Embed Size (px)

Citation preview

South AustraliaRegional TourismSatellite Accounts2013-14

Tourism Research Australia

August 2015

South Australian Regional Tourism Satellite Accounts 2013-14

iDeloitte Access Economics

ContentsExecutive Summary .................................................................................................................. v

1 Introduction ................................................................................................................... 11.1 Industry context ................................................................................................................ 11.2 Satellite accounting........................................................................................................... 11.3 Accounting concepts ......................................................................................................... 31.4 Regional context ............................................................................................................... 41.5 Report structure ............................................................................................................... 5

2 Summary of Results ........................................................................................................ 62.1 Key tourism aggregates ..................................................................................................... 62.2 Tourism consumption ....................................................................................................... 72.3 Tourism output ................................................................................................................. 92.4 Tourism Gross Value Added ............................................................................................ 112.5 Tourism employment ...................................................................................................... 142.6 Detailed comparison data ............................................................................................... 17

3 Key trends in tourism.................................................................................................... 223.1 Adelaide ......................................................................................................................... 223.2 Regional South Australia ................................................................................................. 233.3 Regional trends ............................................................................................................... 253.4 Relative industry performance ........................................................................................ 26

4 Regional profiles ........................................................................................................... 31

Appendix A : Explanatory notes .............................................................................................. 58

Appendix B : Glossary ............................................................................................................. 59

Appendix C : Indirect trade flows ............................................................................................ 59

References ............................................................................................................................. 59Limitation of our work ............................................................................................................... 60

ChartsChart 2.1 : Tourism contribution to Adelaide and South Australian regional economies, 2013-147

Chart 2.2 : Regional tourism consumption at purchasers prices, 2013-14.................................. 7

Chart 2.3 : Domestic and international contribution to tourism consumption, 2013-14 ............ 8

Chart 2.4 : Regional direct tourism output at basic prices, 2013-14 ........................................... 9

Chart 2.5 : Relative contribution of direct and indirect tourism output, 2013-14 ..................... 11

Chart 2.6 : Regional direct tourism GVA at basic prices, 2013-14 ............................................ 12

Chart 2.7 : Domestic and international contribution to direct tourism GVA, 2013-14 ............. 12

Chart 2.8 : Source market contribution to direct GVA, 2013-14............................................... 13

Chart 2.9 : Contribution of tourism GVA to each regional economy, 2013-14 .......................... 14

South Australian Regional Tourism Satellite Accounts 2013-14

iiDeloitte Access Economics

Chart 2.10 : Regional direct tourism employed persons, 2013-14 ........................................... 15

Chart 2.11 : Status breakdown of persons directly employed in tourism industry, 2013-14 ..... 15

Chart 2.12 : Direct tourism contribution to each regional economy, 2013-14.......................... 18

Chart 2.13 : Indirect tourism contribution to each regional economy, 2013-14 ....................... 18

Chart 2.14 : Total tourism contribution to each regional economy, 2013-14 ........................... 19

Chart 3.1 : Adelaide’s comparative GVA growth, 2006-07 to 2013-14 (Indexed: 2006=100) .... 22

Chart 3.2 : Adelaide’s direct tourism GVA and employment, 2006-07 to 2013-14 ................... 23

Chart 3.3 : Tourism’s share of GRP and Employment, Adelaide, 2006-07 to 2013-14............... 23

Chart 3.4 : Regional SA comparative GVA growth, 2006-07 to 2013-14 (Indexed: 2006=100) .. 24

Chart 3.5 : Regional SA direct tourism GVA and employment, 2006-07 to 2013-14 ................. 24

Chart 3.6 : Tourism’s share of GRP and Employment, regional SA, 2006-07 to 2013-14 ........... 25

Chart 3.8 : Industry growth comparison (Index: 2006=100) ..................................................... 27

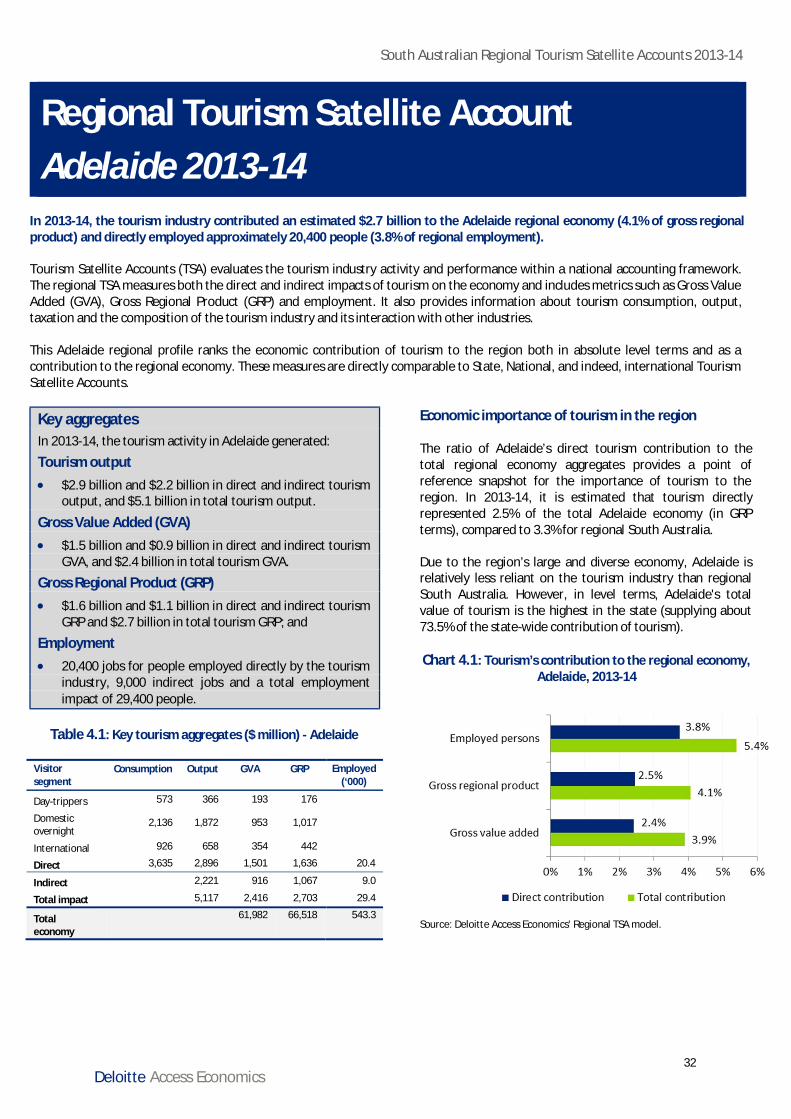

Chart 4.1 : Tourism’s contribution to the regional economy, Adelaide, 2013-14 ..................... 32

Chart 4.2 : Contribution of tourism to employment, Adelaide, 2013-14 .................................. 33

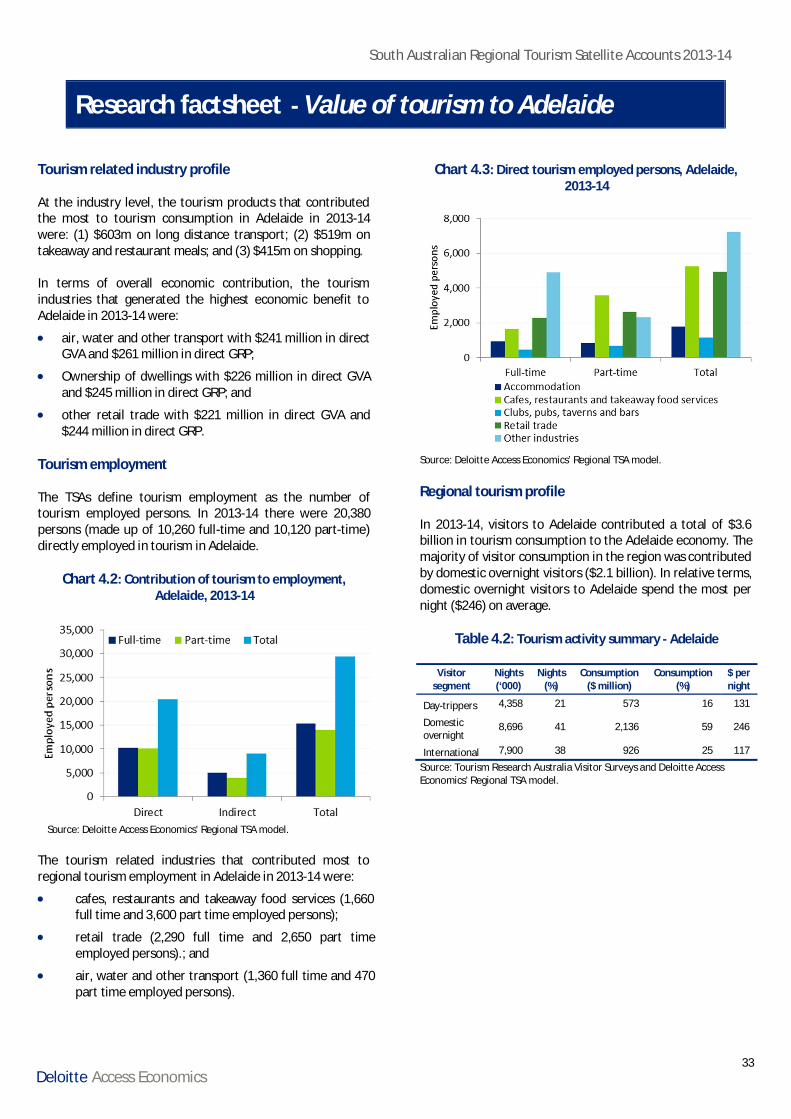

Chart 4.3 : Direct tourism employed persons, Adelaide, 2013-14 ........................................... 33

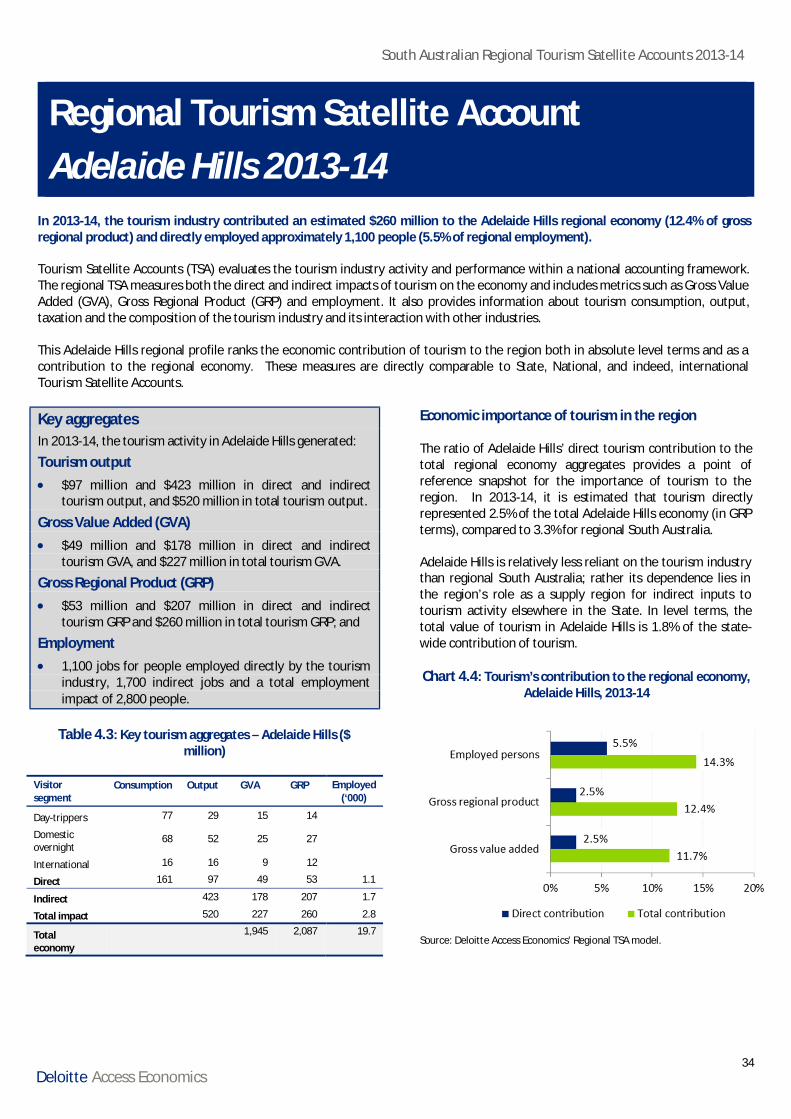

Chart 4.4 : Tourism’s contribution to the regional economy, Adelaide Hills, 2013-14 .............. 34

Chart 4.5 : Contribution of tourism to employment, Adelaide Hills, 2013-14 ........................... 35

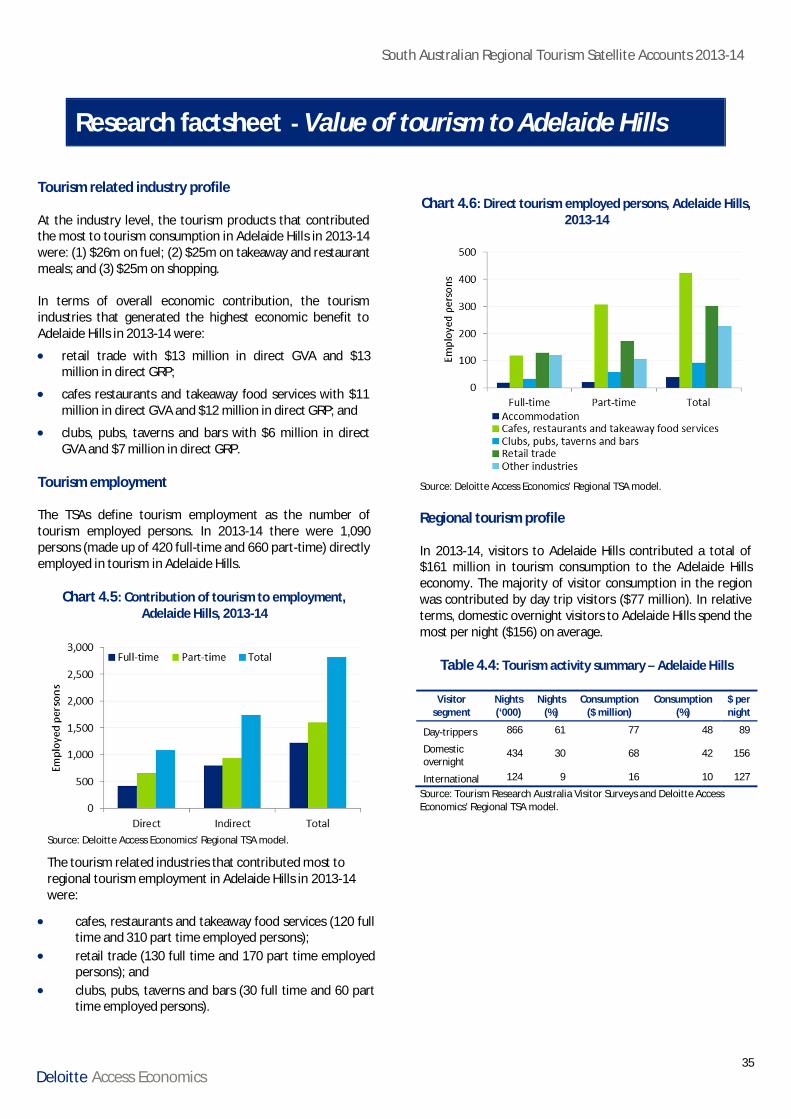

Chart 4.6 : Direct tourism employed persons, Adelaide Hills, 2013-14..................................... 35

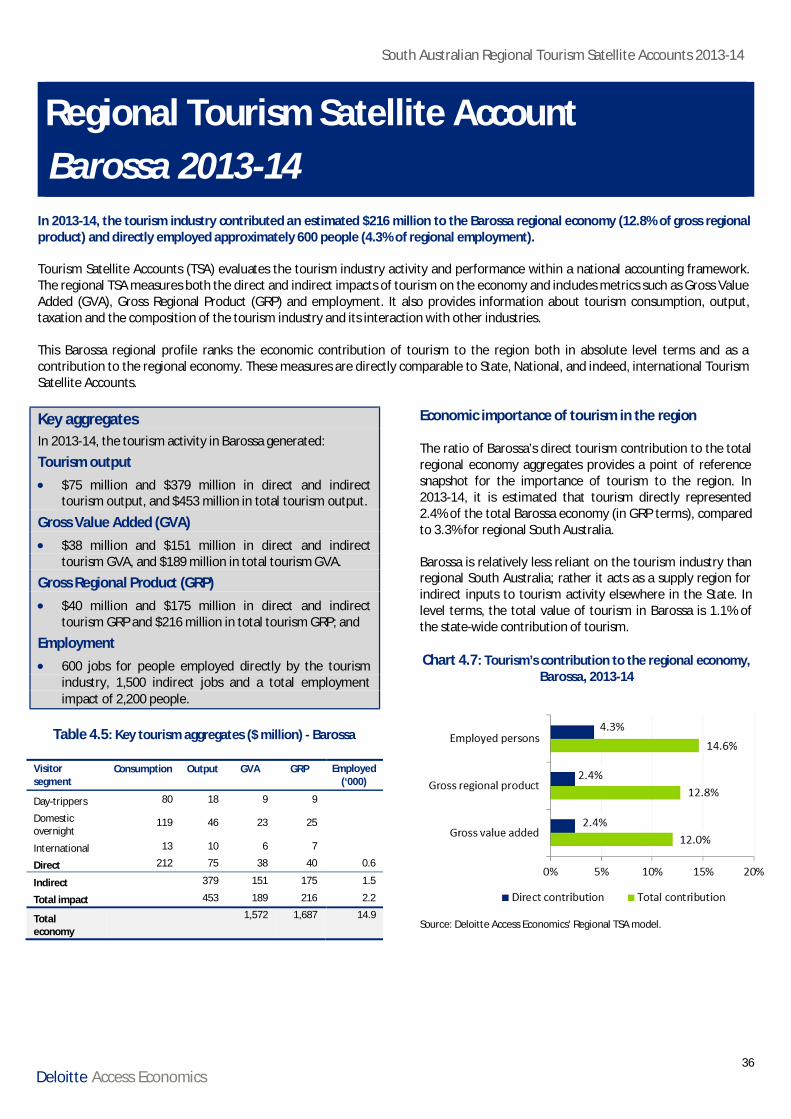

Chart 4.7 : Tourism’s contribution to the regional economy, Barossa, 2013-14 ....................... 36

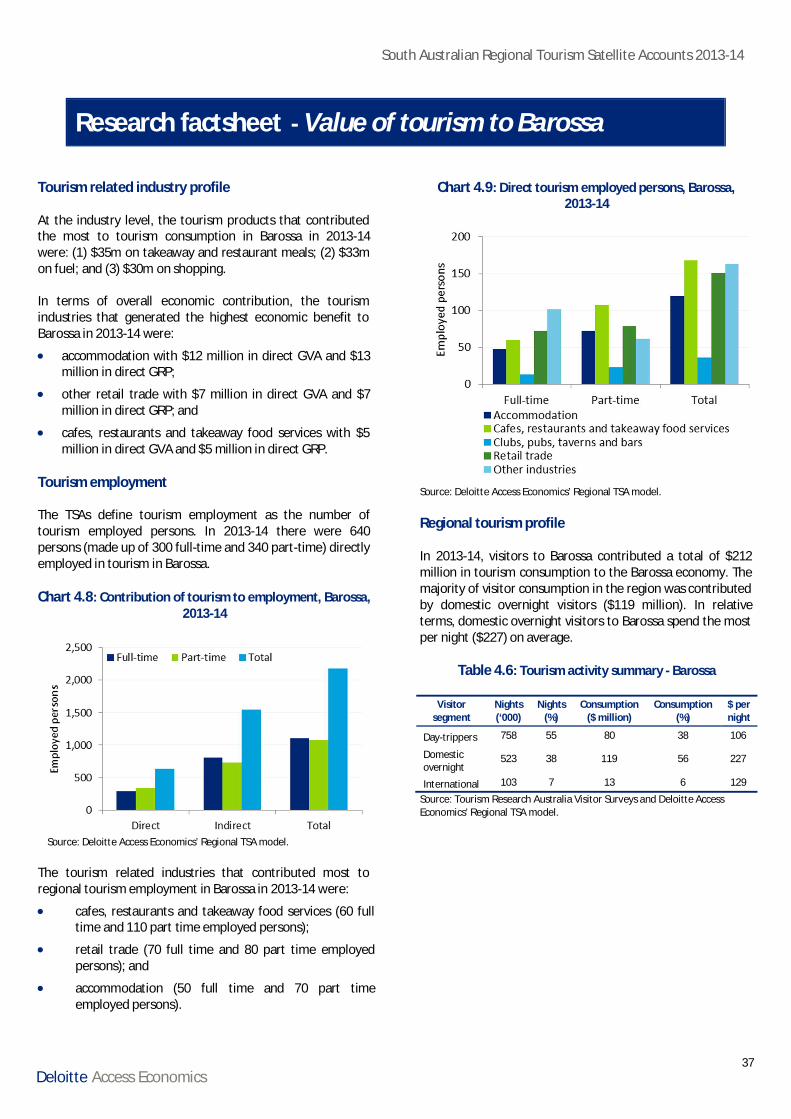

Chart 4.8 : Contribution of tourism to employment, Barossa, 2013-14 .................................... 37

Chart 4.9 : Direct tourism employed persons, Barossa, 2013-14............................................. 37

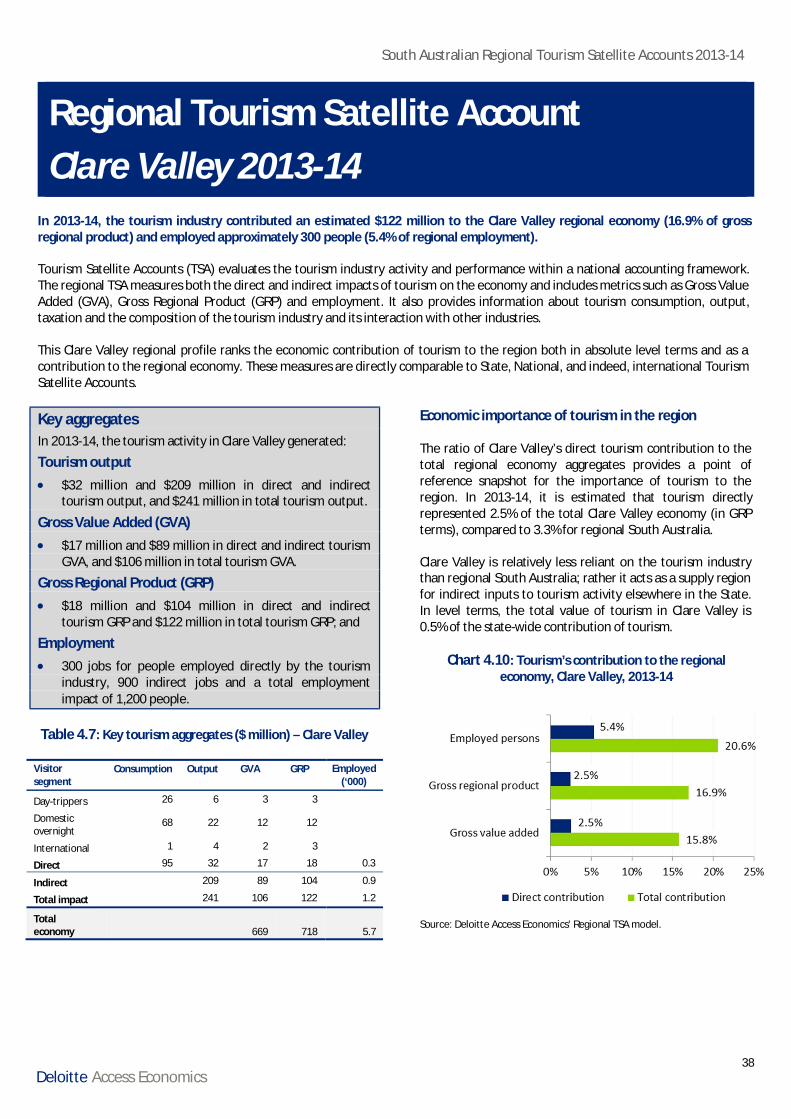

Chart 4.10 : Tourism’s contribution to the regional economy, Clare Valley, 2013-14 ............... 38

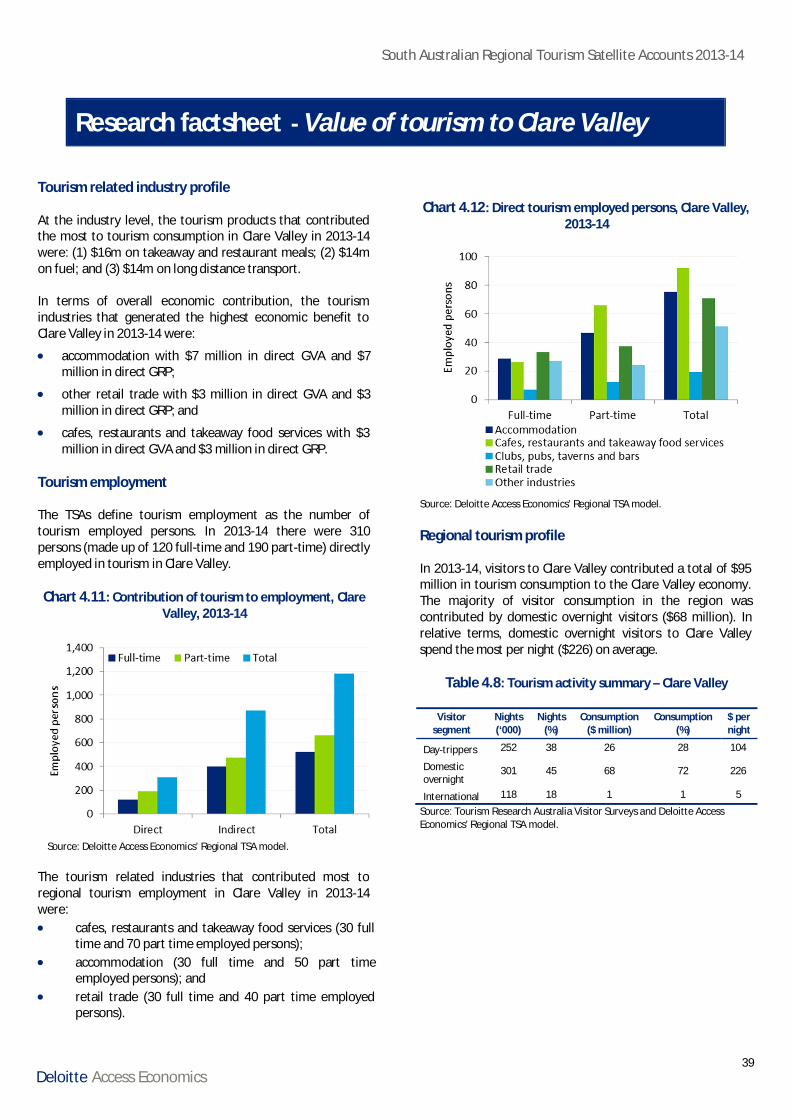

Chart 4.11 : Contribution of tourism to employment, Clare Valley, 2013-14............................ 39

Chart 4.12 : Direct tourism employed persons, Clare Valley, 2013-14 ..................................... 39

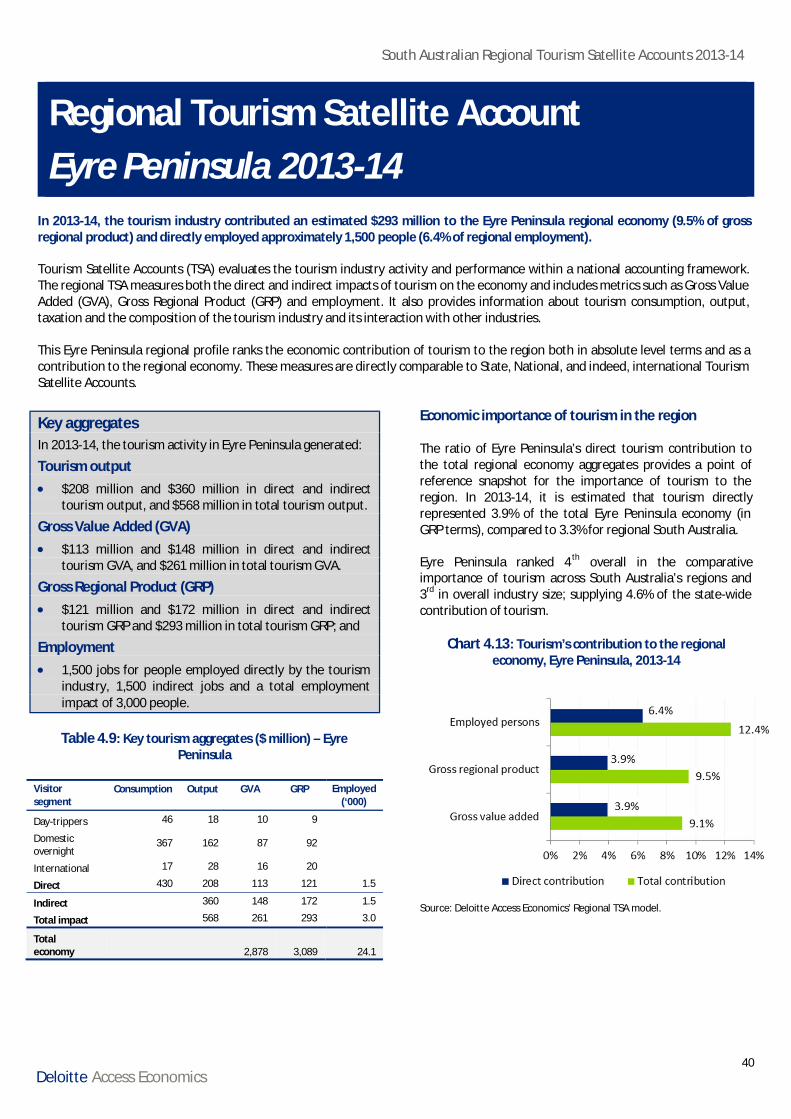

Chart 4.13 : Tourism’s contribution to the regional economy, Eyre Peninsula, 2013-14 .......... 40

Chart 4.14 : Contribution of tourism to employment, Eyre Peninsula, 2013-14 ....................... 41

Chart 4.15 : Direct tourism employed persons, Eyre Peninsula, 2013-14 ................................. 41

Chart 4.16 : Tourism’s contribution to the regional economy, Fleurieu Peninsula, 2013-14 ..... 42

Chart 4.17 : Contribution of tourism to employment, Fleurieu Peninsula, 2013-14 ................. 43

Chart 4.18 : Direct tourism employed persons, Fleurieu Peninsula, 2013-14 ........................... 43

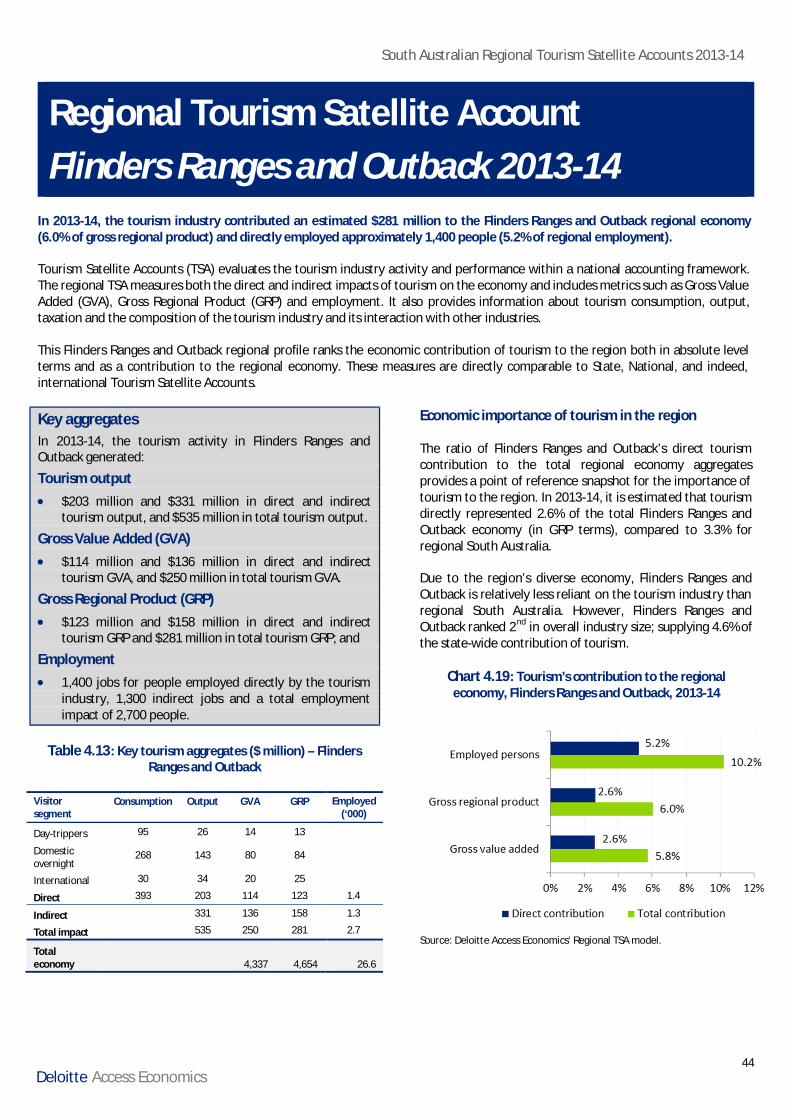

Chart 4.19 : Tourism’s contribution to the regional economy, Flinders Ranges and Outback, 2013-14 44

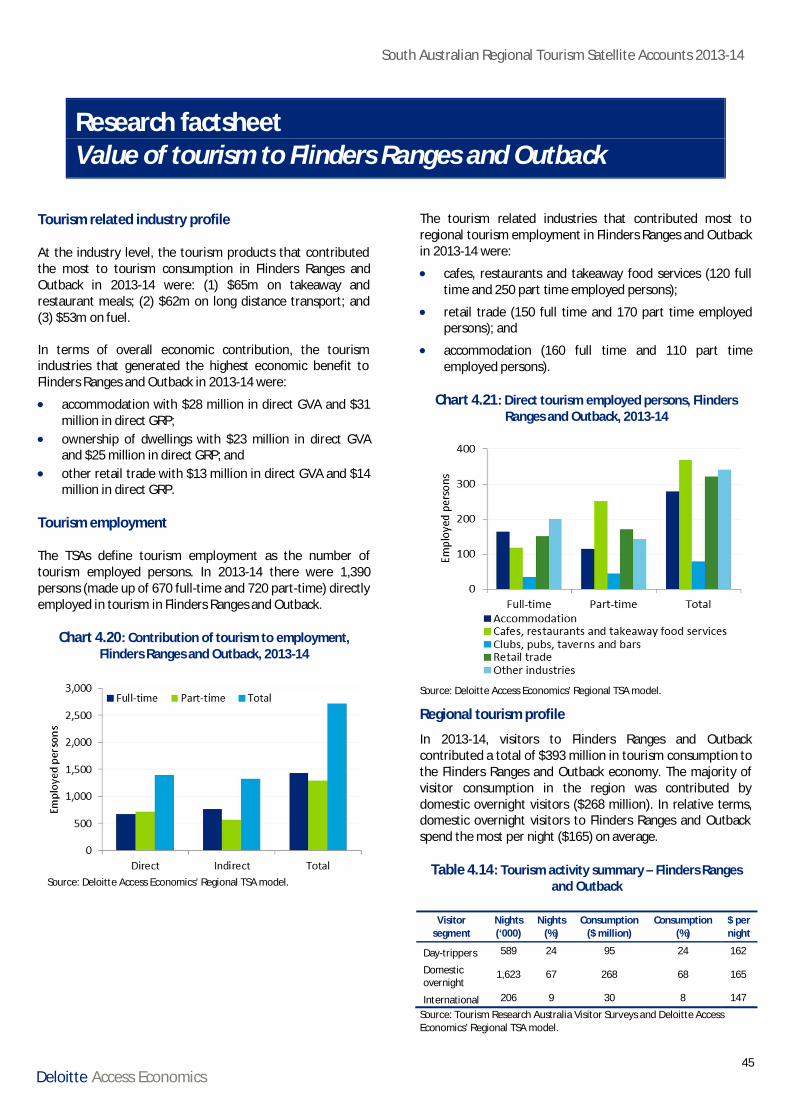

Chart 4.20 : Contribution of tourism to employment, Flinders Ranges and Outback, 2013-14 . 45

Chart 4.21 : Direct tourism employed persons, Flinders Ranges and Outback, 2013-14 ........... 45

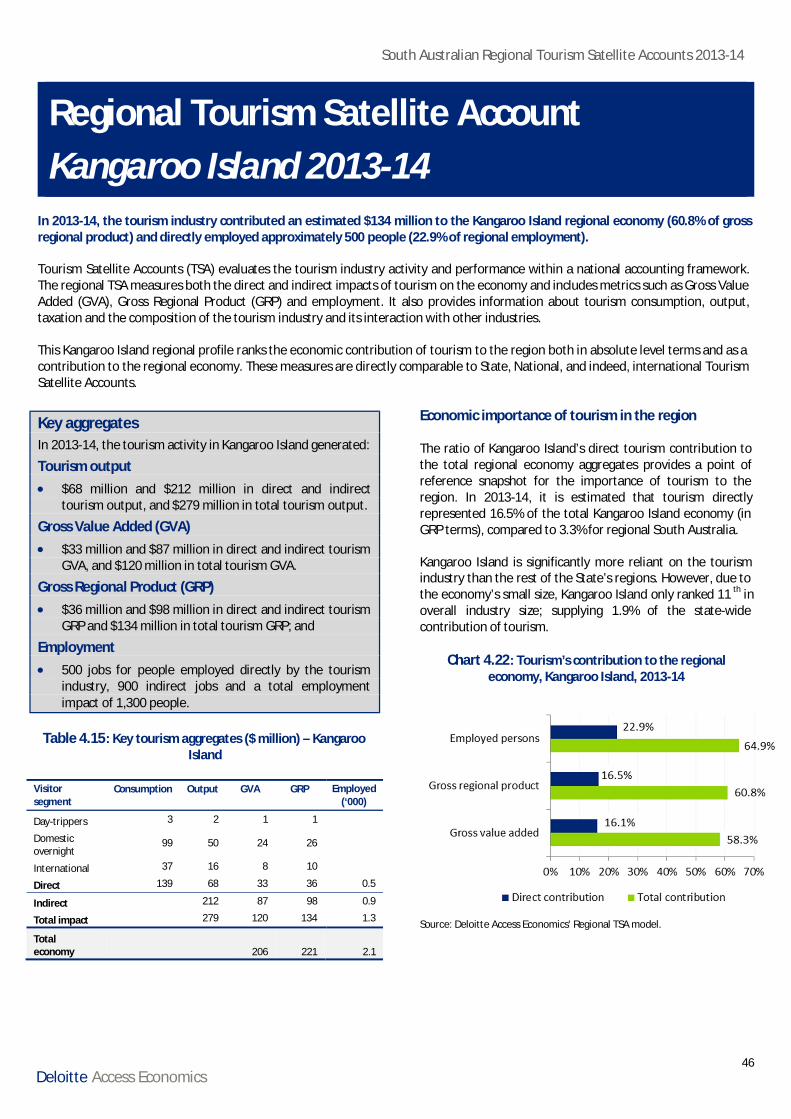

Chart 4.22 : Tourism’s contribution to the regional economy, Kangaroo Island, 2013-14 ........ 46

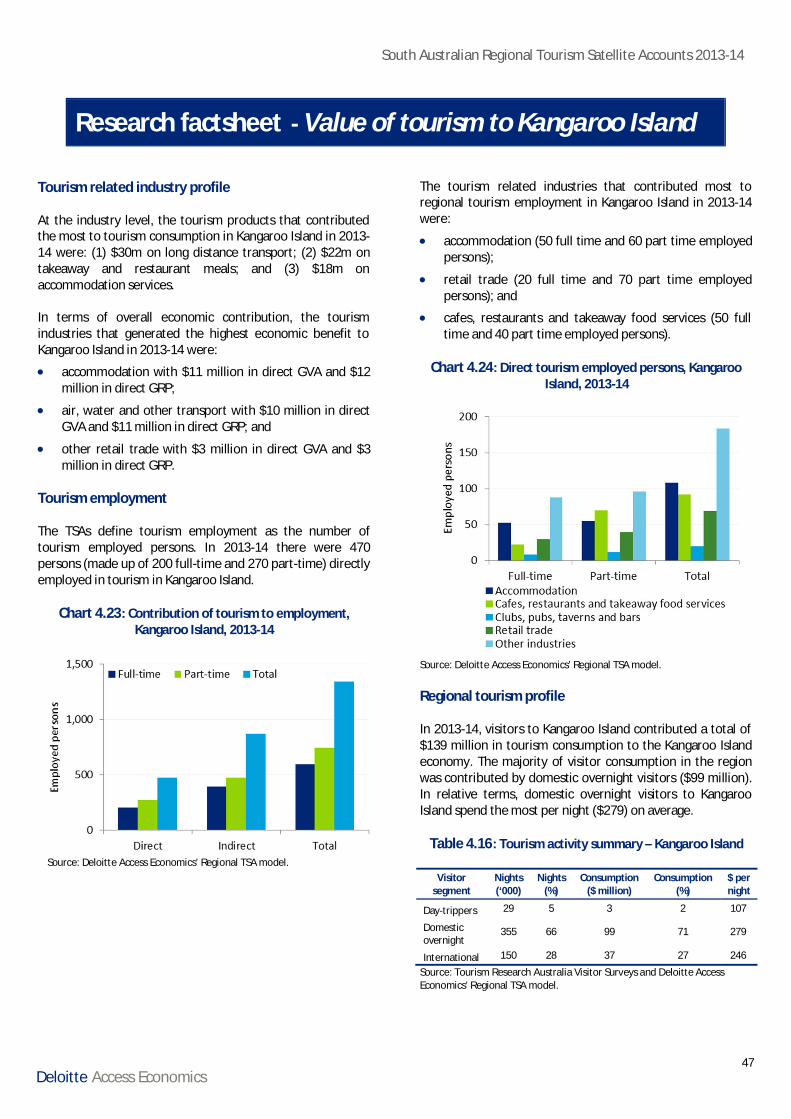

Chart 4.23 : Contribution of tourism to employment, Kangaroo Island, 2013-14 ..................... 47

Chart 4.24 : Direct tourism employed persons, Kangaroo Island, 2013-14 ............................... 47

South Australian Regional Tourism Satellite Accounts 2013-14

iiiDeloitte Access Economics

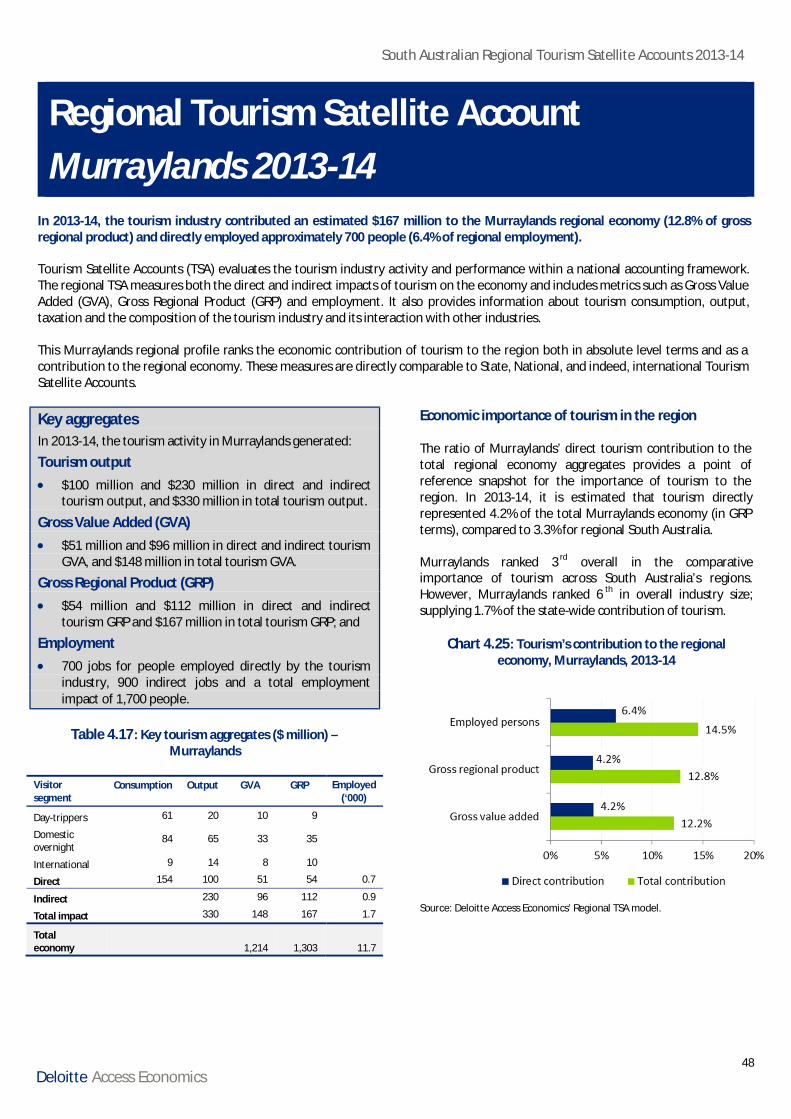

Chart 4.25 : Tourism’s contribution to the regional economy, Murraylands, 2013-14 ............. 48

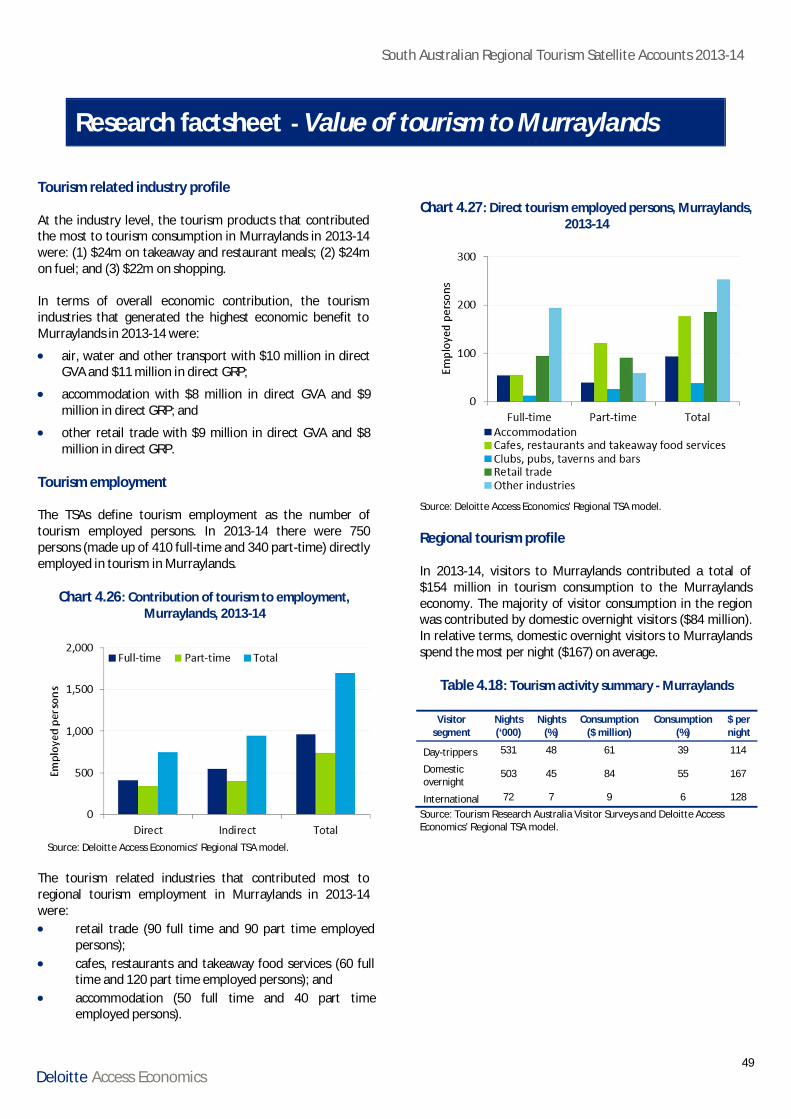

Chart 4.26 : Contribution of tourism to employment, Murraylands, 2013-14 .......................... 49

Chart 4.27 : Direct tourism employed persons, Murraylands, 2013-14 .................................... 49

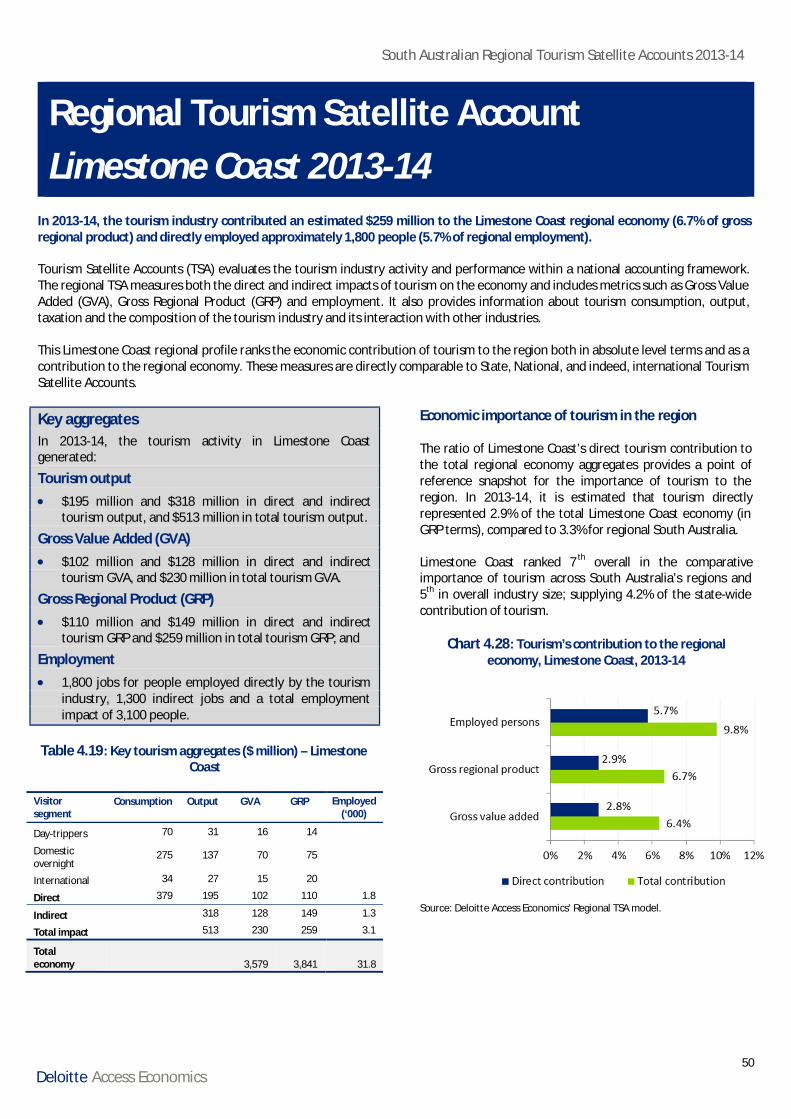

Chart 4.28 : Tourism’s contribution to the regional economy, Limestone Coast, 2013-14 ....... 50

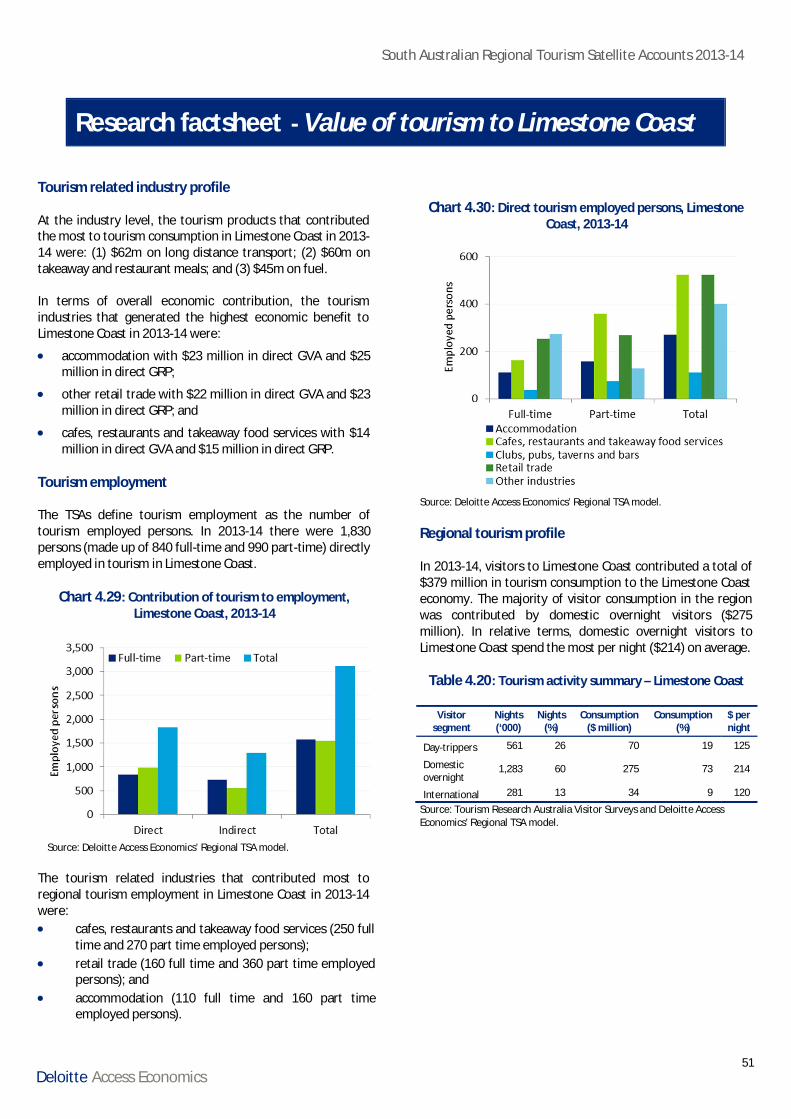

Chart 4.29 : Contribution of tourism to employment, Limestone Coast, 2013-14 .................... 51

Chart 4.30 : Direct tourism employed persons, Limestone Coast, 2013-14 .............................. 51

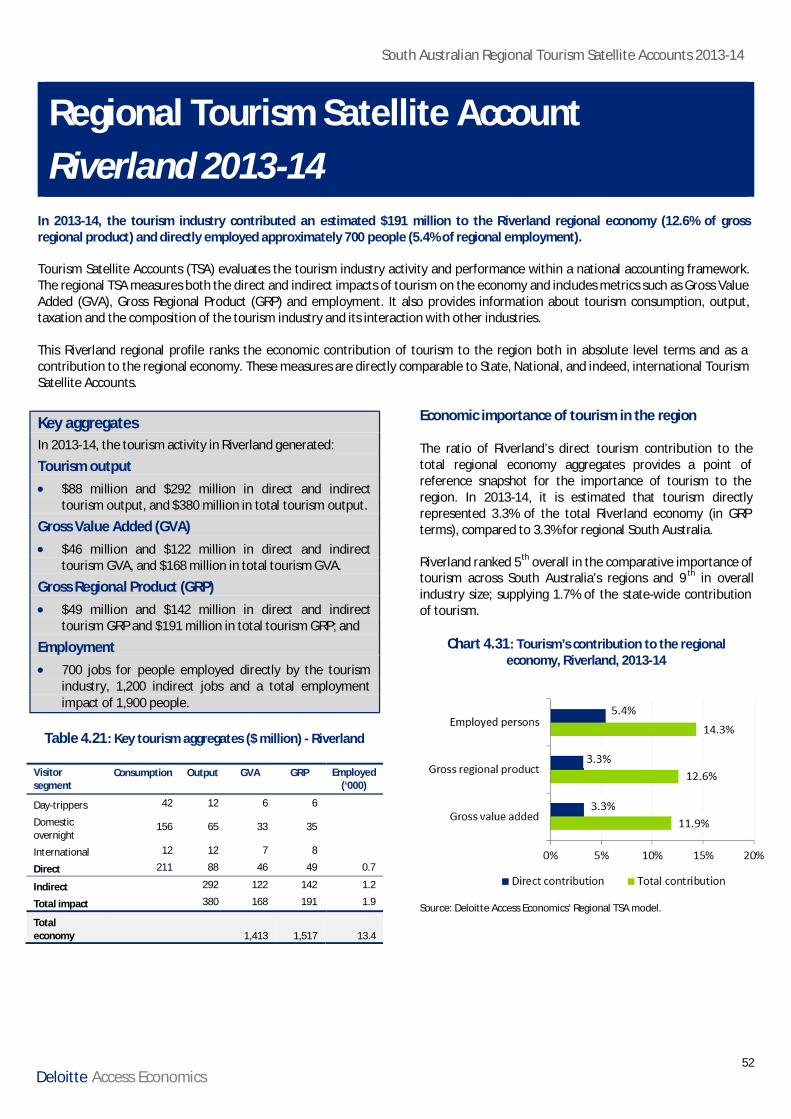

Chart 4.31 : Tourism’s contribution to the regional economy, Riverland, 2013-14 .................. 52

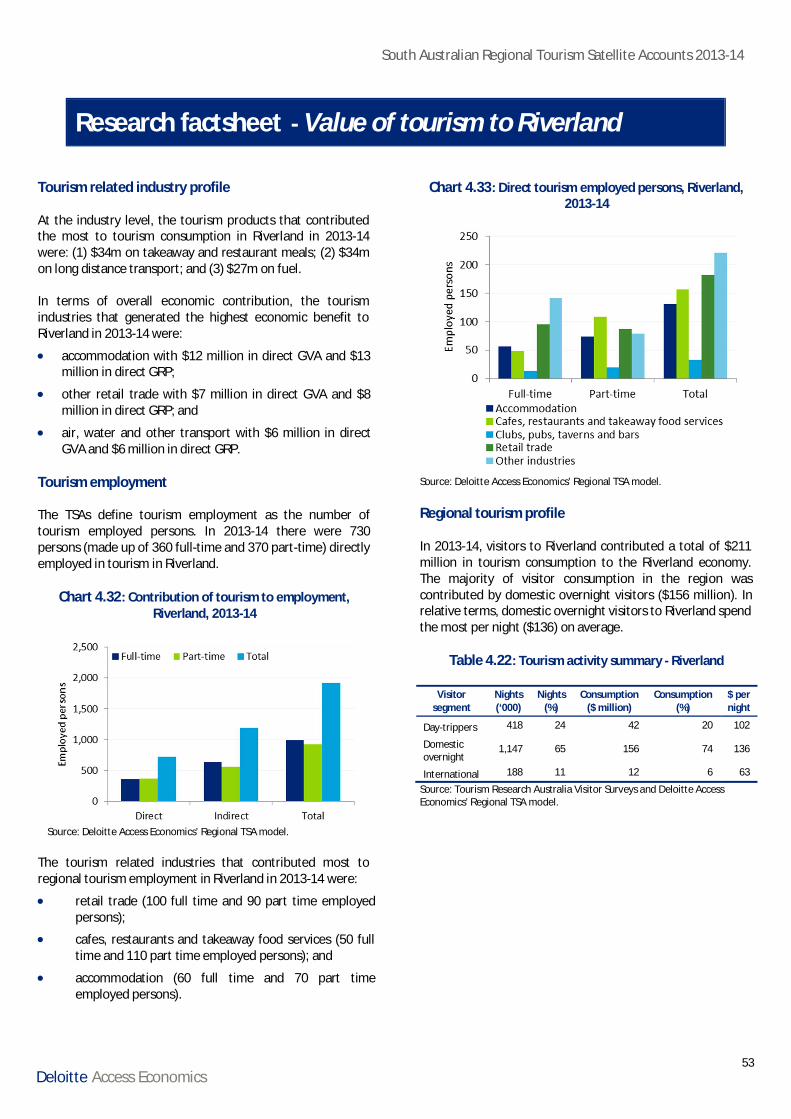

Chart 4.32 : Contribution of tourism to employment, Riverland, 2013-14 ............................... 53

Chart 4.33 : Direct tourism employed persons, Riverland, 2013-14 ......................................... 53

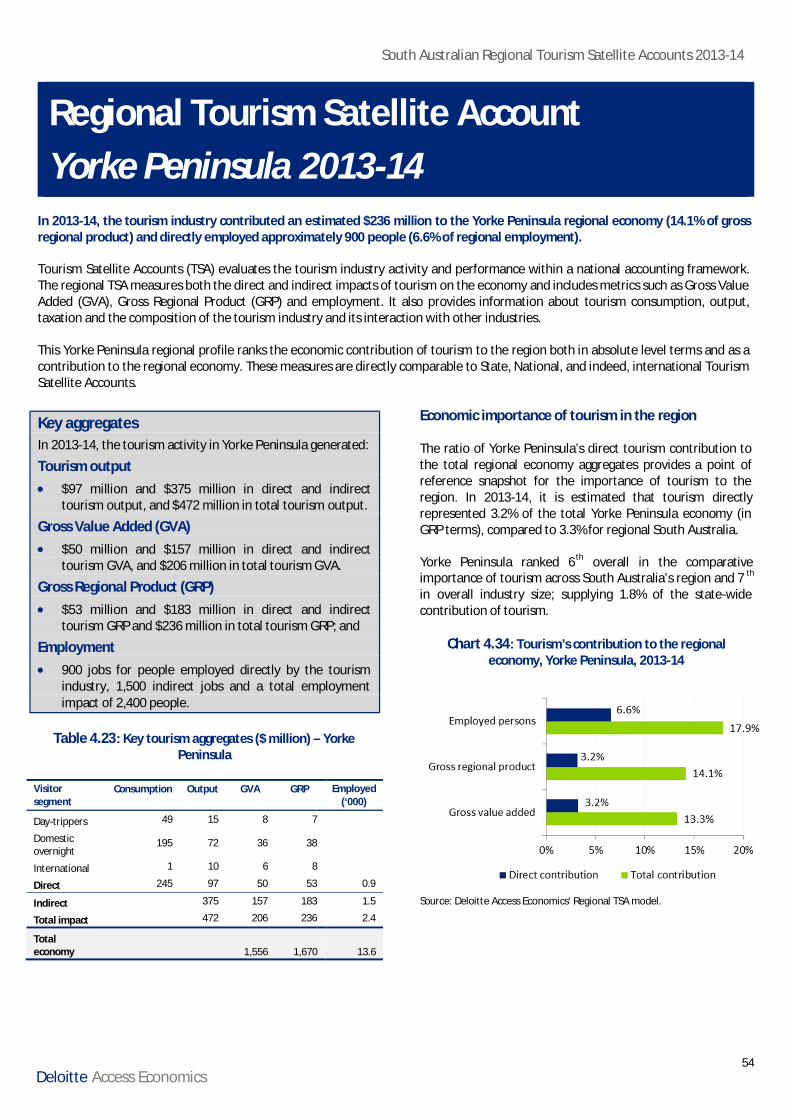

Chart 4.34 : Tourism’s contribution to the regional economy, Yorke Peninsula, 2013-14 ........ 54

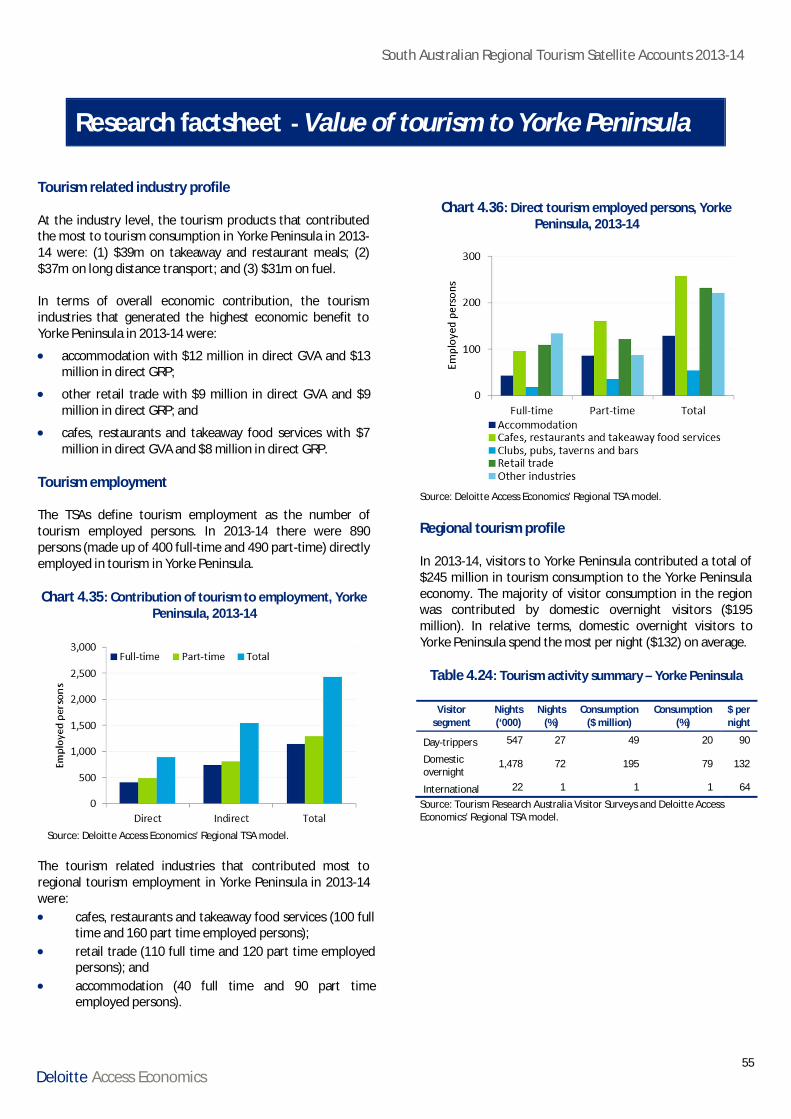

Chart 4.35 : Contribution of tourism to employment, Yorke Peninsula, 2013-14 ..................... 55

Chart 4.36 : Direct tourism employed persons, Yorke Peninsula, 2013-14 ............................... 55

TablesTable 2.1 : Regional economy key aggregates, 2013-14 .......................................................... 17

Table 2.2 : Comparative importance of tourism to local economies, 2013-14 ......................... 17

Table 2.3 : Contribution of tourism by region, 2013-14 ........................................................... 20

Table 2.4 : Importance of tourism to South Australia’s regions, 2013-14 ................................. 21

Table 3.1 : Tourism GVA by region ($ million), 2006-07 to 2013-14 ........................................ 28

Table 3.2 : Tourism GRP by region ($ million), 2006-07 to 2013-14 ........................................ 29

Table 3.3 : Tourism employment by region, 2006-07 to 2013-14 ............................................ 30

Table 4.1 : Key tourism aggregates ($ million) - Adelaide ........................................................ 32

Table 4.2 : Tourism activity summary - Adelaide ..................................................................... 33

Table 4.3 : Key tourism aggregates – Adelaide Hills ($ million) ................................................ 34

Table 4.4 : Tourism activity summary – Adelaide Hills ............................................................. 35

Table 4.5 : Key tourism aggregates ($ million) - Barossa .......................................................... 36

Table 4.6 : Tourism activity summary - Barossa ....................................................................... 37

Table 4.7 : Key tourism aggregates ($ million) – Clare Valley ................................................... 38

Table 4.8 : Tourism activity summary – Clare Valley ................................................................ 39

Table 4.9 : Key tourism aggregates ($ million) – Eyre Peninsula .............................................. 40

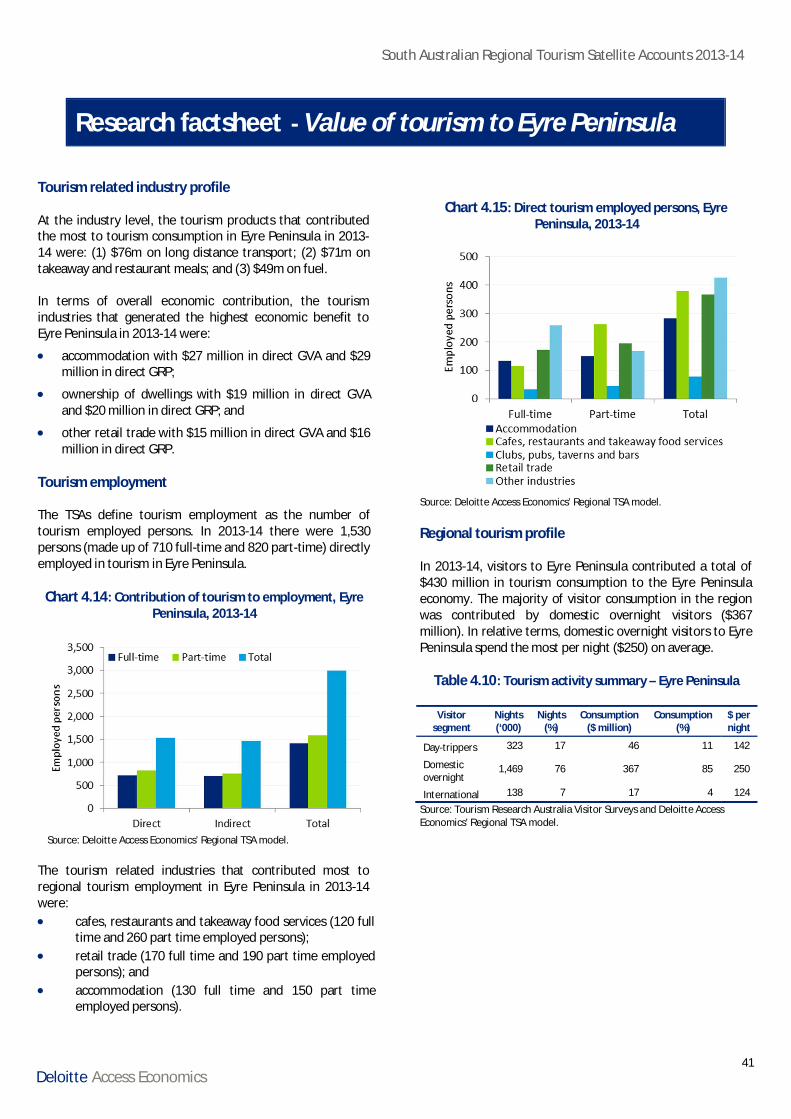

Table 4.10 : Tourism activity summary – Eyre Peninsula ......................................................... 41

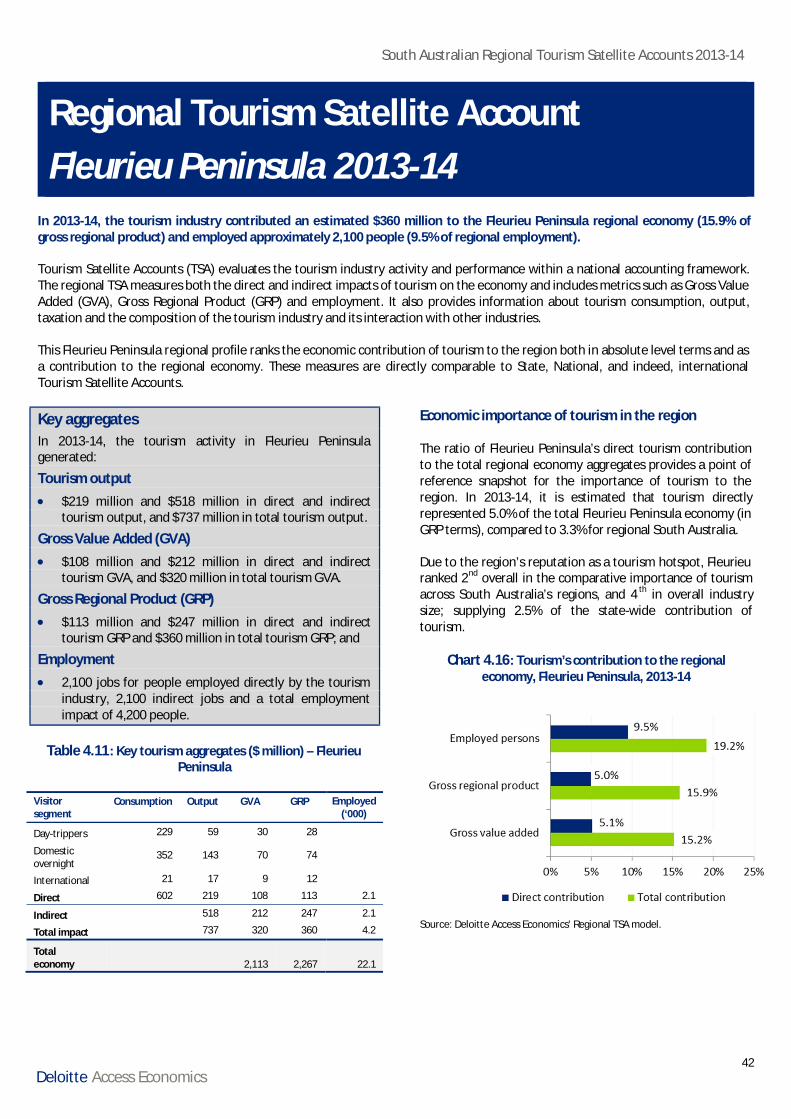

Table 4.11 : Key tourism aggregates ($ million) – Fleurieu Peninsula ....................................... 42

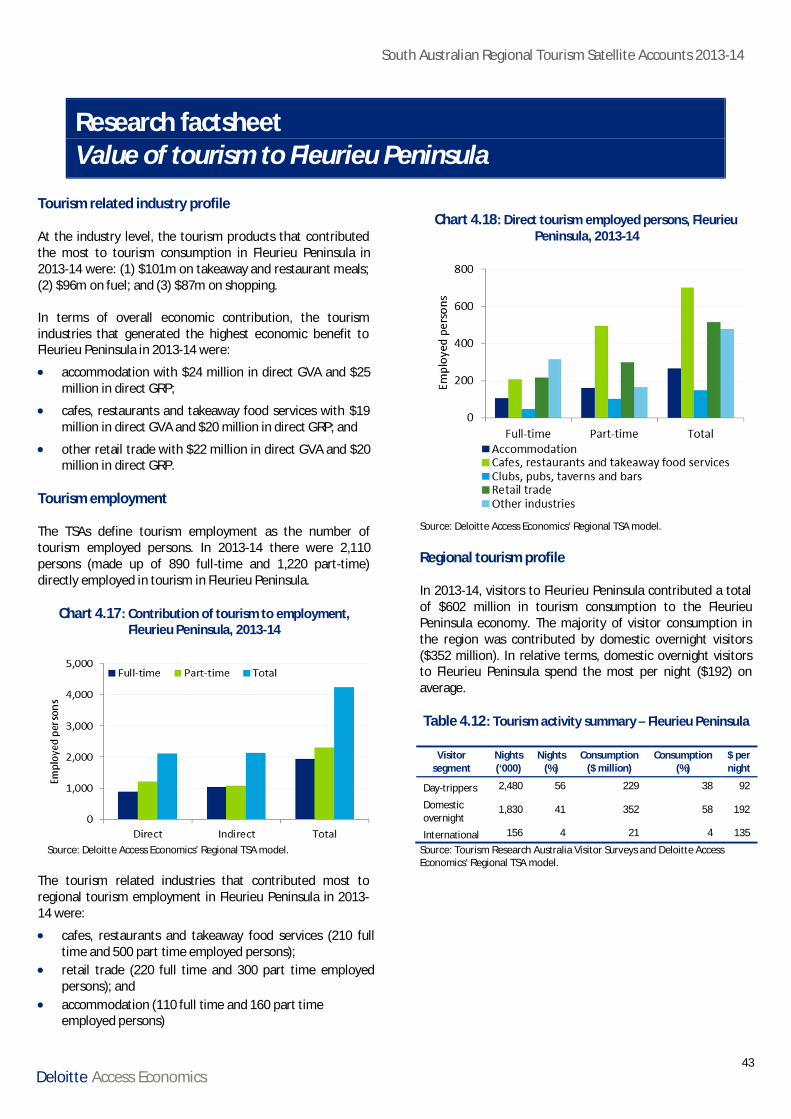

Table 4.12 : Tourism activity summary – Fleurieu Peninsula.................................................... 43

Table 4.13 : Key tourism aggregates ($ million) – Flinders Ranges and Outback ...................... 44

Table 4.14 : Tourism activity summary – Flinders Ranges and Outback ................................... 45

Table 4.15 : Key tourism aggregates ($ million) – Kangaroo Island .......................................... 46

South Australian Regional Tourism Satellite Accounts 2013-14

ivDeloitte Access Economics

Table 4.16 : Tourism activity summary – Kangaroo Island ....................................................... 47

Table 4.17 : Key tourism aggregates ($ million) – Murraylands ............................................... 49

Table 4.18 : Tourism activity summary - Murraylands ............................................................. 49

Table 4.19 : Key tourism aggregates ($ million) – Limestone Coast ......................................... 50

Table 4.20 : Tourism activity summary – Limestone Coast ...................................................... 51

Table 4.21 : Key tourism aggregates ($ million) - Riverland ..................................................... 52

Table 4.22 : Tourism activity summary - Riverland .................................................................. 53

Table 4.23 : Key tourism aggregates ($ million) – Yorke Peninsula .......................................... 54

Table 4.24 : Tourism activity summary – Yorke Peninsula ....................................................... 55

FiguresFigure 1.1 : South Australian Tourism Regions .......................................................................... 4

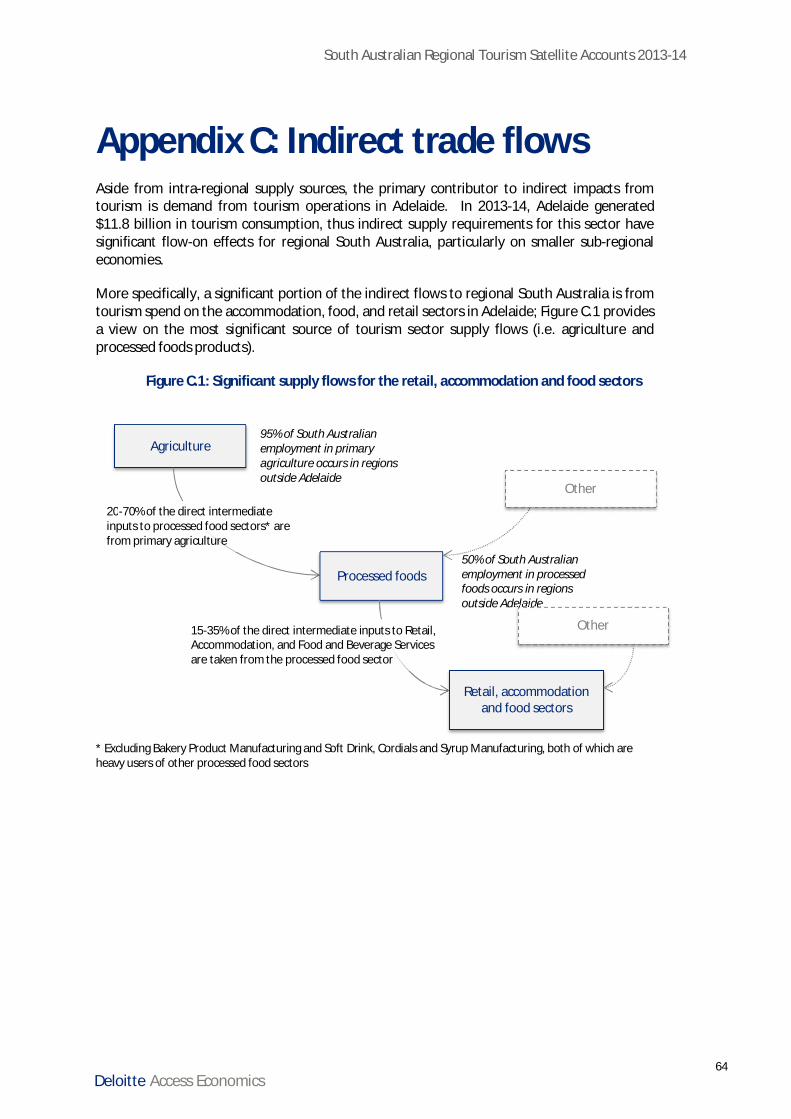

Figure C.1 : Significant supply flows for the retail, accommodation and food sectors .............. 59

South Australian Regional Tourism Satellite Accounts 2013-14

vDeloitte Access Economics

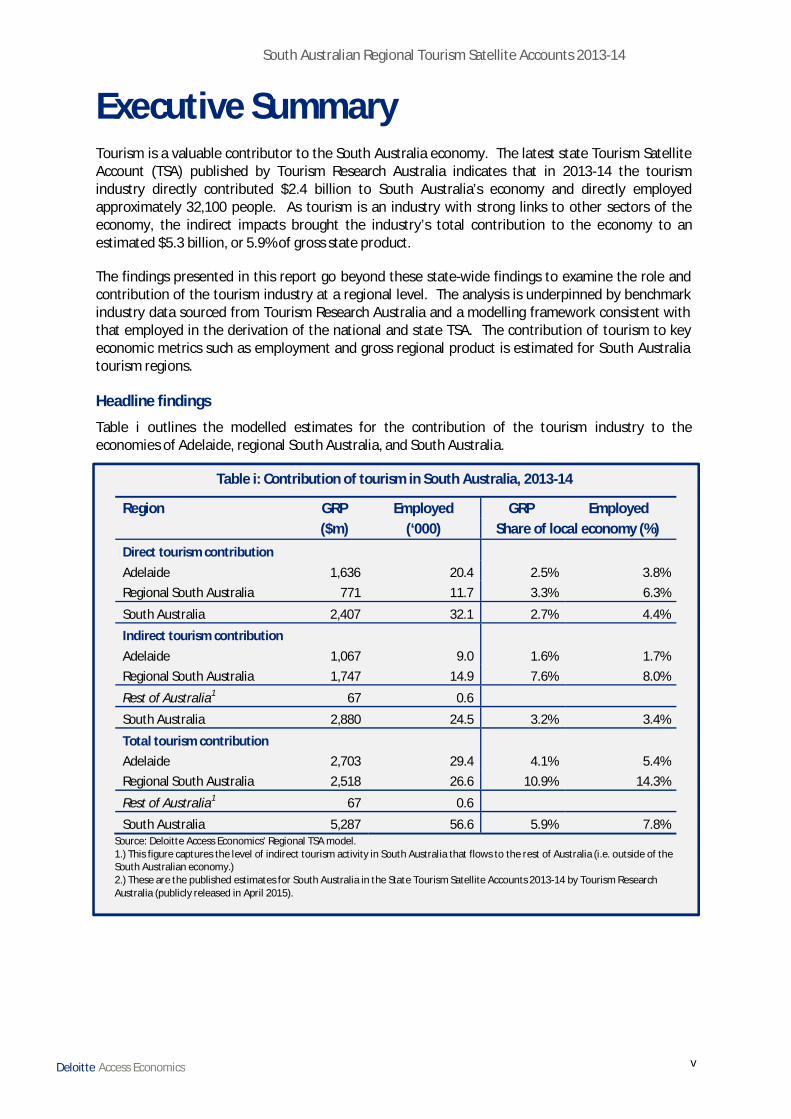

Executive SummaryTourism is a valuable contributor to the South Australia economy. The latest state Tourism SatelliteAccount (TSA) published by Tourism Research Australia indicates that in 2013-14 the tourismindustry directly contributed $2.4 billion to South Australia’s economy and directly employedapproximately 32,100 people. As tourism is an industry with strong links to other sectors of theeconomy, the indirect impacts brought the industry’s total contribution to the economy to anestimated $5.3 billion, or 5.9% of gross state product.

The findings presented in this report go beyond these state-wide findings to examine the role andcontribution of the tourism industry at a regional level. The analysis is underpinned by benchmarkindustry data sourced from Tourism Research Australia and a modelling framework consistent withthat employed in the derivation of the national and state TSA. The contribution of tourism to keyeconomic metrics such as employment and gross regional product is estimated for South Australiatourism regions.

Headline findings

Table i outlines the modelled estimates for the contribution of the tourism industry to theeconomies of Adelaide, regional South Australia, and South Australia.

Table i: Contribution of tourism in South Australia, 2013-14

Region GRP Employed GRP Employed ($m) (‘000) Share of local economy (%)

Direct tourism contributionAdelaide 1,636 20.4 2.5% 3.8%Regional South Australia 771 11.7 3.3% 6.3%

South Australia 2,407 32.1 2.7% 4.4%

Indirect tourism contributionAdelaide 1,067 9.0 1.6% 1.7%Regional South Australia 1,747 14.9 7.6% 8.0%

Rest of Australia1 67 0.6

South Australia 2,880 24.5 3.2% 3.4%

Total tourism contributionAdelaide 2,703 29.4 4.1% 5.4%Regional South Australia 2,518 26.6 10.9% 14.3%

Rest of Australia1 67 0.6

South Australia 5,287 56.6 5.9% 7.8%Source: Deloitte Access Economics’ Regional TSA model.1.) This figure captures the level of indirect tourism activity in South Australia that flows to the rest of Australia (i.e. outside of theSouth Australian economy.)2.) These are the published estimates for South Australia in the State Tourism Satellite Accounts 2013-14 by Tourism ResearchAustralia (publicly released in April 2015).

South Australian Regional Tourism Satellite Accounts 2013-14

viDeloitte Access Economics

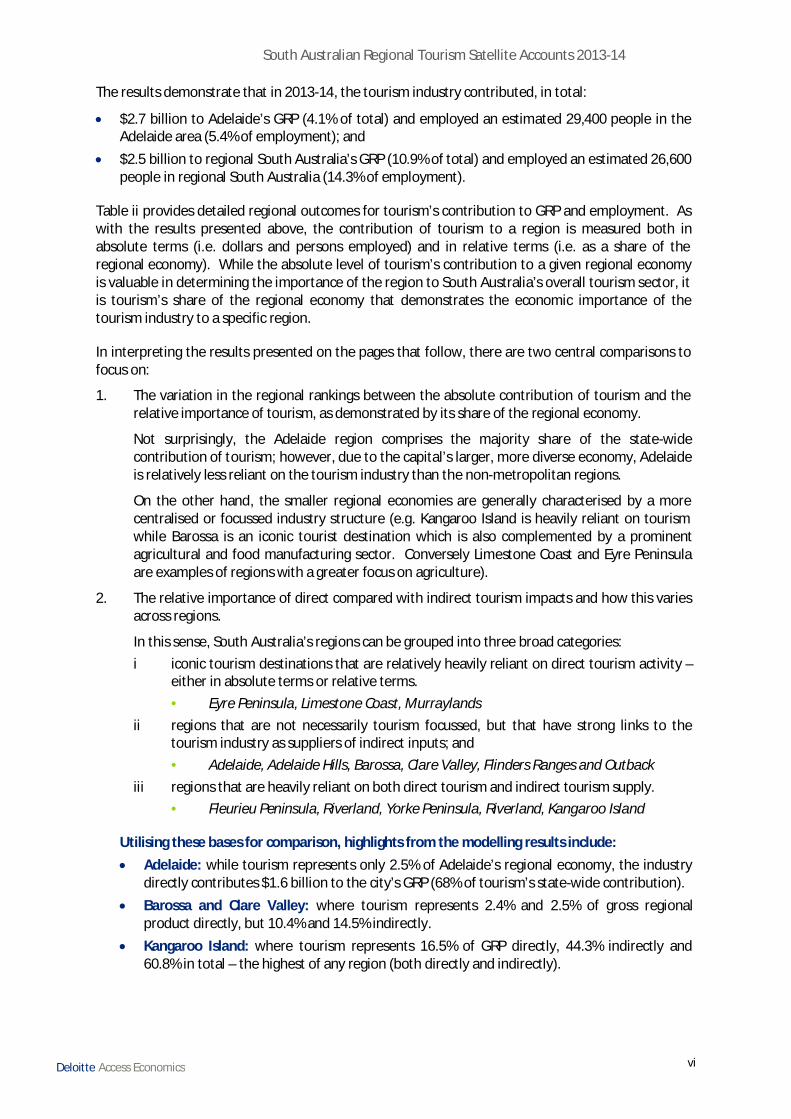

The results demonstrate that in 2013-14, the tourism industry contributed, in total:

· $2.7 billion to Adelaide’s GRP (4.1% of total) and employed an estimated 29,400 people in theAdelaide area (5.4% of employment); and

· $2.5 billion to regional South Australia’s GRP (10.9% of total) and employed an estimated 26,600people in regional South Australia (14.3% of employment).

Table ii provides detailed regional outcomes for tourism’s contribution to GRP and employment. Aswith the results presented above, the contribution of tourism to a region is measured both inabsolute terms (i.e. dollars and persons employed) and in relative terms (i.e. as a share of theregional economy). While the absolute level of tourism’s contribution to a given regional economyis valuable in determining the importance of the region to South Australia’s overall tourism sector, itis tourism’s share of the regional economy that demonstrates the economic importance of thetourism industry to a specific region.

In interpreting the results presented on the pages that follow, there are two central comparisons tofocus on:

1. The variation in the regional rankings between the absolute contribution of tourism and therelative importance of tourism, as demonstrated by its share of the regional economy.

Not surprisingly, the Adelaide region comprises the majority share of the state-widecontribution of tourism; however, due to the capital’s larger, more diverse economy, Adelaideis relatively less reliant on the tourism industry than the non-metropolitan regions.

On the other hand, the smaller regional economies are generally characterised by a morecentralised or focussed industry structure (e.g. Kangaroo Island is heavily reliant on tourismwhile Barossa is an iconic tourist destination which is also complemented by a prominentagricultural and food manufacturing sector. Conversely Limestone Coast and Eyre Peninsulaare examples of regions with a greater focus on agriculture).

2. The relative importance of direct compared with indirect tourism impacts and how this variesacross regions.

In this sense, South Australia’s regions can be grouped into three broad categories:i iconic tourism destinations that are relatively heavily reliant on direct tourism activity –

either in absolute terms or relative terms.• Eyre Peninsula, Limestone Coast, Murraylands

ii regions that are not necessarily tourism focussed, but that have strong links to thetourism industry as suppliers of indirect inputs; and• Adelaide, Adelaide Hills, Barossa, Clare Valley, Flinders Ranges and Outback

iii regions that are heavily reliant on both direct tourism and indirect tourism supply.• Fleurieu Peninsula, Riverland, Yorke Peninsula, Riverland, Kangaroo Island

Utilising these bases for comparison, highlights from the modelling results include:· Adelaide: while tourism represents only 2.5% of Adelaide’s regional economy, the industry

directly contributes $1.6 billion to the city’s GRP (68% of tourism’s state-wide contribution).· Barossa and Clare Valley: where tourism represents 2.4% and 2.5% of gross regional

product directly, but 10.4% and 14.5% indirectly.· Kangaroo Island: where tourism represents 16.5% of GRP directly, 44.3% indirectly and

60.8% in total – the highest of any region (both directly and indirectly).

South Australian Regional Tourism Satellite Accounts 2013-14

viiDeloitte Access Economics

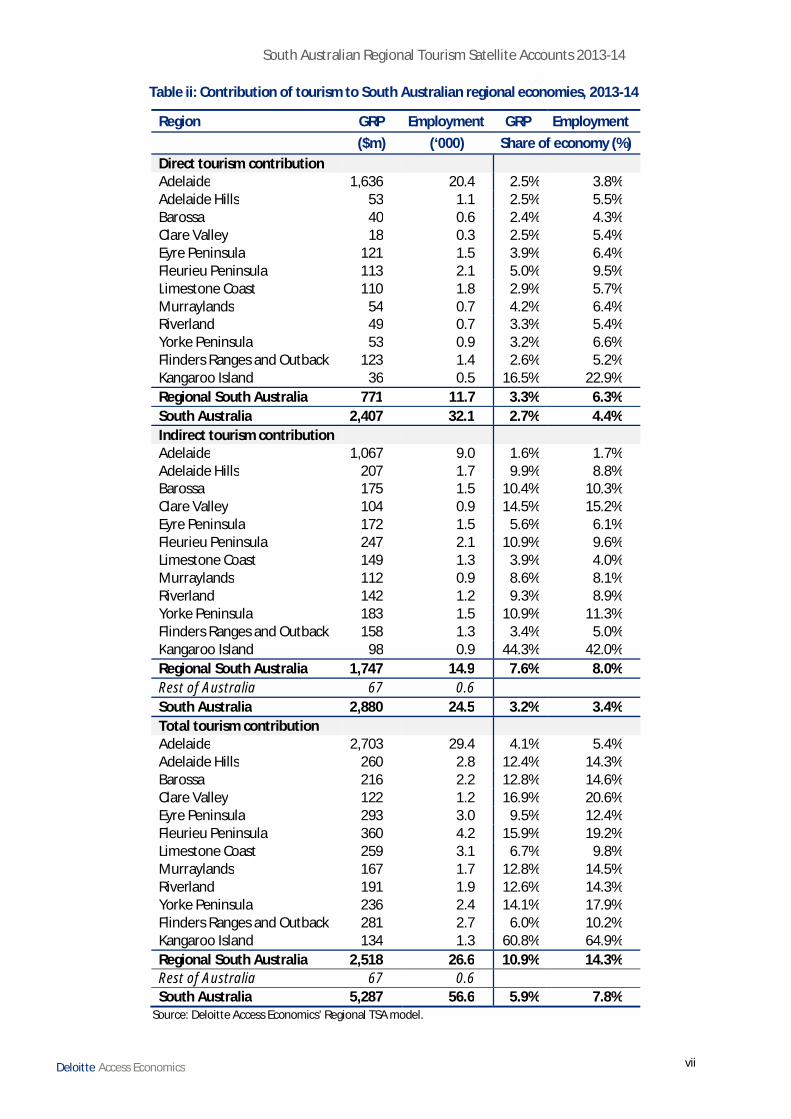

Table ii: Contribution of tourism to South Australian regional economies, 2013-14

Region GRP Employment GRP Employment ($m) (‘000) Share of economy (%)Direct tourism contributionAdelaide 1,636 20.4 2.5% 3.8%Adelaide Hills 53 1.1 2.5% 5.5%Barossa 40 0.6 2.4% 4.3%Clare Valley 18 0.3 2.5% 5.4%Eyre Peninsula 121 1.5 3.9% 6.4%Fleurieu Peninsula 113 2.1 5.0% 9.5%Limestone Coast 110 1.8 2.9% 5.7%Murraylands 54 0.7 4.2% 6.4%Riverland 49 0.7 3.3% 5.4%Yorke Peninsula 53 0.9 3.2% 6.6%Flinders Ranges and Outback 123 1.4 2.6% 5.2%Kangaroo Island 36 0.5 16.5% 22.9%Regional South Australia 771 11.7 3.3% 6.3%South Australia 2,407 32.1 2.7% 4.4%Indirect tourism contributionAdelaide 1,067 9.0 1.6% 1.7%Adelaide Hills 207 1.7 9.9% 8.8%Barossa 175 1.5 10.4% 10.3%Clare Valley 104 0.9 14.5% 15.2%Eyre Peninsula 172 1.5 5.6% 6.1%Fleurieu Peninsula 247 2.1 10.9% 9.6%Limestone Coast 149 1.3 3.9% 4.0%Murraylands 112 0.9 8.6% 8.1%Riverland 142 1.2 9.3% 8.9%Yorke Peninsula 183 1.5 10.9% 11.3%Flinders Ranges and Outback 158 1.3 3.4% 5.0%Kangaroo Island 98 0.9 44.3% 42.0%Regional South Australia 1,747 14.9 7.6% 8.0%Rest of Australia 67 0.6South Australia 2,880 24.5 3.2% 3.4%Total tourism contributionAdelaide 2,703 29.4 4.1% 5.4%Adelaide Hills 260 2.8 12.4% 14.3%Barossa 216 2.2 12.8% 14.6%Clare Valley 122 1.2 16.9% 20.6%Eyre Peninsula 293 3.0 9.5% 12.4%Fleurieu Peninsula 360 4.2 15.9% 19.2%Limestone Coast 259 3.1 6.7% 9.8%Murraylands 167 1.7 12.8% 14.5%Riverland 191 1.9 12.6% 14.3%Yorke Peninsula 236 2.4 14.1% 17.9%Flinders Ranges and Outback 281 2.7 6.0% 10.2%Kangaroo Island 134 1.3 60.8% 64.9%Regional South Australia 2,518 26.6 10.9% 14.3%Rest of Australia 67 0.6South Australia 5,287 56.6 5.9% 7.8%

Source: Deloitte Access Economics’ Regional TSA model.

South Australian Regional Tourism Satellite Accounts 2013-14

viiiDeloitte Access Economics

Drivers of indirect trade flows

When considering the direct and indirect impacts, upstream trade flows generated by tourismactivity have a significant impact on the regional economy. Accordingly, understanding the factorsthat influence these flows is important to understanding the regional TSA results.

Indirect trade flows are driven by demand for inputs to the tourism sector. For example, when arestaurant meal is served, produce, cutlery and plates must be procured. When the tourism sectoris analysed at a regional level, the availability of such inputs in different areas determines the level ofinter-regional trade that occurs. To again use the restaurant example, if produce can be sourcedlocally, then the indirect impact of the restaurant meals accrues to the local region. However, if thisis not possible – e.g. if the region does not have a fresh produce industry – then these inputs mustbe imported from other regions.

The overarching drivers of indirect trade from a particular region, therefore, are (1) presence of theindustry that produces the input required, and (2) a relatively small trading distance between thesupply and demand regions.

Reflecting the major area of tourism expenditure, a significant portion of the indirect flows fromregional South Australia is related to tourism spend on the accommodation, food, and retail sectorsin Adelaide. Regions such as the Barossa, Clare Valley, Adelaide Hills and Fleurieu Peninsula havesignificant indirect flows from tourism industry activity due to the prominence of their agricultureand manufacturing sectors and due to their close proximity to Adelaide.

The contribution of individual market segments

The Tourism Satellite Accounts present the contribution of the tourism industry under three broadvisitor groups, based on their place of origin (or source market): same-day visitors, domesticovernight visitors and international visitors.

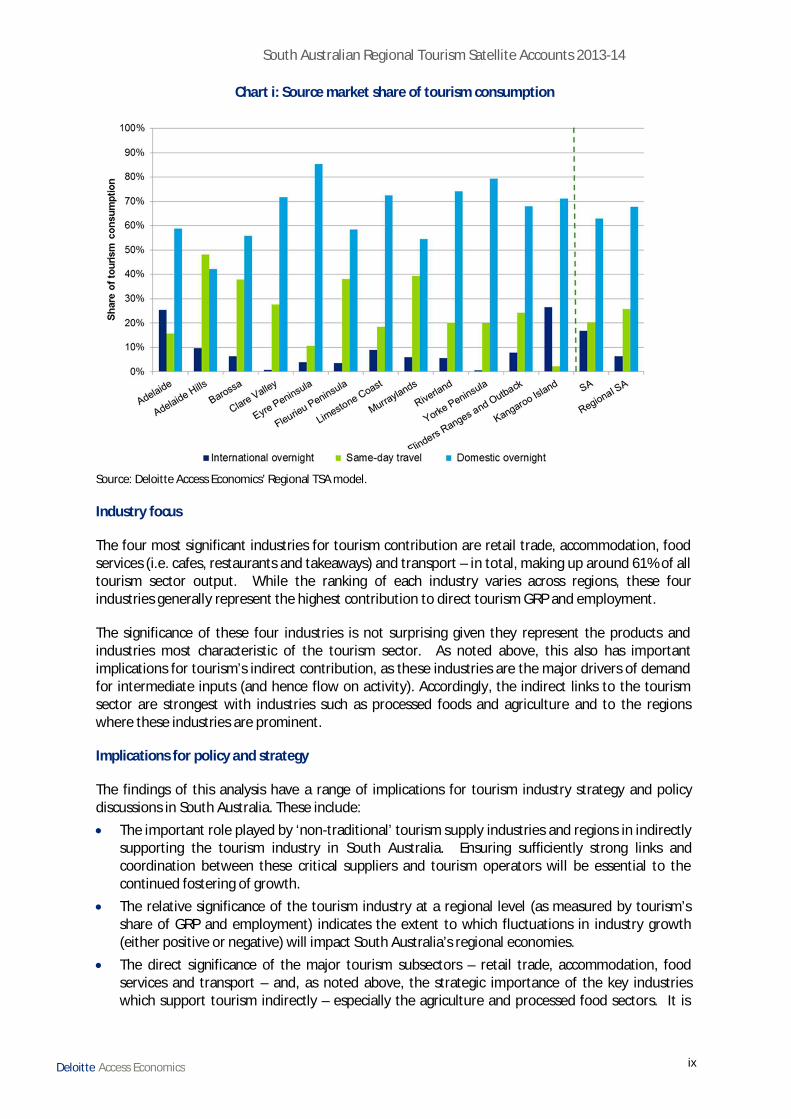

Chart i on the following page shows that international visitors make up 25% of total tourismconsumption in Adelaide, compared to an average of 6% for regional South Australia. Among thenon-metropolitan regions, Kangaroo Island has the greatest reliance on international visitation,making 27% of total tourism consumption in the region. Reflecting this, the vast majority of allinternational tourism consumption – 83% or $926 million – occurs in Adelaide.

Adelaide also catches the majority of domestic overnight visitor consumption for the state, with 51%or $2.1 billion. Additionally, 42% of all same day tourism consumption occurs in the capital withFleurieu Peninsula being the next highest, contributing $229 million or 17% of same dayexpenditure. The regions that are most reliant on same day travel are Adelaide Hills (48% of totaltourism consumption) and Murraylands (39% of total tourism consumption).

South Australian Regional Tourism Satellite Accounts 2013-14

ixDeloitte Access Economics

Chart i: Source market share of tourism consumption

Source: Deloitte Access Economics’ Regional TSA model.

Industry focus

The four most significant industries for tourism contribution are retail trade, accommodation, foodservices (i.e. cafes, restaurants and takeaways) and transport – in total, making up around 61% of alltourism sector output. While the ranking of each industry varies across regions, these fourindustries generally represent the highest contribution to direct tourism GRP and employment.

The significance of these four industries is not surprising given they represent the products andindustries most characteristic of the tourism sector. As noted above, this also has importantimplications for tourism’s indirect contribution, as these industries are the major drivers of demandfor intermediate inputs (and hence flow on activity). Accordingly, the indirect links to the tourismsector are strongest with industries such as processed foods and agriculture and to the regionswhere these industries are prominent.

Implications for policy and strategy

The findings of this analysis have a range of implications for tourism industry strategy and policydiscussions in South Australia. These include:· The important role played by ‘non-traditional’ tourism supply industries and regions in indirectly

supporting the tourism industry in South Australia. Ensuring sufficiently strong links andcoordination between these critical suppliers and tourism operators will be essential to thecontinued fostering of growth.

· The relative significance of the tourism industry at a regional level (as measured by tourism’sshare of GRP and employment) indicates the extent to which fluctuations in industry growth(either positive or negative) will impact South Australia’s regional economies.

· The direct significance of the major tourism subsectors – retail trade, accommodation, foodservices and transport – and, as noted above, the strategic importance of the key industrieswhich support tourism indirectly – especially the agriculture and processed food sectors. It is

South Australian Regional Tourism Satellite Accounts 2013-14

xDeloitte Access Economics

through the coordinated fostering of growth in both of these groups of industries that thefortunes of the tourism sector will most effectively be advanced.

· The reliance of South Australia’s non-metropolitan regions on intrastate overnight and same-daytravel and the regional development opportunity that lies in the continuing to support growth inthese visitor segments.

· The significant untapped potential of international tourism to regional South Australia. If agreater proportion of international visitors to Adelaide can be encouraged to prolong their stayin South Australia for the purposes of visiting the various regional destinations this would resultin material benefits to regional South Australia’s visitor economy.

As the Australian tourism industry continues its pursuit of the 2020 Stretch Goal (Industry Potential),information and analysis such as that presented in this regional TSA report will provide importantevidence to inform policy and industry decision making and, ultimately, to ensure the industry isappropriately positioned to continue to grow its contribution to the South Australian economy.

Deloitte Access Economics

South Australian Regional Tourism Satellite Accounts 2013-14

1Deloitte Access Economics

1 Introduction1.1 Industry context

Tourism is a valuable contributor to the South Australia economy. The latest state Tourism SatelliteAccount (TSA) published by Tourism Research Australia indicates that in 2013-14 the tourismindustry directly contributed $2.4 billion to South Australia’s economy and directly employedapproximately 32,100 people. As tourism is an industry with strong links to other sectors of theeconomy, the indirect impacts brought the industry’s total contribution to the economy to anestimated $5.3 billion, or 5.9% of gross state product.

Adelaide accounts for approximately 84% of all international visitor nights. The remaining portion isdistributed relatively among the other regions. In terms of domestic visitation, Adelaide accounts for43% of domestic nights to the State. Other popular regions are Fleurieu Peninsula (with iconicvineyards and surf spots), Flinders Ranges and Outback, and the Peninsula region (popular amongAdelaide residents for short trips).

In general, those regions that are closer to Adelaide typically attract more visitors and are expectedto receive relatively more of the indirect flow-on effects from direct tourism trade in Adelaide.

Although Adelaide accounts for the most significant portion of tourism expenditure, tourism isrelatively more important to regional South Australia. That is, expenditure related to tourism ismore significant component of all expenditure that occurs in regional South Australia, thanexpenditure that occurs in Adelaide. While the total quantum of tourism activity in Adelaide issignificant, the city is a large and diverse economy. In contrast, South Australia’s regional economiesare significantly smaller and activity will be more focused around fewer industries.

Going forward, there is growing demand for developing a consistent and reliable set of regional leveltourism contribution estimates to improve the information flow for local investment, planning andpolicy. This is the second time Deloitte Access Economics has used this approach to measuring thecontribution of tourism at a regional level and while this methodology is fairly well developed, theprocess of calculating tourism’s contribution to regions should be part of an ongoing discussion.Thus, the analysis and content presented in this publication should act as a spring board for theongoing evaluation of the impact of tourism on the regional economies in South Australia and theother Australian States and Territories. This information will be critical in guiding tourismdevelopment, investment, planning and policy in South Australia, and Australia more broadly.

1.2 Satellite accountingTourism is a unique industry. Unlike most sectors which are characterised by the nature ofproduction (e.g. mining, manufacturing, agriculture), tourism is characterised by the origin of theconsumers. That is, there exists a range of goods and services that are consumed by both locals andvisitors, with the portion that is consumed by visitors being defined as ‘tourism industry’expenditure. Thus, while all the goods that are produced and consumed in meeting tourism demandare embedded in the System of National Accounts, they are not readily apparent because 'tourism' isnot identified as a conventional production industry.

Satellite accounts are an expansion of the national accounts for selected areas of interest (while stillmaintaining the concepts and structures of the core accounts). Tourism Satellite Accounts (TSAs)evaluate tourism industry performance within a national accounting framework, by combining the

South Australian Regional Tourism Satellite Accounts 2013-14

2Deloitte Access Economics

contribution of each of the products and services that make up the industry. Adherence to nationalaccounting techniques makes it possible for TSA estimates to be compared against conventionalindustries such as mining and manufacturing.

The current State and National TSA estimates are based on an internationally recognised andstandardised methodology that has been set by the United Nations World Tourism Organisation(UNWTO) and endorsed by global peak economic and tourism entities. This approach ensures thatAustralian tourism statistics are reliable, relevant and comparable with the tourism statistics of othernations. The regional estimates presented in this report also adhere to the international framework.

Put simply, a TSA measures the direct and indirect impact of tourism on the economy and includesmetrics such as Gross Value Added (GVA), Gross Regional Product (GRP) and employment. It alsoprovides information about tourism consumption, output, taxation and the composition of thetourism industry and its interaction with other industries.

The 'direct' impact of tourism refers to the contribution generated by trade between the visitor andproducer for a good or service that involves a direct physical or economic relationship (e.g. roomrates and additional services provided to visitors staying in a hotel). 'Indirect' impacts represent theflow-on effects created by the demand for inputs from those industries directly supplying goods andservices to visitors (e.g. the hotel industry requirement for fresh and processed food produce for in-house restaurants, as well as bed linen, towels and room furnishings).

1.2.1 State Tourism Satellite Account

The latest State TSAs were produced by TRA (released in April 2015), is the fourth time TRA hasproduced State TSA since it took over from Centre for Economics and Policy (CEP), in 2010, as theprimary reporting agency on State TSAs.

Deloitte Access Economics understands that the data sources and techniques used by TRA have beenconsistent over the three reporting years. However, prior to 2009-10 the CEP and the CooperativeResearch Centre for Sustainable Tourism (STCRC) produced the State TSAs. The modellingtechniques employed by the CEP and STCRC differ to those adopted by TRA. Thus, pre 2009-10 StateTSAs are not directly comparable to current day issues prepared by TRA.

TRA State TSAs go beyond the scope of the National TSA by measuring both the direct and indirectcontribution of the tourism industry. The direct contribution of tourism is strictly measuredaccording to TSA framework defined by UNWTO. However, because the national framework is notdesigned to measure the indirect contribution of tourism, TRA has introduced a second tier to TSAtechnical standards by estimating the economic impacts of indirect effects using input-output (I-O)benchmark modelling techniques.

1.2.2 Regional Tourism Satellite Accounts

The new suite of Regional TSA measures for each of South Australia’s tourism regions complementsboth the national and state technical standards by ensuring consistency with current TSA practices indirect and indirect quantification. The regional nature of the exercise, however, requires a third tierto be introduced to TSA technical standards in order to appropriately determine cross region andcross border trade flows.

Simply applying an economic multiplier to direct tourism value added at a regional level wouldoverstate the sector’s role in some regions and understate it in others. For example, it wouldoverstate the indirect impacts – and therefore the size of the sector – in regions that do not orcannot supply intermediate tourism industry inputs locally, but rather source them from otherregions.

South Australian Regional Tourism Satellite Accounts 2013-14

3Deloitte Access Economics

Effectively and accurately accounting for cross-region trade flows is challenging as reliable data oninter-regional trade arrangements is not currently maintained. Economic models – known as gravitymodels – are typically employed and currently regarded as a best practice approach.

Gravity modelling is a widely applied and empirically tested economic technique to estimating cross-regional trade flows when confronted with incomplete data. The framework is based on economicdemand and supply theory for each commodity, and is impacted by the distance between tworegions as a barrier to trade (e.g. regions with an oversupply of processed foods are more likely toprovide these goods to bordering or closely proximate regions with an excess demand for processedfoods). Deloitte Access Economics employed a gravity modelling technique to develop a concise setof benchmark multipliers that reflect bi-lateral trade flows between South Australia’s regions.

1.3 Accounting conceptsThere are a number of complex steps required to calculate the tourism industry's contribution to aregional economy. Each step is briefly summarised in the following:

1. Derive estimated domestic and international tourism consumption by tourism characteristicexpenditure item . The richest source of data relating to economic activity in the tourismsector is the expenditure patterns of visitors in terms of how much they spend and what theypurchase. The gap in the information is where in Australia the good was purchased. Thus,some manipulation of the available data is required to develop robust regional expenditureprofiles.

2. Isolate taxes and subsidies, and cost of imports sold directly to tourists to derive a ‘clean’profile of tourism consumption at basic prices . The ABS National Accounts: Input-OutputTables (Product Details) (Cat. No. 5215.055.001) contains household final consumption byproduct information, at purchasers’ prices and basic prices, and includes details on net taxes,imports and margins at this level. This Input-Output Product Classification (IOPC) can bedirectly (one-to-one) mapped to tourism characteristic and connected products.

3. Link each of the tourism characteristic (and connected) products to conventional,production-defined industries. That is, to effectively estimate the size of the tourismindustry’s contribution to the economy at a given geographical level requires mapping eachconsumption item to ABS ANZSIC defined production industries. In some cases this is clear cut(e.g. expenditure on hotel accommodation); in others it is not (e.g. expenditure onentertainment and recreation is often poorly defined).

4. Exclude the supply of goods by producers who do not have a direct relationship withconsumers (i.e. cost to retailers of domestic goods sold directly to visitors, including wholesaleand transport margins) using benchmark ratios (derived from ABS input-output (I-O) tables) toderive direct tourism output.

5. Distribute direct tourism output across related supply industries using regional input-outputmultiplier tables, to derive direct tourism value added, regional product and employment .The direct tourism contribution is summed across all industries to calculate the tourismindustry’s contribution to the regional economy.

6. Finally, indirect impacts must also be appropriately represented . At the regional level this is acomplex issue due to the need to account for cross-region trade flows. Simply applying aneconomic multiplier to direct tourism consumption at a regional level would overstate thesector’s role in some regions and understate it in others. To account for these systemdynamics, Deloitte Access Economics has employed a gravity modelling approach to define amatrix of benchmark ratios for deriving indirect effects.

South Australian Regional Tourism Satellite Accounts 2013-14

4Deloitte Access Economics

For consistency and assurance, the regional results are calibrated against the reported 2013-14 StateTSA data for each key output.

Caveat: in order to produce estimates at such a detailed level of granularity, a numberof data manipulations and assumptions are made. The assumptions underlying themodel may have some effect on the quality of the outputs. To limit the potentialimpact, Deloitte Access Economics has employed best practice accounting techniquesand the best available data to provide a robust set of TSA estimates.

For a more detailed understanding of the underlying methodology and concepts to regional tourismsatellite accounting, please refer to the Regional Tourism Satellite Account: Specification Documentand the glossary of terms at the back of this report .

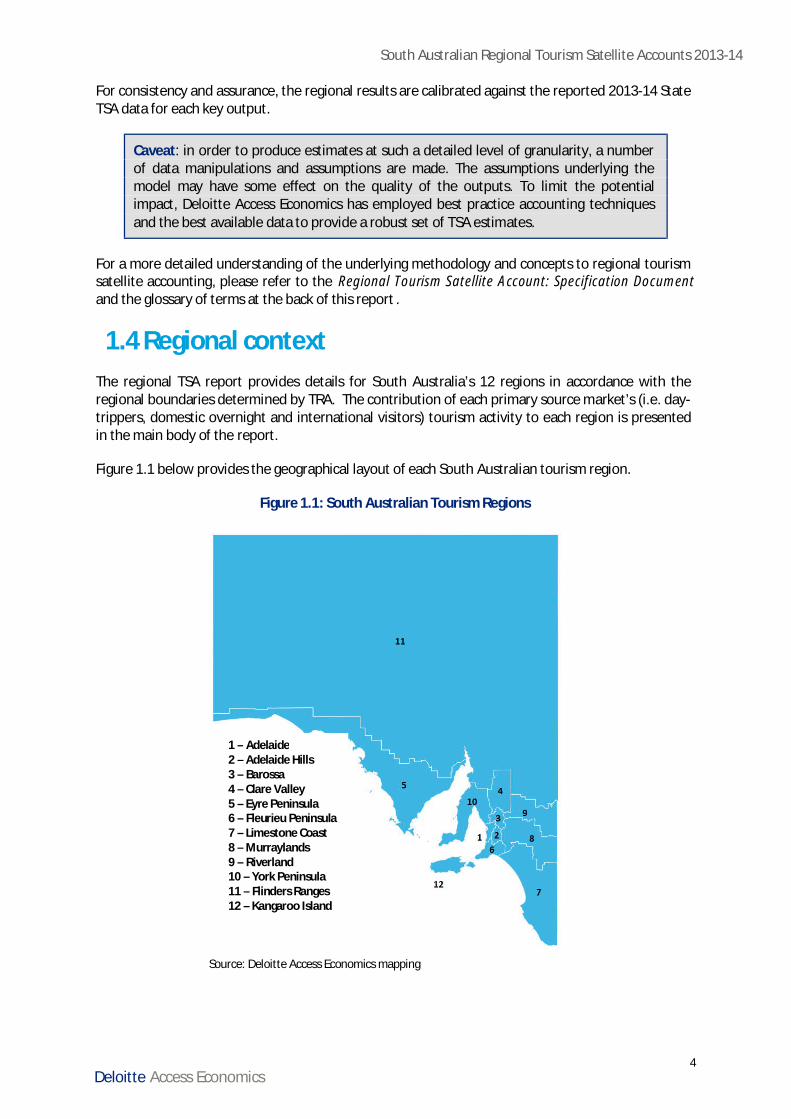

1.4 Regional contextThe regional TSA report provides details for South Australia’s 12 regions in accordance with theregional boundaries determined by TRA. The contribution of each primary source market’s (i.e. day-trippers, domestic overnight and international visitors) tourism activity to each region is presentedin the main body of the report.

Figure 1.1 below provides the geographical layout of each South Australian tourism region.

Figure 1.1: South Australian Tourism Regions

Source: Deloitte Access Economics mapping

1 – Adelaide2 – Adelaide Hills3 – Barossa4 – Clare Valley5 – Eyre Peninsula6 – Fleurieu Peninsula7 – Limestone Coast8 – Murraylands9 – Riverland10 – York Peninsula11 – Flinders Ranges12 – Kangaroo Island

South Australian Regional Tourism Satellite Accounts 2013-14

5Deloitte Access Economics

1.5 Report structureThe remainder of the report is structured as follows:· Section 2: Summary of results : Summarises the key economic aggregates for tourism industry

activity in South Australia’s regions, and provides a ranking of the relative importance oftourism’s contribution to each of the regions.

· Section 3: Key trends in tourism : presents the key historical trends in tourism’s contribution toSouth Australia’s tourism regions, between 2006-07 and 2013-14.

· Section 4: Regional profiles : presents regional profiles for each of the State’s regions. Eachregional profile draws together the key outcomes for tourism’s contribution to the economy in asuccinct, standalone report.

· Appendices: Provides supporting information for the TSA methodology, concepts and definitionsof economic terms.

South Australian Regional Tourism Satellite Accounts 2013-14

6Deloitte Access Economics

2 Summary of ResultsThe primary goal of the research is to quantify the economic contribution of tourism, both direct andindirect, to each region in South Australia for the 2013-14 financial year. The estimates of tourismcontribution presented in this report are in 2013-14 prices. The key indicators presented are:· Gross Regional Product (GRP);· Gross Value Added (GVA);· Employment (both part time and full time employed persons); and· Tourism consumption and output.

For further information on how these indicators are defined, refer to the glossary at the back of thisreport.

2.1 Key tourism aggregatesIn 2013-14 tourism consumption in South Australia totalled $6.7 billion, with Adelaide contributing55% or $3.6 billion and regional South Australia contributing the remaining 45% or $3.0 billion. Thisconsumption generated:· $2.9 billion and $2.2 billion in direct and indirect tourism output, producing $5.1 billion in total

contribution to Adelaide; and $1.4 billion and $3.6 billion in direct and indirect tourism output,producing $5.0 billion in total contribution to regional South Australia;

· $1.5 billion and $0.9 billion in direct and indirect tourism GVA, producing $2.4 billion in totalcontribution to Adelaide; and $0.7 billion and $1.5 billion in direct and indirect tourism GVA,producing $2.2 billion in total contribution to regional South Australia

· $1.6 billion and $1.1 billion in direct and indirect tourism GRP, producing $2.7 billion in totalcontribution to Adelaide; and $0.8 billion and $1.7 billion in direct and indirect tourism GRP,producing $2.5 billion in total contribution to regional South Australia; and

· 20,400 jobs for people employed directly by the tourism industry in Adelaide, with 9,000indirect jobs and a total employment impact in Adelaide of 29,400 people; plus 11,700 jobs forpeople employed directly by the tourism industry in regional South Australia, with 14,900indirect jobs and a total employment impact in regional South Australia of 26,600 people.

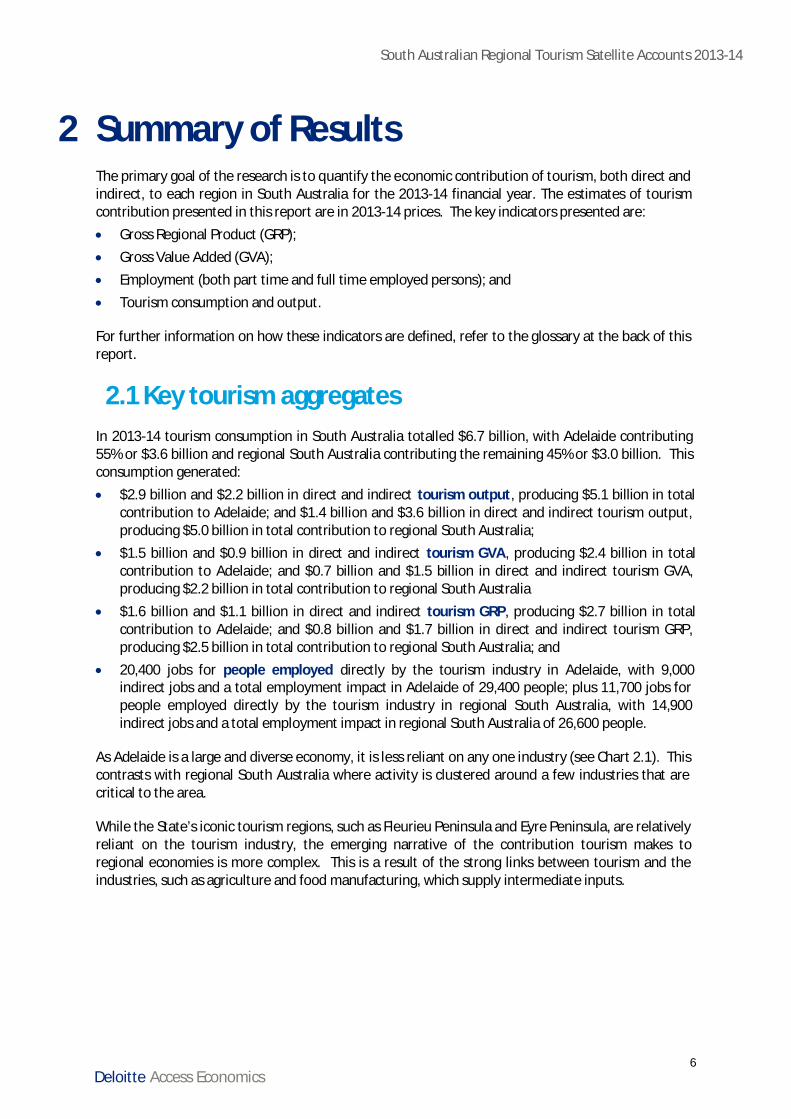

As Adelaide is a large and diverse economy, it is less reliant on any one industry (see Chart 2.1). Thiscontrasts with regional South Australia where activity is clustered around a few industries that arecritical to the area.

While the State’s iconic tourism regions, such as Fleurieu Peninsula and Eyre Peninsula, are relativelyreliant on the tourism industry, the emerging narrative of the contribution tourism makes toregional economies is more complex. This is a result of the strong links between tourism and theindustries, such as agriculture and food manufacturing, which supply intermediate inputs.

South Australian Regional Tourism Satellite Accounts 2013-14

7Deloitte Access Economics

Chart 2.1: Tourism contribution to Adelaide and South Australian regional economies, 2013-14

Source: Deloitte Access Economics’ Regional TSA model.

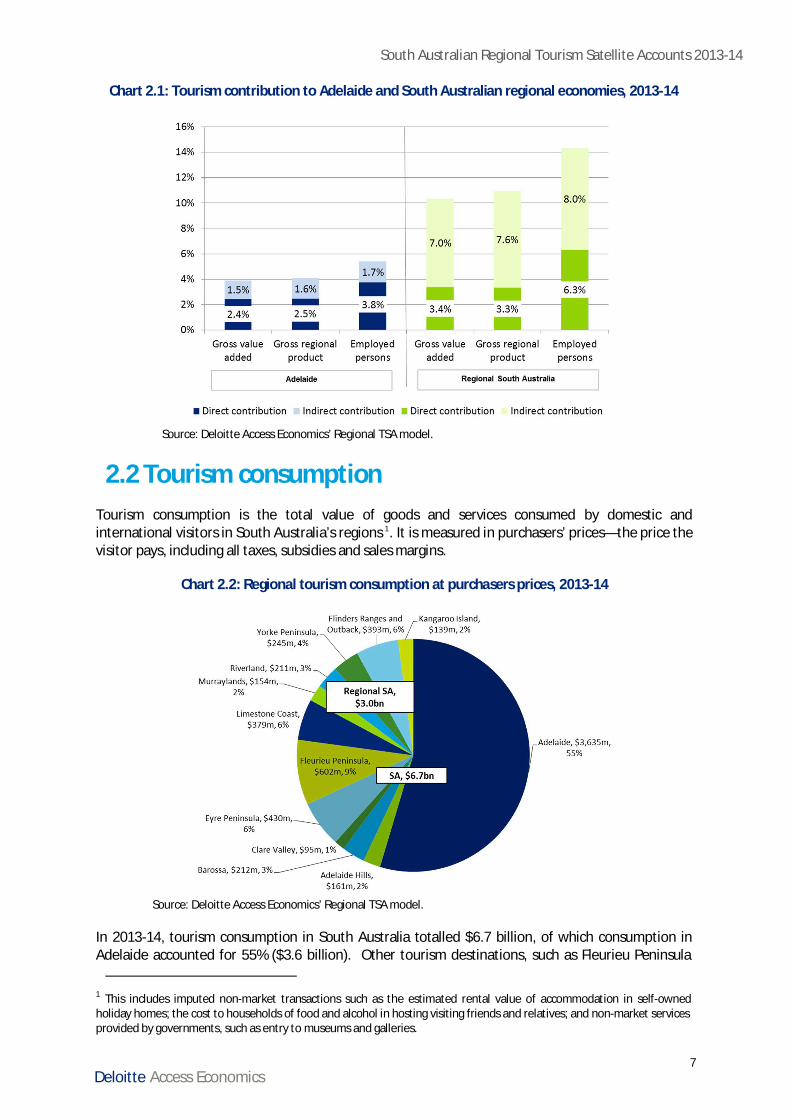

2.2 Tourism consumptionTourism consumption is the total value of goods and services consumed by domestic andinternational visitors in South Australia’s regions 1. It is measured in purchasers’ prices—the price thevisitor pays, including all taxes, subsidies and sales margins.

Chart 2.2: Regional tourism consumption at purchasers prices, 2013-14

Source: Deloitte Access Economics’ Regional TSA model.

In 2013-14, tourism consumption in South Australia totalled $6.7 billion, of which consumption inAdelaide accounted for 55% ($3.6 billion). Other tourism destinations, such as Fleurieu Peninsula

1 This includes imputed non-market transactions such as the estimated rental value of accommodation in self-ownedholiday homes; the cost to households of food and alcohol in hosting visiting friends and relatives; and non-market servicesprovided by governments, such as entry to museums and galleries.

South Australian Regional Tourism Satellite Accounts 2013-14

8Deloitte Access Economics

(9% or $0.6 billion), Flinders Ranges and Outback (6% or $0.4 billion), Eyre Peninsula (6% or $0.4billion) and Limestone Coast (6% or $0.4 billion) made up the bulk of the remaining consumption.

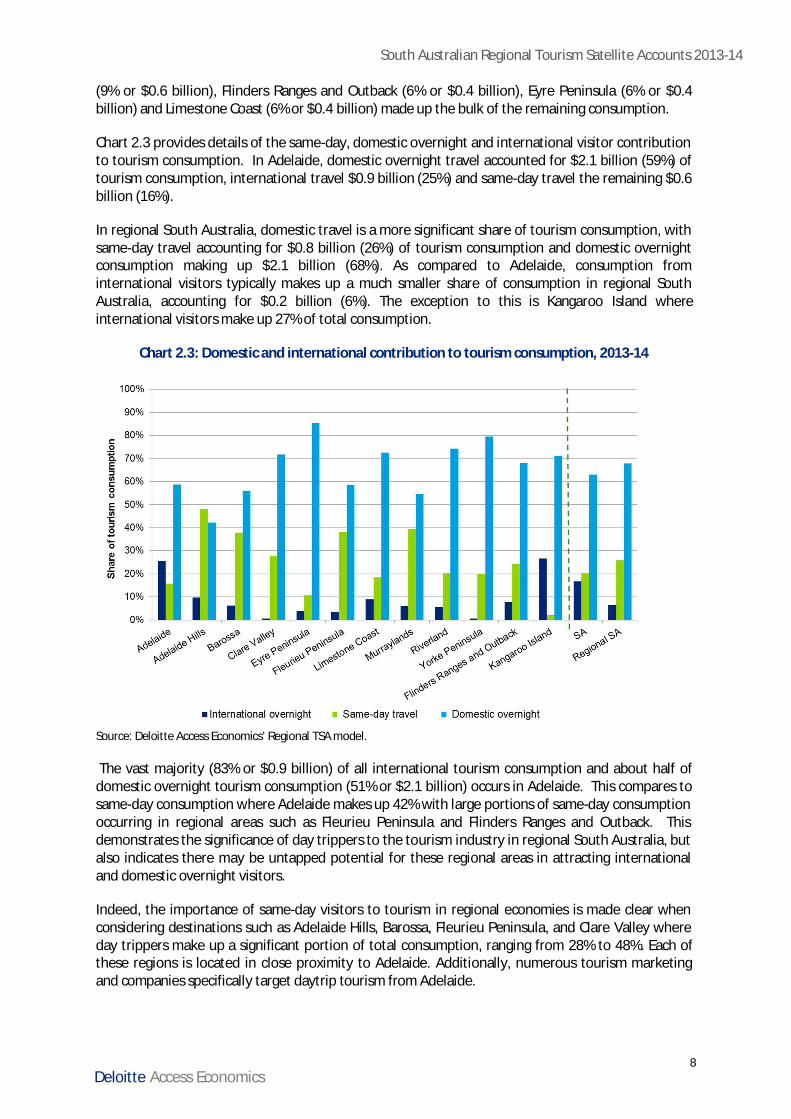

Chart 2.3 provides details of the same-day, domestic overnight and international visitor contributionto tourism consumption. In Adelaide, domestic overnight travel accounted for $2.1 billion (59%) oftourism consumption, international travel $0.9 billion (25%) and same-day travel the remaining $0.6billion (16%).

In regional South Australia, domestic travel is a more significant share of tourism consumption, withsame-day travel accounting for $0.8 billion (26%) of tourism consumption and domestic overnightconsumption making up $2.1 billion (68%). As compared to Adelaide, consumption frominternational visitors typically makes up a much smaller share of consumption in regional SouthAustralia, accounting for $0.2 billion (6%). The exception to this is Kangaroo Island whereinternational visitors make up 27% of total consumption.

Chart 2.3: Domestic and international contribution to tourism consumption, 2013-14

Source: Deloitte Access Economics’ Regional TSA model.

The vast majority (83% or $0.9 billion) of all international tourism consumption and about half ofdomestic overnight tourism consumption (51% or $2.1 billion) occurs in Adelaide. This compares tosame-day consumption where Adelaide makes up 42% with large portions of same-day consumptionoccurring in regional areas such as Fleurieu Peninsula and Flinders Ranges and Outback. Thisdemonstrates the significance of day trippers to the tourism industry in regional South Australia, butalso indicates there may be untapped potential for these regional areas in attracting internationaland domestic overnight visitors.

Indeed, the importance of same-day visitors to tourism in regional economies is made clear whenconsidering destinations such as Adelaide Hills, Barossa, Fleurieu Peninsula, and Clare Valley whereday trippers make up a significant portion of total consumption, ranging from 28% to 48%. Each ofthese regions is located in close proximity to Adelaide. Additionally, numerous tourism marketingand companies specifically target daytrip tourism from Adelaide.

South Australian Regional Tourism Satellite Accounts 2013-14

9Deloitte Access Economics

At the sectoral level, the tourism characteristic and connected products that tended to contributemost to tourism consumption in South Australia’s regions in 2013-14 were:· Takeaway and restaurant meals (making up 14% of consumption in Adelaide and 16% for

regional South Australia on average);· Long distance passenger transportation (ranging from 10% of consumption in Adelaide Hills to

21% in Kangaroo Island; 17% for Adelaide and 15% regional South Australia); and· Shopping (ranging from 10% of consumption in Eyre Peninsula to 15% in Adelaide Hills; 11% in

Adelaide and 12% average for regional South Australia);

Along with fuel and accommodation services, these tourism characteristic and connected productswere the most prominent across all of South Australia’s regions. However, the ranking of thesesectors varied from region to region.

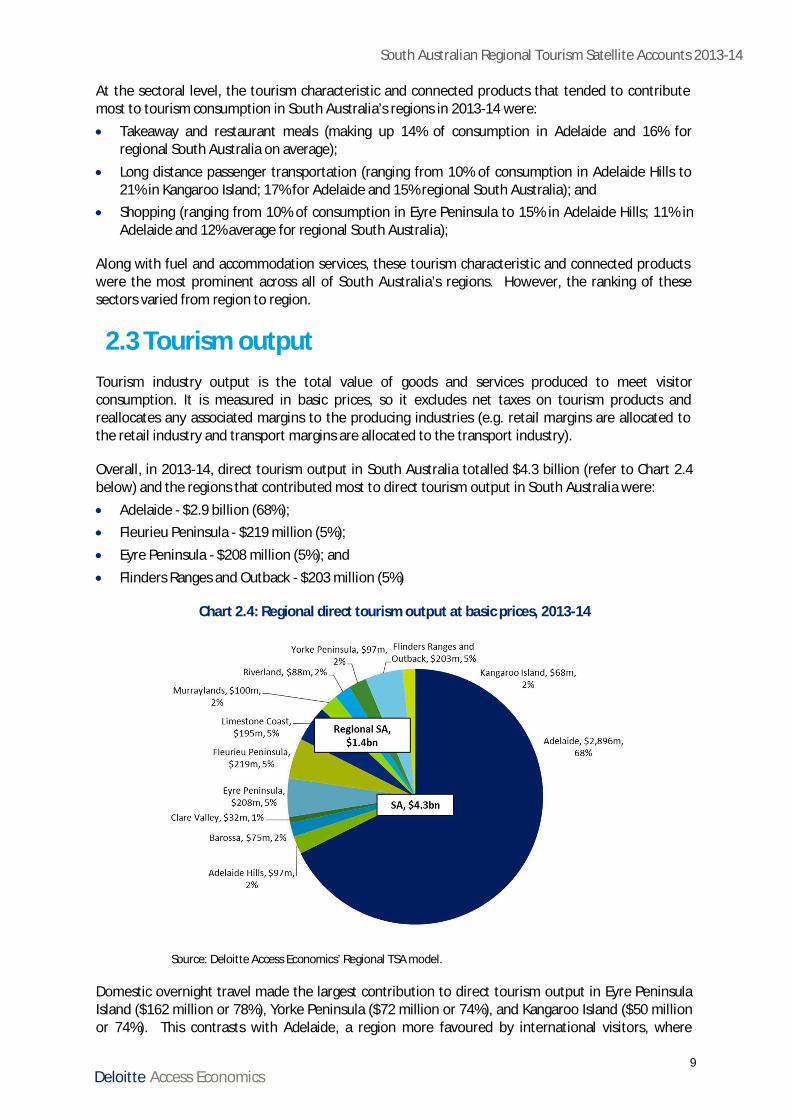

2.3 Tourism outputTourism industry output is the total value of goods and services produced to meet visitorconsumption. It is measured in basic prices, so it excludes net taxes on tourism products andreallocates any associated margins to the producing industries (e.g. retail margins are allocated tothe retail industry and transport margins are allocated to the transport industry).

Overall, in 2013-14, direct tourism output in South Australia totalled $4.3 billion (refer to Chart 2.4below) and the regions that contributed most to direct tourism output in South Australia were:· Adelaide - $2.9 billion (68%);· Fleurieu Peninsula - $219 million (5%);· Eyre Peninsula - $208 million (5%); and· Flinders Ranges and Outback - $203 million (5%)

Chart 2.4: Regional direct tourism output at basic prices, 2013-14

Source: Deloitte Access Economics’ Regional TSA model.

Domestic overnight travel made the largest contribution to direct tourism output in Eyre PeninsulaIsland ($162 million or 78%), Yorke Peninsula ($72 million or 74%), and Kangaroo Island ($50 millionor 74%). This contrasts with Adelaide, a region more favoured by international visitors, where

South Australian Regional Tourism Satellite Accounts 2013-14

10Deloitte Access Economics

domestic overnight visitors made up 65% of direct tourism output. Overall, regional SouthAustralia’s tourism output is more heavily reliant on domestic overnight visitors (69%) and same-dayvisitors (17%) than Adelaide.

At the industry level, the tourism industries that tended to contribute most to total direct tourismoutput in South Australia’s regions in 2013-14 were:· Air, water and other transport (ranging from 35% of direct output in Kangaroo Island to 1% in

Clare Valley; 13% for regional South Australia on average and 20% for South Australia as awhole);

· Accommodation (ranging from 38% of direct output in Clare Valley to 6% in Adelaide Hills; 22%in regional South Australia on average and 14% in South Australia as a whole); and

· Cafes, restaurants and takeaway food services (ranging from 28% of direct output in AdelaideHills to 11% in Kangaroo Island; 17% for regional South Australia on average and 14% for SouthAustralia as a whole);

Along with retail trade, these tourism characteristic and connected industries were the mostprominent across all South Australia’s tourism sub-regions. However, the ranking of these industrieswithin regions varies; depending on the area’s characteristics and geographical location. Forexample, the café, restaurants and takeaway food services industry ranks above air, water and othertransport in Adelaide Hills, Barossa and Clare Valley based on these regions proximity to Adelaide aswell as their status as renowned food and wine destinations.

Indirect output from tourism spend in South Australia’s regions contributed a further $5.9 billion inSouth Australia and $140 million to the Rest of Australia in 2013-14. Adelaide ($2.2 billion or 38%),Fleurieu Peninsula ($518 million or 9%), and Adelaide Hills ($423 million or 7%) were the highestcontributors to indirect tourism output. Interestingly, while Adelaide accounted for nearly 70% ofdirect tourism output, the vast majority of indirect tourism output (62%) was from regional SouthAustralia. This demonstrates the importance of regionally located secondary industries to thetourism industry in South Australia.

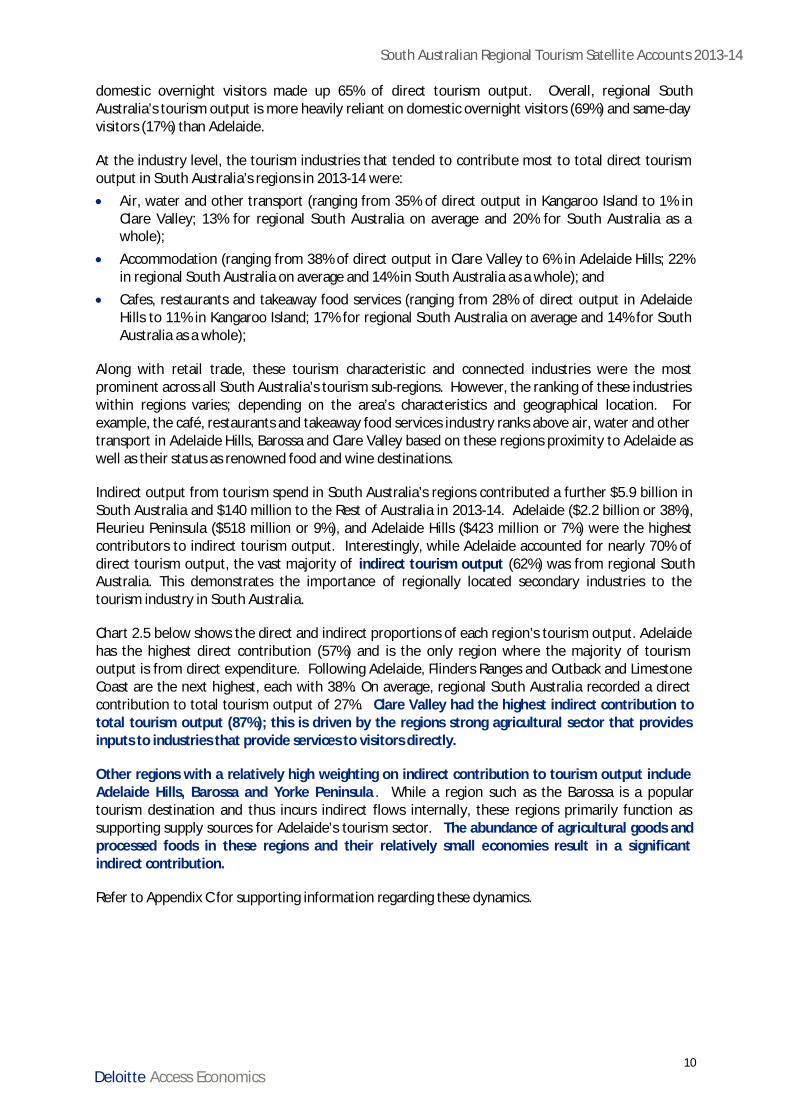

Chart 2.5 below shows the direct and indirect proportions of each region’s tourism output. Adelaidehas the highest direct contribution (57%) and is the only region where the majority of tourismoutput is from direct expenditure. Following Adelaide, Flinders Ranges and Outback and LimestoneCoast are the next highest, each with 38%. On average, regional South Australia recorded a directcontribution to total tourism output of 27%. Clare Valley had the highest indirect contribution tototal tourism output (87%); this is driven by the regions strong agricultural sector that providesinputs to industries that provide services to visitors directly.

Other regions with a relatively high weighting on indirect contribution to tourism output includeAdelaide Hills, Barossa and Yorke Peninsula . While a region such as the Barossa is a populartourism destination and thus incurs indirect flows internally, these regions primarily function assupporting supply sources for Adelaide’s tourism sector. The abundance of agricultural goods andprocessed foods in these regions and their relatively small economies result in a significantindirect contribution.

Refer to Appendix C for supporting information regarding these dynamics.

South Australian Regional Tourism Satellite Accounts 2013-14

11Deloitte Access Economics

Chart 2.5: Relative contribution of direct and indirect tourism output, 2013-14

Source: Deloitte Access Economics’ Regional TSA model.

2.4 Tourism Gross Value AddedTourism GVA is considered the most accurate measure of the contribution of tourism to aneconomy. It includes the total labour income and revenue attributable to the industry, less net taxespaid on products and is measured in basic prices.

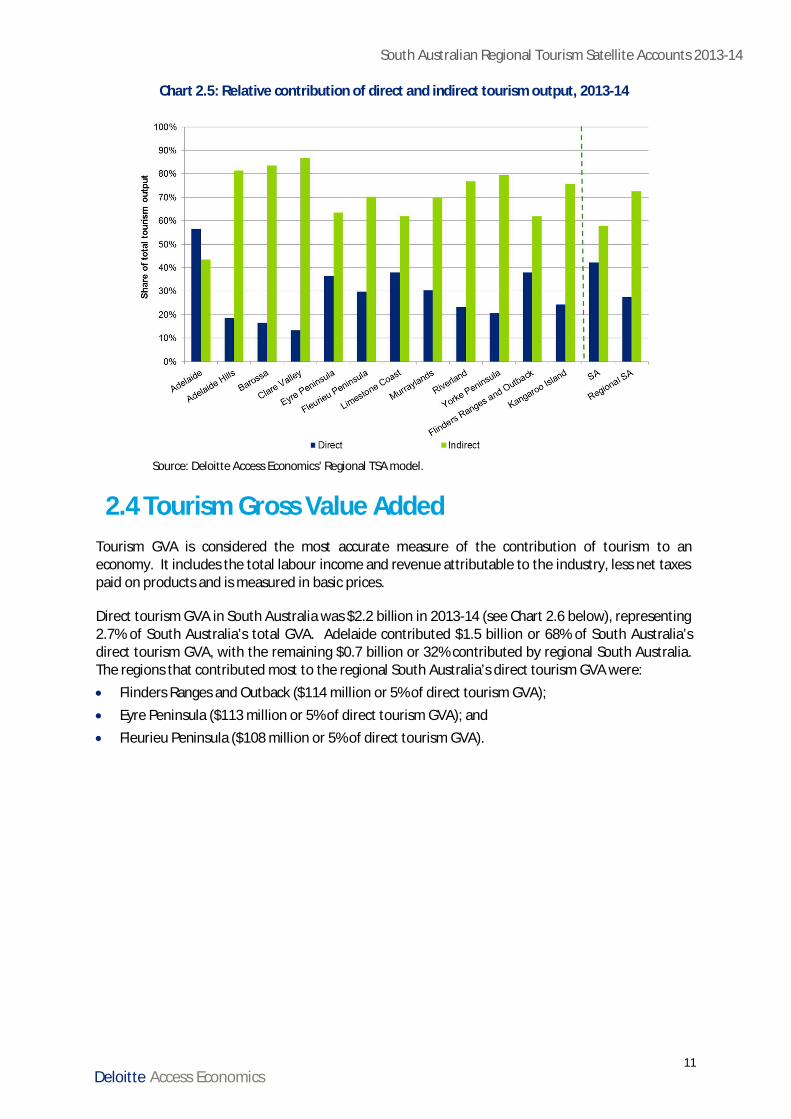

Direct tourism GVA in South Australia was $2.2 billion in 2013-14 (see Chart 2.6 below), representing2.7% of South Australia’s total GVA. Adelaide contributed $1.5 billion or 68% of South Australia’sdirect tourism GVA, with the remaining $0.7 billion or 32% contributed by regional South Australia.The regions that contributed most to the regional South Australia’s direct tourism GVA were:· Flinders Ranges and Outback ($114 million or 5% of direct tourism GVA);· Eyre Peninsula ($113 million or 5% of direct tourism GVA); and· Fleurieu Peninsula ($108 million or 5% of direct tourism GVA).

South Australian Regional Tourism Satellite Accounts 2013-14

12Deloitte Access Economics

Chart 2.6: Regional direct tourism GVA at basic prices, 2013-14

Source: Deloitte Access Economics’ Regional TSA model.

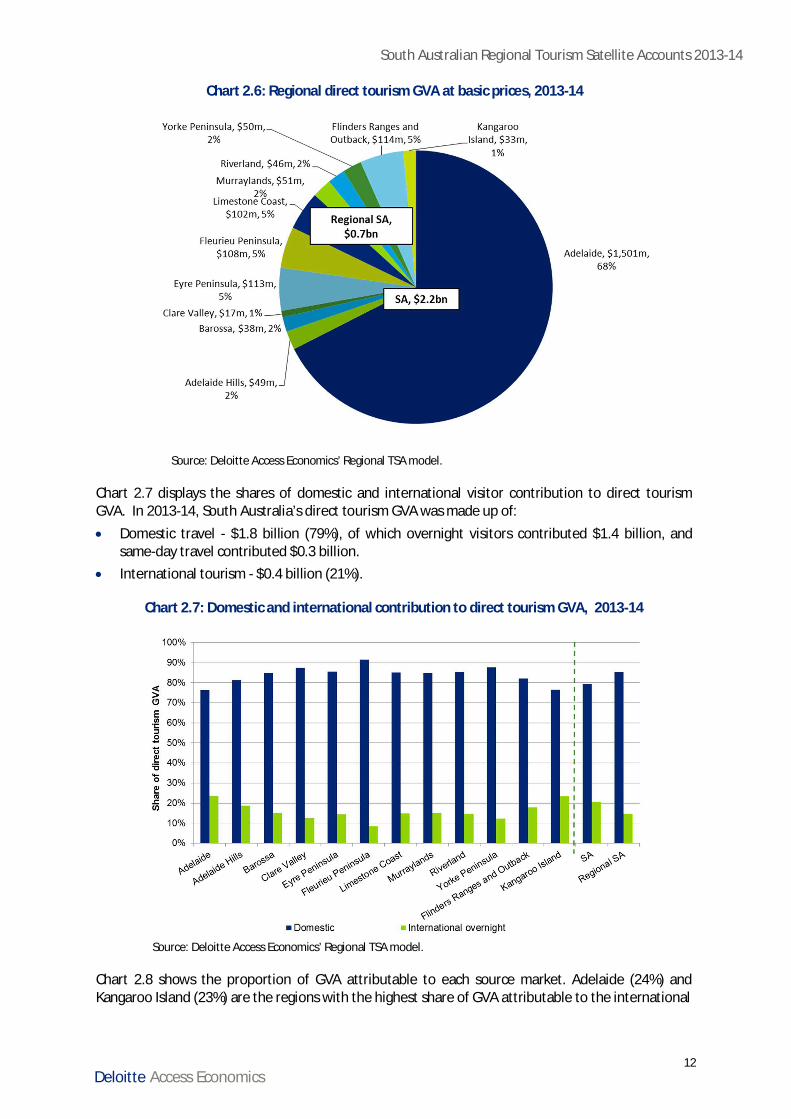

Chart 2.7 displays the shares of domestic and international visitor contribution to direct tourismGVA. In 2013-14, South Australia’s direct tourism GVA was made up of:· Domestic travel - $1.8 billion (79%), of which overnight visitors contributed $1.4 billion, and

same-day travel contributed $0.3 billion.· International tourism - $0.4 billion (21%).

Chart 2.7: Domestic and international contribution to direct tourism GVA, 2013-14

Source: Deloitte Access Economics’ Regional TSA model.

Chart 2.8 shows the proportion of GVA attributable to each source market. Adelaide (24%) andKangaroo Island (23%) are the regions with the highest share of GVA attributable to the international

South Australian Regional Tourism Satellite Accounts 2013-14

13Deloitte Access Economics

segment. Overall, same-day travel and domestic overnight travel is a larger share of direct GVA inregional South Australia than in Adelaide.

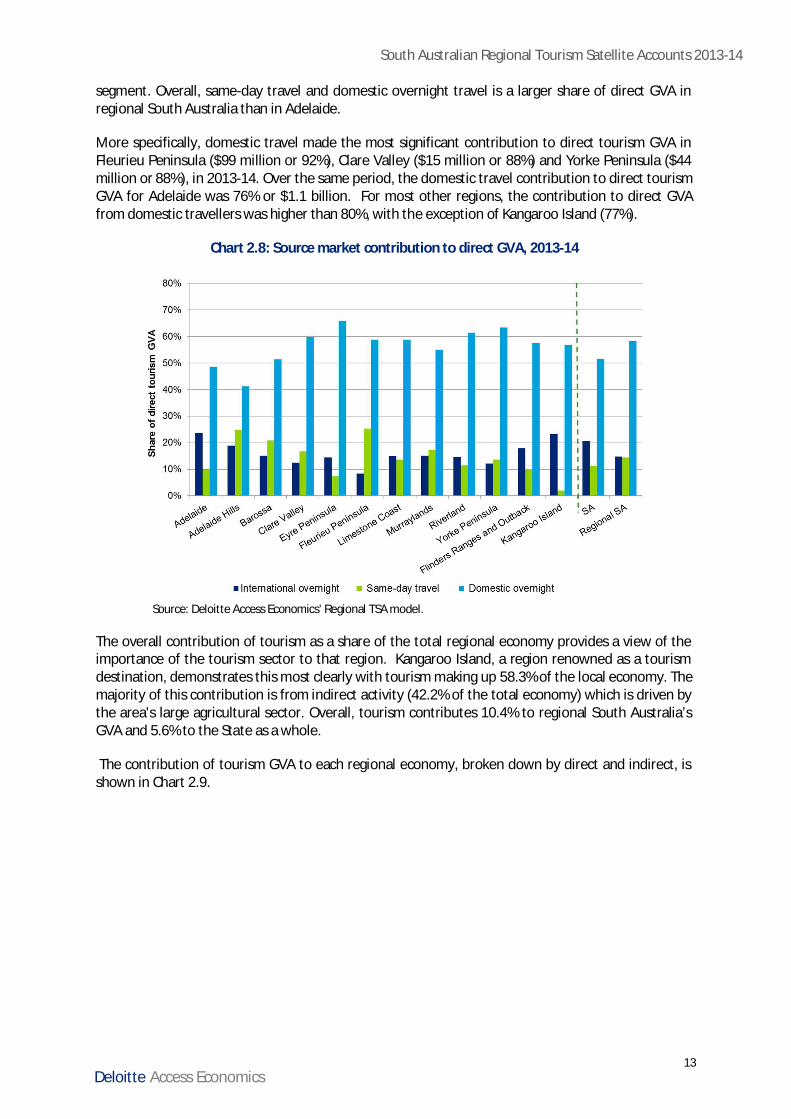

More specifically, domestic travel made the most significant contribution to direct tourism GVA inFleurieu Peninsula ($99 million or 92%), Clare Valley ($15 million or 88%) and Yorke Peninsula ($44million or 88%), in 2013-14. Over the same period, the domestic travel contribution to direct tourismGVA for Adelaide was 76% or $1.1 billion. For most other regions, the contribution to direct GVAfrom domestic travellers was higher than 80%, with the exception of Kangaroo Island (77%).

Chart 2.8: Source market contribution to direct GVA, 2013-14

Source: Deloitte Access Economics’ Regional TSA model.

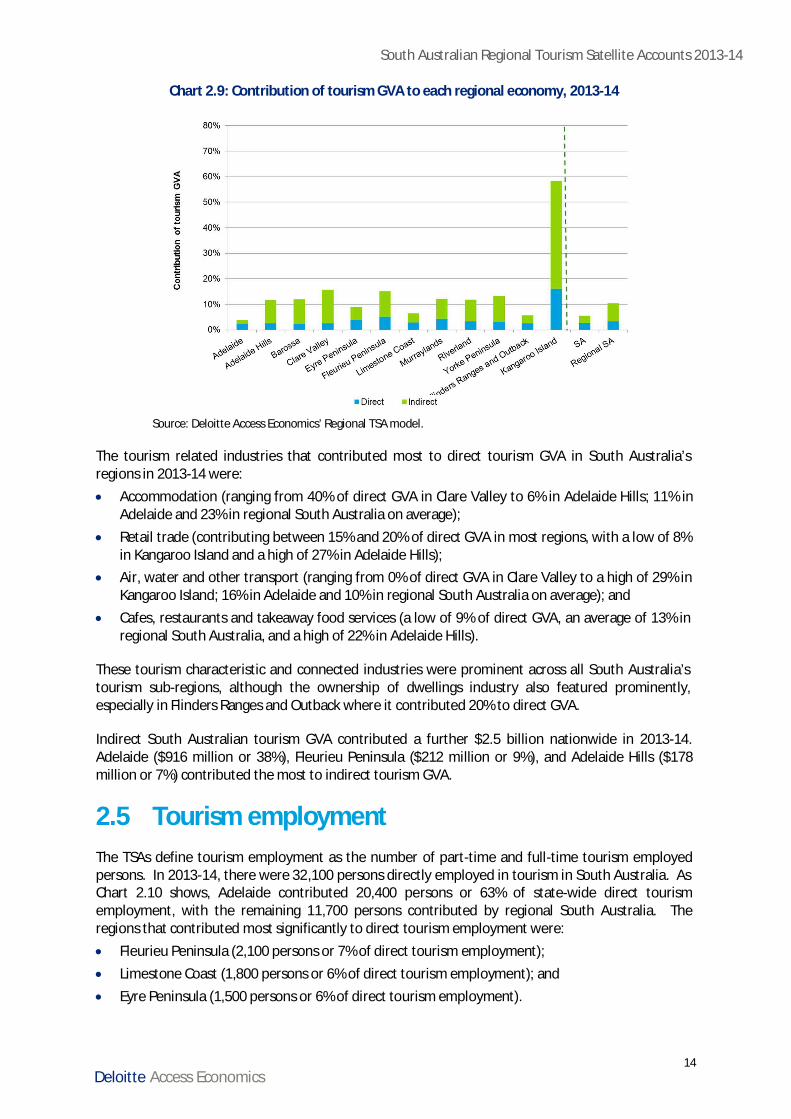

The overall contribution of tourism as a share of the total regional economy provides a view of theimportance of the tourism sector to that region. Kangaroo Island, a region renowned as a tourismdestination, demonstrates this most clearly with tourism making up 58.3% of the local economy. Themajority of this contribution is from indirect activity (42.2% of the total economy) which is driven bythe area’s large agricultural sector. Overall, tourism contributes 10.4% to regional South Australia’sGVA and 5.6% to the State as a whole.

The contribution of tourism GVA to each regional economy, broken down by direct and indirect, isshown in Chart 2.9.

South Australian Regional Tourism Satellite Accounts 2013-14

14Deloitte Access Economics

Chart 2.9: Contribution of tourism GVA to each regional economy, 2013-14

Source: Deloitte Access Economics’ Regional TSA model.

The tourism related industries that contributed most to direct tourism GVA in South Australia’sregions in 2013-14 were:· Accommodation (ranging from 40% of direct GVA in Clare Valley to 6% in Adelaide Hills; 11% in

Adelaide and 23% in regional South Australia on average);· Retail trade (contributing between 15% and 20% of direct GVA in most regions, with a low of 8%

in Kangaroo Island and a high of 27% in Adelaide Hills);· Air, water and other transport (ranging from 0% of direct GVA in Clare Valley to a high of 29% in

Kangaroo Island; 16% in Adelaide and 10% in regional South Australia on average); and· Cafes, restaurants and takeaway food services (a low of 9% of direct GVA, an average of 13% in

regional South Australia, and a high of 22% in Adelaide Hills).

These tourism characteristic and connected industries were prominent across all South Australia’stourism sub-regions, although the ownership of dwellings industry also featured prominently,especially in Flinders Ranges and Outback where it contributed 20% to direct GVA.

Indirect South Australian tourism GVA contributed a further $2.5 billion nationwide in 2013-14.Adelaide ($916 million or 38%), Fleurieu Peninsula ($212 million or 9%), and Adelaide Hills ($178million or 7%) contributed the most to indirect tourism GVA.

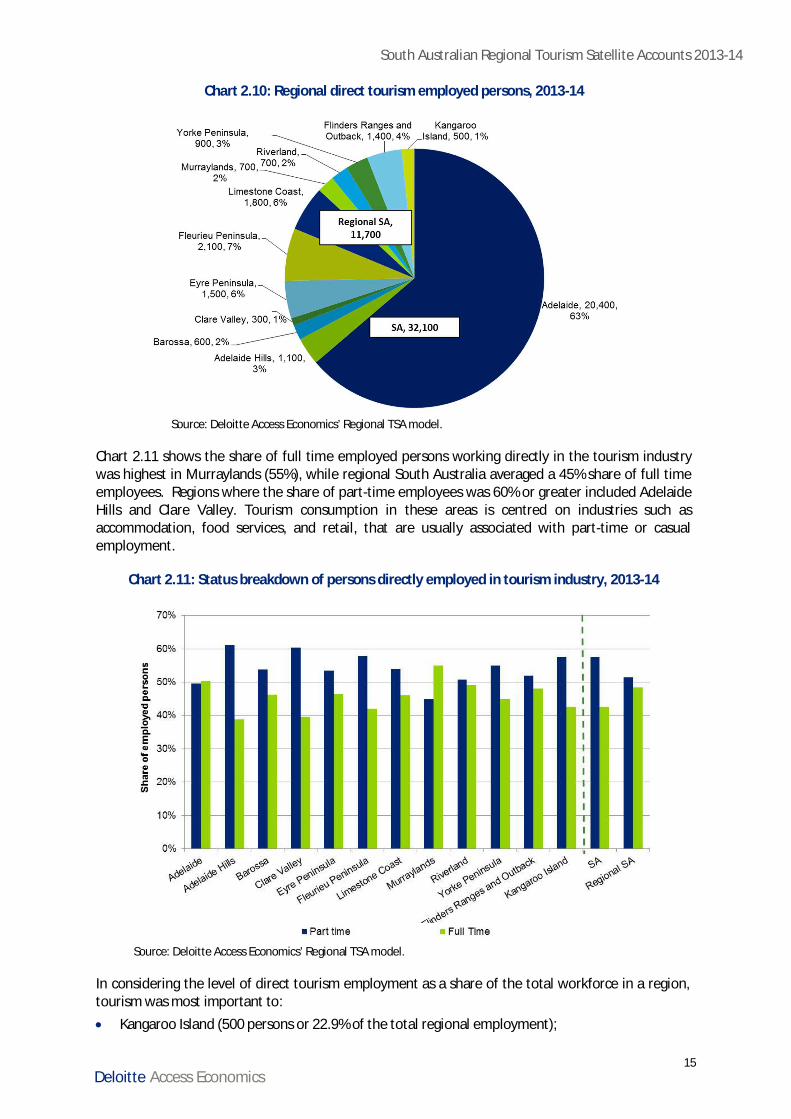

2.5 Tourism employmentThe TSAs define tourism employment as the number of part-time and full-time tourism employedpersons. In 2013-14, there were 32,100 persons directly employed in tourism in South Australia. AsChart 2.10 shows, Adelaide contributed 20,400 persons or 63% of state-wide direct tourismemployment, with the remaining 11,700 persons contributed by regional South Australia. Theregions that contributed most significantly to direct tourism employment were:· Fleurieu Peninsula (2,100 persons or 7% of direct tourism employment);· Limestone Coast (1,800 persons or 6% of direct tourism employment); and· Eyre Peninsula (1,500 persons or 6% of direct tourism employment).

South Australian Regional Tourism Satellite Accounts 2013-14

15Deloitte Access Economics

Chart 2.10: Regional direct tourism employed persons, 2013-14

Source: Deloitte Access Economics’ Regional TSA model.

Chart 2.11 shows the share of full time employed persons working directly in the tourism industrywas highest in Murraylands (55%), while regional South Australia averaged a 45% share of full timeemployees. Regions where the share of part-time employees was 60% or greater included AdelaideHills and Clare Valley. Tourism consumption in these areas is centred on industries such asaccommodation, food services, and retail, that are usually associated with part-time or casualemployment.

Chart 2.11: Status breakdown of persons directly employed in tourism industry, 2013-14

Source: Deloitte Access Economics’ Regional TSA model.

In considering the level of direct tourism employment as a share of the total workforce in a region,tourism was most important to:· Kangaroo Island (500 persons or 22.9% of the total regional employment);

South Australian Regional Tourism Satellite Accounts 2013-14

16Deloitte Access Economics

· Fleurieu Peninsula (2,100 persons or 9.5% of the total regional employment); and· Yorke Peninsula (900 persons or 6.6% of the total regional employment).

While employment in the following economies was relatively less reliant on the tourism industry:· Adelaide (20,400 persons or 3.8% of the total regional employment); and· Barossa (600 persons or 4.3% of the total regional employment).

Additionally, a further 9,000 and 14,900 people were employed indirectly in Adelaide and regionalSouth Australia respectively – with a further 600 indirectly employed throughout the Rest ofAustralia - as a result of supply services to tourism industry activity in 2013-14. Combined withdirect tourism employment, this represented total employment from tourism of 29,400 or 5.4% ofall employment in Adelaide and 26,600 or 14.3% of total employment in regional South Australia.

South Australian Regional Tourism Satellite Accounts 2013-14

17Deloitte Access Economics

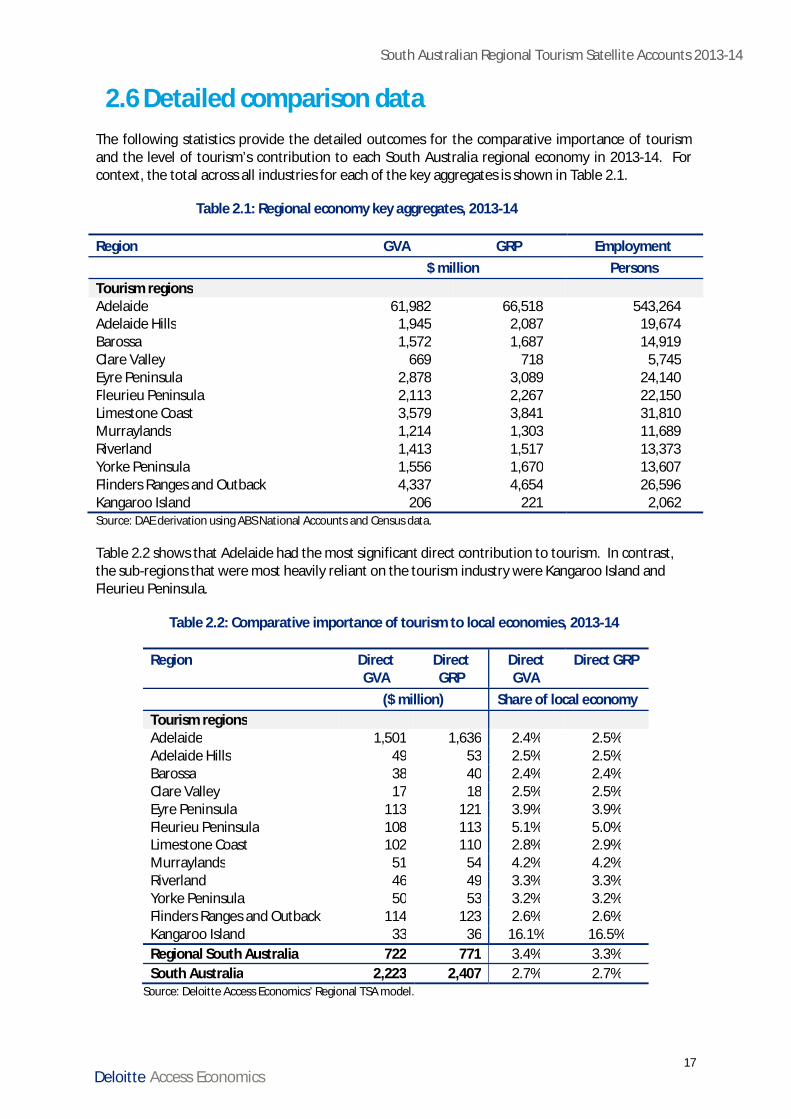

2.6 Detailed comparison dataThe following statistics provide the detailed outcomes for the comparative importance of tourismand the level of tourism’s contribution to each South Australia regional economy in 2013-14. Forcontext, the total across all industries for each of the key aggregates is shown in Table 2.1.

Table 2.1: Regional economy key aggregates, 2013-14

Region GVA GRP Employment $ million PersonsTourism regionsAdelaide 61,982 66,518 543,264Adelaide Hills 1,945 2,087 19,674Barossa 1,572 1,687 14,919Clare Valley 669 718 5,745Eyre Peninsula 2,878 3,089 24,140Fleurieu Peninsula 2,113 2,267 22,150Limestone Coast 3,579 3,841 31,810Murraylands 1,214 1,303 11,689Riverland 1,413 1,517 13,373Yorke Peninsula 1,556 1,670 13,607Flinders Ranges and Outback 4,337 4,654 26,596Kangaroo Island 206 221 2,062Source: DAE derivation using ABS National Accounts and Census data.

Table 2.2 shows that Adelaide had the most significant direct contribution to tourism. In contrast,the sub-regions that were most heavily reliant on the tourism industry were Kangaroo Island andFleurieu Peninsula.

Table 2.2: Comparative importance of tourism to local economies, 2013-14

Region DirectGVA

DirectGRP

DirectGVA

Direct GRP

($ million) Share of local economyTourism regionsAdelaide 1,501 1,636 2.4% 2.5%Adelaide Hills 49 53 2.5% 2.5%Barossa 38 40 2.4% 2.4%Clare Valley 17 18 2.5% 2.5%Eyre Peninsula 113 121 3.9% 3.9%Fleurieu Peninsula 108 113 5.1% 5.0%Limestone Coast 102 110 2.8% 2.9%Murraylands 51 54 4.2% 4.2%Riverland 46 49 3.3% 3.3%Yorke Peninsula 50 53 3.2% 3.2%Flinders Ranges and Outback 114 123 2.6% 2.6%Kangaroo Island 33 36 16.1% 16.5%Regional South Australia 722 771 3.4% 3.3%South Australia 2,223 2,407 2.7% 2.7%

Source: Deloitte Access Economics’ Regional TSA model.

South Australian Regional Tourism Satellite Accounts 2013-14

18Deloitte Access Economics

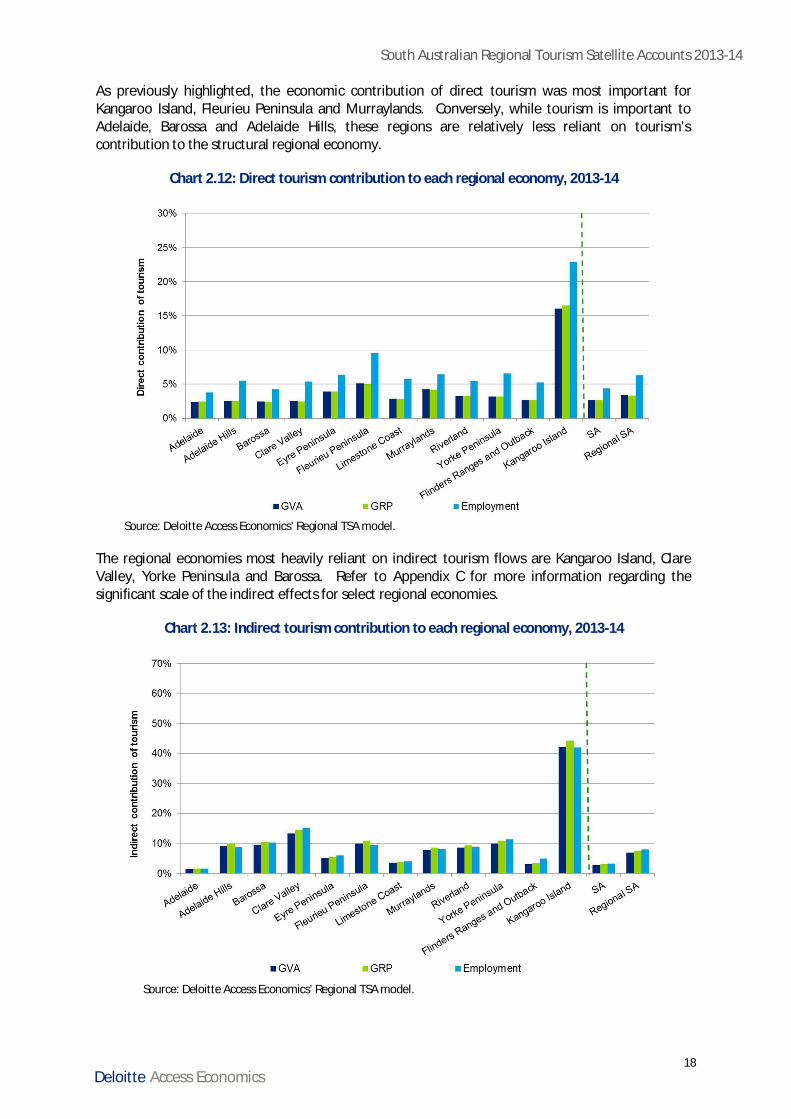

As previously highlighted, the economic contribution of direct tourism was most important forKangaroo Island, Fleurieu Peninsula and Murraylands. Conversely, while tourism is important toAdelaide, Barossa and Adelaide Hills, these regions are relatively less reliant on tourism’scontribution to the structural regional economy.

Chart 2.12: Direct tourism contribution to each regional economy, 2013-14

Source: Deloitte Access Economics’ Regional TSA model.

The regional economies most heavily reliant on indirect tourism flows are Kangaroo Island, ClareValley, Yorke Peninsula and Barossa. Refer to Appendix C for more information regarding thesignificant scale of the indirect effects for select regional economies.

Chart 2.13: Indirect tourism contribution to each regional economy, 2013-14

Source: Deloitte Access Economics’ Regional TSA model.

South Australian Regional Tourism Satellite Accounts 2013-14

19Deloitte Access Economics

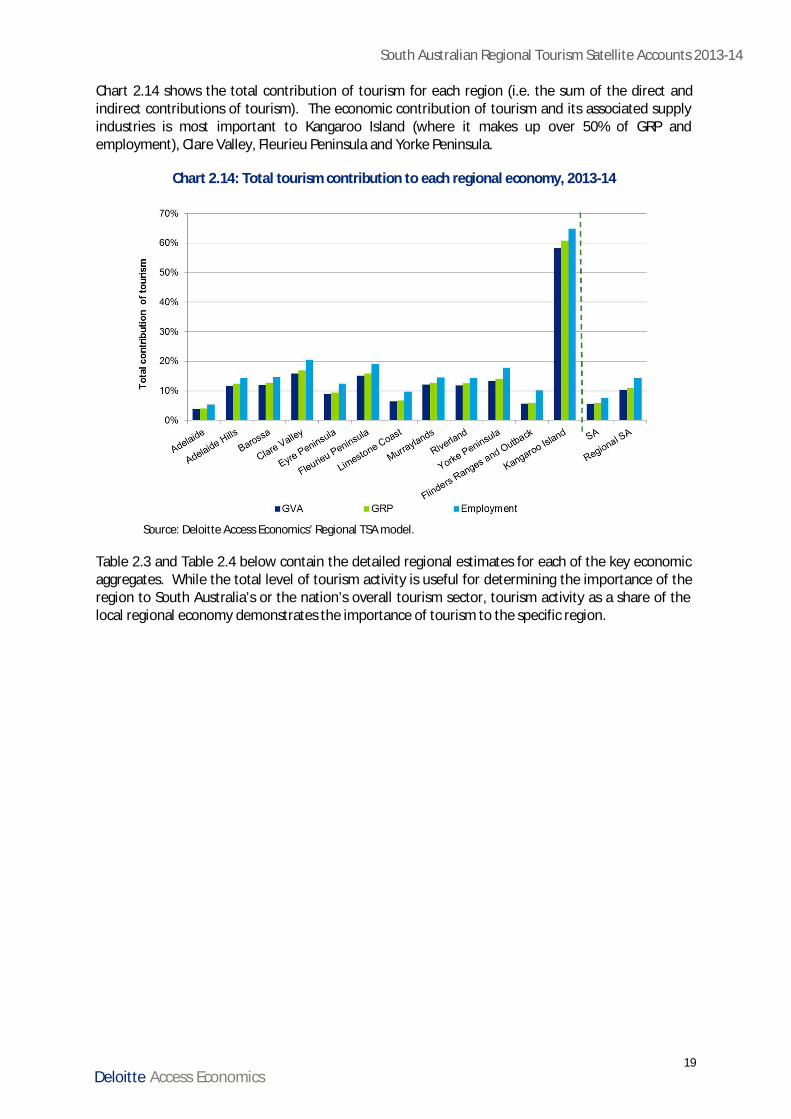

Chart 2.14 shows the total contribution of tourism for each region (i.e. the sum of the direct andindirect contributions of tourism). The economic contribution of tourism and its associated supplyindustries is most important to Kangaroo Island (where it makes up over 50% of GRP andemployment), Clare Valley, Fleurieu Peninsula and Yorke Peninsula.

Chart 2.14: Total tourism contribution to each regional economy, 2013-14

Source: Deloitte Access Economics’ Regional TSA model.

Table 2.3 and Table 2.4 below contain the detailed regional estimates for each of the key economicaggregates. While the total level of tourism activity is useful for determining the importance of theregion to South Australia’s or the nation’s overall tourism sector, tourism activity as a share of thelocal regional economy demonstrates the importance of tourism to the specific region.

South Australian Regional Tourism Satellite Accounts 2013-14

20Deloitte Access Economics

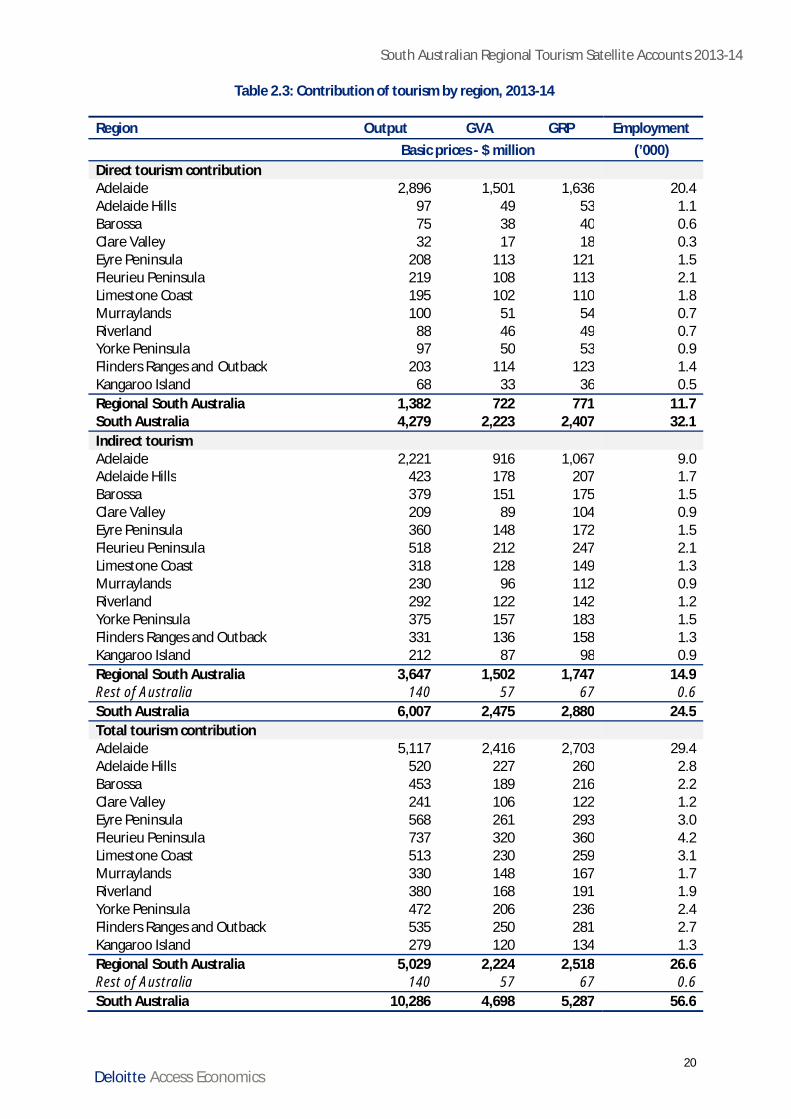

Table 2.3: Contribution of tourism by region, 2013-14

Region Output GVA GRP Employment Basic prices - $ million (’000)Direct tourism contributionAdelaide 2,896 1,501 1,636 20.4Adelaide Hills 97 49 53 1.1Barossa 75 38 40 0.6Clare Valley 32 17 18 0.3Eyre Peninsula 208 113 121 1.5Fleurieu Peninsula 219 108 113 2.1Limestone Coast 195 102 110 1.8Murraylands 100 51 54 0.7Riverland 88 46 49 0.7Yorke Peninsula 97 50 53 0.9Flinders Ranges and Outback 203 114 123 1.4Kangaroo Island 68 33 36 0.5Regional South Australia 1,382 722 771 11.7South Australia 4,279 2,223 2,407 32.1Indirect tourismAdelaide 2,221 916 1,067 9.0Adelaide Hills 423 178 207 1.7Barossa 379 151 175 1.5Clare Valley 209 89 104 0.9Eyre Peninsula 360 148 172 1.5Fleurieu Peninsula 518 212 247 2.1Limestone Coast 318 128 149 1.3Murraylands 230 96 112 0.9Riverland 292 122 142 1.2Yorke Peninsula 375 157 183 1.5Flinders Ranges and Outback 331 136 158 1.3Kangaroo Island 212 87 98 0.9Regional South Australia 3,647 1,502 1,747 14.9Rest of Australia 140 57 67 0.6South Australia 6,007 2,475 2,880 24.5Total tourism contributionAdelaide 5,117 2,416 2,703 29.4Adelaide Hills 520 227 260 2.8Barossa 453 189 216 2.2Clare Valley 241 106 122 1.2Eyre Peninsula 568 261 293 3.0Fleurieu Peninsula 737 320 360 4.2Limestone Coast 513 230 259 3.1Murraylands 330 148 167 1.7Riverland 380 168 191 1.9Yorke Peninsula 472 206 236 2.4Flinders Ranges and Outback 535 250 281 2.7Kangaroo Island 279 120 134 1.3Regional South Australia 5,029 2,224 2,518 26.6Rest of Australia 140 57 67 0.6South Australia 10,286 4,698 5,287 56.6

South Australian Regional Tourism Satellite Accounts 2013-14

21Deloitte Access Economics

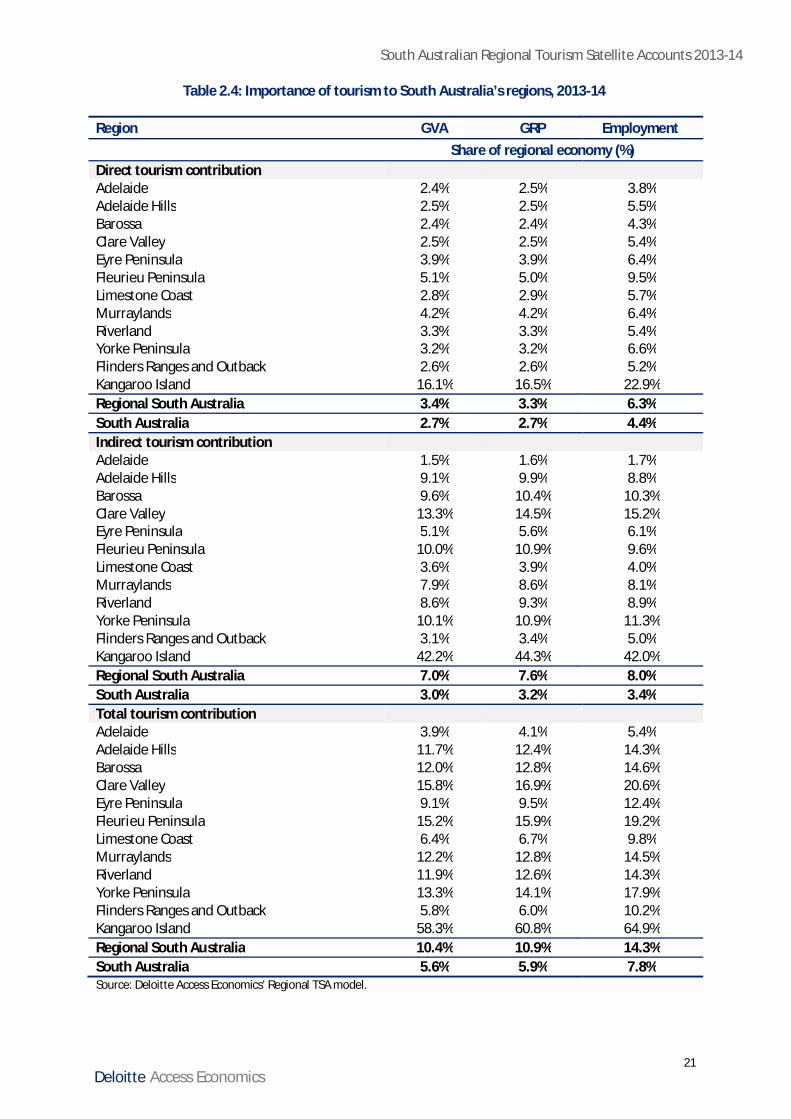

Table 2.4: Importance of tourism to South Australia’s regions, 2013-14

Region GVA GRP Employment Share of regional economy (%)Direct tourism contributionAdelaide 2.4% 2.5% 3.8%Adelaide Hills 2.5% 2.5% 5.5%Barossa 2.4% 2.4% 4.3%Clare Valley 2.5% 2.5% 5.4%Eyre Peninsula 3.9% 3.9% 6.4%Fleurieu Peninsula 5.1% 5.0% 9.5%Limestone Coast 2.8% 2.9% 5.7%Murraylands 4.2% 4.2% 6.4%Riverland 3.3% 3.3% 5.4%Yorke Peninsula 3.2% 3.2% 6.6%Flinders Ranges and Outback 2.6% 2.6% 5.2%Kangaroo Island 16.1% 16.5% 22.9%Regional South Australia 3.4% 3.3% 6.3%South Australia 2.7% 2.7% 4.4%Indirect tourism contributionAdelaide 1.5% 1.6% 1.7%Adelaide Hills 9.1% 9.9% 8.8%Barossa 9.6% 10.4% 10.3%Clare Valley 13.3% 14.5% 15.2%Eyre Peninsula 5.1% 5.6% 6.1%Fleurieu Peninsula 10.0% 10.9% 9.6%Limestone Coast 3.6% 3.9% 4.0%Murraylands 7.9% 8.6% 8.1%Riverland 8.6% 9.3% 8.9%Yorke Peninsula 10.1% 10.9% 11.3%Flinders Ranges and Outback 3.1% 3.4% 5.0%Kangaroo Island 42.2% 44.3% 42.0%Regional South Australia 7.0% 7.6% 8.0%South Australia 3.0% 3.2% 3.4%Total tourism contributionAdelaide 3.9% 4.1% 5.4%Adelaide Hills 11.7% 12.4% 14.3%Barossa 12.0% 12.8% 14.6%Clare Valley 15.8% 16.9% 20.6%Eyre Peninsula 9.1% 9.5% 12.4%Fleurieu Peninsula 15.2% 15.9% 19.2%Limestone Coast 6.4% 6.7% 9.8%Murraylands 12.2% 12.8% 14.5%Riverland 11.9% 12.6% 14.3%Yorke Peninsula 13.3% 14.1% 17.9%Flinders Ranges and Outback 5.8% 6.0% 10.2%Kangaroo Island 58.3% 60.8% 64.9%Regional South Australia 10.4% 10.9% 14.3%South Australia 5.6% 5.9% 7.8%Source: Deloitte Access Economics’ Regional TSA model.

South Australian Regional Tourism Satellite Accounts 2013-14

22Deloitte Access Economics

3 Key trends in tourism3.1 Adelaide

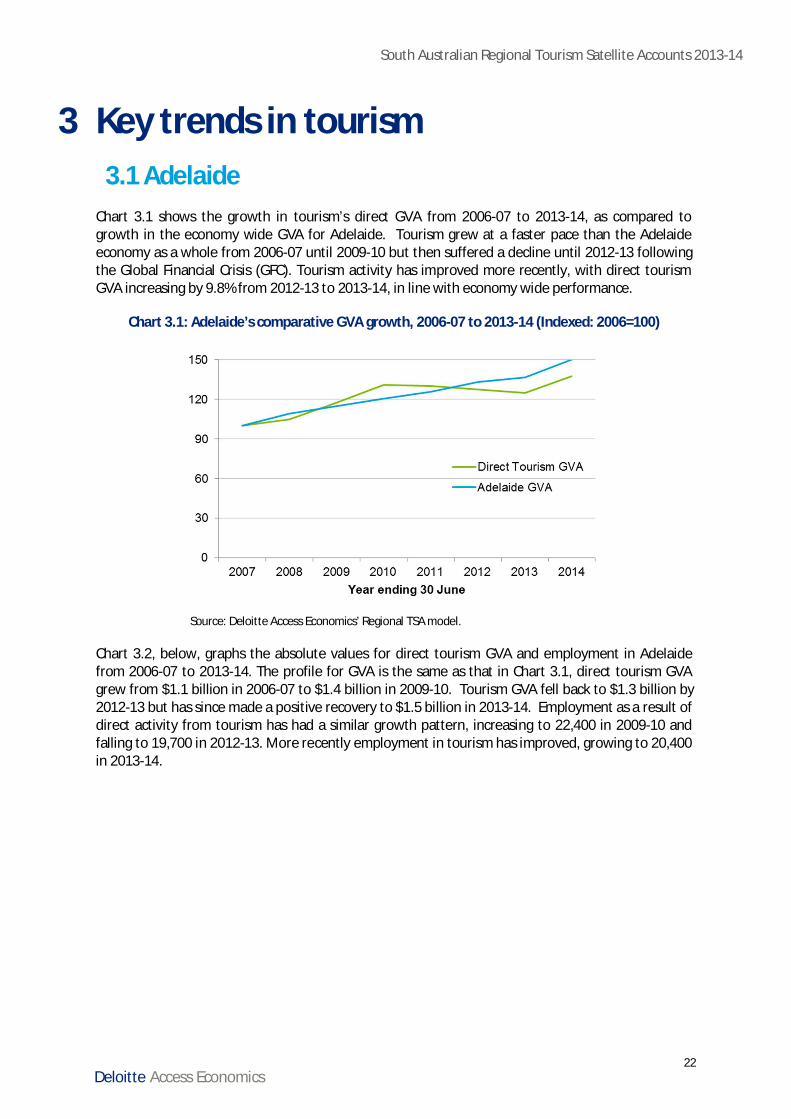

Chart 3.1 shows the growth in tourism’s direct GVA from 2006-07 to 2013-14, as compared togrowth in the economy wide GVA for Adelaide. Tourism grew at a faster pace than the Adelaideeconomy as a whole from 2006-07 until 2009-10 but then suffered a decline until 2012-13 followingthe Global Financial Crisis (GFC). Tourism activity has improved more recently, with direct tourismGVA increasing by 9.8% from 2012-13 to 2013-14, in line with economy wide performance.

Chart 3.1: Adelaide’s comparative GVA growth, 2006-07 to 2013-14 (Indexed: 2006=100)

Source: Deloitte Access Economics’ Regional TSA model.

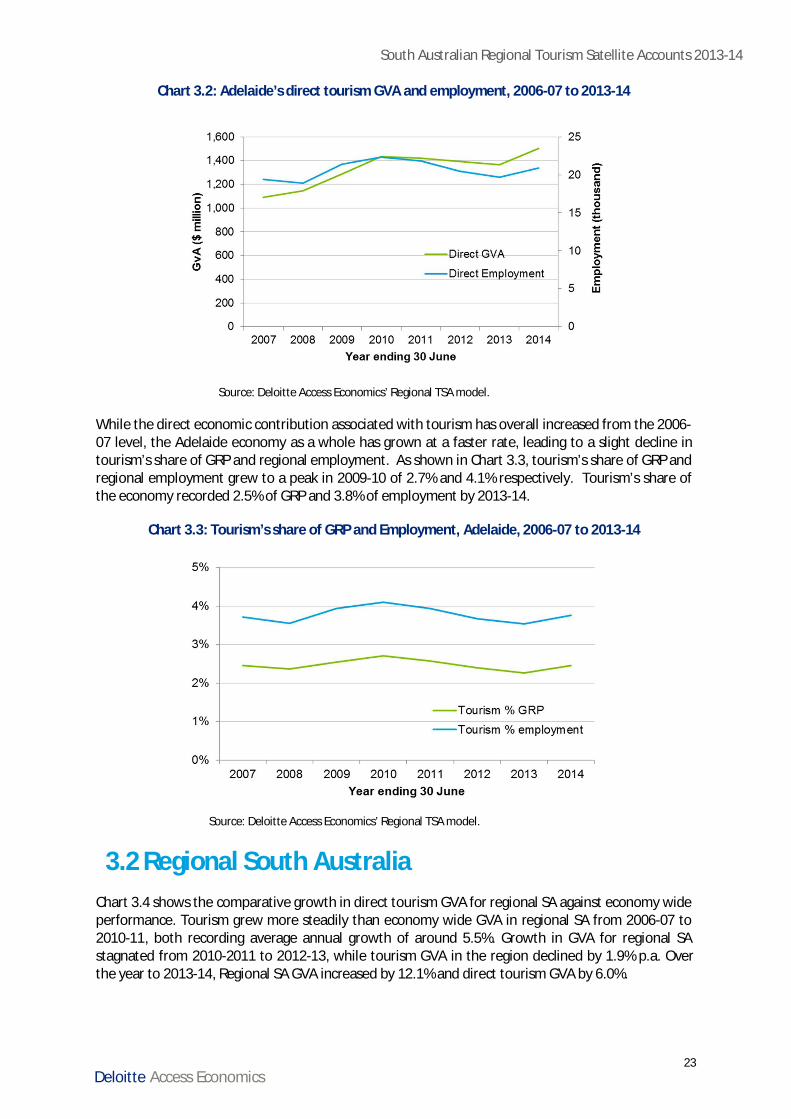

Chart 3.2, below, graphs the absolute values for direct tourism GVA and employment in Adelaidefrom 2006-07 to 2013-14. The profile for GVA is the same as that in Chart 3.1, direct tourism GVAgrew from $1.1 billion in 2006-07 to $1.4 billion in 2009-10. Tourism GVA fell back to $1.3 billion by2012-13 but has since made a positive recovery to $1.5 billion in 2013-14. Employment as a result ofdirect activity from tourism has had a similar growth pattern, increasing to 22,400 in 2009-10 andfalling to 19,700 in 2012-13. More recently employment in tourism has improved, growing to 20,400in 2013-14.

South Australian Regional Tourism Satellite Accounts 2013-14

23Deloitte Access Economics

Chart 3.2: Adelaide’s direct tourism GVA and employment, 2006-07 to 2013-14

Source: Deloitte Access Economics’ Regional TSA model.

While the direct economic contribution associated with tourism has overall increased from the 2006-07 level, the Adelaide economy as a whole has grown at a faster rate, leading to a slight decline intourism’s share of GRP and regional employment. As shown in Chart 3.3, tourism’s share of GRP andregional employment grew to a peak in 2009-10 of 2.7% and 4.1% respectively. Tourism’s share ofthe economy recorded 2.5% of GRP and 3.8% of employment by 2013-14.

Chart 3.3: Tourism’s share of GRP and Employment, Adelaide, 2006-07 to 2013-14

Source: Deloitte Access Economics’ Regional TSA model.

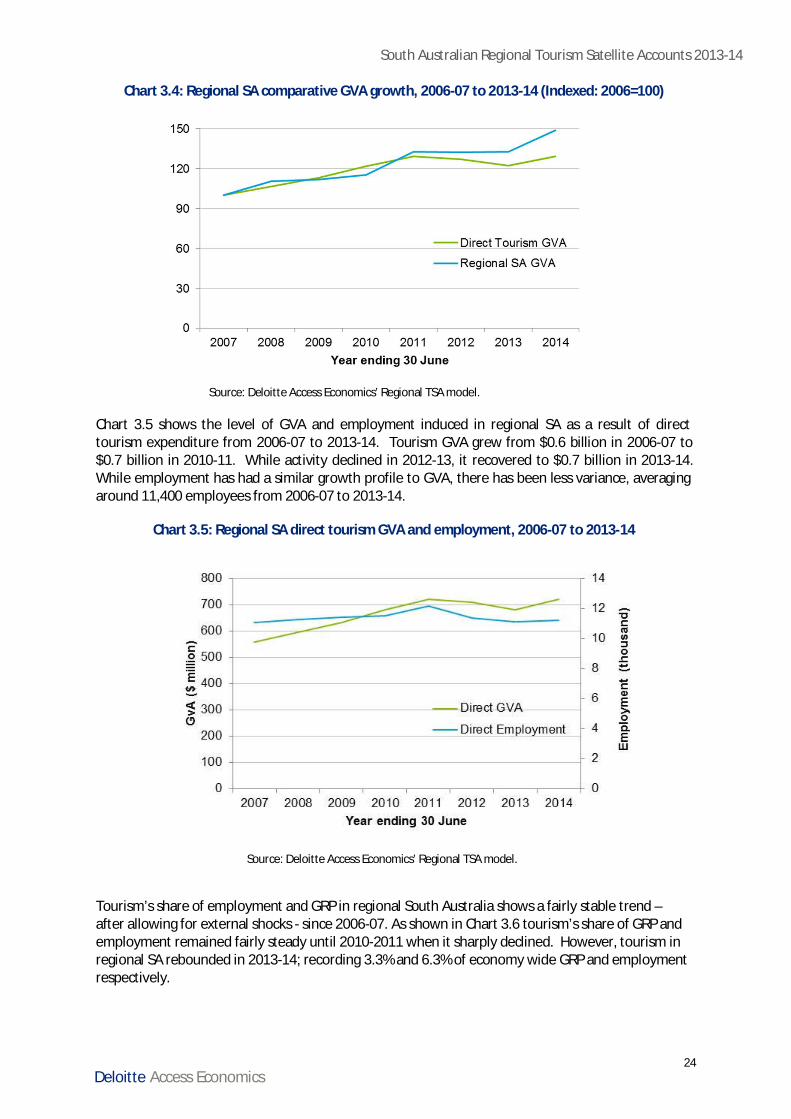

3.2 Regional South AustraliaChart 3.4 shows the comparative growth in direct tourism GVA for regional SA against economy wideperformance. Tourism grew more steadily than economy wide GVA in regional SA from 2006-07 to2010-11, both recording average annual growth of around 5.5%. Growth in GVA for regional SAstagnated from 2010-2011 to 2012-13, while tourism GVA in the region declined by 1.9% p.a. Overthe year to 2013-14, Regional SA GVA increased by 12.1% and direct tourism GVA by 6.0%.

South Australian Regional Tourism Satellite Accounts 2013-14

24Deloitte Access Economics

Chart 3.4: Regional SA comparative GVA growth, 2006-07 to 2013-14 (Indexed: 2006=100)

Source: Deloitte Access Economics’ Regional TSA model.

Chart 3.5 shows the level of GVA and employment induced in regional SA as a result of directtourism expenditure from 2006-07 to 2013-14. Tourism GVA grew from $0.6 billion in 2006-07 to$0.7 billion in 2010-11. While activity declined in 2012-13, it recovered to $0.7 billion in 2013-14.While employment has had a similar growth profile to GVA, there has been less variance, averagingaround 11,400 employees from 2006-07 to 2013-14.

Chart 3.5: Regional SA direct tourism GVA and employment, 2006-07 to 2013-14

Source: Deloitte Access Economics’ Regional TSA model.

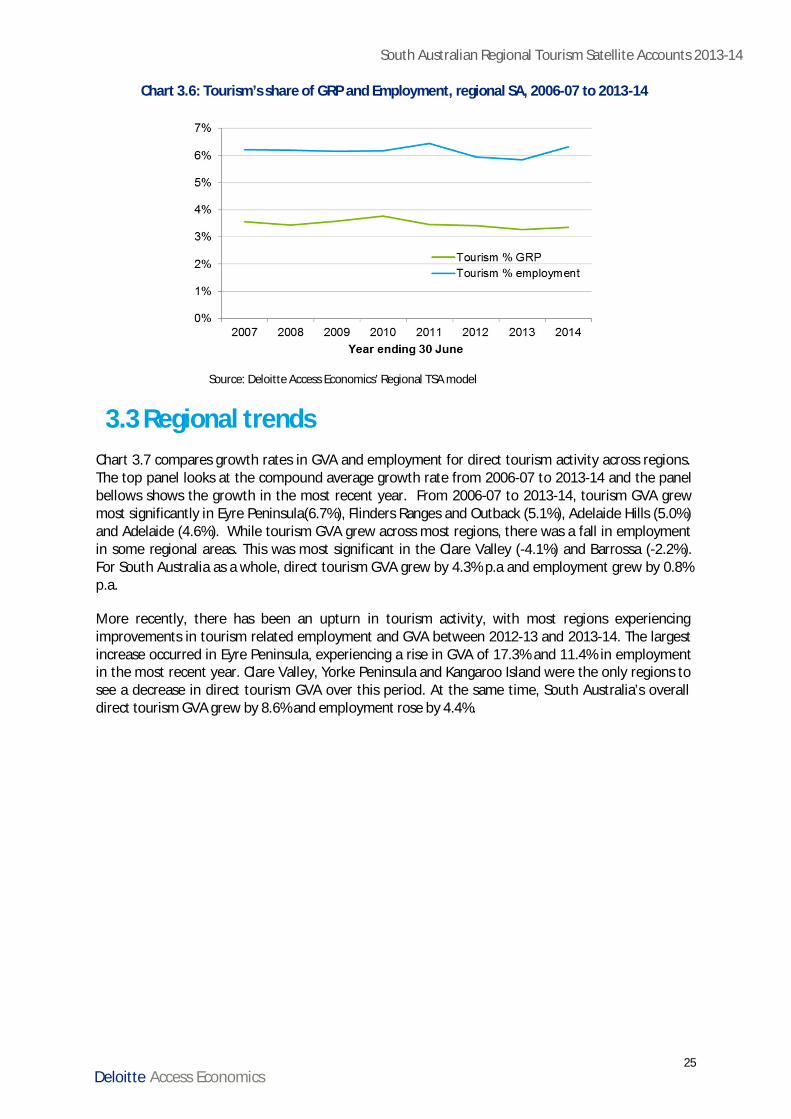

Tourism’s share of employment and GRP in regional South Australia shows a fairly stable trend –after allowing for external shocks - since 2006-07. As shown in Chart 3.6 tourism’s share of GRP andemployment remained fairly steady until 2010-2011 when it sharply declined. However, tourism inregional SA rebounded in 2013-14; recording 3.3% and 6.3% of economy wide GRP and employmentrespectively.

South Australian Regional Tourism Satellite Accounts 2013-14

25Deloitte Access Economics

Chart 3.6: Tourism’s share of GRP and Employment, regional SA, 2006-07 to 2013-14

Source: Deloitte Access Economics’ Regional TSA model

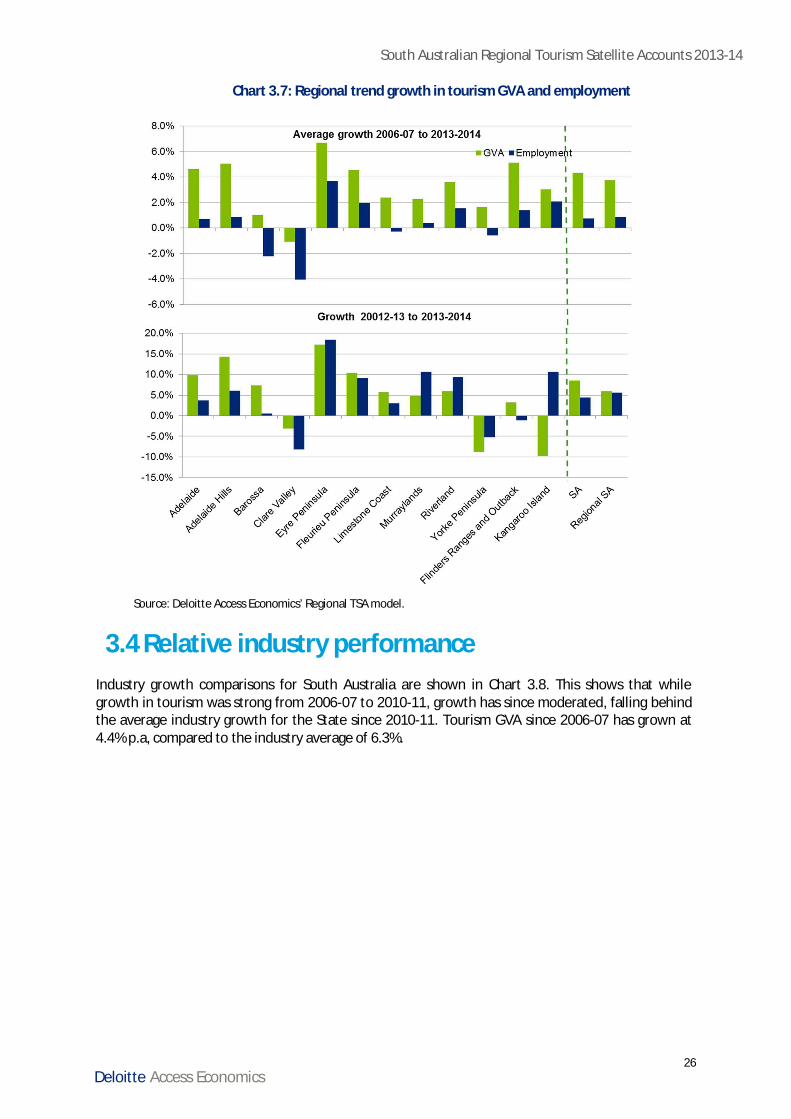

3.3 Regional trendsChart 3.7 compares growth rates in GVA and employment for direct tourism activity across regions.The top panel looks at the compound average growth rate from 2006-07 to 2013-14 and the panelbellows shows the growth in the most recent year. From 2006-07 to 2013-14, tourism GVA grewmost significantly in Eyre Peninsula(6.7%), Flinders Ranges and Outback (5.1%), Adelaide Hills (5.0%)and Adelaide (4.6%). While tourism GVA grew across most regions, there was a fall in employmentin some regional areas. This was most significant in the Clare Valley (-4.1%) and Barrossa (-2.2%).For South Australia as a whole, direct tourism GVA grew by 4.3% p.a and employment grew by 0.8%p.a.

More recently, there has been an upturn in tourism activity, with most regions experiencingimprovements in tourism related employment and GVA between 2012-13 and 2013-14. The largestincrease occurred in Eyre Peninsula, experiencing a rise in GVA of 17.3% and 11.4% in employmentin the most recent year. Clare Valley, Yorke Peninsula and Kangaroo Island were the only regions tosee a decrease in direct tourism GVA over this period. At the same time, South Australia’s overalldirect tourism GVA grew by 8.6% and employment rose by 4.4%.

South Australian Regional Tourism Satellite Accounts 2013-14

26Deloitte Access Economics

Chart 3.7: Regional trend growth in tourism GVA and employment

Source: Deloitte Access Economics’ Regional TSA model.

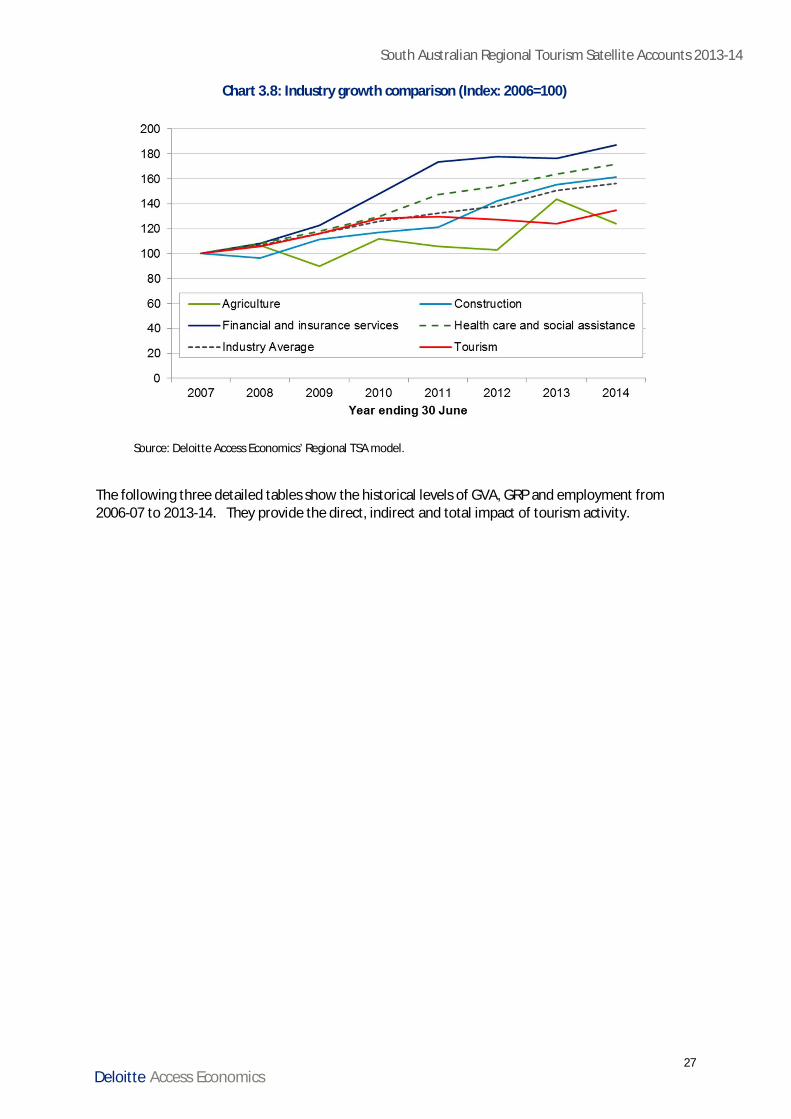

3.4 Relative industry performanceIndustry growth comparisons for South Australia are shown in Chart 3.8. This shows that whilegrowth in tourism was strong from 2006-07 to 2010-11, growth has since moderated, falling behindthe average industry growth for the State since 2010-11. Tourism GVA since 2006-07 has grown at4.4% p.a, compared to the industry average of 6.3%.

South Australian Regional Tourism Satellite Accounts 2013-14

27Deloitte Access Economics

Chart 3.8: Industry growth comparison (Index: 2006=100)

Source: Deloitte Access Economics’ Regional TSA model.

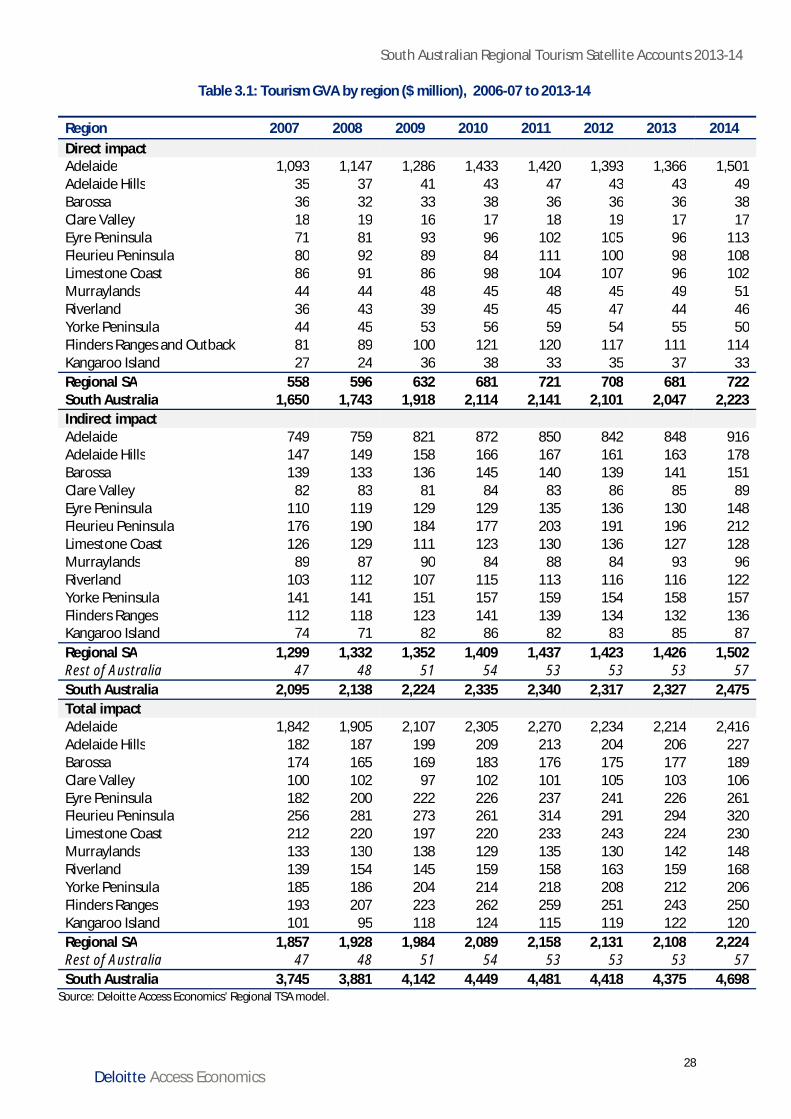

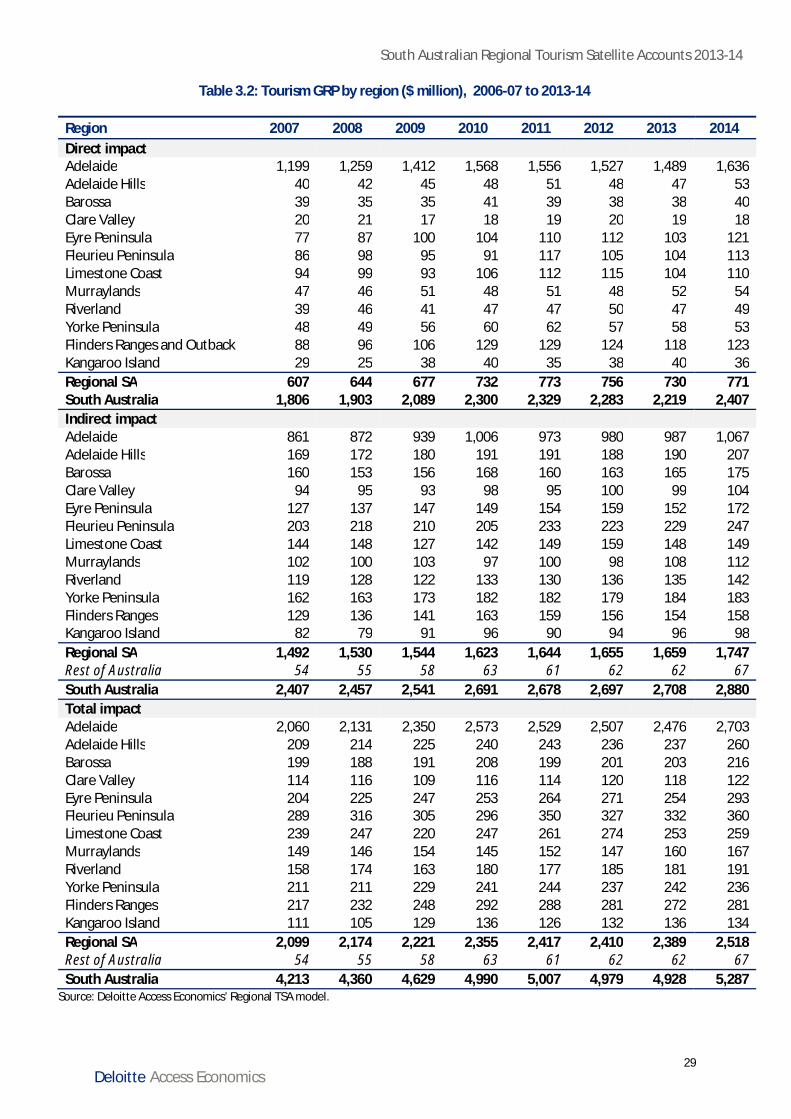

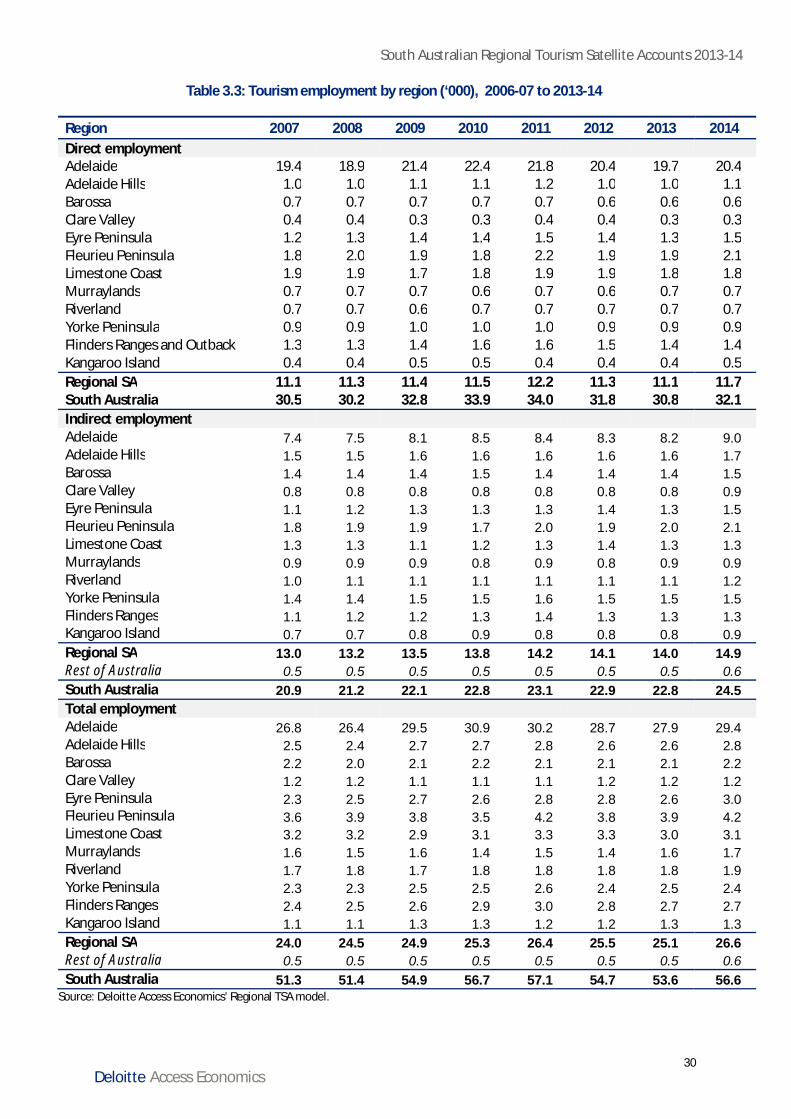

The following three detailed tables show the historical levels of GVA, GRP and employment from2006-07 to 2013-14. They provide the direct, indirect and total impact of tourism activity.

South Australian Regional Tourism Satellite Accounts 2013-14

28Deloitte Access Economics

Table 3.1: Tourism GVA by region ($ million), 2006-07 to 2013-14

Region 2007 2008 2009 2010 2011 2012 2013 2014Direct impactAdelaide 1,093 1,147 1,286 1,433 1,420 1,393 1,366 1,501Adelaide Hills 35 37 41 43 47 43 43 49Barossa 36 32 33 38 36 36 36 38Clare Valley 18 19 16 17 18 19 17 17Eyre Peninsula 71 81 93 96 102 105 96 113Fleurieu Peninsula 80 92 89 84 111 100 98 108Limestone Coast 86 91 86 98 104 107 96 102Murraylands 44 44 48 45 48 45 49 51Riverland 36 43 39 45 45 47 44 46Yorke Peninsula 44 45 53 56 59 54 55 50Flinders Ranges and Outback 81 89 100 121 120 117 111 114Kangaroo Island 27 24 36 38 33 35 37 33Regional SA 558 596 632 681 721 708 681 722South Australia 1,650 1,743 1,918 2,114 2,141 2,101 2,047 2,223Indirect impactAdelaide 749 759 821 872 850 842 848 916Adelaide Hills 147 149 158 166 167 161 163 178Barossa 139 133 136 145 140 139 141 151Clare Valley 82 83 81 84 83 86 85 89Eyre Peninsula 110 119 129 129 135 136 130 148Fleurieu Peninsula 176 190 184 177 203 191 196 212Limestone Coast 126 129 111 123 130 136 127 128Murraylands 89 87 90 84 88 84 93 96Riverland 103 112 107 115 113 116 116 122Yorke Peninsula 141 141 151 157 159 154 158 157Flinders Ranges 112 118 123 141 139 134 132 136Kangaroo Island 74 71 82 86 82 83 85 87Regional SA 1,299 1,332 1,352 1,409 1,437 1,423 1,426 1,502Rest of Australia 47 48 51 54 53 53 53 57South Australia 2,095 2,138 2,224 2,335 2,340 2,317 2,327 2,475Total impactAdelaide 1,842 1,905 2,107 2,305 2,270 2,234 2,214 2,416Adelaide Hills 182 187 199 209 213 204 206 227Barossa 174 165 169 183 176 175 177 189Clare Valley 100 102 97 102 101 105 103 106Eyre Peninsula 182 200 222 226 237 241 226 261Fleurieu Peninsula 256 281 273 261 314 291 294 320Limestone Coast 212 220 197 220 233 243 224 230Murraylands 133 130 138 129 135 130 142 148Riverland 139 154 145 159 158 163 159 168Yorke Peninsula 185 186 204 214 218 208 212 206Flinders Ranges 193 207 223 262 259 251 243 250Kangaroo Island 101 95 118 124 115 119 122 120Regional SA 1,857 1,928 1,984 2,089 2,158 2,131 2,108 2,224Rest of Australia 47 48 51 54 53 53 53 57South Australia 3,745 3,881 4,142 4,449 4,481 4,418 4,375 4,698

Source: Deloitte Access Economics’ Regional TSA model.

South Australian Regional Tourism Satellite Accounts 2013-14

29Deloitte Access Economics

Table 3.2: Tourism GRP by region ($ million), 2006-07 to 2013-14