Embed Size (px)

DESCRIPTION

The Strategic Case for Gold Amsterdam 11 October 2009. Disclaimer. - PowerPoint PPT Presentation

Citation preview

The Strategic Case for GoldAmsterdam

11 October 2009

Disclaimer

The information and opinions contained in this presentation have been obtained from sources believed to be reliable, but no representation or warranty, express or implied, is made that such information is accurate or complete and it should not be relied upon as such. This presentation does not purport to make any recommendation or provide investment advice to the effect that any gold related transaction is appropriate for all investment objectives, financial situations or particular needs. Prior to making any investment decisions investors should seek advice from their advisers on whether any part of this presentation is appropriate to their specific circumstances. This presentation is not, and should not be construed as, an offer or solicitation to buy or sell gold or any gold related products. Expressions of opinion are those of the World Gold Council only and are subject to change without notice.

2

Introducing World Gold Council

• Funded by the world’s leading gold

mining companies

• We promote the use of gold in all its

forms through marketing activities in

major international markets.

• Offices in key consuming countries:

India

China

Middle East

United States

MEMBERSMEMBERS

Agnico EagleAgnico Eagle

AngloGold AshantiAngloGold Ashanti

Barrick Gold CorporationBarrick Gold Corporation

Coeur d’Alene Mines CorporationCoeur d’Alene Mines Corporation

Compania de Minas BuenaventuraCompania de Minas Buenaventura

Eldorado GoldEldorado Gold

GoldcorpGoldcorp

Gold Fields LimitedGold Fields Limited

HarmonyHarmony

IAM GoldIAM Gold

Kinross Gold CorporationKinross Gold Corporation

Newmont Mining CorporationNewmont Mining Corporation

Peter Hambro MiningPeter Hambro Mining

Yamana GoldYamana Gold

ASSOCIATESASSOCIATES

CediminCedimin

China National Gold CorporationChina National Gold Corporation

The Hutti Gold Mines CompanyThe Hutti Gold Mines Company

Kahama MiningKahama Mining

Minera Yanacocha S.R.L.Minera Yanacocha S.R.L.

Mitsubishi Materials CorporationMitsubishi Materials Corporation

Royal Gold IncRoyal Gold Inc..

Outline

• Demand and supply fundamentals – resilient demand and constrained supply

• The outlook• Key investment attributes

– A hedge against inflation– A hedge against dollar movements– A safe haven and insurance policy – A diversifier

4

Demand and Supply Fundamentals

Q2 tonnage down 9% on Q2 2008 6

-

200

400

600

800

1,000

1,200

1,400

Q1'06 Q3'06 Q1'07 Q3'07 Q1'08 Q3'08 Q1'09

Total identifiable demand (tonnes)

Jewellery Consumption Industrial & Dental Identifiable Investment London PM fix (US$/oz)

Source: GFMS

Price volatility a constraint on jewellery demand7

10000

15000

20000

25000

30000

35000

40000

45000

50000

55000

200

400

600

800

1000

1200

1400

1600

1800

02-Jan-04 02-Jan-05 02-Jan-06 02-Jan-07 02-Jan-08 02-Jan-09

The five year daily gold price (per oz) in selected currencies

$US Euro New Turkish Lira Indian Rupees, rhsSource: WGC based on Global Insight data

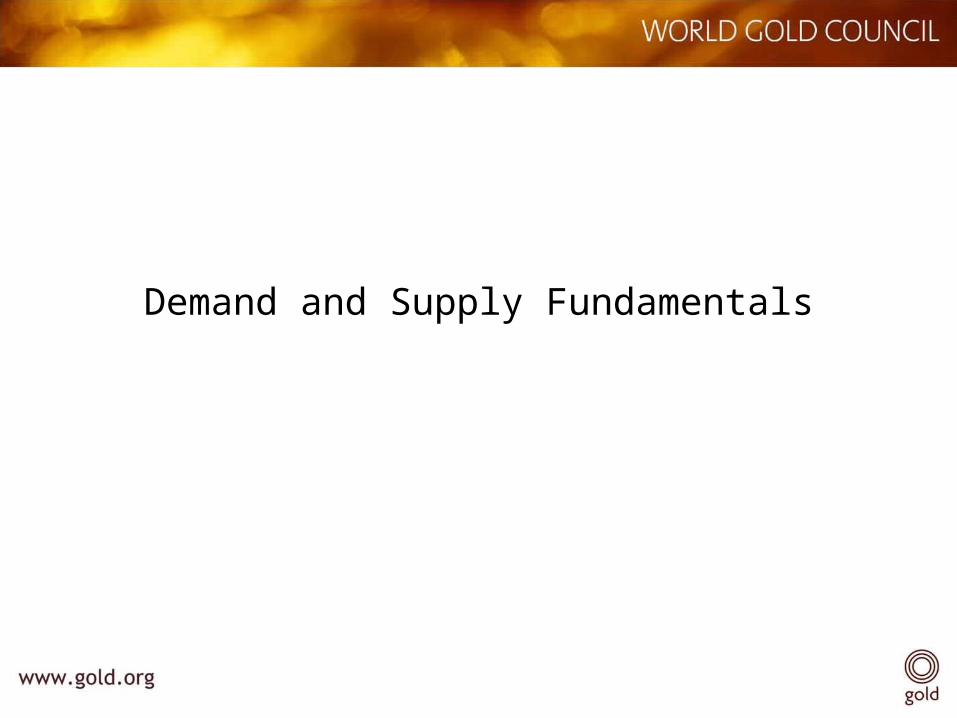

China the lone positive jewellery story

-60

-50

-40

-30

-20

-10

0

10

Jewellery by country (tonnes, Q2'09 vs Q2'08, % change)

Source: GFMS

8

A breakdown of investment demand

Tonnes, Q2’08 Tonnes, Q2’09 % change

Identifiable investment

151.9 222.4 46

Net retail investment 147.9 165.7 12

ETFs and similar 4.0 56.7 1315

“Inferred investment” 10.2 195.1 1657

“Total” investment 162.1 417.4 157

Source: GFMS

9

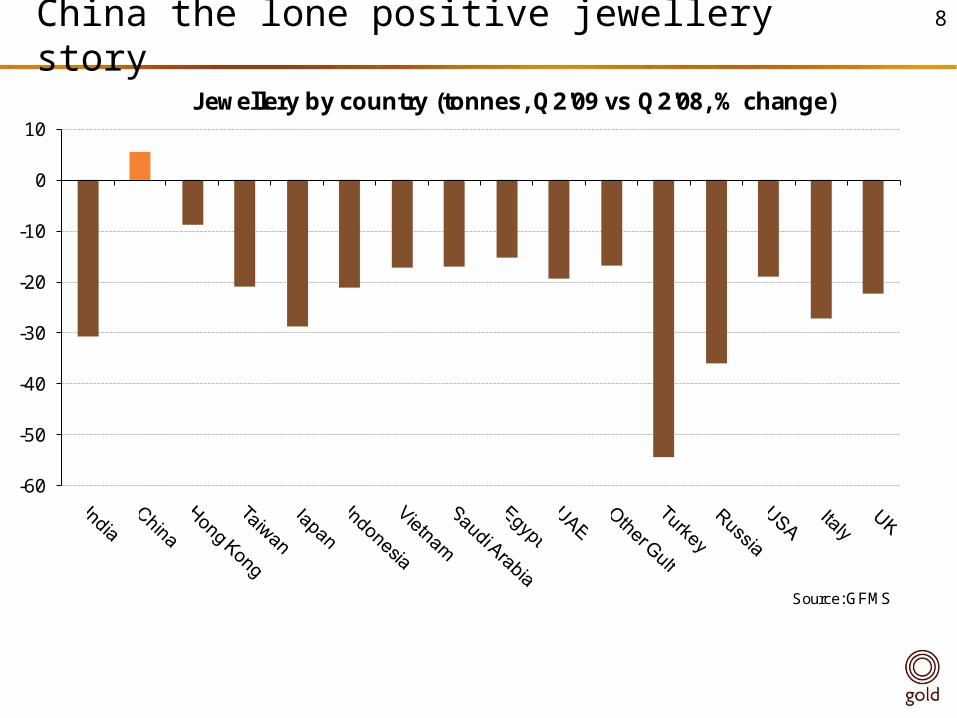

European flows remain very buoyant

-20

0

20

40

60

80

100

120

140

160

180

Q1'05 Q3'05 Q1'06 Q3'06 Q1'07 Q3'07 Q1'08 Q3'08 Q1'09

European retail investment demand, tonnes

Other (Europe) Switzerland Germany France

Source: GFMS

10

ETF flows generally long term in nature 11

200

300

400

500

600

700

800

900

1000

1100

0

200

400

600

800

1000

1200

1400

1600

1800

2000

Jan-06 Jul-06 Jan-07 Jul-07 Jan-08 Jul-08 Jan-09 Jul-09

Holdings in Exchange Traded Funds (tonnes) and the gold price, Jan 06 - Sep 09

Other funds 'GLD' Gold price, $US/oz, rhs

Source: www.exchangetradedgold.com, Global Insight

Share of identifiable demand

Q2 2008

Jewellery 66%

Industrial 15%

IdentifiableInvestment

19%

Q2 2009

Jewellery 56%

Industrial 13%

IdentifiableInvestment

31%

Source: GFMS

12

Total Q2 supply down 23% on Q1 2009

-200

-

200

400

600

800

1,000

1,200

1,400

Q1'05 Q3'05 Q1'06 Q3'06 Q1'07 Q3'07 Q1'08 Q3'08 Q1'09

Quarterly supply in tonnes

Total mine supply Official sector sales Recycled gold Source: WGC, GFMS

13

Net central bank sales have continued to reduce

-100

0

100

200

300

400

500

H1'02 H1'03 H1'04 H1'05 H1'06 H1'07 H1'08 H1'09

Supply from net central bank sales in tonnes

Non-CBGA CBGA Source: GFMS, WGC, IMF

14

The Strategic Investment Casefor Gold

Why gold? A safe haven and form of insurance

• A simple asset• No default risk• No counterparty risk• Liquid• Gold’s history

– As a means of exchange– As the centre of the global monetary system

16

Gold is a hedge against inflation uncertainty

• Inflation or deflation? • Gold is a long run hedge against inflation• Yet, a period of deflation suggests ongoing

economic uncertainty, so safe haven flows would remain underpinned

• Medium to longer term, inflation is a significant risk

17

Gold is a long run hedge against the US dollar

18

0.58

0.61

0.64

0.67

0.70

0.73

0.76

0.79

0.82650

700

750

800

850

900

950

1000

1050

Aug-07 Oct-07 Dec-07 Feb-08 Apr-08 Jun-08 Aug-08 Oct-08 Dec-08 Feb-09 Apr-09 Jun-09 Aug-09

Gold and $/Euro

Gold Dollar/Euro (RHS, Inverted)

Source: Global Insight

Gold is a diversifier

Correlations, weekly returns 3 years ending June 2009

Gold

Gold 1.00

FTSE 100 -0.22

DAX 30 -0.20

S&P500 -0.10

MSCI World Ex UK -0.28

LB /BarCap Global Treasuries Index , TR, GBP

0.02

LB/BarCap Global Treasuries Index, TR, Euro -0.01

Euribor, 3 month 0.01

UK Lending Rate, 3 month 0.03Red text denotes that correlation coefficient is not significantly different from zero.Violet text denotes that correlation coefficient is negative (5% level of significance).

Data: Global Insight, Lehman Bros., WGC

19

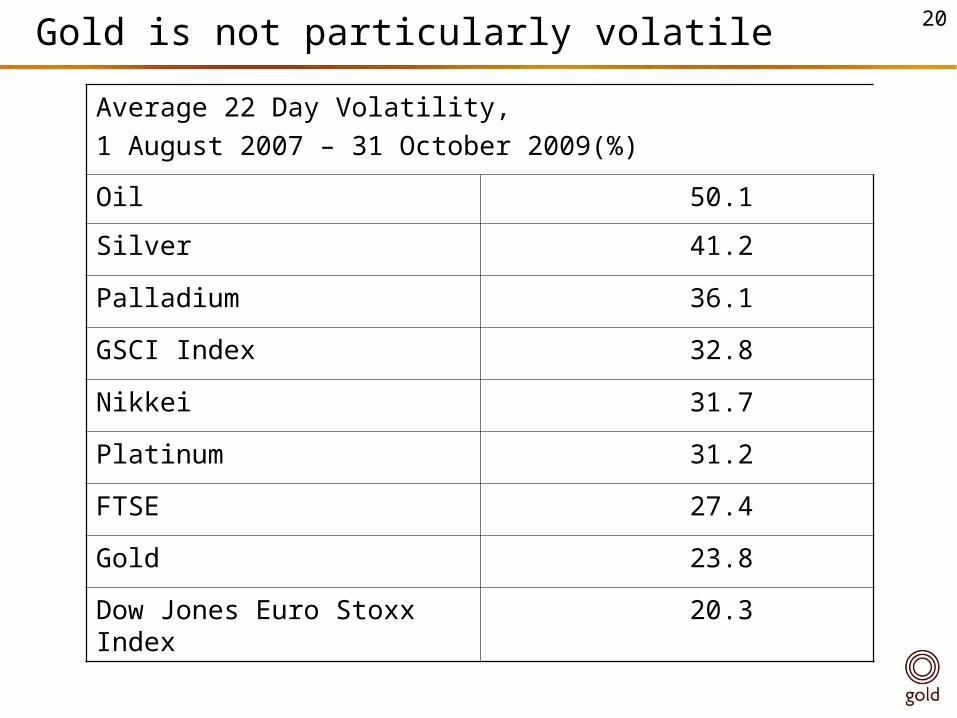

Gold is not particularly volatile

Average 22 Day Volatility, 1 August 2007 – 31 October 2009(%)

Oil 50.1

Silver 41.2

Palladium 36.1

GSCI Index 32.8

Nikkei 31.7

Platinum 31.2

FTSE 27.4

Gold 23.8

Dow Jones Euro Stoxx Index 20.3

20

WHERE DOES GOLD FIT INTO A PORTFOLIO?

Results with gold added

Optimal Portfolios Composition Map

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

4.3% 4.4% 4.6% 5.1% 5.6% 6.2% 6.9% 7.6% 8.3% 9.1% 9.9% 10.9% 11.9%volatility

allo

ca

tio

n

UK Gilts Short UK Gilts Medium UK Gilts LongGlobal Bonds UK Equities Europe Ex UK EquitiesNorth American Equities Pacific Equities Gold

22

Over and above a commodity basketOptimal Portfolios Composition Map

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

4.3% 4.3% 4.6% 4.9% 5.4% 6.0% 6.7% 7.3% 8.0% 8.8% 9.6% 10.5% 11.4%

volatility

allo

cati

on

UK Gilts Short UK Gilts Medium UK Gilts LongGlobal Bonds UK Equities Europe Ex UK EquitiesNorth American Equities Pacific Equities GoldCommodities

23

Summary

• The demand for gold has shown considerable resilience across the economic cycle

• The three sectors provide a source of balance• The outlook for supply remains constrained• High levels of uncertainty – economic, inflation,

currency – are supportive for gold • Gold’s biggest strength is its diversification

properties - the focus on diversification and risk management are expected to continue

24

Questions?

www.gold.org www.invest.gold.org

25

![Retailer Awards 2017 Winners List - Wine-Searcher Awards Results.pdfGold French List in Amsterdam Bolomey Wijnimport Gold French List in Antwerp [Antwerpen] Finest Wines Gold French](https://img.pdfslide.net/doc/110x75/5e3777d7880cb0549b364b5c/retailer-awards-2017-winners-list-wine-searcher-awards-resultspdf-gold-french.jpg)