Embed Size (px)

Citation preview

Discussion Paper No. 28

THE IMPACT OF THE U.S. POLICY-MIX

ON U.S.-JAPAN ECONOMIES

Simulation Analysis using - -

the U.S.-Japan Link Model

by

World Economic Model Group

Economic Research Institute,

Economic Planning Agency,

Tokyo, Japan

Discussion Paper No. 28

THE IMPACT OF THE U.S. POLICY-MIX

ON U.S. -JAPAN ECONOMIES *

Simulat ion Analysis using - -

the U.S. -Japan Link Model

by

World Economic Model Group

December 1983

Economic Research Inst i tute

Economic Planning Agency

Tokyo, Japan

* This report was compiled by the Economic Research Inst i tute ,

the Economic Planning Agency. I t seeks to g ive an outl ine both

of the types of research currently underway at the Inst i tute

and of the ideas being formulated in the process .

We would also l ike to have the opinions of those reading this report

on i ts contents . This report is the work of the World Economic

Model Group, and does not represent the of f ic ia l v iew of the

Economic Research Inst i tute , the Economic Planning Agency.

Contents

Introduct ion · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 1

A. Object ives · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 1

B. Methodology · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 2 I . Development of the U.S. Pol icy-Mix · · · · · · · · · · · · · · · · · · · · · · · · · · · 2 I I . Impact on the U.S. Economy · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 4

A. On the business c l imate , interest rates , and inf lat ion · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 4

B. On general government budget def ic i ts · · · · · · · · · · · · · · · 7

C. On the current account balance · · · · · · · · · · · · · · · · · · · · · · · · · · 8

D. On the dol lar e f fect ive exchange rate · · · · · · · · · · · · · · · · · · 9

III . Impact on the Japanese Economy · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 10

A. Direct impact o f the U.S. pol icy-mix on the Japanese economy · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 10

B. Japanese monetary pol icy vis -a-v is the

depreciat ion of yen and the ef fects o f this pol icy · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 11

C. Comparison of the impact o f U.S. economic

pol icy and Japanese f iscal pol icy on Japan's current account surplus · · · · · · · · · · · · · · · · · · · · · · · · · 12

IV. Conclusion · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 14 Appendix 1 : Assumptions made in this Simulation · · · · · · · · · · · · · · 25

I . Assumptions Regarding the U.S. Pol icy-Mix II . Assumptions Regarding Japanese Economic Pol icy

Appendix 2 : Points for Consideration in Interpret ing

the Results · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 29

-1-

Introduct ion

A. Object ives

The recent pol icy-mix of the United States is

characterized by a combination of a t ight monetary pol icy

deriving from the new operat ional procedures inaugurated in

October 1979, and the f iscal pol icy adopted by the Reagan

Administrat ion.

How did this pol icy-mix deepen the recession in the

United States (1980-82) tr iggered by the second oi l cr is is ,

and inf luence the appreciat ion of the dol lar (1980-83)? To

what extent did this pol icy-mix af fect the Japanese business

cyc le (1980-1983) , the depreciat ion of the yen (1981-83) and

the large current account surplus (1983)? Our object ive in

this s tudy is to c lar i fy these issues quantitat ively using

the U.S. -Japan l ink model ( to be explained later) . The

report does not seek to evaluate the U.S. pol icy-mix or

Japanese economic pol icy . With this point in mind, the

fo l lowing analys is was conducted for two di f ferent periods :

1) recession in the United States from 1980 to 1982; and 2)

recovery which began in early 1983.

-2-

B . Methodology

This analys is was conducted by l inking Japan and U.S.

econometric models with a world trade l inkage model . These

models have been completely reest imated, with good results

for the f inal tests , and are referred to as the "U.S. -Japan

l ink model . " The sample data for the reest imation covers

the period up to 1981. This report is based on a mult ipl ier

test appl ied to the f ive -year period 1977-81. In other words,

the ef fects o f var ious types o f pol icy combinations, such as

the U.S. pol icy-mix or the Japanese pol icy mentioned below,

were analyzed by this interpolat ion test period. The results

o f this s imulat ion were reinterpreted as the ef fect o f U.S.

pol icy-mix during 1980-83 (see "Points for Considerat ion in

Interpret ing the Results" in Appendix 2) .

Accordingly , this analysis should be understood as an

interim report on the work begun in Apri l 1983 with the aim

of ful ly revis ing the EPA World Economic Model . I t a lso

shows one appl icat ion of the model to be ut i l ized from here

on.

I . Development of the U.S. Pol icy-Mix

(1) In October 1979, i t was decided to shi f t the inter-

mediate target o f monetary pol icy of the Federal Reserve

-3-

Board from federal fund rates to quantitat ive indicators

such as bank reserves and money supply . Because of the

confusion fo l lowing this and other inst i tut ional changes,

the money market in the f irst hal f o f 1980 experienced

vio lent f luctuations in credit avai labi l i ty and interest

rates . In the meanwhile , inf lat ion continued to accelerate .

(2) Consequently , the Federal Reserve Board switched to a

t ight monetary pol icy from the end of 1980.

(3) After taking of f ice in 1981, the Reagan Administrat ion

continued the exist ing t ight monetary pol icy advocated by

monetarists , whi le i ts f iscal pol icy was based on supply-

s ide economics . This was a mixture o f money supply restraints

to bring down the inf lat ion rate , and tax reductions to

increase savings and product ivity .

(4) This t ight monetary pol icy resulted in unprecedentedly

high interest rates , which once again pushed business act ivity

into recession from the second hal f o f 1981 through 1982.

In 1982, unemployment soared to over 10 percent .

(5 ) The inf lat ion rate o f the consumer price index s lowed

considerably from 1982.

(6 ) From mid-1982, the Federal Reserve Board re laxed i ts

t ight monetary pol icy s l ightly and interest rates decl ined,

though they began to r ise again in ear ly 1983.

-4-

(7 ) The ef fects o f three separate reduct ions in personal

income tax (October 1981, July 1982 and July 1983) helped

the U.S. economy start a rapid recovery from 1983.

(8) The impact o f these pol ic ies on the U.S. and Japanese

economies were calculated through s imulat ion based on the

U.S. -Japan l ink model , with the fo l lowing results .

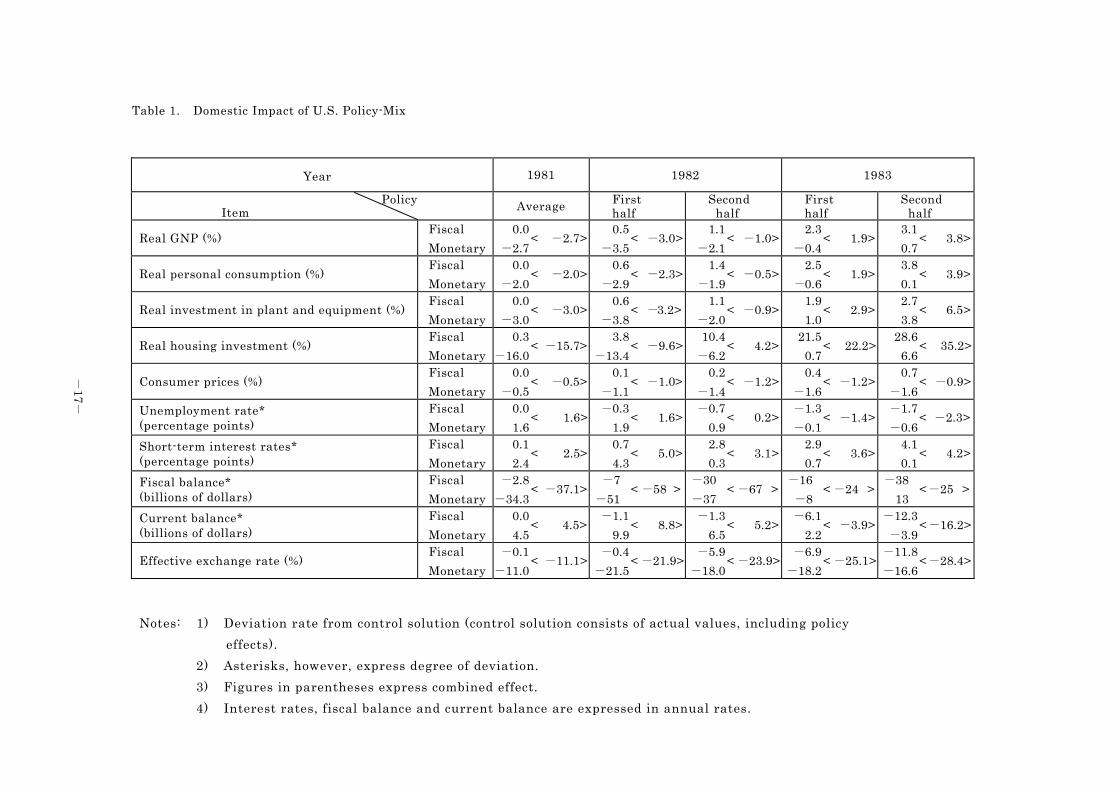

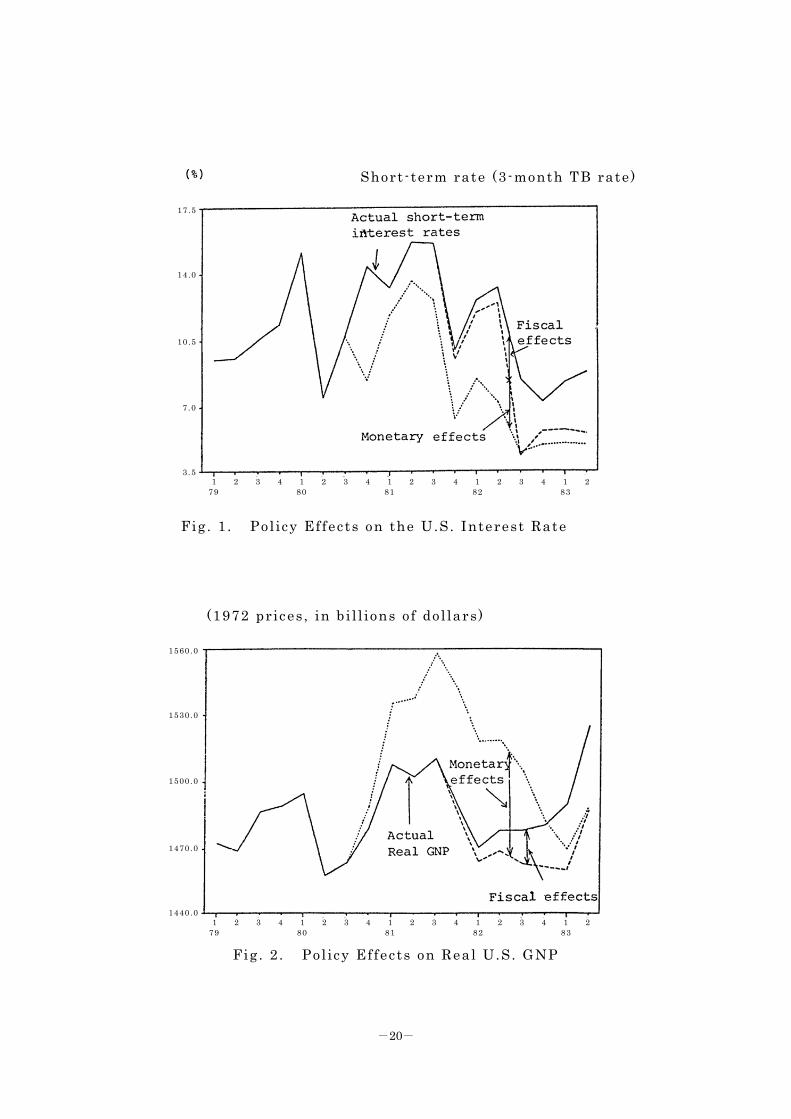

I I . Impact on the U.S. Economy

(Refer to Table 1 , Figs . 1-3. )

A. Impact on the Business Cl imate, Interest Rates , and

Inf lat ion

(1) The t ighter monetary pol icy init iated in the latter

hal f o f 1980 raised short -term interest rates by 4 .3

percentage points in the f irst hal f o f 1982.

(2 ) I t diminished personal consumption by 2 .9 percent ,

pr ivate investment in plant and equipment by 3 .8 percent ,

and housing investment by 13.4 percent . The result was a

3 .5 percent drop in GNP. I t is thus c lear that monetary

restraint had a major def lat ionary ef fect .

(3) The 5 percent cut in personal income taxes in the fourth

quarter of 1981 increased personal consumption by 0 .6 percent ,

pr ivate investment in plant and equipment by 0 .6 percent ,

and housing investment by 3 .8 percent in the f irst -hal f o f

-5-

1982. This tax reduct ion also caused a 0 .5 percent growth

in GNP. But because of the t ight monetary pol icy , the

recession continued and the net impact on GNP was a 3 .0

percent decl ine in the f irst hal f o f 1982.

(4) At the start o f the second hal f o f 1982, the t ight

monetary pol icy was re laxed to an extent , and personal

income taxes were cut for a second t ime, by 10 percent .

(5) In the second hal f o f 1982, the U.S. pol icy-mix

contr ibuted to a r ise in short -term interest rates o f 3 .1

percentage points . The breakdown showed that out o f this

total r ise , 2 .8 percentage points were attr ibutable to

expansionary f iscal pol icy result ing from the increased

demand for money, whi le 0 .3 percentage points were due to

monetary pol icy . In 1983, short -term interest rates rose by

4 .1 percentage points due mainly to the ef fects o f the f iscal

pol icy . Because long-term interest rates do not react

immediately to short -term rate increases ( the term structure

of interest rates ) , the impact o f the t ight monetary pol icy

on long term interest rates remained strong through 1982

(1 .9 percentage points higher) and 1983 (1 .6 percentage

points higher) . When the ef fects o f f iscal pol icy on

interest rates are included, the total e f fect o f the pol icy-

mix was a r ise in long term interest rates of 2 .5 percentage

points in 1982 and 3.3 percentage points in 1983.

-6-

(6 ) In the second hal f o f 1982, the ef fects o f monetary

pol icy on personal consumption were minus 1 .9 percent , whi le

those of tax cuts were plus 1 .4 percent . The pol icy-mix as

a whole continued to operate as a minus factor . Regarding

private investment in plant and equipment, monetary po l icy

ef fects were minus 2 .0 percent and tax cut ef fects were plus

1 .1 percent- -a combined total o f minus 0 .9 percent . In

housing investment, however , the minus ef fects o f the

monetary pol icy were exceeded by the favorable e f fects o f

tax reductions, g iving an overal l gain of 4 .2 percent . With

regard to the impact on GNP, the plus 1 .1 percent ef fect o f

the f iscal pol icy was of fset by a 2 .1 percent decl ine due to

monetary pol icy , result ing in an overal l 1 .0 percent decrease.

(7) In the f irst hal f o f 1983, the combined ef fect on

aggregated demand of tax reduct ions and re laxed monetary

controls f rom the second hal f o f 1982 was an 1 .9 percent

increase in GNP supported by increases in al l expenditure

i tems.

(8) In July 1983, income tax was cut for a third t ime, again

by 10 percent and i t is predicted that the expansionary ef fect

on GNP in the second hal f o f 1983 wil l be about 3 .8 percent .

This e f fect wi l l increase housing investment, pr ivate plant

and equipment investment and personal consumption, in that

order .

-7-

(9 ) The t ight monetary pol icy 's e f fect in curbing inf lat ion,

which was i ts primary object ive , helped lower the consumer

price index over the entire period, with a 1 .2 percent decl ine

in the second hal f o f 1982. Subsequently , however , the

decelerat ing inf lat ion rate of the consumer price index was

halted by the business recovery mentioned above .

B. Impact on General Government Budget Def ic i ts

(10) The general government budget def ic i t widened due to

tax reductions even when increased tax revenues stemming

from business improvements due to the tax reduct ion were

taken into account . The def ic i ts increased by $7 bi l l ion in

the f irst hal f o f 1982, $30 bi l l ion in the second hal f o f

1982, $16 bi l l ion in the f irst hal f o f 1983, and $38 bi l l ion

in the second hal f o f 1983.

(11) When the def ic i ts created by the t ight monetary pol icy

that tr iggered the recession are combined, they give a $58

bi l l ion def ic i t for the f irst hal f o f 1982 and $67 bi l l ion

def ic i t for the second hal f . In 1983, increased tax revenues

reduced the def ic i t to approximately $24.5 bi l l ion ( f igures

on annual basis ) .

(12) The fo l lowing factors are also behind recent def ic i t

increases , a l though they are not included in this model

analys is : 1 ) increases in interest payments on publ ic debt

-8-

due to the larger def ic i t and higher interest rates ; 2) lower

corporate tax revenues due to accelerated depreciat ion; 3 )

the def ic i t due to the recession induced by the second oi l

cr is is .

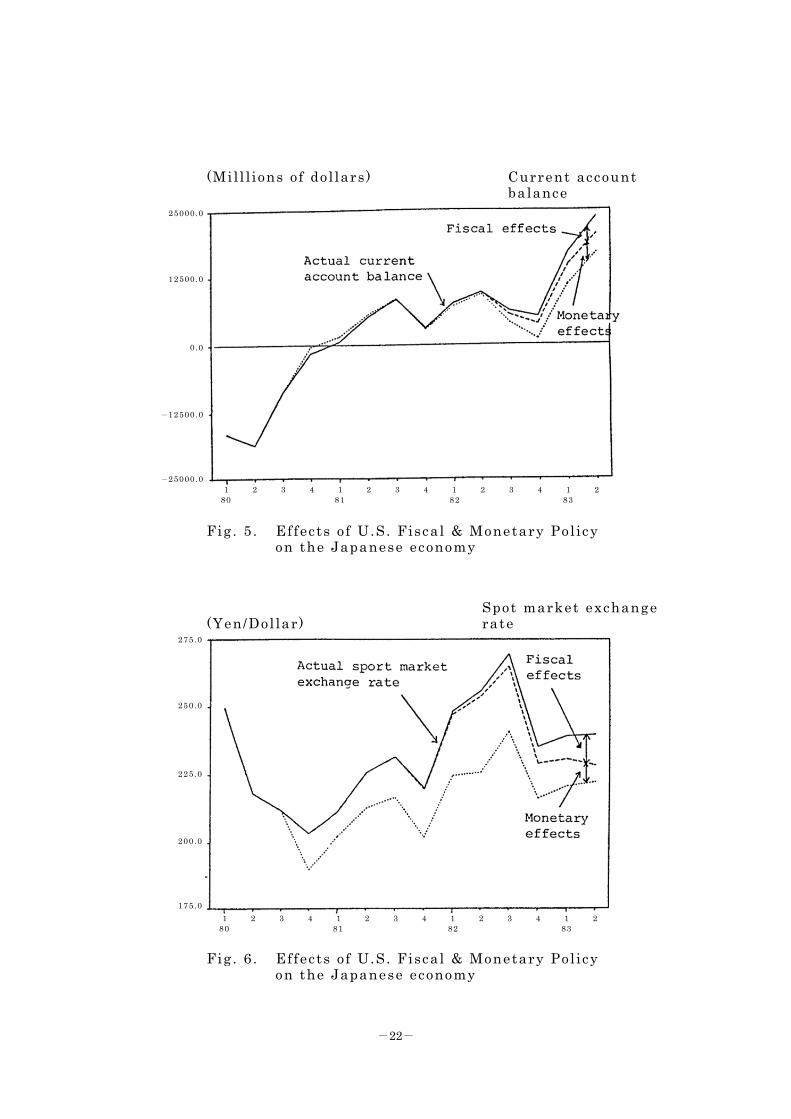

C. Impact on the Current Account Balance

(13) Regarding the ef fects on trade in goods and services ,

net exports , de f ined as exports minus imports , decl ined in

both 1982 and 1983. This was because forces working for

increases in net exports were more than of fset by counter-

forces working for decl ines in net exports . The former

forces inc luded the recession caused by t ight money and

strengthened internat ional competit iveness caused by the

s lowing inf lat ion rate . The latter counterforces inc luded a

contract ion in world trade due to the recession in the United

States , a decl ine in international competit iveness attr ibutable

to the appreciat ion of the dol lar , and the increased payments

o f investment income because of high interest rates , a l l o f

which contributed to a decrease in net exports in 1982-83.

Net exports decl ined ( in other words, net imports increased)

especial ly sharply in 1983, accounting for nearly 20 percent

o f the incremental o f domestic demand.

-9-

(14) Despite the decrease in net exports mentioned above,

the current account remained in surplus unti l mid-1982,

because o f the J-Curve ef fect tr iggered by the appreciat ion

of the dol lar . The subsequent business recovery increased

imports and weakened internat ional competit iveness because

the appreciat ion of the dol lar resulted in a massive current

account def ic i t in the second hal f o f 1983 (equivalent to

0 .6 percent of nominal GNP, approximately $16 bi l l ion on an

annual basis ) .

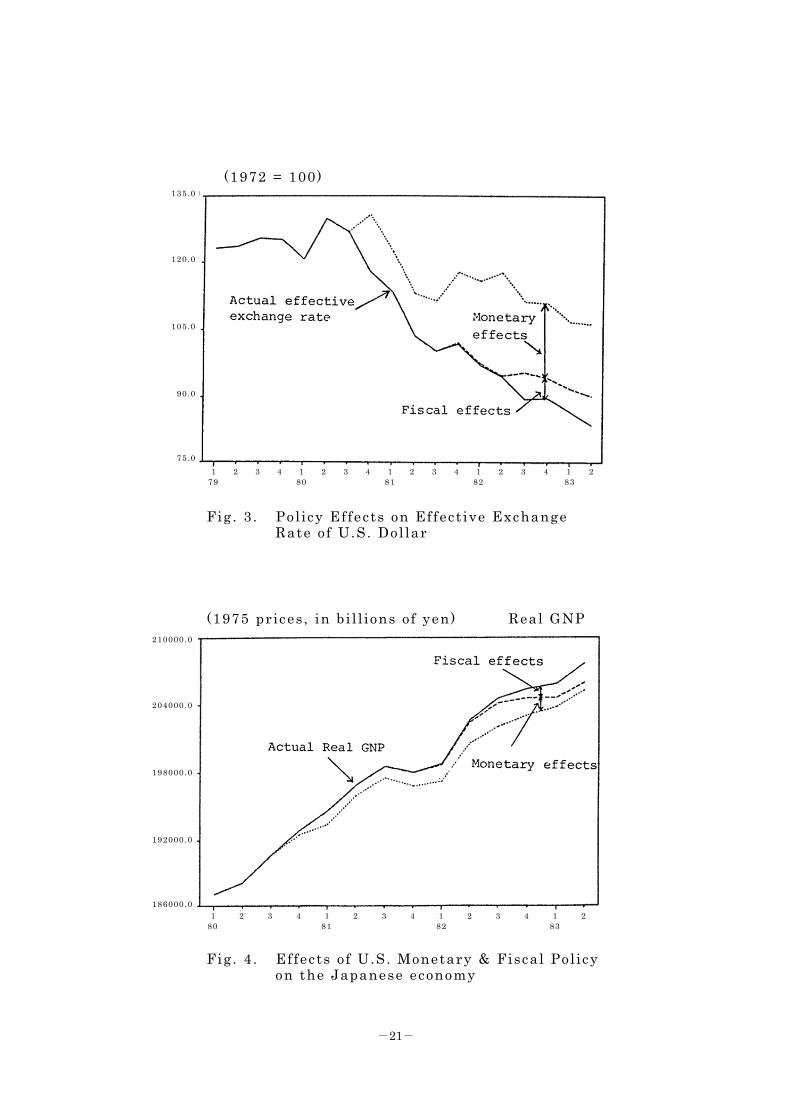

D. Impact on the Dol lar Effect ive Exchange Rate

(15) The high interest rates due to the t ight monetary pol icy

and expansionary f iscal pol icy widened the gap between

domestic and foreign interest rates , prompting an inf low of

capital into the U.S. and a consequently sharp appreciat ion

in the ef fect ive exchange dol lar rate . Namely, the monetary

pol icy boosted the value of the dol lar by approximately 22

percent during the f irst hal f o f 1982 and the subsequent

re laxation of monetary restr ict ions contributed less and

less to the dol lar appreciat ion. Instead, however , f iscal

pol icy contributed more and more to the appreciat ion of the

dol lar . In the latter hal f o f 1983, the combined ef fect o f

monetary and f iscal pol icy was a 28.4 percent appreciat ion

of the dol lar .

-10-

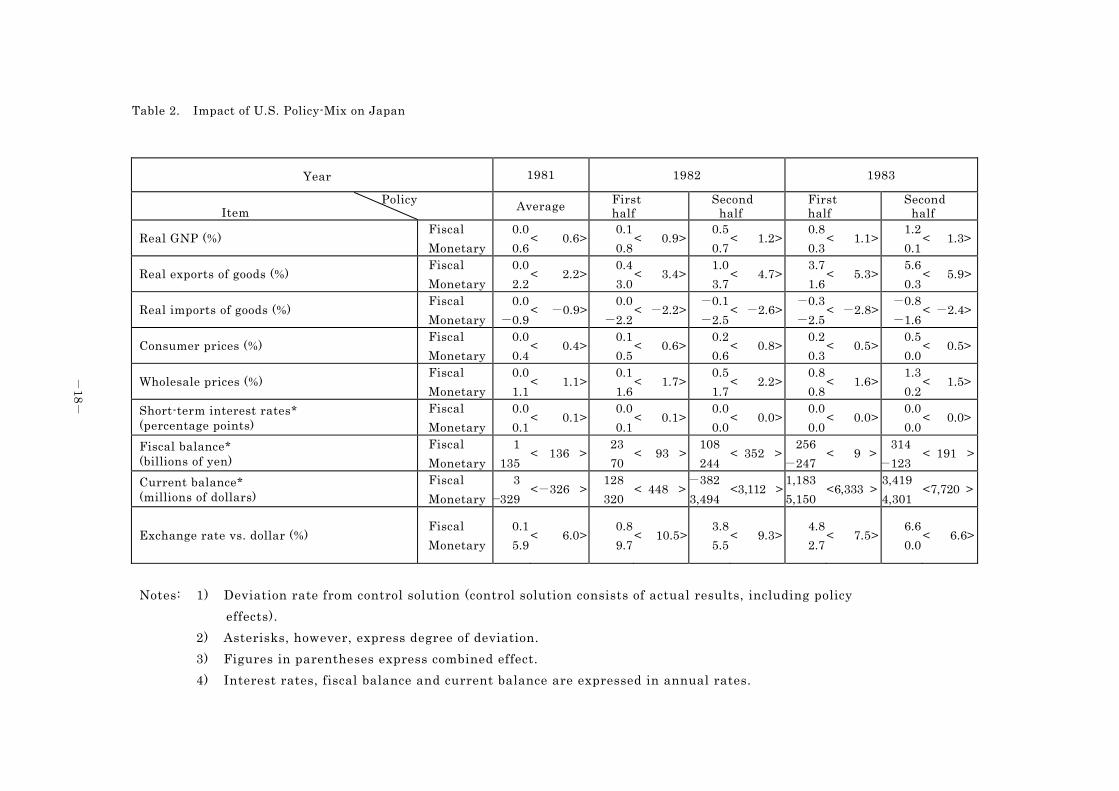

I II . Impact on the Japanese Economy

A. Direct Impact o f the U.S. Pol icy-Mix on the Japanese

Economy

(Refer to Table 2 , Figs . 4-6. )

(1) High interest rates result ing from the U.S. pol icy-mix

widened the gap between domestic and overseas interest rates ,

and generated incipient capital in f lows into the U.S. As a

consequence, the yen depreciated by 10.5 percent in the f irst

hal f o f 1982, by 9 .3 percent in the second hal f , by 7 .5

percent in the f irst hal f o f 1983 and by 6 .6 percent in the

second hal f . (A 10 percent depreciat ion represents approxi -

mately minus 25 yen to the dol lar . )

(2 ) The depreciat ion of the yen pushed the dol lar pr ice o f

Japanese export down by over 5 percent in 1982 and about 4

percent in 1983, thus strengthening Japan's internat ional

competit iveness .

(3) Despite the contract ion in world trade due to the U.S.

recession, Japan's strengthened international competi t iveness

boosted Japanese exports by 4 .1 percent in 1982. In 1983,

the U.S. economy recovered and world trade expanded, which

together with the internat ional competit iveness of Japanese

exports , resulted in a 5 .6 percent increase in Japanese

exports o f goods.

-11-

(4 ) Imports were also af fected by the depreciat ion of the

yen, and decl ined by 2 .5 percent in both 1982 and 1983.

(5) This resulted in an increase o f over $1.7 bi l l ion in

the current account surplus in 1982, and that o f about $7.0

bi l l ion in 1983.

(6) Ref lect ing higher exports , the GNP grew by 1 .03 percent

in 1982 and 1.20 percent in 1983.

B. Japan's Monetary pol icy vis -a-vis the Yen's Depreciat ion

and the Effects o f This Pol icy

(7) Because o f high U.S. interest rates , the yen depreciated

against tne dol lar and induced the Bank of Japan to delay

lowering the Off ic ial Discount Rate and to adopt a pol icy of

higher market interest rates . This was because the Bank of

Japan feared that further depreciat ion of the yen would lead

to a rekindl ing o f inf lat ion and also to an increase in net

exports . As a result , market interest rates rose by 0 .65

percentage points in 1982 and by 0 .80 percentage points in

1983.

(8) This act ion taken by the Bank of Japan produced a 0 .2

percent and 0.3 percent def lat ionary ef fect on GNP in 1982

and 1983, respect ively .

(9) The ef fects o f the pol icy on the exchange rate o f the

yen were a 0 .66 percent appreciat ion ( just under two yen per

-12-

dol lar) in 1982, and a 0 .91 percent appreciat ion ( just over

two yen per dol lar) in 1983.

(10) The appreciat ion caused by this monetary pol icy created

a $20 mil l ion current account def ic i t in 1982, whereas

def lat ionary ef fects produced a $100 mil l ion surplus in 1983.

(11) The consumer price index fe l l by about 0 .15 percent in

both 1982 and 1983.

(12) In short , the def lat ionary ef fects on GNP mentioned

above const i tute the cost o f insulat ing the yen 's exchange

rate , the consumer price index, and net exports , f rom the

U.S. pol icy-mix.

C. Comparison of the Impact o f U.S. Economic Pol icy and

Japanese Fiscal Pol icy on the Expansion of Japan's

Current Account Surplus

(13) To what extent is the recent increase in Japan's current

account surplus due to s luggish domestic demand? Is this a

major or minor factor compared to the impact o f the U.S.

pol icy-mix on the surplus increase? To analyze these issues ,

the ef fects o f Japanese f iscal pol icy have to be taken into

account .

(14) A po l icy a imed to reconstruct government f inances

through restraining f iscal expenditures was adopted in the

-13-

FY 1981 budget . What was the inf luence of this po l icy on

the exchange rate and current account imbalance? To respond

to these quest ions, a case was s imulated in which the average

rat io o f publ ic investment to GNP during 1976-80 (9 .6 percent ,

in 1975 prices) remained unchanged from the fourth quarter

of 1981. This assumption impl ies the "neutral approach" of

f iscal management to the business cycle . Then, the di f ference

between the f iscal reconstruct ion approach and the neutral

approach was calculated.

(15) According to this comparison, the pol icy to restrain

publ ic spending had a def lat ionary ef fect on GNP of 0 .67

percent in 1982 and 0.98 percent in 1983.

(16) This caused a decrease in the value of imports and an

increase in the value of exports , and expanded the current

account surplus by just under $1 bi l l ion in 1982, and just

over $1.4 bi l l ion in 1983. This is smal l compared to the

previously mentioned ef fects o f the U.S. pol icy-mix on the

incremental o f Japan's current account surplus . The pol icy

to restr ict publ ic works expenditure strengthened the yen by

0 .49 percent ( just over one yen per dol lar) in 1982 and by

1 .27 percent ( just under three yen per dol lar) in 1983.

(17) While publ ic works expenditure was cut down by just

over ¥1.3 tr i l l ion, tax revenues also fe l l due to the

-14-

def lat ionary ef fects o f such expenditure cuts , and when that

revenue decl ine is subtracted, improvements in the government

imbalance were just short o f ¥800 bi l l ion in 1982 and ¥600

bi l l ion in 1983.

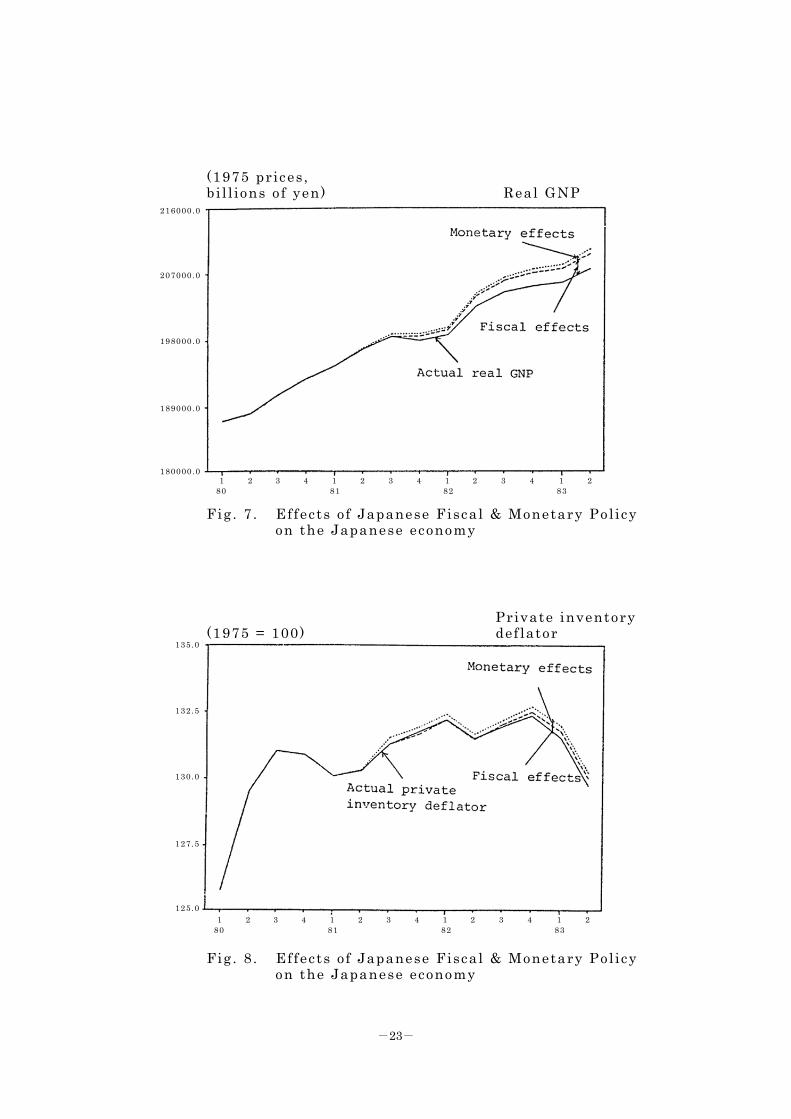

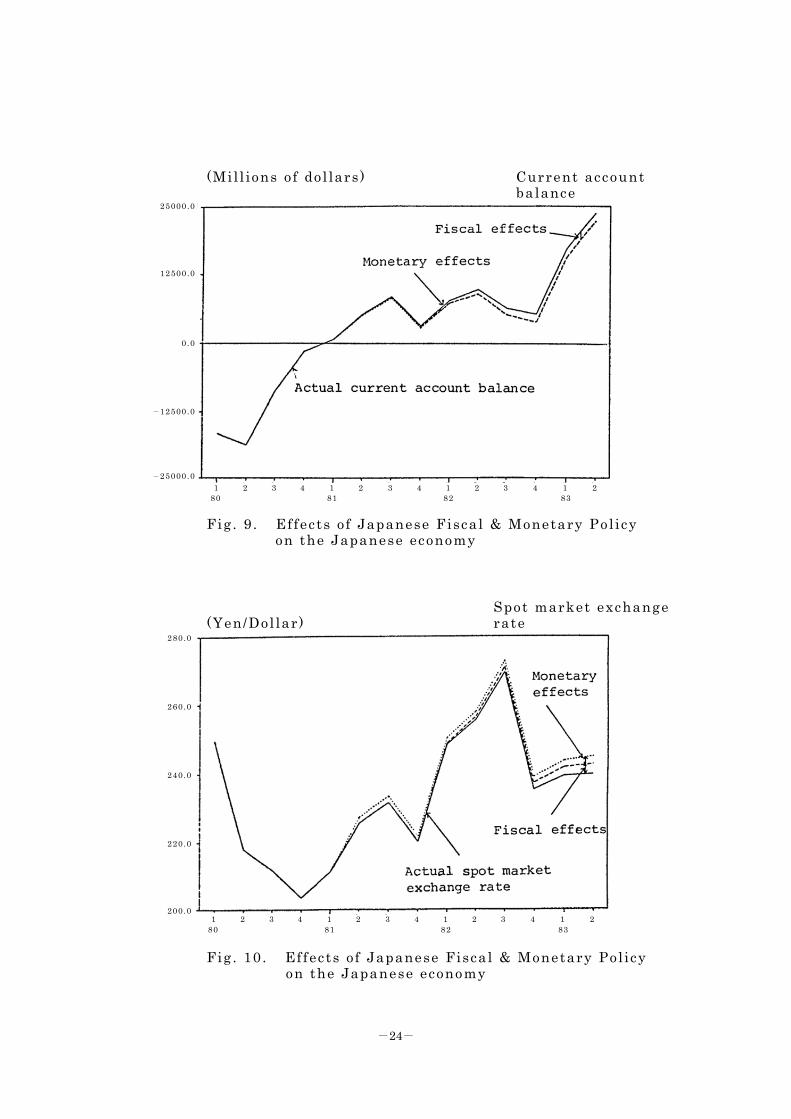

IV. Conclusion

The above s imulat ion analysis can be summarized for the

major economic var iables as fo l lows.

(1) Causes of high U.S. interest rates

With regard to short -term interest rates , U.S. monetary

pol icy played an important ro le in a higher interest rate

(by 2 .4 percentage points in 1981, 2 .3 percentage points in

1982, and 0 .4 percentage points in 1983) , a lthough there is

a trend for f iscal pol icy to be more important in rais ing

interest rates (1 .8 percentage points in 1982 and 3.5

percentage points in 1983) .

(2) Increase in U.S. general government budget def ic i ts

Through 1982, the def ic i t created by the recession

tr iggered by the t ight monetary pol icy accounted for the

bulk of the total de f ic i t ($34 bi l l ion in 1981, and $44

bi l l ion in 1982) . S ince 1983, the def ic i t has increased due

mainly to tax reductions (amounting to $3 bi l l ion in 1981,

$19 bi l l ion in 1982 and further to $27 bi l l ion in 1983) .

-15-

(3 ) U.S. business recovery

The tax cut po l icy is a major contributor to the

recovery, rais ing GNP by 2 .7 percent in 1983. Regarding the

business recovery pattern, however , whi le personal consump-

t ion rose 2 .9 percent , housing investment by 28.7 percent ,

and pr ivate investment in plant and equipment by 4 .7 percent ,

net exports decl ined by c lose to 20 percent o f the incremental

o f the domestic demand in 1983, ref lect ing the strong dol lar

and expanded domestic demand.

(4 ) Ef fect ive dol lar exchange rate

Due to the U.S. pol icy-mix, the do l lar appreciated by

11.1 percent in 1981, 22.9 percent in 1982 and 26.8 percent

in 1983.

(5) Yen depreciat ion s ince 1981

This was primari ly the result o f the U.S. pol icy-mix,

which contr ibuted to the depreciat ion of the yen by 6 .0

percent in 1981, 9 .9 percent in 1982 and 7.1 percent in 1983

(a 10 percent depreciat ion represents a f loatdown of approxi -

mately 25 yen per dol lar ) . In contrast , both Japanese

monetary and f iscal pol ic ies strengthened the yen in 1982

and 1983, within the range of just over one yen to just under

three yen per dol lar .

-16-

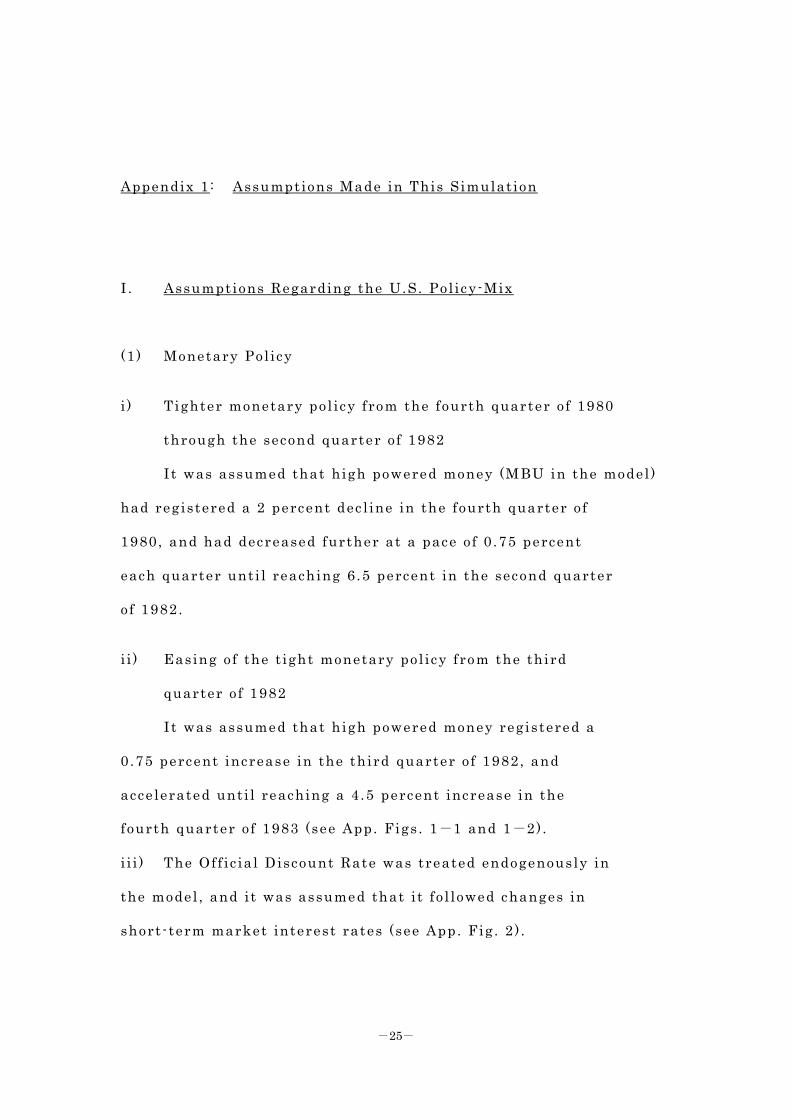

(6 ) Japan's current account surplus increase in 1983

Here too the U.S. pol icy-mix played a major ro le .

While this pol icy-mix produced a $7 bi l l ion surplus in

Japan's current account , Japan's f iscal pol icy produced just

over $1.4 bi l l ion in surplus, and i ts monetary po l icy $100

mil l ion.

(7 ) Increase in Japan's real GNP in 1983

Expansion in net exports o f goods is the major factor ,

increasing GNP by 1 .1 percent . The greater part o f this

increase was the result o f the strengthened do l lar together

with the expanded U.S. domestic demand induced by the U.S.

pol icy-mix.

-17

-

Table 1. Domestic Impact of U.S. Policy-Mix

Year 1981 1982 1983

Item Policy

Average First half

Secondhalf

Firsthalf

Secondhalf

Real GNP (%) Fiscal

Monetary

0.0

-2.7< -2.7>

0.5

-3.5 < -3.0>

1.1

-2.1< -1.0>

2.3

-0.4< 1.9>

3.1

0.7< 3.8>

Real personal consumption (%) Fiscal

Monetary

0.0

-2.0< -2.0>

0.6

-2.9 < -2.3>

1.4

-1.9< -0.5>

2.5

-0.6< 1.9>

3.8

0.1< 3.9>

Real investment in plant and equipment (%)Fiscal

Monetary

0.0

-3.0< -3.0>

0.6

-3.8 < -3.2>

1.1

-2.0< -0.9>

1.9

1.0< 2.9>

2.7

3.8< 6.5>

Real housing investment (%) Fiscal

Monetary

0.3

-16.0< -15.7>

3.8

-13.4 < -9.6>

10.4

-6.2< 4.2>

21.5

0.7< 22.2>

28.6

6.6< 35.2>

Consumer prices (%) Fiscal

Monetary

0.0

-0.5< -0.5>

0.1

-1.1 < -1.0>

0.2

-1.4< -1.2>

0.4

-1.6< -1.2>

0.7

-1.6< -0.9>

Unemployment rate* (percentage points)

Fiscal

Monetary

0.0

1.6< 1.6>

-0.3

1.9 < 1.6>

-0.7

0.9< 0.2>

-1.3

-0.1< -1.4>

-1.7

-0.6< -2.3>

Short-term interest rates* (percentage points)

Fiscal

Monetary

0.1

2.4< 2.5>

0.7

4.3 < 5.0>

2.8

0.3< 3.1>

2.9

0.7< 3.6>

4.1

0.1< 4.2>

Fiscal balance* (billions of dollars)

Fiscal

Monetary

-2.8

-34.3< -37.1>

-7

-51 < -58 >

-30

-37< -67 >

-16

-8< -24 >

-38

13<-25 >

Current balance* (billions of dollars)

Fiscal

Monetary

0.0

4.5< 4.5>

-1.1

9.9 < 8.8>

-1.3

6.5< 5.2>

-6.1

2.2< -3.9>

-12.3

-3.9<-16.2>

Effective exchange rate (%) Fiscal

Monetary

-0.1

-11.0< -11.1>

-0.4

-21.5 < -21.9>

-5.9

-18.0< -23.9>

-6.9

-18.2< -25.1>

-11.8

-16.6<-28.4>

Notes: 1) Deviation rate from control solution (control solution consists of actual values, including policy

effects).

2) Asterisks, however, express degree of deviation.

3) Figures in parentheses express combined effect.

4) Interest rates, fiscal balance and current balance are expressed in annual rates.

-18

-

Table 2. Impact of U.S. Policy-Mix on Japan

Year 1981 1982 1983

Item Policy

Average First half

Secondhalf

Firsthalf

Secondhalf

Real GNP (%) Fiscal

Monetary

0.0

0.6< 0.6>

0.1

0.8 < 0.9>

0.5

0.7< 1.2>

0.8

0.3< 1.1>

1.2

0.1< 1.3>

Real exports of goods (%) Fiscal

Monetary

0.0

2.2< 2.2>

0.4

3.0 < 3.4>

1.0

3.7< 4.7>

3.7

1.6< 5.3>

5.6

0.3< 5.9>

Real imports of goods (%) Fiscal

Monetary

0.0

-0.9< -0.9>

0.0

-2.2 < -2.2>

-0.1

-2.5< -2.6>

-0.3

-2.5< -2.8>

-0.8

-1.6< -2.4>

Consumer prices (%) Fiscal

Monetary

0.0

0.4< 0.4>

0.1

0.5 < 0.6>

0.2

0.6< 0.8>

0.2

0.3< 0.5>

0.5

0.0< 0.5>

Wholesale prices (%) Fiscal

Monetary

0.0

1.1< 1.1>

0.1

1.6 < 1.7>

0.5

1.7< 2.2>

0.8

0.8< 1.6>

1.3

0.2< 1.5>

Short-term interest rates* (percentage points)

Fiscal

Monetary

0.0

0.1< 0.1>

0.0

0.1 < 0.1>

0.0

0.0< 0.0>

0.0

0.0< 0.0>

0.0

0.0< 0.0>

Fiscal balance* (billions of yen)

Fiscal

Monetary

1

135< 136 >

23

70 < 93 >

108

244< 352 >

256

-247< 9 >

314

-123< 191 >

Current balance* (millions of dollars)

Fiscal

Monetary

3

-329<-326 >

128

320 < 448 >

-382

3,494<3,112 >

1,183

5,150<6,333 >

3,419

4,301<7,720 >

Exchange rate vs. dollar (%) Fiscal

Monetary

0.1

5.9< 6.0>

0.8

9.7 < 10.5>

3.8

5.5< 9.3>

4.8

2.7< 7.5>

6.6

0.0< 6.6>

Notes: 1) Deviation rate from control solution (control solution consists of actual results, including policy

effects).

2) Asterisks, however, express degree of deviation.

3) Figures in parentheses express combined effect.

4) Interest rates, fiscal balance and current balance are expressed in annual rates.

-19

-

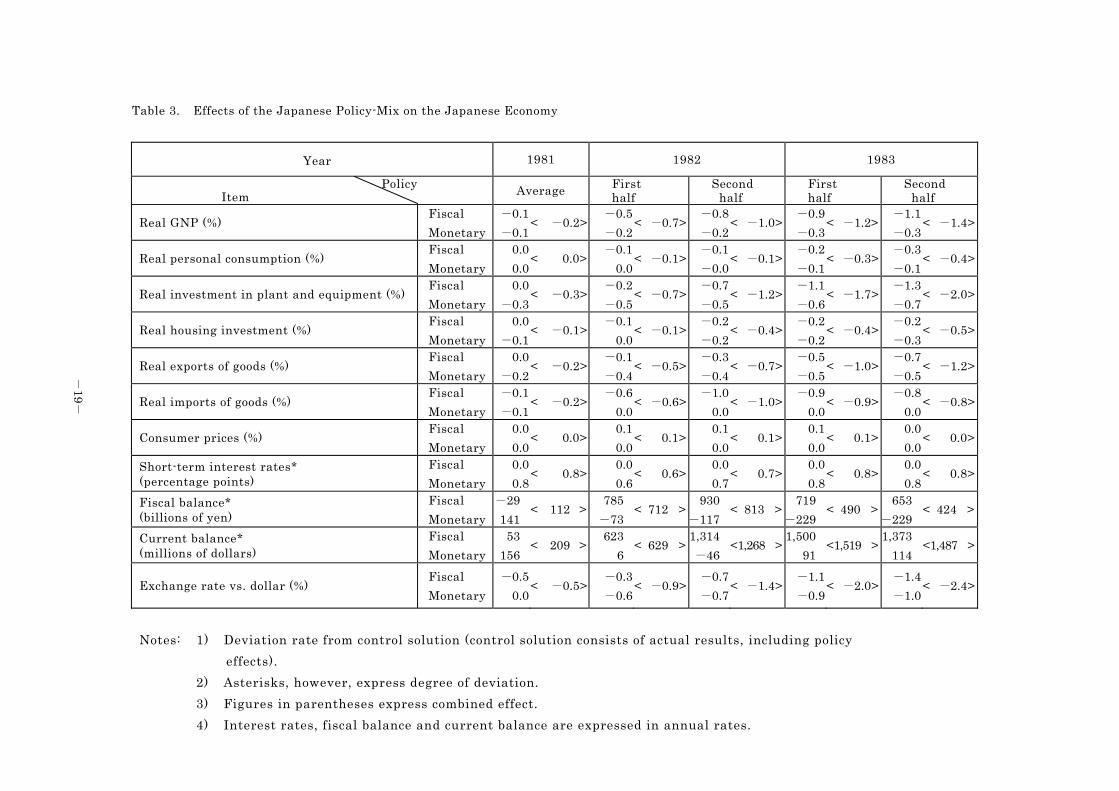

Table 3. Effects of the Japanese Policy-Mix on the Japanese Economy

Year 1981 1982 1983

Item Policy

Average First half

Secondhalf

Firsthalf

Secondhalf

Real GNP (%) Fiscal

Monetary

-0.1

-0.1< -0.2>

-0.5

-0.2 < -0.7>

-0.8

-0.2< -1.0>

-0.9

-0.3< -1.2>

-1.1

-0.3< -1.4>

Real personal consumption (%) Fiscal

Monetary

0.0

0.0< 0.0>

-0.1

0.0 < -0.1>

-0.1

-0.0< -0.1>

-0.2

-0.1< -0.3>

-0.3

-0.1< -0.4>

Real investment in plant and equipment (%)Fiscal

Monetary

0.0

-0.3< -0.3>

-0.2

-0.5 < -0.7>

-0.7

-0.5< -1.2>

-1.1

-0.6< -1.7>

-1.3

-0.7< -2.0>

Real housing investment (%) Fiscal

Monetary

0.0

-0.1< -0.1>

-0.1

0.0 < -0.1>

-0.2

-0.2< -0.4>

-0.2

-0.2< -0.4>

-0.2

-0.3< -0.5>

Real exports of goods (%) Fiscal

Monetary

0.0

-0.2< -0.2>

-0.1

-0.4 < -0.5>

-0.3

-0.4< -0.7>

-0.5

-0.5< -1.0>

-0.7

-0.5< -1.2>

Real imports of goods (%) Fiscal

Monetary

-0.1

-0.1< -0.2>

-0.6

0.0 < -0.6>

-1.0

0.0< -1.0>

-0.9

0.0< -0.9>

-0.8

0.0< -0.8>

Consumer prices (%) Fiscal

Monetary

0.0

0.0< 0.0>

0.1

0.0 < 0.1>

0.1

0.0< 0.1>

0.1

0.0< 0.1>

0.0

0.0< 0.0>

Short-term interest rates* (percentage points)

Fiscal

Monetary

0.0

0.8< 0.8>

0.0

0.6 < 0.6>

0.0

0.7< 0.7>

0.0

0.8< 0.8>

0.0

0.8< 0.8>

Fiscal balance* (billions of yen)

Fiscal

Monetary

-29

141< 112 >

785

-73 < 712 >

930

-117< 813 >

719

-229< 490 >

653

-229< 424 >

Current balance* (millions of dollars)

Fiscal

Monetary

53

156< 209 >

623

6 < 629 >

1,314

-46<1,268 >

1,500

91<1,519 >

1,373

114<1,487 >

Exchange rate vs. dollar (%) Fiscal

Monetary

-0.5

0.0< -0.5>

-0.3

-0.6 < -0.9>

-0.7

-0.7< -1.4>

-1.1

-0.9< -2.0>

-1.4

-1.0< -2.4>

Notes: 1) Deviation rate from control solution (control solution consists of actual results, including policy

effects).

2) Asterisks, however, express degree of deviation.

3) Figures in parentheses express combined effect.

4) Interest rates, fiscal balance and current balance are expressed in annual rates.

-20-

Short - term rate (3-month TB rate)

Fig . 1 . Pol icy Effects on the U.S. Interest Rate

(1972 prices , in bi l l ions of dol lars)

Fig . 2 . Pol icy Effects on Real U.S. GNP

1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 79 80 81 82 83

1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 79 80 81 82 83

17 .5

14 .0

10 .5

7 .0

3 .5

1560 .0

1530 .0

1500 .0

1470 .0

1440 .0

-21-

(1972 = 100)

Fig . 3 . Pol icy Effects on Effect ive Exchange

Rate of U.S. Dol lar

(1975 prices , in bi l l ions of yen) Real GNP

Fig . 4 . Ef fects o f U.S. Monetary & Fiscal Pol icy on the Japanese economy

1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 79 80 81 82 83

1 2 3 4 1 2 3 4 1 2 3 4 1 2 80 81 82 83

135.0

120.0

105.0

90 .0

75 .0

210000.0

204000.0

198000.0

192000.0

186000.0

-22-

(Mi l l l ions of dol lars) Current account balance

Fig . 5 . Ef fects o f U.S. Fiscal & Monetary Pol icy on the Japanese economy

Spot market exchange (Yen/Dol lar) rate

Fig . 6 . Ef fects o f U.S. Fiscal & Monetary Pol icy

on the Japanese economy

1 2 3 4 1 2 3 4 1 2 3 4 1 2 80 81 82 83

1 2 3 4 1 2 3 4 1 2 3 4 1 2 80 81 82 83

275.0

250.0

225.0

200.0

175.0

25000.0

12500.0

0 .0

-12500.0

-25000.0

-23-

(1975 prices , b i l l ions o f yen) Real GNP

Fig . 7 . Ef fects o f Japanese Fiscal & Monetary Pol icy on the Japanese economy

Private inventory (1975 = 100) def lator

Fig . 8 . Ef fects o f Japanese Fiscal & Monetary Pol icy

on the Japanese economy

1 2 3 4 1 2 3 4 1 2 3 4 1 2 80 81 82 83

1 2 3 4 1 2 3 4 1 2 3 4 1 2 80 81 82 83

135.0

132.5

130.0

127.5

125.0

216000.0

207000.0

198000.0

189000.0

180000.0

-24-

(Mi l l ions o f dol lars) Current account balance

Fig . 9 . Ef fects o f Japanese Fiscal & Monetary Pol icy on the Japanese economy

Spot market exchange (Yen/Dol lar) rate

Fig . 10. Ef fects o f Japanese Fiscal & Monetary Pol icy

on the Japanese economy

25000.0

12500.0

0 .0

-12500.0

-25000.0

280.0

260.0

240.0

220.0

200.0

1 2 3 4 1 2 3 4 1 2 3 4 1 2 80 81 82 83

1 2 3 4 1 2 3 4 1 2 3 4 1 2 80 81 82 83

-25-

Appendix 1 : Assumptions Made in This Simulat ion

I . Assumptions Regarding the U.S. Pol icy-Mix

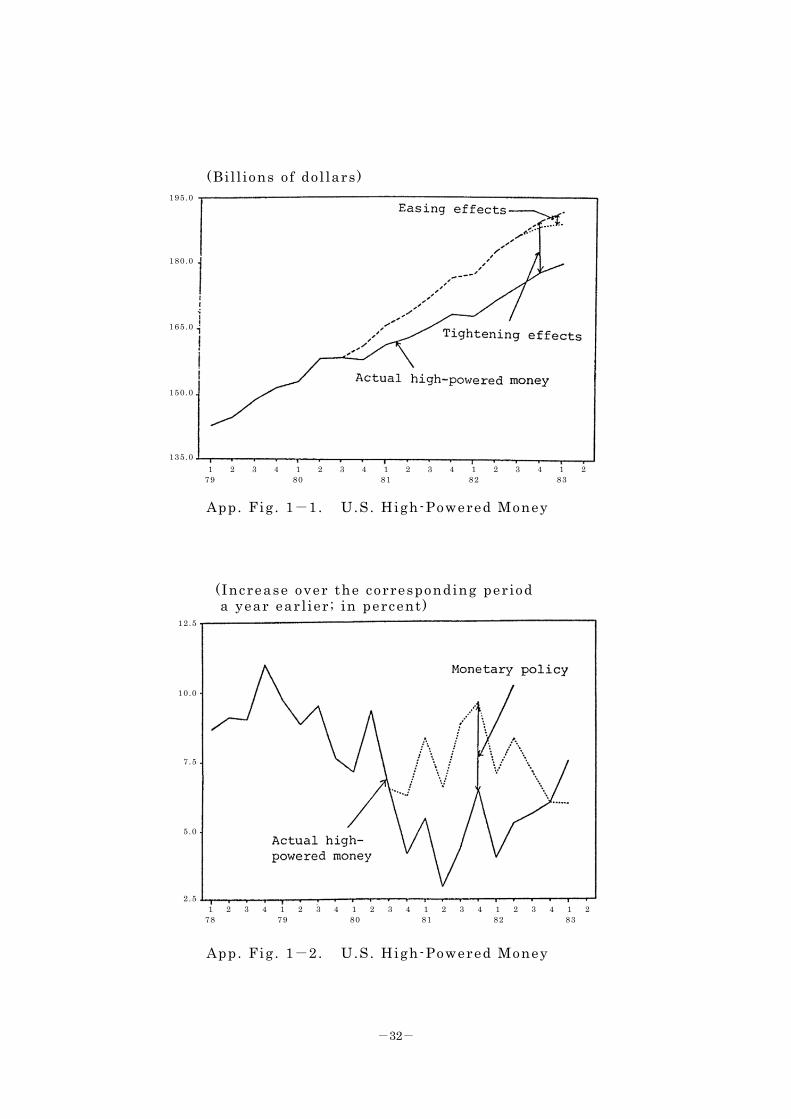

(1) Monetary Pol icy

i ) Tighter monetary pol icy from the fourth quarter o f 1980

through the second quarter o f 1982

It was assumed that high powered money (MBU in the model )

had registered a 2 percent dec l ine in the fourth quarter o f

1980, and had decreased further at a pace of 0 .75 percent

each quarter unti l reaching 6 .5 percent in the second quarter

o f 1982.

i i ) Easing o f the t ight monetary pol icy from the third

quarter of 1982

I t was assumed that high powered money registered a

0 .75 percent increase in the third quarter o f 1982, and

accelerated unti l reaching a 4 .5 percent increase in the

fourth quarter o f 1983 (see App. Figs . 1-1 and 1-2) .

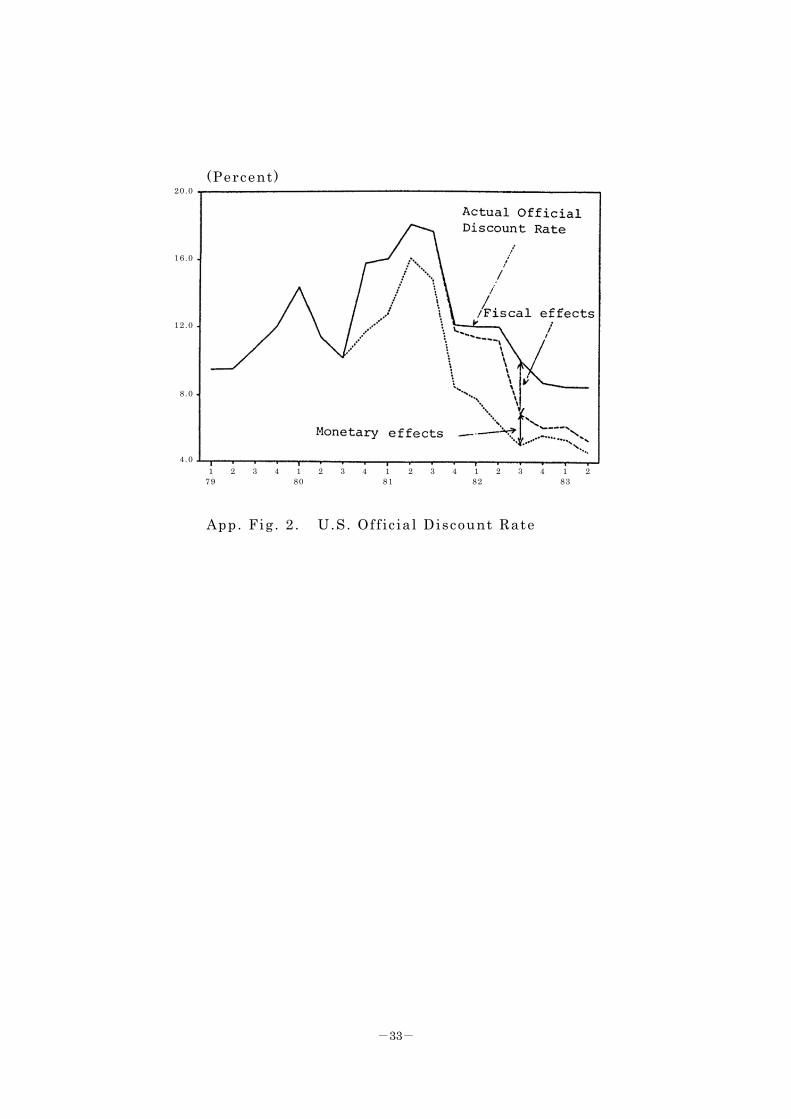

i i i ) The Off ic ial Discount Rate was treated endogenously in

the model , and i t was assumed that i t fo l lowed changes in

short -term market interest rates (see App. Fig . 2) .

-26-

(2 ) Fiscal Pol icy

i ) Cuts in Personal Income Tax

The marginal tax rate was reduced by approximately 25

percent over three years . The assumption made for our

s imulat ion was a total decl ine in revenues from personal

income tax of 25 percent over three years , as fo l lows:

Fourth quarter , 1981 . . . . . 5 percent

Third quarter , 1982 . . . . 10 percent

Third quarter , 1983 . . . . 10 percent

i i ) Other Fiscal Pol ic ies

In addit ion to cuts in personal income tax, the f iscal

pol icy of the Reagan Administrat ion included the fo l lowing:

1 . Changes in expenditure structure ( increase in

defence spending, curbs on social security and

other expenditures)

2 . Corporate tax reductions through accelerated

depreciat ion and easing investment taxes

3 . Increases in indirect tax

These three areas were not included in our analysis

mainly because of the di f f iculty in identi fy ing their content

quanti tat ively and the fact that the model s tructure is not

suf f ic ient ly equiped to handle these po l icy measures .

-27-

I I . Assumptions Regarding Japanese Economic Pol icy

(1 ) Of f ic ial Discount Rate

The actual Off ic ial Discount Rate was as fo l lows:

- Second to third quarter of 1981 . . . . 6 .25 percent

- Fourth quarter of 1981 to third quarter o f 1983 . . . . . . . . . . . . . . 5 .50 percent

- Since fourth quarter o f 1983 . . . . . . . 5 .00 percent

This represents a considerable delay in reducing the

of f ic ia l d iscount rate . The re lat ive scope of the t ight

monetary pol icy was indicated by the di f ference between these

actual rates and the present 5 percent Of f ic ial Discount

Rate (assuming that the rate was cut to 5 percent in the

second quarter of 1981) .

(2) Quanti tat ive Monetary Pol icy

Actual trends in high-powered money did not increase

from the second quarter o f 1982, remaining virtual ly on a

par with previous year levels . This indicated that the rate

of increase in high powered money was lower than the annual

average increase of about 12.5 percent during 1978-81, the

s lowdown in the rate o f increase being taken to represent

the quantitat ive scope of the t ight monetary po l icy .

-28-

(3 ) Fiscal Pol icy

The decrease in the rat io o f publ ic investment to GNP

after the second hal f o f 1981 compared to the average for

1976-80 (9 .6 percent , in 1975 pr ices) was interpreted as a

decl ine in publ ic investment attr ibutable to f iscal

reconstruct ion. This represents decreases in publ ic invest-

ment of 3 percent in the second hal f o f 1981, and of about 6

percent from the second quarter o f 1982.

-29-

Appendix 2 : Points for Considerat ions in Interpret ing the

Results

(1 ) The in-sample period used to compute mult ipl iers was

from 1977 to 1981, not from 1980 to 1983, when the pol ic ies

analysed here were actual ly implemented. In this report ,

the mult ipl ier analysis carr ied out for 1977-81 was inter-

preted as the actual pol icy e f fects in 1980-83.

Mult ipl iers are represented as deviat ions from the

control so lut ions, which were so adjusted as to trace actual

values in the in-sample period of 1977-81. Mult ipl iers were

calculated by applying shocks which were assumed ( in Appendix 1)

to represent economic pol ic ies actual ly undertaken in 1980-83

to the control so lut ions. These mult ipl iers are

interpreted as the ef fects o f actual pol ic ies and expressed

in percent or in terms of absolute values . Figures 1-10 in

the text were drawn by deducting such pol icy e f fects from

actual values of 1980-83.

(2) In calculat ing pol icy ef fects , monetary pol icy s imula-

t ion was used f irst and then s imulat ion of the whole pol icy-

mix was run. The di f ference between the two s imulat ions was

taken as the ef fects o f f iscal pol icy , though the model is

-30-

not perfect ly l inear . However , as the model maintains almost

total l inearit ies in the neighborhood o f the control so lut ion,

there are only minor discrepancies in the results , i f the

order o f pol icy s imulat ion is a ltered. This method of

calculat ion was appl ied to both the U.S. and Japan.

(3) Of the World Economic Model , only the Japanese , U.S.

and world trade l inkage models ( inc luding the regional model )

were used, whi le seven other countries (West Germany, France,

U.K. , I taly , Canada, Austral ia and South Korea) were treated

as exogenous.

(4) Because the models for the 7 countries apart from the

U.S. and Japan were treated exogenously , exchange rates

other than the yen-dol lar were also treated as exogeneous.

As such, the ef fect ive dol lar exchange rate ( the weighted

average o f dol lar rates in 10 currencies) was determined

through a " f lex" method in such a way that the U.S. overal l

balance of payments was balanced for each quarter .

(5 ) As the seven countries other than the U.S. and Japan

were treated exogenously , no considerat ion was given to 1)

the def lat ionary ef fect o f high interest rate pol ic ies which

-31-

European countries might be forced to adopt to combat inf la-

t ion imported through the appreciat ion of the dol lar ; 2) the

ef fects o f higher exports from various countries as a result

o f the weakening o f their currencies against the dol lar ; 3)

the ef fect o f the decl ine of the U.S. business c l imate on

other countries ' export demand. These factors can be taken

into considerat ion only when the EPA world econometric model

is fu l ly l inked up, a task which is expected to be achieved

by February 1984.

-32-

(Bi l l ions of dol lars )

App. Fig . 1-1. U.S. High-Powered Money

( Increase over the corresponding period a year ear l ier ; in percent)

App. Fig . 1-2. U.S. High-Powered Money

1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 79 80 81 82 83

1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 78 79 80 81 82 83

12 .5

10 .0

7 .5

5 .0

2 .5

195.0

180.0

165.0

150.0

135.0

-33-

(Percent)

App. Fig . 2 . U.S. Of f ic ial Discount Rate

1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 79 80 81 82 83

20 .0

16 .0

12 .0

8 .0

4 .0

![SHIFTING TRADE WINDS: U.S. BILATERALISM & ASIA-PACIFIC ... · U.S. withdrawal from the TPP was the start of a more inward-looking U.S. trade policy, [Asia - Pacific economies] picked](https://img.pdfslide.net/doc/110x75/5f96a63de0efad0e205b0ad3/shifting-trade-winds-us-bilateralism-asia-pacific-us-withdrawal-from.jpg)