Embed Size (px)

Citation preview

Zhengfei GuanFeng Wu

Dong Hee Suh

IFAS/GCREC, University of FloridaSept. 7, 2016

Tomato Production, Trade, and the Impact of the Suspension Agreement

• Industry Overviewo US & Florida Production, Price and Valueo Mexican Productiono Trade with Mexico

• Suspension Agreement & Impacto Floor price and binding effecto Impact on Import volume, market price and volatility

o Main data sources: USDA-NASS, Department of Commerce

Outline

Florida largest supplier of fresh tomatoes in the U.S.

Dominates the U.S. winter fresh tomato market

But production has been declining.

Florida Tomato Industry

Production

2639

950

0

500

1000

1500

2000

2500

3000

3500

4000

4500

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Million lbs US and Florida Fresh Tomato Production2005: Total 3.8B lbs, FL 1.6B lbs

US Florida California

Acreage

97500

33000

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

AcreUS and Florida Fresh Tomato Acreage

US Florida California

Production Value

1243

453

0

200

400

600

800

1000

1200

1400

1600

1800

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

million $ U.S. and Florida Fresh Tomato Production Values2005: $1.6B, FL $0.8B (higher than CA)

National Florida California

Yield per Acre

295 (1180 Bx)

0

50

100

150

200

250

300

350

400

450

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

CWT/Acre

Florida California

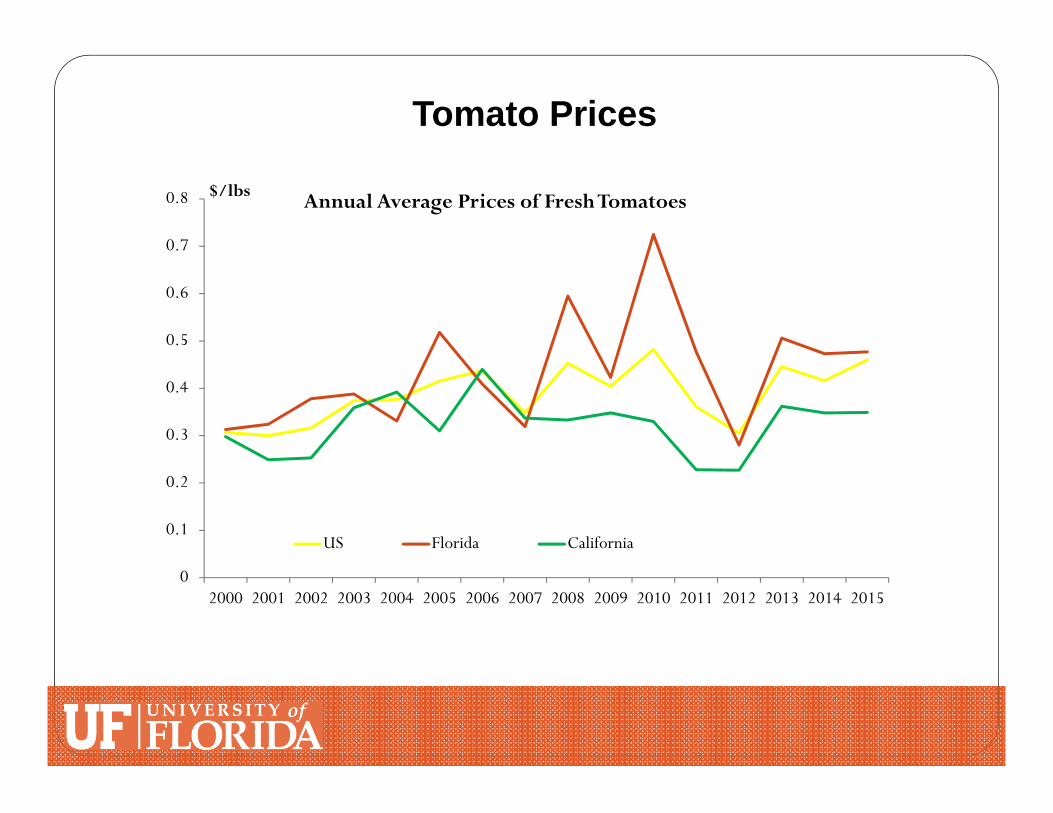

Tomato Prices

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

$/lbs Annual Average Prices of Fresh Tomatoes

US Florida California

Mexican Competition

Florida and Mexico compete for the U.S. fresh tomato market historically.

Total imports ~$3.5B lbs, of which Mexican imports account for about 90%.

• Mexican Production, Trade, & Government Support

Mexican Production

66966173 6392

6945

63335934

6609

5370

75707237

7796

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Million lbs Mexican Fresh Tomao Production Red Total

Imports of Mexico tomatoes have increased sharply in recent years.

Market share was about 20% smaller than Florida’s in 2000, is now more than 3 times higher than Florida’s.

Imports Growth

FL Production and Imports from Mexico

3137

949.9

0

500

1000

1500

2000

2500

3000

3500

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Million lbs Imports from Mexico Florida Production

The Mexican greenhouse horticulture received substantial amount of government support.

In 2009,SAGARPA announced a strategic project to support protected agriculture.

Greenhouses: $1.2 million Peso/ha, up to $3 m peso per project (~ $250k in 2009).

Furthermore, support covers 50% of specialized training and technical assistance (up to $100,000 peso)

The same applies to greenhouse insurance, market studies; certification (GAP&GMP); promotion of protected agriculture product, etc.

Mexican Support of Protected Agriculture

Mexican Protected Production

70% of tomatoes are produced under this technology 15,000 Hectares (37,000 acres) in 2014/15 better quality, better pest control Reduced weather risk exposure, more predictable

supply higher prices Higher yield Year hectares acres

2009/10 4000 9884

2010/11 13000 32124

2011/12 14700 36324

Mexican Tomato Yield

Percentage of Protected Production

Red mainly from protected production (total production 70% from protected, but the % for red tomatoes higher).

50% US imports produced from “greenhouse” (adapted & controlled environment) in 2014/2015.

Suspension of Antidumping Investigation (filed in Apr 1996) Initial agreement (Dec 6, 1996) set reference prices at:

$ 0.2108 per pound (Winter: October 23 - June 30) $ 0.172 per pound (Summer: July 1 - October 22)

Ref. Price Winter (Oct 23‐Jun 30) Summer (Jul 1‐Oct 22)1996 0.2108 0.1722003 0.2169 0.1722013 0.31 0.2458

Suspension Agreement

A new suspension agreement (March 4, 2013); New reference prices 50% higher

Suspension Agreement

Domestic & Import Prices

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

$/lb US and Mexican Tomato Annual Prices at Major Shipping Points (open field, adapted env.)

US MX

Occurrence Binding Floor Prices (1998-2016)Weekly Prices of the U.S. and Mexican Tomatoes, 1998 - 2016

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

2

$/lb Restrained us price MX Price

% of the restrained weeks: Before: 22% After: 30%

Weekly Prices of the U.S. and Mexican Tomatoes, 2010 - 2016

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2.00

1/2/10

3/6/10

5/8/10

7/10

/10

9/11

/10

11/13/10

1/15

/11

3/19

/11

5/21

/11

7/23

/11

12/17/11

2/18

/12

4/21

/12

6/23

/12

8/25

/12

10/27/12

1/5/13

3/9/13

5/11

/13

7/13

/13

9/14

/13

11/23/13

1/25

/14

3/29

/14

5/31

/14

8/2/14

10/4/14

12/6/14

2/7/15

4/11

/15

6/13

/15

8/15

/15

10/17/15

12/19/15

2/20

/16

4/23

/16

6/25

/16

$/lb Restrained us price MX Price

% of the restrained weeks: Before: 19% After: 30%

Occurrence Binding Floor Prices (2010-2016)

U.S. Tomato Prices and Reference Prices

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80 $/lbRF us price

Domestic & Floor Prices

Impact of Agreement (1998-2016)

Before After

Average Import Price 0.45 0.54

Average Domestic Prices 0.42 0.50

Volatility of Import Prices 0.21 0.19

Volatility of Domestic Prices 0.22 0.15

% of the restrained prices 22% 30%

Import and Domestic Prices Before (1998-2013) and After (2013-2016)

Impact of Agreement (2010-2016)

2010-2013 After

Average Import Price 0.47 0.54

Average Domestic Prices 0.50 0.50

Volatility of Import Prices 0.21 0.19

Volatility of Domestic Prices 0.27 0.15

% of the restrained prices 19% 30%

Import and Domestic Prices Before (2010-2013) and After (2013-2016)

Concluding Remarks

US/FL acreage continued to decrease but production and value stable after 2013 Suspension Agreement.

Average weekly import prices increased by 15%. Imports continued to increase after Agreement. The two prices are now more correlated.

More in-depth price analysis showed: Increase in import prices boosted US price after new Agreement.

Agreement helped! But is that enough?