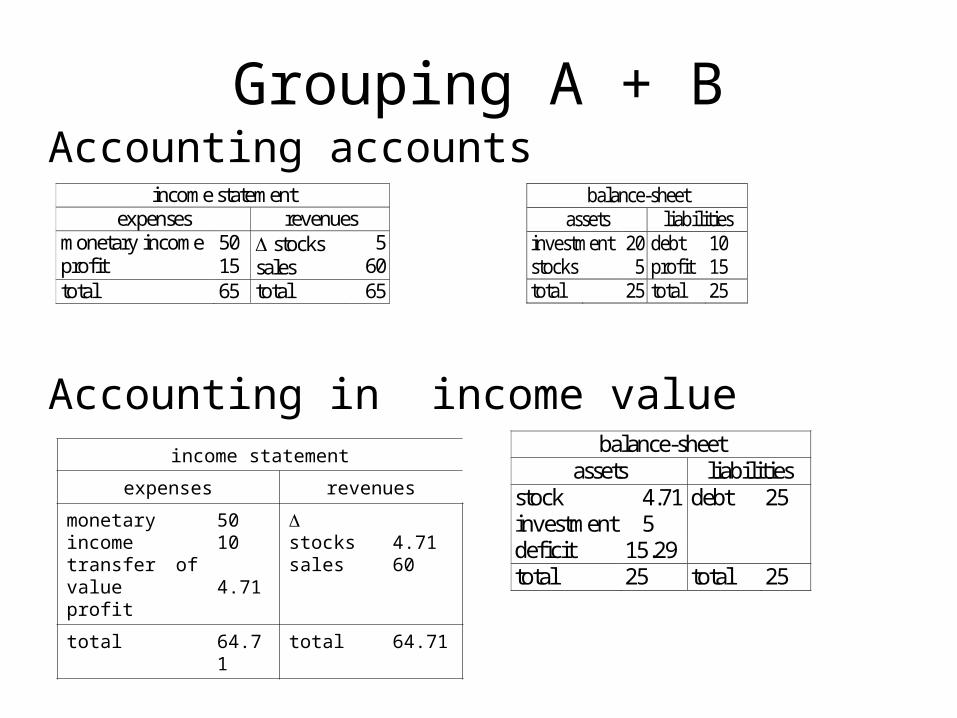

Grouping A + BAccounting accounts

Accounting in income valuebalance-sheet

assets liabilities stock investment

4.71 5

debt 25

deficit 15.29 total 25 total 25

balance-sheet assets liabilities

investment stocks

205

debt profit

10 15

total 25 total 25

income statement expenses revenues

monetary income profit

50 15

stocks sales

5 60

total 65 total 65

income statement

expenses revenues

monetary incometransfer of valueprofit

5010 4.71

stockssales

4.7160

total 64.71 total 64.71

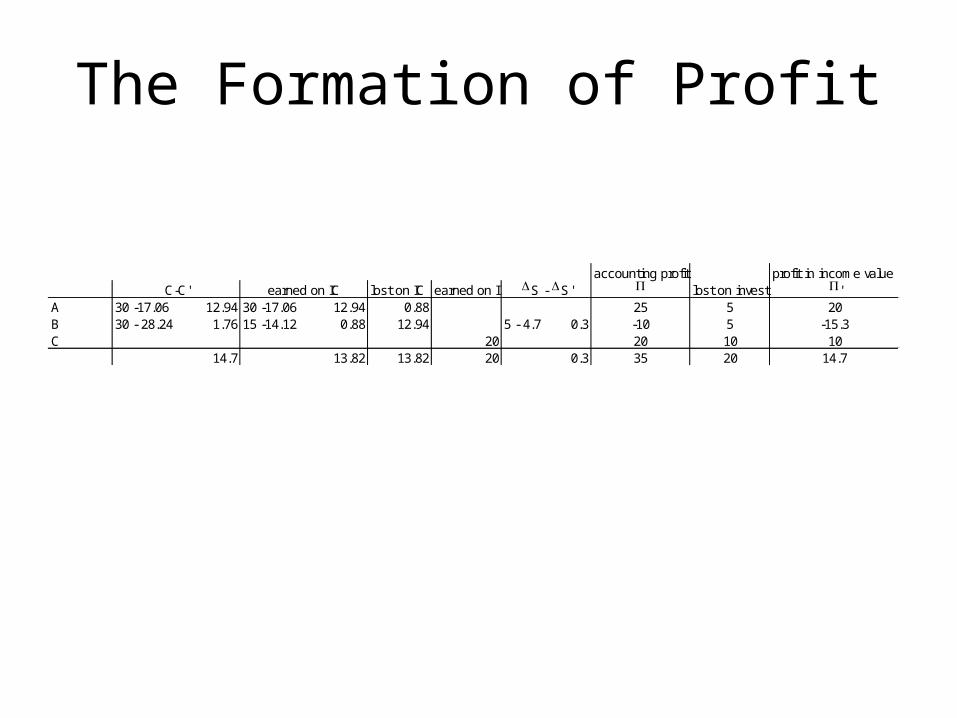

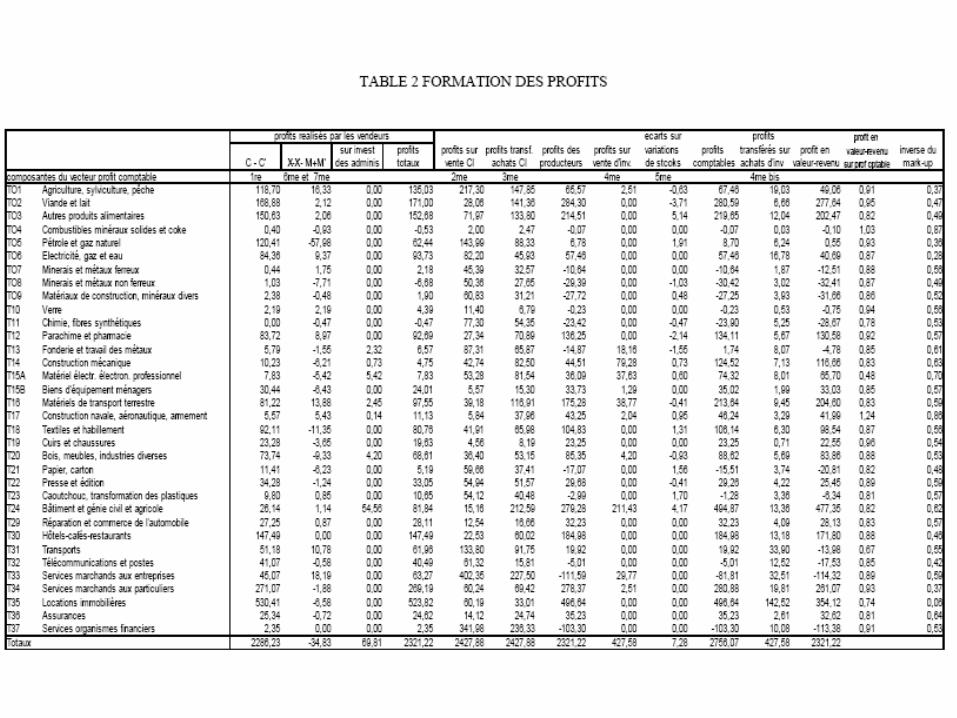

The Formation of Profit

accounting profit profit in income valuelost on IC earned on I lost on invest '

A 30 -17.06 12.94 30 -17.06 12.94 0.88 25 5 20B 30 - 28.24 1.76 15 -14.12 0.88 12.94 5 - 4.7 0.3 -10 5 -15.3C 20 20 10 10

14.7 13.82 13.82 20 0.3 35 20 14.7

C-C' earned on IC S - S'

, that is revenues minus monetary incomes minus purchase of intermediate consumption.That can be written: , that is revenues minus onetary incomes minus purchase of intermediate consumption.That can be written:

The goal is to show that profit, as it is calculated by the accountants is (in a closed economy):

= (C

- C

') + (IC - IC')u - (tIC - tIC')u + ( I - I ')u + ( S

- S

')

In which the 2nd term is the gain made by each industry when selling intermediate consumption goods, the 3rd one loss when by buying these same goods, the fourth the gain earned when selling fixed capital, and the last one results from the evaluation of

stocks at the end of the year. tu being the horizontal unity-vector (1……1)

By definition the retained profit is t = t

- tVA

' - tu IC, that is revenues

minus monetary incomes minus purchase of intermediate consumption.

That can be written:

=

- VA

' - tIC u

Using the I.O.T. in income-value we have:

tVA

' = t

' - tu IC’ or VA

' = t

' - tIC’ u

so =

-

' – (tIC u - tIC’ u )

When we develop

-

' using respectively I.O.T in prices and values we get:

= (C

- C

') + (IC – IC’) u + ( I - I ')u + ( S

- S

') – (tIC u - tIC’ u )

q.o.d.