Embed Size (px)

Citation preview

12 22 March 2018

The Indonesian Tourism Industry: A Bright Future and Opportunities for Australia Jarryd de Haan Research Analyst Indian Ocean Research Programme

Summary

Tourism in Indonesia has more than doubled over the past decade, with some media reports

claiming that 2017 saw over fifteen million tourists visit the archipelago state. The tourism

industry has flourished and become a major driver of the economy and a central feature of

Key Points

The Indonesian tourism industry is a major economic driver and will

continue to be fuelled by the surge of inbound tourists from China.

The lack of tourism infrastructure and the funds needed to remedy it will

be a major challenge for Indonesia. It is a problem that could hamper the

goal of attracting twenty million tourists in 2019.

The growing “halal tourism” market holds significant potential for

Indonesia.

While Australian tourists play a key role in the Indonesian tourism

industry, the same cannot be said for the number of Indonesian tourists

coming to Australia.

Adjusting Australian visa requirements for Indonesian tourists to better

match those of other South-East Asian countries could help to encourage

a larger Indonesian presence in the Australian tourism industry.

Page 2 of 10

the government’s economic growth strategy. To facilitate further growth, the Indonesian

Government is hoping to replicate the success of Bali as a tourist destination in a number of

other locations spread across Indonesia.

Analysis

Overview and Future Obstacles

The tourism industry is a major economic driver for Indonesia. In 2016, foreign exchange

earnings from tourism totalled $16.3 billion. When indirect and induced incomes from travel

and tourism are included (such as investment spending and spending by employees), that

figure increases to $72.4 billion, or approximately 6.2 per cent of GDP in 2016. This level

ranks Indonesia’s tourism industry as the twenty-second largest in the world, according to

the World Travel & Tourism Council. It is larger than the average tourism industry in South-

East Asia, but smaller than those of Australia, Thailand and the Philippines.1 Strong growth is

expected for the Indonesian industry, with indirect and induced incomes predicted to reach

$141.3 billion annually by 2027, according to the World Travel & Tourism Council report.

The Indonesian Government, however, may be too optimistic in its growth projections. In

2016, Tourism Minister Arief Yahya claimed that he wishes to double the number of

international visitors coming to Indonesia to total over twenty million by 2019. Yahya has

made similar ambitious claims before. In 2014, he told Reuters that he wished to double the

number of Chinese visitors by 2016, but, in reality, the number grew by only 45.6%; although

that is still an impressive figure.

1 ‘Travel and Tourism: Economic Impact 2017 Indonesia’, World Travel & Tourism Council, 2017, p. 8.

Page 3 of 10

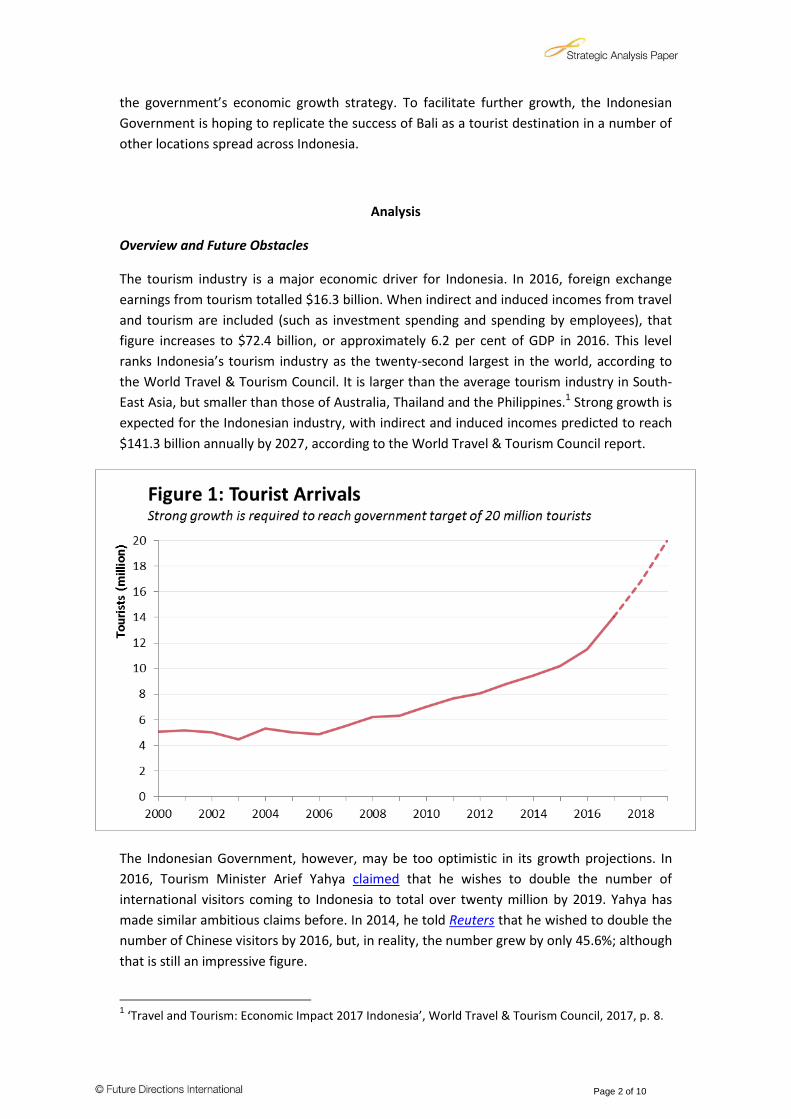

His most recent claim also appears too ambitious. Given that 2017 saw 14 million foreign

arrivals, the minimum growth rate required to reach 20 million tourists by 2019 is 19.4% per

annum. As seen in Figure 1, that is a difficult target, given that the growth rate for foreign

arrivals over the past five years has averaged 11.9%. Consistent growth of around 20 per

cent for three years straight would be unprecedented in Indonesian history and is a rare

occurrence for other tourism industries throughout South-East Asia. So, while not

impossible, achieving such a high target does seem unlikely.

There are also obstacles facing Indonesia’s tourism industry, namely, poor infrastructure and

the lack of investment required to fund the necessary infrastructure projects. From 2015 to

2019, the funds required to meet Indonesia’s overall infrastructure needs amount to

approximately $450 to $520 billion. Looking at projected government spending in contrast

to investment and other contributions, it is likely that the government will fall short of the

required funds for infrastructure by at least $120 billion.2 To fill that funding gap, the

Indonesian Government has made a number of bilateral agreements with countries such as

China and Japan and sought loans from the World Bank and the Asia Infrastructure

Investment Bank. According to PricewaterhouseCoopers, however, many of those

agreements are fraught with challenges, due to being politically, rather than commercially,

driven. As a result, funds tend to be slowly dispensed and often not fully utilised.3

That has left tourist-related infrastructure in a poor position. According to the World

Economic Forum (WEF) in its 2017 Travel and Tourism Competitiveness Report, tourist

service infrastructure was the worst performing area in its analysis of the Indonesian tourism

industry.4 With a score of 3.1 out of seven, Indonesia’s tourist service infrastructure is worse

than that of Kenya and only slightly better than Venezuela. Ground and port transport

infrastructure is also ranked poorly in the report. While the Indonesian Government has

recognised the poor state of infrastructure, in remedying that problem it must consider the

potential environmental impact of developing new hotels, roads or airports. That must be

done not only for the sake of general environmental concerns, such as native wildlife, but

also to preserve the forests and beaches as tourist attractions. In the WEF Report, Indonesia

ranked poorly in environmental sustainability, but highly in natural resources. Maintaining

those natural resources should be a vital component of Indonesia’s tourism industry.

2 Smith, J., Rizal, S., Wiryawan, A., Boothman, T. and Harrison G., ‘Indonesia Infrastructure: Stable

Foundations for Growth’, PwC Indonesia, 2016, pp. 7-10. 3 Ibid., p. 11.

4 ‘The Travel & Tourism Competitiveness Report 2017: Paving the way for a more Sustainable and

Inclusive Future’, Insight Report, World Economic Forum, p. 186.

Page 4 of 10

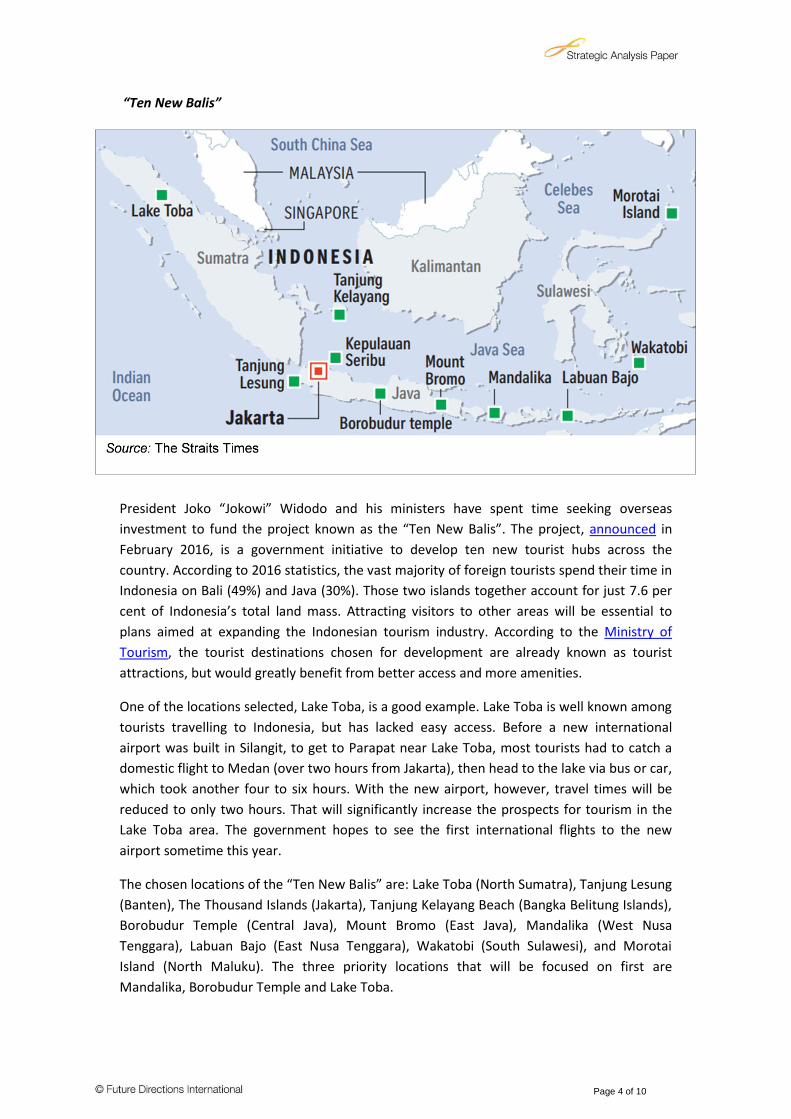

“Ten New Balis”

President Joko “Jokowi” Widodo and his ministers have spent time seeking overseas

investment to fund the project known as the “Ten New Balis”. The project, announced in

February 2016, is a government initiative to develop ten new tourist hubs across the

country. According to 2016 statistics, the vast majority of foreign tourists spend their time in

Indonesia on Bali (49%) and Java (30%). Those two islands together account for just 7.6 per

cent of Indonesia’s total land mass. Attracting visitors to other areas will be essential to

plans aimed at expanding the Indonesian tourism industry. According to the Ministry of

Tourism, the tourist destinations chosen for development are already known as tourist

attractions, but would greatly benefit from better access and more amenities.

One of the locations selected, Lake Toba, is a good example. Lake Toba is well known among

tourists travelling to Indonesia, but has lacked easy access. Before a new international

airport was built in Silangit, to get to Parapat near Lake Toba, most tourists had to catch a

domestic flight to Medan (over two hours from Jakarta), then head to the lake via bus or car,

which took another four to six hours. With the new airport, however, travel times will be

reduced to only two hours. That will significantly increase the prospects for tourism in the

Lake Toba area. The government hopes to see the first international flights to the new

airport sometime this year.

The chosen locations of the “Ten New Balis” are: Lake Toba (North Sumatra), Tanjung Lesung

(Banten), The Thousand Islands (Jakarta), Tanjung Kelayang Beach (Bangka Belitung Islands),

Borobudur Temple (Central Java), Mount Bromo (East Java), Mandalika (West Nusa

Tenggara), Labuan Bajo (East Nusa Tenggara), Wakatobi (South Sulawesi), and Morotai

Island (North Maluku). The three priority locations that will be focused on first are

Mandalika, Borobudur Temple and Lake Toba.

Page 5 of 10

In developing those locations, the government hopes to expand tourism as an economic

behemoth, without devaluing existing tourist destinations. It is highly unlikely that Indonesia

could accommodate twenty million tourists in 2019 without diverting some of those tourists

to locations other than Bali. That would have the added benefit of creating local jobs in the

new tourist areas.

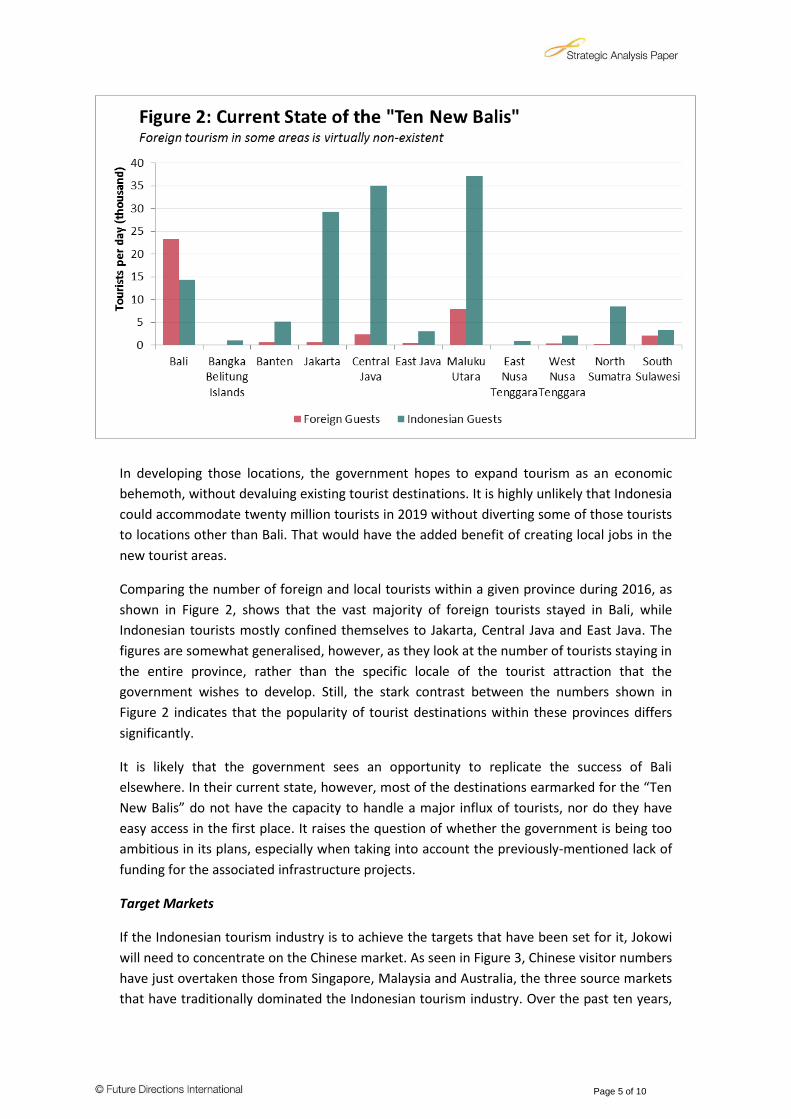

Comparing the number of foreign and local tourists within a given province during 2016, as

shown in Figure 2, shows that the vast majority of foreign tourists stayed in Bali, while

Indonesian tourists mostly confined themselves to Jakarta, Central Java and East Java. The

figures are somewhat generalised, however, as they look at the number of tourists staying in

the entire province, rather than the specific locale of the tourist attraction that the

government wishes to develop. Still, the stark contrast between the numbers shown in

Figure 2 indicates that the popularity of tourist destinations within these provinces differs

significantly.

It is likely that the government sees an opportunity to replicate the success of Bali

elsewhere. In their current state, however, most of the destinations earmarked for the “Ten

New Balis” do not have the capacity to handle a major influx of tourists, nor do they have

easy access in the first place. It raises the question of whether the government is being too

ambitious in its plans, especially when taking into account the previously-mentioned lack of

funding for the associated infrastructure projects.

Target Markets

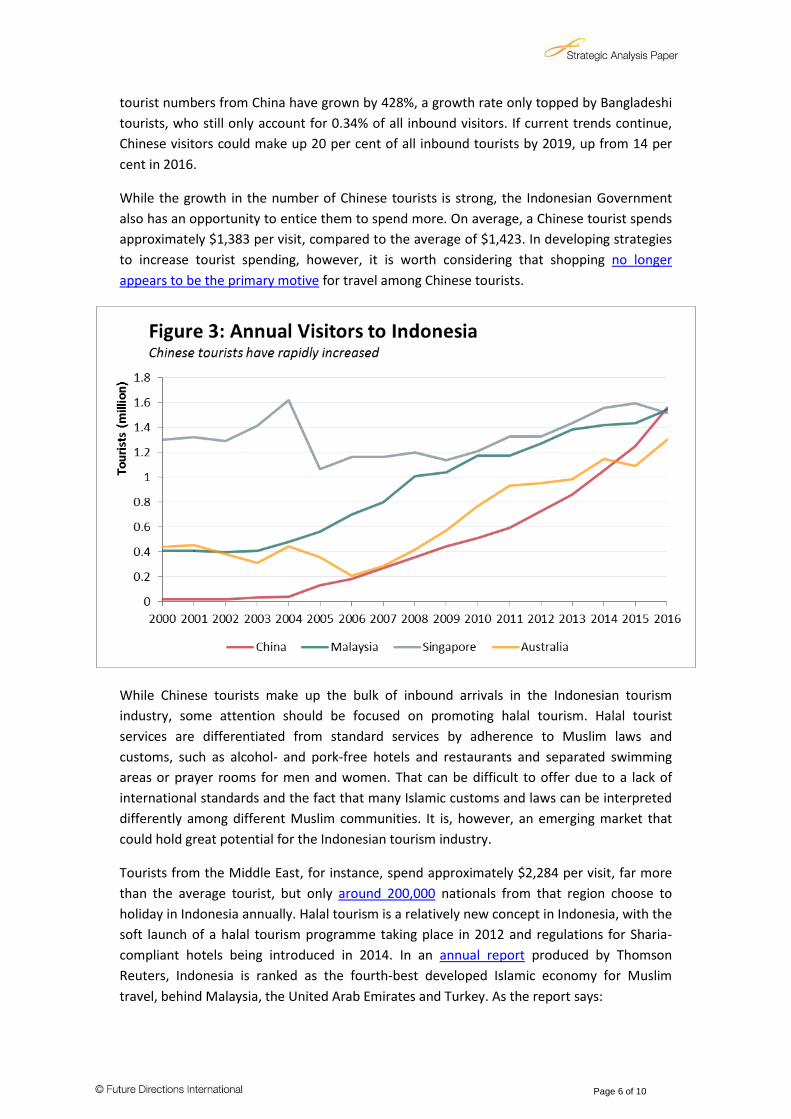

If the Indonesian tourism industry is to achieve the targets that have been set for it, Jokowi

will need to concentrate on the Chinese market. As seen in Figure 3, Chinese visitor numbers

have just overtaken those from Singapore, Malaysia and Australia, the three source markets

that have traditionally dominated the Indonesian tourism industry. Over the past ten years,

Page 6 of 10

tourist numbers from China have grown by 428%, a growth rate only topped by Bangladeshi

tourists, who still only account for 0.34% of all inbound visitors. If current trends continue,

Chinese visitors could make up 20 per cent of all inbound tourists by 2019, up from 14 per

cent in 2016.

While the growth in the number of Chinese tourists is strong, the Indonesian Government

also has an opportunity to entice them to spend more. On average, a Chinese tourist spends

approximately $1,383 per visit, compared to the average of $1,423. In developing strategies

to increase tourist spending, however, it is worth considering that shopping no longer

appears to be the primary motive for travel among Chinese tourists.

While Chinese tourists make up the bulk of inbound arrivals in the Indonesian tourism

industry, some attention should be focused on promoting halal tourism. Halal tourist

services are differentiated from standard services by adherence to Muslim laws and

customs, such as alcohol- and pork-free hotels and restaurants and separated swimming

areas or prayer rooms for men and women. That can be difficult to offer due to a lack of

international standards and the fact that many Islamic customs and laws can be interpreted

differently among different Muslim communities. It is, however, an emerging market that

could hold great potential for the Indonesian tourism industry.

Tourists from the Middle East, for instance, spend approximately $2,284 per visit, far more

than the average tourist, but only around 200,000 nationals from that region choose to

holiday in Indonesia annually. Halal tourism is a relatively new concept in Indonesia, with the

soft launch of a halal tourism programme taking place in 2012 and regulations for Sharia-

compliant hotels being introduced in 2014. In an annual report produced by Thomson

Reuters, Indonesia is ranked as the fourth-best developed Islamic economy for Muslim

travel, behind Malaysia, the United Arab Emirates and Turkey. As the report says:

Page 7 of 10

Indonesia moves into the top ten straight to fourth place, realising its

potential as a top destination for Muslim [travellers], aided by

substantial efforts to develop Halal Tourism in the country, reflected in

a high ecosystem score, as well as a substantial increase in media

discussion on halal tourism.5

Promoting halal tourism should not be confined to Middle Eastern countries alone. South

Asian countries, such as India, Pakistan and Bangladesh, are all in relatively close proximity

to Indonesia. In 2016, approximately 500,000 tourists from the South Asian region visited

Indonesia.

Given the popularity of Bali for Australian holidaymakers, Australia may be seen more as a

solid, reliable market, rather than a priority for the Indonesian tourism industry. Even so, it

still holds great significance in the overall bilateral relationship. In a previous Strategic

Analysis Paper, tourism was identified as the most important aspect of the Australia-

Indonesia economic relationship, from the perspective of Jakarta.

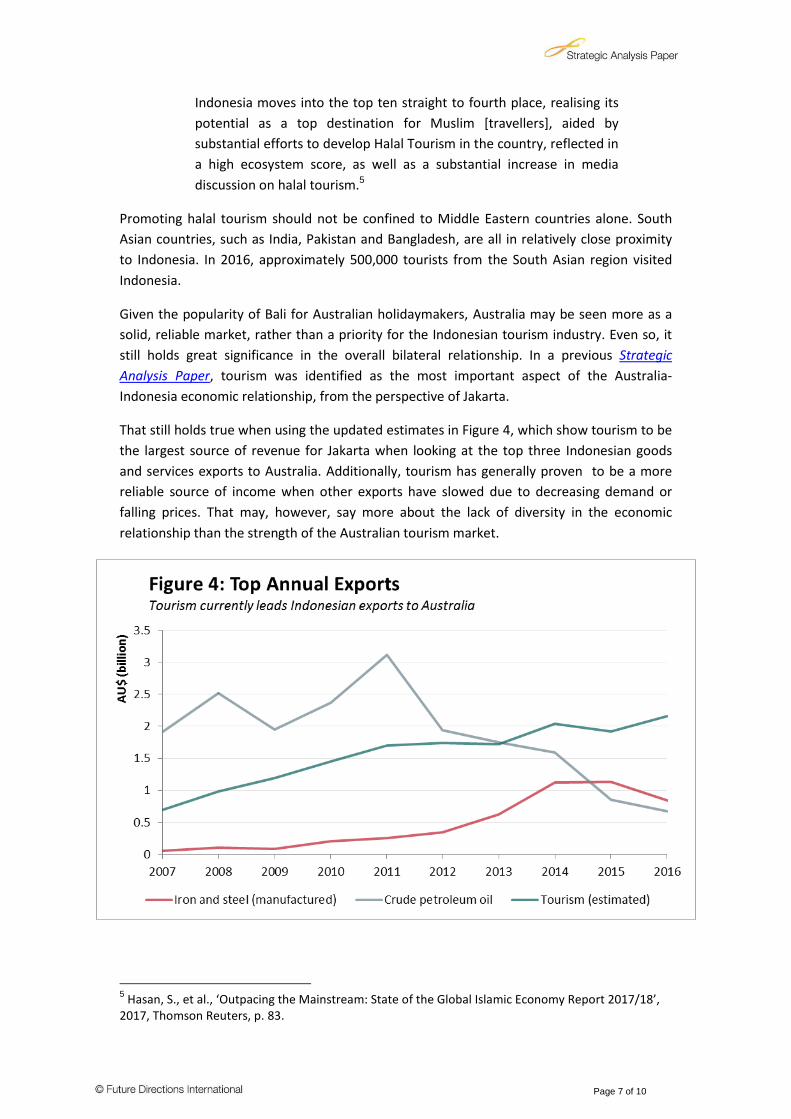

That still holds true when using the updated estimates in Figure 4, which show tourism to be

the largest source of revenue for Jakarta when looking at the top three Indonesian goods

and services exports to Australia. Additionally, tourism has generally proven to be a more

reliable source of income when other exports have slowed due to decreasing demand or

falling prices. That may, however, say more about the lack of diversity in the economic

relationship than the strength of the Australian tourism market.

5 Hasan, S., et al., ‘Outpacing the Mainstream: State of the Global Islamic Economy Report 2017/18’,

2017, Thomson Reuters, p. 83.

Page 8 of 10

Indonesian Tourists in Australia

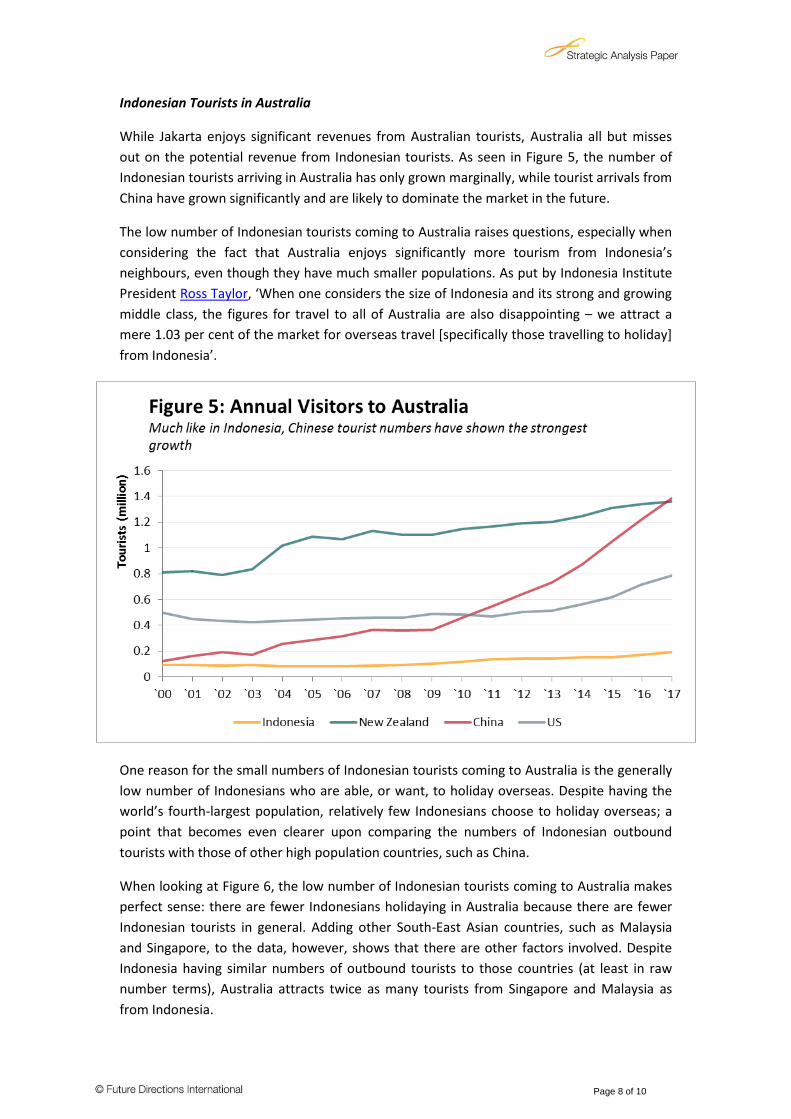

While Jakarta enjoys significant revenues from Australian tourists, Australia all but misses

out on the potential revenue from Indonesian tourists. As seen in Figure 5, the number of

Indonesian tourists arriving in Australia has only grown marginally, while tourist arrivals from

China have grown significantly and are likely to dominate the market in the future.

The low number of Indonesian tourists coming to Australia raises questions, especially when

considering the fact that Australia enjoys significantly more tourism from Indonesia’s

neighbours, even though they have much smaller populations. As put by Indonesia Institute

President Ross Taylor, ‘When one considers the size of Indonesia and its strong and growing

middle class, the figures for travel to all of Australia are also disappointing – we attract a

mere 1.03 per cent of the market for overseas travel [specifically those travelling to holiday]

from Indonesia’.

One reason for the small numbers of Indonesian tourists coming to Australia is the generally

low number of Indonesians who are able, or want, to holiday overseas. Despite having the

world’s fourth-largest population, relatively few Indonesians choose to holiday overseas; a

point that becomes even clearer upon comparing the numbers of Indonesian outbound

tourists with those of other high population countries, such as China.

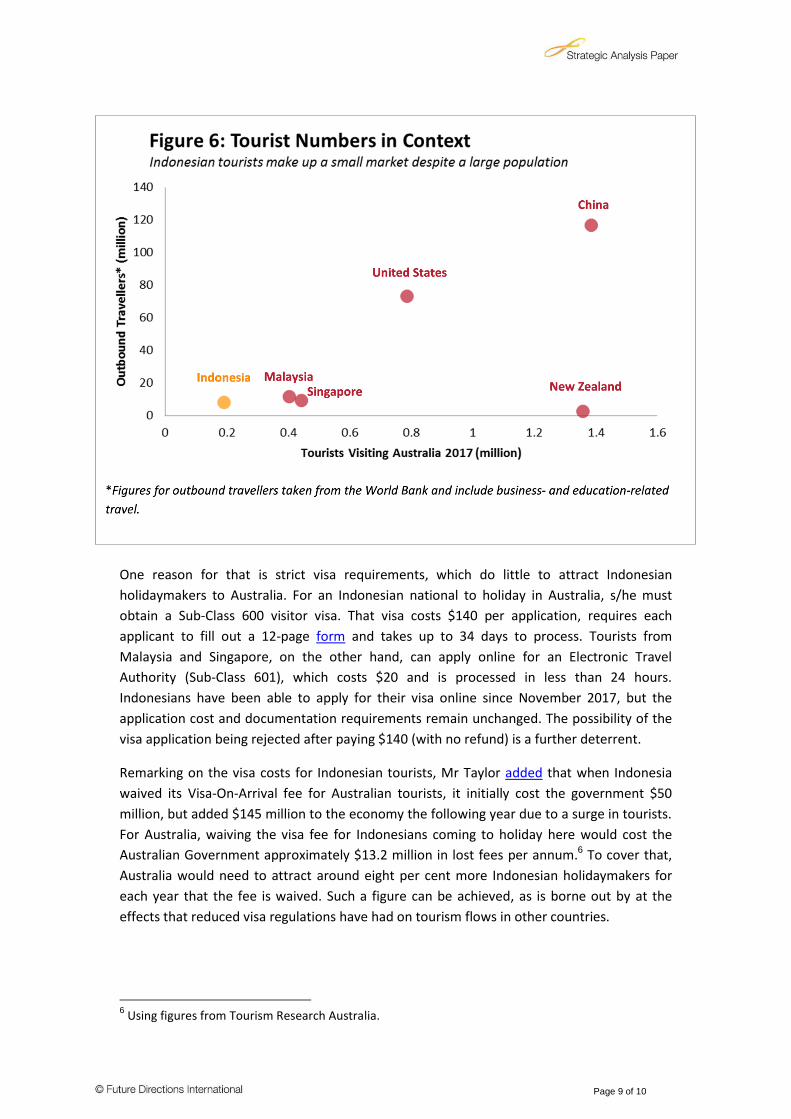

When looking at Figure 6, the low number of Indonesian tourists coming to Australia makes

perfect sense: there are fewer Indonesians holidaying in Australia because there are fewer

Indonesian tourists in general. Adding other South-East Asian countries, such as Malaysia

and Singapore, to the data, however, shows that there are other factors involved. Despite

Indonesia having similar numbers of outbound tourists to those countries (at least in raw

number terms), Australia attracts twice as many tourists from Singapore and Malaysia as

from Indonesia.

Page 9 of 10

One reason for that is strict visa requirements, which do little to attract Indonesian

holidaymakers to Australia. For an Indonesian national to holiday in Australia, s/he must

obtain a Sub-Class 600 visitor visa. That visa costs $140 per application, requires each

applicant to fill out a 12-page form and takes up to 34 days to process. Tourists from

Malaysia and Singapore, on the other hand, can apply online for an Electronic Travel

Authority (Sub-Class 601), which costs $20 and is processed in less than 24 hours.

Indonesians have been able to apply for their visa online since November 2017, but the

application cost and documentation requirements remain unchanged. The possibility of the

visa application being rejected after paying $140 (with no refund) is a further deterrent.

Remarking on the visa costs for Indonesian tourists, Mr Taylor added that when Indonesia

waived its Visa-On-Arrival fee for Australian tourists, it initially cost the government $50

million, but added $145 million to the economy the following year due to a surge in tourists.

For Australia, waiving the visa fee for Indonesians coming to holiday here would cost the

Australian Government approximately $13.2 million in lost fees per annum.6 To cover that,

Australia would need to attract around eight per cent more Indonesian holidaymakers for

each year that the fee is waived. Such a figure can be achieved, as is borne out by at the

effects that reduced visa regulations have had on tourism flows in other countries.

6 Using figures from Tourism Research Australia.

Page 10 of 10

Conclusion

Things are looking up for the Indonesian tourism industry. Although challenges such as the

lack of infrastructure will need to be addressed, they will not necessarily damage the

industry and are more likely to merely restrict its potential. It is unlikely that Indonesia will

see twenty million tourists in 2019, despite the strong growth recorded in 2017.

Considering the Australian tourism industry and the lack of Indonesian tourists, however,

expensive and bureaucratic visa requirements could be directly hindering the number of

arrivals. Unlike the challenges facing Indonesia’s tourism industry, that could be fixed

relatively easily to facilitate significantly more Indonesian visitor arrivals in the longer term.

*****

Any opinions or views expressed in this paper are those of the individual author, unless stated to be those of Future

Directions International.

Published by Future Directions International Pty Ltd.

80 Birdwood Parade, Dalkeith WA 6009, Australia.

Tel: +61 8 9389 9831 Fax: +61 8 9389 8803

Web: www.futuredirections.org.au

![Factors Influencing Motivation of the Tourism Actors in the ......Journal of Indonesian Tourism and Development Studies J. Ind. Tour. Dev. Std., Vol.5, No.3, September 2017 [195] Factors](https://img.pdfslide.net/doc/110x75/60d402d68b0bcc461a457d0e/factors-influencing-motivation-of-the-tourism-actors-in-the-journal-of-indonesian.jpg)