Embed Size (px)

Citation preview

This presentation remains the property of The Pensions Regulator and should not be reproduced without express permission

Pension scheme fundingin the current environment

ACA Sessional Meeting

Tim Keogh FIA/Chinu Patel FIA13th June 2012

This presentation remains the property of The Pensions Regulator and should not be reproduced without express permission

Objectives

• Provide more insight into our thinking behind the Annual Funding statement

• Explain how the statement should help trustee and employers facing the challenge of current difficult conditions

• Clarify our expectations from trustees

• Clarify what trustees can expect from us

• Q & A

This presentation remains the property of The Pensions Regulator and should not be reproduced without express permission

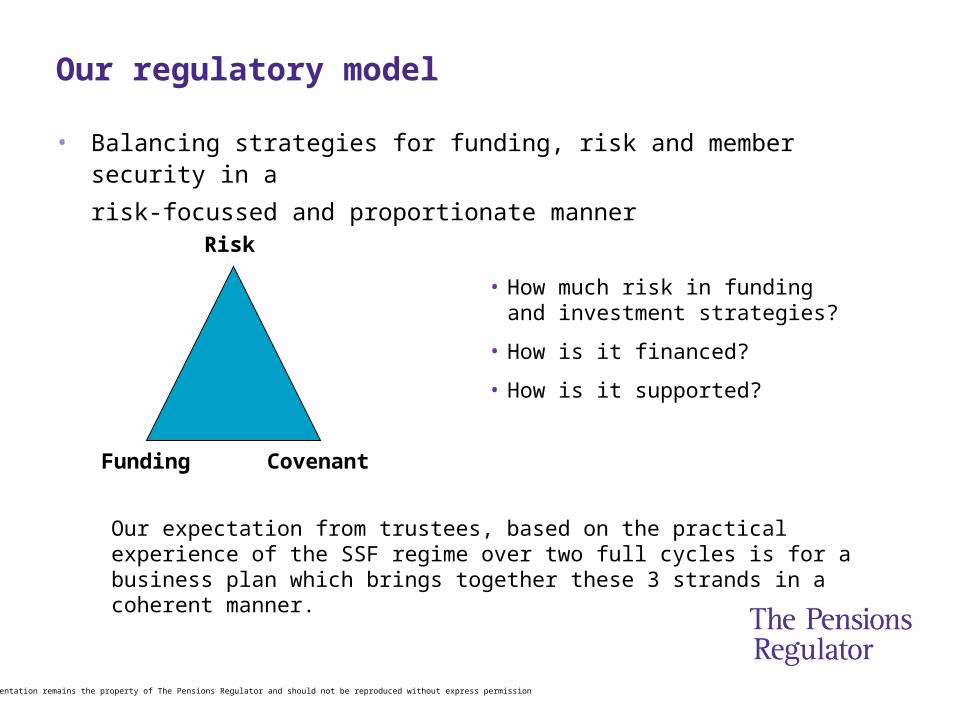

Our regulatory model

• Balancing strategies for funding, risk and member security in a

risk-focussed and proportionate manner

Risk

Funding Covenant

• How much risk in funding and investment strategies?

• How is it financed?

• How is it supported?

Our expectation from trustees, based on the practical experience of the SSF regime over two full cycles is for a business plan which brings together these 3 strands in a coherent manner.

This presentation remains the property of The Pensions Regulator and should not be reproduced without express permission

A re-statement of our earlier guidance

• Technical provisions– Primary measure of liability– Not to be compromised to make recovery plan affordable– Embedded risk should depend on available sponsor support

• Recovery plans– Determined by reasonable affordability to sponsor– Flexible in design and (within reason) length, to deal with individual circumstances.– Can be supported by non-cash elements

• Investment risk when used as a financing tool– Must take account of available sponsor support (which may be volatile over time)– Trustees should have realistic plans of how the sponsor will provide additional support if

expected returns are not realised whilst there is still time.

• Sponsor support– Numerous forms, some more accessible than others– Can be volatile and may erode quickly– Needs regular monitoring and clarity about actions that would be taken and in what

circumstances

This presentation remains the property of The Pensions Regulator and should not be reproduced without express permission

"UK plc" funding development 2008 - date

-300

-250

-200

-150

-100

-50

0

50

100

Mar

-08

Jun

-08

Sep

-08

Dec

-08

Mar

-09

Jun

-09

Sep

-09

Dec

-09

Mar

-10

Jun

-10

Sep

-10

Dec

-10

Mar

-11

Jun

-11

Sep

-11

Dec

-11

Mar

-12

Month end

Su

rplu

s/(d

efic

it)

GB

Pb

n

T3 T4 T5 CPI T6 T7

PPF basis changes

Current context: difficult financial conditions

• Aggregate position of all schemes covered by April statement estimated to be as follows (blue) and compared with PPF7800 index for same schemes (green).

TPs (in blue line) defined as gilts plus same outperformance as at previous valuation

Limitations to our data makes this suitable for big picture analyses only.

• Expect most deficits to be worse than 3 years ago

• Volatile markets = Volatile deficits

• Scheme specific variations -depending on many individual factors

This presentation remains the property of The Pensions Regulator and should not be reproduced without express permission

Sources of deficit

31.3.12 update

• Some respite from CPI saving

• Contributions, despite being at record levels, neutralised by net investment and other misc losses

• But significant loss from having to mark to current market

• March 2012 deficits smaller than Dec 2011(and attribution to individual factors may be different)

Warning: This is aggregate analyses based on highly summarised data and may not be representative of individual schemes whose results will depend on many scheme specific factors.

-300 -200 -100 0 100 200 300

Initial deficit Mar10

CPI saving

3 years' DRCs

Equities underperform

Yields fall

Misc

Deficit Dec11

This presentation remains the property of The Pensions Regulator and should not be reproduced without express permission

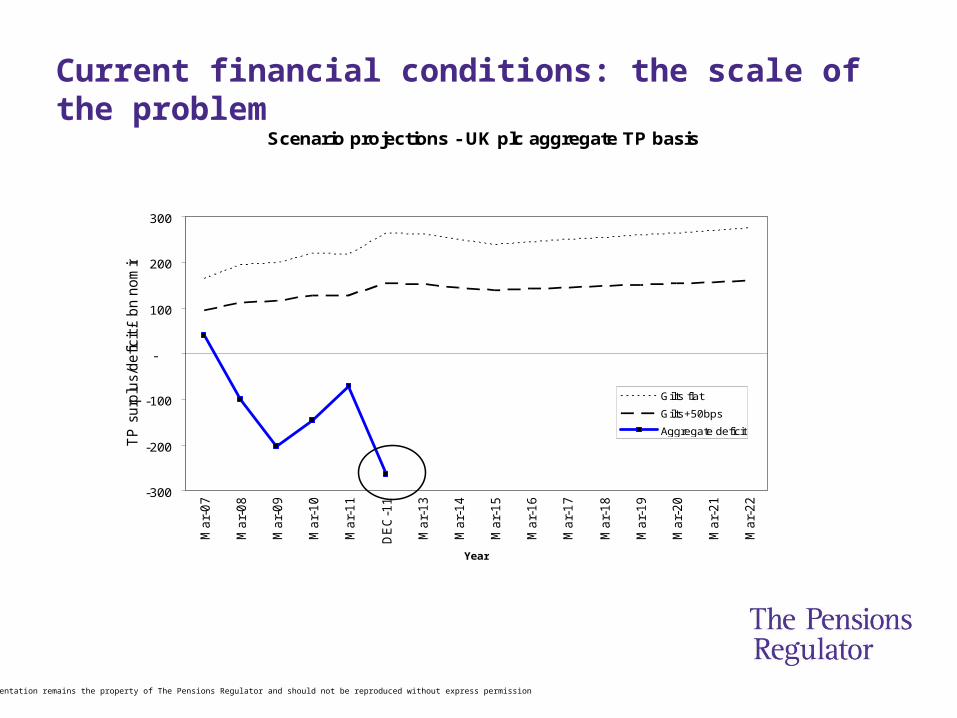

Current financial conditions: the scale of the problem

Scenario projections - UK plc aggregate TP basis

-300

-200

-100

-

100

200

300M

ar-

07

Ma

r-0

8

Ma

r-0

9

Ma

r-1

0

Ma

r-1

1

DE

C-1

1

Ma

r-1

3

Ma

r-1

4

Ma

r-1

5

Ma

r-1

6

Ma

r-1

7

Ma

r-1

8

Ma

r-1

9

Ma

r-2

0

Ma

r-2

1

Ma

r-2

2

Year

TP

su

rplu

s/d

efic

it £

bn

no

min

al

Gilts flat

Gilts+50bps

Aggregate deficit

This presentation remains the property of The Pensions Regulator and should not be reproduced without express permission

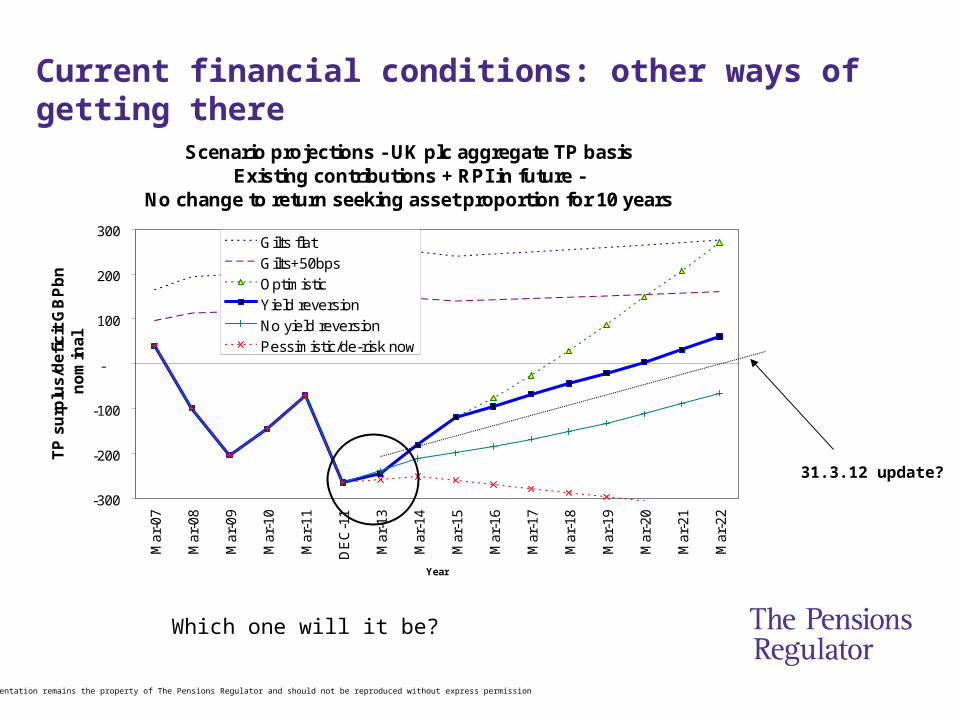

Current financial conditions: a new norm or a temporary aberration?

Scenario projections - UK plc aggregate TP basisExisting contributions + RPI in future -

No change to return seeking asset proportion for 10 years

-300

-200

-100

-

100

200

300

Ma

r-0

7

Ma

r-0

8

Ma

r-0

9

Ma

r-1

0

Ma

r-1

1

DE

C-1

1

Ma

r-1

3

Ma

r-1

4

Ma

r-1

5

Ma

r-1

6

Ma

r-1

7

Ma

r-1

8

Ma

r-1

9

Ma

r-2

0

Ma

r-2

1

Ma

r-2

2

Year

TP

su

rplu

s/de

ficit

£ b

n n

om

ina

l

Gilts flat

Gilts+50bps

Yield reversion

No yield reversion

This presentation remains the property of The Pensions Regulator and should not be reproduced without express permission

Scenario projections - UK plc aggregate TP basisExisting contributions + RPI in future -

No change to return seeking asset proportion for 10 years

-300

-200

-100

-

100

200

300

Mar

-07

Mar

-08

Mar

-09

Mar

-10

Mar

-11

DE

C-1

1

Mar

-13

Mar

-14

Mar

-15

Mar

-16

Mar

-17

Mar

-18

Mar

-19

Mar

-20

Mar

-21

Mar

-22

Year

TP

su

rplu

s/d

efi

cit

GB

Pb

n

no

min

al

Gilts flat

Gilts+50bps

Optimistic

Yield reversion

No yield reversion

Pessimistic/de-risk now

Current financial conditions: other ways of getting there

31.3.12 update?

Which one will it be?

This presentation remains the property of The Pensions Regulator and should not be reproduced without express permission

Coping with current conditions: TPs

• A reminder that legislation requires trustees to take a prudent approach towards setting TPs, regardless of market conditions

• We therefore expect trustees to hold the strength of their TPs

• Smoothing TPs not consistent with asset valuations; volatility needs to be managed not hidden

• There is flexibility to cope with volatility and other aspects of the current financial landscape in the design of recovery plans

• If trustees have a strong view about what may be ‘normal’, and they want to factor it explicitly in their funding plan, then our preference is for this to be done in the recovery plan assumptions, together with a documented contingency plan

This presentation remains the property of The Pensions Regulator and should not be reproduced without express permission

-300 -200 -100 0 100 200 300

Initial deficit Mar12

Discount rate unwind

Contributions current + RPI

Short term yield reversion

10 years' prudence unwound

TP Surplus Mar22

The power of recovery plans

31.3.12 update?

• Ultimately DRCs are the most important

• Views about future economic scenarios may or may not be realised, and could hamper return to solvency unless underpinned by suitable contingency plans

• That is why we are encouraging trustees to focus on the flexibility of recovery plans to cope with current conditions

This presentation remains the property of The Pensions Regulator and should not be reproduced without express permission

Future recovery plans: our expectations

• Guiding principle: reasonable affordability without compromising sponsor’s viability

• In general we expect contributions to be maintained in real terms or increased in line with business performance

• Higher increases if previous level of contributions was low relative to what the sponsor could have afforded

• Servicing debt and capex are essential elements of strong businesses – should be seen to be improving sponsor covenant

• When cash leaves the company the pension creditor should receive an equitable share

• Reassess dividend payments where there is a substantial risk of pension obligations not being met

• If affordability is reduced longer recovery plans may be acceptable but justification needed for material extension

• Trustees should document the justification for any reductions – good governance

This presentation remains the property of The Pensions Regulator and should not be reproduced without express permission

Impact vs affordability

Scenario 2

Scenario 1

Scenario 3

Worsened little change Improved

Impact on scheme(=need for contribution change or equivalent)

High

Covenant/Affordability

Low

Nil Polestar Uniq

This presentation remains the property of The Pensions Regulator and should not be reproduced without express permission

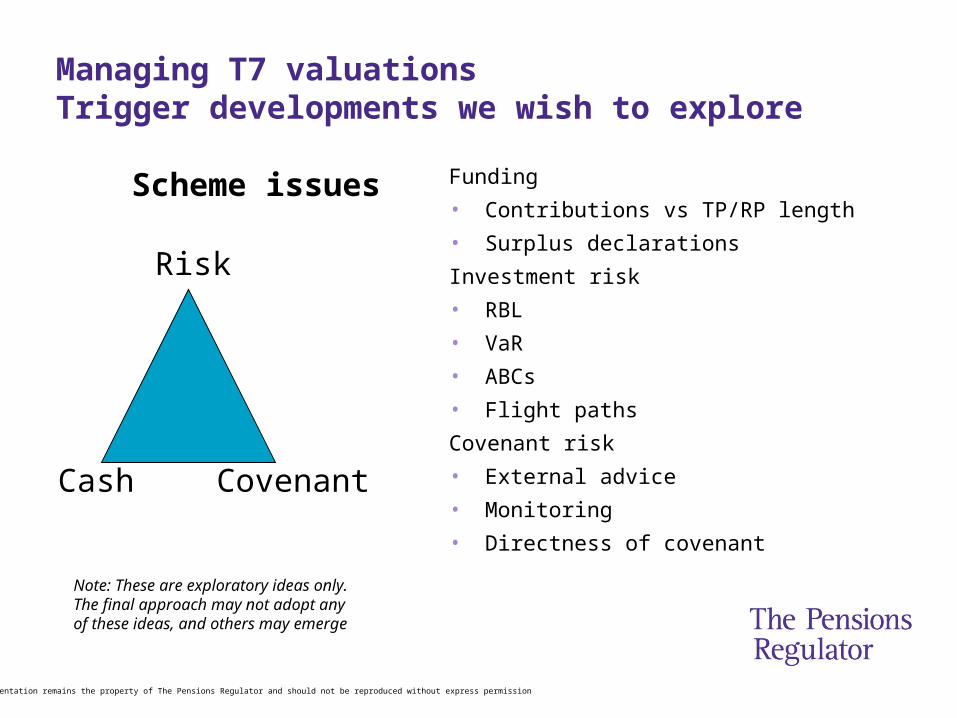

Managing T7 valuations

Scheme issues TPR process issues

Pro-active

Targeted Segmented

Risk

Cash Covenant

This presentation remains the property of The Pensions Regulator and should not be reproduced without express permission

The Pensions Regulator: process

• Pro-active

– More interested in early engagement

• Targeted on key risks

– These are

• Covenant

• Investment

• Inadequacy of contributions

– TP/RP length is means to an end only

• Evolve triggers to better address key risks

• Segmented

– Increasingly discriminate between different situations in terms of our approach

Pro-active

Targeted Segmented

This presentation remains the property of The Pensions Regulator and should not be reproduced without express permission

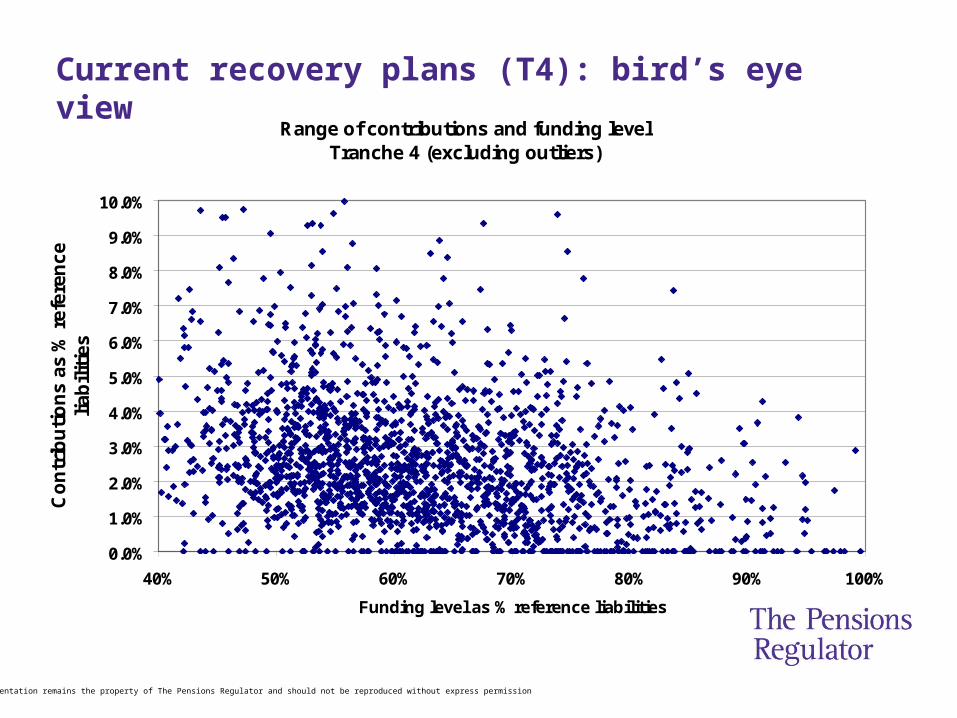

Current recovery plans (T4): bird’s eye view

Range of contributions and funding levelTranche 4 (excluding outliers)

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

40% 50% 60% 70% 80% 90% 100%

Funding level as % reference liabilities

Co

ntr

ibu

tio

ns

as %

ref

eren

ce

liab

iliti

es

This presentation remains the property of The Pensions Regulator and should not be reproduced without express permission

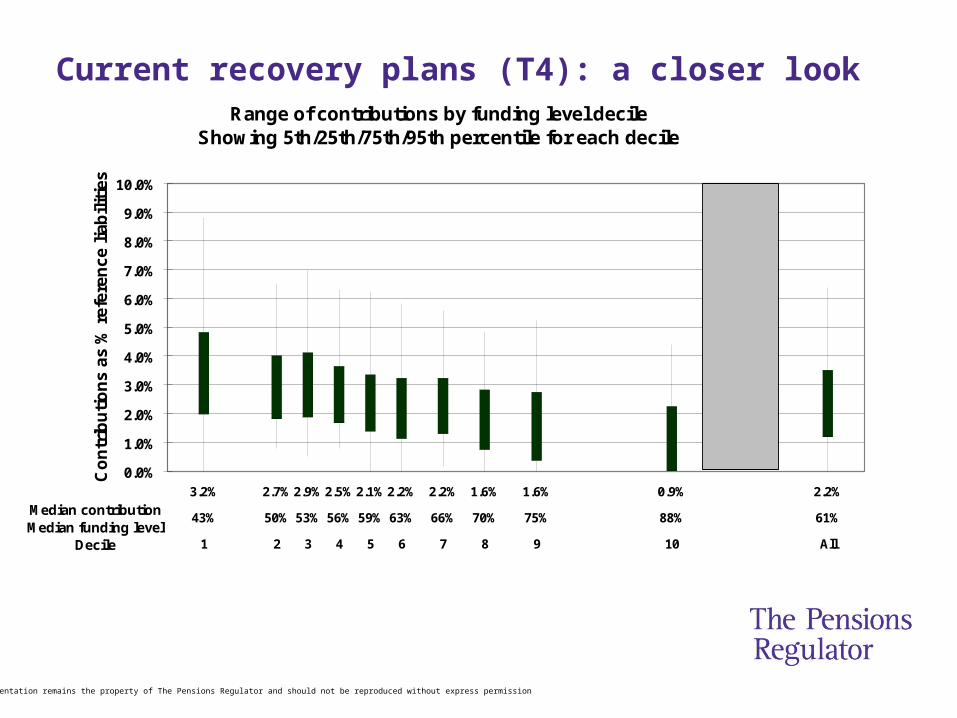

Current recovery plans (T4): a closer lookRange of contributions by funding level decile

Showing 5th/25th/75th/95th percentile for each decile

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

3.2% 2.7%2.9%2.5% 2.1%2.2% 2.2% 1.6% 1.6% 0.9% 2.2%

43% 50% 53% 56% 59% 63% 66% 70% 75% 88% 61%

1 2 3 4 5 6 7 8 9 10 All

Median contribution Median funding level

Decile

Co

ntr

ibu

tio

ns

as

% r

efer

en

ce l

iab

ilit

ies

This presentation remains the property of The Pensions Regulator and should not be reproduced without express permission

Managing T7 valuationsTrigger developments we wish to explore

Scheme issues

Risk

Cash Covenant

Note: These are exploratory ideas only. The final approach may not adopt any of these ideas, and others may emerge

Funding

• Contributions vs TP/RP length

• Surplus declarations

Investment risk

• RBL

• VaR

• ABCs

• Flight paths

Covenant risk

• External advice

• Monitoring

• Directness of covenant

This presentation remains the property of The Pensions Regulator and should not be reproduced without express permission

Next Steps• Review of information submitted to us (work in progress). We may seek more

information on

– Contributions

– Levels of risk

– Investment risk mitigation (through swaps etc)

– Covenant

• A proactive engagement from us in some cases whilst valuations are in progress

– Where we have previously indicated substantial concerns

– In cases that we have not closed because of ongoing concerns

– Less than 100 schemes and all in excess of £500m.

• Updates to our triggers to reflect new priorities

• A much more focused review process

– We will still look at all schemes post-submission

– But expect a smaller number of more assertive interventions

This presentation remains the property of The Pensions Regulator and should not be reproduced without express permission

Sum up – our overall expectation

• Increasingly joined up funding/investment/covenant

• Business plan, including clarity about strength of sponsor support, where it resides and how accessible it will be if and when needed.

• Parental support / wider group support increasingly formalised

• Monitoring covenant and suitable actions that may be taken and in what circumstances

• Trustees to be flexible where covenant is weaker and tolerance needed, but with corresponding shareholder restraint

• There are many well managed schemes doing the right things. We are happy to work with them to identify models of best practice.

• We want to get ahead of issues for schemes where this is not the case, in part by pro-active engagement

This presentation remains the property of The Pensions Regulator and should not be reproduced without express permission

Questions?