Embed Size (px)

Citation preview

These materials have been prepared by the CASBO Financial Services Professional Council, Sacramento Section. They have not been reviewed by State CASBO for approval, so therefore are not an official statement of CASBO.

APRIL 3-6, 2013, LONG BEACH, CA

FIN21CASH FLOW PROJECTIONS

2

2013 CASBO ANNUAL CONFERENCE & SCHOOL BUSINESS EXPO

CASH FLOW PROJECTIONS

Session ID FIN21

Financial Services Professional Council

Sacramento Section

Friday April 5, 2013

11:00 a.m. – 12:00 p.m.

Presented by

Diane Lacombe

El Dorado County Office of Education

3

2013 CASBO ANNUAL CONFERENCE & SCHOOL BUSINESS EXPO

Agenda

• Cash Concepts and Challenges

• Building Cash Flow Projections

• Review and Analysis

4

CASH CONCEPTS & CHALLENGES

5

2013 CASBO ANNUAL CONFERENCE & SCHOOL BUSINESS EXPO

Cash Management is Vital• One of the 15 conditions that most

frequently indicates fiscal distress is poor cash flow analysis and reconciliation

• All districts that have been taken over by the state ran out of cash

• Cost of running low on cash is high

6

2013 CASBO ANNUAL CONFERENCE & SCHOOL BUSINESS EXPO

Cash ≠ Fund Balance• Example:

• Cash is 10% of

• Fund Balance

714,636.96

7,716,085.10

Example:

Cash is 10% of

Fund Balance

7

2013 CASBO ANNUAL CONFERENCE & SCHOOL BUSINESS EXPO

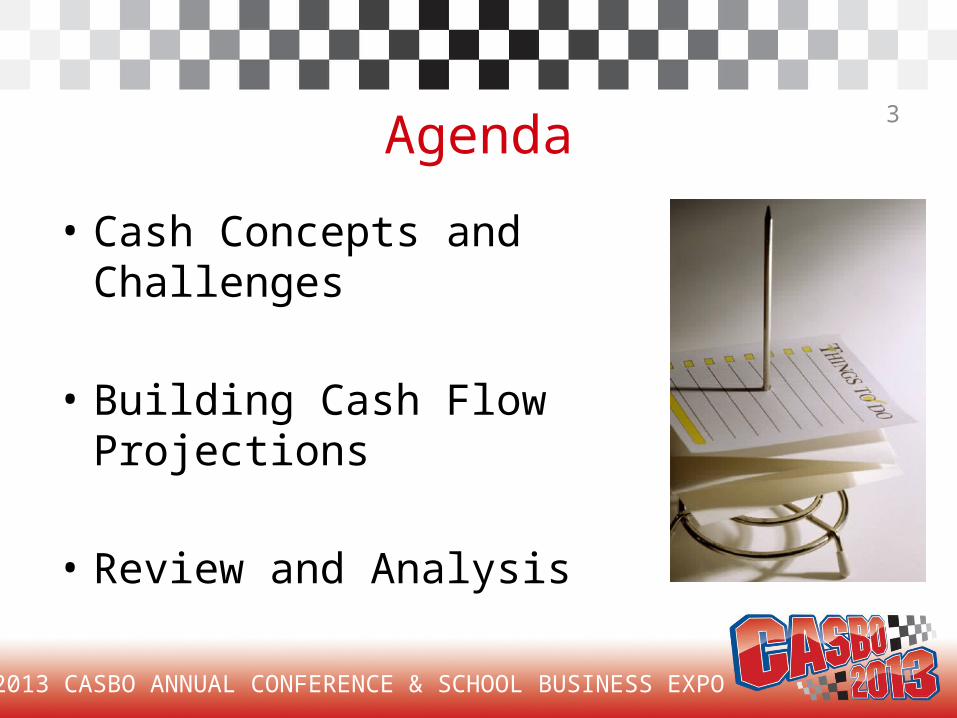

Cash vs. Fund Balance • Fund balance does not reveal what the

cash level will be Cash 100$ A/R

Assets 100$

A/P -

Fund Bal 100$

Cash -$ A/R 120

Assets 120$

A/P 20

Fund Bal 100$

Cash 120$ A/R

Assets 120$

A/P 20

Fund Bal 100$

Cash 40$ A/R 80

Assets 120$

A/P 20

Fund Bal 100$

8

2013 CASBO ANNUAL CONFERENCE & SCHOOL BUSINESS EXPO

Cash vs. Fund Balance• High fund balance

does not necessarily mean high cash levels

• It is possible to have greater than minimum reserve levels, yet be out of cash

A/R DetailsRL State Aid 1,100,000 Federal (Spec Ed, Title I, etc) 100,000 State (CSR, Lottery, etc) 300,000 Local (Spec Ed fm SELPA) 100,000

1,600,000

BudgetRevenue 8,900,000 Expenditures 9,100,000 Excess (Deficiency) (200,000)

Beginning Balance 1,300,000 Ending Balance 1,100,000 12%

Components of Fund BalanceCash (300,000) A/R 1,600,000

Assets 1,300,000 A/P 200,000 Ending Balance 1,100,000

9

2013 CASBO ANNUAL CONFERENCE & SCHOOL BUSINESS EXPO

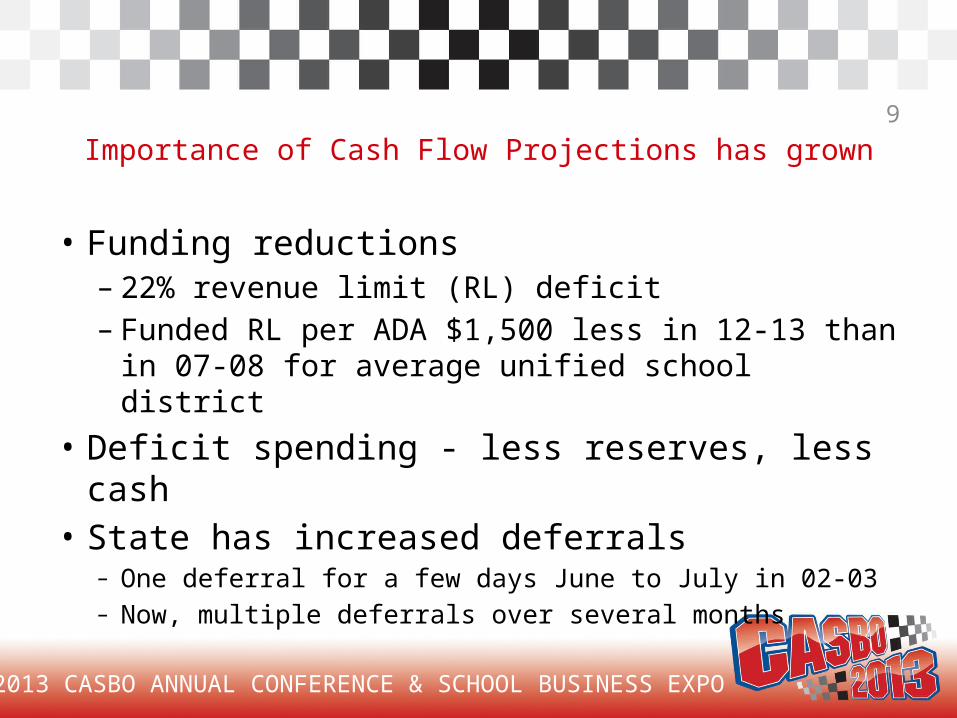

Importance of Cash Flow Projections has grown

• Funding reductions – 22% revenue limit (RL) deficit– Funded RL per ADA $1,500 less in 12-13 than

in 07-08 for average unified school district

• Deficit spending - less reserves, less cash• State has increased deferrals

– One deferral for a few days June to July in 02-03– Now, multiple deferrals over several months

10

2013 CASBO ANNUAL CONFERENCE & SCHOOL BUSINESS EXPO

Delayed Apportionment Funding

2013-142012-13Feb to Jul

$700MJul to Sep

$500MJul to Dec

Aug to Dec$600M

$800MOct to Dec

Mar to Apr

$900M

End of Fiscal Year

Apr to Jul $419M

$679M now $176M

Apr to Aug / July

May to Jul$800M

May to Aug / July$1.0B now $1.18B

100%

Jun to Jul

Mar to Aug

$764M

Within year

deferrals

Cross-year deferrals

Since Proposition 30 tax initiative passed, cross

year deferrals are reduced by $2.1 billion

$2.0B now $532M

$1.3B now $1.029B

Apr to Aug

11

2013 CASBO ANNUAL CONFERENCE & SCHOOL BUSINESS EXPO

Revenue Limit – Deferrals• Districts that receive a higher percentage

of RL as state aid are hit hardestRevenue Limit Example District A District B District C

Revenue Limit $10,000,000 $10,000,000 $10,000,000

Property Taxes $ 9,000,000 $ 5,000,000 $ 1,000,000

Education Protection Account $ 1,000,000 $ 2,000,000 $ 2,000,000

State Aid $ 3,000,000 $ 7,000,000

Cross Year Deferrals @30% $ -0- $ 900,000 $ 2,100,000

12

2013 CASBO ANNUAL CONFERENCE & SCHOOL BUSINESS EXPO

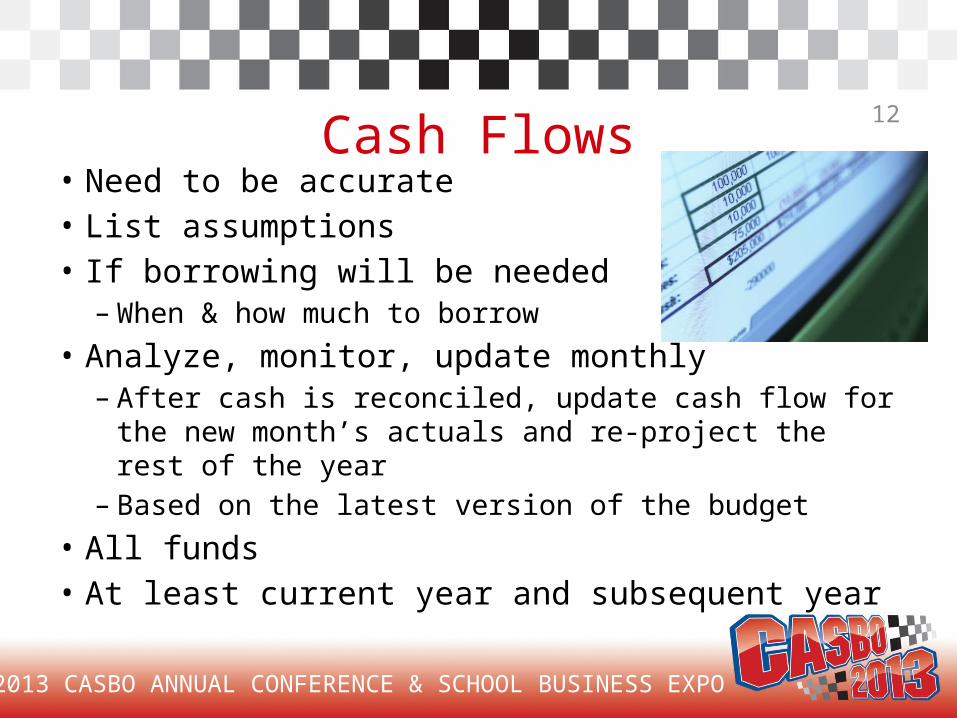

Cash Flows• Need to be accurate• List assumptions• If borrowing will be needed

– When & how much to borrow

• Analyze, monitor, update monthly – After cash is reconciled, update cash flow for the new

month’s actuals and re-project the rest of the year– Based on the latest version of the budget

• All funds• At least current year and subsequent year

13

BUILDING CASH FLOW PROJECTIONS

14

2013 CASBO ANNUAL CONFERENCE & SCHOOL BUSINESS EXPO

Cash Flow Format1 2 11 12 13

Object July August . . . May June Accruals Adjustments TOTAL Budget

A. BEGINNING CASH 9110 0 0 0 0

B. RECEIPTS

Revenue Limit Sources

Principal Apportionment 8010-8019 0 0 0 0 0 0 0 0

Property Taxes 8020-8079 0 0 0 0 0 0 0 0

TOTAL RECEIPTS 0 0 0 0 0 0 0 0

C. DISBURSEMENTS

Certificated Salaries 1000-1999 0 0 0 0 0 0 0 0

Classified Salaries 2000-2999 0 0 0 0 0 0 0 0

TOTAL DISBURSEMENTS 0 0 0 0 0 0 0 0

D. BALANCE SHEET TRANSACTIONS

ASSETS

Cash Not in Treasury 9111-9199 0 0 0 0 0 0 0

Accounts Receivable 9200-9299 0 0 0 0 0 0 0

Subtotal Assets 0 0 0 0 0 0 0

LIABILITIES 0

Suspense Clearing 9910 0 0 0 0 0 0 0

TOTAL BALANCE SHEET TRANSACTIONS 0 0 0 0 0 0 0

E.0 0 0 0 0 0 0

F.ENDING CASH (A + E) 0 0 0 0

G. -

Beginning Balances

(Ref. Only)

ACTUALS THROUGH THE MONTH OF (Enter Month Name):

NET INCREASE/DECREASE (B - C + D)

ENDING CASH, PLUS CASH ACCRUALS AND ADJUSTMENTS

15

2013 CASBO ANNUAL CONFERENCE & SCHOOL BUSINESS EXPO

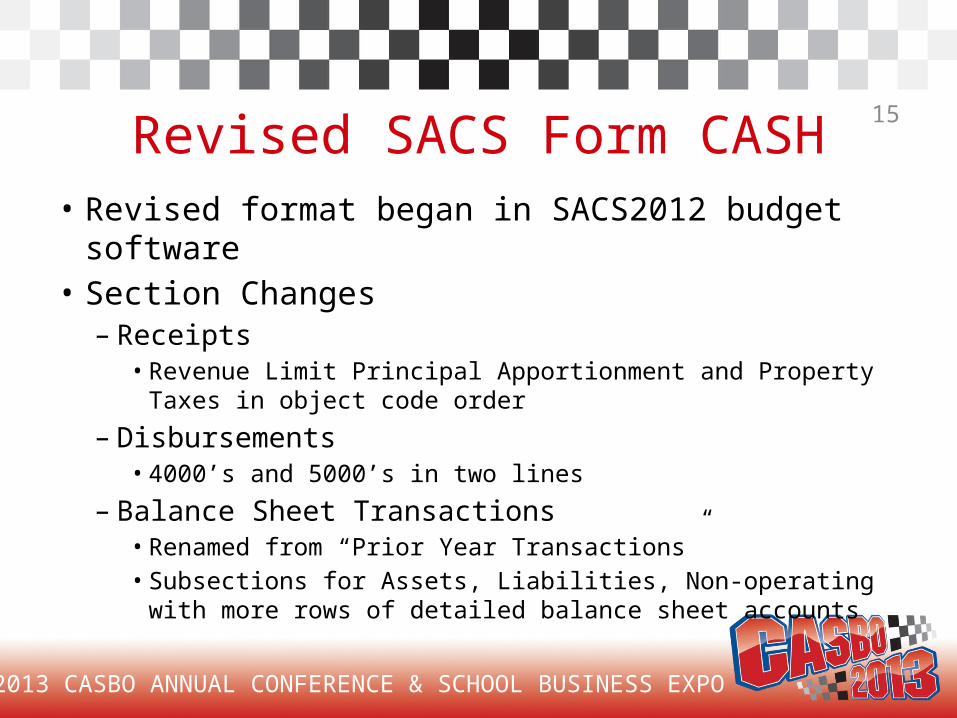

Revised SACS Form CASH• Revised format began in SACS2012 budget software• Section Changes

– Receipts • Revenue Limit Principal Apportionment and Property Taxes in

object code order

– Disbursements• 4000’s and 5000’s in two lines

– Balance Sheet Transactions• Renamed from “Prior Year Transactions”• Subsections for Assets, Liabilities, Non-operating with more

rows of detailed balance sheet accounts

16

2013 CASBO ANNUAL CONFERENCE & SCHOOL BUSINESS EXPO

New SACS Form CASH• New columns

– Beginning Balances (Balance Sheet Transactions)• Allows entry of beginning balances as reference• Example – enter beginning Accounts Receivable balance, can

compare to total ARs projected to be received during months of cash flow projections

– Adjustments• Noncash differences (not accruals) between cash transactions and amounts

budgeted• Example -carryover that is budgeted but will not be spent this year

– Budget• Facilitates comparison of cash flow totals to budget

• Subsequent year cash flow tab available

17

2013 CASBO ANNUAL CONFERENCE & SCHOOL BUSINESS EXPO

Building a Cash Flow Projection• Projected budget/interim

– Best if it is done before starting

cash flow projection

• Columns– Completed months = actual amounts– Upcoming months = projected amounts– Accruals for cash in/out that will occur after June 30– Adjustments column – noncash adjustments

• Example: carryover that is budgeted but will not be spent this year

• Estimating cash inflows and outflows– Dividing the budgeted amount by 12 months

is not a good strategy

18

2013 CASBO ANNUAL CONFERENCE & SCHOOL BUSINESS EXPO

Templates

• Can use a template to help prepare cash flow– Create your own, modify an existing one– FCMAT Budget Explorer Cash Flow tool– EDCOE Cash Flow Template

• http://edcoe.org/departments/business_services/CFO_Corner.html

• EDCOE template tips– Start on “Welcome” and “Instructions” tab– Go slowly, step-by-step

19

2013 CASBO ANNUAL CONFERENCE & SCHOOL BUSINESS EXPO

Templates• Template ideas

– Format to make it easier• Match your financial system reports• Final result that matches SACS format

– Make template do the math• Input budget and actuals to date, template calculates

balance• Calculate % expected each month, monthly % x balance

– Have detailed schedule that feeds into summary schedule

• Break out elements in more detail – revenues, balance sheet, etc.

20

2013 CASBO ANNUAL CONFERENCE & SCHOOL BUSINESS EXPO

Revenue Limit – State AidSome ways to project month by month:

1. Spread remaining budget over upcoming months using estimated apportionment schedule percentages

2. Use Payment Schedule Summary Excel spreadsheet provided by CDE

In Principal Apportionment http://www.cde.ca.gov/fg/aa/pa/ See applicable fiscal year / certification period Look in Funding Excel Files

21

2013 CASBO ANNUAL CONFERENCE & SCHOOL BUSINESS EXPO

Estimated Principal Apportionment Schedule

MonthEducation Code Section (E.C.)14041(a)(2)

Education Code Section (E.C.)14041(a)(7)

Education Code Section (E.C.)14041(a)(8)

Jul 2012 - - -Aug 2012 2.02% 6.06% 12.12%Sep 2012 12.73% 26.19% 41.19%Oct 2012 4.86% 8.11% 8.11%Nov 2012 9.00% - -Dec 2012 17.39% 19.64% 28.58%Jan 2013 9.00% 6.00% 6.00%Feb 2013 5.62% 4.24% -Mar 2013 2.45% 1.85% -Apr 2013 0.36% 0.27% -

May 2013 0.00% 0.00% -Jun 2013 0.00% 0.00% 0.00%Jul 2013 25.16% 19.01% 4.00%

Aug 2013 11.41% 8.62% -Total 100.00% 100.00% 100.00%

*Source – 12/21/12 SSC article

22

2013 CASBO ANNUAL CONFERENCE & SCHOOL BUSINESS EXPO

CDE Principal Apportionment Summary• Summary of certification by LEA

County Code

District Code

School District Total Revenue

Limit(0000-8011)

Charter School General Purpose

Entitlement(0000-8015)

Charter School Categorical Block

Grant(0000-8590)

Core Academic Program

(Supplemental Instruction,

Grades K-12)(0000-8590)

Gifted and Talented Education Program

(0000-8590)

Total County Office Funds

Transfer(0000-8011)

Total Principal Apportionment

A-2 A-3 A-4 A-5 A-15 A-22 B-1

56 72553 $ 9,030,040.00 $ - $ - $ 72,084.00 $ 42,444.00 $ (179,040.00) $ 8,990,306.00 56 72553 $ - $ 425,319.00 $ 136,409.00 $ - $ - $ - $ 561,952.00 56 72553 $ - $ 694,671.00 $ 261,688.00 $ 4,203.00 $ - $ - $ 963,416.00 56 72561 $ 10,981,217.00 $ - $ - $ 42,166.00 $ 27,173.00 $ (152,561.00) $ 10,965,287.00 56 72579 $ 140,134.00 $ - $ - $ - $ - $ - $ 140,134.00 56 72587 $ 11,791,179.00 $ - $ - $ 31,565.00 $ 23,995.00 $ (30,780.00) $ 11,860,249.00 56 72611 $ 291,995.00 $ - $ - $ 964.00 $ 5,269.00 $ - $ 306,934.00 56 72611 $ - $ 259,059.00 $ 72,109.00 $ 414.00 $ - $ - $ 334,418.00 56 72546 $ 34,877,592.00 $ - $ - $ 168,964.00 $ 102,837.00 $ (105,722.00) $ 39,067,157.00 56 72546 $ - $ 893,596.00 $ 230,718.00 $ - $ - $ - $ 1,124,314.00

OtherRL RL TOTAL

23

2013 CASBO ANNUAL CONFERENCE & SCHOOL BUSINESS EXPO

CDE Payment Schedule• Schedule of Principal Apportionment payments

– Includes RL State Aid + others (Adult, GATE, etc.)

CALIFORNIA DEPARTMENT OF EDUCATIONCertification of the 2012-13 Advance Apportionment

Monthly Payment Schedule by LEA

Regular Monthly Payment

Partial Repayment of July Deferral

Equals Amount in (4)

September Total

Sum of (10) and (11)

October Payment Before Deferral

October Deferred to

January(45.9620623% of

October Payment)

October Payment

(13) minus (14)

(2) (10) (11) (12) (13) (14) (15)8,990,306$ 809,128$ 335,471$ 1,144,599$ 809,128$ 371,892$ 437,236$

561,952$ 50,576$ 20,969$ 71,545$ 50,576$ 23,246$ 27,330$ 963,416$ 86,707$ 35,950$ 122,657$ 86,707$ 39,852$ 46,855$

10,965,287$ 986,876$ 409,167$ 1,396,043$ 986,876$ 453,589$ 533,287$ 140,134$ 12,612$ 5,229$ 17,841$ 12,612$ 5,797$ 6,815$

11,860,249$ 1,067,422$ 442,562$ 1,509,984$ 1,067,422$ 490,609$ 576,813$ 4,985,297$ 448,677$ 186,025$ 634,702$ 448,677$ 206,221$ 242,456$

46,719,385$ 4,204,745$ 1,743,322$ 5,948,067$ 4,204,745$ 1,932,588$ 2,272,157$ 306,934$ 27,624$ 11,453$ 39,077$ 27,624$ 12,697$ 14,927$ 334,418$ 30,098$ 12,479$ 42,577$ 30,098$ 13,834$ 16,264$

Advance Principal Apportionment

September 2012 October 2012

TOTALOct

payment

24

2013 CASBO ANNUAL CONFERENCE & SCHOOL BUSINESS EXPO

Revenue Limit – Education Protection Account (EPA)

• 2012-13, all EPA will be received in June

• After 2012-13, EPA to be received quarterly

25

2013 CASBO ANNUAL CONFERENCE & SCHOOL BUSINESS EXPO

Revenue Limit – Property Taxes

• Paid based on actual collections– Main tax receipt months are

December and April– Does your county auditor-controller have an estimated

property tax schedule?

• Education Revenue Augmentation Fund (ERAF) apportionments

• Redevelopment Funds• Charter School In-Lieu Transfers

26

2013 CASBO ANNUAL CONFERENCE & SCHOOL BUSINESS EXPO

Charter School In-Lieu Transfers• Education Code 47635 describes transfers

in lieu of property taxes to charter schools from the sponsoring LEA – Annual amount

Property Tax per ADA* x Charter ADA* Total District + Charter ADA

– Schedule of transfers P-2 Annual

Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Feb6% 12% 8% 8% 8% 8% 8% 2/6 1/6 1/6 1/6 Balance PY adj

Based on Prior Year P-2 Based on P-1 Balance owed

27

2013 CASBO ANNUAL CONFERENCE & SCHOOL BUSINESS EXPO

Charter School In-Lieu Transfers• EC schedule does not

correspond to actual property tax collections

• EC schedule was not affected by changes to RL State Aid schedule (5-5-9, deferrals)– Charter and District could

agree upon alternate schedule of transfers

28

2013 CASBO ANNUAL CONFERENCE & SCHOOL BUSINESS EXPO

Federal Revenues• SACS object codes 8100-8299• Title I, Title II, etc• Special Education• When do you expect to receive these

revenues?– May depend on when you spend them and

when you report that you’ve spent them– Quarterly federal cash management reporting

29

2013 CASBO ANNUAL CONFERENCE & SCHOOL BUSINESS EXPO

State Revenues• Some programs paid in Principal Apportionment • Tier 3 programs - 5-5-9 schedule• Economic Impact Aid - 20% x 5• Lottery - quarterly• Class Size Reduction

– Partly deferred across fiscal years

• CDE provides an estimated cash flow schedule for select categorical programs– CDE Finance & Grants Allocations & Apportionments

Categorical Programs Estimated Cash Flow Schedule – http://www.cde.ca.gov/fg/aa/ca/estcashflow.asp– Can use to calculate percent by month

30

2013 CASBO ANNUAL CONFERENCE & SCHOOL BUSINESS EXPO

Local Revenues

• SELPA apportionment transfers• Interagency revenues• Transportation Fees• Other local revenue• Consortium revenue• When do you expect to receive

these revenues?

31

2013 CASBO ANNUAL CONFERENCE & SCHOOL BUSINESS EXPO

Salaries• Historical percentage outflow by month is a reliable indicator

– Will include periodic payments e.g. longevity, stipends– Takes into account salary roll backs or other % changes

32

2013 CASBO ANNUAL CONFERENCE & SCHOOL BUSINESS EXPO

Salaries

• Certificated and classified monthly patterns differ• Recent changes may not be reflected in prior year

trends and should be addressed– Furlough days when not converted to a salary decrease– 10 paychecks to 12 paychecks– Program redesign, e.g. summer school– School year changes, e.g. instructional days, staff

development days– One time restoration payments

33

2013 CASBO ANNUAL CONFERENCE & SCHOOL BUSINESS EXPO

Benefits• Mostly driven by payroll• Prior year trends or consistent with

salaries• Some independent of payroll

– Retiree benefits– Golden handshake payments

34

2013 CASBO ANNUAL CONFERENCE & SCHOOL BUSINESS EXPO

Supplies & Services• Prior year trends are more erratic but still

better than dividing by 12– Less working days in December to issue warrants– June crush to pay invoices instead of accruing– School year start-up ordering in early summer with payments

coming due in August or September

• Best to analyze big outflows separately– Utilities & phones…seasonal fluctuations, two payments in a

month

– Pass-thru/subagreement outflows link to inflow

35

2013 CASBO ANNUAL CONFERENCE & SCHOOL BUSINESS EXPO

Capital Outlay• Capital expenditures in the general fund

– Few

– Infrequent

– One-time

– Some leases…recurring and predictable

36

2013 CASBO ANNUAL CONFERENCE & SCHOOL BUSINESS EXPO

Other Outflows• Interfund transfers out

– Should be in the budget

– Some funds regularly receive annual transfers from the general fund, e.g. food services

• Debt payments– Be sure to include these …make a big difference in cash

balance

37

2013 CASBO ANNUAL CONFERENCE & SCHOOL BUSINESS EXPO

Balance Sheet Accounts• Assets

– Accounts Receivable• When will you receive them?• If cleared to revenue before receipt,

consider tracking separately in revenue section of cash flow projection

– Due from Other Funds• When will the other fund pay this fund?

– Prepaid expenditures• When you clear, hits the expenditure and

the balance sheet account (object 9330) – net $0 cash

38

2013 CASBO ANNUAL CONFERENCE & SCHOOL BUSINESS EXPO

Balance Sheet Accounts• Liabilities

– Accounts Payable from prior year• When will you pay them?

– Use Tax Liability• Accumulates during the year, paid quarterly or yearly

– Workers Compensation Liability• Accumulates when payroll is processed• Paid periodically, such as twice a year

– Health & Welfare Liability• Accumulates when payroll is processed

– May be higher in some months than others due to 10, 11, 12 month employees, etc

• Paid to vendor monthly• Plans may not align with July to June fiscal year

39

2013 CASBO ANNUAL CONFERENCE & SCHOOL BUSINESS EXPO

Balance Sheet Accounts• Liabilities (cont.)

– Dues Liability– Voluntary Deductions– Summer Set Aside

• 10 or 11 month employees paid in 12 months• Set aside amounts during the year from payroll• Paid out at the end in the summer

– Due to Other Funds• When will this fund pay to the other fund?

– Current Loans (TRANs)• When will you receive TRAN proceeds?• When will you have TRAN repayments?

– Deferred Revenue • When you clear, hits revenue and deferred revenue

(object 9650) – net $0 cash

40

2013 CASBO ANNUAL CONFERENCE & SCHOOL BUSINESS EXPO

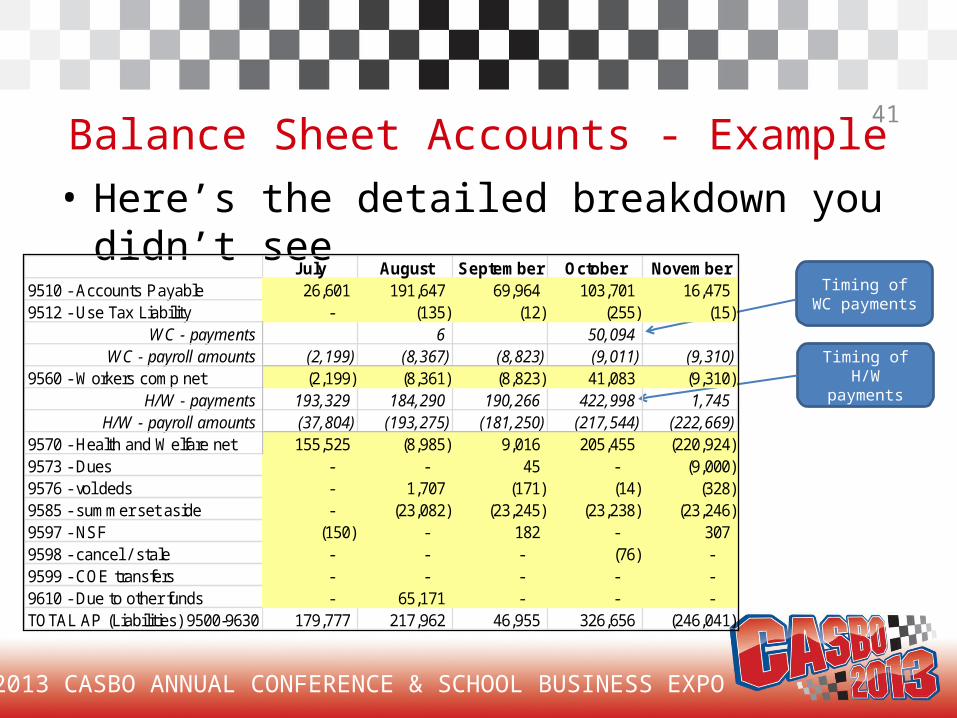

Balance Sheet Accounts – Example

• The cash flow report from your financial system shows the following for Liability accounts 9500-9630

• Does this makes sense?

July August September October November Accounts Payable............9500-9630 179,777 217,962 46,955 326,656 (246,041)

41

2013 CASBO ANNUAL CONFERENCE & SCHOOL BUSINESS EXPO

Balance Sheet Accounts - Example• Here’s the detailed breakdown you didn’t see

July August September October November9510 - Accounts Payable 26,601 191,647 69,964 103,701 16,475 9512 - Use Tax Liability - (135) (12) (255) (15)

WC - payments 6 50,094 WC - payroll amounts (2,199) (8,367) (8,823) (9,011) (9,310)

9560 - Workers comp net (2,199) (8,361) (8,823) 41,083 (9,310) H/W - payments 193,329 184,290 190,266 422,998 1,745

H/W - payroll amounts (37,804) (193,275) (181,250) (217,544) (222,669) 9570 - Health and Welfare net 155,525 (8,985) 9,016 205,455 (220,924) 9573 - Dues - - 45 - (9,000) 9576 - vol deds - 1,707 (171) (14) (328) 9585 - summer set aside - (23,082) (23,245) (23,238) (23,246) 9597 - NSF (150) - 182 - 307 9598 - cancel / stale - - - (76) - 9599 - COE transfers - - - - - 9610 - Due to other funds - 65,171 - - - TOTAL AP (Liabilities) 9500-9630 179,777 217,962 46,955 326,656 (246,041)

Timing of H/W payments

Timing of WC payments

42

2013 CASBO ANNUAL CONFERENCE & SCHOOL BUSINESS EXPO

Multiyear Cash Flow• Use current year cash flow and multiyear

projection to build a multiyear cash flow projection– Projected ending cash for current year is

beginning cash for subsequent year– Similar trends but adjust for changes

• For example, EPA arrives in June in 2012-13 but quarterly in 2013-14

43

REVIEW AND ANALYSIS

44

2013 CASBO ANNUAL CONFERENCE & SCHOOL BUSINESS EXPO

Review the Cash Flow Projection

• Totals column sums the cash in/out, accruals and adjustments for each type of category (revenues, expenditures, etc)– Do amounts match totals in budget?

• Revenues• Expenditures• Net Increase/Decrease

45

2013 CASBO ANNUAL CONFERENCE & SCHOOL BUSINESS EXPO

Is the Cash Flow Projection Reasonable?

• Comparison to Fund Balance– Is the total ending cash plus accruals and

adjustments shown in the cash flow projection reasonably close to the ending fund balance shown in the budget?

Example• In the spring, district prepared cash flow

projection to look at potential cash borrowing needs for the following fiscal year

46

2013 CASBO ANNUAL CONFERENCE & SCHOOL BUSINESS EXPO

Comparison to Fund Balance• District’s initial cash flow

– Negative balances in Oct, Nov, Feb, Mar, May, Jun

– June ending cash $(113,335)– Accruals $ 366,699– Total $ 253,363

• Looked like district would need some in-year and cross year borrowing

• Looked like once all accruals received, the district would have $253,363 fund balance

47

2013 CASBO ANNUAL CONFERENCE & SCHOOL BUSINESS EXPO

Comparison to Fund Balance• However…

– Budget ending fund balance $521,792– Cash flow total $253,363

• Why the difference?

• After research, found– July 1 beginning balance was entered incorrectly– Estimated payables of $45,000 were not listed

48

2013 CASBO ANNUAL CONFERENCE & SCHOOL BUSINESS EXPO

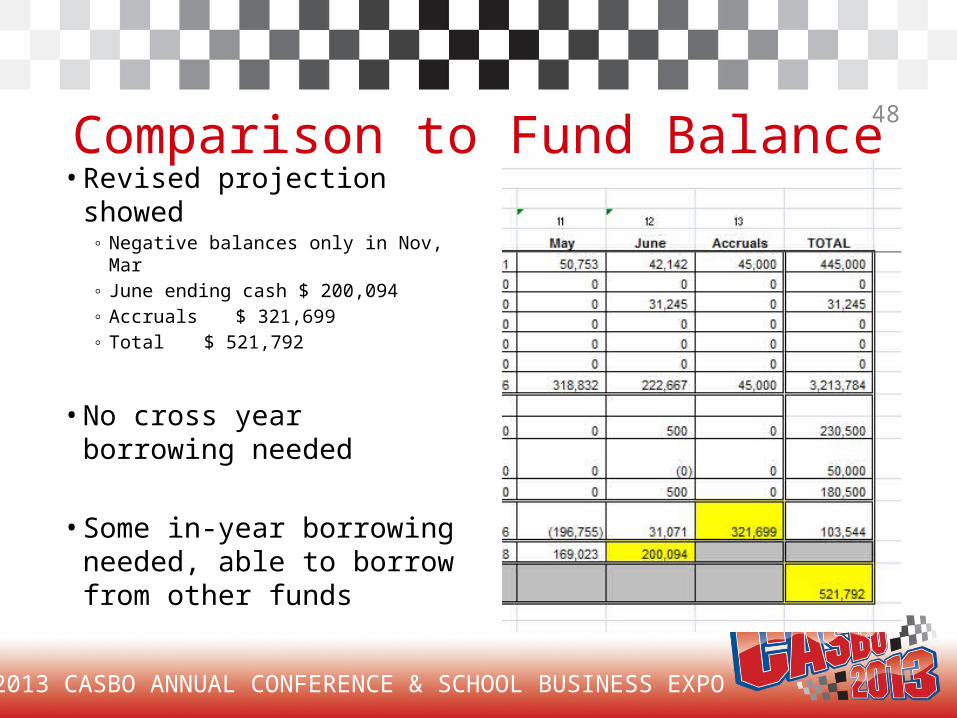

Comparison to Fund Balance• Revised projection

showed◦ Negative balances only in Nov, Mar◦ June ending cash $ 200,094◦ Accruals $ 321,699◦ Total $ 521,792

• No cross year borrowing needed

• Some in-year borrowing needed, able to borrow from other funds

49

2013 CASBO ANNUAL CONFERENCE & SCHOOL BUSINESS EXPO

Negative Balances?• Look to see if there are projected negative cash

balances• If so, what borrowing options

are being considered?– Inter-fund borrowing

• Need to know cash availability• May need separate cash flow

projections for other funds

– Borrowing from COE / County– TRANs

50

2013 CASBO ANNUAL CONFERENCE & SCHOOL BUSINESS EXPO

Borrowing Options• Internal borrowing

– From other funds of the LEA – EC 42603– Up to 75% of the cash in the lending fund– Borrowing fund must earn enough to repay– Paid back generally within a year

• External borrowing– From COE - EC 42621, 42622 and 47603 (thru 7/1/17)

• Up to 85% of anticipated revenues• If COE is willing and able

– From County Treasurer – EC 42620, CA Const. Art. XVI, § 6

• No loans after last Monday in April• Up to 85% of anticipated revenues

– Tax and Revenue Anticipation Notes (TRANs) – GC 53852

51

2013 CASBO ANNUAL CONFERENCE & SCHOOL BUSINESS EXPO

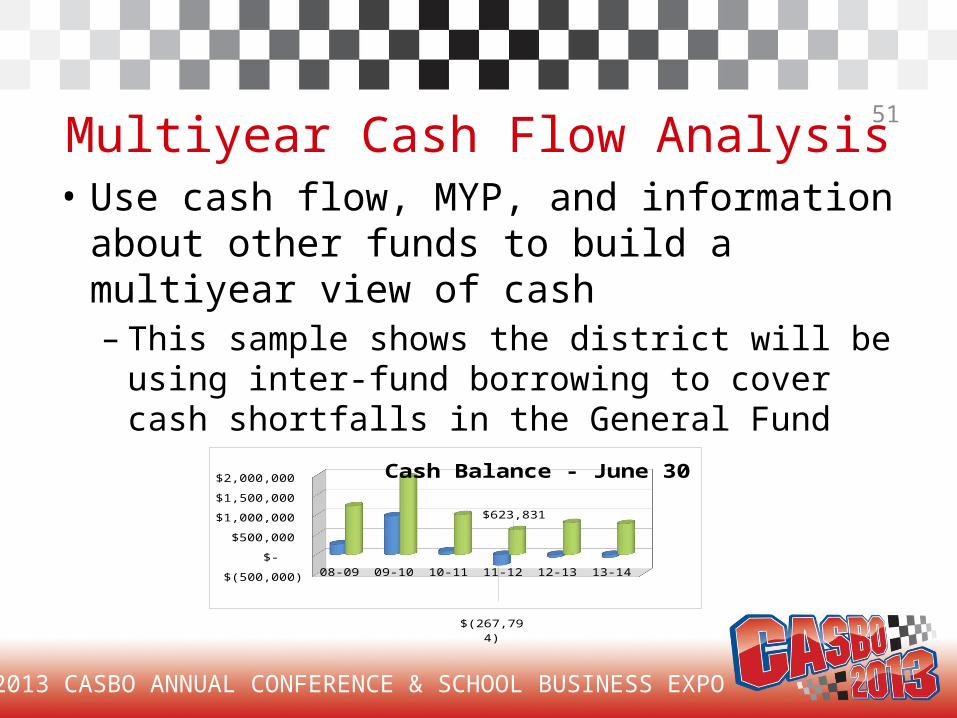

Multiyear Cash Flow Analysis• Use cash flow, MYP, and information about

other funds to build a multiyear view of cash– This sample shows the district will be using

inter-fund borrowing to cover cash shortfalls in the General Fund

08-09 09-10 10-11 11-12 12-13 13-14 $(500,000)

$-

$500,000

$1,000,000

$1,500,000

$2,000,000

$(267,794)

$623,831

Cash Balance - June 30

General Fund All Funds

52

2013 CASBO ANNUAL CONFERENCE & SCHOOL BUSINESS EXPO

Questions?

Thank you for providing feedback by completing an evaluation