Embed Size (px)

DESCRIPTION

The Oklahoma Stocker Industry. Derrell S. Peel Oklahoma State University. The Beef Industry. Demand Marketing System Production. Cattle and Beef Markets. Demand What gets produced How much gets produced Who gets it. Cattle and Beef Markets. Marketing System - PowerPoint PPT Presentation

Citation preview

The Oklahoma Stocker Industry

Derrell S. PeelDerrell S. Peel

Oklahoma State UniversityOklahoma State University

The Beef Industry

• Demand

• Marketing System

• Production

Cattle and Beef Markets

• Demand– What gets produced– How much gets produced– Who gets it

Cattle and Beef Markets

• Marketing System– Moves products from “Gate to Plate”– Time, Place and Form functions

• Storage (When)• Transportation (Where)• Processing (What Changes)

Cattle and Beef Markets

• Production– How things get produced

• What resources are used

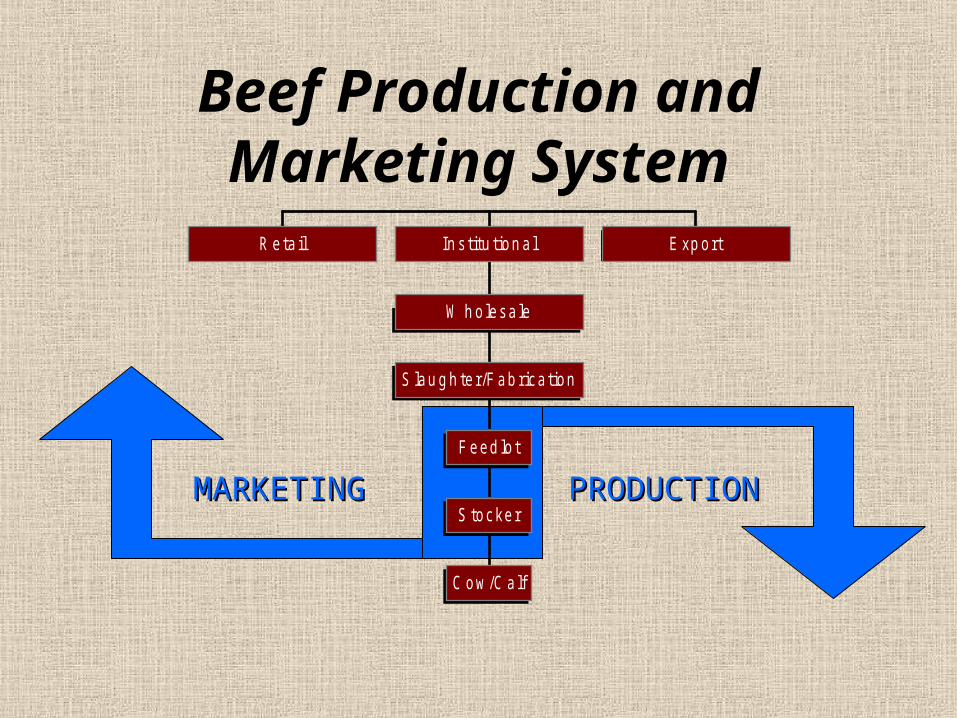

Beef Production and Marketing System

R eta il

C ow /C a lf

S tocker

F eed lo t

S lau g h te r/F ab rica tion

W h o lesa le

In s titu tion a l E xp ort

MARKETINGMARKETING PRODUCTIOPRODUCTIONN

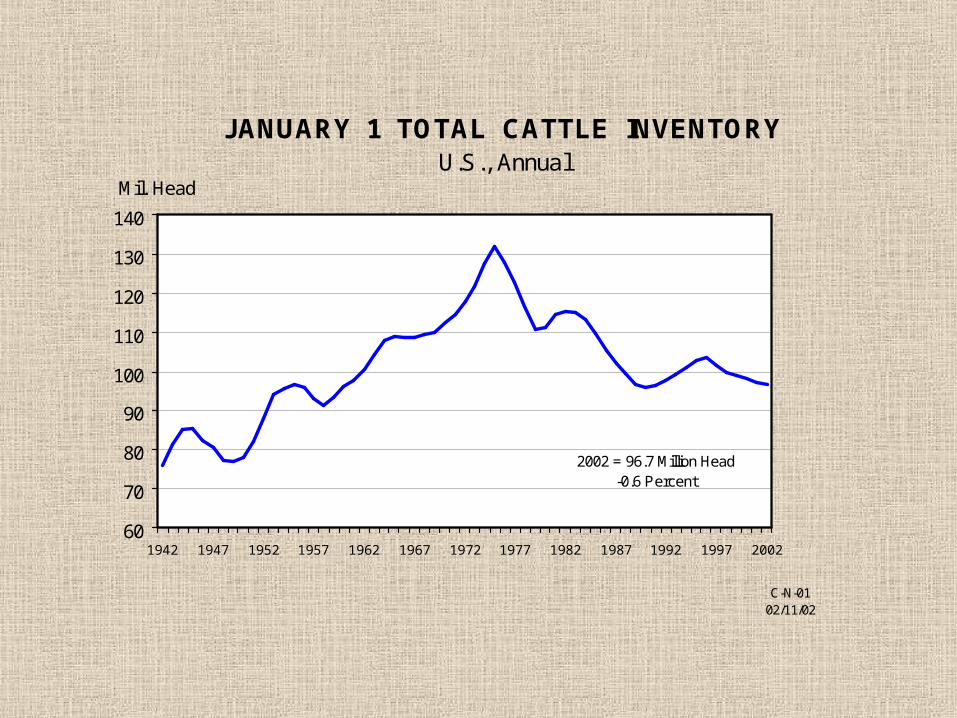

JANUARY 1 TOTAL CATTLE INVENTORYU.S., Annual

60

70

80

90

100

110

120

130

140

1942 1947 1952 1957 1962 1967 1972 1977 1982 1987 1992 1997 2002

Mil. Head

C-N-0102/11/02

-0.6 Percent2002 = 96.7 Million Head

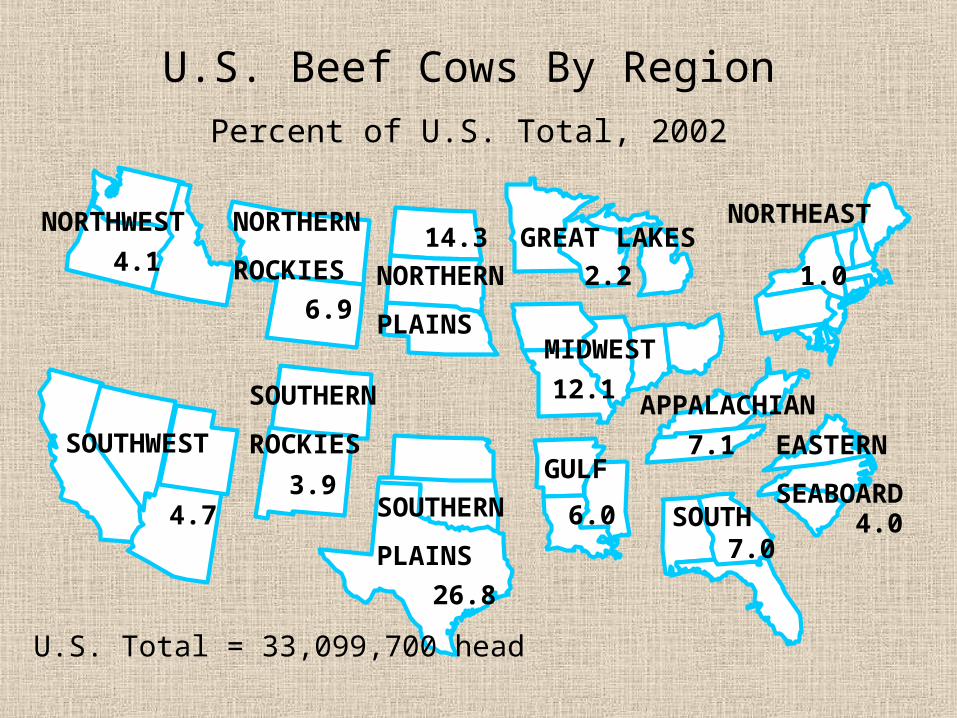

U.S. Beef Cows By RegionPercent of U.S. Total, 2002

NORTHWESTNORTHERN

ROCKIES NORTHERN

PLAINS

SOUTHERN

PLAINS

GREAT LAKESNORTHEAST

MIDWEST

GULF

APPALACHIAN

SOUTH

SOUTHWEST

SOUTHERN

ROCKIES EASTERN

SEABOARD 6.0

4.1

4.7

6.9

3.9

14.3

26.8

12.1

2.2

7.1

7.0 4.0

1.0

U.S. Total = 33,099,700 head

Regional Share of Beef Cows,

January 1, 2002

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

North

west

South

west

N.Roc

kies

S.Roc

kies

N.Plai

ns

S.Plai

ns

G.Lak

es

Midw

est

Gulf

South

Appala

chian

E.Sea

boar

d

North

east

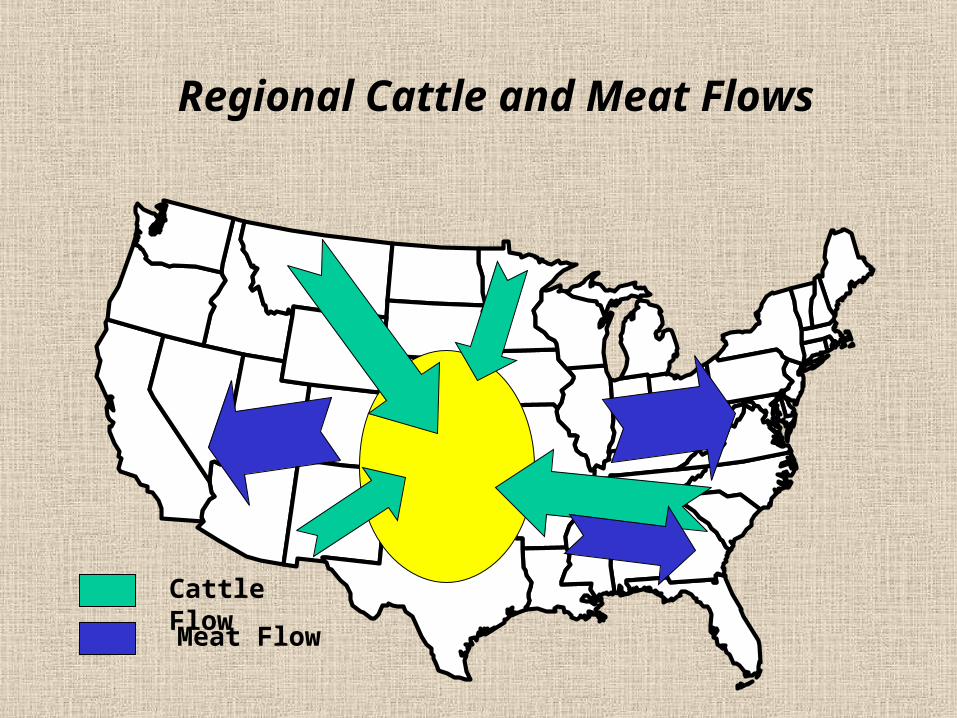

Regional Cattle and Meat Flows

Cattle Flow

Meat Flow

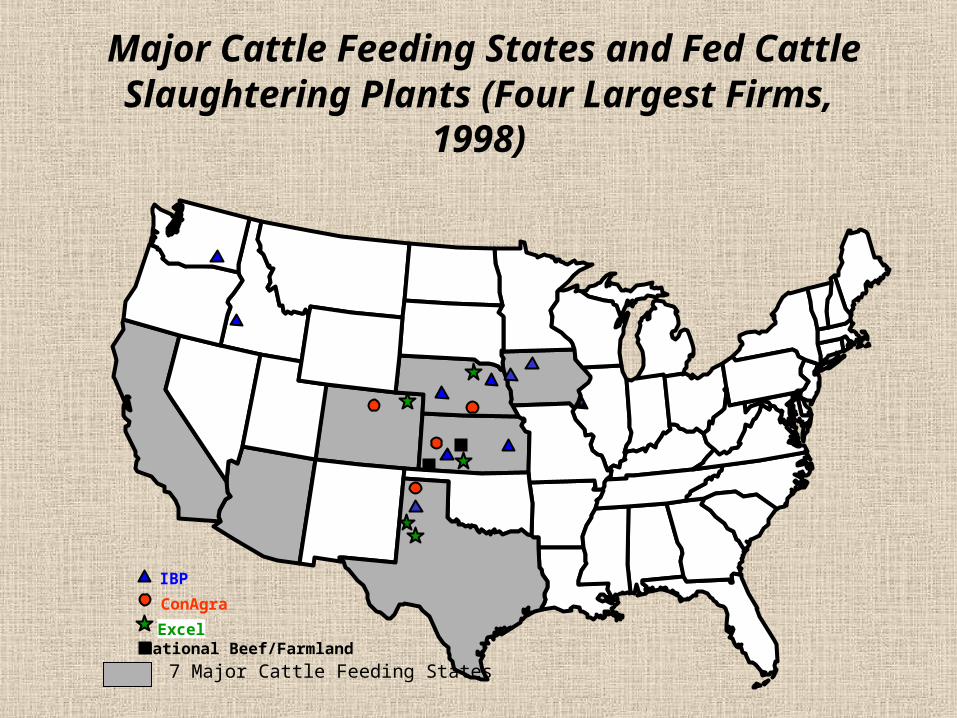

Major Cattle Feeding States and Fed Cattle Slaughtering Plants (Four

Largest Firms, 1998)

IBP

ConAgra

ExcelNational Beef/Farmland

7 Major Cattle Feeding States

What is the Stocker Industry?

The U.S. Stocker Industry

• A very important but poorly understood sector of the beef industry– geographically widespread– diverse production systems– hard to measure

Characteristics of Stocker Production

• Animal Growth (versus fattening)• Use of Forages (versus

concentrates)• Viable Enterprise

– Time Required

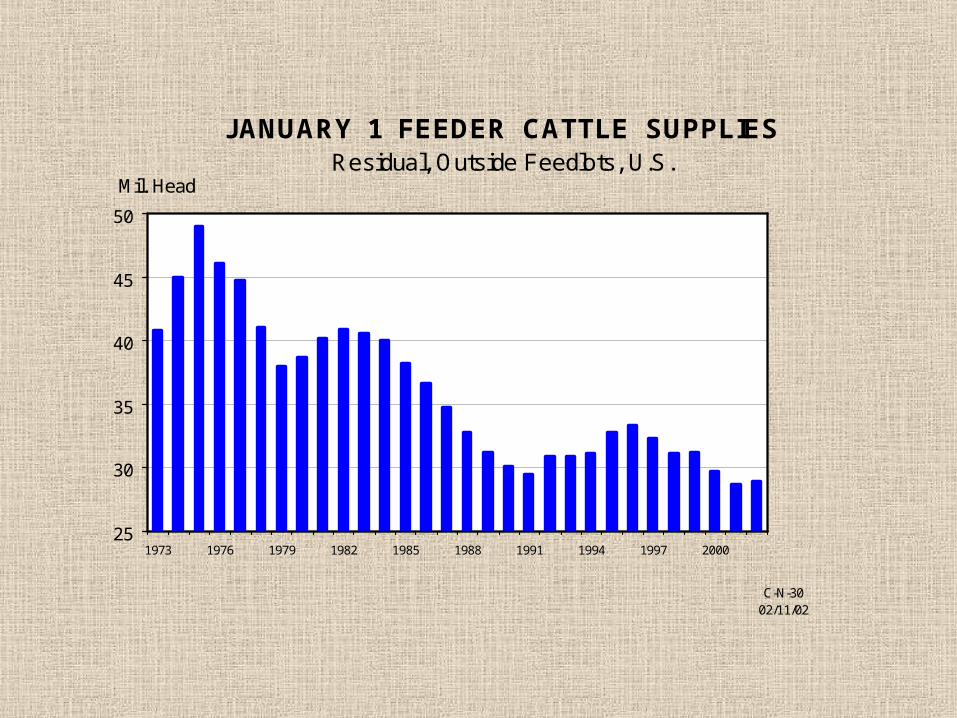

JANUARY 1 FEEDER CATTLE SUPPLIESResidual, Outside Feedlots, U.S.

25

30

35

40

45

50

1973 1976 1979 1982 1985 1988 1991 1994 1997 2000

Mil. Head

C-N-3002/11/02

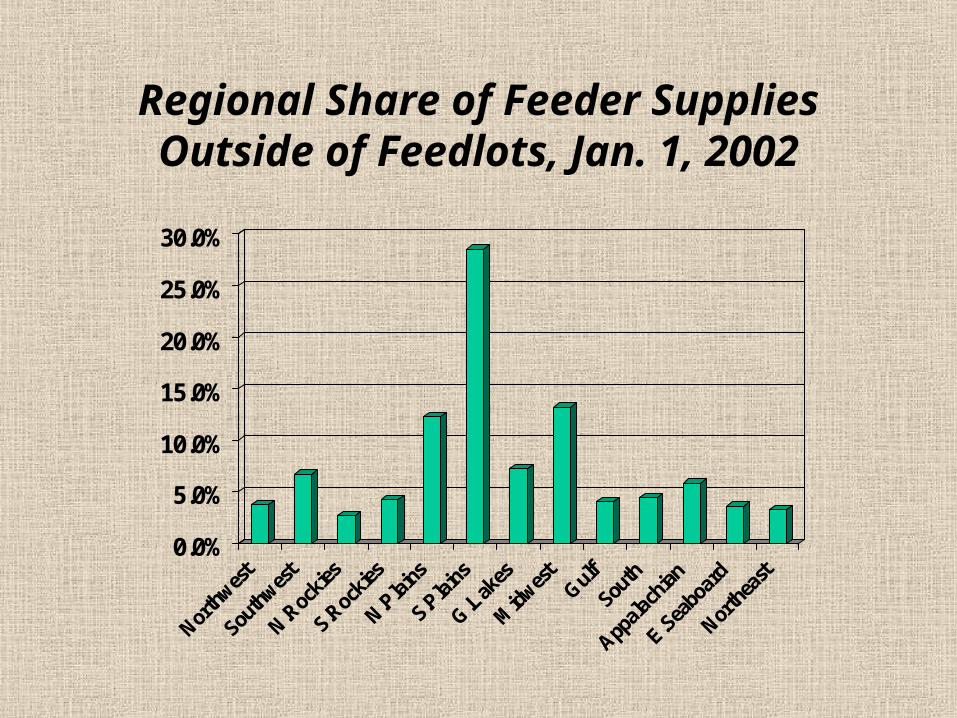

Regional Share of Feeder Supplies

Outside of Feedlots, Jan. 1, 2002

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

North

west

South

west

N.Roc

kies

S.Roc

kies

N.Plai

ns

S.Plai

ns

G.Lak

es

Midw

est

Gulf

South

Appala

chian

E.Sea

boar

d

North

east

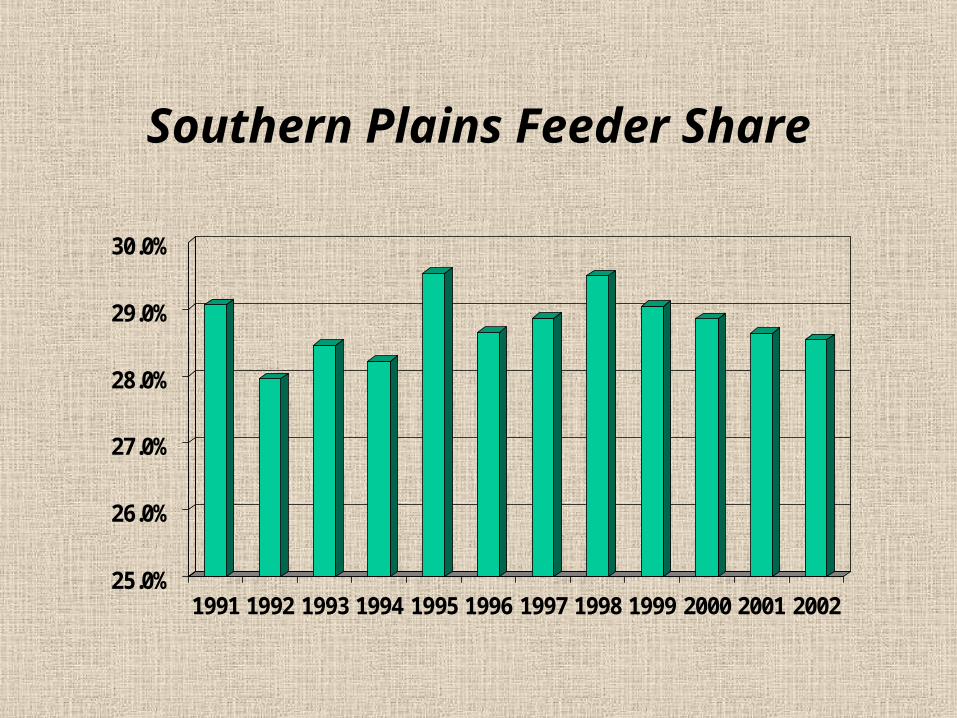

Southern Plains Feeder Share

25.0%

26.0%

27.0%

28.0%

29.0%

30.0%

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

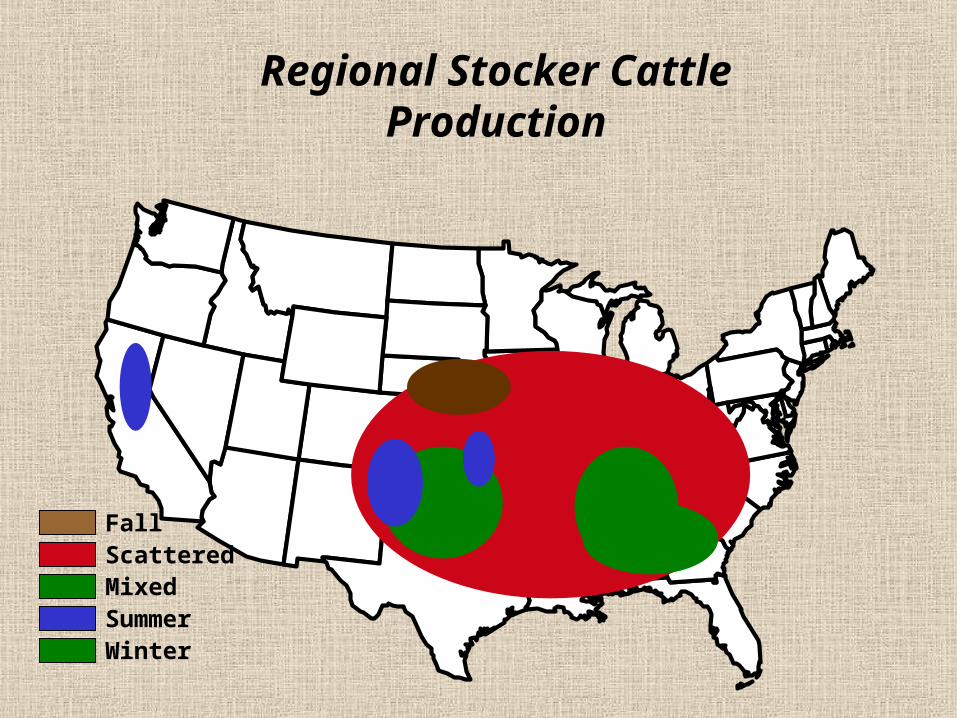

Diversity of Stocker Production

• Grazing– Summer

• Season Long/Early Intensive• Native Range/Tame Pasture• Crop Aftermath

– Winter• Annual Cool Season• Perennial Cool Season

Diversity of Stocker Production

• Semi-confinement– Put and Take– Creep Feeding– Dry Winter

• Confinement – Harvested Forages

Regional Stocker Cattle Production

ScatteredMixedSummerWinter

Fall

Okla

Washington

Idaho

California

Colorado Kansas

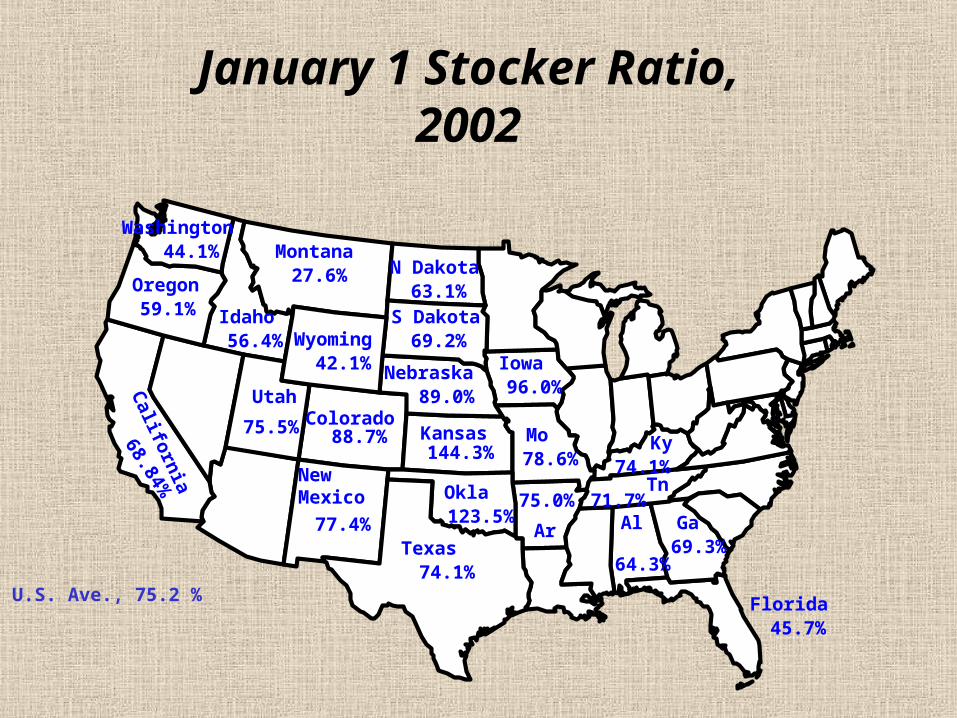

U.S. Ave., 75.2 %

January 1 Stocker Ratio, 2002

Wyoming

Montana

Oregon

New Mexico

68.84%

44.1%

59.1%

27.6%

56.4%42.1%

88.7%144.3%

123.5%77.4%

75.5%

Utah

Texas74.1%

78.6%

45.7%Florida

74.1%

63.1%N Dakota

S Dakota 69.2%

89.0%Nebraska

Mo Ky

71.7%

Tn

Al

64.3%

69.3%

GaAr

75.0%

Iowa 96.0%

Okla

Washington

Idaho

California

Colorado Kansas

U.S. Ave., 75.2 %

January 1 Stocker Ratio, 2002

Wyoming

Montana

Oregon

New Mexico

68.84%

44.1%

59.1%

27.6%

56.4%42.1%

88.7%144.3%

123.5%77.4%

75.5%

Utah

Texas74.1%

78.6%

45.7%Florida

74.1%

63.1%N Dakota

S Dakota 69.2%

89.0%Nebraska

Mo Ky

71.7%

Tn

Al

64.3%

69.3%

GaAr

75.0%

Iowa 96.0%

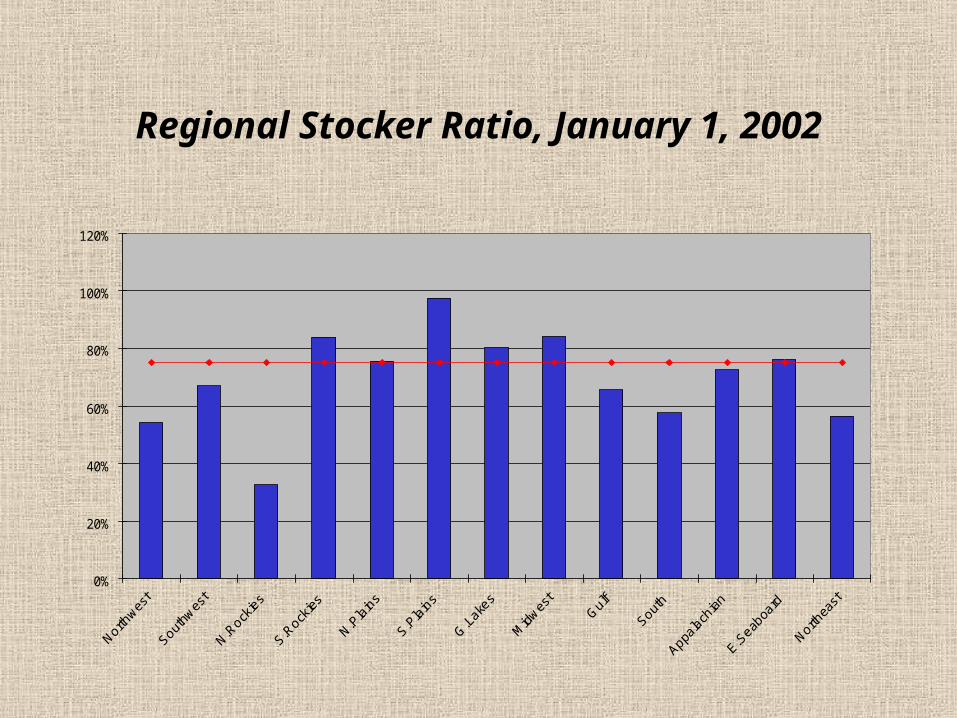

Regional Stocker Ratio, January 1, 2002

0%

20%

40%

60%

80%

100%

120%

Unique Role of Winter Stockers

• Fall demand for wheat stockers helps offset seasonally large fall marketings of calves

• Helps stabilize seasonal price patterns

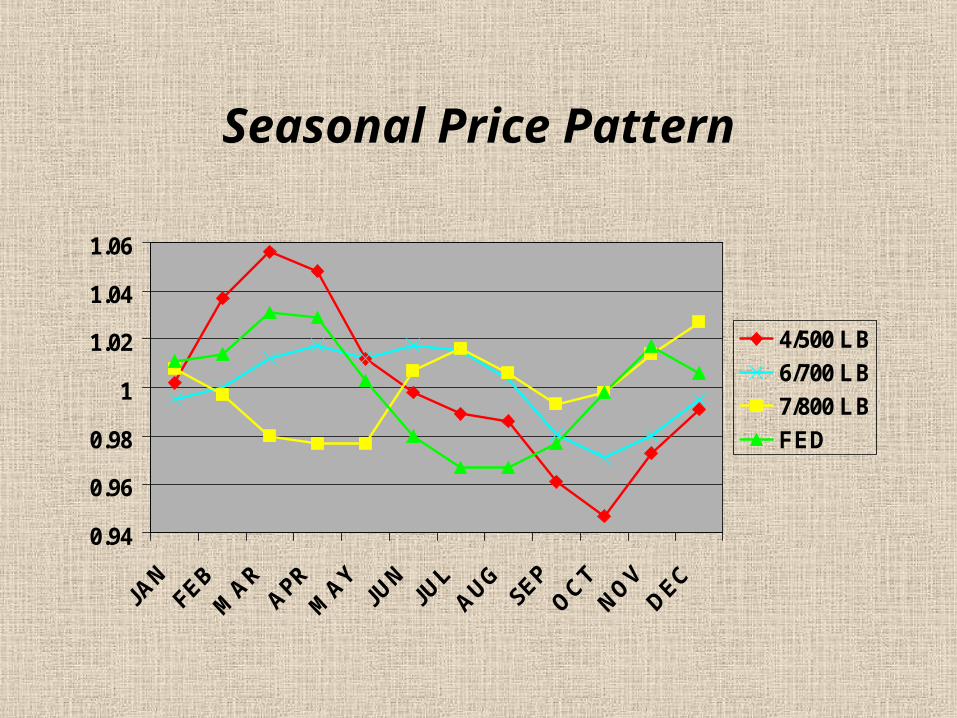

Seasonal Price Pattern

0.94

0.96

0.98

1

1.02

1.04

1.06

4/500 LB

6/700 LB

7/800 LB

FED

What is the “Job” of the Stocker Industry?

• Stocker gains are the cheapest beef cattle gains

• Beef industry flexibility• Feed industry balance• Quality Improvement

The Production Role of Stockers

• Utilize forages for cheap gain• Increase feeder cattle weight/age• Upgrade cattle quality

The Inventory Role of Stockers

• Allocate feeder cattle supplies over time– seasonally– year-to-year

• Provide variation in cattle slaughter age

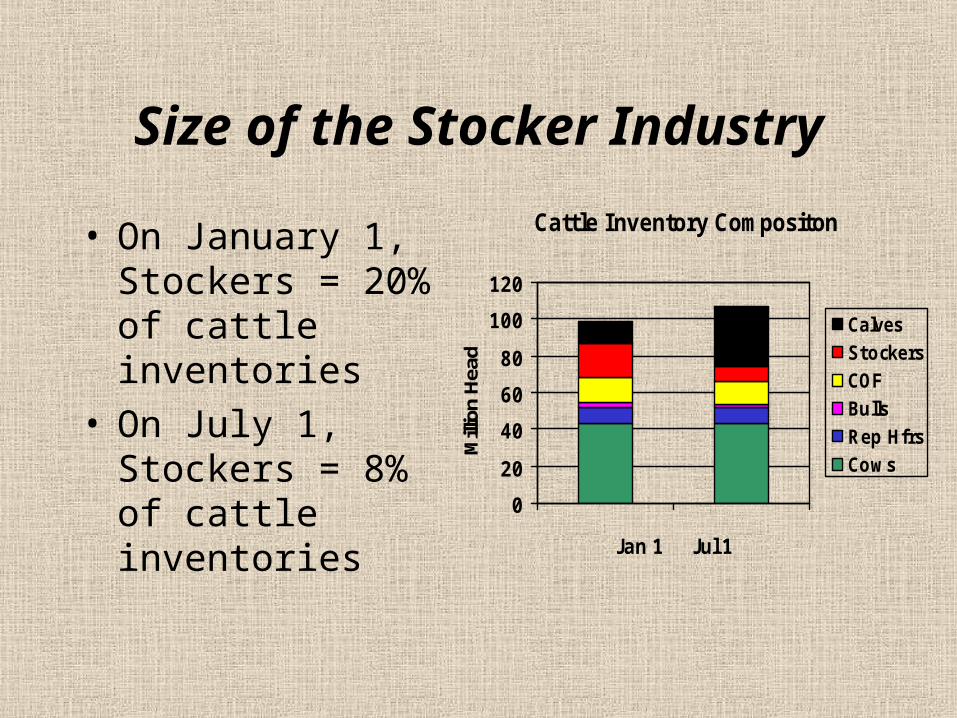

Size of the Stocker Industry

• On January 1, Stockers = 20% of cattle inventories

• On July 1, Stockers = 8% of cattle inventories

Cattle Inventory Compositon

0

20

40

60

80

100

120

Jan 1 Jul 1

Mill

ion

Hea

d

CalvesStockersCOFBullsRep HfrsCows

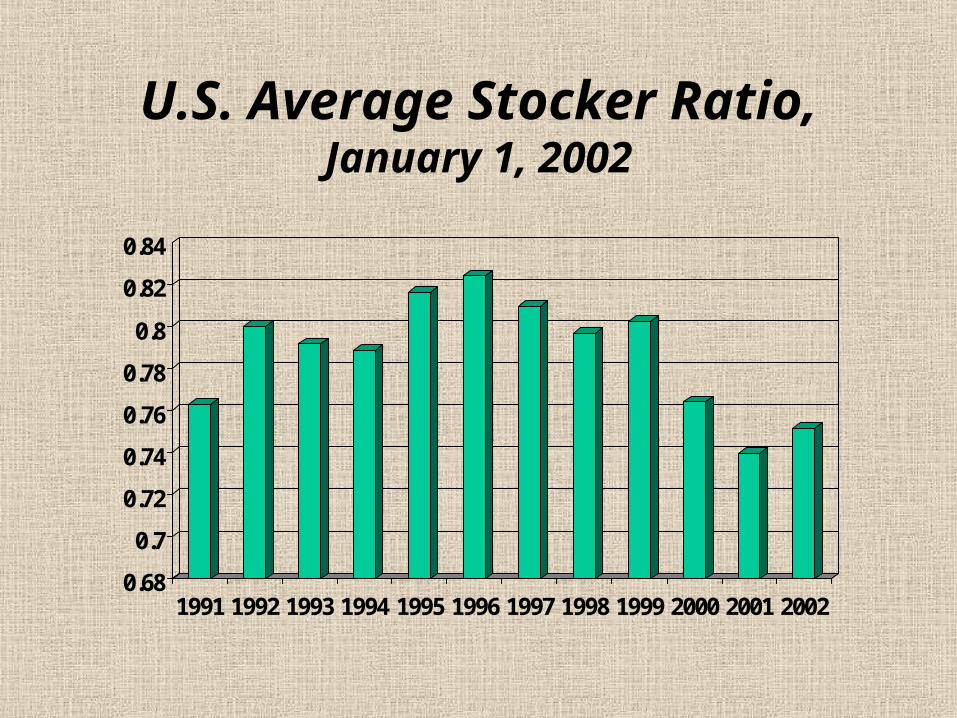

U.S. Average Stocker Ratio,

January 1, 2002

0.68

0.7

0.72

0.74

0.76

0.78

0.8

0.82

0.84

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

The Market-Balance Role of Stockers

• Maintain economic balance between livestock, grain and forage markets– respond to economic shocks

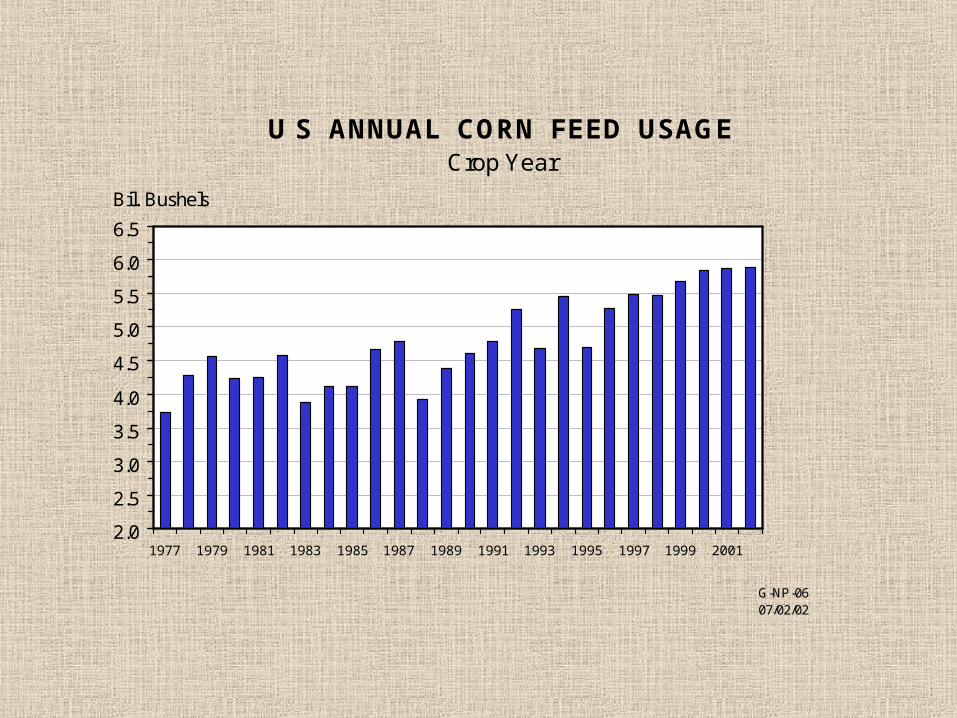

U S ANNUAL CORN FEED USAGECrop Year

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

1977 1979 1981 1983 1985 1987 1989 1991 1993 1995 1997 1999 2001

Bil. Bushels

G-NP-0607/02/02

The Stocker Industry Is The Beef Industry “Shock Absorber”

How Does The How Does The Stocker Industry Stocker Industry Accomplish All Accomplish All These Things?These Things?

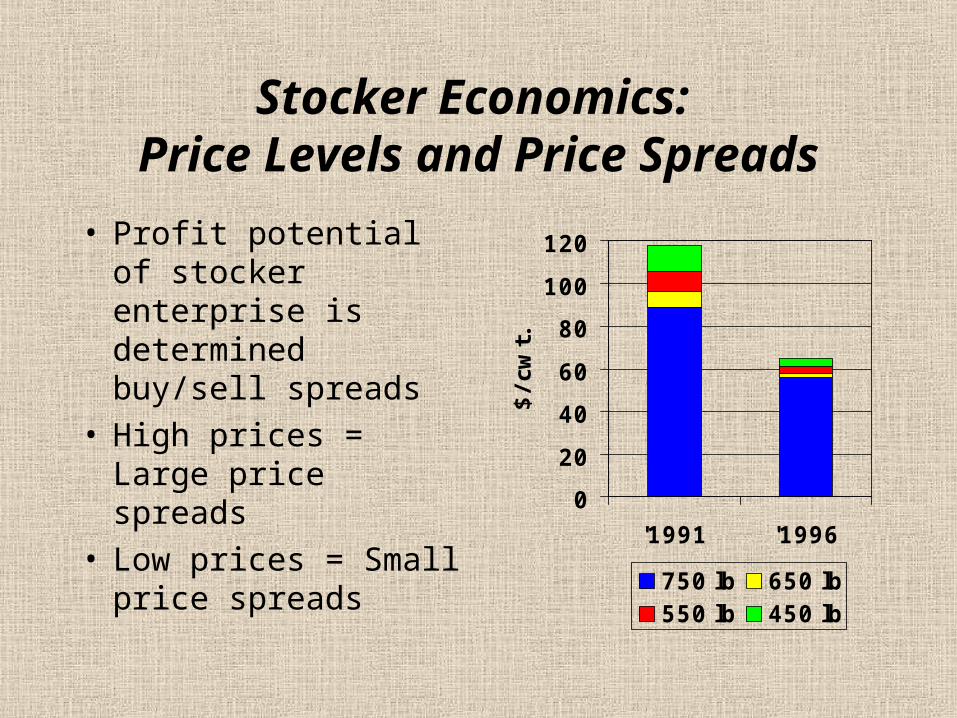

Stocker Economics: Price Levels and Price

Spreads• Profit potential of

stocker enterprise is determined buy/sell spreads

• High prices = Large price spreads

• Low prices = Small price spreads

0

20

40

60

80

100

120

'1991 '1996$/c

wt.

750 lb 650 lb550 lb 450 lb

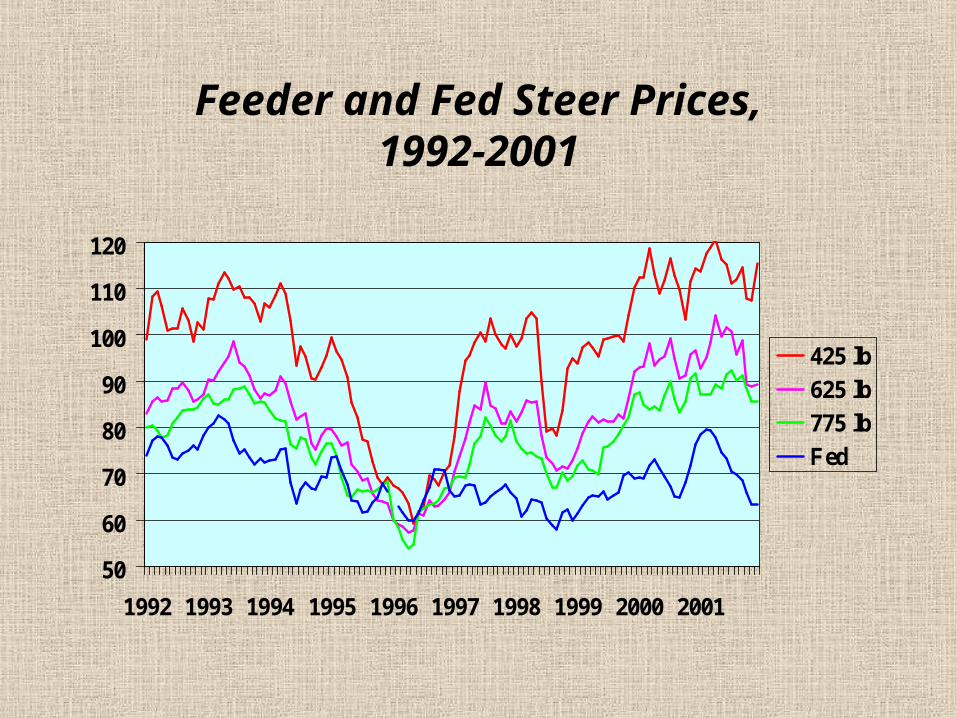

Feeder and Fed Steer Prices,1992-2001

50

60

70

80

90

100

110

120

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

425 lb

625 lb

775 lb

Fed

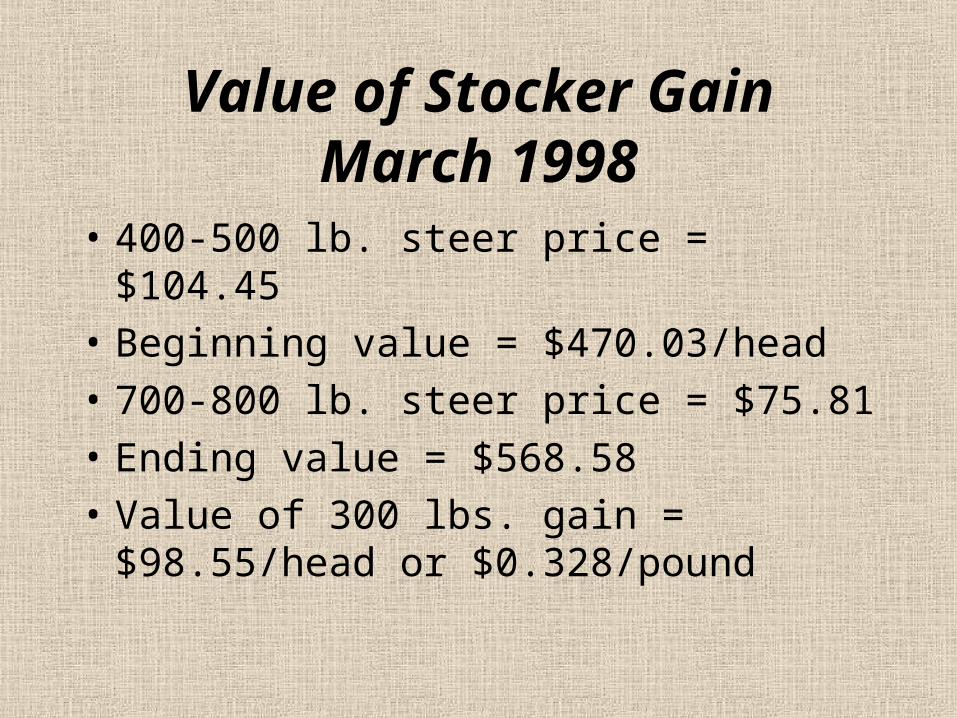

Value of Stocker GainMarch 1998

• 400-500 lb. steer price = $104.45• Beginning value = $470.03/head• 700-800 lb. steer price = $75.81• Ending value = $568.58• Value of 300 lbs. gain =

$98.55/head or $0.328/pound

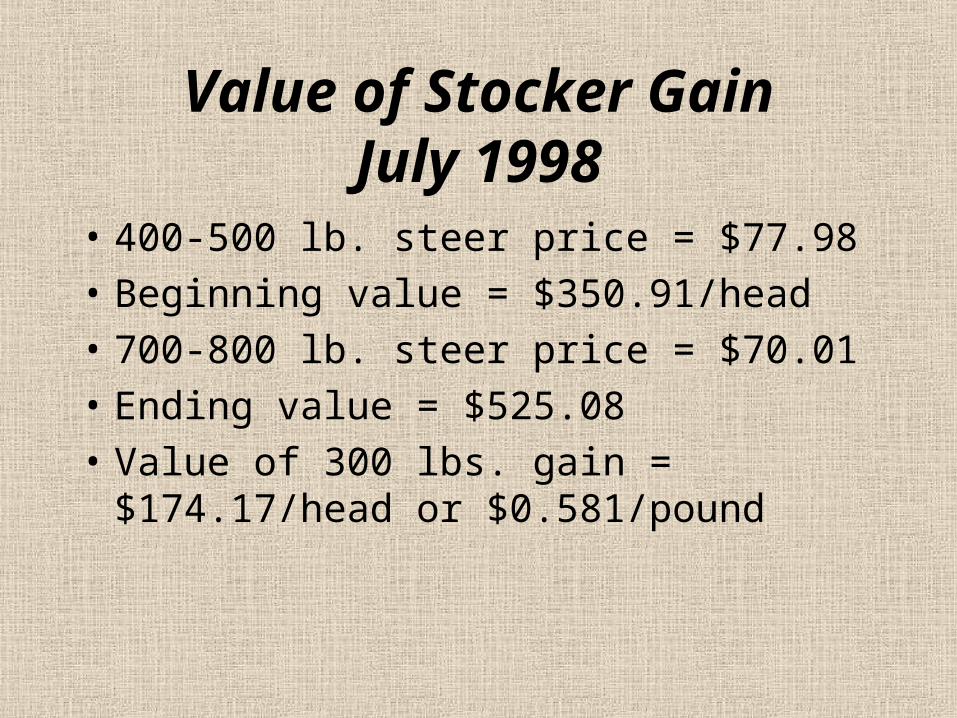

Value of Stocker GainJuly 1998

• 400-500 lb. steer price = $77.98• Beginning value = $350.91/head• 700-800 lb. steer price = $70.01• Ending value = $525.08• Value of 300 lbs. gain =

$174.17/head or $0.581/pound

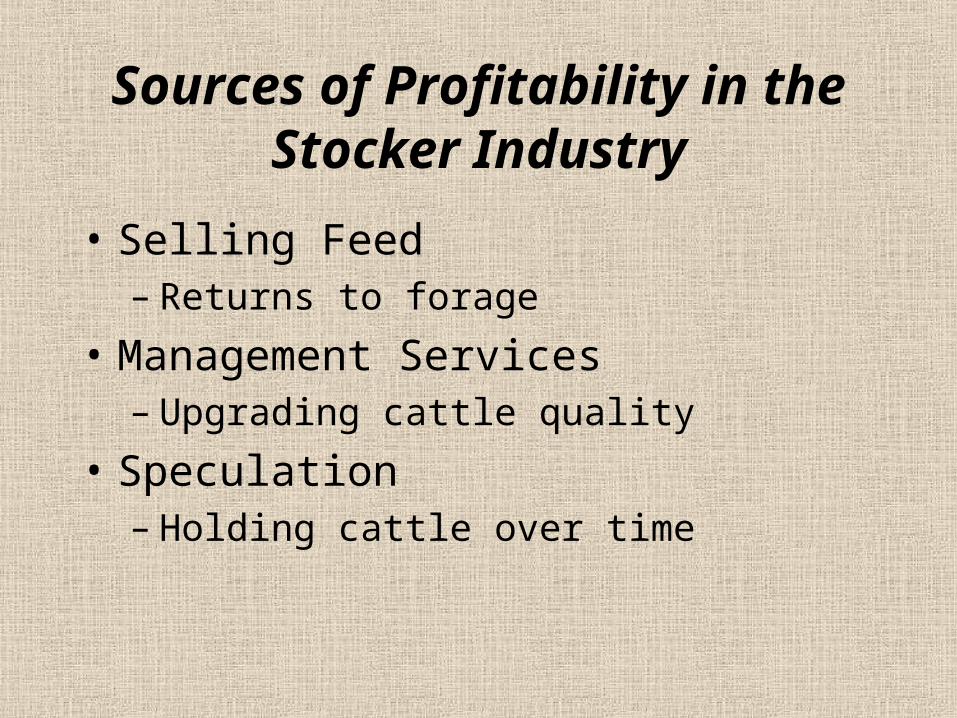

Sources of Profitability in the Stocker Industry

• Selling Feed– Returns to forage

• Management Services– Upgrading cattle quality

• Speculation– Holding cattle over time

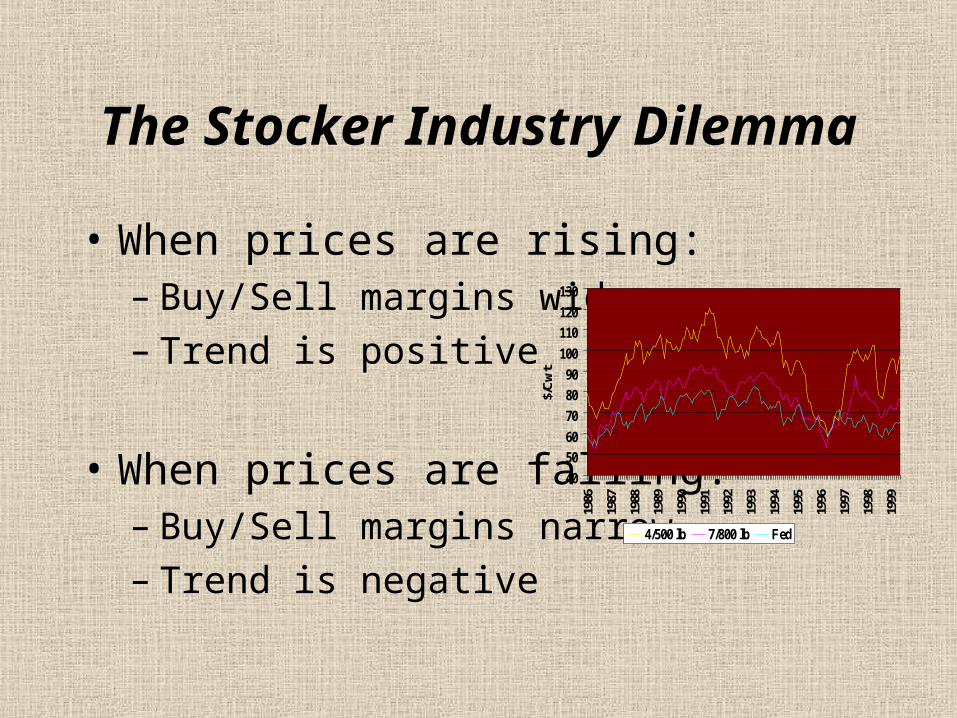

The Stocker Industry Dilemma

• When prices are rising:– Buy/Sell margins widen– Trend is positive

• When prices are falling:– Buy/Sell margins narrow– Trend is negative

40

50

60

70

80

90

100

110

120

130

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

$/C

wt

4/500 lb 7/800 lb Fed

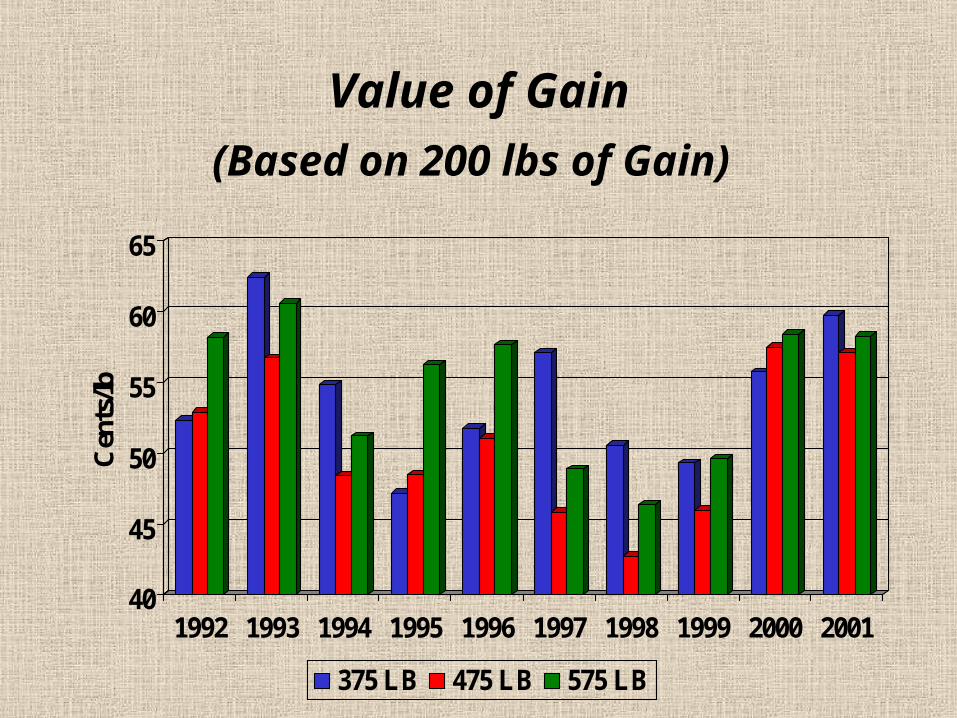

Value of Gain(Based on 200 lbs of Gain)

40

45

50

55

60

65

Cen

ts/lb

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

375 LB 475 LB 575 LB

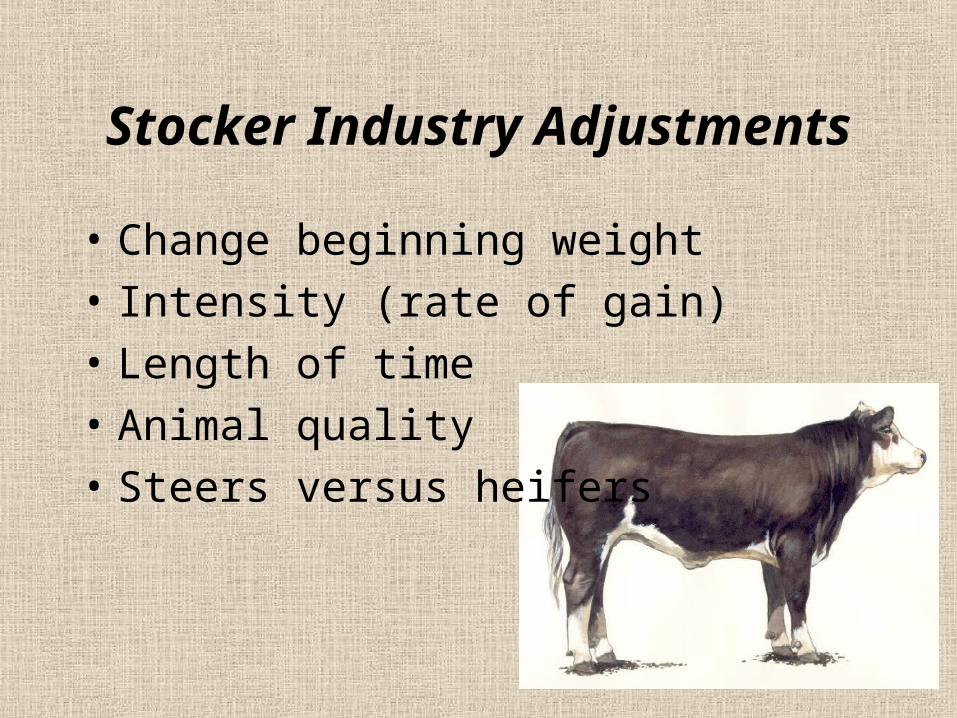

Stocker Industry Adjustments

• Change beginning weight• Intensity (rate of gain)• Length of time• Animal quality• Steers versus heifers

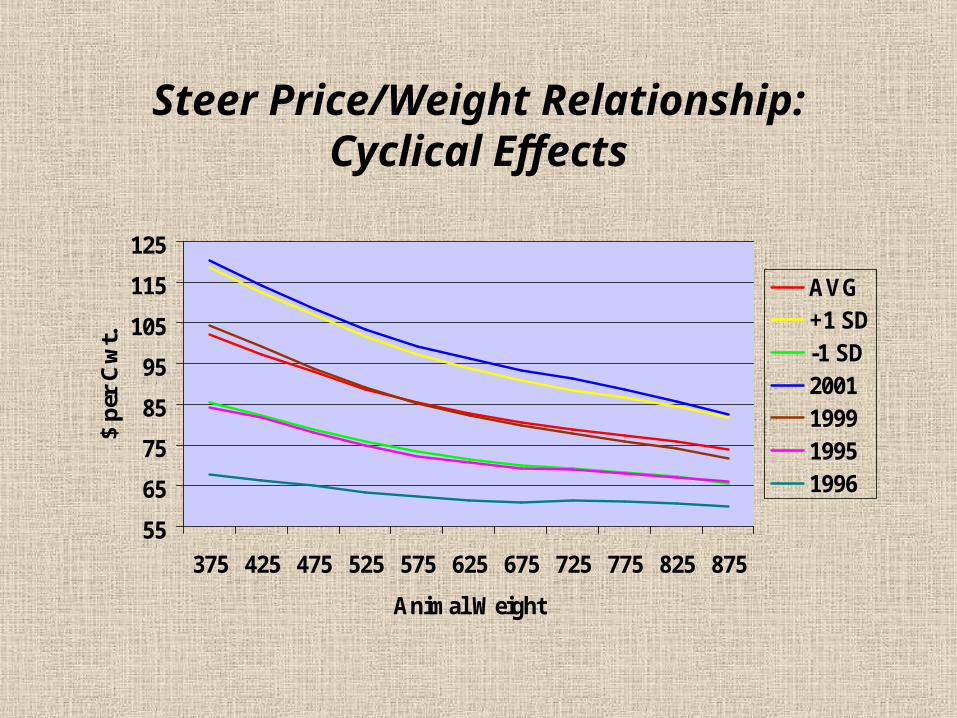

Steer Price/Weight Relationship:Cyclical Effects

55

65

75

85

95

105

115

125

375 425 475 525 575 625 675 725 775 825 875

Animal Weight

$ p

er C

wt.

AVG+1 SD-1 SD2001199919951996

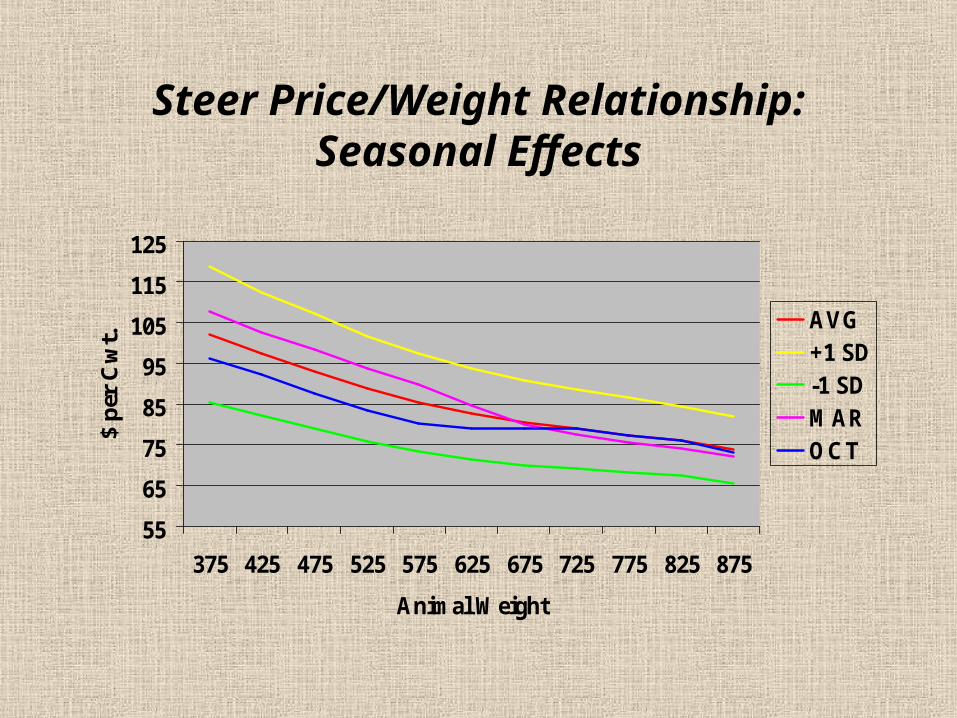

Steer Price/Weight Relationship:Seasonal Effects

55

65

75

85

95

105

115

125

375 425 475 525 575 625 675 725 775 825 875

Animal Weight

$ p

er C

wt.

AVG+1 SD-1 SDMAROCT

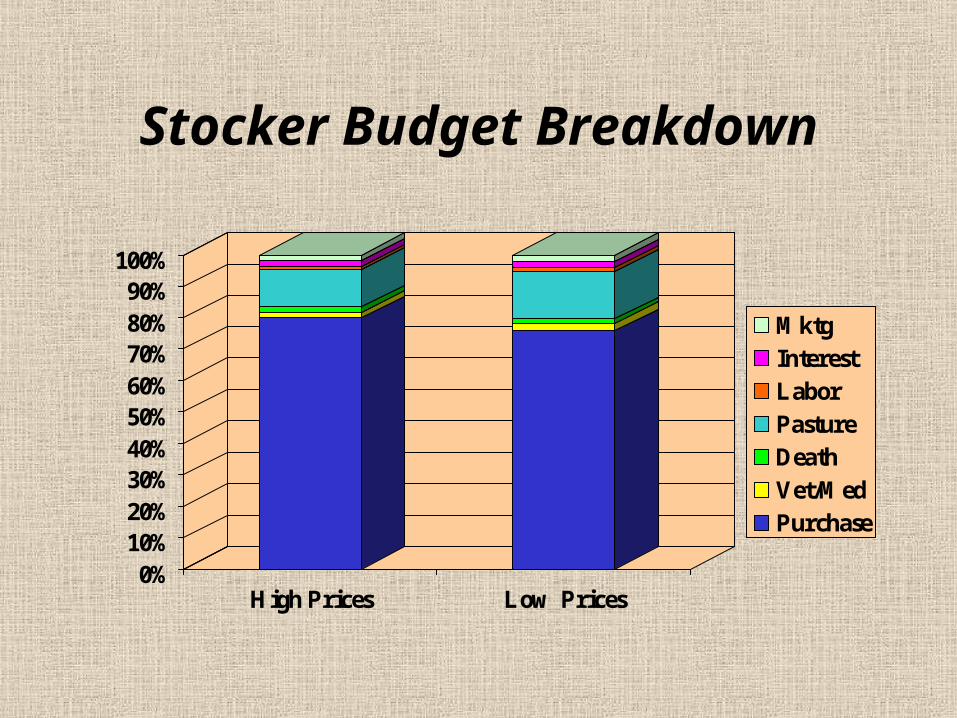

Stocker Budget Breakdown

0%10%20%30%40%50%60%70%80%90%

100%

High Prices Low Prices

MktgInterestLaborPastureDeathVet/MedPurchase

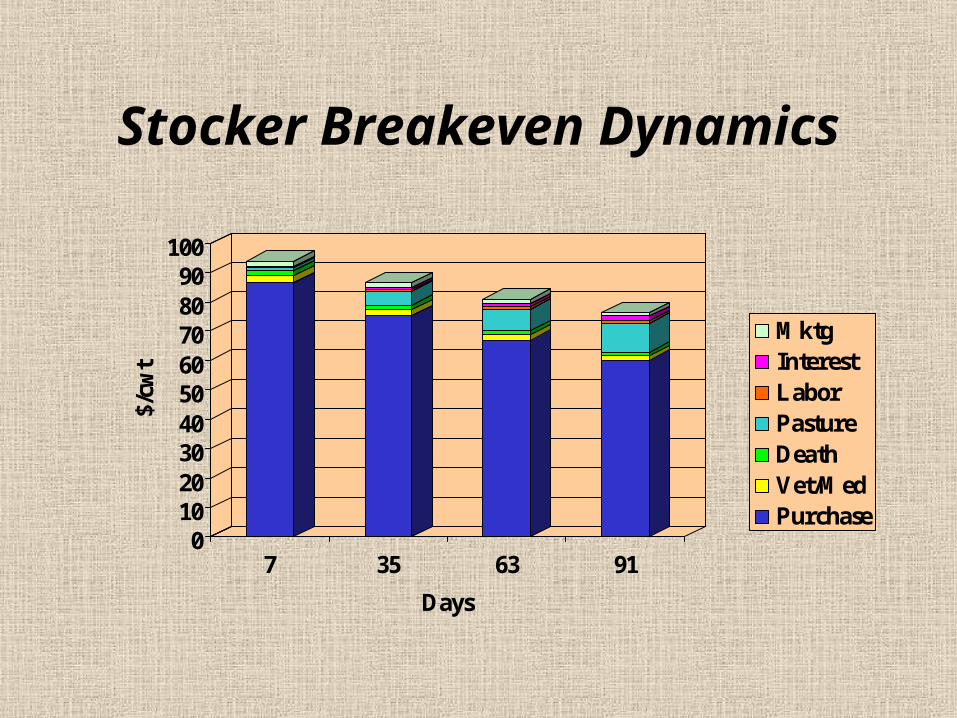

Stocker Breakeven Dynamics

0102030405060708090

100

$/cw

t

7 35 63 91

Days

MktgInterestLaborPastureDeathVet/MedPurchase

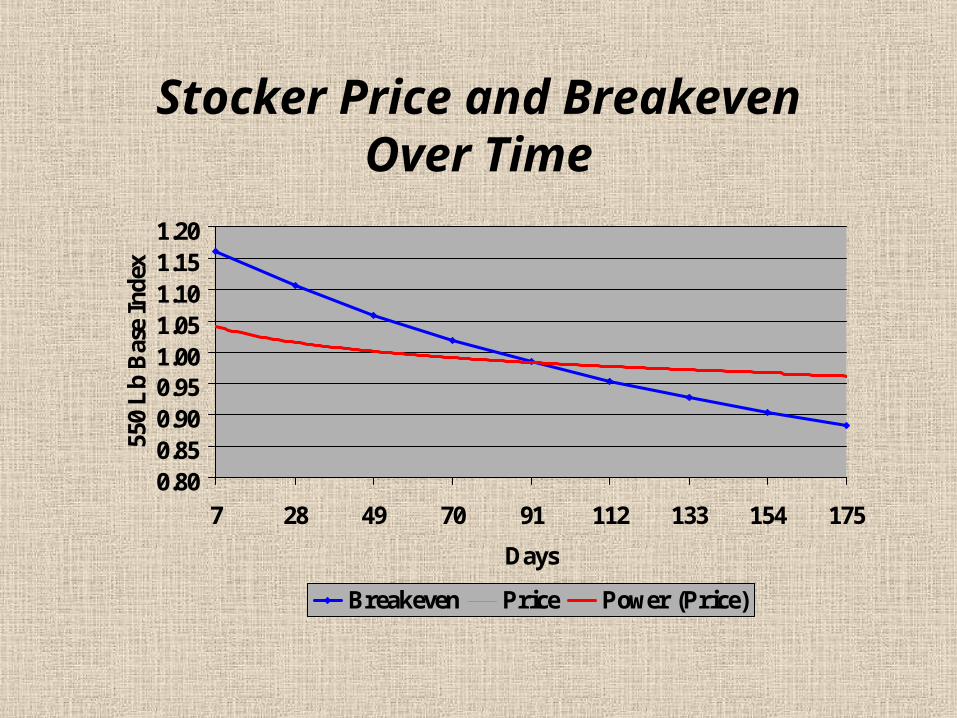

Stocker Price and BreakevenOver Time

0.800.850.900.951.001.051.101.151.20

7 28 49 70 91 112 133 154 175

Days

550

Lb

Bas

e In

dex

Breakeven Price Power (Price)

Major Factors Affecting Stocker Profitability

• Purchase Price• Time• Feed Cost• Animal Performance

Summary

• Stocker industry plays a vital role in the cattle industry

• Southern Plains winter wheat pasture grazing plays a unique role

• Stocker production is especially important in Oklahoma