Embed Size (px)

Citation preview

The Mergers & Acquisitions

Review

Law Business Research

third Edition

Editor

Simon Robinson

LawBusinessResearch

The Official Research Partner of the International Bar Association

Strategic research partners of the ABA International section

Th

e Mer

ger

s & A

cq

uisitio

ns R

eview

Edito

rSim

on

Ro

binso

n

LawBusinessResearch

The Mergers & AcquisiTions review

third edition

reproduced with permission from Law Business research Ltd.This article was first published in The Mergers & Acquisitions Review, 3rd Edition

(published in September 2009 – editor Simon Robinson).

For further information please [email protected]

The Mergers & Acquisitions

Reviewthird edition

editor

siMon robinson

LAw business reseArch LTd

PubliShERGideon Roberton

MARkETinG MAnAGERAdam Sargent

EdiToRiAl ASSiSTAnTnick drummond-roe

production editorJonathan cowie

SubEdiToRSJonathan Allen

kathryn SmulandAriana FramptonSarah dookhun

editor-in-chieFCallum Campbell

MAnAGinG diRECToRRichard davey

Published in the united kingdom by law business Research ltd, london

87 lancaster Road, london, W11 1QQ, uk© 2009 law business Research ltd

© Copyright in individual chapters vests with the contributors First published 2007

no photocopying: copyright licences do not apply.The information provided in this publication is general and may not apply in a specific

situation. legal advice should always be sought before taking any legal action based on the information provided. The publishers accept no responsibility for any acts

or omissions contained herein. Although the information provided is accurate as of August 2009, be advised that this is a developing area. Enquiries concerning reproduction should be sent to

law business Research, at the address above.

Enquiries concerning editorial content should be directed to the publisher [email protected]

iSbn 0-9542890-7-2

Printed in Great britain by Encompass Print Solutions, derbyshire

Tel: +44 870 897 3239

i

ACknoWlEdGEMEnTS

The publisher acknowledges and thanks the following law firms for their learned assistance throughout the preparation of this book:

AdvokATFiRMAET hJoRT dA

ÆLeX

AllEnS ARThuR RobinSon

AMARChAnd & MAnGAldAS & SuRESh A ShRoFF & Co

AndERSon Mo Ri & ToMoTSunE

ARiAS, FábREGA & FábREGA

ARiAS & Muñoz

bATlinER WAnGER bATlinER

BeLL GuLLy

bEdEll CRiSTin

bERnoTAS & doMinAS GliMSTEdT

boJoviC dASiC koJoviC ATToRnEyS AT lAW

boWMAn GilFillAn

bREdin PRAT

bRiGARd & uRRuTiA AboGAdoS SA

ChARlES AdAMS RiTChiE & duCkWoRTh

CRAvATh, SWAinE & MooRE llP

diTTMAR & indREniuS

doMAnSki zAkRzEWSki PAlinkA sp k

EliG ATToRnEyS AT lAW

EubEliuS

F CASTElo bRAnCo & ASSoCiAdoS

GlATzovA & Co, v.o.s.

GliMSTEdT And PARTnERS

GliMSTEdT STRAuS & PARTnERS

GoRRiSSEn FEdERSPiEl kiERkEGAARd

hEnGElER MuEllER

kElEMEniS & Co

khAn & ASSoCiATES

ii

kiM & ChAnG

lAWCASTlES

lAW FiRM hAnz EkoviC, RAdAkoviC & PARTnERS

MAkES & PARTnERS lAW FiRM

MAnnhEiMER SWARTlinG AdvokATbyRå

MARvAl, o’FARREll & MAiRAl

MAThESon oRMSby PREnTiCE

MiRo SEniCA And ATToRnEyS, d.o.o.

MonASTyRSky, zyubA, STEPAnov & PARTnERS

Mondini RuSConi STudio lEGAlE

MoREno bAldiviESo ESTudio dE AboGAdoS

nAGy éS TRóCSányi ÜGyvédi iRodA

nAuTAduTilh

oSlER, hoSkin & hARCouRT llP

PAyET, REy, CAuvi AboGAdoS

PEnkov, MARkov & PARTnERS

QuEvEdo & PonCE

RuzickA CSEkES s.r.o.

S hoRoWiTz & Co

SAnTAMARinA y STETA, S.C.

SChEllEnbERG WiTTMER

SChönhERR REChTSAnWälTE GMbh

SlAuGhTER And MAy

STAMFoRd lAW CoRPoRATion

SullivAn & CRoMWEll llP

ToRRES, PlAz & ARAuJo

TuCA zbâRCEA & ASoCiA tii

uRÍA MEnéndEz

vASil kiSil & PARTnERS

vEiRAno AdvoGAdoS

WildGEn, PARTnERS in lAW

WinklER PARTnERS

ACknoWlEdGEMEnTS

v

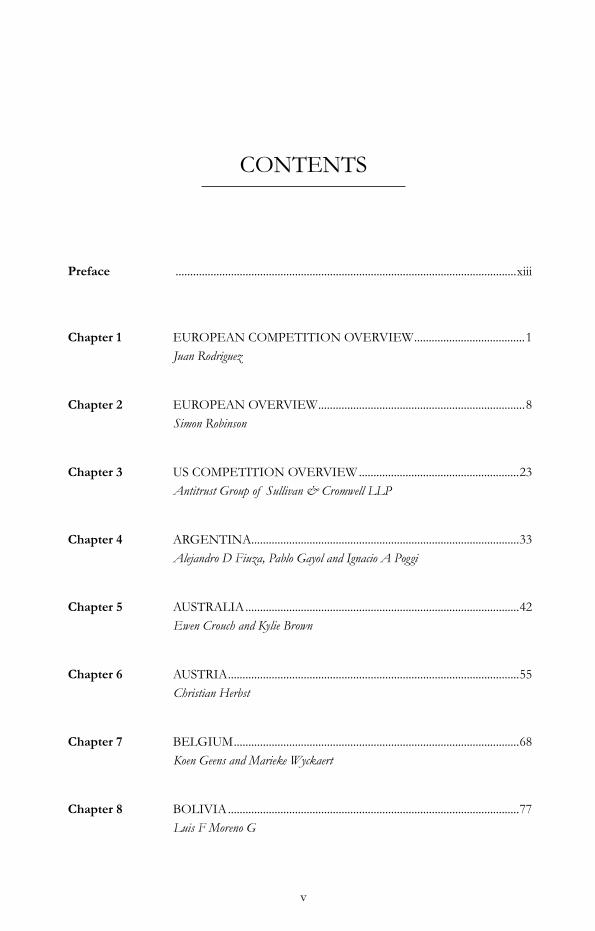

ConTEnTS

Preface .....................................................................................................................xiii

Chapter 1 EuRoPEAn CoMPETiTion ovERviEW ......................................1Juan Rodriguez

Chapter 2 EuRoPEAn ovERviEW .......................................................................8Simon Robinson

Chapter 3 uS CoMPETiTion ovERviEW .......................................................23Antitrust Group of Sullivan & Cromwell LLP

Chapter 4 ARGEnTinA............................................................................................33Alejandro D Fiuza, Pablo Gayol and Ignacio A Poggi

Chapter 5 AuSTRAliA ..............................................................................................42Ewen Crouch and Kylie Brown

Chapter 6 AuSTRiA ....................................................................................................55Christian Herbst

Chapter 7 bElGiuM ..................................................................................................68Koen Geens and Marieke Wyckaert

Chapter 8 boliviA ....................................................................................................77Luis F Moreno G

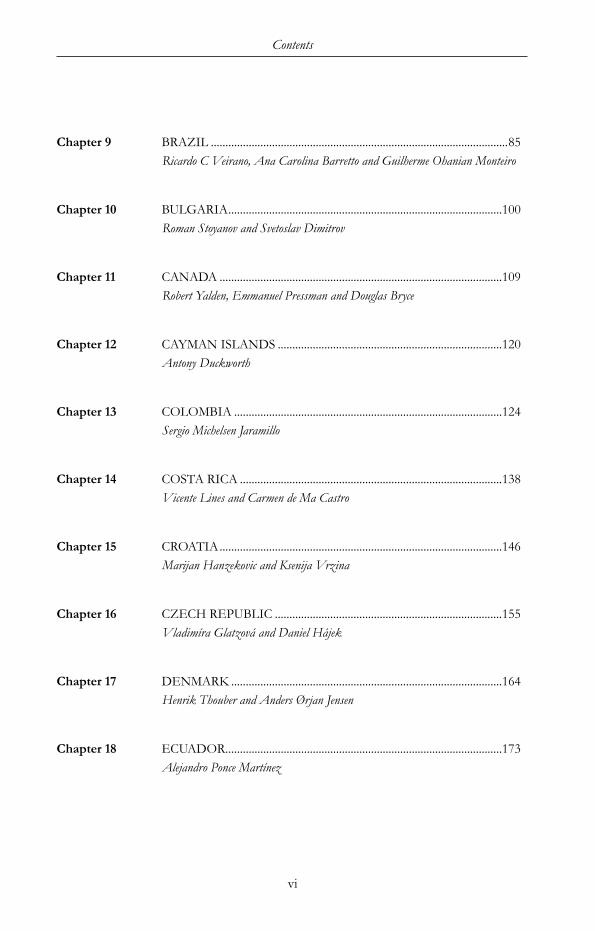

Contents

vi

Chapter 9 bRAzil ......................................................................................................85Ricardo C Veirano, Ana Carolina Barretto and Guilherme Ohanian Monteiro

Chapter 10 bulGARiA ..............................................................................................100Roman Stoyanov and Svetoslav Dimitrov

Chapter 11 CAnAdA .................................................................................................109Robert Yalden, Emmanuel Pressman and Douglas Bryce

Chapter 12 CAyMAn iSlAndS .............................................................................120Antony Duckworth

Chapter 13 ColoMbiA ............................................................................................124Sergio Michelsen Jaramillo

Chapter 14 CoSTA RiCA ..........................................................................................138Vicente Lines and Carmen de Ma Castro

Chapter 15 CRoATiA .................................................................................................146Marijan Hanzekovic and Ksenija Vrzina

Chapter 16 CzECh REPublic ..............................................................................155Vladimíra Glatzová and Daniel Hajek

Chapter 17 dEnMARk .............................................................................................164Henrik Thouber and Anders Ørjan Jensen

Chapter 18 ECuAdor ...............................................................................................173Alejandro Ponce Martínez

Contents

vii

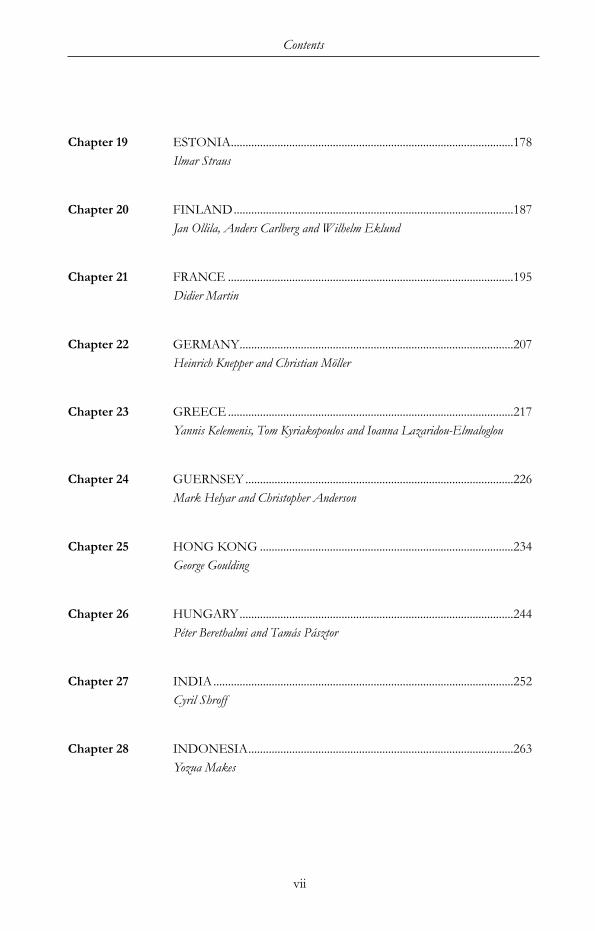

Chapter 19 ESToniA .................................................................................................178Ilmar Straus

Chapter 20 FinlAnd ................................................................................................187Jan Ollila, Anders Carlberg and Wilhelm Eklund

Chapter 21 FRAnCe ..................................................................................................195Didier Martin

Chapter 22 GERMAny ..............................................................................................207Heinrich Knepper and Christian Möller

Chapter 23 Greece ..................................................................................................217Yannis Kelemenis, Tom Kyriakopoulos and Ioanna Lazaridou-Elmaloglou

Chapter 24 GuERnSEy ............................................................................................226Mark Helyar and Christopher Anderson

Chapter 25 honG konG .......................................................................................234George Goulding

Chapter 26 hunGARy ..............................................................................................244Péter Berethalmi and Tamás Pásztor

Chapter 27 indiA .......................................................................................................252Cyril Shroff

Chapter 28 indonESiA ...........................................................................................263Yozua Makes

Contents

viii

Chapter 29 iRElAnd ................................................................................................273Patrick Spicer

Chapter 30 iSRAEL .....................................................................................................283Clifford Davis and Keith Shaw

Chapter 31 iTAly........................................................................................................291Luca Tiberi and Giovanni Stucchi

Chapter 32 JAPAn .......................................................................................................304Hiroki Kodate and Risa Fukuda

Chapter 33 koREA .....................................................................................................314Jong Koo Park, Michael Yu and Yun Goo Kwon

Chapter 34 lATviA ....................................................................................................327Maris Butans

Chapter 35 liEChTEnSTEin ................................................................................334Martin Batliner and Brigitte Vogt

Chapter 36 liThuAniA ............................................................................................343Paulius Gruodis

Chapter 37 luxEMbouRG .....................................................................................351François Brouxel and Sufian Bataineh

Chapter 38 MExiCo ..................................................................................................361Alejandro Luna Arena and Héctor A Garza Cervera

Contents

ix

Chapter 39 nEThERlAndS ...................................................................................374Willem Calkoen

Chapter 40 nEW zEAlAnd ...................................................................................394Glenn Joblin

Chapter 41 niGeriA .................................................................................................406L Fubara Anga

Chapter 42 noRWAy .................................................................................................412Jørn A Uggerud and Elin Rostveit

Chapter 43 PAkiSTAn ...............................................................................................423Mansoor Hassan Khan

Chapter 44 PAnAMA ..................................................................................................432Eduardo de Alba and Julianne Canavaggio

Chapter 45 peru .........................................................................................................438José Antonio Payet, Carlos A Patrón and Susan Castillo

Chapter 46 PolAnd..................................................................................................449Bartosz Marcinkowski and Krzysztof A Zakrzewski

Chapter 47 PoRTuGAL ............................................................................................459Rodrigo Almeida Dias

Chapter 48 RoMAniA ...............................................................................................469Stefan Damian

Contents

x

Chapter 49 RuSSiA .....................................................................................................479Alexander Zyuba, Alena Shubina and Pavel Popov

Chapter 50 SERbiA .....................................................................................................488Tijana Kojovic and Mirjana Mladenovic

Chapter 51 SinGAPoRe ..........................................................................................493Lee Suet-Fern and Elizabeth Kong Sau-Wai

Chapter 52 SlovAkiA ..............................................................................................505Jana Pagácová

Chapter 53 SlovEniA ..............................................................................................517Melita Trop and Uroš Podobnik

Chapter 54 SouTh AFRiCA ....................................................................................527Ezra Davids and Rudolph du Plessis

Chapter 55 SPAin ........................................................................................................535Christian Hoedl and Javier Ruiz-Cámara

Chapter 56 SWEdEn .................................................................................................546Biörn Riese, Eva Hägg and Anna Lundgren

Chapter 57 SWiTzERlAnd ....................................................................................556Lorenzo Olgiati, Martin Weber and Jean Jacques Ah Choon

Chapter 58 TAiWAn ...................................................................................................568Steven J Hanley

Contents

xi

Chapter 59 TAnzAniA .............................................................................................578Ngassa Dindi

Chapter 60 TuRkEy ..................................................................................................590Tunc Lokmanhekim and Berna Asik

Chapter 61 ukRAine ................................................................................................597Denis Lysenko and Anna Babych

Chapter 62 uniTEd kinGdoM ...........................................................................610Simon Robinson

Chapter 63 uniTEd STATES ..................................................................................634Richard Hall and Mark Greene

Chapter 64 vEnEzuElA .........................................................................................649 Guillermo de la Rosa, Juan D Alfonzo, Luis G Monteverde, Pedro Uriola, Nelson Borjas and Ana C González

Appendix 1 AbouT ThE AuThoRS ....................................................................661

Appendix 2 ConTRibuTinG lAW FiRMS’ ConTACT dETAilS ..............705

xiii

The past year has seen the financial crisis continue to escalate. Financial markets have witnessed a number of events that have had global effects, from the collapse of Lehman Brothers in September 2008, to Iceland’s banking crisis and the nationalisation of various financial institutions by several governments. The consensus is that the decision not to rescue Lehman was a mistake, although, to date, this appears to be an isolated – if serious – error by the authorities in response to the banking sector crisis. Other responses to these turbulent market conditions include the decision to reduce interest rates to historically unprecedented levels and massive fiscal stimulus in many countries. More controversially, several monetary authorities have implemented a ‘quantitative easing’ policy. Taken together, these efforts seem, at the moment anyway, to have averted a full-scale depression, but this has clearly been achieved at the price of huge public-sector deficits and substantial debt burdens for future generations.

The current debate centres around whether the next stage will be a continuing crisis, a return to ‘normality’ or, as seems more likely, a slow and anaemic recovery. In any case, many observers predict significantly higher levels of inflation than seen in recent years. Although some tentatively predict that a recovery from the financial crisis is on the horizon, the topic remains one of ferocious debate.

Some questioned whether the banking crisis would seriously affect the wider economy. The last year has proved beyond doubt that those who predicted a wider financial crisis were correct. The crisis in the real economy has much further to run and a significant increase in unemployment, particularly in Europe, regrettably seems inevitable.

M&A activity has reflected this crisis. Lending remains very constrained and the most significant activity has been in the financial sector, although property companies are also severely stressed. The less welcome development over the past year or so has been the steady stream of distressed corporate rescues, some by takeover. More optimistically, many are now commenting that, for those with cash, there are bargains to be had.

From the lawyers’ perspective, the next stages are likely to be of great interest as the authorities take steps to rebuild confidence in financial institutions. The regulatory architecture will change significantly, although the final form is not yet obvious.

I again wish to thank all the contributors for their continued support and cooperation – and all the unnamed others who have helped to produce this book, which, given the current economic climate, should hopefully provide interesting reading.

Simon RobinsonSlaughter and MayLondonAugust 2009

prEFAcE

178

i OVERViEWOF2008/2009M&AACTiViTY

M&A activities in Estonia in 2008/2009 have faced a slight decrease in comparison with the level of 2007/2008. According to the information published on the website of the Competition Board of Estonia, 21 permissions for concentrations were issued in the second half of 2008 and in the first half of 2009. This is 30 per cent less than during 2007/2008.

M&A activity in 2008/2009 was heavily affected by the global financial crisis and by the following economic crisis. Due to the liberal and open Estonian economy, the first signs of economic slowdown in Estonia occurred in autumn 2008, mainly in the real estate sector. The difficulties of financing deals that started with the real estate sector spread rapidly to other fields of the economy, which has caused the discontinuation of acquisition activities in the first half of 2009. However, the activity in the field of mergers has been more lively, especially among small and midsize companies.

Even though the number of permissions granted for concentrations in 2008/2009 is not significantly smaller than during the previous period, the actual situation in M&A activities is less positive than the numbers indicate. There have been very few major M&A transactions in 2008/2009 and the main transactions to which the concentration permissions are given can be regarded as small or medium-sized transactions that have small transaction value and influence to the particular sector. Despite the fact that the supply exceeds the demand in the market of businesses for sale, the prices of the companies to which new owners are looking are still higher than what possible investors are willing to pay.

The main factors influencing existing M&A activities are the need to engage extra capital, expand market share and specialisation. The difficult financial situation has given many better-capitalised companies a chance to acquire their competitors and expand

* Ilmar Straus is a partner at Glimstedt Straus & Partners.

Chapter19

EsToniAIlmar Straus*

Estonia

179

their business activities. However, the decrease of industrial production by 33 per cent during recent months shows that many companies in Estonia would rather struggle for survival than make plans for any M&A activities, even though a merger could be the chance for many to survive the difficult times.

ii GENERALiNTRODUCTiONTOTHEM&ALEGiSLATiVEFRAMEWORK

The Commercial Code (entered into force in 1995, latest amendments in 2009) provides the fundamental statutory framework for merges of companies. Along with the Central Register of securities Act (entered into force in 2001, latest amendments in 2009), the Commercial Code sets forth the principal rules for share transfers, imposing notification requirements and terms, defines the competence, rights and duties of company shareholders and governing bodies and deals with the reorganisation, merger and restructuring of companies. It also regulates matters pertaining to statutory capital, shares and funds of companies.

There is no special legislative framework for shareholder agreements either in the Commercial Code or in the Law of obligations Act (entered into force in 2002, latest amendments in 2009). Therefore, the provisions of the General Part of the Civil Code Act (entered into force in 2002, latest amendments in 2009) and the general part of the Law of obligations Act, as well as principles of good faith and reasonability, apply.

The Law of obligations Act regulates the purchase and sale of corporate entities. The Republic of Estonia Employment Contracts Act (entered into force in 1992, new regulation in force as of 1 July 2009) also applies to the transfer of an enterprise or its independent part from one person to another.

Merger regulation is set forth in the Competition Act (entered into force 2001, latest amendments in 2008). The Estonian Competition Board exercises state supervision over the implementation of the Competition Act. A merger is subject to review by the Estonian Competition Board if, during the previous financial year, the turnover of the parties to the concentration in Estonia exceeded 100 million kroonis and if the turnover of each of at least two parties to the concentration in Estonia exceeded 30 million krooni, except for the concentrations inside a group. The Competition Board shall not exercise control over the implementation of the provisions regarding mergers, which are under the direct supervision of the European Commission according to the EC Merger Regulation (Council Regulation (EC) no. 139/2004 of 20 January 2004 on the control of concentrations between undertakings).

The provisions regarding the public offer of securities and takeover bids exercised to acquire voting rights in public limited companies that are registered in Estonia and of which all or a certain type of shares are listed on an Estonian exchange or traded on an Estonian market, are set forth in the securities Market Act (entered into force in 2004, latest amendments in 2009). Rules for takeover bids are further specified by Regulation no. 71 of the Minister of Finance of 28 May 2002 (amended in 2008).

The Competition Act and the securities Market Act also set forth administrative liability for misdemeanours that occur during M&A deals (e.g., submitting false information with the Competition Board, not notifying the Competition Board of the concentration,

Estonia

180

breaching the conditions of the concentration authorisation). Criminal liability for offences relating to competition (e.g., abuse of a dominant position, agreements, decisions and concerted practices prejudicing free competition, failure to notify a concentration, enforcement of a concentration without a permission to concentrate and concentration that damages competition), for offences relating to securities circulation (e.g., abuse of internal information) and for offences relating to money laundering is set forth in the Penal Code (entered into force 2002, latest amendments in 2009).

The Estonian legislator has not adopted any legislative measures to deal with the financial crisis. However, the Estonian General Part of the Civil Code Act was amended in such a way that the application of the regulation under which the transaction is invalid due to its contradiction of good morals or public order is significantly widened. The transaction is void if the party to the transaction knew or should have known during the time the transaction took place that the other party made the transaction, inter alia, due to its extraordinary needs and the transaction was made under adverse conditions to the other party. This principle is applicable to all transactions. However, there is no settled court practice with regard to this amendment and thus it is not clear whether it could also be applicable to transactions that are made during the financial crisis under the extraordinary needs of one of the parties and adverse conditions to the latter.

iii DEVELOPMENTSiNCORPORATEANDTAKEOVERREGULATiONSANDTHEiRiMPACT

At the beginning of 2009, the regulation on conditional increase of the share capital in the Estonian Commercial Code was amended. The purpose of the amendment is to simplify the procedures under which the new shares can be issued for those companies that have listed their shares on the stock exchange or who are planning to list their shares on the stock exchange. The purpose of the new regulation is that the issued shares shall be transferred to the new owner and trading with the new shares is permitted as soon as they are paid for. The previous regulation was stricter with regard to the transfer of the new shares and thus the period between payment for the shares and granting the new owner a right to trade with these shares was longer. This might have caused a delay in an adequate response to the change in the prices of the shares and eventually damage the property of the new shareholder. The new amendment should guarantee better functioning of the stock exchange.

The amendments to the Estonian securities Market Act specified the regulation of compulsory takeover bids of companies that are listed on the stock exchange. Generally, the regulation provides that if somebody has gained control over the company, it is obliged to make a takeover bid. However, the Financial supervisory Authority has a right to make an exception from the obligation to make a compulsory takeover bid, if the company in control makes a respective application. Under the amendment to the Estonian Securities Market Act, grounds for such exceptions made by the Financial supervisory Authority are broadened in order to allow such exceptions in more complicated transactions as well as in such alterations or reorganisation of the companies and in cases related to pledges and encumbrances.

Estonia

181

The new Reorganisation Act (in force as of 28 December 2008) has had the most significant influence on the corporate regulation allowing companies facing temporary financial difficulties to protect themselves for a certain time period from the initiation of bankruptcy proceedings against them and transform the claims of the creditor, inter alia extend the terms for the performance of obligations, fulfil financial claims in instalments and reduce the amount of debt. The aim of the Reorganisation Act is to reorganise the companies and give them a new opportunity to carry out their business. However, in practice, many of the started reorganisation proceedings have ended because the company has damaged the interests of its creditors or has violated the obligation to cooperate with the court and reorganisation adviser.

In 2007, the Estonian Ministry of Justice introduced a highly successful expedited procedure for making entries in the Commercial Register, also known as the turbo procedure, which involved the establishment of an E-filing portal for submitting documentation and applications with the Commercial Register via the internet. Persons are identified and transactions confirmed by using an Estonian iD card and a digital signature, which unfortunately grants access to the E-filing portal only to Estonian citizens. All this makes it possible to establish a company within two hours and its aim is to submit different documents and data to the Commercial Register via the internet. In 2009, companies are already entitled to submit their annual reports for 2008 to the Commercial Register via the internet and in 2010, companies are expected to use only the internet for submitting their annual reports. Hence, more and more interactions with the authorities can be performed via the internet and this shall considerably save time and make the managing of companies easier.

iV FOREiGNiNVOLVEMENTiNM&ATRANSACTiONS

According to the data published by the Bank of Estonia, direct foreign investment to Estonia decreased by 5 per cent in 2008 and the decrease is expected to be even bigger in 2009. The official forecast provides that the decrease could be up to 10 per cent. As there are no official statistics on foreign involvement in M&A transactions, these numbers reflect the trend that during the period of 2008/2009, the number of M&A transactions has decreased as has foreign involvement.

However, direct foreign investments amounted to 2.6 billion kroons in the first quarter of 2009, having decreased by nearly a third in comparison with the previous quarter. Despite the global economic recession, direct investments made to Estonia have made up more than 3 per cent of the gross domestic product in the second half of 2008 and first half of 2009, which is a good result as estimated by the Bank of Estonia.

The formation of the aforementioned amount of direct investment to Estonia was mainly driven by the reinvested earnings of credit institutions. Meanwhile, direct investment in real estate, renting and business activities has decreased.

The direct investments made into Estonia mainly came from sweden with some from France and Belgium. The main attraction for swedish investors has so far been the electronics and the timber industries. With regard to the latter the focus of interest has changed from processing timber to owning the forest land and its management.

Estonia

182

Estonian investments were primarily channelled into Latvia but were also channeled to Lithuania and Cyprus.

in addition to the financial crisis, one reason for the decrease of M&A activities and foreign involvement in it is the threat of devaluation of the Estonian national currency. The aim of the current government is to join the Eurozone at the first opportunity. This is regarded as one of the possibilities to boost the economy and it will certainly have a positive influence on M&A activities.

V SiGNiFiCANTTRANSACTiONS,KEYTRENDSANDHOTiNDUSTRiES

i The sale of the Elcoteq production unit to Ericsson

The biggest player in the Estonian electronics industry, a Finnish company, Elcoteq, has decided to sell a large part of its Tallinn production unit to Ericsson, a swedish infirm and currently the world’s largest supplier in telecommunication. The deal was initiated because of Elcoteq’s plan to concentrate the production of electronic components to its biggest plant in Hungary and thus Elcoteq has concluded a €30 million deal with Ericsson. This deal does not mean that Elcoteq, as the largest exporter in Estonia for a long time, leaves the country – it shall keep its presence through a smaller production unit. The sale of Elcoteq’s production unit is planned to be completed during 2009.

ii The purchase of OÜ Põlva Piim by AS Tere

The largest Estonian dairy company, As Tere, acquired at the end of 2008 a smaller dairy company, oÜ Põlva Piim, which was known for its strong trademarks and high quality. The value of the deal was approximately €10 million. The main reasoning behind the deal was As Tere’s plan to improve its position in the Estonian market and its production capacity. As Tere belongs to a group of companies that also includes As Kalev, the largest chocolate factory in Estonia. The purchase of oÜ Põlva Piim was followed by the failed attempt of the owners of As Tere to enter the media business.

iii The sale of the Väo power plant to French energy company Dalkia

in the beginning of 2009 an Estonian company, Us invest As subsidiary norman invest oÜ, sold all of its shares in the holding company of Väo power plant to As Tallinna Küte, which is part of the Dalkia Group, the leading European energy provider. As the result of the transaction, Dalkia gained full ownership of a newly built power plant near Tallinn and guaranteed its stronger presence in Estonia. The price of the deal was never made public, but its magnitude is allegedly approximately €50 million.

iv The sale of AS Väätsa Agro to its pledgee

The low price of milk has caused difficulties for many agricultural companies during the past six months. The biggest of its kind in Estonian, As Väätsa Agro, was hit hardest and the owners were forced to sell the company to Hanseatic Capital, its biggest pledgee. Hanseatic Capital is a mezzanine capital provider which is not active in managing the

Estonia

183

acquired company. The price of the acquisition was not made public. it is likely that Hanseatic Capital will resell As Väätsa Agro as soon as it receives a good offer.

v Baltic common market

The main trend in the Estonian M&A market has remained the same – the investors, both local and foreign, are attracted by the possibility of gaining access to the markets of all three Baltic States by putting through only one deal. It has become quite popular not to acquire a single company that performs business in only Estonia, but to acquire a group of companies and especially the ones that are already active in three or two Baltic states. However, the weakest Baltic economy – Latvia – has discouraged possible investors and focusing in one country instead of the whole region seems to be the trend for 2010/2011. However, in the long run, the Baltic region seems to be inevitably one region in the eyes of possible investors.

Even though at present there is not much M&A activity, the end of 2009 and the beginning of 2010 are expected to be busy times for everybody involved in M&A activities. The number of companies for sale is higher than ever before. The prices of the target companies that still do not meet the price level the investors are willing to offer will hopefully decrease, which will give a good starting point for the transactions.

vi Hot industries

For several years the hottest industry was construction, which received most of the FDi. This is currently the industry in which the economic crisis has hit hardest. As the economic crisis has hit almost all of the economic areas, there are very few sectors that have stayed intact. These are the iT and high-technology sectors, which still experience steady growth and high profitability.

A fine example of an iT technology company is Playtech Estonia, which belongs to the international group of companies Playtech Group, and has become the largest developer of online gambling solutions. in the high-tech field, there are a large number of small companies that are well known for their innovative products. one of these is Modesat Communications, which is the innovation leader in high-capacity and reliable modulator-demodulator DSP cores for wired and wireless broadband solutions.

These companies usually also enjoy support from Enterprise Estonia, which is the largest institution within the national support system for entrepreneurship, providing financial assistance, advice, cooperation opportunities and training for entrepreneurs, research establishments and the public and private sector.

Vi FiNANCiNGM&A:MAiNSOURCESANDDEVELOPMENTS

In addition to the overall slowdown of the economy, M&A activities were also heavily influenced by the financial crisis. For the past eight months, the big scandinavian banks present in Estonia (e.g., swedbank, sEB, Dankse Pank and nordea) have been very reluctant in giving any financial support for M&A activities. As in other countries, the banks themselves faced liquidity problems and went through turbulent times. In addition, one big reason for not giving loans has been the threat of devaluation of the Estonian national currency.

Estonia

184

Together with the scandinavian banks, venture capital firms have also been actively involved in M&A activities. However, currently they face liquidity problems and have mainly pulled back from the field.

Presently, the future is significantly brighter and the financial institutions have money that they could invest into M&A activities. However, their clear message for the future has so far been that the business plan under which any loan could be granted should have much stronger financial figures and each project to which credit is granted will be examined much more thoroughly. In addition, the security requirements imposed by the financial institutions are significantly higher.

Vii EMPLOYMENTLAW

As of 1 July 2009 the new and long-disputed Estonian Employment Contracts Act comes into force. The new law brings employment relations closer to the traditional contractual relations in which parties are equal. This shall make employment relations more dynamic, especially in respect of the rights an employer has. For example, the cost of terminating an employment contract is significantly lower due to the lowered premiums paid by the employer to the employee, which shall make it easier to reorganise business activities. Taking into account the economic downturn, the employer can also temporarily decrease the salary of an employee due to a severe economic situation for three months during a 12-month period. These changes will probably contribute to the popularity of acquiring companies in Estonia.

The new Employment Contract Act also provides that employment agreements shall be considered to be transferred to the new employer upon the transfer of the enterprise or its independent part from one person to another based on any legal ground, provided that the same or similar activities are continued after the transfer. However, the new law establishes higher protection standards for the employees in case of the transfer of an enterprise. namely, the time period when the old and the new employer are equally responsible for the claims of the employees is increased to five years. This puts an extra burden on the former owner of the enterprise.

There are no specific employee-related mandatory obligations set forth in the Estonian takeover rules other than an obligation of the board of the target company to inform the employees of the target of the takeover bid.

Viii TAXLAW

The recent economic downturn has brought the matter of company taxation to the centre of political debate. During 2008 several material amendments to the Estonian tax legislation were made and came into effect as of 1 January 2009.

At the beginning of 2000, Estonia introduced a unique corporate income taxation system according to which Estonian companies pay income tax only when they distribute their profits or when they make payments not related to their business. it is important to understand that the tax liability is merely deferred in Estonia and that distributed profits are tax-exempt at the shareholder level, not at the level of the company distributing profits. The difference from a classical corporate taxation system is only technical

Estonia

185

because the moment of taxation is postponed until the profits are distributed. in order to minimise the possible risk of the Estonian corporate income tax being deemed to be a withholding tax within the meaning of Article 5(1) of the Parent-subsidiary Directive (50/435/ECC), the Estonian Parliament made several amendments to the income Tax Act on March 2008 (e.g., annual taxation period, advance payments, etc.). However, on 26 June 2008, the European Court of Justice delivered its landmark ruling (Burda GmbH, C-284/06) rejecting the European Commission’s argument that a tax levied at the level of the distributing company could have the same effect economically as a withholding tax and therefore should be precluded by the Directive. It became clear that the Estonian tax system is in line with the relevant EU law, and therefore, on november 2008, the Parliament decided to abolish most of the amendments adopted in the spring.

In addition to the abolishment of the previous law, the Parliament made the following important changes applicable as of 1 January 2009.a The equalisation of liquidation proceeds, payments upon share payback and

upon reduction of share capital, in the amount in which they exceed monetary and non-monetary contributions to the equity of the company, with dividends. Until the end of 2008 such payments were treated as capital gains and were tax exemp at the level of the company. From 2009 these payments constitute a part of the company’s taxable base. In order to avoid double taxation, these payments are tax exempt at the level of the recipient. Therefore, all company profits are subject to taxation at the corporate level despite the way they are taken out of the company.

b The threshold of participation exemption is reduced from 15 per cent (2008) to 10 per cent (2009). Thus, if an Estonian parent company (or permanent establishment of a non-resident) distributes dividends that it has received from its subsidiary (in the EU or switzerland and the latter company is a taxable person, or in a third non-low tax country and tax has been paid in the relevant country), the Estonian parent company is not obliged to pay tax, if it meets the holding criteria at the moment of receiving the dividends.

c The withholding taxation on dividend paid to non-residents is fully abolished (irrespective of the holding participation; 15 per cent was required in 2008). Therefore, non-resident portfolio investors will benefit from the amendment.

d Temporary freezing of annual lowering of the tax rates as of 2009. Thus, the profit distributions made by Estonian companies are still subject to 21/79 (corresponding to 21 per cent on the gross amount = distribution + tax) corporate income tax in 2009, 20/80 in 2010, 19/81 in 2011 and 18/82 in 2012. In the light of the constitutional principle of legal certainty, this amendment is highly questionable.

Effective as of 1 July 2009, the standard VAT rate has been increased from 18 per cent to 20 per cent. it is worth mentioning here that the reduced VAT rate (5 per cent) was increased to 9 per cent as of 1 January 2009.

As a rule, VAT shall not be imposed on the supply of securities (shares). Until the end of 2008, the Estonian VAT legislation did not include provisions considering the supply of shares in a real estate company as a supply of immoveable property. However, as of 1 January 2009, the Estonian VAT Act provides that VAT shall be imposed on the

Estonia

186

transfer of shares in an Estonian real estate company that meets the criteria set forth in the VAT Act.

Finally, it should be mentioned that the Estonian Tax and Customs Board started to issue advance tax rulings in 2008. The ruling represents a binding assessment issued by the Estonian tax authorities regarding taxation of a specific transaction or set of transactions completed in the future by a specific taxable person.

iX COMPETiTiONLAW

The last amendment to the Competition Act relevant to M&A dates back to 2006, when the jurisdictional thresholds for the application of the merger control were changed. Under the changed provisions instead of the three previous criteria, two shall be applicable (i.e., merger control is applicable if: during the previous financial year, the aggregate worldwide turnover of the parties to the concentration exceeded 100 million kroons (previously 500 million kroons); and during the previous financial year, aggregate worldwide turnover of each of at least two parties to the concentration exceeded 30 million kroons (previously 100 million kroons)). Therefore, as the aggregated turnover of the parties to the concentration was decreased, more concentration cases are now subject to monitoring from the Competition Board. However, the number of the concentration permissions granted has not significantly risen during the last few years and there has even been a decrease during 2008/2009. This shows that competition issues are not particularly crucial matters in most M&A cases.

X OUTLOOK

The economic downturn in Estonia is expected to last at least for another few years. in light of the hope that the rest of the world’s economy will recover within the next year, Estonia would be a good environment for carrying out M&A activities, especially for foreign investors. There are lots of companies for sale and the prices of those companies are expected to decrease in order to meet the level in which the possible buyers are ready to buy.

It has yet to be seen what the result would be of the attempt of the Estonian government to join the Eurozone, but this aim will probably not be fulfilled within next few years. Therefore the threat of devaluation remains and it is unfortunately one additional factor that keeps possible investors away from the Baltic region, including Estonia.

About the Authors

Ilmar StrauS

Glimstedt Straus & Partners

Mr Ilmar Straus is a founder of the law firm Glimstedt Straus & Partners and currently he is head of the corporate practice group. Ilmar has been a member of the Estonian Bar Association for 10 years. Ilmar has clients from a wide range of business areas, starting from financial institutions and ending with big international pharmaceutical companies. He is well known for his ability to obtain excellent personal contacts with his clients. Ilmar has been recently mentioned as a leading individual in Chambers Global, and The Client’s Guide 2009.

Ilmar obtained a bachelor’s degree from Tartu University (BA, cum laude) and he has also graduated Columbia University Law School (NYC, LLM, graduated in 1998) and he is fluent in Estonian, English, French and Russian.

GlImStedt StrauS & PartnerSRävala pst 5Tallinn 10143Estonia Tel: +372 6 309 170Fax: +372 6 309 [email protected] www.glimstedt.ee