Embed Size (px)

Citation preview

1

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES

THE INSTITUTE OF CHARTERED SECRETARIES AND

ADMINISTRATORS

International Qualifying Scheme Examination

CORPORATE SECRETARYSHIP

DECEMBER 2014

Suggested Answer

The suggested answers are published for the purpose of assisting students in their

understanding of the possible principles, analysis or arguments that may be identified in each

question

2

SECTION A

1.

Jasser International Holdings Limited (JIHL) is a company incorporated in

Bermuda with limited liability. Its shares are listed on the main board of the Stock

Exchange of Hong Kong. Its group of companies is principally engaged in the

fast-food sector in Hong Kong.

Gulibee Limited (GL) is a limited liability company incorporated in the British Virgin

Islands and its core business is food processing and distribution in Hong Kong,

Taiwan and Malaysia. GL is a wholly-owned subsidiary of Gulibee Holding Limited

(GHL), an international conglomerate.

Peter Chan, an executive director of JIHL, has worked out a five-year business

plan for JIHL which aims to expand JIHL’s businesses worldwide and to open

restaurants and fast-food chains in Taiwan and Malaysia in 2015. In order to fulfill

this plan, Mr. Chan proposes to the board of directors that JIHL should acquire GL

from GHL. All board members of JIHL agree with Mr. Chan’s proposal and

anticipate that the acquisition of GL is essential to the continued operation and

growth of JIHL’s business.

GHL basically agrees to sell its entire shareholding (i.e. 50,000 shares of US$1

each) and the business of GL to JIHL for a consideration of HK$330,000,000

under the terms of the sales and purchase agreement (SPA) to be finalised by

JIHL and GHL.

After a series of negotiations, JIHL as the purchaser and GHL as the seller agree

to enter into the SPA on 8 December 2014 (the transaction date). The

consideration will be paid by JIHL to GHL in the following manner:

1. 10% to be paid by cash/cheque on the transaction date;

2. 90% to be paid on the date when 50,000 shares in GL are duly transferred

from GHL to JIHL (within 15 days of the transaction date).

90% of the consideration (i.e. HK$297,000,000) is funded by a bank loan for which

a property owned by JIHL (located at Flat A, 11 Floor, Trade Square, 21 Wong

Chuk Hang Road, Hong Kong) is pledged as security to the bank. The terms of the

SPA and the consideration are determined by an arm’s length negotiation

between JIHL and GHL.

3

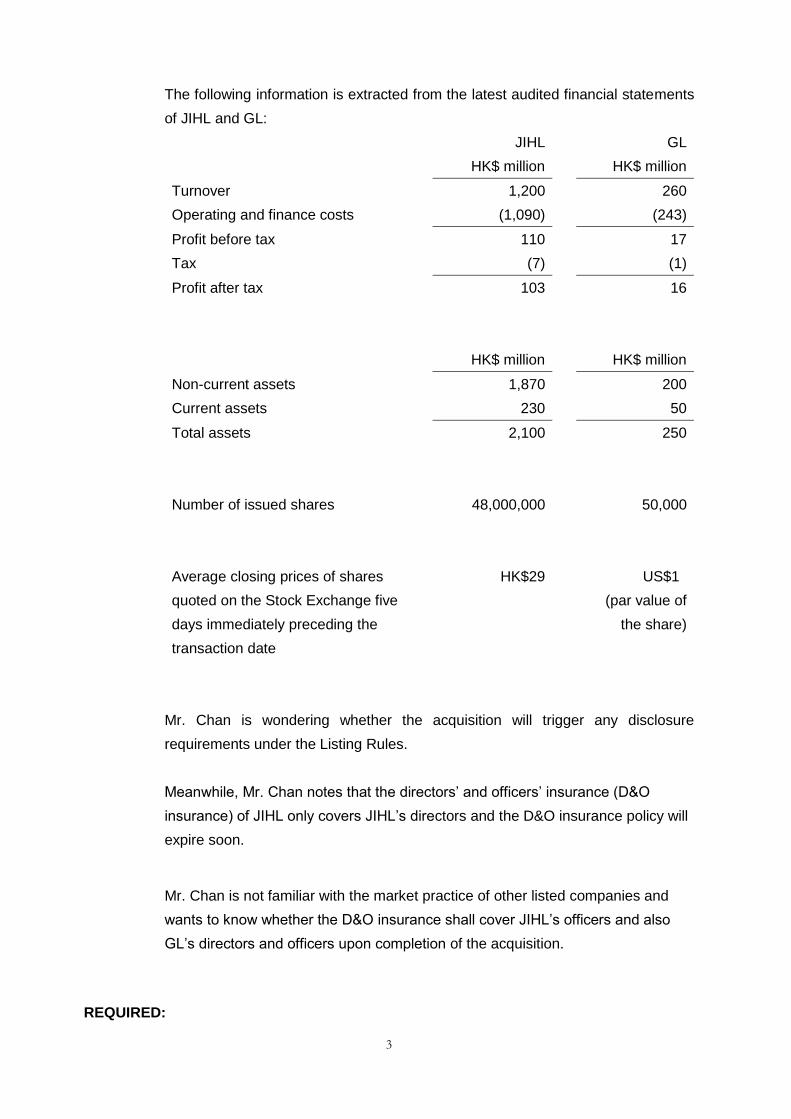

The following information is extracted from the latest audited financial statements

of JIHL and GL:

JIHL GL

HK$ million HK$ million

Turnover 1,200 260

Operating and finance costs (1,090) (243)

Profit before tax 110 17

Tax (7) (1)

Profit after tax 103 16

HK$ million HK$ million

Non-current assets 1,870 200

Current assets 230 50

Total assets 2,100 250

Number of issued shares 48,000,000 50,000

Average closing prices of shares

quoted on the Stock Exchange five

days immediately preceding the

transaction date

HK$29 US$1

(par value of

the share)

Mr. Chan is wondering whether the acquisition will trigger any disclosure

requirements under the Listing Rules.

Meanwhile, Mr. Chan notes that the directors’ and officers’ insurance (D&O

insurance) of JIHL only covers JIHL’s directors and the D&O insurance policy will

expire soon.

Mr. Chan is not familiar with the market practice of other listed companies and

wants to know whether the D&O insurance shall cover JIHL’s officers and also

GL’s directors and officers upon completion of the acquisition.

REQUIRED:

4

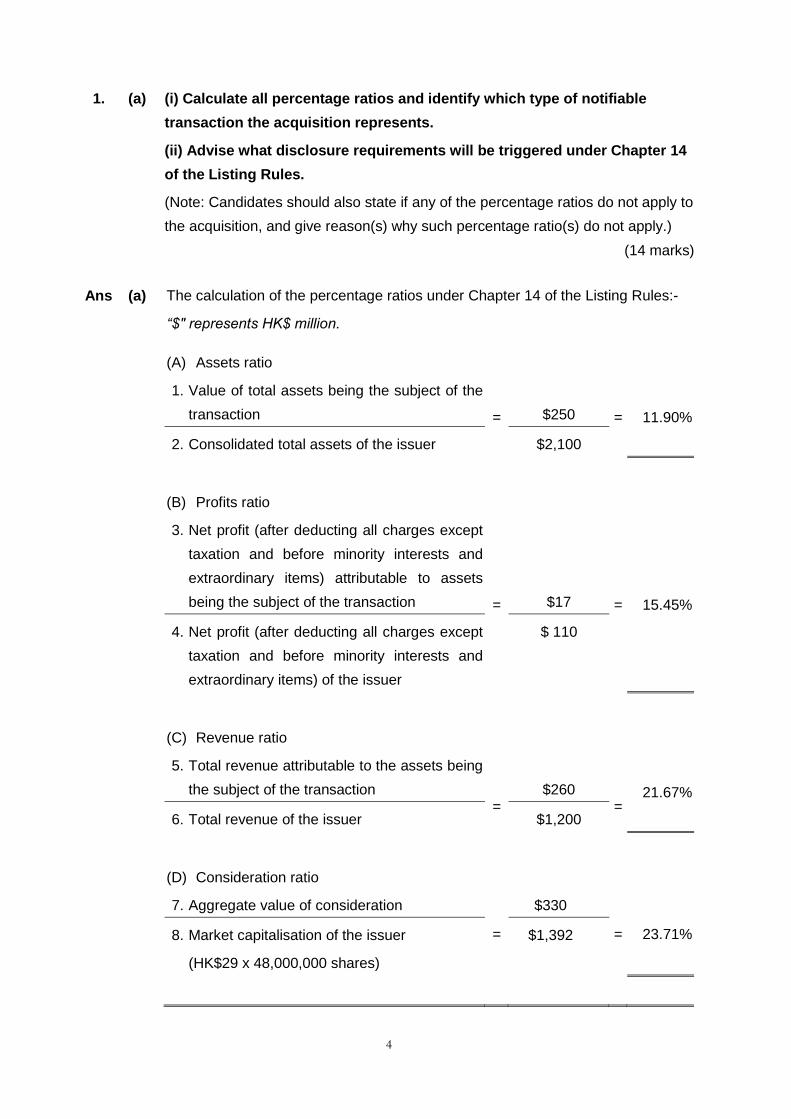

1. (a) (i) Calculate all percentage ratios and identify which type of notifiable

transaction the acquisition represents.

(ii) Advise what disclosure requirements will be triggered under Chapter 14

of the Listing Rules.

(Note: Candidates should also state if any of the percentage ratios do not apply to

the acquisition, and give reason(s) why such percentage ratio(s) do not apply.)

(14 marks)

Ans (a) The calculation of the percentage ratios under Chapter 14 of the Listing Rules:-

“$" represents HK$ million.

(A) Assets ratio

1. Value of total assets being the subject of the

transaction : = $250 = 11.90%

2. Consolidated total assets of the issuer $2,100

(B) Profits ratio

3. Net profit (after deducting all charges except

taxation and before minority interests and

extraordinary items) attributable to assets

being the subject of the transaction : = $17 = 15.45%

4. Net profit (after deducting all charges except

taxation and before minority interests and

extraordinary items) of the issuer

$ 110

(C) Revenue ratio

5. Total revenue attributable to the assets being

the subject of the transaction

= $260

= 21.67%

6. Total revenue of the issuer $1,200

(D) Consideration ratio

7. Aggregate value of consideration

=

$330

= 23.71% 8. Market capitalisation of the issuer

(HK$29 x 48,000,000 shares)

$1,392

5

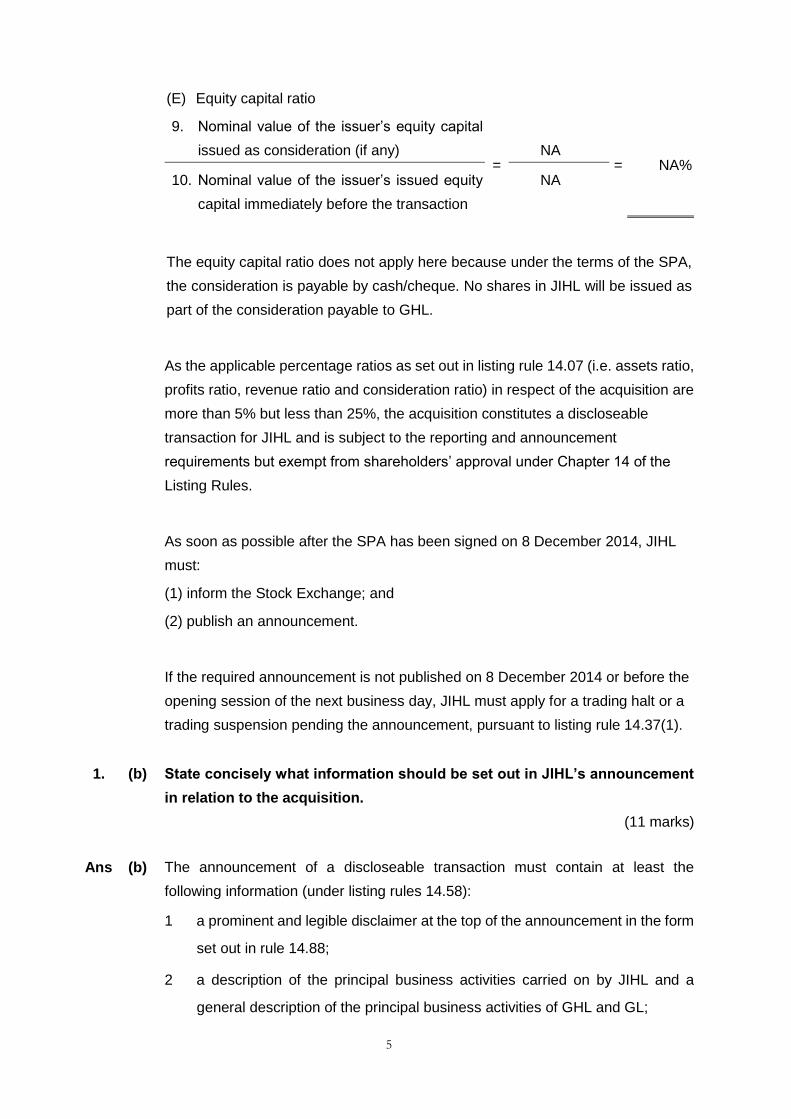

(E) Equity capital ratio

9. Nominal value of the issuer’s equity capital

issued as consideration (if any) =

NA = NA%

10. Nominal value of the issuer’s issued equity

capital immediately before the transaction

NA

The equity capital ratio does not apply here because under the terms of the SPA,

the consideration is payable by cash/cheque. No shares in JIHL will be issued as

part of the consideration payable to GHL.

As the applicable percentage ratios as set out in listing rule 14.07 (i.e. assets ratio,

profits ratio, revenue ratio and consideration ratio) in respect of the acquisition are

more than 5% but less than 25%, the acquisition constitutes a discloseable

transaction for JIHL and is subject to the reporting and announcement

requirements but exempt from shareholders’ approval under Chapter 14 of the

Listing Rules.

As soon as possible after the SPA has been signed on 8 December 2014, JIHL

must:

(1) inform the Stock Exchange; and

(2) publish an announcement.

If the required announcement is not published on 8 December 2014 or before the

opening session of the next business day, JIHL must apply for a trading halt or a

trading suspension pending the announcement, pursuant to listing rule 14.37(1).

1. (b) State concisely what information should be set out in JIHL’s announcement

in relation to the acquisition.

(11 marks)

Ans (b) The announcement of a discloseable transaction must contain at least the

following information (under listing rules 14.58):

1 a prominent and legible disclaimer at the top of the announcement in the form

set out in rule 14.88;

2 a description of the principal business activities carried on by JIHL and a

general description of the principal business activities of GHL and GL;

6

3 the date of the transaction;

4 JIHL must confirm that, to the best of the directors’ knowledge, information

and belief having made all reasonable enquiry, GHL is independent of JIHL

and of connected persons of JIHL;

5 the aggregate value of the consideration, how it is to be satisfied and details

of payment on a deferred basis, if any;

6 the basis upon which the consideration was determined;

7 the value (book value and valuation, if any) of GL which is the subject of the

transaction;

8 where applicable, the net profits (both before and after taxation) attributable

to GL which are the subject of the transaction for the two financial years

immediately preceding the transaction;

9 the reasons for entering into the transaction, the benefits which are expected

to accrue to JIHL as a result of the transaction;

10 a statement that the directors of JIHL believe that the terms of the transaction

are fair and reasonable and in the interests of the shareholders as a whole;

and

11 details of any guarantee and/or other security given or required as part of or

in connection with the transaction.

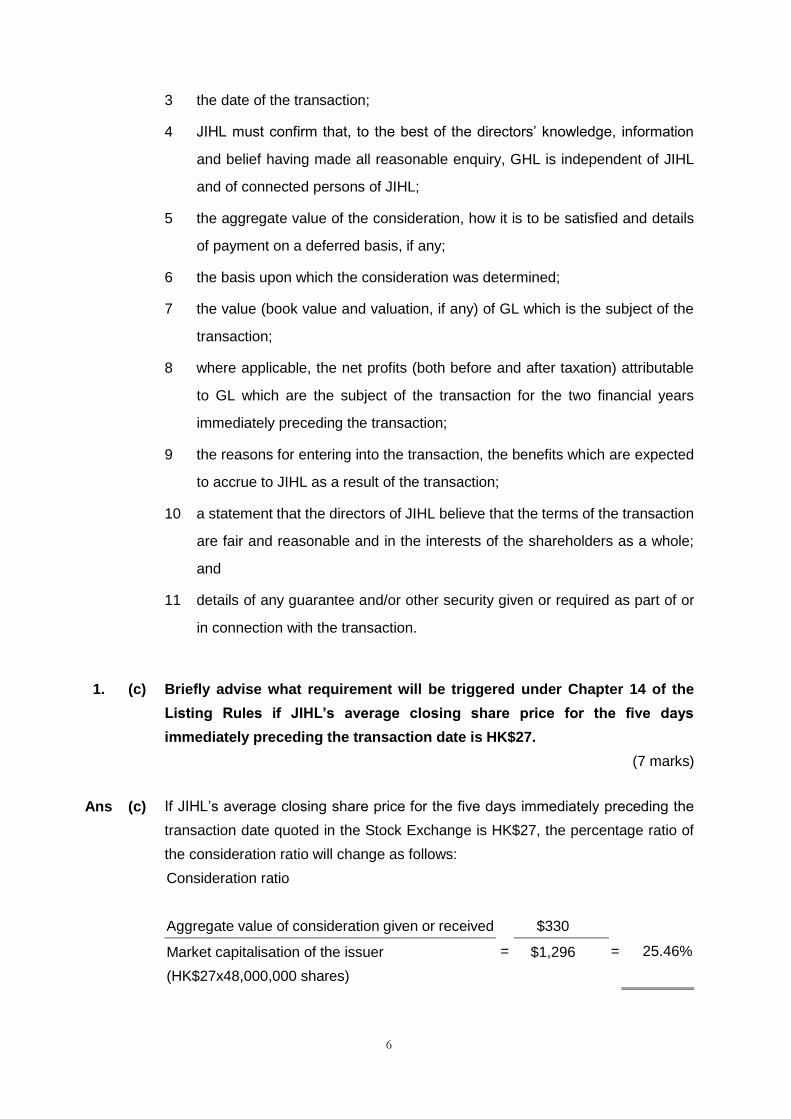

1. (c) Briefly advise what requirement will be triggered under Chapter 14 of the

Listing Rules if JIHL’s average closing share price for the five days

immediately preceding the transaction date is HK$27.

(7 marks)

Ans (c) If JIHL’s average closing share price for the five days immediately preceding the

transaction date quoted in the Stock Exchange is HK$27, the percentage ratio of

the consideration ratio will change as follows:

Consideration ratio

Aggregate value of consideration given or received

=

$330

= 25.46% Market capitalisation of the issuer

(HK$27x48,000,000 shares)

$1,296

7

As the consideration ratio is more than 25% but is less than 100%, the acquisition

now constitutes a major transaction for JIHL and is subject to the reporting,

announcement and shareholders’ approval requirements under Chapter 14 of the

Listing Rules.

JIHL is not only required to inform the Exchange and publish an announcement,

but is also required to:

(1) issue a circular to shareholders within 15 days after the publication of the

announcement;

(2) include an accountants’ report on GL, the company being acquired, and

information required under listing rules 14.63, 14.66 and 14.67 in the circular;

and

(3) obtain shareholders’ approval.

(4)

1. (d) Discuss whether JIHL should ensure that its D&O insurance policy covers

JIHL’s officers and also GL’s directors and officers upon completion of the

acquisition.

(8 marks)

(Total: 40 marks)

Ans (d) The core purpose of directors’ and officers’ insurance (D&O insurance) is to

provide financial protection for directors and officers against the consequences of

their actual or alleged ‘wrongful acts’ when acting in the scope of their duties.

In accordance with code provision A1.8 of Corporate Governance Code (Appendix

14), JIHL should arrange appropriate insurance cover in respect of legal action

against its directors.

D&O insurance plays a role in promoting corporate governance and

enterprise-wide risk management in the company.

A ‘wrongful act’ must be something done in the capacity of director or officer. D&O

insurance normally covers the following persons/entity:

1 directors (executives, non-executives and independent non-executives) for

personal liability;

8

2 officers (including usually the chief executive officer, chief financial officer,

company secretary or other named executives) for personal liability; and

3 the ‘insured company’ for company liability. Usually, the company itself, parent

and/or subsidiary companies may be covered as the ‘insured company’.

D&O insurance covers a claim alleging a wrongful act of directors and officers for

the:

1 company liability to indemnify the directors and/or officers against any liability

and defence costs; and

2 personal liability of the directors and/or officers against any liability and

defence costs.

Different companies need different degrees of coverage. The terms of the D&O

insurance depend on JIHL’s own circumstances or business environment. It is

advisable for the terms of the D&O insurance to cover JIHL’s directors and

officers. It shall also cover GL’s directors and officers for the purpose of promoting

corporate governance and for the enterprise-wide risk management of JIHL’s

group of companies.

9

SECTION B

2.

Bossa Limited is a Hong Kong private company incorporated in 2008 and it

adopted Table A in the First Schedule of the old Companies Ordinance (Cap. 32)

as its articles of association. Mr. Au, a director of Bossa Limited, notes that the

new Companies Ordinance (Cap. 622) (new CO) has come into operation with

effect from 3 March 2014, which includes the abolition of the requirement to have a

memorandum of association as a constitutional document of a local company.

Mr. Au is wondering whether Bossa Limited should take any action to comply with

the new CO with respect to the abolition of memorandum of association.

REQUIRED:

2. (a) State concisely:

(i) the major changes in the new CO with respect to the abolition of

memorandum of association and what mandatory clauses shall be

included in the articles of association, and

(ii) the reason for abolishing memorandum of association as a constitutional

document of a local company.

(15 marks)

Ans (a) Major changes

1. Under the old Companies Ordinance (Cap. 32), a company formed in Hong

Kong was required to have a memorandum of association (MA) and articles

of association (AA). Under the new Companies Ordinance (new CO), a

company incorporated in Hong Kong is only required to have AA. The MA is

abolished under the new CO and information currently contained in the MA

will be set out in the AA.

2. There are no transitional arrangements for abolition of the MA. The change

took immediate effect upon the new CO coming into force on 3 March 2014.

3. The deeming provision set out in section 98 of the new CO provides that

provisions of the MA of an existing company (i.e. a company formed and

10

registered under the old Companies Ordinance) will be deemed to be

regarded as provisions of the company’s AA.

4. As a result of the migration to no-par, any provision which states the amount

of share capital with which the company proposes to be registered or is

registered is regarded as deleted and any such condition that divides the

share capital into shares of a fixed amount is also regarded as deleted

(section 98(4)).

Mandatory clauses shall be included in AA

5. Sections 81 to 85 of the new CO set out that the AA of companies

incorporated under the new CO must contain the following mandatory

articles:

a. the name of the company (section 81);

b. the objects of the company (only for a company which has been granted a

licence to dispense with the use of the word ‘limited’ in its name under

section 103 of the new CO) (section 82);

c. details of members’ liabilities (section 83);

limited company - the articles must state that the liability of its

members is limited (section 83(1)),

unlimited company - the articles must state that the liability of its

members is unlimited (section 83(2)),

d. details of liabilities or contribution of members (section 84)

company limited by shares - the articles must state that the liability of

its members is limited to any amount unpaid on shares held by the

members (section 84(1)),

company limited by guarantee - the articles must state that each

member undertakes that if the company is wound up, the member, or

within one year after ceasing to be a member, will contribute an

amount required, not exceeding a specified amount, to the company’s

assets ( section 84(2)),

e. details of initial capital and initial shareholding (section 85)

11

6. The articles of a company with a share capital may state the maximum

number of shares that the company may issue (section 85(2)). However, this

is not mandatory.

Reasons for abolishing the MA

1. The MA used to contain the objects clause of a company. The objects clause

of a company is now less significant given the abolition of doctrine of ultra

vires, and all companies now have the capacity and rights of a natural

person;

2. There is no mandatory requirement under the new CO to request any

company to state its objects clause in its constitutional documents, except for

those companies which have been granted a licence under section 103; and

3. All information provided on incorporation as required by sections 81 to 85 of

the new CO now has to be contained in the AA.

Thus, the need to retain the MA as a separate constitutional document has

diminished.

2. (b) Advise Mr. Au of any actions that Bossa Limited should take in respect of its

existing memorandum and articles of association.

(5 marks)

(Total: 20 marks)

Ans (b) Actions Bossa Limited should take in respect of its existing Memorandum and

Articles of Association

1. The new CO does not require existing companies to amend their AA.

2. The deeming provision of section 98 of the new CO provides that provisions

of the MA of an existing company will be deemed to be regarded as

provisions of the AA of the company.

3. The new CO abolishes the concepts of authorised capital and par value. As a

12

result of the migration to the no-par regime, provisions in the existing MA or

AA of a company which state the amount of authorised share capital and the

nominal or par value of its shares are regarded as deleted.

4. Table A, in so far as not modified by the provisions of the new CO, will

continue to apply to existing companies which had adopted Table A as their

AA.

5. The company should review its AA to ensure that the company will be able to

take advantage of some of the new initiatives under the new CO, for example,

(i) the provisions on financial assistance for acquisition of shares, (ii)

non-court based reduction of capital, and (iii) capitalisation of profits under the

new no-par regime.

13

3.

IC Technology Inc. is a limited liability company incorporated in Japan. Its principal

businesses are the provision of testing services for IC products; designing,

developing and selling IC testing software and products; and the provision of

research and consultancy services for IC technology.

Mr. Oisha, a director of IC Technology Inc., wishes to expand the company’s

businesses into Mainland China and plans to list the company’s shares on the

Main Board of the Hong Kong Stock Exchange. However, the company’s financial

performance does not meet the Main Board listing requirements.

Mr. Oisha’s alternative plan is to list the company’s shares initially on the Growth

Enterprise Market (GEM), and thereafter transfer the listing from GEM to the Main

Board.

REQUIRED:

3. (a) Advise Mr. Oisha of the listing requirements for the GEM of the Hong Kong

Stock Exchange.

(10 marks)

Ans (a) Listing requirements of Growth Enterprise Market (GEM)

1. Financial requirements

A GEM new applicant must have a trading record of at least two financial years

comprising:

i. A positive cashflow generated from operating activities in the ordinary and

usual course of business of at least HK$20 million in aggregate for the two

financial years immediately preceding the issue of the listing document; and

ii. Market cap of at least HK$100 million at the time of listing.

2. Acceptable jurisdictions

Applicants incorporated outside Hong Kong and other recognised jurisdictions

seeking a primary listing on GEM are assessed on a case-by-case basis and

have to demonstrate they are subject to appropriate standards of shareholder

protection, which are at least equivalent to those required under Hong Kong

law.

3. Accounting standards

14

A new applicant's accounts must be prepared in accordance with either Hong

Kong Financial Reporting Standards or International Financial Reporting

Standards.

For GEM new applicants, accounts prepared in accordance with US GAAP are

acceptable if the company is listed, or will be simultaneously listed, on either

the New York Stock Exchange or the NASDAQ National Market.

4. Suitability for listing

Both the issuer and its business must, in the opinion of the Exchange, be

suitable for listing.

An issuer or its group (other than an investment company) whose assets

consist wholly or substantially of cash or short-dated securities will not

normally be regarded as suitable for listing, except where the issuer or group is

solely or mainly engaged in the securities brokerage business.

5. Operating history and management

A GEM new applicant must have a trading record of at least two full financial

years with:

1. substantially the same management throughout the two full financial

years; and

2. continuity of ownership and control throughout the full financial year

immediately preceding the issue of the listing document.

The Exchange may accept a shorter trading record period and waive or vary

the ownership and management requirements for:

1. newly-formed ‘project’ companies; and

2. natural resource exploitation companies, when supported by reasons

acceptable to the Exchange.

6. Minimum market capitalisation

HK$100 million

7. Public float and market capitalisation of public float

15

HK$30 million

At least 25% of the issuer's total issued share capital must at all times be held

by the public.

8. Spread of shareholders

The equity securities in the hands of the public should be held among at least

100 holders.

9. Offering mechanism

A new applicant is free to decide on its offering mechanism and may list on the

Exchange by way of placing only.

10. New issue price

The GEM Listing Rules do not impose conditions on the new issue price.

However, new shares cannot be issued at a price below their nominal value.

3. (b) Is there an automatic transfer mechanism from GEM to the Main Board?

What are the advantages of transferring from GEM to the Main Board, and

what are the effects on the company’s securities after such a transfer?

(10 marks)

(Total: 20 marks)

Ans (b) There is no automatic transfer mechanism from GEM to the Main Board.

Qualification for transfer

A GEM-listed company may apply for a transfer of listing of its securities from

GEM to the Main Board under Chapter 9A of the Main Board Listing Rules:

1. if it meets all the qualifications for listing on the Main Board;

2. once it complies with GEM rule 18.03 in respect of its financial results for the

first full financial year commencing after the date of its listing on GEM; and

3. if in the 12 months preceding the transfer application and until the

commencement of dealings in its securities on the Main Board, it has not been

the subject of any disciplinary investigation by the Exchange in relation to a

serious breach or potential serious breach of any GEM Listing Rules or

Exchange Listing Rules.

Advantage of transfer

16

Under the streamlined transfer procedure of Chapter 9A of the Main Board Listing

Rules, the following listing qualifications and disclosure requirements do not apply

to the transfer of a listing from GEM to the Main Board:

1. all requirements relating to application procedures, listing documents and the

prospectus under Chapters 9, 11 and 11A (the prospectus will be replaced by

regulatory announcements published electronically);

2. all requirements under Chapter 3A relating to the appointment and obligations

of a sponsor;

3. the latest financial period reported by the reporting accountants under the

Main Board listing rule 8.06.

Moreover, the Main Board initial listing fee is reduced by 50% for GEM transfer

applicants.

Effect of transfer on the security

1. Upon successful transfer of listing of an issuer’s equity securities from GEM to

the Main Board, the listing on GEM of any options, warrants or similar rights or

convertible equity securities in the same issuer will be automatically

transferred to the Main Board; and

2. An application for a transfer of listing must relate to all classes of securities (if

more than one) already listed on GEM, including all further securities of the

relevant classes issued or proposed to be issued.

17

4. Albert Li holds 31% of the voting shares in Lucky Holdings (Cayman) Limited,

which is a limited liability company incorporated in the Cayman Islands whose

shares are listed on the Hong Kong Stock Exchange.

His wife, Mrs. Li, has acquired 1% shares in Lucky Holdings (Cayman) Limited on

the Stock Exchange over the past four months and intends to acquire additional

shares in the company.

Mr. Li wonders if he is required to make a general offer to the shareholders of

Lucky Holdings (Cayman) Limited.

REQUIRED:

4. (a) As the company secretary of Lucky Holdings (Cayman) Limited, advise Mr. Li

in what circumstances he needs to make a general offer under the Code on

Takeovers and Mergers and evaluate if his case will trigger any obligation for

a general offer.

(9 marks)

Ans (a) 1. A general offer is a mandatory offer made to all shareholders of Lucky

Holdings (Cayman) Limited to acquire their shares at a stated price under the

Rule 26 of the Code on Takeovers and Mergers.

2. Subject to exceptions, a general offer may be required when any one of the

following circumstances exist:

(a) any person acquires, whether by a series of transactions over a period of

time or not, 30% or more of the voting rights of a company;

(b) two or more persons acting in concert collectively hold less than 30% of

the voting rights of a company, and any one or more of them acquires

voting rights with the effect of increasing their collective holding of voting

rights to 30% or more of the voting rights of the company;

(c) any person holds not less than 30% but not more than 50% of the voting

rights of a company and that person acquires, in any period of 12

months, additional voting rights with the effect of increasing that

person’s holding of voting rights of the company by more than 2%; or

18

(d) two or more persons acting in concert collectively hold not less than

30%, but not more than 50%, of the voting rights of a company, and any

one or more of them acquires, in any period of 12 months, additional

voting rights with the effect of increasing their collective holding of voting

rights of the company by more than 2%.

3. The existing circumstance (i.e. Mr. Li holds 31% and Mrs. Li acquiries less

than 2% within the 12-month period) does not trigger an obligation to make a

general offer.

4. An obligation to make a general offer is triggered if any one of the following

circumstances occur within the 12-month period:

(a) Mrs. Li acquires 2% or more additional shares, or

(b) Mr. Li and Mrs. Li collectively acquire 2% or more additional shares.

5. The general offers must be extended to the holders of each class of equity

share capital of Lucky Holdings (Cayman) Limited, whether the class carries

voting rights or not.

6. The offer price must be in cash, or accompanied by a cash alternative, and

must not be less the highest price paid by the offeror (i.e. Mr. Li) or any

person acting in concert (i.e. Mrs. Li) for the shares within six months from the

date of acquisition of shares in the market.

4. (b) List and discuss the general principles laid down by the Code on Takeovers

and Mergers on making a general offer.

(11 marks)

(Total: 20 marks)

Ans (b) The main purpose of the Code on Takeovers and Mergers is to afford fair

treatment for shareholders who are affected by takeovers. It seeks to require

equality of treatment of shareholders, timely and adequate information to be

disclosed by the companies concerned to enable shareholders to make informed

decisions, and to ensure a fair and informed market in the securities concerned.

According to the Code on Takeovers and Mergers, the general principles for

making a general offer are as follows:

1. All shareholders are to be treated even-handedly and all shareholders of the

same class are to be treated similarly.

2. If control of a company changes or if the control is acquired or consolidated, a

19

general offer to all shareholders is normally required.

3. During the course of an offer, neither an offeror nor the offeree company nor

any of their respective advisors may furnish information to some shareholders

which is not made available to all shareholders.

4. An offeror should announce an offer only after careful and responsible

consideration.

5. Shareholders should be given sufficient information, advice and time to reach

an informed decision on an offer. No relevant information should be withheld.

All documents must be prepared with the highest possible degree of care,

responsibility and accuracy.

6. All persons concerned with offers should make full and prompt disclosure of

all relevant information and take every precaution to avoid the creation or

continuance of a false market.

7. Rights of control should be exercised in good faith and the oppression of

minority or non-controlling shareholders is always unacceptable.

8. Directors of an offeror and the offeree company must always, in advising their

shareholders, act only in their capacity as directors and not have regard to

their personal or family shareholdings or their personal relationships with the

companies. They should only consider the shareholders’ interests taken as a

whole when they are giving advice to shareholders.

9. The board of the offeree company may not take any action in relation to the

affairs of the company, without the approval of shareholders in general

meeting, which could effectively result in any bona fide offer being frustrated

or in the shareholders being denied any opportunity to decide on its merits.

10. All parties concerned are required to co-operate with the Executive of the

Securities and Futures Commission, the Panel and the Takeovers Appeal

Committee, and to provide all relevant information.

20

5. The Corporate Governance Code and Corporate Governance Report (Appendix

14) of the Main Board Listing Rules specify that listed companies must include a

corporate governance report in their annual reports. The corporate governance

report must contain all the information set out in paragraphs G to P of Appendix 14

(mandatory disclosure requirements). Any failure to do so will be regarded as a

breach of the Listing Rules.

REQUIRED:

5. (a) Describe in detail what information pursuant to the mandatory disclosure

requirements in paragraphs I to L of Appendix 14 should be included in the

corporate governance report.

(Note to candidates:

Paragraph I: Board of Directors

Paragraph J: Chairman and Chief Executive

Paragraph K: Non-Executive Directors

Paragraph L: Board Committees)

(14 marks)

Ans (a) The following information should be disclosed in the corporate governance report,

pursuant to the mandatory disclosure requirements in paragraphs I to L of

Appendix 14 of the Main Board Listing Rules:

I. BOARD OF DIRECTORS

(a) Composition of the board, by category of directors, including name of

chairman, executive directors, non-executive directors and independent

non-executive directors;

(b) Number of board meetings held during the financial year;

(c) Attendance of each director, by name, at the board and general meetings;

(d) For each named director, the number of board or committee meetings

he/she attended and separately the number of board or committee

meetings attended by his/her alternate. Attendance at board or committee

meetings by an alternate director should not be counted as attendance by

the director himself;

(e) A statement of the respective responsibilities, accountabilities and

21

contributions of the board and management. In particular, a statement of

how the board operates, including a high level statement on the types of

decisions taken by the board and those delegated to management;

(f) Details of non-compliance (if any) with rules 3.10(1) and (2), and 3.10A

and an explanation of the remedial steps taken to address

non-compliance. This should cover non-compliance with appointment of a

sufficient number of independent non-executive directors and appointment

of an independent non-executive director with appropriate professional

qualifications, or accounting or related financial management expertise;

(g) Reasons why the company considers an independent non-executive

director to be independent where he/she fails to meet one or more of the

guidelines for assessing independence set out in rule 3.13;

(h) Relationships (including financial, business, family or other material/

relevant relationship(s)), if any, between board members and in particular,

between the chairman and the chief executive; and

(i) How each director, by name, complied with A.6.5. (Continuous

Professional Development)

J. CHAIRMAN AND CHIEF EXECUTIVE

(a) The identity of the chairman and chief executive; and

(b) Whether the roles of the chairman and chief executive are separate and

exercised by different individuals.

K. NON-EXECUTIVE DIRECTORS

The term of appointment of non-executive directors.

L. BOARD COMMITTEES

The following information for each of the remuneration committee, nomination

committee and audit committee, and corporate governance functions:

(a) The role and function of the committee;

(b) The composition of the committee and whether it comprises independent

non-executive directors, non-executive directors and executive directors

(including their names and identifying in particular the chairman of the

committee);

(c) The number of meetings held by the committee during the year to discuss

22

matters and the record of attendance of members, by name, at meetings

held during the year; and

(d) A summary of the work during the year.

(e)

5. (b) Evaluate the major difference(s) between the disclosure obligations of a

Hong Kong incorporated private company and a Hong Kong listed company,

and state the rationale behind the differences.

(6 marks)

(Total: 20 marks)

Ans (b) Major differences in disclosure obligations and the rationale for the differences are

as follows:

Hong Kong incorporated private company

1. A private company must have clauses to achieve the following in its articles of

association:

a. restrict a member’s right to transfer shares;

b. limit the number of members to 50; and

c. prohibit any invitation to the public to subscribe for any shares or

debentures in the company.

Shares of a private company are not freely transferrable in the market.

Generally speaking, the public has less interest in the corporate information of

private companies.

2. If there is any alteration to the company’s constitution or capital structure

and/or change of directors/company secretary, a private company has a

statutory obligation under the Companies Ordinance to file a form with the

Companies Registry. The public may access copies of the filed forms from the

Companies Registry.

3. A private company does not have an obligation to comply with the disclosure

requirements under the Listing Rules and the Securities and Futures

Ordinance.

Listed company

23

1. As the shares of a listed company are listed on the Stock Exchange Hong

Kong Limited, shares of listed companies are freely transferrable in the

market. Potential investors have more interest on the corporate information of

listed companies.

2. A listed company (whether incorporated in Hong Kong or registered as an

overseas company) has a statutory obligation to comply with the filing

requirements under the Companies Ordinance. The public may access copies

of the filed forms from the Companies Registry.

3. Listed companies are also required to comply with the disclosure

requirements under the Listing Rules and the Securities and Futures

Ordinance.

24

6.

Benny Ho is the sole shareholder and sole director of Win-win Imports and

Exports Limited, a private company incorporated in Hong Kong. The company is

an import and export trading firm which sources various types of raw materials

and

re-exports the raw materials to other countries. The company has made

remarkable profits in the past few years.

Due to Benny’s poor health, the company’s business operations ceased for six

months. Benny plans to take a short break from his business and dissolve the

company, although he will consider resuming the company’s business operations

later if his health improves. In these circumstances, Benny does not want to

liquidate the company and wants your advice on a feasible way of dissolving the

company.

REQUIRED:

6. (a) Distinguish the major differences between deregistration and striking off.

(6 marks)

Ans (a) Both deregistration and striking off will result in dissolving a company.

Deregistration is initiated by the company by application to the Company

Registry, whilst striking off is initiated by the Registrar of Companies.

Deregistration

A defunct solvent company which meets the required conditions under section

750(2) of the Companies Ordinance may be dissolved by applying for

deregistration. Deregistration is a relatively simple, inexpensive and quick

procedure for dissolving defunct solvent companies.

A company is required to file annual returns and observe its obligations under the

Companies Ordinance until it has been dissolved.

A company dissolved by deregistration may apply to the Court of First Instance

for restoration.

25

Striking off

The Registrar of Companies may strike the name of a company off the

Companies Register under Division 1 of Part 15 of the Companies Ordinance

where the Registrar has reasonable cause to believe that the company is not in

operation or carrying on business. The company shall be dissolved when its

name is struck off the Companies Register. Striking off is a statutory power

conferred on the Companies Registrar; a company cannot apply for striking off.

A company dissolved by striking off by the Registrar of Companies may apply for

restoration by the Court of First Instance or by administrative restoration of the

Companies Registrar.

6. (b) Describe precisely the conditions and requirements for a company to make

an application for deregistration.

(6 marks)

Ans (b) 1. Only a local private company or a local company limited by guarantee, other

than those companies specified in section 749(2) of the Companies

Ordinance, may apply for deregistration. The company must be a defunct

solvent company.

2. The company must meet the following conditions before making an

application for deregistration:

a. All the members of the company agree to the deregistration;

b. The company has not commenced operation or business or has not been

in operation or carried on business during the three months immediately

before the application;

c. The company has no outstanding liabilities;

d. The company is not a party to any legal proceedings;

e. The company’s assets do not consist of any immovable property situated

in Hong Kong;

f. If the company is a holding company, none of its subsidiary's assets

consist of any immovable property situated in Hong Kong.

3. The company must obtain a Notice of No Objection to a Company being

Deregistered (Notice of No Objection) from the Commissioner of Inland

Revenue (the Commissioner) by making an application to the Commissioner

together with the application fee of HK$270.

26

4. An application for deregistration in a Form NDR1 should be delivered to the

Registrar of Companies within three months from the date of issue of the

Notice of No Objection, together with the required fee of HK$420 and the

Notice of No Objection.

6. (c) Discuss critically whether Win-win Imports and Exports Limited should

apply for dormant status and what procedures it must follow under the

Companies Ordinance to apply for, and cease to be, dormant.

(8 marks)

(Total: 20 marks)

Ans (c) Under the Companies Ordinance, a private company (with some exceptions) is

allowed to declare itself a dormant company if it has not entered into an

accounting transaction or it specifies a date after which it will not enter into an

accounting transaction. The exceptions are as follows:

1. a bank

2. a deposit taking company

3. an insurance company

4. a registered dealer

5. an investment adviser

6. a commodity trader

7. a foreign exchange trader

8. a trustee of mandatory provident fund schemes

9. a holding company of any of the above companies

10. a company which fell into one of the above categories during the preceding

five years

Accounting transactions are those transactions which are required to be recorded

in the company’s books of account. They are:

1. receipts and expenditures of money;

2. sales and purchases of goods; and

3. assets and liabilities of the company.

Accounting transactions do not include any payments of fees which are required

27

to be paid by any ordinances.

A dormant company is exempt from the statutory requirements of holding annual

general meetings, filing annual returns*, appointing auditors and preparing

audited accounts. (*However, a private company is still required to deliver an

annual return for the year in which it declares itself to be dormant if the effective

date on which the company becomes dormant falls after the 42nd day after the

anniversary of its date of incorporation.)

However the company still needs to pay a business registration fee every year.

Win-win Imports and Exports Limited is a qualified private company. Declaring

the company dormant is therefore an efficient way of maintaining the company if

no accounting transaction occurs. The company will then be exempt from the

above mentioned statutory requirements and paying the relevant fees, e.g. audit

fee, to maintain its existence. If Benny restarts the company’s business in the

future, he will not need to go through the incorporation procedure again in order

to activate the company.

Procedures for becoming a dormant company:

The company must pass and file a special resolution to the Registrar of

Companies:

(a) declaring that the company will become dormant either as from the date

of delivery of the special resolution to the Registrar of Companies or a

later date that is specified in the special resolution; and

(b) authorising the director to file the special resolution with the Registrar of

Companies.

Ceasing to be a dormant company:

A dormant company may cease to be dormant when a special resolution

declaring that the company intends to enter into an accounting transaction is

delivered to Registrar of Companies for registration; or there is an accounting

transaction in relation to the company.

END