Embed Size (px)

Citation preview

275

RAFAEL LA PORTADartmouth College

ANDREI SHLEIFERHarvard University

The Unofficial Economy and Economic Development

ABSTRACT In developing countries, informal firms account for up to abouthalf of all economic activity. Using data from World Bank firm-level surveys,we find that informal firms are small and extremely unproductive comparedwith even the small formal firms in the sample, and especially relative to thelarger formal firms. Formal firms are run by much better educated managersthan informal ones and use more capital, have different customers, markettheir products, and use more external finance. Few formal firms have ever oper-ated informally. This evidence supports the dual economy (“Wal-Mart”) theoryof development, in which growth comes about from the creation of highly pro-ductive formal firms. Informal firms keep millions of people alive but disappearas the economy develops.

In many developing countries, unofficial economic activity—that con-ducted by unregistered firms or by registered firms but hidden from

taxation—accounts for between a third and a half of the total. This sharedeclines sharply as the economy develops. Despite the sheer magnitude ofunofficial activity, little is understood about its role in economic develop-ment, and in particular about how important “officializing” this hiddenactivity and the resources devoted to it might be for economic growth.

In this paper we attempt to shed some light on these issues by presentingsome new facts about the unofficial (also called “informal”) economy andinterpreting them in light of various theories. We begin by reviewing thebasic stylized facts: that the unofficial economy is huge, that it shrinkssharply in relative terms as the economy develops, and that various policyvariables that determine the costs and benefits of becoming and stayingofficial influence its size. This evidence is consistent with the generally

11472-06_La Porta_rev2.qxd 3/6/09 1:13 PM Page 275

accepted view that unofficial firms avoid paying taxes and adhering to reg-ulations, but lose access to public goods and other benefits of official status,such as external finance. Much of the existing literature on the unofficialeconomy emphasizes these public policy aspects of the problem.1

Yet crucial as this perspective might be, it says little about the role ofunofficial firms in development. There are three broad views of this role,which we refer to as the romantic view, the parasite view, and the dualeconomy (“dual” for short) view. According to the romantic view, whichwe associate with the work of Hernando de Soto,2 unofficial firms are eitheractually or potentially extremely productive but are held back by govern-ment taxes and regulations, as well as by lack of secure property rights andaccess to finance. Pending the necessary legal reforms, “four billion peoplearound the world are robbed of the chance to better their lives and climb outof poverty, because they are excluded from the rule of law.”3 If the barriersto official status were lowered and capital supplied through microfinance,unofficial firms would register, borrow, and take advantage of other benefitsof official status, and by doing so expand and spark economic growth. Thekey aspect of this optimistic view is that unofficial firms are fundamentallysimilar to official ones but are kept down by policy. In particular, unofficialfirms should look similar to official firms with respect to characteristics notaffected by government policies, such as the characteristics of their entre-preneurs (for example, their education).

The other two views are more skeptical about unofficial firms and in par-ticular see them as quite unproductive, not just because they are deprived ofthe benefits of official status, but also because they are run by entrepreneurswith lower human capital. In these alternative views, development comesabout not so much from the unleashing of informal firms as from their dis-placement by efficient formal firms, usually run by totally different people.This is the “Wal-Mart” theory of development.

The latter two views differ in what they see as the benefits and theharms of the unofficial sector. The parasite view, associated primarily withthe excellent empirical studies by the McKinsey Global Institute, seesunofficial firms primarily from the perspective of their illegality. These

276 Brookings Papers on Economic Activity, Fall 2008

1. This literature includes de Soto (1989), Loayza (1996), Johnson, Kaufmann, andShleifer (1997), Friedman and others (2001), Djankov and others (2002), Almeida andCarneiro (2006), Dabla-Norris, Gradstein, and Inchauste (2008), and Russo (2008), as wellas the recent work on Brazil by De Paula and Scheinkman (2008), Monteiro and Assunção(2006), and Fajnzylber, Maloney, and Montes Rojas (2006).

2. De Soto (1989, 2000).3. United Nations (2008, p. 1).

11472-06_La Porta_rev2.qxd 3/6/09 1:13 PM Page 276

firms need to stay small to avoid detection and therefore lack the necessaryscale to produce efficiently. However, the “substantial cost advantage thatinformal companies gain by avoiding taxes and regulations more than off-sets their low productivity and small scale.”4 This cost advantage allowsunofficial firms to undercut the prices of official firms. Informal firms, then,hurt growth both because their small scale makes them unproductive andbecause they take away market share from bigger, more productive formalcompetitors. According to one McKinsey report, “The high proportion ofsmall firms in service industries makes them particularly likely to operateinformally, ignoring tax requirements, employee benefits, and other regu-lations. This is a much larger barrier to growth than most policymakersin emerging—and developed—economies acknowledge. Steps to reduceinformality in local service sectors will be rewarded by rapid increases intheir productivity, growth, and employment.”5 The first step in redressingthe problems created by informal firms is to “add resources and beef up agovernment’s audit capabilities.”6 More broadly, government policy shouldaim to eradicate informal firms by reducing tax evasion and increasing theenforcement of government regulations.

The dual view, associated in our minds with traditional developmenteconomics,7 likewise emphasizes the inherent inefficiency of unofficialfirms. This view is intimately related to the “big push” models of develop-ment economics, which see the coordinated transition from the informal,preindustrial economy to the formal, industrial one as the crucial strategyof economic development.8 The earliest formal model of the unofficialeconomy is that of James Rauch,9 who uses the framework of Robert Lucasto consider the allocation of talent between the unofficial and the officialsectors.10 In Rauch’s framework, workers with lower human capital workin informal and smaller firms and receive lower wages, whereas those withhigher human capital are allocated to the larger and more productive firmsand receive higher wages.11

Unlike the romantic view, the dual view predicts that unofficial firmsshould look very different from official firms in their characteristics not

RAFAEL LA PORTA and ANDREI SHLEIFER 277

4. Farrell (2004, p. 28).5. Baily, Farrell, and Remes (2005, p. 18).6. Farrell (2004, p. 34).7. Harris and Todaro (1970).8. For example, Rosenstein-Rodan (1943); Rostow (1960); Murphy, Shleifer, and

Vishny (1989).9. Rauch (1991).

10. Lucas (1978).11. See also Amaral and Quintin (2006) and de Paula and Scheinkman (2008).

11472-06_La Porta_rev2.qxd 3/6/09 1:13 PM Page 277

affected by government policies. Productive entrepreneurs are willing topay taxes and bear the cost of government regulation in order to advertisetheir products, raise outside capital, and access public goods. Such entre-preneurs find it more profitable to run the bigger, official firms than thesmaller, unofficial ones. In contrast, the increase in firm value that less ableentrepreneurs or managers could generate by operating formally is notlarge enough to offset the additional costs from taxes and regulations. Thestrong prediction of the dual view is that managers and assets are matchedthrough a sorting process that results in low-ability managers being pairedwith low-quality assets.

Unlike the parasite view, the dual view does not see the unofficial firmsas threatening the official ones, because they are hugely inefficient andhence unlikely to be able to charge lower prices for the same products.Indeed, official and unofficial firms operate largely in different marketsand have different customers. The dual view sees the unofficial firms asproviders of a livelihood to millions, perhaps billions, of extremely poorpeople,12 and it cautions against any policies that would raise the costs ofthese firms. This view sees the hope of economic development in policies,such as human capital, tax, and regulatory policies, that promote the creationof official firms, letting the unofficial ones die as the economy develops.The official firms thus created will be new firms run by new people, notpreviously unofficial firms.13

To shed light on these alternative views, this paper follows the presen-tation of basic correlations with a comparative analysis of the characteris-tics and productivity of official and unofficial firms in several developingcountries. We use three sets of surveys of both official and unofficial firmsconducted recently by the World Bank. The first set, known as EnterpriseSurveys, covers small, medium-size, and large registered firms in nearly100 countries. We use these surveys largely for comparison. The secondset, known as Informal Surveys, covers primarily unregistered, but alsosome registered, small firms in about a dozen countries. The third set, knownas Micro Surveys, covers primarily registered, but also some unregistered,small firms in about a dozen countries (mostly different from those coveredby the Informal Surveys). These surveys enable us to make comparative

278 Brookings Papers on Economic Activity, Fall 2008

12. Tokman (1992).13. The sharp distinction we have drawn between the parasite and the dual views is too

extreme. For example, informal firms may compete with formal ones in some industries andnot in others, and they might pose a greater competitive threat at higher levels of economicdevelopment, when they perhaps become more similar to formal firms. We will return to thediscussion of the relevance of the two views after presenting some of the data.

11472-06_La Porta_rev2.qxd 3/6/09 1:13 PM Page 278

statements about the size, inputs, management characteristics, and—in arough way—productivity of both official and unofficial firms.

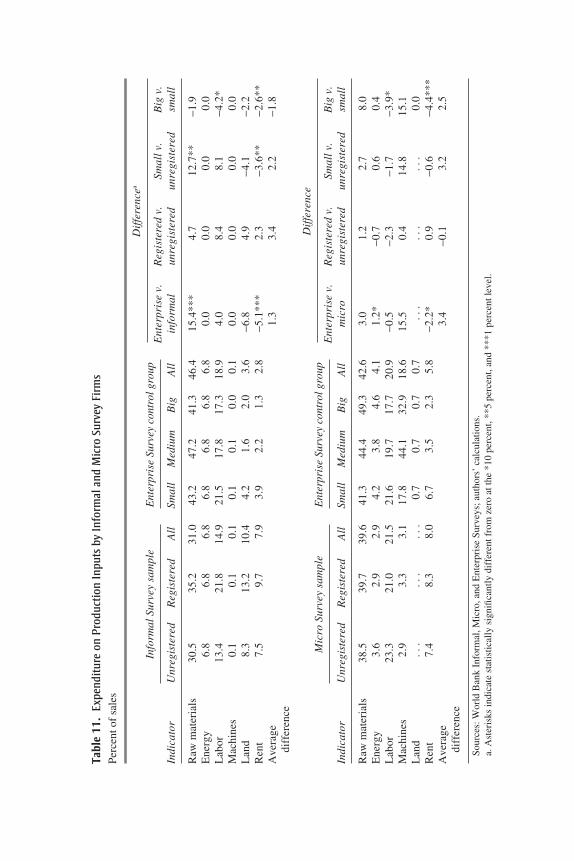

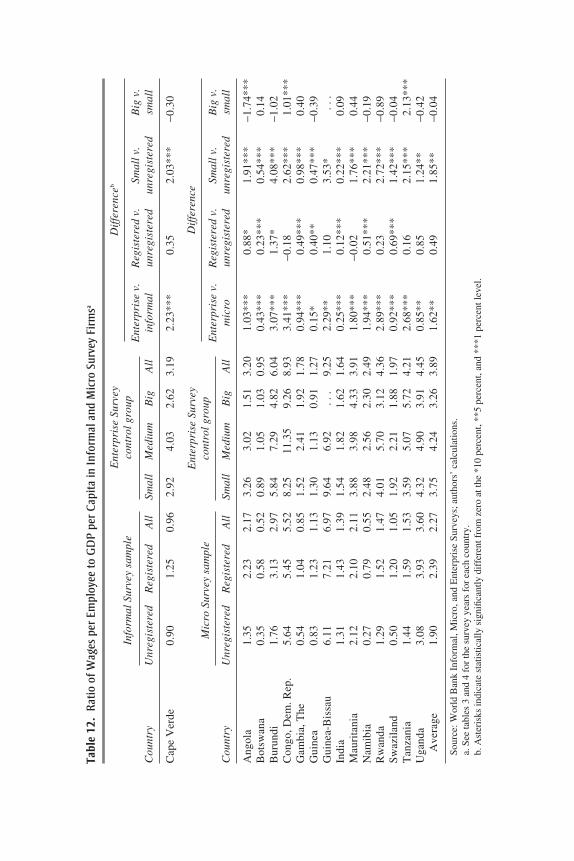

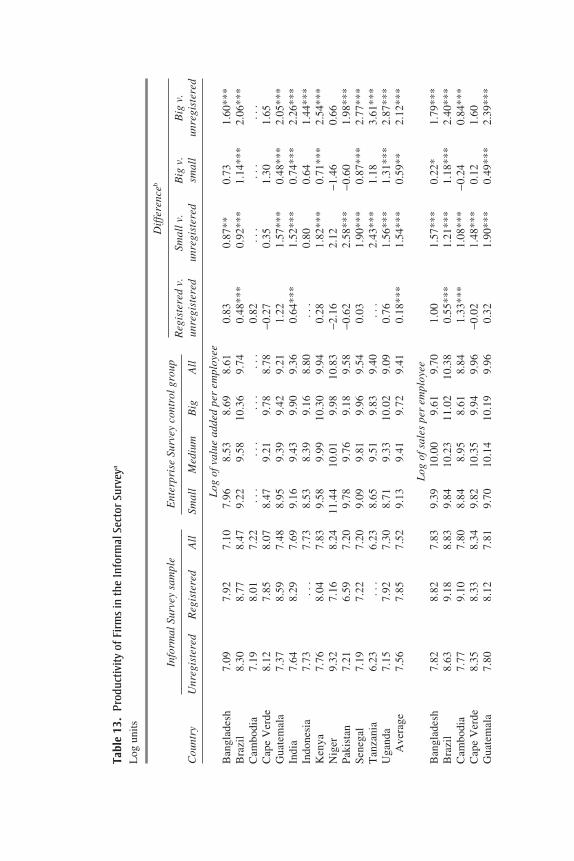

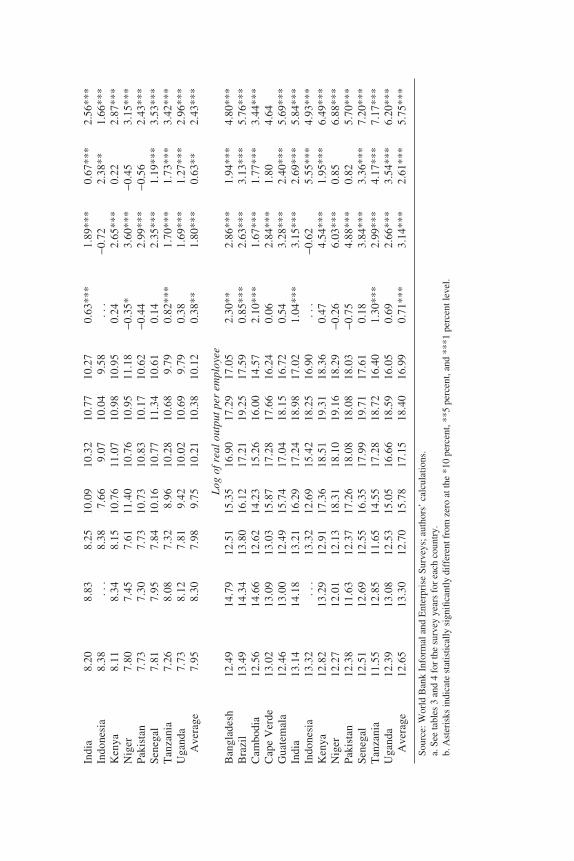

We note from the start that the data we use have many problems, notleast because we focus on firms that are by definition avoiding the gov-ernment’s notice. Nonetheless, our findings tend to favor the dual viewover the romantic and the parasite views. The unofficial firms in the sur-veys tend to be small and unproductive compared even with the small butregistered firms (which themselves are much less productive than largerregistered firms). The unofficial firms also use lower-quality inputs andhave less access to public goods and finance. Extremely few of the regis-tered firms have ever operated as unregistered, again suggesting, as arguedby Rauch,14 that the two groups are very separate animals. The evidencepoints to a substantial difference between the registered and the unregis-tered firms in the human capital of their managers and suggests that thisgap in human capital drives many other differences, including the qualityof inputs and access to finance. The unregistered firms pay sharply lowerwages to their employees, again consistent with the dual model.

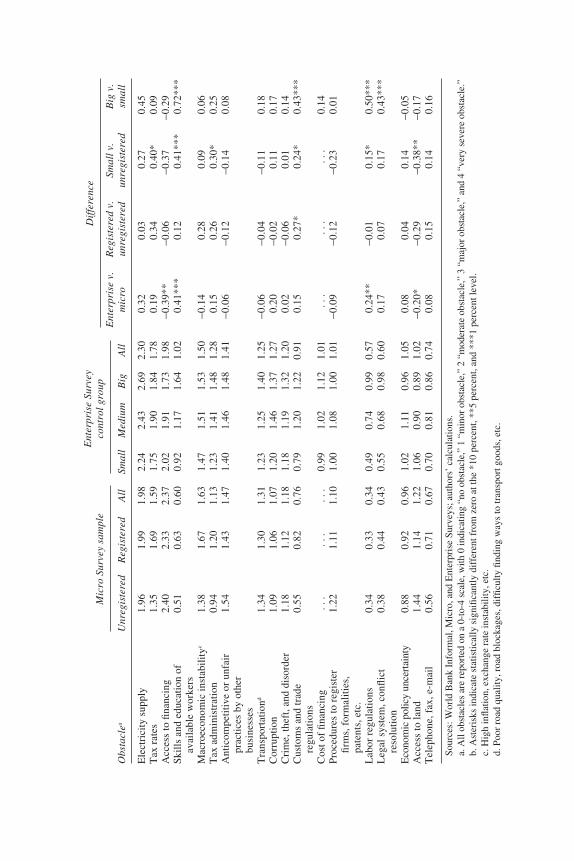

As a final step, we consider how firms perceive their obstacles todoing business as reported in the three surveys. Informal firms see lackof access to markets and finance as their biggest problems. Formal firmsalso emphasize those, but taxes, tax administration, and problems withelectricity supply as well. The legal system, regulations, and registrationprocedures rank lower as obstacles to doing business among both formaland informal firms. Finally, the surveys offer little evidence that theunregistered firms pose much of a competitive threat to the registered ones:the latter do not treat such competition (or unfair competition more gen-erally) as a serious problem. This last result does not support the parasiteview of the unofficial economy, which focuses on price undercutting byinformal firms.

Over all, the evidence paints a relatively consistent picture. There isvery little support for the romantic view, and indeed the differences in pro-ductivity between formal and informal firms are so large that it is hard tobelieve that simply registering unregistered firms would eliminate the gap.On the other hand, there is little support for the parasite view either, and theevidence suggests that subjecting unofficial firms to stronger enforcementwould devastate the livelihood of millions of people surviving near sub-sistence. The evidence rather points to the dual view, with the fairly stan-dard implication that the hope of economic development lies in the creation

RAFAEL LA PORTA and ANDREI SHLEIFER 279

14. Rauch (1991).

11472-06_La Porta_rev2.qxd 3/6/09 1:13 PM Page 279

of large registered firms, run by educated managers and utilizing modernpractices, including modern technology, marketing, and finance.

The Size of the Informal Economy and Its Determinants

Measuring the informal economy is inherently difficult. To start with, theinformal economy encompasses very different phenomena. One is hiddenfirms. Such firms hide all of their output from the police, the tax authorities,or the regulators. Another phenomenon is hidden output. Output may behidden even by registered firms to reduce their tax liability. Both phenom-ena occur in all developing countries. Indeed, the face of informality maychange as the economy develops, from near-universal informality at earlierstages to mere tax avoidance as the economy grows richer.

Beyond these conceptual issues, there are serious practical problemsin measuring hidden firms and output. Nevertheless, a variety of methodshave been proposed. Since each method has its strengths and weaknesses,we gathered data on seven measures of the informal economy based onalternative methodologies and sources. All these measures of the informaleconomy are, if anything, likely to understate its true size.

Surveys are the most direct, although necessarily subjective, measure.We assembled data on two survey measures. The first is an indicator ofunofficial or unregistered business activity from the World EconomicForum’s Global Competitiveness Report 2006–2007.15 Top businessleaders from 125 countries were asked to estimate the size of the infor-mal sector using a 1-to-7 scale, where 1 indicates that more than 50 per-cent of economic activity is unrecorded and 7 that all of it is registered.For comparability with the other measures, we rescaled this index on ascale from 0 to 50 percent of GDP. The 50 percent cutoff adopted by theGlobal Competitiveness Report is arbitrary and introduces a downwardbias in this measure. The second survey measure is the percentage oftotal sales that a typical establishment reports for tax purposes, from theWorld Bank Enterprise Surveys. The respondents are the top managersof registered businesses in (mostly) developing countries. Accordingly,this measure of tax evasion likely understates the size of the informaleconomy, as entrepreneurs in the informal sector are not surveyed. Thismeasure of tax evasion is available for 95 countries. Most countries havebeen surveyed twice, and we average the available observations between2002 and 2006.

280 Brookings Papers on Economic Activity, Fall 2008

15. World Economic Forum (2007).

11472-06_La Porta_rev2.qxd 3/6/09 1:13 PM Page 280

An alternative method infers the size of the informal economy fromobservable variables, such as the incidence of micro- and small enterprises,the male participation rate in the labor force, the fraction of workers con-tributing to social security, electricity consumption, and currency in circu-lation. We gathered data on three such indicators.

The first is the percentage of the active labor force that is self-employed,where self-employment is defined by the International Labour Office toinclude “jobs where the remuneration is directly dependent upon the profitsderived from the goods and services produced,”16 but not work by unpaidfamily workers, although the incidence of informality among the latter isprobably high. This is admittedly a crude measure. In most developingcountries there is a strong association between self-employment and infor-mal activity, as most self-employed tend to be low-skilled, unregisteredworkers.17 Of course, self-employment in developing countries may be highnot only because informality is prevalent, but also because self-employmentis common in agriculture. For this reason our second objective indicatoris the percentage of workers in the nonagricultural sector who are self-employed. Other interpretations of self-employment are also possible. Inparticular, self-employment has been used as an indicator of entrepreneurialactivity in the United States. However, the vast majority of self-employedworkers in our data are, in fact, “own-account” workers who do not hire per-sons to work for them. Camilo Mondragón-Vélez and Ximena Peña-Pargashow along these lines that the self-employed are rarely business ownersin Colombia.18 Data on self-employment are collected through populationcensuses as well as through household or labor force surveys.19 Data on totaland nonagricultural self-employment are available for 133 countries and96 countries, respectively, from the International Labour Organization.

The third objective indicator is based on electricity consumption. Foreach country the ratio of electricity consumption to GDP for a base periodis calculated and then extrapolated to the present, assuming that the elastic-ity of electricity consumption to GDP is one.20 The size of the informalsector is then computed as the difference between GDP as estimated from

RAFAEL LA PORTA and ANDREI SHLEIFER 281

16. International Labour Office (2007).17. Loayza and Rigolini (2006).18. Mondragón-Vélez and Peña-Parga (2008).19. There are two known biases in the self-employment data. First, OECD statistics

relate to civilian employment and, as such, leave out the armed forces. Second, self-employment statistics in most Latin American countries relate to urban areas only. Bothbiases tend to understate the true size of self-employment.

20. Johnson and others (1997); Ernste and Schneider (1998).

11472-06_La Porta_rev2.qxd 3/6/09 1:13 PM Page 281

this ratio and official GDP. This measure of the informal economy under-states its size to the extent that informal activities are less electricity inten-sive than formal activities, and to the extent that technological progressallows for increased output per unit of electricity. This indicator is avail-able for 57 countries from Eric Friedman and coauthors.21

Still another approach to measuring the informal economy models hid-den output as a latent variable, using several indicator and causal variables.This is the approach followed by Friedrich Schneider to estimate a multi-ple indicators, multiple causes (MIMIC) model.22 The indicator variablesinclude the labor force participation rate among persons aged 18–64, annualGDP growth, and the change in local currency in circulation per capita.The causal variables are the tax-to-GDP ratio, the Heritage Foundationindex of economic freedom, the unemployment rate, GDP per capita, andlagged values of the latent variable. This measure of the informal economy,which is available for 145 countries,23 is only as good as the model thatsupports it. Later in this section we present evidence that the correlationbetween the size of the informal economy and variables such as tax rates isnot particularly robust.

As a final robustness check, we gathered data on a direct measure of theformal economy: the number of registered businesses per 1,000 inhabitants.This measure, too, has problems. The number of firms per capita mayincrease with development, for example, as product variety expands. Itmay also be affected by cross-country differences in entrepreneurship.Finally, the data on total registered firms may be biased upward, especiallyin developing countries, because of underreporting of firms that have closedor exited. Data on the number of registered businesses are available for83 countries from the World Bank’s World Development Indicators dataset.

We group the determinants of the size of the unofficial economy intothree broad categories: the cost of becoming formal, the cost of stayingformal, and the benefits of being formal. As a proxy for the cost of becom-ing formal, we use the logarithm of the number of procedures required tolegally start a business, from the 2002 paper by Simeon Djankov andcoauthors and the World Bank’s Doing Business 2008.24 The costs of stay-ing formal include paying taxes and obeying government regulations; weuse six proxies for these costs. First, we use two measures of the cost of

282 Brookings Papers on Economic Activity, Fall 2008

21. Friedman and others (2001).22. Schneider (2007).23. Schneider (2007).24. World Bank (2007); Djankov and others (2002).

11472-06_La Porta_rev2.qxd 3/6/09 1:13 PM Page 282

paying taxes, from a 2008 paper by Djankov and coauthors:25 total taxes(except for labor taxes) payable by businesses after accounting for deduc-tions and exemptions; and the time it takes to prepare, file, and pay (orwithhold) corporate income tax, value-added tax, and social security con-tributions, in hours per year. Second, we capture the cost of complyingwith labor laws with three variables: an index of the difficulty of hiring anew worker; an index of the difficulty and expense of firing a redundantworker; and the nonwage labor costs (payroll taxes and social security pay-ments) associated with hiring a new worker as a percentage of the worker’ssalary. Data on complying with labor laws are from Juan Botero and coau-thors and Doing Business 2008.26 Third, we capture the cost of red tapeusing the percentage of senior management’s time spent in dealing withrequirements imposed by government regulations (such as taxes, cus-toms, labor regulations, licensing, and registration); this includes timespent interacting with officials, completing forms, and other tasks. Thisvariable is from the World Bank’s Enterprise Surveys.

The benefits of being formal include expanded access to both publicgoods and finance. Regarding public goods, registered business may find iteasier than unregistered ones to use the courts to enforce property rightsand adjudicate disputes. We use two proxies for the efficiency of courts:the log of the number of steps required to collect on a bounced check, fromthe 2003 paper by Djankov and coauthors and Doing Business 2008;27

and the efficiency of the bankruptcy procedure, from a recent paper byDjankov and coauthors.28 We measure the quality of property rights usingindices of corruption and the rule of law from Daniel Kaufmann, Aart Kraay,and Massimo Mastruzzi.29 In addition, we use the density of the paved roadnetwork from World Development Indicators as a rough proxy for thescope of the domestic market. Finally, we measure the benefits of access tofinance using three indicators of the size of financial markets. The firsttwo indicators are standard: private credit and the market capitalization ofdomestic firms, both as a ratio to GDP. These two variables are also fromthe World Development Indicators. The third measure of the size of finan-cial markets is a subjective indicator of the ease of access to credit, fromthe World Economic Forum’s Global Competitiveness Report 2006–2007.The index ranges from 1 (impossible) to 7 (easy).

RAFAEL LA PORTA and ANDREI SHLEIFER 283

25. Djankov and others (2008b).26. Botero and others (2004).27. Djankov and others (2003).28. Djankov and others (2008a).29. Kaufmann, Kraay, and Mastruzzi (2005).

11472-06_La Porta_rev2.qxd 3/6/09 1:13 PM Page 283

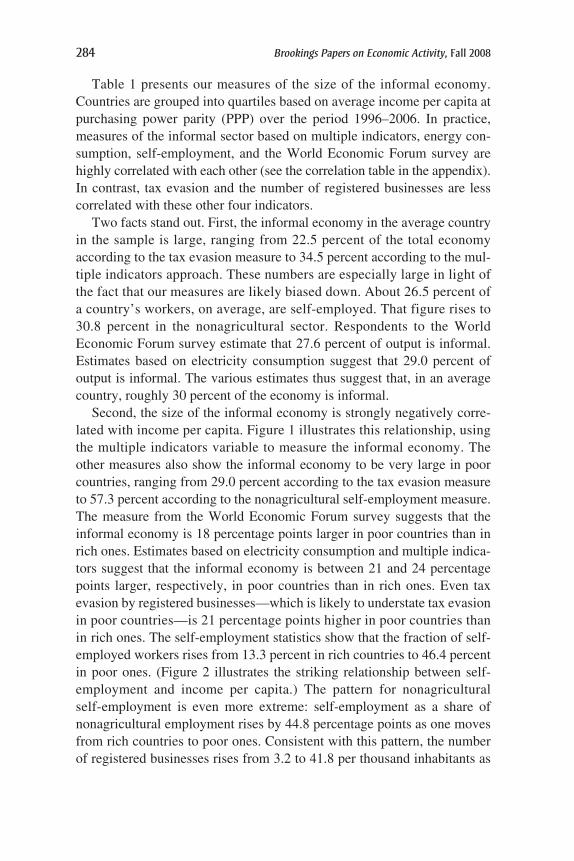

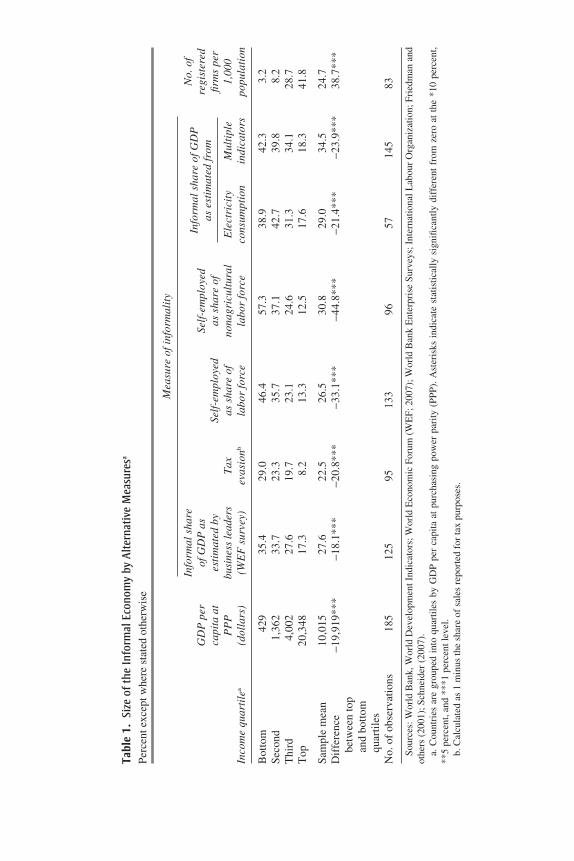

Table 1 presents our measures of the size of the informal economy.Countries are grouped into quartiles based on average income per capita atpurchasing power parity (PPP) over the period 1996–2006. In practice,measures of the informal sector based on multiple indicators, energy con-sumption, self-employment, and the World Economic Forum survey arehighly correlated with each other (see the correlation table in the appendix).In contrast, tax evasion and the number of registered businesses are lesscorrelated with these other four indicators.

Two facts stand out. First, the informal economy in the average countryin the sample is large, ranging from 22.5 percent of the total economyaccording to the tax evasion measure to 34.5 percent according to the mul-tiple indicators approach. These numbers are especially large in light ofthe fact that our measures are likely biased down. About 26.5 percent ofa country’s workers, on average, are self-employed. That figure rises to30.8 percent in the nonagricultural sector. Respondents to the WorldEconomic Forum survey estimate that 27.6 percent of output is informal.Estimates based on electricity consumption suggest that 29.0 percent ofoutput is informal. The various estimates thus suggest that, in an averagecountry, roughly 30 percent of the economy is informal.

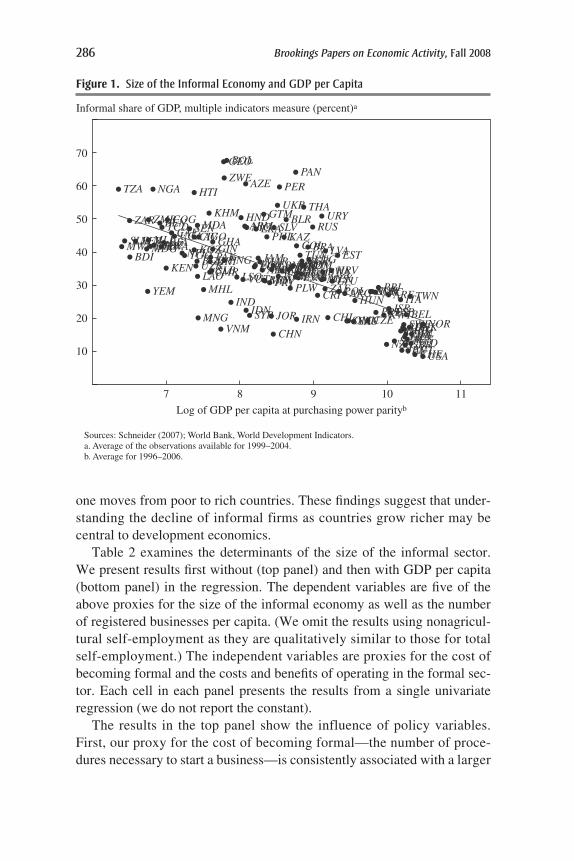

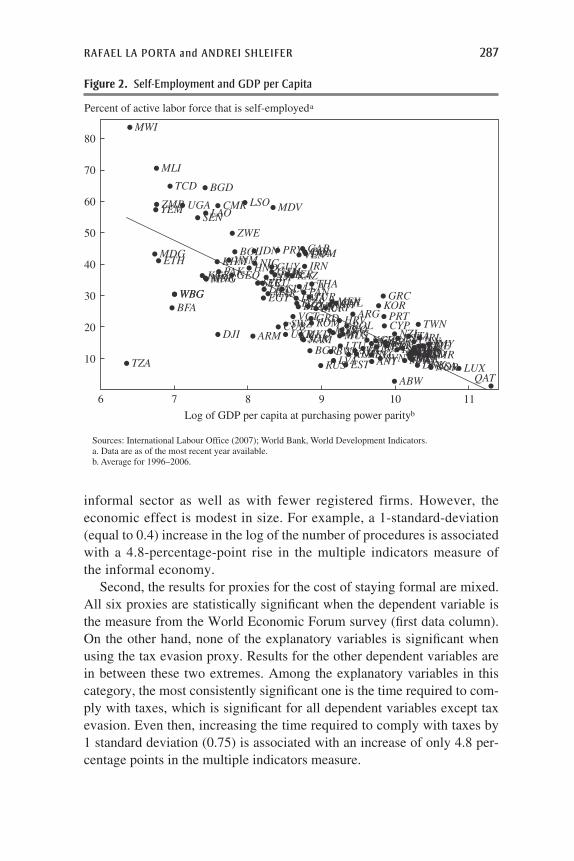

Second, the size of the informal economy is strongly negatively corre-lated with income per capita. Figure 1 illustrates this relationship, usingthe multiple indicators variable to measure the informal economy. Theother measures also show the informal economy to be very large in poorcountries, ranging from 29.0 percent according to the tax evasion measureto 57.3 percent according to the nonagricultural self-employment measure.The measure from the World Economic Forum survey suggests that theinformal economy is 18 percentage points larger in poor countries than inrich ones. Estimates based on electricity consumption and multiple indica-tors suggest that the informal economy is between 21 and 24 percentagepoints larger, respectively, in poor countries than in rich ones. Even taxevasion by registered businesses—which is likely to understate tax evasionin poor countries—is 21 percentage points higher in poor countries thanin rich ones. The self-employment statistics show that the fraction of self-employed workers rises from 13.3 percent in rich countries to 46.4 percentin poor ones. (Figure 2 illustrates the striking relationship between self-employment and income per capita.) The pattern for nonagriculturalself-employment is even more extreme: self-employment as a share ofnonagricultural employment rises by 44.8 percentage points as one movesfrom rich countries to poor ones. Consistent with this pattern, the numberof registered businesses rises from 3.2 to 41.8 per thousand inhabitants as

284 Brookings Papers on Economic Activity, Fall 2008

11472-06_La Porta_rev2.qxd 3/6/09 1:13 PM Page 284

Tabl

e 1.

Size

of t

he In

form

al E

cono

my

by A

ltern

ativ

e M

easu

resa

Perc

ent e

xcep

t whe

re s

tate

d ot

herw

ise

Mea

sure

of i

nfor

mal

ity

Info

rmal

sha

reN

o. o

f G

DP

per

of

GD

P a

s Se

lf-e

mpl

oyed

regi

ster

ed

capi

ta a

t es

tim

ated

by

Self

-em

ploy

edas

sha

re o

ffir

ms

per

PP

P

busi

ness

lead

ers

Tax

as

sha

re o

fno

nagr

icul

tura

lE

lect

rici

ty

Mul

tipl

e 1,

000

Inco

me

quar

tile

a(d

olla

rs)

(WE

F s

urve

y)ev

asio

nbla

bor

forc

ela

bor

forc

eco

nsum

ptio

nin

dica

tors

popu

lati

on

Bot

tom

429

35.4

29.0

46.4

57.3

38.9

42.3

3.2

Sec

ond

1,36

233

.723

.335

.737

.142

.739

.88.

2T

hird

4,00

227

.619

.723

.124

.631

.334

.128

.7T

op20

,348

17.3

8.2

13.3

12.5

17.6

18.3

41.8

Sam

ple

mea

n10

,015

27.6

22.5

26.5

30.8

29.0

34.5

24.7

Dif

fere

nce

−19,

919*

**−1

8.1*

**−2

0.8*

**−3

3.1*

**−4

4.8*

**−2

1.4*

**−2

3.9*

**38

.7**

*be

twee

n to

p an

d bo

ttom

qu

arti

les

No.

of

obse

rvat

ions

185

125

9513

396

5714

583

Sour

ces:

Wor

ld B

ank,

Wor

ld D

evel

opm

ent I

ndic

ator

s; W

orld

Eco

nom

ic F

orum

(W

EF;

200

7); W

orld

Ban

k E

nter

pris

e Su

rvey

s; I

nter

natio

nal L

abou

r O

rgan

izat

ion;

Fri

edm

an a

ndot

hers

(20

01);

Sch

neid

er (

2007

).a.

Cou

ntri

es a

re g

roup

ed i

nto

quar

tiles

by

GD

P pe

r ca

pita

at

purc

hasi

ng p

ower

par

ity (

PPP)

. Ast

eris

ks i

ndic

ate

stat

istic

ally

sig

nific

antly

dif

fere

nt f

rom

zer

o at

the

*10

per

cent

, **

5 pe

rcen

t, an

d **

*1 p

erce

nt le

vel.

b. C

alcu

late

d as

1 m

inus

the

shar

e of

sal

es r

epor

ted

for

tax

purp

oses

.

Info

rmal

sha

re o

f GD

P

as e

stim

ated

from

11472-06_La Porta_rev2.qxd 3/6/09 1:13 PM Page 285

one moves from poor to rich countries. These findings suggest that under-standing the decline of informal firms as countries grow richer may becentral to development economics.

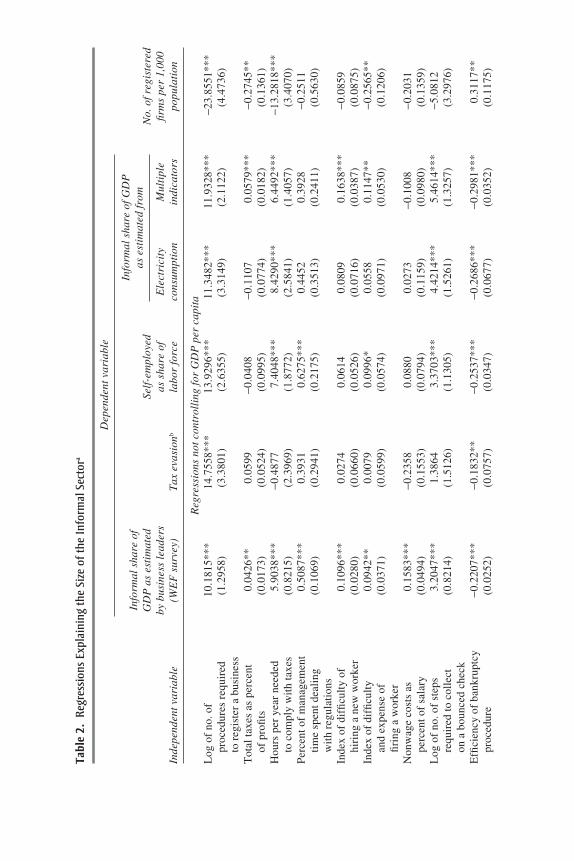

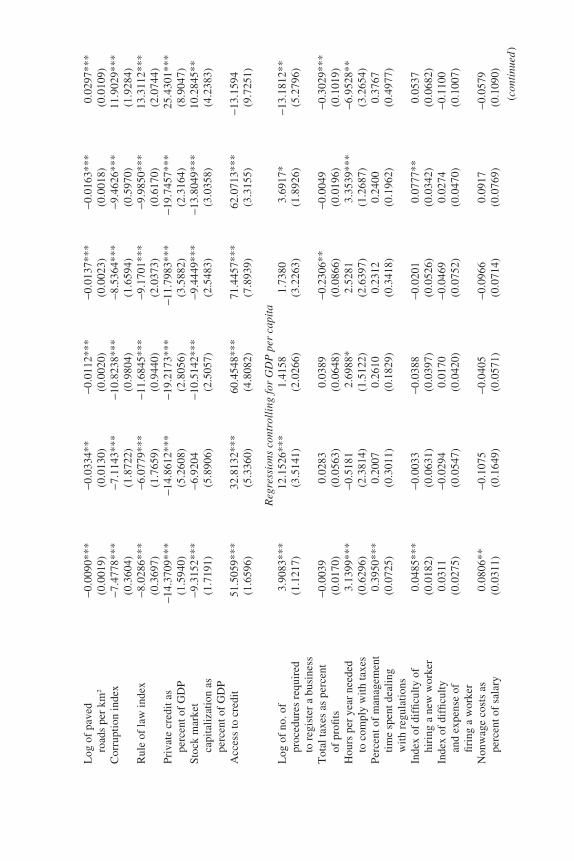

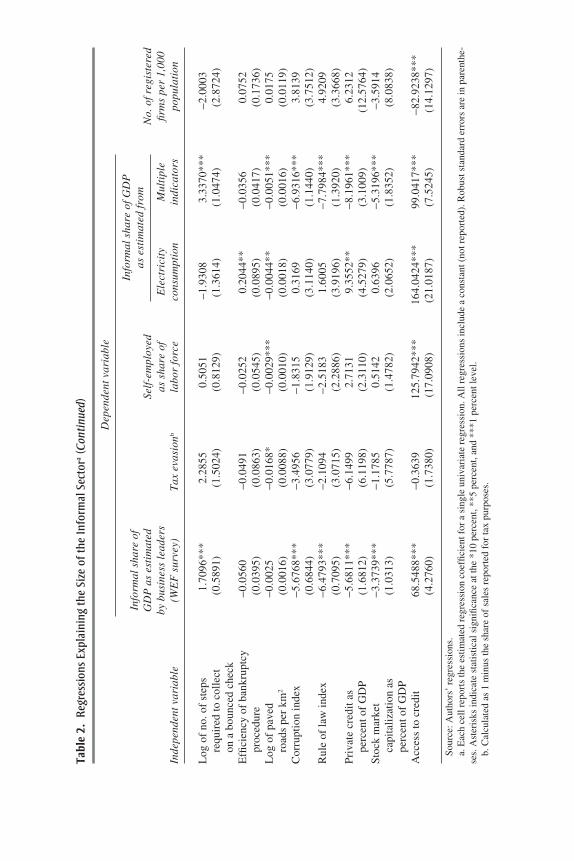

Table 2 examines the determinants of the size of the informal sector.We present results first without (top panel) and then with GDP per capita(bottom panel) in the regression. The dependent variables are five of theabove proxies for the size of the informal economy as well as the numberof registered businesses per capita. (We omit the results using nonagricul-tural self-employment as they are qualitatively similar to those for totalself-employment.) The independent variables are proxies for the cost ofbecoming formal and the costs and benefits of operating in the formal sec-tor. Each cell in each panel presents the results from a single univariateregression (we do not report the constant).

The results in the top panel show the influence of policy variables.First, our proxy for the cost of becoming formal—the number of proce-dures necessary to start a business—is consistently associated with a larger

286 Brookings Papers on Economic Activity, Fall 2008

AGO

ALB

AREARG

ARM

AUSAUT

AZE

BDI

BEL

BEN

BFA

BGD BGRBIH

BLR

BOL

BRA

BTNBWA

CAF

CAN

CHE

CHL

CHN

CIV

CMR

COG

COL

CRI

CZEDEUDNK

DOMDZAECUEGY

ESP

ESTETH

FIN

FJI

FRA

FSM

GBR

GEO

GHAGIN

GRC

GTM

HKG

HND

HRV

HTI

HUNIDN

IND

IRLIRN

ISRITA

JAM

JOR

JPN

KAZ

KEN

KGZ

KHM

KIR

KOR

KWT

LAOLBN

LKA

LSO LTU

LVAMAR

MDA

MDG

MDV MEXMHL

MKD

MLI

MNG

MOZ

MRTMWI

MYSNAM

NER

NGA

NIC

NLD

NOR

NPL

NZL

OMN

PAK

PANPER

PHL

PLW

PNG

POL PRI

PRT

PRY

ROM

RUS

RWA

SAU

SEN

SGP

SLB

SLESLV

SVK

SVN

SWESYR

TCD

TGO

THA

TONTUN

TUR

TWN

TZA

UGA

UKRURY

USA

UZB VEN

VNM

VUT WSMYEM

YUG

ZAF

ZARZMB

ZWE

70

60

50

40

30

20

10

7 8 9 10 11

Log of GDP per capita at purchasing power parityb

Informal share of GDP, multiple indicators measure (percent)a

Sources: Schneider (2007); World Bank, World Development Indicators.a. Average of the observations available for 1999–2004.b. Average for 1996–2006.

Figure 1. Size of the Informal Economy and GDP per Capita

11472-06_La Porta_rev2.qxd 3/6/09 1:13 PM Page 286

informal sector as well as with fewer registered firms. However, theeconomic effect is modest in size. For example, a 1-standard-deviation(equal to 0.4) increase in the log of the number of procedures is associatedwith a 4.8-percentage-point rise in the multiple indicators measure ofthe informal economy.

Second, the results for proxies for the cost of staying formal are mixed.All six proxies are statistically significant when the dependent variable isthe measure from the World Economic Forum survey (first data column).On the other hand, none of the explanatory variables is significant whenusing the tax evasion proxy. Results for the other dependent variables arein between these two extremes. Among the explanatory variables in thiscategory, the most consistently significant one is the time required to com-ply with taxes, which is significant for all dependent variables except taxevasion. Even then, increasing the time required to comply with taxes by1 standard deviation (0.75) is associated with an increase of only 4.8 per-centage points in the multiple indicators measure.

RAFAEL LA PORTA and ANDREI SHLEIFER 287

ABW

ANT

ARG

ARM ATG

AUSAUTBEL

BFA

BGD

BGRBHS

BLZ

BOL

BRA

BRBBWA

CANCHE

CHL

CMR

COL

CRI

CUB CYPCZE

DEU

DJI

DMA

DNK

DOM

DZA

ECUEGY

ESP

EST

ETH

FINFRA

GAB

GBR

GEO

GRC

GRD

GTMGUY

HKG

HND

HRV

HUN

IDN

IMYIRL

IRN

ISLISRITA

JAM

JPN

KAZKGZKHM

KNA

KOR

LAO

LCALKA

LSO

LTU

LUXLVA MAC

MARMDA

MDG

MDV

MEX

MKD

MLI

MLT

MNG

MUS

MWI

MYSNAM NCL

NIC

NLDNOR

NZL

OMN

PAK

PAN

PERPHL

POL

PRI

PRT

PRY

QAT

ROM

RUS

SEN

SGP

SLV

SMR

SURSVK

SVN SWE

SWZ

SYC

SYR

TCD

THA

TTO

TUNTUR

TWN

TZA

UGA

UKR

URY

USA

VCT

VENVNM

WBGWBG

YEM

ZAF

ZMB

ZWE

70

80

60

50

40

30

20

10

6 7 8 9 10 11

Log of GDP per capita at purchasing power parityb

Percent of active labor force that is self-employeda

Sources: International Labour Office (2007); World Bank, World Development Indicators.a. Data are as of the most recent year available.b. Average for 1996–2006.

Figure 2. Self-Employment and GDP per Capita

11472-06_La Porta_rev2.qxd 3/6/09 1:13 PM Page 287

Tabl

e 2.

Reg

ress

ions

Exp

lain

ing

the

Size

of t

he In

form

al S

ecto

ra

Dep

ende

nt v

aria

ble

Info

rmal

sha

re o

f G

DP

as

esti

mat

ed

Self

-em

ploy

ed

No.

of r

egis

tere

dby

bus

ines

s le

ader

s as

sha

re o

f E

lect

rici

tyM

ulti

ple

firm

s pe

r 1,

000

Inde

pend

ent v

aria

ble

(WE

F s

urve

y)T

ax e

vasi

onb

labo

r fo

rce

cons

umpt

ion

indi

cato

rspo

pula

tion

Reg

ress

ions

not

con

trol

ling

for

GD

P p

er c

apit

aL

og o

f no

. of

10.1

815*

**14

.755

8***

13.9

296*

**11

.348

2***

11.9

328*

**−2

3.85

51**

*pr

oced

ures

req

uire

d (1

.295

8)(3

.380

1)(2

.635

5)(3

.314

9)(2

.112

2)(4

.473

6)to

reg

iste

r a

busi

ness

Tot

al ta

xes

as p

erce

nt

0.04

26**

0.05

99−0

.040

8−0

.110

70.

0579

***

−0.2

745*

*of

pro

fits

(0.0

173)

(0.0

524)

(0.0

995)

(0.0

774)

(0.0

182)

(0.1

361)

Hou

rs p

er y

ear

need

ed

5.90

38**

*−0

.487

77.

4048

***

8.42

90**

*6.

4492

***

−13.

2818

***

to c

ompl

y w

ith

taxe

s(0

.821

5)(2

.396

9)(1

.877

2)(2

.584

1)(1

.405

7)(3

.407

0)P

erce

nt o

f m

anag

emen

t 0.

5087

***

0.39

310.

6275

***

0.44

520.

3928

−0.2

511

tim

e sp

ent d

eali

ng

(0.1

069)

(0.2

941)

(0.2

175)

(0.3

513)

(0.2

411)

(0.5

630)

wit

h re

gula

tion

sIn

dex

of d

iffi

cult

y of

0.

1096

***

0.02

740.

0614

0.08

090.

1638

***

−0.0

859

hiri

ng a

new

wor

ker

(0.0

280)

(0.0

660)

(0.0

526)

(0.0

716)

(0.0

387)

(0.0

875)

Inde

x of

dif

ficu

lty

0.09

42**

0.00

790.

0996

*0.

0558

0.11

47**

−0.2

565*

*an

d ex

pens

e of

(0

.037

1)(0

.059

9)(0

.057

4)(0

.097

1)(0

.053

0)(0

.120

6)fi

ring

a w

orke

rN

onw

age

cost

s as

0.

1583

***

−0.2

358

0.08

800.

0273

−0.1

008

−0.2

031

perc

ent o

f sa

lary

(0.0

494)

(0.1

553)

(0.0

794)

(0.1

159)

(0.0

980)

(0.1

359)

Log

of

no. o

f st

eps

3.20

47**

*1.

3864

3.37

03**

*4.

4214

***

5.46

14**

*−5

.081

2re

quir

ed to

col

lect

(0

.821

4)(1

.512

6)(1

.130

5)(1

.526

1)(1

.325

7)(3

.297

6)on

a b

ounc

ed c

heck

Effi

cien

cy o

f ba

nkru

ptcy

−0

.220

7***

−0.1

832*

*−0

.253

7***

−0.2

686*

**−0

.298

1***

0.31

17**

proc

edur

e(0

.025

2)(0

.075

7)(0

.034

7)(0

.067

7)(0

.035

2)(0

.117

5)

Info

rmal

sha

re o

f GD

P

as e

stim

ated

from

11472-06_La Porta_rev2.qxd 3/6/09 1:13 PM Page 288

Log

of

pave

d −0

.009

0***

−0.0

334*

*−0

.011

2***

−0.0

137*

**−0

.016

3***

0.02

97**

*ro

ads

per

km2

(0.0

019)

(0.0

130)

(0.0

020)

(0.0

023)

(0.0

018)

(0.0

109)

Cor

rupt

ion

inde

x−7

.477

8***

−7.1

143*

**−1

0.82

38**

*−8

.536

4***

−9.4

626*

**11

.902

9***

(0.3

604)

(1.8

722)

(0.9

804)

(1.6

594)

(0.5

970)

(1.9

284)

Rul

e of

law

inde

x−8

.028

6***

−6.0

779*

**−1

1.68

45**

*−9

.170

1***

−9.9

850*

**13

.311

2***

(0.3

697)

(1.7

659)

(0.9

440)

(2.0

373)

(0.6

170)

(2.0

744)

Pri

vate

cre

dit a

s −1

4.37

09**

*−1

4.86

12**

*−1

9.21

73**

*−1

1.79

83**

*−1

9.74

57**

*25

.430

1***

perc

ent o

f G

DP

(1.5

940)

(5.2

608)

(2.8

056)

(3.5

882)

(2.3

164)

(8.9

047)

Sto

ck m

arke

t −9

.315

2***

−6.9

204

−10.

5142

***

−9.4

449*

**−1

3.80

49**

*10

.284

5**

capi

tali

zati

on a

s (1

.719

1)(5

.890

6)(2

.505

7)(2

.548

3)(3

.035

8)(4

.238

3)pe

rcen

t of

GD

PA

cces

s to

cre

dit

51.5

059*

**32

.813

2***

60.4

548*

**71

.445

7***

62.0

713*

**−1

3.15

94(1

.659

6)(5

.336

0)(4

.808

2)(7

.893

9)(3

.315

5)(9

.725

1)

Reg

ress

ions

con

trol

ling

for

GD

P p

er c

apit

aL

og o

f no

. of

3.90

83**

*12

.152

6***

1.41

581.

7380

3.69

17*

−13.

1812

**pr

oced

ures

req

uire

d (1

.121

7)(3

.514

1)(2

.026

6)(3

.226

3)(1

.892

6)(5

.279

6)to

reg

iste

r a

busi

ness

Tot

al ta

xes

as p

erce

nt

−0.0

039

0.02

830.

0389

−0.2

306*

*−0

.004

9−0

.302

9***

of p

rofi

ts(0

.017

0)(0

.056

3)(0

.064

8)(0

.086

6)(0

.019

6)(0

.101

9)H

ours

per

yea

r ne

eded

3.

1399

***

−0.5

181

2.69

88*

2.52

813.

3539

***

−6.9

528*

*to

com

ply

wit

h ta

xes

(0.6

296)

(2.3

814)

(1.5

122)

(2.6

397)

(1.2

687)

(3.2

654)

Per

cent

of

man

agem

ent

0.39

50**

*0.

2007

0.26

100.

2312

0.24

000.

3767

tim

e sp

ent d

eali

ng

(0.0

725)

(0.3

011)

(0.1

829)

(0.3

418)

(0.1

962)

(0.4

977)

wit

h re

gula

tion

sIn

dex

of d

iffi

cult

y of

0.

0485

***

−0.0

033

−0.0

388

−0.0

201

0.07

77**

0.05

37hi

ring

a n

ew w

orke

r(0

.018

2)(0

.063

1)(0

.039

7)(0

.052

6)(0

.034

2)(0

.068

2)In

dex

of d

iffi

cult

y 0.

0311

−0.0

294

0.01

70−0

.046

90.

0274

−0.1

100

and

expe

nse

of

(0.0

275)

(0.0

547)

(0.0

420)

(0.0

752)

(0.0

470)

(0.1

007)

firi

ng a

wor

ker

Non

wag

e co

sts

as

0.08

06**

−0.1

075

−0.0

405

−0.0

966

0.09

17−0

.057

9pe

rcen

t of

sala

ry(0

.031

1)(0

.164

9)(0

.057

1)(0

.071

4)(0

.076

9)(0

.109

0)

(con

tinu

ed)

11472-06_La Porta_rev2.qxd 3/6/09 1:13 PM Page 289

Log

of

no. o

f st

eps

1.70

96**

*2.

2855

0.50

51−1

.930

83.

3370

***

−2.0

003

requ

ired

to c

olle

ct

(0.5

891)

(1.5

024)

(0.8

129)

(1.3

614)

(1.0

474)

(2.8

724)

on a

bou

nced

che

ckE

ffici

ency

of

bank

rupt

cy−0

.056

0−0

.049

1−0

.025

20.

2044

**−0

.035

60.

0752

proc

edur

e(0

.039

5)(0

.086

3)(0

.054

5)(0

.089

5)(0

.041

7)(0

.173

6)L

og o

f pa

ved

−0.0

025

−0.0

168*

−0.0

029*

**−0

.004

4**

−0.0

051*

**0.

0175

road

s pe

r km

2(0

.001

6)(0

.008

8)(0

.001

0)(0

.001

8)(0

.001

6)(0

.011

9)C

orru

ptio

n in

dex

−5.6

768*

**−3

.495

6−1

.831

50.

3169

−6.9

316*

**3.

8139

(0.6

844)

(3.0

779)

(1.9

129)

(3.1

140)

(1.1

440)

(3.7

512)

Rul

e of

law

inde

x−6

.479

3***

−2.1

094

−2.5

183

1.60

05−7

.798

4***

4.92

09(0

.709

5)(3

.071

5)(2

.288

6)(3

.919

6)(1

.392

0)(3

.366

8)P

riva

te c

redi

t as

−5.6

811*

**−6

.149

92.

7131

9.35

52**

−8.1

961*

**6.

2312

perc

ent o

f G

DP

(1.6

812)

(6.1

198)

(2.3

110)

(4.5

279)

(3.1

009)

(12.

5764

)S

tock

mar

ket

−3.3

739*

**−1

.178

50.

5142

0.63

96−5

.319

6***

−3.5

914

capi

tali

zati

on a

s (1

.031

3)(5

.778

7)(1

.478

2)(2

.065

2)(1

.835

2)(8

.083

8)pe

rcen

t of

GD

PA

cces

s to

cre

dit

68.5

488*

**−0

.363

912

5.79

42**

*16

4.04

24**

*99

.041

7***

−82.

9238

***

(4.2

760)

(1.7

380)

(17.

0908

)(2

1.01

87)

(7.5

245)

(14.

1297

)

Sour

ce: A

utho

rs’

regr

essi

ons.

a. E

ach

cell

repo

rts

the

estim

ated

reg

ress

ion

coef

ficie

nt f

or a

sin

gle

univ

aria

te r

egre

ssio

n. A

ll re

gres

sion

s in

clud

e a

cons

tant

(no

t rep

orte

d). R

obus

t sta

ndar

d er

rors

are

in p

aren

the-

ses.

Ast

eris

ks in

dica

te s

tatis

tical

sig

nific

ance

at t

he *

10 p

erce

nt, *

*5 p

erce

nt, a

nd *

**1

perc

ent l

evel

.b.

Cal

cula

ted

as 1

min

us th

e sh

are

of s

ales

rep

orte

d fo

r ta

x pu

rpos

es.

Tabl

e 2.

Reg

ress

ions

Exp

lain

ing

the

Size

of t

he In

form

al S

ecto

ra(C

onti

nued

)

Dep

ende

nt v

aria

ble

Info

rmal

sha

re o

f G

DP

as

esti

mat

ed

Self

-em

ploy

ed

No.

of r

egis

tere

dby

bus

ines

s le

ader

s as

sha

re o

f E

lect

rici

tyM

ulti

ple

firm

s pe

r 1,

000

Inde

pend

ent v

aria

ble

(WE

F s

urve

y)T

ax e

vasi

onb

labo

r fo

rce

cons

umpt

ion

indi

cato

rspo

pula

tion

Info

rmal

sha

re o

f GD

P

as e

stim

ated

from

11472-06_La Porta_rev2.qxd 3/6/09 1:13 PM Page 290

Third, the proxies for the benefits of being formal are consistently asso-ciated with the size of the informal sector and the number of registeredfirms: the only two exceptions are court formalism (the number of stepsnecessary to collect on a bounced check) in the regressions for tax evasionand registered firms. The economic impact, in terms of the multiple indica-tors measure, of increasing these variables by 1 standard deviation rangesfrom 5.8 percentage points for court formalism to 9.6 percentage points forthe rule of law. In sum, without controlling for income per capita, both thecost of becoming formal and the benefits of operating in the formal sectorhave a reliable but modest impact on the size of the informal economy. Ourproxies for the cost of operating in the formal sector also have a modesteffect but are less often significant.

Next, we rerun the previous regressions adding GDP per capita as anindependent variable. The motivation is that the extent of the informaleconomy may be correlated with a country’s development level. In poorcountries the informal economy may provide subsistence income for work-ers unable to find formal employment. To the extent that informal firmsavoid labor laws, the benefits of informality may be larger in the labor-intensive activities common in poor countries than in the capital-intensiveactivities common in rich countries. Along the same lines, informality maydecline as more transactions are intermediated through the financial system.Finally, tax compliance may rise with income per capita as governmentsbecome more efficient at collecting taxes.

The bottom panel of table 2 shows the coefficients for the variables ofinterest when we control for GDP per capita. (As in the top panel, we do notreport the constant. Nor do we report the coefficient for GDP per capita, butit is strongly significant in all regressions.) Most of the estimated coefficientsfall in value and lose significance compared with the regressions withoutGDP per capita. Indeed, the coefficients remain consistently significant(11 of the 15 regressions) only for the World Economic Forum survey.Results for the other dependent variables are mostly insignificant. Ourproxy for the cost of becoming formal remains significant in four of the sixregressions (World Economic Forum survey, tax evasion, multiple indica-tors, and registered firms). Among the proxies for the cost of operating in theformal sector, the strongest variable is the time to comply with taxes, whichis significant in four of the six regressions. Yet in contrast to the results ontax rates, nonwage costs are significant in only one regression. Finally,among the proxies for the benefits of operating in the formal sector, thestrongest variables are road density (significant in four regressions) and thesubjective assessment of access to credit (significant in five regressions).

RAFAEL LA PORTA and ANDREI SHLEIFER 291

11472-06_La Porta_rev2.qxd 3/6/09 1:13 PM Page 291

The results using objective measures of the development of financial mar-kets are mixed: private credit remains significant in three regressions, butmarket capitalization does so in only two regressions.

In sum, GDP per capita is the most robust predictor of the size of theinformal economy. The most straightforward interpretation of the resultsin this section is that the informal economy is a manifestation of under-development. It recedes as the economy develops, perhaps because publicgoods become better and financial markets larger, or because avoidingdetection becomes harder. It remains a crucial, and open, question whetherthis decline of the informal sector results from the conversion of informalfirms to official status, or from their death and replacement by formal firms.

An alternative interpretation is that we are overcorrecting by includ-ing GDP per capita. In particular, GDP per capita is strongly correlated(70 percent or better) with the efficiency of bankruptcy procedures, pri-vate credit, corruption, and the rule of law (see the correlation table inthe appendix). Interestingly, variables that explicitly capture a country’seconomic structure (such as the share of agriculture in GDP; results notreported) leave much of the explanatory power of GDP per capita unchanged.Although GDP per capita is strongly correlated with some of the determi-nants of the size of the informal economy, multicollinearity is unlikely toexplain why tax rates, nonwage costs, and labor laws work so poorly whenwe control for GDP per capita. We return to this issue below when weexamine the productivity of informal firms, using micro data.

Although the cross-country evidence reveals some interesting patterns,it is merely suggestive and does not discriminate among the three viewsof the role of the informal economy. For this we need micro data, whichwe analyze next. Accordingly, the remainder of the paper is organized asfollows. The next section describes our data on informal and formal firms.We ask such questions as: Are informal firms engines of growth as theromantic view would hold? For example, do informal firms grow quicklyand over time join the formal sector? Is there evidence that—consistentwith the parasite view—formal and informal firms operate in the samemarkets or that formal firms fear competition from informal firms? Whatevidence is there that—as predicted by the dual view—informal firms haveinferior assets and management?

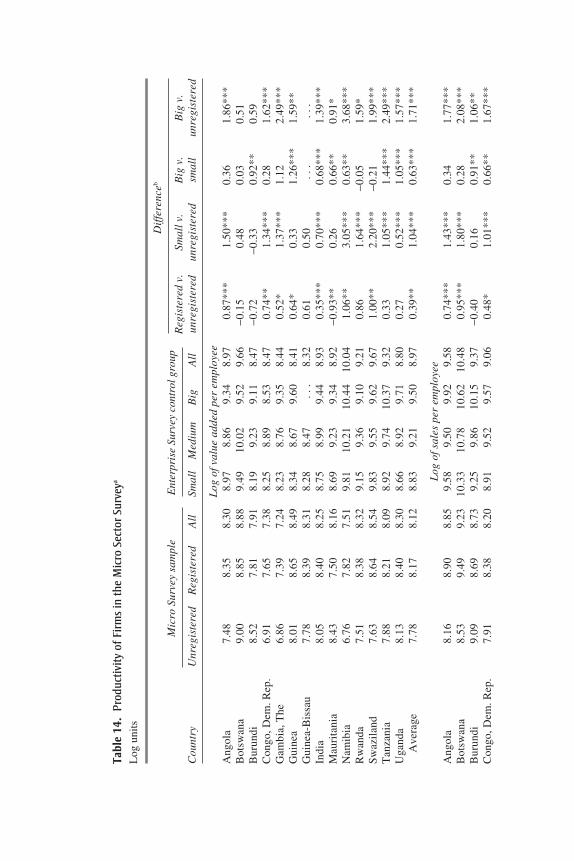

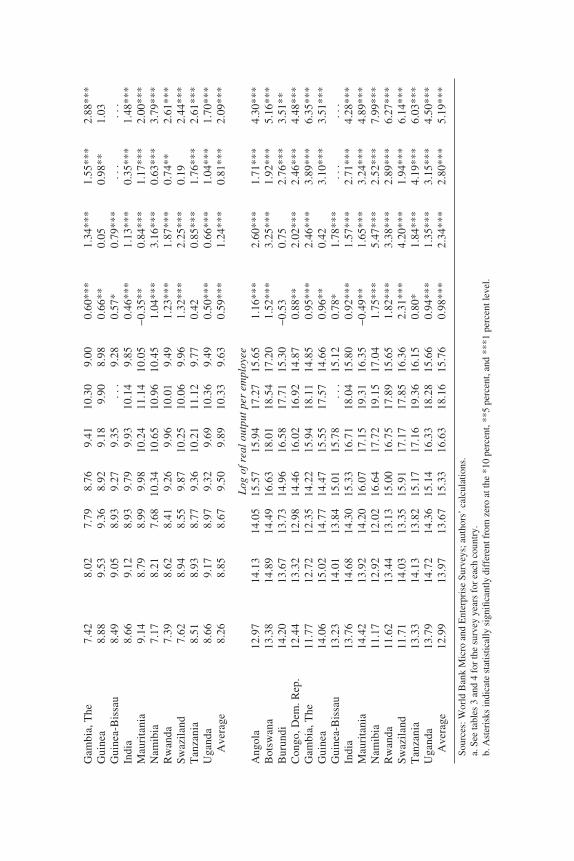

The third section is the heart of the paper. It presents evidence on therelative productivity of formal and informal firms. We ask five questions.First, are our data on productivity reliable? Second, how big are the differ-ences in productivity between formal and informal firms? We want to knowwhether the prediction of the parasite view that informal firms have a cost

292 Brookings Papers on Economic Activity, Fall 2008

11472-06_La Porta_rev2.qxd 3/6/09 1:13 PM Page 292

advantage is borne out by the data. Third, what views of the informal econ-omy are consistent with the observed differences in productivity? We wantto examine whether it is plausible to believe—as in the romantic view—thatall that is holding back informal firms are high taxes and bad governmentregulation. Fourth, what accounts for the difference in the productivity offormal and informal firms? The goal is to see whether differences in pro-ductivity can be traced to differences in inputs. Finally, what evidence isthere that more-able managers run firms with better assets? Evidence of astrong selection effect would support the dual view and cast doubt on theprediction of the romantic view that relieving informal firms from oppres-sive taxes and regulation would put an end to poverty as we know it.

The fourth section focuses on obstacles to doing business, as reportedby firms in all three surveys. We ask which of several problems, such asmarket access, financing, taxes, and regulations, but also unfair competi-tion, are perceived as principal obstacles to doing business. These resultsshed light on the alternative theories but perhaps bear most directly on theparasite theory. The final section concludes with some implications of theevidence.

Characteristics of Informal Firms

In this section we describe our data and present simple descriptive statistics.Our basic approach is to compare, country by country, the relative perfor-mance of formal and informal firms. To do so, we combine data from threeWorld Bank surveys of individual firms. The first survey—the EnterpriseSurvey—covers formal firms and is available for 105 countries. The othertwo surveys—the Informal and Micro Surveys—contain information onboth informal and formal firms in a few poor countries. The InformalSurvey is available for 13 countries: Bangladesh, Brazil, Cambodia,Cape Verde, Guatemala, India, Indonesia, Kenya, Niger, Pakistan, Senegal,Tanzania, and Uganda.30 With the exception of Brazil, all these countrieswere below the world median income per capita in 2003 (equal to $5,322),and 7 out of 13 were below the 25th percentile (equal to $1,682). The MicroSurvey is available for 14 mostly African countries: Angola, Botswana,Burundi, Democratic Republic of the Congo, The Gambia, Guinea, Guinea-Bissau, India, Mauritania, Namibia, Rwanda, Swaziland, Tanzania, andUganda. With the exception of Botswana, all were below the world median

RAFAEL LA PORTA and ANDREI SHLEIFER 293

30. The World Bank also carried out an Informal Survey of Cameroon in 2006. How-ever, data on sales are missing from that survey.

11472-06_La Porta_rev2.qxd 3/6/09 1:13 PM Page 293

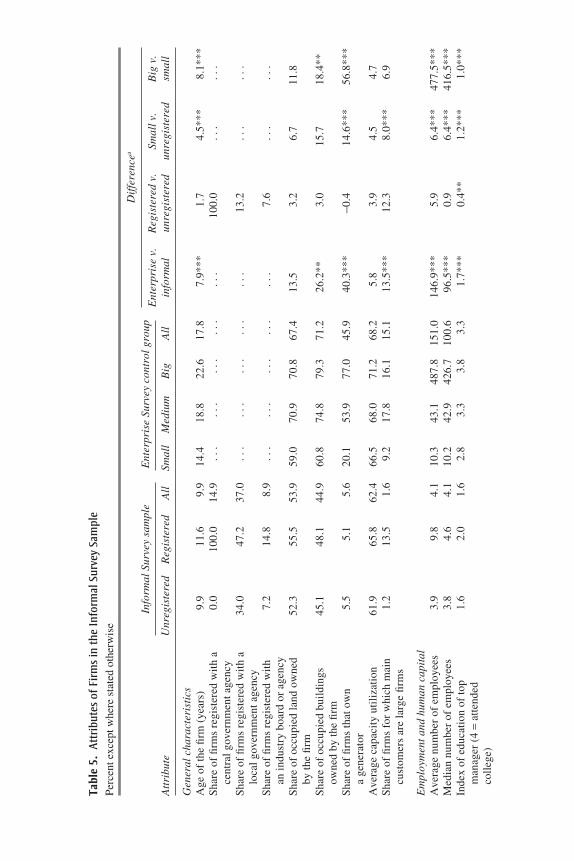

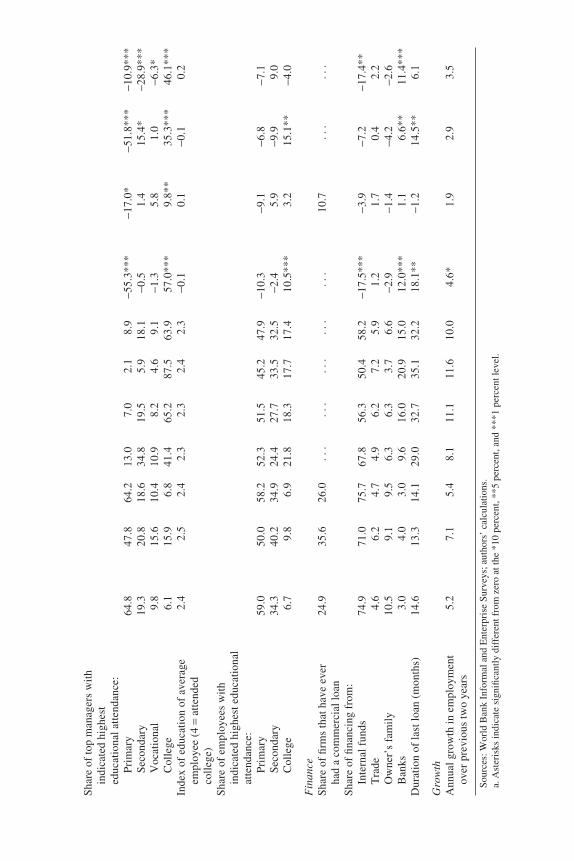

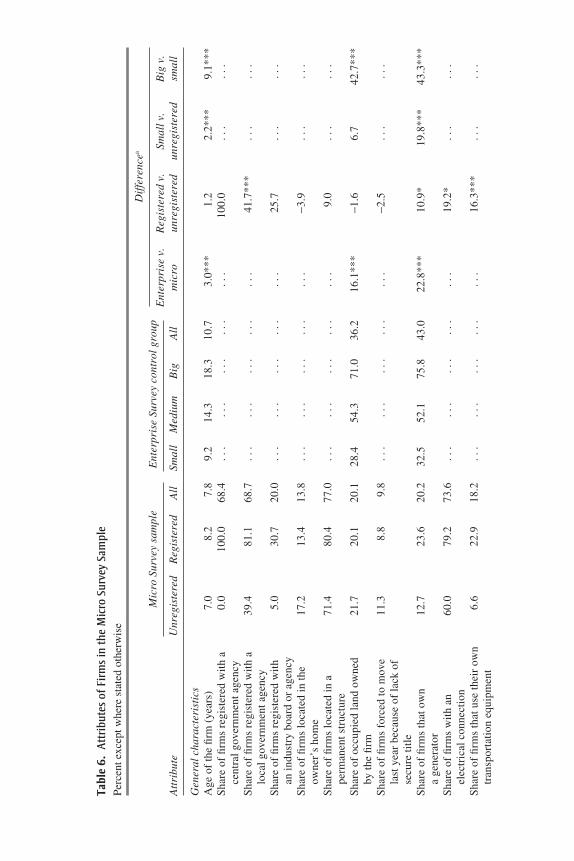

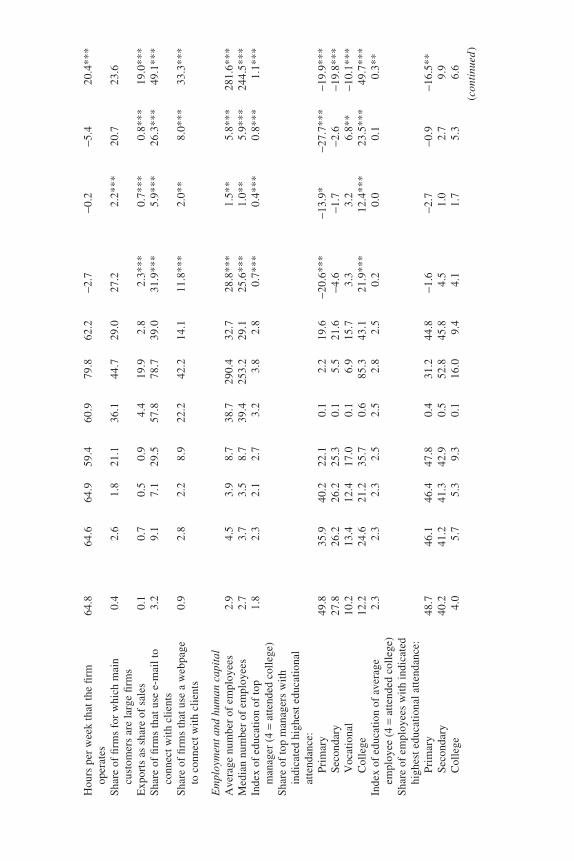

income per capita in 2006 (equal to $6,224), and 9 out of 14 were belowthe 25th percentile (equal to $1,965). The concept of informality used in theInformal and Micro Surveys focuses on registration (as we discuss below,there are several possible kinds of registration). Although questions abouttax avoidance are asked, they are indirect. As discussed in the precedingsection, this definition has both advantages and conceptual limitations.

Before describing the data in detail, we need to preempt a possible mis-conception about the nature of the firms in our data. In the context of poorcountries, the term “informal firm” evokes the image of street hawkersselling goods out of baskets, or of eateries in front of homes. In fact, such animage is a good description of how the very poor make a living.31 However,the informal firms in our sample do not fit that image. For example, firmsaccounting for roughly 85 percent of the observations in the Informal andMicro Surveys have, in addition to the entrepreneur, two employees ormore. The informal firms in our sample are likely to be substantially moreproductive than the own-account workers described by Abhijit Banerjeeand Esther Duflo.

Data

All three World Bank surveys have a similar structure and differ mainlyin the firms that they sample. It is easiest to start by describing the Enter-prise Survey, the source for our control group of registered or formal firms.It covers mainly manufacturing and certain services firms with five or moreemployees in 105 countries. The earliest available data are from 2002 andthe latest from 2007. The initial step in carrying out an Enterprise Surveyinvolves contacting the government statistical office of the relevant countryto request a list of registered establishments. In some instances the WorldBank supplements the government’s list with firms registered with thechamber of commerce of the relevant country or listed by Dun & Bradstreetor by similar private vendors of business directories. Thus, although firmsin the Enterprise Survey may hide some of their output, the governmenttypically knows of their existence. We refer to these firms as “registered”and define the term below. The next step involves contacting the firms thatwill be sampled. Enterprise Surveys use either simple random sampling orrandom stratified sampling. A local World Bank contractor telephones eachfirm to set up an interview with the person who most often deals with banksor government agencies. At that stage, firms with fewer than five employeesare dropped from the sample, as are government-owned establishments,

294 Brookings Papers on Economic Activity, Fall 2008

31. Banerjee and Duflo (2007).

11472-06_La Porta_rev2.qxd 3/6/09 1:13 PM Page 294

cooperatives, and community-owned establishments. Typical final samplesizes range between 250 and 1,500 businesses per country. As described onthe Enterprise Surveys website, “The core questionnaire is organized in twoparts. The first part seeks managers’ opinions on the . . . business environ-ment. The second part focuses on productivity measures and is often com-pleted with the help of the chief accountant or human resource manager.”

The World Bank has also conducted separate surveys of informal firmsto complement the Enterprise Survey in countries with large informaleconomies. Initially, data on the unofficial sector were collected throughthe “Informal Sector” questionnaire. Starting in 2005, the World Bankswitched to the “Micro Sector” questionnaire while phasing out the Infor-mal Sector questionnaire. Institutional amnesia makes it hard to ascertainthe precise methodology followed with the Informal Sector questionnaire.Nevertheless, the basic outlines of what was done are clear. World Bankcontractors identified neighborhoods perceived to have a large number ofinformal firms. These neighborhoods were then divided into enumerationblocks, which were then surveyed on foot.32

A similar methodology was followed to implement the Micro Sectorquestionnaire. A local contractor selected districts and zones within eachdistrict where, based on national information sources, there was a highconcentration of establishments with fewer than five employees (“micro”establishments). The contractor then created a comprehensive list of allestablishments in these zones. Finally, the contractor selected randomlyfrom that list and went door to door to set up interviews with the top man-agers of the selected establishments. Although the Micro Survey targetsestablishments with fewer than five employees, larger establishments arenot dropped from the sample. In fact, establishments with fewer than fiveemployees account for only 50 percent of the Micro Survey sample.

Participation in the surveys is voluntary, and respondents are not paidto participate.33 Respondents are asked sequentially about the businessenvironment, infrastructure, government relations, employment, financing,and firm productivity. There is some variation in the response rate acrossquestions. To illustrate, out of 6,466 Informal and Micro firms surveyed,we have the age of 6,412 firms, the number of employees of 6,416 firms,the sales of 6,136 firms, the fraction of investment financed internally of5,689 firms, assessments of the fraction of taxes typically evaded by firms

RAFAEL LA PORTA and ANDREI SHLEIFER 295

32. Jorge Rodriguez Meza, World Bank, personal correspondence with the authors, June 27, 2008.

33. We lack detailed data on nonparticipation rates. In Mali, the only country for whichwe have data on nonparticipation, the refusal rate is 9 percent.

11472-06_La Porta_rev2.qxd 3/6/09 1:13 PM Page 295

in their industry of 4,670 firms, and capacity utilization of 3,083 firms.Since Informal and Micro firms typically do not keep detailed records oftheir operations, some respondents may simply not have the informationbeing asked. Unfortunately, we have no way of quantifying the biases, ifany, from missing data.

Critically, the Informal and Micro Surveys cover registered firms as wellas firms that exist without the government’s knowledge (“unregistered”firms). In the remainder of this paper, we focus on informality understoodin terms of hidden firms rather than hidden output. To compare the perfor-mance of registered and unregistered firms, we need to define what it meansto be registered. The questions regarding the legal status of the firm areworded differently in the Informal and the Micro questionnaires. In theInformal Survey we rely on the respondent’s answer to whether firms are“registered with any agency of the central government.” In practical terms,firms are registered with an agency of the central government if they haveobtained a tax identification number. In the Micro Survey, we rely onthe respondent’s answer to whether firms have either “registered with theOffice of the Registrar . . . or other government institutions responsible forcommercial registration” or “obtained a tax identification number from thetax administration or other agency responsible for tax registration.”34 Bothsurveys also keep track of whether firms are registered with “any localgovernment agency” or with any “industry board or agency.” We focus onregistration with the central government because this form of registrationis more directly relevant to avoiding taxes, enforcing contracts, and raisingfinance. We will also present statistics on municipal and industry boardregistration. In sum, the Informal and Micro Surveys allow us to examinethe productivity of (small) registered and unregistered firms, whereas theEnterprise Survey provides information on the productivity of registeredfirms that have at least five employees.

Descriptive Statistics

Tables 3 and 4 list the countries surveyed and present the number ofobservations and average sales for the Informal and Micro samples, respec-tively. Most of the surveys (19 out of a total of 27) were carried out inAfrican countries, but 6 surveys were done in Asia and 2 in Latin America.India, Uganda, and Tanzania were surveyed with both the Informal and theMicro questionnaires. As indicated earlier, most countries covered by the

296 Brookings Papers on Economic Activity, Fall 2008

34. We obtain very similar results if the definition of “registered” firms in the MicroSurvey includes only firms that have a tax identification number.

11472-06_La Porta_rev2.qxd 3/6/09 1:13 PM Page 296

Informal and Micro Surveys are poor. The average income per capita incurrent purchasing power terms is roughly $2,400 and ranges from $281 inCongo to $12,744 in Botswana.

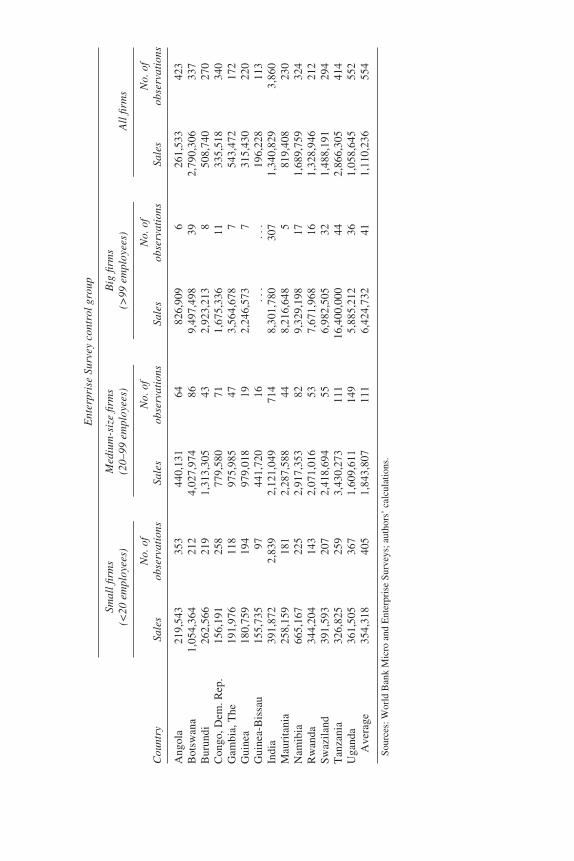

The Informal Survey covered 13 countries. The surveys were typicallycarried out in 2003 and, on average, have 223 firms with nonmissing salesin each country. The Micro Surveys were carried out in 14 countries in2006 and, on average, have 214 firms with nonmissing sales per country.The World Bank also carried out Enterprise Surveys in parallel with therelevant Informal and Micro Surveys. We use firms from the EnterpriseSurvey as the control group. The average number of firms in the controlgroup with available sales data is 474 for the Informal sample and 554 forthe Micro sample and ranges from 53 in Niger (table 3) to 3,860 in India(table 4).

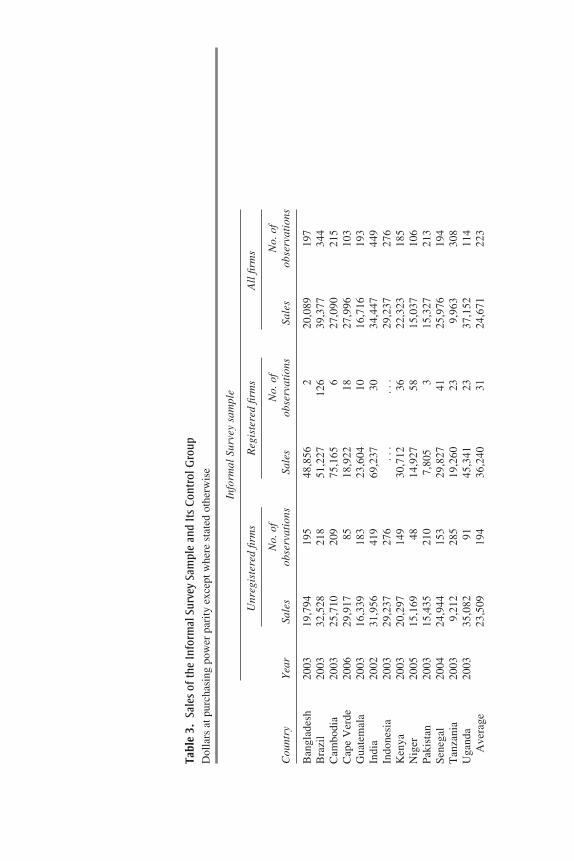

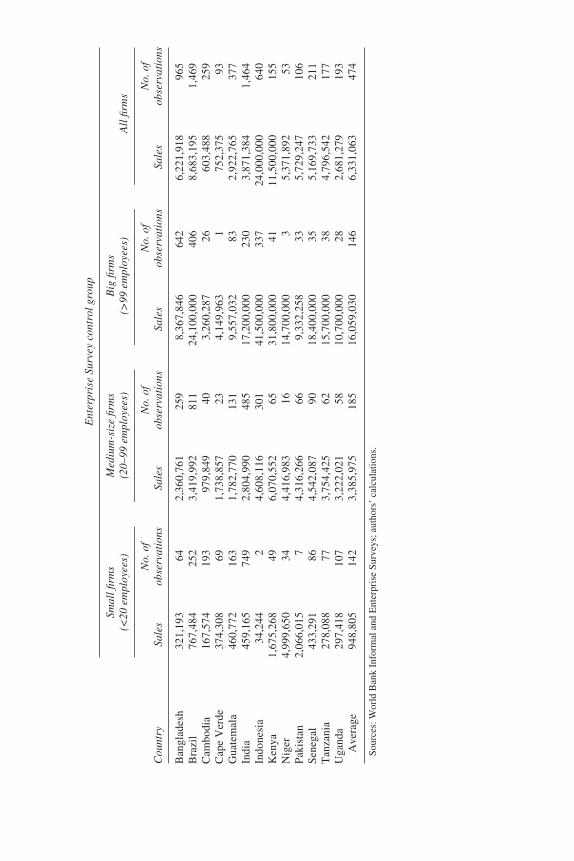

Throughout the paper we emphasize productivity differences betweenregistered and unregistered firms and between small and big firms. Criti-cally, whereas firms in the Informal Survey are typically unregistered, firmsin the Micro Survey are typically registered. The average Informal Surveyhas 31 registered firms out of a total of 223 firms, whereas the averageMicro Survey has 137 registered firms out of a total of 214 firms. Toexamine differences in size, we group Enterprise Survey firms into threecategories according to the number of employees: fewer than 20 (“small”),between 20 and 99 (“medium”), and 100 or more (“big”). When assessingsome of our results on productivity, it is worth keeping in mind that thedistribution of firms across these three categories is fairly uneven. Forexample, there is 1 big firm with nonmissing sales data (out of 93) in thecontrol group for firms in Cape Verde, but there are 337 (out of 640) in thecontrol group for firms in Indonesia (table 3). Perhaps because of the smallnumber of observations, there are few extreme outliers in the data; thesemost likely result from errors in currency units. To mitigate the role of out-liers, we cap at the 95th percentile the value of sales, sales per employee,and value added per employee in each country and in each survey. Cappingdoes not qualitatively change the results we present.

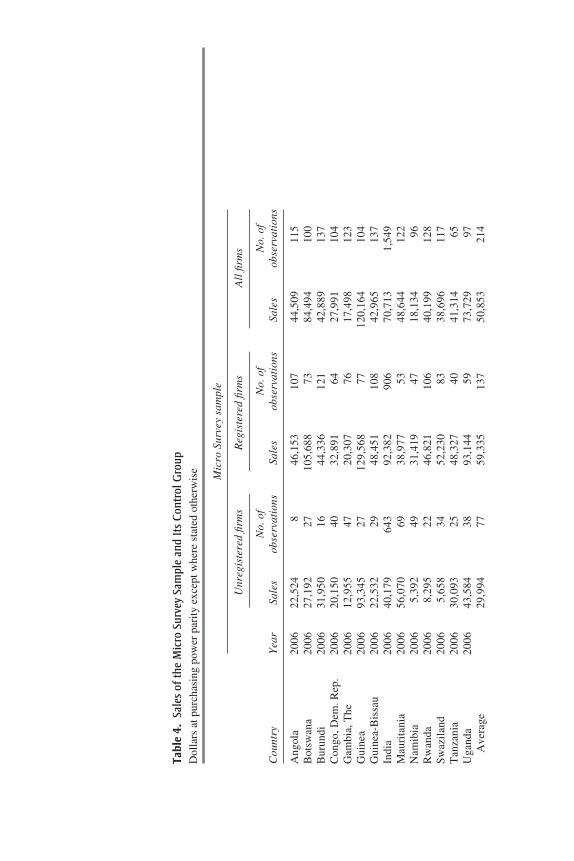

The most striking fact in tables 3 and 4 is that the average annual salesof firms in the Informal and Micro Surveys are tiny even in comparisonwith those of small firms in the Enterprise Survey. Specifically, averagesales are $24,671 for Informal Survey firms but $948,805 for small firms inthe Enterprise Survey control group for those countries. Similarly, averagesales are $50,853 for Micro Survey firms but $354,318 for small firms inthat control group. Unregistered firms are even smaller than the average firmin the Informal and Micro Surveys. For example, in the Informal Survey

RAFAEL LA PORTA and ANDREI SHLEIFER 297

11472-06_La Porta_rev2.qxd 3/6/09 1:13 PM Page 297

Tabl

e 3.

Sale

s of

the

Info

rmal

Sur

vey

Sam

ple

and

Its

Cont

rol G

roup

Dol

lars

at p

urch

asin

g po

wer

par

ity e

xcep

t whe

re s

tate

d ot

herw

ise

Info

rmal

Sur

vey

sam

ple

Unr

egis

tere

d fir

ms

Reg

iste

red

firm

sA

ll fi

rms

No.

of

No.

of

No.

of

Cou

ntry

Yea

rSa

les

obse

rvat

ions

Sale

sob

serv

atio

nsSa

les

obse

rvat

ions

Ban

glad

esh

2003

19,7

9419

548

,856

220

,089

197

Bra

zil

2003

32,5

2821

851

,227

126

39,3

7734

4C

ambo

dia

2003

25,7

1020

975

,165

627

,090

215

Cap

e V

erde

2006

29,9

1785

18,9

2218

27,9

9610

3G

uate

mal

a20

0316

,339

183

23,6

0410

16,7

1619

3In

dia

2002

31,9

5641

969

,237

3034

,447

449

Indo

nesi

a20

0329

,237

276

...

...

29,2

3727

6K

enya

2003

20,2

9714

930

,712

3622

,323

185

Nig

er20

0515

,169

4814

,927

5815

,037

106

Pak

ista

n20

0315

,435

210

7,80

53

15,3

2721

3S

eneg

al20

0424

,944

153

29,8

2741

25,9

7619

4T

anza

nia

2003

9,21

228

519

,260

239,

963

308

Uga

nda

2003

35,0

8291

45,3

4123

37,1

5211

4A

vera

ge23

,509

194

36,2

4031

24,6

7122

3

11472-06_La Porta_rev2.qxd 3/6/09 1:13 PM Page 298

Ent

erpr

ise

Surv

ey c

ontr

ol g

roup

Smal

l firm

sM

ediu

m-s

ize

firm

s B

ig fi

rms

(<20

em

ploy

ees)

(20–

99 e

mpl

oyee

s)(>

99 e

mpl

oyee

s)A

ll fi

rms

No.

of

No.

of

No.

of

No.

of

Cou

ntry

Sale

sob

serv

atio

nsSa

les

obse

rvat

ions

Sale

sob

serv

atio

nsSa

les

obse

rvat

ions

Ban

glad

esh

321,

193

642,

360,

761

259

8,36

7,84

664

26,

221,

918

965

Bra

zil

767,

484

252

3,41

9,99

281

124

,100

,000

406

8,68

3,19

51,

469

Cam

bodi

a16

7,57

419

397

9,84

940

3,26

0,28

726

603,

488

259

Cap

e V

erde

374,

308

691,

738,

857

234,

149,

963

175

2,37

593

Gua

tem

ala

460,

772

163

1,78

2,77

013

19,

557,

032

832,

922,

765

377

Indi

a45

9,16

574

92,

804,

990

485

17,2

00,0

0023

03,

871,

384

1,46

4In

done

sia

34,2

442

4,60

8,11

630

141

,500

,000

337

24,0

00,0

0064

0K

enya

1,67

5,26

849

6,07

0,55

265

31,8

00,0

0041

11,5

00,0

0015

5N

iger

4,99

9,65

034

4,41

6,98

316

14,7

00,0

003

5,37

1,89

253

Pak

ista

n2,

066,

015

74,

316,

266

669,

332,

258

335,

729,

247

106

Sen

egal

433,

291

864,

542,

087

9018

,400

,000

355,

169,

733

211

Tan

zani

a27

8,08

877

3,75

4,42

562

15,7

00,0

0038

4,79

6,54

217

7U

gand

a29

7,41

810

73,

222,

021

5810

,700

,000

282,

681,

279

193

Ave

rage

948,

805

142

3,38

5,97

518

516

,059

,030

146

6,33

1,06

347

4

Sour

ces:

Wor

ld B

ank

Info

rmal

and

Ent

erpr

ise

Surv

eys;

aut

hors

’ ca

lcul

atio

ns.

11472-06_La Porta_rev2.qxd 3/6/09 1:13 PM Page 299

Tabl

e 4.

Sale

s of

the

Mic

ro S

urve

y Sa

mpl

e an

d It

s Co

ntro

l Gro

upD

olla

rs a

t pur

chas

ing

pow

er p

arity

exc

ept w

here

sta

ted

othe

rwis

e

Mic

ro S

urve

y sa

mpl

e

Unr

egis

tere

d fir

ms

Reg

iste

red

firm

sA

ll fi

rms

No.

of

No.

of

No.

of

Cou

ntry

Yea

rSa

les

obse

rvat

ions

Sale

sob

serv

atio

nsSa

les

obse

rvat

ions

Ang

ola

2006

22,5

248

46,1

5310

744

,509

115

Bot

swan

a20

0627

,192

2710

5,68

873

84,4

9410

0B

urun

di20

0631

,950

1644

,336

121

42,8

8913

7C

ongo

, Dem

. Rep

.20

0620

,150

4032

,891

6427

,991

104

Gam

bia,