Embed Size (px)

Citation preview

r

2

This presentation contains certain forward-looking statements. These forward-looking statements may be identified by words such as ‘believes’, ‘expects’, ‘anticipates’, ‘projects’, ‘intends’, ‘should’, ‘seeks’, ‘estimates’, ‘future’ or similar expressions or by discussion of, among other things, strategy, goals, plans or intentions. Various factors may cause actual results to differ materially in the future from those reflected in forward-looking statements contained in this presentation, among others:

1 pricing and product initiatives of competitors;2 legislative and regulatory developments and economic conditions;3 delay or inability in obtaining regulatory approvals or bringing products to market; 4 fluctuations in currency exchange rates and general financial market conditions; 5 uncertainties in the discovery, development or marketing of new products or new uses of existing products,

including without limitation negative results of clinical trials or research projects, unexpected side-effects of pipeline or marketed products;

6 increased government pricing pressures; 7 interruptions in production 8 loss of or inability to obtain adequate protection for intellectual property rights; 9 litigation;10 loss of key executives or other employees; and11 adverse publicity and news coverage.

Any statements regarding earnings per share growth is not a profit forecast and should not be interpreted to mean that Roche’s earnings or earnings per share for this year or any subsequent period will necessarily match or exceed the historical published earnings or earnings per share of Roche.

For marketed products discussed in this presentation, please see full prescribing information on our website –www.roche.com

All mentioned trademarks are legally protected

33

Roche DiagnosticsGrowth through Innovation

Dianne Young, Investor Relations Officer - DiagnosticsLandsbanki event, Paris, March 18 2008

4

Overall Performance

Business Areas

Strategy for Future Growth

Personalised Healthcare

5

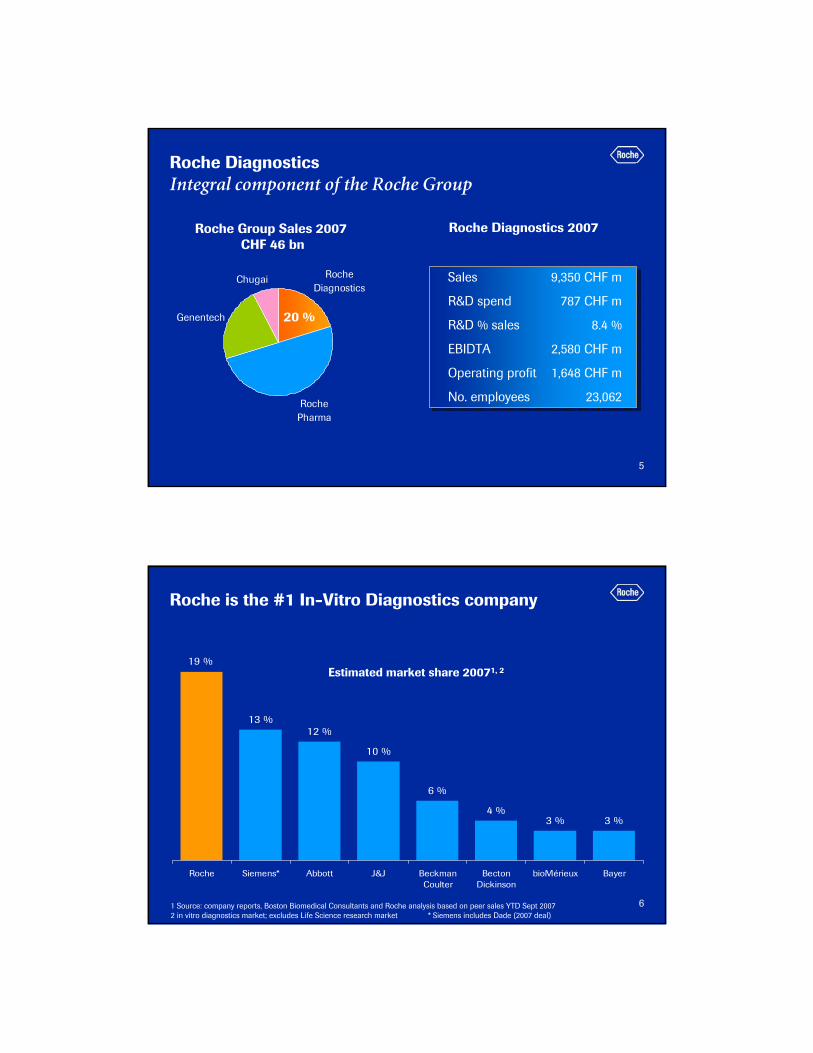

Roche DiagnosticsIntegral component of the Roche Group

Roche Diagnostics

Roche Pharma

Genentech

Chugai

20 %

Roche Group Sales 2007 CHF 46 bn

Roche Diagnostics 2007

Sales 9,350 CHF m

R&D spend 787 CHF m

R&D % sales 8.4 %

EBIDTA 2,580 CHF m

Operating profit 1,648 CHF m

No. employees 23,062

Sales 9,350 CHF m

R&D spend 787 CHF m

R&D % sales 8.4 %

EBIDTA 2,580 CHF m

Operating profit 1,648 CHF m

No. employees 23,062

6

Roche is the #1 In-Vitro Diagnostics company

3 %3 %4 %

6 %

10 %

12 %13 %

19 %

Roche Siemens* Abbott J&J BeckmanCoulter

BectonDickinson

bioMérieux Bayer

1 Source: company reports, Boston Biomedical Consultants and Roche analysis based on peer sales YTD Sept 20072 in vitro diagnostics market; excludes Life Science research market * Siemens includes Dade (2007 deal)

Estimated market share 20071, 2

7

1,148

3,216

692

4,294

Applied Science MolecularDiagnostics

ProfessionalDiagnostics

Diabetes Care

Market sales and position 2007Strongly positioned

MarketPosition

#7 #1 #1 #1

CHF 9,350 m

8

27.6%28.6%

31.7%31.2%

28.5%27.6%

18%19%18%17%16%

'02 '03 '04 '05 '06 '07

2007: Strong cash generationHigh margins relative to peers

EBITDA(% of Sales)

Roche*

Peers**

*Before exceptional items **peer group: Abbott Dx., Bayer Dx., Beckman Coulter, Becton Dickinson, Dade Behring, JNJ

9

Overall Performance

Business Areas

Strategy for Future Growth

Personalised Healthcare

10

0

1

2

3

4

5

2005 2006 2007

Immunochemistry Clinical ChemistryPOC products other

Professional DiagnosticsDouble-digit immunochemistry growth for 7th consecutive year

• Gained market share through strong instrument placements

– Elecsys 2010, cobas 6000, cobas e 411 systems

• Immunochemistry sales benefiting from new markers

– NT-proBNP, Trop T, TSH, Vitamin D, MPA

• Clinical Chemistry testing volume increased, dampened by pricing pressure

• Key transactions to access new markets– BioVeris acquisition (clinical trials)– OCD/ Novartis* agreement (HCV)

CHF billion

+8 %1

+13 %

+3 %

1 local growth * Ortho-Clinical Diagnostics, Inc. and Novartis Vaccines & Diagnostics

+7 %

11

Diabetes Care New product portfolio restoring growth

• Accu-Chek Aviva driving growth in key markets

• Accu-Chek Compact Plus and Accu-Chek Active strong contributors

• Accu-Chek Spirit (insulin pump) continues gaining momentum

• Launched:– Accu-Chek Performa

– Accu-Chek Compact Plus (new)

– Accu-Chek 360o

2004 2005 2006 2007

3%3%

10%

5%

DeclineMature flagship

product

Accu-Chek Advantage

StabilisationRejuvenated portfolio

Accu-Chek Performa

Accu-Chek Spirit

GrowthLeverage portfolio

Accu-Chek Compact

PlusAccu-Chek

Aviva

12

Molecular Diagnostics Automated platforms supporting virology market share

• Growth +3 % excluding industrial business, which declined as guided

• Blood screening:

– Continued up-take cobas s 201 system & cobas TaqScreen MPX Test in EU

– WNV test for cobas s 201 system FDA approved

– Contract with Japanese Red Cross renewed 5 yrs

• Virology benefiting from successful launch of CAP/CTM HIV Test in the US

1 local growth

+4 %

-1 %

0

400

800

1200

2005 2006 2007Virology Blood ScreeningOther Industrial Business

-2 %1

-49 %

CHF million

13

Overall Performance

Business Areas

Strategy for Future Growth

Personalised Healthcare

14

Applied Science Molecular Diagnostics

Professional Diagnostics

Diabetes Care

Life Science In Vitro Diagnostics

Researchers

Academia Pharma Biotech

Patients

Patients Consumers

Professionals

Wards/ClinicsCommercial labs Hospitals Physicians

In Vitro Diagnostics

Roche Diagnostics - overviewOperating five businesses in three distinct markets

Ventana Medical Systems

15

The Challenge…

Cost pressures

Unmet medical needs

Information complexity

Skilled labor shortages

Roche Diagnostics - Professional testing strategy Innovate to improve healthcare

Our Response…

We will innovate in

…to improve healthcare

Testing Efficiency Medical Value

16

Professional testing strategy – Testing efficiencyAddress increasing customer complexity

InstrumentInnovation

MenuBreadth

Workflow& IT

Testing Efficiency

17

Professional testing strategy – Testing efficiencyTotal solution provider to laboratories

InstrumentInnovation

• Modular platform

• Multiple configurations

• All lab sizes

Workflow& IT

cobas IT 3000 cobas IT 5000

Work AreaManagement

LaboratoryInformation System

cobas IT 1000

Point of CareData Management

MenuBreadth

Full menu on single platform

Cardiac: NT-proBNP, Trop TEndocrinology: Vitamin D3 Transplantation: MPARheumatoid Arthritis: anti-CCPSepsis: IL-6, ProcalcitoninVirology: anti-HCV, CMV

18

Professional testing strategy – Medical valueAddress unmet medical needs

Medical Value

DevelopNew

Content

ApplyContent forNew Uses

DecentralizeTesting

19

Professional testing strategy – Medical valueNew tests, new uses, new places

DevelopNew

Content

GenomicsRNA/ DNA

ProteomicsPeptides / Proteins

22 markercandidates

>12 markercandidates

Colon Cancer

ApplyContent forNew Uses

Rule-out HF (ER)Short-term monitoring (ER)

Targeted screening (Primary Care)Long-term monitoring (Outpatient/Primary Care)

Therapy stratification ACS (ER)Preoperative testing (Inpatient)

Population screening (Primary Care)

20082003 NT-proBNP Trial Program

DecentraliseTesting Hospital

PrimaryCare Patient

Patient Self-testing

20

Acquisitions - complement current portfolio Expanded technology offering for in vitro diagnostics

Testing on TissueIHC FISH/ CISH/

SISHProtein

expression

ElecsysAmpliChip

microarray

TaqMan

PCR

Testing after NA/ protein extraction

Molecular Diagnostics

Professional Diagnostics

In Vitro Diagnostics

Applied Science

Life Science

Researchers

Academia Pharma Biotech

Professionals

Wards/ClinicsCommercial labs Hospitals Physicians

Diabetes Care

Patients

Patients Consumers

In Vitro Diagnostics

Ventana Medical Systems

21

Applied Science

Life Science

Researchers

Academia Pharma Biotech

Diabetes Care

Patients

Patients Consumers

In Vitro Diagnostics

Roche Diagnostics - overviewOperating five businesses in three distinct markets

Molecular Diagnostics

Professional Diagnostics

In Vitro Diagnostics

Professionals

Wards/ClinicsCommercial labs Hospitals Physicians

Ventana Medical SystemsVentana Medical Systems

22

Applied Science

Life Science

Researchers

Academia Pharma Biotech

Roche Diagnostics – Applied ScienceFocusing on strategic growth areas

MicroarraySequencing

Genomic research

RT-PCR

LightCycler

Sequencing

Microarrays

Market: 800 m USDGrowth: +3 %

Market: 600 m USDGrowth: +13 %

454 Life Sciences

5%

NimbleGen3%

Source: Analyst reports, Company reports, Roche Analysis All growth rates in local currency

23

Roche Diagnostics – Applied Science Complete solution provider for Genomic Research

Genomics

Targ

etD

etec

tion

Proteomics Cytomics

RT-PCR 2D-GE MS Function Flow IHC/ISH SequencingMicroarray

DNA, RNA Proteins Cells Tissues

24

Diabetes Care

Patients

Patients Consumers

In Vitro Diagnostics

Roche Diagnostics – Diabetes CareEstablish “Circle of Care” management of diabetes for patients and providers

Provide comprehensive solutions beyond glucose monitoring

Restore growth with complete Accu-Chek portfolio

Delivery

Circleof Care Advice

Monitoring

25

Overall Performance

Business Areas

Strategy for Future Growth

Personalised Healthcare

26

LifeSciences Pharma

Roche Group – StrategyDifferentiation through Personalised Healthcare

In VitroDiagnostics

• Innovative and medically differentiated products/services

• Patient-tailored treatment that deliver tangible improvement to the health, quality of life and life expectancy of patients

• Leading in the development & commercialisation of targeted drugs & companion diagnostic tests

Increasingmedical value

to patients& physicians

27

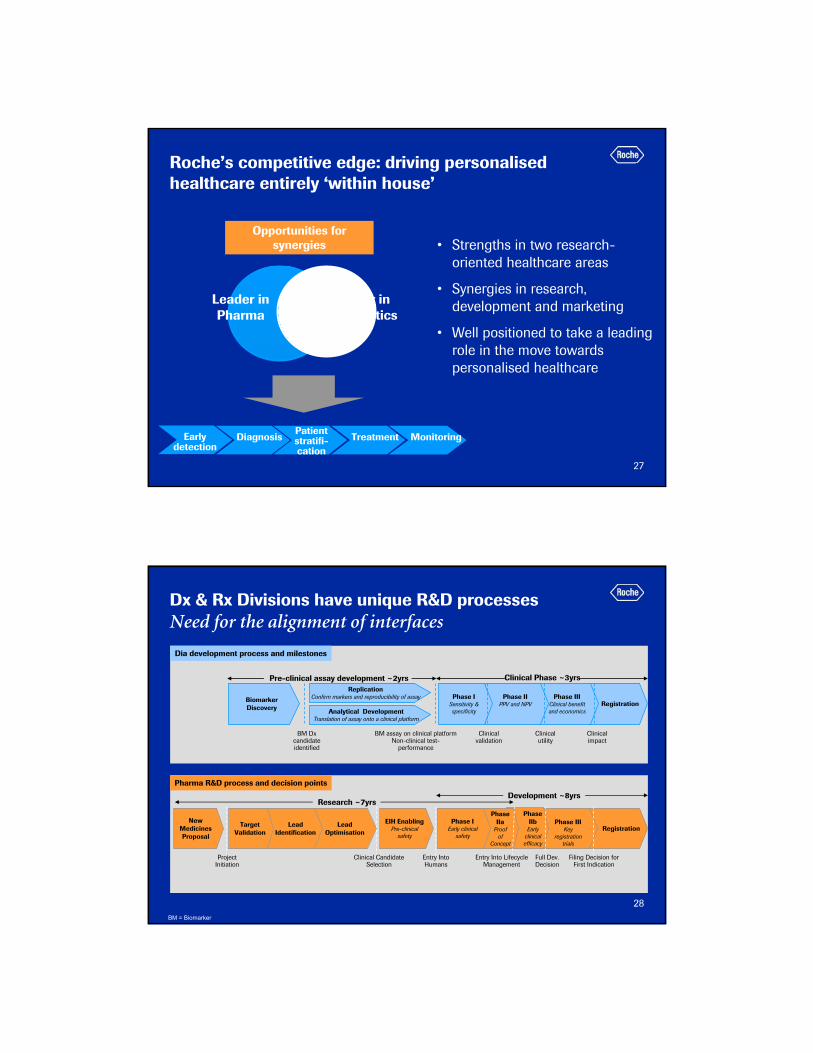

Roche’s competitive edge: driving personalisedhealthcare entirely ‘within house’

• Strengths in two research-oriented healthcare areas

• Synergies in research, development and marketing

• Well positioned to take a leading role in the move towards personalised healthcare

Opportunities for synergies

Leader inPharma

Leader in Diagnostics

Earlydetection

DiagnosisPatientstratifi-cation

Treatment Monitoring

28

Dia development process and milestones

RegistrationBiomarker Discovery

Phase IIIClinical benefit and economics

Phase IIPPV and NPV

Phase ISensitivity & specificity

BM Dx candidate identified

BM assay on clinical platformNon-clinical test-

performance

ReplicationConfirm markers and reproducibility of assay

Clinical impact

Clinical utility

Clinical validation

Analytical DevelopmentTranslation of assay onto a clinical platform

Pre-clinical assay development ~2yrs Clinical Phase ~3yrs

Dx & Rx Divisions have unique R&D processesNeed for the alignment of interfaces

BM = Biomarker

RegistrationPhase III

Key registration

trials

Phase IIb

Early clinical efficacy

Phase IIa

Proof of

Concept

EIH EnablingPre-clinical

safety

Lead Optimisation

Lead Identification

Target Validation

New Medicines Proposal

Project Initiation

Clinical Candidate Selection

Entry Into Humans

Phase IEarly clinical

safety

Entry Into Lifecycle Management

Full Dev. Decision

Filing Decision for First Indication

Research ~7yrsDevelopment ~8yrs

Pharma R&D process and decision points

29

Research CommercialiseDevelop

Applied Science

Molecular Diagnostics

Professional Diagnostics

Creating the interface Align to Pharma Disease Biology Areas

Inflammation/ Autoimmunity

Virology

Oncology

Diagnostics LiaisonManagers

Pharma

Diagnostics

Metabolism

CNS

Ventana Medical Systems

30

Integration of biomarkers across developmentFor every Pharma project

External & Internal Innovation

Research Development Marketing

Co-Develop with Diagnostics

Phase IPhase 0 Phase II Phase III FilingPhase IV

MarketTargetSelection

Lead Generation/

Optimization

Modeling & Simulation

Biomarker Development

More Internal Innovation

Clinical Research & Exploratory Development

Clinical Development

Confirmatory PhasePoCExploratory PhaseDiscoveryPhase

31

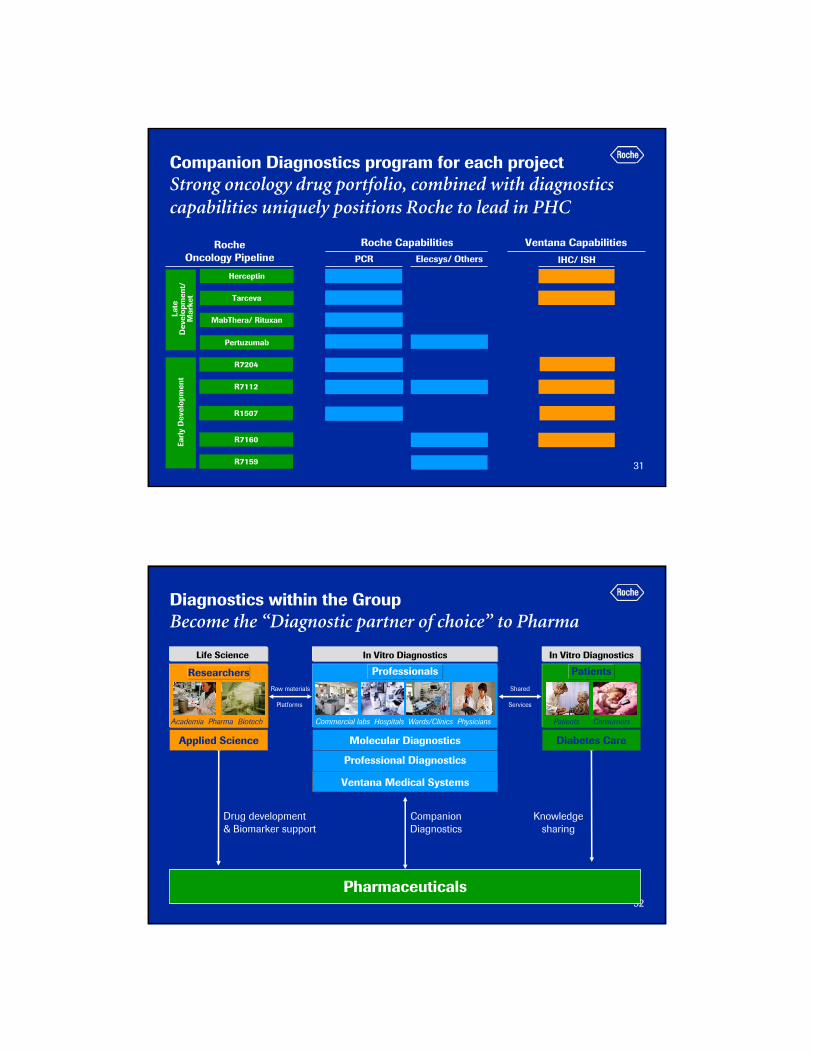

RocheOncology Pipeline PCR Elecsys/ Others

Roche Capabilities Ventana Capabilities

Herceptin

’ Tarceva

MabThera/ Rituxan

Pertuzumab

R7159

R7112

R7160Earl

y D

evel

opm

ent

Late

D

evel

opm

ent/

M

arke

t

R1507

R7204

IHC/ ISH

Companion Diagnostics program for each projectStrong oncology drug portfolio, combined with diagnostics capabilities uniquely positions Roche to lead in PHC

32

Raw materials

Platforms

CompanionDiagnostics

Drug development& Biomarker support

Knowledgesharing

Shared

Services

Pharmaceuticals

Diagnostics within the GroupBecome the “Diagnostic partner of choice” to Pharma

Molecular Diagnostics

Professional Diagnostics

In Vitro Diagnostics

Applied Science

Life Science

Researchers

Academia Pharma Biotech

Professionals

Wards/ClinicsCommercial labs Hospitals Physicians

Diabetes Care

Patients

Patients Consumers

In Vitro Diagnostics

Ventana Medical Systems

33

Summary

• Focus on medical value

• Strengthen and expand current business

• Fill strategic gaps

• Lead in personalised healthcare

PharmaIn VitroDiagnostics

Increasingmedical

valueto patients

& physicians

LifeSciences

34

Appendix

35

Sales in CHF billion USD2006 2007 CHF local growth

% change in

2007: Industry-leading sales growth continued

Pharmaceuticals 33.3 36.8 10 11 15

Diagnostics 8.7 9.3 7 6 12

Roche Group 42.0 46.1 10 10 15

36

Professional Diagnostics* 3,929 4,294 9 8 14 %

Diabetes Care 3,020 3,216 6 5 11 %

Molecular Diagnostics 1,175 1,148 -2 -2 2 %

Applied Science 623 692 11 11 16 %

Roche Diagnostics 8,747 9,350 7 6 12 %

2007: Diagnostics sales by business areaGrowth driven by Professional Diagnostics

* Amalgamation of Centralized Diagnostics and Near Patient Testing

% change in USD2006 2007 CHF local growthSales CHF million