Embed Size (px)

Citation preview

The Twelfth Five-Year Plan for Economic and Social Development

and the Macroeconomic Outlook

Lawrence J. Lau, Ph. D.Chairman, CIC International (Hong Kong) Co., Limited

Ralph and Claire Landau Professor of Economics, The Chinese Univ. of Hong Kongand

Kwoh-Ting Li Professor in Economic Development, Emeritus, Stanford University

The Ongoing Transformation of China’s Growth PatternAcademic Summit: China Development Forum 2011

Beijing, 19 March 2011

Tel: (852)3710-6888; Fax: (852)2104-6938Email: [email protected]; WebPages: www.igef.cuhk.edu.hk/ljl

Lawrence J. Lau 2

Outline

The Twelfth Five-Year Plan for National Economic and Social Development

The Macroeconomic Outlook

Concluding Remarks

Lawrence J. Lau 3

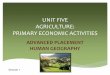

The Eleventh Five-Year Plan for National Economic and Social Development

The 11th Five-Year Plan for National Economic and Social Development officially ended on 31 December 2010.

Most of the targets were achieved or exceeded, including the reduction in energy consumption per unit GDP by 20 percent compared to year end 2005.

The 11th Five-Year Plan provided for a target rate of growth of real GDP of 7.5% per annum between 2005 and 2010. The actual rate of growth achieved was 11.2% per annum.

The only other major target not achieved was the percentage of GDP expended on R&D—the target was 2% and the actual achieved was 1.8%.

Lawrence J. Lau 4

The Twelfth Five-Year Plan for National Economic and Social Development

The Twelfth Five-Year Plan for National Economic and Social Development was approved by the National People’s Congress a week ago. It is mostly an indicative plan rather than a mandatory plan.

The most remarkable feature was that the target growth rate was lowered from 7.5% per annum of the 11th Five- Year Plan to 7% per annum. I am sure that this target will be exceeded, just as the target was exceeded in the last Plan. However, what the reduction in the target growth rate signals is the determination of the Chinese Government to de-emphasise quantitative economic growth and to focus on the quality of the economic growth.

Lawrence J. Lau 5

The Twelfth Five-Year Plan for National Economic and Social Development

The Plan provides for increased expenditures for education and healthcare, especially in the rural regions, environmental preservation and protection, and air and water pollution control. It also has mandatory targets for improvement in energy efficiency and reduction in carbon emission.

It also provides for improvements in the income distribution through taxation, transfer payments and targeted government expenditures on education and health care.

Lawrence J. Lau 6

The Twelfth Five-Year Plan for National Economic and Social Development

One principal theme of the Twelfth Five-Year Plan is the transformation in the mode of Chinese economic development—firstly, from export-oriented to domestic demand-oriented and secondly, from input-driven to technical progress-driven or innovation-driven.

The Plan aims at essentially balanced international trade, and I believe it is achievable.

Lawrence J. Lau 7

The Twelfth Five-Year Plan for National Economic and Social Development

While many problems have arisen in the Chinese economy within the past decade— for example, income disparity, environmental degradation, inadequate infrastructure and corruption—it is fair to say that everyone has benefited from the economic reform and opening since 1978, albeit to varying degrees, and few want to return to the central planning days.

The Chinese Government leaders have also demonstrated their ability to confront important challenges and solve difficult problems.

China is one of the very few socialist countries that have made a smooth transition from a centrally planned to a market economy. It is a model for other transition economies such as Vietnam and potential transition economies such as Cuba, Laos, and North Korea.

Lawrence J. Lau 8

The Macroeconomic Outlook

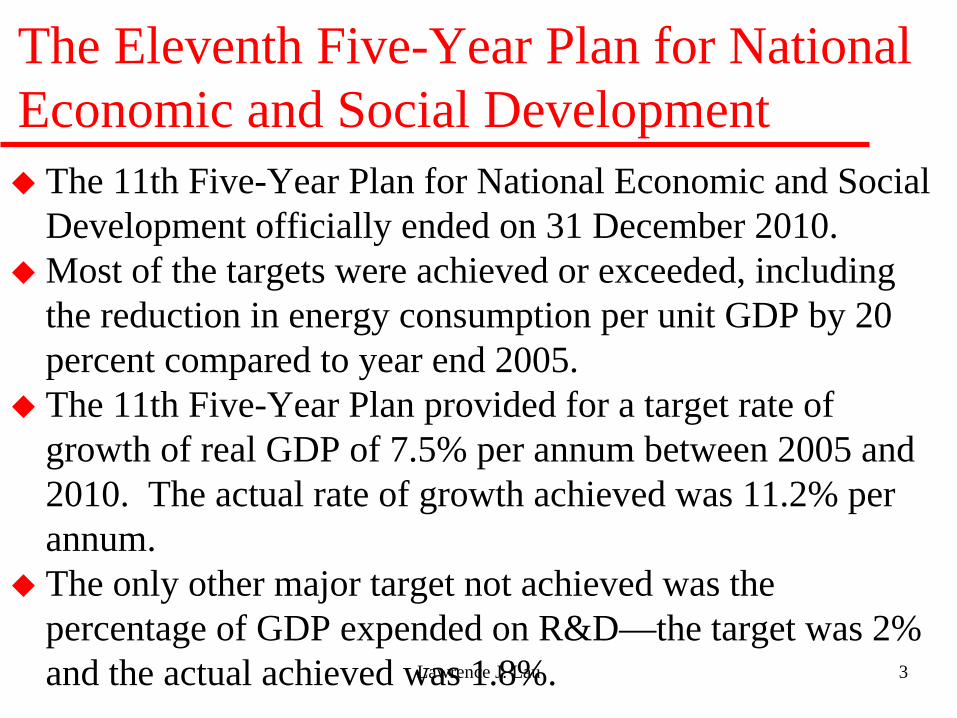

The Chinese economy grew 9.1% in 2009 and approximately 10.3% in 2010 even as the European and U.S. economies remained in recession.

The outlook is that there will be a gradual slowdown of the economy in 2011, to perhaps around 8%, which is actually a positive development for the Chinese economy.

While this may seem like a significant slowdown from 10.3%, but there are reasons to believe that the impact of the slowdown on Chinese employment is not that severe.

Lawrence J. Lau 99

Quarterly Rates of Growth of Chinese Real GDP, Y-o-Y

Quarterly Rates of Growth of Real GDP (YoY)

-5%

0%

5%

10%

15%

20%

25%

1983

q119

83q3

1984

q119

84q3

1985

q119

85q3

1986

q119

86q3

1987

q119

87q3

1988

q119

88q3

1989

q119

89q3

1990

q119

90q3

1991

q119

91q3

1992

q119

92q3

1993

q119

93q3

1994

q119

94q3

1995

q119

95q3

1996

q119

96q3

1997

q119

97q3

1998

q119

98q3

1999

q119

99q3

2000

q120

00q3

2001

q120

01q3

2002

q120

02q3

2003

q120

03q3

2004

q120

04q3

2005

q120

05q3

2006

q120

06q3

2007

q120

07q3

2008

q120

08q3

2009

q120

09q3

2010

q120

10q3

Perc

ent p

er a

nnum

GDPQ1 GDPQ2

GDPQ3 GDPQ4

Lawrence J. Lau 10

Monthly Rates of Growth of Real Value- added of the Industrial Sector, Y-o-Y

10

Monthly Rates of Growth of Real Value-Added of the Industrial Sector, Year-over-Year

0

5

10

15

20

25

Jan-

95A

pr-9

5Ju

l-95

Oct

-95

Jan-

96A

pr-9

6Ju

l-96

Oct

-96

Jan-

97A

pr-9

7Ju

l-97

Oct

-97

Jan-

98A

pr-9

8Ju

l-98

Oct

-98

Jan-

99A

pr-9

9Ju

l-99

Oct

-99

Jan-

00A

pr-0

0Ju

l-00

Oct

-00

Jan-

01A

pr-0

1Ju

l-01

Oct

-01

Jan-

02A

pr-0

2Ju

l-02

Oct

-02

Jan-

03A

pr-0

3Ju

l-03

Oct

-03

Jan-

04A

pr-0

4Ju

l-04

Oct

-04

Jan-

05A

pr-0

5Ju

l-05

Oct

-05

Jan-

06A

pr-0

6Ju

l-06

Oct

-06

Jan-

07A

pr-0

7Ju

l-07

Oct

-07

Jan-

08A

pr-0

8Ju

l-08

Oct

-08

Jan-

09A

pr-0

9Ju

l-09

Oct

-09

Jan-

10A

pr-1

0Ju

l-10

Oct

-10

Jan-

11

%

Lawrence J. Lau 1111

Monthly Rates of Growth of Chinese Fixed Assets Investment, Y-o-Y

Monthly Rates of Growth of Fixed Investment since 2000, Year-over-Year

0

10

20

30

40

50

60

Jan-

00A

pr-0

0Ju

l-00

Oct

-00

Jan-

01A

pr-0

1Ju

l-01

Oct

-01

Jan-

02A

pr-0

2Ju

l-02

Oct

-02

Jan-

03A

pr-0

3Ju

l-03

Oct

-03

Jan-

04A

pr-0

4Ju

l-04

Oct

-04

Jan-

05A

pr-0

5Ju

l-05

Oct

-05

Jan-

06A

pr-0

6Ju

l-06

Oct

-06

Jan-

07A

pr-0

7Ju

l-07

Oct

-07

Jan-

08A

pr-0

8Ju

l-08

Oct

-08

Jan-

09A

pr-0

9Ju

l-09

Oct

-09

Jan-

10A

pr-1

0Ju

l-10

Oct

-10

Jan-

11

Perc

ent

Lawrence J. Lau 1212

Monthly Rates of Growth of Chinese Real Retail Sales, Y-o-Y

Monthly Rates of Growth of Real Retail Sales since 2000, Year-over-Year

0

5

10

15

20

25

30

35

Jan-

00A

pr-0

0Ju

l-00

Oct

-00

Jan-

01A

pr-0

1Ju

l-01

Oct

-01

Jan-

02A

pr-0

2Ju

l-02

Oct

-02

Jan-

03A

pr-0

3Ju

l-03

Oct

-03

Jan-

04A

pr-0

4Ju

l-04

Oct

-04

Jan-

05A

pr-0

5Ju

l-05

Oct

-05

Jan-

06A

pr-0

6Ju

l-06

Oct

-06

Jan-

07A

pr-0

7Ju

l-07

Oct

-07

Jan-

08A

pr-0

8Ju

l-08

Oct

-08

Jan-

09A

pr-0

9Ju

l-09

Oct

-09

Jan-

10A

pr-1

0Ju

l-10

Oct

-10

Jan-

11

Perc

ent

Lawrence J. Lau 13

The Macroeconomic Outlook

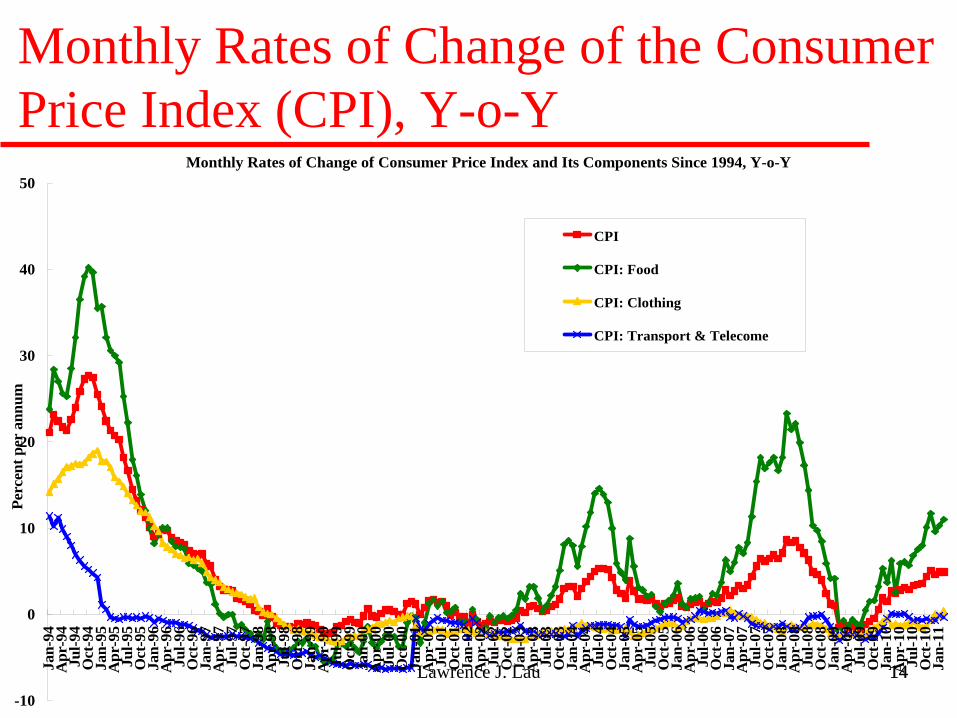

The rate of inflation of goods and services, as measured by the consumer price index, reached a peak of 5.1% year-over-year in November, 2010.

For 2010 as a whole, the rate of inflation exceeded the objective of the Chinese Government of 3% slightly, at 3.3%.

However, the bulk of the increase in the consumer price index (approximately 70%) was caused by the increase in food prices (principally vegetables), due mostly to weather and not to monetary factors. The core rate of inflation, that is, the rate of inflation net of the changes in the prices of agricultural and energy goods, has remained relatively tame at the 1-1.5% per annum level, as has been the case in the past few years.

Moreover, given the excess production capacity in many key industries, such as steel, cement, and glass, it is unlikely that there will be much inflation in the prices of goods.

Lawrence J. Lau 1414

Monthly Rates of Change of the Consumer Price Index (CPI), Y-o-Y

Monthly Rates of Change of Consumer Price Index and Its Components Since 1994, Y-o-Y

-10

0

10

20

30

40

50

Jan-

94A

pr-9

4Ju

l-94

Oct

-94

Jan-

95A

pr-9

5Ju

l-95

Oct

-95

Jan-

96A

pr-9

6Ju

l-96

Oct

-96

Jan-

97A

pr-9

7Ju

l-97

Oct

-97

Jan-

98A

pr-9

8Ju

l-98

Oct

-98

Jan-

99A

pr-9

9Ju

l-99

Oct

-99

Jan-

00A

pr-0

0Ju

l-00

Oct

-00

Jan-

01A

pr-0

1Ju

l-01

Oct

-01

Jan-

02A

pr-0

2Ju

l-02

Oct

-02

Jan-

03A

pr-0

3Ju

l-03

Oct

-03

Jan-

04A

pr-0

4Ju

l-04

Oct

-04

Jan-

05A

pr-0

5Ju

l-05

Oct

-05

Jan-

06A

pr-0

6Ju

l-06

Oct

-06

Jan-

07A

pr-0

7Ju

l-07

Oct

-07

Jan-

08A

pr-0

8Ju

l-08

Oct

-08

Jan-

09A

pr-0

9Ju

l-09

Oct

-09

Jan-

10A

pr-1

0Ju

l-10

Oct

-10

Jan-

11

Perc

ent p

er a

nnum

CPI

CPI: Food

CPI: Clothing

CPI: Transport & Telecome

Lawrence J. Lau 1515

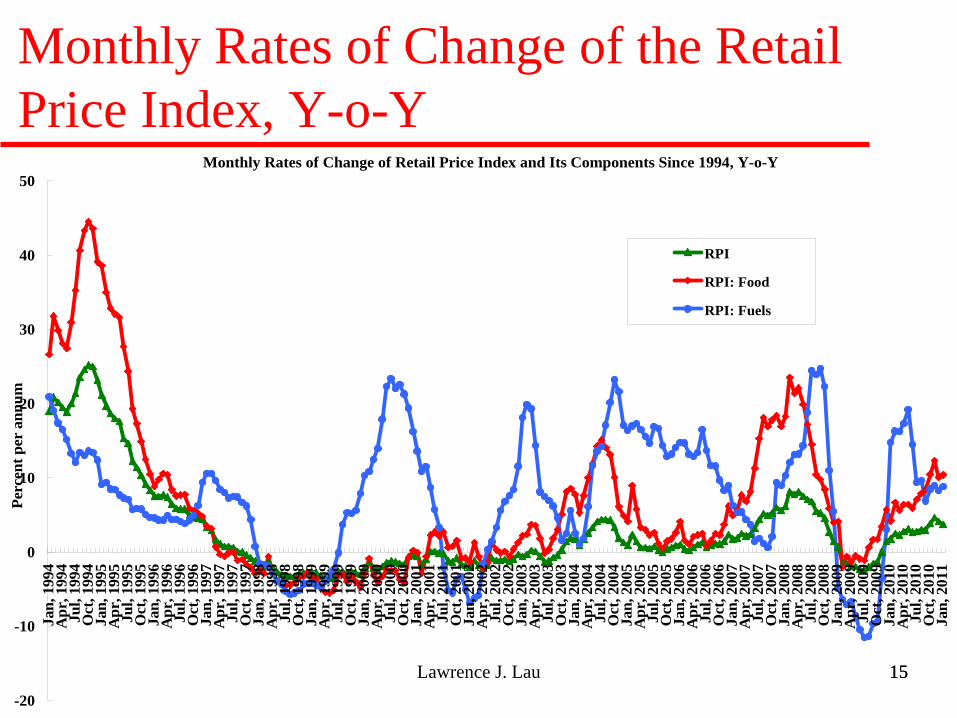

Monthly Rates of Change of the Retail Price Index, Y-o-Y

Monthly Rates of Change of Retail Price Index and Its Components Since 1994, Y-o-Y

-20

-10

0

10

20

30

40

50

Jan,

199

4A

pr, 1

994

Jul,

1994

Oct

, 199

4Ja

n, 1

995

Apr

, 199

5Ju

l, 19

95O

ct, 1

995

Jan,

199

6A

pr, 1

996

Jul,

1996

Oct

, 199

6Ja

n, 1

997

Apr

, 199

7Ju

l, 19

97O

ct, 1

997

Jan,

199

8A

pr, 1

998

Jul,

1998

Oct

, 199

8Ja

n, 1

999

Apr

, 199

9Ju

l, 19

99O

ct, 1

999

Jan,

200

0A

pr, 2

000

Jul,

2000

Oct

, 200

0Ja

n, 2

001

Apr

, 200

1Ju

l, 20

01O

ct, 2

001

Jan,

200

2A

pr, 2

002

Jul,

2002

Oct

, 200

2Ja

n, 2

003

Apr

, 200

3Ju

l, 20

03O

ct, 2

003

Jan,

200

4A

pr, 2

004

Jul,

2004

Oct

, 200

4Ja

n, 2

005

Apr

, 200

5Ju

l, 20

05O

ct, 2

005

Jan,

200

6A

pr, 2

006

Jul,

2006

Oct

, 200

6Ja

n, 2

007

Apr

, 200

7Ju

l, 20

07O

ct, 2

007

Jan,

200

8A

pr, 2

008

Jul,

2008

Oct

, 200

8Ja

n, 2

009

Apr

, 200

9Ju

l, 20

09O

ct, 2

009

Jan,

201

0A

pr, 2

010

Jul,

2010

Oct

, 201

0Ja

n, 2

011

Perc

ent p

er a

nnum

RPI

RPI: Food

RPI: Fuels

Lawrence J. Lau 1616

The Rates of Growth of Money Supply and Loans, Year-over-Year

The Rates of Growth of Money Supply and Loans, Year-over-Year

0

5

10

15

20

25

30

35

40

45

Jan-

01A

pr-0

1Ju

l-01

Oct

-01

Jan-

02A

pr-0

2Ju

l-02

Oct

-02

Jan-

03A

pr-0

3Ju

l-03

Oct

-03

Jan-

04A

pr-0

4Ju

l-04

Oct

-04

Jan-

05A

pr-0

5Ju

l-05

Oct

-05

Jan-

06A

pr-0

6Ju

l-06

Oct

-06

Jan-

07A

pr-0

7Ju

l-07

Oct

-07

Jan-

08A

pr-0

8Ju

l-08

Oct

-08

Jan-

09A

pr-0

9Ju

l-09

Oct

-09

Jan-

10A

pr-1

0Ju

l-10

Oct

-10

Jan-

11

Perc

ent

Money Supply (M1)

Money Supply (M2)

Loans

Lawrence J. Lau 17

The Macroeconomic Outlook

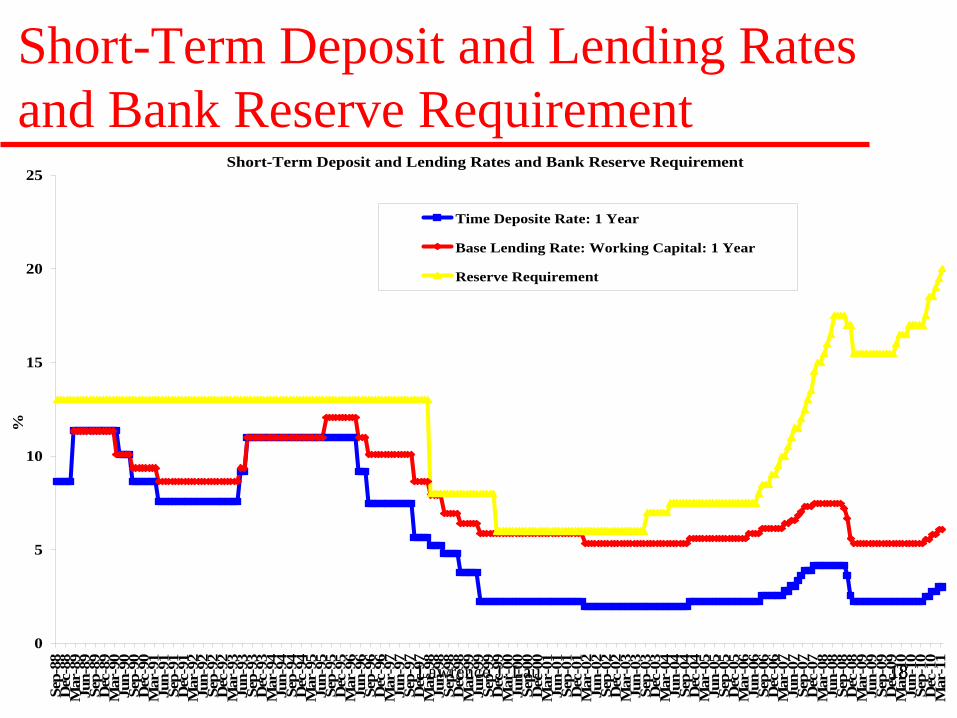

However, there has been significant inflation in the prices of assets such as real estate in the last year or two due to the implementation of the economic stimulus package and the significant increases in the rates of growth of money supply and commercial bank credit.

Measures have been taken recently to contain the asset price bubble. State-owned enterprises that have not been explicitly authorised are now forbidden to invest in real estate. Bank lending rules have also been tightened so as to discourage the purchases of more than one residential unit by a single household. Recently, the People’s Bank of China, the central bank, has increased the rate of interest and also the reserve requirement ratio a few times.

Lawrence J. Lau 1818

Short-Term Deposit and Lending Rates and Bank Reserve Requirement

Short-Term Deposit and Lending Rates and Bank Reserve Requirement

0

5

10

15

20

25

Sep-

88D

ec-8

8M

ar-8

9Ju

n-89

Sep-

89D

ec-8

9M

ar-9

0Ju

n-90

Sep-

90D

ec-9

0M

ar-9

1Ju

n-91

Sep-

91D

ec-9

1M

ar-9

2Ju

n-92

Sep-

92D

ec-9

2M

ar-9

3Ju

n-93

Sep-

93D

ec-9

3M

ar-9

4Ju

n-94

Sep-

94D

ec-9

4M

ar-9

5Ju

n-95

Sep-

95D

ec-9

5M

ar-9

6Ju

n-96

Sep-

96D

ec-9

6M

ar-9

7Ju

n-97

Sep-

97D

ec-9

7M

ar-9

8Ju

n-98

Sep-

98D

ec-9

8M

ar-9

9Ju

n-99

Sep-

99D

ec-9

9M

ar-0

0Ju

n-00

Sep-

00D

ec-0

0M

ar-0

1Ju

n-01

Sep-

01D

ec-0

1M

ar-0

2Ju

n-02

Sep-

02D

ec-0

2M

ar-0

3Ju

n-03

Sep-

03D

ec-0

3M

ar-0

4Ju

n-04

Sep-

04D

ec-0

4M

ar-0

5Ju

n-05

Sep-

05D

ec-0

5M

ar-0

6Ju

n-06

Sep-

06D

ec-0

6M

ar-0

7Ju

n-07

Sep-

07D

ec-0

7M

ar-0

8Ju

n-08

Sep-

08D

ec-0

8M

ar-0

9Ju

n-09

Sep-

09D

ec-0

9M

ar-1

0Ju

n-10

Sep-

10D

ec-1

0M

ar-1

1

%

Time Deposite Rate: 1 Year

Base Lending Rate: Working Capital: 1 Year

Reserve Requirement

Lawrence J. Lau 19

The Macroeconomic Outlook

There is not much any central bank can do about agricultural prices. No head of a central bank anywhere in the World has been able to control the weather.

The key in reining in asset prices, especially real estate prices, is to assure that there is a continuing dependable and steady supply going forward. Only the expectation of supply availability can change price expectations. The Government must therefore try to create the expectation of regular increases of actual and potential supply through its policy and its actual behaviour.

Lawrence J. Lau 20

The Macroeconomic Outlook

If the public expects that residential units will be just as available next year, and hence concludes that there is no need to rush out to buy something now, the real estate price bubble can be more readily contained.

Other instruments in addition to the rate of interest include the strict control, perhaps even prohibition, of financing of any non-owner-occupied residential unit, and increasing the equity (down payment) ratio. The introduction of a property tax as a source of revenue for local governments will also help to discourage speculation as well as reduce the dependence of local governments on revenue from the sale of land leases and hence on maintaining high and rising expectations of land prices.

Lawrence J. Lau 21

The Macroeconomic Outlook

Even with increases in the levels of minimum wage rates in the different provinces, regions and municipalities, the real wage rate of unskilled, entry-level labour has basically remained stable and is expected to be stable for a long time because of the continuing existence of significant surplus labour in the Chinese economy.

However, there is upward pressure on the real wage rates of skilled and experienced labour, which is actually in short supply, especially as Chinese enterprises move up the value-added chain. The recent high-profile wage settlements made by Honda and Foxconn plants in China provided for wage increases of 24 percent and 30 percent respectively.

But given the trend of rapid expansion of Chinese tertiary education in recent years, with 6 million new graduates projected annually, the increase in the real wage rate of even skilled labour is likely to be relatively limited going forward.

Lawrence J. Lau 22

The Relative Unimportance of International Trade

There is a common mis-impression that the Chinese economy is highly dependent on exports, and in particular, on its export surpluses, as a source of growth.

The facts are that China only began to have a significant trade surplus vis-a-vis the World in 2005, whereas the Chinese economy has been growing at an average real rate of approximately 10 percent per annum since 1978.

It should therefore be clear that the trade surpluses could not have been an important source of growth for the Chinese economy during the past three decades. Chinese economic growth does not depend on Chinese trade surpluses.

Lawrence J. Lau 23

The Trade Surplus has been Declining

The Chinese trade surplus has continued to decline, especially as a percentage of GDP. This trend is expected to continue. I expect Chinese international trade vis-à-vis the whole world to be essentially balanced in a couple of years, without necessarily any large adjustments in the Yuan exchange rate.

One reason that this is possible is the gradual closing of the savings-investment gap in China, as well as the substantial real appreciation of the Yuan versus the U.S.$ that has occurred since mid-2005, to the tune of 25%.

Lawrence J. Lau 2424

Chinese Monthly Exports, Imports and Trade Balance, US$

Chinese Monthly Exports, Imports and Trade Balance of Goods, in U.S. Dollars

-10

0

10

20

30

40

50

60

70

80

90

100

110

120

130

140

150

160

Jan-

92A

pr-9

2Ju

l-92

Oct

-92

Jan-

93A

pr-9

3Ju

l-93

Oct

-93

Jan-

94A

pr-9

4Ju

l-94

Oct

-94

Jan-

95A

pr-9

5Ju

l-95

Oct

-95

Jan-

96A

pr-9

6Ju

l-96

Oct

-96

Jan-

97A

pr-9

7Ju

l-97

Oct

-97

Jan-

98A

pr-9

8Ju

l-98

Oct

-98

Jan-

99A

pr-9

9Ju

l-99

Oct

-99

Jan-

00A

pr-0

0Ju

l-00

Oct

-00

Jan-

01A

pr-0

1Ju

l-01

Oct

-01

Jan-

02A

pr-0

2Ju

l-02

Oct

-02

Jan-

03A

pr-0

3Ju

l-03

Oct

-03

Jan-

04A

pr-0

4Ju

l-04

Oct

-04

Jan-

05A

pr-0

5Ju

l-05

Oct

-05

Jan-

06A

pr-0

6Ju

l-06

Oct

-06

Jan-

07A

pr-0

7Ju

l-07

Oct

-07

Jan-

08A

pr-0

8Ju

l-08

Oct

-08

Jan-

09A

pr-0

9Ju

l-09

Oct

-09

Jan-

10A

pr-1

0Ju

l-10

Oct

-10

Jan-

11

USD

bill

ions Exports, fob

Imports, cif

Trade Balance

Lawrence J. Lau 25

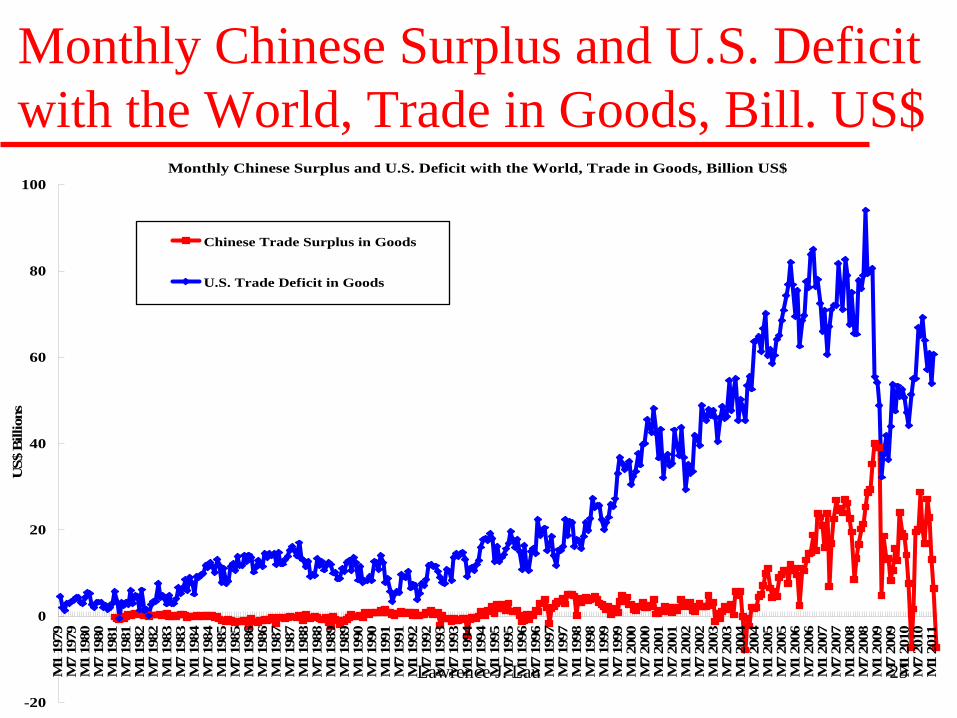

Monthly Chinese Surplus and U.S. Deficit with the World, Trade in Goods, Bill. US$

Monthly Chinese Surplus and U.S. Deficit with the World, Trade in Goods, Billion US$

-20

0

20

40

60

80

100

M1

1979

M7

1979

M1

1980

M7

1980

M1

1981

M7

1981

M1

1982

M7

1982

M1

1983

M7

1983

M1

1984

M7

1984

M1

1985

M7

1985

M1

1986

M7

1986

M1

1987

M7

1987

M1

1988

M7

1988

M1

1989

M7

1989

M1

1990

M7

1990

M1

1991

M7

1991

M1

1992

M7

1992

M1

1993

M7

1993

M1

1994

M7

1994

M1

1995

M7

1995

M1

1996

M7

1996

M1

1997

M7

1997

M1

1998

M7

1998

M1

1999

M7

1999

M1

2000

M7

2000

M1

2001

M7

2001

M1

2002

M7

2002

M1

2003

M7

2003

M1

2004

M7

2004

M1

2005

M7

2005

M1

2006

M7

2006

M1

2007

M7

2007

M1

2008

M7

2008

M1

2009

M7

2009

M1

2010

M7

2010

M1

2011

US$

Bill

ions

Chinese Trade Surplus in Goods

U.S. Trade Deficit in Goods

Lawrence J. Lau 26

Chinese National Savings and Gross Domestic Investment as Percents of GDP

Chinese National Savings and Gross Domestic Investment as a Percent of GDP since 1952

0

10

20

30

40

50

60

1952

1953

1954

1955

1956

1957

1958

1959

1960

1961

1962

1963

1964

1965

1966

1967

1968

1969

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Perc

ent

Savings Rate

Investment Rate

Lawrence J. Lau 27

Case-Shiller U.S. Home Price Index, Chinese Trade Surplus & U.S. Trade Deficit, Bill. US$

Case-Shiller U.S. Home Price Index, Chinese Trade Surplus and U.S. Trade Deficit

60

80

100

120

140

160

180

200

220

Jan-

00A

pr-0

0Ju

l-00

Oct

-00

Jan-

01A

pr-0

1Ju

l-01

Oct

-01

Jan-

02A

pr-0

2Ju

l-02

Oct

-02

Jan-

03A

pr-0

3Ju

l-03

Oct

-03

Jan-

04A

pr-0

4Ju

l-04

Oct

-04

Jan-

05A

pr-0

5Ju

l-05

Oct

-05

Jan-

06A

pr-0

6Ju

l-06

Oct

-06

Jan-

07A

pr-0

7Ju

l-07

Oct

-07

Jan-

08A

pr-0

8Ju

l-08

Oct

-08

Jan-

09A

pr-0

9Ju

l-09

Oct

-09

Jan-

10A

pr-1

0Ju

l-10

Oct

-10

Jan-

11

2000

Q1=

100

-10

0

10

20

30

40

50

60

70

80

90

100

USD

bill

ions

Case-Shiller Home Price Index

U.S. Trade Deficit with the World

Chinese Trade Surplus with the World

Lawrence J. Lau 2828

The Nominal and Real Yuan/US$ Exchange Rates

The Nominal and Real Yuan/US$ Exchange Rates (1994 prices)

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

8.5

9.0

Jan-

94A

pr-9

4Ju

l-94

Oct

-94

Jan-

95A

pr-9

5Ju

l-95

Oct

-95

Jan-

96A

pr-9

6Ju

l-96

Oct

-96

Jan-

97A

pr-9

7Ju

l-97

Oct

-97

Jan-

98A

pr-9

8Ju

l-98

Oct

-98

Jan-

99A

pr-9

9Ju

l-99

Oct

-99

Jan-

00A

pr-0

0Ju

l-00

Oct

-00

Jan-

01A

pr-0

1Ju

l-01

Oct

-01

Jan-

02A

pr-0

2Ju

l-02

Oct

-02

Jan-

03A

pr-0

3Ju

l-03

Oct

-03

Jan-

04A

pr-0

4Ju

l-04

Oct

-04

Jan-

05A

pr-0

5Ju

l-05

Oct

-05

Jan-

06A

pr-0

6Ju

l-06

Oct

-06

Jan-

07A

pr-0

7Ju

l-07

Oct

-07

Jan-

08A

pr-0

8Ju

l-08

Oct

-08

Jan-

09A

pr-0

9Ju

l-09

Oct

-09

Jan-

10A

pr-1

0Ju

l-10

Oct

-10

Jan-

11

Yua

n pe

r U

.S. D

olla

r The Nominal Exchange Rate, Yuan/US$

The Real Exchange Rate, Yuan/US$

Lawrence J. Lau 29

The Relative Unimportance of International Trade

Chinese trade surplus as a percent of Chinese GDP fluctuated between -4.5 percent and 4.5 percent between 1982 and 2004 with an average of less than 2 percent of GDP. It then rose to almost 9 percent in 2007. It has since declined significantly and is around 3 percent. It is expected to continue to decline over the next few years.

Lawrence J. Lau 30

Chinese Trade Balance of Goods & Services as a Percent of GDP, 1982-

Chinese Trade Balance of Goods and Services as a Percent of GDP

-6

-4

-2

0

2

4

6

8

10

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Perc

ent

Lawrence J. Lau 31

The Relative Unimportance of International Trade

Chinese exports as a ratio of GDP rose steadily beginning in 1978 and reached a peak of almost 40 percent in 2006 and then began to decline to approximately 25 percent in 2009.

While this ratio appears large, it is not when compared to Hong Kong, Singapore, South Korea and Taiwan, where exports are more than 100 percent of the respective GDPs.

And the Chinese Exports/GDP ratio actually exaggerates the importance of exports in the Chinese economy because it fails to take into account the low domestic value-added content of Chinese exports.

Lawrence J. Lau 32

Chinese Exports of Goods and Services as a Percent of GDP, 1970-present

Chinese Exports of Goods and Services as a Ratio of GDP since 1970

0

5

10

15

20

25

30

35

40

45

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Perc

ent

Lawrence J. Lau 33

The Relative Unimportance of International Trade

The fact that the Chinese economy has continued to grow at an average rate of approximately 10% per annum since the beginning of the global financial crisis in 2007 is ample proof that the Chinese economy has been at least partially de-coupled from the rest of the World, and in particular, from the United States and Europe, both of which have been and still are mired in economic recession.

Lawrence J. Lau 34

Concluding Remarks

The long-term sustainable sources of Chinese aggregate demand will be internal: household and public consumption, investment in infrastructure, including high- speed inter-urban trains, owner-occupied residential housing, investment in education and health care, urbanisation (building new cities), urban mass-transit systems, environmental protection and preservation, energy conservation and renewable energy, and the green economy.

Consumption will rise, as GDP per capita and wage rate rise and the social safety net is gradually perfected. But savings rate will remain high for a long time.

Lawrence J. Lau 35

Concluding Remarks

International trade will continue to be somewhat important, but not critical, to the growth of the Chinese economy. Exports as a share of Chinese GDP will probably continue to decline over time, as befitting a large, continental economy. Chinese economic growth will be marginally, but not critically, affected by a large decline in its exports, as demonstrated by its experience in the past couple of years as well as during the 1997-1998 East Asian currency crisis. Thus, it will be able to survive even prolonged economic recessions in the European and U.S. economies.

Lawrence J. Lau 36

Concluding Remarks

For 2011, the short-term economic targets are to achieve a rate of growth of 8 percent and a rate of inflation of 4 percent. I am confident that both targets are achievable.