Embed Size (px)

Citation preview

The role of CenTral europe in The German eConomy the political consequences

Konrad popławski

The role of CenTral europe in The German eConomy the political consequences

Konrad popławski

WaRsaWjune 2016

© copyright by ośrodek studiów Wschodnichim. Marka Karpia / centre for eastern studies

content editoRMateusz Gniazdowski, anna Kwiatkowska-drożdż

editoRhalina Kowalczyk

co-opeRationKatarzyna Kazimierska, anna Łabuszewska

tRanslationjim todd GRaphic desiGn paRa-buch

photoGRaph on coVeRshutterstock

dtpGroupMedia

FiGuResWojciech Mańkowski

publisheRośrodek Studiów Wschodnich im. marka Karpia centre for eastern studies

ul. Koszykowa 6a, Warsaw, polandphone + 48 /22/ 525 80 00Fax: + 48 /22/ 525 80 40osw.waw.pl

isbn 978-83-62936-84-7

contents

Theses /5

InTroducTIon /8

I. the adVantaGes oF centRal euRope FRoM the peRspectiVe oF GeRMany /10

II. the deVelopMent oF tRade betWeen GeRMany and the V4 /15

1. The role of central europe as a key trading partner for Germany /152. The position of individual V4 states in their trade with Germany /203. risks associated with the V4’s dependence on trade with Germany /25

III. the FloW oF inVestMents betWeen GeRMany and V4 /31

1. The flow of investments between Germany and V4 /312. Motives for investment /353. The investment climate in the V4 countries from the perspective of German

investors /39

IV. the political pRospects FoR econoMic coopeRation /44

V. APPendIX /48

1. The automotive sector /482. The electro-mechanical sector /503. The logistics sector /534. The energy sector /535. The retail sector /566. The banking sector /60

PRA

CE

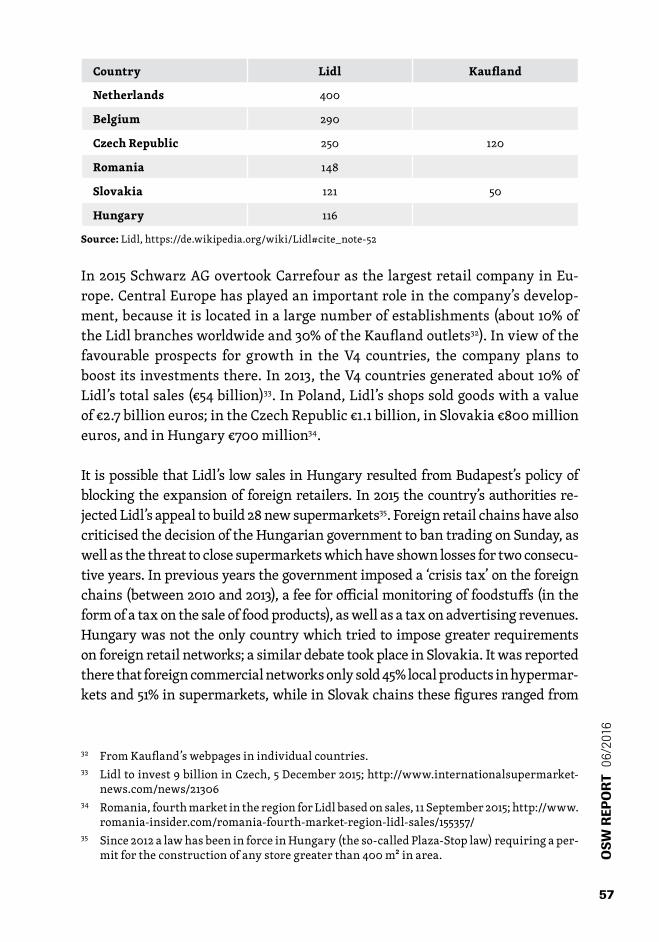

OSW

09/

2012

5

OSW

REP

OR

T 0

6/20

16

Theses

• The economic cooperation between Germany and Central Europe hasbroughtmutualbenefitsinrecentyears.Since1989,GermanyhasbecomethemostimportanttradingandinvestmentpartnerfortheV4states,whichhashadsignificantimpactontheevolutionoftheeconomicmodelofCen-tralEurope,andhelpedintheprocessofmodernisingtheregion.Germancompaniesfromtheautomotive,financialandenergysectors,amongoth-ers,havegainedsignificantmarketsharesinthosecountries.Thedevelop-mentofeconomiclinksbetweenGermanyandtheV4stateshasalsobeenbeneficial forGermany itself.Taken together, theVisegradGroup stateshavebecomeGermany’smostimportantglobalpartnerbothinexportsandimports.Theyhavemanaged–assomeofthefewstateswithoutanysig-nificantresourcesofrawmaterials–tomaintainrelativelybalancedtraderelations,showingsurplusesorminordeficitsintheirtradewithGermany.

• Overthelastdecade,CentralEuropehasbecomeanimportantsourceforimproving the international competitiveness of the German economy.Firstly,movingfactoriesfromGermanytoV4becameanelementoflower-ingproductioncostsformanyGermancompanies.ThepressurebusinessexertedonGermanworkerstoreducelabourcostswasalsoanimportantelement.Secondly, in the faceofmajorproblemscausedbya lackof en-gineers,GermanbusinessesmovedpartoftheirR&DactivitiestoCentralEurope,orattractedqualifiedworkersfromtheregiontoGermany.

• TheeconomiccooperationbetweenGermanyandCentralEuropehasbeenboosted by investmentsfinanced fromEuropeanUnion funds.GermanyhasbeenbyfarthelargestbeneficiaryofinvestmentsintheV4statesfromtheEU’scohesionpolicy.Thankstothis,Germanyhasbeenabletorelyonadditionalexportstothesecountries,tothetuneof€30billioninthepe-riod2004-151.Germanyhasbenefitednotonlydirectly,fromthecontractsitacquired,butalsoindirectly;asignificantproportionofthesefundshasbeenspentoninfrastructure,whichhasmadeiteasiertotransportgoodsbetweenGermanyandCentral&EasternEurope.

1 AssessmentofthebenefitsobtainedbytheEU-15memberstatesasaresultoftheimplemen-tationofthecohesionpolicyinthecountriesoftheVisegradGroup.Finalreport.TheStruc-turalResearchInstitute.London,December2011;http://ibs.org.pl/app/uploads/2015/12/Oce-na-korzy%C5%9Bci-uzyskiwanych-przez-pa%C5%84stwa-UE-15-w-wyniku-realizacji-poli-tyki-sp%C3%B3jno%C5%9Bci-w-krajach-Grupy-Wyszehradzkiej.pdf

PRA

CE

OSW

09/

2012

6

OSW

REP

OR

T 06

/201

6

• OverrecentyearstheV4countrieshaveprovedabletoproducepartsandgoodsforGermancompaniesinanefficientmanner.Inrecentyears,theautomotive, electro-mechanical, electricity and retail trade sectors havesignificantly increased their expansion inCentralEurope. It is expectedthatGermancompanieswillmovetheseR&DactivitiestoCentralEurope,whichwouldbeimpossibletoconductinGermany,forexampleduetoalackofengineers.However,thisprocesswillprobablynotbeverylargeinscale.

• OneconditionfortheV4statestoachievelevelsoftradecooperationwithGermanyonthelevelofcountriessuchasAustria,Belgium,theNetherlandsorSwitzerlandisthattheyshouldbeabletosellGermancompaniestheirownproducts,withhighaddedvalue.ThereisstillgreatpotentialtodeepeneconomiccooperationbetweenGermanyandtheV4countries.InadditiontothetraditionaladvantagesofCentralEurope,suchasgeographicalprox-imity,traditionsofindustrialproduction,lowlabourcosts,andreliability& security of supply,German companies appreciate the new elements ofcompetitiveness in the region, such as the stability of economicdevelop-mentandpolitical-institutionalconditions,everbetterinfrastructure,andthehighlevelsofthelocalworkers’qualificationsandproductivity.

• CentralEurope’sgreatdependenceonGermantradeandinvestmentposesanumberofrisksfortheregion’seconomicdevelopment.First,Germanyspecialisesinexportingcapitalgoodsbasedontraditionalindustrialcom-panies.GermancompanieshavestillnotshownanysignificantsuccessesintheITsector,whichmaydeterminethestrengthoftheeconomyinthefuture.Secondly,theroleofCentralEuropeasanassemblyplantforGer-mancompaniesislinkedinthemediumtermwiththeriskoflosingthatpositiontocountrieswithlowerproductioncosts.Inaddition,thesaleofproductsfromCentralEuropeunderthebrandnamesofGermancompa-niesdoesnothelpinmakingtheirown,globallyrecognisablebrands;itisthusdifficult tomakesignificantmarginsandescape fromthe so-calledmiddleincometrap.

• The current period of global political and economic instability has in-creasedtheimportanceofCentralEuropeforGermany.Firstly,theregion’sgeographicalproximityensuresthatthiseconomiccooperationwillnotbedisturbedbygeopoliticalproblems,andthereisnoriskthatthecontinuityofsupplywillbeinterrupted.Secondly,duetotheeurocrisis,thedisputeoverthefutureshapeoftheEU’seconomicpolicyhasintensified.Germanyneedsallieswhowillpromoteafree-marketmodeloftheUnion,basedon

PRA

CE

OSW

09/

2012

7

OSW

REP

OR

T 0

6/20

16

theprinciplesoffiscaldiscipline,intheclashwiththemorestatistvisionoftheEUrepresentedbyFrance,butprobablyalsobyleftist-ruledGreeceandPortugal,andalsoperhapsSpain.

• Inthecomingyears,GermanymaybecomeinterestedinbringingCentralEuropeovertoitssideinavarietyofdisputes,suchasthereformoftheeuro-zone,therevisionoftheEU’sclimateandenergypolicy,andalsotheproblemsintheEU’seasternandsouthernneighbourhoods.Sofar,despitethedynamicallydevelopingeconomiccooperationinrecentyears,Germa-nydoesnotappeartoshowanyparticularinterestindeepeningitspoliticalcooperationwithCentralEurope.Enhancedcooperationwithintheframe-workoftheV4mayhelpGermanytobecomemoresensitivetotheregion’sinterests,especiallyas itseemspossiblethatBerlincanreachacommonpositionwiththeV4onmanyEUissues.

• An importantprerequisite for improving cooperationbetweenGermanyandCentral Europe is to informGermanpublic opinion, through inten-sivepromotionalactivities,aboutthesignificantscaleoftheirmutualeco-nomicties.Germany’sdynamicallydeepeningcooperationhaspassedtheGermanmediaby,incontrasttotheirconsiderablenumberofreportsandanalysisonthedevelopmentofeconomicrelationswiththeBRICcountries.Thisalsostems fromGermaneconomists’ lackof interest inCentralEu-rope.AftertheaccessionofthecountriesoftheregiontotheEU,thein-terestareasofmanyscientificcentresshiftedfurthereastwards.GermanpoliticalinstitutionsareconductingonlysmallamountsofanalyticalworkintheareaofCentralEurope.Thisleadstomisunderstandingsofthesitu-ationintheregion,andtoanincorrectnarrativestatingthatfundingfromthe cohesionpolicy is onlyawayoffinancing thepoorermember stateswhichdoesnotguaranteeGermanyanyeconomicbenefits.

• The effects of the possible breakup of the Schengen area are difficult toquantify. An increased bureaucratic burden on the movement of goodsbetweenGermanyandV4wouldcertainlyimpedetradeandgeneratead-ditionalcosts.ItwouldlikelybeabigproblemfortheGermanautomotiveandlogisticssectors,inwhichtimeofdeliveryplaysanimportantroleincompetitiveness.Forthisreason,itcanalsobeexpectedthatGermancom-paniesinvolvedinCentralEuropewillopposestricterbordercontrols.

PRA

CE

OSW

09/

2012

8

OSW

REP

OR

T 06

/201

6

InTroducTIon

ManyexpertsinterpretedtheaccessionoftheCzechRepublic,Hungary,Slo-vakiaandPolandtotheEuropeanUnionasthe‘endofhistory’intheireconom-icrelationswith theGermany.Since2004 therehavebeen fewcomparativestudiesonthedevelopmentofeconomicrelationsbetweenGermanyandCen-tralEurope.Thefollowingreportisintendedtofillthisgap,anditspurposeistoanswerthequestionofhoweconomicrelationsbetweenGermanyandthecountriesoftheVisegradGroup(V4)havechangedinthelightofthesignificantpoliticalandeconomicchangeswithintheEuropeanUnionoverrecentyears.

TheCzechRepublic,Poland,SlovakiaandHungaryhavebeenselectedasex-amplesofthegeneralchangesinthelinksbetweenGermanyandCentralEu-rope,whichhavealsoaffectedGermany’srelationshipswithothercountriesintheregion,suchasBulgaria,RomaniaandtheBalticstates.Fromtheper-spectiveofGermany’sbusinesselites,thecountriesoftheregionarelinkedbymanysimilarities,suchasthefollowing:

• geographicalproximityandculturalsimilarity;• uniformmarketruleswhichapplythroughouttheEU;• long-standingindustrialtraditions,andthesubstantialparticipationofin-

dustrialproductionintheirGDPs;• thesignificantshareofforeigncapitalintheirmanufacturingandfinan-

cialsectors;• aneconomicmodelbasedonexports,withthesignificantparticipationof

foreigncompanies;• small or insignificant rawmaterial resources, and great dependence on

theirimport;• energysystemsbasedonpowerplantswhichusecoalandnuclearenergy,

fuelswhichareincreasinglybeingdisplacedfromtheEU;• significantresourcesofskilledworkerswithlowerwageexpectationsthan

theircounterpartsinWesternEurope;• relativelygoodeconomicperformancesagainstthebackdropoftheEUas

awholeduringtheglobalfinancialcrisisandthecrisiswithintheeuro-zone.

Germany is Central Europe’s most important economic partner, and in re-cent years this link has brought forthmutual economic benefits. However,it isworthconsideringthestabilityoftheeconomicmodelthathasevolved,andalsoaskinghowthecloseeconomiccooperationbetweentheV4statesand

PRA

CE

OSW

09/

2012

9

OSW

REP

OR

T 0

6/20

16

Germanymaybeusedtoincreasethelevelofinnovation.Theproblemofthecapacitytodesignandmanufacturemoderngoodsandservices isbecomingmoreimportantinthedebatewithinCentralEuropeontheso-called‘middleincometrap’.Thisisdefinedasariskofexhaustingexistingenginesofgrowth,andtheinabilitytotransitionfromaproductionmodelbasedonlowlabourcoststoonebasedonqualityandinnovation,resultinginhigherwages.

Three sourcesof informationwereused inpreparing this report.ThemainmethodologyappliedinthestudywastheanalysisofeconomicindicatorsintradeandinvestmentbetweenGermanyandtheV4countries.Inaddition,thestudywasbasedonconversationswithabout30experts,mostlyfromGerma-nybutalsotheV4states:representativesofGermanministriesatthefederalandregional (Länder) levels, aswellasembassies,businessassociations, re-searchinstitutes,chambersofcommerceandforeigninvestmentagenciesintheCzechRepublic,Poland,HungaryandSlovakia.Thisinformationhasbeensupplemented by case studies from themost importantGerman industries,withananalysisoftheirsituationintheV4states.

PRA

CE

OSW

09/

2012

10

OSW

REP

OR

T 06

/201

6

I. The advanTages of cenTral europe from The perspecTIve of germany

In recent years, the region of Central Europe has continued its quite rapidgrowth, and ithasdealt relativelywellwith theglobal economicdownturnpost-2009,especiallywhenconsideringthesituationintheeuro-zoneasaref-erencepoint.Itsstrongereconomicposition,alongwiththechangeinpoliticalconditionsinEurope,makesitanevenmoreattractivepartnerforGermanythanbefore.

From theGermanpoint of view, the regionofCentralEuropehas since the1990sdisplayedanumberofcommonfeatures.ThebasiccharacteristicsoftheV4countries’economies–suchastheirindustrialtraditions,lowlabourcosts,culturalandgeographicproximity,andaskilledworkforce–madethemanidealareafortheexpansionoftradeandinvestment.Fromtheoutset,Germa-nyinvolveditselfintheeconomictransitionprocessinthecountriesofCen-tralEurope,perceivinganopportunitytogainpolitical,economicandsecuritybenefits.Germany’sgoalwastoestablishstrongrelationshipswithCentralEu-rope,tolinkitpoliticallywithWesternstructures,andbuildupaneconomichinterlandforitselfintheregion.

CentralEurope’seconomicimportanceforGermanyhasriseninrecentyears,asthehighefficiencyofthebusinesseslocatedintheregionhashelpedthemostimportantbranchesoftheGermaneconomytokeeptheiroutputcom-petitiveduringtheglobaleconomicdownturn.Thankstoitsrelatively lowwagesandhighproductivity,CentralEuropehasbecomeafactoryforGer-manproductsontheEUmarketwhoseproductioncouldnothavebeenmovedto Asia. After entering the euro-zone, Germany’s economic situation wasevaluatedverycriticallybothathomeandabroad.Theeconomyremainedstagnant for several years after German reunification. Unemployment inGermany between 1991 and 2001, especially in the new Länder, remainedatahighlevelofaround20%;publicdebtrose,andthecountry’sexchangepaymentsdeficitwithothercountriesremainedhigh.Germany,alongwithFrance,wasthefirsttobreaktherulesonthebudgetdeficitintheeuro-zone.InresponsetothediagnosisofeconomistswhoblamedGermany’sproblemson its overly high labour costs, the government in Berlin introduced a re-formpackagein2003-5calledAgenda2010,limitingsocialbenefits,improv-ingbusinessconditionsandmakingthelabourmarketmoreflexible.Underpressurefromthesereforms,aswellasthethreatbyGermancompaniesthattheywouldtransferjobstothecountriesofCentralandEasternEurope,the

PRA

CE

OSW

09/

2012

11

OSW

REP

OR

T 0

6/20

16

Germantradeunionsloweredtheirwagedemands,focusingonkeepingtheirplantsinGermanyrunning.MoresavingsweregeneratedbymovingpartoftheproductionfromGermanytocountrieswithlowerlabourcosts–thatis,countriesinAsiaandCentralEurope.

ThecentralEuropeanstateshavebecomeanimportantproductioncentreontheEUmarket.Theyhavebecomeanattractiveplacetoinvestcapital,espe-cially forGermansmall-andmedium-sizedbusinesses,becauseafter theyenteredtheEUtheir legislationwasalreadyclosetoGermantaxlaws,andtheirstandardsoflegalprotectionwerehigherthanthoseofotheremergingeconomies.Forthesereasons,investmentinCentralEuropewasalsoeasierforthesmall-andmedium-sizedenterprisessector,whichisstronginGer-many.Moreover,somebulkygoodsdestinedfortheEuropeanmarket,suchas cars ormachinery,were notworth producing in Asia due to transportcosts.Itisnoteworthythatsince2009,GermanautomotivecompanieshavebuiltuptheirproductioncapacityinCentralEuropeinordertogeneratesav-ings.Thesourceofthesesavingswasnolongerlabourcostsalone,whichhadrisen considerably in previous years, but also increased efficiency thankstothefactories’highproductivityandtheimprovingqualificationsoflocalworkers.

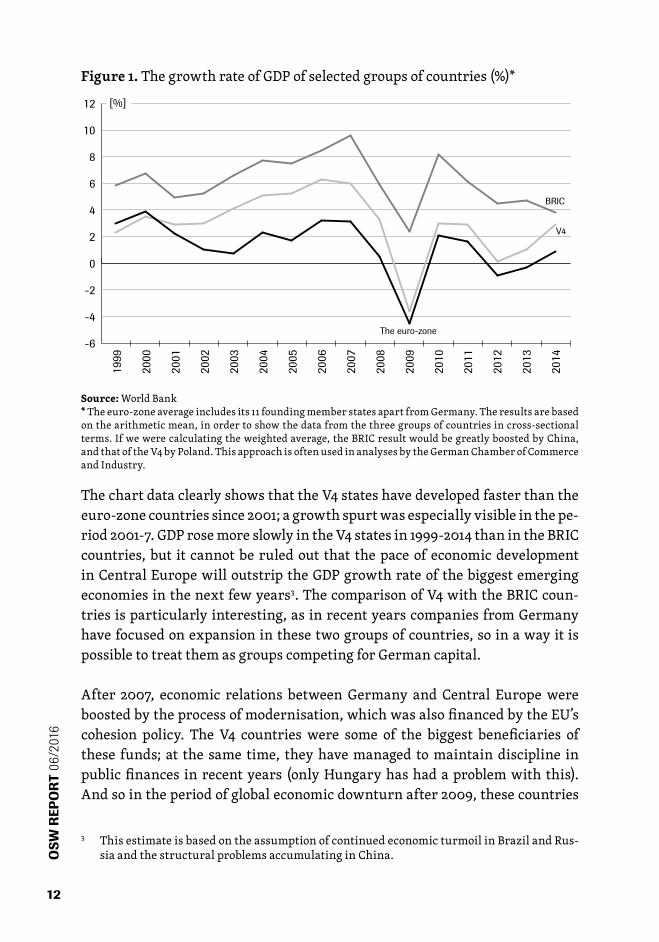

In recent years, the favourable economic situation of the central Europeancountriescontinued,whichincreasedtheirattractivenessasamarketingpart-nerforGermanyagainstthebackgroundofanincreasinglydifficultglobaleco-nomicsituation.TheVisegradGroup’smemberstateshavebeenabletomain-tainahighrateofeconomicdevelopment.Intheperiod1999-2014,theaverageGDPperpersoninthesecountriesrosefrom60%to75%oftheEUaverage2.

2 GDP per capita, consumption per capita and price level indices, December 2015; http://ec.europa.eu/eurostat/statistics-explained/index.php/GDP_per_capita,_consumption_per_capita_and_price_level_indices

PRA

CE

OSW

09/

2012

12

OSW

REP

OR

T 06

/201

6

Figure 1.ThegrowthrateofGDPofselectedgroupsofcountries(%)*

2000

1999

2014

2013

2012

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

The euro-zone

BRIC

V4

-6

-4

-2

0

2

4

6

8

10

12 [%]

source:WorldBank*Theeuro-zoneaverageincludesits11foundingmemberstatesapartfromGermany.Theresultsarebasedonthearithmeticmean,inordertoshowthedatafromthethreegroupsofcountriesincross-sectionalterms.Ifwewerecalculatingtheweightedaverage,theBRICresultwouldbegreatlyboostedbyChina,andthatoftheV4byPoland.ThisapproachisoftenusedinanalysesbytheGermanChamberofCommerceandIndustry.

ThechartdataclearlyshowsthattheV4stateshavedevelopedfasterthantheeuro-zonecountriessince2001;agrowthspurtwasespeciallyvisibleinthepe-riod2001-7.GDProsemoreslowlyintheV4statesin1999-2014thanintheBRICcountries,but it cannotberuledout that thepaceofeconomicdevelopmentinCentralEuropewilloutstriptheGDPgrowthrateofthebiggestemergingeconomiesinthenextfewyears3.ThecomparisonofV4withtheBRICcoun-triesisparticularlyinteresting,asinrecentyearscompaniesfromGermanyhavefocusedonexpansioninthesetwogroupsofcountries,soinawayitispossibletotreatthemasgroupscompetingforGermancapital.

After 2007, economic relations betweenGermany andCentral Europewereboostedbytheprocessofmodernisation,whichwasalsofinancedbytheEU’scohesion policy. The V4 countrieswere some of the biggest beneficiaries ofthese funds; at the same time, theyhavemanaged tomaintaindiscipline inpublicfinances inrecentyears (onlyHungaryhashadaproblemwiththis).Andsointheperiodofglobaleconomicdownturnafter2009,thesecountries

3 ThisestimateisbasedontheassumptionofcontinuedeconomicturmoilinBrazilandRus-siaandthestructuralproblemsaccumulatinginChina.

PRA

CE

OSW

09/

2012

13

OSW

REP

OR

T 0

6/20

16

maintainedhighlevelsofpublicinvestment.Thiswasthereverseofthesitu-ationinmanyothercountries,especiallyinthesouthoftheeuro-zone,whichsignificantlyreducedtheirbudgetaryexpenditureunderthethreatof insol-vency.GermanywasbyfarthegreatestbeneficiaryoftheinvestmentintheV4countriesfinancedby theEU’s cohesionpolicy.Thanks to this,Germanywasableatleasttorelyonadditionalexportstothesecountries,tothetuneof€30billionintheperiod2004-154.ThankstotheinvestmentsfromthecohesionfundinCentralEurope,Germanygainednotonlydirectly,fromthecontractsit acquired, but also indirectly; a significant proportion of these fundswasspentoninfrastructure,whichmadeiteasiertotransportgoodsbetweenGer-manyandCentral&EasternEurope.ThiswasofgreatimportanceforGermanautomotivecompanies, forwhomgood transportnetworkswereaconditionforbuildingmodernproductionfacilitiesintheV4states.

OnthequestionofreformingtheEU,thecountriesofCentralEuropeandGer-manyoftenfoundthemselvesonoppositesidespolitically.ThedominantlineofdisputeswasthedivisionintooldandnewEUcountries.TheV4stateswerewaryoftheextensionofthepowersofEUinstitutionsattheexpenseofthoseoftheirowncountries,andtheylongresistedtheintroductionoftheLisbonTreaty.ThedistrusttowardsthecentralEuropeanEUstateswhichjoinedin2004wasboostedbytheirsupportfortheUSinterventioninIraq,forwhichtheyfacedstrongcriticismfromFranceandGermany.Thelowerlevelofeco-nomicdevelopmentinCentralEuropeencouragedthesecountriestoresisttheintroductionofcertainintegrationsolutions,suchastheunificationofCITtaxrates.Thecountriesintheregionoftenopposedstricterclimatepolicies,whichBrusselssawasoneoftheelementsoftheEU’scommonidentity.In2010,whentheeuro-zonecrisisbegan,anewdividinglineappearedintheEUbetweenthecountriesofNorthandSouth.Itappeared,however,thatthesoutherncoun-triesof theeuro-zone, suchasGreece,Spain,FranceandPortugal,havenotusedtheirmembershipoftheeuro-zonetoimprovetheirtradingcompetitive-ness,andafter2010theybegantostrugglewitheconomicproblems.Germany,whichdecidedtofreezepayrises,makeitslabourmarketmoreflexible,andcutbackonsocialbenefits,founditselfinamuchbetterposition.Thiswasun-comfortableforBerlin,becausethemonetaryunionnowincludedasignificant

4 Report:assessmentofthebenefitsobtainedbytheEU-15memberstatesasaresultoftheim-plementationofthecohesionpolicyinthecountriesoftheVisegradGroup,December2011;http://ibs.org.pl/app/uploads/2015/12/Ocena-korzy%C5%9Bci-uzyskiwanych-przez-pa%C5%84stwa-UE-15-w-wyniku-realizacji-polityki-sp%C3%B3jno%C5%9Bci-w-krajach-Grupy-Wyszehradzkiej.pdf,p.52.

PRA

CE

OSW

09/

2012

14

OSW

REP

OR

T 06

/201

6

numberofmemberstateswithproblems,andthustherewasariskthattheywould throw the burden of their problems ontoGermany.One symptomofthiswastheisolationofGermany’srepresentativesontheforumoftheEuro-peanCentralBank,whosedecisionsoftenwentagainstBerlin’sdemands.Inthissituation,thecountriesofCentralEuropewhichhadjoinedtheeuro-zone,suchasEstonia,Lithuania,LatviaandSlovakia,provedtobevaluablealliesforGermany.BratislavawasoneofthemostvocalopponentstograntingloanstoAthens,whichatthattimewasthreatenedbyinsolvency.

TheV4stateswillbeanimportantvoiceinanydebateonfurtherreformstotheEuropeanUnioninthenextfewyears.Whenthattimecomes,Germanywillbeontheoppositesidetothesoutherneuro-zonecountriesbecauseofitsdifferenteconomicconditions.Currentlyadeepeninggapcanbeobservedbe-tweenGermany,whichhasregisteredafavourableeconomicperformanceandisreducingitsdebt,andthemonetaryunion’ssoutherncountries,whosedebtsarestillrising.Inanyfuturedebate,Berlinwillprobablystandforamorefree-marketEU,anditisnotclearwhetheritwillbeabletocountonsupportinthismatterfromLondon,whichisconsideringleavingtheUnion.CentralEurope,whichistiedtoGermanybystrongeconomicinterests,mayprovetobeakeypartnerinthequestionofreformingtheEU.

PRA

CE

OSW

09/

2012

15

OSW

REP

OR

T 0

6/20

16

II. The developmenT of Trade beTween germany and The v4

Inrecentyears,theV4grouphasbecomeoneofGermany’skeytradepartners,ina relationship thathascomecloser to reachingequality.Notonly isGer-manytheV4group’smostimportanttradingpartner,butalsoviceversa;theV4statesasoneregionareakeypartnerforGermany.Itisalsoworthemphasis-ingthatalthoughtheGermaneconomyisabletogenerateatradesurpluswithmostcountriesoftheworld,itmaintainsarelativebalancewiththeV4states’economies.TheircooperationwithGermanyoffersawiderangeofbenefits,andhasagoodopportunitytodevelop,especiallyduringtheglobaleconomicdownturn.Despite this, strongeconomicrelationswithGermanyalonewillnothelptheV4countriestoescapetheso-calledmiddleincometrap.ItishardtoexpectthatGermancompanieswillbereadytomovetheirR&Dactivitytotheregiononalargerscale,asthisisanareawhichgeneratesthemostprofitfortheGermaneconomy.ThehithertoprofitablecollaborationwithGermanymaydiscouragemanycompaniesfromCentralEuropefromlimitingtheirde-pendenceonGermancompaniesandworkingonproducingtheirownincreas-inglytechnicallyadvancedproducts.

1. The role of central europe as a key trading partner for germany

Inthelastdecade,theroleofforeigntradeintheGermaneconomyhasgrownextremelyrapidly.Since2007, theV4countries taken togetherhavebecomeGermany’s important trading partner, providing the most components forGermanexporters(aftertheUSA),andthuscontributingtotheimprovementinthetradingcompetitivenessofGermany’seconomy.

Inthelasttenyears,thedevelopmentoftradehasbecomeoneofGermany’smost important sources of economic growth, especially since internal con-sumptionhasnotproventobeanimportantdriverofeconomicdevelopment.In the years 2004-8, Germany’s turnover rose very dynamically, thanks togoodtimesintheeuro-zoneandontheemergingmarkets.Thebiggestreces-sion inpost-warGermanhistory in2009,whenGDPfellby5%,didnot leadtoaprolongedweakeningofgrowthinGermany.Despitetheinitialcollapseof German trading, the losseswere quickly recovered, and in the next fewyearssalesofGermanproductsabroadrosesteadily.TradingcompetitivenessprovedtobeoneofthemainfactorsmaintainingstableeconomicgrowthinGermany,andwhichalsostrengthenedthecountry’simageasastrongecono-mywhichhadmanagedtoresisttheeconomiccrisis.Themostvisiblesymbol

PRA

CE

OSW

09/

2012

16

OSW

REP

OR

T 06

/201

6

ofthispowerwasthetradesurplus,whichhadbeenrisingforadecade.Since2012,Germanyhasrecordedthelargestcurrent-accountsurplusintheworld5.In2014 itamountedtoUS$285billion,whichwasalmostdoublethevalueofthat of second-rankedChina (US$150billion) andalmost three timeshigherthanthird-rankedSaudiArabia(US$100billion)6.ThescaleofthesuccessofGermanexports isgreater thanwhencomparedwith thesituationofmanyothercountriesintheeuro-zone,suchasGreece,SpainorPortugal,whichinrecentyearshavebeengrapplingwiththeconsequencesofsignificantcurrentaccountdeficitswhichthreatentobankruptthem.

Figure 2.Germanexportstoselectedcountriesaroundtheworld,andtotheV4group(€billion)

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0

20

40

60

80

100

120

0

20

40

60

80

100

120

Japan

Russia

V4

V4

USA

USA

France

France

Great Britain

Great Britain

EXPORTS

Netherlands

China

Japan

Russia

IMPORTS

Netherlands

China

[€ billion]

[€ billion]

source:FederalStatisticalOffice

5 Goodstradeisoneofthekeyfactorsshapingthecurrentaccountvalue,whichrepresentsthestateofcashflowsbetweenthecountryandabroad.

6 DeutschlandhatweltweitgrößtenExportüberschuss,Die Welt,2February2015;http://www.welt.de/wirtschaft/article137024573/Deutschland-hat-weltweit-groessten-Exportueber-schuss.html

PRA

CE

OSW

09/

2012

17

OSW

REP

OR

T 0

6/20

16

ThereisadirectrelationshipbetweentheimprovementoftheGermanecon-omyoverrecentyearsanditsclosercommercialrelationswithCentralEu-rope.TheV4countriesareplayinganevergreaterrole,fromthepointofviewofGermaneconomicinterests,becausetheyhavebeenreceivingthelargestshareofexports.Backin2008theV4grouptakentogetherbecamethemostimportantbuyersofGermangoods;however,duringtheeconomiccrisisin2009,theyreducedtheirdemandforGermangoodstoagreaterextentthan,for example, France. In subsequentyears theirpositiongradually revived.Asaresult, in2014Germancompaniessoldgoodsworth€112billionintheV4countries–9.8%morethaninFrance,acountrywhichisricherandmorepopulousthanalltheV4statestogether.TheV4countriesalsoovertookChi-nainthisrespect,by50%,andRussiabyafactoroffour,eventhoughRus-siaisrecognisedinGermanyasanextremelylucrativemarket.ItshouldbenotedthatthestrongpositionoftheV4countrieswouldnothavebeenpossi-blewithouttheirstrongintegrationintothesupplychainofGermany,whosecompaniesownmanyfactoriesinthesecountries.ThisalsoboostsGermanexports.Ononehand,GermanplantslocatedinV4countriesacquiresomeoftheirpartsfromtheirmother-factoriesinGermany.Ontheother,thehighlevelofexportsfromGermanytotheV4countriesalsoresultsfromthelat-ter’sgreaterpurchasingpower,becausetheyarebuyingagrowingpropor-tion of the added value from the production of flagshipGerman products,suchascarsormachinery.

Thetrendinimportshasdevelopedsomewhatdifferently.Since2004,theV4statestakentogetherhavebeenthemost importantexportersontotheGer-manmarket,andtheirpositiondidnotfalterevenduringthecrisisin2009,thegreatestrecessioninpost-warGermanhistory.ItisworthnotingthatGer-manimportsfromtheV4countrieshavecontinuedatarelativelystablelevel,comparedwiththestagnationofimportsfromChina,RussiaandFranceoverthelastfiveyears.ThistestifiestothegreatimportanceofthefactorieslocatedinV4countriesinmaintainingthepricecompetitivenessofGermanindustry.Ononehand,companiesfromGermanyprefernottoincreasetheirsuppliesfromothercountries,whilestillbringinginevermoregoodsfromtheV4coun-tries.Ontheotherhand,Germancompanieshavebeenlookingfornewsup-pliersinCentralEurope,whoadmittedlywouldnotoffersuchlowproductioncostsascountriesinAsia,butwhoseproductivityandproductionqualitycouldmatchthoseofcountriesinWesternEurope.

PRA

CE

OSW

09/

2012

18

OSW

REP

OR

T 06

/201

6

Figure 3.ValueofGermany’sforeigntradewithindividualcountriesper capi-ta(€thousands)between2004-2014

2004 20062005 20082007 20102009 2011 2012 2013 2014

Belgium

V4

Netherlands

Austria

Switzerland

Great Britain

France

0

2

4

6

8

10

12 [€ thousands per capita]

source:FederalStatisticalOffice

AninterestingperspectiveontradebetweenGermanyandV4isrevealedbyasummaryoftradeper capita,whichshowstheintensityofthetrading.FromthechartweseethattheV4statesarecharacterisedbyhighertradewithGer-manyper capita thancountriessuchasFranceor theUnitedKingdom,withasignificantincreaseafter2009.AmongtheV4countriestherearelargevari-ations. In2014, theCzechRepublic,withnearly€7000perperson,hadonlyslightlylowertradeper capitawithGermanythanBelgium.HungaryandSlo-vakia’stradewithGermanyranataround€4000,andPolandslightlyless,with€2300per capita–nevertheless,runningaheadofBritainandapproachingthelevelofFrance.FromthisitcanalsobeconcludedthattheV4statesstillhavegreatpotentialtoexpandtheirtradewithGermany.TheexampleofcountriesmorestronglyintegratedwiththeGermaneconomy,suchasAustria,Belgium,theNetherlandsorSwitzerland,showsthatthevalueoftradeper capitacouldreach€10,000perannum.However,itshouldbepointedoutthatthehighlevelofGermantradewiththesecountriesalsostemsfromtheirabilitytoselltheirowntechnologies toGermanbusinesses.This is thereforenotarelationshipbasedlargelyonmanufacturingproductstotheorderofGermancompanies,asitisinthecaseofV4.

PRA

CE

OSW

09/

2012

19

OSW

REP

OR

T 0

6/20

16

Figure 4.ProportionofdeliveriesfromselectedcountriesinGermanexports7(%)

0.0

0.5

1.0

1,5

2.0

2.51995 2000 2005 2009 2011

[%]

USA V4 France GreatBritain

Italy ChinaRussia

source:TheOECD-WTOTradeinValueAdded(TiVA)database,May2013;http://stats.oecd.org/

ThefiguresfromtheOECDandtheWTOdatabasesallowustoexaminewhatproportionofGermanexportswasbasedoncomponentsmadebyindividualstates.TheroleoftheV4countriesassuppliersforGermanexporters,along-sideChinaandRussia,hasincreasedsignificantlyinrecentyears.In1995,theproductionofV4comprisedaddedvalueinGermanoverseassalesof0.7%;overthenext 16years this indicator tripledto2.1%. Inthisway, theV4countriestooksecondplace(aftertheUS)asthemostimportantsuppliersforGermanexporters,aheadofFrance,Britain,Russia,ItalyandChina.ThismeansthattheV4countrieshavebecomeoneofthemostimportantregionsinGermany’ssupplychain,aswellasanimportantsourceofthecompetitivenessofGermancompanies,especiallyfortheautomotive(3.3%ofvalueaddedinforeignsales)andconstruction industries (2.7%).Combiningthisdatawiththefigures forforeigntradebetweenGermanyandV4,wecancometo theconclusionthat21%ofallGermanimportsfromV4areusedinonwardexports(in1995,thisfigureamountedto13%).

The development of Germany’s commercial relationswith the V4 countriesstillhasconsiderablepotentialfordevelopment,togetherwiththeincreasing-lysophisticatedtiesbetweenthesecountries.Itseemsthattheprospectsformoderateeconomicgrowth,orevenstagnation,inEuropewillboostGermancompanies’interestinreducingproductioncostsbymovingpartoftheirac-tivitytoCentralEurope,whichwillbeassociatedwithanincreaseinimports

7 ThisdataisavailablethankstothemethodologydevelopedjointlybytheWorldTradeOr-ganisationandtheOECD.Detailsofthemethodologyavailableat:https://www.wto.org/eng-lish/res_e/statis_e/miwi_e/tradedataday13_e/oecdbrochurejanv13_e.pdf

PRA

CE

OSW

09/

2012

20

OSW

REP

OR

T 06

/201

6

fromthesecountries.ThegrowthinprosperityoftheV4countrieswillthusresultinincreasedGermanexportstothem.

TheV4countries’successintheirrelationswithGermanyisbasedonstableconditionsfordevelopment,aswellastheirgeographicalproximity,whichhasenabledthesignificantinvolvementofGermansmallandmedium-sizedenter-prises.Forthisreason,GermantradewiththeV4countrieshasamuchhighervaluethanwithother,muchlargerstatessuchasJapan,RussiaorTurkey.Thisthereforedemonstratestheveryhighdegreeofmutualcomplementaritybe-tweenGermanyandtheV4countries.

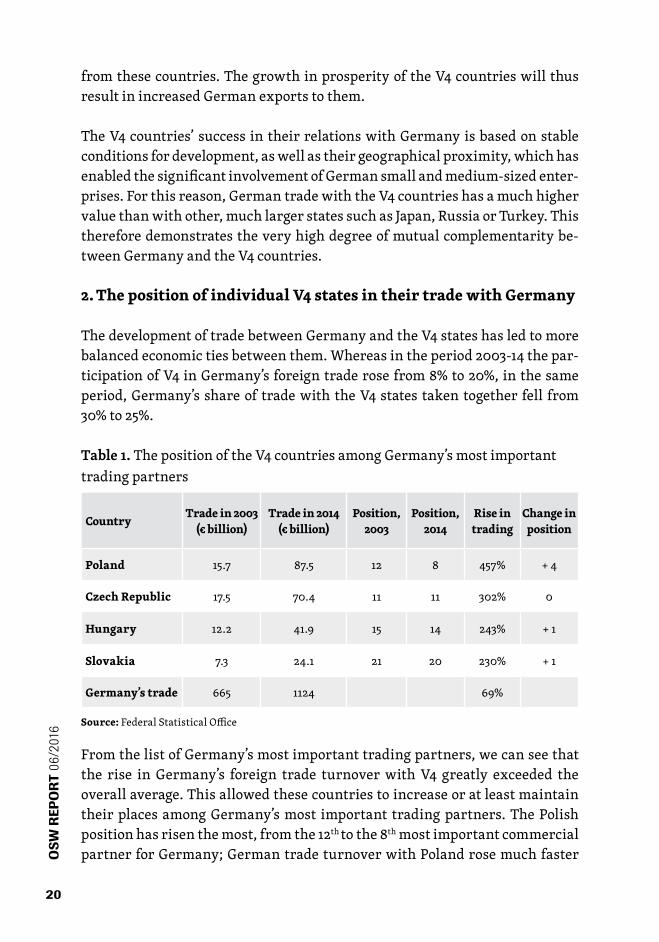

2. The position of individual v4 states in their trade with germany

ThedevelopmentoftradebetweenGermanyandtheV4stateshasledtomorebalancedeconomictiesbetweenthem.Whereasintheperiod2003-14thepar-ticipationofV4inGermany’sforeigntraderosefrom8%to20%,inthesameperiod,Germany’sshareoftradewiththeV4statestakentogetherfell from30%to25%.

Table 1.ThepositionoftheV4countriesamongGermany’smostimportanttradingpartners

country Trade in 2003(€ billion)

Trade in 2014(€ billion)

position, 2003

position, 2014

rise in trading

change in position

poland 15.7 87.5 12 8 457% +4

czech republic 17.5 70.4 11 11 302% 0

hungary 12.2 41.9 15 14 243% +1

slovakia 7.3 24.1 21 20 230% +1

germany’s trade 665 1124 69%

source:FederalStatisticalOffice

FromthelistofGermany’smostimportanttradingpartners,wecanseethatthe rise inGermany’s foreign trade turnoverwithV4 greatly exceeded theoverallaverage.ThisallowedthesecountriestoincreaseoratleastmaintaintheirplacesamongGermany’smost important tradingpartners.ThePolishpositionhasrisenthemost,fromthe12thtothe8thmostimportantcommercialpartnerforGermany;GermantradeturnoverwithPolandrosemuchfaster

PRA

CE

OSW

09/

2012

21

OSW

REP

OR

T 0

6/20

16

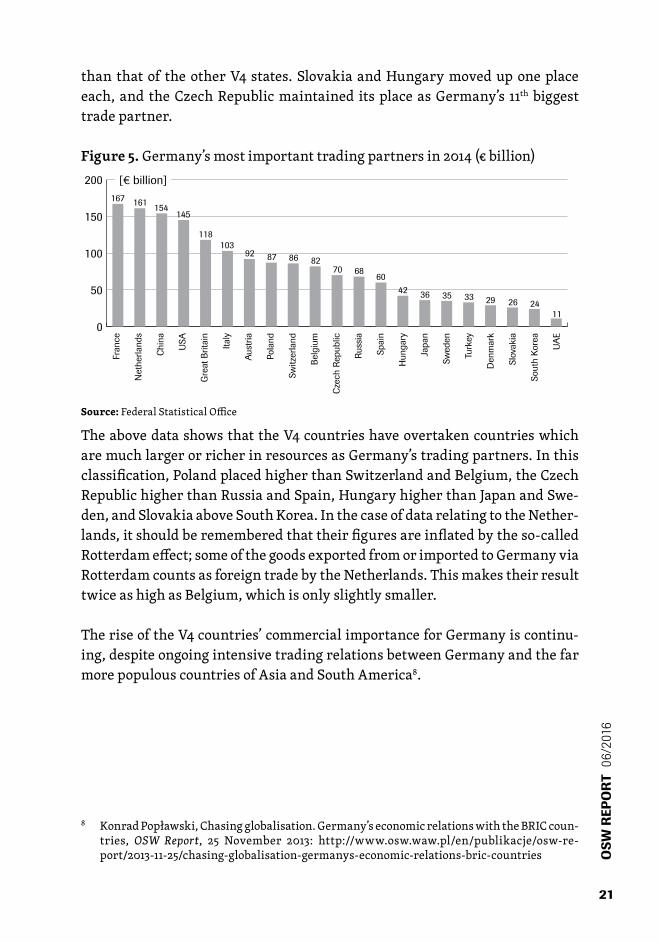

thanthatof theotherV4states.SlovakiaandHungarymoveduponeplaceeach,andtheCzechRepublicmaintained itsplaceasGermany’s 11thbiggesttradepartner.

Figure 5.Germany’smostimportanttradingpartnersin2014(€billion)

0

50

100

150

200

Fran

ce

Net

herla

nds

Chin

a

USA

Gre

at B

ritai

n

Italy

Aust

ria

Pola

nd

Switz

erla

nd

Belg

ium

Czec

h Re

publ

ic

Russ

ia

Spai

n

Hun

gary

Japa

n

Swed

en

Turk

ey

Den

mar

k

Slov

akia

Sout

h Ko

rea

UAE

[€ billion]167 161 154

118103

92 87 86 8270 68

6042 36 35 33 29 26 24

11

145

source:FederalStatisticalOffice

TheabovedatashowsthattheV4countrieshaveovertakencountrieswhicharemuchlargerorricherinresourcesasGermany’stradingpartners.Inthisclassification,PolandplacedhigherthanSwitzerlandandBelgium,theCzechRepublichigherthanRussiaandSpain,HungaryhigherthanJapanandSwe-den,andSlovakiaaboveSouthKorea.InthecaseofdatarelatingtotheNether-lands,itshouldberememberedthattheirfiguresareinflatedbytheso-calledRotterdameffect;someofthegoodsexportedfromorimportedtoGermanyviaRotterdamcountsasforeigntradebytheNetherlands.ThismakestheirresulttwiceashighasBelgium,whichisonlyslightlysmaller.

TheriseoftheV4countries’commercialimportanceforGermanyiscontinu-ing,despiteongoingintensivetradingrelationsbetweenGermanyandthefarmorepopulouscountriesofAsiaandSouthAmerica8.

8 KonradPopławski,Chasingglobalisation.Germany’seconomicrelationswiththeBRICcoun-tries, OSW Report, 25 November 2013: http://www.osw.waw.pl/en/publikacje/osw-re-port/2013-11-25/chasing-globalisation-germanys-economic-relations-bric-countries

PRA

CE

OSW

09/

2012

22

OSW

REP

OR

T 06

/201

6

Figure 6.Germany’sshareintheV4countries’foreigntrade

20042003 2005 2006 2007 2008 2009 2010 2011 2012 2013 201415

20

25

30

35

40 [%]

Czech Republic

Hungary

Poland

Slovakia

source:UnitedNationsConferenceonTradeandDevelopment;http://unctadstat.unctad.org

Intheperiod2003-14theGermanshareintheV4states’foreigntradebegantofall,thankstowhichGermany’sdominantpositionwasreducedfrom30%to25% for theV4groupasawhole.During the sameperiod, the totalpar-ticipationoftheV4statesinGermany’sforeigntraderosefrom7.9%to20%.DeeperanalysisallowsustoconcludethattheindividualV4countrieshavemaintained theirdependenceson tradewithGermany tovaryingdegrees.Intheperiod2003-14,inthecaseoftheCzechRepublicthisindicatorfellby6percentagepoints(pp)to29%;forHungary,itfell3ppto26%;forPoland,2.5ppto24%;andforSlovakia,9ppto19%.Thischangeshouldbeconsideredasdesirable,because it increases thegeographicaldiversificationof theV4countries’foreigntrade.

PRA

CE

OSW

09/

2012

23

OSW

REP

OR

T 0

6/20

16

Figure 7.Germany’sexportstoandimportsfromindividualVisegradGroupcountries(€billion)

200420032002200120001999 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Czech Republic

Hungary

Slovakia

0

10

20

30

40

50 [€ billion] Poland

200420032002200120001999 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Hungary

0

10

20

30

40

50 [€ billion]

Poland

EXPORTS

IMPORTS

Czech Republic

Slovakia

source:FederalStatisticalOffice

GermanexportstoindividualV4countrieshavebeenproportionaltothesizeoftheireconomies,whichresultsfromthesimilarityoftheirdemandforGer-mangoods.AfteraccessiontotheEU,salesofgoodsfromGermanytoPolanddevelopedmostrapidly(15%annuallyonaverage)alittlemoreslowlytoSlo-vakia(10%)andtheCzechRepublic(9%),andmostslowlyinHungary(5.5%).Theeconomiccrisisin2009affectedexportsfromGermanytotheV4,whichdroppedby20-30%.Germancompaniestookthelongesttimetorecoverfromthelossesof2009inexportstoHungary,achievingthisonlyafterfiveyears,whereasinthecaseoftheotherV4statesthreeyearswasenough.

InanalysingGermanimportsfromtheV4countries,theverystrongpositionoftheCzechRepublicisnoteworthy.TheGermanmarketreceivesonlyslightlyfewergoods fromtheCzechRepublic than itdoes fromthemuch largerPo-land.CzechmanufacturersprovideGermanywithfarmoregoodsper capitathanSlovakiaorHungary.However,ifwelookatthedynamicsofthegrowth

PRA

CE

OSW

09/

2012

24

OSW

REP

OR

T 06

/201

6

ofimportstoGermanyfromtheV4countriesaftertheiraccessiontotheEU,Polandistheleader(withanaveragegrowthrateof15%),followedbytheCzechRepublic(12%),Slovakia(7.5%)andHungary(6.5%).

Figure 8.Germany’stradebalancewithselectedcountries(€billion)

2004 2014201320122005 2006 2007 2008 2009 2010 2011-30

-20

-10

0

10

20

30

40

50 [€ billion]USA

* Slovakia / ** Czech Republic / *** Hungary*****

Poland

Norway

Russia

China

France Great Britain

*

source:FederalStatisticalOffice

Inrecentyears,Germanyexperiencedanegativebalanceoftradewithraw-materialsupplierssuchasNorwayandRussia,aswellasitsmajorsubcontrac-tors,suchasChina.Germanyremainedapositivetradebalancewithhighlydevelopedstates,suchastheUSA,GreatBritain,FranceandAustria.Againstthisbackground,itstradebalancewiththeCzechRepublic,SlovakiaandHun-garywasclosetoeven.InitiallyPolandsawagrowingtradedeficitwithGer-many,althoughthishasfallen inrecentyears, to the levelof€8billion.TheotherV4countries,afterseveralyearsofrelativestability,havebegunexperi-encingasurplusintradewithGermany.However,theseresultsrequiresomeclarification.Data from thePolishMainStatisticalOffice shows thatPolandactuallyrecordedatradesurpluswithGermanyforseveralyears9.Theability

9 PolishdatashowsthatPolandhadatradesurpluswithGermanyin2014of€6.5billion,asithadrecordedabout€4billionmoreinexportstoGermany(€43.6billion)and€10billionlessinimportsfromGermany(€37billioneuros).AccordingtotheinformationfromtheMainStatisticalOffice,thesedifferencesstemfromthefactthatinGermanstatistics,goodssentfromChinatoPolandviatheGermanportsarecountedasexportsfromGermanytoPoland.IfPolishcalculationshadbeenconsideredinthefigure,Poland’stradepositionwithregardtoGermanywouldbeclosertothatoftheotherV4states.(Responsebythevice-presidentoftheMainStatisticalOffice,undertheauthorityofthePresidentoftheCouncilofMinisters,

PRA

CE

OSW

09/

2012

25

OSW

REP

OR

T 0

6/20

16

togenerateabalancedtraderelationship,however,doesnotderivefromthecurrentattractivenessofV4productsforGermanconsumers,butratherfromexportsfromtheGermanfactorieslocatedinthesecountries.

3. risks associated with the v4’s dependence on trade with germany

ThetradestructuresofbothGermanyandtheV4statesaresimilar.Certainsectors predominate, such as: machinery, vehicles, and chemical products.CompaniesfromtheseindustriesaretheleadingbusinessesinGermany,andatthesametimemajorinvestorsintheV4states.SuchtradewillbringbenefitstotheV4countriesinthemediumterm,butinthelongtermitisassociatedwith the risk of dependence on overly homogeneous production structures,andonfailuretodevelopintheIT&telecommunicationssector.

Figure 9.StructureofGermany’sexporttoV4countriesin2014(%)*

Cars & vehicles34.2%

POLAND CZECH REPUBLIC

Finished products10.3%

Food & tobacco7.4%

Raw materials7.0%

Chemical products15.4%

Semi-finished goods19.4%

Other6.3%

Cars & vehicles44.3% Finished products

9.6%

Food & tobacco4.6%

Raw materials5.5%

Chemical products12.8%

Semi-finished goods17.7%

Other5.5%

Cars & vehicles56.9%

HUNGARY SLOVAKIA

Finished products8.1%

Food & tobacco5.9%

Raw materials1.4%

Chemical products10.0%Semi-finished goods

15.2%

Other4.3%

Cars & vehicles46.1%

Finished products13.6%

Food & tobacco3.8%

Raw materials3.5%

Chemical products9.6%Semi-finished goods

18.3%

Other5.0%

Cars & vehicles34.2%

POLAND CZECH REPUBLIC

Finished products10.3%

Food & tobacco7.4%

Raw materials7.0%

Chemical products15.4%

Semi-finished goods19.4%

Other6.3%

Cars & vehicles44.3% Finished products

9.6%

Food & tobacco4.6%

Raw materials5.5%

Chemical products12.8%

Semi-finished goods17.7%

Other5.5%

Cars & vehicles56.9%

HUNGARY SLOVAKIA

Finished products8.1%

Food & tobacco5.9%

Raw materials1.4%

Chemical products10.0%Semi-finished goods

15.2%

Other4.3%

Cars & vehicles46.1%

Finished products13.6%

Food & tobacco3.8%

Raw materials3.5%

Chemical products9.6%Semi-finished goods

18.3%

Other5.0%

*CategoriesbasedontheSITCclassification.The‘food&tobacco’categoryalsocoversliveanimals,animalandvegetablefatsandoils.The‘rawmaterials’categoryincludesminerals,aswellasnon-mine-ralitemssuchasrubber,cottonandironore.The‘semi-finishedgoods’categoryincludesitemssuchaspaper,textiles,cementandsteel.The‘other’categorycoversfurniture,clothing,shoes,cameras,booksandtoysamongothers(seehttp://unstats.un.org/unsd/cr/registry/regcst.asp?Cl=14).source:FederalStatisticalOffice

toquestionno.22326onthediscrepanciesofstatisticsontradebetweentheRepublicofPo-landandtheGermanFederalRepublic,presentedbytheCSOandtheFederalStatisticalOf-fice;http://orka2.sejm.gov.pl/IZ6.nsf/main/275B09FA)

PRA

CE

OSW

09/

2012

26

OSW

REP

OR

T 06

/201

6

ThestructureofGermanexportstotheindividualV4countriesissimilar.ThemajorityofsalesbyGermancompaniesaretheflagshipproductsofthecoun-try’seconomy,namelymachinesandcars:mosttoHungary,slightlylesstotheCzechRepublicandSlovakia,andtheleasttoPoland.ItisworthpointingoutthatsomeoftheseexportswerecomponentsforthefactoriesoftheGermancorporationslocatedinthesecountries.AsignificantshareoftheexportsfromGermanytoV4ismadeupofsemi-finishedgoods,otherfinishedproductsandchemicalproducts.Poland,whichimportsamuchsmallerpercentageofcarsfromGermanythanotherV4countries,receivesproportionatelymoregoodsfromothercategories.ThisprobablyaccountsforthesmallerparticipationofGermanautomotivefactoriesintradebetweenPolandandGermany.Ononehand,itshowsthelowerinvolvementofGermancarcompaniesinPolandinrelationtothesizeoftheeconomythanintherestofV4.Ontheother,thead-vantageofsucharelationshipisthatthePolisheconomyislesssusceptibletocrisesontheautomotivemarket.Forexample,in2009,whenglobalcarmarketsalescollapsed, theeconomiesof theCzechRepublic,SlovakiaandHungaryfellintorecession,whilePolandwasabletomaintaineconomicgrowth.

Figure 10.ThestructureofGermanimportsfromV4countriesin2014(%)

Cars & vehicles34.3%

POLAND CZECH REPUBLIC

Finished products14.6%

Food & tobacco10.0%

Raw materials6.2%Chemical products

6.6%

Semi-finished goods19.4%

Other8.8%

Cars & vehicles54.0%

Finished products11.2%

Food & tobacco2.8%

Raw materials4,6%

Chemical products4.7%

Semi-finished goods15.3%

Other7.3%

Cars & vehicles66.2%

HUNGARY SLOVAKIA

Finished products9.8%

Food & tobacco3.5%

Raw materials1.8%

Chemical products4.0%

Semi-finished goods9.3%

Other5.3%

Cars & vehicles62.7%

Finished products9,8%

Food & tobacco0,9%

Raw materials1,7%

Chemical products3,3%Semi-finished goods

15,3%

Other6,3%

Cars & vehicles34.3%

POLAND CZECH REPUBLIC

Finished products14.6%

Food & tobacco10.0%

Raw materials6.2%Chemical products

6.6%

Semi-finished goods19.4%

Other8.8%

Cars & vehicles54.0%

Finished products11.2%

Food & tobacco2.8%

Raw materials4,6%

Chemical products4.7%

Semi-finished goods15.3%

Other7.3%

Cars & vehicles66.2%

HUNGARY SLOVAKIA

Finished products9.8%

Food & tobacco3.5%

Raw materials1.8%

Chemical products4.0%

Semi-finished goods9.3%

Other5.3%

Cars & vehicles62.7%

Finished products9,8%

Food & tobacco0,9%

Raw materials1,7%

Chemical products3,3%Semi-finished goods

15,3%

Other6,3%

source:FederalStatisticalOffice

ThestructureofGermanimportsfromtheV4countries issimilartothatofexports.ItisworthnotingthatinGermany’stradewiththeCzechRepublic,

PRA

CE

OSW

09/

2012

27

OSW

REP

OR

T 0

6/20

16

SlovakiaandHungary,theautomotivesector’sshareishigherinimportsthanexports.ThismeansthatthesethreeV4stateshavebeenabletoachieveasur-pluswithGermany in the trade of cars and car parts.Despite the fact thatasignificantportionoftherevenuegoestotheGermanautomotivecompanieswhichownthefactories,italsobenefitstheCzechRepublic,SlovakiaandHun-gary,thankstogreateremploymentinthesecountries,aswellasincreasedtaxreceipts.Comparedtothesecountries,tradebetweenGermanyandPolandinautomotiveproductsismuchmorebalanced.WhenanalysingtheremainingcategoriesofGermanimportsfromtheV4countries,wenoticetherelativelysmallproportionofchemicalproducts,duetothecontinuedstrongpreferenceofGermanchemicalcompaniestomaintainproductioninGermany.Onefea-tureofGermanimportsfromPolandis(asinthecaseofexports)greaterdi-versitythaninthecaseoftheotherV4states.AlargepercentageofPoland’sexportstoGermanyisrepresentedbyfoodstuffsandfinishedproducts.

WhenanalysingtheOECDdata,wemayaddthat49%ofthecarpartsexportedfromPolandtoGermanyareimportedbyautomotivecompaniesfromGerma-nyfortheirownexports.FortheCzechRepublic,thisratiois32%,forSlova-kia29%andforHungary21%.Thesituationregardingtheexportofpartsformachinesissimilar; inthecaseofPoland,53%ofpartssenttoGermanyarere-exportedonwards,inthecaseofSlovakia42%,intheCzechRepublic32%,andHungary27%.PolandprovidesmorecomponentsforproductsexportedbyGermancompaniesthantheotherV4countries.

ThisclosedependenceonGermanyposesariskofinstabilityfortheeconom-icdevelopmentofCentralEurope.TheeconomicdevelopmentofGermanyisbasedonthelargeparticipationofforeigntrade,duetowhichthecountryisdependentonthebusinesscycleontheglobalmarketplacetoagreaterextentthanotherlargeeconomies.Ifglobaltradeslowsdownoverthenextfewyears,Germanymaysufferfromthismorethanthosememberstateswhicharede-veloping thanks todomestic factors. It isnotknownwhetherGermanywillbeabletomaintainitsconsiderabletradesurplus.Manycountries,aswellastheInternationalMonetaryFund,havecriticisedGermanyinrecentyearsforrunningamodelofeconomicdevelopmentwhichisunbalancedandcontrib-utestotheemergenceofglobalimbalances.Germany’shightradesurplushasbeenaconsiderablesourceofincomeforGermancompanies.However,italsocontributestosignificantimbalancesintheeuro-zone,sincetheincomeisnotspentwithinGermanyitself,butinsteadistransferredabroad,intheformofeitherinvestmentsorloans,forexample,tothemostindebtedcountriesintheeuro-zone.Atthesametime,infrastructureinGermanyhasbeenneglected,

PRA

CE

OSW

09/

2012

28

OSW

REP

OR

T 06

/201

6

and its condition has deteriorated over recent years.However, it cannot beruledoutthatthissituationwillchangeoverthenextfewyears.Germanyhasrecentlywitnessedarevivalindomesticdemand;theGermangovernmentisalsoawareoftheproblemsofthelowlevelofinvestmentinthecountry.Sig-mar Gabriel, Vice-Chancellor and economy minister, suggested in January2016that€600billioneurosshouldbeinvestedininfrastructuredevelopment,education,andsupportingthecarindustryby2025(bymeansofasurchargeonthepurchaseofelectriccars)10.

GermanyhasforyearsbeencriticisedbytheUnitedStates,someeuro-areastates,aswellas internationaleconomicinstitutionssuchastheIMF11andtheOECD12,forbasingitseconomicdevelopmentonexports,generatinghightradesurplusesandinsufficientgrowthindomesticdemand.Germany’sin-ternationalcompetitivenessisbasedinparticularonthesuccessoftheauto-motiveandelectro-mechanical sectors.Thedynamicdevelopmentof theseindustries in recent years stemmed in largepart from thedevelopment ofemergingeconomiesthatneedmachinesandvehiclestocarryoutthepro-cessofmodernisation.Thedevelopedeconomies,andinparticulartheeuro-zone,werenotsuchanattractiveoutletmarketbecauseoftheneedtoimple-mentbudgetarysavings.Inthefaceofrisinggeopoliticalthreats,structuralproblems, the fall in income from the saleof rawmaterials, aswell as theriskofcapitaloutflow,itseemsthattheemergingeconomieswillnotbeableinsubsequentyearstoreplacethedevelopedcountriesingeneratingglobaleconomicgrowth.Amongthecountriesthathavegeneratedlargecommer-cialbenefitsforGermanyinrecentyears,twoareinseriouscrisis(BrazilandRussia),andthesituationofChina–thethirdandmostimportantoftheBRICstatesfortheGermanmarket–isfraughtwithincreasinguncertainty.Ifthecleardeclineinthegrowthrateofemergingeconomiesprovestobeadurablephenomenon,demandforGermancapitalgoodswillfall,whichinturnwillreducethelevelofordersfromthefactoriesofGermancompanieslocatedintheV4states.

10 SPD:600MilliardenEurofürModernisierung,Handelsblatt,29January2016,p.7.11 KonradPopławski,Germanyisdefendingitsexports-basedmodelofeconomicdevelopment,

OSW Analyses,17November2010;http://www.osw.waw.pl/en/publikacje/analyses/2010-11-17/germany-defending-its-exports-based-model-economic-development

12 Germany:KeepingtheEdge:CompetitivenessforInclusiveGrowth,BetterPoliciesSeries,OECD,February2014,p.6-8;http://www.oecd.org/germany/Better-policies-germany.pdf

PRA

CE

OSW

09/

2012

29

OSW

REP

OR

T 0

6/20

16

Figure 11.GDPgrowthinselectedEUcountriesin2009(%)

-7-6-5-4-3-2-10123

HungaryGermanySlovakiaEU28GreatBritain

CzechRepublicSpainFrance

Poland

[%]

source:Eurostat

The risks associatedwith becoming dependent on a favourable situation inworldtradearewellillustratedbytheeconomicsituationinEuropein2009.Theworldenteredrecession,andglobaltradeflowsingoodsfellby12%.TheglobalcrisisaffectedGermanyandtheV4countries(exceptPoland)toanex-ceptionaldegree;theysawworseresultsthantheaveragefortheEUasawhole.TheCzechRepublic,Germany,SlovakiaandHungaryrecordedsomeofthebig-gestfallsinGDPintheworldatthattime,incontrasttothosecountrieswhichhadlesshomogeneousstructuresofproduction.

Thecooperationbetween theV4countriesandGermanyposes the risk thattheV4stateswillbecomestuckinthegroupofcountrieswithamediumlevelofdevelopment. Inrecentyears, theconceptof the ‘middle incometrap’hasbeguntoenjoyacertainpopularity.Onthebasisofhistoricalstudies,econo-mistshaveconcludedthatitdoesnotrequireuniqueskillsforagivenstatetoenterthegroupofcountrieswithanaverageGDP,asjustkeepinglabourcostslowisenough.It ismuchmoreofachallengeto jointheeliteofthehighest-developedcountries,becausetodosoitisnecessarytobuildanationalsystemof innovation, that is, tocreate the institutionalandeconomicconditions tomakemodern,competitiveandprofitableproductsandservices.Manystateshaveprovedunabletoovercomethisobstacleinthepast13.

TheeconomiccooperationbetweentheV4countriesandGermany,whichhasbeenunbalancedbysalesofgoodsundertheirownbrandnames,maybefac-ingtwothreats.ThelucrativenatureofthecooperationbetweenV4businessesandtheirGermanpartnerscoulddeprivetheformerofthemotivationtotakerisks in developing their own technologies and brands. Thewage increases

13 FernandoGabrielIm,DavidRosenblatt,Middle-IncomeTraps-AConceptualandEmpiricalSurvey,WorldBank2013;http://www-wds.worldbank.org/external/default/WDSContent-Server/WDSP/IB/2013/09/09/000158349_20130909085739/Rendered/PDF/WPS6594.pdf

PRA

CE

OSW

09/

2012

30

OSW

REP

OR

T 06

/201

6

linkedtothiscouldleadtothelossofothercountries,whowouldofferlowerwages.Inaddition,thestrategyofassemblingproductsforGermancompaniesisinthelongrunlinkedtotheriskofjoblossesintheindustry,ashappenedinthecaseofSpain,ItalyandtheUnitedKingdom,tothebenefitofother,cheap-ercountriessuchasTurkeyorUkraine.SellingproductsfromCentralEuropeunderthebrandnamesofcompaniesfromGermanydoesnothelpincreatingtheirown,powerful,recognisablebrandsonaglobalscale,andthisisanes-sentialconditionforobtainingsignificantprofitmargins.

Secondly, thedevelopmentof theV4 states’ economic cooperationwithGer-many has not been associatedwith an influx of knowledge connectedwithinformationandcommunicationtechnologies,whichwouldseemtobeakeyfactorinfutureeconomicsuccess.Germancompaniesdonotspecialiseinthisfield.Forthisreason,headsofGermancompanieshavebeenwatchingtheex-pansionofAmericanandChineseICTsectorenterprisesintotraditionalmar-ketsandtheirattemptstocreatedriverlesscarswithgrowingunease,asthiscouldthreatenthestrongpositionoftheGermanautomotiveindustry.In2015Volkswagen’schairmanMartinWinterkornmentionedforthefirsttimethatITcompaniessuchasAppleandGoogle,whicharepursuingadvancedstudyondriverlesscars,couldbehisfirm’smaincompetitorsinthefuture14.LeadersoftheGermaneconomyhavegraspedthatiftheysimplyremainmanufactur-ersofdevicesandmachines, theywillbereducing theirprofitsand leavingsubstantialpartsoftheminthehandsofthemanufacturersofthesoftwaretheyuse15.Inthepastfewyears,forexample,Samsunghasfounditselfinsuchasituation;itmakesonlysmallmarginsonitsmobilephones,whilemostoftheprofitsgotoGoogle,withitsAndroidoperatingsystem.

14 Winterkorn:BegrüßedasEngagementvonApple,Googleundco.;http://www.manager-magazin.de/unternehmen/autoindustrie/winterkorn-begruesse-engagement-von-apple-google-und-co-a-1021447.html

15 Germany’sindustry:DoesDeutschlanddodigital?,Economist,21November2015;http://www.economist.com/news/business/21678774-europes-biggest-economy-rightly-worried-digitisation-threat-its-industrial

PRA

CE

OSW

09/

2012

31

OSW

REP

OR

T 0

6/20

16

III. The flow of InvesTmenTs beTween germany and v4

Inrecentyears,investmentrelationsbetweenGermanyandthecountriesoftheV4havedevelopedintensively,butunilaterally.Germanyisthekeysup-plierofforeigncapitalformostofthesecountries,anditisGermaninvestorswhohave thusdetermined thedirections inwhich foreign tradehasdevel-oped.However,thisisnotauniquesituation.Manycountrieshavebeennetre-cipientsofcapitalfromGermany,asthankstoasignificantincreaseinexportsinrecentyears,companiesfromGermanyhavehadconsiderableresourcesofcashfreetomakesuchinvestments.TheinfluxofinvestmentfromGermanytoV4,however,wouldnothavebeenpossiblewithoutasignificantimprove-mentintheattractivenessofinvestinginCentralEurope,inwhichtheassess-mentofPolandhasimprovedthemost.

1. The flow of investments between germany and v4

Foreigntradeturnoverbetweencountriescanbesubjecttolargefluctuations.Forthisreason,thelevelofinvestmentisareliableindicatorshowingthedegreeofmaturityofeconomiccooperation,sincetheplacementofinvestmentsinagivencountryisamoreaccurateanalysisofthatcountry’sprospectsfordevelopment.Onthebasisofinvestmentdata,itcanclearlybeseenthattheeconomictiesbe-tweenGermanyandtheV4statesarestrengthening.However,ananalysisoftheinvestmentstreamsallowsustodiscernthestillsignificantlevelsofasymmetryinthoserelationships.Germanyisthelargestproviderofnetcapitaltothemem-berstates,thusaffectingthedirectionoftheV4states’economicdevelopment.

Figure 12.TheshareofGermancapitalininvestmentflowstotheV4coun-triesin2008and2012(%)

[%]

0

5

10

15

20

25

Poland Slovakia

2008 2012

CzechRepublic

Hungary Poland Slovakia CzechRepublic

Hungary

source:DatabasesofthecentralbanksoftheV4countries

PRA

CE

OSW

09/

2012

32

OSW

REP

OR

T 06

/201

6

Inrecentyears,Germanyhasretained itspositionas the largest investor inalltheV4states,withtheexceptionoftheCzechRepublic,wheretheNether-landscamewellahead.TheshareofGermancapitalininvestmentsintheV4countriesincreasedslightlyinthecasesofPolandandHungary,anddecreasedslightlyintheCzechRepublicandSlovakia.Ingeneral,itcanthereforebecon-cludedthatGermany’spositionasaninvestor intheV4countrieshasdevel-opedsteadilyoverthepastfewyears.

Figure 13.TotalforeigndirectinvestmentbyGermanyinselectedcountriesandintheV4states(€billion)

2004 2005 2006 2009 2010 2011 20120

50

100

150

200

250

300 [€ billion]USA

V4Netherlands

FranceChinaRussia

Great Britain

source:Bundesbank

Intheperiod2004-12,thevalueofforeigninvestmentsfromGermanyintheV4countrieshasdoubled,from€36billionto€77billion.TheV4statestakento-getherareoneofthemaintargetsofGermaninvestment,andin2012theyover-tooktheNetherlands(€74billion),whichistraditionallylinkedtoGermanybyverystrongeconomicrelationships,andwhichisGermany’smostimportantlogisticshub.ThemostimportantplaceswhereGermancapitalisinvestedaretheUnitedStates(€269billion)andtheUnitedKingdom(€120billion),whichasstrongfinancialcentresprovideanumberofservicesforcompaniesfromGermany.InvestmentsbyGermancompaniesinChina(€42billion)weresig-nificantlylowerthanintheV4countries,althoughtheyhaveexpandedveryrapidly.German capital located inRussia (€21 billion)was also significantlylowerinvaluethanthefundsinvestedinV4countries,althoughthesefiguresdonottakeintoaccountthestillsignificantoutflowofinvestmentsfromRus-siaduetothewarinUkraine.Fromthisdata,itcanbeconcludedthatinarela-tivelyshortperiodoftime,theV4countriesmanagedtoattractnotonlythebigGermancompanies,butalsosmall-andmedium-sizedenterprises,thankstowhichthescaleofGermaninvestmentintheV4hascometoexceedthatinChinaorRussia.

PRA

CE

OSW

09/

2012

33

OSW

REP

OR

T 0

6/20

16

Figure 14.ForeigndirectInvestmentintheV4countries

20042003 2005 2006 2007 2008 2009 2010 2011 201220020

5

10

15

20

25

30 [€ billion]

Poland

Slovakia

Czech Republic

Hungary

source:Bundesbank

AnalysisofGermaninvestmentinindividualV4countriesclearlyshowsthatthe Czech Republic has attractedmost investment. In recent years, Polandhasbeguntocatchupwiththem;HungarycomesinthirdplaceandSlovakiafourth.However,comparingthesevalueswiththepopulationofeachcountry,weseethatPolandreceivesbyfartheleastinvestment,onlyaboutathirdoftheinvestmentper capitaofwhatHungaryandSlovakiareceives,andaquarteroftheCzechRepublic.ThismeansthattheintensityofGermaninvestmentsinPolandismuchlowerthaninotherV4countries.Despitethis,wecanseethatthisdifferenceisslowlybeinglevelledout.InvestmentgrowthfromGermanyin theperiod2004-12was fastest inPoland (a cumulative increaseof 160%);nextwereSlovakia(129%)andtheCzechRepublic(111%),andHungaryinaverydistantfourthplace(32%).

RecentyearshavebroughtasteepriseincapitalcommitmentinCentralEuropefromGermanindustriessuchastheautomotiveandlogisticalsectors,whichhaverecognisedtheadvantagesofinvestingintheregioninordertoimprovetheircompetitivenessandconsolidatetheirpositionontheworldmarket.Foritspart,theretailindustryhaslaunchedadynamicexpansionintheregion,takingadvantageofthegrowingconsumptionwhichhasreinforceditsposi-tioninEurope.Forothersectors,suchasenergyorbanking,thelastfewyearshavebeenaperiodofstagnation,oratimeinwhichtoverifytheirinvestmentopportunities. Generally it can be noted, however, that German businesseshaveincreasedthescopeoftheirinvestmentsinCentralEurope,totheextentthattheirfinancialsituationshaveallowed(seeAppendix).

PRA

CE

OSW

09/

2012

34

OSW

REP

OR

T 06

/201

6

Figure 15.TheinfluenceofindividualcountriesonthebalanceofsecondaryincomeofGermany(€billion)

-3

-2

-1

0

1

2

3

4 Hungary

Czech Republic

Poland

20042003200220012000 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

[€ billion]

source:Theauthor’sowncalculations,basedontheBundesbank’sdatabase:MakroökonomischeZeitre-ihen,http://www.bundesbank.de/Navigation/DE/Statistiken/Zeitreihen_Datenbanken/Makrooekono-mische_Zeitreihen/makrooekonomische_zeitreihen_node.html

Byanalysingbalanceof secondary income,whichshowwhat thebalanceofprofitflowsandassetsheld abroad looks like,we canpartially evaluate thesizeofthebenefitintheformofdividendsfromGermaninvestmentsintheV4countries.Thedatashowsthatintheperiod2004-12,investmentinHun-garyproduced€22billionofrevenues, intheCzechRepublic€14billion,andinPoland€1.6billion(figuresforSlovakiaarenotavailable);inallcountries,then,atrendtowardsgrowthisvisible.ItseemsthatGermany’sdeficitinre-lationswithPolandintheperiod2000-6shouldbereadasresultingfromthefactthatGermancompanieshavemainlyinvestedwithoutreceivingsignifi-cantreturnsontheirinvestments.Inrecentyears,theoutflowofcapitalfromPolandmayhavebeeninhibitedbythegrowingnumberofPolishworkersinGermany,whotransfersomeoftheirearningsbacktotheirowncountry.

Figure 16.ThevalueofforeigndirectinvestmentsfromV4countriesinGermanyin2008and2012(€billion)

[€ billion]

0.0

0.5

1.0

1.5

2.0

Poland Slovakia

2008 2012

CzechRepublic

Hungary Poland Slovakia CzechRepublic

Hungary

0.6

0.1

0.30.1

2.0

0.01

0.30.1

source:DatabaseoftheV4countries’centralbanks

A comparison of investment flows from Germany to the V4 countries withcapitalflowingintheoppositedirectionallowsustoperceivetheconsiderable

PRA

CE

OSW

09/

2012

35

OSW

REP

OR

T 0

6/20

16

imbalanceininvestmentpotentialsonbothsides.ThevalueofV4capitalin-volvedinGermanymadeuponly3.5%oftheGermanfundsinvestedinV4.ItisclearthattheonlycountrythatsignificantlyincreaseditsinvestmentinGer-manywasPoland.ThevalueofPolishcapitalinvestedinGermanyinthepe-riod2008-12roseby233%to€2billion,whilethescaleoftheinvestmentcom-mitmentsoftheCzechRepublic,SlovakiaandHungaryremainedunchangedorevendecreased.TheincreasedinvolvementofPolishcompanies’capitalinGermanycouldbetheresultoftheimprovingcompetitivenessofPolishcompa-nies,suchasthefurnitureorcomputersectors,whichhasbeguntochallengesomeoftheirGermancompetitors.Intheperiod2008-13,23%ofPolishinvest-mentsinGermanywereinthecomputerindustry,16%infinancialservicesforcompanies,and14%inmachineproduction.ManyPolishcompanieshavealsodecidedtoentertheGermanmarketinordertoreceivethelabel‘MadeinGer-many’,whichcouldbeavaluableassetintheirfurtherexpansionontoforeignmarkets.Theanalysisshowsthat41%ofPolishinvestmentprojectsinGerma-nyinvolvedopeningsalesandmarketingdivisions,18%coveredtheopeningofcompanyheadquartersinGermany,and11%involvedofferingservicesthere16.

2. motives for investment

ThemainmotiveforGermancompaniestoinvestinCentralEuropeissalesandcustomerserviceonthelocalmarket,aswellasreducingcosts.GermancapitalthereforeoftengoestotheV4countriesinordertogeneratesavingsonproduc-inggoodswhichareoftensoldinthecountriesofwesternEurope.Withdif-ferencesinpaystillremaining,suchtrendsarequitenatural.Theproblemis,however,thatGermancompaniesstilldonotseeCentralandEasternEuropeasplacesinwhichtoinvestinresearchanddevelopment,evenoverthenextten years, deeming the developed countries to bemore attractive locations.ChinaandIndiaarealsomoreattractiveinthisrespect;becausetheyaresuchlargeandgeographicallyremotemarkets,moreandmoreGermancompaniessee theadvantage in locating theirR&Dcentres close to the factories there.Ontheonehand,thiscouldmeanthattheV4countriesaregeographicallytoocloseandhavetoosimilarstructuresofproductiontoGermanytobeabletoat-tractGermanR&Dinvestments.Ontheotherhand,however,thegeographicalandculturalproximityofCentralEuropecouldbeanopportunitytoprovidebusinessprocessoutsourcinginthisregionforGermancompanies.

16 PolnischeUnternehmenerobernneueMärkte,10November2014;http://www.gtai.de/GTAI/Navigation/DE/Trade/Maerkte/suche,t=polnische-unternehmen-erobern-neue-maerkte,did=1112698.

PRA

CE

OSW

09/

2012

36

OSW

REP

OR

T 06

/201

6

Figure 17.ThepopularityofdifferentregionsasinvestmentlocationsforGermanindustry,andthemainmotivesforinvestmentin2014

0

10

20

30

40

50 [%]

Reduction of costs

Production on local market

Sales/Customer service

Russia, Ukraine,Turkey, non-EUBalkan states

EU-15 China North America Asia(except China)

New EU states SouthAmerica

47 46

36

28

21 2017

source:Europapunkteterneut–KostendruckwiederwichtigerAuslandsinvestitioneninderIndustrieFrühjahr2015,theGermanChamberofIndustryandCommerce,Berlin2015,p.15

AnanalysisoftheinvestmentrelationshipbetweenGermanyandV4shouldstartbyexaminingthosecountries’popularityasinvestmentlocations(givenasanum-berabovethebars),andthemotivesforinvestinginthosecountries(giveninsidethefigures).ThedatashowsthatthenewEUcountries17,whichincludetheV4,arethefifthmostpopulardestinationforinvestmentfromGermanindustries.How-ever,consideringthatthenewEUmemberstatesaretheregionwiththesmallestpotentialintermsofeconomyandpopulation,thentheirpositionismoresignifi-cant.TheyaremorefrequentlychosenforGermanindustrialinvestmentsthanSouthAmerica,Turkey,orcountriesinEasternandSouthernEurope.

AnalysingthemotivesbehindtheinvestmentofGermancapitalinCentralEu-rope,wecanseehowdifferentthisregionisfromotherpartsoftheworld.ThedatashowsthatthemostimportantpurposeofinvestinginthenewEUcoun-triesistoselltocustomersonthedomesticmarkets,andtoofferthemservices(42%).Comparedwithotherregions,movestoreducecostsmakeupasignificantproportionoftheinvestmentsinthenewEUcountries(39%).NootherregionisusedbyGermanindustryinthiswaytoreduceproductioncosts.However,thisresult isnotsurprising,becausegiventhattheEUisasinglemarket,movingproductiontothecheapestregionisanaturalprocess.Inothercountriestherearespecialrequirementsforaspecificproportionofproductiontobeoflocalori-gin,aswellasbureaucraticbarrierslimitingproductionforothermarkets.That

17 Inthisfigure,the‘new’EUcountriesmeansthosememberstateswhichjoinedtheEUafter2003.

PRA

CE

OSW

09/

2012

37

OSW

REP

OR

T 0

6/20

16

iswhyonly18%ofGermaninvestmentinChinaisaimedatreducingproductioncosts.AlessimportantmotiveforinvestinginnewEUcountriescomparedtootherregionsisproductionforthelocalmarkets(19%),asthisisamuchmoreimportantreasontoinvestcapitalinNorth&SouthAmericaandChina.

StudiessuggestthatChinaandCentralEuropeservecompletelydifferentfunc-tionsfortheGermaneconomy.CentralEuropeismuchmoreattractiveduetoitsgeographicalandculturalproximity18;itoffersmoderateproductioncosts,high-ly-qualifiedhumancapitalandincreasingproductivity,andisthelocationfortheproductionofmorespecialisedandcomplexgoods,primarilyfortheEuro-peanmarket.Chinainturn,duetolowwages,largenumbersofengineers,averylargeavailabilityofsuppliers,theproximityofresources,anditshugeinternalmarket,isalocationformass-producedgoodsaimedatthelocalmarket,andalsoinpartat foreignmarkets.Akeydifferencebetweenthesetworegions is theflexibilityofproductionandthesecurityoftechnology.ProductioninChinain-volvestherisksoftechnologyleaksandunpredictablegovernmentactions,andthereisalsolessflexibilityinadaptingproductiontosignificantrecentfluctua-tionsinglobaldemand,asitrequiresquitesometimetoadapt.Italsorequiresmuchgreateroutlayonlogistics.CentralEuropeoffersamorestableinstitution-alframework,aswellashighflexibilityinadaptingproductiontoglobalfluctua-tionsindemand,sothatproducerscankeeptightercontroloftheproduction.

Figure 18.Themostattractiveregionsforresearchanddevelopment(onascalefrom1–unimportantto4–veryimportant)

00.51.01.52.02.53.03.54.0

2015 2025

Wes

tern

Eur

ope

USA

& Ca

nada

Chin

a

Indi

a

Cent

ral &

Eas

tern

Euro

pe

Braz

il

Japa

n

Sout

h Ko

rea

Mex

ico

Turk

ey

Russ

ia &

CIS

3.83.8

3.12.8

1.8

2.3

1.81.5 1.51.6

1.3 1.41.2 1.2 1.3 1.2 1.31.4

1.8

2.22.6

2.9

source:Surveyentitled‘R&DLandscapeby2025:EineTrendstudiederROIManagementConsultingAG.EinWegweiserdurchdieTrendsimglobalenManagementvonForschungundEntwicklung,2013,p.11

18 H.-G.Scheibe,ChinaoderOsteuropa?RichtigeAntwortaufeinefalscheFrage;http://www.roi.de/fileadmin/ROI_DIALOG/ab_DIALOG_38/ROI__DIALOG_41_web.pdf

PRA

CE

OSW

09/

2012

38

OSW

REP

OR

T 06

/201

6

StudiessuggestthattheV4countrieswillnotbeaprioritytargetforinnovationtransferoverthenexttenyears.Accordingtoasurveycarriedoutamongthedecision-makersof60Germanmedium-andlarge-sizedcompanies,thecoun-triesofcentral&easternEuropearethefourthmost important locationforR&Dinvestment(jointly withIndia)afterWesternEurope,NorthAmericaandChina.Theirpositionwillbe strengthenedby2025,but theirdistance fromWesterncountriesandChinawillstillbesignificant.ThestudyalsofoundthatthepositionofCentral&EasternEuropewillbeparticularlyimportantintheR&Dfieldoftheautomotiveindustry,butlesssointheproductionsector.

Thereareslightlymoreoptimisticconclusionsfromotherstudies,whichshowthatGermancompaniesarebecomingmoreinterestedinmovingvariousinter-nalactivities,suchasfinancialandhumanresourcesmanagement,toforeignaffiliates. In2011,65%ofcompaniespreferred tokeep theirprincipalactivi-tiesinGermany,19%favouredtransferringsomeoftheseprocessestoCentral&EasternEurope,andonly3%tootheremergingeconomiessuchasBrazil,ChinaorIndia19.Itisprimarilytransportandlogisticscompaniesthataremov-ingtheiractivitiestoCentral&EasternEurope(25%ofthemhavebranchesintheregion),aswellasbanking(24%),andIT(24%).Companiesfromthebank-ing,energyandwatersupplyindustrieshavechosenCentral&EasternEuropeas theplace to test theirnewservicesand software.The survey shows thatthebiggestbarrierstomovingelementsoftheirinternalactivitytothisregionarequestionsofdatasecurityandaninsufficientknowledgeofEnglishintheregion.ItseemstobeintheinterestsofCentralEuropetosupportthetrendtomovethebusinessprocessoutsourcingservicesofGermancompaniestotheregion,sinceattractingsuchinvestmentsmayofferawayofescapingthemid-dleincometrap,.Theseworksallowhighaddedvaluetobemovedtothetargetcountriesandensuretheemploymentofhighlyskilledworkers.

19 Studie:OsteuropagewinntAkzeptanzbeimOutsourcing,14February2012;http://www.presseportal.de/pm/50272/2198077

PRA

CE

OSW

09/

2012

39

OSW

REP

OR

T 0

6/20

16

3. The investment climate in the v4 countries from the perspective of german investors

Overthepasttwoyears,theinvestmentattractivenessoftheV4countrieshasincreased considerably in the eyes of German investors. In 2014 Poland ob-tainedthebestvaluesofspecificindicatorsforinvestmentattractiveness.Datafrom the surveys confirms that German investors’ evaluation of Hungary’seconomicpolicyweremuchhigherthantheconsiderablecriticismintheGer-manpresswouldsuggest.

Figure 19.EvaluationoftheinvestmentattractivenessoftheV4countries(1–best,6–worst)

2013 2014 20152008 2009 2010 2011 2012

4.5

4.0

3.5

3.0

2.5

Slovakia

Poland

Czech Republic

Hungary

source: Economic Survey in Central and Eastern Europe 2015, the German Chamber of Industry andCommerce;http://www.ahkungarn.hu/fileadmin/ahk_ungarn/Dokumente/Bereich_CC/Publikationen/Konjunktur/2015/AHK-Konjunkturumfrage_MOE_2015_final.pdf

Inrecentyears,assessmentsoftheV4countries’investmentattractivenesshaveclearlyimproved.Intheperiod2006-12theseratingswerequitestable;theleaderwasPoland(2.8),theCzechRepublic(3),Slovakia(3.2)andHungary(3.6).TheV4countries’assessmentsimprovedsignificantlyin2013,whichmayhavebeentheresultofbettereconomicconditionsinthosecountriesthanintheeuro-zone.ItseemsthatGermaninvestorsmostlyappreciatedthegreaterpoliticalstabilityintheV4countriesthaninWesterncountries,aswellastheir lowerlevelsofdebtcomparedtoWesterncountries.ThebiggestchangewasPoland’sadvancetofirstplaceasalocationforinvestmentsasof2013,aswellastheworseningassessmentofHungary.TheattractivenessoftheHungarianeconomydeterio-ratedin2009,soevenbeforePrimeMinisterViktorOrbáncametopower,anddidsoagaininthethirdyearofhisrule.ThepoorerperceptionofHungaryisnotthereforeconnectedonlyto itscontroversialeconomicpolicy,butratherwiththeoveralleconomicsituation,linkedtoitshighdebt.

PRA

CE

OSW

09/

2012

40

OSW

REP

OR

T 06

/201

6

Figure 20.ThepercentageofGermancompanieswhichintendtoincreaseinvestmentinindividualcountries(%)

2009 2010 2011 2012 2013 20140

10

20

30

40

50

60 [%]

Hungary

Slovakia

Czech Republic

Poland

source:EconomicSurveyinCentralandEasternEurope2015,asabove

Analysisofthediagramshowsthatthepercentageofcompaniesplanningtoin-creaseinvestmentafterthedeclinein2009hasincreasedandremainsstable.Inrecentyears,aroundathirdofthecompaniesinterviewedintendedtoboostin-vestment.DespitetheweakerratingofHungary’sattractivenessinthedatacitedearlier,thisdoesnotappeartohaveaffectedthedesiretoinvest.Inthisrespect,HungarydoesnotdiffersignificantlyfromtheotherV4states.InrecentyearsGermancompanieshavebeenslightlymore likely to increase investments inHungarythaninSlovakia.Poland(39%)exhibitedmorefavourableassessmentsthanHungary(35%),theCzechRepublic(33%)andSlovakia(30%).

Figure 21.ThepercentageofGermancompanieswhichintendtoincreaseemploymentinindividualcountries(%)

20152008 2009 2010 2011 2012 2013 2014

Czech Republic

Hungary

Poland

0

10

20

30

40

50

60

70

80 [%]

Slovakia

source:EconomicSurveyinCentralandEasternEurope2015,asabove

PRA

CE

OSW

09/

2012

41

OSW

REP

OR

T 0

6/20

16

IntermsoftheintentiontoincreaseemploymentintheV4countries,Polandreceived thebestassessment,an improvementoverrecentyears.43%of thecompaniesinterviewedintendtoincreaseemploymentonthePolishmarket,36%intheCzechRepublic,35%inHungary,and33%inSlovakia.

Figure 22.ThepercentageofGermancompanieswhichsupporttheintroduc-tionoftheeuroinindividualcountries(percent)

20152009 2010 2011 2012 2013 20140

10

20

30

40

50

60

70

80

90

100 [%]

Czech Republic

Hungary

Poland

source:EconomicSurveyinCentralandEasternEurope2015,asabove.

Therehave been clear changeswith respect toGerman investors’ attitudetowardsplans to introduce theeuro in those countriesof theV4whichdonot yet use it. Support for this issue amongGerman companies has fallensignificantlyintheCzechRepublic,PolandandHungarytosimilardegrees,probablyasaresultofthecrisisinthemonetaryunion;nevertheless,aslightmajoritystillsupports the introductionof thesinglecurrency.Whereas in2009about90%ofintervieweesbelievedtheadoptionoftheeurowouldbebeneficialfortheircompanies,in2014thepercentagewasonlyslightlymorethan 50%.Thismaymean that someGerman companieshavebeen takingadvantageoftheV4currenciesweakeningagainsttheeuro,whichensuresadditionalsavingsforthem.

PRA

CE

OSW

09/

2012

42

OSW

REP

OR

T 06

/201

6

Figure 23.Investors’assessmentsofindividualaspectsofcompetitiveness:percentagesassatisfactoryorverysatisfactory(%)

0

20

40

60

80

100CzechRepublic Poland Slovakia Hungary

[%]

Membershipin EU

Employees'qualifications

Employees'productivity

and motivation

Quality ofacademiceducation

Labourcosts

Employees'availability

Quality andavailability

of local branches

source:EconomicSurveyinCentralandEasternEurope2015,asabove

WhencarryingoutadeeperanalysisofthefactorsthatmeettheexpectationsofGermancompanies,itisworthnotingthestrongpositionofPoland,whichleadsthewayinallcategories.Itsgoodpositionstemsprimarilyfromthequal-ityandavailabilityofitshumancapital.SlovakiacomparestoPolandinmanycategories,althoughitshowsworseperformancesparticularlyintermsofaca-demicquality,aswellas (toa lesserextent) thequalificationsof itsemploy-ees.Hungary’sresultsarelowerthanSlovakiaandPoland;Germaninvestorsappreciate(inPolandandSlovakiatosimilardegrees)onlyHungary’slabourcostsanditsaccessibilitytolocalsuppliers.TheCzechRepublicdeviatesfromtheothercountriesinalmostallcategories.Theirlowerpositionmay,ontheonehand,arise fromGerman investors’higherexpectationsof thecountry,andontheotherfromitslowereconomicperformanceinrecentyears.

Figure 24.Investors’assessmentsofindividualaspectsofcompetitiveness:percentagesasunsatisfactoryorveryunsatisfactory(%)

0

20

40

60

80

100CzechRepublic

Poland Slovakia Hungary[%]