Embed Size (px)

Citation preview

“…to raise new ideas and improve policy debates through quality information and analysis on issues shaping New Hampshire’s future.”

Kicking Into a Higher Gear

Exeter Area Chamber of Commerce

Wednesday, January 28, 2015

Board of DirectorsJames Putnam, Chair

David Alukonis

Eric Herr

Dianne Mercier

Catherine A. Provencher

Todd I. Selig

Michael Whitney

Daniel Wolf

Martin L. Gross, Chair Emeritus

Directors Emeritus William H. Dunlap

Sheila T. Francoeur

Stuart V. Smith, Jr.

Donna Sytek

Brian F. Walsh

Anecdotal evidence from Fed Bank of Boston,

January 14, 2015• Sales or revenues are ahead of year-earlier levels according to

most New England business contacts in the manufacturing, retail, and advertising and consulting sectors.

• Commercial real estate markets are steady to improving and most residential real estate markets in the region continue to see price increases and sales declines.

• With a few exceptions, manufacturers and retailers are not increasing employment, while advertising and consulting firms continue to add modestly to headcounts.

• Cost pressures vary, with selective price increases planned by several respondents.

• The 2015 outlook is positive for almost all responding firms.

NH – Less of a decline, but a slower recovery

92.0

93.0

94.0

95.0

96.0

97.0

98.0

99.0

100.0

101.0

102.0

Dec

200

7 =

100

Index of Total NonFarm Employment (Seasonally Adjusted)

US NE NH

New England

United States

New Hampshire

Manufacturing, construction and financial activities have not

recovered, government shrinks

Source: NH Economic and Labor Market Information Bureau

-8,700

-3,500

-5,100

-3,600

1,100

4,700

100

-4,500

-400 -100

5,200

1,200

4,100 4,1004,900

-2,700

-10,000

-8,000

-6,000

-4,000

-2,000

0

2,000

4,000

6,000

Change in New Hampshire Jobs

Oct 08 to Oct 11

Oct 11 to Oct 14

2011-2013 job growth still leans toward below average wage jobs

Source: NH Economic and Labor Market Information Bureau

5,803

7,089

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Above Average Wage Below Average Wage

Change in NH Jobs from 2011 to 2013 by Average Wage Paid

Portsmouth Area growth in Finance and Health Care

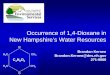

Rockingham County unemployment declines as employment increases

New Hampshire Job Creation – Region and US

Percent Change in Payroll Employment Over Previous Ten Years

-10%

0%

10%

20%

30%

40%

50%

60%

70%

1/1/

1979

1/1/

1981

1/1/

1983

1/1/

1985

1/1/

1987

1/1/

1989

1/1/

1991

1/1/

1993

1/1/

1995

1/1/

1997

1/1/

1999

1/1/

2001

1/1/

2003

1/1/

2005

1/1/

2007

1/1/

2009

1/1/

2011

1/1/

2013

US NE NH

New Hampshire

New England

United States

The Great Convergence

Migration slowed in last decade

-20,000

-15,000

-10,000

-5,000

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Net Migration Into and Out of New Hampshire

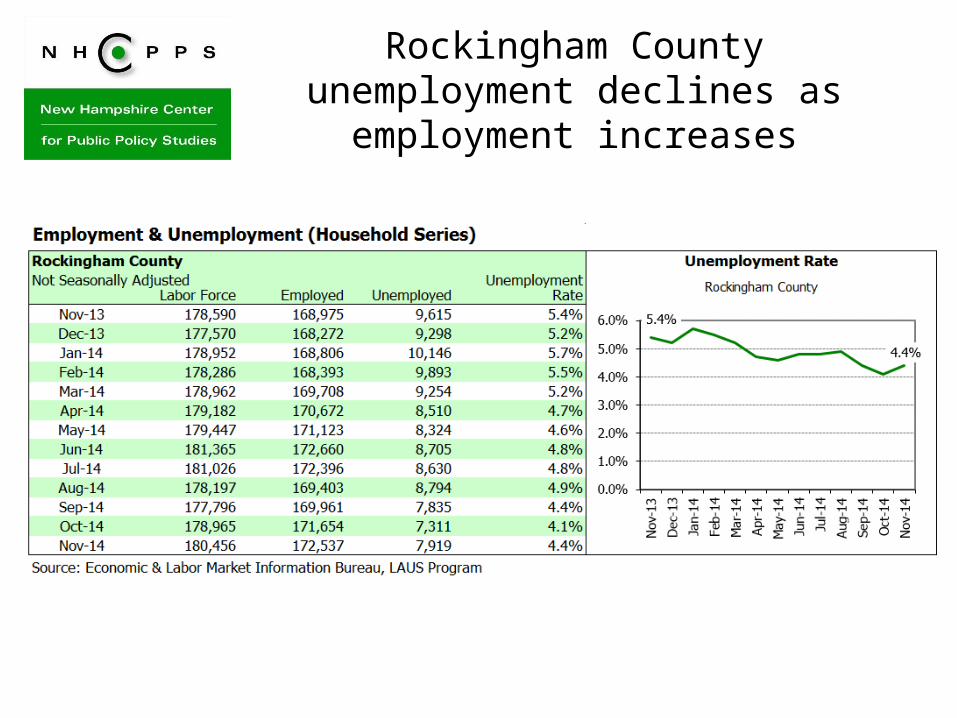

NH Residential Real Estate Sales and Prices

10

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

0

5,000

10,000

15,000

20,000

25,000

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

NH Single-Family Residential Home Sales and Price (MLS)Source: NH Association of REALTORS

Units sold Median Price

Median Home Price

Number of Units Sold

Decline from the Peak:Sales -40% from 2004Price -25% from 2005

2014 YTD thru Nov.

Similar trends in Rockingham County

11

Rockingham County

0

1,000

2,000

3,000

4,000

5,000

6,000

$150,000

$170,000

$190,000

$210,000

$230,000

$250,000

$270,000

$290,000

$310,000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Nu

mb

er S

old

Med

ian

So

ld P

rice

MLS Residential Property Sales By Year

Median Price Number Sold

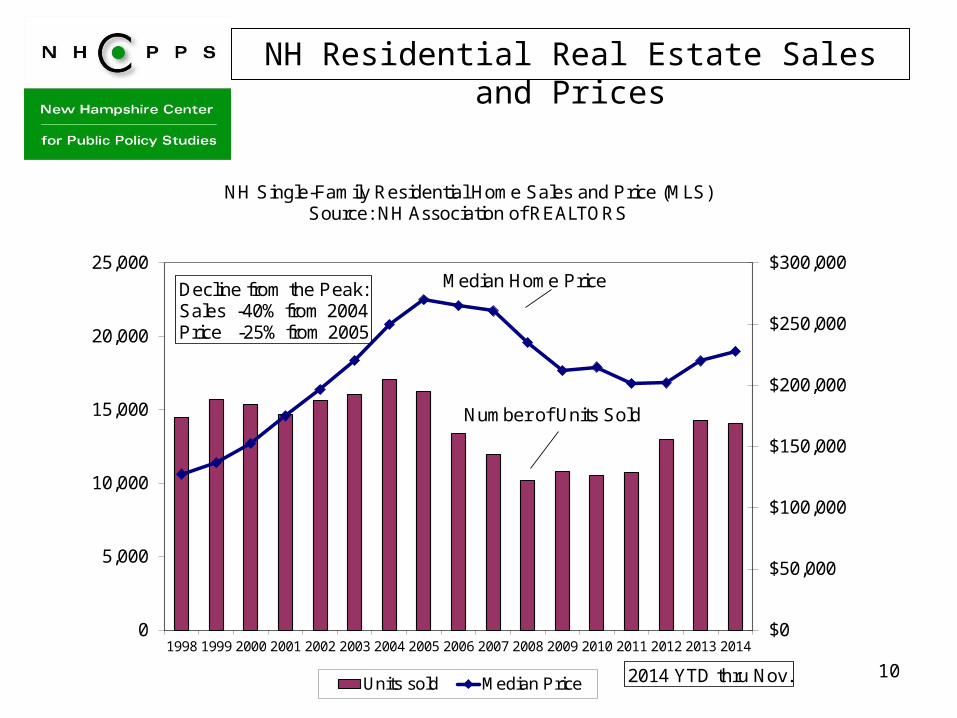

Home Prices Return to the Long Term Trend:

$134,749

$141,372

$152,500

$170,158

$188,089

$206,266

$227,807

$237,976

$226,354

$216,598

$187,954

$170,164

$169,787

$154,410

$151,504

$162,622

$165,787

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

NH Single-Family Residential Home Price (MLS)Source: NH Association of REALTORS

Median Price 2000 Inflation Adjusted

Median Home Price

Inflation Adjusted Price

1313

But Rental Prices Have Continued to Rise

New Hampshire Rents – NHHFA SurveysState of New Hampshire

$400

$500

$600

$700

$800

$900

$1,000

$1,100

$1,200

Ren

t

Median Gross Rental Cost

All Units 2-Bedroom Units

1414

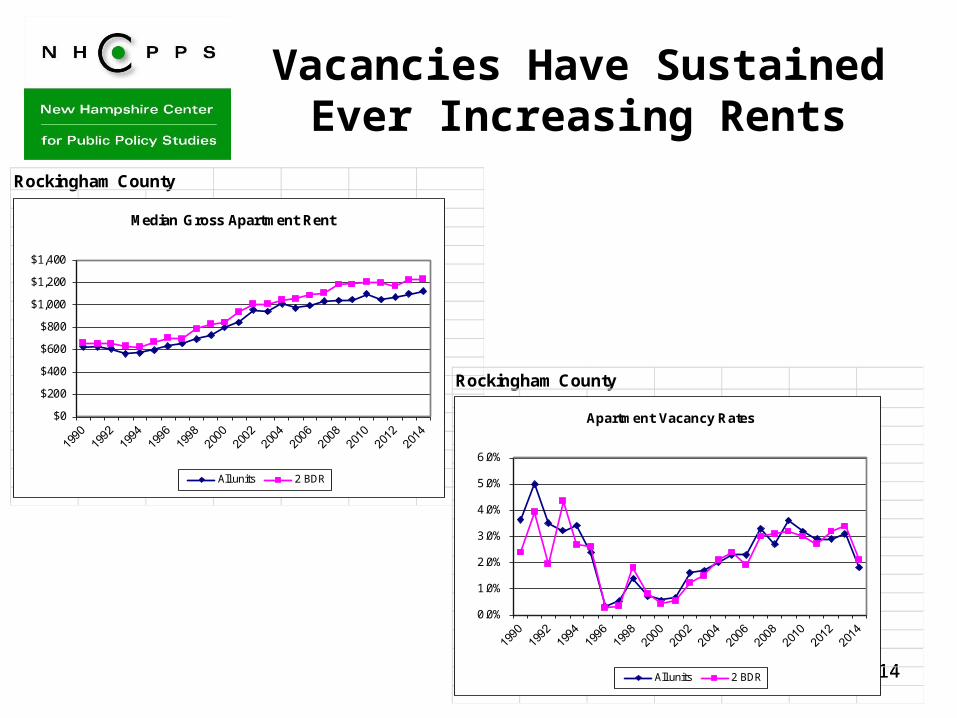

Vacancies Have Sustained Ever Increasing Rents

Rockingham County

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

Median Gross Apartment Rent

All units 2 BDR

Rockingham County

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

Apartment Vacancy Rates

All units 2 BDR

1515

Another Sign of a “Normal” Housing Market

1.00

1.20

1.40

1.60

1.80

2.00

2.20

2.40

Ratio of Existing Home Price to Median 2BDRrent

Rockingham CountyNew Hampshire

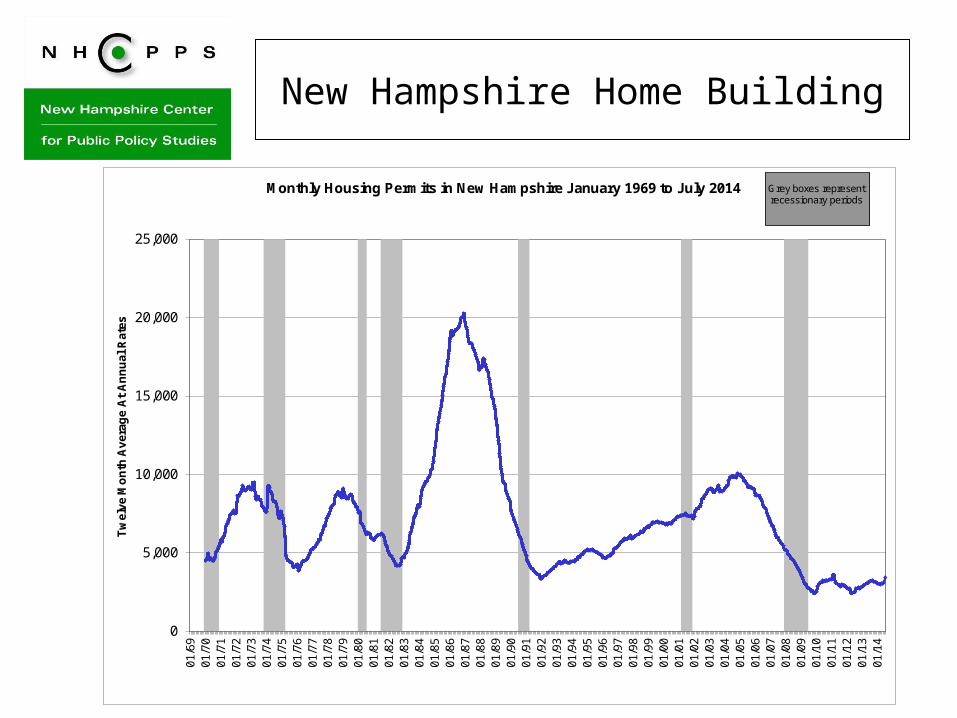

New Hampshire Home Building

0

5,000

10,000

15,000

20,000

25,000

01/6

901

/70

01/7

101

/72

01/7

301

/74

01/7

501

/76

01/7

701

/78

01/7

901

/80

01/8

101

/82

01/8

301

/84

01/8

501

/86

01/8

701

/88

01/8

901

/90

01/9

101

/92

01/9

301

/94

01/9

501

/96

01/9

701

/98

01/9

901

/00

01/0

101

/02

01/0

301

/04

01/0

501

/06

01/0

701

/08

01/0

901

/10

01/1

101

/12

01/1

301

/14

Tw

elv

e M

on

th A

ver

age

At

An

nu

al R

ates

Monthly Housing Permits in New Hampshire January 1969 to July 2014 Grey boxes represent recessionary periods

NH Foreclosures – Worst is Over

0

100

200

300

400

500

600

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

Jan-

12

Jul-1

2

Jan-

13

Jul-1

3

Jan-

14

Jul-1

4

Source: Real Data Corp. compiled by NH Housing

NH Monthly Foreclosure Deeds

Actual Trend

Real Estate Activity 40% below the Peak

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180Ju

l-99

Jul-0

0

Jul-0

1

Jul-0

2

Jul-0

3

Jul-0

4

Jul-0

5

Jul-0

6

Jul-0

7

Jul-0

8

Jul-0

9

Jul-1

0

Jul-1

1

Jul-1

2

Jul-1

3

Jul-1

4

Jul-1

5

Mill

ion

s

12 Month Running

Real Estate Transfer

New Hampshire State Revenue

Source: Monthly Revenue Focus, NH Dept. of Admin Services

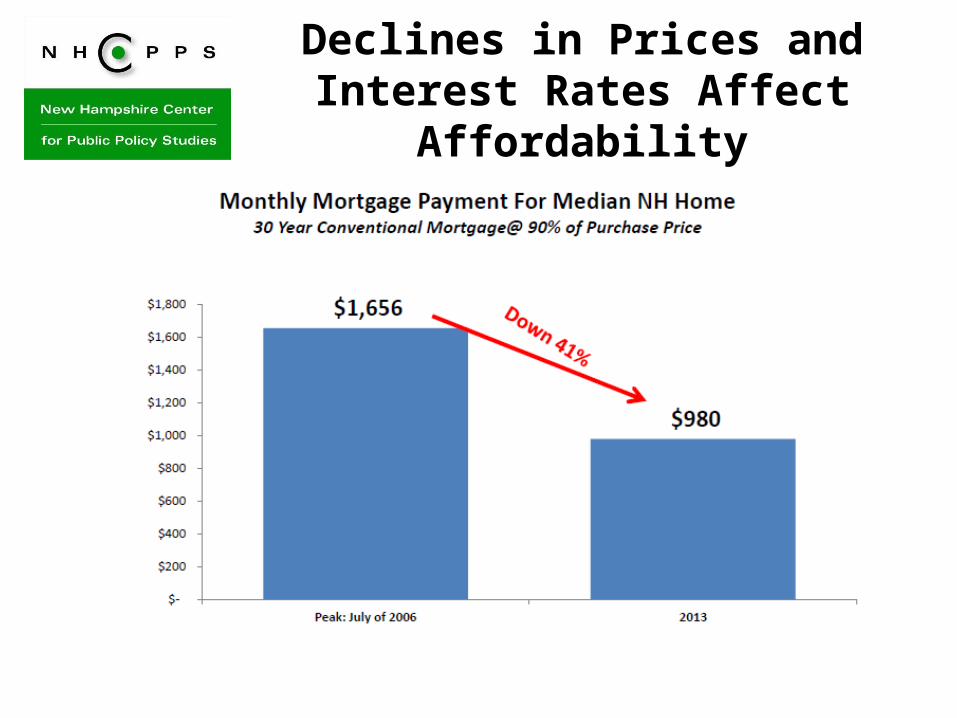

Declines in Prices and Interest Rates Affect Affordability

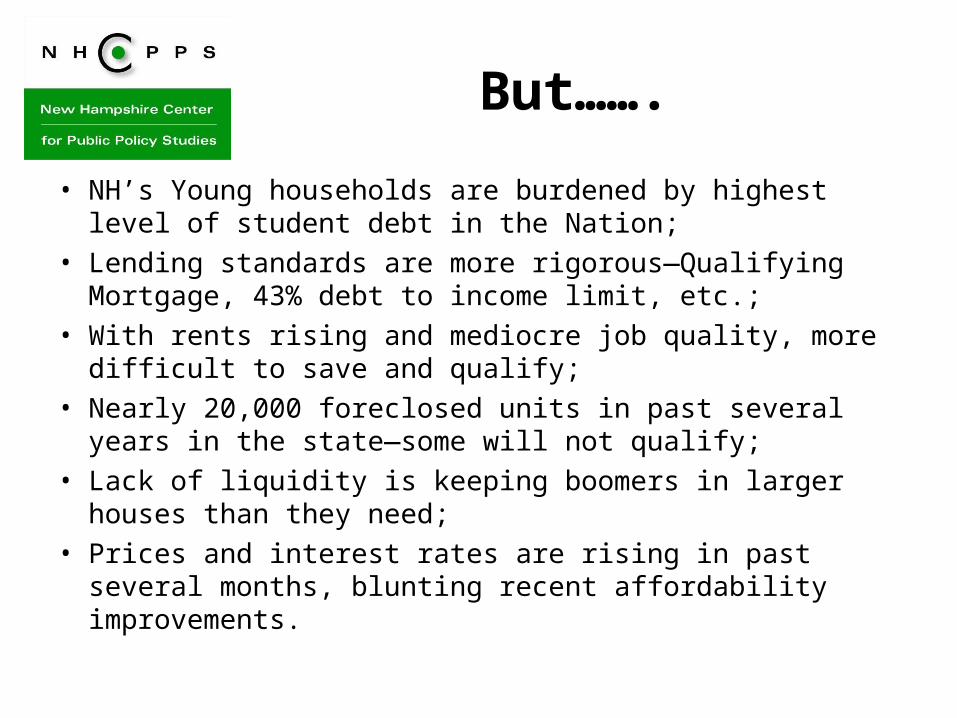

But…….

• NH’s Young households are burdened by highest level of student debt in the Nation;

• Lending standards are more rigorous—Qualifying Mortgage, 43% debt to income limit, etc.;

• With rents rising and mediocre job quality, more difficult to save and qualify;

• Nearly 20,000 foreclosed units in past several years in the state—some will not qualify;

• Lack of liquidity is keeping boomers in larger houses than they need;

• Prices and interest rates are rising in past several months, blunting recent affordability improvements.

2121

NH’s Changing Housing Environment Has Consequences

• New Hampshire’s population growth is slowing down

• Job quality is poor• Elders will be increasingly

larger share of owners and renters

• Young home buyers are challenged

• Recent trend away from ownership and towards rental

• Different problems in different regions

• General public, town officials and business are not aware of issues affecting NH’s housing

• Fewer new households, and fewer families

• Overpayment problems for low income renters

• Elder overpayment, and Elders not aware of options available

• Future home owners not aware of ownership pitfalls and advantages

• Multi-family production shortages

• Geographic diversity more important than urban core.

• Town officials not comfortable changing existing regulations.

Environment Consequences

Full report at: http://www.nhpolicy.org/report/housing-in-nh-pt-1-big-houses-small-households

NEEP Forecast for New Hampshire October 2014

• The Granite State will add only a few hundred manufacturing jobs over the next five years. However, it is expected that Granite State manufacturing output will continue to increase in the forecast period as it has in the past five years.

• In the private services sector employment will increase by about 2.0 percent annually in the forecast period. The fastest rate of growth will occur in Professional and Business Services, followed by Leisure & Hospitality, and Education and Health Services employment.

• The New Hampshire real estate market has finally seen a return to normal (pre housing bubble) price appreciation and sales growth, according to state realtors. Foreclosure recordings declined steadily over the past year. The state rental market remains strong with rental costs leveling and vacancies remaining below 5 percent in most areas.

Look to an Improving National Economy, Pushed by Housing

and Low Energy Prices

Labor Market Improves

Businesses Have Never Been as Profitable…

Sources: BEA, Moody’s Analytics

After-tax corporate profit margin, %

26

…And Have a Significant Energy Advantage

Sources: Country sources, Moody’s Analytics

Natural gas price, $ mmbtu

Industrial electricity prices, $ Mwh

U.S.

China

Italy

Korea

Japan

India

Germany

U.K.

France

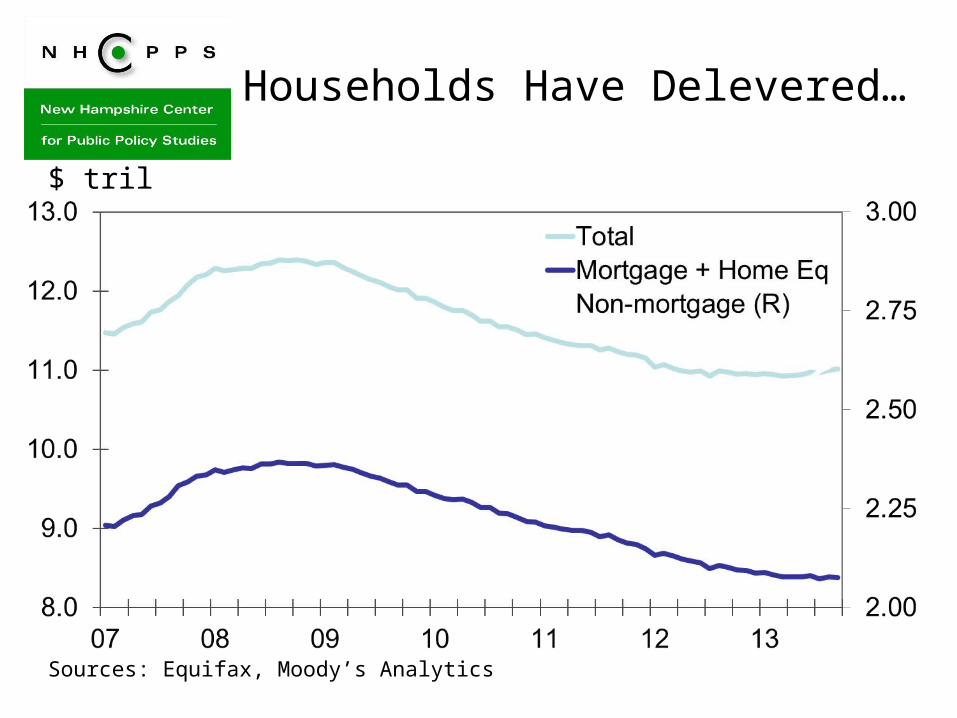

Households Have Delevered…

Sources: Equifax, Moody’s Analytics

$ tril

Sources: Census, Moody’s Analytics

Vacant homes for sale, for rent and held off market, ths

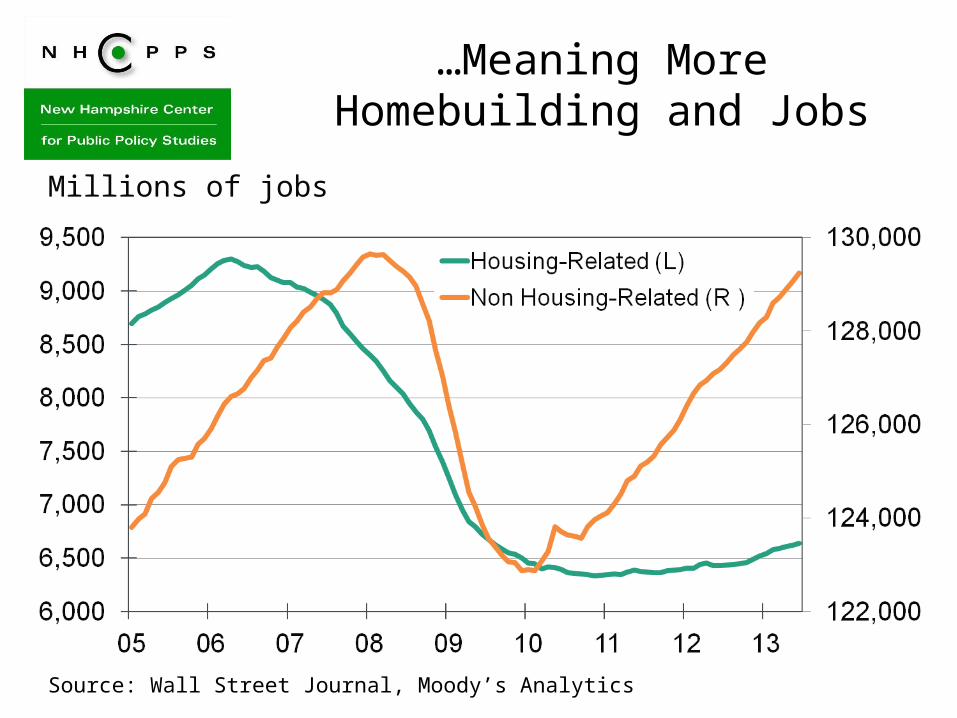

Housing Will Provide the Catalyst…

…Meaning More Homebuilding and Jobs

Source: Wall Street Journal, Moody’s Analytics

Millions of jobs

New Hampshire Center for New Hampshire Center for Public Policy StudiesPublic Policy Studies

Want to learn more?• Online: nhpolicy.org• Facebook: facebook.com/nhpolicy• Twitter: @nhpublicpolicy• Our blog: policyblognh.org• (603) 226-2500

“…to raise new ideas and improve policy debates through quality information and analysis on issues shaping New Hampshire’s future.”

30

Board of DirectorsJames Putnam, Chair

David Alukonis

Eric Herr

Dianne Mercier

Catherine A. Provencher

Todd I. Selig

Michael Whitney

Daniel Wolf

Martin L. Gross, Chair Emeritus

Directors Emeritus William H. Dunlap

Sheila T. Francoeur

Stuart V. Smith, Jr.

Donna Sytek

Brian F. Walsh

NH excels on “current climate” indicators

Area Indicator NH RankWFHousing Homeownership rates 2Regulatory Pollution Abatement / $ Value Added 3EdWorkFrc High School grad rate 4Cultural Voter turnout rate 4EdWorkFrc Pct of pop in Science & Engineering workforce 5EdWorkFrc Pct w/Associates+ 6EdWorkFrc Percent of children aged 3-4 in preschool 6Fiscal State Business Tax Climate Index 7Fiscal Public health/welfare spending per person in poverty 7GrowthReten Manufacturing Supercluster Concentration (LQ) 7

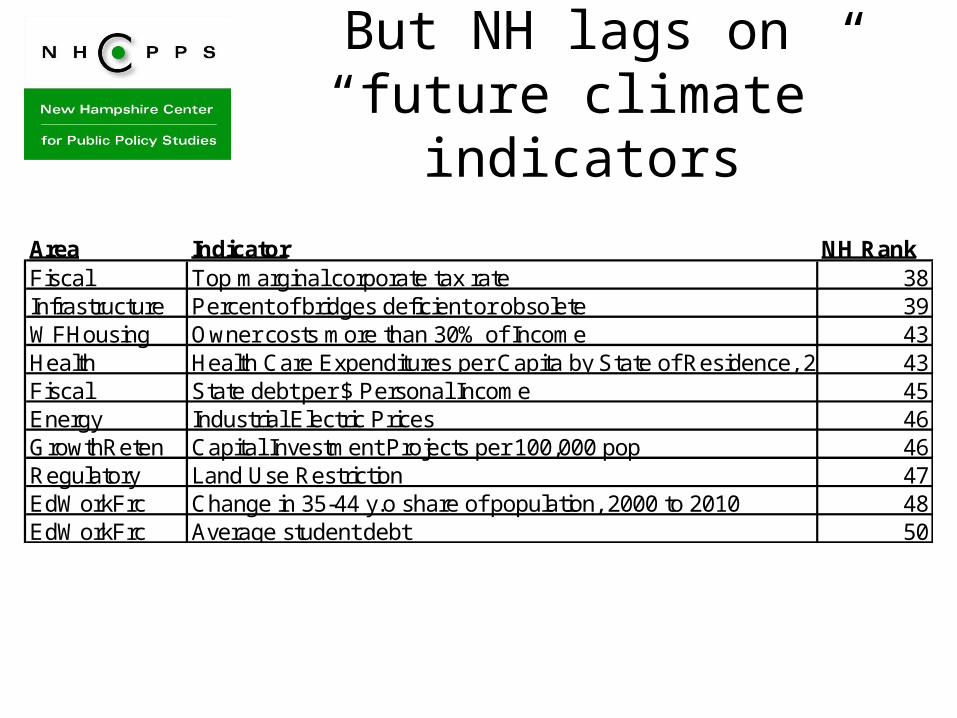

But NH lags on “future climate” indicators

Area Indicator NH RankFiscal Top marginal corporate tax rate 38Infrastructure Percent of bridges deficient or obsolete 39WFHousing Owner costs more than 30% of Income 43Health Health Care Expenditures per Capita by State of Residence, 2009 43Fiscal State debt per $ Personal Income 45Energy Industrial Electric Prices 46GrowthReten Capital Investment Projects per 100,000 pop 46Regulatory Land Use Restriction 47EdWorkFrc Change in 35-44 y.o share of population, 2000 to 2010 48EdWorkFrc Average student debt 50