Embed Size (px)

Citation preview

The Pricing of Risk in Emerging Credit Markets: Bonds versus Loans

WILLIAM MILES*

Much of the volatility in emerging markets in the 1990s stems from the fact that the major form of foreign investment is the bond rather than the bank loans which predominated until the debt crisis of the 1980s. Bondholders are too dispersed to negotiate with during a liquidity shortfall. Thus, a shortage of reserves becomes a full-blown crisis. This was not the case in the 1980s when banks, as the major creditors, often lent to countries in arrears. The risk to a loan is therefore rescheduling, while the risk to a bond is default. Empirically pricing loans and bonds as assets reveals that bonds incorporate the greater risk of default into their spreads. Debentures are thus riskier credit than loans. As developing countries now obtain most finance through these risky instruments, the volatility of the 1990s is better understood. (JEL F34)

Introduction

The decade of the 1990s has been characterized by large capital inflows to emerging markets, as well as major financial and currency crises. It is initially puzzling why there should be such volatility in this decade. Internally, developing countries have generally embarked on reforms, making them much more attractive to investors. Externally, until the Asian crisis, commodity prices, whose variability had played a role in the 1980s debt difficulties, had been relatively stable. Additionally, interest rates in G-7 countries, also a contributing factor to the problems of the last decade, have been less burdensome than in the late 1970s and early 1980s. Why then the turmoil of the 1990s?

It is argued here that a major factor for this turmoil is the change in the financial environment due to the form that investment takes. Specifically, in the 1990s, bonds are the main conduit of financial flows from the first to the third world. ~ In the 1980s, the major instrument was the bank loan. With loans, there was a relationship between the bank and the borrowing country. Banks would lend to countries believed to be experiencing liquidity as opposed to solvency problems. During the debt crisis, many countries received fresh funds from banks in response to arrears (such a strategy did not work in this case as falling commodity prices turned the problem into one of solvency, not liquidity). Most of the difficulties of this decade, however, are liquidity crises [Chang and Velasco, 1998]. Nations find themselves temporarily short of reserves relative to foreign currency obligations coming due. While a banker could roll over debt or provide emergency credit in case of such a cash flow shortfall, as was done in the 1980s,

*Wichita State University--U.S.A. The author would like to thank Werner Baer, Joseph Finnerty, Kyung So Im, William Maloney, and an anonymous referee for helpful comments.

221

222 IAER: MAY 2000, VOL. 6, NO. 2

dispersed bondholders do not. Thus, a liquidity shortfall can become a major balance-of- payments crisis. According to Sachs et al. [1996], the Mexican crisis in December 1994, for example, was precipitated when bondholders refused to roll over Tesobonos coming due, despite the fact that Mexico's solvency was not in question [p. 44]:

"This problem was exacerbated by the fact that there were many bondholders, operating on information obtained third-hand or fourth-hand from the general press, rather than a small number of banks that could have coordinated among themselves to help keep Mexico liquid. The panic on government securities quickly led to a generalized panic on the Mexican economy."

Chang and Velasco [1998, p. 18] point to similar actions by holders of Asian bonds as that crisis commenced.

To date, no studies have formally investigated the impact of this riskier form of financing on the vulnerability to crisis. This paper aims to fill this gap. Previous literature indicates that the risk to loans is rescheduling, while the risk to bonds is default. The former situation is less dire than the latter, so loan spreads are, in theory, less affected by risk factors than bond rates. This paper will test this hypothesis for the 1990s hard currency bond and loan issues for emerging markets. Panel estimation for bond and loan spreads, as well as a seemingly unrelated regressions (SUR) model used to formally test for the differing impacts of risk factors on loan and bond prices, confirms that bonds are riskier assets than loans. This helps to explain the volatility we observe in this decade of bond finance.

This paper proceeds as follows. Literature on the differences between loans and bonds will be reviewed. How bonds and loans to emerging markets are priced as assets in the 1990s will then be examined. The results confirm that bonds are priced to incorporate greater default probabilities and, hence, are riskier instruments. Since nations are financing themselves with this riskier credit, increased volatility is more easily understood.

Loans and Bonds: Previous Literature

If capital markets were perfect (or complete in an Arrow-Debreu sense), bonds and loans would be perfect substitutes, indeed identical instruments. How the two forms of debt differ and coexist has thus been the subject of much speculation in finance literature. Fama [1985] and Diamond [1991] have emphasized the role of banks in developing relationships with and gathering information about customers. These are activities in which bondholders do not take part. Chemmanur and Fulghieri [1994] stress the important role of debt renegotiations in times of financial distress. Again, banks specialize in information about their customers while bondholders do not. If there is a repayment problem for the borrower, the bank will expend some resources to determine whether the customer is undergoing cash flow problems or if the enterprise is no longer viable. Assuming the former is the case, the loan will be renegotiated. Owners of bonds will not expend resources to determine whether or not a customer is viable and will generally

MILES: BONDS VERSUS LOANS 223

liquidate the security. Thus, borrowers concerned about their own repayment abilities will choose banks to avoid being forced into bankruptcy in case of liquidity shortfalls.

This model has relevance for bank and bond lending to less developed countries (LDCs). Cline [1995, p. 192] claims that larger banks did not tend to dump their LDC debt on the secondary market during the crisis of the 1980s. It is not possible to assess a corresponding bondholder response since bonds were a very small fraction of developing country debt. It is unlikely, however, that bondholders would have reacted the same way since they are so dispersed. It is true that the debt crisis of the 1930s was largely a bond problem, and there were long, drawn-out negotiations. However, this was due to the existence of bondholder committees. Such committees do not exist today, so protracted renegotiation is extremely difficult in the modern era of bond finance.

In the wake of the debt crisis in 1982, several authors looked at the differences between the two debt instruments in the international market. Most prominent among these was the work by Folkerts-Landau [1985], who offered an explanation for the dominance of bank lending over bond issue in the 1970s. Banks were relatively cohesive compared to bondholders and could form coalitions to deal with delinquent sovereign borrowers. Rather than defaulting outright, the debtor would work out a payment plan with the financial institutions. Countries that got into such difficulties were subject to being rationed out of future credit by the cohesive front formed by banks if they failed to carry out stabilization and repayment plans. This was not a possibility with dispersed owners of securities. Thus, the risk of a loan is rescheduling, while the risk of a bond is default, a worse event. Folkerts-Landau concluded that bank spreads should reflect less risk than those on debentures.

Edwards [1986] empirically tested some sovereign debt theories and the propositions regarding loans and bonds as mentioned above. He noted that some other observers had come to conclusions that differed from Folkerts-Landau. Gersovitz [1985] had noted that the lack of sanctions besides calling a bond into default meant that countries might be less willing to miss payments on a bond. In fact, throughout the debt crisis, only three countries ever missed amortization payments on debentures. This may be due, in part, to the fact that bond debt for LDCs, in the 1980s, was much smaller than bank loan debt. In Latin America in 1986, outstanding bonds amounted to $18 billion, while long-term bank loans were $238 billion [Cline, 1995, p. 438]. Implicitly, loans were subordinate to bonds. Therefore, it may be the case that bonds were less risky than loans if this line of reasoning is accepted. Moreover, Eaton and Gersovitz [1981] had noted that bonds may be more information-intensive forms of investment than loans since the former are sold on prospectus. Thus, not all observers believed that loans were less risky, and the relative risk of each instrument is an empirical issue.

Edwards [1986] was the first to systematically compare loans and bonds as emerging market debt. His primary purpose was to test some sovereign debt theories. Also in this case, both loan and bond spreads were analyzed and compared. The author acknowledges the conflicting hypotheses presented by Folkerts-Landau [ 1985] and Gersovitz [ 1985]. If the former is correct, then according to Edwards [p. 570], "it is expected that spreads on bank loans and spreads on bonds will be determined in a different way, with the latter

224 IAER: MAY 2000, VOL. 6, NO. 2

being more sensitive to those variables, that, according to the theory, affect the level of country risk."

Edwards then estimated fixed-effects models for loans and bonds. The adjusted R 2 for loans was larger than that for bonds through several specifications. A SUR model was then run to directly compare the pricing of loans and bonds. Tests of equality of coefficients were conducted to see how different risk factors individually affect spreads on each instrument. Edwards was able to reject the null of equality for several variables, most prominently the ratio of investment to gross national product (GNP). Edwards emphasizes that the different coefficient for the investment-to-GNP ratio implies that loans and bonds are priced differently (the coefficient was larger in absolute value for loan spreads than for bonds).

What can be inferred from the results? The evidence would appear to support Gersovitz. In the panels, the coefficients on the loan equations are generally larger and often more significant than those for bonds. Moreover, the better fit to the loan model in terms of its adjusted R 2 would indicate that the risk variables employed affect loans more than bonds. Thus, it would appear that for the 1970s and early 1980s, the evidence presented by Edwards supports the notion that, for some reason, bonds were safer than loans. Does this mean that Folkerts-Landau was wrong? Not necessarily, for Folkerts- Landau was likely correct that loan rates do not incorporate full risk.

Certainly, deposit insurance and the fact that loans could be rescheduled make loans less risky than bonds. The caution one should have in interpreting results for the earlier 1970s inflow episode is that the LDC bond market of that period is not a proper yardstick against which to judge bank credit. That is because the bond market for developing countries in those years was very thin and, with the exception of a few small issues, such nations were largely rationed out of this market between the 1930s and the 1990s. As noted, the small amount of bond debt made bonds implicitly senior to loans. Failing to service bonds would not save much foreign exchange but would get one more set of creditors angry. Therefore, most nations, even those with serious debt problems, continued servicing bonds in the 1980s. Thus, it is perhaps not surprising that over the period of Edwards' estimation, bond rates do not seem to react as much to changing risk factors as do loans. The proper market to compare with loans, to see if the theories are valid on loans being less risky than debentures, is a liquid market with active trading of debt securities. This kind of market now exists for LDC bonds.

Bonds and Loans in the 1990s: An Empirical Investigation

As yet, there has been no investigation comparing loan and bond spread determinants in the 1990s. The differing effects of risk factors on each instrument are especially important in this instance and are of more consequence than understanding the functioning of a particular credit market. This is due to the fact that, as mentioned, most crises this decade involve liquidity rather than solvency. If bankers were the major creditors, such episodes could be avoided or at least ameliorated. However, this hypothesis depends on

MILES: BONDS VERSUS LOANS 225

bond spreads actually incorporating greater risk than loan prices. That is therefore empirically investigated.

To analyze the nature of the bond and loan markets for developing countries in the 1990s, the methodology of Feder and Just [1977], Edwards [1986], and Ozler [1992, 1993] will be taken as a starting point. The spread over the risk-free rate will be regressed for loans and bonds using panel estimation. This spread will be the annual average excess over the risk-free price of foreign currency credit for each country. 2 This is necessary as the regressors are only available annually. A SUR will then be run, and the hypothesis of coefficient equality will be formally tested across equations. The years covered are 1991 through 1994, the period just before Mexico's devaluation crisis. Thus, no crisis episodes distort estimation. The data for loan and bond spreads was obtained from Private Market Financing for Developing Countries [International Monetary Fund (IMF), 1995]. All obligations are medium- and long-term (at least one year). Data on the regressors was obtained from WorldDebt Tables [World Bank, various] and International Financial Statistics [IMF, various].

The explanatory variables employed are similar to those utilized previously in the literature. The first is imports as a percentage of GNP. This is a measure of openness to world trade. A country more open to trade will have more incentive to repay as openness implies dependence on the world trade system. Default could mean being shut out of future borrowing, and the more open the economy, the more painful this shut-out will be. This reasoning is in line with the Eaton-Gersovitz [1981] theory. However, Edwards refers to Frenkel [1983] and notes that an open economy is more subject to external shocks, which could interfere with the willingness and ability to repay. Thus, the sign of this coefficient is not completely clear a priori.

The second independent variable is investment as a fraction of GDP. Following Cooper and Sachs [1985], the more a country invests, the more future output it will have that it can commit to repayment. Investment thus serves as a signal that the country is undertaking sound projects with its borrowings and will be able to meet its obligations. The hypothesized sign of this coefficient is negative. That is, more investment as a fraction of output should, other variables constant, lower the spread a country must pay for funds.

The next two regressors are liquidity measures: reserves to output and debt service as a fraction of exports. Since the bonds and loans in question are denominated in hard currency, reserves as a fraction of GNP provides a measure of the funds available to service payments coming due in the immediate future. The hypothesized sign on this variable is negative. Exports are the main method of gaining foreign exchange, so debt service as a fraction of exports provides a measure of how burdensome current payments are on a nation's capacity to avoid arrears. The hypothesized sign is positive. It will be interesting to note the differential impact, if any, on loan and bond rates.

Per capita GNP also enters as an explanatory variable. Ozler [1993] has employed per capita income as a measure of a country's development. The more wealthy a country is, all else equal, the less likely it is to default. For banks, a wealthy country that gets into repayment problems is more likely to be a customer that the institution will have future

226 IAER: MAY 2000, VOL. 6, NO. 2

dealings with and will want to retain. Thus, it will be more likely to enter into negotiations with this country and reschedule. On the other hand, a poor nation is more likely to be written off by the bank. Knowing this in advance, it is hypothesized that poorer countries will pay a higher spread.

A dummy variable has been added for those nations that took part in the Brady debt resolution plans. These agreements lowered either the principal or the interest or both received by lending banks. Banks were thus "burned" by such countries. Ozler [1993] documented the effect of 1930s defaults on 1970s bank spreads. She found that those developing countries which had failed to repay bond obligations in the midst of the depression were charged higher rates, even when controlling for other factors such as reserves and per capita GDP. Clearly then, a country which had failed to repay in the recent past will be perceived as a greater risk, and the hypothesized sign of this dummy is positive.

Finally, for bonds only, dummies representing private placements and issues by public entities were employed. There are three categories of bonds defined by the IMF: sovereign, public sector, and private. During the debt crisis, the central governments of nations such as Argentina and Chile assumed the debt of private companies. For some nations, there may have been little difference between public and private debt. However, most of the modern capital flows are to private enterprises and it may not be realistic to believe that governments will assume them. Thus, the hypothesized sign of the private and public dummy variables is positive.

Estimation and Results

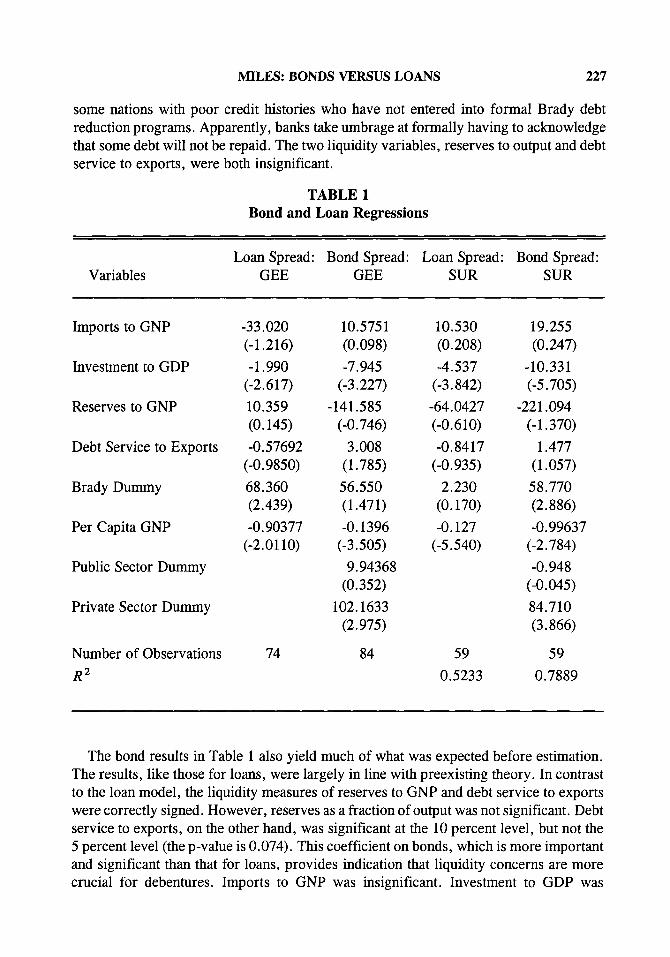

The results of the separate bond and loan regressions are shown in Table 1. The spreads are defined as the difference between the actual yield contracted and the prevailing yield on industrial country government bonds in the same currency and comparable maturity of the particular loan or bond. The average spread for a given country over a year is taken as the dependent variable. This is necessary as the regressors are available only annually. The panel technique employed is the generalized estimating equation (GEE) estimator, pioneered by Zeger and Liang [1986]. Standard errors are estimated using White's [1980] heteroskedasticity-consistent covariance matrix. This contrasts with Edwards who used fixed-effects estimation. The GEE estimator is robust to nonnormality and autocorrelation however. Moreover, use of the fixed-effects technique would preclude investigating the impact of the Brady deal on spreads since this dummy could not be included in a fixed-effects regression (it will be perfectly correlated with the fixed-effect intercept).

The results for loans indicate confirmation of most of the a priori hypotheses. Imports affect the spread negatively, although their effect is not quite significant at the 20 percent level. Investment as a fraction of gross domestic product (GDP) also lowers the spread, and the coefficient is significant at the 5 percent level. Per capita GNP decreases the interest cost and has a significant parameter estimate. Brady debt reduction clearly raises the rate paid for loans, as expected. This is somewhat interesting as the sample included

MILES: BONDS VERSUS LOANS 227

some nations with poor credit histories who have not entered into formal Brady debt reduction programs. Apparently, banks take umbrage at formally having to acknowledge that some debt will not be repaid. The two liquidity variables, reserves to output and debt service to exports, were both insignificant.

TABLE 1 Bond and Loan Regressions

Loan Spread: Bond Spread: Loan Spread: Bond Spread: Variables GEE GEE SUR SUR

Imports to GNP -33.020 10.5751 10.530 19.255 (-1.216) (0.098) (0.208) (0.247)

Investment to GDP - 1.990 -7.945 -4.537 - 10.331 (-2.617) (-3.227) (-3.842) (-5.705)

Reserves to GNP 10.359 -141.585 -64.0427 -221.094 (0.145) (-0.746) (-0.610) (-1.370)

Debt Service to Exports -0.57692 3.008 -0.8417 1.477 (-0.9850) (1.785) (-0.935) (1.057)

Brady Dummy 68.360 56.550 2.230 58.770 (2.439) (1.471) (0.170) (2.886)

Per Capita GNP -0.90377 -0.1396 -0.127 -0.99637 (-2.0110) (-3.505) (-5.540) (-2.784)

Public Sector Dummy 9.94368 -0.948 (0.352) (-0.045)

Private Sector Dummy 102.1633 84.710 (2.975) (3.866)

Number of Observations 74 84 59 59

R 2 0.5233 0.7889

The bond results in Table 1 also yield much of what was expected before estimation. The results, like those for loans, were largely in line with preexisting theory. In contrast to the loan model, the liquidity measures of reserves to GNP and debt service to exports were correctly signed. However, reserves as a fraction of output was not significant. Debt service to exports, on the other hand, was significant at the 10 percent level, but not the 5 percent level (the p-value is 0.074). This coefficient on bonds, which is more important and significant than that for loans, provides indication that liquidity concerns are more crucial for debentures. Imports to GNP was insignificant. Investment to GDP was

228 IAER: MAY 2000, VOL. 6, NO. 2

negative and significant, as expected. Also, the magnitude, in absolute value, was substantially higher than for loans, as can be observed. Per capita GNP has a statistically significant impact, and while the Brady Plan is correctly signed, it is only significant at the 15 percent level.

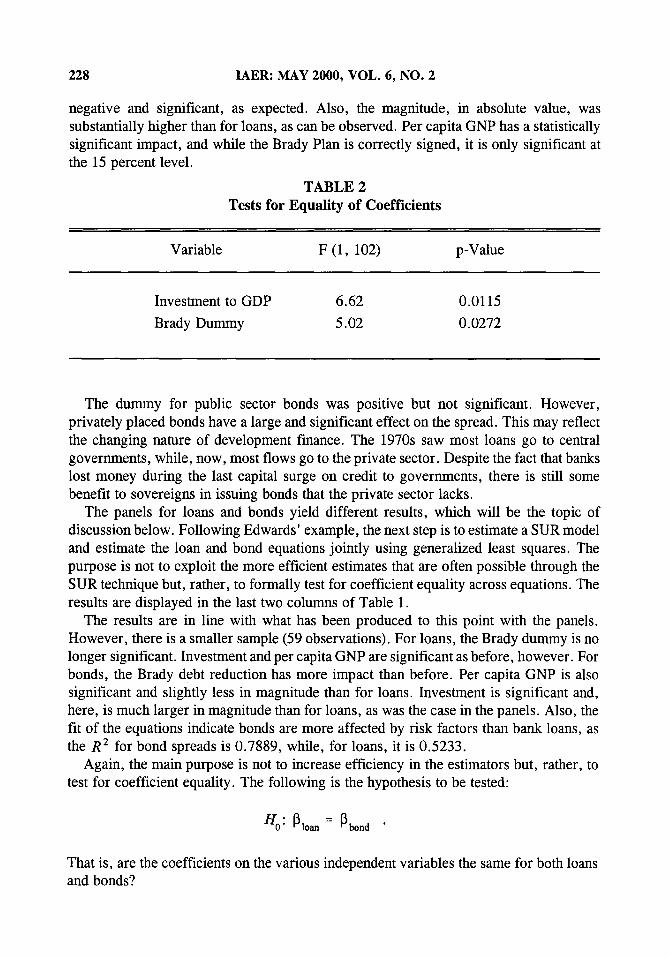

TABLE 2 Tests for Equality of Coefficients

Variable F (1, 102) p-Value

Investment to GDP 6.62 0.0115

Brady Dummy 5.02 0.0272

The dummy for public sector bonds was positive but not significant. However, privately placed bonds have a large and significant effect on the spread. This may reflect the changing nature of development finance. The 1970s saw most loans go to central governments, while, now, most flows go to the private sector. Despite the fact that banks lost money during the last capital surge on credit to governments, there is still some benefit to sovereigns in issuing bonds that the private sector lacks.

The panels for loans and bonds yield different results, which will be the topic of discussion below. Following Edwards' example, the next step is to estimate a SUR model and estimate the loan and bond equations jointly using generalized least squares. The purpose is not to exploit the more efficient estimates that are often possible through the SUR technique but, rather, to formally test for coefficient equality across equations. The results are displayed in the last two colunms of Table 1.

The results are in line with what has been produced to this point with the panels. However, there is a smaller sample (59 observations), For loans, the Brady dummy is no longer significant. Investment and per capita GNP are significant as before, however. For bonds, the Brady debt reduction has more impact than before. Per capita GNP is also significant and slightly less in magnitude than for loans. Investment is significant and, here, is much larger in magnitude than for loans, as was the case in the panels. Also, the fit of the equations indicate bonds are more affected by risk factors than bank loans, as the R 2 for bond spreads is 0.7889, while, for loans, it is 0.5233.

Again, the main purpose is not to increase efficiency in the estimators but, rather, to test for coefficient equality. The following is the hypothesis to be tested:

/-/0: : 13bond

That is, are the coefficients on the various independent variables the same for both loans and bonds?

MILES: BONDS VERSUS LOANS 229

The test for each individual parameter is an F-test. The test statistics for investment and the Brady plan are shown in Table 2. The null hypothesis of equality cannot be rejected at the 5 percent level for the parameters on imports, debt service, reserves, and per capita GNP. The hypothesis of equality can be rejected for the Brady dummy, with bonds being more affected.

Moreover and in keeping with previous empirical studies, the null of equality for the investment coefficient can be rejected. Capital accumulation from output has played a role in determining creditworthiness in Cooper and Sachs [1985] and Edwards [1984]--the higher the level of the former, the higher the level of the latter. The greater investment in the present, the greater output will be in the future and, thus, the more a country has to lose from sanctions in the event of default. The bond market is clearly more sensitive than the loan market in this regard. Thus, loans and bonds for emerging markets are priced differently.

It can clearly be concluded that for the 1990s, unlike the 1970s, bonds are more risky than loans. Whatever financial efficiency interpretation one may draw, it is clearly the case that bondholders do not make provisions for renegotiation and withdraw quickly from markets in times of crisis. Is this new development a positive one for developing countries? The experience of this decade does not merit an unambiguous answer. Bonds flow to many countries unable to obtain bank credit, and this is clearly a positive development. However, in the event of a crisis, just when external funds have their highest marginal value, bond funding is prone to suddenly drying up. Banks, on the other hand, have shown a willingness to work with debtors experiencing liquidity difficulties.

Conclusions

A vital difference between the inflows of capital to developing countries in the 1970s and 1990s is in the main financial form taken by such investment. In the previous period, bank loans predominated, while, in the present decade, securities (but mostly bonds) have played the major role. The last episode ended after a dramatic increase in interest rates was coupled with very large changes in the prices of commodities, upon which LDCs depend to generate funds for repayment. While there have been changes in interest rates and commodity prices in the 1990s, they were not (prior to such episodes as those in Mexico in 1994 and Asia in 1997) nearly as dramatic as those observed during the last debt crisis. Thus, the observed volatility in financial markets this decade partly results from the security nature of the new investment. In particular, how loans and bonds are priced gives insight into how investors and countries become vulnerable to crisis.

If markets were complete, loans and bonds would be identical instruments. They are clearly different forms of credit however, and estimation here has revealed that they are priced to reflect different levels of risk. As studies of earlier periods have discovered, loans and bonds are priced differently in the 1990s. However, the evidence allows drawing the further inference that loans to LDCs reflect less risk than bonds. The growth in bonds for developing countries in the 1990s has led to a market that functions like a traditional market for debentures, pricing risk to more fully reflect the probability of

230 IAER: MAY 2000, VOL. 6, NO. 2

default than banks do. However, this does not imply that bonds are better for emerging markets since banks, in their traditional role of relationship lenders, are more likely to work with nations undergoing financial difficulties.

The policy implications of this development in emerging market finance are not yet clear. Certainly, banning the issue of bonds or crude capital controls are not advocated. Also, it is certainly the case that economic fundamentals have played their role in the volatility of the 1990s. However, policymakers, when making decisions based on their country's financial vulnerability, will want to look at the composition of debt relative to reserves and other measures, not just in the sense of maturity, but how much is owed to institutions and how much is held by dispersed bondholders. A nation's reserve position, for instance, may look relatively safe if overall foreign debt is not high, but it may be at greater risk if most of the obligations are in bond form. Those in charge of monetary and fiscal policy should thus be aware of how security obligations can change their vulnerability to crisis. Actual policy prescriptions are a topic for further research, but it is clear that the new era of bond finance in emerging markets is a very different one than that which prevailed in the bank loan era of the 1970s,

Footnotes

.

2.

For information on loan and bond composition, equity and other capital flows to emerging market countries, and returns on various categories of capital, see IMF [1995, pp. 71-9]. The countries in the sample were Algeria, Argentina, Bahrain, Barbados, Brazil, Chile, China, Columbia, Costa Rica, Czech Republic, Egypt, Hong Kong, Hungary, India, Indonesia, Ivory Coast, Korea, Kuwait, Lesotho, Liberia, Macao, Malaysia, Malta, Mauritius, Mexico, Morocco, Oman, Pakistan, Panama, Philippines, Poland, Quatar, Romania, Russia, Singapore, Slovenia, South Africa, Taiwan, Thailand, Tunisia, Trinidad and Tobago, Turkey, United Arab Emirates, Uruguay, Uzbekistan, Venezuela, Vietnam, and Zimbabwe.

References

Chang, Roberto; Velasco, Andres. "Financial Crises in Emerging Markets: A Canonical Model," Federal Reserve Bank of Atlanta, working paper, 98-10, March 1998.

Chemmanur, Thomas; Fulghieri, Paolo. "Reputation, Renegotiation and the Choice Between Bank Loans and Publicly Traded Debt," Review of Financial Studies, 7, 3, Fall 1994, pp. 475-506.

Cline, William. International Debt Reexamined, Washington, DC: Institute for International Economics, 1995.

Cooper, Richard; Sachs, Jeffrey. "Borrowing Abroad: The Debtor's Perspective," in Gordon Smith; John Cuddington, eds.,InternationalDebt and the Developing Countries, Washington, DC: World Bank, 1985, pp. 21-60.

Diamond, Douglas. "Monitoring and Reputation: The Choice Between Bank Loans and Directly Placed Bonds, Journal of Political Economy, 99, 3, August 1991, pp. 689-719.

Eaton, Jonathan; Gersovitz, Mark. "Debt with Potential Repudiation: Theoretical and Empirical Analysis," Review of Economic Studies, 48, 152, April 1981, pp. 289-309.

MILES: BONDS VERSUS LOANS 231

Edwards, Sebastian. "LDC Borrowing and Foreign Default Risk: An Empirical Analysis, "American Economic Review, 74, 4, September 1984, pp. 726-34.

. "The Pricing of Bonds and Loans in International Markets: An Empirical Analysis of Developing Countries' Foreign Borrowing," European Economic Review, 30, 3, June 1986, pp. 565-89.

Fama, Eugene. "What's Different About Banks?," Journal of Monetary Economics, 15, 1, January 1985, pp. 29-39.

Feder, Gershon; Just, Richard E. "An Analysis of Credit Terms in the Eurodollar Market," European Economic Review, 9, 2, May 1977, pp. 221-43.

Folkerts-Landau, David. "The Changing Role of International Bank Lending in Development Finance," IMF Staff Papers, 32, 2, June 1985, pp. 316-33.

Frenkel, Jacob. "International Liquidity and Monetary Control," in George von Furstenburg, ed., International Money and Credit: The Policy Roles, Washington DC: International Monetary Fund, 1983, pp. 65-109.

Gersovitz, Mark. "Banks' International Lending Decisions: What We Know and Implications for Future Research," in Gordon Smith; John Cuddington, eds., International Debt and the Developing Countries, Washington DC: World Bank, 1985, pp. 61-78.

International Monetary Fund. Private Market FinancingforDeveloping Countries, Washington, DC: IMF, November 1995, pp. 70-84.

k . International Financial Statistics, Washington DC: IMF, various. Ozler, Sule. "The Evolution of Credit Terms: An Empirical Study of Commercial Bank Lending to

Developing Countries," Journal of Development Economics, 38, 1, January 1992, pp. 79-97. n - "Have Commercial Banks Ignored History?," American Economic Review, 83, 3, June 1993,

pp. 608-20. Sachs, Jeffrey; Tornell, Aaron; Velasco, Andres. "The Collapse of the Mexican Peso: What Have

We Learned,"NBER Working Papers, 4142, June 1996. White, Halbert. "A Heteroskedastic-Consistent Covariance Matrix Estimator and a Direct Test for

Heteroskedasticity," Econometrica, 48, 1980, pp. 817-38. World Bank. World Debt Tables, Washington, DC: World Bank, various. Zeger, Scott L.; Liang, Kung-Yee. "Longtitudinal Data Analysis for Discrete and Continuous

Outcomes," Biometrics, 42, 1, March 1986, pp. 121-30.

![Junk Bonds & Bridge Loans Presentation[1]](https://img.pdfslide.net/doc/110x75/577d33f61a28ab3a6b8c38a6/junk-bonds-bridge-loans-presentation1.jpg)