Embed Size (px)

Citation preview

The Philippines Economic Outlook 2017 by Aekapol Chongvilaivan Country Economist Philippines Country Office

Taking Off in A Strong Headwind

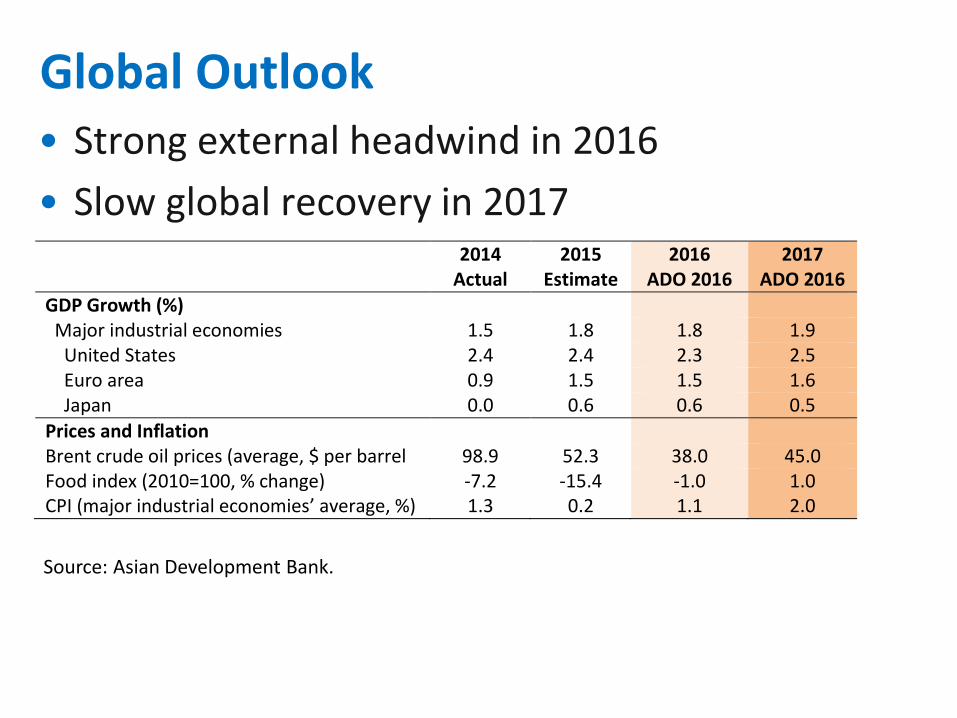

Global Outlook

Source: Asian Development Bank.

• Strong external headwind in 2016

• Slow global recovery in 2017 2014

Actual 2015

Estimate 2016

ADO 2016 2017

ADO 2016

GDP Growth (%) Major industrial economies 1.5 1.8 1.8 1.9 United States 2.4 2.4 2.3 2.5 Euro area 0.9 1.5 1.5 1.6 Japan 0.0 0.6 0.6 0.5

Prices and Inflation Brent crude oil prices (average, $ per barrel 98.9 52.3 38.0 45.0 Food index (2010=100, % change) -7.2 -15.4 -1.0 1.0 CPI (major industrial economies’ average, %) 1.3 0.2 1.1 2.0

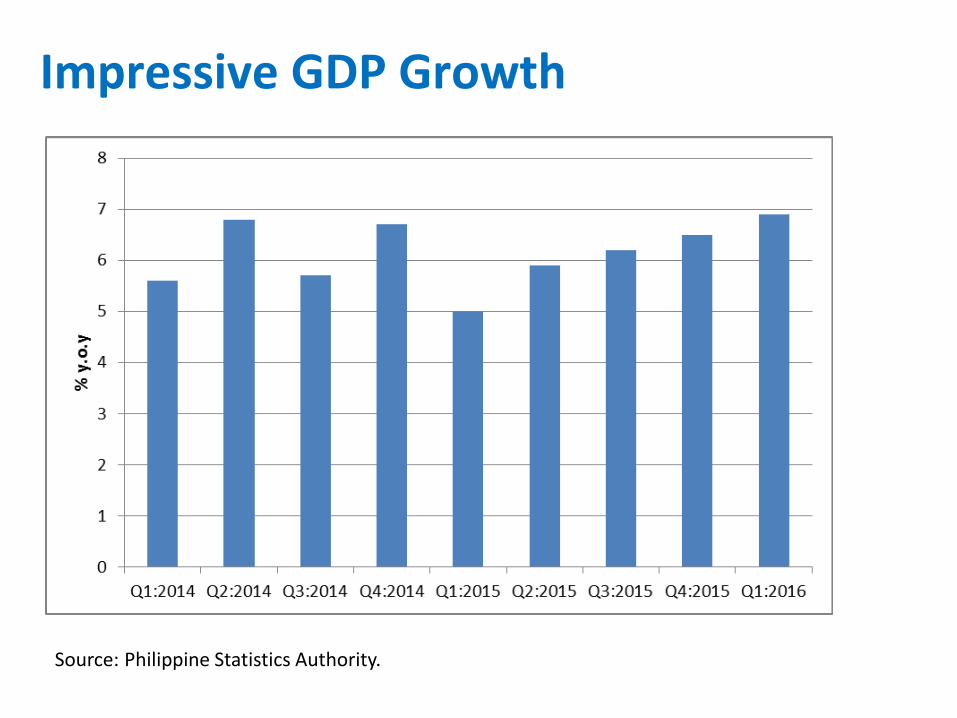

Impressive GDP Growth

Source: Philippine Statistics Authority.

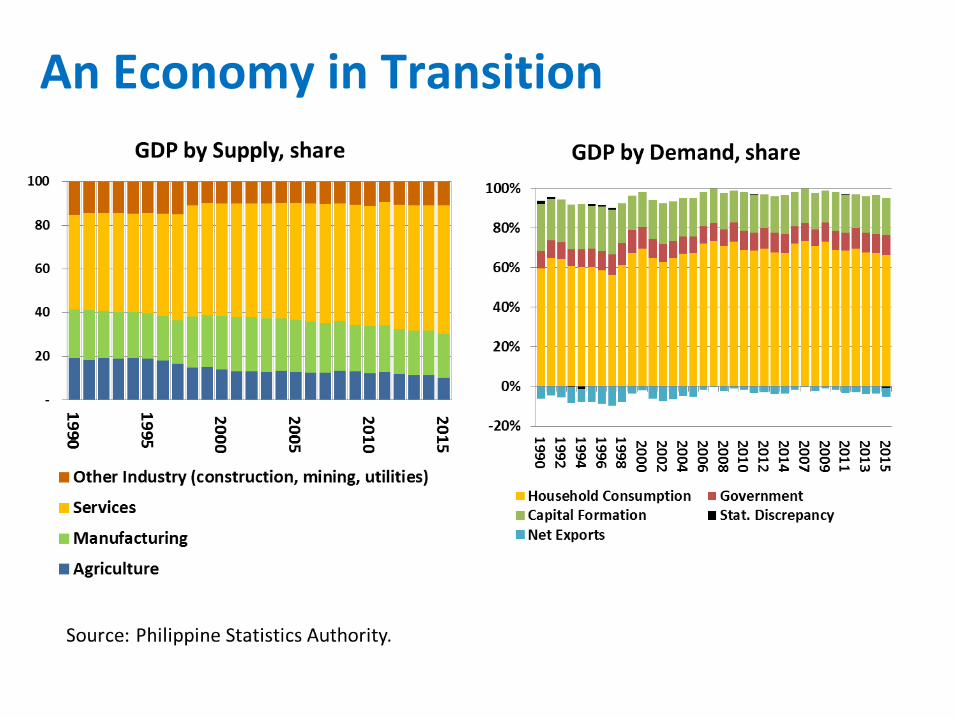

An Economy in Transition

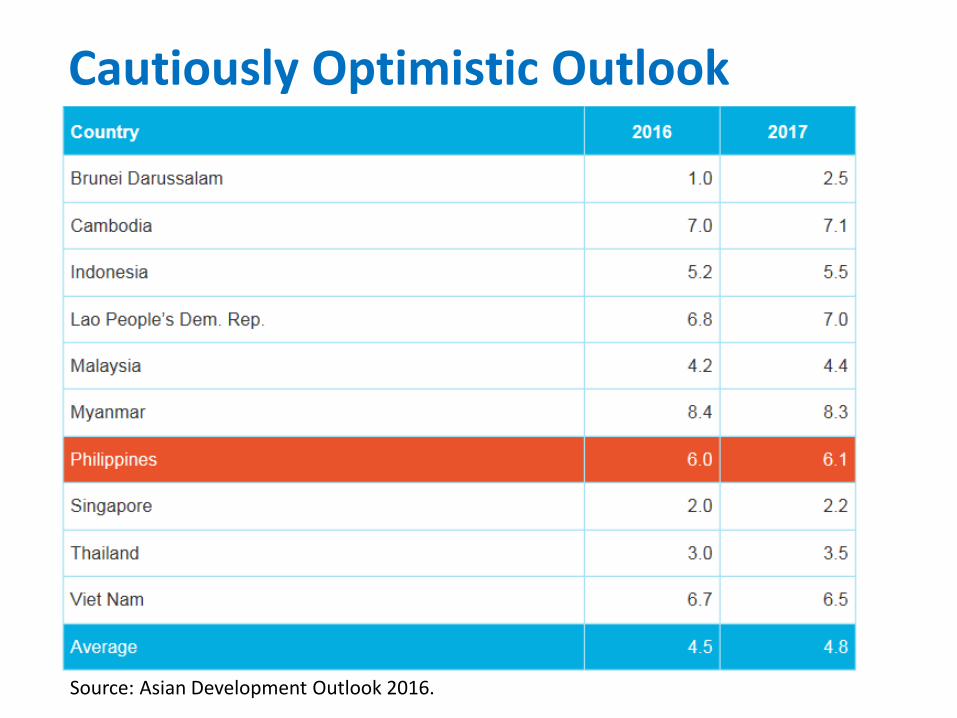

Cautiously Optimistic Outlook

Source: Asian Development Outlook 2016.

Recent Economic Developments

• Upbeat growth partly driven by election-related spending

• Fixed capital investment rose 25.6%

• Booms in (public)construction, manufacturing, and service sectors

• Slow down in remittances to 3.0%

• Merchandise exports fell 7.3%

• Agriculture sector affected by El Nino, but less severe than expected

Post-election slowdown

• Slower pace in Q2-Q4 2016 anticipated

• Pre-election spending effects depleting

• Weak demand for merchandise exports

• Exports to Japan flat; Exports to US, EU, China falling

• Imports on the rise due to strong domestic demand

• Private and Public investment expected to ease

Faster Pace in 2017

• Slightly stronger growth of 6.1% expected in 2017

• Improving, albeit slowly, economic performance of the US and EU

• New administration ramping up infrastructure investment and public spending

• Ripple effects of Brexit on PHI “unlikely”

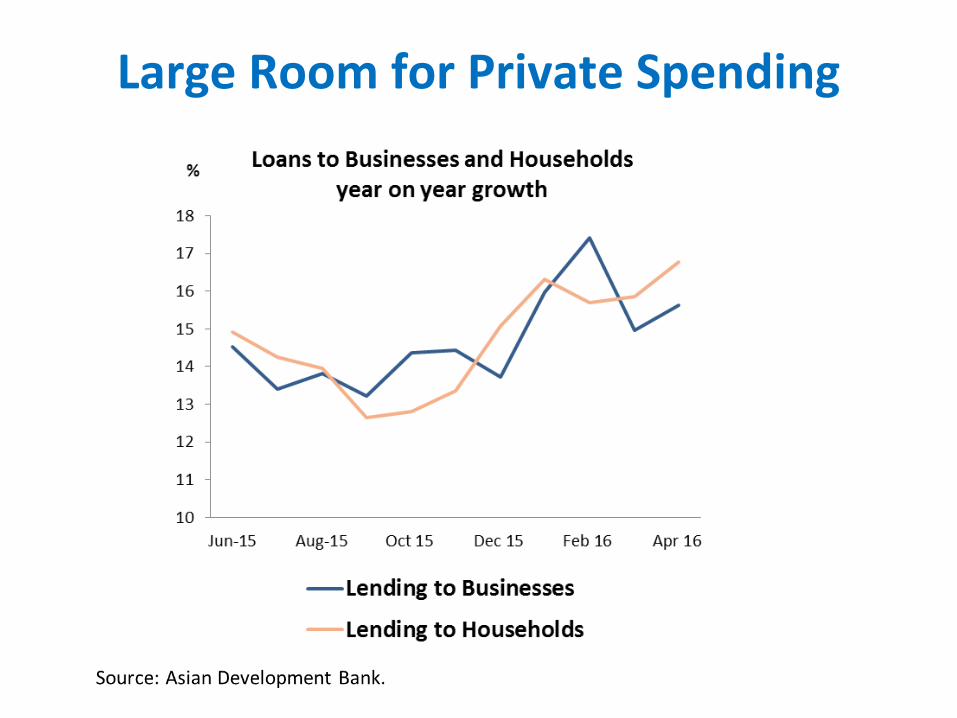

Large Room for Private Spending

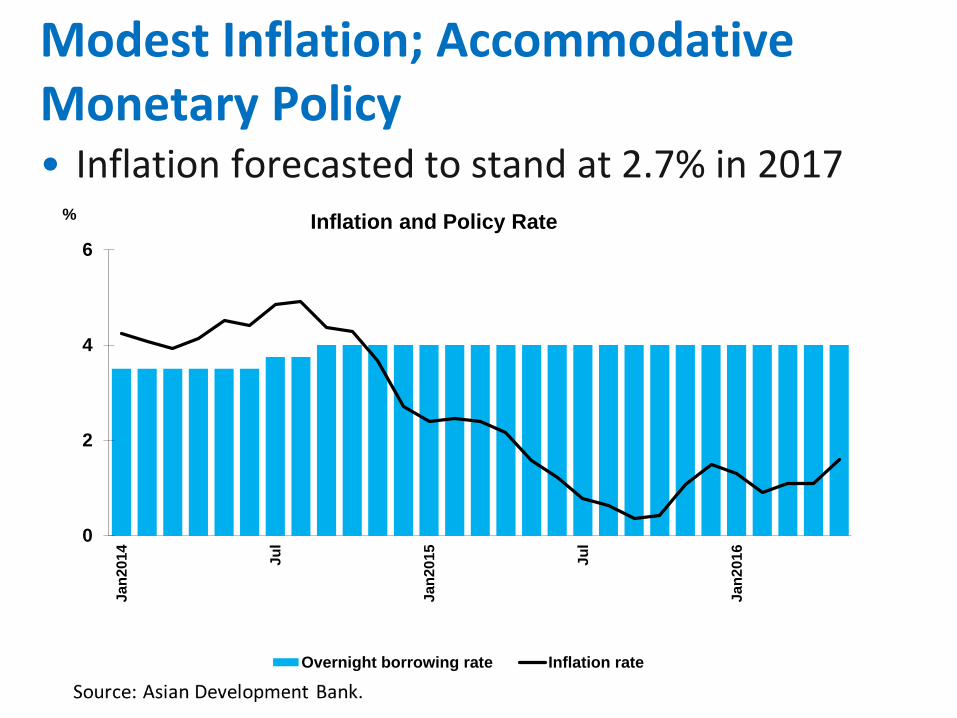

Modest Inflation; Accommodative Monetary Policy • Inflation forecasted to stand at 2.7% in 2017

0

2

4

6

Jan

2014

Ju

l

Jan

2015

Ju

l

Jan

2016

% Inflation and Policy Rate

Overnight borrowing rate Inflation rate

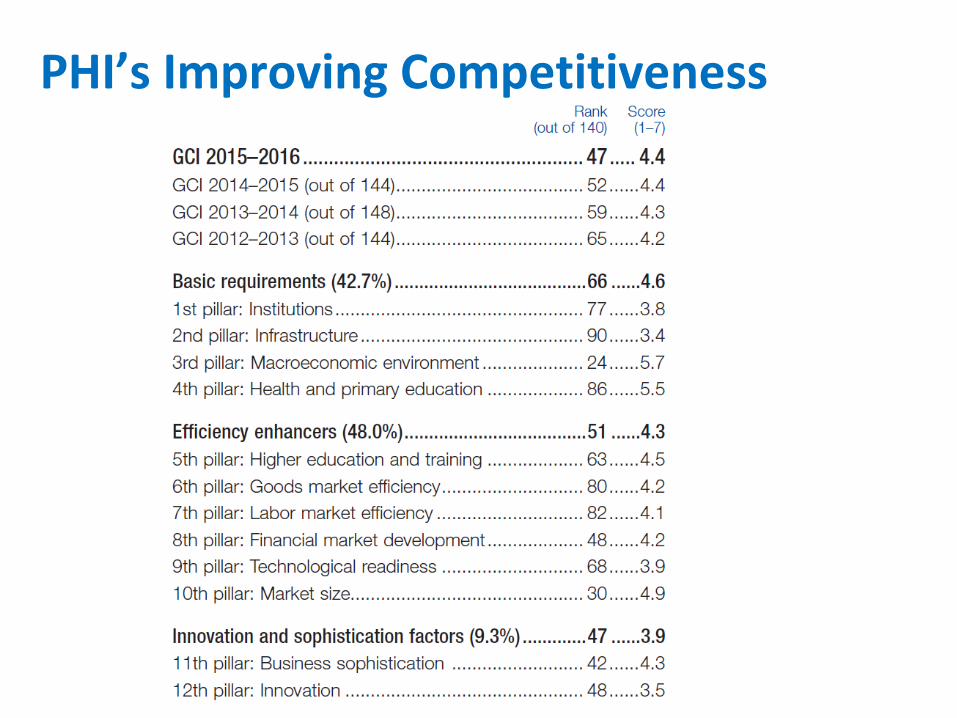

PHI’s Improving Competitiveness

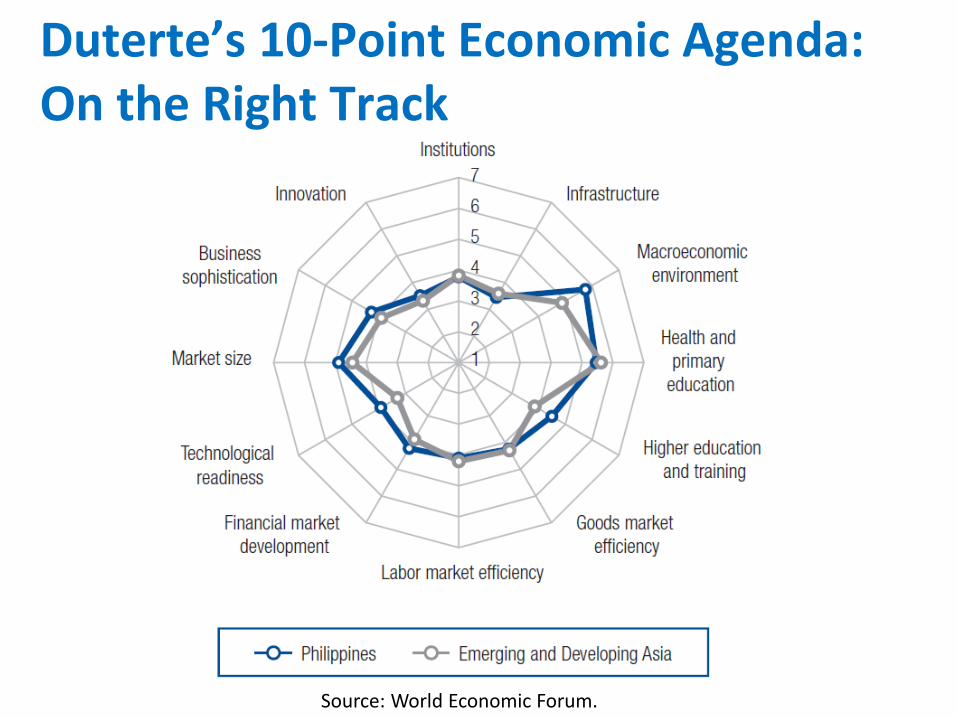

Duterte’s 10-Point Economic Agenda: On the Right Track

Source: World Economic Forum.

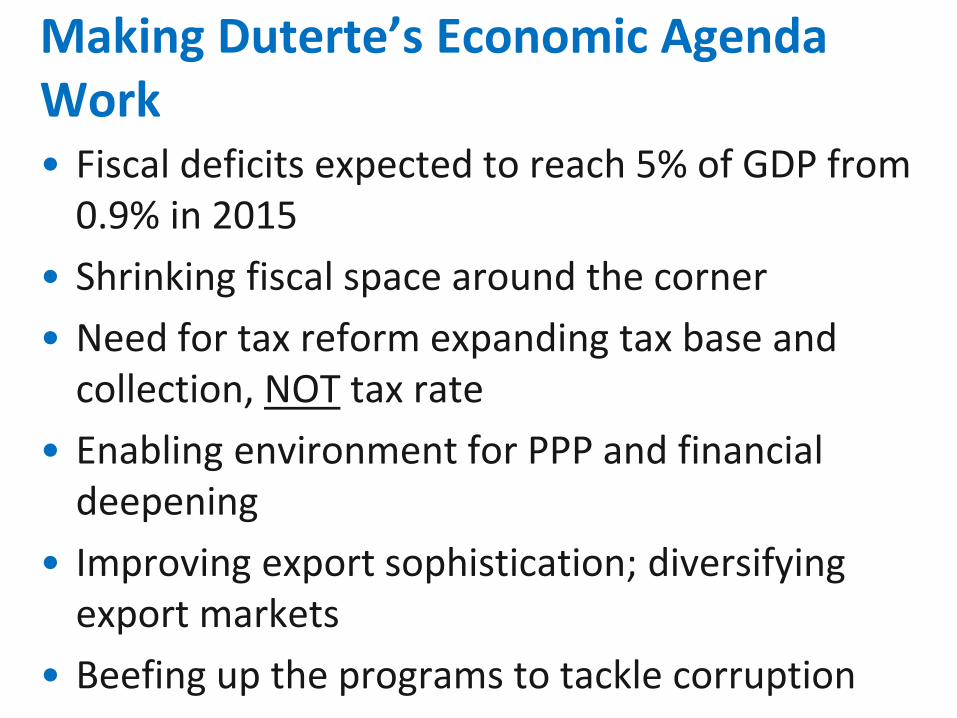

Making Duterte’s Economic Agenda Work • Fiscal deficits expected to reach 5% of GDP from

0.9% in 2015

• Shrinking fiscal space around the corner

• Need for tax reform expanding tax base and collection, NOT tax rate

• Enabling environment for PPP and financial deepening

• Improving export sophistication; diversifying export markets

• Beefing up the programs to tackle corruption

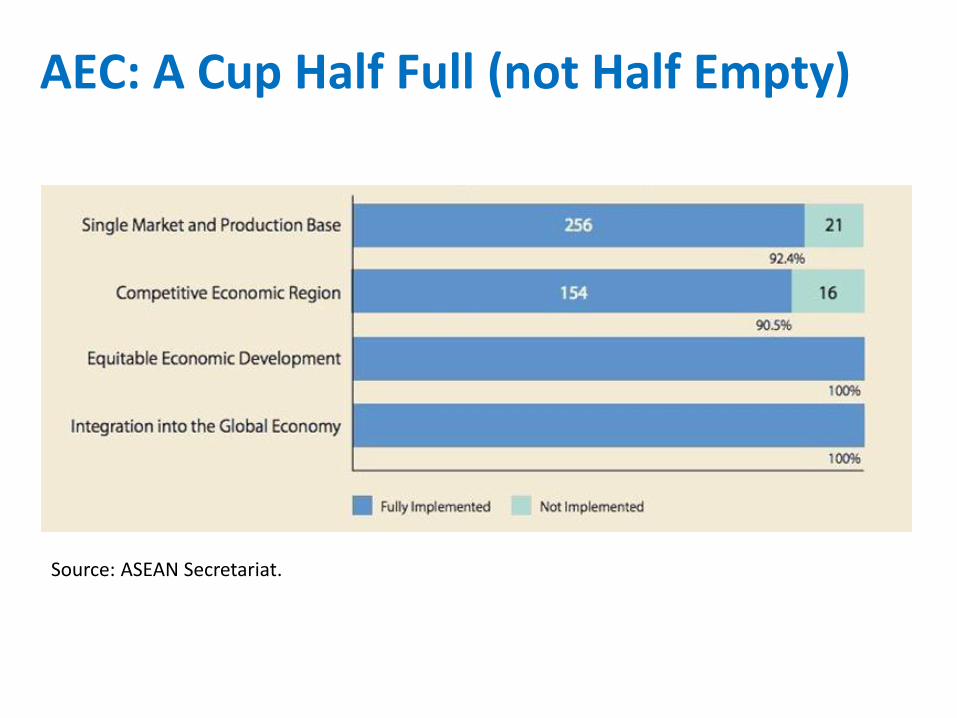

AEC: A Cup Half Full (not Half Empty)

Source: ASEAN Secretariat.

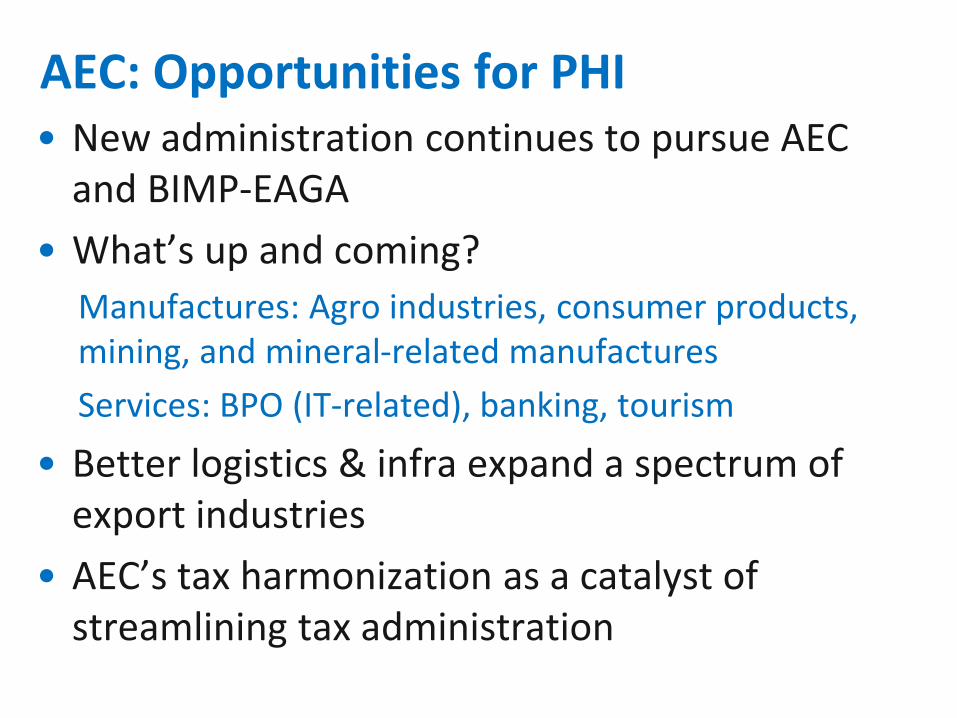

AEC: Opportunities for PHI • New administration continues to pursue AEC

and BIMP-EAGA

• What’s up and coming?

Manufactures: Agro industries, consumer products, mining, and mineral-related manufactures

Services: BPO (IT-related), banking, tourism

• Better logistics & infra expand a spectrum of export industries

• AEC’s tax harmonization as a catalyst of streamlining tax administration

For more information: [email protected]