Embed Size (px)

Citation preview

The Rise of the Hybrid Consumer

Mid-market beware

Rabobank International

Food & Agribusiness Research and Advisory

www.rabotransact.comwww.rabobank.com/f&a

Author :Marc Kennis

[email protected]+31 30 71 23179

The Rise of the Hybrid Consumer

Disclaimer: This document is issued by Coöperatieve Centrale Raiffeisen-Boerenleenbank B.A. incorporated in the Netherlands, trading asRabobank International (“RI”). The information and opinions contained in this document have been compiled or arrived at from sourcesbelieved to be reliable, but no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness. This document is for information purposes only and is not, and should not be construed as, an offer or a commitment by RI or any of itsaffiliates to enter into a transaction, nor is it professional advice. This information is general in nature only and does not take into account an individual’s personal circumstances. All opinions expressed in this document are subject to change without notice. Neither RI, nor otherlegal entities in the group to which it belongs, accept any liability whatsoever for any loss howsoever arising from any use of this documentor its contents or otherwise arising in connection therewith. This document may not be reproduced, distributed or published, in whole or in part, for any purpose, except with the prior written consent of RI. All copyrights, including those within the meaning of the DutchCopyright Act, are reserved. Dutch law shall apply. By accepting this document you agree to be bound by the foregoing restrictions. © Rabobank International Utrecht Branch, Croeselaan 18, 3521 CB, Utrecht, the Netherlands +31 30 216 0000

Mid-market beware

Contents | i

ContentsPage

Section 1

The rise of the hybrid consumer: Mid-market beware! . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Section 2

Market dualisation is largely attributable to hybrid consumer behaviour . . . . . . . . . . . . . . . . . . . . 3

The beer market as an example . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

Section 3

Hybrid consumption is driven by socio-demographic changes, retailers’ strategies

and macroeconomic developments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

Socio-demographics: Women and Millennials are the predominant drivers of hybrid consumption 5

Women’s improving purchasing power and influence over household spending . . . . . . . . . . . . . . . . 5

Increasing labour market penetration . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

Narrowing of the gender pay gap . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

Generations Y and Z: More hybrid in their spending patterns . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

Millennials an increasingly dominant factor . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

Food retailers’ strategies facilitate and stimulate hybrid spending patterns . . . . . . . . . . . . . . . . . . . . . . . 8

The social acceptance to shop at hard discounters . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

Increasing penetration of private label . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

The role of the internet . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

How successful are retailers that target the extreme ends of the market? . . . . . . . . . . . . . . . . . . . . . . . 10

Recent macroeconomic developments reinforce hybrid consumption patterns . . . . . . . . . . . . . . . . . . . 11

EU growth sluggish in 2013 and muted in the longer term . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

The US first to emerge from the ruins of the crisis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

Budget-induced down trading will continue in Europe . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

Section 4

Hybrid consumption is a secular phenomenon: The hybrid consumer is here to stay! . . . . . . . . . 15

Section 5

Standard mid-market products will lose out . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

Section 6

Adapt or fade away? Strategic action required . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

The continued need to distinguish . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

Shifting distribution channels: From foodservice to retail to online . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

A different marketing approach: Behavioural segmentation of consumers . . . . . . . . . . . . . . . . . . . . . . 19

Danger of brand erosion by perception . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

Capturing the hybrid opportunity: Strategies and tactics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

Cluster I: The consumer and product positioning . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

Smarter marketing to gain share of the hybrid consumer’s wallet . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

Need for more active brand management . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

Premiumisation to address the high end of the market . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

Reverse positioning within a segment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

The best of both worlds: A hybrid product offering . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

Category domination: Covering the entire category . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

Two birds with one stone: Addressing several consumer issues at once . . . . . . . . . . . . . . . . . . . . . . . . . 23

Variations in package sizes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

Cluster II: Internal processes and priorities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

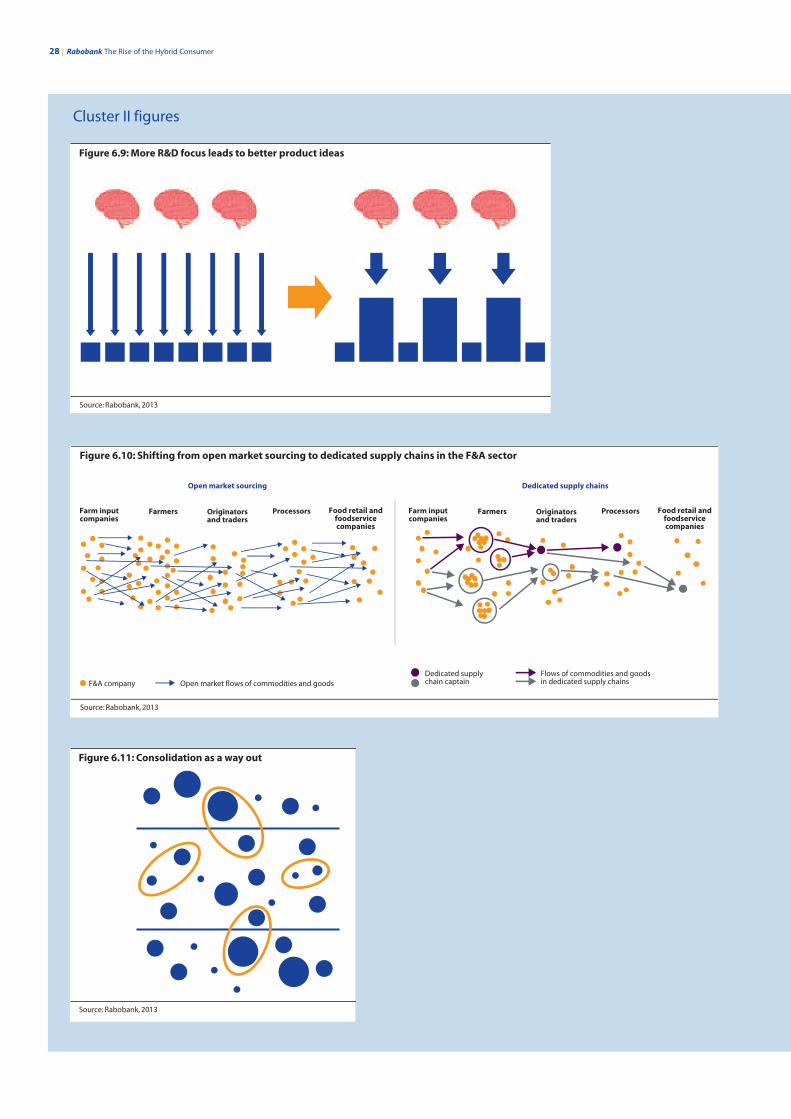

More focus within research and development programmes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

Value engineering: Same product, lower costs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

Transparency and cooperation to better leverage on the hybrid opportunity . . . . . . . . . . . . . . . . . . . 26

Aligning the supply chain . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

Consolidation as a way out . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

Conclusion: Mid-market beware of the hybrid consumer . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

Section 1 The rise of the hybrid consumer: Mid-market beware! | 1

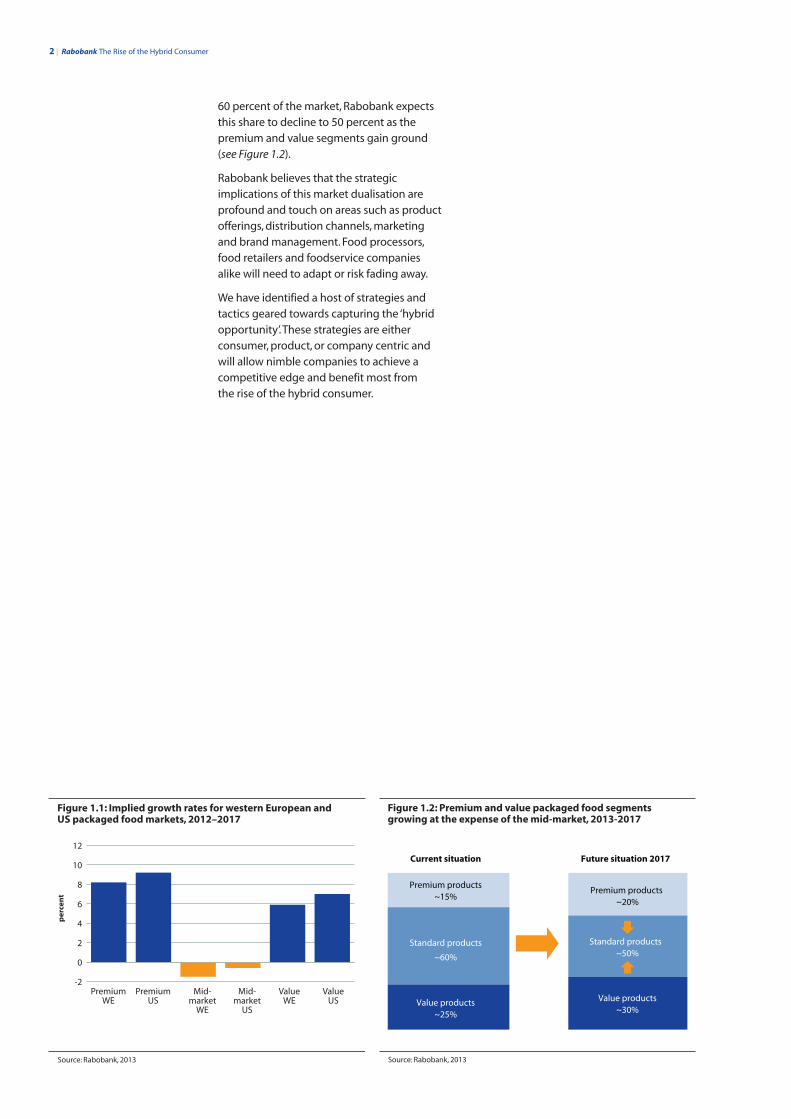

Rabobank expects the mid-market ofstandard, non-distinct food products todecline in the coming years as hybridconsumers increasingly opt for either basic,value products or more expensive, higherquality products at the premium end of theproduct spectrum. While the extreme ends of the market are set to grow by high single-digit numbers, we expect the mid-market to decline by 1 percent to 2 percent perannum through 2017.

Consumer preferences are as varied asconsumers themselves. Consumers havetraditionally been segmented into differentcategories based on their socio-demographiccharacteristics and historical spendingpatterns. A typical consumer spends theirhousehold food budget within one or maybetwo, adjacent, market segments (i.e. the value, mid-market or premium segment),depending on their social and financial status.

However, over the past decade we have seenconsumers moving towards the extreme endsof the spectrum, trading down to the valuesegment for basic everyday groceries whilesimultaneously trading up to the premiumsegment for socially and emotionally relevantproducts. As a result of this new consumptionpattern, the mid-market has been underpressure as products in this segment areperceived to offer neither quality nor value to today’s hybrid consumer.

Driving this hybrid behaviour are severalsocio-demographic developments, such as the increasing financial empowerment of women and the growing influence ofMillennials. Both groups have a relatively high tendency towards hybrid consumerbehaviour. Other drivers are related toretailers’ strategies that facilitate tradingdown and up more than in the past (e.g. through hard discount formats andprivate-label offerings). Finally, we believe that in recent years the prolonged economicdownturn in many developed markets hasaccelerated the existing market dualisation.

Going forward, we do not expect a reversal of the hybrid consumption trends as the maindrivers are of a long-term and secular nature(i.e. independent of economic cycles).Consequently, the growth rate of standardfood products in developed markets isexpected to substantially lag behind thegrowth rate of premium and value foodproducts in the next five years. While thelatter two segments are expected to grow by mid to high single-digit numbers through2017, Rabobank expects the market forstandard, non-distinct food products to benegative on average in developed markets in Europe and North America (See Figure 1.1).

These growth rate differentials will translateinto substantial shifts in market shares for the premium, mid-market and valuesegments of the overall food markets. Whilethe mid-market currently accounts for about

1 The rise of the hybrid consumer: Mid-market beware!

60 percent of the market, Rabobank expectsthis share to decline to 50 percent as thepremium and value segments gain ground(see Figure 1.2).

Rabobank believes that the strategicimplications of this market dualisation areprofound and touch on areas such as productofferings, distribution channels, marketingand brand management. Food processors,food retailers and foodservice companiesalike will need to adapt or risk fading away.

We have identified a host of strategies andtactics geared towards capturing the ‘hybridopportunity’. These strategies are eitherconsumer, product, or company centric andwill allow nimble companies to achieve acompetitive edge and benefit most from the rise of the hybrid consumer.

2 | Rabobank The Rise of the Hybrid Consumer

Figure 1.1: Implied growth rates for western European and US packaged food markets, 2012–2017

Source: Rabobank, 2013

per

cen

t

-2

0

2

4

6

8

10

12

ValueUS

ValueWE

Mid-market

US

Mid-market

WE

PremiumUS

PremiumWE

Figure 1.2: Premium and value packaged food segments growing at the expense of the mid-market, 2013-2017

Source: Rabobank, 2013

Premium products

Current situation Future situation 2017

Premium products ~15%

~20%

Standard products Standard products

~60% ~50%

Value productsValue products~30%~25%

Section 2 Market dualisation is largely attributable to hybrid consumer behaviour | 3

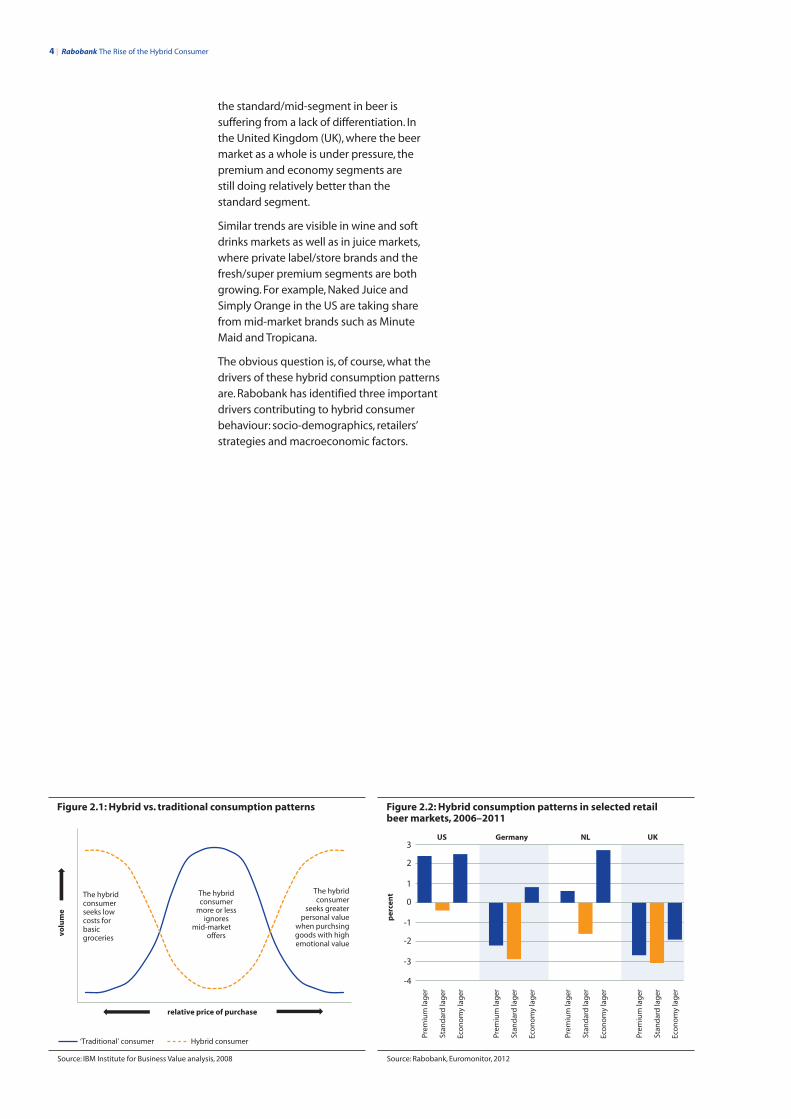

Life used to be easier for consumer-productmarketers when consumers fit nicely intodifferent categories based on criteria such as age, gender, education, income level andethnic background. However, over the pastdecade, the category boundaries havebecome blurred and a new type of consumerhas emerged: the hybrid consumer.

Hybrid consumers trade down in basicgrocery categories and trade up in productcategories that are socially and emotionallysignificant to them. Generally speaking, theseconsumers are moving towards the extremeends of product spectrums and away fromthe mid-market, as the latter is typicallyperceived to offer neither quality nor value.

Because hybrid consumers are less focusedon mid-market products and brands, they often trade down when it comes topurchasing everyday value-for-money items,such as basic groceries. However, these sameconsumers may use the money saved bytrading down to trade up to premium, high-end products that matter most from anemotional and social perspective, such asdesigner shoes, the latest smartphones, high-end coffee varieties, fine dining and premiumbrands in supermarkets (see Figure 2.1).

While some academic research on this topichas been done in recent years1, it is easy towitness the hybrid consumer in action on a daily basis as shopping at hard discountsupermarkets has become widely acceptablefor middle income households in developed

markets. Shopping at discount supermarketsis now commonplace for the majority ofconsumers and is even considered smartshopping. At the same time, many of thesesame consumers may use the money theysave to purchase premium products at higherend, retail formats.

This hybrid behaviour not only relates to thequestion of whether to trade up or down butalso to the choice of food category. Hybridconsumers may consciously choose to eathealthy and/or functional food at one mealoccasion and choose indulgent, less healthyfood and snacks at the next. In other words, it is not uncommon for the hybrid consumerto be a customer of both the high-endestablishment category, serving healthy or organic foods, and the quick servicerestaurant (QSR) category.

The beer market as an exampleA good example of hybrid consumptionpatterns is provided by the beverages market.Beer, for instance, is a relatively homogenousproduct compared to other food categories,and as such, the market data in selectedmarkets clearly illustrates hybridconsumption patterns. Economic motivesmay drive some consumers to trade down to economy lager, while other consumers witha strong preference for premium/craft beersare driving growth in this category, althoughthey may choose to trade down in another(see Figure 2.2). In the United States (US), theNetherlands and Germany, for instance,

2 Market dualisation is largely attributable tohybrid consumer behaviour

1 The Hybrid Consumer:

Exploring the Drivers of a New

Consumer Behaviour Type

(H. Leppanen and Chr. Gronroos, 2009).

4 | Rabobank The Rise of the Hybrid Consumer

the standard/mid-segment in beer is suffering from a lack of differentiation. In the United Kingdom (UK), where the beermarket as a whole is under pressure, thepremium and economy segments are still doing relatively better than the standard segment.

Similar trends are visible in wine and softdrinks markets as well as in juice markets,where private label/store brands and thefresh/super premium segments are bothgrowing. For example, Naked Juice and Simply Orange in the US are taking sharefrom mid-market brands such as Minute Maid and Tropicana.

The obvious question is, of course, what thedrivers of these hybrid consumption patternsare. Rabobank has identified three importantdrivers contributing to hybrid consumerbehaviour: socio-demographics, retailers’strategies and macroeconomic factors.

Figure 2.1: Hybrid vs. traditional consumption patterns

Source: IBM Institute for Business Value analysis, 2008

relative price of purchase

volu

me

The hybrid consumer

more or less ignores

mid-market offers

The hybrid consumer seeks low costs for basic groceries

‘Traditional’ consumer Hybrid consumer

The hybrid consumer

seeks greater personal value

when purchsing goods with high emotional value

Figure 2.2: Hybrid consumption patterns in selected retail beer markets, 2006–2011

Source: Rabobank, Euromonitor, 2012

per

cen

t

US Germany NL UK

-4

-3

-2

-1

0

1

2

3

Eco

no

my

lag

er

Stan

dar

d la

ger

Prem

ium

lag

er

Eco

no

my

lag

er

Stan

dar

d la

ger

Prem

ium

lag

er

Eco

no

my

lag

er

Stan

dar

d la

ger

Prem

ium

lag

er

Eco

no

my

lag

er

Stan

dar

d la

ger

Prem

ium

lag

er

Section 3 Hybrid consumption is driven by socio-demographic changes, retailers’ strategies and macroeconomic developments | 5

Consumer behaviour in general is influencedby many factors, including advertising andpromotions, peer pressure, social status,disposable income and, of course, individualconsumer preferences. We believe hybridconsumer behaviour is attributable to three main factors; socio-demographicdevelopments, food retailers’ strategies and, in part, macroeconomic developments.

Socio-demographics: Women andMillennials are the predominantdrivers of hybrid consumptionSeveral socio-demographic developmentshave been driving hybrid consumptionpatterns for a number of years. Morespecifically, these developments includewomen’s improving purchasing powercoupled with their increasing influence over household spending, and the growingimportance of younger generations inrelation to consumer spending as a whole.The long-term nature of these developmentsimplies that they will remain a driving forcefor years to come.

Women’s improving purchasing powerand influence over household spendingRabobank believes the combination of women’s increasing labour marketpenetration, the declining gender pay gap,the typical differences in shopping behaviourbetween men and women, and the increasing

influence of women over householdspending, play a crucial role in thedevelopment of hybrid consumption patterns in developed markets.

An Australian study revealed that “femalesappear more objective in their approach to important grocery store characteristics.Females tend towards price, discounts, value for money, consistent and competitiveprices as well as low, everyday prices.”2

Other research shows that a growing numberof women in developed markets areincreasingly involved in household purchasedecisions, ranging from small to big-ticketitems. For instance, on average, women in theUS control or influence more than 70 percentof household spending including spending3

on homes, cars, vacations, groceries andhealth care.

With this in mind, we believe a closer look at women’s empowerment in developedmarkets will provide a substantial part of theanswer to the question of who the hybridconsumer is.

Increasing labour market penetrationWhen looking at women’s participation in thelabour market over time, we can clearly seeupward trends in most developed markets(see Figure 3.1). The notable exception is in the US, where the rate has been declining formore than a decade. Historically, women’s

3 Hybrid consumption is driven by socio-demographic changes, retailers’ strategiesand macroeconomic developments

2 Gender Differences and Store

Characteristics: A Study of Australian

Supermarket Consumers,

Dr. Gary Mortimer, Queensland

University of Technology, Queensland,

Dr. Peter Clarke, Griffith University,

Queensland, 2010.

3 Boston Consulting Group, 2009.

6 | Rabobank The Rise of the Hybrid Consumer

participation in the US workforce has beenhigher than in other developed markets and,after having levelled off around the turn ofthe century, it has started to decline as babyboomers are entering retirement.

However, in most developed markets,women’s labour market participation is on the rise4. While we may see occasionalinterruptions of the rising trend (e.g. as aresult of economic crisis), going forward, weexpect further increases in the female labourmarket penetration rate, driven by structuralreforms to tax and benefit systems as well asreforms of labour laws and working hourlegislation in the EU, especially in geographiescoming from lower levels of participation,such as Germany and the UK.

Narrowing of the gender pay gapThe historical difference in remunerationbetween men and women, the so-calledgender pay gap, has been declining in manydeveloped markets, on the back of severalfactors, including increasing flexibility inworking arrangements (see Figure 3.2). The decline of the gender pay gap is a further contributor to women’s improvingpurchasing power.

Where does this leave men in the hybridconsumer discussion? While men willnaturally remain an important consumergroup in general, Rabobank believes womenspecifically are an important driver of hybridconsumption patterns because of the typicaldifferences in shopping behaviour betweenmen and women and the increasing influenceof women over household spending. Thecombination of an increasing penetration of the labour market by women and thedeclining gender pay gap play a crucial role

in the development of hybrid consumptionpatterns in developed markets, in our view.

Generations Y and Z: More hybrid in theirspending patternsDemographics also play a part in the rise ofthe hybrid consumer. Often more concernedwith the specs of the latest iPhone thanwhere exactly they will eat their next meal,Generation Y, born between 1980 and themid-1990s, and Generation Z, born starting inthe early to mid-1990s, will increasingly play arole in hybrid consumption patterns. Forexample, trading down and saving money onbasic groceries allows Generation Y to spendmore money on ‘socially relevant’ products aswell as on the occasional dinner party andfood out-of-home. The latter could includevalue-for-money fast food as well as premiumfood-on-the-go or dining at high-endrestaurants.

Rabobank believes Generations Y and Z, alsoknown as Millennials, will take the hybridconsumption trend to the next level. Forinstance, while growing up with social mediahas increased brand awareness for thesegenerations it has also reduced brand loyalty,in part facilitated by the proverbialabundance of ‘like’ buttons on the internet.For the most part, Millennials rate products on merits rather than on the specific brandthe product is labelled with. At the same time,they are generally more health-conscious and environmentally aware than previousgenerations were at the same age, andconvenience is also highly valued. In terms ofproduct attributes, these generations look forconvenience, health and sustainability, whichtranslate into premium, and thus higherpriced, products.

4 European Central Bank, Monthly

Bulletin, June 2012.

Figure 3.1: Female labour participation rate in developed markets, 2000–2010

Australia US

Source: World Bank, Rabobank, 2013

UK Germany Netherlands

48

50

52

54

56

58

60

201020052000

per

cen

t

Figure 3.2: The gender pay gap in select countries (gap as percentage of male remuneration), 2006–2010

Source: Australian Bureau of Statistics, Eurostat, US Census Bureau, Rabobank, 2013

15

16

17

18

19

2021

22

23

24

25

20102009200820072006

per

cen

t

AustraliaUSUKNetherlandsFranceSpainGermanyEU

Section 3 Hybrid consumption is driven by socio-demographic changes, retailers’ strategies and macroeconomic developments | 7

However, Millennials’ purchasing power is notat full strength yet as Generation Y is makingits second or third career step, whileGeneration Z is largely still busy getting aneducation or building work experience.Therefore, in order to be able to trade up inthe socially and emotionally relevant productcategories, it is necessary to trade down inothers. Consequently, Rabobank believesthese generations are more likely to be hybridin their consumption patterns than earliergenerations, which creates challenges andopportunities for food processors, retailersand foodservice companies.

Millennials an increasingly dominant factorLooking forward five to ten years, asGeneration Y moves up the career ladder and Generation Z enters the labour market,Rabobank expects Millennials to have aserious impact on consumer spending. Astheir purchasing power increases, so willoverall hybrid consumption patterns.

However, the exact impact going forward willdiffer from country to country, depending onthe composition of the population. In the US,

for instance, we expect Millennials to be avery dominant, if not the most dominant, agegroup by 2020, which is largely attributable tothe relatively large influx of young migrants(see Figure 3.3).

In the UK, the projected composition of thepopulation is somewhat more ambiguous,with Generation Y being one of the largestage groups by 2020 (see Figure 3.4). However,Generation Z is projected to be smaller than Generation Y.

The situation in Germany is quite different.After a peak in the birth rate in the early1960s, population growth has continued to slide, resulting in Germany’s currentpopulation being the second-oldest in theworld after Japan’s. Even though Millennials in Germany will gain in relative dominance as the population ages over time, Germanbaby boomers will still be the dominant agegroup by 2020.

Even though the extent to which Millennialswill increase their dominance in thecomposition of populations will vary fromone country to another, their influence onconsumer spending as a whole will increase

Figure 3.3: US population tree

1990 2012 2020

0

5,00

0,00

0

10,0

00,0

00

15,0

00,0

00

20,0

00,0

00

25,0

00,0

00 0

5,00

0,00

0

10,0

00,0

00

15,0

00,0

00

20,0

00,0

00

25,0

00,0

00 0

5,00

0,00

0

10,0

00,0

00

15,0

00,0

00

20,0

00,0

00

25,0

00,0

00

Source: US Census Bureau, Rabobank, 2013

10-14

20-24

30-34

40-44

50-54

60-64

70-74

80-84

90-94

100+

10-14

20-24

30-34

40-44

50-54

60-64

70-74

80-84

90-94

100+

10-14

20-24

30-34

40-44

50-54

60-64

70-74

80-84

90-94

100+

Generation Y

Generation Y

Generation Z

Generation Y

Generation Z

Hybrid consumer behaviour ... is it a middle class thing?When considering hybrid consumer spending in a context of social classes, the initial view might be that hybrid spendingis mostly a middle class phenomenon. After all, consumers need to have the financial means to trade up, which the lowestincome group generally does not have. Alternatively, the highest income group has no financial incentive to trade down.Consequently, one might conclude that hybrid spending must be a middle class phenomenon.

However, according to recent data from Kantar Media TGI, lower income groups are known to be big on brands, while inGermany, for example, more than 30 percent of people within the highest income group regularly shop at hard discounters.

At the end of the day, we believe most consumers are likely to be hybrid in their spending patterns to some extent,regardless of how much money they make.

8 | Rabobank The Rise of the Hybrid Consumer

across the board given their increasing shareas a percentage of the total population.

Therefore, Rabobank believes food processors,retailers and foodservice companies need tomake it a point to include hybrid consumptionpatterns stemming from the rising dominance ofMillennials in their overall corporate strategies.

Food retailers’ strategies facilitate andstimulate hybrid spending patternsA very interesting aspect of hybrid spendingpatterns is the way in which food retailershave developed their business models overthe years. Rabobank believes that, to a largeextent, retailers’ strategies have facilitatedhybrid consumption patterns. The advent of the hard discounter, for instance, added to consumers’ options to trade down as didthe growing private-label offering. In recentyears, private label has also expanded into the premium segment and now alsofacilitates up-trading. Another more recentdevelopment is the role of the internet in grocery shopping.

The social acceptance to shop at hard discountersRabobank believes the growing dominanceof hard discounters, and more specifically, themiddle-class social acceptance of shopping athard discounters, has played a crucial role infacilitating consumers’ trading down in thebasic grocery category.

Hard discounters—not to be confused withbargain stores, such as Walmart in the US,which typically have 20 times more stock-keeping units (SKUs) compared to harddiscounters—have been active and growingin many developed markets for at least adecade. Over the years, the clientele thatfrequents these outlets has become very

diverse, ranging from the lowest to thehighest income groups. For instance, inGermany, hard discounters account for 43 percent of the market in the lowest incomequartile and 34 percent in the highest.5

In our view, in order for hard discounters to account for one-third of this market,shopping at discounters has not only becomecommonplace for all income groups but it has also become socially accepted among the higher income groups.

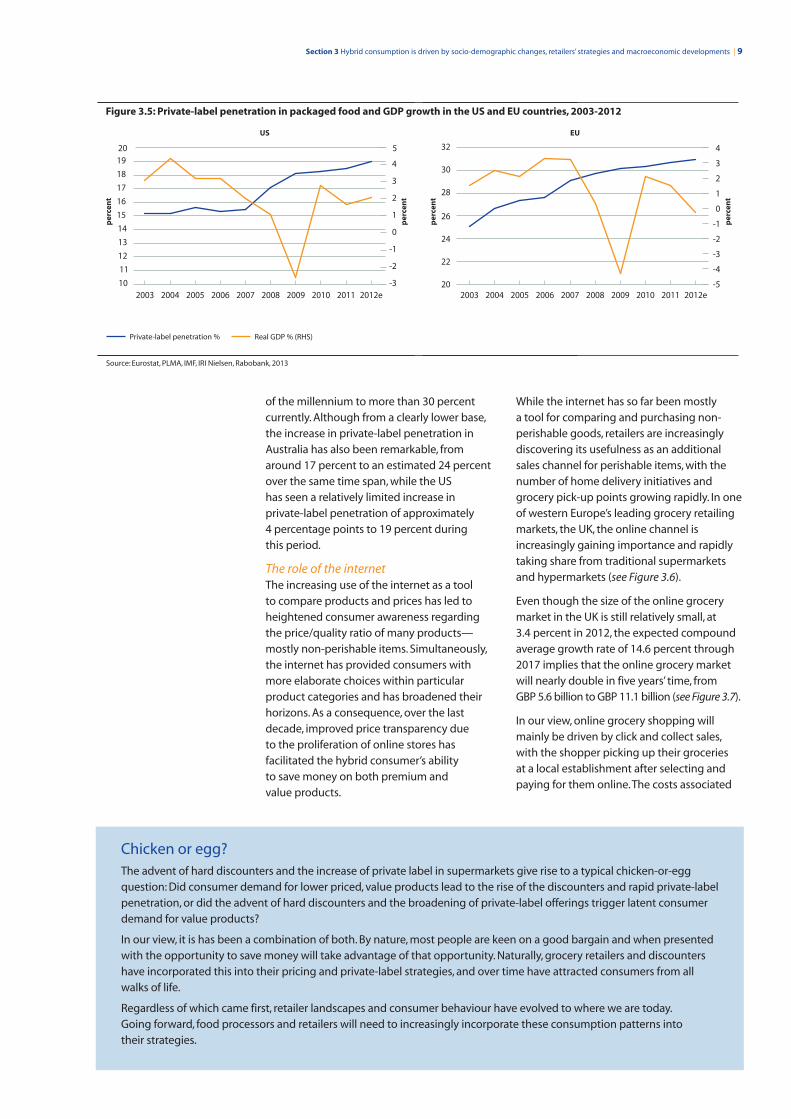

Increasing penetration of private labelAn equally important development in foodretailers’ strategies has been the increase ofprivate-label penetration in supermarkets,particularly in western Europe (see Figure 3.5).As an addition to A and B brands, privatelabels in supermarkets provide consumerswith different choices, especially in the midand value segments of various productcategories. Consumers thus have moreoptions to trade down from B brands toprivate label without necessarilycompromising on quality.

While private label was initially gearedtowards the value end of the productspectrum, in recent years, private label hasexpanded to the premium end of thesupermarket shelves. As a result, private labelnow not only facilitates down-trading butalso increasingly allows consumers to tradeup to the premium food category. This isparticularly apparent at full service andupmarket retailers that now increasinglyenable hybrid consumers to trade up through premium private-label products.

The share of private label in packaged food in western European supermarkets rose fromapproximately 25 percent around the turn

5 Harvard Business Review, 2009.

Figure 3.4: UK population tree

1990 2012 2020

Source: US Census Bureau, Rabobank, 2012

0

1,00

0,00

0

2,00

0,00

0

3,00

0,00

0

4,00

0,00

0

5,00

0,00

0 0

1,00

0,00

0

2,00

0,00

0

3,00

0,00

0

4,00

0,00

0

5,00

0,00

00

1,00

0,00

0

2,00

0,00

0

3,00

0,00

0

4,00

0,00

0

5,00

0,00

0

6,00

0,00

0

10-14

20-24

30-34

40-44

50-54

60-64

70-74

80-84

90-94

100+

10-14

20-24

30-34

40-44

50-54

60-64

70-74

80-84

90-94

100+

10-14

20-24

30-34

40-44

50-54

60-64

70-74

80-84

90-94

100+

Generation Y

Generation Y

Generation Z

Generation Y

Generation Z

Section 3 Hybrid consumption is driven by socio-demographic changes, retailers’ strategies and macroeconomic developments | 9

of the millennium to more than 30 percentcurrently. Although from a clearly lower base,the increase in private-label penetration inAustralia has also been remarkable, fromaround 17 percent to an estimated 24 percentover the same time span, while the US has seen a relatively limited increase inprivate-label penetration of approximately 4 percentage points to 19 percent during this period.

The role of the internetThe increasing use of the internet as a tool to compare products and prices has led toheightened consumer awareness regardingthe price/quality ratio of many products—mostly non-perishable items. Simultaneously,the internet has provided consumers withmore elaborate choices within particularproduct categories and has broadened theirhorizons. As a consequence, over the lastdecade, improved price transparency due to the proliferation of online stores hasfacilitated the hybrid consumer’s ability to save money on both premium and value products.

While the internet has so far been mostly a tool for comparing and purchasing non-perishable goods, retailers are increasinglydiscovering its usefulness as an additionalsales channel for perishable items, with thenumber of home delivery initiatives andgrocery pick-up points growing rapidly. In oneof western Europe’s leading grocery retailingmarkets, the UK, the online channel isincreasingly gaining importance and rapidlytaking share from traditional supermarketsand hypermarkets (see Figure 3.6).

Even though the size of the online grocerymarket in the UK is still relatively small, at 3.4 percent in 2012, the expected compoundaverage growth rate of 14.6 percent through2017 implies that the online grocery market will nearly double in five years’ time, from GBP 5.6 billion to GBP 11.1 billion (see Figure 3.7).

In our view, online grocery shopping willmainly be driven by click and collect sales,with the shopper picking up their groceries at a local establishment after selecting andpaying for them online. The costs associated

Figure 3.5: Private-label penetration in packaged food and GDP growth in the US and EU countries, 2003-2012

Private-label penetration % Real GDP % (RHS)

Source: Eurostat, PLMA, IMF, IRI Nielsen, Rabobank, 2013

20

22

24

26

28

30

32

2012e201120102009200820072006200520042003

per

cen

t

EUUS

10

11

12

13

14

15

16

17

18

1920

2012e201120102009200820072006200520042003

per

cen

t

per

cen

t

per

cen

t

-5

-4

-3

-2

-1

0

1

2

3

4

-3

-2

-1

0

1

2

3

4

5

Chicken or egg?The advent of hard discounters and the increase of private label in supermarkets give rise to a typical chicken-or-eggquestion: Did consumer demand for lower priced, value products lead to the rise of the discounters and rapid private-labelpenetration, or did the advent of hard discounters and the broadening of private-label offerings trigger latent consumerdemand for value products?

In our view, it is has been a combination of both. By nature, most people are keen on a good bargain and when presentedwith the opportunity to save money will take advantage of that opportunity. Naturally, grocery retailers and discountershave incorporated this into their pricing and private-label strategies, and over time have attracted consumers from allwalks of life.

Regardless of which came first, retailer landscapes and consumer behaviour have evolved to where we are today. Going forward, food processors and retailers will need to increasingly incorporate these consumption patterns into their strategies.

10 | Rabobank The Rise of the Hybrid Consumer

with home delivery of groceries that areordered online are relatively high comparedto purchasing the same items insupermarkets or through click and collectservices. For instance, in the Netherlands,delivery costs can be as high as EUR 12.95 fora shopping basket with a minimal value ofEUR 70. Therefore, we expect home deliveryservices to be adopted by the masses onlyonce delivery costs fall to levels acceptable to the mainstream consumer. In the meantime,Rabobank believes that online groceryshopping and home delivery present anotherdimension to hybrid consumption patterns ashaving one’s groceries delivered to the homecan be regarded as another form of tradingup for the hybrid consumer.

How successful are retailers that target theextreme ends of the market?Hybrid consumer behaviour is well illustratedby the growth rates of different supermarketformats (see Figure 3.8). Looking at long-term revenue growth rates between 2007 and 2011, we see that the above averageperformers in the US are either harddiscounters, such as Aldi, or premium formats, such as Whole Foods and HE ButtGrocery. Mid-market formats, such as Safewayand Delhaize, are among the companies that displayed relatively low growth duringthis period.

We see similar trends in western Europe. Inthe UK, for instance, hard discounters andpremium retail formats in particular havebeen performing well, with consumersfavouring high quality and value-for-moneyretail formats (see Figure 3.9). Average long-term growth rates for mid-market operators,such as Morrison’s, Tesco, Sainsbury and Asda, have been clearly lower than at hard

discounters such as Aldi and Lidl as well asupmarket retailer, Waitrose. The notableexception has been Marks & Spencer Food(M&S Food) retailing, which we would haveexpected to show above average growth inan environment where consumers opt forhigh quality or value. Instead, despite beingan upmarket retailer, M&S Food has shownlower growth when compared to the averagegrowth rate of the UK food retail sector ineach year since 2007.

Looking at the diverse French supermarketsector, we mostly see value-for-money anddiscount formats performing above averagein terms of revenue growth in the last fiveyears, with Système U being a notable mid-market exception (see Figure 3.10). Other mid-market operators, Carrefour and Casino, areclearly underperforming the broader sector.

Retail markets in Germany and theNetherlands are largely skewed towards harddiscounters and mid to value type retailformats, especially when compared to themuch more diverse retail landscapes in theUK, France and the US (see Figure 3.11).Therefore, it is more difficult to discern hybridconsumption patterns based on retailergrowth rates in these countries.

Overall, we believe that in many developedmarkets, hybrid consumer patterns arereflected in growth rates of retail formats that are positioned at either the premium or value end of the market. Retail formatsgeared towards the mid-market are clearlyshowing lower growth rates over a longerperiod than their peers at the extreme ends of the spectrum.

Figure 3.6: UK grocery retailing market share by channel, 2012–2017

Source: IGD, Rabobank, 2013

2012 2017

per

cen

t

0

5

10

15

20

25

30

35

40

45

2017

Oth

erre

taile

rs

On

line

Dis

cou

nte

rs

Co

nven

ien

ce

Smal

lsu

per

mar

kets

Sup

er-

hyp

erm

arke

ts

Figure 3.7: Market size of UK online grocery market, 2011–2017

Source: IGD, Rabobank, 2013

GB

P b

illio

n

0

2

4

6

8

10

12

2017201620152014201320122011

Section 3 Hybrid consumption is driven by socio-demographic changes, retailers’ strategies and macroeconomic developments | 11

Recent macroeconomic developments reinforce hybridconsumption patternsHybrid behaviour on the part of consumersposes serious challenges to marketing,product development and strategydepartments at retailers, foodservicecompanies and food processors alike. The existing trend of market dualisation isforcing companies to rethink their strategicpositioning in their respective markets.

To add a layer of complexity to the situation,the economic headwind in many developedmarkets since 2008 has led to an accelerationof this dualisation (see Figure 3.12). Forced byconstraints on disposable income and fallingconfidence, consumers have been tradingdown even more than before when it comesto grocery shopping. At the same time,consumers still want to indulge themselves,

even in times of economic hardship, forinstance by dining out.

In addition, because budget constraints limitthe number of times consumers can afford toeat out, some opt to trade up to higher endrestaurants, but at a frequency that is clearlylower than before. Others trade down towardsvalue-for-money operators, such as QSRs.Generally, the mid-market suffers as it is perceived to offer neither value nor great quality.

Data on the average incomes of the middleclass in the US indicate rising incomes in the middle part of the last decade (see Figure 3.13). However, following a peak in 2007, purchasing power has declined. We see a similar pattern in western Europe’smain economies,6 albeit that incomes peaked in 2008 rather than 2007.

6 Germany, the UK, the Netherlands,

Italy, Spain and France (purchasing

power standard), 2005-2011.

Figure 3.8: Growth rates of US supermarket formats, 2007–2011, CAGR

Source: Euromonitor, Rabobank, September 2012

per

cen

t

hybrid territory

-4

-2

0

2

4

6

8

10

12

2007-2011 CAGRTr

ader

Jo

e’s

Ald

i Gro

up

Wh

ole

Fo

od

sM

arke

t

HE

Bu

tt G

roce

ry

Wal

-Mar

t St

ore

s

Pub

lix S

up

erM

arke

ts

Kro

ger

Ave

rag

e

Roy

al A

ho

ld

Seve

n &

I H

old

ing

s

Targ

et C

orp

Mei

jer I

nc

Del

hai

ze G

rou

p

S

afew

ay

S

up

erva

lu

Figure 3.9: Growth rates of UK supermarket formats, 2007–2012, CAGR

Source: IGD, Rabobank, 2013

per

cen

t

hybrid territory

0

3

6

9

12

15

Ald

i UK

&

Irel

and

Lid

l UK

Wai

tro

se

Mo

rris

on

s

Ave

rag

e

Asd

a

Tesc

o

Sain

sbu

ry’s

Mu

sgra

veG

rou

p

SPA

R

Mar

ks &

Sp

ence

r(F

oo

d)

Figure 3.10: Growth rates of French supermarket formats, 2007–2012, CAGR

Source: IGD, Rabobank, 2013

per

cen

t

hybrid territory

-2

-1

0

1

2

3

4

5

6

Lecl

erc

Syst

ème

U

Pica

rd

Lid

l

Ald

i

ITM

Ave

rag

e

Cas

ino

Fra

nce

Au

chan

Gro

up

Lou

is D

elh

aize

Car

refo

ur G

rou

p

12 | Rabobank The Rise of the Hybrid Consumer

These developments underline thedeteriorating financial situation for themiddle classes in both the US and westernEuropean economies since the outbreak ofthe Great Recession and the subsequentsovereign debt crisis in Europe.

We believe existing hybrid consumptionpatterns have been strengthened on the backof the decline in real household incomes,leading to a more pronounced dualisation of the market in recent years as consumersmake more choices based on budgetaryconstraints. It is therefore interesting to lookahead to see how this might impactdeveloped markets in the years to come.

EU growth sluggish in 2013 and muted inthe longer termThe Rabobank Annual Outlook 2013highlighted that the near-term prospects forthe eurozone and UK economies were ratherdim (see Figure 3.14). For 2013, we expect

growth to pick up very slightly in theeurozone on the back of improved financialconditions, mainly due to the combinedefforts of the eurozone leaders and theEuropean Central Bank. Growth will remainvery unevenly distributed in 2013 across themonetary union, with the continued recessionin the four southern European economiescombined with minor growth elsewhere.Eurozone member states in the west will likelyescape a recession in 2012/13, althoughgrowth will remain significantly below theregion’s growth capacity.

Rabobank expects an average annual growth of 1 percent to 1.5 percent for theeurozone during the period 2014 to 2018 (see Figure 3.15). For the western part of theeurozone, this may translate into slightlyhigher growth over this period. The UK will bedoing somewhat better than the eurozone,supported by higher employment rates and

Figure 3.11: Growth rates of Dutch and German supermarket formats, 2007–2012 CAGR

Dutch German

Source: IGD, Rabobank, 2013

per

cen

t

-1

0

1

2

3

4

5

6

7

8

per

cen

t

0

1

2

3

4

5

6

Lid

l

Jum

bo

Ald

i

Alb

ert

Hei

jn

Ave

rag

e

Plu

s

Dir

k va

nd

en B

roek

C10

00

SPA

R

Edek

a G

rou

p

Net

to N

ord

Glo

bu

s

Ave

rag

e

Lid

l

Rew

e G

rou

p

Do

hle

Ald

i

Met

ro G

rou

p

Figure 3.12: Migration of consumer spending in developed markets, 2000-2013

Source: Rabobank, 2013

2000 2005 2010 Today

Premium

Mid-market

Value

Hybrid behaviour Economic crisisacceleratesdualisation

H b id b h i Economic crisisaccelerates

Figure 3.13: Average income (and net worth of US middle class households, 2000–2011(inflation corrected, 2011 USD)

Average income (LHS) Net worth (RHS)

Source: US Census Bureau, US Federal Reserve SCF, Rabobank, 2013

50,000

51,000

52,000

53,000

54,000

55,000

56,000

57,000

58,000

59,000

USD

USD

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

2011

2010

2009

2008

2007

2006

2005

2004

2003

2002

2001

2000

Section 3 Hybrid consumption is driven by socio-demographic changes, retailers’ strategies and macroeconomic developments | 13

lower overall inflation, both of which arebenefiting consumers.

Ongoing austerity measures in the EU andrelatively high rates of unemployment arelikely to weigh on the outlook for consumerspending for a considerable period. Therefore, consumer spending growth is likely to substantially lag behind overalleconomic output.

Given this macroeconomic environment, we expect consumers will continue to tradedown in basic groceries, while the premiumsegment will continue to benefit fromconsumers seeking high quality in relevantproduct categories.

The US first to emerge from the ruins of the crisisWith respect to the medium to longer termoutlook, the growth prospects for the USeconomy are better than for western Europe.The US is much more advanced in terms ofdeleveraging debt among households and in the financial sector, while both the labourand housing markets have been improvingrecently. Population growth is a relativelystrong contributor to US economic growthdue in part to increasing immigration.

One of the key long-term risks facing USpolicymakers is the need for a stronger fiscal adjustment as the IMF projects that the federal government deficit will average4.5 percent in the period 2015 to 2017. Weexpect consumer spending to grow at a lesserpace than overall economic output in thecoming years, albeit probably at a higher pacethan in western Europe. Beyond 2014, the IMFforecasts US GDP growth at 3.6 percent onaverage through 2017. This is clearly higher

than pre-crisis levels and will support longerterm consumer spending.

Budget-induced down trading will continue in Europe Summarising the implications for hybridconsumption patterns, we expect the UK andwestern European countries in the eurozoneto display longer term economic growth ratesthat will be lower than pre-Great Recessionlevels. The US, by contrast, is expected to pickup speed in 2013 and to show growth rateswell in excess of what was seen prior to 2008.

Based on the muted projections for theeurozone and the UK, Rabobank expects that consumer budgets will remain pressuredfor some time to come, prolonging budget-induced down trading. In our view, thepremium segment will continue to benefitfrom consumers looking to treat themselveson occasion, crisis or not.

As the recovery in the US gets underway, we expect down trading will no longer bepredominantly budget-induced but rathervoluntary, as we believe consumers willcontinue to seek out value-for-moneygroceries even when their financial situation improves.

7 Western eurozone includes

Germany, France, Belgium,

Ireland, the Netherlands, Finland,

Luxembourg and Austria.

Figure 3.14: Near-term GDP growth forecasts for developed economies, 2012–2014

Source: IMF, Rabobank, 20127

2012 2013 2014

per

cen

t

-.5

0

.5

1.0

1.5

2.0

2.5

3.0

3.5

AustraliaWesterneurozone

UKUS

Figure 3.15: Projected longer term growth rates in developed economies, 2015–2017

Source: IMF, Rabobank 2012

per

cen

t

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

AustraliaWestern eurozoneUKUS

14 | Rabobank The Rise of the Hybrid Consumer

Genie of consumer awareness is out of the bottle Looking at the prospects for the US in particular, one could argue that with the improving economic conditions consumerswill resume trading up to mid-market products as their financial position improves. However, in our view, it is by no meanscertain that the mid-market will regain its lost territory once economic developments improve. For example, in thepackaged food segment, private label has successfully retained the ground it had won during the downturn.

The consumer awareness of clear choices that has grown in the past decade (i.e. choices between premium and valueproducts versus non-distinct, mid-market products) is not likely to diminish going forward if recent developments inprivate label are any guide. Consequently, we believe it is highly unlikely that, once economic conditions in developedmarkets improve materially, hybrid consumption patterns will reverse significantly, if at all.

In other words, Rabobank believes food processors and retailers will be forced to cope with hybrid consumer patterns intheir long-term strategic planning as we do not expect that this genie can be put back in the bottle.

Section 4 Hybrid consumption is a secular phenomenon: The hybrid consumer is here to stay! | 15

Based on the earlier discussion onmacroeconomic developments andaccelerated trading down on the back ofthese developments, one might argue thathybrid consumption patterns are driven byincreasing inequality in income distributions.In other words, with rising unemploymentand an increasing group of consumers having less money to spend, consumers arebecoming hybrid in their spending patternsnot by choice but because they have to.However, Rabobank believes that hybridconsumption patterns (i.e. both trading upand trading down) follow a trend that issecular to economic cycles. In other words, we expect to see hybrid consumptionpatterns continue even when developedeconomies pick up steam and disposableincomes increase.

One example of this trend would be thesuperior long-term performance (i.e. throughthe economic cycle) of food retail formats that are geared towards the premium andvalue segments when compared to mid-market formats. In addition, socio-demographic developments in developedmarkets, also of a secular nature, reinforcehybrid consumption patterns.

As a further illustration of the secularity ofhybrid spending patterns, we have looked at income distribution in a number ofdeveloped economies. If one were to arguethat hybrid consumption is driven by incomeinequality, then the reverse should also hold(i.e. higher income equality supports the mid-

market segment). However, we see hybridspending patterns even in the most incomeegalitarian countries (i.e. Sweden, Finland andNorway) as measured by the GINI coefficient8

(see Figure 4.1).

For instance, looking at the market forScandinavian bulk ice cream (typically 750 millilitre or 1 litre packages), we clearlysee a multi-year trend away from mid-marketproducts and towards premium products in particular (see Figure 4.2). While the valuesegment has also seen its market shareincrease over the same time frame, the extentof this expansion has been smaller than forthe premium segment. In the meantime, themid-market segment has seen its share dropfrom 57 percent in 2007 to an approximate 41 percent in 2012.

Hybrid patterns in Scandinavia have not onlybeen witnessed in recent years, but are alsoprojected for the foreseeable future. Takinganother example, value and premium beercategories are anticipated to outperform themid-market standard beer category as theyhave in the past six years (see Figure 4.3).

These examples clearly suggest that hybridconsumption patterns largely moveindependently from economic cycles anddifferences in income distribution. In our view,such secularity implies that hybrid consumersand their spending patterns are a long-termphenomenon and are here to stay.

4 Hybrid consumption is a secular phenomenon:The hybrid consumer is here to stay!

8 The Gini coefficient measures

the inequality, for example, in levels of

income. A Gini coefficient of zero

expresses perfect equality, while a

Gini coefficient of one expresses

maximal inequality.

16 | Rabobank The Rise of the Hybrid Consumer

In summary, having looked at socio-demographic developments, retailers’strategies and macro-economicdevelopments, Rabobank believes that acombination of factors on both the demandside (consumers) and the supply side (food retailers and foodservice companies)has resulted in hybrid consumption patterns.These may be influenced by short-termmacroeconomic developments, but are of a long-term secular nature. As such, we believe the hybrid consumer will be a long-term phenomenon that requiresquantification in order to assess theopportunity for food processors, food retailers and foodservice companies.

Figure 4.3: Average growth rates for Scandinavian beer markets, 2006–2011 vs. 2011–2016

Source: Euromonitor, Rabobank, 2013

2006-2011 2011-2016

per

cen

t

01

23

45

67

89

10

Economy lagerStandard lagerPremium lager

Figure 4.1: GINI coefficients for selected developed economies

Source: OECD, Rabobank, 2013

Around 2000 Mid-2000s Late-2000s

0

.05

.10

.15

.20

.25

.30

.35

.40

US

UK

Au

stra

lia

Jap

an

Ger

man

y

Net

her

lan

ds

Fran

ce

Swed

en

Fin

lan

d

No

rway

Figure 4.2: Scandinavian bulk ice cream market by segment, 2007–2012

Premium Mid-market

Source: Euromonitor, Rabobank, 2013

Value

0

10

20

30

40

50

60

201220112010200920082007

per

cen

t

Section 5 Standard mid-market products will lose out | 17

One of the main issues in trying to quantifyhybrid consumption patterns is related to thefact that the money saved by trading down ina certain product category is typically spentwhen consumers trade up in a completelyunrelated product category. For instance,money saved by trading down in frozen orcanned vegetables from non-distinct, moreexpensive, mid-market alternatives may bespent on premium on-the-go sandwiches, finedining or premium bakery products for theweekend breakfast table. Or consumers mightchoose to spend it on non-food items, such as consumer electronics or fashion. In otherwords, the money flows stemming fromhybrid consumption patterns are difficult, ifnot impossible, to map per product category.However, on an aggregated basis, and lookingacross different product categories, we canestimate a breakdown of the different market segments.

Using category pricing data and defining themedian price within a category as the mid-market price point, we have assumed that thepremium and value alternatives are priced at120 percent and 80 percent compared to themid-market product, respectively.

Taking into account a range of different foodcategories in the US and western Europe,including ice cream, sweet biscuits, beer,spirits and chocolate confectionery, we have categorised packaged food sales intopremium, mid-market and value segments. In our calculations, the mid-market ofstandard products currently accounts forapproximately 60 percent of the packaged

food market as a whole. The premium andvalue segments make up around 15 percentand 25 percent, respectively (see Figure 5.1).

Using industry data and companyinformation, we have calculated thebreakdown of the three market segments infive years’ time (i.e. through 2017). Rabobankexpects the premium segment to expand its share to 20 percent from its current 15 percent, while the value segment isexpected to increase its share from 25 percentto 30 percent. We expect the share of the mid-market to decline from 60 percent to 50 percent during the same time frame.Naturally, these numbers will vary from oneproduct category to another and from onecountry to the next.

As an illustration of this hybrid consumptionpattern, we expect the mid-segment of theice cream markets in western Europe and the US to see average shares decline from 34 percent in 2012 to 25 percent in 2017. At the same time, we see the premiumsegment of this category expanding its sharefrom 36 percent to 44 percent, while the valuesegment is expected to increase its sharefrom below 30 percent to around 32 percent.

While at first glance, these market sharemovements may not appear too unsettling,we believe that a more dramatic viewemerges when looking at the concomitantlyimplied growth rates for the three packagedfood segments in western Europe and the US in the next five years.

5 Standard mid-market products will lose out

18 | Rabobank The Rise of the Hybrid Consumer

Relating the expected breakdown of thepremium, mid-market and value segments to the projected size of the packaged foodmarkets in the US and western Europe in 2017 reveals a very clear cut picture with littleroom for ambiguity as to the need for marketparticipants to respond to this marketdualisation. While both the premium andvalue segments in western Europe and the US are expected to show mid to highsingle-digit average annual growth rates inthe next five years, by contrast, we expect the addressable mid-markets for packagedfoods will, on average, exhibit declines (see Figure 5.2). By comparison, the averageoverall growth rate for packaged food inthese markets is estimated at 2 percent to 3 percent during the same period.

The substantial differences in growth ratesbetween the premium and value segmentson the one hand and the mid-market on theother have profound implications for foodprocessors, retailers and foodservicecompanies alike. Strategic action is required if not already undertaken.

Figure 5.1: Premium and value segments of overall food market growing at the expense of the mid-market, 2013–2017

Source: Rabobank, 2013

Premium products

Current situation Future situation 2017

Premium products ~15%

~20%

Standard products Standard products

~60% ~50%

Value productsValue products~30%~25%

Figure 5.2: Implied growth rates for western European and US packaged food markets, 2012–2017

Source: Rabobank, 2013

per

cen

t

-2

0

2

4

6

8

10

12

ValueUS

ValueWE

Mid-market

US

Mid-market

WE

PremiumUS

PremiumWE

Section 6 Adapt or fade away? Strategic action required | 19

The very substantial growth differentials between the various food retail segments imply thatfood companies that are not well positioned need to re-evaluate their strategies in the context ofproduct attributes, distribution channels, marketing and brand management.

The continued need to distinguishHybrid consumers are moving towards both ends of the product spectrum, where they seek differentiated and distinguishing products in the premium segment and basic value-for-money items in the value segment. Consequently, food processors, retailers and foodservicecompanies need to continuously distinguish themselves either on quality or price or, preferably,both. In addition, bringing new and exciting products to market requires ongoing innovation on the part of food processors. It may seem self-evident, but inability to accomplish any of the above will lead companies to feel the full impact of consumers moving away from the mid-market.

Shifting distribution channels: From foodservice to retail to onlineThe internet has provided hybrid consumers with a very powerful tool to compare and purchase products. Until a few years ago, product sales through the internet were mostly geared towards non-food items and services. However, food and beverage retail sales areincreasingly being conducted online, with groceries either being delivered to the home oravailable for pick-up at a nearby distribution hub. Food processors and retailers alike now have a further incentive to distinguish themselves to woo hybrid consumers as they compare products and prices online.

In parallel to the growth of the internet as a sales channel for food and beverage products,Rabobank believes that the ongoing economic weakness in developed markets, particularlywestern Europe, may lead to a further round of trading down, resulting in shifting distributionchannels. For instance, consumers may choose to prepare meals at home rather than purchasingfood from QSRs, resulting in more retail sales at the expense of foodservice sales. Similarly,‘premium’ cooking from scratch at home instead of fine dining out-of-home will have acomparable effect on wholesale food and beverage distribution channels, which food processorsneed to consider when formulating future strategies.

A different marketing approach: Behavioural segmentation of consumersMarketing is an additional challenge stemming from hybrid consumption patterns, particularlyfor processors of branded food and beverage products. It has become increasingly difficult toaddress different consumer groups based on demographic segmentation, as consumers nolonger stick to the consumption patterns associated with their traditional segment. Instead,consumers take their pick from different product categories in a wide variety of price ranges.

6 Adapt or fade away? Strategic action required

20 | Rabobank The Rise of the Hybrid Consumer

Individualisation and the resulting hybrid consumption patterns require marketers to addressconsumers based on the different roles they have at different times of the day as well as personalpreferences. This behavioural segmentation is replacing demographic segmentation and willrequire many food processors and retailers to rethink their marketing approach.

Danger of brand erosion by perceptionWhile iconic brands are becoming even more iconic, brand loyalty in general is declining due toincreased transparency and the amount of information available to consumers. Therefore, brandcommoditisation is a clear risk for non-distinct brands that are not truly authentic, for instance,regarding brand experience and health claims, but where marketing is used to create an aura ofartificial authenticity.

Furthermore, in a world where private label is used not only to penetrate the value range of foodcategories but also increasingly by food retailers to expand their offering at the premium end ofthe spectrum, there is a clear risk of brand erosion as consumers’ perceptions of brands are likelyto deteriorate due to the introduction of higher priced, premium private-label products. In orderto avoid brand erosion by consumer perception, food processors need to actively manage andposition their brands, perhaps more actively than they initially deem necessary.

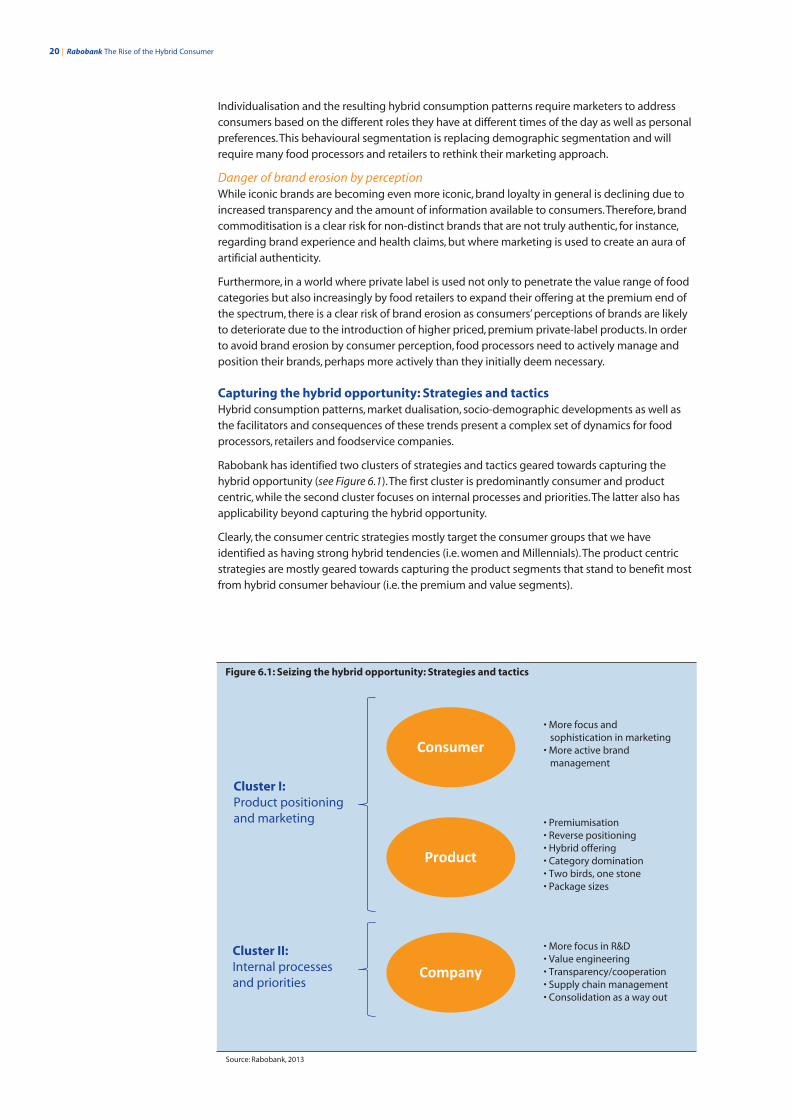

Capturing the hybrid opportunity: Strategies and tacticsHybrid consumption patterns, market dualisation, socio-demographic developments as well asthe facilitators and consequences of these trends present a complex set of dynamics for foodprocessors, retailers and foodservice companies.

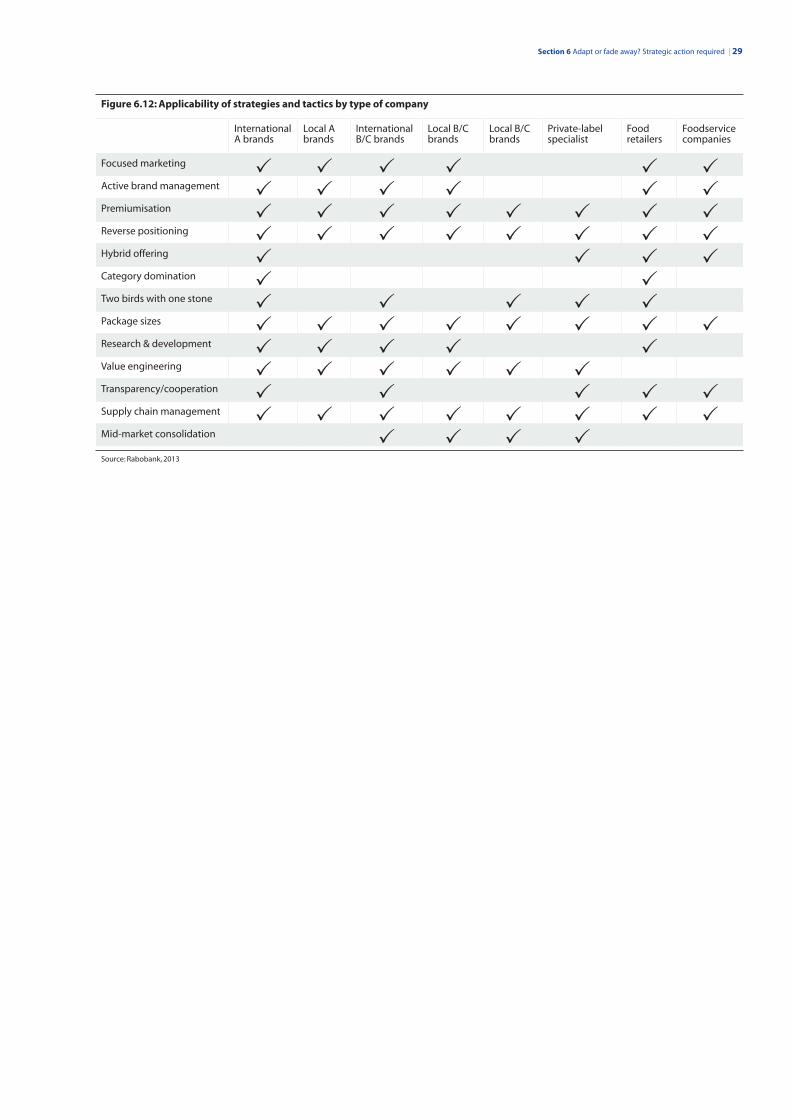

Rabobank has identified two clusters of strategies and tactics geared towards capturing thehybrid opportunity (see Figure 6.1). The first cluster is predominantly consumer and productcentric, while the second cluster focuses on internal processes and priorities. The latter also hasapplicability beyond capturing the hybrid opportunity.

Clearly, the consumer centric strategies mostly target the consumer groups that we haveidentified as having strong hybrid tendencies (i.e. women and Millennials). The product centricstrategies are mostly geared towards capturing the product segments that stand to benefit mostfrom hybrid consumer behaviour (i.e. the premium and value segments).

Figure 6.1: Seizing the hybrid opportunity: Strategies and tactics

Source: Rabobank, 2013

Company

Product

Consumer

• Premiumisation • Reverse positioning • Hybrid offering • Category domination • Two birds, one stone• Package sizes

• More focus and sophistication in marketing

• More active brand management

• More focus in R&D• Value engineering• Transparency/cooperation• Supply chain management• Consolidation as a way out

Cluster I: Product positioningand marketing

Cluster II: Internal processes and priorities

Section 6 Adapt or fade away? Strategic action required | 21

9 As opposed to above-the-line

marketing (i.e. mass media

marketing such as advertising

on TV and in newspapers).

Cluster I: The consumer and product positioningSmarter marketing to gain share of the hybrid consumer’s walletGlobal economic headwind is keeping many food processors’ marketing budgets under pressure.Furthermore, in light of hybrid consumption patterns, many food processors are being forced tomake product portfolio choices. Therefore, Rabobank believes increased focus on the marketingof high impact products (i.e. products with substantial upward revenue potential) will putexisting marketing budgets to best use (see Figure 6.2). While this strategy will further contributeto the commoditisation of non-distinct brands, it should help agile food processors become moreeffective in capturing the higher end of the hybrid opportunity in particular.

Need for more active brand managementIn spite of all marketing efforts, if consumers do not perceive products in the way foodprocessors, food retailers or foodservice companies intend, sales numbers will likely disappoint.Even established brands, which are likely considered strong and dominant within their respectivecategories, are susceptible to brand erosion if they are not properly maintained.

Therefore, active product positioning and brand management are required to achieve andmaintain a certain consumer perception. For many food companies, this may entail moreproactive market research into consumer preferences and trends. For others, it may requirestepping up their efforts in benchmarking their product and packaging attributes versus those of their peers and taking appropriate action.

Premiumisation to address the high end of the marketOne obvious way for food processors to capture part of the hybrid demand is to ‘premiumise’ the product offering (see Figure 6.4). In other words, move up to the premium segment of aspecific product category by, for instance, offering healthier alternatives, using more naturalingredients, using fair trade ingredients and by incorporating corporate social responsibility aswell as sustainable business practices. Additionally, more convenient packaging, especially forfood on-the-go, and offering trendy must-have alternatives at the higher end of the market willhelp food processors in premiumising their product offering.

The roles people play Behavioural segmentation of target consumers implies that marketing processes need to become more sophisticated. For instance, consumers identified as having a high propensity to show hybrid consumer behaviour (i.e. women andMillennials) are not part of a homogenous group. Therefore, segmentation needs to take place based on the different roles people play at different times of the day, the moment of purchase and consumption as well as the context in whichproducts are consumed. In many ways, this approach can be compared to the way in which Google produces search resultsas they are based on current search criteria (i.e. a certain role at a certain moment in time) as well as on patterns derivedfrom earlier searches.

Behavioural segmentation also relates to the way in which companies try to reach consumers once identified. We believefurther marketing focus on reaching the right consumers in their orientation phase, right before and at the moment ofpurchase, through digital, online and on-site marketing, so-called below-the-line marketing,9 will help companies gain a higher share of the hybrid consumer’s wallet.

For example, in a number of western European potato chip markets we have seen established, higher end brandsbecoming mid-market brands in consumers’ perception in recent years. This was the result of retailers introducingpremium, private-label potato chips positioned above these higher end brands, de facto demoting these brands to mid-market offerings and resulting in market share losses (see Figure 6.3).

More active brand management would have prevented these higher end brands from eroding.

22 | Rabobank The Rise of the Hybrid Consumer

Reverse positioning within a segmentIn addition to premiumisation, another viable strategy to capture share of the hybrid consumer’swallet is reverse positioning within a segment (i.e. offering ‘value’ products within the premiumsegment and offering ‘premium’ products within the value segment) (see Figure 6.5). In additionto attracting hybrid consumers to the premium and value segments, this strategy allows retailersto cater to consumers that have become more cost-conscious due to waning consumerconfidence and purchasing power.

While offering less expensive product varieties at high-end retail outlets may initially appearcounter-intuitive, by doing so, food processors and retailers can retain format-sensitive clienteleby allowing them to continue shopping at the same format but at different price points.

Alternatively, through premiumising products in the value segment towards the upper end of thesegment, food processors and retailers enable consumers to trade down to lower price pointswithout necessarily feeling as if they have traded down.

The best of both worlds: A hybrid product offeringAddressing both the value and premium segments within a specific category, by using the value products to sell premium products, can be an effective way to attract hybrid consumers(see Figure 6.6). Supermarket retailers as well as foodservice outlets can use this strategy to attractcustomers with value-for-money propositions, while simultaneously aiming to sell premium,more expensive products to these same customers.

Category domination: Covering the entire categoryA strategy to capture hybrid consumers no matter which segment they migrate to is centredaround offering the entire product range from value to premium within a specific category,covering both extremes of the product range as well as the mid-segment (see Figure 6.7).Prerequisites for this strategy are scale and clear focus on a certain category as well as geography.Full coverage of a product spectrum is typically achieved through mergers and acquisitions inaddition to autonomous growth.

Perhaps one of the best examples of a company that has been successful in premiumising its product offering is Frenchspirits company, Pernod Ricard. Following a clear strategy of moving the majority of its products into the higher echelonsof the respective product categories, the company is now deriving 75 percent of its sales from premium type products,such as Absolut Vodka and Chivas Regal. On the back of its premiumisation strategy, Pernod Ricard’s operating margin hasgrown from less than 20 percent in 2005 to nearly 26 percent in its most recent fiscal year.

Waitrose is one example of an upmarket retailer in the UK which began offering bakery products under a premium privatelabel, thereby enabling increasingly cost-conscious but format-sensitive customers to continue shopping at their favouritehigh-end supermarket but at lower price points.

A donut is an example of a value product that can be ‘upgraded’ to premium within the value segment by adding differentsorts of sprinkles, fillings or frostings. Another example of premiumisation in the value segment is given by Lidl in the UK.The hard discounter is increasing its deluxe range of products to enable customers to treat themselves to luxury productsat affordable prices. For food processors and retailers, upgraded value products should be a source of margin expansion.

UK-based QSR, Pret-a-Manger, for instance, offers coffee to-go at relatively low price points to generate traffic andsimultaneously aims to sell higher priced food products, such as premium sandwiches.

Section 6 Adapt or fade away? Strategic action required | 23

Two birds with one stone: Addressing several consumer issues at onceIn a two-birds-with-one-stone strategy, food companies and retailers can develop products andconcepts that simultaneously address issues which are top of mind with consumers while stillmeeting consumer preferences (see Figure 6.8). Provided that the product quality is sufficient, webelieve that the hybrid consumer can be tempted to spend more money than originally plannedon products offered through a two-birds-with-one-stone strategy as these products addressmultiple consumer requirements or issues at the same time. As such, Rabobank believes thisstrategy could be an interesting source of margin expansion when executed successfully.

Variations in package sizesOn the value end of the spectrum in particular, variations in package sizes can be an effectivetactic to address consumer budget constraints, especially in light of ongoing economic weaknessin developed markets. For instance, smaller package sizes and portions introduced at lowerabsolute price points than the original package size, address several issues.

Firstly, in light of weak economic conditions, smaller portions allow consumers to still buy theirfavourite brands, but at lower price points. Secondly, within the more expensive categories,selling products in smaller portions can help consumers manage their weekly household cashflow more efficiently. This issue has become especially pressing in developed markets that areexperiencing rapidly deteriorating economic fundamentals. Finally, smaller package sizes at lower price points can be a good tactic to tap into new distribution channels, such as discountsupermarkets.

Even though unit prices of smaller packages are typically lower than the price of the originalpackage size, in many cases, smaller portions and packages can go hand in hand with higherselling prices per quantity unit (kilogramme, litre etc.) and potentially higher margins.

While smaller package sizes are generally aimed at making products available to a wider group of consumers, enlarging package sizes of specific, bulk-like products is typically aimed atenhancing the value perception for consumers and can be equally effective in gaining share of hybrid consumers’ wallets.

Unilever’s domination of the ice cream segment in western Europe is a good example of a company’s portfolio coveringthe entire product spectrum. With a 32 percent share of the market, the company is able to truly dominate this segmentusing various brands and price points.

Over the years, Unilever’s existing product portfolio of dairy-based and water-based ice cream has been expanded throughacquisitions such as Ben & Jerry’s.

A-brands, such as Magnum, have simultaneously been strongly supported in their autonomous growth, with Magnumbecoming a billion-plus brand in terms of revenues.

This combination of growth strategies has resulted in Unilever’s domination of the US and European ice cream markets.

In light of constrained consumer budgets, scratch cooking with fresh ingredients can be positioned as less expensivecompared to ordering in or eating out, while it also addresses the renewed cocooning trend currently witnessed in manydeveloped markets. In addition, advocating the use of fresh ingredients also plays into the health and wellness trend.