Embed Size (px)

Citation preview

This presentation has been prepared for the 2016 General Insurance Seminar.The Institute Council wishes it to be understood that opinions put forward herein are not necessarily

those of the Institute and the Council is not responsible for those opinions.

This presentation has been prepared for the 2016 General Insurance Seminar.The Institute Council wishes it to be understood that opinions put forward herein are not necessarily

those of the Institute and the Council is not responsible for those opinions.

International Motor Insurance

trends

Kitty Ho

This presentation has been prepared for the 2016 General Insurance Seminar.The Institute Council wishes it to be understood that opinions put forward herein are not necessarily

those of the Institute and the Council is not responsible for those opinions.

Agenda• Claim frequency and size trends

• Claim fraud

• “Bad risks” pool

• Distribution

• Telematics

• Autonomous vehicles

This presentation has been prepared for the 2016 General Insurance Seminar.The Institute Council wishes it to be understood that opinions put forward herein are not necessarily

those of the Institute and the Council is not responsible for those opinions.

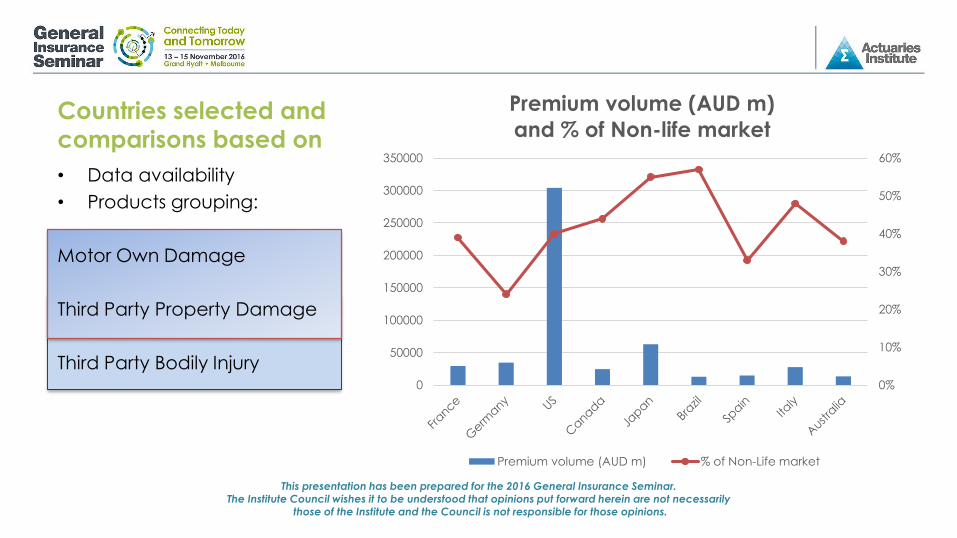

Countries selected and

comparisons based on

• Data availability

• Products grouping:

Motor Own Damage

Third Party Property Damage

Third Party Bodily Injury0%

10%

20%

30%

40%

50%

60%

0

50000

100000

150000

200000

250000

300000

350000

Premium volume (AUD m)

and % of Non-life market

Premium volume (AUD m) % of Non-Life market

This presentation has been prepared for the 2016 General Insurance Seminar.The Institute Council wishes it to be understood that opinions put forward herein are not necessarily

those of the Institute and the Council is not responsible for those opinions.

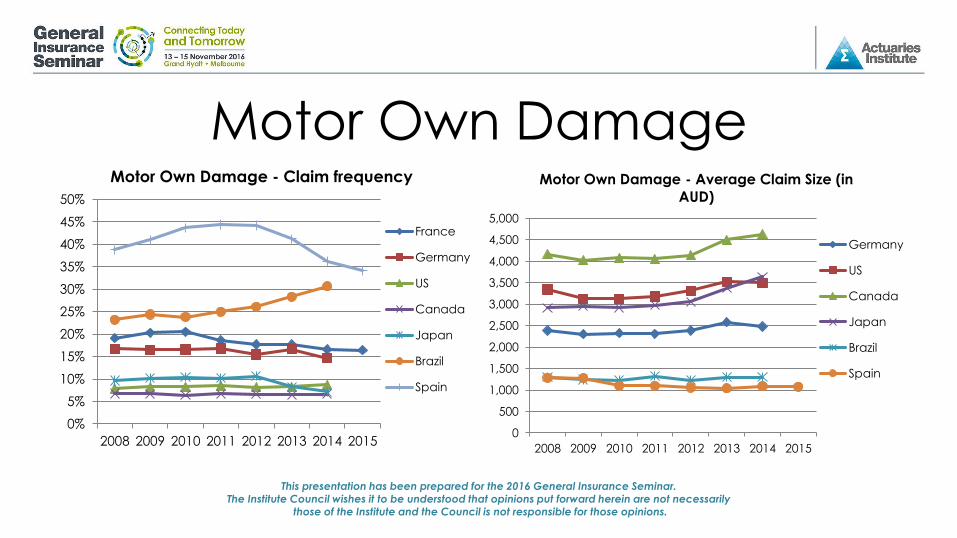

Motor Own Damage

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

2008 2009 2010 2011 2012 2013 2014 2015

Motor Own Damage - Claim frequency

France

Germany

US

Canada

Japan

Brazil

Spain

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

2008 2009 2010 2011 2012 2013 2014 2015

Motor Own Damage - Average Claim Size (in

AUD)

Germany

US

Canada

Japan

Brazil

Spain

This presentation has been prepared for the 2016 General Insurance Seminar.The Institute Council wishes it to be understood that opinions put forward herein are not necessarily

those of the Institute and the Council is not responsible for those opinions.

Third Party Property Damage

0

1,000

2,000

3,000

4,000

5,000

6,000

2008 2009 2010 2011 2012 2013 2014 2015

Motor Third Party Property Damage - Average

Claim Size (in AUD)

Germany

US

Canada

Japan

Brazil

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

2008 2009 2010 2011 2012 2013 2014 2015

Motor Third Party Property Damage - Claim

frequency

France

Italy

US

Canada

Japan

Spain

This presentation has been prepared for the 2016 General Insurance Seminar.The Institute Council wishes it to be understood that opinions put forward herein are not necessarily

those of the Institute and the Council is not responsible for those opinions.

MOD and TPPD combined

-

1,000

2,000

3,000

4,000

5,000

6,000

2009 2010 2011 2012 2013 2014 2015

Motor Third Party Property Damage and Own

Damage - Average Claim Size (in AUD)

Spain

US

Canada

Japan

Australia

0%

5%

10%

15%

20%

25%

30%

2009 2010 2011 2012 2013 2014 2015

Motor Third Party Property Damage and Own

Damage - Claim frequency

France

US

Canada

Japan

Australia

This presentation has been prepared for the 2016 General Insurance Seminar.The Institute Council wishes it to be understood that opinions put forward herein are not necessarily

those of the Institute and the Council is not responsible for those opinions.

Third Party Bodily Injury

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

2008 2009 2010 2011 2012 2013 2014 2015

Motor Third Party Bodily Injury - Average Claim

Size (in AUD)

Italy

US

Canada

Japan

Spain

Australia

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

2008 2009 2010 2011 2012 2013 2014 2015

Motor Third Party Bodily Injury - Claim

frequency

France

Italy

US

Canada

Japan

Spain

Australia

This presentation has been prepared for the 2016 General Insurance Seminar.The Institute Council wishes it to be understood that opinions put forward herein are not necessarily

those of the Institute and the Council is not responsible for those opinions.

Claims fraudTwo examples of claims fraud mitigation:

- Canada

- Italy

This presentation has been prepared for the 2016 General Insurance Seminar.The Institute Council wishes it to be understood that opinions put forward herein are not necessarily

those of the Institute and the Council is not responsible for those opinions.

CanadaFighting Fraud and Reducing Automobile

Insurance Rates Act 2014 and other initiatives

• Simplification of claim resolution system

• Consumer protection specific to the vehicle

towing and storage industries

• Changes to minor injury guidelines for claims

assessment

• Changes to coverage (increase standard

benefit level for medical and rehab benefits

but standard duration reduced from 10 to 5

years)

• CANATICS – analytical tools to identify

suspicious claims

This presentation has been prepared for the 2016 General Insurance Seminar.The Institute Council wishes it to be understood that opinions put forward herein are not necessarily

those of the Institute and the Council is not responsible for those opinions.

Italy - Integrated Anti-fraud Database

IVASS Insurance supervisor

Motor registry

database

Database of vehicle thefts and

losses

Tax database

National database

of residents

Central injury

archive

Drivers’ licence

database

This presentation has been prepared for the 2016 General Insurance Seminar.The Institute Council wishes it to be understood that opinions put forward herein are not necessarily

those of the Institute and the Council is not responsible for those opinions.

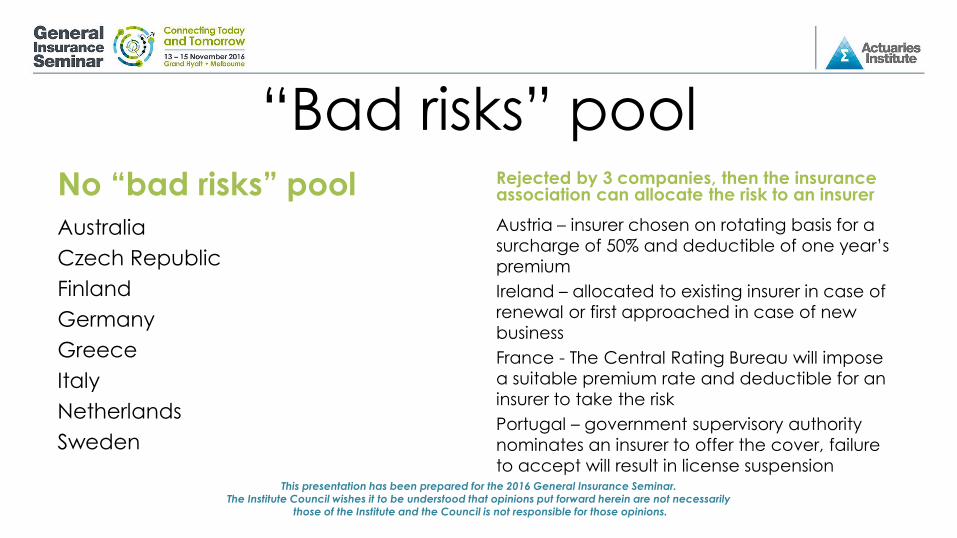

“Bad risks” poolNo “bad risks” pool

Australia

Czech Republic

Finland

Germany

Greece

Italy

Netherlands

Sweden

Rejected by 3 companies, then the insurance association can allocate the risk to an insurer

Austria – insurer chosen on rotating basis for a

surcharge of 50% and deductible of one year’s

premium

Ireland – allocated to existing insurer in case of

renewal or first approached in case of new

business

France - The Central Rating Bureau will impose

a suitable premium rate and deductible for an

insurer to take the risk

Portugal – government supervisory authority

nominates an insurer to offer the cover, failure

to accept will result in license suspension

This presentation has been prepared for the 2016 General Insurance Seminar.The Institute Council wishes it to be understood that opinions put forward herein are not necessarily

those of the Institute and the Council is not responsible for those opinions.

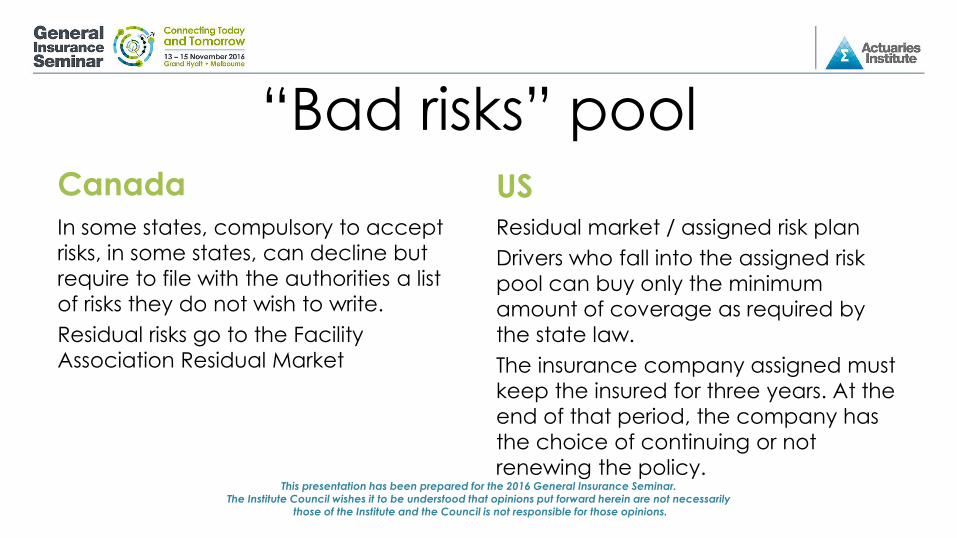

“Bad risks” poolCanada

In some states, compulsory to accept

risks, in some states, can decline but

require to file with the authorities a list

of risks they do not wish to write.

Residual risks go to the Facility

Association Residual Market

USResidual market / assigned risk plan

Drivers who fall into the assigned risk

pool can buy only the minimum

amount of coverage as required by

the state law.

The insurance company assigned must

keep the insured for three years. At the

end of that period, the company has

the choice of continuing or not

renewing the policy.

This presentation has been prepared for the 2016 General Insurance Seminar.The Institute Council wishes it to be understood that opinions put forward herein are not necessarily

those of the Institute and the Council is not responsible for those opinions.

“Bad risks” poolKorea

Assigned Insurance Plan pool for

Special risks include hire cars, tourist

coaches, express buses and other

types of commercial vehicles / policies

with poor claim records.

All non-life insurers are members of the

pool, which is managed by Korean Re.

The company ceding the risk retains

30% and distributes the balance to the

other pool members.

This presentation has been prepared for the 2016 General Insurance Seminar.The Institute Council wishes it to be understood that opinions put forward herein are not necessarily

those of the Institute and the Council is not responsible for those opinions.

DistributionStill dominated by agents and brokers

• Countries with more than 50% sold by agents and brokers: Belgium, Canada, Denmark, Germany, Italy, Japan, Netherlands, Norway, Portugal, Korea, Spain, Switzerland

• Insurance for Commercial vehicles

• In Switzerland, agents handle all the paperwork and completes the registration process

Countries with more direct sales:

Austria, Australia, Denmark, Greece, Ireland, UK, US

Internet? • Sales are limited

• Only around 10% of sales at most for some countries

• Internet mainly used for information and promotional purposes, comparison sites

• Sales initiated online are completed by personal contact by telephone

This presentation has been prepared for the 2016 General Insurance Seminar.The Institute Council wishes it to be understood that opinions put forward herein are not necessarily

those of the Institute and the Council is not responsible for those opinions.

Telematics / UBI• Globally, insurers have

implemented telematics products

or have pilots in progress.

• Collecting information on driving

behavior, attract lower-risk drivers,

price competitively

• Regulatory issues and privacy

concerns

This presentation has been prepared for the 2016 General Insurance Seminar.The Institute Council wishes it to be understood that opinions put forward herein are not necessarily

those of the Institute and the Council is not responsible for those opinions.

Telematics / UBI examplesDenmark Alka is a company that uses telematics to

record the speed before and after any

accident.

It costs DKK 1,000 to have the device installed

and having it cuts premium by 25%.

It is also used to find stolen vehicles and to

summon ambulance assistance in the event of

major accidents.

This presentation has been prepared for the 2016 General Insurance Seminar.The Institute Council wishes it to be understood that opinions put forward herein are not necessarily

those of the Institute and the Council is not responsible for those opinions.

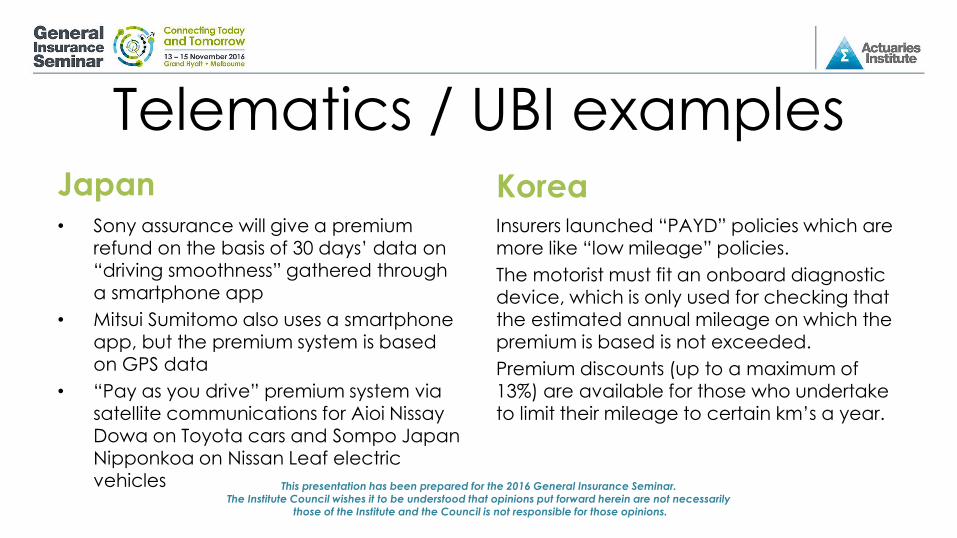

Telematics / UBI examplesJapan• Sony assurance will give a premium

refund on the basis of 30 days’ data on “driving smoothness” gathered through a smartphone app

• Mitsui Sumitomo also uses a smartphone app, but the premium system is based on GPS data

• “Pay as you drive” premium system via satellite communications for Aioi Nissay

Dowa on Toyota cars and Sompo Japan Nipponkoa on Nissan Leaf electric vehicles

KoreaInsurers launched “PAYD” policies which are more like “low mileage” policies.

The motorist must fit an onboard diagnostic device, which is only used for checking that the estimated annual mileage on which the premium is based is not exceeded.

Premium discounts (up to a maximum of 13%) are available for those who undertake to limit their mileage to certain km’s a year.

This presentation has been prepared for the 2016 General Insurance Seminar.The Institute Council wishes it to be understood that opinions put forward herein are not necessarily

those of the Institute and the Council is not responsible for those opinions.

Autonomous vehiclesPicture on the next 5 to 10 years

- Transition to driverless cars

- What will happen with respect to claims and pricing?

- Consider the big picture including public policy, sharing and transit

This presentation has been prepared for the 2016 General Insurance Seminar.The Institute Council wishes it to be understood that opinions put forward herein are not necessarily

those of the Institute and the Council is not responsible for those opinions.

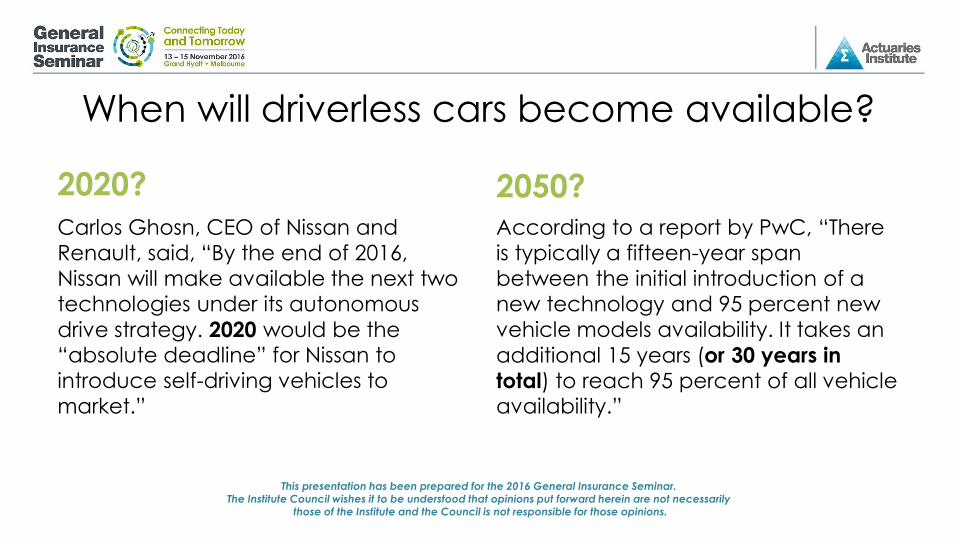

When will driverless cars become available?

2020?

Carlos Ghosn, CEO of Nissan and

Renault, said, “By the end of 2016,

Nissan will make available the next two

technologies under its autonomous

drive strategy. 2020 would be the “absolute deadline” for Nissan to

introduce self-driving vehicles to

market.”

2050?According to a report by PwC, “There

is typically a fifteen-year span

between the initial introduction of a

new technology and 95 percent new

vehicle models availability. It takes an

additional 15 years (or 30 years in

total) to reach 95 percent of all vehicle availability.”

This presentation has been prepared for the 2016 General Insurance Seminar.The Institute Council wishes it to be understood that opinions put forward herein are not necessarily

those of the Institute and the Council is not responsible for those opinions.

Transition to driverless carsConventional, non-automated vehicles

Semi-automated vehicles with driver assistance e.g. cars with

intelligent cruise control and lane-keeping mechanisms allow

drivers to travel on a highway without putting their hands on a

steering wheel

Conditional automation

High automation

Fully automated self-driving vehicles

This presentation has been prepared for the 2016 General Insurance Seminar.The Institute Council wishes it to be understood that opinions put forward herein are not necessarily

those of the Institute and the Council is not responsible for those opinions.

What will happen to…

Claims experience?

Reduction in collision frequency for

new vehicles

Collision by driver error will reduce, but

collision caused by defects will

increase

Increase in complexity and cost of

repairs

Claims resolution?Responsibility determination for

collisions (autonomous / conventional

vehicles)

Coverage becomes product liability

Insurers need to know if vehicle is in

self-driving mode and when a driver

assumes control

This presentation has been prepared for the 2016 General Insurance Seminar.The Institute Council wishes it to be understood that opinions put forward herein are not necessarily

those of the Institute and the Council is not responsible for those opinions.

What will happen to…

Pricing?Ratemaking will be a challenge with

no history of losses

Brokers and agents may find it difficult

to understand the underwriting

outcomes

Insurance for aircraft, ships and trains

with substantial automation may

provide guidance

This presentation has been prepared for the 2016 General Insurance Seminar.The Institute Council wishes it to be understood that opinions put forward herein are not necessarily

those of the Institute and the Council is not responsible for those opinions.

In the next 10 years…

“Automated vehicles: Implications for the Insurance

Industry in Canada” The Insurance Institute Canada

Over the next 10 years,

• Conventional vehicles will likely account for 70 - 90% of the kilometres driven on Canadian roads.

• Semi-automated cars and trucks will likely account for 10 - 25% of the kilometres driven.

• Self-driving vehicles will likely account for < 5% of the kilometres driven on public

roads.

This presentation has been prepared for the 2016 General Insurance Seminar.The Institute Council wishes it to be understood that opinions put forward herein are not necessarily

those of the Institute and the Council is not responsible for those opinions.

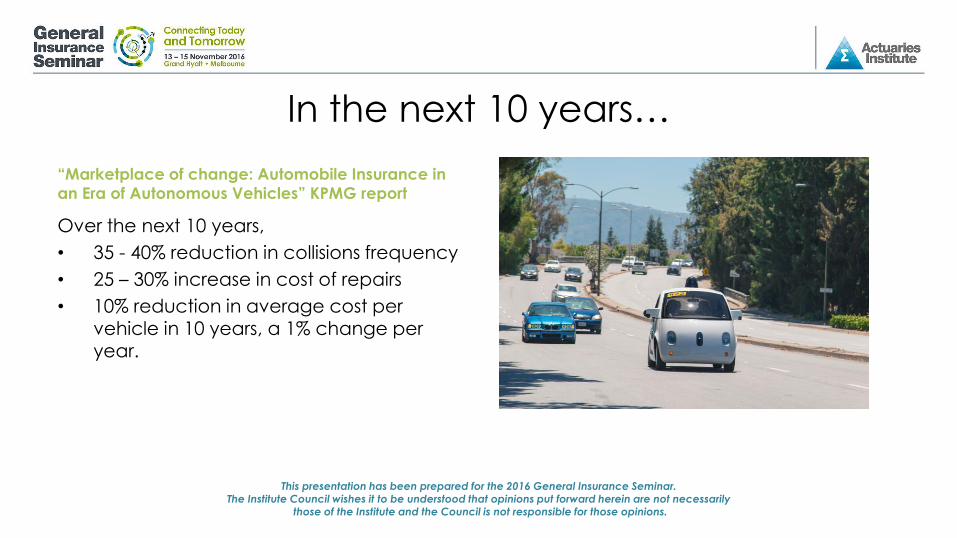

In the next 10 years…

“Marketplace of change: Automobile Insurance in

an Era of Autonomous Vehicles” KPMG report

Over the next 10 years,

• 35 - 40% reduction in collisions frequency

• 25 – 30% increase in cost of repairs

• 10% reduction in average cost per vehicle in 10 years, a 1% change per year.

This presentation has been prepared for the 2016 General Insurance Seminar.The Institute Council wishes it to be understood that opinions put forward herein are not necessarily

those of the Institute and the Council is not responsible for those opinions.

In the next 10 years…

Determination of legal responsibility

• Insurance coverage is designed around

responsibility and the capacity for managing

risk

• The focus of insurance coverage will remain on

the driver, for at least the next 10 years,

because drivers will remain responsible for the

overall safe operation of conventional and

semi-automated vehicles.

• Failure of the new driver assistance

technologies will be found responsible, at least

in part, for some future collisions.

• The design of insurance coverage will need to

evolve.

This presentation has been prepared for the 2016 General Insurance Seminar.The Institute Council wishes it to be understood that opinions put forward herein are not necessarily

those of the Institute and the Council is not responsible for those opinions.

How will this all fit into the big picture including public

policy, sharing and transit?

• Government policies and funding on transportation systems (urbanisation, public transport, road infrastructure for

self-driving vehicles)

• Sharing economy will most likely result in reduction in car ownership. The investment bank Barclays projects that the number of owned vehicles will decline by 50% over the next 25 years due to increased sharing of self-driving vehicles.

This presentation has been prepared for the 2016 General Insurance Seminar.The Institute Council wishes it to be understood that opinions put forward herein are not necessarily

those of the Institute and the Council is not responsible for those opinions.

Warren Buffett, CEO of Berkshire Hathaway

“If you could come up with anything

involved with driving that would cut

accidents by 30%, 40% or 50%, that

would be wonderful. But we would not be holding a party at our insurance

company.”