Embed Size (px)

Citation preview

DIRECTORATE GENERAL FOR INTERNAL POLICIES

POLICY DEPARTMENT B: STRUCTURAL AND COHESION POLICIES

AGRICULTURE AND RURAL DEVELOPMENT

THE POULTRY AND EGG SECTORS:EVALUATION OF THE

CURRENT MARKETSITUATION AND

FUTURE PROSPECTS

STUDY

This document was requested by the European Parliament's Committee on [Regional Development].

AUTHOR(S)

Mr Conrad CaspariDr Edward OliverMr John NgangaMs Mariana Ricci

RESPONSIBLE ADMINISTRATOR

Mr Albeert MASSOTPolicy Department Structural and Cohesion PoliciesEuropean ParliamentB-1047 BrusselsE-mail: [email protected]

LINGUISTIC VERSIONS

Original: [EN]

ABOUT THE EDITOR

To contact the Policy Department or to subscribe to its monthly newsletter please write to:[email protected]

Manuscript completed in April 2010Brussels, © European Parliament, 2010

This document is available on the Internet at:http://www.europarl.europa.eu/studies

DISCLAIMER

The opinions expressed in this document are the sole responsibility of the author and do not necessarily represent the official position of the European Parliament.

Reproduction and translation for non-commercial purposes are authorized, provided the source is acknowledged and the publisher is given prior notice and sent a copy.

DIRECTORATE GENERAL FOR INTERNAL POLICIES

POLICY DEPARTMENT B: STRUCTURAL AND COHESION POLICIES

AGRICULTURE AND RURAL DEVELOPMENT

THE POULTRY AND EGG SECTORS:EVALUATION OF THE

CURRENT MARKETSITUATION AND

FUTURE PROSPECTS

STUDY

AbstractFont: Verdana 11, Dark Blue Max 80 wordsText should be between 30 and 80 words.

[IP/B/AGRI/IC2009-045 April 2010

PE XXX.YYY EN

THE POULTRY AND EGG SECTORS: EVALUATION OF THE CURRENT MARKET SITUATION AND FUTURE PROSPECTS____________________________________________________________________________________________

3

Contents

LIST OF ABBREVIATIONS ...................................................................................................................3

LIST OF TABLES.....................................................................................................................................3

LIST OF FIGURES ...................................................................................................................................3

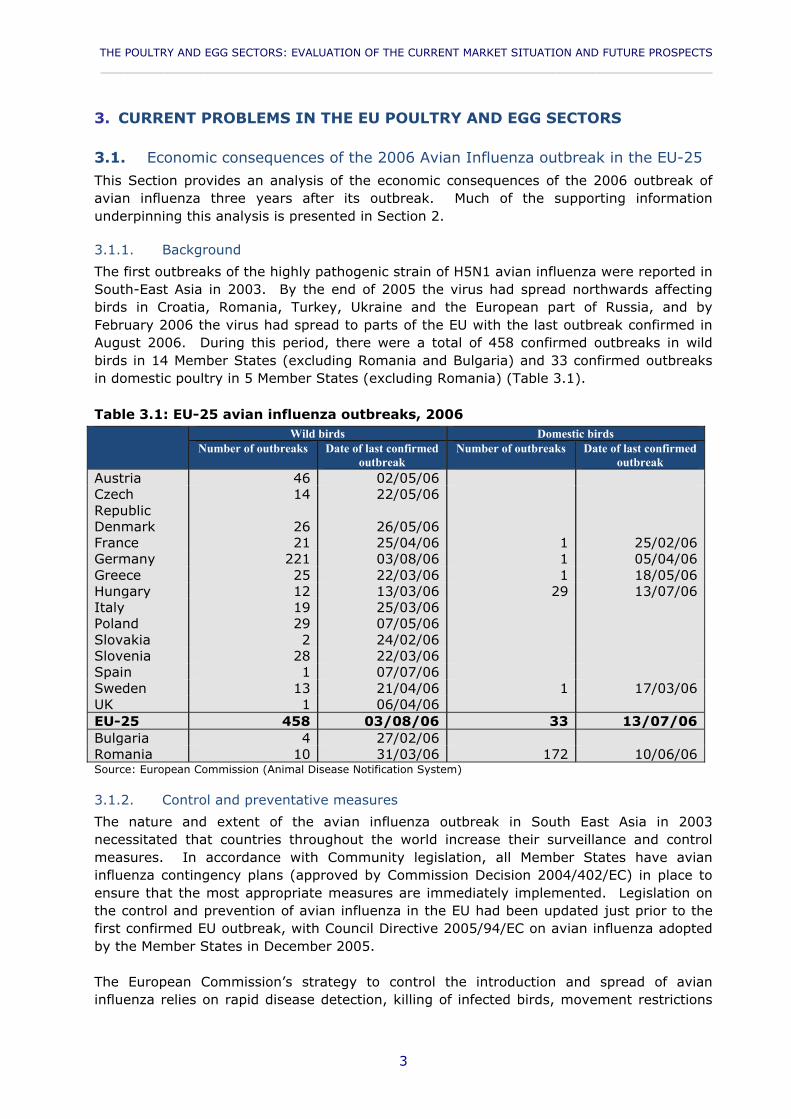

1. INTRODUCTION .....................................................................................................................3

1.1. Background...................................................................................................................................... 3

1.2. Objective of the report............................................................................................................... 4

1.3. Structure of the report............................................................................................................... 4

2. THE CURRENT SITUATION OF THE EU POULTRY MEAT AND EGG SECTOR..................................................................................................................................................3

2.1. Poultry meat.................................................................................................................................... 32.1.1. Production.................................................................................................................................................32.1.2. Consumption.............................................................................................................................................32.1.3. Trade .........................................................................................................................................................42.1.4. Employment..............................................................................................................................................62.1.5. Key driving factors.....................................................................................................................................8

2.2. Egg sector......................................................................................................................................... 82.2.1. Production.................................................................................................................................................82.2.2. Consumption.............................................................................................................................................92.2.3. Trade .......................................................................................................................................................112.2.4. Employment............................................................................................................................................15

2.3. The commercial structures used in the poultry meat and egg sectors.............. 32.3.1. Structure of the poultry meat production sector .....................................................................................32.3.2. Structure of the egg production sector.....................................................................................................62.3.3. Organisational structure ...........................................................................................................................8

2.4. Assessment of the common organisation for the poultry and egg markets ... 32.4.1. Background ...............................................................................................................................................32.4.2. Common organisation of the poultry meat market..................................................................................32.4.3. Common organisation of the egg market .................................................................................................5

3. CURRENT PROBLEMS IN THE EU POULTRY AND EGG SECTORS.......3

3.1. Economic consequences of the 2006 Avian Influenza outbreak in the EU-2533.1.1. Background ...............................................................................................................................................33.1.2. Control and preventative measures .........................................................................................................33.1.3. Economic impact.......................................................................................................................................43.1.4. EU financial measures to support the poultry meat and egg sectors .......................................................4

Policy Department B: Structural and Cohesion Policies____________________________________________________________________________________________

4

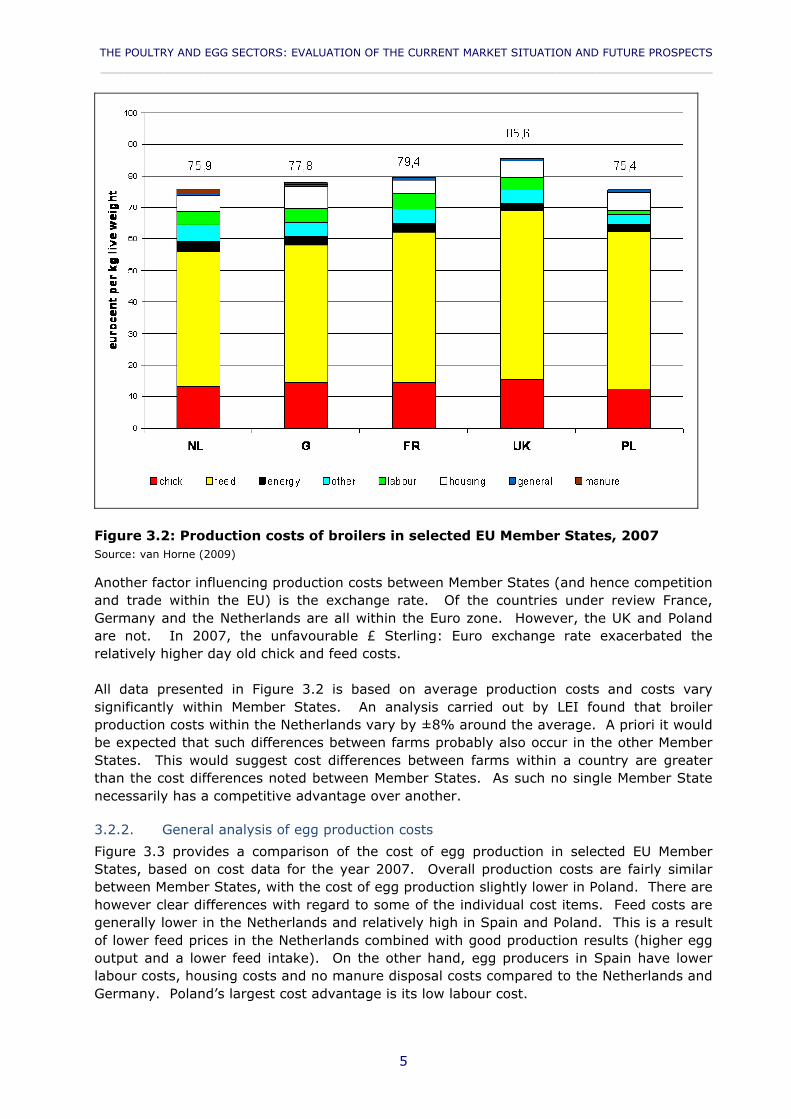

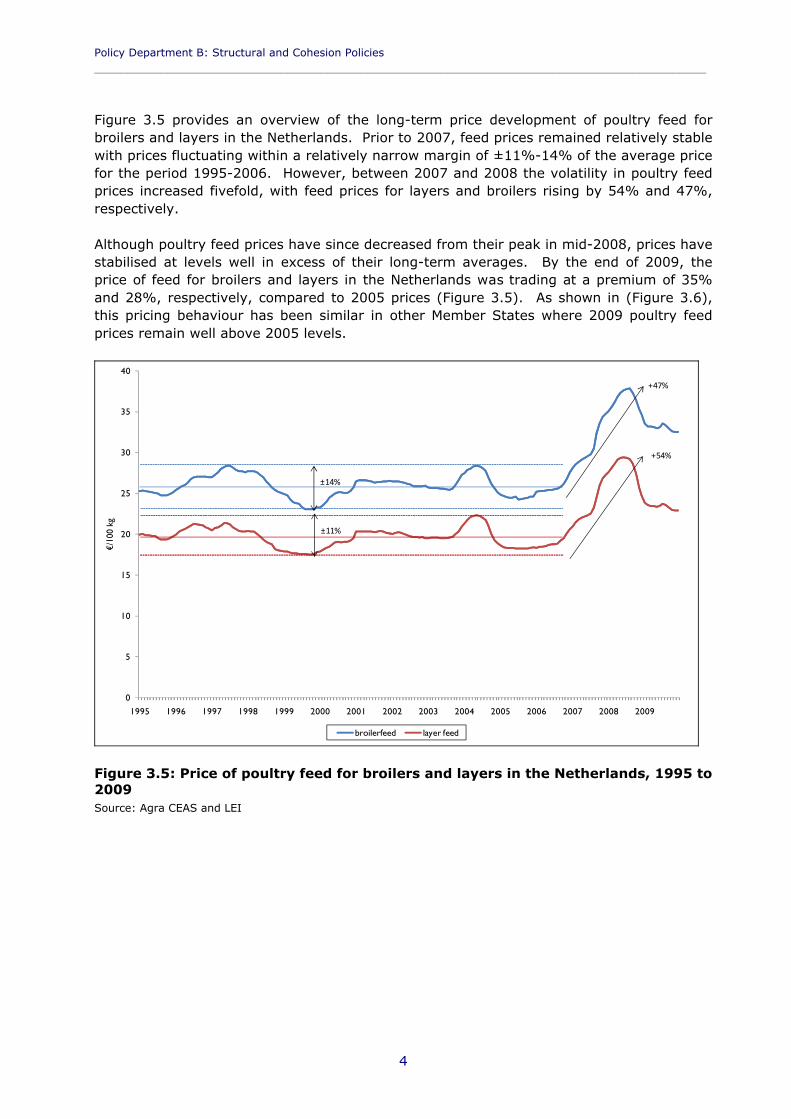

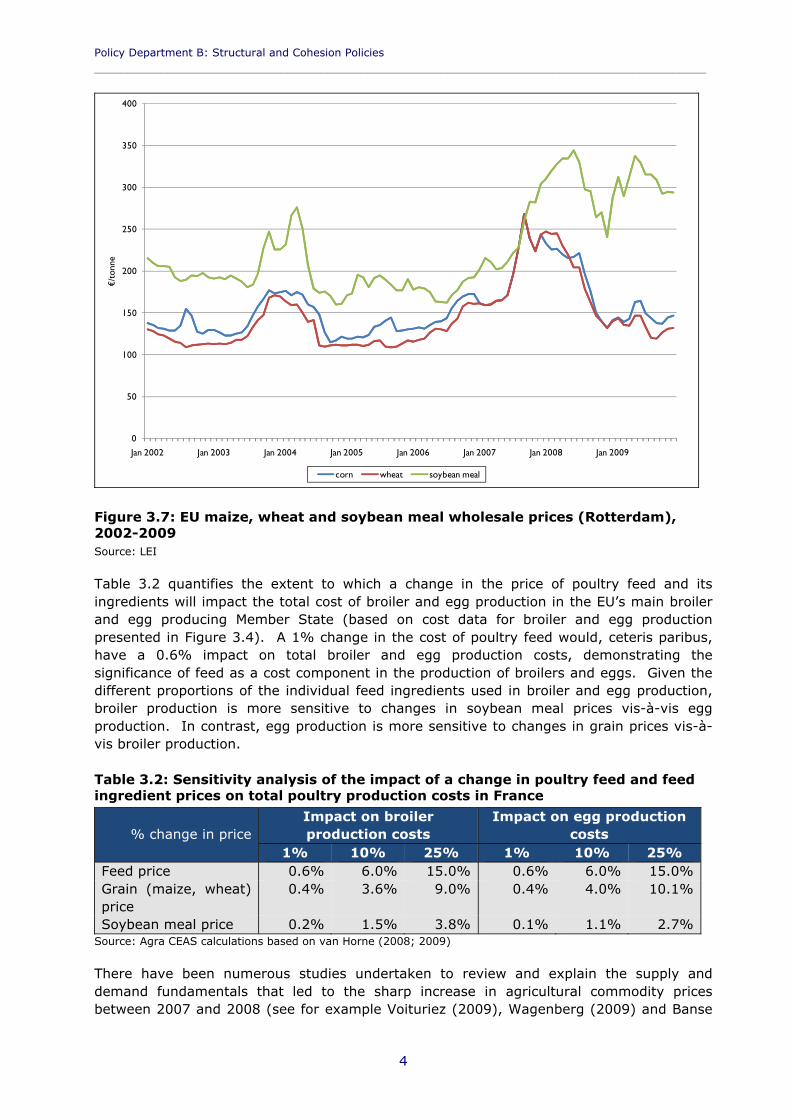

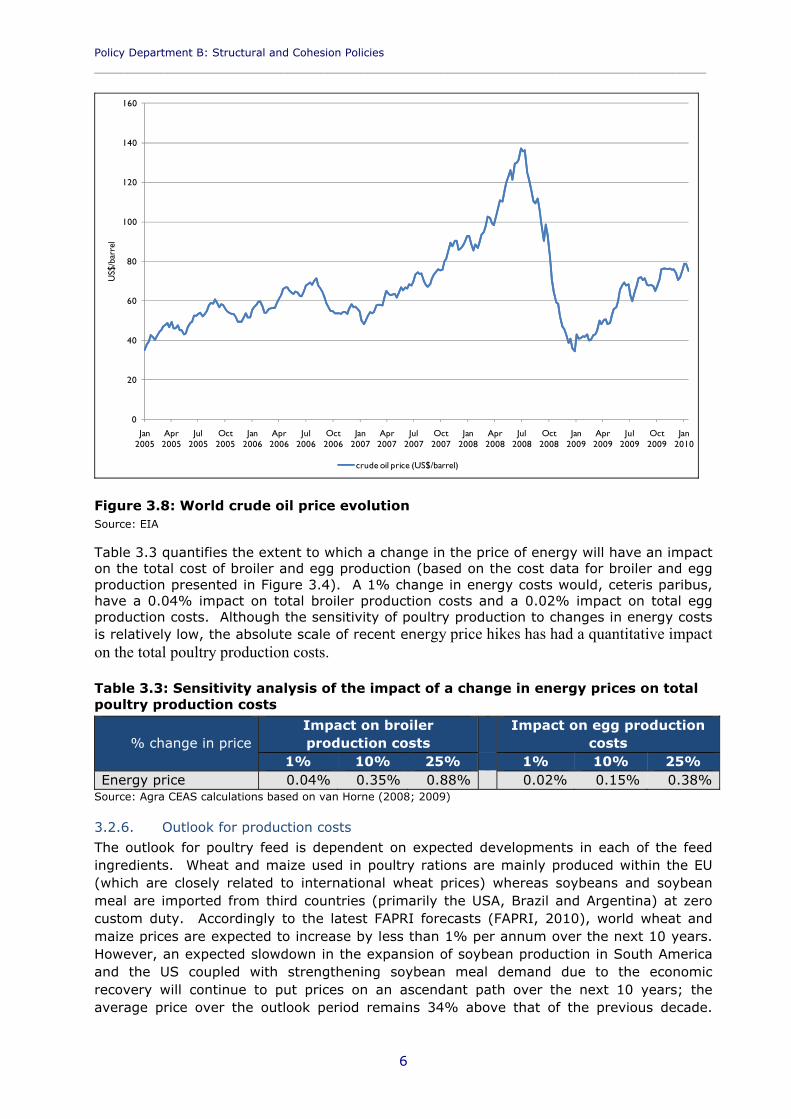

3.2. Evaluation of the effect of increasing input prices ...................................................... 43.2.1. General analysis of broiler production costs ............................................................................................43.2.2. General analysis of egg production costs .................................................................................................53.2.3. Comparison of broiler and egg production costs......................................................................................63.2.4. Analysis of feed costs ................................................................................................................................ 33.2.5. Analysis of energy costs ............................................................................................................................53.2.6. Outlook for production costs ....................................................................................................................6

4. IMPACT OF ANIMAL WELFARE LEGISLATION IN THE POULTRY AND EGG SECTORS.......................................................................................................................3

4.1. Background...................................................................................................................................... 3

4.2. Legislation........................................................................................................................................ 34.2.1. Chickens kept for meat production ..........................................................................................................44.2.2. Laying hens................................................................................................................................................44.2.3. EU welfare legislation and third country imports .....................................................................................5

4.3. Animal welfare legislation in third countries ................................................................. 6

4.4. Advantages and disadvantages of EU animal welfare legislation ........................ 64.4.1. Advantages................................................................................................................................................64.4.2. Disadvantages ...........................................................................................................................................7

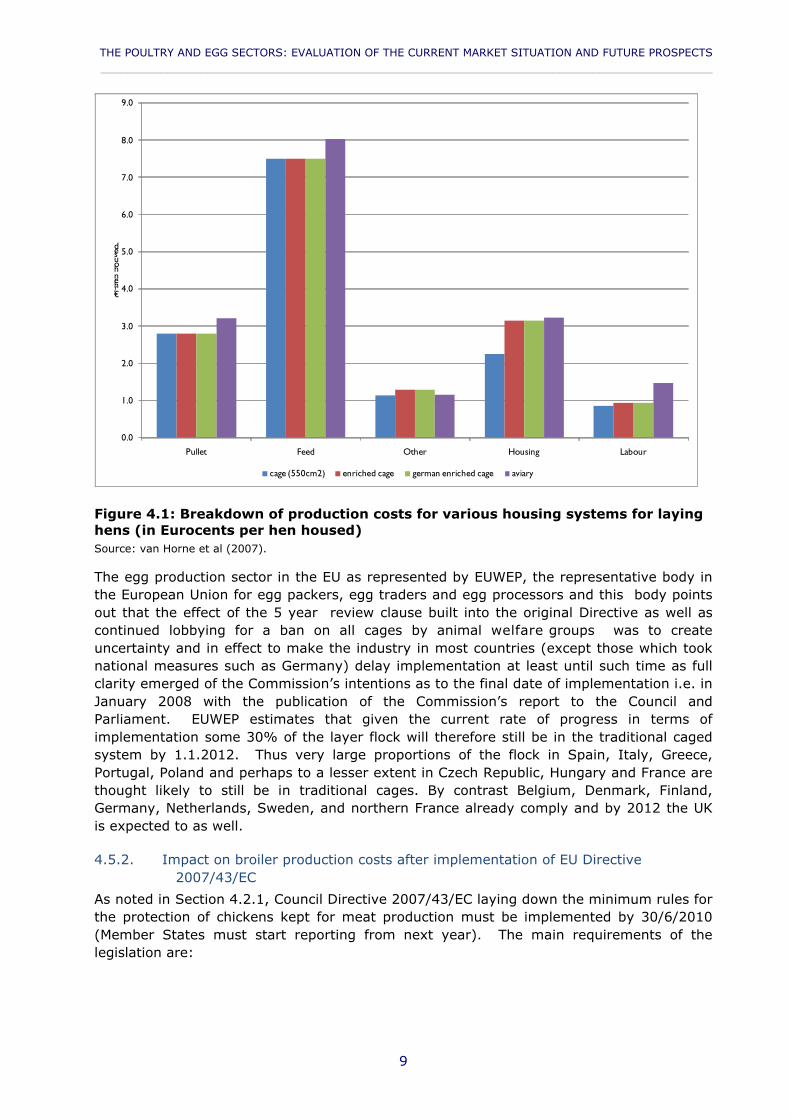

4.5. Impact of EU animal welfare legislation vis-à-vis third country production .. 74.5.1. Potential impact on egg production costs of EU Directive 99/74/EC .......................................................74.5.2. Impact on broiler production costs after implementation of EU Directive 2007/43/EC ..........................94.5.3. EU’s competitive position on the world egg market...............................................................................114.5.4. EU’s competitive position on the world poultry meat market ...............................................................19

4.6. EU support for compliance with animal welfare legislation.................................. 21

4.7. The outlook for animal welfare legislation in the EU................................................ 21

5. CONCLUSIONS AND RECOMMENDATIONS........................................................3

6. REFERENCES.............................................................................................................................3

7. ANNEX 1: LAYER INDUSTRY IN THE USA, BRAZIL, ARGENTINA AND INDIA .........................................................................................................................................3

7.1. USA ...................................................................................................................................................... 3

7.2. Brazil ................................................................................................................................................... 3

7.3. India.................................................................................................................................................... 3

7.4. Argentina .......................................................................................................................................... 4

THE POULTRY AND EGG SECTORS: EVALUATION OF THE CURRENT MARKET SITUATION AND FUTURE PROSPECTS____________________________________________________________________________________________

3

LIST OF ABBREVIATIONS

AGRI Agriculture and Rural Development Committee

ALDE Group of the Alliance of Liberals and Democrats for Europe

BAS Brake-assist systems

CAP Common Agricultural Policy

CFP Common Fisheries Policy

CMO Common market organisation

CoR Committee of the Regions

CULT Culture and Education Committee

ECOSOC Economic and Social Committee

ECTS European Credit Transfer System

EPP-ED Group of the European People's Party and European Democrats

FAO Food and Agriculture Organisation of the United Nations

FPS Frontal protection systems

GDP Gross Domestic Product

GM Genetically-modified

Greens/EFA Greens/European Free Alliance

GUE/NGL Confederal Group of the European United Left - Nordic Green Left

IFI International Fund for Ireland

IND/DEM Independence/Democracy Group

THE POULTRY AND EGG SECTORS: EVALUATION OF THE CURRENT MARKET SITUATION AND FUTURE PROSPECTS____________________________________________________________________________________________

3

LIST OF TABLES

Table 2 1: Self-sufficiency rate in selected EU Member States, 2009 ............................... 3Table 2 2: Poultry meat production and processing sector employment, number of

enterprises and turnover by EU Member State in 2007 ........................................... 7Table 2 3: Self sufficiency in egg production in selected EU Member States, 2008 ...........12Table 2 4: Major EU egg importers, 2008 (tonnes).......................................................12Table 2 5: EU-27 countries with high egg self sufficiency levels, 2008............................14Table 2 6: Major egg exporters in the EU, 2008 (tonnes)..............................................14Table 2.7: Strengths and weaknesses of integrated production ...................................... 5Table 2.8: Strengths and weaknesses of non-integrated production ................................ 6Table 3.1: EU-25 avian influenza outbreaks, 2006 3Table 3.2: Sensitivity analysis of the impact of a change in poultry feed and feed ingredient

prices on total poultry production costs in France................................................... 4Table 3.3: Sensitivity analysis of the impact of a change in energy prices on total poultry

production costs ................................................................................................ 6Table 4.1: Current European legislation on animal welfare relevant for egg and poultry sectors

3Table 4.2: Maximum stocking densities for broilers in selected EU Member States, 2006 ..10Table 4.3: Production costs at different stocking densities ............................................11

LIST OF FIGURESFigure 2.1: Major EU poultry producers, 2008 .............................................................. 3Figure 2.2: Evolution of poultry production in the EU-15 and EU-27, 1996 – 2009 (‘000

tonnes) ............................................................................................................ 42.3: Production (‘000 tonnes) and self-sufficiency levels (%) in the European Union, 1995 –

2009 ................................................................................................................ 3Figure 2.4: Total (‘000 tonnes) and per capita (kg/head) poultrymeat consumption in the

EU, 1995 – 2009................................................................................................ 4Figure 2.5: EU poultry imports from third countries, 2005 – 2009 (tonnes)...................... 3Figure 2.6: Main third countries exporters of poultrymeat to the EU, 2009 (%) ................ 4Figure 2.7: Main destinations for extra-EU exports of poultrymeat, 2008 (%) .................. 5Figure 2.8: Extra-EU 27 exports of poultrymeat, 2000 – 2009 (‘000 tonnes).................... 6Figure 2.9: EU-27 egg production share by country, 2009 ............................................. 8Figure 2.10: Egg production (‘000 tonnes) and self-sufficiency levels (%) in the EU, 1998 –

2009 ................................................................................................................ 9Figure 2.11: Egg consumption per capita in the EU, 1998 – 2009 (kg/head) ...................10Figure 2.12: EU egg consumption, 1998 – 2009 (‘000 tonnes) ......................................11Figure 2.13: Imports of egg to the EU-27 (Intra and Extra), 1999 – 2009 ......................13Figure 2.14: Volume and value of EU -27 egg exports (intra- and extra-EU), 1999 – 200915Figure 2.15: Family farm income development in the Netherlands on broiler farms,

1992/1993-2009, (Euro/ farm)............................................................................ 4Figure 2.16: Farm income of broiler farms (in Euros per year) in the Netherlands (free

market) and France (integrated) in the period 2001 to 2008 ................................... 5Figure 2.17: EU laying hens by system of production, 2009 (%)..................................... 7Figure 2.18: Percentage of layers kept in different housing systems in 17 EU Member

States, 2008 ..................................................................................................... 8Figure 2.19: Intervention logic: Poultry meat CMO ....................................................... 4Figure 2.20: Intervention logic: Eggs CMO................................................................... 6

Figure 3.1: Immediate impact of avian influenza on EU poultry meat and egg consumption3Figure 3.2: Production costs of broilers in selected EU Member States, 2007.................... 5

Policy Department B: Structural and Cohesion Policies____________________________________________________________________________________________

4

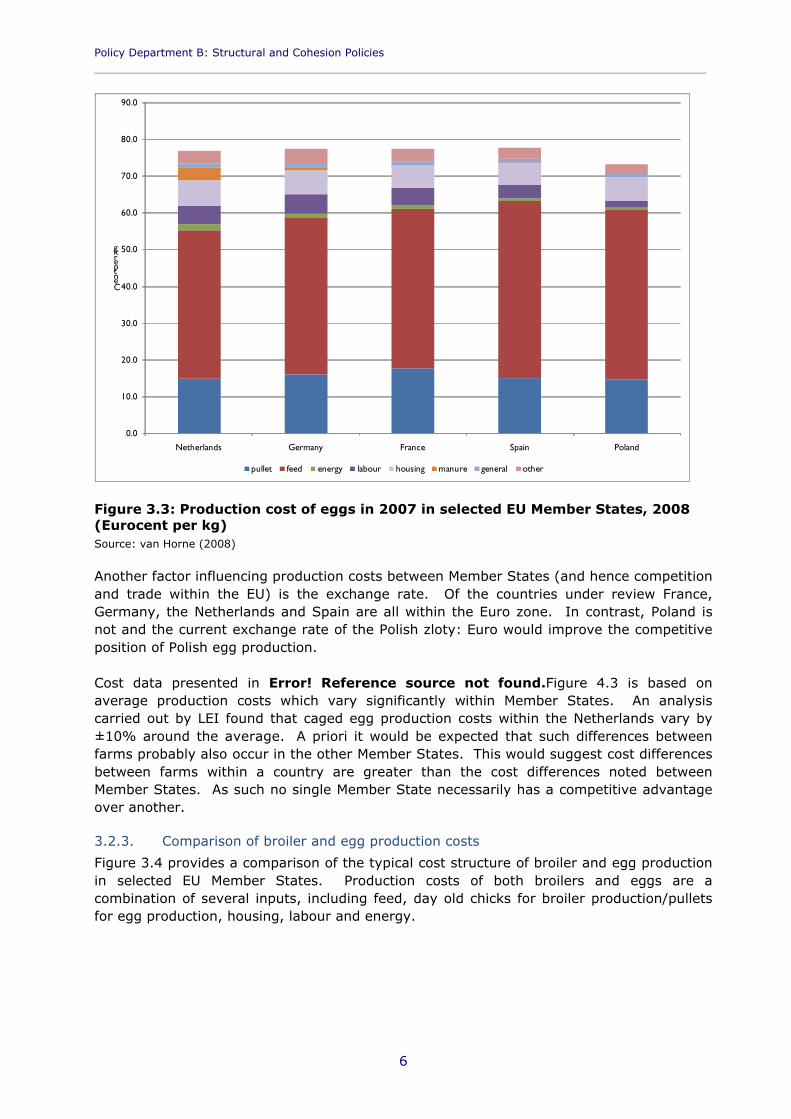

Figure 3.3: Production cost of eggs in 2007 in selected EU Member States, 2008 (Eurocent per kg) ............................................................................................................. 6

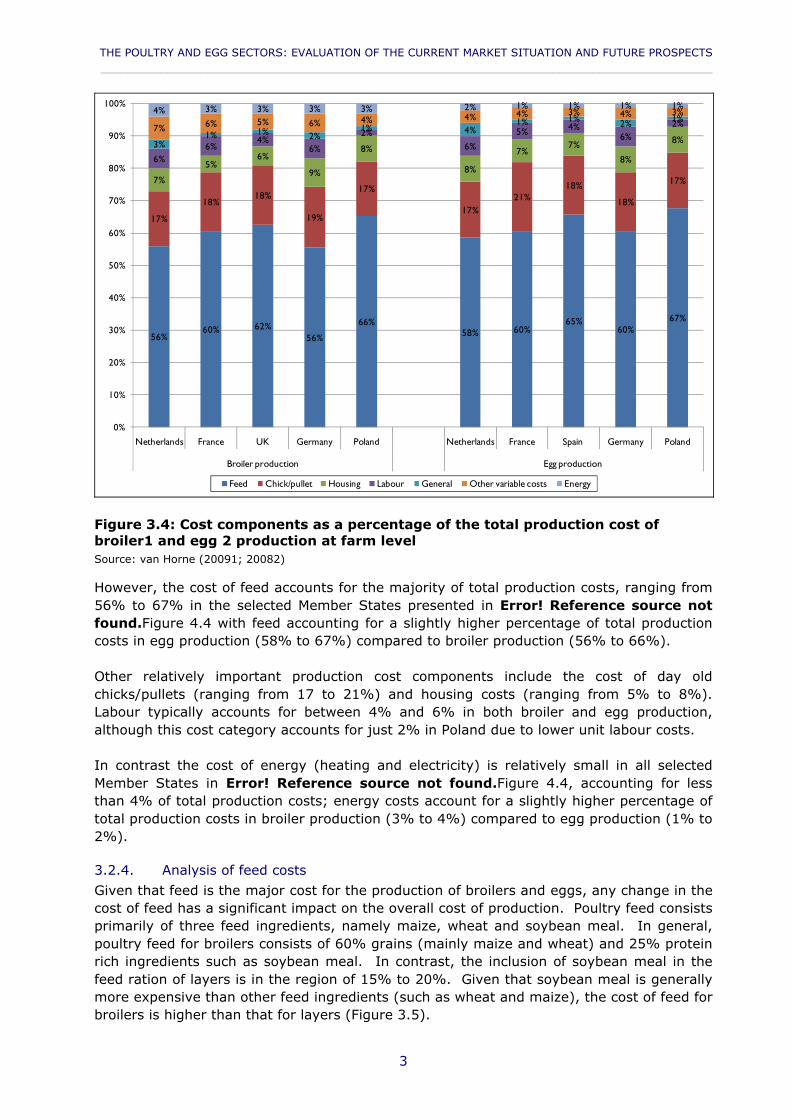

Figure 3.4: Cost components as a percentage of the total production cost of broiler1 and egg2 production at farm level.............................................................................. 3

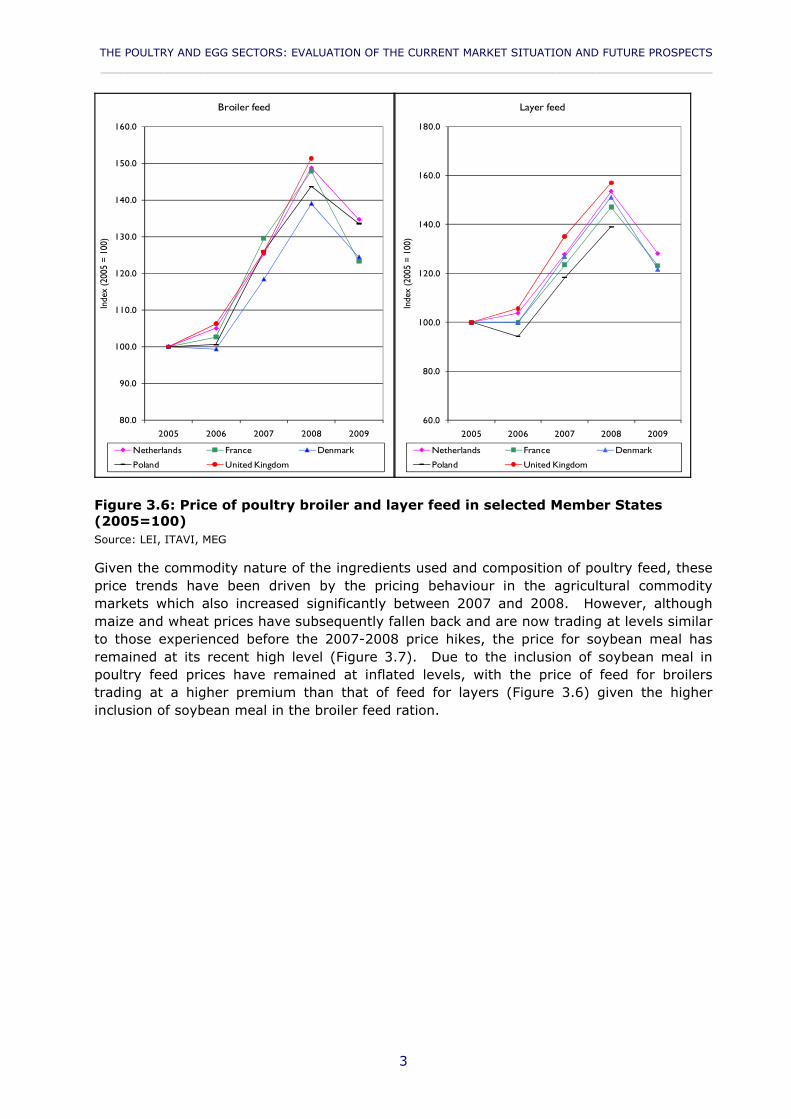

Figure 3.5: Price of poultry feed for broilers and layers in the Netherlands, 1995 to 2009.. 4Figure 3.6: Price of poultry broiler and layer feed in selected Member States (2005=100) . 3Figure 3.7: EU maize, wheat and soybean meal wholesale prices (Rotterdam), 2002-2009 4Figure 3.8: World crude oil price evolution................................................................... 6

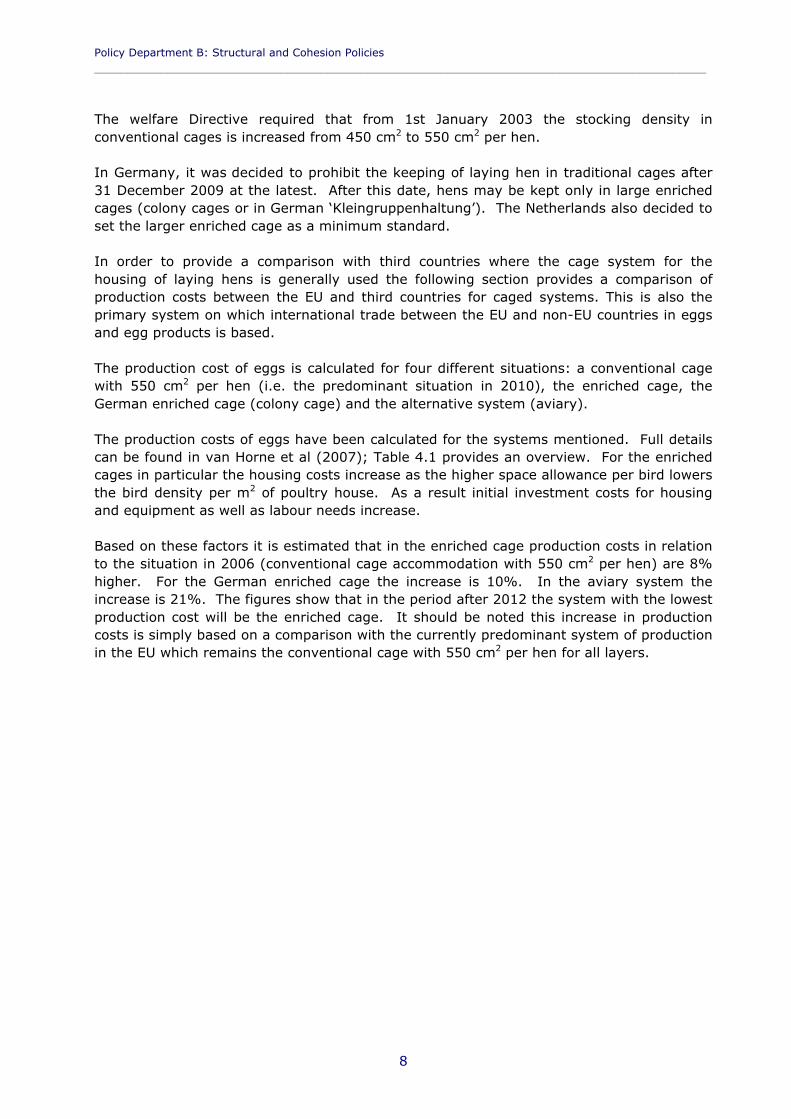

Figure 4.1: Breakdown of production costs for various housing systems for laying hens (in Eurocents per hen housed) ................................................................................. 9

Figure 4.2: Production costs for eggs in the EU and selected third countries, 2008 (Eurocent per kg) ............................................................................................................12

Figure 4.3: Offer price of shell eggs in Germany from EU and non-EU countries 2008, (Eurocents per kg shell eggs) .............................................................................13

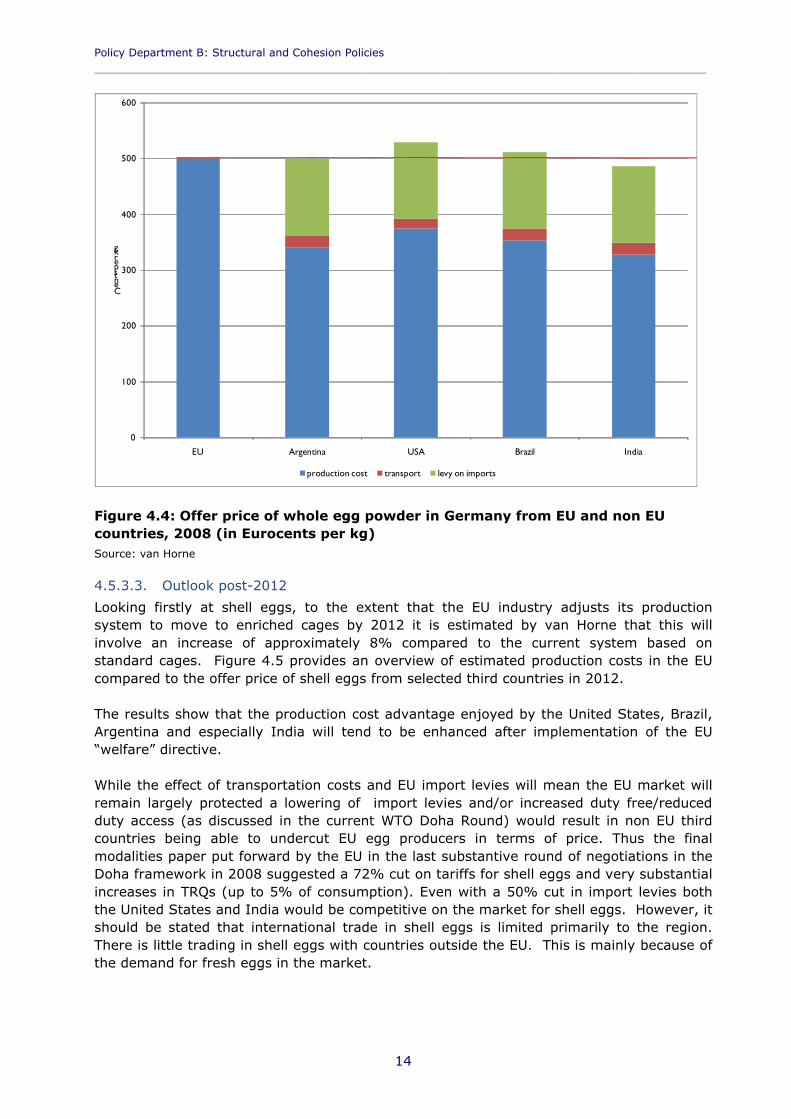

Figure 4.4: Offer price of whole egg powder in Germany from EU and non EU countries, 2008 (in Eurocents per kg), ...............................................................................14

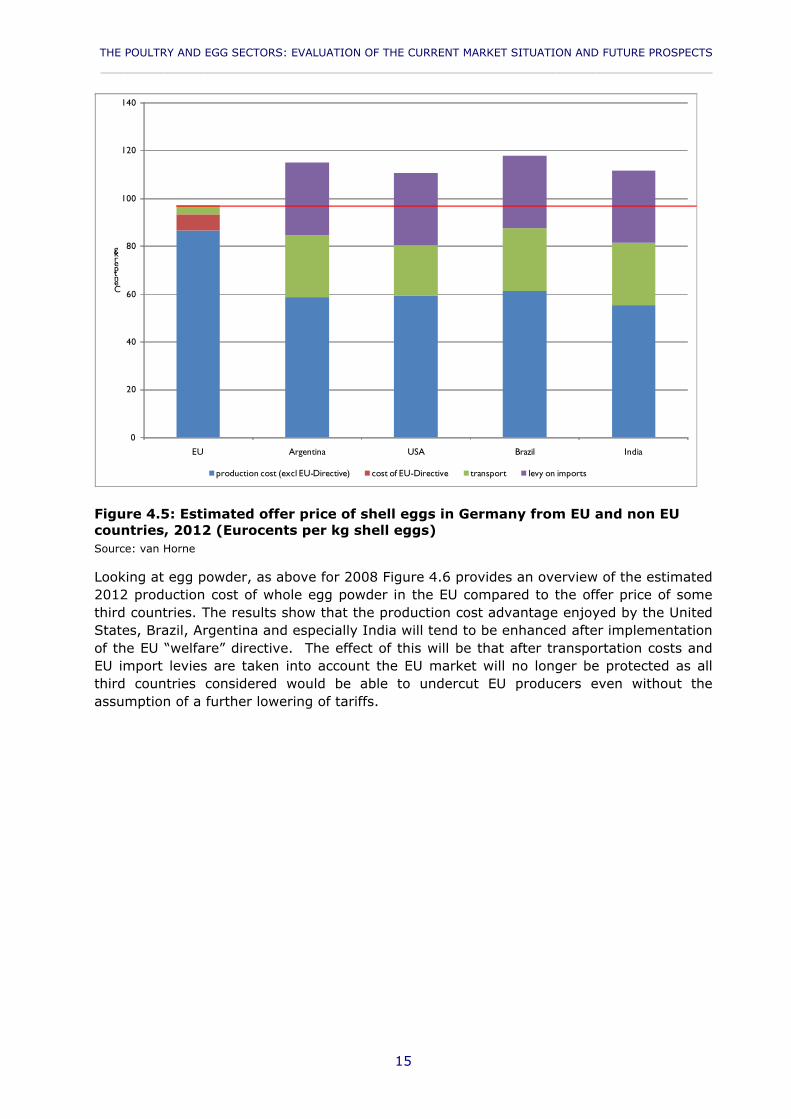

Figure 4.5: Estimated offer price of shell eggs in Germany from EU and non EU countries, 2012 (Eurocents per kg shell eggs) .....................................................................15

Figure 4.6: Estimated offer price of whole egg powder in EU (average of selected countries) and selected third countries, 2012, (in Eurocents per kilogram)..............................16

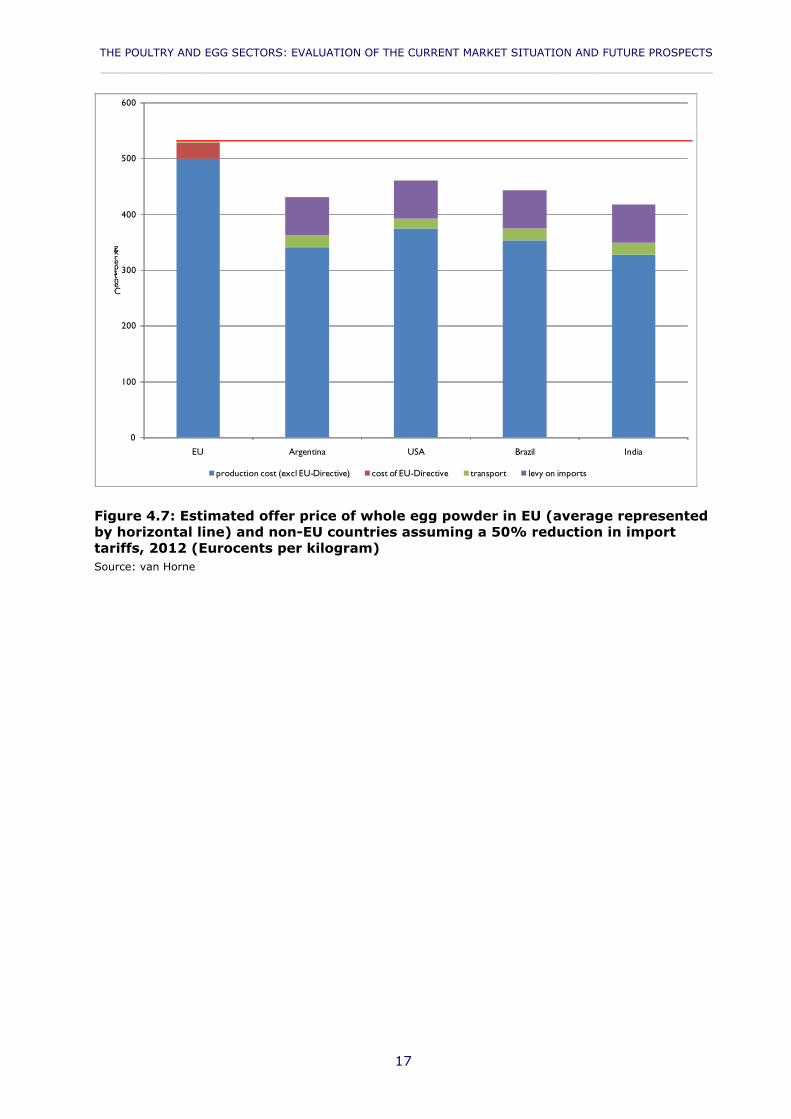

Figure 4.7: Estimated offer price of whole egg powder in EU (average represented by horizontal line) and non-EU countries assuming a 50% reduction in import tariffs, 2012 (Eurocents per kilogram) ...................................................................................17

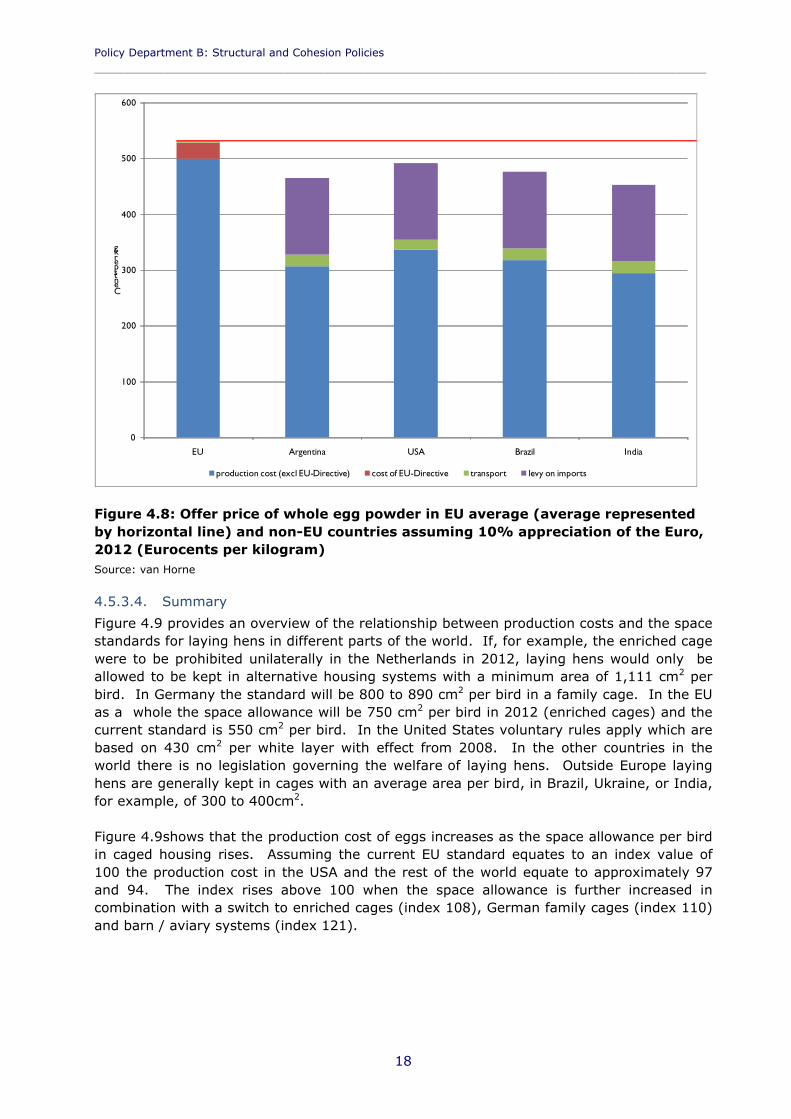

Figure 4.8: Offer price of whole egg powder in EU average (average represented by horizontal line) and non-EU countries assuming 10% appreciation of the Euro, 2012 (Eurocents per kilogram) ...................................................................................18

Figure 4.9: Relationship between costs for animal welfare (wide bar; cost index on left-hand axis) and the area per laying hen (small bar; space allowance per hen in cm2 on right-hand axis)................................................................................................19

Figure 4.10: EU and third country broiler production and slaughter costs, 2007...............20

THE POULTRY AND EGG SECTORS: EVALUATION OF THE CURRENT MARKET SITUATION AND FUTURE PROSPECTS____________________________________________________________________________________________

3

1. INTRODUCTION

1.1. Background

The terms of reference make clear that not only is the poultry meat sector the fastest growing meat production sector globally, this sector is also most likely to provide low price animal protein, especially in middle and low-income countries.

Poultry sectors in the developed world are highly integrated and benefit from considerable economies of scale and advanced technology. Pressure for further consolidation strengthens the trend toward intensification both here and in developing countries.

The EU egg and poultry sector is an important contributor to overall EU agricultural output accounting for 6.3 % of EU agricultural output (2006) with a value of some Euro 23.3 billion in 2007 and is one of the most intensive farming systems in the EU. However, the EU is losing international market share to Brazil as a result of currency movements and high domestic production costs and became a net importer of poultry meat for the first time in 20071 as domestic consumption continued to increase. In addition, and as noted in the terms of reference, Brazilian poultry exporters have recently purchased several European poultry processors guaranteeing commercial outlets for Brazilian products in the EU2.

Whilst global egg production has increased dramatically over the 25 years, the EU share of total production has decreased. The terms of reference note that China has increased its share of world production substantially while production in the USA and the Russian Federation has declined. The increase in production and share of world production in Mexico, India and Brazil was also noted. Whilst a proportion of the growth in egg production in these countries is likely to have met increasing domestic demand, increases in the production of, and trade in, egg products have taken place. Egg production in the EU has risen since the mid 1990s but has not matched rising demand and there has therefore been a decline in self sufficiency levels.

The EU poultry and egg regimes are “light” with export refunds and import tariffs being the only forms of support under Council Regulation (EC) No 1234/2007 and Commission Regulation 589/2008. Public support can be provided to assist the modernisation of egg packing stations and slaughtering plants, but not to increase production capacity. The sectors are also affected by a number of pieces of EU legislation with relevance to food safety, public and animal health, trade and marketing standards for poultry meat and eggs.

Animal welfare legislation in the poultry sector covers production, transport and slaughter. Additionally, Directive 2007/43/EC sets out, with effect from July 2010, minimum standards for the welfare of broiler chickens on farm. The main provision of the Directive is to reduce the stocking density of broiler chickens by setting a maximum stocking density.

Animal welfare legislation regarding laying hens will lead to a ban on traditional battery cages by 20123, although production in enriched cages will still be allowed.

1 European Commission DG AGRI Agricultural Situation Report 2008, Brussels 20092 USDA, Foreign Agricultural Service 3/08.3 Council Directive 1999/74/EC.

Policy Department B: Structural and Cohesion Policies____________________________________________________________________________________________

4

The EU poultry and egg sectors have also been affected by Avian Influenza outbreaks, most notably in 2006, and large increases in input prices from 2007 which reversed a long-termdownward trend. These increases resulted from a mixture of structural and temporary factors ranging from general global population growth to adverse weather conditions and exchange rate movements. Increasing demand from the ethanol industry in the US, Europe and China for in corn and other cereal grains has also had an impact. Although prices fell back from April 2008, the underlying structural pressures remain.

EU poultry production is also affected by animal welfare legislation and the terms of reference notes that several calculations show that the implementation of these Directives would lead to dramatic reductions in terms of farm income. Such a reduction could have further consequences for both employers and employees in the poultry chain.

1.2. Objective of the report

Against this background, the European Parliament’s Committee on Agriculture and Rural Development appointed Agra CEAS Consulting, in conjunction with LEI - Wageningen University and Research Centre in the Netherlands and the Institut Technique de l'Aviculture (ITAVI) in France to carry out an evaluation of the current market situation and future prospects in the poultry and egg sectors. The specific objectives of this research are thus to carry out:

an analysis of the current situation of the European Poultry meat and egg sectors and comparison with the world situation;

an analysis of the consequences of avian influenza three years after the epidemic outbreak;

evaluation of the effect of the increase in input prices; and, impact of the European legislation on the poultry welfare to the increase of the

cost of production and the consequent weakening of the competitiveness of the European poultry meat and egg sectors.

1.3. Structure of the report

Chapter 2 sets out the current situation in the EU poultry meat and egg sectors. This includes a review of the current situation in the EU-27, an analysis of the commercial structures used in the two sectors and an assessment of the common organisation for the poultry and egg markets.

Chapter 3 sets out the current problems in the EU poultry and egg sectors including an analysis of the economic consequences of the 2006 Avian Influenza outbreak, as assessment of the impact of increasing input prices and a review of EU financial measures to support the poultry meat and egg sectors.

Chapter 4 focuses on the impact of animal welfare legislation in the poultry and egg sectors through a discussion on the advantages and disadvantages of EU animal welfare legislation and the impact of this legislation vis-à-vis Third Country production.

Chapter 5 presents our conclusions and recommendations in terms of the drivers of future policy, concrete policy proposals and recommendations to mitigate the cost impact of animal welfare measures.

THE POULTRY AND EGG SECTORS: EVALUATION OF THE CURRENT MARKET SITUATION AND FUTURE PROSPECTS____________________________________________________________________________________________

3

2. THE CURRENT SITUATION OF THE EU POULTRY MEAT AND EGG SECTOR

2.1. Poultry meat

2.1.1. Production

Total EU poultrymeat production is currently 8.5 million tonn4es mostly coming from France, the UK, Germany, Spain and Italy. France is responsible for most of EU’s total production, accounting for 1.7 million tonnes (15.8%), followed by the UK (1.4 million tonnes, 13.2%) and Germany (1.3 million tonnes, 12%). It is important to note that 78% of total EU poultry production comes from EU-15.

Belgium/Luxembourg2.3%

Germany12%

Spain10%

France15.8%

Italy9.4%

Hungary3.7%

Netherlands6.2%

Poland9.5%

Portugal2.7%

Romania2.9%

UK13.2%

Others12.1%

Figure 2.1: Major EU poultry producers, 2008

In terms of the evolution of total EU 15 poultrymeat production between 1996 and 1999 there was a slow (but continuous) growth in output as poultry market demand rose with per capita consumption rising on average 1kg per year (average EU-15). In 1999 due to problems with food scares, cutbacks in production in France, and avian influenza in Italy production decreased by 2%. In 2001 and 2002, production again rose by 3.2% reaching a total of over 9 million tonnes in the EU-15 partly as a as a result of the foot and mouth crisis during which consumers switched from beef to poultry. In 2003 the EU poultry market faced its first major avian influenza impacts with production cuts in France, Italy and Sweden. Mild outbreaks in Belgium and the Netherlands also contributed to a decrease in production of 3.3% in the EU-25 and 4.5% in the EU-15. In some countries including France, Netherlands and Belgium, production has still not returned to pre-2003 levels.

4 According to 2009 AVEC report

Policy Department B: Structural and Cohesion Policies____________________________________________________________________________________________

4

8,000

8,500

9,000

9,500

10,000

10,500

11,000

11,500

12,000

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Poultryproduction('000tonnes)

EU-27 EU-15

Figure 2.2: Evolution of poultry production in the EU-15 and EU-27, 1996 – 2009 (‘000 tonnes)Source: European Commission

The accession of 10 new Member States to the EU increased total production by 19% to a total of 10.7 million tonnes. In 2005 a sharp reported increase in production in Poland, was the main reason a sharp rise in overall EU-27 production.

In 2006, avian influenza occurred was found in wild birds and there were a limited number of outbreaks in domestic flocks and while these did not substantially disrupt production –production fell by 2.5% mostly in the EU-15 –the outbreak led to a loss of confidence amongst producers (see Section 3). Production recovered to reach 11.5 million tonnes in EU-27 in 2007 with poultry prices increasing 9.9% due to short supply. The accession of Bulgaria and Romania in this year added an extra 400,000 tonnes to total EU output. Since 2007 production has remained more or less stable at this level.

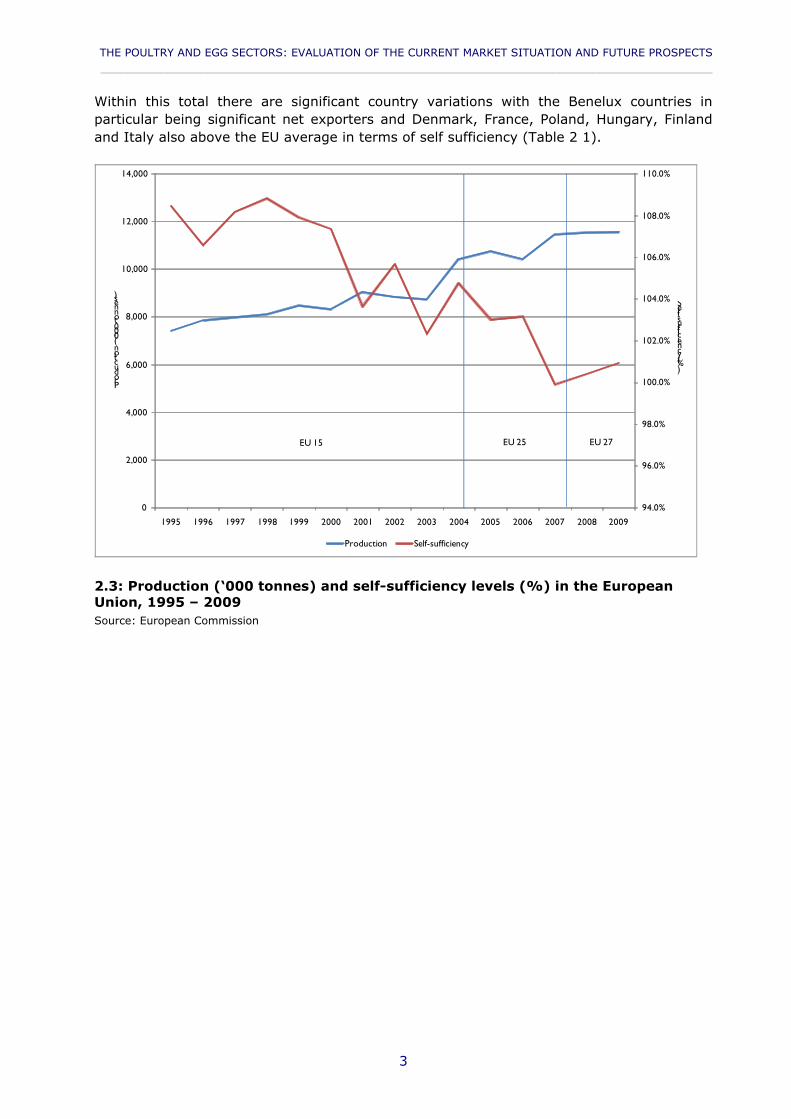

While overall EU production levels have on average been rising since the mid- 1990s, self-sufficiency levels have fallen particularly following the recent enlargements of the EU. As Figure 2.3 shows, the level of self-sufficiency in the EU has steadily decreased from 108.5% in 1995 to 100.9% in 2009

THE POULTRY AND EGG SECTORS: EVALUATION OF THE CURRENT MARKET SITUATION AND FUTURE PROSPECTS____________________________________________________________________________________________

3

Within this total there are significant country variations with the Benelux countries in particular being significant net exporters and Denmark, France, Poland, Hungary, Finland and Italy also above the EU average in terms of self sufficiency (Table 2 1).

94.0%

96.0%

98.0%

100.0%

102.0%

104.0%

106.0%

108.0%

110.0%

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Self-sufficiency(%)

Production('000tonnes)

Production Self-sufficiency

EU 15 EU 25 EU 27

2.3: Production (‘000 tonnes) and self-sufficiency levels (%) in the European Union, 1995 – 2009Source: European Commission

THE POULTRY AND EGG SECTORS: EVALUATION OF THE CURRENT MARKET SITUATION AND FUTURE PROSPECTS____________________________________________________________________________________________

3

Table 2 1: Self-sufficiency rate in selected EU Member States, 2009Member State Self-sufficiency rate

Austria 80%Belgium / Luxembourg 165%Denmark 145%Finland 105%France 120%Germany 87%Greece 79%Ireland 85%Italy 106%Netherlands 188%Portugal 93%Spain 96%Sweden 85%United Kingdom 98%Czech Republic 84%Hungary 124%Latvia 49%Lithuania 80%Poland 118%Slovak Republic 83%

Source: AVEC Annual Report, 2009.Note: Data not available for all Member States

According to one interviewee, the ability to sell all cuts (including lower value ones) and the ability to obtain higher margins on premium products have a significant effect on production in the EU. Currently it is possible for producers to sell all poultry cuts including the low value products. However, if production were to increase to a level that the EU obtained self-sufficiency in poultry breast meat, it is possible that there would be a surplus of low value products, and that it would not be possible to sell all cuts. With respect to premia, there are some premium poultry products such as Label Rouge in France, however quality labels do not play as great a role as in some other livestock industries.

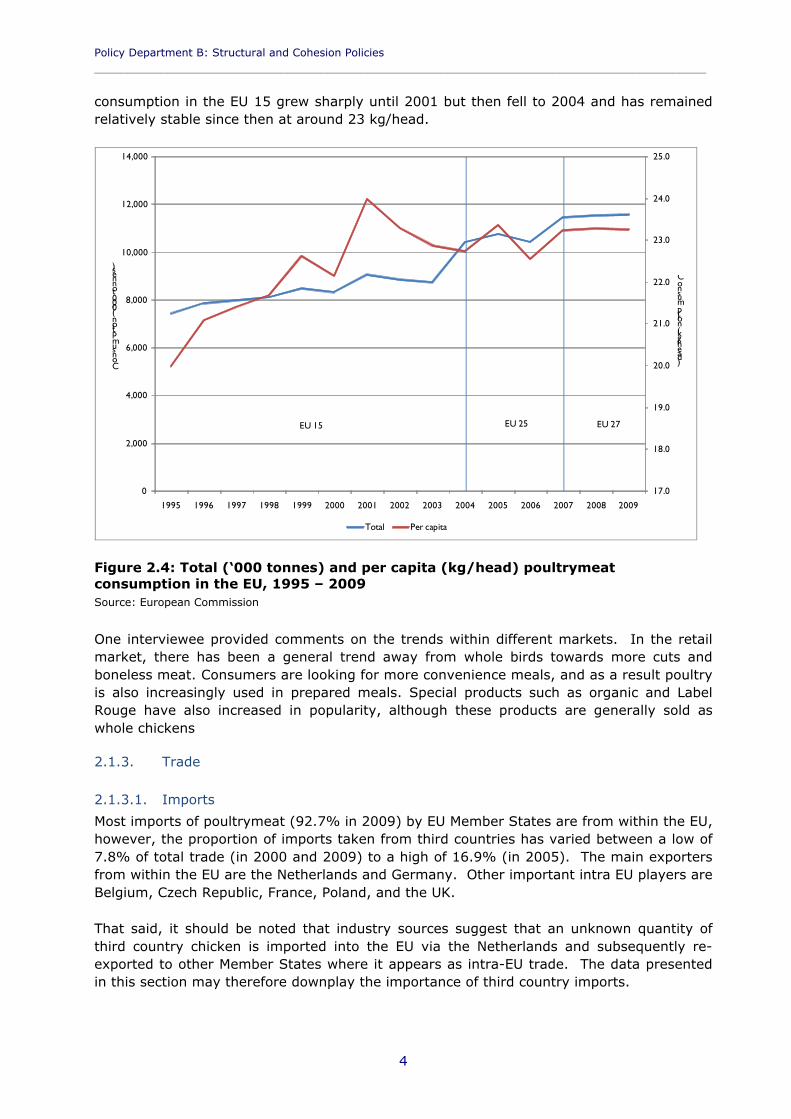

2.1.2. Consumption

Versatile and cheaper than other popular animal proteins (beef and lamb), poultry has a stable market. Poultrymeat is produced more rapidly and uses less space and natural resources than other livestock and from the early 1990s the market share of poultrymeat benefited from the growing view of ‘white meat’ as healthier than red meats and increased use of poultry in frozen processed products and ready-meals. An additional factor in the 1990s was the shift away from beef due to concerns related to BSE.

Figure 2.5 highlights the evolution of poultrymeat consumption (total and per capita) and shows that over the period since 1995 both total and per capita consumption of poultrymeat have only risen due to increase in the number of consumers (after the enlargements in 2004 and 2007). The biggest growth occurred between 1995 and 2001, when total consumption went from 7.4 million tonnes to 9.0 million tonnes, with the biggest increase per capita being 8.2% between 2000 and 2001 (from 22.1 to 23.9 kg/head). With the EU 10 enlargement, total internal use of poultrymeat rose by 20.5% in 2004 and by 4.2% in 2007 after the accession of Bulgaria and Romania.

In per capita terms, the demand for poultrymeat in 2004 after accession increased by 1% while in 2007, the inclusion of Bulgaria and Romania decreased the average per capita consumption by 1.9%. Looking at the available data, it is possible to conclude poultrymeat

Policy Department B: Structural and Cohesion Policies____________________________________________________________________________________________

4

consumption in the EU 15 grew sharply until 2001 but then fell to 2004 and has remained relatively stable since then at around 23 kg/head.

17.0

18.0

19.0

20.0

21.0

22.0

23.0

24.0

25.0

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Consumption(kg/head)C

onsumption('000tonnes)

Total Per capita

EU 15 EU 27EU 25

Figure 2.4: Total (‘000 tonnes) and per capita (kg/head) poultrymeat consumption in the EU, 1995 – 2009Source: European Commission

One interviewee provided comments on the trends within different markets. In the retail market, there has been a general trend away from whole birds towards more cuts and boneless meat. Consumers are looking for more convenience meals, and as a result poultry is also increasingly used in prepared meals. Special products such as organic and Label Rouge have also increased in popularity, although these products are generally sold as whole chickens

2.1.3. Trade

2.1.3.1. Imports

Most imports of poultrymeat (92.7% in 2009) by EU Member States are from within the EU, however, the proportion of imports taken from third countries has varied between a low of 7.8% of total trade (in 2000 and 2009) to a high of 16.9% (in 2005). The main exporters from within the EU are the Netherlands and Germany. Other important intra EU players are Belgium, Czech Republic, France, Poland, and the UK.

That said, it should be noted that industry sources suggest that an unknown quantity of third country chicken is imported into the EU via the Netherlands and subsequently re-exported to other Member States where it appears as intra-EU trade. The data presented in this section may therefore downplay the importance of third country imports.

THE POULTRY AND EGG SECTORS: EVALUATION OF THE CURRENT MARKET SITUATION AND FUTURE PROSPECTS____________________________________________________________________________________________

3

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

1,000,000

2005 2006 2007 2008 2009

Imports(tonnes)

Imports of ooultry from third countries

EU 25 EU 27

Figure 2.5: EU poultry imports from third countries, 2005 – 2009 (tonnes)Source: European Commission, Management Committee

Figure 2.6 shows the evolution of imports in poultry meat since 2005. According to one interviewee, the increase in imports is mainly accounted for by boneless breast meat

Several interviewees commented that the nature of poultrymeat imports had changed over the last decade. Thus during the 1990s and up to 2002 there was a sharp increase in exports of cooked and

salted poultrymeat notably from Thailand and Brazil as the addition of salt enabled the product to enter the EU attracting a lower tariff than the equivalent fresh product. In 2002 the EU decided to change the classification (and duty rate) of the imported product. This led Brazil and Thailand to open a case in the WTO against the EU. Ultimately, as a result of this panel, the EU applied Article XXVIII of GATT; this allowed the EU to align tariffs for different poultrymeat lines, but in 2006 tariff rate quotas (TRQs) were agreed with the main affected parties. According to one interviewee, the tariff lines for turkey preparation and cooked poultrymeat were harmonised at the same time as that for salted poultrymeat as some substitution of products by tariff line was taking place. The same interviewee commented that the EU is applying Article XXVIII of GATT to eight more tariff lines in order to avoid substitution effects with these tariff lines.

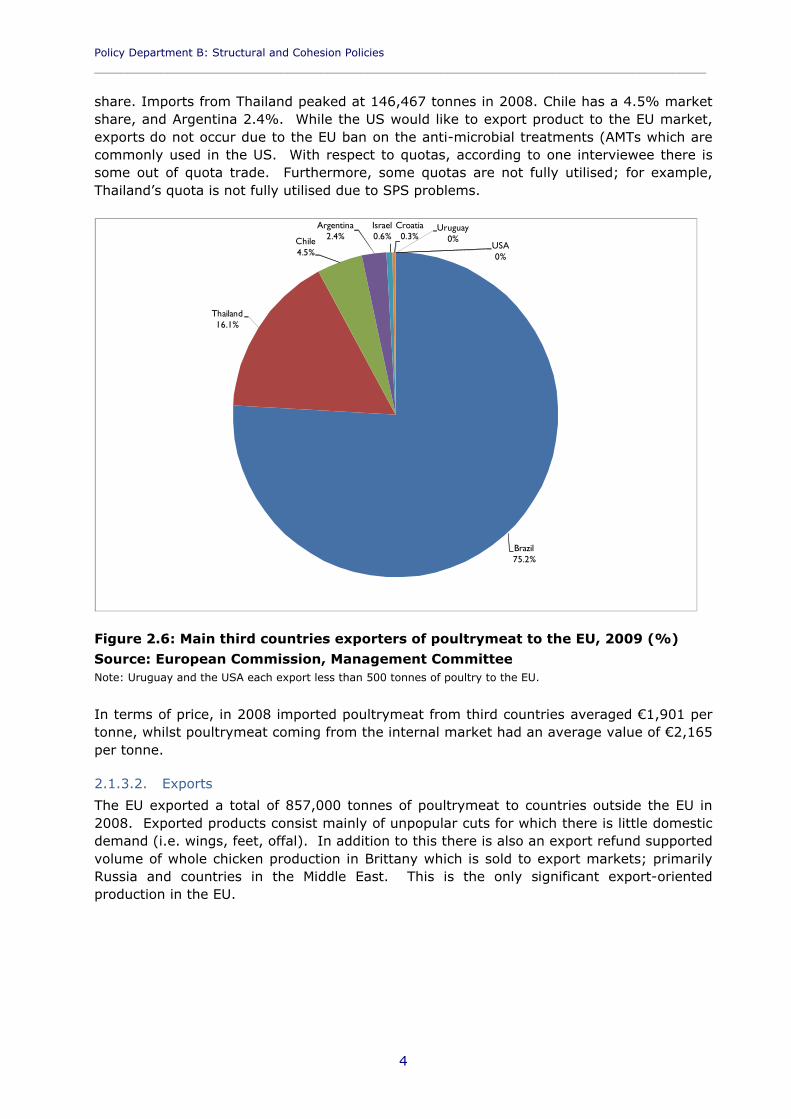

Figure 2.6 and Figure 2.7 present a breakdown of EU poultrymeat imports5 from third countries in 2009. The main origin of third country poultry is Brazil, which accounts for more than 75% of the total. During the period reviewed here, imports from Brazil peaked in 2008 at 679,358 tonnes. The second largest exporter is Thailand, with a 16.1% market

5 Figure based on product code 0207 (meat and edible offal of fowls of the species gallus domesticus, ducks, geese, turkeys and guinea fowls, fresh, chilled or frozen).

Policy Department B: Structural and Cohesion Policies____________________________________________________________________________________________

4

share. Imports from Thailand peaked at 146,467 tonnes in 2008. Chile has a 4.5% market share, and Argentina 2.4%. While the US would like to export product to the EU market, exports do not occur due to the EU ban on the anti-microbial treatments (AMTs which are commonly used in the US. With respect to quotas, according to one interviewee there is some out of quota trade. Furthermore, some quotas are not fully utilised; for example, Thailand’s quota is not fully utilised due to SPS problems.

Brazil75.2%

Thailand16.1%

Chile4.5%

Argentina2.4%

Israel0.6%

Croatia0.3%

USA0%

Uruguay0%

Figure 2.6: Main third countries exporters of poultrymeat to the EU, 2009 (%)

Source: European Commission, Management CommitteeNote: Uruguay and the USA each export less than 500 tonnes of poultry to the EU.

In terms of price, in 2008 imported poultrymeat from third countries averaged €1,901 per tonne, whilst poultrymeat coming from the internal market had an average value of €2,165 per tonne.

2.1.3.2. Exports

The EU exported a total of 857,000 tonnes of poultrymeat to countries outside the EU in 2008. Exported products consist mainly of unpopular cuts for which there is little domestic demand (i.e. wings, feet, offal). In addition to this there is also an export refund supported volume of whole chicken production in Brittany which is sold to export markets; primarily Russia and countries in the Middle East. This is the only significant export-oriented production in the EU.

THE POULTRY AND EGG SECTORS: EVALUATION OF THE CURRENT MARKET SITUATION AND FUTURE PROSPECTS____________________________________________________________________________________________

5

Others32.7%

Vietnam4.6%

Ukraine10.5%Saudi Arabia

11%

Russia21.3%

Hong Kong6.8%

Ghana3.6%

Benin9.6%

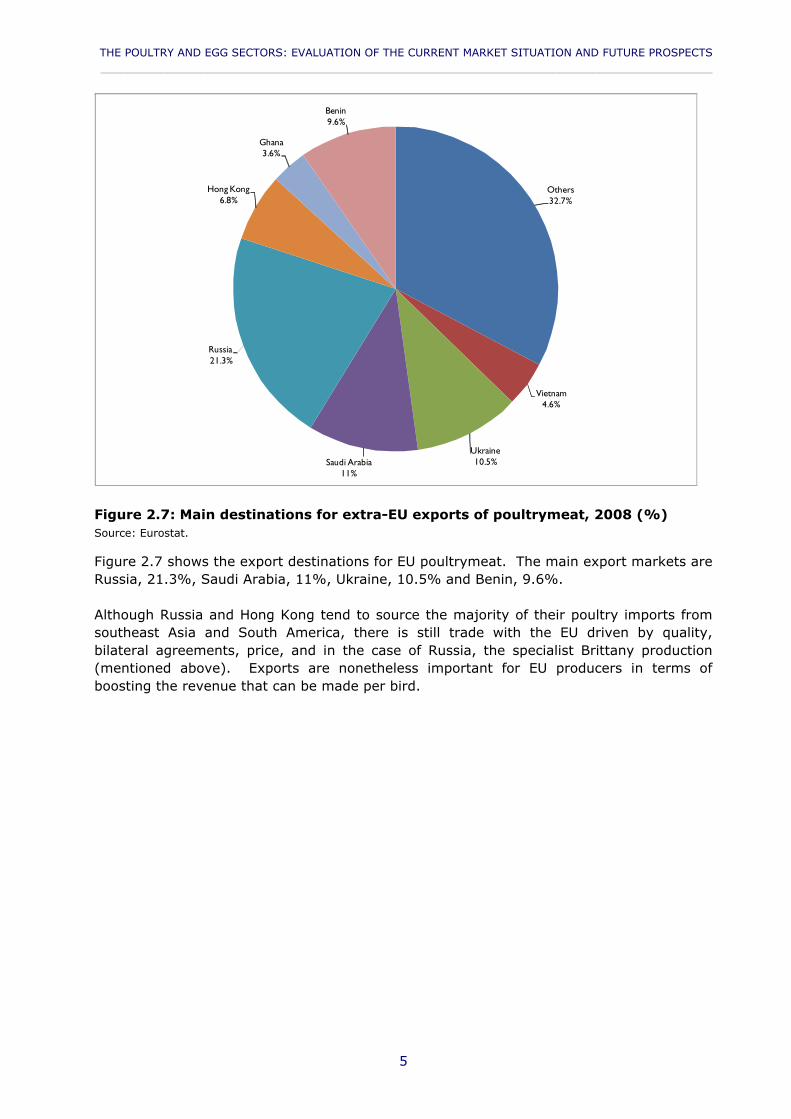

Figure 2.7: Main destinations for extra-EU exports of poultrymeat, 2008 (%)Source: Eurostat.

Figure 2.7 shows the export destinations for EU poultrymeat. The main export markets are Russia, 21.3%, Saudi Arabia, 11%, Ukraine, 10.5% and Benin, 9.6%.

Although Russia and Hong Kong tend to source the majority of their poultry imports from southeast Asia and South America, there is still trade with the EU driven by quality, bilateral agreements, price, and in the case of Russia, the specialist Brittany production (mentioned above). Exports are nonetheless important for EU producers in terms of boosting the revenue that can be made per bird.

Policy Department B: Structural and Cohesion Policies____________________________________________________________________________________________

6

0

100

200

300

400

500

600

700

800

900

1,000

0

200

400

600

800

1,000

1,200

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Value(€million)

Volume('000tonnes)

Volume Value

Figure 2.8: Extra-EU 27 exports of poultrymeat, 2000 – 2009 (‘000 tonnes)Source: Eurostat

Figure 2.8 presents the evolution of EU poultrymeat exports since 1999. Between 2002 and 2007 both the volume and value of exports steadily decreased. After the avian influenza crisis in 2003, several third countries banned imports of poultrymeat from the EU. This situation did not change until 2007 and a fall of 24.5% in volume was registered. In the following years, more markets for EU poultrymeat re-opened but overall exports still did not reach pre-avian influenza levels in value terms.

2.1.4. Employment

The EU poultry meat sector employs an estimated 147,000 persons in production and processing of poultrymeat. Approximately half the numbers employed in the sector are found in three Member States: France, Poland and the United Kingdom which employed approximately 30,000 persons and 22,000 each respectively in 2007.

Eurostat data for employment is incomplete but the available evidence from those Member States reporting shows a variable picture with numbers employed declining since 2000 in Belgium, Ireland, Italy, Hungary, Netherlands, Portugal and Slovakia but rising in Germany, Spain, France, Austria, Finland, Sweden and the United Kingdom (Table 2 1). Within thisoverall picture, it is understood that in slaughterhouses and further processing plants employment has remained relatively stable but

where there has been a decline in employment this has been largely a result of consolidation within the sector6

6 Interview with AVEC

THE POULTRY AND EGG SECTORS: EVALUATION OF THE CURRENT MARKET SITUATION AND FUTURE PROSPECTS____________________________________________________________________________________________

7

Table 2 2: Poultry meat production and processing sector employment, number of enterprises and turnover by EU Member State in 2007

Employment

Employment

Number of enterprises

Number of enterprises

Turnover (Euro million)

Turnover (Euro million)

2000 2007 2000 2007 2000 2007EU-27 147,049 1,970Belgium 2,991 2,637 137 103 823.1 1,204.8Bulgaria 4,162 70 219.0Czech Republic

3,715 35 332.5

Denmark 10 7Germany (including ex-GDR from 1991)

8,698 10,153 74 93 1,968.8 3,497.2

Estonia 0 0 1 0.0Ireland 2,558 1,552 16 405.3Greece 1,540 38 246.5Spain 9,312 10,527 447 220 1,716.4 2,277.0France 29,627 29,898 480 425 5,756.7 6,285.7Italy 14,087 9,878 239 185 2,856.7 2,406.0Cyprus 261 391 15 15 28.0 51.8Latvia 1,115 3 4Lithuania 40 2 5 1.7Luxembourg (Grand-Duché)

0 0 0 0 0.0 0.0

Hungary 15,465 9,808 74 110 687.2 806.7Malta 24 7 1.9Netherlands 4,888 2,637 70 55 1,716.5 1,754.5Austria 730 780 5 12 102.5 148.5Poland 22,467 333 318 866.7 2,447.6Portugal 3,685 3,397 71 54 464.9Romania 5,145 50 190.3Slovenia 1,457 5 4 108.1 158.9Slovakia 2,764 1,685 13 8 119.5 113.9Finland 22 99 3 4 1.8 23.5Sweden 1,436 1,511 19 29 252.3 335.5United Kingdom

21,305 22,455 120 119 3,905.4

Notes: Processing includes slaughtering; for Ireland and Portugal, 2006 data for employment and turnoverSource: Eurostat

According to one interviewee, there has been some consolidation in the broiler sector; the number of poultry farms is decreasing year on year, but the size of the farms is increasing at the same time. The interviewee believed that consolidation in the sector was more common than companies leaving the sector. Data from Eurostat corroborates this;

Policy Department B: Structural and Cohesion Policies____________________________________________________________________________________________

8

between 2000 and 2005, the number of enterprises involved in the production and processing of poultrymeat in the EU-157 fell from 1,691 to 1,279.

2.1.5. Key driving factors

The key factors driving market evolution in the poultry and egg production sectors are discussed in Section 3.2.4 in the context of the analysis of feed costs as well as in Sections 2.1.1.1 and 2.1.2.1 on consumption trends.

2.2. Egg sector

2.2.1. Production

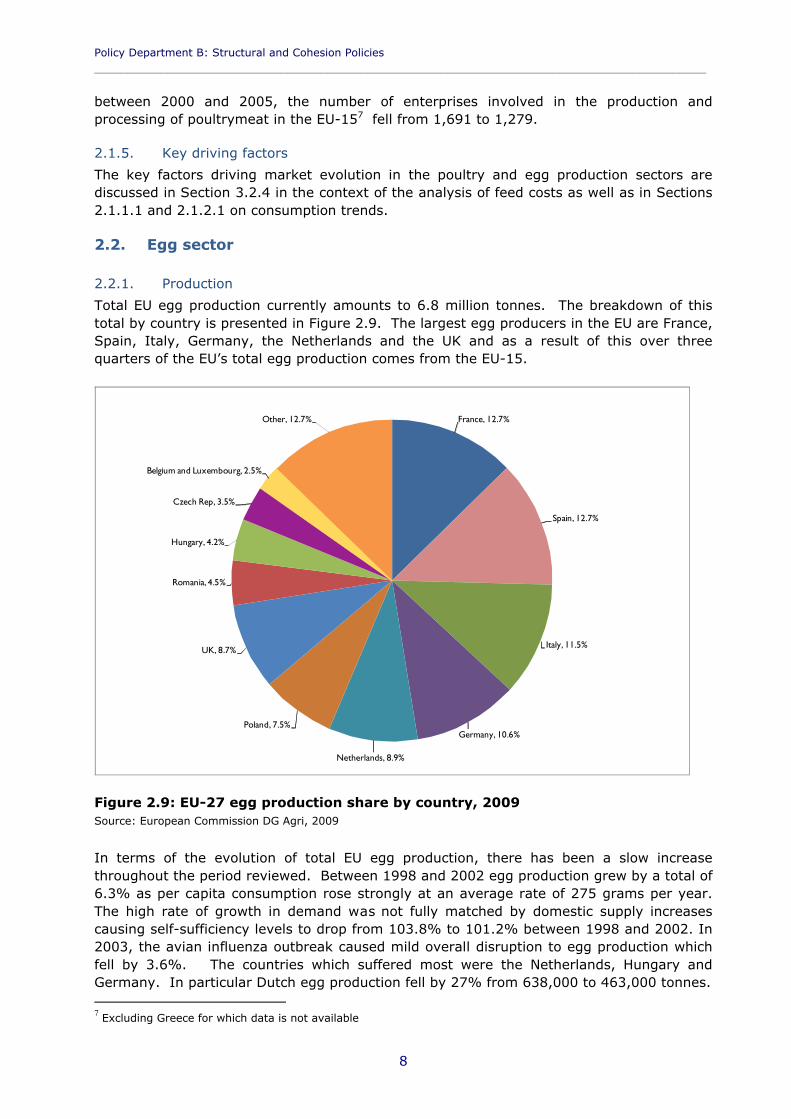

Total EU egg production currently amounts to 6.8 million tonnes. The breakdown of this total by country is presented in Figure 2.9. The largest egg producers in the EU are France, Spain, Italy, Germany, the Netherlands and the UK and as a result of this over three quarters of the EU’s total egg production comes from the EU-15.

France, 12.7%

Spain, 12.7%

Italy, 11.5%

Germany, 10.6%

Netherlands, 8.9%

Poland, 7.5%

UK, 8.7%

Romania, 4.5%

Hungary, 4.2%

Czech Rep, 3.5%

Belgium and Luxembourg, 2.5%

Other, 12.7%

Figure 2.9: EU-27 egg production share by country, 2009Source: European Commission DG Agri, 2009

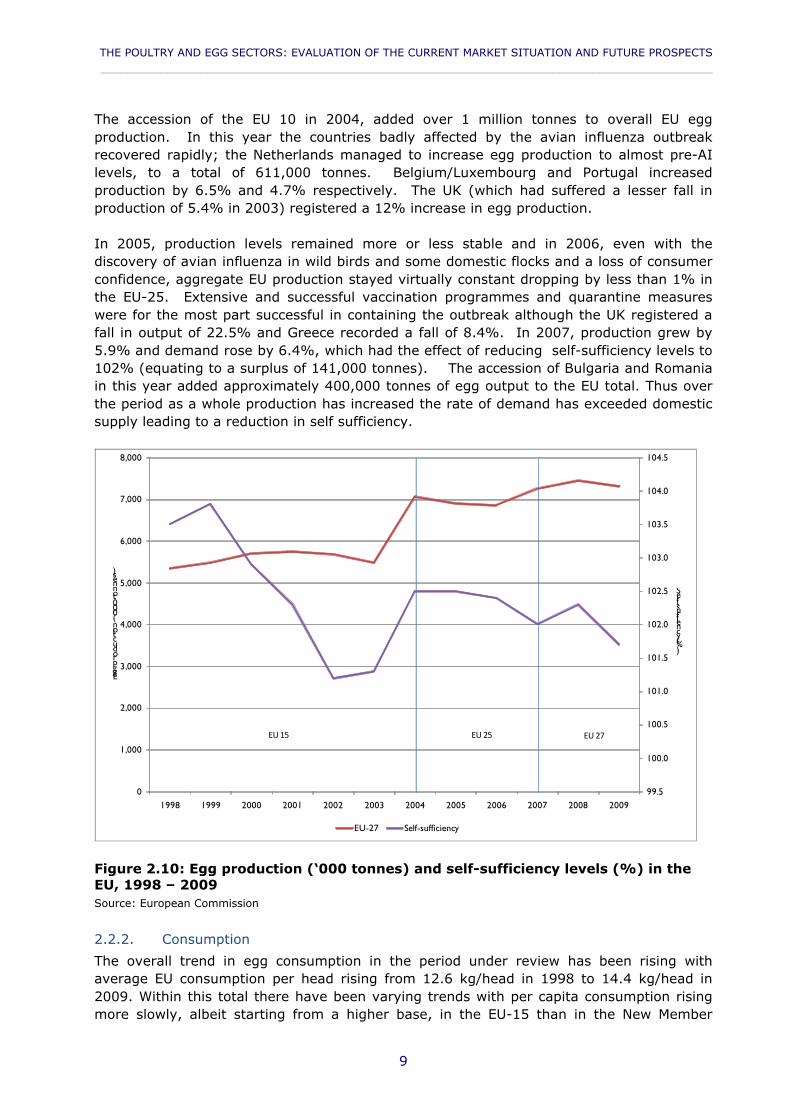

In terms of the evolution of total EU egg production, there has been a slow increase throughout the period reviewed. Between 1998 and 2002 egg production grew by a total of 6.3% as per capita consumption rose strongly at an average rate of 275 grams per year. The high rate of growth in demand was not fully matched by domestic supply increases causing self-sufficiency levels to drop from 103.8% to 101.2% between 1998 and 2002. In 2003, the avian influenza outbreak caused mild overall disruption to egg production which fell by 3.6%. The countries which suffered most were the Netherlands, Hungary and Germany. In particular Dutch egg production fell by 27% from 638,000 to 463,000 tonnes. 7 Excluding Greece for which data is not available

THE POULTRY AND EGG SECTORS: EVALUATION OF THE CURRENT MARKET SITUATION AND FUTURE PROSPECTS____________________________________________________________________________________________

9

The accession of the EU 10 in 2004, added over 1 million tonnes to overall EU egg production. In this year the countries badly affected by the avian influenza outbreak recovered rapidly; the Netherlands managed to increase egg production to almost pre-AI levels, to a total of 611,000 tonnes. Belgium/Luxembourg and Portugal increased production by 6.5% and 4.7% respectively. The UK (which had suffered a lesser fall in production of 5.4% in 2003) registered a 12% increase in egg production.

In 2005, production levels remained more or less stable and in 2006, even with the discovery of avian influenza in wild birds and some domestic flocks and a loss of consumer confidence, aggregate EU production stayed virtually constant dropping by less than 1% in the EU-25. Extensive and successful vaccination programmes and quarantine measures were for the most part successful in containing the outbreak although the UK registered a fall in output of 22.5% and Greece recorded a fall of 8.4%. In 2007, production grew by 5.9% and demand rose by 6.4%, which had the effect of reducing self-sufficiency levels to 102% (equating to a surplus of 141,000 tonnes). The accession of Bulgaria and Romania in this year added approximately 400,000 tonnes of egg output to the EU total. Thus over the period as a whole production has increased the rate of demand has exceeded domestic supply leading to a reduction in self sufficiency.

99.5

100.0

100.5

101.0

101.5

102.0

102.5

103.0

103.5

104.0

104.5

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Self-suffiency(%)

Eggproduction('000tonnes)

EU-27 Self-sufficiency

EU 15 EU 25 EU 27

Figure 2.10: Egg production (‘000 tonnes) and self-sufficiency levels (%) in the EU, 1998 – 2009Source: European Commission

2.2.2. Consumption

The overall trend in egg consumption in the period under review has been rising with average EU consumption per head rising from 12.6 kg/head in 1998 to 14.4 kg/head in 2009. Within this total there have been varying trends with per capita consumption rising more slowly, albeit starting from a higher base, in the EU-15 than in the New Member

Policy Department B: Structural and Cohesion Policies____________________________________________________________________________________________

10

States. Thus per capita consumption in the EU 15 rose from 12.6 kg in 1998 to 13.7 kg per head in 2009; while in the EU 10/12 consumption per head rose from 12.6 kg in 2004 to 12.8 kg per head in 2009. From 2004 to 2009 consumption per head in the EU 10/12 increased by 3.2% while in the EU 15 per capita consumption increased only 0.7%.

Figure 2.11, provides data on egg consumption per capita and indicates a stable level of egg consumption in the EU 15, with the peak in 2004 being the result of accession of New Member States to the EU. Aggregate consumption then levelled off in the following years, due to the lower level of per capita consumption in the EU 12.

11.0

11.5

12.0

12.5

13.0

13.5

14.0

14.5

15.0

15.5

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Consumptionpercapita(kg/head)

Consumption (per capita)

EU 15 EU 25 EU 27

Figure 2.11: Egg consumption per capita in the EU, 1998 – 2009 (kg/head)Source: European Commission

Several interviewees commented that demand for eggs does not suffer during economic downturns, indeed demand may increase as it is the cheapest protein source. Furthermore, one interviewee believed that peer-reviewed scientific evidence negating the link between egg consumption and raised

cholesterol may have contributed to a generally more positive perception of eggs8 and an increase in egg consumption.

Total EU consumption of eggs has risen in line with increased per capita demand rising from 5.8 million tonnes in 1998 to 7.1 million tonnes in 2009. In 2004, the addition of 10 new Member States to the EU increased aggregate EU consumption levels by 1.4 million tonnes

8 Thus for example the British Heart Foundation changed its guidance on egg consumption

THE POULTRY AND EGG SECTORS: EVALUATION OF THE CURRENT MARKET SITUATION AND FUTURE PROSPECTS____________________________________________________________________________________________

11

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Consumption('000tonnes)

Internal use

EU 15 EU 25 EU 27

Figure 2.12: EU egg consumption, 1998 – 2009 (‘000 tonnes)Source: European Commission

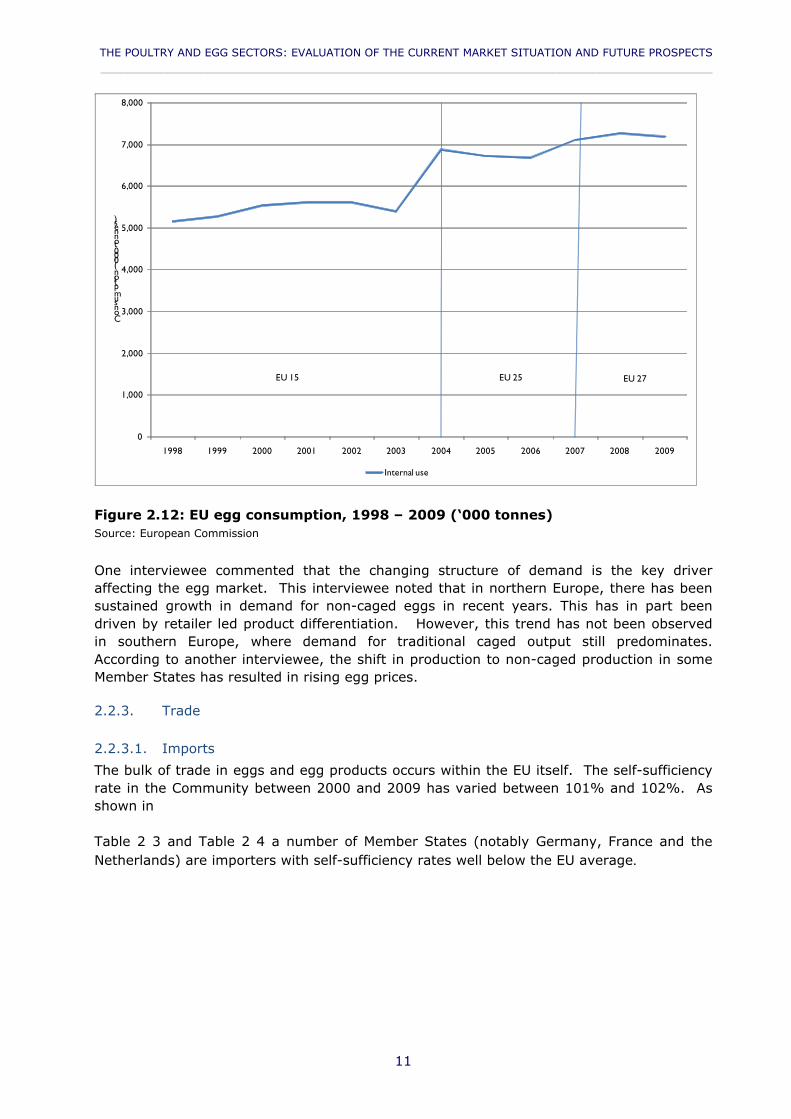

One interviewee commented that the changing structure of demand is the key driver affecting the egg market. This interviewee noted that in northern Europe, there has been sustained growth in demand for non-caged eggs in recent years. This has in part been driven by retailer led product differentiation. However, this trend has not been observed in southern Europe, where demand for traditional caged output still predominates. According to another interviewee, the shift in production to non-caged production in some Member States has resulted in rising egg prices.

2.2.3. Trade

2.2.3.1. Imports

The bulk of trade in eggs and egg products occurs within the EU itself. The self-sufficiency rate in the Community between 2000 and 2009 has varied between 101% and 102%. As shown in

Table 2 3 and Table 2 4 a number of Member States (notably Germany, France and the Netherlands) are importers with self-sufficiency rates well below the EU average.

Policy Department B: Structural and Cohesion Policies____________________________________________________________________________________________

12

Table 2 3: Self sufficiency in egg production in selected EU Member States, 2008

Country Self-sufficiency rateGermany 67%Austria 76%United Kingdom 83%France 86%Sweden 94%Portugal 96%

Source: ZMP, 2008

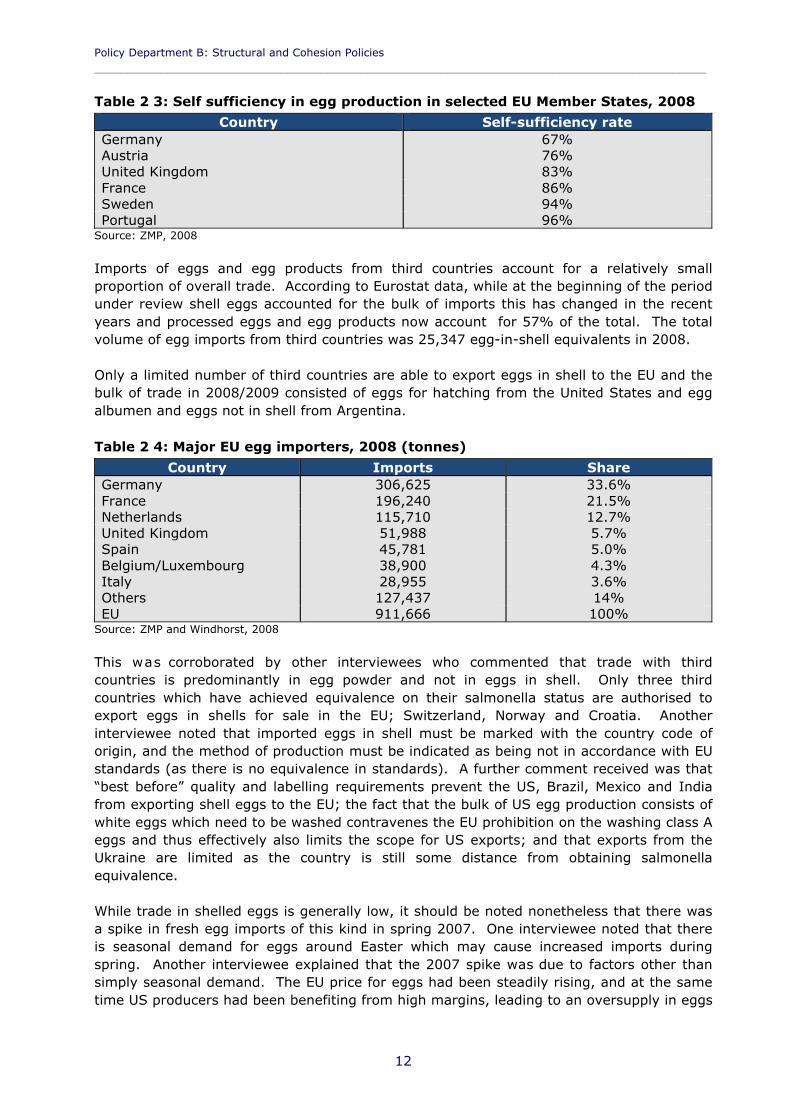

Imports of eggs and egg products from third countries account for a relatively small proportion of overall trade. According to Eurostat data, while at the beginning of the period under review shell eggs accounted for the bulk of imports this has changed in the recent years and processed eggs and egg products now account for 57% of the total. The total volume of egg imports from third countries was 25,347 egg-in-shell equivalents in 2008.

Only a limited number of third countries are able to export eggs in shell to the EU and the bulk of trade in 2008/2009 consisted of eggs for hatching from the United States and egg albumen and eggs not in shell from Argentina.

Table 2 4: Major EU egg importers, 2008 (tonnes)

Country Imports ShareGermany 306,625 33.6%France 196,240 21.5%Netherlands 115,710 12.7%United Kingdom 51,988 5.7%Spain 45,781 5.0%Belgium/Luxembourg 38,900 4.3%Italy 28,955 3.6%Others 127,437 14%EU 911,666 100%

Source: ZMP and Windhorst, 2008

This was corroborated by other interviewees who commented that trade with third countries is predominantly in egg powder and not in eggs in shell. Only three third countries which have achieved equivalence on their salmonella status are authorised to export eggs in shells for sale in the EU; Switzerland, Norway and Croatia. Another interviewee noted that imported eggs in shell must be marked with the country code of origin, and the method of production must be indicated as being not in accordance with EU standards (as there is no equivalence in standards). A further comment received was that “best before” quality and labelling requirements prevent the US, Brazil, Mexico and India from exporting shell eggs to the EU; the fact that the bulk of US egg production consists of white eggs which need to be washed contravenes the EU prohibition on the washing class A eggs and thus effectively also limits the scope for US exports; and that exports from the Ukraine are limited as the country is still some distance from obtaining salmonella equivalence.

While trade in shelled eggs is generally low, it should be noted nonetheless that there was a spike in fresh egg imports of this kind in spring 2007. One interviewee noted that there is seasonal demand for eggs around Easter which may cause increased imports during spring. Another interviewee explained that the 2007 spike was due to factors other than simply seasonal demand. The EU price for eggs had been steadily rising, and at the same time US producers had been benefiting from high margins, leading to an oversupply in eggs

THE POULTRY AND EGG SECTORS: EVALUATION OF THE CURRENT MARKET SITUATION AND FUTURE PROSPECTS____________________________________________________________________________________________

13

in the US and ultimately a fall in the price of US eggs. With a favourable exchange rate, US producers exported a large quantity of shelled eggs to the EU for short period.

According to one interviewee, there may be greater imports of powdered egg products in future. This issue is further analysed in Section 4.

The total value of EU imports from third countries averaged €52.6 million between 1998 and 2009. It should be noted that in the period since 2004, there has been a gradual increase in the value of imports from €51.4 million in 2001 to €62.9 million in 2004 and €62.3 in 2009. Between 2001 and 2009 volumes declined from 23,000 tonnes to 13,000 tonnes suggesting a sharp increase in the value per tonne of product imported.

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

0

100

200

300

400

500

600

700

800

900

1,000

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Value(€millions)

Volume('000tonnes)

Volume imports Intra Volume imports Extra Value imports Intra Value imports Extra

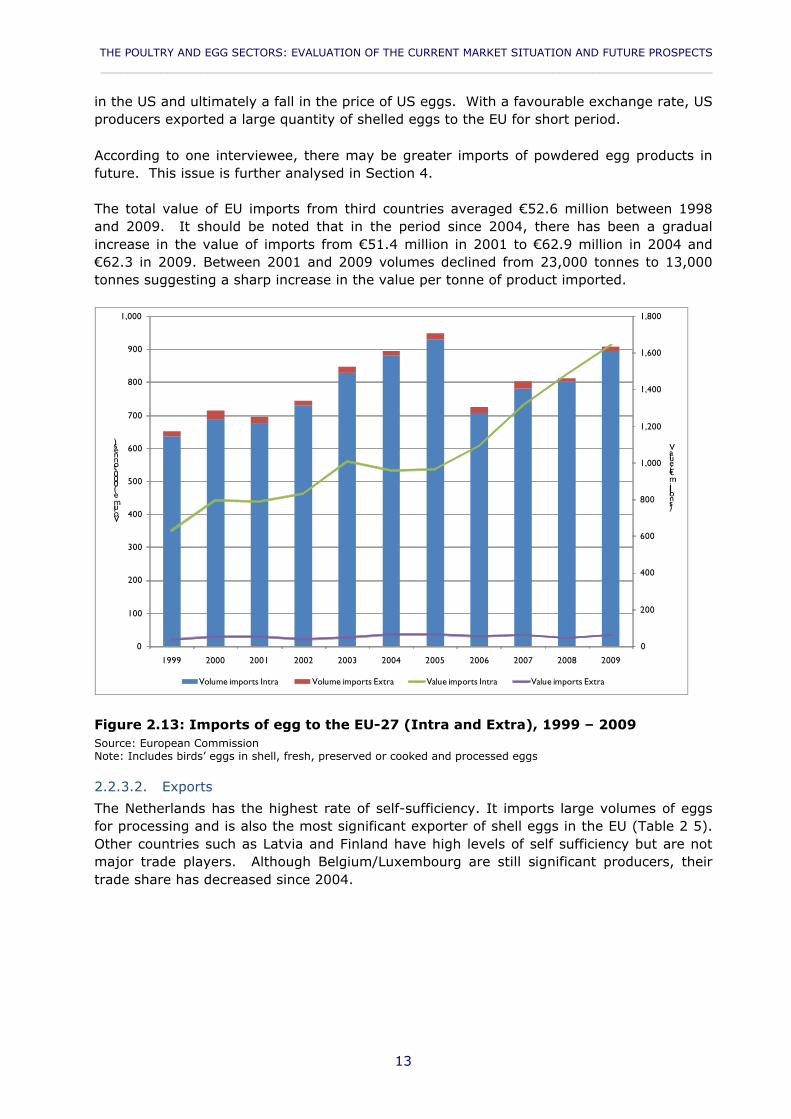

Figure 2.13: Imports of egg to the EU-27 (Intra and Extra), 1999 – 2009Source: European CommissionNote: Includes birds’ eggs in shell, fresh, preserved or cooked and processed eggs

2.2.3.2. Exports

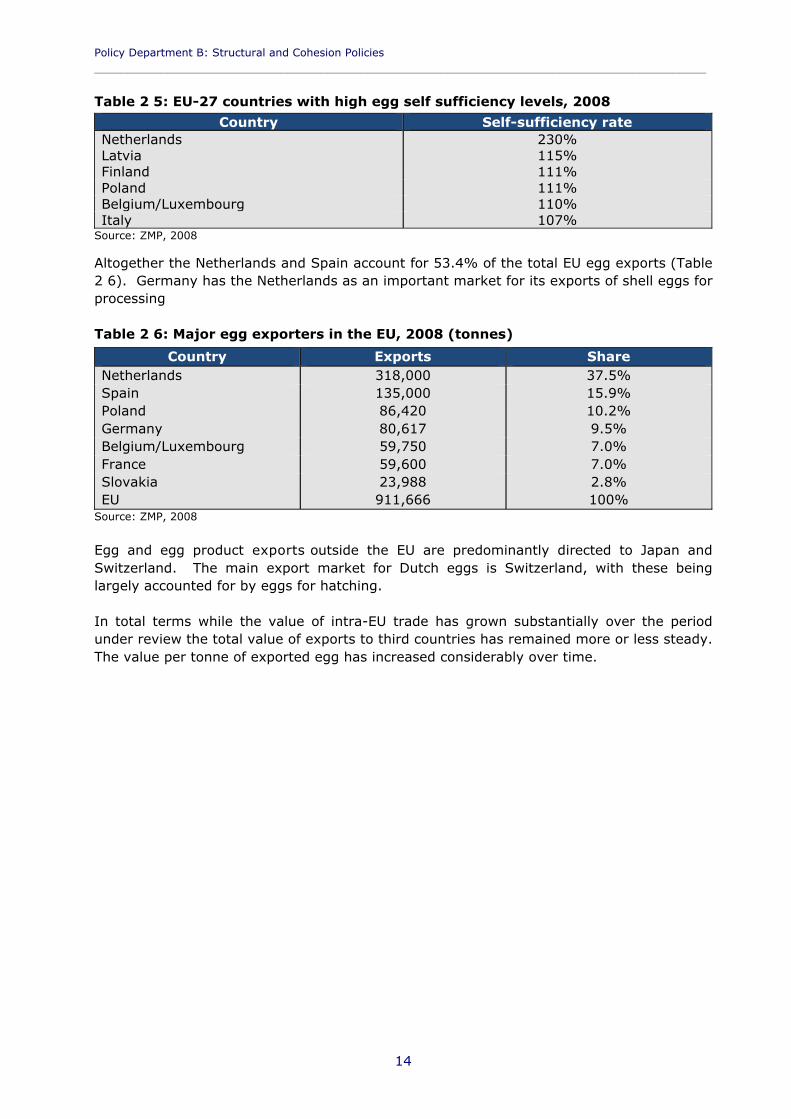

The Netherlands has the highest rate of self-sufficiency. It imports large volumes of eggs for processing and is also the most significant exporter of shell eggs in the EU (Table 2 5). Other countries such as Latvia and Finland have high levels of self sufficiency but are not major trade players. Although Belgium/Luxembourg are still significant producers, their trade share has decreased since 2004.

Policy Department B: Structural and Cohesion Policies____________________________________________________________________________________________

14

Table 2 5: EU-27 countries with high egg self sufficiency levels, 2008

Country Self-sufficiency rateNetherlands 230%Latvia 115%Finland 111%Poland 111%Belgium/Luxembourg 110%Italy 107%

Source: ZMP, 2008

Altogether the Netherlands and Spain account for 53.4% of the total EU egg exports (Table 2 6). Germany has the Netherlands as an important market for its exports of shell eggs for processing

Table 2 6: Major egg exporters in the EU, 2008 (tonnes)

Country Exports ShareNetherlands 318,000 37.5%Spain 135,000 15.9%Poland 86,420 10.2%Germany 80,617 9.5%Belgium/Luxembourg 59,750 7.0%France 59,600 7.0%Slovakia 23,988 2.8%EU 911,666 100%

Source: ZMP, 2008

Egg and egg product exports outside the EU are predominantly directed to Japan and Switzerland. The main export market for Dutch eggs is Switzerland, with these being largely accounted for by eggs for hatching.

In total terms while the value of intra-EU trade has grown substantially over the period under review the total value of exports to third countries has remained more or less steady. The value per tonne of exported egg has increased considerably over time.

THE POULTRY AND EGG SECTORS: EVALUATION OF THE CURRENT MARKET SITUATION AND FUTURE PROSPECTS____________________________________________________________________________________________

15

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

0

200

400

600

800

1,000

1,200

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Value(€millions)

Volume('000tonnes)

Volume export Intra Volume export Extra Value export Intra Value export Extra

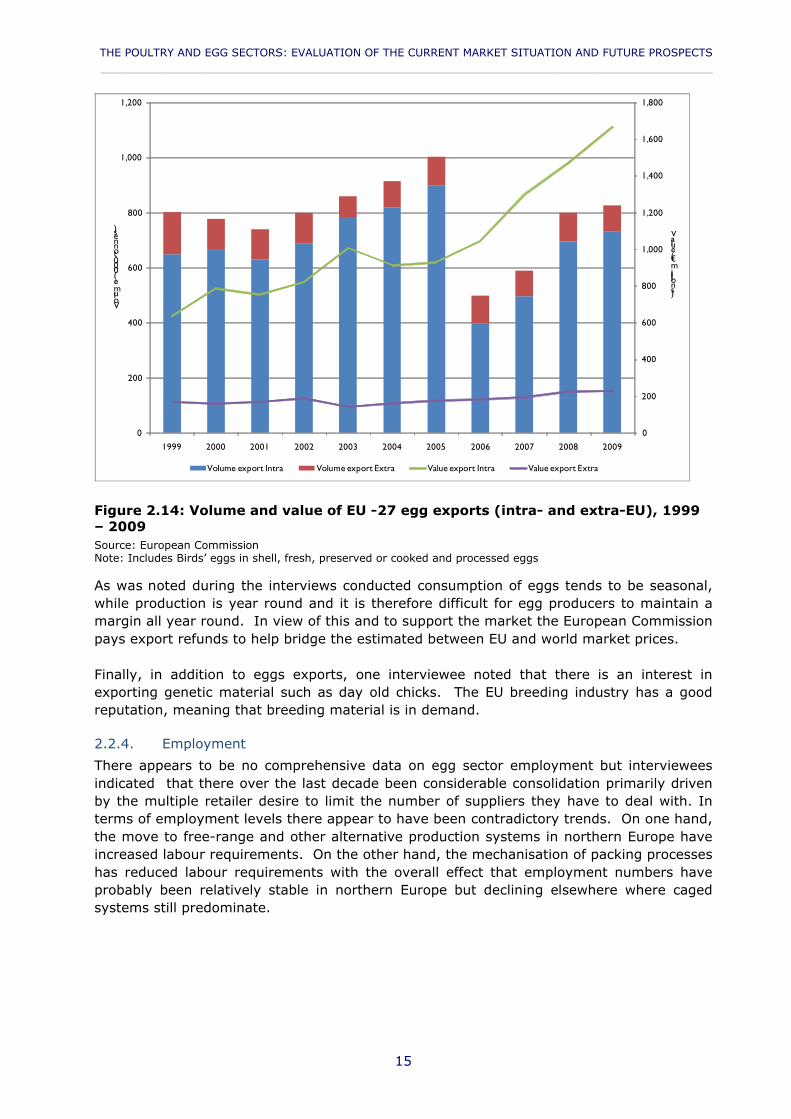

Figure 2.14: Volume and value of EU -27 egg exports (intra- and extra-EU), 1999 – 2009Source: European CommissionNote: Includes Birds’ eggs in shell, fresh, preserved or cooked and processed eggs

As was noted during the interviews conducted consumption of eggs tends to be seasonal, while production is year round and it is therefore difficult for egg producers to maintain a margin all year round. In view of this and to support the market the European Commission pays export refunds to help bridge the estimated between EU and world market prices.

Finally, in addition to eggs exports, one interviewee noted that there is an interest in exporting genetic material such as day old chicks. The EU breeding industry has a good reputation, meaning that breeding material is in demand.

2.2.4. Employment

There appears to be no comprehensive data on egg sector employment but interviewees indicated that there over the last decade been considerable consolidation primarily driven by the multiple retailer desire to limit the number of suppliers they have to deal with. In terms of employment levels there appear to have been contradictory trends. On one hand, the move to free-range and other alternative production systems in northern Europe have increased labour requirements. On the other hand, the mechanisation of packing processes has reduced labour requirements with the overall effect that employment numbers have probably been relatively stable in northern Europe but declining elsewhere where caged systems still predominate.

THE POULTRY AND EGG SECTORS: EVALUATION OF THE CURRENT MARKET SITUATION AND FUTURE PROSPECTS____________________________________________________________________________________________

3

2.3. The commercial structures used in the poultry meat and egg sectors

2.3.1. Structure of the poultry meat production sector

Broiler production can be considered to be either integrated or non-integrated. These approaches are set out below and are followed by a concise comparison:

Integrated production. In France, Germany, Italy and Spain standard poultry meat production is mainly organised through integrators. This process was started in the 1970s in Brittany as part of a push from feed compounders to integrate forwards whereas in the 1980s and 1990s integration reflected more of a backward push from slaughterhouses so that by the year 2000 the share of the four largest companies in the output of the sector had reached 57%. Integrators own the processing plant and often also the hatchery and the feed mill. Towards the broiler farmers integrators use contracts to vertically coordinate poultry production. Broiler farmers remain the owners of production buildings, but most technical choices (from one day chicks to feed suppliers, or even the type of buildings) are made by the integrator, who also plan chick placements in coordination with the slaughterhouses and market needs. Producers are often organised in production organisations (producers groups, mainly cooperatives), which negotiate the terms of the contracts with the industry. This is the situation in, for example, France and Germany. In France, most contracts afford some guaranteed margins for producers.

Non-integrated production. In some EU countries, for example, the Netherlands, Belgium and Poland, the production of poultry meat is not integrated. This means that each link of the production chain is independent of the others. Slaughterhouses, hatcheries and feed mills are separate independent companies and broiler farmers operate independently. Farmers buy the day old chicks from a hatchery and the feed from a feed mill. The birds are grown and sold to a slaughterhouse. This is done based on a long-term agreement for the supply of chickens. In the integrated system the broiler farmer has a contract with an integrator who delivers the day old chicks and feed and collects the grown birds for slaughter. The consequence of the non integrated system is that farmers are more directly confronted with the fluctuations in the markets for feed and broilers.

As a foreword, according to one interviewee, it is not easy to differentiate between integrated and non-integrated production. The interviewee believed that integration existed in most chains, but the degree of integration varied; while some companies control the whole operation, others have contracts with other operators in the chain; ultimately there are very few farms which sell chickens independently of the purchase of feed and day-old chicks. The same interviewee commented that poultry production requires considerable advanced planning (e.g. parent and grandparent stock), and cannot be adjusted rapidly.

The Farm Accountancy Data Network (FADN) gives insights into the financial performance of broiler farms (see paragraph 3.2). In December 2009 LEI published the results for 2008 and provided an estimate for the year 2009 (LEI, 2009).

Figure 2.15 shows that family farm income in the sector fluctuates significantly between years. These fluctuations are mainly caused by changes in input prices (for example, feed prices) and market prices for broilers. In 2006 income was low as a result of low market prices: demand for poultry meat was reduced because of the extensive media attention

Policy Department B: Structural and Cohesion Policies____________________________________________________________________________________________

4

given to avian influenza in wild birds in some European countries. In 2008 average family farm income was approximately zero. Despite higher market prices for broilers, the very significant increase in input costs (especially feed) in that year was too high to generate an income for the farmer. The estimate for the average family farm income in 2009 is €35,000.

-40

-20

0

20

40

60

80

100

120

Income(€'000)

Figure 2.15: Family farm income development in the Netherlands on broiler farms, 1992/1993-2009, (Euro/ farm).Source: LEI (2009).Note: From 2001 the registration period changed from a marketing (May to April) to a calendar year basis.

As is indicated above, income in poultry production is mainly influenced by the level and variability of poultry and feed prices. Poultry meat prices inevitably fluctuate from year to year in line with the variations in supply and demand on the European market. Farmers in countries like the Netherlands and Poland accept and respond to these price fluctuations by changing their production pattern mainly through changes in the density (number of broilers per square meter in a poultry house) and increasing or decreasing the empty period between flocks. These changes are made in cooperation with the poultry slaughterhouses as they are in direct contact with the market.

In Member States with integrated production the farmers receive a contract payment. The risk arising from high feed prices or low poultry meat prices are mainly carried by the integrator. Working with integrators the broiler farmer tends to have a more stable income over time with just minor fluctuations between years. The broiler famer is directly linked to the industry through a contract. This integration contract almost completely disconnects the farmers from the market and the main market risks are transferred to the industry. However, the market nevertheless affects revenues by influencing the farms’ level of activity. In France, data from the Chambres d’Agriculture indicates that productivity differences (kg of live weight produced/m²/year) explain 58 % of the gap between lower

THE POULTRY AND EGG SECTORS: EVALUATION OF THE CURRENT MARKET SITUATION AND FUTURE PROSPECTS____________________________________________________________________________________________

5

quartile in terms of margins and the highest. This is in large part due to the number of rotations which are laid down by the integrators.

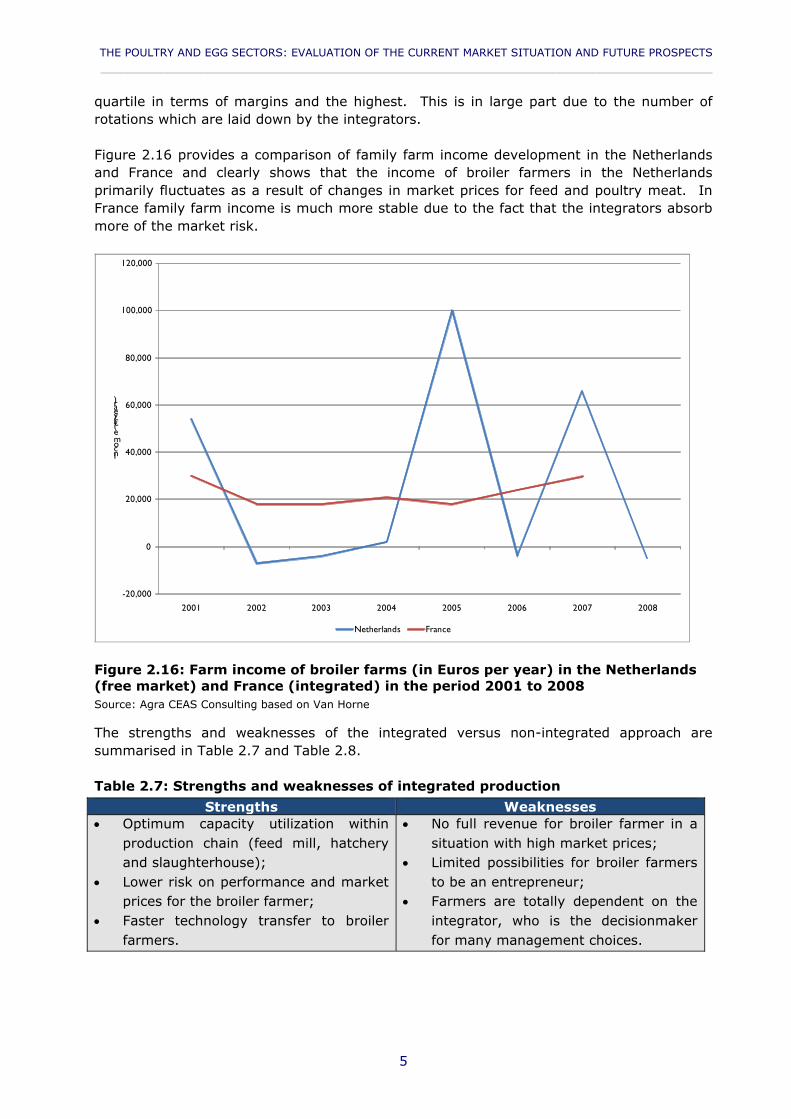

Figure 2.16 provides a comparison of family farm income development in the Netherlands and France and clearly shows that the income of broiler farmers in the Netherlands primarily fluctuates as a result of changes in market prices for feed and poultry meat. In France family farm income is much more stable due to the fact that the integrators absorb more of the market risk.

-20,000

0

20,000

40,000

60,000

80,000

100,000

120,000

2001 2002 2003 2004 2005 2006 2007 2008

Income(€/year)

Netherlands France

Figure 2.16: Farm income of broiler farms (in Euros per year) in the Netherlands (free market) and France (integrated) in the period 2001 to 2008Source: Agra CEAS Consulting based on Van Horne

The strengths and weaknesses of the integrated versus non-integrated approach are summarised in Table 2.7 and Table 2.8.

Table 2.7: Strengths and weaknesses of integrated production

Strengths Weaknesses Optimum capacity utilization within

production chain (feed mill, hatchery and slaughterhouse);

Lower risk on performance and market prices for the broiler farmer;

Faster technology transfer to broiler farmers.

No full revenue for broiler farmer in a situation with high market prices;

Limited possibilities for broiler farmers to be an entrepreneur;

Farmers are totally dependent on the integrator, who is the decisionmaker for many management choices.

Policy Department B: Structural and Cohesion Policies____________________________________________________________________________________________

6

Table 2.8: Strengths and weaknesses of non-integrated productionStrengths Weaknesses

High motivation for farmers to have good production performance ;

Competition between hatcheries, feed mills and slaughterhouses to do business with broiler farmers.

Potentially large fluctuations in income for broiler farmers due to changes in input and output prices;

Large cash requirements, tending to create dependence on loans and vulnerability to changes in interest rates for broiler farmers;

No strong incentive for maximising efficiency within production chain.

2.3.2. Structure of the egg production sector

2.3.2.1. Egg production systems

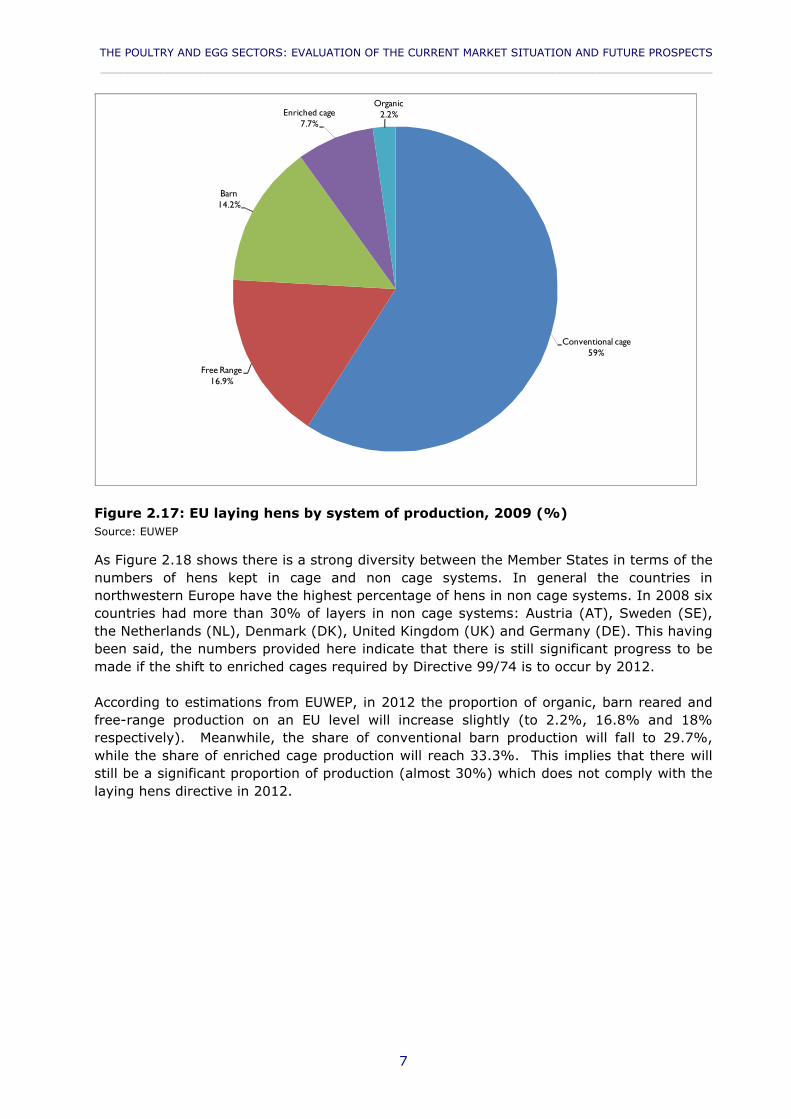

Figure 2.17 presents a breakdown of layers in different egg production systems in the EU-27 as estimated by the EU egg industry representative organisation EUWEP based on European Commission DG Agri data in 2009. It should be noted that these figures are provisional and assume: a) that use of enriched cages will have grown from 19.2 million (5% of total units) in 2008 to 30 million units in 2009; b) that the number of layers in barn systems will have risen from 50.4 million to 55 million and c) that some Member State data has not changed year on year. Using these assumptions and noting also that the ‘free range’ category includes an estimated 34.2 million backyard hens in Romania it is evident that the traditional caged system still accounts for some 59% of layers or 228.4 out of a total of 387.7 million layers in the EU.

In the predominant caged or confined housing system almost all management activities are automated: mechanical feeding, ventilation and egg collection. As a result of the high level of automation and mechanisation and labour requirements are relatively low.

Non cage or alternative systems have the common feature that the layers are kept in large barns with litter on the floor and freedom of movement for the birds within the poultry house. Although also in these housing systems automation levels are high some management activities cannot be automated. The farmer needs to regularly monitor the birds visually by going into the barn. There is also a large labour input in terms of collecting those eggs in the barn which are laid outside the laying nest. Alternative housing systems therefore have a significantly higher labour input per 1,000 hens than cage systems. At the same time a high level of stockmanship is needed in order to obtain satisfactory production results. For this reason farms with alternative housing systems are frequently relatively small and run by a family (family farms). In the Netherlands, Germany and the UK barn eggs and free range eggs are mainly produced on small and medium size farms with less than 100,000 layers. In France, the main share of alternative output is produced in farms with less than 20,000 hens (some 8,000 hens on average), compared to cage egg production where the average size of unit is approximately 55,000 hens.

THE POULTRY AND EGG SECTORS: EVALUATION OF THE CURRENT MARKET SITUATION AND FUTURE PROSPECTS____________________________________________________________________________________________

7

Conventional cage59%

Free Range16.9%

Barn14.2%

Enriched cage7.7%

Organic2.2%

Figure 2.17: EU laying hens by system of production, 2009 (%)Source: EUWEP

As Figure 2.18 shows there is a strong diversity between the Member States in terms of the numbers of hens kept in cage and non cage systems. In general the countries in northwestern Europe have the highest percentage of hens in non cage systems. In 2008 six countries had more than 30% of layers in non cage systems: Austria (AT), Sweden (SE), the Netherlands (NL), Denmark (DK), United Kingdom (UK) and Germany (DE). This having been said, the numbers provided here indicate that there is still significant progress to be made if the shift to enriched cages required by Directive 99/74 is to occur by 2012.

According to estimations from EUWEP, in 2012 the proportion of organic, barn reared and free-range production on an EU level will increase slightly (to 2.2%, 16.8% and 18% respectively). Meanwhile, the share of conventional barn production will fall to 29.7%, while the share of enriched cage production will reach 33.3%. This implies that there will still be a significant proportion of production (almost 30%) which does not comply with the laying hens directive in 2012.

Policy Department B: Structural and Cohesion Policies____________________________________________________________________________________________

8

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

AT SE NL DK UK DE IT FI FR BE HU SK PL EL CZ ES LT

Proportionoflayersbysystem

Cage Free range Barn Organic

Figure 2.18: Percentage of layers kept in different housing systems in 17 EU Member States, 2008Source: Agra CEAS based on ITAVI from euro com

2.3.3. Organisational structure

The organisational structure in the egg sector is very different from the poultry meat sector. As is indicated above, in the poultry meat sector production in many EU countries is organized by integrators who own the processing plant, the hatchery and a feed mill. Farmers own the poultry houses and produce broilers on contract. As the birds have to be slaughtered at specific weights contract production is important to vertically coordinate the production. This is called fully integrated production where farmers produce broilers under production contracts. Egg production is either organized in a (semi-) integrated way or without any coordination. The situation varies greatly between Member States. The particular organisational structure which prevails is also related to the housing systems (cage versus alternative production):

Integrated production. In many EU countries there are large companies holding more than 1 million layers in cage systems. This is clearly the situation in the UK, Germany, Spain, Italy and Poland. In these countries substantial portions of the chain are integrated in that pullet rearing, layers, feed supply, packing, processing and marketing to the retailer are all in the hands of a single company or co-operative (Agra CEAS, 2004). These integrated companies own and pack a significant proportion of national production. In France, production is often organized by the feed mills (often cooperative groups), who provide feed and pullets to the producers. In the Netherlands feed mills also play an important role in supplying feed and advice to farms. Layer farmers are independent entrepreneurs taking full risk for changes in input (feed and pullet) and output (eggs) prices. At the other end of the scale are other countries where a relatively fragmented production structure is accompanied by a marked lack of concentration at both the production and egg packer level. This is the situation in countries such as Portugal,

THE POULTRY AND EGG SECTORS: EVALUATION OF THE CURRENT MARKET SITUATION AND FUTURE PROSPECTS____________________________________________________________________________________________

9

Greece, Romania and also (partly in) Poland. In other countries such as Austria, producer groups play a significant role in the marketing of the eggs. In most countries, however, packer concentration is relatively low and producers will either own their own packing station, or have arrangements to sell to independent packers who will bundle supplies on short-term supply or price contracts from a relatively limited number of producers.

The processing sector is much more concentrated than the packing sector with many Member States (Sweden, Finland, Denmark, Portugal, Greece, Austria, Belgium and Ireland) having fewer than four processors.

All EU-15 Member States do, however, have at least one processing facility. Where processors are limited in number they tend to focus on breaking second quality eggs, mainly for the domestic market, and usually liquid products only. Often these liquid products include blends and mixes in order to capture greater added value. The drying sector is being increasingly concentrated and many smaller scale processors have stopped this activity in the face of competition.

As is indicated above there is a relation between housing system, farm size and integrated production. Large integrators tend to keep hens in cages on large farms. In countries with a high percentage of hens kept in alternative housing systems the average farm size is smaller and a larger proportion of production in non-integrated. However, large groups or producers of cage eggs may often also integrate some alternative egg producers, to complete the range of products they can offer to distributors.