Embed Size (px)

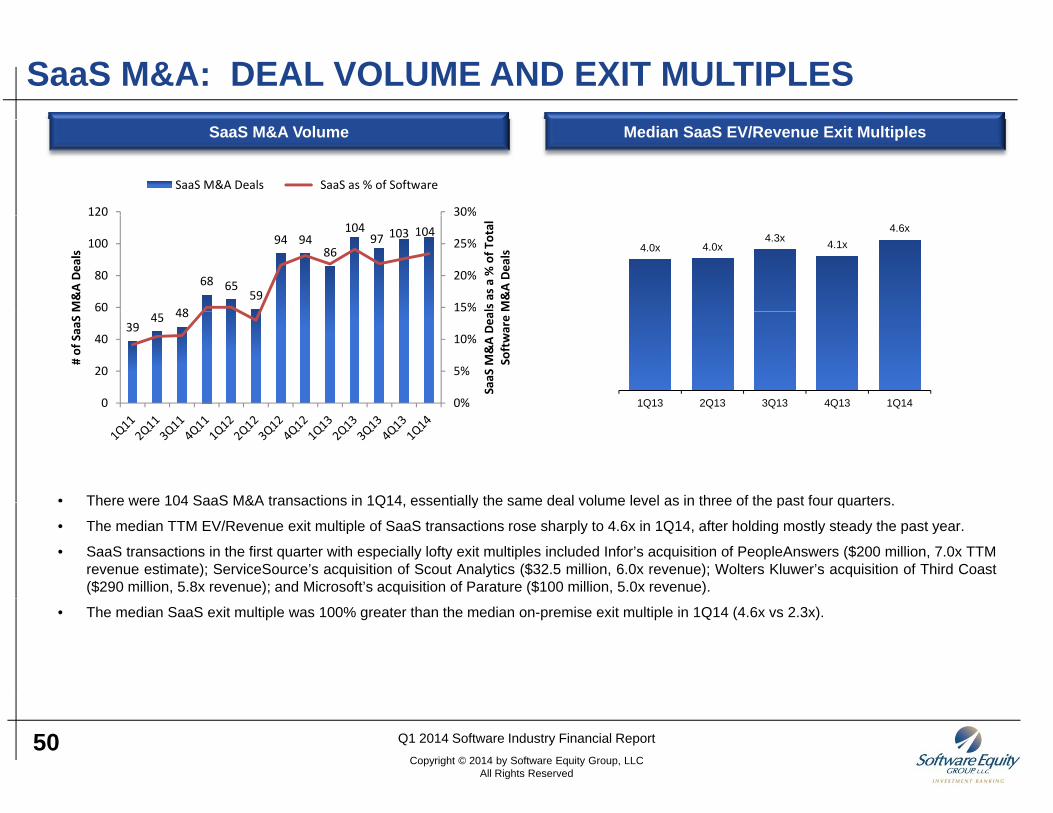

Citation preview

The Software IndustryThe Software IndustryThe Software Industry Financial Report

The Software Industry Financial Report

S ft E it G L L CSoftware Equity Group, L.L.C.12220 El Camino RealSuite 320San Diego, CA [email protected](858) 509-2800

SOFTWARE INDUSTRY FINANCIAL REPORT CONTENTSAbout Software Equity Group

Leaders in Software M&A 4Extensive Global Reach 5

Software Industry MacroeconomicsGlobal GDP 7Global GDP 7U.S. GDP and Unemployment 8Global IT Spending 9E-Commerce and Digital Advertising Spend 10Stock Market Performance 11

Public Software Financial and Valuation PerformanceThe SEG Software Index 13The SEG Software Index: Financial Performance 14-15The SEG Software Index: Market Multiples 16-17The SEG Software Index by Product Category 18The SEG Software Index by Product Category: Financial Performance 19The SEG Software Index by Product Category: Market Multiples 20

Public SaaS Company Financial and Valuation PerformanceThe SEG SaaS Index 22The SEG SaaS Index: Financial Performance 23-24The SEG SaaS Index: Market Multiples 25-29Th SEG S S I d b P d t C t 30 31The SEG SaaS Index by Product Category 30-31The SEG SaaS Index by Product Category: Financial Performance 32The SEG SaaS Index by Product Category: Market Multiples 33

Public Internet Company Financial and Valuation PerformanceThe SEG Internet Index 35Th SEG I t t I d Fi i l P f 36 37The SEG Internet Index: Financial Performance 36-37The SEG Internet Index: Market Multiples 38-39The SEG Internet Index by Product Category 40The SEG Internet Index by Product Category: Financial Performance 41The SEG Internet Index by Product Category: Market Multiples 42

1 Q1 2014 Software Industry Financial ReportCopyright © 2014 by Software Equity Group, LLC

All Rights Reserved

SOFTWARE INDUSTRY FINANCIAL REPORT CONTENTSSoftware Industry M&A Market Update

Software/SaaS M&A Deal Volume and Spending 44Software M&A Exit Multiples 45Software M&A by Ownership Structure and Size 46Software M&A by Vertical and Horizontal Markets 47ySoftware M&A Deal Volume by Product Category 48Software M&A Exit Valuations by Product Category 49SaaS M&A Deal Volume and Exit Multiples 50SaaS M&A by Product Category 51SaaS M&A 1Q14 Transactions 52-54Internet M&A: Deal Volume and Exit Multiples 55Internet M&A: By Product Category 56

AppendixSEG Software Index Key Metrics 58-61SEG Software Index Key Metrics by Product Category 62-63SEG SaaS Index Key Metrics 64SEG SaaS Index Key Metrics by Product Category 65 SEG Internet Index Key Metrics 66-68SEG Internet Index Key Metrics by Product Category 691Q14 Select Public Sellers 701Q14 Mega Deals 711Q14 Mega Deals 711Q14 Most Active Buyers 72About Software Equity Group 73

2 Q1 2014 Software Industry Financial ReportCopyright © 2014 by Software Equity Group, LLC

All Rights Reserved

ABOUT SOFTWARE EQUITY GROUP

3

• Industry leading boutique investment bank founded in

LEADERS IN SOFTWARE M&AIndustry leading boutique investment bank, founded in 1992, representing public and private software and internet companies seeking:

• Strategic exit• Growth capital

We Do Deals.

Growth capital• Buyout • Inorganic growth via acquisition• Buy and sell-side mentoring• Fairness opinions and valuationsFairness opinions and valuations

• Sell-side client revenue range: $5 - 75 million• Buy-side clients include private equity firms and

NASDAQ, NYSE and foreign exchange listed companies• Clients span virtually every software technology, product

category, delivery model and vertical market• Global presence providing advice and guidance to more

th 2 000 i t d bli i th h t USthan 2,000 private and public companies throughout US, Canada, Europe, Asia-Pacific, Africa and Israel

• Strong cross-functional team leveraging transaction, operating, legal and engineering experience

• Unparalleled software industry reputation and track record.

• Highly referenceable base of past clients

4 Q1 2014 Software Industry Financial ReportCopyright © 2014 by Software Equity Group, LLC

All Rights Reserved

EXTENSIVE GLOBAL REACH

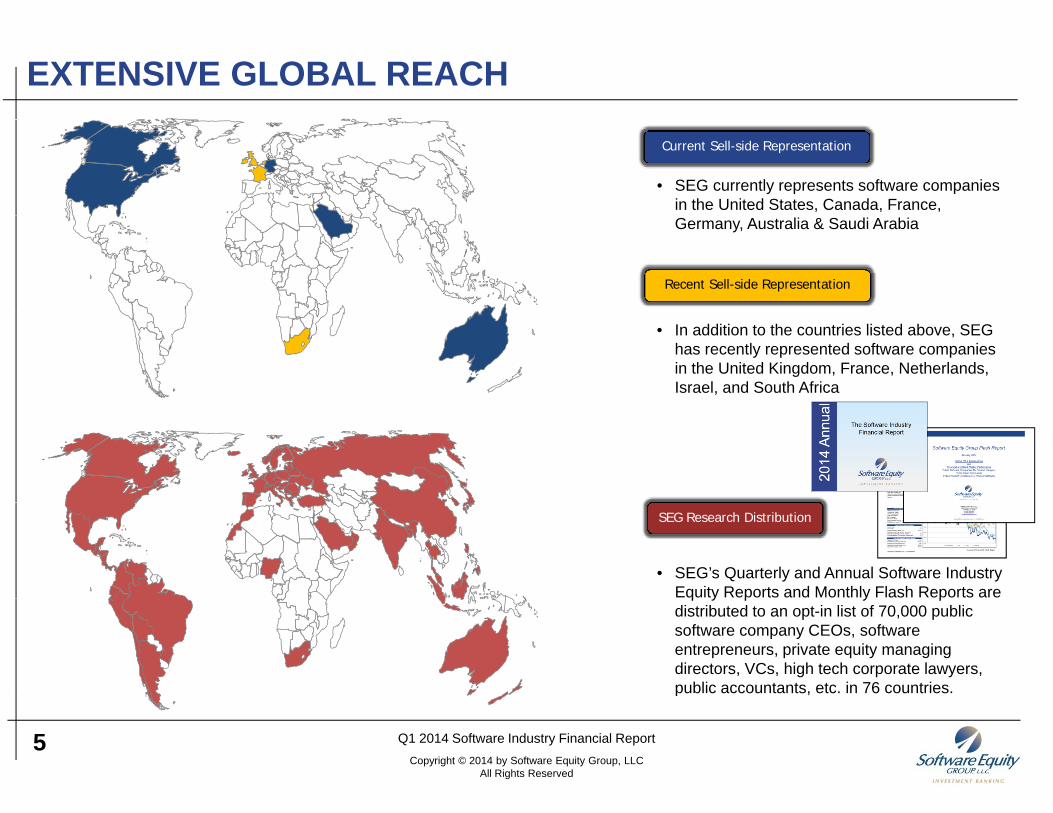

Current Sell-side Representation

• SEG currently represents software companies in the United States, Canada, France,

Recent Sell-side Representation

Germany, Australia & Saudi Arabia

• In addition to the countries listed above, SEG has recently represented software companies in the United Kingdom, France, Netherlands, Israel, and South Africa

SEG Research Distribution

• SEG’s Quarterly and Annual Software Industry Equity Reports and Monthly Flash Reports are q y p y pdistributed to an opt-in list of 70,000 public software company CEOs, software entrepreneurs, private equity managing directors, VCs, high tech corporate lawyers, public accountants, etc. in 76 countries.

5 Q1 2014 Software Industry Financial ReportCopyright © 2014 by Software Equity Group, LLC

All Rights Reserved

p ,

SOFTWARE INDUSTRY MACROECONOMICS

6

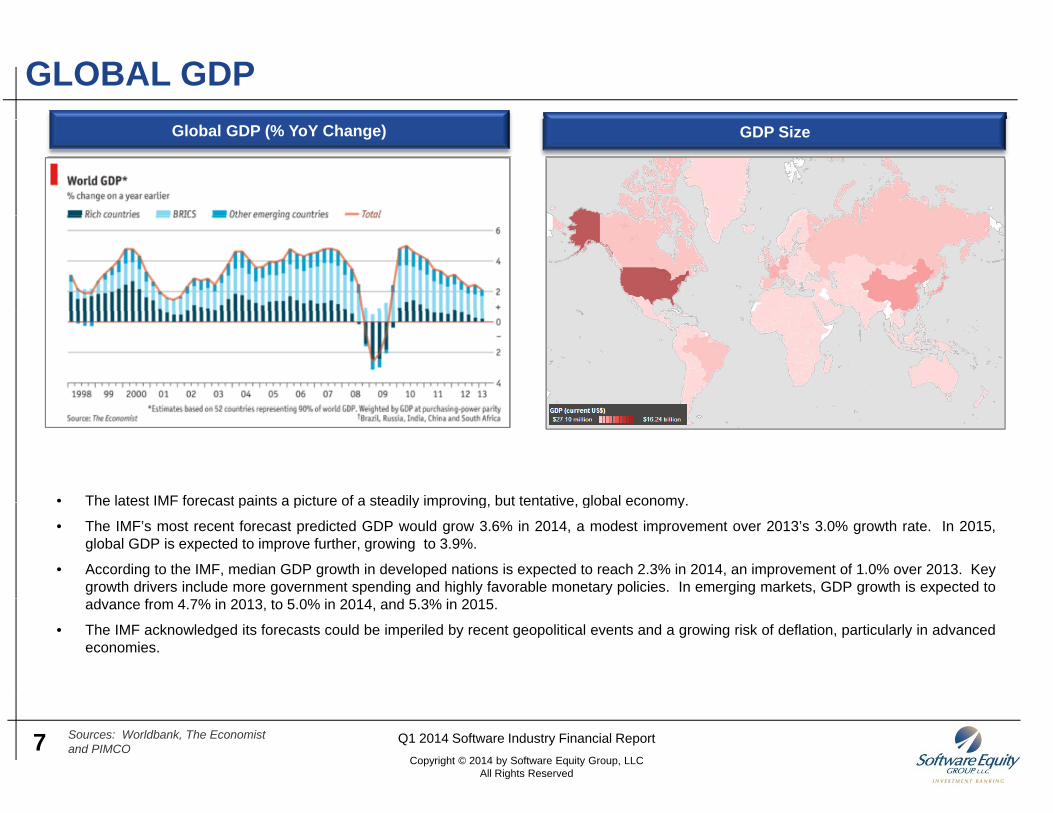

GLOBAL GDPGDP SizeGlobal GDP (% YoY Change)

• The latest IMF forecast paints a picture of a steadily improving but tentative global economyThe latest IMF forecast paints a picture of a steadily improving, but tentative, global economy.

• The IMF’s most recent forecast predicted GDP would grow 3.6% in 2014, a modest improvement over 2013’s 3.0% growth rate. In 2015,global GDP is expected to improve further, growing to 3.9%.

• According to the IMF, median GDP growth in developed nations is expected to reach 2.3% in 2014, an improvement of 1.0% over 2013. Keygrowth drivers include more government spending and highly favorable monetary policies. In emerging markets, GDP growth is expected toadvance from 4.7% in 2013, to 5.0% in 2014, and 5.3% in 2015.

• The IMF acknowledged its forecasts could be imperiled by recent geopolitical events and a growing risk of deflation, particularly in advancedeconomies.

7 Q1 2014 Software Industry Financial ReportCopyright © 2014 by Software Equity Group, LLC

All Rights Reserved

Sources: Worldbank, The Economist and PIMCO

U.S. GDP AND UNEMPLOYMENT

5.0%3.7%

3 1%4.1% 4.1%

4%

6%

8%

10%GDP % GrowthUnemployment Rate

-0.7%

1.5%

-0.7%

2.2%1.7%

2.6%3.1%

0.4%

2.5%1.3%

2.0%1.3%

3.1%

0.4%

2.5%1.8%

2.6% 2.0%

-2%

0%

2%

4%

-2.7%

-5.4%-6.4%

-8%

-6%

-4%

-2%

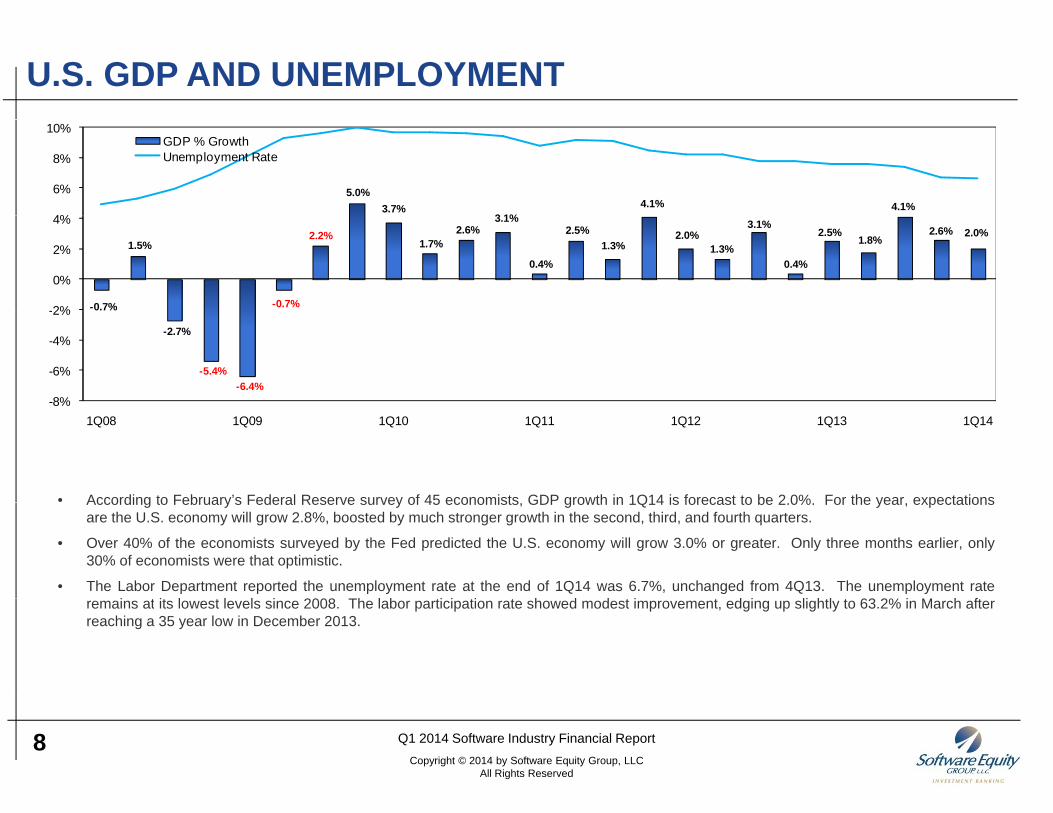

• According to February’s Federal Reserve survey of 45 economists GDP growth in 1Q14 is forecast to be 2 0% For the year expectations

1Q08 1Q09 1Q10 1Q11 1Q12 1Q13 1Q14

According to February s Federal Reserve survey of 45 economists, GDP growth in 1Q14 is forecast to be 2.0%. For the year, expectationsare the U.S. economy will grow 2.8%, boosted by much stronger growth in the second, third, and fourth quarters.

• Over 40% of the economists surveyed by the Fed predicted the U.S. economy will grow 3.0% or greater. Only three months earlier, only30% of economists were that optimistic.

• The Labor Department reported the unemployment rate at the end of 1Q14 was 6.7%, unchanged from 4Q13. The unemployment ratei t it l t l l i 2008 Th l b ti i ti t h d d t i t d i li htl t 63 2% i M h ftremains at its lowest levels since 2008. The labor participation rate showed modest improvement, edging up slightly to 63.2% in March after

reaching a 35 year low in December 2013.

8 Q1 2014 Software Industry Financial ReportCopyright © 2014 by Software Equity Group, LLC

All Rights Reserved

GLOBAL IT SPENDINGGlobal IT Spending by CategoryGlobal IT Spending (% YoY Change)

9.0%

6.0%

8.0%

6.0%4 8%

2.0% 2.0%

4.8%

2007 2008 2009 2010 2011 2012 2013 2014 (F)

10 0%

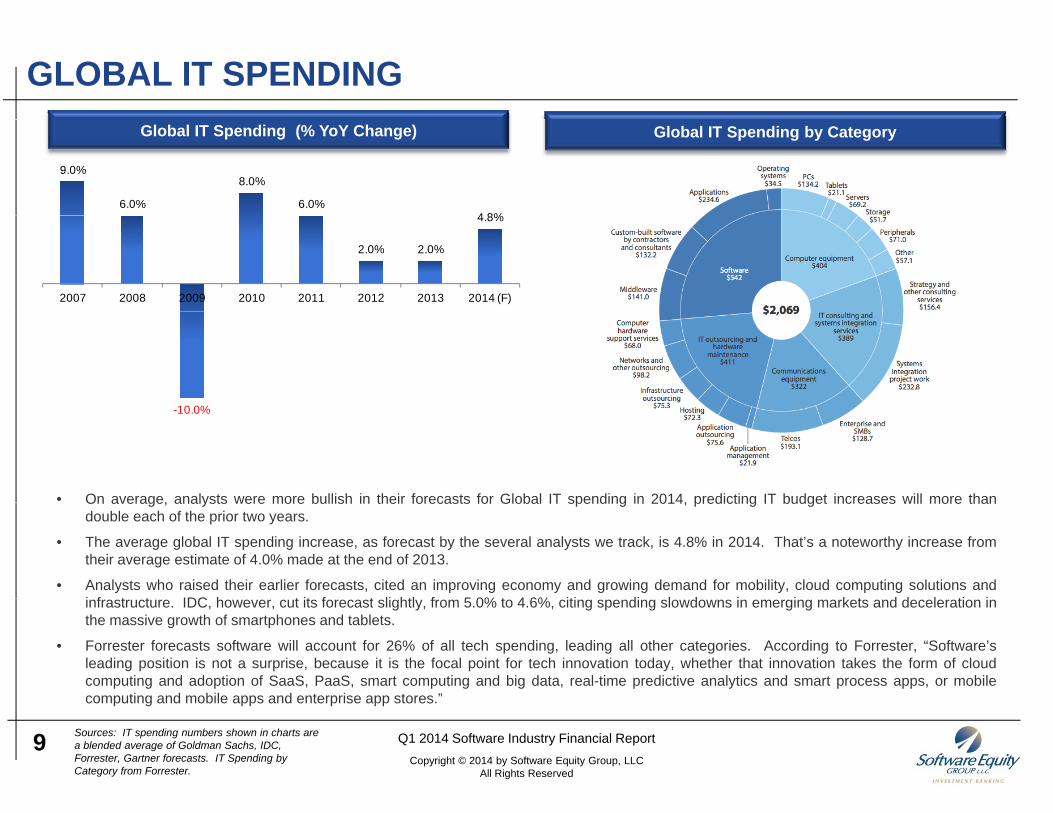

• On average, analysts were more bullish in their forecasts for Global IT spending in 2014, predicting IT budget increases will more than

-10.0%

On average, analysts were more bullish in their forecasts for Global IT spending in 2014, predicting IT budget increases will more thandouble each of the prior two years.

• The average global IT spending increase, as forecast by the several analysts we track, is 4.8% in 2014. That’s a noteworthy increase fromtheir average estimate of 4.0% made at the end of 2013.

• Analysts who raised their earlier forecasts, cited an improving economy and growing demand for mobility, cloud computing solutions andi f t t IDC h t it f t li htl f 5 0% t 4 6% iti di l d i i k t d d l ti iinfrastructure. IDC, however, cut its forecast slightly, from 5.0% to 4.6%, citing spending slowdowns in emerging markets and deceleration inthe massive growth of smartphones and tablets.

• Forrester forecasts software will account for 26% of all tech spending, leading all other categories. According to Forrester, “Software’sleading position is not a surprise, because it is the focal point for tech innovation today, whether that innovation takes the form of cloudcomputing and adoption of SaaS, PaaS, smart computing and big data, real-time predictive analytics and smart process apps, or mobile

ti d bil d t i t ”

9 Q1 2014 Software Industry Financial ReportCopyright © 2014 by Software Equity Group, LLC

All Rights Reserved

Sources: IT spending numbers shown in charts are a blended average of Goldman Sachs, IDC, Forrester, Gartner forecasts. IT Spending by Category from Forrester.

computing and mobile apps and enterprise app stores.”

E-COMMERCE AND DIGITAL ADVERTISING SPENDDigital Advertising SpendE-Commerce Spend

25%

30%

$12

$14

B)

Digital Advertising Spend ($B) YoY Percent Change20%

$60

$70E-Commerce Spend ($B) YoY Percent Change

5%

10%

15%

20%

$6

$8

$10

YoY

Cha

nge

dver

tisin

g R

even

ue ($

B

5%

10%

15%

$30

$40

$50

$

YoY

Cha

nge

erce

Spe

ndin

g ($

B)

-10%

-5%

0%

$0

$2

$4

Dig

ital A

d

-5%

0%

$0

$10

$20

Y

E-C

omm

e

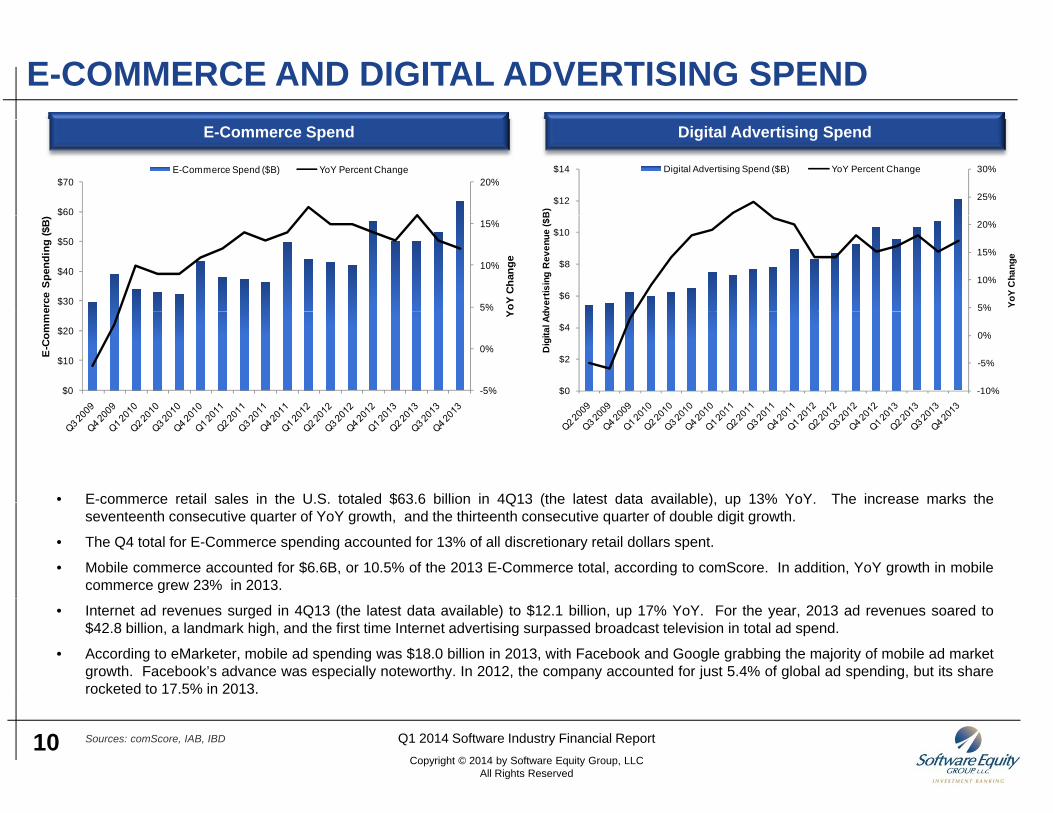

• E-commerce retail sales in the U.S. totaled $63.6 billion in 4Q13 (the latest data available), up 13% YoY. The increase marks theE commerce retail sales in the U.S. totaled $63.6 billion in 4Q13 (the latest data available), up 13% YoY. The increase marks theseventeenth consecutive quarter of YoY growth, and the thirteenth consecutive quarter of double digit growth.

• The Q4 total for E-Commerce spending accounted for 13% of all discretionary retail dollars spent.

• Mobile commerce accounted for $6.6B, or 10.5% of the 2013 E-Commerce total, according to comScore. In addition, YoY growth in mobilecommerce grew 23% in 2013.

• Internet ad revenues surged in 4Q13 (the latest data available) to $12.1 billion, up 17% YoY. For the year, 2013 ad revenues soared to$42.8 billion, a landmark high, and the first time Internet advertising surpassed broadcast television in total ad spend.

• According to eMarketer, mobile ad spending was $18.0 billion in 2013, with Facebook and Google grabbing the majority of mobile ad marketgrowth. Facebook’s advance was especially noteworthy. In 2012, the company accounted for just 5.4% of global ad spending, but its sharerocketed to 17.5% in 2013.

10 Q1 2014 Software Industry Financial ReportCopyright © 2014 by Software Equity Group, LLC

All Rights Reserved

Sources: comScore, IAB, IBD

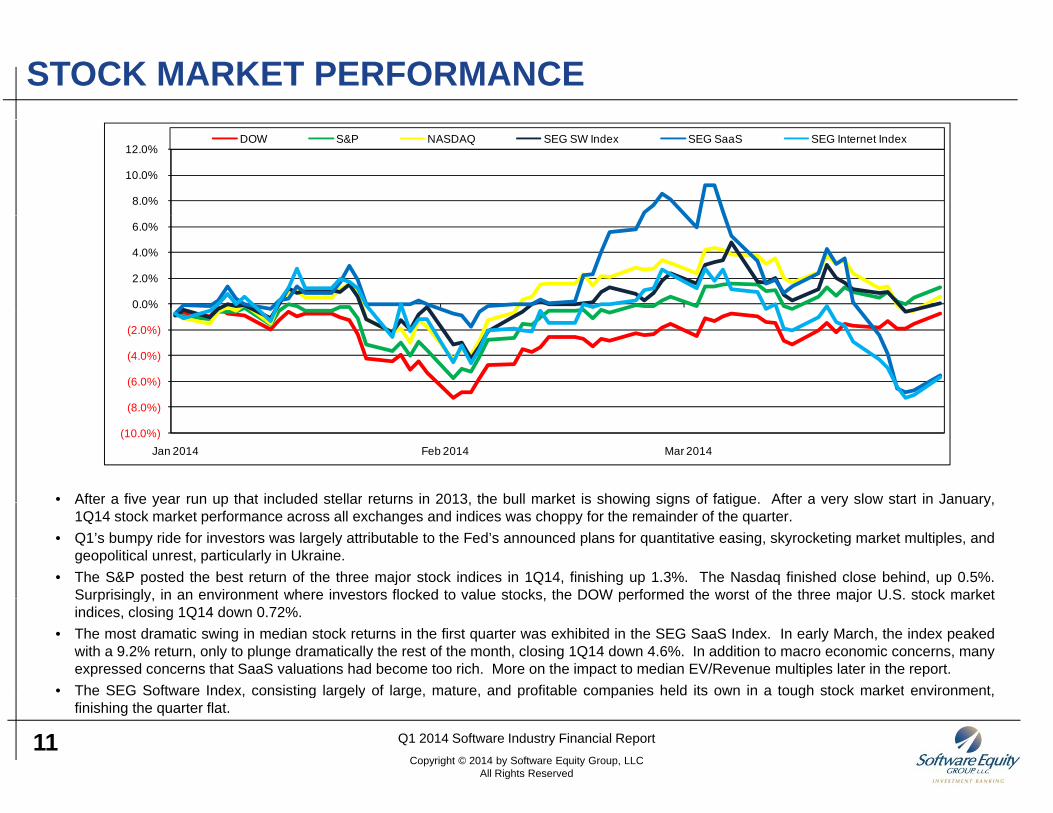

STOCK MARKET PERFORMANCE

8.0%

10.0%

12.0% DOW S&P NASDAQ SEG SW Index SEG SaaS SEG Internet Index

0.0%

2.0%

4.0%

6.0%

(8 0%)

(6.0%)

(4.0%)

(2.0%)

• After a five year run up that included stellar returns in 2013, the bull market is showing signs of fatigue. After a very slow start in January,

(10.0%)

(8.0%)

Jan 2014 Feb 2014 Mar 2014

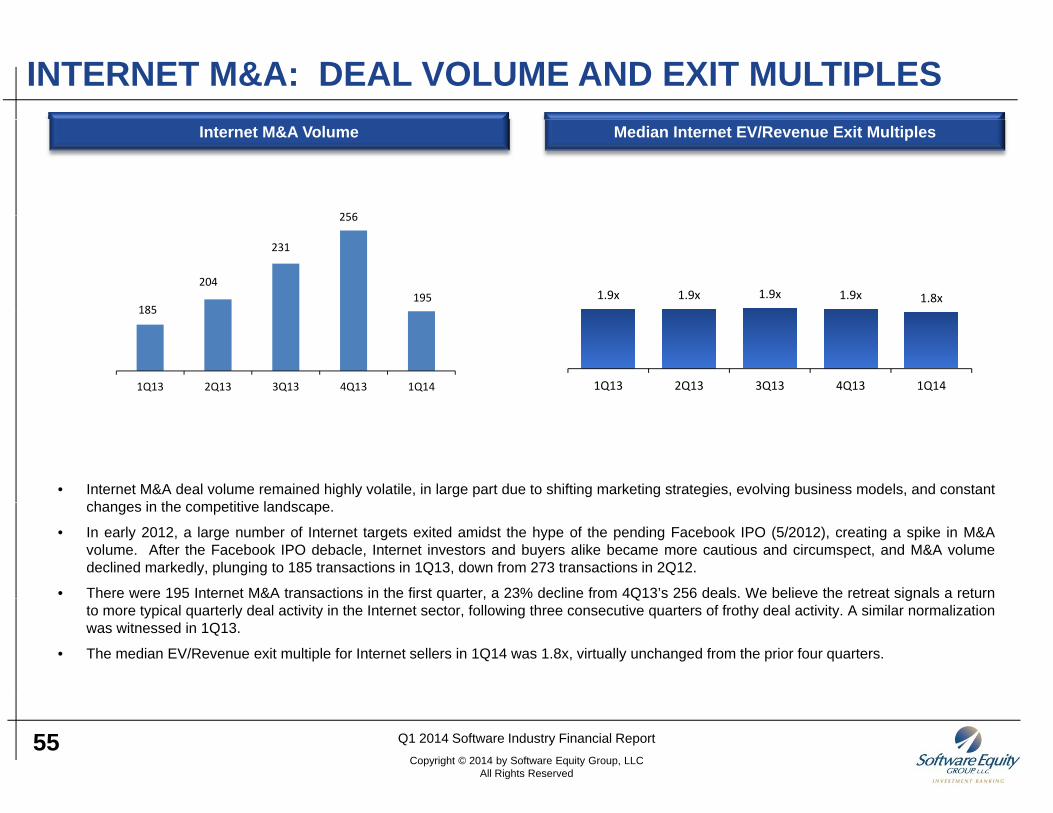

After a five year run up that included stellar returns in 2013, the bull market is showing signs of fatigue. After a very slow start in January,1Q14 stock market performance across all exchanges and indices was choppy for the remainder of the quarter.

• Q1’s bumpy ride for investors was largely attributable to the Fed’s announced plans for quantitative easing, skyrocketing market multiples, andgeopolitical unrest, particularly in Ukraine.

• The S&P posted the best return of the three major stock indices in 1Q14, finishing up 1.3%. The Nasdaq finished close behind, up 0.5%.Surprisingly, in an environment where investors flocked to value stocks, the DOW performed the worst of the three major U.S. stock marketSurprisingly, in an environment where investors flocked to value stocks, the DOW performed the worst of the three major U.S. stock marketindices, closing 1Q14 down 0.72%.

• The most dramatic swing in median stock returns in the first quarter was exhibited in the SEG SaaS Index. In early March, the index peakedwith a 9.2% return, only to plunge dramatically the rest of the month, closing 1Q14 down 4.6%. In addition to macro economic concerns, manyexpressed concerns that SaaS valuations had become too rich. More on the impact to median EV/Revenue multiples later in the report.

• The SEG Software Index, consisting largely of large, mature, and profitable companies held its own in a tough stock market environment,

11 Q1 2014 Software Industry Financial ReportCopyright © 2014 by Software Equity Group, LLC

All Rights Reserved

The SEG Software Index, consisting largely of large, mature, and profitable companies held its own in a tough stock market environment,finishing the quarter flat.

THE SEG SOFTWARE INDEX

PUBLIC SOFTWARE COMPANY FINANCIAL ANDPUBLIC SOFTWARE COMPANY FINANCIAL AND VALUATION PERFORMANCE

12

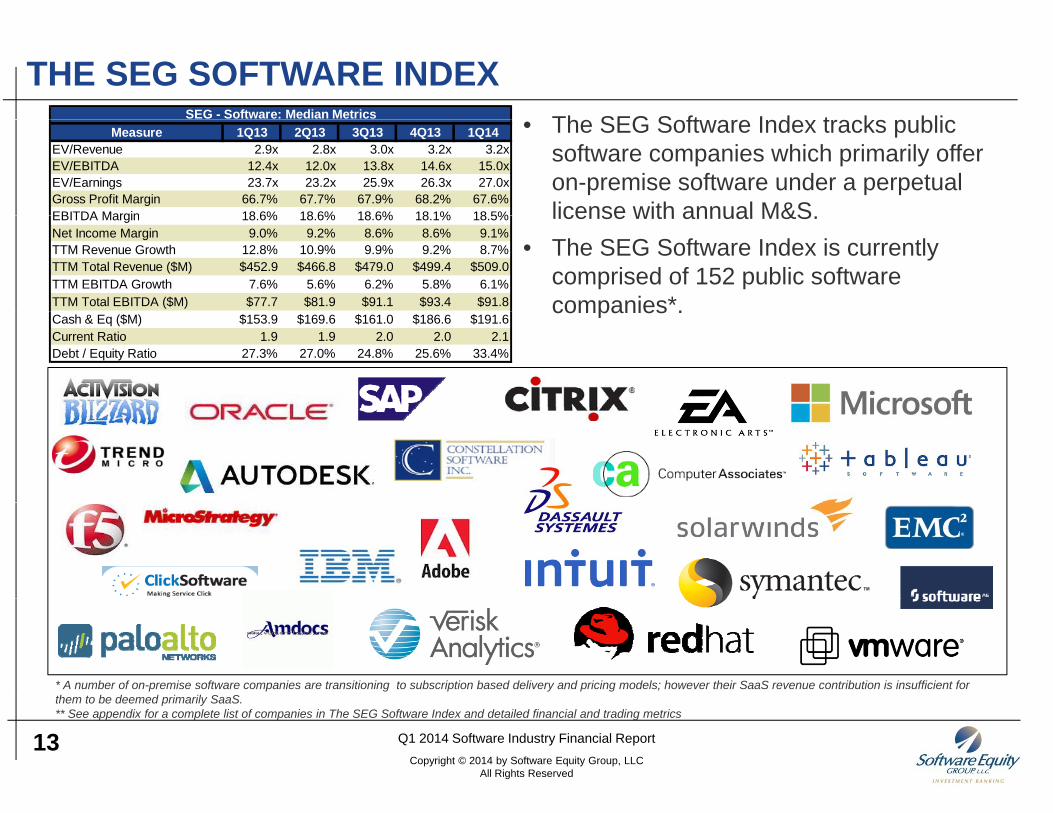

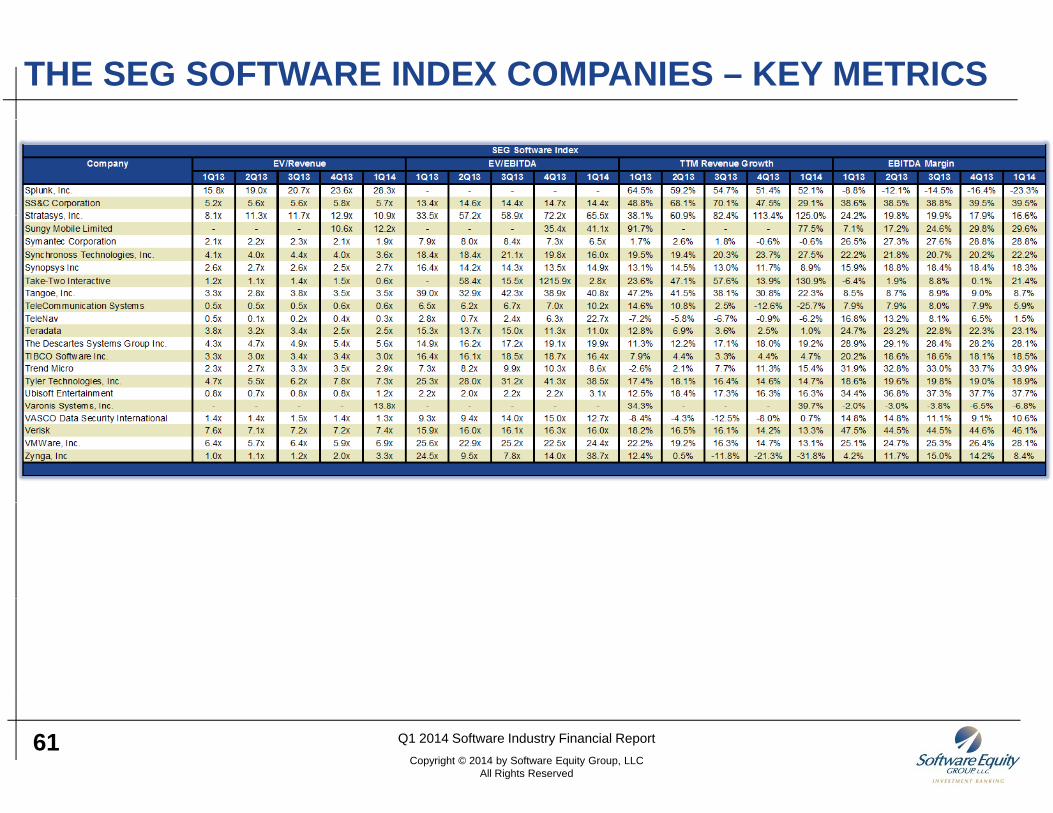

THE SEG SOFTWARE INDEXTh SEG S ft I d t k bliSEG - Software: Median Metrics • The SEG Software Index tracks public software companies which primarily offer on-premise software under a perpetual license with annual M&S

Measure 1Q13 2Q13 3Q13 4Q13 1Q14EV/Revenue 2.9x 2.8x 3.0x 3.2x 3.2xEV/EBITDA 12.4x 12.0x 13.8x 14.6x 15.0xEV/Earnings 23.7x 23.2x 25.9x 26.3x 27.0xGross Profit Margin 66.7% 67.7% 67.9% 68.2% 67.6%EBITDA Margin 18 6% 18 6% 18 6% 18 1% 18 5% license with annual M&S.

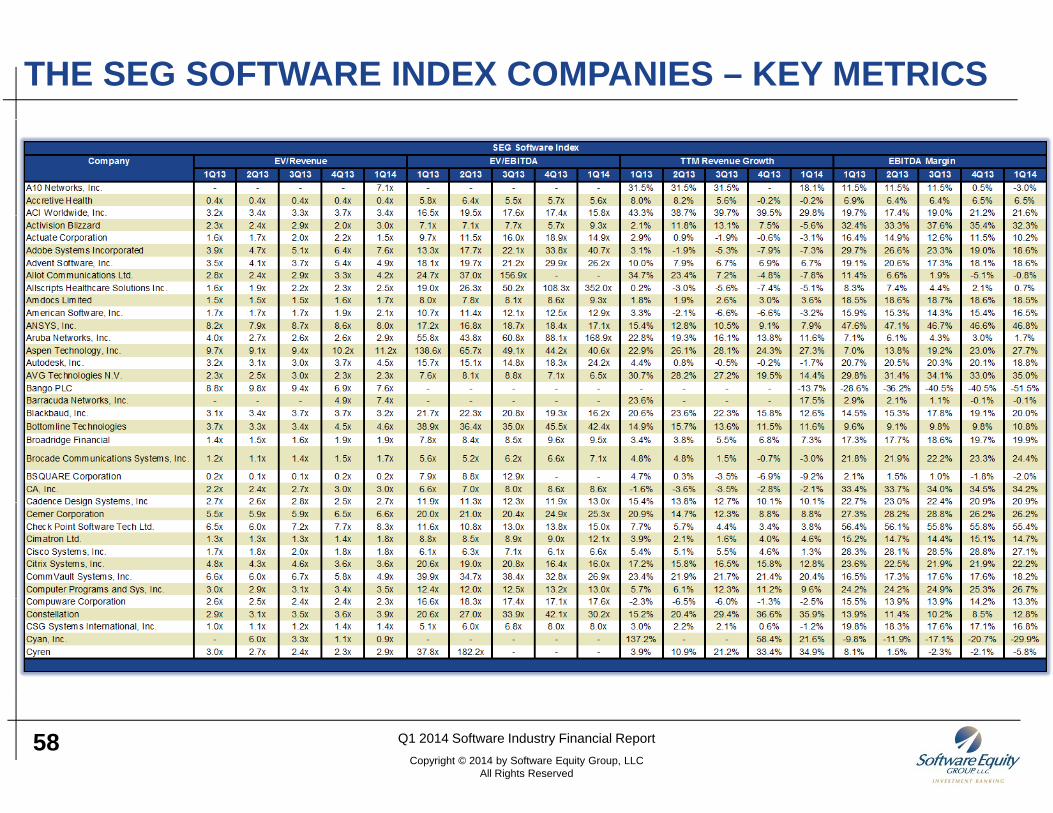

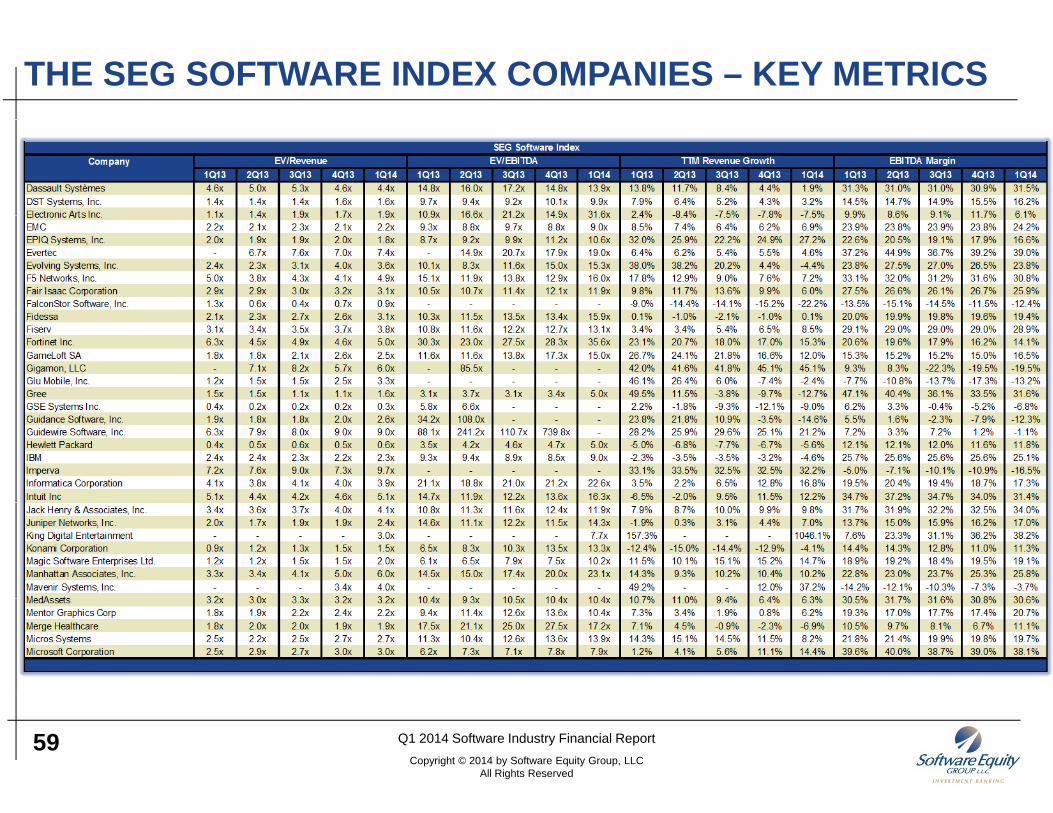

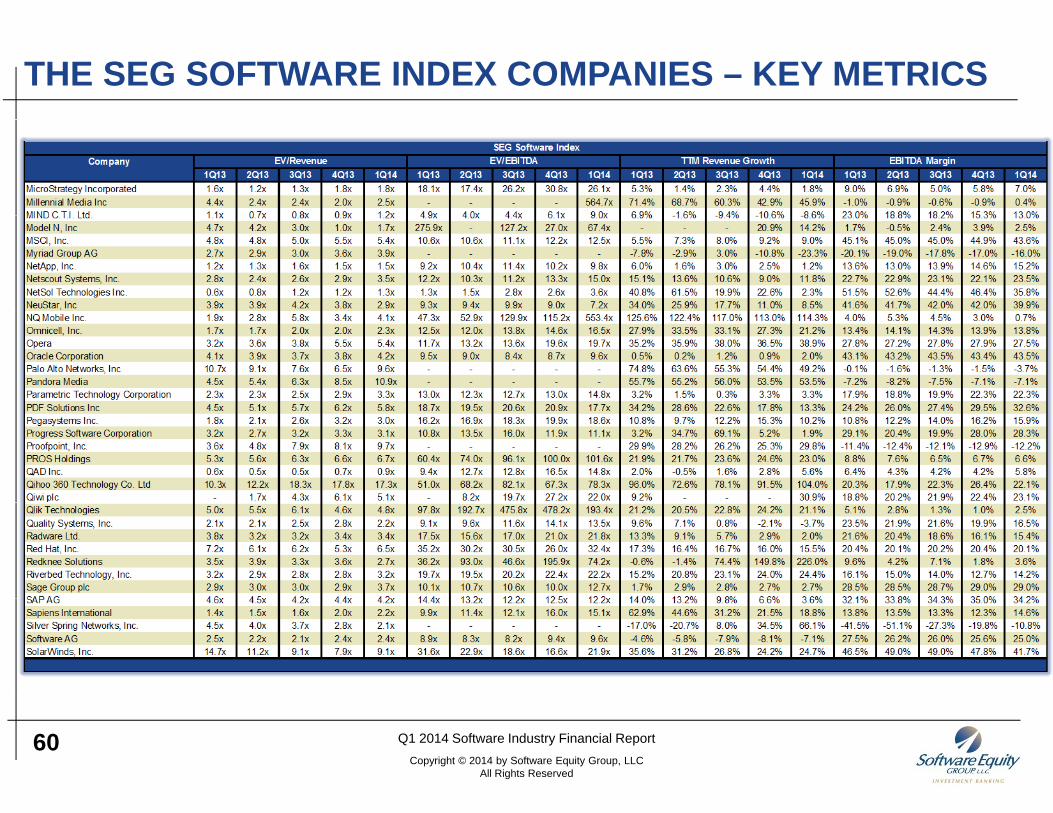

• The SEG Software Index is currently comprised of 152 public software companies*.

EBITDA Margin 18.6% 18.6% 18.6% 18.1% 18.5%Net Income Margin 9.0% 9.2% 8.6% 8.6% 9.1%TTM Revenue Growth 12.8% 10.9% 9.9% 9.2% 8.7%TTM Total Revenue ($M) $452.9 $466.8 $479.0 $499.4 $509.0TTM EBITDA Growth 7.6% 5.6% 6.2% 5.8% 6.1%TTM Total EBITDA ($M) $77.7 $81.9 $91.1 $93.4 $91.8 companies .Cash & Eq ($M) $153.9 $169.6 $161.0 $186.6 $191.6Current Ratio 1.9 1.9 2.0 2.0 2.1Debt / Equity Ratio 27.3% 27.0% 24.8% 25.6% 33.4%

* A number of on-premise software companies are transitioning to subscription based delivery and pricing models; however their SaaS revenue contribution is insufficient for

13 Q1 2014 Software Industry Financial ReportCopyright © 2014 by Software Equity Group, LLC

All Rights Reserved

them to be deemed primarily SaaS. ** See appendix for a complete list of companies in The SEG Software Index and detailed financial and trading metrics

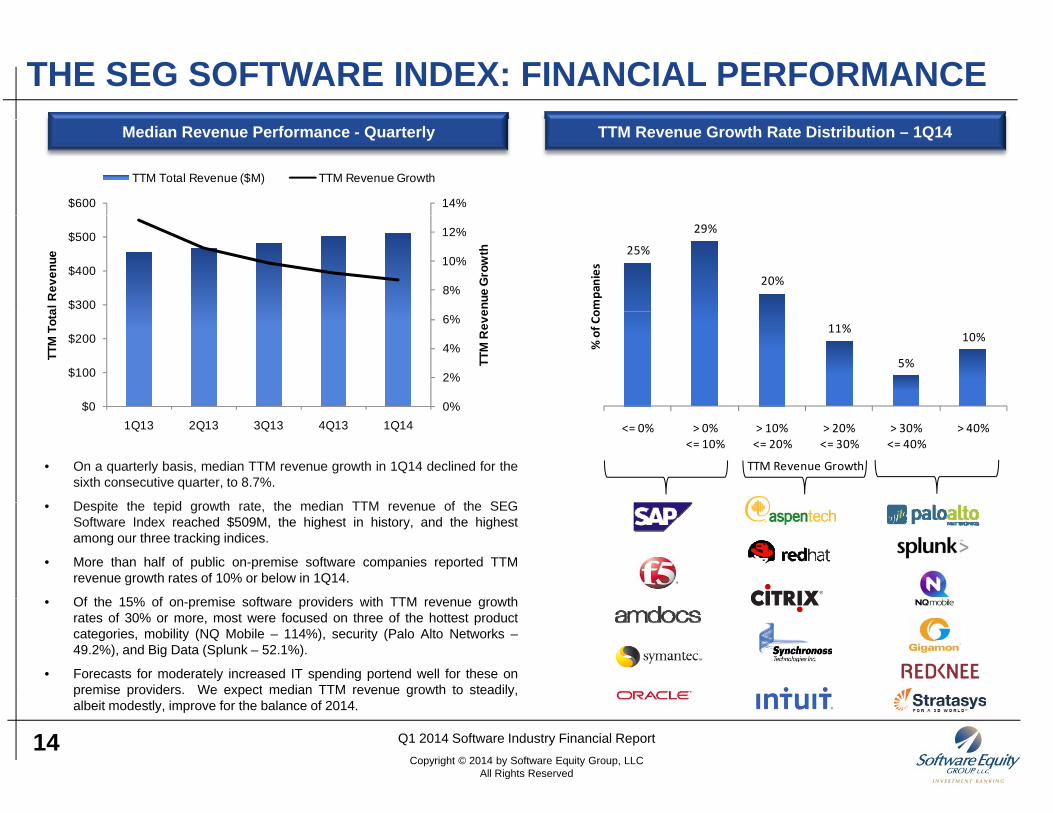

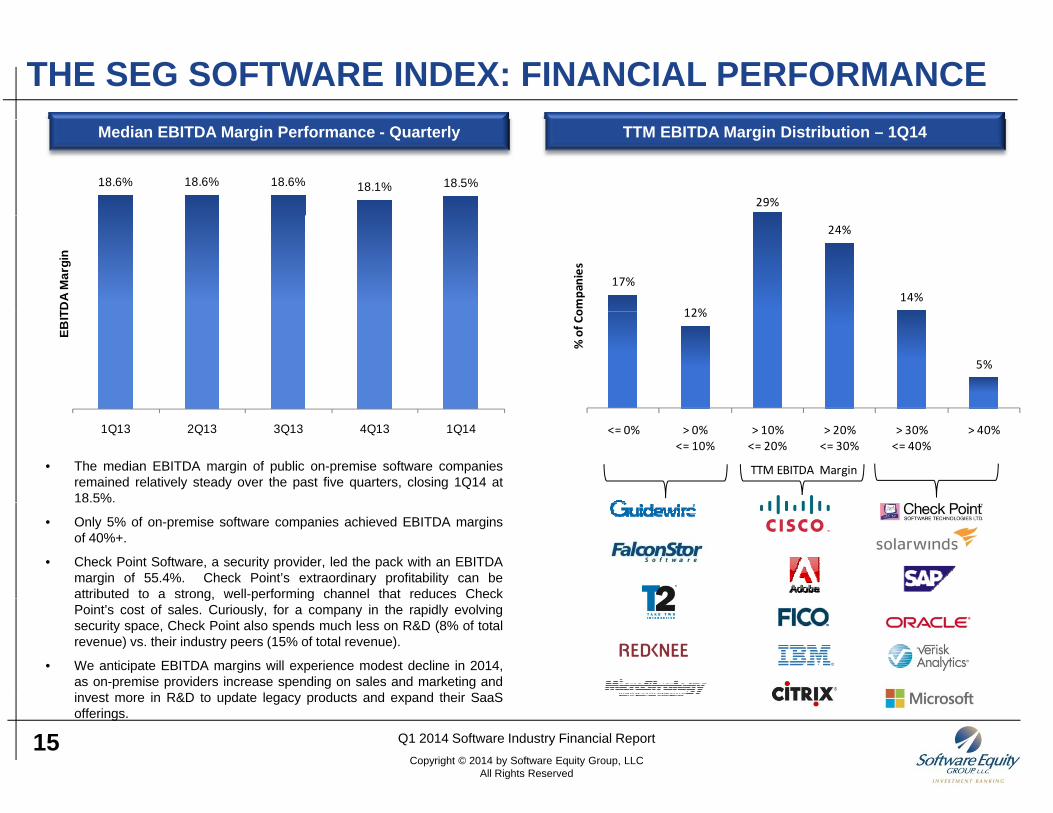

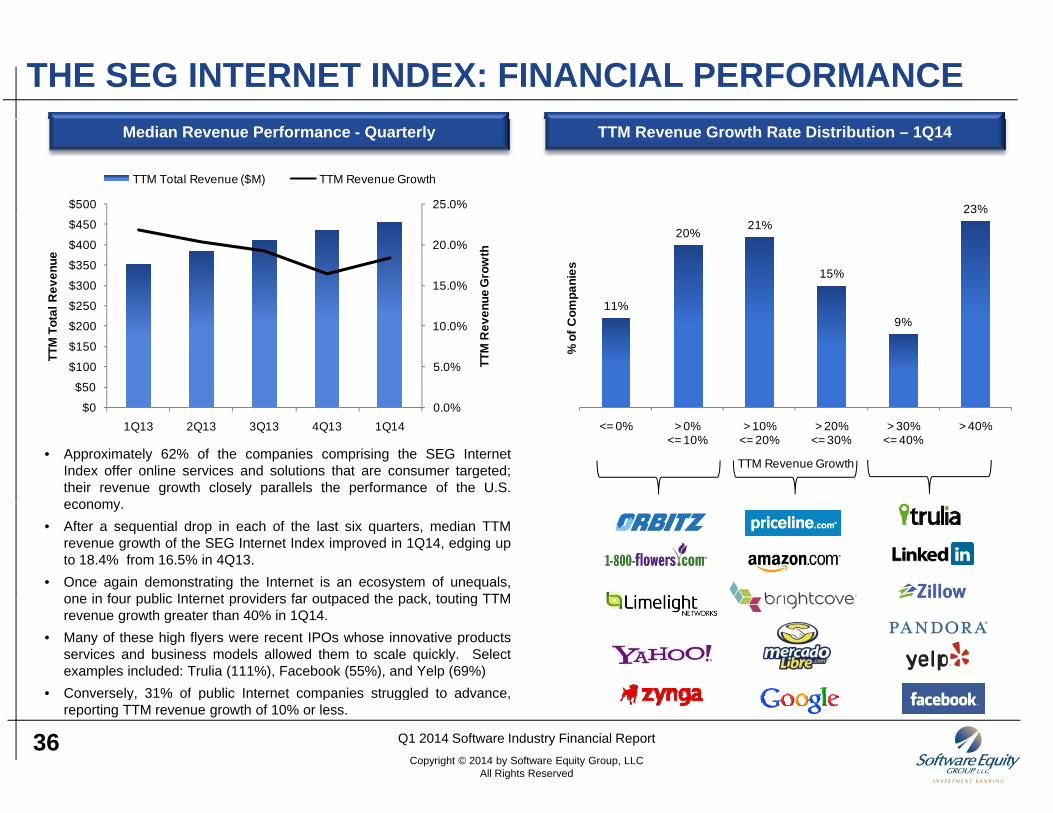

THE SEG SOFTWARE INDEX: FINANCIAL PERFORMANCEMedian Revenue Performance - Quarterly TTM Revenue Growth Rate Distribution – 1Q14

14%$600

TTM Total Revenue ($M) TTM Revenue Growth

8%

10%

12%

$300

$400

$500

enue

Gro

wth

al R

even

ue

25%

29%

20%

ompanies

0%

2%

4%

6%

$0

$100

$200

TTM

Rev

e

TTM

Tot

a

11%

5%

10%

% of C

o

• On a quarterly basis, median TTM revenue growth in 1Q14 declined for thesixth consecutive quarter, to 8.7%.

D it th t id th t th di TTM f th SEG

0%$01Q13 2Q13 3Q13 4Q13 1Q14 <= 0% > 0%

<= 10%> 10%<= 20%

> 20%<= 30%

> 30%<= 40%

> 40%

TTM Revenue Growth

• Despite the tepid growth rate, the median TTM revenue of the SEGSoftware Index reached $509M, the highest in history, and the highestamong our three tracking indices.

• More than half of public on-premise software companies reported TTMrevenue growth rates of 10% or below in 1Q14.

Of th 15% f i ft id ith TTM th• Of the 15% of on-premise software providers with TTM revenue growthrates of 30% or more, most were focused on three of the hottest productcategories, mobility (NQ Mobile – 114%), security (Palo Alto Networks –49.2%), and Big Data (Splunk – 52.1%).

• Forecasts for moderately increased IT spending portend well for these onpremise providers. We expect median TTM revenue growth to steadily,

14 Q1 2014 Software Industry Financial ReportCopyright © 2014 by Software Equity Group, LLC

All Rights Reserved

p e se p o de s e e pect ed a e e ue g o t to stead y,albeit modestly, improve for the balance of 2014.

THE SEG SOFTWARE INDEX: FINANCIAL PERFORMANCETTM EBITDA Margin Distribution – 1Q14Median EBITDA Margin Performance - Quarterly

29%18.6% 18.6% 18.6% 18.1% 18.5%

17%

12%

24%

14%

ompanies

TDA

Mar

gin

12%

5%

% of C

o

EBIT

• The median EBITDA margin of public on-premise software companiesremained relatively steady over the past five quarters, closing 1Q14 at18.5%.

<= 0% > 0%<= 10%

> 10%<= 20%

> 20%<= 30%

> 30%<= 40%

> 40%

TTM EBITDA Margin

1Q13 2Q13 3Q13 4Q13 1Q14

%

• Only 5% of on-premise software companies achieved EBITDA marginsof 40%+.

• Check Point Software, a security provider, led the pack with an EBITDAmargin of 55.4%. Check Point’s extraordinary profitability can beattributed to a strong, well-performing channel that reduces Checkg, p gPoint’s cost of sales. Curiously, for a company in the rapidly evolvingsecurity space, Check Point also spends much less on R&D (8% of totalrevenue) vs. their industry peers (15% of total revenue).

• We anticipate EBITDA margins will experience modest decline in 2014,as on-premise providers increase spending on sales and marketing andi t i R&D t d t l d t d d th i S S

15 Q1 2014 Software Industry Financial ReportCopyright © 2014 by Software Equity Group, LLC

All Rights Reserved

invest more in R&D to update legacy products and expand their SaaSofferings.

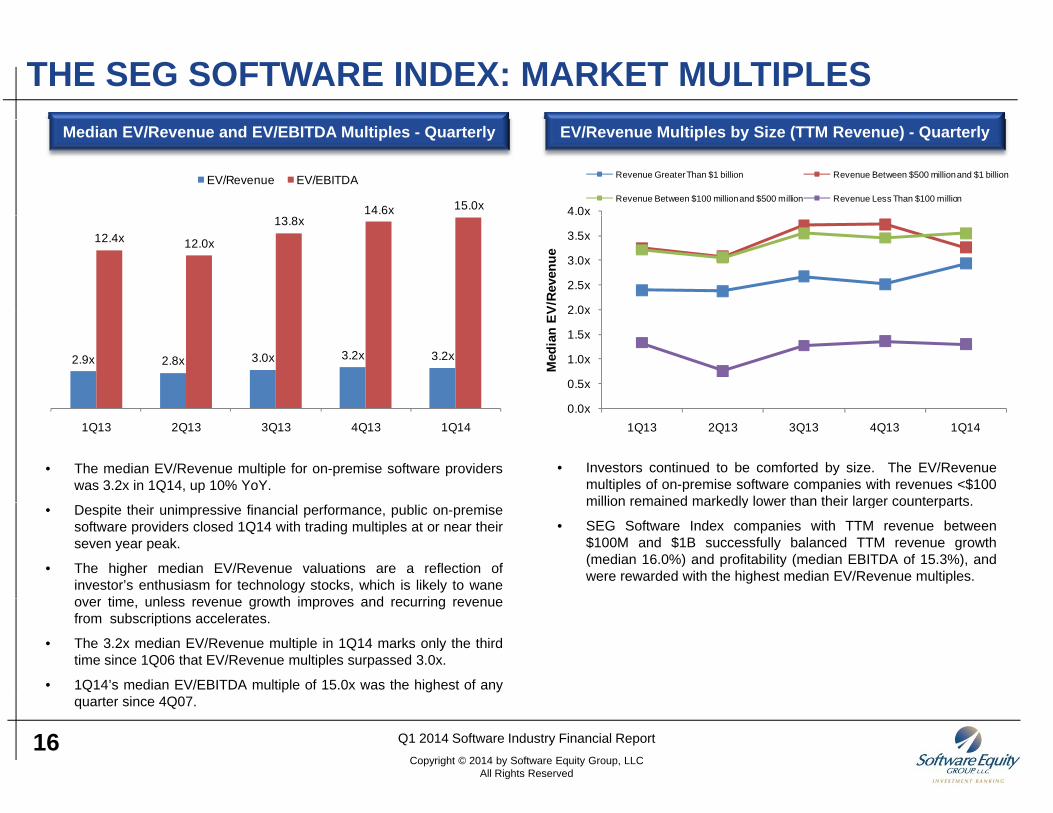

THE SEG SOFTWARE INDEX: MARKET MULTIPLESEV/Revenue Multiples by Size (TTM Revenue) - QuarterlyMedian EV/Revenue and EV/EBITDA Multiples - Quarterly

14.6x 15.0x

EV/Revenue EV/EBITDA

4.0x

Revenue Greater Than $1 billion Revenue Between $500 million and $1 billion

Revenue Between $100 million and $500 million Revenue Less Than $100 million

12.4x 12.0x

13.8x

2 0x

2.5x

3.0x

3.5x

V/Re

venu

e

2.9x 2.8x 3.0x 3.2x 3.2x

0 0x

0.5x

1.0x

1.5x

2.0x

Med

ian

EV

• The median EV/Revenue multiple for on-premise software providerswas 3.2x in 1Q14, up 10% YoY.

• Investors continued to be comforted by size. The EV/Revenuemultiples of on-premise software companies with revenues <$100million remained markedly lower than their larger counterparts

1Q13 2Q13 3Q13 4Q13 1Q140.0x

1Q13 2Q13 3Q13 4Q13 1Q14

• Despite their unimpressive financial performance, public on-premisesoftware providers closed 1Q14 with trading multiples at or near theirseven year peak.

• The higher median EV/Revenue valuations are a reflection ofinvestor’s enthusiasm for technology stocks, which is likely to wane

ti l th i d i

million remained markedly lower than their larger counterparts.

• SEG Software Index companies with TTM revenue between$100M and $1B successfully balanced TTM revenue growth(median 16.0%) and profitability (median EBITDA of 15.3%), andwere rewarded with the highest median EV/Revenue multiples.

over time, unless revenue growth improves and recurring revenuefrom subscriptions accelerates.

• The 3.2x median EV/Revenue multiple in 1Q14 marks only the thirdtime since 1Q06 that EV/Revenue multiples surpassed 3.0x.

• 1Q14’s median EV/EBITDA multiple of 15.0x was the highest of any

16 Q1 2014 Software Industry Financial ReportCopyright © 2014 by Software Equity Group, LLC

All Rights Reserved

quarter since 4Q07.

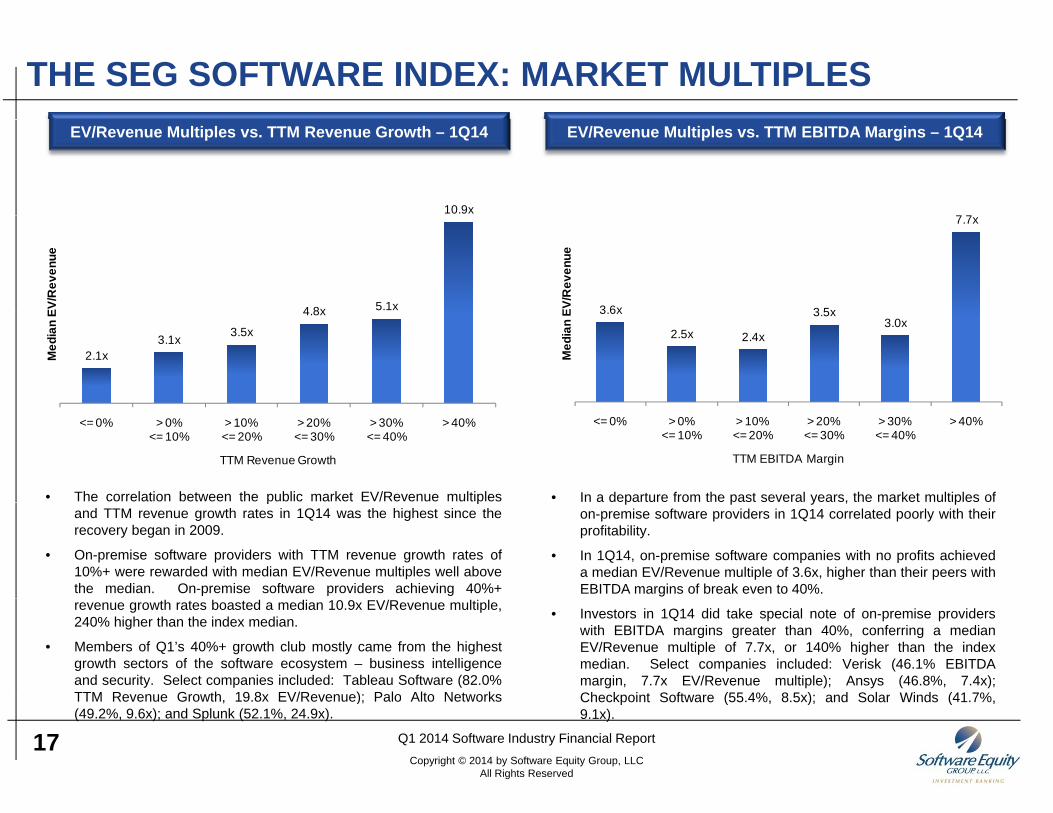

THE SEG SOFTWARE INDEX: MARKET MULTIPLESEV/Revenue Multiples vs. TTM EBITDA Margins – 1Q14EV/Revenue Multiples vs. TTM Revenue Growth – 1Q14

10.9x7 7

4 8x 5.1xEV/R

even

ue

3 6x 3 5x

7.7x

EV/R

even

ue

2.1x3.1x 3.5x

4.8x

Med

ian

E 3.6x

2.5x 2.4x

3.5x3.0x

Med

ian

E

• The correlation between the public market EV/Revenue multiples • In a departure from the past several years, the market multiples of

<= 0% > 0%<= 10%

> 10%<= 20%

> 20%<= 30%

> 30%<= 40%

> 40%

TTM Revenue Growth

<= 0% > 0%<= 10%

> 10%<= 20%

> 20%<= 30%

> 30%<= 40%

> 40%

TTM EBITDA Margin

p pand TTM revenue growth rates in 1Q14 was the highest since therecovery began in 2009.

• On-premise software providers with TTM revenue growth rates of10%+ were rewarded with median EV/Revenue multiples well abovethe median. On-premise software providers achieving 40%+

p p y , pon-premise software providers in 1Q14 correlated poorly with theirprofitability.

• In 1Q14, on-premise software companies with no profits achieveda median EV/Revenue multiple of 3.6x, higher than their peers withEBITDA margins of break even to 40%.

revenue growth rates boasted a median 10.9x EV/Revenue multiple,240% higher than the index median.

• Members of Q1’s 40%+ growth club mostly came from the highestgrowth sectors of the software ecosystem – business intelligenceand security. Select companies included: Tableau Software (82.0%TTM Re en e Gro th 19 8 EV/Re en e) Palo Alto Net orks

• Investors in 1Q14 did take special note of on-premise providerswith EBITDA margins greater than 40%, conferring a medianEV/Revenue multiple of 7.7x, or 140% higher than the indexmedian. Select companies included: Verisk (46.1% EBITDAmargin, 7.7x EV/Revenue multiple); Ansys (46.8%, 7.4x);Ch k i t S ft (55 4% 8 5 ) d S l Wi d (41 7%

17 Q1 2014 Software Industry Financial ReportCopyright © 2014 by Software Equity Group, LLC

All Rights Reserved

TTM Revenue Growth, 19.8x EV/Revenue); Palo Alto Networks(49.2%, 9.6x); and Splunk (52.1%, 24.9x).

Checkpoint Software (55.4%, 8.5x); and Solar Winds (41.7%,9.1x).

THE SEG SOFTWARE INDEX BY PRODUCT CATEGORY

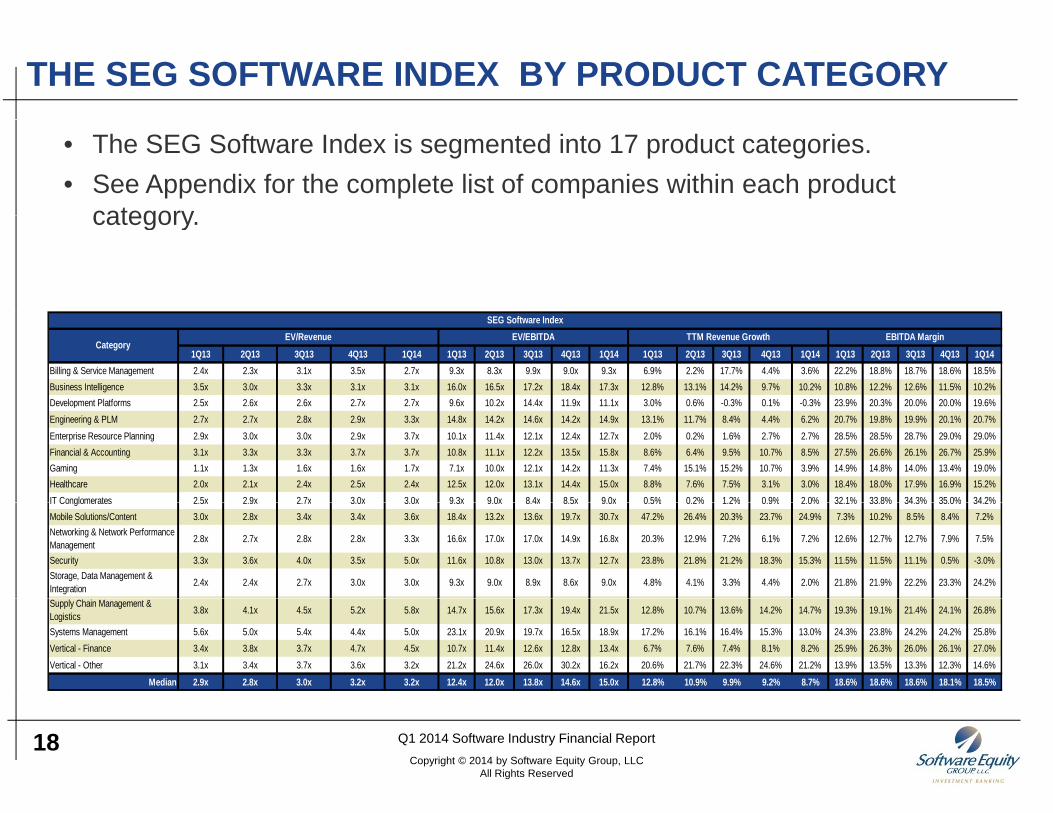

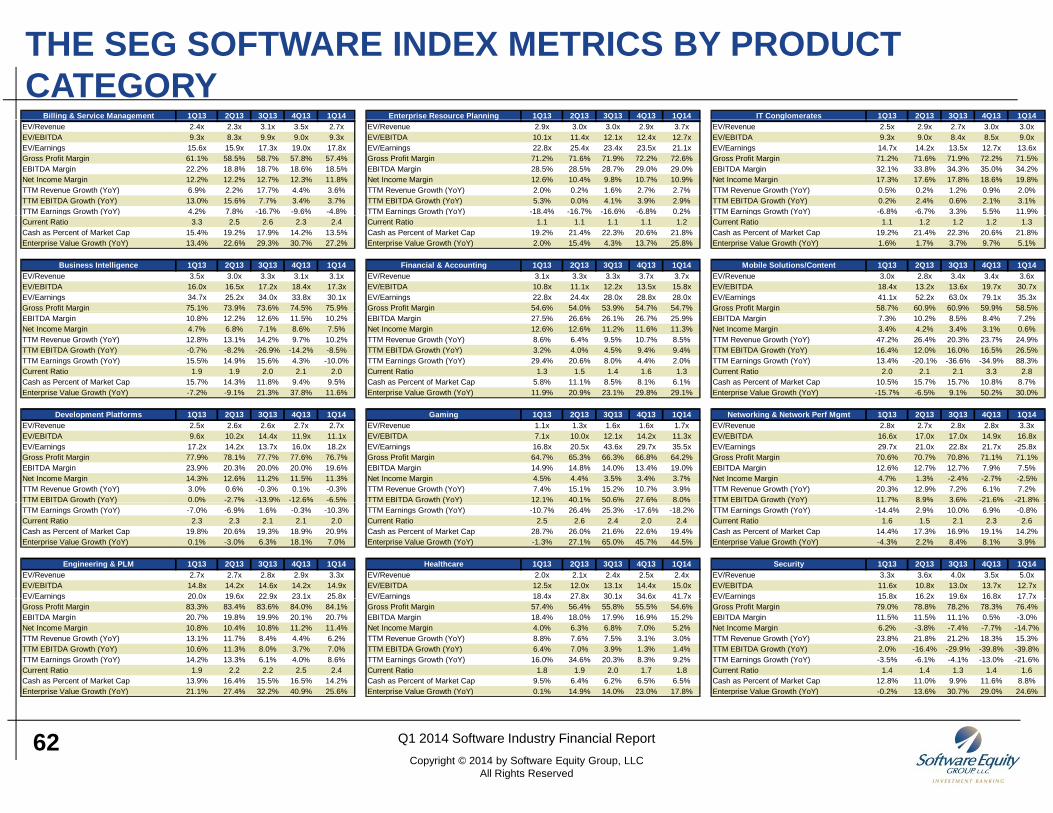

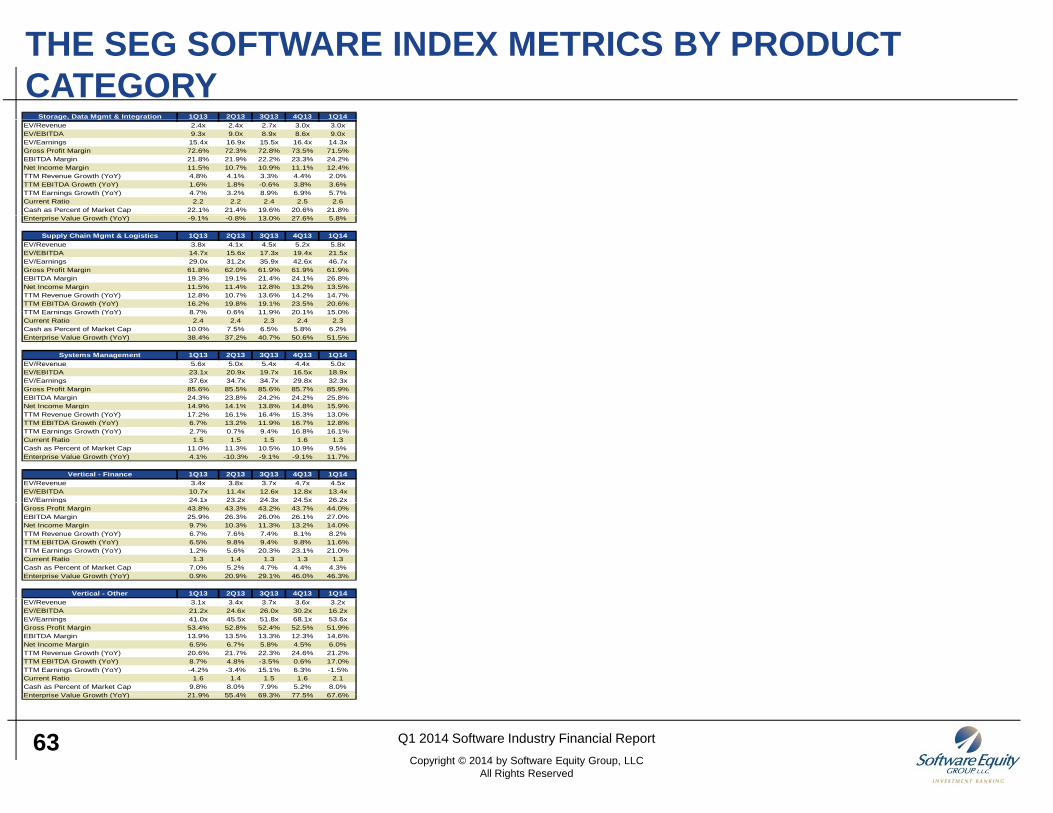

• The SEG Software Index is segmented into 17 product categories.• See Appendix for the complete list of companies within each product

categorycategory.

1Q13 2Q13 3Q13 4Q13 1Q14 1Q13 2Q13 3Q13 4Q13 1Q14 1Q13 2Q13 3Q13 4Q13 1Q14 1Q13 2Q13 3Q13 4Q13 1Q14Billing & Service Management 2.4x 2.3x 3.1x 3.5x 2.7x 9.3x 8.3x 9.9x 9.0x 9.3x 6.9% 2.2% 17.7% 4.4% 3.6% 22.2% 18.8% 18.7% 18.6% 18.5%Business Intelligence 3.5x 3.0x 3.3x 3.1x 3.1x 16.0x 16.5x 17.2x 18.4x 17.3x 12.8% 13.1% 14.2% 9.7% 10.2% 10.8% 12.2% 12.6% 11.5% 10.2%Development Platforms 2.5x 2.6x 2.6x 2.7x 2.7x 9.6x 10.2x 14.4x 11.9x 11.1x 3.0% 0.6% -0.3% 0.1% -0.3% 23.9% 20.3% 20.0% 20.0% 19.6%

SEG Software Index

CategoryEV/Revenue EV/EBITDA TTM Revenue Growth EBITDA Margin

pEngineering & PLM 2.7x 2.7x 2.8x 2.9x 3.3x 14.8x 14.2x 14.6x 14.2x 14.9x 13.1% 11.7% 8.4% 4.4% 6.2% 20.7% 19.8% 19.9% 20.1% 20.7%Enterprise Resource Planning 2.9x 3.0x 3.0x 2.9x 3.7x 10.1x 11.4x 12.1x 12.4x 12.7x 2.0% 0.2% 1.6% 2.7% 2.7% 28.5% 28.5% 28.7% 29.0% 29.0%Financial & Accounting 3.1x 3.3x 3.3x 3.7x 3.7x 10.8x 11.1x 12.2x 13.5x 15.8x 8.6% 6.4% 9.5% 10.7% 8.5% 27.5% 26.6% 26.1% 26.7% 25.9%Gaming 1.1x 1.3x 1.6x 1.6x 1.7x 7.1x 10.0x 12.1x 14.2x 11.3x 7.4% 15.1% 15.2% 10.7% 3.9% 14.9% 14.8% 14.0% 13.4% 19.0%Healthcare 2.0x 2.1x 2.4x 2.5x 2.4x 12.5x 12.0x 13.1x 14.4x 15.0x 8.8% 7.6% 7.5% 3.1% 3.0% 18.4% 18.0% 17.9% 16.9% 15.2%IT Conglomerates 2 5x 2 9x 2 7x 3 0x 3 0x 9 3x 9 0x 8 4x 8 5x 9 0x 0 5% 0 2% 1 2% 0 9% 2 0% 32 1% 33 8% 34 3% 35 0% 34 2%IT Conglomerates 2.5x 2.9x 2.7x 3.0x 3.0x 9.3x 9.0x 8.4x 8.5x 9.0x 0.5% 0.2% 1.2% 0.9% 2.0% 32.1% 33.8% 34.3% 35.0% 34.2%Mobile Solutions/Content 3.0x 2.8x 3.4x 3.4x 3.6x 18.4x 13.2x 13.6x 19.7x 30.7x 47.2% 26.4% 20.3% 23.7% 24.9% 7.3% 10.2% 8.5% 8.4% 7.2%Networking & Network Performance Management 2.8x 2.7x 2.8x 2.8x 3.3x 16.6x 17.0x 17.0x 14.9x 16.8x 20.3% 12.9% 7.2% 6.1% 7.2% 12.6% 12.7% 12.7% 7.9% 7.5%

Security 3.3x 3.6x 4.0x 3.5x 5.0x 11.6x 10.8x 13.0x 13.7x 12.7x 23.8% 21.8% 21.2% 18.3% 15.3% 11.5% 11.5% 11.1% 0.5% -3.0%Storage, Data Management & Integration 2.4x 2.4x 2.7x 3.0x 3.0x 9.3x 9.0x 8.9x 8.6x 9.0x 4.8% 4.1% 3.3% 4.4% 2.0% 21.8% 21.9% 22.2% 23.3% 24.2%

Supply Chain Management & Logistics 3.8x 4.1x 4.5x 5.2x 5.8x 14.7x 15.6x 17.3x 19.4x 21.5x 12.8% 10.7% 13.6% 14.2% 14.7% 19.3% 19.1% 21.4% 24.1% 26.8%

Systems Management 5.6x 5.0x 5.4x 4.4x 5.0x 23.1x 20.9x 19.7x 16.5x 18.9x 17.2% 16.1% 16.4% 15.3% 13.0% 24.3% 23.8% 24.2% 24.2% 25.8%Vertical - Finance 3.4x 3.8x 3.7x 4.7x 4.5x 10.7x 11.4x 12.6x 12.8x 13.4x 6.7% 7.6% 7.4% 8.1% 8.2% 25.9% 26.3% 26.0% 26.1% 27.0%Vertical - Other 3.1x 3.4x 3.7x 3.6x 3.2x 21.2x 24.6x 26.0x 30.2x 16.2x 20.6% 21.7% 22.3% 24.6% 21.2% 13.9% 13.5% 13.3% 12.3% 14.6%

Median 2.9x 2.8x 3.0x 3.2x 3.2x 12.4x 12.0x 13.8x 14.6x 15.0x 12.8% 10.9% 9.9% 9.2% 8.7% 18.6% 18.6% 18.6% 18.1% 18.5%

18 Q1 2014 Software Industry Financial ReportCopyright © 2014 by Software Equity Group, LLC

All Rights Reserved

1Q14 Median YoY Change in Revenue Growth1Q14 Median TTM Revenue Growth

THE SEG SOFTWARE INDEX BY PRODUCT CATEGORY:FINANCIAL PERFORMANCE

1Q14 Median YoY Change in Revenue Growth1Q14 Median TTM Revenue Growth

(131%)

3.6%10.2%

(0.5%)6.2%

2 7%

Billing & Service ManagementBusiness Intelligence

Development PlatformsEngineering & PLM

Enterprise Resource Planning

(47.6%)(20.2%)

(52.6%)34 8%

Billing & Service ManagementBusiness Intelligence

Development PlatformsEngineering & PLM

Enterprise Resource Planning2.7%8.5%

3.9%3.0%

2.0%24.9%

7.2%

Enterprise Resource PlanningFinancial & Accounting

GamingHealthcare

IT ConglomeratesMobile Solutions/Content

Networking & Network Performance …

34.8% (0.3%)

(47.1%)(65.3%)

(47.3%)(64.6%)

Enterprise Resource PlanningFinancial & Accounting

GamingHealthcare

IT ConglomeratesMobile Solutions/Content

Networking & Network Performance…

343.5%

15.3%2.0%

14.7%13.0%

8.2%21.2%

gSecurity

Storage, Data Management & IntegrationSupply Chain Management & Logistics

Systems ManagementVertical - Finance

Vertical - Other

(64.6%)(35.6%)

(57.7%)15.0%

(24.8%)21.8%

2.6%

Networking & Network Performance …Security

Storage, Data Management & IntegrationSupply Chain Management & Logistics

Systems ManagementVertical - Finance

Vertical - Other

1Q14 Median YoY Change EBITDA Margin1Q14 Median TTM EBITDA Margin(16.4%)

(5.9%)(18.1%)

0 1%

Billing & Service ManagementBusiness Intelligence

Development PlatformsEngineering & PLM

18.5%10.2%

19.6%

Billing & Service ManagementBusiness Intelligence

Development Platforms0.1% 1.9%

(5.9%)27.5%

(17.8%)6.7%

(2.1%)

Engineering & PLMEnterprise Resource Planning

Financial & AccountingGaming

HealthcareIT Conglomerates

Mobile Solutions/Content

20.7%29.0%

25.9%19.0%

15.2%34.2%

7 2%

Engineering & PLMEnterprise Resource Planning

Financial & AccountingGaming

HealthcareIT Conglomerates

M bil S l ti /C t t( )

(40.2%)

11.0% 38.4%

6.1% 4.3%

Networking & Network Performance …Security

Storage, Data Management & IntegrationSupply Chain Management & Logistics

Systems ManagementVertical - Finance

7.2%7.5%

(3.0%)24.2%

26.8%25.8%27 0%

Mobile Solutions/ContentNetworking & Network Performance …

SecurityStorage, Data Management & Integration

Supply Chain Management & LogisticsSystems Management

Vertical - Finance

19 Q1 2014 Software Industry Financial ReportCopyright © 2014 by Software Equity Group, LLC

All Rights Reserved

5.1% Vertical - Other27.0%14.6%

Vertical - FinanceVertical - Other

THE SEG SOFTWARE INDEX BY PRODUCT CATEGORY:MARKET MULTIPLES

Median 1Q14 YoY Change in EV/Revenue Multiples1Q14 Median EV/Revenue Multiples Median 1Q14 YoY Change in EV/Revenue Multiples1Q14 Median EV/Revenue Multiples

2.7x3.1x

2.7x3.3x

Billing & Service ManagementBusiness Intelligence

Development PlatformsEngineering & PLM

10.1% (9.1%)

7.3% 21.6%

Billing & Service ManagementBusiness Intelligence

Development PlatformsEngineering & PLM

3.7x3.7x

1.7x2.4x

3.0x

Enterprise Resource PlanningFinancial & Accounting

GamingHealthcare

IT Conglomerates

28.4% 17.0%

52.3% 20.5% 22.6%

18 6%

Enterprise Resource PlanningFinancial & Accounting

GamingHealthcare

IT ConglomeratesM bil S l ti /C t t3.6x

3.3x5.0x

3.0x5.8x

5 0x

Mobile Solutions/ContentNetworking & Network Performance …

SecurityStorage, Data Management & Integration

Supply Chain Management & LogisticsSystems Management

18.6% 15.8%

51.2% 23.5%

52.0% (10 6%)

Mobile Solutions/ContentNetworking & Network Performance …

SecurityStorage, Data Management & Integration

Supply Chain Management & LogisticsSystems Management

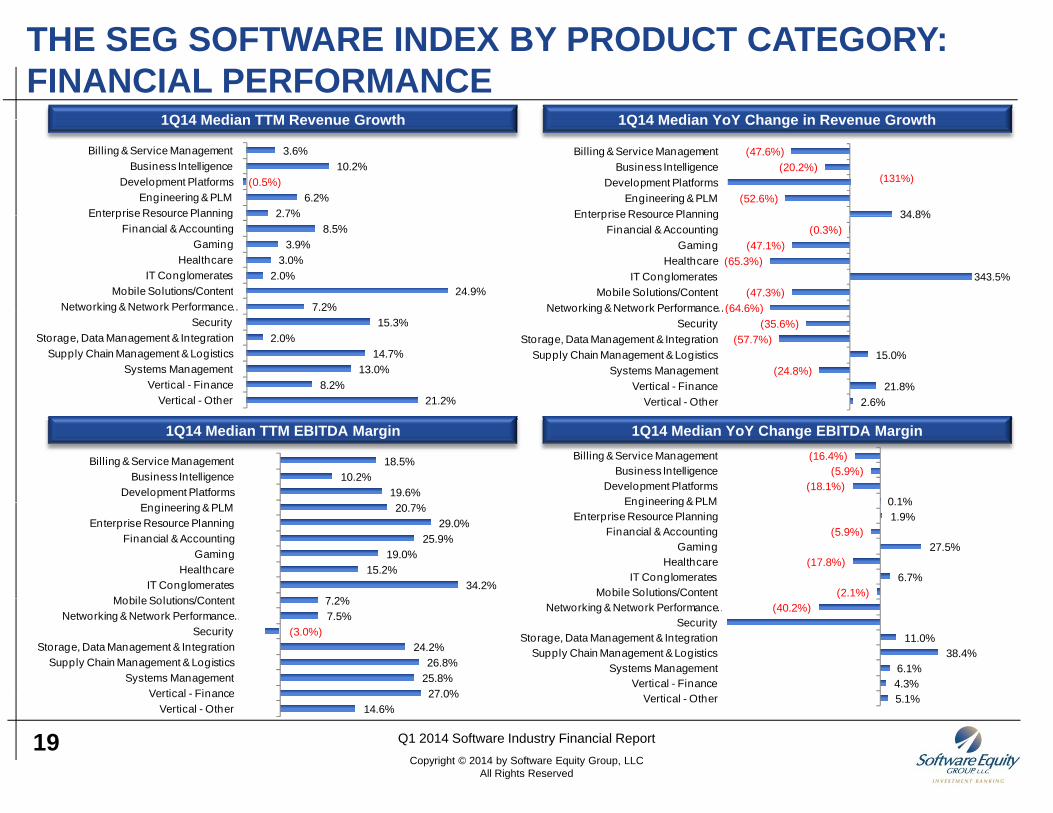

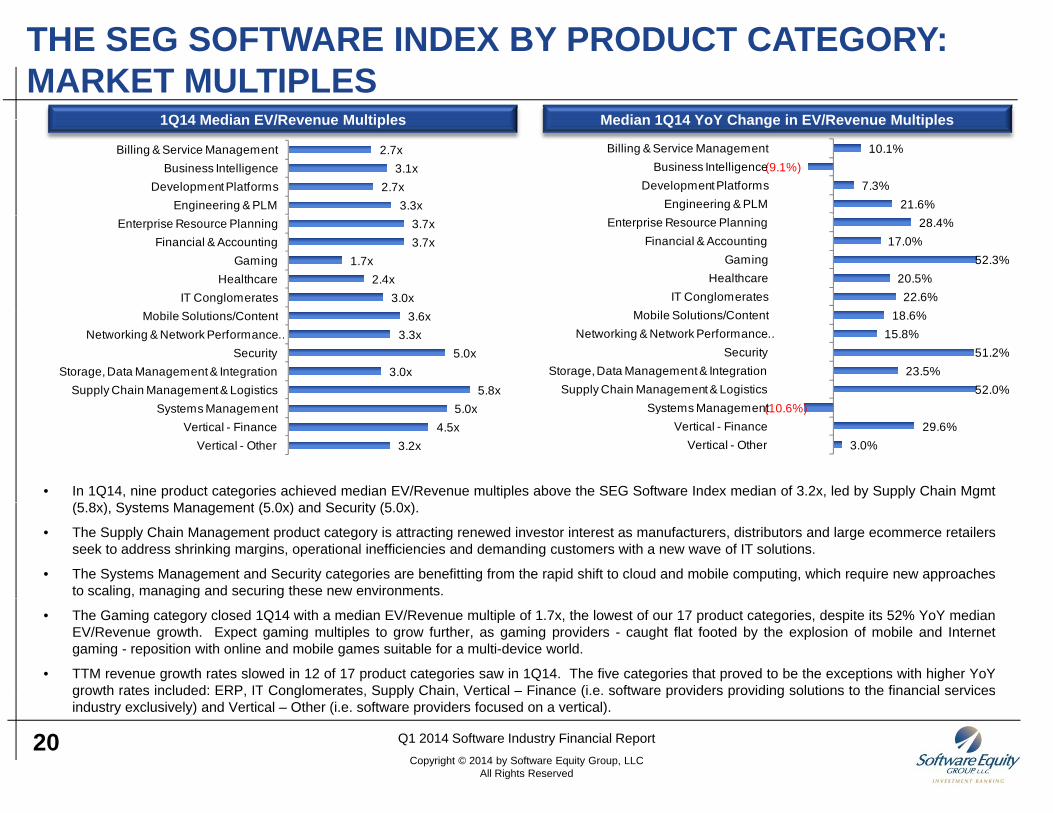

• In 1Q14, nine product categories achieved median EV/Revenue multiples above the SEG Software Index median of 3.2x, led by Supply Chain Mgmt(5 8 ) S t M t (5 0 ) d S it (5 0 )

5.0x4.5x

3.2x

Systems ManagementVertical - Finance

Vertical - Other

(10.6%)29.6%

3.0%

Systems ManagementVertical - Finance

Vertical - Other

(5.8x), Systems Management (5.0x) and Security (5.0x).

• The Supply Chain Management product category is attracting renewed investor interest as manufacturers, distributors and large ecommerce retailersseek to address shrinking margins, operational inefficiencies and demanding customers with a new wave of IT solutions.

• The Systems Management and Security categories are benefitting from the rapid shift to cloud and mobile computing, which require new approachesto scaling, managing and securing these new environments.

• The Gaming category closed 1Q14 with a median EV/Revenue multiple of 1.7x, the lowest of our 17 product categories, despite its 52% YoY medianEV/Revenue growth. Expect gaming multiples to grow further, as gaming providers - caught flat footed by the explosion of mobile and Internetgaming - reposition with online and mobile games suitable for a multi-device world.

• TTM revenue growth rates slowed in 12 of 17 product categories saw in 1Q14. The five categories that proved to be the exceptions with higher YoYgrowth rates included: ERP, IT Conglomerates, Supply Chain, Vertical – Finance (i.e. software providers providing solutions to the financial services

20 Q1 2014 Software Industry Financial ReportCopyright © 2014 by Software Equity Group, LLC

All Rights Reserved

growth rates included: ERP, IT Conglomerates, Supply Chain, Vertical Finance (i.e. software providers providing solutions to the financial servicesindustry exclusively) and Vertical – Other (i.e. software providers focused on a vertical).

THE SEG SaaS INDEX

PUBLIC S S COMPANY FINANCIAL ANDPUBLIC SaaS COMPANY FINANCIAL AND VALUATION PERFORMANCE

21

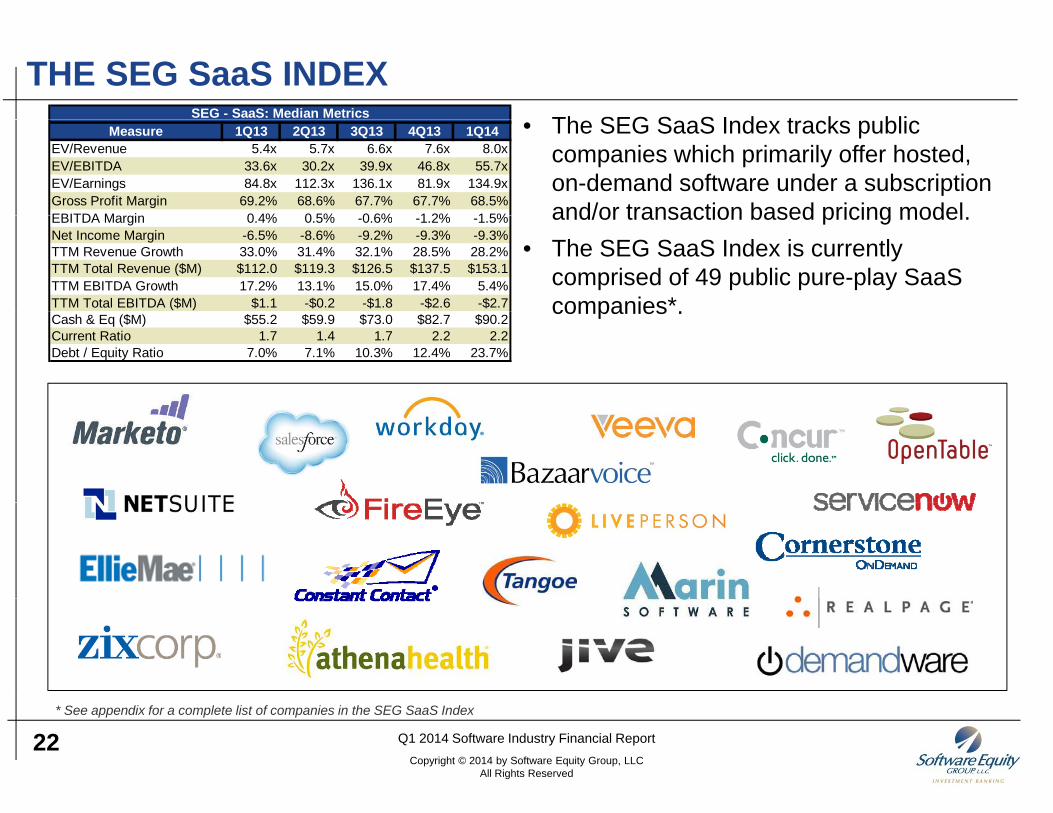

Th SEG S S I d t k bli

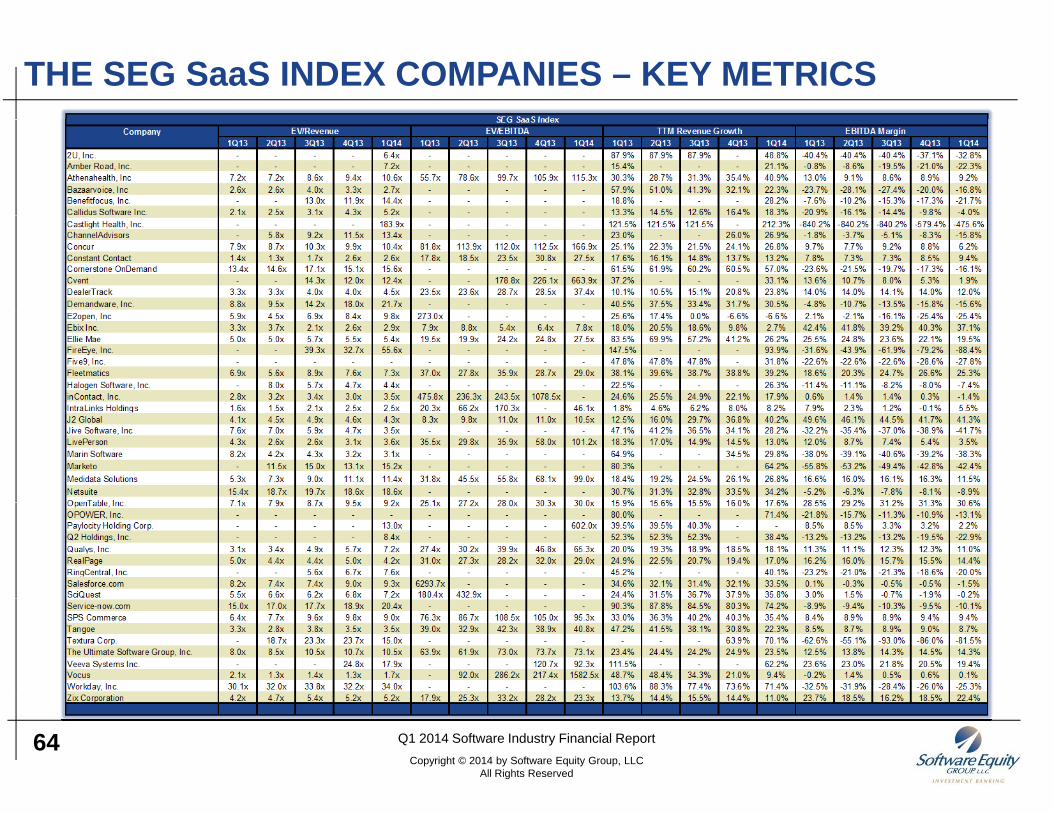

THE SEG SaaS INDEXSEG - SaaS: Median Metrics • The SEG SaaS Index tracks public

companies which primarily offer hosted, on-demand software under a subscription and/or transaction based pricing model

Measure 1Q13 2Q13 3Q13 4Q13 1Q14EV/Revenue 5.4x 5.7x 6.6x 7.6x 8.0xEV/EBITDA 33.6x 30.2x 39.9x 46.8x 55.7xEV/Earnings 84.8x 112.3x 136.1x 81.9x 134.9xGross Profit Margin 69.2% 68.6% 67.7% 67.7% 68.5%EBITDA M i 0 4% 0 5% 0 6% 1 2% 1 5% and/or transaction based pricing model.

• The SEG SaaS Index is currently comprised of 49 public pure-play SaaS companies*

EBITDA Margin 0.4% 0.5% -0.6% -1.2% -1.5%Net Income Margin -6.5% -8.6% -9.2% -9.3% -9.3%TTM Revenue Growth 33.0% 31.4% 32.1% 28.5% 28.2%TTM Total Revenue ($M) $112.0 $119.3 $126.5 $137.5 $153.1TTM EBITDA Growth 17.2% 13.1% 15.0% 17.4% 5.4%TTM Total EBITDA ($M) $1.1 -$0.2 -$1.8 -$2.6 -$2.7 companies .Cash & Eq ($M) $55.2 $59.9 $73.0 $82.7 $90.2Current Ratio 1.7 1.4 1.7 2.2 2.2Debt / Equity Ratio 7.0% 7.1% 10.3% 12.4% 23.7%

22 Q1 2014 Software Industry Financial ReportCopyright © 2014 by Software Equity Group, LLC

All Rights Reserved

* See appendix for a complete list of companies in the SEG SaaS Index

THE SEG SaaS INDEX: FINANCIAL PERFORMANCETTM Revenue Growth Rate Distribution – 1Q14Revenue Performance - Quarterly

28%34.0%$180

TTM Total Revenue ($M) TTM Revenue Growth

17%19% 19%

ompa

nies

29 0%

30.0%

31.0%

32.0%

33.0%

$80

$100

$120

$140

$160

nue

Gro

wth

al R

even

ue

2%

6%9%

% o

f Co

25 0%

26.0%

27.0%

28.0%

29.0%

$0

$20

$40

$60

$80

TTM

Rev

e

TTM

Tot

a

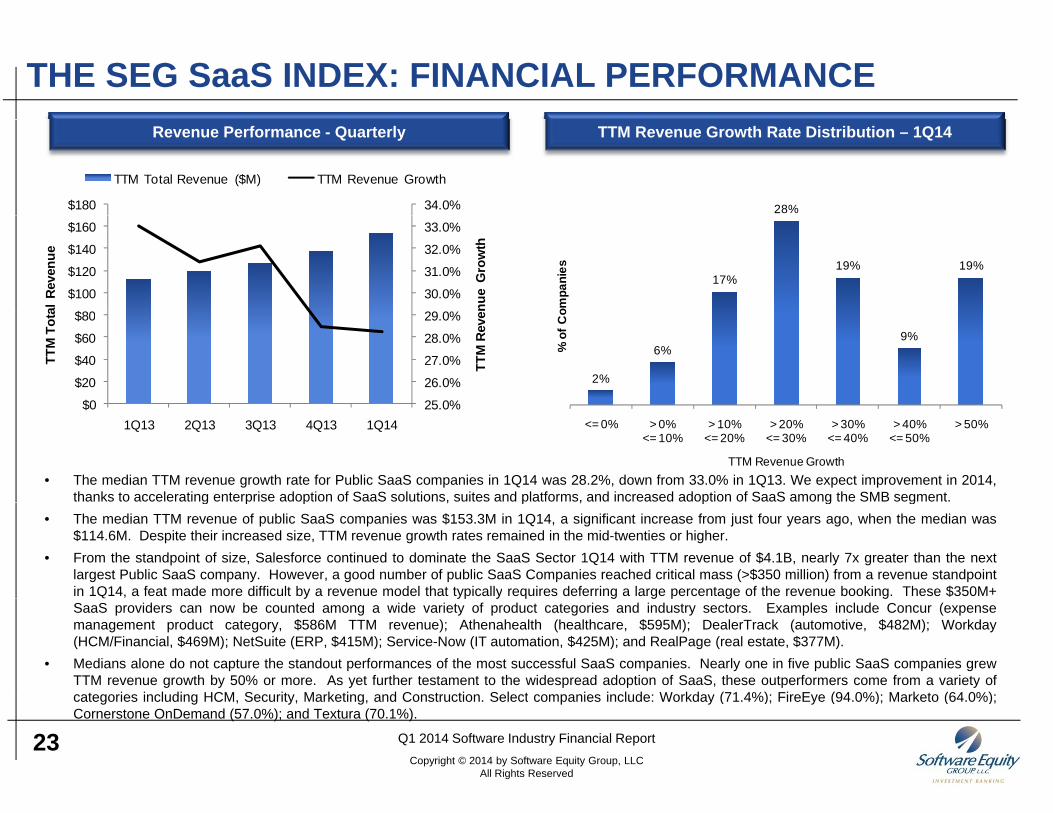

• The median TTM revenue growth rate for Public SaaS companies in 1Q14 was 28.2%, down from 33.0% in 1Q13. We expect improvement in 2014,thanks to accelerating enterprise adoption of SaaS solutions, suites and platforms, and increased adoption of SaaS among the SMB segment.

<= 0% > 0%<= 10%

> 10%<= 20%

> 20%<= 30%

> 30%<= 40%

> 40%<= 50%

> 50%

TTM Revenue Growth

25.0%$01Q13 2Q13 3Q13 4Q13 1Q14

g p p , p , p g g• The median TTM revenue of public SaaS companies was $153.3M in 1Q14, a significant increase from just four years ago, when the median was

$114.6M. Despite their increased size, TTM revenue growth rates remained in the mid-twenties or higher.• From the standpoint of size, Salesforce continued to dominate the SaaS Sector 1Q14 with TTM revenue of $4.1B, nearly 7x greater than the next

largest Public SaaS company. However, a good number of public SaaS Companies reached critical mass (>$350 million) from a revenue standpointin 1Q14, a feat made more difficult by a revenue model that typically requires deferring a large percentage of the revenue booking. These $350M+y yp y q g g p g gSaaS providers can now be counted among a wide variety of product categories and industry sectors. Examples include Concur (expensemanagement product category, $586M TTM revenue); Athenahealth (healthcare, $595M); DealerTrack (automotive, $482M); Workday(HCM/Financial, $469M); NetSuite (ERP, $415M); Service-Now (IT automation, $425M); and RealPage (real estate, $377M).

• Medians alone do not capture the standout performances of the most successful SaaS companies. Nearly one in five public SaaS companies grewTTM revenue growth by 50% or more. As yet further testament to the widespread adoption of SaaS, these outperformers come from a variety of

t i i l di HCM S it M k ti d C t ti S l t i i l d W kd (71 4%) Fi E (94 0%) M k t (64 0%)

23 Q1 2014 Software Industry Financial ReportCopyright © 2014 by Software Equity Group, LLC

All Rights Reserved

categories including HCM, Security, Marketing, and Construction. Select companies include: Workday (71.4%); FireEye (94.0%); Marketo (64.0%);Cornerstone OnDemand (57.0%); and Textura (70.1%).

THE SEG SaaS INDEX: FINANCIAL PERFORMANCETTM EBITDA Margin Distribution – 1Q14Median EBITDA Margin Performance - Quarterly

54%0.5% 54%

mpa

nies

0.4%0.5%

1Q13 2Q13 3Q13 4Q13 1Q14

A M

argi

n

21%

15%

4% 6%

% o

f Co

-0.6%

-1.2%1 5%

EBIT

DA

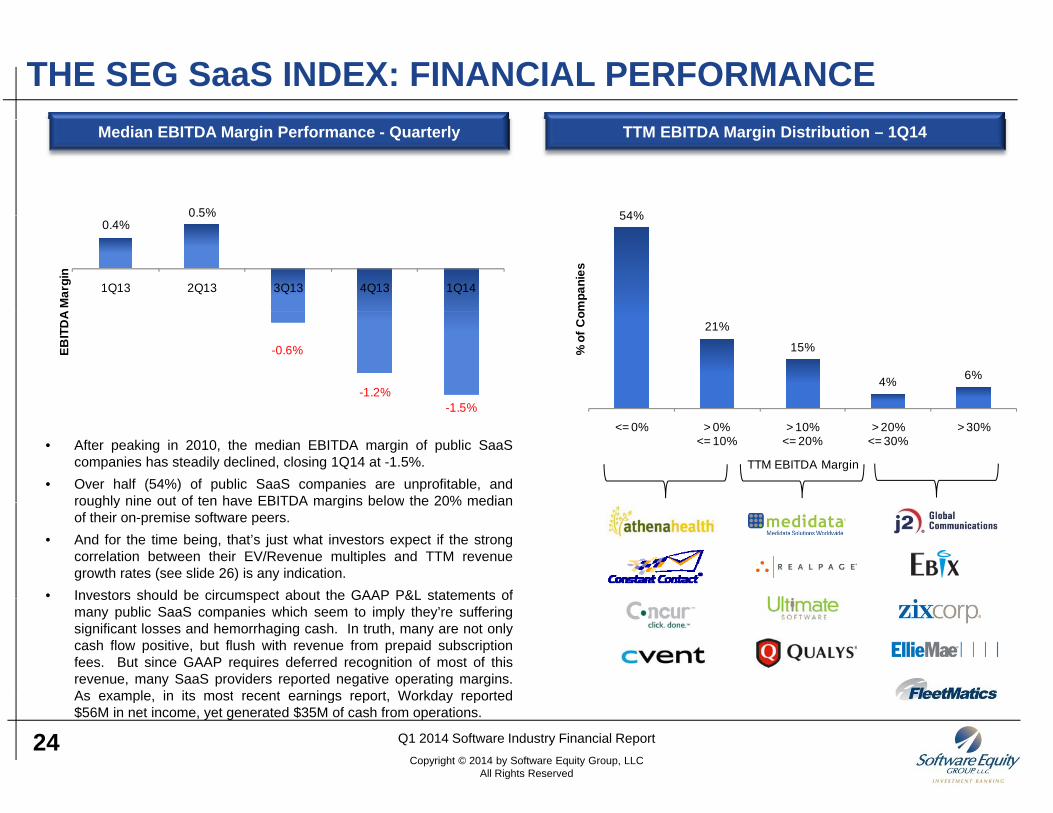

• After peaking in 2010, the median EBITDA margin of public SaaScompanies has steadily declined, closing 1Q14 at -1.5%.

• Over half (54%) of public SaaS companies are unprofitable, androughly nine out of ten have EBITDA margins below the 20% median

<= 0% > 0%<= 10%

> 10%<= 20%

> 20%<= 30%

> 30%

TTM EBITDA Margin

-1.5%

roughly nine out of ten have EBITDA margins below the 20% medianof their on-premise software peers.

• And for the time being, that’s just what investors expect if the strongcorrelation between their EV/Revenue multiples and TTM revenuegrowth rates (see slide 26) is any indication.

• Investors should be circumspect about the GAAP P&L statements ofInvestors should be circumspect about the GAAP P&L statements ofmany public SaaS companies which seem to imply they’re sufferingsignificant losses and hemorrhaging cash. In truth, many are not onlycash flow positive, but flush with revenue from prepaid subscriptionfees. But since GAAP requires deferred recognition of most of thisrevenue, many SaaS providers reported negative operating margins.As example in its most recent earnings report Workday reported

24 Q1 2014 Software Industry Financial ReportCopyright © 2014 by Software Equity Group, LLC

All Rights Reserved

As example, in its most recent earnings report, Workday reported$56M in net income, yet generated $35M of cash from operations.

THE SEG SaaS INDEX: MARKET MULTIPLESEV/Revenue Multiple Distribution – 1Q14Median EV/Revenue and EV/EBITDA Multiples - Quarterly

55.7x

EV/Revenue EV/EBITDA

33.6x30.2x

39.9x

46.8x 49%

ompa

nies

5.4x 5.7x 6.6x 7.6x 8.0x

0% 2%

9% 12%

2%7%

2%

12%

5%

% o

f Co

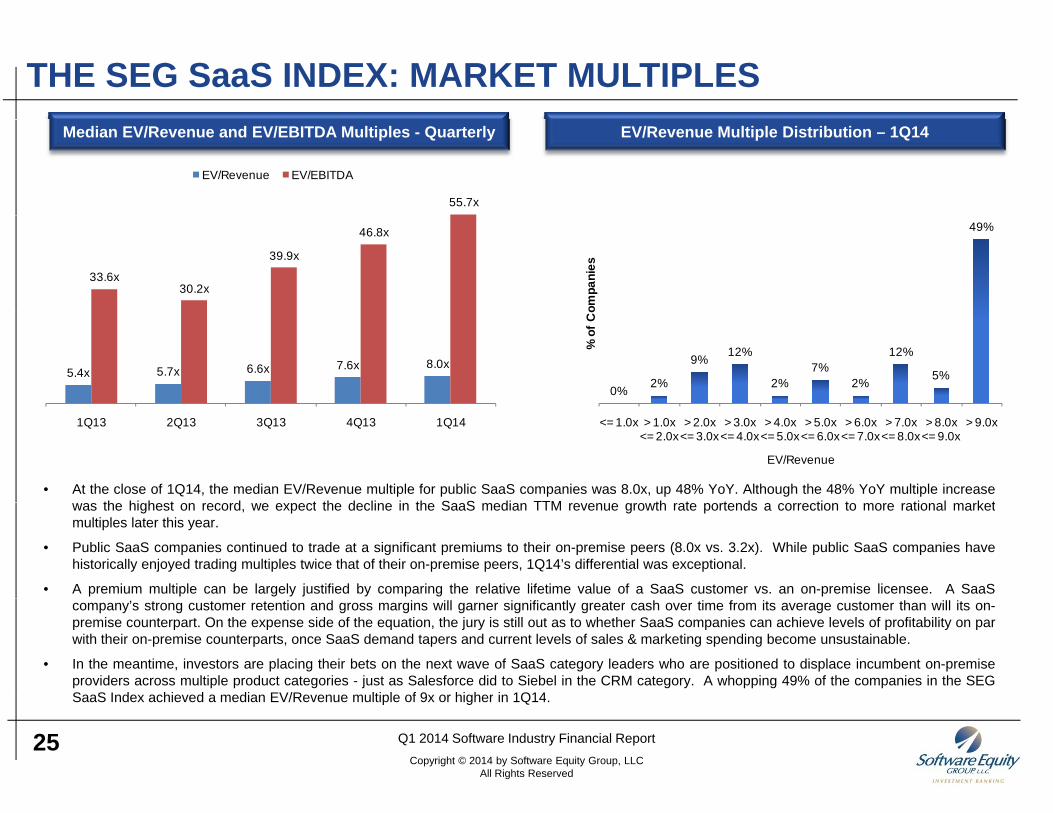

• At the close of 1Q14, the median EV/Revenue multiple for public SaaS companies was 8.0x, up 48% YoY. Although the 48% YoY multiple increaseth hi h t d t th d li i th S S di TTM th t t d ti t ti l k t

1Q13 2Q13 3Q13 4Q13 1Q14 <= 1.0x > 1.0x<= 2.0x

> 2.0x<= 3.0x

> 3.0x <= 4.0x

> 4.0x<= 5.0x

> 5.0x<= 6.0x

> 6.0x<= 7.0x

> 7.0x<= 8.0x

> 8.0x<= 9.0x

> 9.0x

EV/Revenue

was the highest on record, we expect the decline in the SaaS median TTM revenue growth rate portends a correction to more rational marketmultiples later this year.

• Public SaaS companies continued to trade at a significant premiums to their on-premise peers (8.0x vs. 3.2x). While public SaaS companies havehistorically enjoyed trading multiples twice that of their on-premise peers, 1Q14’s differential was exceptional.

• A premium multiple can be largely justified by comparing the relative lifetime value of a SaaS customer vs. an on-premise licensee. A SaaScompany’s strong customer retention and gross margins will garner significantly greater cash over time from its average customer than will its on-premise counterpart. On the expense side of the equation, the jury is still out as to whether SaaS companies can achieve levels of profitability on parwith their on-premise counterparts, once SaaS demand tapers and current levels of sales & marketing spending become unsustainable.

• In the meantime, investors are placing their bets on the next wave of SaaS category leaders who are positioned to displace incumbent on-premiseproviders across multiple product categories - just as Salesforce did to Siebel in the CRM category. A whopping 49% of the companies in the SEGS S I d hi d di EV/R lti l f 9 hi h i 1Q14

25 Q1 2014 Software Industry Financial ReportCopyright © 2014 by Software Equity Group, LLC

All Rights Reserved

SaaS Index achieved a median EV/Revenue multiple of 9x or higher in 1Q14.

THE SEG SaaS INDEX: MARKET MULTIPLESEV/Revenue Multiples vs. TTM EBITDA Margins – 1Q14EV/Revenue Multiples vs. TTM Revenue Growth Rates – 1Q14

19.1x

EV/Reven

ue

9.6x

6.3x7.2x

6.3x

EV/R

even

ue

0.0x2.5x

4.7x 5.4x

9.2x7.0x

Med

ian E 4.3x

Med

ian

E

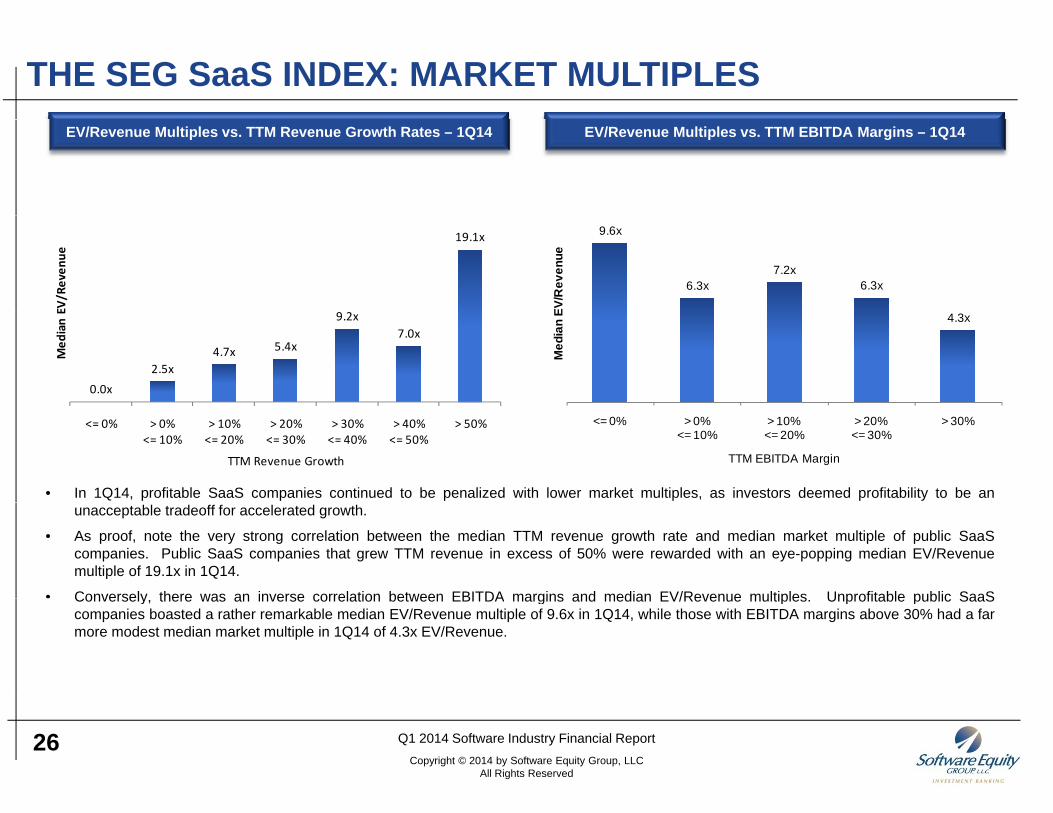

• In 1Q14, profitable SaaS companies continued to be penalized with lower market multiples, as investors deemed profitability to be an

<= 0% > 0%<= 10%

> 10%<= 20%

> 20%<= 30%

> 30%<= 40%

> 40%<= 50%

> 50%

TTM Revenue Growth

<= 0% > 0%<= 10%

> 10%<= 20%

> 20%<= 30%

> 30%

TTM EBITDA Margin

unacceptable tradeoff for accelerated growth.

• As proof, note the very strong correlation between the median TTM revenue growth rate and median market multiple of public SaaScompanies. Public SaaS companies that grew TTM revenue in excess of 50% were rewarded with an eye-popping median EV/Revenuemultiple of 19.1x in 1Q14.

• Conversely there was an inverse correlation between EBITDA margins and median EV/Revenue multiples Unprofitable public SaaSConversely, there was an inverse correlation between EBITDA margins and median EV/Revenue multiples. Unprofitable public SaaScompanies boasted a rather remarkable median EV/Revenue multiple of 9.6x in 1Q14, while those with EBITDA margins above 30% had a farmore modest median market multiple in 1Q14 of 4.3x EV/Revenue.

26 Q1 2014 Software Industry Financial ReportCopyright © 2014 by Software Equity Group, LLC

All Rights Reserved

TTM

THE SEG SaaS INDEX: MARKET MULTIPLESCompany Ticker EV (Median)

TTM Revenue

Revenue Growth

EV/Revenue

TTM EBITDA

EBITDA Margin

EV/EBITDA

Castlight Health, Inc. CSLT $2,386 $13 212% 183.9x -$62 -475.6% -FireEye, Inc. FEYE $8,974 $162 94% 55.6x -$143 -88.4% -Workday, Inc. WDAY $15,928 $469 71% 34.0x -$119 -25.3% -Demandware, Inc. DWRE $2,247 $104 31% 21.7x -$16 -15.6% -Service-now.com NOW $8,644 $425 74% 20.4x -$43 -10.1% -Netsuite N $7,723 $415 34% 18.6x -$37 -8.9% -V S t I VEEV $3 754 $210 62% 17 9 $41 19 4% 92 3Veeva Systems Inc. VEEV $3,754 $210 62% 17.9x $41 19.4% 92.3xCornerstone OnDemand CSOD $2,892 $185 57% 15.6x -$30 -16.1% -Marketo MKTO $1,457 $96 64% 15.2x -$41 -42.4% -Textura Corp. TXTR $610 $41 70% 15.0x -$33 -81.5% -Benefitfocus, Inc. BNFT $1,507 $105 28% 14.4x -$23 -21.7% -ChannelAdvisors ECOM $913 $68 27% 13.4x -$11 -15.8% -OPOWER, Inc. OPWR n/a $89 71% 13.2x -$12 -13.1% -Paylocity Holding Corp. PCTY $1,175 $91 - 13.0x $2 2.2% 602.0xCvent NYSE:CV $1 374 $111 33% 12 4x $2 1 9% 663 9x Top 25%

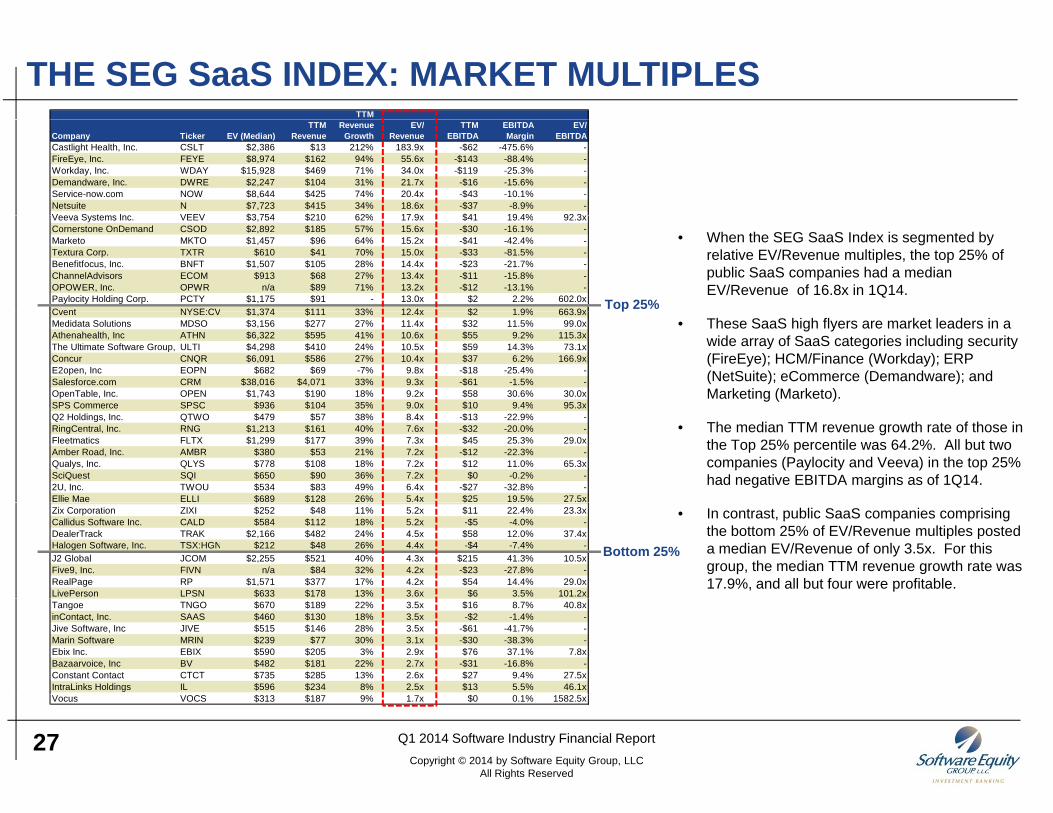

• When the SEG SaaS Index is segmented by relative EV/Revenue multiples, the top 25% of public SaaS companies had a median EV/Revenue of 16.8x in 1Q14.

Cvent NYSE:CV $1,374 $111 33% 12.4x $2 1.9% 663.9xMedidata Solutions MDSO $3,156 $277 27% 11.4x $32 11.5% 99.0xAthenahealth, Inc ATHN $6,322 $595 41% 10.6x $55 9.2% 115.3xThe Ultimate Software Group, ULTI $4,298 $410 24% 10.5x $59 14.3% 73.1xConcur CNQR $6,091 $586 27% 10.4x $37 6.2% 166.9xE2open, Inc EOPN $682 $69 -7% 9.8x -$18 -25.4% -Salesforce.com CRM $38,016 $4,071 33% 9.3x -$61 -1.5% -OpenTable, Inc. OPEN $1,743 $190 18% 9.2x $58 30.6% 30.0xSPS Commerce SPSC $936 $104 35% 9 0x $10 9 4% 95 3x

p• These SaaS high flyers are market leaders in a

wide array of SaaS categories including security (FireEye); HCM/Finance (Workday); ERP (NetSuite); eCommerce (Demandware); and Marketing (Marketo).

SPS Commerce SPSC $936 $104 35% 9.0x $10 9.4% 95.3xQ2 Holdings, Inc. QTWO $479 $57 38% 8.4x -$13 -22.9% -RingCentral, Inc. RNG $1,213 $161 40% 7.6x -$32 -20.0% -Fleetmatics FLTX $1,299 $177 39% 7.3x $45 25.3% 29.0xAmber Road, Inc. AMBR $380 $53 21% 7.2x -$12 -22.3% -Qualys, Inc. QLYS $778 $108 18% 7.2x $12 11.0% 65.3xSciQuest SQI $650 $90 36% 7.2x $0 -0.2% -2U, Inc. TWOU $534 $83 49% 6.4x -$27 -32.8% -Ellie Mae ELLI $689 $128 26% 5.4x $25 19.5% 27.5x

• The median TTM revenue growth rate of those in the Top 25% percentile was 64.2%. All but two companies (Paylocity and Veeva) in the top 25% had negative EBITDA margins as of 1Q14.

$ $ $Zix Corporation ZIXI $252 $48 11% 5.2x $11 22.4% 23.3xCallidus Software Inc. CALD $584 $112 18% 5.2x -$5 -4.0% -DealerTrack TRAK $2,166 $482 24% 4.5x $58 12.0% 37.4xHalogen Software, Inc. TSX:HGN $212 $48 26% 4.4x -$4 -7.4% -J2 Global JCOM $2,255 $521 40% 4.3x $215 41.3% 10.5xFive9, Inc. FIVN n/a $84 32% 4.2x -$23 -27.8% -RealPage RP $1,571 $377 17% 4.2x $54 14.4% 29.0xLivePerson LPSN $633 $178 13% 3.6x $6 3.5% 101.2x

Bottom 25%

• In contrast, public SaaS companies comprising the bottom 25% of EV/Revenue multiples posted a median EV/Revenue of only 3.5x. For this group, the median TTM revenue growth rate was 17.9%, and all but four were profitable.

Tangoe TNGO $670 $189 22% 3.5x $16 8.7% 40.8xinContact, Inc. SAAS $460 $130 18% 3.5x -$2 -1.4% -Jive Software, Inc JIVE $515 $146 28% 3.5x -$61 -41.7% -Marin Software MRIN $239 $77 30% 3.1x -$30 -38.3% -Ebix Inc. EBIX $590 $205 3% 2.9x $76 37.1% 7.8xBazaarvoice, Inc BV $482 $181 22% 2.7x -$31 -16.8% -Constant Contact CTCT $735 $285 13% 2.6x $27 9.4% 27.5xIntraLinks Holdings IL $596 $234 8% 2.5x $13 5.5% 46.1x

27 Q1 2014 Software Industry Financial ReportCopyright © 2014 by Software Equity Group, LLC

All Rights Reserved

Vocus VOCS $313 $187 9% 1.7x $0 0.1% 1582.5x

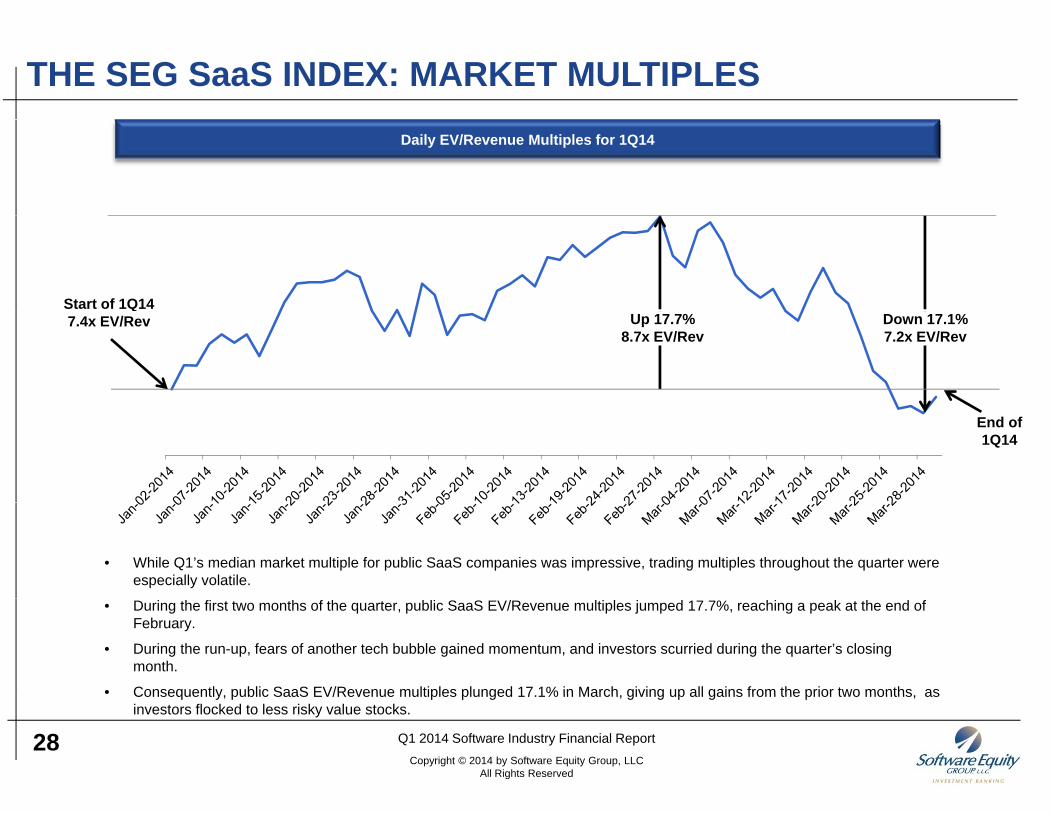

THE SEG SaaS INDEX: MARKET MULTIPLESDaily EV/Revenue Multiples for 1Q14

Start of 1Q14Up 17.7%

8.7x EV/RevDown 17.1%7.2x EV/Rev

7.4x EV/Rev

End of 1Q14

• While Q1’s median market multiple for public SaaS companies was impressive, trading multiples throughout the quarter were especially volatile.

• During the first two months of the quarter, public SaaS EV/Revenue multiples jumped 17.7%, reaching a peak at the end of February.

• During the run-up, fears of another tech bubble gained momentum, and investors scurried during the quarter’s closing month.

• Consequently public SaaS EV/Revenue multiples plunged 17 1% in March giving up all gains from the prior two months as

28 Q1 2014 Software Industry Financial ReportCopyright © 2014 by Software Equity Group, LLC

All Rights Reserved

Consequently, public SaaS EV/Revenue multiples plunged 17.1% in March, giving up all gains from the prior two months, as investors flocked to less risky value stocks.

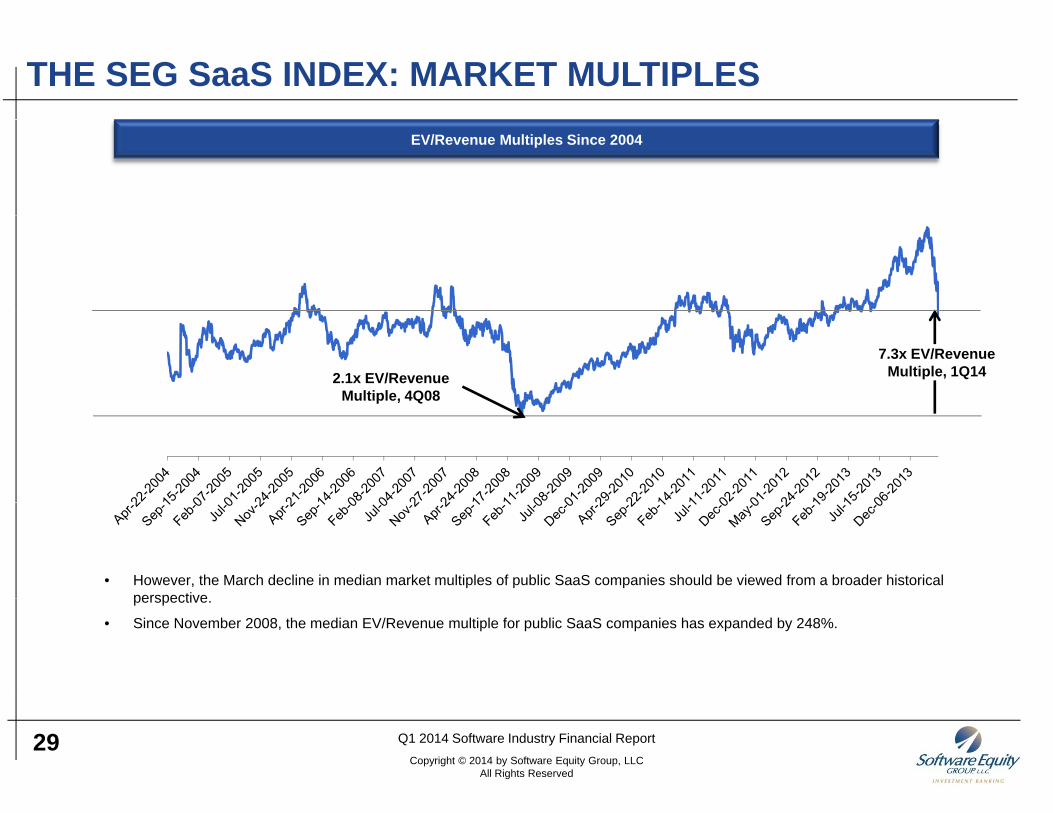

THE SEG SaaS INDEX: MARKET MULTIPLESEV/Revenue Multiples Since 2004

7.3x EV/Revenue Multiple, 1Q142.1x EV/Revenue

Multiple, 4Q08

• However, the March decline in median market multiples of public SaaS companies should be viewed from a broader historical perspectiveperspective.

• Since November 2008, the median EV/Revenue multiple for public SaaS companies has expanded by 248%.

29 Q1 2014 Software Industry Financial ReportCopyright © 2014 by Software Equity Group, LLC

All Rights Reserved

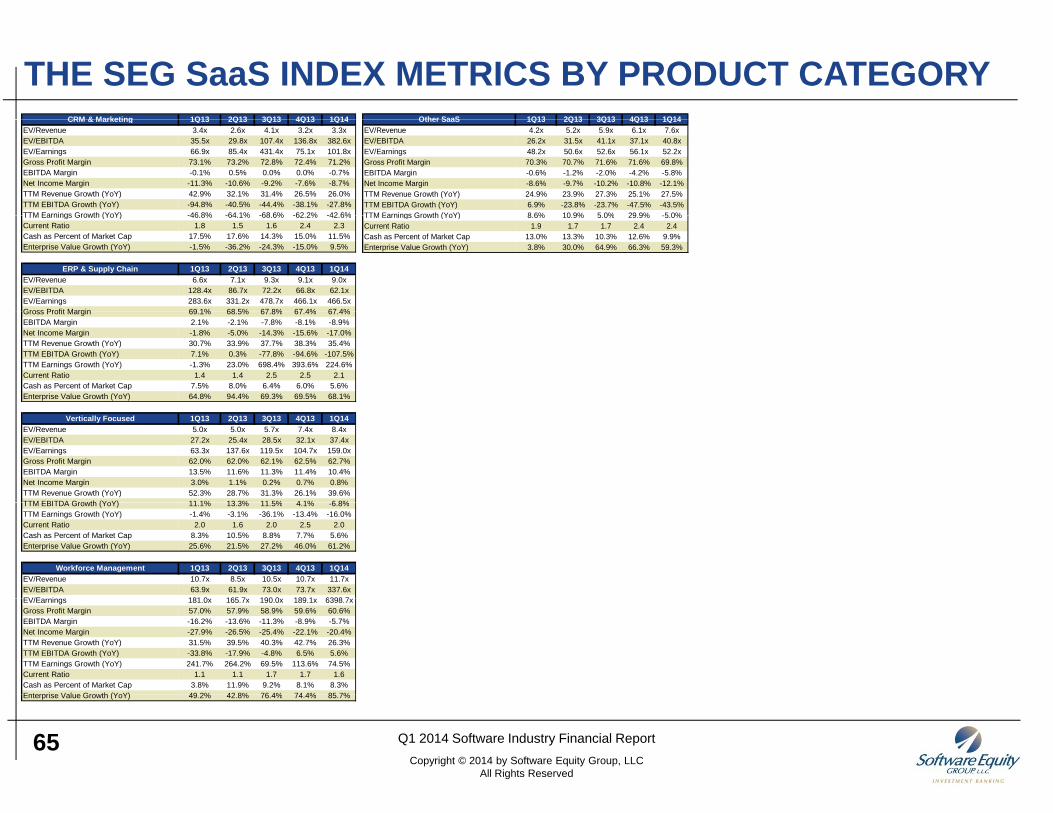

THE SEG SaaS INDEX BY PRODUCT CATEGORY• The SEG SaaS Index is currently comprised of 49 publicly listed SaaS companies.

Four distinct SaaS product categories had a sufficient number for us to analyzetrends and compare results.

• Representative companies for each SaaS categories are referenced below. Thecomplete list of companies, as well as detailed financial data about each, can befound in the Appendix.

CRM & Marketing ERP & Supply Chain Vertically Focused Workforce ManagementCRM & Marketing ERP & Supply Chain Vertically Focused Workforce Management

30 Q1 2014 Software Industry Financial ReportCopyright © 2014 by Software Equity Group, LLC

All Rights Reserved

THE SEG SaaS INDEX BY PRODUCT CATEGORY• In addition to these four SaaS product categories, there are a number of emerging

SaaS product categories that currently lack sufficient number to yield reliable trenddata, but nevertheless demonstrate continued adoption of SaaS across verticalmarkets and traditionally on premise product categoriesmarkets and traditionally on-premise product categories.

eCommerce Healthcare Real Estate SecurityLife Sciences

31 Q1 2014 Software Industry Financial ReportCopyright © 2014 by Software Equity Group, LLC

All Rights Reserved

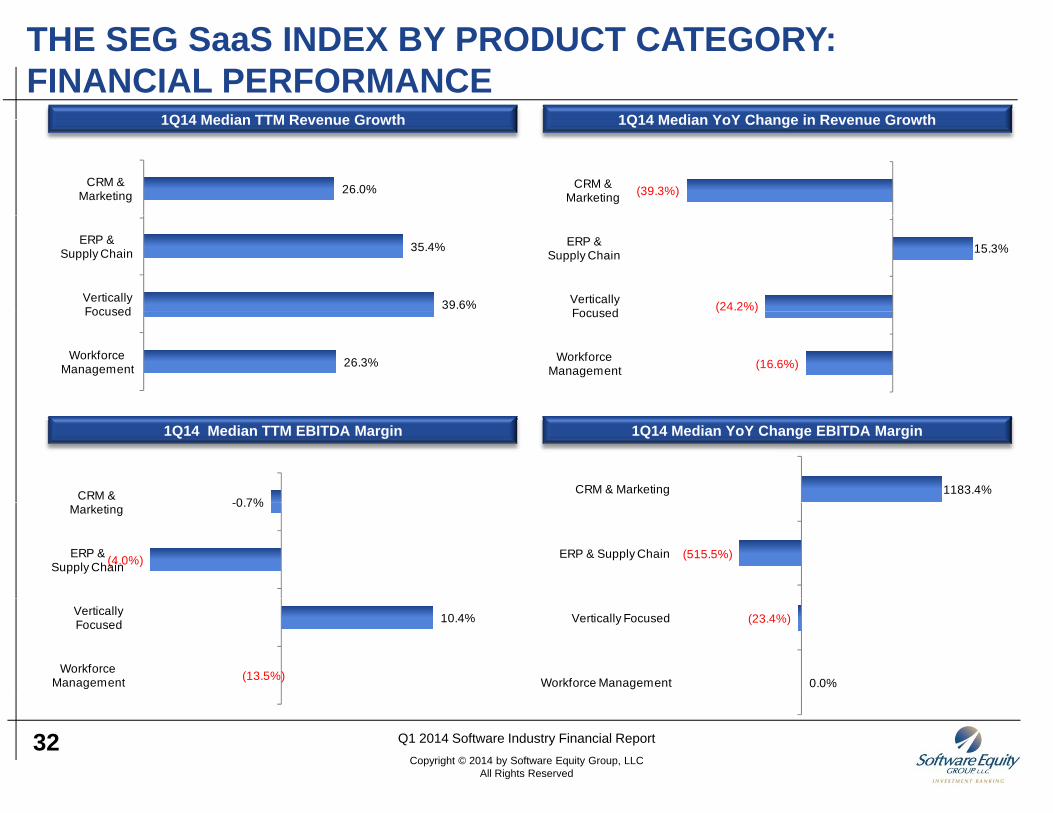

THE SEG SaaS INDEX BY PRODUCT CATEGORY: FINANCIAL PERFORMANCE

1Q14 Median YoY Change in Revenue Growth1Q14 Median TTM Revenue Growth 1Q14 Median YoY Change in Revenue Growth1Q14 Median TTM Revenue Growth

26.0%CRM &Marketing (39.3%)CRM &

Marketing

35.4%

39.6%

ERP &Supply Chain

VerticallyFocused

15.3%

(24.2%)

ERP &Supply Chain

VerticallyFocused

26.3%

Focused

WorkforceManagement

( )

(16.6%)

Focused

WorkforceManagement

1Q14 Median YoY Change EBITDA Margin1Q14 Median TTM EBITDA Margin

0 7%CRM & 1183.4% CRM & Marketing-0.7%

(4.0%)

Marketing

ERP &Supply Chain

(515.5%)ERP & Supply Chain

10.4%

(13.5%)

VerticallyFocused

WorkforceManagement

(23.4%)

0.0%

Vertically Focused

Workforce Management

32 Q1 2014 Software Industry Financial ReportCopyright © 2014 by Software Equity Group, LLC

All Rights Reserved

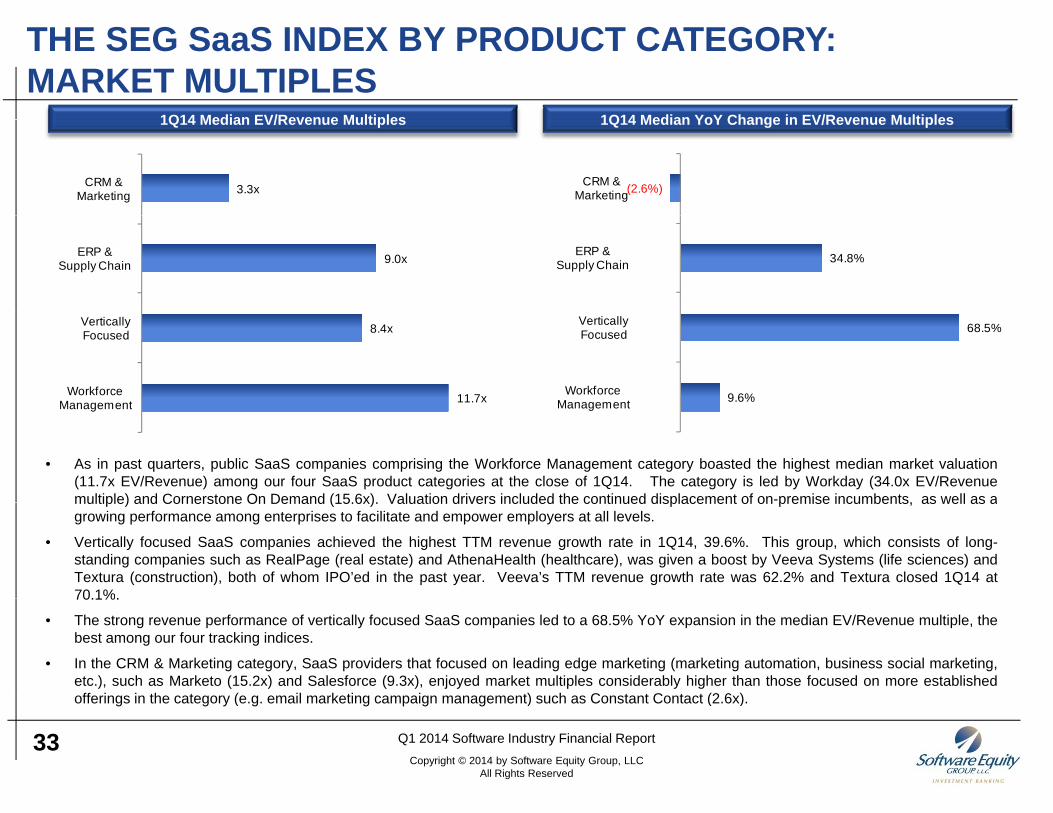

THE SEG SaaS INDEX BY PRODUCT CATEGORY: MARKET MULTIPLES

1Q14 Median YoY Change in EV/Revenue Multiples1Q14 Median EV/Revenue Multiples 1Q14 Median YoY Change in EV/Revenue Multiples1Q14 Median EV/Revenue Multiples

3.3xCRM &Marketing (2.6%)CRM &

Marketing

9.0xERP &Supply Chain 34.8% ERP &

Supply Chain

8.4x

11.7x

VerticallyFocused

WorkforceManagement

68.5%

9.6%

VerticallyFocused

WorkforceManagement

• As in past quarters, public SaaS companies comprising the Workforce Management category boasted the highest median market valuation(11.7x EV/Revenue) among our four SaaS product categories at the close of 1Q14. The category is led by Workday (34.0x EV/Revenuemultiple) and Cornerstone On Demand (15.6x). Valuation drivers included the continued displacement of on-premise incumbents, as well as a

Management Management

multiple) and Cornerstone On Demand (15.6x). Valuation drivers included the continued displacement of on premise incumbents, as well as agrowing performance among enterprises to facilitate and empower employers at all levels.

• Vertically focused SaaS companies achieved the highest TTM revenue growth rate in 1Q14, 39.6%. This group, which consists of long-standing companies such as RealPage (real estate) and AthenaHealth (healthcare), was given a boost by Veeva Systems (life sciences) andTextura (construction), both of whom IPO’ed in the past year. Veeva’s TTM revenue growth rate was 62.2% and Textura closed 1Q14 at70.1%.70.1%.

• The strong revenue performance of vertically focused SaaS companies led to a 68.5% YoY expansion in the median EV/Revenue multiple, thebest among our four tracking indices.

• In the CRM & Marketing category, SaaS providers that focused on leading edge marketing (marketing automation, business social marketing,etc.), such as Marketo (15.2x) and Salesforce (9.3x), enjoyed market multiples considerably higher than those focused on more established

ff i i th t ( il k ti i t) h C t t C t t (2 6 )

33 Q1 2014 Software Industry Financial ReportCopyright © 2014 by Software Equity Group, LLC

All Rights Reserved

offerings in the category (e.g. email marketing campaign management) such as Constant Contact (2.6x).

THE SEG INTERNET INDEX

PUBLIC INTERNET COMPANY FINANCIAL ANDPUBLIC INTERNET COMPANY FINANCIAL AND VALUATION PERFORMANCE

34

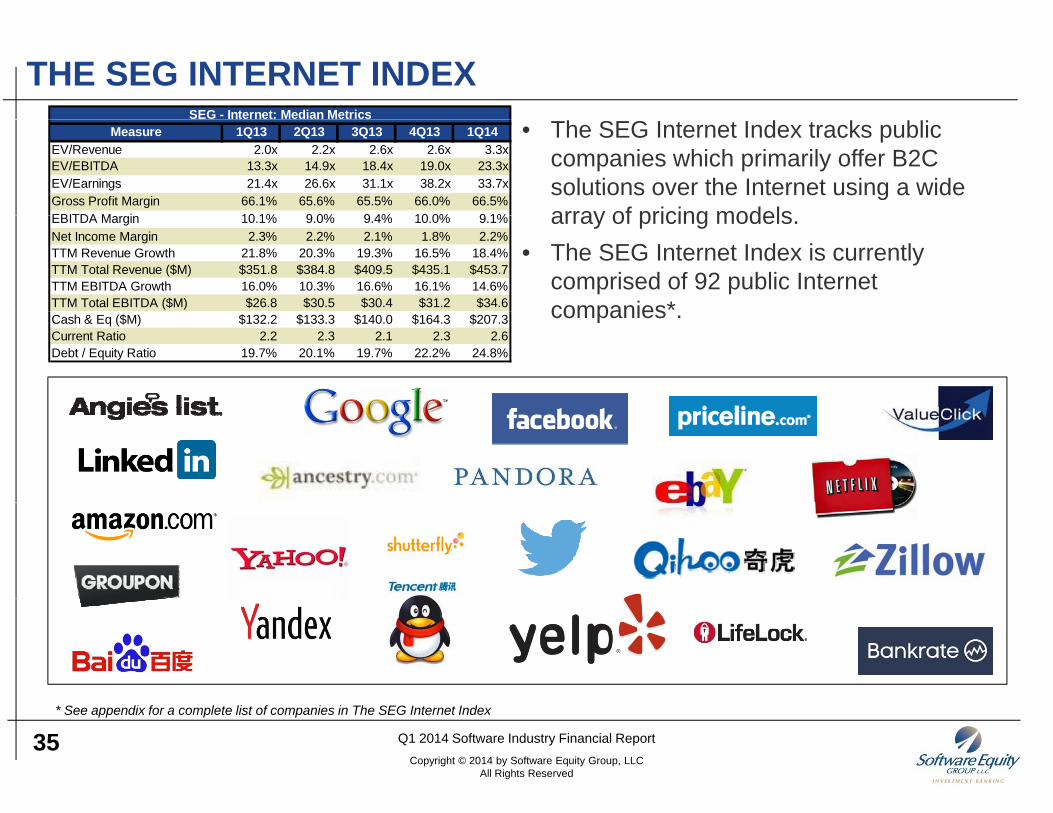

THE SEG INTERNET INDEXSEG - Internet: Median Metrics

• The SEG Internet Index tracks public companies which primarily offer B2C solutions over the Internet using a wide array of pricing models

Measure 1Q13 2Q13 3Q13 4Q13 1Q14EV/Revenue 2.0x 2.2x 2.6x 2.6x 3.3xEV/EBITDA 13.3x 14.9x 18.4x 19.0x 23.3xEV/Earnings 21.4x 26.6x 31.1x 38.2x 33.7xGross Profit Margin 66.1% 65.6% 65.5% 66.0% 66.5%EBITDA M i 10 1% 9 0% 9 4% 10 0% 9 1% array of pricing models.

• The SEG Internet Index is currently comprised of 92 public Internet companies*

EBITDA Margin 10.1% 9.0% 9.4% 10.0% 9.1%Net Income Margin 2.3% 2.2% 2.1% 1.8% 2.2%TTM Revenue Growth 21.8% 20.3% 19.3% 16.5% 18.4%TTM Total Revenue ($M) $351.8 $384.8 $409.5 $435.1 $453.7TTM EBITDA Growth 16.0% 10.3% 16.6% 16.1% 14.6%TTM Total EBITDA ($M) $26.8 $30.5 $30.4 $31.2 $34.6 companies .Cash & Eq ($M) $132.2 $133.3 $140.0 $164.3 $207.3Current Ratio 2.2 2.3 2.1 2.3 2.6Debt / Equity Ratio 19.7% 20.1% 19.7% 22.2% 24.8%

35 Q1 2014 Software Industry Financial ReportCopyright © 2014 by Software Equity Group, LLC

All Rights Reserved

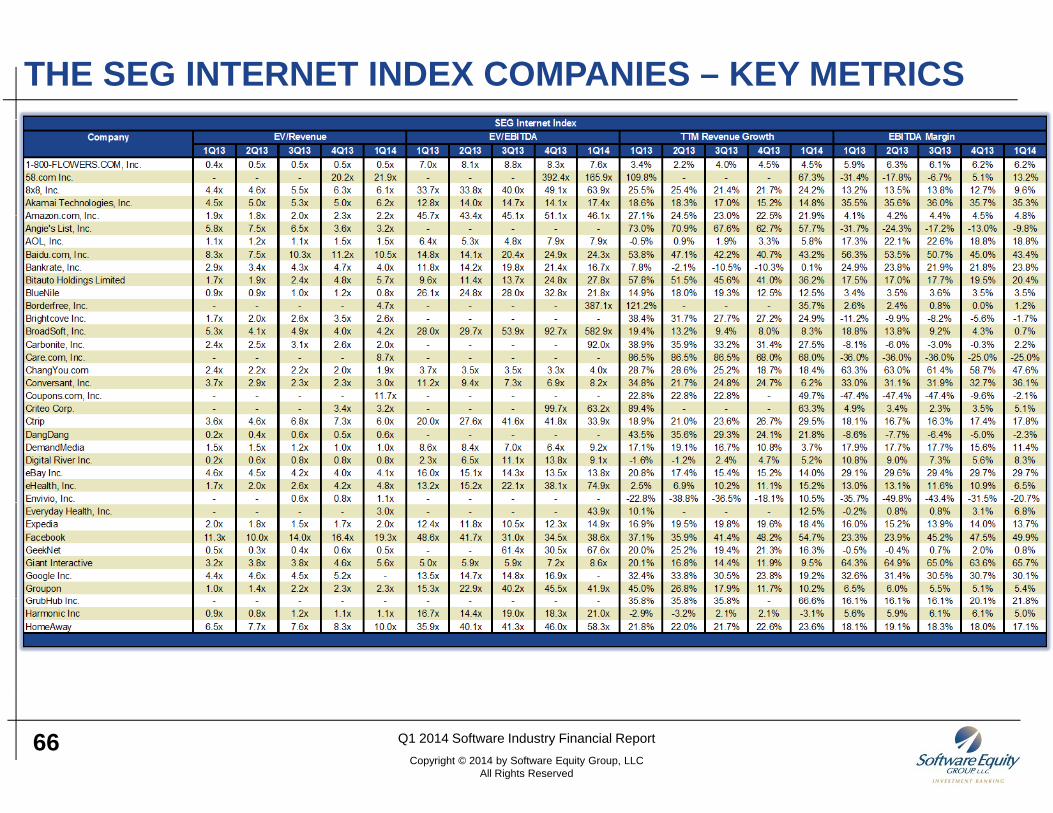

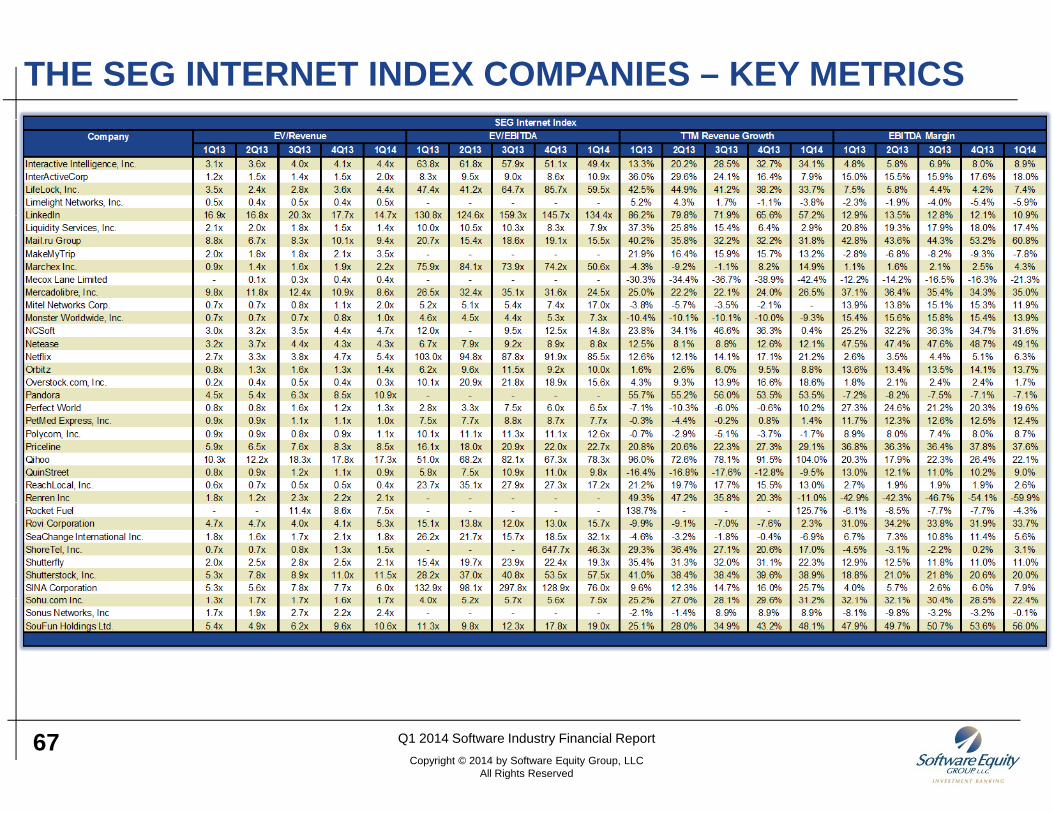

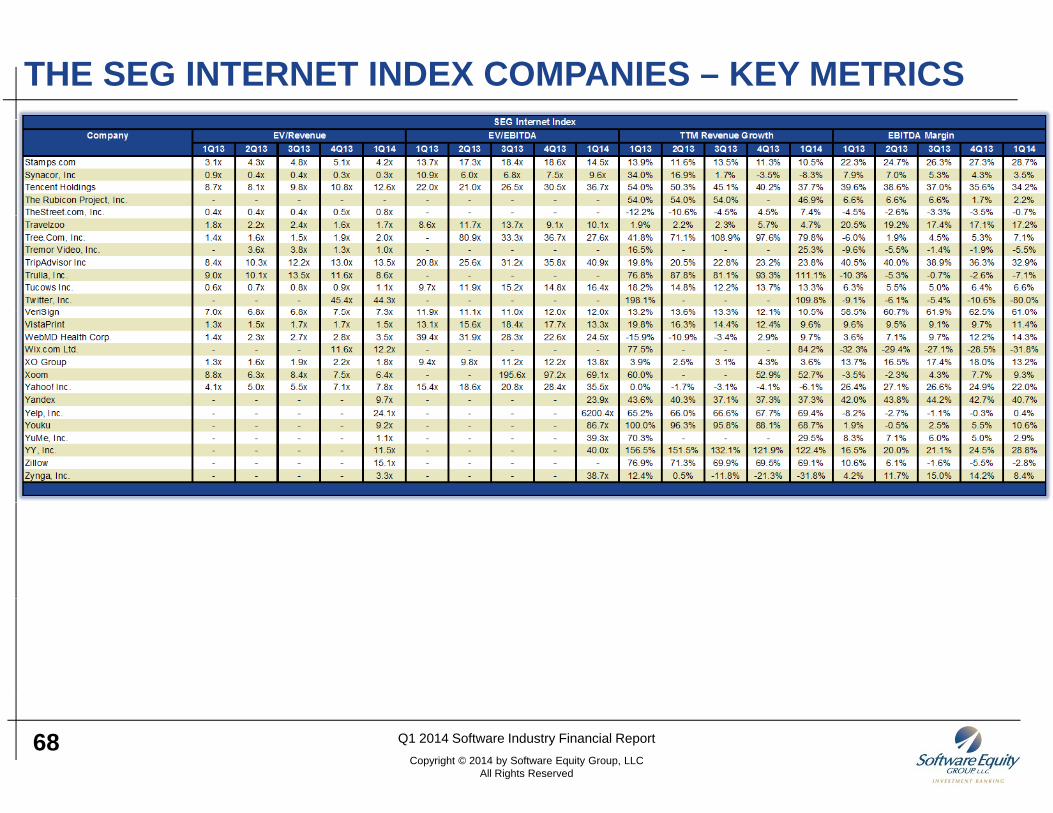

* See appendix for a complete list of companies in The SEG Internet Index

THE SEG INTERNET INDEX: FINANCIAL PERFORMANCETTM Revenue Growth Rate Distribution – 1Q14Median Revenue Performance - Quarterly

25.0%$500

TTM Total Revenue ($M) TTM Revenue Growth

23%

15.0%

20.0%

$250

$300

$350

$400

$450

nue

Gro

wth

al R

even

ue

11%

20%21%

15%

ompa

nies

0 0%

5.0%

10.0%

$0

$50

$100

$150

$200

TTM

Rev

e

TTM

Tot

a

9%

% o

f Co

• Approximately 62% of the companies comprising the SEG InternetIndex offer online services and solutions that are consumer targeted;their revenue growth closely parallels the performance of the U.S.economy

0.0%$01Q13 2Q13 3Q13 4Q13 1Q14 <= 0% > 0%

<= 10%> 10%

<= 20%> 20%

<= 30%> 30%

<= 40%> 40%

TTM Revenue Growth

economy.• After a sequential drop in each of the last six quarters, median TTM

revenue growth of the SEG Internet Index improved in 1Q14, edging upto 18.4% from 16.5% in 4Q13.

• Once again demonstrating the Internet is an ecosystem of unequals,one in four public Internet providers far outpaced the pack touting TTMone in four public Internet providers far outpaced the pack, touting TTMrevenue growth greater than 40% in 1Q14.

• Many of these high flyers were recent IPOs whose innovative productsservices and business models allowed them to scale quickly. Selectexamples included: Trulia (111%), Facebook (55%), and Yelp (69%)

• Conversely 31% of public Internet companies struggled to advance

36 Q1 2014 Software Industry Financial ReportCopyright © 2014 by Software Equity Group, LLC

All Rights Reserved

• Conversely, 31% of public Internet companies struggled to advance,reporting TTM revenue growth of 10% or less.

THE SEG INTERNET INDEX: FINANCIAL PERFORMANCETTM EBITDA Margin Distribution – 1Q14Median EBITDA Margin Performance – Quarterly

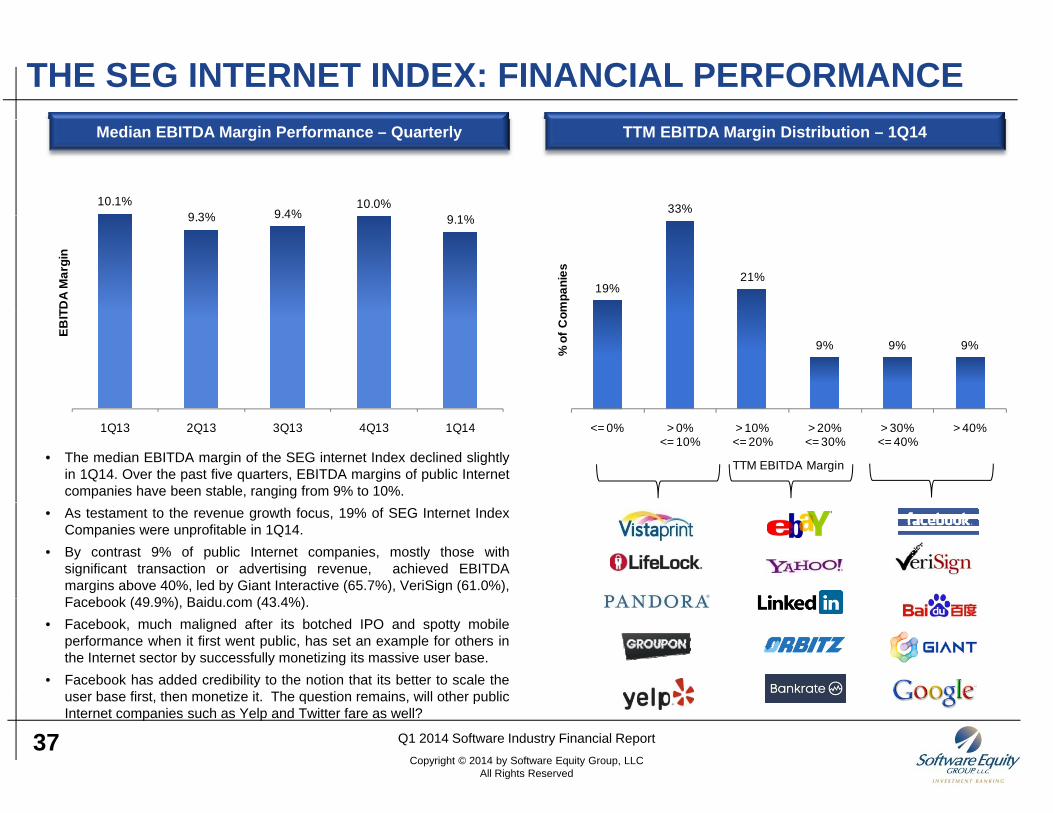

33%10.1%9 3% 9 4%

10.0%9 1%

19%21%

mpa

nies

9.3% 9.4% 9.1%

TDA

Mar

gin

9% 9% 9%% o

f Com

EBIT

• The median EBITDA margin of the SEG internet Index declined slightlyin 1Q14. Over the past five quarters, EBITDA margins of public Internetcompanies have been stable, ranging from 9% to 10%.

<= 0% > 0%<= 10%

> 10%<= 20%

> 20%<= 30%

> 30%<= 40%

> 40%

TTM EBITDA Margin

1Q13 2Q13 3Q13 4Q13 1Q14

• As testament to the revenue growth focus, 19% of SEG Internet IndexCompanies were unprofitable in 1Q14.

• By contrast 9% of public Internet companies, mostly those withsignificant transaction or advertising revenue, achieved EBITDAmargins above 40%, led by Giant Interactive (65.7%), VeriSign (61.0%),F b k (49 9%) B id (43 4%)Facebook (49.9%), Baidu.com (43.4%).

• Facebook, much maligned after its botched IPO and spotty mobileperformance when it first went public, has set an example for others inthe Internet sector by successfully monetizing its massive user base.

• Facebook has added credibility to the notion that its better to scale theuser base first then monetize it The question remains will other public

37 Q1 2014 Software Industry Financial ReportCopyright © 2014 by Software Equity Group, LLC

All Rights Reserved

user base first, then monetize it. The question remains, will other publicInternet companies such as Yelp and Twitter fare as well?

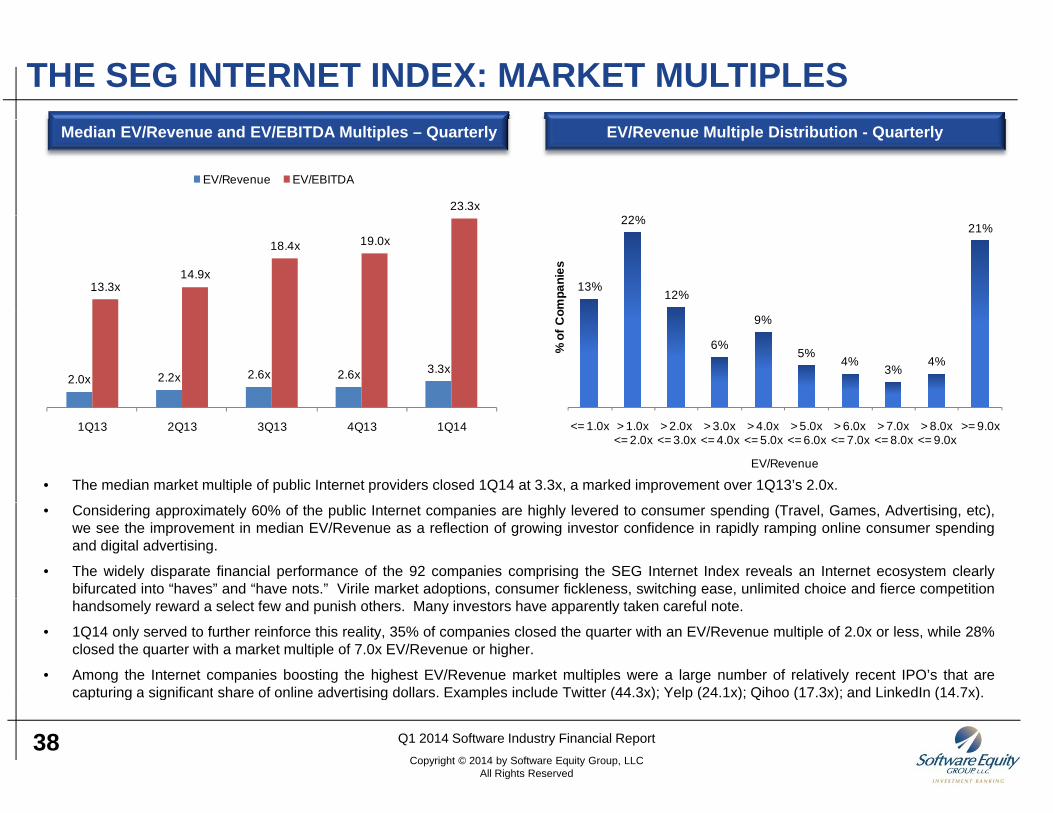

THE SEG INTERNET INDEX: MARKET MULTIPLESEV/Revenue Multiple Distribution - QuarterlyMedian EV/Revenue and EV/EBITDA Multiples – Quarterly

23.3x

EV/Revenue EV/EBITDA

%

13.3x14.9x

18.4x 19.0x

13%

22%

12%

21%

ompa

nies

2.0x 2.2x 2.6x 2.6x 3.3x

6%

9%

5%4%

3%4%

% o

f Co

• The median market multiple of public Internet providers closed 1Q14 at 3.3x, a marked improvement over 1Q13’s 2.0x.

1Q13 2Q13 3Q13 4Q13 1Q14 <= 1.0x > 1.0x<= 2.0x

> 2.0x<= 3.0x

> 3.0x <= 4.0x

> 4.0x<= 5.0x

> 5.0x<= 6.0x

> 6.0x<= 7.0x

> 7.0x<= 8.0x

> 8.0x<= 9.0x

>= 9.0x

EV/Revenue

• Considering approximately 60% of the public Internet companies are highly levered to consumer spending (Travel, Games, Advertising, etc),we see the improvement in median EV/Revenue as a reflection of growing investor confidence in rapidly ramping online consumer spendingand digital advertising.

• The widely disparate financial performance of the 92 companies comprising the SEG Internet Index reveals an Internet ecosystem clearlybifurcated into “haves” and “have nots.” Virile market adoptions, consumer fickleness, switching ease, unlimited choice and fierce competitionhandsomely reward a select few and punish others. Many investors have apparently taken careful note.

• 1Q14 only served to further reinforce this reality, 35% of companies closed the quarter with an EV/Revenue multiple of 2.0x or less, while 28%closed the quarter with a market multiple of 7.0x EV/Revenue or higher.

• Among the Internet companies boosting the highest EV/Revenue market multiples were a large number of relatively recent IPO’s that arecapturing a significant share of online advertising dollars Examples include Twitter (44 3x); Yelp (24 1x); Qihoo (17 3x); and LinkedIn (14 7x)

38 Q1 2014 Software Industry Financial ReportCopyright © 2014 by Software Equity Group, LLC

All Rights Reserved

capturing a significant share of online advertising dollars. Examples include Twitter (44.3x); Yelp (24.1x); Qihoo (17.3x); and LinkedIn (14.7x).

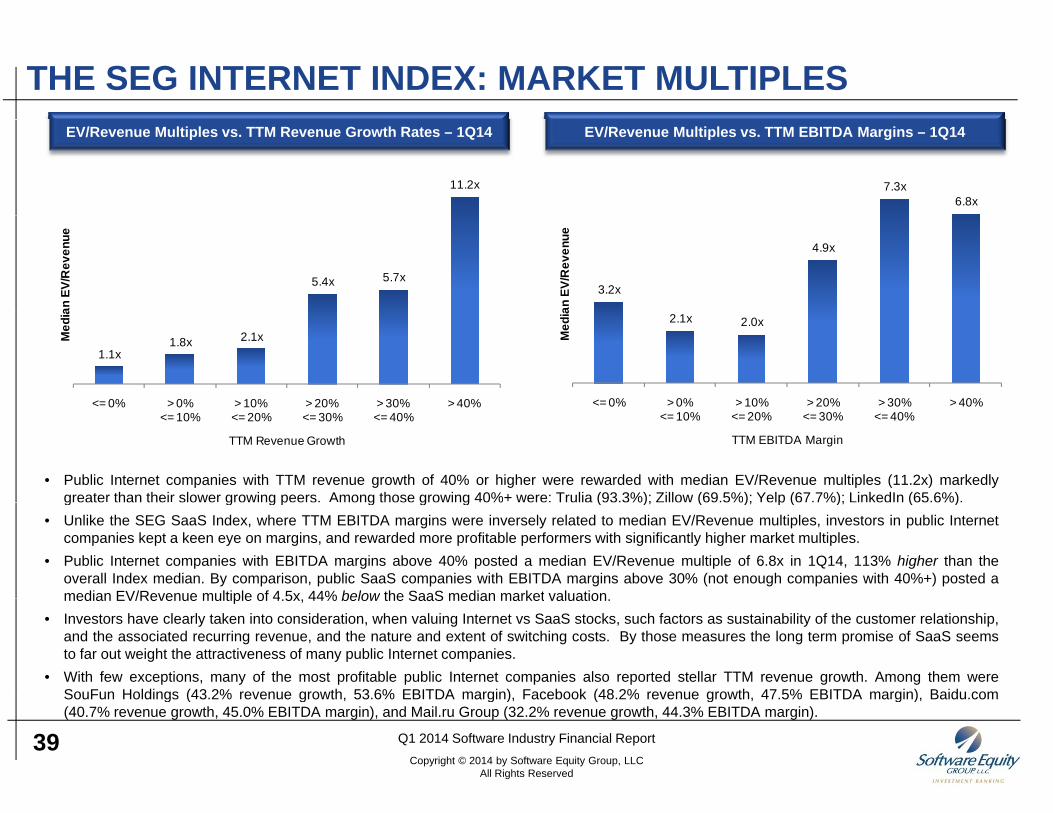

THE SEG INTERNET INDEX: MARKET MULTIPLESEV/Revenue Multiples vs. TTM EBITDA Margins – 1Q14EV/Revenue Multiples vs. TTM Revenue Growth Rates – 1Q14

11.2x 7.3x6.8x

5.4x 5.7x

an E

V/R

even

ue

3.2x

4.9x

an E

V/R

even

ue

1.1x1.8x 2.1x

<= 0% > 0% > 10% > 20% > 30% > 40%

Med

ia 2.1x 2.0x

<= 0% > 0% > 10% > 20% > 30% > 40%

Med

ia

• Public Internet companies with TTM revenue growth of 40% or higher were rewarded with median EV/Revenue multiples (11.2x) markedlygreater than their slower growing peers. Among those growing 40%+ were: Trulia (93.3%); Zillow (69.5%); Yelp (67.7%); LinkedIn (65.6%).

0% 0%<= 10%

10%<= 20%

20%<= 30%

30%<= 40%

40%

TTM Revenue Growth

<= 10% <= 20% <= 30% <= 40%

TTM EBITDA Margin

g g g p g g g % ( %); ( %); p ( %); ( %)• Unlike the SEG SaaS Index, where TTM EBITDA margins were inversely related to median EV/Revenue multiples, investors in public Internet

companies kept a keen eye on margins, and rewarded more profitable performers with significantly higher market multiples.• Public Internet companies with EBITDA margins above 40% posted a median EV/Revenue multiple of 6.8x in 1Q14, 113% higher than the

overall Index median. By comparison, public SaaS companies with EBITDA margins above 30% (not enough companies with 40%+) posted amedian EV/Revenue multiple of 4 5x 44% below the SaaS median market valuationmedian EV/Revenue multiple of 4.5x, 44% below the SaaS median market valuation.

• Investors have clearly taken into consideration, when valuing Internet vs SaaS stocks, such factors as sustainability of the customer relationship,and the associated recurring revenue, and the nature and extent of switching costs. By those measures the long term promise of SaaS seemsto far out weight the attractiveness of many public Internet companies.

• With few exceptions, many of the most profitable public Internet companies also reported stellar TTM revenue growth. Among them wereSouFun Holdings (43 2% revenue growth 53 6% EBITDA margin) Facebook (48 2% revenue growth 47 5% EBITDA margin) Baidu com

39 Q1 2014 Software Industry Financial ReportCopyright © 2014 by Software Equity Group, LLC

All Rights Reserved

SouFun Holdings (43.2% revenue growth, 53.6% EBITDA margin), Facebook (48.2% revenue growth, 47.5% EBITDA margin), Baidu.com(40.7% revenue growth, 45.0% EBITDA margin), and Mail.ru Group (32.2% revenue growth, 44.3% EBITDA margin).

THE SEG INTERNET INDEX BY PRODUCT CATEGORY• The SEG Internet Index is segmented into eight product categories. • Representative companies in each Internet category are referenced below.• See the appendix for the complete list of companies within each product• See the appendix for the complete list of companies within each product

category.

Ad Tech & Lead Gen Commerce Content & Media GamingAd Tech & Lead Gen Commerce Content & Media Gaming

Infrastructure Services Social Travel

40 Q1 2014 Software Industry Financial ReportCopyright © 2014 by Software Equity Group, LLC

All Rights Reserved

THE SEG INTERNET INDEX BY PRODUCT CATEGORY: FINANCIAL PERFORMANCE

1Q14 Median YoY Change in Revenue Growth1Q14 Median TTM Revenue Growth 1Q14 Median YoY Change in Revenue Growth1Q14 Median TTM Revenue Growth

27.6%

15.2%

Ad Tech &Lead Generation

Commerce

(22.2%)

(25.7%)

Ad Tech &Lead Generation

Commerce

7.9%

11.2%

8.9%

52 7%

Content & Media

Gaming

Infrastructure

S i

(37.2%)

(49.1%)

(3.3%)

Content & Media

Gaming

Infrastructure

52.7%57.2%

21.0%

Services

Social

Travel

26.2%

(12.2%)

8.5%

Services

Social

Travel

1Q14 Median YoY Change EBITDA Margin1Q14 Median TTM EBITDA Margin

6.8%Ad Tech &Lead Generation

(9.0%)

4 %

Ad Tech &Lead Generation

C7.3%

13.2%

32.9%

6.1%

Commerce

Content & Media

Gaming

Infrastructure

45.5%

(3.8%)

(8.1%)

(16.4%)

Commerce

Content & Media

Gaming

Infrastructure6.1%

7.4%

10.9%

17.2%

ast uctu e

Services

Social

Travel

( )

(0.5%)

(15.5%)

(5.0%)

Services

Social

Travel

41 Q1 2014 Software Industry Financial ReportCopyright © 2014 by Software Equity Group, LLC

All Rights Reserved

THE SEG INTERNET INDEX BY PRODUCT CATEGORY: MARKET MULTIPLES

1Q14 YoY Change in Median EV/Revenue Multiples1Q14 Median EV/Revenue Multiples

3.2xAd Tech &Lead Generation 39.6% Ad Tech &

Lead Generation

1.2x

3.5x

3.8x

1 9

Commerce

Content & Media

Gaming

I f t t

30.7% 128.2%

40.6%

11 2%

Commerce

Content & Media

Gaming

I f t t1.9x

4.2x

14.7x

4.8x

Infrastructure

Services

Social

Travel

11.2%

18.6%

61.0%

69.6%

Infrastructure

Services

Social

Travel

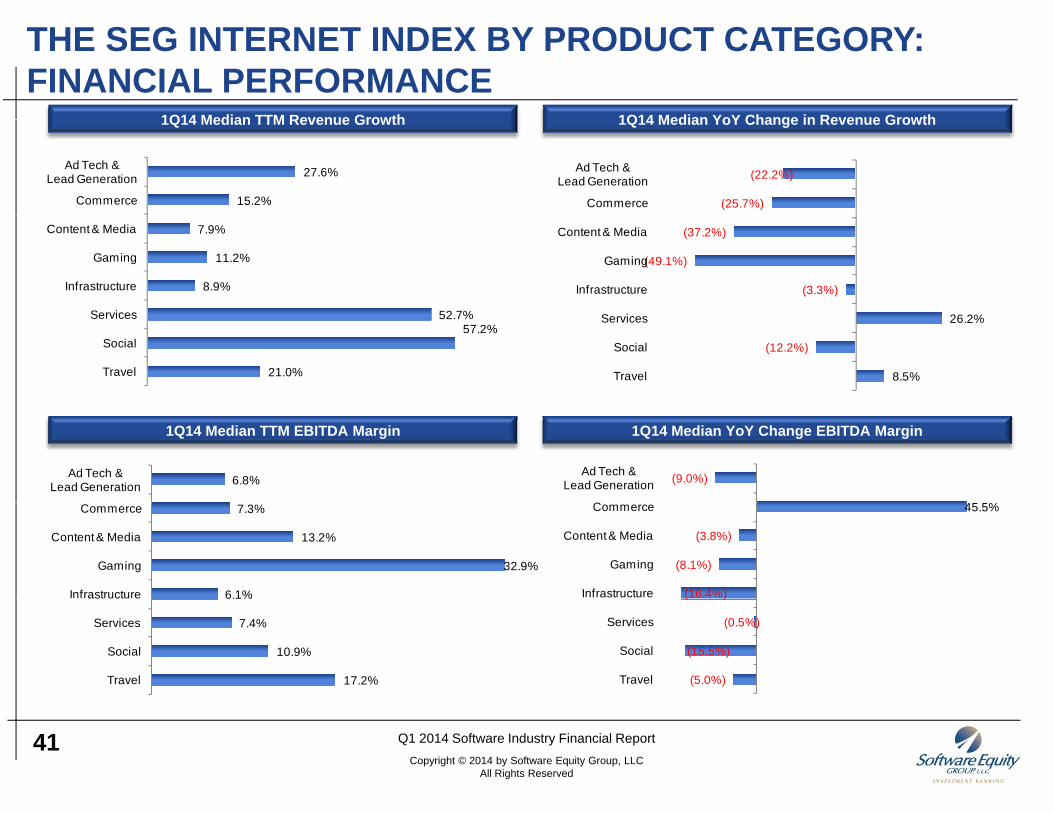

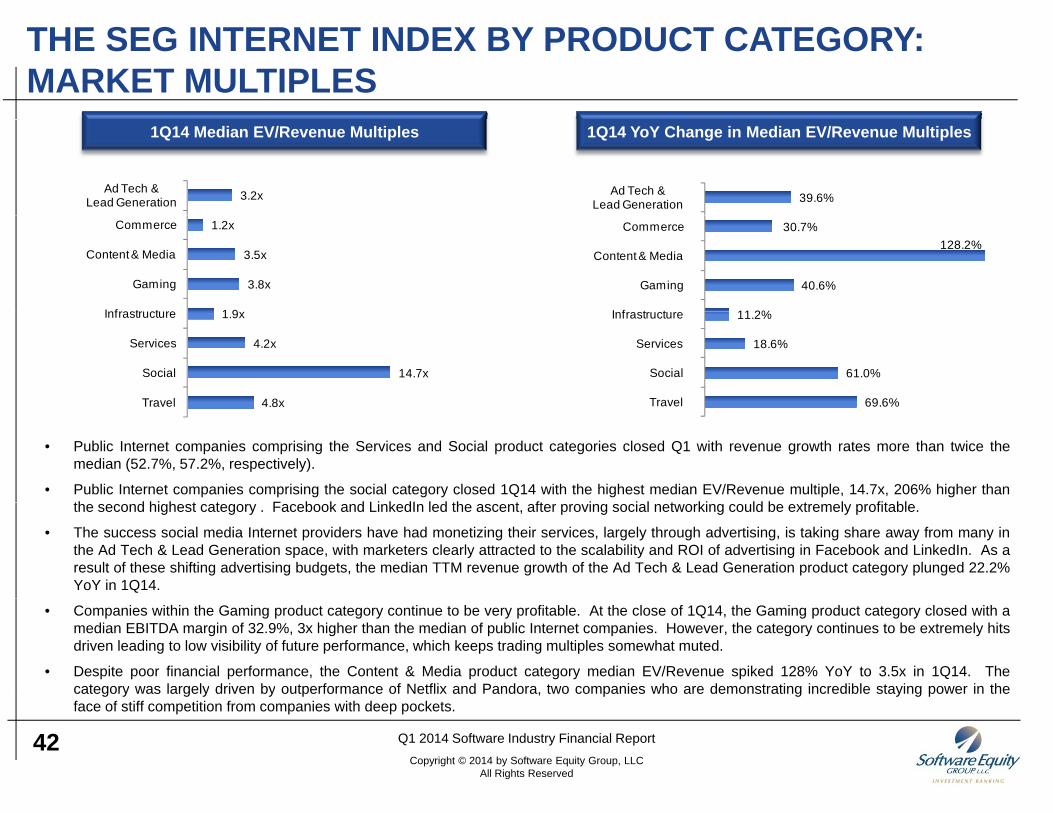

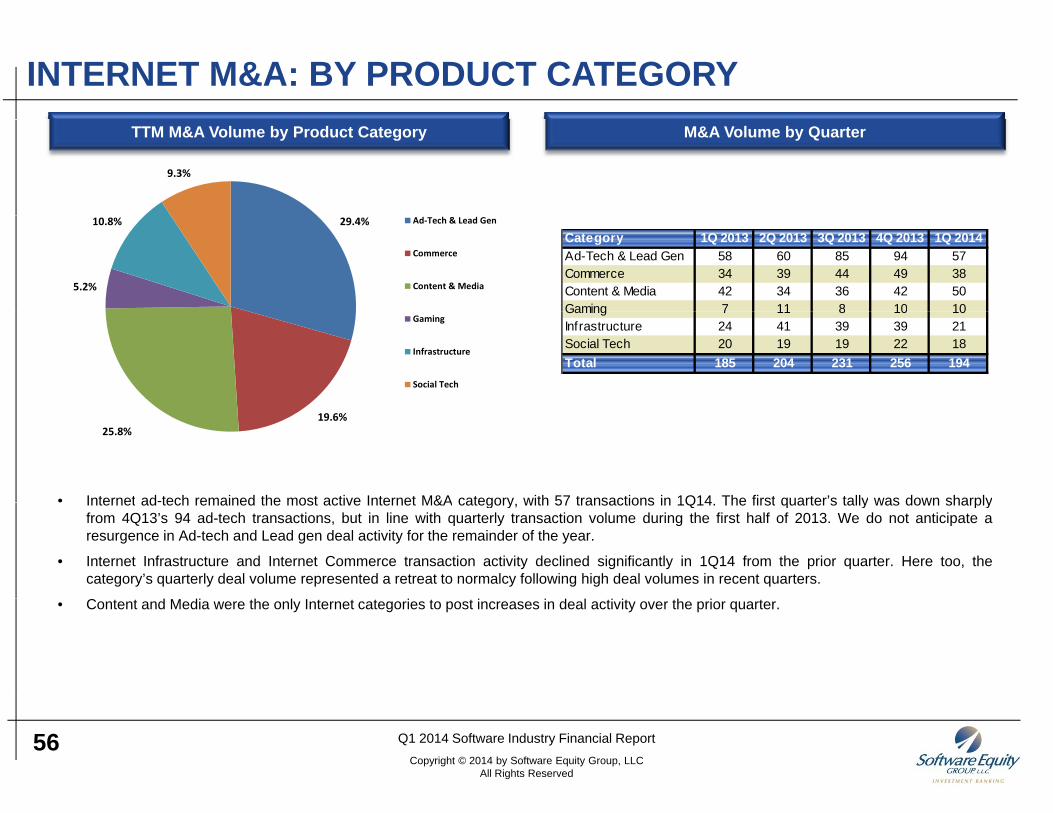

• Public Internet companies comprising the Services and Social product categories closed Q1 with revenue growth rates more than twice themedian (52.7%, 57.2%, respectively).

• Public Internet companies comprising the social category closed 1Q14 with the highest median EV/Revenue multiple, 14.7x, 206% higher thanth d hi h t t F b k d Li k dI l d th t ft i i l t ki ld b t l fit bl

8

the second highest category . Facebook and LinkedIn led the ascent, after proving social networking could be extremely profitable.

• The success social media Internet providers have had monetizing their services, largely through advertising, is taking share away from many inthe Ad Tech & Lead Generation space, with marketers clearly attracted to the scalability and ROI of advertising in Facebook and LinkedIn. As aresult of these shifting advertising budgets, the median TTM revenue growth of the Ad Tech & Lead Generation product category plunged 22.2%YoY in 1Q14.

• Companies within the Gaming product category continue to be very profitable. At the close of 1Q14, the Gaming product category closed with amedian EBITDA margin of 32.9%, 3x higher than the median of public Internet companies. However, the category continues to be extremely hitsdriven leading to low visibility of future performance, which keeps trading multiples somewhat muted.

• Despite poor financial performance, the Content & Media product category median EV/Revenue spiked 128% YoY to 3.5x in 1Q14. Thecategory was largely driven by outperformance of Netflix and Pandora, two companies who are demonstrating incredible staying power in the

42 Q1 2014 Software Industry Financial ReportCopyright © 2014 by Software Equity Group, LLC

All Rights Reserved

g y g y y p , p g y g pface of stiff competition from companies with deep pockets.

SOFTWARE INDUSTRY M&A MARKET UPDATE

43

SOFTWARE/SaaS M&A DEAL VOLUME AND SPENDINGMedian On-Premise Software EV/Revenue Exit MultiplesU.S. Software Mergers & Acquisitions Activity

426 430

454 456432 454

435406 394

431 444455

444

$$30

$35

450

500$54

$50 0

$60.0

ons)

394

$13.1

$21.3

$23.4

$23.1

$15.8

$20.8

$20.2 $22.8

$31.4

$15

$20

$25

200

250

300

350

400

Value (BIllions)

Num

ber o

f Deals

$37$40

$42 $41 $41 $42

$36$39

$36 $35$40

$43

$30.0

$40.0

$50.0

e De

al Value

(Milli

$12.6

$15.8

$12.3

$

$9.9

$0

$5

$10

0

50

100

150

200

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14

)

N

$0.0

$10.0

$20.0

11 11 11 11 12 12 12 12 13 13 13 13 14

TTM A

verag

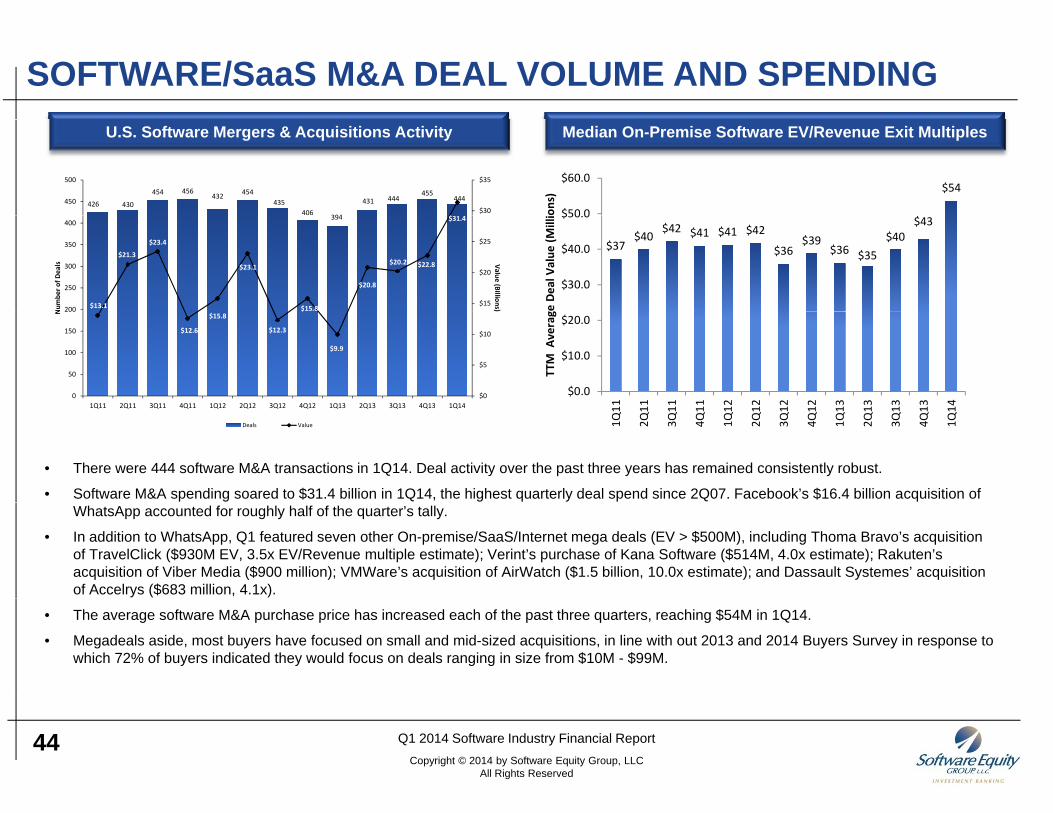

• There were 444 software M&A transactions in 1Q14. Deal activity over the past three years has remained consistently robust.

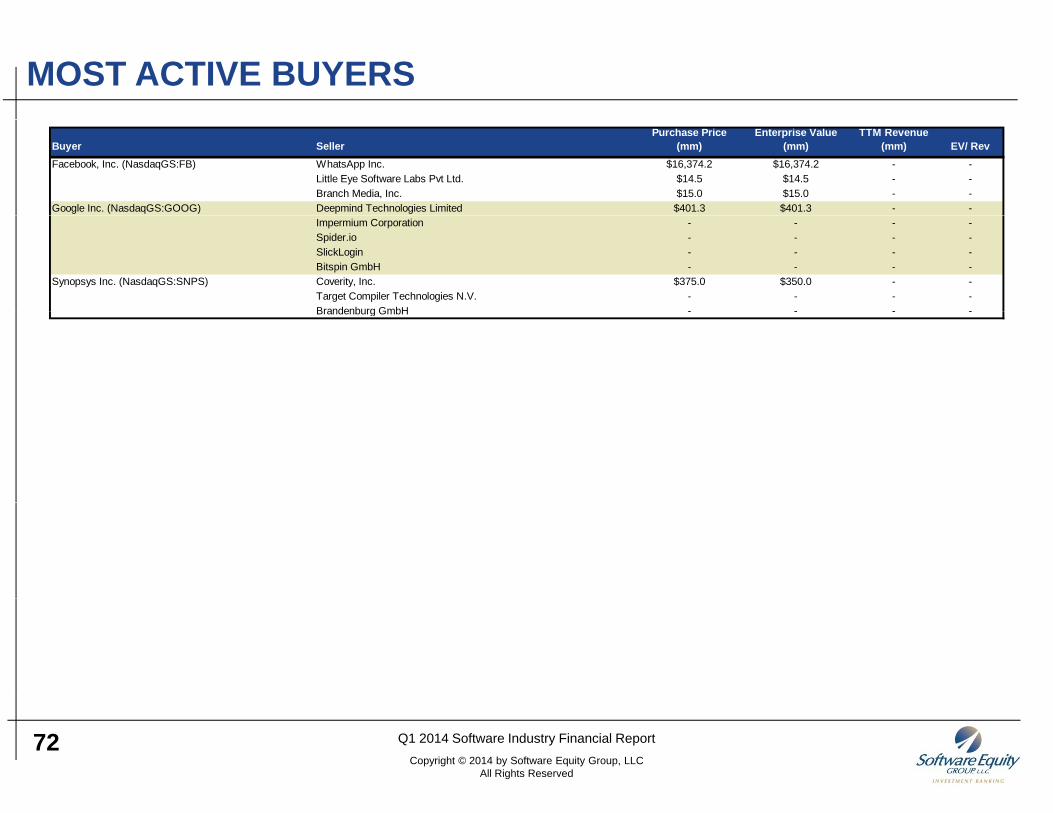

• Software M&A spending soared to $31.4 billion in 1Q14, the highest quarterly deal spend since 2Q07. Facebook’s $16.4 billion acquisition of

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14

Deals Value 1Q1

2Q1

3Q1

4Q1

1Q1

2Q1

3Q1

4Q1

1Q1

2Q1

3Q1

4Q1

1Q1

WhatsApp accounted for roughly half of the quarter’s tally.

• In addition to WhatsApp, Q1 featured seven other On-premise/SaaS/Internet mega deals (EV > $500M), including Thoma Bravo’s acquisition of TravelClick ($930M EV, 3.5x EV/Revenue multiple estimate); Verint’s purchase of Kana Software ($514M, 4.0x estimate); Rakuten’s acquisition of Viber Media ($900 million); VMWare’s acquisition of AirWatch ($1.5 billion, 10.0x estimate); and Dassault Systemes’ acquisition of Accelrys ($683 million, 4.1x).

• The average software M&A purchase price has increased each of the past three quarters, reaching $54M in 1Q14.

• Megadeals aside, most buyers have focused on small and mid-sized acquisitions, in line with out 2013 and 2014 Buyers Survey in response to which 72% of buyers indicated they would focus on deals ranging in size from $10M - $99M.

44 Q1 2014 Software Industry Financial ReportCopyright © 2014 by Software Equity Group, LLC

All Rights Reserved

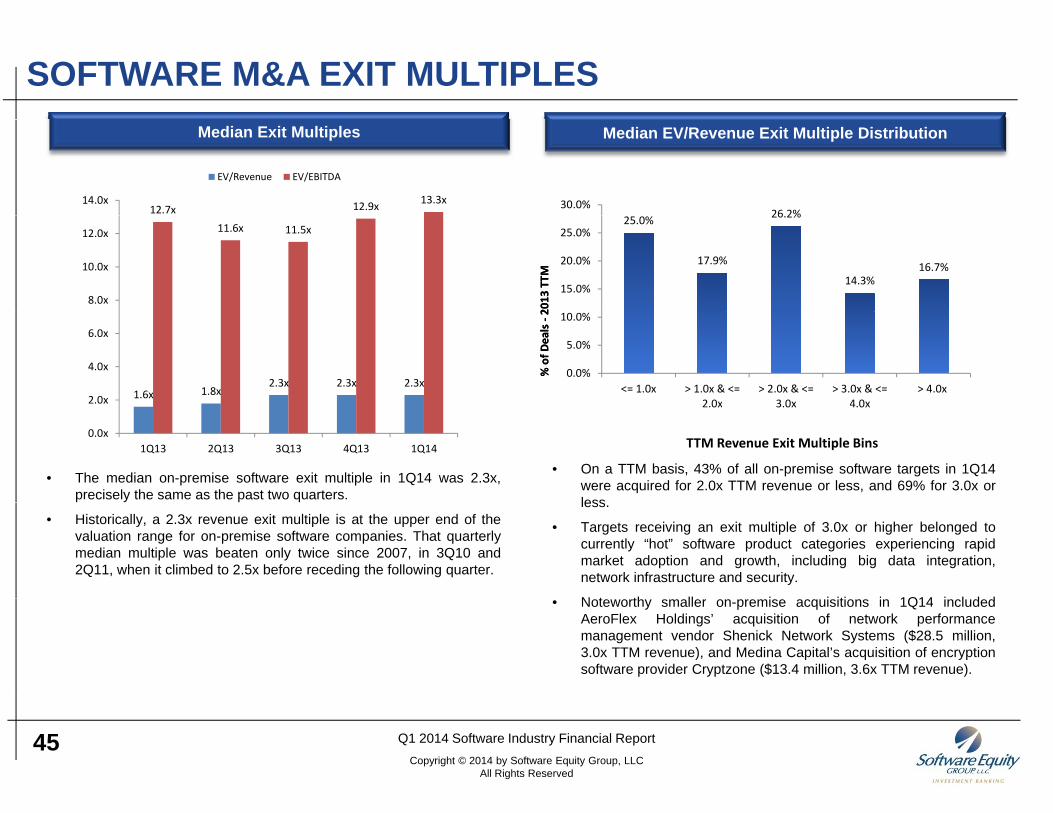

SOFTWARE M&A EXIT MULTIPLESMedian Exit Multiples Median EV/Revenue Exit Multiple Distribution

26 2%30.0%12.7x 12.9x 13.3x14.0x

EV/Revenue EV/EBITDA

25.0%

17.9%

26.2%

14.3%16.7%

15.0%

20.0%

25.0%

2013

TTM

2013

TTM

11.6x 11.5x

8.0x

10.0x

12.0x

0.0%

5.0%

10.0%

<= 1.0x > 1.0x & <=2.0x

> 2.0x & <=3.0x

> 3.0x & <=4.0x

> 4.0x

% of D

eals‐2

% of D

eals‐2

1.6x 1.8x2.3x 2.3x 2.3x

2.0x

4.0x

6.0x

• The median on-premise software exit multiple in 1Q14 was 2.3x,precisely the same as the past two quarters.

• On a TTM basis, 43% of all on-premise software targets in 1Q14were acquired for 2.0x TTM revenue or less, and 69% for 3.0x orless

2.0x 3.0x 4.0x

TTM Revenue Exit Multiple Bins0.0x

1Q13 2Q13 3Q13 4Q13 1Q14

• Historically, a 2.3x revenue exit multiple is at the upper end of thevaluation range for on-premise software companies. That quarterlymedian multiple was beaten only twice since 2007, in 3Q10 and2Q11, when it climbed to 2.5x before receding the following quarter.

less.

• Targets receiving an exit multiple of 3.0x or higher belonged tocurrently “hot” software product categories experiencing rapidmarket adoption and growth, including big data integration,network infrastructure and security.

N t th ll i i iti i 1Q14 i l d d• Noteworthy smaller on-premise acquisitions in 1Q14 includedAeroFlex Holdings’ acquisition of network performancemanagement vendor Shenick Network Systems ($28.5 million,3.0x TTM revenue), and Medina Capital’s acquisition of encryptionsoftware provider Cryptzone ($13.4 million, 3.6x TTM revenue).

45 Q1 2014 Software Industry Financial ReportCopyright © 2014 by Software Equity Group, LLC

All Rights Reserved

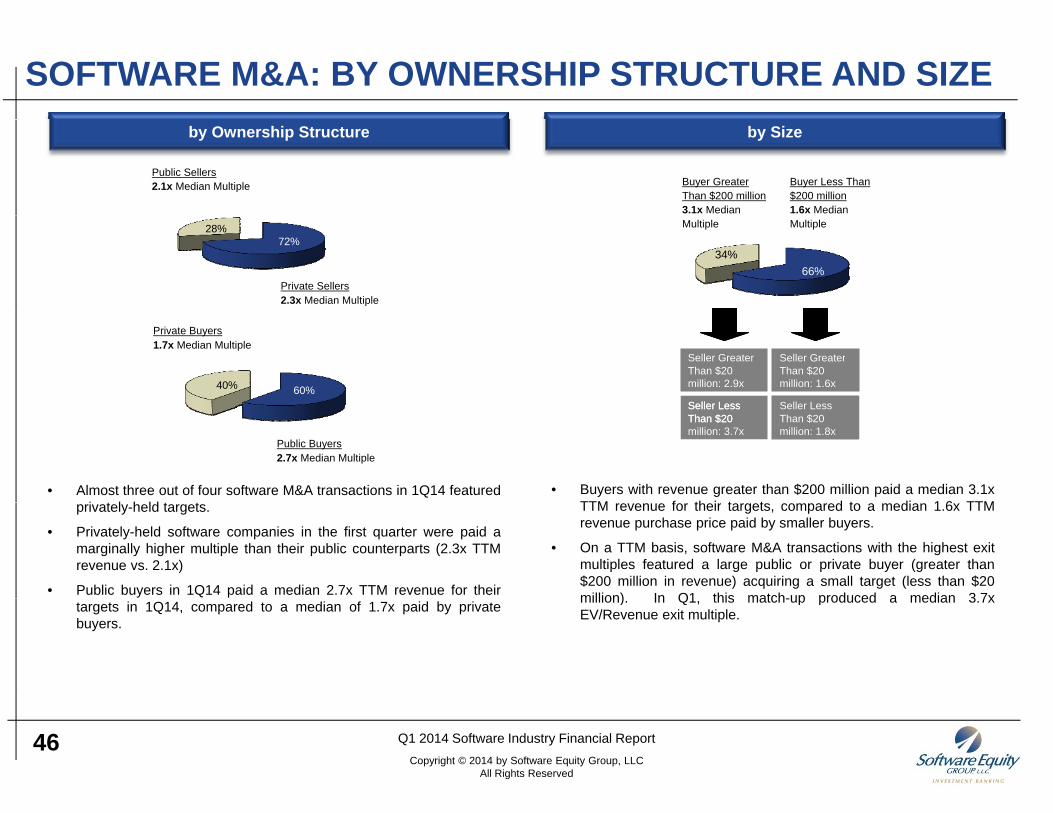

SOFTWARE M&A: BY OWNERSHIP STRUCTURE AND SIZEby Sizeby Ownership Structure

Public Sellers 2.1x Median Multiple Buyer Less Than

$200 million 1.6x Median

Buyer Greater Than $200 million 3.1x Median

Private Sellers 2.3x Median Multiple

72%28%

66%34%

Multiple Multiple

Private Buyers 1.7x Median Multiple

60%40%

Seller LessSeller Less

Seller Greater Than $20 million: 1.5x

Seller Greater Than $20 million: 0.8x

Seller LessSeller Less

Seller Greater Than $20 million: 1.6x

Seller Greater Than $20 million: 2.9x

• Almost three out of four software M&A transactions in 1Q14 featuredi t l h ld t t

• Buyers with revenue greater than $200 million paid a median 3.1xTTM f th i t t d t di 1 6 TTM

Public Buyers 2.7x Median Multiple

Seller Less Than $20 million: 2.4x

Seller Less Than $20 million: 3.7x

Seller Less Than $20 million: 1.8x

Seller Less Than $20

million

privately-held targets.

• Privately-held software companies in the first quarter were paid amarginally higher multiple than their public counterparts (2.3x TTMrevenue vs. 2.1x)

• Public buyers in 1Q14 paid a median 2.7x TTM revenue for their

TTM revenue for their targets, compared to a median 1.6x TTMrevenue purchase price paid by smaller buyers.

• On a TTM basis, software M&A transactions with the highest exitmultiples featured a large public or private buyer (greater than$200 million in revenue) acquiring a small target (less than $20million) In Q1 this match-up produced a median 3 7xtargets in 1Q14, compared to a median of 1.7x paid by private

buyers.

million). In Q1, this match-up produced a median 3.7xEV/Revenue exit multiple.

46 Q1 2014 Software Industry Financial ReportCopyright © 2014 by Software Equity Group, LLC

All Rights Reserved

Horizontal & Vertical M&A Median EV/Revenue Exit

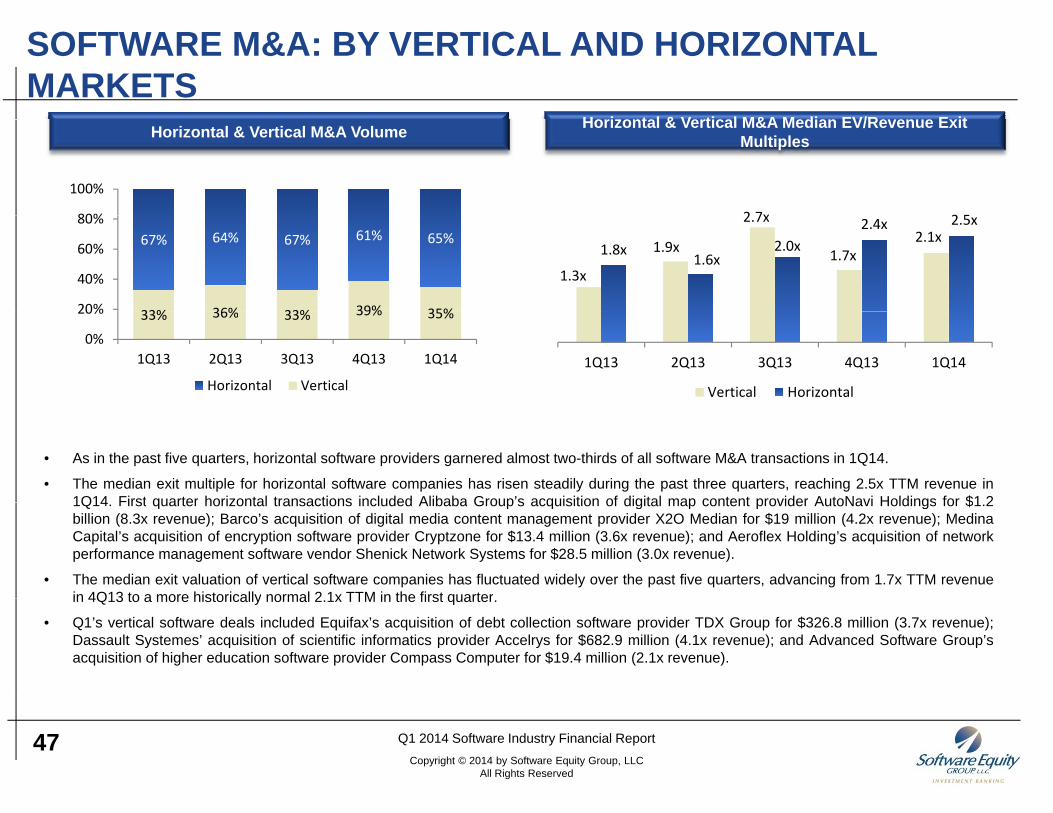

SOFTWARE M&A: BY VERTICAL AND HORIZONTAL MARKETS

Horizontal & Vertical M&A Median EV/Revenue Exit MultiplesHorizontal & Vertical M&A Volume

80%

100%

2 7x 2 5

33% 36% 33% 39% 35%

67% 64% 67% 61% 65%

20%

40%

60%

80%

1.3x

1.9x

2.7x

1.7x2.1x

1.8x1.6x

2.0x2.4x 2.5x

33% 36% 33% 39% 35%

0%

20%

1Q13 2Q13 3Q13 4Q13 1Q14

Horizontal Vertical1Q13 2Q13 3Q13 4Q13 1Q14

Vertical Horizontal

• As in the past five quarters, horizontal software providers garnered almost two-thirds of all software M&A transactions in 1Q14.

• The median exit multiple for horizontal software companies has risen steadily during the past three quarters, reaching 2.5x TTM revenue in1Q14 First quarter horizontal transactions included Alibaba Group’s acquisition of digital map content provider AutoNavi Holdings for $1 21Q14. First quarter horizontal transactions included Alibaba Group s acquisition of digital map content provider AutoNavi Holdings for $1.2billion (8.3x revenue); Barco’s acquisition of digital media content management provider X2O Median for $19 million (4.2x revenue); MedinaCapital’s acquisition of encryption software provider Cryptzone for $13.4 million (3.6x revenue); and Aeroflex Holding’s acquisition of networkperformance management software vendor Shenick Network Systems for $28.5 million (3.0x revenue).

• The median exit valuation of vertical software companies has fluctuated widely over the past five quarters, advancing from 1.7x TTM revenuein 4Q13 to a more historically normal 2 1x TTM in the first quarterin 4Q13 to a more historically normal 2.1x TTM in the first quarter.

• Q1’s vertical software deals included Equifax’s acquisition of debt collection software provider TDX Group for $326.8 million (3.7x revenue);Dassault Systemes’ acquisition of scientific informatics provider Accelrys for $682.9 million (4.1x revenue); and Advanced Software Group’sacquisition of higher education software provider Compass Computer for $19.4 million (2.1x revenue).

47 Q1 2014 Software Industry Financial ReportCopyright © 2014 by Software Equity Group, LLC

All Rights Reserved

SOFTWARE M&A ACTIVITY BY PRODUCT CATEGORY

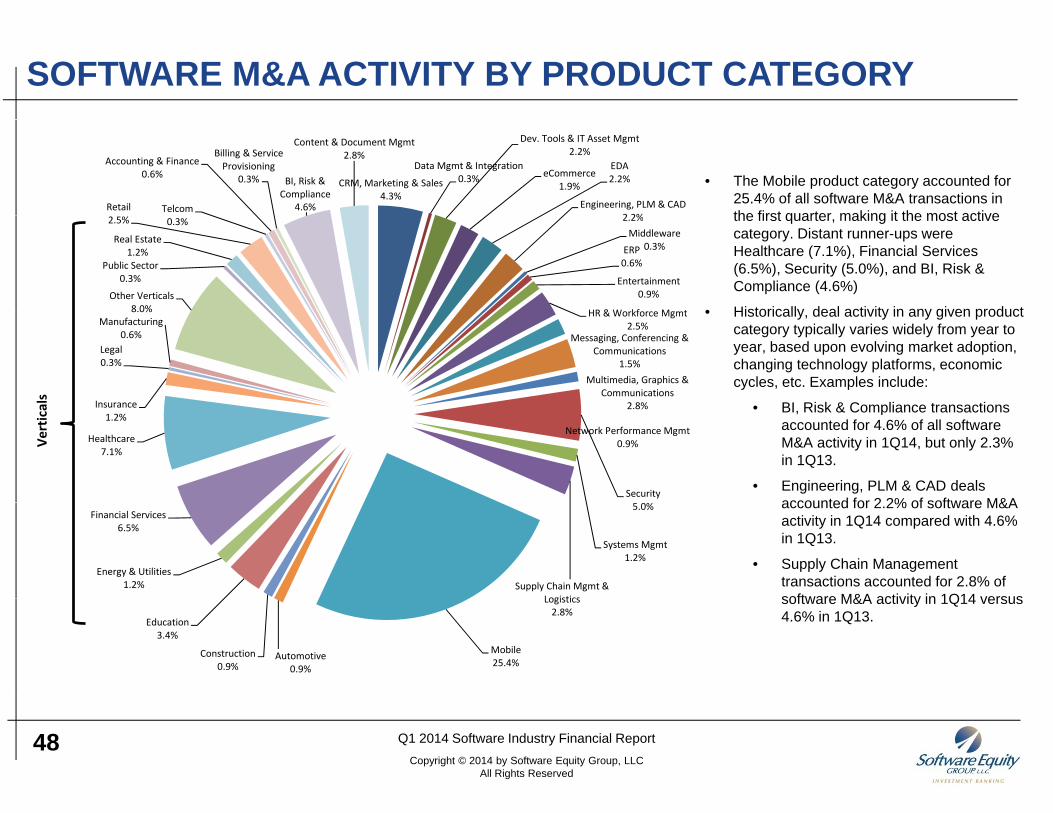

• The Mobile product category accounted for 25.4% of all software M&A transactions in the first quarter making it the most active

CRM, Marketing & Sales4.3%

Data Mgmt & Integration0.3%

Dev. Tools & IT Asset Mgmt2.2%

eCommerce1.9%

EDA2.2%

Engineering, PLM & CAD2 2%

Retail Telcom

Accounting & Finance0.6%

Billing & Service Provisioning

0.3% BI, Risk & Compliance

4.6%

Content & Document Mgmt2.8%

the first quarter, making it the most active category. Distant runner-ups were Healthcare (7.1%), Financial Services (6.5%), Security (5.0%), and BI, Risk & Compliance (4.6%)

• Historically deal activity in any given product

2.2%Middleware

0.3%ERP0.6%

Entertainment0.9%

HR &W kf M t

Other Verticals8.0%

Public Sector0.3%

Real Estate1.2%

2.5% 0.3%

• Historically, deal activity in any given product category typically varies widely from year to year, based upon evolving market adoption, changing technology platforms, economic cycles, etc. Examples include:

• BI Risk & Compliance transactions

HR & Workforce Mgmt2.5%

Messaging, Conferencing & Communications

1.5%Multimedia, Graphics &

Communications2 8%Insurance

Legal0.3%

Manufacturing0.6%

8.0%

als

• BI, Risk & Compliance transactions accounted for 4.6% of all software M&A activity in 1Q14, but only 2.3% in 1Q13.

• Engineering, PLM & CAD deals accounted for 2 2% of software M&A

2.8%

Network Performance Mgmt0.9%

Security

Healthcare7.1%

Insurance1.2%

Vertica

accounted for 2.2% of software M&A activity in 1Q14 compared with 4.6% in 1Q13.

• Supply Chain Management transactions accounted for 2.8% of software M&A activity in 1Q14 versus

5.0%

Systems Mgmt1.2%

Supply Chain Mgmt & Logistics

Energy & Utilities1.2%

Financial Services6.5%

software M&A activity in 1Q14 versus 4.6% in 1Q13.

Logistics2.8%

Mobile25.4%

Automotive0.9%

Construction0.9%

Education3.4%

48 Q1 2014 Software Industry Financial ReportCopyright © 2014 by Software Equity Group, LLC

All Rights Reserved

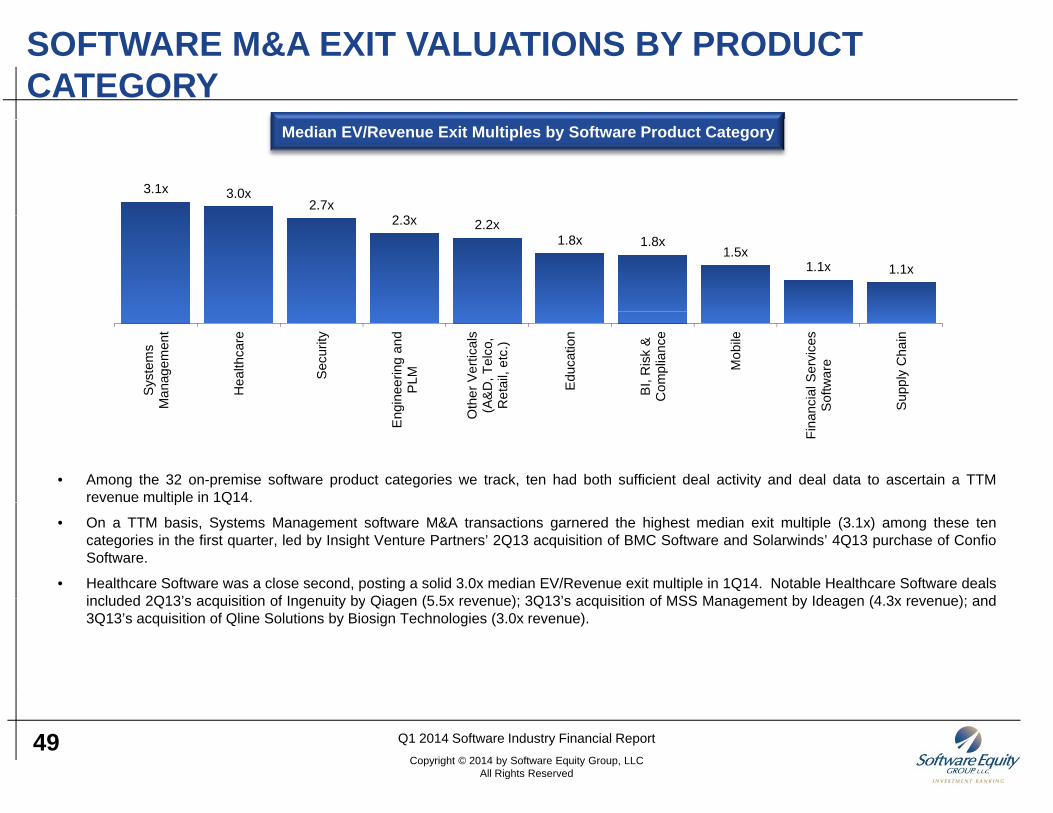

SOFTWARE M&A EXIT VALUATIONS BY PRODUCT CATEGORY

Median EV/Revenue Exit Multiples by Software Product Category

3.1x 3.0x2.7x

2 32.3x 2.2x1.8x 1.8x

1.5x1.1x 1.1x

Sys

tem

sM

anag

emen

t

Hea

lthca

re

Sec

urity

gine

erin

g an

dP

LM

ther

Ver

tical

sA&

D, T

elco

,R

etai

l, et

c.)

Edu

catio

n

BI,

Ris

k &

Com

plia

nce

Mob

ile

cial

Ser

vice

sS

oftw

are

Sup

ply

Cha

in

• Among the 32 on-premise software product categories we track, ten had both sufficient deal activity and deal data to ascertain a TTMrevenue multiple in 1Q14.

M

Eng O

t (A R

Fina

n S S

p Q

• On a TTM basis, Systems Management software M&A transactions garnered the highest median exit multiple (3.1x) among these tencategories in the first quarter, led by Insight Venture Partners’ 2Q13 acquisition of BMC Software and Solarwinds’ 4Q13 purchase of ConfioSoftware.

• Healthcare Software was a close second, posting a solid 3.0x median EV/Revenue exit multiple in 1Q14. Notable Healthcare Software dealsincluded 2Q13’s acquisition of Ingenuity by Qiagen (5 5x revenue); 3Q13’s acquisition of MSS Management by Ideagen (4 3x revenue); andincluded 2Q13’s acquisition of Ingenuity by Qiagen (5.5x revenue); 3Q13’s acquisition of MSS Management by Ideagen (4.3x revenue); and3Q13’s acquisition of Qline Solutions by Biosign Technologies (3.0x revenue).

49 Q1 2014 Software Industry Financial ReportCopyright © 2014 by Software Equity Group, LLC

All Rights Reserved